Abstract

Taking as our focus the city of London over the last decade, we use state-held records of house sales to consider the impact of competition for housing resources in the luxury property market. This data suggests that the use of offshore investment vehicles and the concealment of wealth from national tax agencies have become key mechanisms by which housing resources have been exploited by the wealthy and their capital deployed by agents of the rich. Using the concept of wealth chains, we consider these methods of capital accumulation as these extending flows of managed capital become ‘anchored’ within specific urban spaces, in this case the luxury housing market of inner West London. Our analysis of a selection of these chains shows that the prevailing political management of the property economy benefits those already winning the war of inequality while looking to augment their capital and shield it from tax and regulation. The ultra-wealthy, financial intermediaries and multinational corporations have created chains articulated across space, with the effect of undermining the value of dwellings as homes, and have replaced them with assets to be traded in pursuit of private and offshore wealth gains. The result is an urban context that favours already advantaged and powerful interests and enables the avoidance of tax obligations desperately needed at a time of austerity and intense housing need.

Introduction

The machine fuelled by property investment and international wealth has had the effect of shifting the role of homes into assets more often traded for capital accumulation. In this article, we argue that houses are more likely to be used in this way where significant incentives exist for the wealthy, and the funds that they invest in, to purchase, manipulate and accumulate property in urban land markets. We examine the architecture of intermediaries (tax and finance advisers, fund managers and vehicles by which money is laundered, invested and stored in housing) that grease the slopes down which capital descends into urban centres globally (Hall, 2018). Our focus is on one such city, London, and a key area of its housing market – the London borough of Kensington and Chelsea.

The 2011 census showed that Kensington had 9169 homes with ‘no usual resident’ in the borough (around 10.5%), while for its neighbour, the borough of Westminster, the figure stands at 14,294 (13.5% of households). Kensington itself records that only 1652 properties are unoccupied. More than a third of these vacant homes (603) are recorded as having been empty for more than two years, with the owners paying a 50% premium on their council tax. A further 1010 are classified as unoccupied and substantially unfurnished, while the other 39 have been unoccupied for less than a year, with building work in progress. Owners include the former New York mayor Michael Bloomberg, a string of oligarchs, foreign royalty and multimillionaire businesspeople, a Ukrainian billionaire fighting extradition to the US, a high-profile luxury property developer and a senior television executive. Other unoccupied properties are owned by offshore companies, including Dukes Lodge London Ltd, part of Christian Candy’s luxury property business, which is listed as owning 26 homes in a 1930s mansion block valued at £85m in 2015, and Smech Properties Ltd, owned by Sheikh Mohammed bin Rashid Al Maktoum, the vice-president of the United Arab Emirates and ruler of Dubai (Walker and Pegg, 2017). In this context, property may appear less as something devoted to core social needs and more akin to an ornament of status or, more broadly, the functioning of a system devoted to capital expansion (Madden and Marcuse, 2016). Our concern in this article is to elaborate on the economic architectures and logics that underpin this latter function. By focusing on these processes in terms of ideas about chains of wealth (which we define below) that connect the city to other tax jurisdictions and systems of ownership, we can see how these mechanisms are used to extract further value from land market assets by the already wealthy. Our aim is to offer a critical assessment of these processes by focusing on their appearance in a city characterised by extensive rounds of investment activity of this kind. In doing so, we raise questions about the deeper harms generated by an increasingly financialised, offshore and property-based capitalism and the cities in which these relationships are made manifest.

The scholarship of political economy is devoted to the idea that the economy itself should be seen ‘within its social and political context rather than … as a separate entity driven by its own set of rules based on individual self-interest’ (Mackinnon and Cumbers, 2007: 14). The housing market, like other markets, is not some free-floating set of activities and institutions. In reality it is embedded within, and managed by, a wider series of political relations and regulations. This political field is itself contested, by actors and institutions with unequal power positions. As critical scholars highlight, this politics is engaged with and supportive of existing interests and powerful constituencies, including those of developers and the property industry more broadly (Ansell, 2014). It is therefore inappropriate to view the housing market as simply a series of open choices or transactions. Various regulations, macroeconomic policies, subsidies and tax arrangements are all part of the architecture of this political economy.

Cities and housing markets can be seen as a field upon which immensely uneven sets of self-interested actors and institutions engage in contests to win out through processes of investment activity, in politics itself, in forms of investment and in the capture of key resources (Atkinson, Parker and Burrows, 2017) which can be used to generate flows of rental income. If we examine thinking on this urban field from some years ago, we can see that some of its worst excesses were diluted by other actions by the state and key actors who had a role in managing and softening the tendency for capital to take over the city. The ability of the state to provide collectively consumed goods in the domains of housing and health, for example, offered a means by which the potential for socially disastrous outcomes could be mitigated (Castells, 1972; Merrifield, 2014). For Pahl (1970, 1975), social policy and urban planning softened some of the more excessive social and economic inequalities that might otherwise emanate from patterns of ownership under capitalism. For Pahl, the urban manager is the key figure in mediating the relationship between ownership, the state and the local residents. Such managers work around planning and local government officials and engage with developers, estate agents and other interests operating to augment capital.

Urban managers performed an intermediary function. This function operates to the extent that such managers were generally able to influence the allocation of key social resources in the city in order to mediate and soften the more regressive and destabilising impacts of capital on the city (Burrows et al., 2017). We follow this line of thinking, but in a contemporary urban context characterised by low regulation, declining state investment and massive construction and investment by capital actors (Hall, 2018; Minton, 2017). In this context, the notable emergence of buy-to-leave ownership (housing assets purchased by surplus capital and left unoccupied) can be linked to the presence of international wealth chains that circumvent and undermine the capacity for urban managers to allocate key resources like housing. Such outcomes have particularly emerged in the prime and super-prime central London property markets, exemplified by areas like the Royal Borough of Kensington and Chelsea (hereafter Kensington), the focus of this study. Buy-to-leave sees the ultra-rich acquire properties and deliberately leave them empty so as not to incur any of the costs associated with acting as landlords, and with the ability to liquidate those assets when advantageous market conditions arise. Another motivation for such investments may be the use of property as a means of resting illicitly sourced wealth prior to sale and the ‘laundering’ of that capital so that it can be reinserted into legitimate funds (Bullough, 2018).

