Abstract

Capital investment is vital for sustainable tourism growth, particularly in times of geopolitical turmoil. This study examines how tourism investment was influenced by geopolitical risks considering social globalization as a moderating factor. Data were collected from 18 developing economies between 1995 and 2018. The results from the fixed effects and the least squares dummy variable–corrected methods show that the geopolitical risks negatively affect capital investment in tourism, with social globalization playing a moderating role in alleviating the adverse effect. The results were robust to different measures and analyses. The study advances our understanding of sustainable tourism growth amid geopolitical turmoil. Policymakers, especially those from developing economies, are suggested to be vigilant about the media atmosphere of geopolitics and enhancing social globalization as a countermeasure against politically turbulent times. The study also provides implications for alleviating the impact of the global pandemic on tourism investment.

Keywords

Introduction

It is well recognized that the tourism industry is susceptible to geopolitical turmoil, natural disasters, and health crises such as the current COVID-19 pandemic (Dahles and Susilowati 2015; Seabra, Reis, and Abrantes 2020). Most of the previous studies have focused on the impact of geopolitical risks on the demand side of tourism, such as tourist arrivals (Balli, Uddin, and Shahzad 2019; Demir, Gozgor, and Paramati 2019; Tiwari, Das, and Dutta 2019), tourism receipts (Alola, Cop, and Adewale 2019), and inbound tourism as measured by visits or revenues generated from the tourism sector (Saha, Su, and Campbell 2017). However, investment in the supply side that sustains tourism growth has received little research attention, despite the investment-side perspective having been investigated in the literature on macroeconomic phenomena (Apergis et al. 2018; Bilgin, Gozgor, and Karabulut 2020; Bloom, Bond, and Van Reenen 2007; Collier and Hoeffler 2004; Enders and Sandler 2006). Given the importance and uniqueness of the tourism investment patterns amid geopolitical turmoil for sustainable tourism growth, the impact of geopolitical risks on tourism investment requires prompt research attention.

Geopolitical risk refers to the risk that is associated with conflicts between states competing for territory. Geopolitical risk captures both the risk of a potential conflict and risks associated with the escalation of a conflict (Caldara and Iacoviello 2019). Geopolitical risks are a key factor to be considered in the capital investment decision process. Therefore, this study examines the effects of geopolitical risks on capital investments in the supply side of tourism, considering the role of social globalization, which may alleviate the negative impact of the geopolitical risks on tourism investment. Our central hypothesis is that a surge in the level of geopolitical risks causes a decrease in tourism investment as capital is mainly profit-driven and susceptible to geopolitical risks. Using panel data from 1995 to 2018 from 18 developing countries, we observe that the geopolitical risks decrease travel and tourism investment. We also use the geopolitical risk (GPR) index constructed by searching newspapers with a string of relevant keywords based on an algorithm to provide a more comprehensive picture of geopolitics’ role in tourism. The GPR index is comparable across the countries, thus an ideal measure for analyzing its impact on travel and tourism investments across countries. The results were robust by various sensitivity checks. Additionally, in the quantitative literature, social globalization, defined as the interchange of views, ideas, and social values between nations (Dwyer 2015), is neglected as it is hard to measure. In this article, we particularly investigate the moderating role of social globalization via employing the special indices of social globalization collected from three different dimensions.

Our study makes three significant contributions to the tourism literature. First, to our knowledge, the mainstream tourism studies center on the demand side. This article is the first research analyzing the effects of geopolitical risks, particularly on the tourism market’s supply side, denoted by travel and tourism investment. Second, this study is the first attempt to investigate the moderating role of social globalization in the relationship between geopolitical risks and tourism investment. The proxies of social globalization distinguish between de facto (outcome-oriented) and de jure (policy-related) indicators and are decomposed into interpersonal, informational, and cultural globalization to gain in-depth and specific insights. Third, unlike most previous studies that use firm-level or microlevel data (see, e.g., Akron et al. 2020) to analyze firm-specific investment decisions, we use the country-level data rather than the firm-level data, which provides a macro-view of capital investment in the tourism industry.

Literature Review and Hypothesis Development

Risks and Tourism

Several studies have examined travelers’ perceptions of risks and the corresponding effect on their travel behaviors and destination choices. For example, Roehl and Fesenmaier (1992) categorize their survey respondents according to their preferences for perceived travel risks and then study how the heterogeneity in risk preference affects their travel behaviors. Sönmez and Graefe (1998) find that perceived risks and safety are strong predictors for avoiding dangerous regions rather than planning to visit them. Reisinger and Mavondo (2005) investigate the effect of cultural and psychographic factors on perceptions of travel risk on intentions to travel internationally. Sharifpour et al. (2014) particularly investigate the effects of prior tourist knowledge on their perceived risks. Similarly, Park and Tussyadiah (2017) examine perceived risk in mobile travel booking with a smartphone. Karl (2018) pays attention to tourists’ self-assessments of risk and uncertainty in travel decision making. As Williams and Baláž (2015) point out, this line of research focuses on understanding the multiple dimensions of perceived risks and factors contributing to perceived risks.

Several other studies have looked into objective macro-risks instead of perceived risks. For instance, Smeral (2010) analyzes the macroeconomic effects of the global recession and its impact on inbound tourism. Lee and Chen (2021) investigate the impacts of country risks—including political, financial, and economic on tourism development. In this study, we focus on capital investment decisions in tourism, which is neglected in the literature. We extend the spectrum of objective macro-risks from within-country macro-risks (Lee and Chen 2021) to between-country macro-risks. Moreover, we aim to explore the potential moderating role of social globalization on the relationship between geopolitical risks and tourism investment. We not only consider the investor as an economic agent but also as a social agent in the world.

