Abstract

Total Quality Management (TQM) is a comprehensive approach that helps organizations succeed in maintaining high standards of operations and improving financial performance. The study examines the association between TQM and hospital financial performance. A cross-sectional survey using a previously validated questionnaire was conducted among hospital leaders, including directors, managers, heads of departments, and supervisors in Jordan. The sample was 172 leaders. Descriptive statistics were used to summarize variables of interest and multivariable logistic regression was employed to understand the association between TQM and financial performance in university teaching hospitals. The study found that implementation of TQM and financial performance among university teaching hospitals are moderate based on hospital leaders’ perspectives. Moreover, the high implementation of TQM in university teaching hospitals is more likely to be associated with hospital financial performance’s effectiveness than low implementation. However, the interaction of higher management positions and teamwork appears to have a positive association. Moderate and high teamwork increases the association of higher management positions, such as supervisory role with effective financial performance (aOR = 50.3, P = .004 and aOR = 94, P = .031, respectively). High effective communication of hospitals’ goals and missions to patients and connection with patients through a variety of platforms was associated with a higher odds ratio of effective hospital financial performance (OR = 20.3, P = .023). The study focused on university teaching hospitals; a setting underrepresented in empirical TQM literature. Moreover, it measured the association between TQM and financial performance, a narrower and more tangible outcome than overall quality or satisfaction. There is an association between TQM and the financial performance of university teaching hospitals. The study draws the attention of university teaching hospital managers to the importance of implementing TQM to enhance the financial performance and its outcomes.

Highlights

● There is an association between TQM and the financial performance of university teaching hospitals.

● University teaching hospitals need to improve the implementation of all TQM concepts.

● Implementing TQM concepts enhances the financial performance and outcomes of university teaching hospitals.

Introduction

The Total Quality Management (TQM) model has gained widespread acceptance in the last 30 years. The organization’s resources and capacity to create a connection between its performance and sustainable development practices are the main focus of the resource-based view of a company. 1 A conceptual framework that clarifies the connection between TQM and organizational performance is introduced in a study by Li et al. 2 The environmental, social, and economic facets of business sustainability are significantly and favorably impacted by TQM adoption. Because TQM has a strong emphasis on continuous improvement, it reduces costs by making effective use of internal resources. The Institute of Medicine (IOM) has defined quality as “the degree to which health care services for individuals and populations increase the likelihood of desired outcomes and are consistent with current professional knowledge.” 3 Whereas, TQM is defined “as an integrated process involving all systems and employees in a continuous effort to improve quality, reduce cost, and enhance service to [the] customer.” 4

Improving the business’s economic sustainability has several benefits, including increased customer satisfaction, reduced errors, and improved operational effectiveness—all of which are attained by using TQM. 1 The social aspect of sustainability refers to the moral actions that companies do to advance societal welfare. 5 A clear link has been discovered by researchers between TQM and the long-term financial viability of companies. 6 A study examined the impact of applying TQM on institutions’ performance. It compared each institution’s performance to a control group. Easton and Jarrell’s study (1998) showed improved institutions’ performance with more advanced TQM implementation. 7

Applying TQM concepts influences employees’ performance, which in turn directly affects the whole organization’s performance. 8 Studies revealed that TQM not only greatly influences organizational performance, especially financial performance, but also the relationship between customer loyalty, and financial performance.9,10 Managers in the healthcare industry utilize a quality approach to implement and maintain sustainability and a competitive advantage in their organizations. Several studies have examined the relationship between implementing TQM concepts and performance in the healthcare sector and they found that TQM improve the performance.11 -14 Prior evidence suggest that TQM increases efficiency, boosts growth, and increases profitability. 15 Some of the best solutions used for increasing incomes were training, and empowering staff, removing unnecessary activities, standardizing working processes, and improving the work environment. Healthcare organizations need to measure the effectiveness of TQM regarding financial performance because most investments are justified based on their impact on financial measures. In addition, the financial performance measures directly reflect whether the healthcare organization’s implementation of the strategy leads to generating wealth by contributing to the healthcare organization’s value. Moreover, organizational characteristics such as the size of the organization, capital intensity, diversification of services, and implementation all influence the gains from TQM.