The consequences of property investment by international, offshore capital formations are complex and multiple. For one thing, there have been concerns about the over-use or ‘take’ on residential space through second home ownership by foreign nationals, the inflation of property prices and the use of property for money laundering. Another feature of this investment-housing landscape is the creation of sizeable sections of the city that are empty or heavily under-used as homes. Atkinson (2018) has argued that empty houses are part of a wider problem of underutilised housing resources that has emerged under conditions in which capital investment by the international super-rich creates a landscape of empty property that may be termed necrotecture – dead residential space operating almost solely in the interests of capital accumulation.

The awful paradox of the creation of vacant homes is that while necrotecture entrenches itself, the wider city is experiencing a deep, pernicious housing crisis (Minton, 2017) amidst a pronounced need for more affordable and available housing. In an open competition for such housing, those with massive resources are able to outbid and ‘misuse’ homes as pure investment assets. Planners and local authorities are largely unable to challenge these phenomena, as we see in cities like London and New York today. An urban system that incentivises and enables capital to thrive while urban social conditions wither frames the goal of this article to consider the production and consumption of homes that are unwanted and unneeded except to serve the function of capital expansion. By examining evidence of buy-to-leave investment by the rich and their agents, we seek to reveal what has long been the invisible architecture of a system that operates across national and institutional contexts in the name of capital expansion.

The article is structured as follows. The first section examines the role of housing capital in the contemporary political economic context. The second uses Private Eye’s (n.d.) Land Registry database (1994–2014) to examine purchases of Kensington land and property by foreign entities. Founded in 1961, Private Eye is a British satirical and investigative current affairs magazine. In September 2015, Private Eye published a searchable online map of all the properties in England and Wales owned by offshore companies. The database used Land Registry data released under Freedom of Information laws, then linked to approximately 100,000 land registry entries and their specific addresses. In this way, Private Eye was able to map all leasehold and freehold interests acquired by offshore companies between 2005 and 2014. Using the same data, Private Eye subsequently published a database of all properties acquired by offshore companies from 1999 to 2014, showing the address, the offshore corporate owners and, where available, the price paid. The cleaned up version of this database provides the empirical basis for our study.

The article uses the idea of wealth chains as an analytical tool to disentangle the complex ownership structures that are designed to minimise tax liabilities and accelerate profit rates. Wealth chains bring the question of ownership structures into sharp relief by helping us to identify the vehicles and arrangements through which ownership is achieved. This empirical analysis highlights massive flows of international capital into the London property arena, with enormous advantages and under-taxation, either from the city or from the national system. The final section considers the implications of our findings.

Housing and the circulation of capital

The role of housing in the global economy and as a means of capital expansion has been increasingly recognised since the financial crisis of 2008 (Aalbers and Christophers, 2014). In Marx’s (1992 [1867]) work, land and property are the basis of capital. His analysis is undertaken from three different viewpoints: capital in the process of circulation, capital as a social relation and capital in its ideological cloak. Marx’s schema

The reproduction schema tells us that some of the money capital that is realised through the sale of goods is re-advanced back into production, but not all. The money capital that is not taken back into production has to be stored. Money is an obvious store of value, but it is not the only one. Housing is another, a point emphasised by Lefebvre (1996) and Harvey (2001) in their analyses of the role of the built environment as a second, additional circuit of capital flows and accumulation. This role of the city has, of course, become enhanced under conditions of financialised capitalism (Forrest and Hirayama, 2015) and has been of increasing interest to analysts.

Housing’s quality as a potential store of money is an attribute shared with other assets, such as fine art, wines and other collector items. Houses and other collector items possess a dual character, serving as either use value or exchange value. Buying a home involves choices linked to assessments about the degree to which it will satisfy the need for shelter, a place for daily family and household life and so on. This is the intrinsic use value of the house. But as Aalbers and Christophers (2014: 14) point out, houses are also bought to exploit housing’s ‘exchange value, which derives from the fact that value is stored in housing-cum-land’.

What is notable about capital circulation in Marx is that it periodically breaks down and ‘crisis’, a perennial feature caused by obstacles and barriers that arise in the circulation process, ensues. One such obstacle concerns the question of what post-Keynesian economists call ‘effective demand’. Essentially this is a problem of insufficient consumption relative to the goods and services produced during the circuit of capital, so that: If people cannot afford to buy things, or choose to hoard their savings instead of consuming them, circulation grinds to a halt: value cannot be realized, and thus reinvested; and if value cannot be realized, capitalists will soon stop producing it. (Aalbers and Christophers, 2014: 5)

When this occurs, there is in effect a crisis of effective demand. Aalbers and Christophers (2014: 5) identify two twin threats to the circulation of capital. First, generalised poverty among the mass of consumers is a clear and present danger to the accumulation of capital. And, second, an anxious and precarious working class is likewise a threat to capital’s domination because the lack of confidence that follows means the working class is likely to save (or hoard) rather than spend and consume. In cities like London, such a crisis has not been evident to date because it is not a closed system and, despite a decade of austerity, massive flows of international capital have arrived to take advantage of the security, stability and openness of the city’s property market. It is this feature of capital in general, and of London’s relationship to it in particular, that forms a plank of our analysis of the way in which wealth has come to flow into the city.

Housing has a unique character. It is an exchangeable store of value and, when combined with mortgage debt, a house (someone’s home) can be used to help fund effective demand when other sources dry up. The idea of using debt to fund accumulation derives from Keynes and the public demand management programme that prevailed from 1945 to the early 1970s. Keynesian demand management broke down in the 1970s, and by the 1980s capital was reconstituted along neoliberal lines where free markets were cast as the motors of accumulation and where stabilisation of the economy and fending off crisis became a matter for a system of ‘privatised Keynesianism’ where houses and mortgage finance played a critical role. Under this system, instead of the government issuing debt to stabilise the economy and fund economic activity, it was the debt of the consumer that helped to fund effective demand (Crouch, 2009).

The second conceptualisation of capital in Marx is capital as a social relation. Marx’s reproduction schema tells us that when capital circulates, value is accumulated, distributed and redistributed, and then stored as what we term wealth: Such wealth takes numerous forms, among them cash money and company securities (often held in pensions), but it is of immense significance that in many capitalist societies residential property is the largest individual wealth/asset class although at the same time many – in some countries most – households own no residential property whatsoever. As such, it is in housing that the vast wealth inequalities of capitalist societies, which we hear so much about today, are often most visible and most material. (Aalbers and Christophers, 2014: 8)

Marx’s third conceptualisation of capital is of capital in its ideological guise. As Stuart Hall (1979) has shown, capital has an ideological content that is constituted and reconstituted from epoch to epoch. Right at the core of this ideology, there are two essential propositions:

The absolute centrality of private property, the monopoly power over which is ‘both the beginning point and the end point of all capitalist activity’ (Harvey, 2002: 97).

