Abstract

In recent years, policymakers and development practitioners have focused on the potential of remittances for economic growth. The World Bank projects that remittances will soon outpace overseas aid and foreign direct investment combined in low- and middle-income countries. This article examines how remittances, or what I call ‘diasporic capital’, sustain urban financialisation at multiple scales. Most research on urban restructuring in the financialisation literature has focused on major corporations, management actors and financial markets without considering the specific sources of capital flows. Diasporic capital flow is facilitated through a unique financial architecture and an incoherent regulatory framework distinct from foreign direct investment. Drawing from interviews conducted with government stakeholders, private sector representatives and members of the Vietnamese diaspora, this article examines the actors, motivations, mechanisms, regulations and products that shape and constitute diasporic capital flow. I argue that classical notions of remittances as money supporting the social reproduction of family are outdated and do not reflect emergent forms of diasporic investments in Ho Chi Minh City’s financialised landscape.

Introduction

After the fall of Saigon in 1975, hundreds of thousands of Vietnamese refugees evacuated South Vietnam; the majority of them would resettle in the United States in the following decades (Parsons and Vézina, 2018). The Vietnamese government branded these refugees as traitors, as they posed ideological and social threats to Vietnam’s communist ambitions (Chan and Tran, 2011). The exiled refugees, with few avenues and incentives to return home, observed how their homeland was rapidly deteriorating as a consequence of prolonged warfare and the poorly implemented collectivist economic strategies (Small, 2018). Because left-behind families were often suffering, the refugees began remitting commodities to Vietnam. In the 1970s and 1980s, the remittances were generally material goods; however, they began to take monetary form in the following decades (Small, 2018). By 2002, remittances from overseas Vietnamese overtook foreign direct investment (FDI) as the highest contributor of external capital, and in 2020, FDI net inflow in Vietnam stood at $15.8 billion compared to $17.2 billions of remittances (World Bank, 2022b). This article investigates where this money goes and its purposes.

Firstly, this article explains the historical context leading to remittance’s rise in popularity as a critical resource for development. It then contextualises financialisation in a Global South context, where diasporic capital and non-financial logics are facilitating the financialisation of housing. Finally, this article argues that remittances (diasporic capital) contribute to rampant speculative real estate development. Urban studies research has historically prioritised FDI over remittances since the latter was considered merely family aid. Research on real estate in Vietnam has followed this trend, focusing empirically on FDI and its constitutive actors and processes against a backdrop of rapid globalisation and integration (Jung and Lee, 2017; Kim, 2020). This has limited policymakers’ collection of national and international statistics on remittances, leading to unreliable estimates (Alvarez et al., 2015) and limiting understanding of their impact on urbanisation.

Literature review

Capital as a development

Beginning in the 1970s, financial crises percolating across developed and emerging economies perplexed central banks worldwide, elevating the role of finance institutions like the International Monetary Fund (IMF) and their policies as solutions for economic relief (Biglaiser and DeRouen, 2010; Ferguson, 2010). By the 1980s, a survey of 181 IMF member states found that 41 countries were experiencing an economic crisis and ‘108 others had “significant” problems’ (Lindgren et al., 1996: 20). Vietnam as a war-fatigued economy suffered even further under a US-placed embargo, which prohibited the country from accessing development assistance (Irvin, 1995). External financing through FDI therefore became a promising remedy for countries to overcome development hurdles (Stiglitz, 2000).

The World Bank (2020) defines FDI as a cross-border investment by which a resident investor of a sending economy assumes an equity position of a foreign enterprise in a receiving economy, owning at least 10% of that business. As a form of transnational capital flow, FDI is considered to be a critical resource in developing countries that are starved of capital (Borensztein et al., 1998; Liu and Lin, 2014) due to its purported association with increased economic growth and technology transfer (Benassy-Quere et al., 2007; Borensztein et al., 1998). Beginning in the 1980s, countries around the world began to create enabling conditions for FDI to reconcile with the diminishing availability of commercial lending (Carkovic and Levine, 2002).

While FDI created acute economic consequences in some East Asian economies (Furman et al., 1998: 23), it also helped propel major urban development in others. Neighbouring China has benefited tremendously from real-estate driven foreign direct investments. Between 1997 and 2005, real estate represented the second largest FDI-receiving sector in China (Wong et al., 2019). With decision-making on urban development relegated to local authorities due to fiscal burdens in the 1970s, local governments in China saw FDI as a potential catalyst for local revenue generation. Tax revenues collected from land transactions reached as high as 55% of cities’ expenditure on land development projects, suggesting a direct link between FDI and growth in urban built environments whereby foreign capital becomes supplementary income for local governments with resource constraints (Wu, 2001).