Geopolitical Risks

Researchers have shown continuous interest in studying the effects of geopolitical risks since the 9-11 attacks, which influenced the global economy and many industries, particularly the tourism industry, in the world. Most of the studies investigate geopolitics’ effect on territorial disputes, diplomatic tensions, and terrorism on a wide range of economic issues (Enders and Sandler 2006; Gupta et al. 2004; Saha and Yap 2014; Tavares 2004). Overall, terrorism decreases capital inflows (Collier and Hoeffler 2004; Enders and Sandler 2006), slows downs economic growth, and thus causes spillover costs among trading partners (Murdoch and Sandler 2002, 2004) and affects the stock returns and the price volatility of stock markets at the national and global levels (Abadie and Gardeazabal 2003; Chen and Siems 2004; Drakos 2004). Moreover, economic and political uncertainty adversely affects private investments (Bloom, Bond, and Van Reenen 2007; Dixit, Dixit, and Pindyck 1994).

The earlier studies seem to interpret and measure geopolitical risks in a somewhat arbitrary way. Each of them arbitrarily captures a narrow subset of geopolitics risks while there is a full spectrum (Demiralay and Kilincarslan 2019). There has been no consensus on how to measure geopolitical risks until Caldara and Iacoviello (2019). They employ a text-search algorithm to count the number of occurrences of a word string consisting of war, terrorism, military, geopolitics, and such in articles published in leading national and international newspapers to construct an index of GPR. The index is allowed to change with the updates of newspapers and choices of "keywords," but the underlying logic stays intact as long as the algorithm is the same. This method provides flexibility, stability, and a fairly comprehensive picture. It has been spread quickly and adopted by researchers to cover a broader spectrum of geopolitics (Balli, Uddin, and Shahzad 2019; Bilgin, Gozgor, and Karabulut 2020; Demiralay and Kilincarslan 2019; Tiwari, Das, and Dutta 2019).

The Impact of Geopolitical Risks on the Tourism Industry

Compared with other industries, the international tourism industry is one of the first falling dominoes activated by the push from certain geopolitical risks. Drakos (2004) reports that terrorism significantly affects specific industries, such as airlines and tourism. In the tourism literature, most of the studies focus on the adverse effects of geopolitical risks on inbound tourism, such as the visits to or revenues from the tourism sector (Demir, Gozgor, and Paramati 2019), the number of tourist arrivals (Tiwari, Das, and Dutta 2019), and the tourism receipts (Alola, Cop, and Adewale 2019). Demiralay and Kilincarslan (2019) observe the negative impact of geopolitical risks on travel and leisure indices’ stock returns in the three regions of Asia-Pacific, Europe, and North America. Balli, Uddin, and Shahzad (2019) show that the impact of geopolitical risk on international tourism demand is negligible in countries that are popular tourist destinations. In short, tourism supply (capital investment in travel and tourism) is, to some extent, neglected in the tourism literature, apart from Akron et al. (2020), who suggest the negative impact of economic policy uncertainty (EPU) on corporate investment in hospitality and tourism industries in only the single developed economy of the United States. Similarly, many other prior studies in tourism also choose a particular country (Alola, Cop, and Adewale 2019; Tiwari, Das, and Dutta 2019) or a limited number of regions (Demiralay and Kilincarslan 2019) when discussing the effect of geopolitical risks, apart from Demir, Gozgor, and Paramati (2019) who conducted a cross-country study and report the adverse effect of geopolitical risks on inbound tourism.

More recently, there is an increasing trend in the literature that highlights the role of economic policy uncertainty (EPU) in tourism and the role of geopolitical risks. The majority of these studies (Akron et al. 2020; Demir, Gozgor, and Paramati 2020; Demiralay and Kilincarslan 2019; Tiwari, Das, and Dutta 2019) employ the EPU index based on a text-search algorithm over the leading newspapers with a different string of chosen words consisting of "uncertain" or "uncertainty" and "economy" or "economical," which draws a distinctive line between the EPU index and GPR index concerning the implied information they capture from newspapers. The EPU index concentrates on the economic news, while the GPR index emphasizes geopolitical news. Furthermore, the EPU index indicates a much milder atmosphere and tone than the GPR index. According to Tiwari, Das, and Dutta (2019), GPR’s influence is stronger than that of EPU and, additionally, the GPR has long-run implications. In contrast, the EPU holds short-run consequences on inbound tourism.

As discussed earlier, most studies emphasize the effect of geopolitical risks on tourism demand (Alola, Cop, and Adewale 2019; Balli, Uddin, and Shahzad 2019; Demir, Gozgor, and Paramati 2019; Drakos 2004; Song et al. 2012; Tiwari, Das, and Dutta 2019), neglecting supply. Studies have indicated a decrease in capital investment in general when geopolitical risks exist (Araña and León 2008; Saha and Yap 2014; Thompson 2011). It is no surprise that capital is "footloose" and switches between territories searching for the most favorable regulatory regimes where the profits and interests can be realized with the fewest risks. From an economic view, we argue the tourism industry is more vulnerable to geopolitical risks than many other industries as the effect of geopolitical risk is almost immediate and direct in the tourism industry with the cancellation of trips and suspension of flights, instantly leading to excessive supply in tourism. Therefore, the capital would respond by closing up shops and facilities in the local tourism industry. That is, tourism supply (capital investment) decreases with geopolitical risks. Thus,

Hypothesis 1: The tourism supply (capital investment) is negatively related to geopolitical risks in general.