The primacy of markets, characterised by ‘free’ competition, as the superior mechanism for the allocation of resources.

Recalling our earlier discussion of housing’s dual character (use value and exchange value), Forrest and Wissink (2017), reflecting on the continued relevance of Ray Pahl’s (1975)Whose City, ask: ‘What difference, if any, does it make if those providing a service see it essentially in terms of exchange value rather than use value?’ It is an issue raised but not explored in their article, but it is precisely the issue that we take up here. Much has changed in the 50 years since Pahl; most importantly from our point of view is the fact that the intermediaries and gatekeepers are now spread all over the globe. The bankers, financial advisers, lenders, real estate brokers, lawyers, auditors, active investors, property developers and accountants who are involved in this story all operate at different spatial scales – local, national and international – irrespective of where they are domiciled. As Forrest and Wissink (2017) point out, knowledge of their operations has tended to be fragmented, opaque and partial. We set out to interrogate the role of transnational real estate in the global wealth chains of the ultra-rich and the mediating role of active investors, property developers, asset managers and the offshore world. We want to uncover the inner mechanics and logic of the global intermediaries and transnational real estate agents involved.

An emerging literature (Barnes and Prior, 2009; Carlen, 2008; Davies, 2014; Forrest and Wissink, 2017; Hall, 2018; Harrington, 2016; Hay and Beaverstock, 2016; Quentin and Campling, 2018; Sharman, 2017) now fixes on the role of the intermediary. The original question asked by Pahl in Whose City? will today no doubt be answered in much the same way that Pahl and his contemporaries answered some 50 years ago – it is possessed by capital and capitalists. The city remains an inherently unequal space but, in addition, its managers and gatekeepers have been imbued with a more neoliberal outlook. What is unchanged is that these agents still play a crucial, ameliorating role in the distribution of the city’s resources. What Pahl makes clear is that their role should be studied empirically. In the words of Forrest and Wissink (2017: 163): Pahl can help to further this evolving agenda for empirical research, focusing on the complex system of gatekeepers that are the agents of a transformed capitalist order. The location and character of these gatekeepers might have changed but Pahl reminds us that empirical research into their functioning can take us a long way if we want to seriously question and expose issues of power and inequality.

It is to these issues that we now turn.

Global wealth chains: Property developers, active investors, asset managers and local authorities

From the early 1980s, the international political economy became subject to structural changes wrought upon it by the ideological force of neoliberalism and its tendency to generate investment environments increasingly advantageous to capital. These processes, often captured in ideas of commodification and globalisation, enabled wealth creation in more sophisticated and transnational ways. Above all, these processes enabled the widespread establishment of free markets as the central organising mechanism of social and economic behaviour, not only for particular national contexts but also for international capital flows (Harvey, 2005). In this period, new forms of private investment started to gain traction as corporations expanded their activities beyond national boundaries, often through processes of subcontracting and outsourcing, with some arguing that this was directly connected to the deepening financialisation of the world economy (Milberg and Winkler, 2009). These initial steps constituted the start of implicit value chains that led to a period marked by careful and strategic actions by the wealthy and their agents to accumulate, expand and protect their capital at the international scale. Two deep structural changes were to emerge from this. First, a geographical shift in the location of manufacturing from the developed to the underdeveloped world resulting from a geographically unbounded search for higher profits. Second, an organisation of the global economy where power is now increasingly concentrated at the top of the value chain while being more fragmented at the bottom, both in terms of firms and countries.

Value chains are based on the idea that products and services are offered by extended systems of producers, suppliers and other actors like financiers – extending flows and patterns of value across geographies, states and sectors. Global Wealth Chains (GWCs) are related to value chains, but they are in fact very different from them. Wealth chains operate to enable the extraction of value and the creation of wealth through opaque transnational and inter-sector movements of capital by taking advantage of varying taxation regimes. In essence they represent attempts at hiding and benefiting capital, defined as ‘transacted forms of capital operating multi-jurisdictionally for the purposes of wealth creation and protection’ (Seabrooke and Wigan, 2017: 2). This concept prompts us to consider the close role of the London housing market (to give just one example of these processes in action) in operating as an anchor point as these wealth chains ‘touch down’ and extract value from concrete locations. Here, net flows of international capital flow out of, rather than into, the city, as is commonly understood, as profits are taken offshore. These processes occur through the use of offshore vehicles, varying exchange rates and advantageous tax measures to protect and expand the capital holdings of investors.

Wealth chains provide the primary analytical lens in our study. Nevertheless, researchers and scholars in the area of GWCs are confronted with silence on two key issues. The first involves value chain research which, while providing powerful ‘tools for locating value creation, allocation and capture’ (Seabrooke and Wigan, 2014: 7), is mostly silent on the link between value chains, financial innovations and particular legal innovations created by firms, lawyers and investing agents. The second is a general silence about the offshore world in economics, since economic theory tends to reside quite firmly within the boundaries of established national and international law rather than in the grey zones in between, which remain unspecified and unmeasured as a result (though see Bullough, 2018; Urry, 2014). However, Seabrooke and Wigan (2017) offer a useful theoretical framework through which these silences might begin to be addressed. The authors use four key determinants of the governance of GWCs, and these help us to understand how GWCs are formed and articulated and how they change. The four determinants are the complexity of transactions; regulatory liability; innovation capacities among suppliers of products; and the degree of their explicit coordination.

Wealth chains can be seen as a kind of pooling device, or mechanism, that can be used to merge, protect and expand the wealth and assets of the rich. Key examples can be found in the way that Amazon or Google as corporate actors work to sub-contract and use transfer pricing between subsidiaries within their own company to expand profits. Another example, relevant for our purposes here, would be offshore investment shell companies which are used to conceal the identities of owners and which are strongly associated with purchases to launder money as well as evading ‘local’ taxes (Platt, 2015). In relation to the focus of this article, a key feature of the wealth chain is that it brings together a legion of actors and institutions – real estate professionals, lawyers, bankers, legislators, multinational corporations and international networks. Its institutional professionals are also supported by ‘multi-language electronic technologies and websites … linking people, capital and properties across nation state boundaries’ (Robertson and Rogers, 2017: 2). The network is nevertheless anchored in a physical geography, but these spaces are subject to varying legal regimes that are on- or offshore from legal and tax perspectives. Our focus here is on the relationship between a series of offshore wealth chains which share the particular destination for value extraction in the onshore location of the London Borough of Kensington and Chelsea, and those physical properties purchased and traded by owners who are then able to secure benefits by avoiding and evading taxes as they siphon profits back into the offshore world.