Amidst capital shortages following periods of FDI decline in 1997 and in the aftermath of the 2008 recession, coupled with stagnating overseas aid, another source of foreign capital – remittances – caught the attention of many national governments and multilateral institutions like the World Bank. Finance capital from a country’s overseas diaspora represents one of many transnational capital flows that accelerate spatial transformation (Buch et al., 2002; other capital sources include foreign bank lending, foreign direct investment and portfolio investments). By official definition, remittances differ from FDI because they involve individuals and households, not businesses. While frequently discussed in public policy and research, there is no cohesive definition of ‘remittances’ in the academic literature (Alfieri and Havinga, 2006). As the international organisation responsible for establishing the definitional parameters for the capital flow of its member nation-states, the IMF (1948: 47) defines remittances as transfers between ‘immigrants and others to their relatives and friends abroad’, charitable donations and reparations. The World Bank (2022a) also defines remittances as employee compensation for ‘border, seasoning, and other short-term workers’ and personal transfers between ‘resident and non-resident individuals’. While remittances have a long and rich history, encompassing material goods to ideas and values – also called social remittances – Page (2020: 403) argues that ‘most attention at the moment is paid to international remittances of money’.

The convergence of diasporic capital and the financialisation of housing

Remittances have grown in importance and size in many countries, often exceeding exports and FDI inflow (World Bank, 2022a). As remittances proliferate, their historical role as resources for social reproduction of remitter households become overshadowed by their incorporation in market logics as reliable revenue for boosting national economic productivity (Adams and Page, 2005; Hudson, 2008). A number of new financial instruments like securitisation mechanisms and diaspora bonds have since emerged (Hudson, 2008; Kunz et al., 2020; World Bank, 2019; Zapata, 2018), including new measurements to improve the reporting of remittance inflow (Hudson, 2008). Now a ‘multi-billion industry’ with significant stakes for people, businesses and institutions, the growing complexity and multitude of mechanisms that support the remittance landscape have been referred to by scholars as the ‘financialization of remittances’ (Guermond, 2022: 372; Warnecke-Berger, 2022).

As Harvey (1989b: 22) contends, ‘capital accumulation and the production of urbanization go hand in hand’. The urban is the ontological terrain through which global circuits of capital not only capture, but appropriate, surplus in key productive sectors (Harvey, 2006). Expanding as a consequence of available surplus and demand for increased profitability (Foster, 2010; Harvey, 2006; Sweezy and Magdoff, 1985), financialisation describes much of the modern economy in which profits are generated not from trade and production, the pillars of the Fordist economy, but instead from the financial sector (Krippner, 2005). The shift away from the Fordist–Keynesian economics coincides with what Harvey (1989a: 141) refers to as ‘flexible accumulation’.

Recent research has exposed the historical and path-dependent nature of financialisation in countries beyond the United States and Europe (Aalbers, 2017; He et al., 2020; Wu et al., 2020). For example, financialisation in China has defied the western logic of commodification and has instead followed patterns of housing assetisation fuelled by high savings rates, market liberalisation and enabling state policies (Chen and Wu, 2020; Wu et al., 2020). While similar conditions can be observed in Vietnam, such as the general widening of regulatory conditions for overseas investments (Vo and Anderson, 2020), this article demonstrates how assetisation fails to fully account for the financialisation of housing in Ho Chi Minh City (HCMC). Prior research on Vietnam, while limited, has demonstrated the potential for overseas remittances to fuel real estate speculation (Thien Thu and Perera, 2011).

Scholars have only recently taken an interest in studying the intersection between remittances and global financial accumulation (Kunz et al., 2020; Warnecke-Berger, 2022). The financialisation of remittances (FOR) literature extends existing financialisation research by proposing a unique way of researching and talking about remittances as a distinct resource category with analytical insights. Whereas the broader financialisation literature has privileged major actors of ‘high finance’ (Hart and Sharp, 2015), among which are banks, corporate managers, other finance companies (Chen et al., 2015; Hudson, 2008; Krippner, 2005), the complexities of the FOR infrastructure has been overlooked. While this study naturally overlaps with the literature on FOR, it does not focus on how remittances have become financialised but instead reveals how remittances have coalesced with favourable economic and political conditions to accelerate housing financialisation in HCMC.

Within the financialisation literature, housing has been an ‘absorber of a “wall of money”’ (Fernandez and Aalbers, 2016: 73). Although the growing FOR literature has contributed much needed theoretical contributions by illustrating how remittances can lead to financial inclusion and new financial tools and power asymmetries, the topic of how FOR intersects with burgeoning real estate investments remains an unexplored area of research. This is despite growing evidence of remittances affecting urban real estate in countries like Ghana (Obeng-Odoom, 2010), Colombia (Zapata, 2018) and Kenya (Kibunyi et al., 2017), a likely consequence of the inadequate accounting system to monitor how remittances are spent upon reaching the intended recipients (World Bank, 2022a). This study contributes to a growing body of research on financialisation in emerging economies by bridging overlapping, but previously separate, literature on FOR and the financialisation of housing (Fernandez and Aalbers, 2020; Fields, 2017).