The Moderating Role of Social Globalization

The tourism literature mainly interprets "globalization" as "rising income," followed by "rising consumption" in international tourism (Crouch 1994; Dwyer 2015), which then attracts investment in local tourism supply (Cortes-Jimenez and Pulina 2010). However, over-reliance on international tourism makes tourism industries in developing countries highly vulnerable to global geopolitical risks. This economic globalization since the 1990s has been materialized through a central channel of multinational enterprises (MNEs), which are the key drivers of international capital investment, assumingly incentivized by profits (Dwyer 2015). Profit-driven economic globalization has led to a series of consequences, such as increasing income inequalities and decreasing overall welfare domestically (Antràs, De Gortari, and Itskhoki 2017). These economic globalization concerns trigger antiglobalization activities worldwide, such as the Trump Administration’s trade protectionism policies.

Despite the antiglobalization trend, exchanging ideas, views, and values is inevitable in the modern era. Social globalization meets the needs of citizens for communications that strengthen the ties between societies, while economic globalization builds on the economic needs of MNEs. Subsequently, MNEs may suspend certain international cooperation when the environment is unfavorable. However, it is unlikely to block cross-border information flow and social exchange. Compared with economic globalization, social globalization does not receive sufficient attention from scholars. In this study, we focus on the moderating role of social globalization to narrow the research gap. Generally, people have the desire to share joys and sorrows. We argue that, in general, social globalization helps shorten psychological distance and increase mutual understandings between peoples around the world. During troubled times, social globalization may reinforce people’s connections in different countries and create a sense of global solidarity. These aspects of social globalization can affect the effects of geopolitical risks (amount of risk investors are willing to take) on tourism investments. Therefore, we propose the following hypothesis:

Hypothesis 2: Social globalization significantly alleviates the adverse impact of geopolitical risk on capital investment in travel and tourism.

We decompose social globalization into three components: interpersonal globalization, informational globalization, and cultural globalization.

First, unlike profit-driven MNEs, it is more likely for individuals to hold out rather than withdraw a helping hand to an acquaintance in trouble (Greitemeyer, Rudolph, and Weiner 2003; Sacco, Milana, and Dunn 1985). We argue that interpersonal globalization narrows the social distances between peoples from various nations. Though they may come from different backgrounds, acquaintances with social proximity tend to show more empathy and sympathy to each other during difficult times than distant strangers. We then propose the following hypothesis:

Hypothesis 2a: Interpersonal globalization significantly alleviates the adverse impact of geopolitical risk on capital investment in travel and tourism.

Second, informational globalization indicates that people worldwide are likely to share more information and gain easier access to public information, which reduces information asymmetry between people. People with more accurate and in-time information are more likely to assess information objectively without exaggeration (Miranda and Saunders 2003; Yang and Maxwell 2011). This evidence implies that information globalization may help alleviate more-than-necessary fears and concerns in difficult times. We, therefore, propose the following hypothesis:

Hypothesis 2b: Informational globalization significantly alleviates the adverse impact of geopolitical risk on travel and tourism capital investment.

Finally, cultural globalization implies that peoples from various nations share social norms and cultural values, leading to in-depth understandings and profound awareness between people with different backgrounds (Leung et al. 2005; Rockstuhl et al. 2011). Cultural globalization tends to encourage mutual respect between people (Smith et al. 2013), thus helping reduce institutional bias and improve the understanding between groups and nations regardless of ethnicity or religion, which is expected to reduce the negative impact of geopolitical risks on tourism. We then propose the following hypothesis:

Hypothesis 2c: Cultural globalization significantly alleviates the adverse impact of geopolitical risk on capital investment in travel and tourism.

Data and Method

Data

The primary variable of interest is the GPR index, which is calculated for 18 developing economies, namely, Argentina, Brazil, PR China, Colombia, India, Indonesia, Israel, Malaysia, Mexico, Philippines, Russian Federation, Saudi Arabia, South Africa, South Korea, Thailand, Turkey, Ukraine, and Venezuela. We use the data set collected by Caldara and Iacoviello (2019). The GPR index focuses on the number of articles related to geopolitical acts, tensions, and threats relative to the number of all articles in 11 leading global newspapers. The index’s average is defined as 100 over 2000-2009 (see for more detail at https://www.matteoiacoviello.com/gpr.htm). Therefore, for example, the value of 120 in 2018 in the Russian Federation means that the country has a 20% higher GPR in 2018 than in 2000–2009. Note that we use both the current and lagged coefficients of the GPR index in the logarithmic form. The lagged indicator implies that the GPR’s impact on capital investment in travel and tourism (CITT) and capital investment in travel and tourism per capita (CITTPC) may be delayed since the decision on travel and tourism investments can be shaped in the long run.

We analyze two tourism supply measures: (a) the level of CITT and (b) the per capita CITT; that is, the total amount of investment is divided into the country’s population. These measures include new capital investment spending by all industries (domestic and foreign direct investments) directly involved in travel and tourism. The measures show investment spending by other industries on specific tourism assets such as new visitor accommodation and passenger transport equipment, restaurants, and leisure facilities.