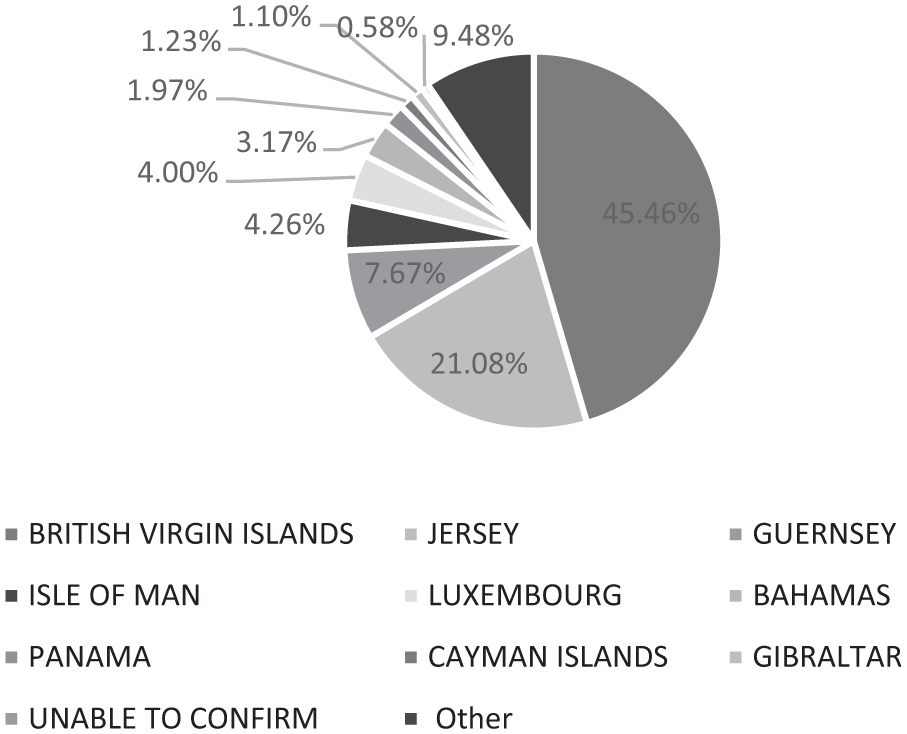

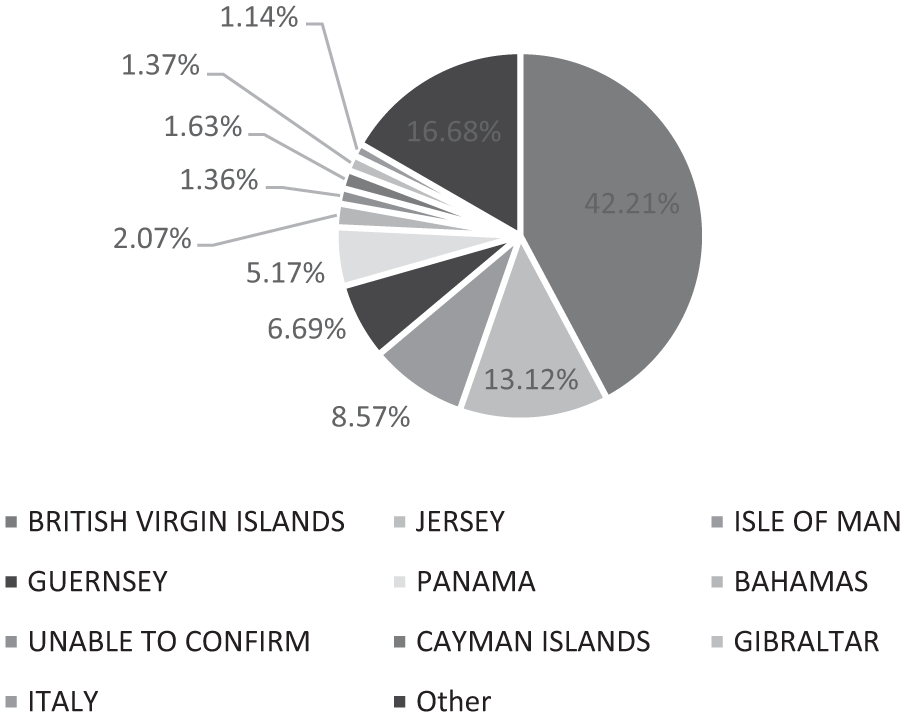

Significant amounts of property bought in Kensington in the decades 1994–2014 were bought from overseas and through tax havens. One effect of this is that ownership is very hard to establish, and this is likely a motivation for the use of shell companies and purchases through offshore trusts. Figures 1 and 2 show that over 45% of all property titles owned by overseas entities in Kensington are registered in the British Virgin Islands, and approximately 80% of all property purchased by foreign entities in Kensington are registered in tax havens. One of the clearest ways of understanding how and why the very rich use the offshore world in this way to purchase prime real estate in London comes from the Paradise Papers (Montalban, 2017). The release of these papers helps us to untangle the kinds of complex webs of arrangements used through purchasing arrangements. For example, in analysing this data we can see that Blackstone’s (a US private equity group) £480 million purchase of Chiswick Park (a business park in West London) demonstrates the routine practice of seeking tax advice from Price Waterhouse Cooper (PwC), a leading Multinational Corporation (MNC) accounting firm with its headquarters in the UK. The advice offered fixed on four objectives (Osborne, 2017):

Reduction of taxes on acquisition;

Reduction of continuing income, corporate, withholding and other taxes in Luxembourg, Jersey and the UK;

The implementation of structures that provided flexibility for additional acquisitions, separation, development and divestment;

The minimisation of tax ‘on exit’ from the UK, Luxembourg and Jersey.

Geographic distribution of ownership, number of titles.

Geographic distribution of ownership (% of property value).

The efforts revealed by this process highlight the elaborate nature of wealth chains. In this particular case, seven companies were created in Luxembourg to facilitate the transaction. Each company cost €75, and for this trivial outlay Blackstone was able to significantly reduce the tax burden on the £30 million in rent it received each year, and subsequently on the £780 million sale of a major part of Chiswick Park to Chinese investors in 2014. The vehicle for the transaction was what is called a Profit Participation Loan (PPL) in which the lender receives a part of the profits in return for the provision of capital. Essentially this involved funds from Blackstone’s property company through five of the new Luxembourg companies packaged as PPLs. The crucial point here is that these funds are treated as equity by the lender and debt by the recipient. This allows the lender to treat the interest received as dividends and, in turn, means that the recipient can offset the interest on repayments against profits while the lender can treat the interest paid as dividends and thus reduce their tax burden.