While TQM has shown positive outcomes in many sectors, there are limitations. Pros include structured continuous improvement, enhanced staff engagement, and improved service quality and financial performance. However, cons involve the significant resource investment required, resistance from staff, cultural misalignment, and the potential for implementation fatigue or superficial adoption. 16

Although many studies in different countries have examined the relationship between TQM and performance across different sectors, there is still a gap in the context of university teaching hospitals, specifically in developing countries such as Jordan. The current literature focuses on general organizational performance. Hence, this study fills a significant gap by providing evidence on the association between TQM and financial performance in academic healthcare settings, this helps hospital managers align quality initiatives with financial sustainability. Therefore, the objective of this study is to examine the association between TQM and university hospital financial performance.

Methods

The study employed a cross-sectional design and abided by the STROBE guidelines; see Appendix. The study was conducted on a sample of 2 university teaching hospitals from Jordan during the period from November 2023 to February 2024. The study population was all university teaching hospital managers or leaders, such as directors, managers, heads of departments, and supervisors. The inclusion criteria encompassed all healthcare professionals working in university teaching hospitals who held managerial or leadership positions. A total of 236 individuals met these criteria. The study questionnaire was randomly distributed among this population. Participation in this study was voluntary. One hundred seventy-two participants completed the questionnaire. To estimate the percentage of high financial performance with a 95% confidence level, 5% margin of error, estimated percentage of high final performance of 50%, and population size of 236, a minimum of 147 participants was required (http://www.raosoft.com/samplesize.html). Therefore, the study sample size was representative of the study population.

The study questionnaire is valid and reliable. It was adopted from previous studies.17,18 The questionnaire includes demographic questions such as age, gender, education level, position, and years of experience, and 17 statements regarding financial performance distributed among 3 categories, which were budget allocation, human resources, and process and procedures. The classification of the level of effectiveness of the financial performance was based on the mean score. Ineffective means the mean score is 1 to 2.33; Moderate means the mean score is 2.33 to 3.67; Effective means the mean score is 3.68 to 5.00. The final section had 23 statements about the implementation of TQM concepts. There were 5 categories under the last section, which were teamwork among employees, management commitment, patient-focused organization, employee involvement in decision-making, and effective communication. The choices were strongly agreed, agree, neutral, disagree, and strongly disagree. We used the Statistical Package for Social Scientists (SPSS) program for data analysis. Descriptive statistics such as count, percentage, mean, and standard deviation were used. The classification of TQM implementation was based on the mean score. The TQM implementation was classified as low, moderate, and high. Low means the mean score is 1 to 2.33; Moderate means the mean score is 2.33 to 3.67; high means the mean score is 3.68 to 5.00. The study used descriptive statistics to summarize and determine relationships among variables of interest.

In terms of association, an univariable model was used to estimate the association between TQM and university hospital financial performance. Next, we used a multivariable logistic regression to predict the effectiveness of hospital financial performance from the influence of TQM implementation while adjusting for staff characteristics. However, we break down TQM into subdomains of teamwork among employees, management commitment, patient-focused organization, employee involvement in decision-making, and effective communication. We employed logistic regression because our outcome variable of interest (effectiveness of hospital financial performance) is a nominal variable that has more than 2 levels, namely, budget allocations, human resources, and processes and procedures. Finally, we employed a multivariable logistic regression model to assess the effect of staff characteristics and TQM on the perceived effectiveness of hospital financial performance, with the interaction between teamwork culture and the occupation of hospital staff. The aim here was to test the hypothesis that the association between the positions of leadership staff on the effectiveness of hospital financial performance was different for the levels of teamwork. We categorized both TQM and financial performance as ordinal: ineffective, moderate, and effective.