To merge the gap between these two literatures, this paper proposes the application of ‘diasporic capital’ as a heuristic for analysing the current financialisation of housing in emerging economies. In framing remittances as ‘diasporic capital’, I argue that they also serve as investment capital, not just altruistic monetary transfers between members of a household. I define diasporic capital as a resource and investment flow channelled into economic sectors like real estate. Diasporic capital recasts remittances’ theoretical presuppositions – the assumptions about its historical role as resources for social reproduction and present promises as a development tool – and instead interrogates it as a catalyst for accumulation. This reframing draws from Bourdieu’s (1986) theoretical opposition to dichotomies in sociological studies by removing the definitional boundaries and assumptions between FDI and remittances as distinct levers of financialisation. As this article demonstrates, diasporic capital behaves similarly to FDI by financing real estate ventures in HCMC despite differing accounting methods.

While several authors have studied remittances in Vietnam, they have focused on how this capital source transforms and mediates kinship ties (Small, 2018; Thai, 2014). However, national statistics reveal that only an estimated 6% of remittances are channelled for family aid while 25% are channelled into real estate in HCMC (VOV, 2022). An estimated $1 billion in remittances routes to HCMC annually for real estate development, although the actual amount might be much higher (Tien Phong, 2018). This study is among the first to address the gap in the literature on diasporic capital and housing financialisation. As scholars have argued, financialisation remains ‘under researched and undertheorized’ (Wu et al., 2020: 1485) and epistemologically ‘imprecise’ in the Global South (Aalbers, 2016: 3).

Context

From 2010 to 2020, over $142 billion in foreign remittances were sent to Vietnam, averaging more than 5% of the country’s gross domestic product between 2010 and 2020 (World Bank, 2022b). The country also received more remittances than foreign direct investment between 2010 and 2020. HCMC absorbs the majority of remittances entering the country (Reuters, 2021), as it is where most Vietnamese refugees departed and nearly half of its residents have relatives residing abroad (HCMC Government, 2022; Pfau and Giang, 2009; Small, 2018). HCMC received approximately $6.1 billion remittances in 2020, which appears significant when compared to the city’s gross regional domestic product of $59.1 billion that same year (HCMC Statistics Office, 2020).

The current intensity of diasporic investments in HCMC is perhaps surprising given that, at varying historical moments, overseas Vietnamese and the Vietnamese government have considered each other enemies (Chan and Tran, 2011). Even the Viet Kieu who return see themselves as victims of historical and political violence and maintain strong anti-Communist sentiments (Small, 2012) targeted at both ‘communist political ideology’ and the government at large (Le, 2015). Despite this resistance, many overseas Vietnamese – nearly 150,000 people during Lunar New Year alone – returned to HCMC despite unfavourable and cynical views of the government (Hong, 2016). This was a remarkable increase from the 8000 returners in 1986 (Government of Vietnam, 2005a). By 2021, remittances in Ho Chi Minh reached $6.6 billion, representing an increase of 9% from 2020 (HCMC Government, 2022). Understanding diasporic capital’s role in financialisation thus requires a close interrogation of the connection between diasporic capital and housing financialisation.

HCMC as a burgeoning real estate market has generated interest from regional investors. As real estate markets saturate other Southeast Asian cities, HCMC becomes a new spatial fix for speculative capital. Global real estate and investment companies have demonstrated their eagerness and anticipation for Vietnam to replicate similar growth patterns seen in neighbouring countries (Dang, 2018). Meanwhile, the rapid growth of Vietnam’s real estate sector has been remarkable given the population’s lack of credit access. It is estimated that 70% of adults have a bank account, but approximately half do not have access to credit (Vietnam Investment Review, 2021). This underdeveloped banking sector partially reflects the population’s historical distrust in state-led financial expansion and prevailing ubiquity of cash transactions (Nguyen-Marshall et al., 2012). These conditions generate a new form of financialisation, not based on securitised mortgages or assetisation, but on diasporic capital.

Methodology

This study draws on site observations and 30 interviews conducted with government stakeholders (8), private sector representatives (13) and members of the Vietnamese diaspora (9) in HCMC between 2018 and 2019. Interviews with returning migrants helped identify and track overseas Vietnamese’s investments in real estate. Initial interviews with the chair of HCMC’s government liaison office for overseas Vietnamese led to other meetings and events where I met overseas Vietnamese. Due to Vietnam’s collectivist culture, many interviewees wanted to ‘help’ the researcher as a direct or indirect favour; this facilitated the use of snowball methodologies to solicit additional contacts after each interview (Nguyen, 2015: 38). Government officials responsible for overseas Vietnamese affairs were open to meeting with me, as it advanced their objectives to connect with overseas Vietnamese, and they could recruit me into joint governmental meetings about HCMC’s development. Real estate brokers and sales staff were also generous with their time because they viewed me as a potential client, despite my insistence otherwise (though one would attempt to sell me a $550,000 condo). Despite difficulties finding overseas Vietnamese in HCMC, most were amenable to discussing their financial matters. The Vietnamese respondents talked openly about money and did not consider their financial investments to be abnormal or problematic. These interviews were triangulated with other accounts from primary and secondary sources like government news reports, governmental meetings, local real estate conferences and business meetings in HCMC.