The two London companies that managed the properties (Blackstone Property Management Ltd and Broadgate Estates Ltd) were deemed to be independent agents of the unit trust, thereby avoiding tax liabilities that would normally accrue to UK companies. In 2013 (two years after the purchase), PwC again provided advice to Blackstone; this time the accountants’ advice centred on how Blackstone could refinance its holdings before putting Chiswick Park up for sale. The substance of this process is important since it was clearly important to minimise all tax liabilities in order to increase earnings. Of course there is absolutely nothing illegal about these arrangements or the advice given. The actual amount of the PPL advised by PwC was £131 million, paid by Blackstone’s funds to the Luxembourg company at the top of this wealth chain. As Chiswick Park was held in a Jersey trust company when Blackstone acquired it, the company was able to purchase prime real estate without paying stamp duty so long as it remained part of a Collective Investment Scheme (CIS). To ensure this status was maintained, the purchase was made through two of the newly created Luxembourg companies (Chestnut 1 Sarl and Chestnut 2 Sarl). PwC advised that any income derived from the UK properties would not be subject to Luxembourg taxes because of the double taxation treaty between the two countries.

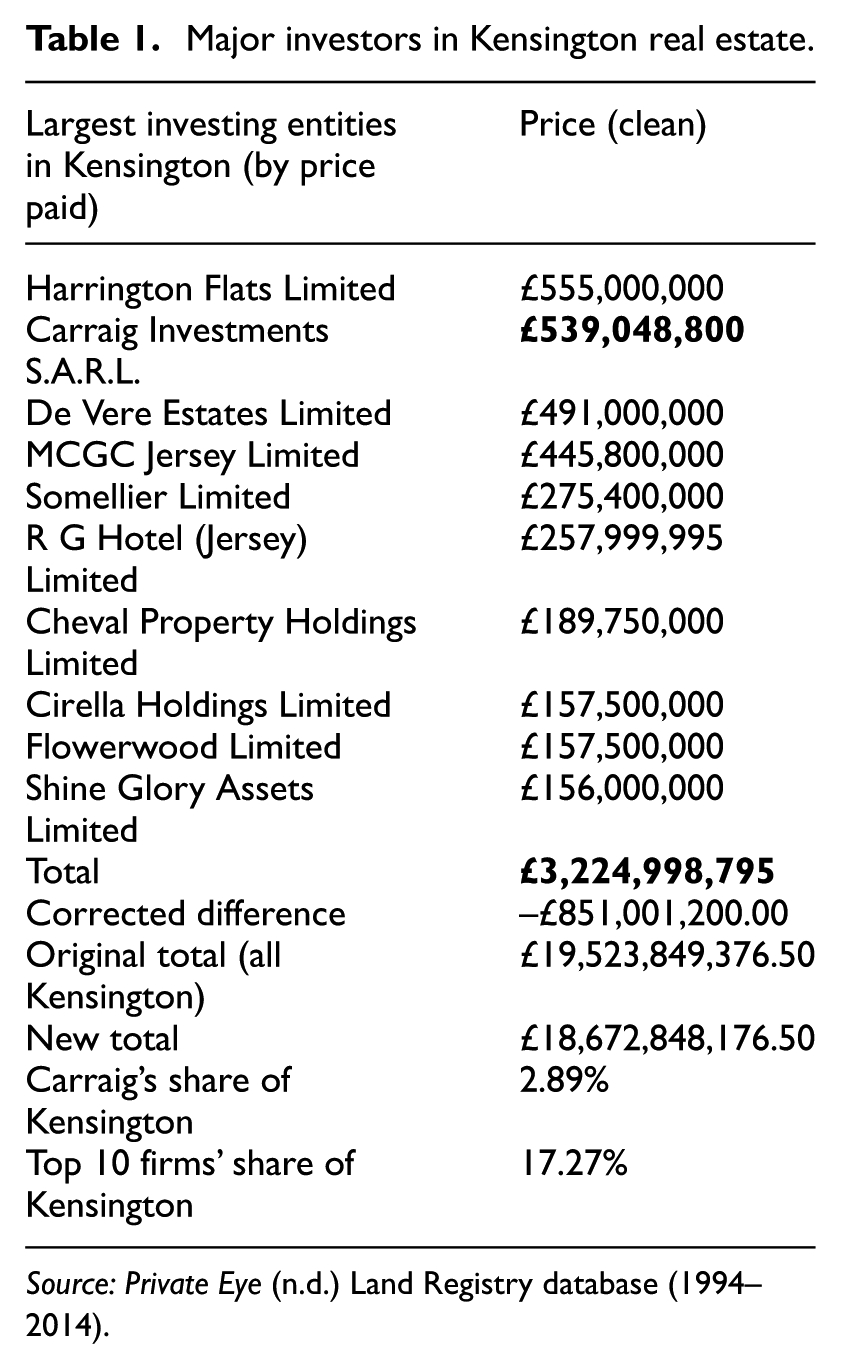

The 10 companies shown in Table 1 own 17% (measured by aggregate purchase value) of the properties bought by foreign investors in Kensington between 1994 and 2014. The amounts paid for property, bought by or through wealth chains, are extraordinarily high. We can see this by focusing on the role of Carraig Investments SARL, the second largest investor, which accounted for around 3% of the total £18.6 billion paid by offshore companies for property in Kensington. The company is registered and headquartered in Luxembourg.

Major investors in Kensington real estate.

Source: Private Eye (n.d.) Land Registry database (1994–2014).