Results

Descriptive Analysis

One hundred seventy-two participants completed the questionnaire. The demographic characteristics of the study sample are summarized in Table 1, which shows male participants were 59.9%. There were more participants in the age group 41 to 50 years old (44.2%). Half of the participants were supervisors (50%), while participants with a bachelor’s degree comprised 75%. There were more participants with experience of more than 15 years (39.5%).

Numbers and Percentages of Demographic Variables of the Participants.

Table 2 (Panel A) shows the level of effectiveness of financial performance domains as perceived by hospital leaders. The classification of the financial performance domains was based on the level of effectiveness (ineffective, moderate, and effective) based on the mean score as perceived by hospital leaders. The mean score for the financial performance domains together was 3.52 (SD = 0.67), implying that the level of financial performance effectiveness was moderate. In addition, the effectiveness of each domain of effective financial performance was also moderate in the participating hospitals.

Level of Effectiveness of Financial Performance and Implementation of TQM Domains as Perceived by University Teaching Hospitals Leaders.

The mean score is 1 to 2.33 (Ineffective); The mean score is 2.33 to 3.67 (Moderate); The mean score is 3.68 to 5.00 (Effective).

The mean score is 1 to 2.33 (Low); The mean score is 2.33 to 3.67 (Moderate); The mean score is 3.68 to 5.00 (High).

Table 2 (Panel B) shows the level of implementation of TQM domains as perceived by hospital leaders. The classification of the TQM domains was based on the level of implementation (low, moderate, and high) based on the mean score as perceived by hospital leaders. The mean score for TQM domains together was 3.55 (SD = 0.78), implying the level of TQM implementation was moderate. The healthcare leaders believe that they were implementing TQM at a moderate level. In addition, each domain of TQM was also implemented moderately in the participating hospitals.

Base Model

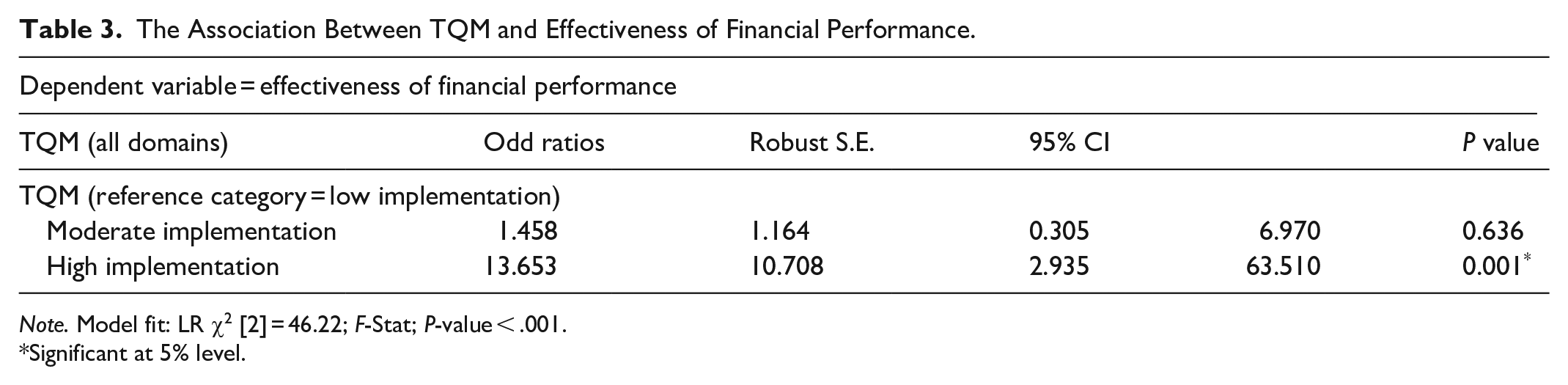

The estimated base bivariate model of the influence of TQM implementation on the effectiveness of hospital financial performance. The regression results in Table 3 show that high implementation of TQM in hospitals is more likely to be associated with the effectiveness of hospital financial performance compared with low implementation.