We define this measure as the CITTPC. Both measures are defined by the real United States dollar (USD) prices in the logarithmic form, and the related data are obtained from World Travel and Tourism Council (WTTC) (2021). The empirical analyses cover the period from 1995 to 2018, and the beginning year is due to the availability of data from CITT.

To investigate the effect of social globalization (hypothesis 2), we use the overall index of social globalization as well as its subindices, that is, de facto (outcome-oriented) and de jure (policy-related) social globalization. De facto variables capture the facts directly related to social globalization in a country. In contrast, de jure variables indicate the potential of infrastructure development and the country’s institutional environment. To be specific, these two indices also have six subindices, which are tagged as follows: (i) interpersonal globalization (de facto) based on international students, international tourism, international voice traffic, migration, and transfers); (ii) interpersonal globalization (de jure) based on the freedom to visit, international airports, and telephone subscriptions; (iii) informational globalization (de facto) based on high-tech exports, international patents, and used Internet bandwidth; (iv) informational globalization (de jure) based on Internet access, press freedom, and television access; (v) cultural globalization (de facto) based on IKEA stores, international trademarks, McDonald’s restaurant, trade in cultural goods, and trade in personal services; and (vi) cultural globalization (de jure) based on civil liberties, gender parity, and human capital. The related data are downloaded from the ETH Zurich’s website (kof.ethz.ch/en/forecasts-and-indicators/indicators/kof-globalization -index.html) (Gygli et al. 2019).

We also use various types of control variables in the empirical analysis. We control the income effect (measured by per capita gross domestic product [GDP]) and the price effect (measured by lending interest rates). These are the main control variables in the empirical analysis. We also use several indicators that could affect the capital investments in travel and tourism, which show the structure of the economy and macroeconomic stances, such as domestic credit provided by the financial sector, urban population, total population, and trade openness. We obtain these data from the dataset of the World Bank (2021). Following Dogru, Sirakaya-Turk, and Crouch (2017), the log of tourist arrivals and log of tourism receipts (measures of tourism demand) are also included as additional controls. As the results do not vary, they are not reported to save space.

We also control the market regulations by using two indicators: economic freedom (index from 0 to 10) and business regulations (index from 0 to 10). A higher level of these indices means lower market regulation. The related data are obtained from Gwartney, Lawson, and Hall (2019). Furthermore, we control economic globalization indicators, such as globalization of financial flows (the index of financial globalization) and globalization of trade (the index of trade globalization). Both indices are defined from 0 to 100, and the related data are obtained from Gygli et al. (2019).

Table 1 provides brief descriptive statistics of the data set and defines variables in detail and their sources (the dependent and the explanatory variables are stationary).

Descriptive Summary Statistics.

In Table 2, we provide a correlation matrix for leading indicators in the data set.

Correlation Matrix.

Note: CITT = capital investment in travel and tourism; CITTPC = capital investment in travel and tourism per capita; GPR = geopolitical risk; GDP = gross domestic product.

As shown in Table 2, the correlation between CITT and CITTPC is positive, as expected. There is a negative correlation between capital investments in travel and tourism (CITT and CITTPC) and GPR index. Investments are positively associated with the per capita GDP, and negatively correlated with the lending interest rates. Overall, the correlations are in line with theoretical expectations. However, the GPR index is positively correlated with per capita GDP, and negatively correlated with interest rates. Per capita GDP is negatively correlated with lending interest rates, as expected.

Model and Estimation Procedures

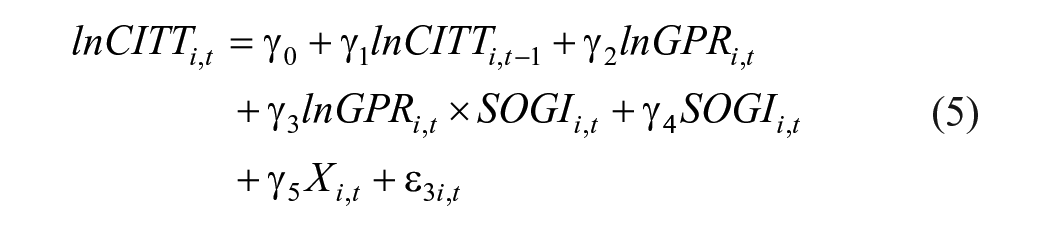

Following the central hypothesis, we can write down the empirical models as such:

In equations (1) to (4), i denotes countries, and t represents the years.

We estimate the models from equations (1) to (4) mainly via the fixed effects (FE) estimations. Besides, we use the bias-corrected least square dummy variable (LSDVC) estimator of Bruno (2005). The LSDVC estimator can solve potential problems due to endogeneity bias and reverse causality (Bilgin, Gozgor, and Karabulut 2020; Bruno 2005; Demir, Gozgor, and Paramati 2019). Here, "bias correction" is started by the Arellano–Bond method. Given that the data set includes 18 countries (N) and 23 years (T), that is, N<T, dynamic panel data estimation procedures will provide inefficient findings because the number of cross sections is less than 25 (Bruno 2005). We treat the FE estimations’ results to the benchmark results and run the LSDVC estimators in a robustness check.

Furthermore, to test hypotheses 2, 2a, 2b, and 2c, we formulate the following model:

where

Empirical Results

Benchmark Regressions for CITT

We report the results for CITT in Table 3. Columns 1 and 2 consider both the per capita income and the lending interest rates as the main control variables.