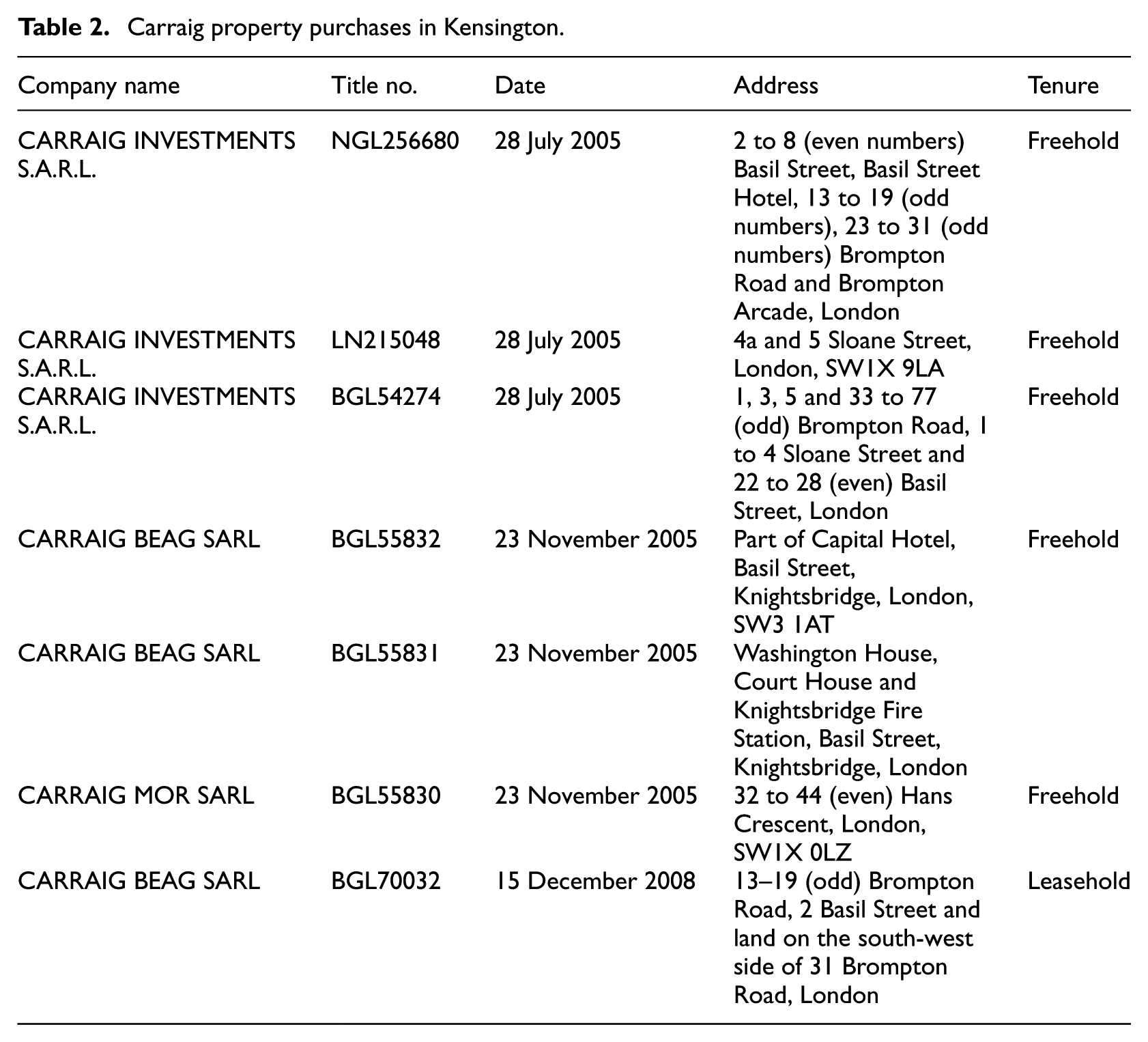

In 2005, a Derek Quinlan-led consortium made up of three Carraig companies – Carraig Investments SARL, Carraig MOR SARL and Carraig BEAG SARL – paid €660m to buy large tracts of land and property in Knightsbridge from the BP Pension Fund. The deal was funded by Anglo Irish Bank, and investors included a group of Irish property developers and a group of solicitors. Quinlan is an Irish businessman prominent in the field of real estate investment and development. He began his career with Coopers and Lybrand as an accountant before joining the Irish Revenue Commissioners as a tax inspector. In 1989, he founded Quinlan Private (a private equity company) as an asset management firm serving high-net-worth individuals (the ultra-rich). Quinlan Private, with offices in Dublin, London and New York, functioned as his main investment vehicle. He enjoyed great success in the period leading up to the peak of the global real estate bubble between 2004 and 2007. However, as with many other companies during the Global Financial Crisis (2007–2009), Quinlan’s day-to-day liquidity was negatively impacted to the extent that he was unable to pay debts when they fell due. In 2009, he was obliged to resign from Quinlan Private and move to Switzerland on the advice of KPMG.

The Carraig purchases relate to seven titles made on either 29 September 2005 or 23 November 2005, with what appears to be an administrative rearrangement on 15 December 2005 where part of Title No. NGL256680 (relating to 13–19 (odd numbers) Brompton Road, 2 Basil Street and land on the south-west side of 31 Brompton Road, London) was transferred from Carraig Investments SARL to Carraig BEAG SARL (see Table 2). The sequencing of the purchases and the companies used suggest that, as in the Blackstone case, some variant of a Collective Investment Scheme (CIS) was utilised in order to acquire these titles. A CIS is defined as: any arrangements with respect to property of any description, including money, the purpose or effect of which is to enable persons taking part in the arrangements (whether by becoming owners of the property or any part of it or otherwise) to participate in or receive profits or income arising from the acquisition, holding, management or disposal of the property or sums paid out of such profits or income. (Collective Investment Schemes Act, Section 235; Financial Conduct Authority, n.d.)

Carraig property purchases in Kensington.

Thus the CIS socialises risk (enabling larger sums of money capital to be raised) and takes advantage of economies of scale. Its sole aim is to earn profit or income for its investors. A ‘Sociétéà Responsabilité Limitée’ (SARL) is a cross between a corporation and a partnership. Its members’ (partners) liability is limited to their contributions to the company. Whereas other corporate entities in Luxembourg (SA, SCA or SAS) cannot grant an advance or loan to finance the purchase of their own shares by a third party, the same does not apply to SARLs (under the Commercial Code). Thus the legal forms utilised in the transaction offer a great deal of flexibility in relation to financing and therefore competitiveness.

In 2010, the Saudi group Olayan, in a joint venture with British property company Chelsfield Partners LLP, bought titles from Avestus (formerly Quinlan Private) for £600 million. 1 An Avestus (formerly Quinlan Private) spokesperson, commenting on the deal, said that they had received an offer they just couldn’t refuse. 2 These titles (listed in Table 2) now make up what has become Knightsbridge Estate K1 Regeneration Project (Knightsbridge Estate is made up of 40 shops and offices between Harvey Nichols and Harrods on the Brompton Road). This is prime property in a prime location in Central London that Chelsfield in its role as asset manager deploys on the asset side of the balance sheet as it seeks to increase the wealth and income of its partners.