The Association Between TQM and Effectiveness of Financial Performance.

Note. Model fit: LR χ2 [2] = 46.22; F-Stat; P-value < .001.

Significant at 5% level.

Model Adjusting for Staff Characteristics and TQM

Next, we adjusted the association between staff characteristics and sub-domains of TQM and the perceived effectiveness of hospital financial performance. We break down TQM into subdomains of teamwork, customer/patient-focused organization, goals, effective communication, and employee involvement. As the bivariate model in Table 4 shows high effective communication of hospitals goals and missions to patients and connection with patients through a variety of platforms was marginally associated with higher odds of effective hospital financial performance (OR = 7.834, P = .054, 95% CI: 0.962-63.812). Compared with less experienced employees, mid-career experience was associated with more effective hospital financial performance. (OR = 5.89, P = .049, 95% CI: 1.007-34.402). Hospital 2 was associated with a 62% lower odds of effective hospital financial performance compared with Hospital 1 (OR 0.381, P = .019, 95% CI 0.170-0.854).

The Association Between TQM and Staff Profiles on Efficacy of Financial Performance.

Note. Model fit: LR χ2 [2] = 60.40; F-Stat; P-value < 0.001.

Significant at 5% level.

Significant at 10% level.

A Model With Interaction

Next, we implemented a model of analysis of the association between staff characteristics and TQM and the perceived effectiveness of hospital financial performance, with interaction between teamwork culture and the occupation of hospital staff. As shown in Table 5, the odds of effective financial performance are lower for supervisors compared with general directors (OR = 0.007, P = .014 < .05, 95% CI: 0.001-0.369). Surprisingly, the odds of effective financial performance are also lower for moderate teamwork compared with low teamwork (OR = 0.029, P = .029, 95% CI: 0.001-0.698). However, the interaction of higher management positions and teamwork appears to have a positive association. Moderate and high teamwork have a statistically significant moderating association by increasing the association of higher management positions, especially supervisors, with effective financial performance compared to general directors (P = .004 and P = .031, respectively).

Examining the Influence and Interactions of TQM and Staff Profiles on Efficacy of Financial Performance.

Note. R2 = 28; Model fit: LR χ2 [2] = 72.20; F-Stat; P-value < 0.001. × implies the interaction of variables.

Significant at 5% level.

Significant at 10% level.

Discussion

The results showed that both the effectiveness of financial performance and the implementation of TQM were moderate in the Jordanian hospitals that participated in this study. In particular, our study suggests that perceived effective hospital TQM is associated with higher odds of effective hospital financial performance. Thus, the implementation of TQM in hospitals is more likely to be associated with the effectiveness of hospital financial performance compared with low implementation. These findings may indicate how important TQM is in enhancing the quality of hospital services, especially from the financial performance side. TQM implementation supports financial departments in helping hospitals achieve their objectives of becoming high-performing institutions. However, hospitals in Jordan do not give enough attention to TQM implementation.17,18 Effectively implementing the TQM concept aids the financial department in solving issues that hinder procedures in the department and enhances the effectiveness of the department. In particular, the foregoing results are consistent with many studies conducted in different sectors and showed that TQM has impact on improving service quality, especially in financial success.19,20 On the other hand, a study by Tarim and Sonmezturk Bolatan found that TQM implementation does not directly influence financial performance in healthcare institutions. However, the same study found an indirect influence of TQM on financial performance. 21

The odds of effective financial performance are lower for supervisors compared with general directors. This result is intuitive given that general directors use financial information to make informed decisions about the day-to-day management of hospitals. This finding may be consistent evidence that general directors support and improve employees’ engagement through performance management to achieve the organization’s goals and objectives. Compared with less experienced employees, mid-career experience was associated with the perceived higher odds of effective hospital financial performance. This result is consistent with a study that showed a positive influence of job experience on financial performance matters.22,23