The Viet Kieu’s empirical specificity presents a case through which to understand financial actors and their decisions in a Global South context (Aalbers, 2017; Lai, 2017). While ‘diaspora’ serves as a unifying term to consolidate the overseas Vietnamese population, they are not a homogenous group (Bose, 2008). Overseas Vietnamese are differentiated both by their countries and cities of resettlement, as well as by their socio-economic conditions and political affiliations (Dang, 2005). The US has the largest share of Vietnamese refugees, with an estimated 2.1 million US-born and US-based Vietnamese in 2017. This represents 46% of the total overseas Vietnamese population (Migration Policy Institute, 2015). Therefore, this study focuses exclusively on overseas Vietnamese from the United States, particularly individuals with kinship ties and a connection to their homeland.

Despite their capital-wielding potential and investment patterns, diasporas remain overlooked actors in financialisation research. Schiller and Caglar (2011) suggest that their absence in urban studies is partly a consequence of how the narratives of and research on migrants have been framed by policy directives. Scholars fail to transcend the conceptual frameworks inherited from policymakers and continue ‘debating assimilation, integration, transnationalism, or diversity’ (Schiller and Caglar, 2011: 2). This article thus builds on earlier calls for research on returning migrants by framing diasporic real estate ventures as financialisation (Chan and Tran, 2011). Interviews with overseas Vietnamese, government representatives and business leaders begin to reveal how diasporic capital, while encumbering speculative behaviour similar to FDI, is governed by distinct financial and non-financial logics.

Results

Financialisation as a sentimental process

The Viet Kieu’s desire to invest in HCMC real estate contrasts with the typical logics of investment which are guided by projected returns (Farragher and Savage, 2008) and faith in economic and government stability (Busse and Hefeker, 2007). Vietnam is an unlikely site for financialisation given that property rights are a relatively modern invention of the Renovation Era (‘doi moi’) liberalisation reforms of 1987 (Kim, 2008). In 1988, a law granted land use rights to entities and individual users, while a decade later, legislation allowed joint ventures with foreign investors. Land law only enabled large commercial projects in 2003 (Nguyen et al., 2016). Though the state still retains full ownership of the land, individuals can use, sell, lease and exchange their properties. Vietnam maintains a burgeoning, if not dynamic, real estate market despite centralised government control of land, collusion among local and political elites (Kim, 2008), and a complex two-price system in which the government compensation rate is notoriously lower than the market rate (Thien Thu and Perera, 2011). Given these conditions, investing in real estate might seem to be a fool’s errand, but this counterintuitive behaviour helps to explain diasporic financialisation.

In interviews, overseas Vietnamese spoke of their early investment activity with ambivalence and disillusionment. They disclosed that they returned to HCMC with aspirations to invest in property. Interviewee 1, a retired real estate investor in his mid-40s, was among the first wave of emigres who ‘evacuated from the regime’ and resettled in California. He has since bought a one-bedroom condo in the city’s commercial district, where sales prices start at $400,000. His decision to return to Vietnam was motivated by his marriage to a local Vietnamese. When asked if he had previously considered investing in Vietnam, he explained his profit-driven motivations: No, when I lived in the United States, I was in the real estate investment business as a builder. Back then, there was a huge market. Even in Orange County where I was, the market was so open, so huge with a lot of room to grow. When I saw the growth [in California] would max out, that was when I stopped. So, I am here in [HCMC] investing by chance.

Another interviewee also mentioned that he never intended to return to Vietnam long-term and invested coincidentally. Interviewee 2 returned to the city to reclaim land his family owned before emigrating to the United States. A third interviewee was saving for a four-story retirement home in HCMC, where she grew up and where her family continues to live. She says, ‘Now that I am near retirement age [in the US] and my daughter graduated from college, I want to spend half my time with family in Vietnam’. As such, there are myriad reasons compelling Viet Kieus to return and invest in their homeland. Though their rationales differ, they all engage in and reproduce the financialisation of housing in HCMC, even if their decisions are not solely financially motivated.