Founded by Suliman Olayan in 1947, the Olayan Group was valued at more than US$10 billion by the Bloomberg Billionaires Index in 2015 (Bloomberg, n.d.). The Olayan Group manages the Olayan family’s international business. According to data compiled by Bloomberg, it is one of the largest shareholders in the Credit Suisse Group AG, with a 4.17 per cent stake. Its website shows that the group owns real estate assets that include 550 Madison Avenue in New York City, the Knightsbridge Estate in Central London and residential buildings in Paris’s 8th arrondissement. The Olayan Group is a private multinational enterprise, an international investor and a diversified commercial and industrial concern with operations in the Middle East. It is one of the largest family-owned holdings in the Middle East. Olayan is ranked No. 1 in the Middle East, with a net worth of US$8 billion on Forbes’ Arab billionaires list in 2016 (Forbes, n.d.). With offices in Saudi Arabia, Europe and the US, the Group specialises in public and private equities, real estate and fixed income securities. The commercial side of the group comprises more than 40 companies centred in Saudi Arabia. This group of companies operates in the distribution, manufacturing and services sectors, and many of the companies operate in partnership with Kimberly Clark, Coca-Cola and General Foods, among other leading multinational or regional firms. Some have operations in other Gulf countries and the wider Middle East.

Another key player in the transformations occurring in central London over the past several decades has been Chelsfield, formed 30 years ago by Sir Stuart Lipton. Few people have left a bigger imprint on London’s landscape and skyline than Lipton – he is responsible for over 1.8 million square metres of property development in London, including Broadgate, Stockley Park and the aforementioned Chiswick Park. In 2015, he set up a new property development company with Peter Rogers (the brother of the architect Lord Rogers of Riverside, also responsible for the design of the ultra-prime residences of One Hyde Park in Knightsbridge). The grist for the Lipton–Rogers mill are large, complex schemes in London, as he commented: The action is in places where traditionally we have not had to look, such as the TMT [technology, media and telecoms] sector, where consumers don’t want plain glass boxes for offices. It is in the tough times like this that the property market gets innovative. We have to think about new ways of doing things, and large and complicated projects are our bag. (Hipwell, 2013)

Chelsfield is a property developer, an active investor and an asset manager with offices in London, Paris, New York, Hong Kong, Tokyo and Shanghai. In its investment fund function, it focuses on corporate takeovers and refinancing in the real estate sector. According to its website (http://www.chelsfield.com/en/home/), Chelsfield’s mission is to ‘create high quality long term assets for long term income and capital appreciation’. In the case of the Knightsbridge Estate, this translates to: ‘repositioning of the tenant mix towards premium luxury and luxury retail’. The development, designed by Fletcher Priests Architects, aims to restore this part of London as a key centre of world-class luxury shopping.

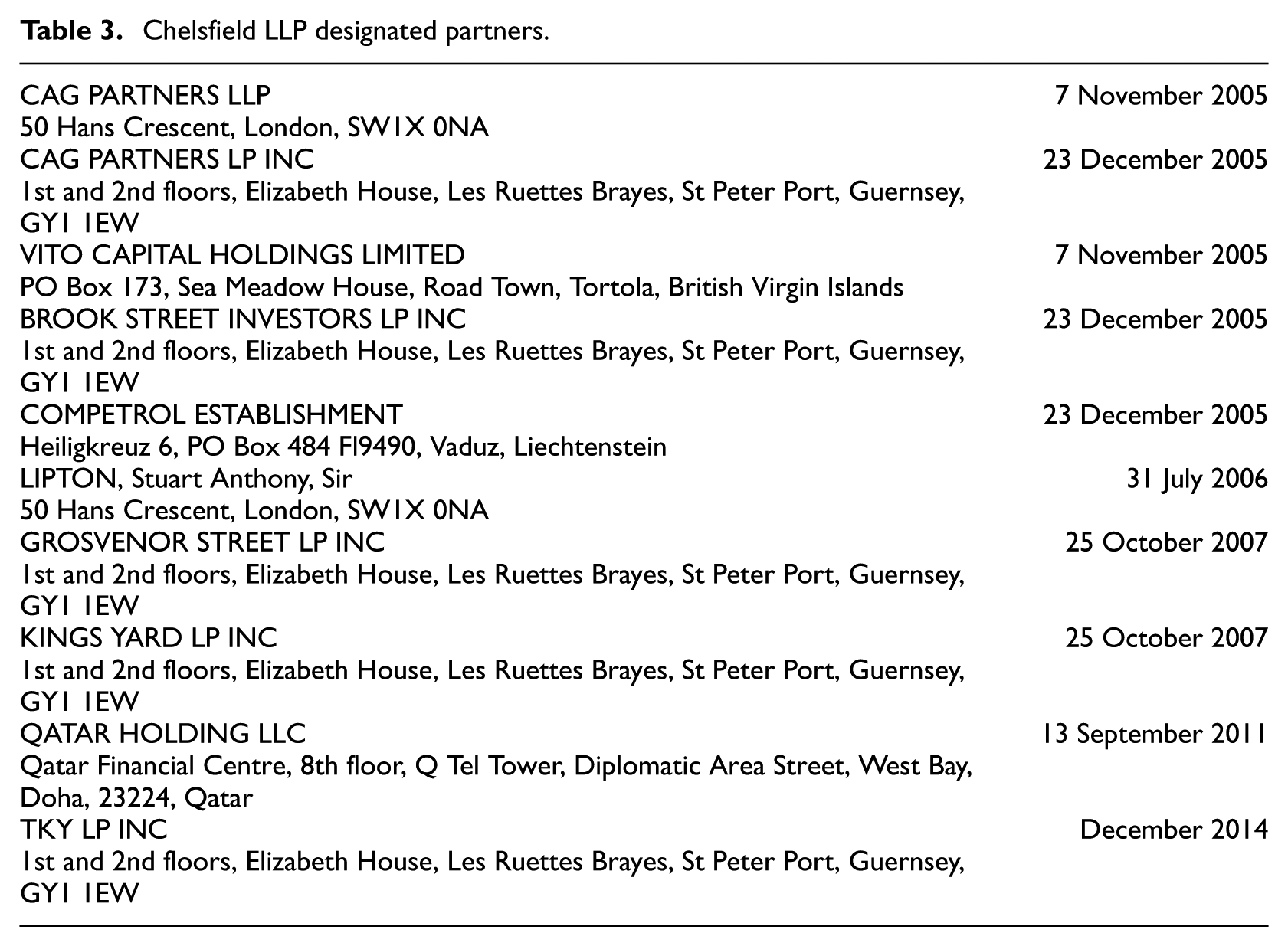

Table 3 lists Chelsfield’s Designated Partners, the dates on which they became partners and their London addresses. All but two (Competrol Establishment and Qatar Holding LLC) of the partners have registered head offices in tax havens that fall within the British sphere (see Shaxson, 2011, for a geopolitical classification of tax havens). Competrol stands out because it is the only one of the partners other than Chelsfield to have directly purchased property (Title No. BGL71719, Flat 8, Lowndes Court, Lowndes Square, London, SW1X 9JJ, on 9 June 2009) in the Knightsbridge Estate regeneration project.

