Abstract

In housing markets there is a trade-off between selling time and selling price, with pricing strategy being the balancing act between the two. Motivated by the Home Report scheme in Scotland, this paper investigates the role of information symmetry played in such a trade-off. Empirically, this study tests if sellers’ pricing strategy changes when more information becomes available and whether this, in turn, affects the trade-off between the selling price and selling time. Using housing transaction data of North-East Scotland between 1998Q2 and 2018Q2, the findings show that asking price has converged to the predicted price of the property since the introduction of the Home Report. While information transparency reduces the effect of ‘overpricing’ on selling time, there is little evidence to show that it reduces the impact of pricing strategy on the final selling price in the sealed-bid context.

Introduction

Sellers in housing markets face a trade-off between selling time and selling price, and pricing setting plays a crucial role in the selling process (Anglin et al., 2003; Arnold, 1999; Knight, 2002). A high asking price may signal a high reservation price, thereby generating higher bids; it may also discourage participation by potential buyers and result in a longer time-on-market (Anglin et al., 2003; Arnold, 1999; Yavas and Yang, 1995). A low asking price may attract more potential buyers, but it also reduces the probability of achieving high selling prices (Anglin et al., 2003; Arnold, 1999; Deng et al., 2012; Horowitz, 1992; Knight et al., 1994; Yavas and Yang, 1995).

Housing markets are also characterised by information asymmetry between sellers and buyers (Clapp et al., 1995; Knight et al., 1994; Levitt and Syverson, 2008). However, housing markets have become increasingly transparent regarding the information provided because of the development of technologies as well as institutional efforts (Chau and Choy, 2011; Eerola and Lyytikäinen, 2015; Pope, 2008). In the UK, schemes such as the Home Information Pack (HIP) in England and the Home Report in Scotland were introduced in the late 2000s to improve information transparency in housing transactions. These movements indicate a transformation from ‘caveat emptor’ (let the buyer beware, sellers have no duty of information disclosure) to ‘caveat venditor’ (let the seller beware, sellers are liable for non-disclosure) rules (Chau and Choy, 2011). This paper aims to empirically investigate how pricing strategies and the trade-off between selling price and selling time are affected by such institutional changes in Scotland.

The rest of the paper is organised as follows. The next section discusses the background of the Scottish housing markets. Literature on pricing strategy in the sealed-bid context is reviewed in the following section, and the case study area and data are described in the fourth section. Section ‘Empirical models’ discusses the empirical strategies in the paper, and empirical results are subsequently presented in the penultimate section. The final section concludes the paper.

The sealed-bid system and the Home Report in Scotland

In Scotland, most properties for sale are listed in a sealed-bid system, where the ‘offers over’ asking price is usually set below the seller’s reservation price (Pryce, 2011). The system appears to be advantageous to sellers as it seeks to maximise the economic rent 1 (Gibb, 1992); consequently, the sealed-bid system is the dominant selling mechanism, particularly in market upswings. Other selling mechanisms such as ‘fixed price’ or ‘price around’ are used when sellers are under pressure to sell and/or properties are of lower quality.

In the market peak of the mid-2000s, setting artificially low asking prices to create competition amongst buyers was a common practice in Scotland. Such practice was criticised for leading people who could not afford the properties to pay for surveys, contributing to house price instability (Smith et al., 2006), while others argued that the low-asking-prices practice would not determine the pace or direction of the market (Levin and Pryce, 2007). With the objectives of improving information transparency and market efficiency, and to address the problems associated with artificially low asking prices, the Scottish government introduced the Home Report scheme in 2008 (Black et al., 2015). Since 1 December 2008, the scheme requires home sellers 2 to provide a Single Survey, 3 an energy report and a questionnaire 4 when listing dwellings on the market. Sellers are responsible for the costs of the Home Report, and potential buyers can access the report free of charge.

Pryce and Gibb (2006) suggest that the scheme is unlikely to alter sellers’ benefits, but the authors are unclear about potential changes in sellers’ behaviours. Based on survey and public consultation data, the Scottish government’s review finds that the scheme met the objectives, particularly in addressing the issue of artificially low asking price, but, as the authors point out, ‘poor market conditions have also played a role’ (Black et al., 2015: 6). On the contrary, other research commissioned by the Scottish government suggests little change in price-setting practices since the introduction of the Home Report (Robertson and Blair, 2014). Recently, the emphasis on comprehensive information has been extended to the private rental sector in Scotland with proposals to include the Home Report in tenement regulations (Sottish Government, The, 2019).