The proliferating inflow of remittances into HCMC’s real estate sector is puzzling since overseas Vietnamese have negative views of the government. Interviewee 3 states, ‘I didn’t trust the government. I could own it [real estate] one day, but they might change the law the next day’. This makes investments risky given a constant fear of land grabs by the state, as well as information asymmetries regarding current land and citizenship laws. As Kim (2010) argues, the introduction of property rights in Vietnam did not entirely protect owners from predation and expropriation by the state. The records of increasing land-related conflicts reported by the Vietnam Inspector General do not fully explain whether these events are becoming more frequent or whether the channels through which dissent is recorded are gaining widespread adoption (Hoang, 2012; Kim, 2010). This suggests that investment behaviour may be motivated by stronger factors than market logics.

Financialisation as a regulatory process

‘Help the family, help the city, help the homeland’, says Nguyen Thanh Phong, Chairman of the HCMC’s People’s Committee. This was the mantra of the annual Mung Xuan (Welcome Spring) festival organised by the HCMC Committee for Overseas Vietnamese Affairs, a subsidiary of the Ministry of Foreign Affairs. The 2019 event – welcoming nearly 1000 Viet Kieus – featured successful overseas Vietnamese who urged their compatriots to commit to the city’s development goals. The Vietnamese government even coined an intimate and endearing term to entice the Viet Kieus: ‘Kieu Bao’. As Chan and Tran (2011: 1105) explain, bao means ‘cells’; dong bao means ‘people with the same cells’, indicating that they are from the same parents, or of the same blood origin… It aims to appeal to the nationalistic sentiment of Viet Kieu, regardless of previous mistrust between them and the communist state, for the benefit of Vietnam’s post-reform nation-building.

Such sentimentality is mirrored by various references to the ‘homeland’ in interviews with overseas Vietnamese. Those interviewed were unified in their conception of Vietnam as their ‘true home’, even if they escaped the country as refugees. Sinatti (2009: 50) argues that, for many, real estate ‘represents an anchorage in the homeland, the place where scattered families recompose their unity and where transnational mobility is contrasted with grounded architecture’. The inseparability of the diaspora from the homeland has long been a focus of academic research (Falzon, 2003). The allure of the return pilgrimage is forged through a ‘collective memory, vision, or myth about their homeland’ (Safran, 1991: 83) even if the act of returning remains elusive. This ‘shared cognitive schema’ remains entrenched even if it involves a high degree of abstraction by distinct groups of individuals who share dissimilar experiences but consider themselves as belonging to one community (Strauss, 2006: 331).

One government official (Interviewee 4) suggested, Everyone wants to return home because there is something about the homeland that pulls them back. Overseas Vietnamese are part and parcel of this country; there is no separation. We will continue to invite, invite, invite and open our arms to those who desire to return.

This sentiment was shared at the 2005 Welcome Spring event when Prime Minister Phan Van Khai declared, ‘those who stay away from their original home cannot live a happy life’ (Government of Vietnam, 2005b: 1).

Beyond encouraging landed investments, sentimentality may also affect where returnees purchase properties. While it is beyond the scope of this paper to determine the spatial patterns of landed investments, interviewee accounts suggest that the logic varies among overseas Vietnamese. Interviewee 1, for instance, chose a central and convenient location in a commercial district whereas Interviewee 2 bought property in his parents’ neighbourhood. Interviewee 1 also commented, ‘Viet Kieu purchase property on emotions and feelings’, rather than purely using cost–benefit analysis. Along the same lines, one government interviewee (Interviewee 5) believed, ‘Overseas Vietnamese tend to choose their hometowns, areas where they or their parents grew up’. This indicates that potential surplus extraction may be a secondary factor in Viet Kieu’s property investments and explains why HCMC is at the centre of remittances, since it is where many overseas Vietnamese lived before departing. Therefore, diasporic investments are not necessarily contingent on commodification.

Financialisation through informal mechanisms

Several factors differentiate diasporic financialisation from existing theories. Firstly, the Vietnamese diaspora is an unsuspecting financial actor within the realm of corporate and investor managers (Aalbers, 2017; Krippner, 2005). Another identifying feature of diasporic investments is the use of informal financial channels for real estate purchases. The nine overseas Vietnamese interviewed shared (without concerns of legality) that they depend on the black market for monetary exchange. Bothersome financial rules in the United States, coupled with a strong, reliable black money market in Vietnam, undermine state efforts to regulate capital flows (Small, 2018). Interviewee 2 explained frankly, ‘A Vietnamese would come to my house in the morning, and I would give him, in cash, hundreds of thousands of dollars. Within half a day, someone in Vietnam would receive that cash in Vietnamese dollars’. Widespread use of such private channels makes accurate calculations of remittances extremely difficult (Hudson, 2008).