The study results suggest that management commitment was associated with the highest odds of perceived effective financial performance. Management commitment is a requirement to support an inspiring vision, and values that lead staff and establish a strategic plan that is understood by all staff. This requires a comprehensive understanding and belief in the TQM concept by supervisors, leaders, and top management in order to reveal their beliefs, understanding, and commitment through their continuous work on TQM in the organization. In the current healthcare environment, managers possess the capability to provide support to push quality activities to the highest level of standard performance. Studies have showed that healthcare managers and leaders have a responsibility to their hospitals to support healthcare policies to offer a high level of quality services to their community.24,25

Results of our study also suggest that focusing on patients is associated with higher perceived effectiveness of financial performance. Hospitals and other organizations depend on their patients/customers to achieve their goals and objectives. As a result, university teaching hospitals need to understand current and future patients’ and customers’ needs, and then improve their services to meet those needs and exceed their expectations. TQM aims to accomplish patients/customers’ needs and exceed their expectations by providing service based on their desires at the minimum cost and at a suitable time. Gavareshki et al fond that reaching customers’ satisfaction is a good indicator of implementing TQM successfully. In modern institutions, customers are the priority. Therefore, institutions should start to implement TQM strategies to reach customer satisfaction. 26 In the healthcare sector, if hospitals have considered the assumption, that patients are at a strong point to evaluate the quality of healthcare services, they should rely on patient satisfaction survey results as the foundation for quality improvement of their services. Toke and Kalpande found that it is important for managers and decision-makers to understand the benefit of TQM and its role in enabling patient satisfaction within their hospitals. 27

Our study suggests that an effective teamwork culture was more likely to be associated with higher perceived effectiveness of financial performance. Effective implementation of TQM requires teamwork and cooperation among an organization’s staff. Nowadays, many organizations have a top-down structure that requires supervision from managers and implementation from the staff to achieve specific projects or objectives. Snongtaweeporn et al refer to the fact that high performance required effective teamwork among all levels of the organization, such as managers, supervisors, information technology staff, finance staff, and others. 28 University teaching hospitals need to create quality improvement teams that include members from different backgrounds. Each team needs representatives from the relevant departments. Kamaruddin et al found that teamwork is an effective key for promoting quality activities and successful achievement. 29 Hospital managers should focus on creating multidisciplinary teams, maintaining effective staff communication, and managing continuous improvement in their hospitals. However, the interaction of higher management positions and teamwork appears to have a positive association. Moderate and high teamwork have a statistically significant moderating effect by increasing the association of higher management positions, especially supervisors, with financial performance compared to general directors. This makes sense because supervisors are in direct contact with employees and because of the positive role of teamwork in employee performance.

All employees of the hospitals should be involved and engaged in quality activities. Aburayya et al mentioned that organizational employees affect the failure and success of quality procedures in different ways, just as managers can. 24 Healthcare workers should be involved in implementing TQM in their institutions. All of them need to carry up the responsibility of providing high quality healthcare services. Staff involvement and empowerment are elements of successfully implementing TQM. A study found that deficit of experience and unclear knowledge regarding TQM implementation, changing conditions of environmental work, and insufficient linkages between staff incentives and their real performance are considered barriers to TQM implementation in a successful manner in healthcare institutions. 30

Effective and open communication among staff and managers creates a gradual commitment to TQM. This leads to improved patient care quality, which can be achieved by creating communication channels within multidisciplinary teams in organizations. Communication between managers and their staff in the healthcare sector is a primary concern in TQM to create a sustained organization. Effective communication of hospital goals and missions to patients and connection with patients through a variety of platforms was associated with higher odds of effective financial performance. This concords with evidence that revealed communication strategies were associated with financial performance and relationship satisfaction. 31 Healthcare organizations need to focus on TQM concepts, to achieve their financial goals.

Strengths and Limitations

This study is among the pioneering studies that examine the association between TQM and financial performance in university teaching hospitals. Furthermore, the study demonstrated the strong association of TQM and university teaching hospitals’ financial performance. As such, hospital managers will find the study’s findings useful in enhancing their hospitals’ financial performance.