Conceptualising pricing strategy in the sealed-bid context

The rationale of setting a low asking price in the sealed-bid system has been explained in several studies. Low asking prices maximise uncertainty by contributing to a larger variance in the asking–selling price differences in a submarket (Pryce, 2011; Smith et al., 2006), which, in turn, may be perceived as an indication of strong growth in selling prices. Estate agents are incentivised to reinforce the perception of a buoyant market by advising on low asking prices (Pryce, 2011). Such a strategy is less effective during market downturns as sellers are more likely to accept the first bid that meets or exceeds their reservation price, and a low asking price could signal a lower bargaining position (Thanos and White, 2014).

It is also important to distinguish between the private and common values in the auction context. Sellers determine pricing strategy according to their private values based on the acquisition prices, housing attributes and selling prices of properties nearby. The ‘common value’ element refers to market professionals’ information on the submarket, on which they base their advice to sellers on pricing strategies (Thanos and White, 2014). Pryce (2011) measures the ‘common value’ element by calculating the dispersion of asking–selling price spread in a submarket. A larger dispersion indicates a weaker ‘common value’ element or a weaker ‘locational convention’. Empirical studies find that with a weaker common value element, time-on-the-market (TOM) is more sensitive to pricing strategies (Pryce, 2011), and both optimal list price and selling price are higher (Deng et al., 2012).

Imperfect information in the housing market results in some elasticity in the demand curve for the individual dwelling (Maclennan et al., 1987). In a rapidly inflating environment, increasing prices contribute to information asymmetry by ‘fracturing the flow of information which is so critical to the operation and clearing of markets’ (Smith et al., 2006: 90). Levitt and Syverson (2008) argue that information asymmetry has resulted in greater pricing distortions and find that estate agents with superior information tend to sell their own properties at higher prices. Rutherford et al. (2007) show similar conclusions. Auction literature also shows that standard auctions are only revenue-maximising when buyers are symmetric and have independent private valuations, but when buyers have interdependent valuations, auctions lose this advantage (Campbell and Levin, 2006; Wang, 1993). Before the Home Report was introduced, asking prices acted as signals to potential buyers that facilitated the narrowing of their search (Anglin et al., 2003). With the Home Report, valuations are more likely to act as reference prices for buyers (Black et al., 2015). As suggested by Ariely and Simonson (2003), when salient reference prices are available, the influence of starting price on the final selling price in an auction diminishes. In the Scottish context, a Home Report valuation also indicates the collateral value for mortgage purposes, thereby reducing the level of financing uncertainty for the buyers. Hence with the Home Report, there seems to be little incentive for the sellers to set an asking price that differs hugely from the valuation. The first empirical objective of this paper is to examine whether the introduction of the Home Report has had a significant impact on sellers’ pricing strategy.

If the Home Report has changed sellers’ pricing behaviours, would it also have an impact on the trade-off between selling price and selling time? Nanda and Ross (2012) show that sellers who disclose more information tend to achieve higher selling prices. In Pope (2008), the disclosure of negative information (such as airport noise) reduces selling prices. Similarly, Chau and Choy (2011) find that properties affected by highway noise are sold for less under the ‘caveat venditor’ rules. The empirical evidence on TOM is mixed. Findings in Wong et al. (2012) imply that information symmetry reduces TOM. Supported by empirical results, Levitt and Syverson (2008) show that sellers with superior information stay on the market for longer at a higher selling price. Rutherford et al. (2007) find that information asymmetry has little impact on TOM. The second empirical objective of this paper, therefore, is to investigate the impact of information transparency on the trade-off between selling price and TOM.

Case study area and data

The study uses residential property transaction data from the Aberdeen Solicitors Property Centre (ASPC). The ASPC primarily serves as a central marketing place for residential properties in North-East Scotland and captures approximately 90% of total transactions in the region. The data set covers the housing market in Aberdeen city, Aberdeenshire and a small part of Angus adjacent to Aberdeenshire from 1984Q2 to 2018Q2.