This evasion of formal value capture is the product of post-war necessity (Small, 2018). Remittances were historically sent through ‘hawala transfers’, transactions dependent on brokers and courier services. Prior to the re-establishment of diplomatic ties with the United States, there were no official avenues through which relatives could send remittance funds. Amidst the technological breakthroughs of the 1990s and the introduction of money transfer services like Western Union and MoneyGram, remittances began to channel through formal institutions, though informal channels remain the preferred method. The black market provided lower fees, personalised messages and confidential delivery to protect from looting by government officials (Small, 2018). Remittances are greatly undercounted due to informal trading networks; however, of the recorded amount, 70% is sent through credit institutions, 28% through remittance transfer companies and 2% through postal mail (Government of Vietnam, 2021).

Despite the lower transaction costs, the informal remittance channels also have risks. These channels historically required Viet Kieus to rely on friends and family members to purchase real estate on their behalf. Prior to the legalisation of overseas investments, the Viet Kieus could not purchase Land Use Rights Certificates, the legal tenders permitting the holder to use the land. The Viet Kieus, therefore, relied on their domestic Vietnamese counterparts to be the de jure titleholder of their real estate. Even today, some overseas Vietnamese do not realise that they have the legal right to purchase land. Interviewee 3, for example, asked her sister to buy land on her behalf – this eventually bred disappointment and legal disputes.

Regulatory conditions for diasporic investments

The ease with which Vietnamese residing abroad can purchase property is a newer development owing to changes to the nation’s land regime and national citizenship laws. Seven legislative changes ultimately enabled overseas Vietnamese to purchase real estate, beginning with the 1992 constitutional amendment to enable the sale, exchange, lease and transfer of land. This was followed by a 2001 pilot experiment led by then-Prime Minister Phan Van Khai for HCMC as part of an effort to ‘encourage them [overseas Vietnamese] to contribute to national construction and development’ (Government of Vietnam, 2000: 1). As one interviewee shared, these governmental actions in the early 2000s signalled to developers the government’s desire for real estate projects that cater to overseas Vietnamese.

Encouraged by the introduction of these laws, Viet Kieus who previously purchased properties under another name began the legal process to reclaim their titles. This required them to produce documentation linking their capital source to the real estate. My interviews revealed that this process to transfer property ownership was fraught with uncooperative family members and friends. Interviewee 1, for instance, is suing his former wife for a home she purchased using his money but did not return after their divorce. Interviews with government officials indicated that these events were common and led to ‘broken families’. Consequently, these outcomes contradicted the state’s espoused goals of national unity.