Capital Investment in Travel and Tourism: FE Estimations (1995–2018).

Note: The dependent variable is the log CITT. The robust standard errors are in parentheses.

p < 0.01, **p < 0.05, *p < 0.10.

All the coefficients of GPR are significant and indicate that the index of the GPR negatively affects CITT. For example, column 1 illustrates the baseline model results (model 1) and reports that a 1% rise in the GPR index yields a 0.21% reduction in CITT at the significant level of 1%. This suggests that tourism investment is sensitive to geopolitical risk fluctuations: the higher the geopolitical risks, the lower the capital investment in tourism, consistent with our central hypothesis. The lagged GPR index results are also in line with the current index of the GPR, which show the negative impact on CITT, but with a smaller magnitude of coefficients in general. In other words, the negative impact lasts and extends into the future, consistent with Tiwari, Das, and Dutta (2019), which find long-run implications of GPR.

As long as per capita income surges, investments in tourism rise as expected in terms of control variables. Moreover, lending interest rates are negatively associated with the CITT since a lower interest rate makes capital cheaper. These results for the control variables are also in line with previous studies, such as Demir, Gozgor, and Paramati (2019).

Benchmark Regressions for CITTPC

We provide the findings for CITTPC in Table 4. Similar to Table 3, columns 1 and 2 consider both the per capita GDP and lending interest rates as the main controls.

Capital Investment in Travel and Tourism per Capita (CITTPC): FE Estimations (1995–2018).

Note: The dependent variable is log CITTPC. The robust standard errors are in parentheses. FE = finite element.

p < 0.01, **p < 0.05, *p < 0.10.

All results demonstrate that the index of the GPR is negatively associated with the CITTPC. The lagged GPR index findings provide similar results concerning the negative impact of lnGPRt–1 on the CITTPC, again consistent with Tiwari, Das, and Dutta (2019). Overall, the adverse effects of both the lagged and current GPR on capital investments in travel and tourism are robust by different models. There is strong supportive evidence for our central hypothesis 1.

The Role of Social Globalization

We further examine the moderating effect of social globalization on the relationship between geopolitical risks and tourism investment. Table 5 presents the detailed sensitivity analysis for the FE estimations.

Including the Role of Social Globalization: FE Estimations (1995–2018).

Note: Main control variables are included. Standard errors are in parentheses. FE = finite element

p < 0.01.

Following previous studies (e.g., Gozgor 2018; Potrafke 2015), we include the overall social globalization indices as well as its subindices: the so-called de jure (policy-related indicators) and de facto (outcome-oriented indicators) measures of social globalization. Furthermore, we add three subindices of these measures: (1) interpersonal globalization, (2) informational globalization, and (3) cultural globalization. Overall, we include 18 different social globalization measures, defined by Gygli et al. (2019).

As shown in Table 5, the impact of the current coefficient and lagged coefficient of the GPR index on the capital investments in travel and tourism (measured by both CITT and CITTPC) is negative, regardless of which type of social globalization indicators we include in the model. Moreover, all coefficients of the GPR indicators are statistically significant. In short, our baseline finding is robust by including 18 indicators of social globalization.

We run the benchmark model by including an interaction term between GPR and social globalization and provide the findings in Table 6. From column 1 to 6, we run the same model (model 5) but with different social globalization indicators.

Capital Investment in Travel and Tourism (CITT): FE Estimations (1995–2018).

Note: The dependent variable is the log CITT. KOFSOGI = KOF index of social globalization (overall); KOFSOGIDF = social globalization (de facto); KOFSOGIDJ = social globalization (de jure); KOFIPGI = interpersonal globalization; KOFINGI = informational globalization; KOFCUGI = cultural globalization; FE = finite element

The robust standard errors are in parentheses.

p < 0.01, **p < 0.05, *p < 0.10.

In Table 6, the unique effect of GPR on tourism investment is represented by everything that is multiplied by GPR in the model. For example, considering the first model (Table 6, column 1), the total effect of the GPR associated with a certain level of KOFSOGI is represented as (–0.784 + 0.009 × KOFSOGI). To be more specific, the results indicate that for each one-unit rise in GPR, the adverse impact of GPR on tourism investment (i.e., –0.784) is reduced by the effect of social globalization (i.e., 0.009 × KOFSOGI), suggesting that the unique effect of GPR on tourism investment varies with different levels of social globalization. Given KOFSOGI has a minimum value of 20.80, an average value of 59.36, and a maximum value of 86.57 (see Table 1), if GPR rises by 1 unit, the tourism investment therefore decreases by 60% at most (i.e., −0.784 + 0.009 × 20.80 = −0.60) and by 0.5% at least (i.e., −0.784 + 0.009 × 86.57 = −0.005), and on average drops by 25% (i.e., −0.784 + 0.009 × 59.36 = −0.25). According to the results, the level of social globalization does neutralize the adverse impact of GPR on tourism investment, and the greater the degree of social globalization, the more adverse the effect it would offset. This supports our main hypothesis, that is, though investors tend to reduce capital investment in tourism when there are geopolitical risks, social globalization ameliorates this tendency. The utility of investors, as human beings, consists of money profits as well as altruistic empathy. Furthermore, all the interaction term coefficients are significantly positive in Table 6, indicating that this conclusion is empirically and consistently supported for social globalization, regardless of how they are measured.