Chelsfield LLP designated partners.

According to the architects, the Chelsfield K1 Knightsbridge Estate regeneration project aimed to ‘reinvigorate, restore and celebrate’ the block above Knightsbridge tube station. The design included retail outlets, new offices, 35 residential flats, an underground car park and a rooftop garden and restaurant. Given the size of the development, in order to comply with local council policy the scheme had to include affordable housing. Chelsfield (through its architect Fletcher Priest) argued: ‘The size of units [flats] are larger than what would normally be associated with affordable housing based on the London Housing Guide’ (Buchanan, 2017). Further, the service charges on the flats ‘would far exceed what would be a sustainable level for affordable housing’. A mix of private and affordable homes was therefore ‘not viable’. The council accepted the submissions and approved the scheme subject to a payment of £12.1m from Chelsfield in lieu of affordable housing at the development. The payment is intended to help the council provide affordable housing in other parts of the borough and/or to renovate existing housing stock. Despite this, it has subsequently emerged that of the nearly £21m the council has received since 2009–2010 for affordable homes, £9.2m remains unspent (Royal Borough of Kensington and Chelsea, 2016). Of the total £57.3m that Kensington had received since 2009–2010, £36.7m remained unspent as of July 2018. All of this takes place in the smallest London borough, with the second highest population density in England and Wales and with extremely limited provision of affordable housing. Similarly, the BBC has reported that none of the developers’ contributions have been used to improve air quality, libraries, sports facilities or health care and that very little has been spent on employment initiatives or children’s playgrounds (Buchanan, 2017).

These examples highlight the complex interweaving of key agents in real estate development and offshore registrations, supported by onshore accountancy advisers working within the law to heavily reduce tax liabilities. The result is a hazy mix of interests working to maximise wealth creation at the boundaries of the law while investing in a landscape of housing and real estate that is used as a means of extracting value, rather than creating wider and beneficial social impacts. Echoing the insights of Seabrooke and Wigan (2017), we would suggest that such examples can be identified as complex systems of avoidance that benefit capitalist investors seeking to play off various jurisdictions of tax and law in order to cement these chains in place.

Conclusion

In this article, we have deployed the idea of wealth chains through close empirical analysis and tracking of land registry data to try and throw light on the forces shaping cities like London over the past decade and more. In locations like Kensington, we see a political economy of property investment that is built around inequalities, an urban politics that favours already advantaged and powerful interests through the maintenance of laissez faire planning (at the local level) and taxation and policing systems at the level of the central state. The concept of wealth chains offers some way of getting inside the black box of strategies of capital expansion. This is because they highlight the transnational and complex key actor and agent figurations of players involved in such efforts at augmenting wealth.

In this article, we have sought to examine key examples of such chains as they touch down upon the particular geographies of the prime property investment fields of a city now strongly associated with the wealthy and their intermediaries. The complexity of arrangements, holdings and patterns of ownership makes such work complicated and time-consuming. This is no coincidence. Holdings of UK property by offshore firms and trusts operate in ways to maximise opacity; this presents a significant challenge for social research to get inside and convey this complexity more broadly. Despite the necessary limits of our approach, we are aware that wider holdings and investments across London, and indeed the UK, are substantial. The scale of laundering, tax avoidance, tax evasion and complex systems of legal offshore ownership represents a major challenge to the kinds of social science labour required to understand and estimate the scale, nature and impact of wealth chains. Such chains operate to channel wealth from these locations and should not be seen as uncomplicated forms of investment in the property market. In the context of massive housing stress in the capital and the crisis in urban management symbolised by the Grenfell Tower catastrophe in Kensington and Chelsea (Burgum, 2019), the massive profitability and lack of accountability of capital is marked. But this, of course, is precisely what capital seeks out in its formation as wealth chains and a force for its own enlargement at the behest of its owners.

The social crisis in the city is arguably exacerbated by the capacity of complex configurations of capitalist systems and the wealthy to circumvent contributions to the organisation of services and core social goods like housing. In this respect, our work returns us to the concerns of analysts like Pahl and Castells who, as we argued earlier, suggested important roles for urban managers and collective forms of provision that traditionally coordinated and managed the more extreme tendencies of the capitalist city to generate inequalities felt acutely around the provision of housing. Our work here, and that of others in recent years, highlights how the capacity of the local state is weakened not only by austerity but also by the ways in which complex wealth chains are able to advance benefits to the wealthy while enabling the avoidance of tax liabilities that might be used to address the kinds of problems experienced in many parts of London today. Wealth chains further enable these forms of wealth creation to evade legal, taxation and planning systems as they are currently set out. The cleavage of interests focused around the division between owner-rentiers and wealth chains, on the one hand, and renter-worker/citizen positions, on the other, highlights a city that has moved increasingly to be aligned with many of the neoliberal plans for a more highly marketised and private system of allocation that has benefited small groups of the already wealthy.

Further empirical work will rely heavily on the ability to access complex and often concealed data sources that have seen periodic releases in recent years. Without such data, wealth chains remain more or less closed entities to which access is extremely difficult to explore. Despite this, the public consequences of these chains – the expansion of wealth inequalities and the avoidance of responsibilities for contributing to the public vitality of national and urban systems – are clearly significant. Our work here offers an initial insight into the potential of such research to help identify the nature of patterns of expanding wealth. Social politics and public anger are increasingly focused on inequality, the crisis in housing (a crisis that has only appeared to expand the fortunes of the already wealthy) and the ineffective role of local and central government presiding over these problems. The misallocation of resources and the production of more or less dead space for the needs of capital rather than communities and workers appear increasingly problematic. It is not yet clear where this social politics will move as the city finds itself facing future crises, but it is perhaps more certain that investment capital will benefit one way or the other.

Footnotes

Acknowledgements

The authors would like to thank Richard Giddings for research support in the production of this article, and Paul Auerbach and Gary Dymski for their general encouragement.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.