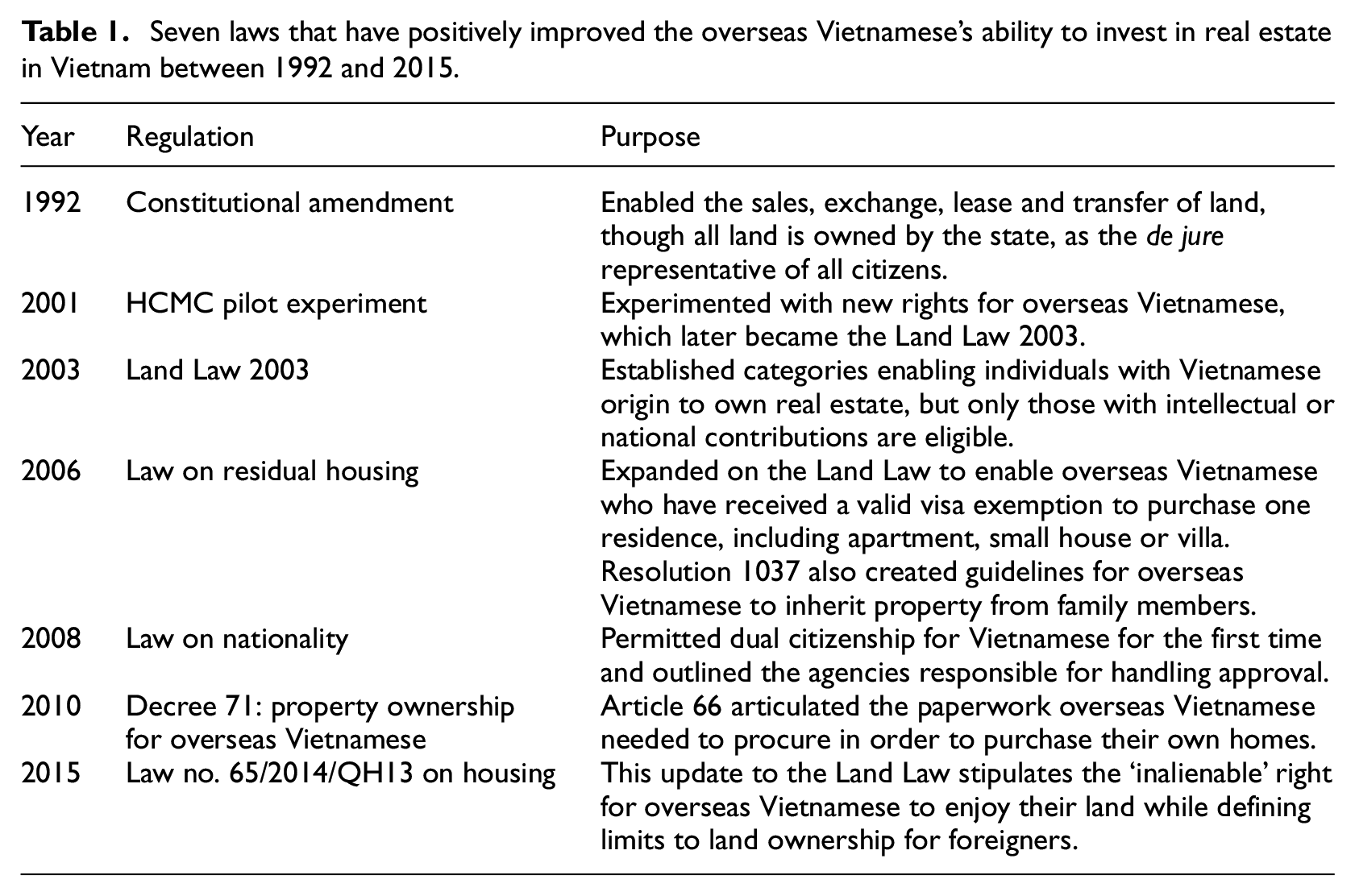

Like previous research (Aalbers, 2016; Fields, 2017), this study found that deregulation of financial controls is not a necessary prerequisite for the financialisation of diasporic capital. Instead, the process is facilitated by changes to legal regimes affecting the mobilities of the overseas Vietnamese and fundamental laws on land ownership. Table 1 displays the seven laws that increasingly made the process of investing in real estate easier for overseas Vietnamese. While Vietnam has made changes to laws on remittance transfers, these efforts did not emerge as a key priority in encouraging or sustaining diasporic investments.

Seven laws that have positively improved the overseas Vietnamese’s ability to invest in real estate in Vietnam between 1992 and 2015.

While these laws were generated at the national level, urban authorities were instrumental in their inception. In the early 2000s, HCMC led a coalition of powerful cities to pressure Hanoi to introduce favourable policies for the overseas population, calling for ‘timely’ suggestions to allow ‘relevant agencies and Viet Kieu…the chance to comment about any draft policies that affect them’ (Sidel, 2007: 12). Specifically, local leaders demanded that ‘Ho Chi Minh City authorities be given more power to settle Viet Kieu related issues’ (Sidel, 2007: 12). Despite efforts towards decentralisation, HCMC remains largely controlled by the national government, with the task of urban planning being delegated to private developers (Huynh, 2015).

The 2015 revision to the land law has made it easier for foreigners to own properties, with two exceptions: foreign companies can obtain land rights for real estate ventures and sell them to foreign individuals, but foreigners cannot hold land use rights and their ownership of the home is limited to 50 years. These rules do not apply to overseas Vietnamese, who are entitled to the rights and privileges of ordinary Vietnamese citizens. Despite this change, it is still difficult for foreigners to find available properties because the new land law restricted properties available to foreigners to areas that are not considered critical for national security. However, the relevant Vietnamese ministries still have not defined the areas considered non-essential, which has caused backlogs in the land available for foreign investments. Given these restrictions, local companies looked to diasporic communities for economic relief.

Capitalising on a new consumer base

In 2002, the Housing Business Investment Joint Stock Company (INTRESCO) began a 252-unit housing complex project later called the ‘Overseas Vietnamese Village’ in HCMC due to percolating rumors about the state’s desire for projects catering to Viet Kieus. The developers initially selected a swampy, agricultural area as the site given the lack of available land in the city centre and underwent a ‘difficult’ compensation process, according to one project assistant. Built on a flood plain with barriers surrounding the development to prevent flooding, the company initially restricted property ownership to overseas Vietnamese, their families and others who could prove their overseas ties. INTRESCO, lacking connections to their targeted clients, would later hire an overseas Vietnamese businessman to begin marketing and selling units to Vietnamese people living in the United States. This large project ultimately failed to attract the necessary investments from overseas Vietnamese, due to unclear land ownership rights for overseas Vietnamese and their fear of government expropriation.

Despite the initial cold response to eager real estate developers, widening policy interventions and HCMC’s growth continued to motivate developers to pander to overseas Vietnamese clients. Diaspora-led financialisation thus coincides with broader trends in regulatory efforts that have made it easier for global capital entry into landed investments, and private developers and brokerage firms have discovered how to take advantage of this expanded class of consumers. Vietnamese developers have helped absorb risk to entice wary overseas Vietnamese by offering small buy-in costs, as low as $12,000 down payment and partnered with major banks to offer interest-free loans up to 80% of the property value. To further incentivise buyers, companies are offering $12,000 vouchers towards the purchase of new vehicles and lottery tickets for gifts worth up to $88,000, including gold bars and household goods. This alignment between real estate actors and the banking system shows a shift to volatile investment portfolios and speculative development.