Additionally, the interaction term of informational globalization with GPR (Table 6, column 5) has a coefficient of 1.1%, larger than the interaction term of interpersonal globalization with GPR (0.7%) and cultural globalization (0.7%). This suggests that in-time, accurate, and easy-to-access information (informational globalization) plays an essential role in soothing the adverse impact of geopolitical risks, in comparison to close acquaintances (interpersonal globalization) and mutual respect and understanding (cultural globalization). Overall, the findings support hypotheses 2a, 2b, and 2c.

Interestingly, the results also show that social globalization negatively affects tourism investment and the effect of GPR reduces the adverse impact. For example, in column 1 of Table 6, the results indicate that for each one-unit rise in KOFSOGI, the adverse impact of KOFSOGI on tourism investment improves with increasing GPR levels (i.e., –0.043 + 0.009 × GPR). The GPR index’s logarithm ranges from a minimum value of 3.576 to a maximum value of 5.565, with a mean value of 4.551 (see Table 1). Therefore, if KOFSOGI increases by one unit, the tourism investment therefore decreases by 1.1% when GPR is the lowest (i.e., –0.043 + 0.009 × 3.576 = −0.011) and falls by 0.2% when GPR is at an average level (i.e., 0.043 + 0.009 × 4.551 = −0.002), but increases by 0.71% when GPR is the highest (i.e., 0.043 + 0.009 × 5.565 = 0.0071). The break-even point is when the logarithm of the GPR index is 4.77. It could be that social globalization, to some extent, deters the desire to travel around. Thus, the decreasing demand dampens the incentive to invest in tourism. For example, the convenience of visiting a museum or a natural spot via Cloud (information globalization), which claims to provide an immersive experience, could put people off taking a real journey.

Furthermore, infrastructure for social globalization is an attractive investment opportunity from the investors’ perspective, but a promising rival for tourism investment. Geopolitical risks could affect the investment decisions between tourism and social infrastructure. Social infrastructure usually requires large long-term dedicated investment while tourism, in comparison, usually asks for short-term investment, which expects quick payback. Given hot money is always searching for investment opportunities, increasing geopolitical risks could divert investment from social infrastructure to tourism.

To further examine our results, we also run the benchmark regressions for CITTPC and provide the findings in Table 7. Table 7 reports findings similar to Table 6, which confirms that our findings are robust at both aggregate and personal levels.

Capital Investment in Travel and Tourism Per Capita (CITTPC): FE Estimations (1995–2018).

Note: The dependent variable is the log CITTPC. KOFSOGI = KOF index of social globalization (overall); KOFSOGIDF = social globalization (de facto); KOFSOGIDJ = social globalization (de jure); KOFIPGI = interpersonal globalization; KOFINGI = informational globalization; KOFCUGI = cultural globalization; FE = finite element.

The robust standard errors are in parentheses. ***p < 0.01, **p < 0.05, *p < 0.10.

Robustness Checks

Results of LSDVC Estimations

In Tables 8 and 9, we provide findings of the LSDVC estimator of Bruno (2005). We deliver results for CITT in Table 8 and the findings for CITTPC in Table 9.

Capital Investment in Travel and Tourism (CITT): LSDVC Estimations (1995–2018).

Note: The dependent variable is log CITT. The robust standard errors are in parentheses, and the p values are in brackets. LSDVC = bias-corrected least square dummy variable.

p < 0.01.

Capital Investment in Travel and Tourism per Capita (CITTPC): LSDVC Estimations (1995–2018).

Note: The dependent variable is log CITTPC. The robust standard errors are in parentheses, and the p values are in brackets. LSDVC = bias-corrected least square dummy variable.

p < 0.01.

According to the results from Tables 8 and 9, the required test results are observed to provide the LSDVC method’s efficiency. Specifically, according to the findings of the Sargan statistic, the over-identifying restriction condition is satisfied. According to the results of the Arellano–Bond test, there is a significant first-order autocorrelation. Nevertheless, the validity of the second-order autocorrelation is rejected.

Similar to the FE estimations, we observe that the lagged dependent variable’s estimated coefficient is positive and significant at the conventional statistical level. All LSDVC estimation results indicate that the GPR index negatively affects the capital investments in travel and tourism. Overall, we also observe that those baseline findings are robust by different estimation techniques.

Additional Control Variables

Following the previous studies (e.g., Bilgin, Gozgor, and Karabulut 2020), we include several other indicators to affect capital investment in general. We report the findings of FE estimations in Appendix I.

We include the domestic credit provided by the financial sector, the urban population, the total population, trade openness, financial globalization, and trade globalization. We also add market regulation indicators, such as the indices of economic freedom and business regulations.

According to the findings, the impact of geopolitical risks (measured by both the current coefficient and the GPR index’s lagged coefficient) on capital investments in travel and tourism (measured by both CITT and CITTPC) remains negative. Therefore, our primary evidence is robust by adding various additional control variables.