On the other hand, there are a few limitations that should be pronounced. Firstly, since the 2 hospitals were in Jordan, generalizability to other hospitals within the country or across countries may be limited. Inclusion or comparison with other facilities may present different distributions and associations between TQM and financial performance. Secondly, the 2 hospitals were teaching hospitals. This means the results may not apply to other types of hospitals. Thirdly, we employed a cross-sectional study, and so no claim of cause-and-effect relationship.

Conclusion

The study aimed to examine the association between TQM and hospital financial performance based on university teaching hospital leaders’ views. While adjusting for the effect of staff characteristics and whether the teamwork culture has association with perceived university teaching hospitals’ effectiveness in financial performance varied with the occupation of the hospital staff. The study found that there was a moderate implementation of all TQM concepts, which include teamwork, management commitment, customer/patient-focused organization, employee involvement, and effective communication. Moreover, the effectiveness of all financial performance domains (budget and financial allocations, human resources, and process and procedures) was moderate. The study also found that high implementation of TQM in university teaching hospitals is more likely to be associated with the effectiveness of financial performance compared with low implementation.

University teaching hospitals need to improve the implementation of all TQM concepts. Managers need to be committed to improving the process or raising the level of healthcare service quality. Customers can assess the level of service quality that was provided to them. Therefore, university teaching hospitals need to align their services with their patients’ needs and expectations to make them satisfied with the services provided. The availability of a diversity of knowledge, skills, and experience in teamwork helps address a variety of complex issues in healthcare services. Teamwork can also increase opportunities to address issues across departmental boundaries. Therefore, university teaching hospitals need to rely on teamwork to create recommendations for improving the level of quality. All university teaching hospitals staff should be involved in introducing healthcare services to patients and held accountable for the overall quality of services. They also must be involved in all improvement processes because they better understand how their contributions can make or break the company. Poor communication among staff increases the probability of failure. whereas effective communication increases the motivation level of the hospital staff and inspires them at every level. Therefore, university teaching hospitals need to employ various methods of communication among their staff. More studies are needed to examine different areas such as the influence of TQM on patients’ experience.

Supplemental Material

sj-pdf-1-inq-10.1177_00469580251359504 – Supplemental material for Association Between Total Quality Management and Financial Performance: Evidence From University Teaching Hospitals

Supplemental material, sj-pdf-1-inq-10.1177_00469580251359504 for Association Between Total Quality Management and Financial Performance: Evidence From University Teaching Hospitals by Ashraf A’aqoulah, Samir Albalas, Hadeel Al-Amayrh, Nisreen Innab, Omar B. Da’ar, Soumitra S. Bhuyan and Raghib Abusaris in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Supplemental Material

sj-pdf-2-inq-10.1177_00469580251359504 – Supplemental material for Association Between Total Quality Management and Financial Performance: Evidence From University Teaching Hospitals

Supplemental material, sj-pdf-2-inq-10.1177_00469580251359504 for Association Between Total Quality Management and Financial Performance: Evidence From University Teaching Hospitals by Ashraf A’aqoulah, Samir Albalas, Hadeel Al-Amayrh, Nisreen Innab, Omar B. Da’ar, Soumitra S. Bhuyan and Raghib Abusaris in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Footnotes

Ethical Considerations

Ethical approval was obtained from the King Abdullah International Medical Research Center (KAIMRC) Institutional review board (IRB) on 23 February 2022 (Ref. No., NRC22R/024/01).

Consent to Participate

Written informed consent was obtained from all participants.

Consent for Publication

Written informed consent for publication was obtained from the study participants.

Author Contributions

A’aqoulah, Albalas, Al-Amayrh, and Innab contributed to the study design. A’aqoulah, Da’ar, and Abusaris analyzed and interpreted data. A’aqoulah, Innab, Bhuyan, Da’ar, and Abusaris reviewed and edited the draft manuscript. All authors read and approved the final manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets are available from the corresponding author upon reasonable request.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.