According to the government and business officials interviewed, most overseas Vietnamese return home during the Lunar New Year. The HCMC Committee for Overseas Vietnamese Affairs hosts their annual Welcome Spring event to coincide with this holiday. Many returning Viet Kieus use Lunar New Year to make big-ticket purchases and important investment decisions. Savills, a global property advisory company, hosts annual ‘tours’ of real estate in the city for overseas Vietnamese during New Years.

When purchasing their homes, Interviewee 6, a marketing staffer, believed that Viet Kieus had the same considerations as other investors: Viet Kieus would be concerned about after-sales-services and a transparent procedure …[and] other priorities of a property investment such as location, developer, and quality. I have worked on some cases with buyers who are Viet Kieu, and I think their concerns are like foreign investors which are about buying procedure, after-sales service, rental yield and capital appreciation.

Though they may be purchasing homes for themselves or their family, overseas Vietnamese are interested in the opportunity to charge rent and earn future yields should they forego their assets. This makes them diasporic capitalists – sentimentality alone cannot account for their landed investments and desire to reinvest surplus wages.

Conclusion

Though financialisation in the Global North relies on accumulation, this paper re-evaluates the universality of this model, arguing that financialisation can manifest locally and contextually without the major actors of high finance. Partially mediated by non-financial motives and sentimentality, financialisation can emerge in developing countries through transnational capital flows without clear specificity on the forms of capital.

This article uses HCMC to illustrate how historical and political forces, in addition to the concentration of speculative private actors and concentrations of capital flow, have coalesced to make the city a prime locale for the financialisation of diasporic capital. It revises the classical understanding of remittances as resources for the family, arguing that remittances are being incorporated into market logics and transcending its categorisation as family aid. Historically contingent and mediated by non-financial ties and unlikely actors, this genre of financialisation – through non-financial institutions using informal channels – is often overlooked by contemporary urban studies. This approach moves beyond market logics, evaluating ‘on the ground’ financialisation which is characterised by negotiation, contention and profit-making across a range of unconventional actors and institutions. The central characters in this study, overseas Vietnamese and their families and network, offer a nuanced perspective on how financialisation can materialise without explicit profit-making motives. The variegated outcomes of financialisation in HCMC reveal the need to consider financialisation beyond the narrow framework of securitised mortgages and commodification. Therefore, I use ‘diasporic’ as a precursor to ‘capital’ to denote how financial and non-financial motives coexist.

As overseas Vietnamese continue to sustain the financialisation of housing, growing remittance flows remain a major source of capital for speculative real estate ventures. This is true even if the diaspora is not primarily motivated by accumulation, but instead seeks to preserve and sustain their link to the homeland. Like real estate financialisation in other economies, the financialisation of diasporic capital relies on overseas Vietnamese as a capital source in addition to a constellation of ancillary actors and institutions. Despite their speculative potential, diasporic capital continues to be treated as an unproblematic income source by development institutions and the Vietnamese government.

This research has important empirical and policy implications for urban planners and policymakers. Firstly, remittances can behave as investment and accumulation, quite distinct from the popular imaginary of family and development aid. Secondly, remittances are often statistically separated from FDI, obscuring their impact on urban real estate investment markets. Finally, this study confirms prior work arguing that commodification is not a prerequisite for financialisation.

The absence of research on remittances in urban studies reflects its historically marginal size compared to FDI. As domestic firms continue to capitalise on overseas capital for speculative development, Vietnamese policymakers need to consider how remittances can be better directed towards local development objectives. As the diaspora becomes more integrated into the economy of their resettlement country, their wage power allows them to engage with the homeland. It is time to dispel the colloquial framing of remittances as money for supporting the consumption needs of one’s left-behind family or as a new development currency. Instead, remittances must be reframed as diasporic capital that permeates the economy and drives urban change.

Footnotes

Acknowledgements

This article benefited immensely from early feedback by Idalina Baptista. I also thank Diane Davis and Neil Brenner for their guidance during the concept’s formative stages, as well as Alexander Rogala for his intellectual engagements with me on the subject of financialisation. I thank the anonymous reviewers, and I am ultimately responsible for the final product and any errors.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Research support for this project came from the Harvard Asia Center, Harvard Ash Center for Democracy and Governance, and the Harvard University Graduate School of Design.

References

Phong. Available at: https://tienphong.vn/post-1051056.tpo (

Phong. Available at: https://tienphong.vn/post-1051056.tpo (