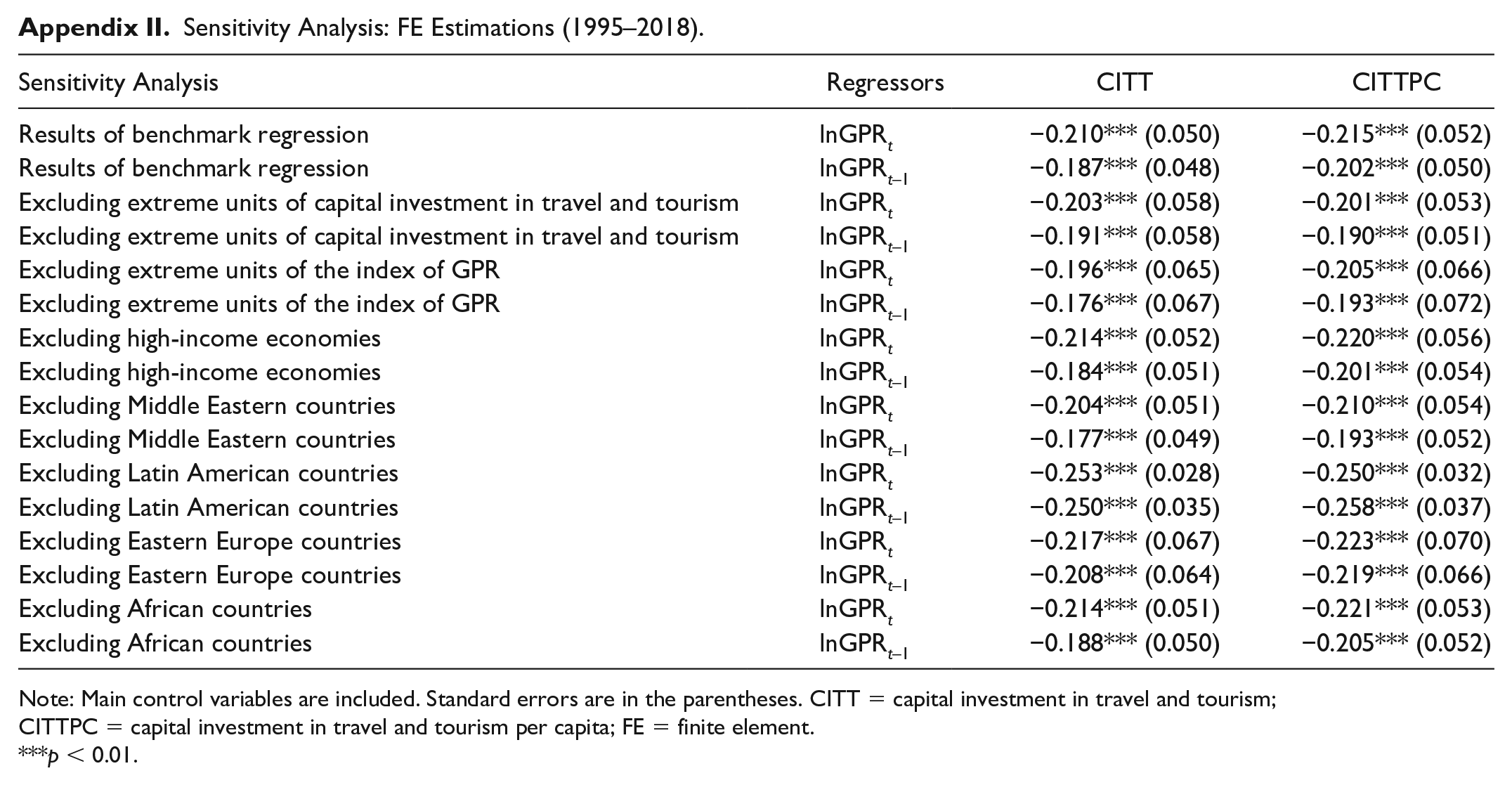

Sensitivity Analyses

Following previous studies (e.g., Bilgin, Gozgor, and Karabulut 2020; Gozgor et al. 2019), we implement various sensitivity checks. We report the related findings in Appendix II.

First, we exclude the dependent variables’ extreme values (CITT and CITTPC) and the primary variable of interest (GPR index). Following Gozgor et al. (2019), we define the extreme values as two standard deviations’ distance from the average value. Second, we exclude some specific countries from the data set since they may determine our main findings. Therefore, we exclude (1) high-income countries, which are defined by the World Bank (i.e., Israel, Saudi Arabia, and South Korea), (2) Middle East countries (i.e., Israel and Saudi Arabia), (3) Latin American countries, (4) Eastern European countries (i.e., Russia, Turkey, and Ukraine), (5) African countries (i.e., South Africa).

According to the findings, the impact of the current coefficient and lagged coefficient of the GPR index on the capital investments in travel and tourism (measured by both CITT and CITTPC) are found to be negative. Moreover, the coefficients of the GPR indices are statistically significant at the 1% level. Overall, the evidence is robust by excluding various countries from the data set.

Conclusions and Discussion

Capital investment is vital for sustainable tourism growth, particularly in times of crisis. Our work’s main objective was to examine the effect of geopolitical risks on capital investment in tourism and how social globalization influences the impact. To our knowledge, this is the first cross-country study in the literature to investigate the relationship between geopolitical risks and tourism supply (investment) in developing economies, where geopolitical risks are usually severer than developed countries. Specifically, we examine the impacts of geopolitical risks on capital investments in travel and tourism in 18 developing economies between 1995 and 2018. Based on a text-search algorithm (Caldara and Iacoviello 2019), we develop a new index of geopolitical risks by searching for "keywords" through the leading newspapers. We find that geopolitical risks negatively affect tourism supply (capital investment in travel and tourism). The results were robust regardless of different capital investment measures in travel and tourism, and different econometric techniques were used by including various control variables and excluding outliers.

Furthermore, this is also the first study to test the moderating role of social globalization between geopolitical risks and tourism investment. We find that social globalization significantly alleviates the adverse impact of geopolitical risks on tourism investment, regardless of which indicator is adopted. Among all indicators, in-time, accurate, and easy-to-access information (informational globalization) plays an essential role in soothing the adverse impact of geopolitical risks, in comparison to close acquaintances (interpersonal globalization) and mutual respect and understanding (cultural globalization).

Overall, geopolitical risks are harmful to the travel and tourism sectors’ investment, consistent with our central hypothesis. Therefore, the main policy implication of this article is to advise policy makers to be vigilant about the media atmosphere of geopolitical risks, be fully aware of its adverse effect on tourism investment, and always have a plan B, such as providing incentives (e.g., subsidies or tax relief) for footloose capital investors to maintain the level of capital investments in travel and tourism. Second, as social globalization plays a moderating role and alleviates the negative effect of geopolitical risks on tourism supply, then policy makers in the tourism industry are advised to have a scheme in mind to promote social globalization, along with economic globalization, as a precautionary step against possible turbulent times, especially for those emerging countries that are more susceptible to geopolitical risks. Furthermore, economy-wise, informational globalization should have priority provided the resources are limited. Our findings are limited to 18 developing economies, where the data for the index of the geopolitical risks are available. Future studies on this subject can focus on each developing economy by using time-series techniques.

The current COVID-19–related uncertainty can change the effects of geopolitical risks on tourism supply in several ways, which can be empirically tested in future studies. First, the pandemic has increased restrictions on people’s movements and goods between countries, which affects the demand for tourism and, ultimately, the tourism supply. Second, the spread of COVID-19 is also related to geography. At this stage, small countries and islands have some advantages over the spread of COVID-19; however, these countries are more vulnerable to COVID-19–related uncertainty shocks. Therefore, the impact of COVID-19 on the tourism supply could be moderated by the country’s size and geography. Third, for certain countries (e.g., Spain, Italy, Turkey), tourism is of strategic importance for the national economy. Governments may increase their role in the tourism sector. As such, COVID-19 can change the tourism sector’s dynamics due to the government’s role. Fourth, COVID-19 can accelerate humanitarian crises (e.g., food insecurity) because of the potential decline of foreign aid. Similarly, the long-standing military conflicts can be exacerbated as a result of COVID-19, which will harm the tourism sector’s investments. As a result, there can be a double jeopardy effect on both geopolitical risks and global tourism investment owing to some governments and companies’ knee-jerk reactions to this global crisis without due consideration and coordination.

Disease risk and geopolitical risk, in terms of their effect on tourism investment, are similar. In the tourism sector, both can be interpreted as worries or concerns for safety, leading to social distance, which eventually affects tourism investment. In other words, both the risks of disease and geopolitics work with a similar underlying mechanism in the tourism sector. Thus, our study helps to reveal the mechanism that can improve our understanding of the COVID-19 effect in the tourism sector. Particularly, the role of social globalization revealed in our study provides an important implication of social globalization’s potential alleviation effect on the global pandemic’s negative impact on tourism investment. Finally, it is important to note that the GPR index is biased toward the Western media as the news mainly comes from the major mainstream media. Given these media tend to focus on certain political issues in developing countries, we should always treat the GPR index with a certain degree of caution.

Footnotes

Appendix

Sensitivity Analysis: FE Estimations (1995–2018).

| Sensitivity Analysis | Regressors | CITT | CITTPC |

|---|---|---|---|

| Results of benchmark regression | lnGPR t | −0.210*** (0.050) | −0.215*** (0.052) |

| Results of benchmark regression | lnGPRt–1 | −0.187*** (0.048) | −0.202*** (0.050) |

| Excluding extreme units of capital investment in travel and tourism | lnGPR t | −0.203*** (0.058) | −0.201*** (0.053) |

| Excluding extreme units of capital investment in travel and tourism | lnGPRt–1 | −0.191*** (0.058) | −0.190*** (0.051) |

| Excluding extreme units of the index of GPR | lnGPR t | −0.196*** (0.065) | −0.205*** (0.066) |

| Excluding extreme units of the index of GPR | lnGPRt–1 | −0.176*** (0.067) | −0.193*** (0.072) |

| Excluding high-income economies | lnGPR t | −0.214*** (0.052) | −0.220*** (0.056) |

| Excluding high-income economies | lnGPRt–1 | −0.184*** (0.051) | −0.201*** (0.054) |

| Excluding Middle Eastern countries | lnGPR t | −0.204*** (0.051) | −0.210*** (0.054) |

| Excluding Middle Eastern countries | lnGPRt–1 | −0.177*** (0.049) | −0.193*** (0.052) |

| Excluding Latin American countries | lnGPR t | −0.253*** (0.028) | −0.250*** (0.032) |

| Excluding Latin American countries | lnGPRt–1 | −0.250*** (0.035) | −0.258*** (0.037) |

| Excluding Eastern Europe countries | lnGPR t | −0.217*** (0.067) | −0.223*** (0.070) |

| Excluding Eastern Europe countries | lnGPRt–1 | −0.208*** (0.064) | −0.219*** (0.066) |

| Excluding African countries | lnGPR t | −0.214*** (0.051) | −0.221*** (0.053) |

| Excluding African countries | lnGPRt–1 | −0.188*** (0.050) | −0.205*** (0.052) |

Note: Main control variables are included. Standard errors are in the parentheses. CITT = capital investment in travel and tourism; CITTPC = capital investment in travel and tourism per capita; FE = finite element.

p < 0.01.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.