5

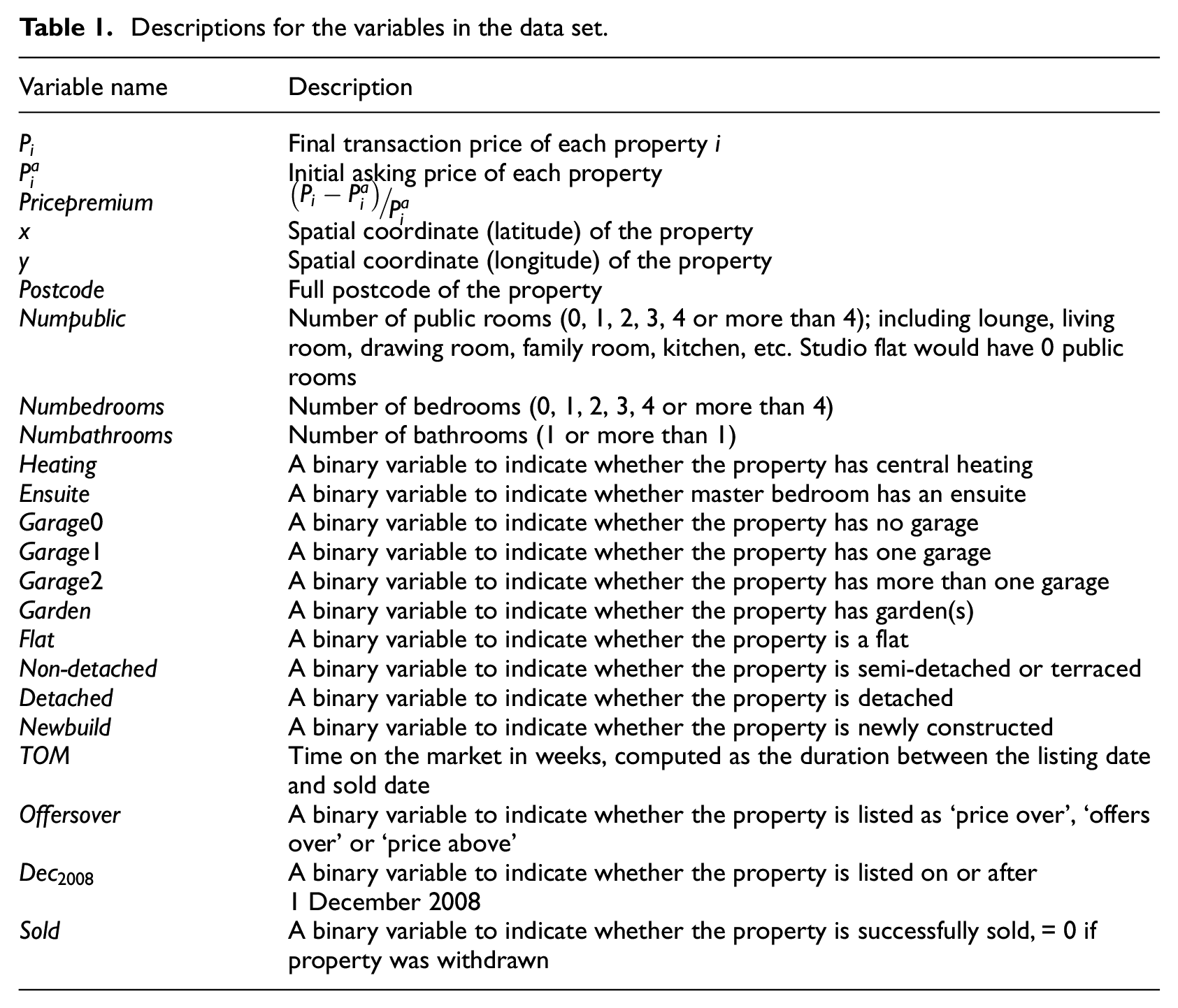

Table 1 shows the description of all variables in the data set. Owing to the availability of the variables

Descriptions for the variables in the data set.

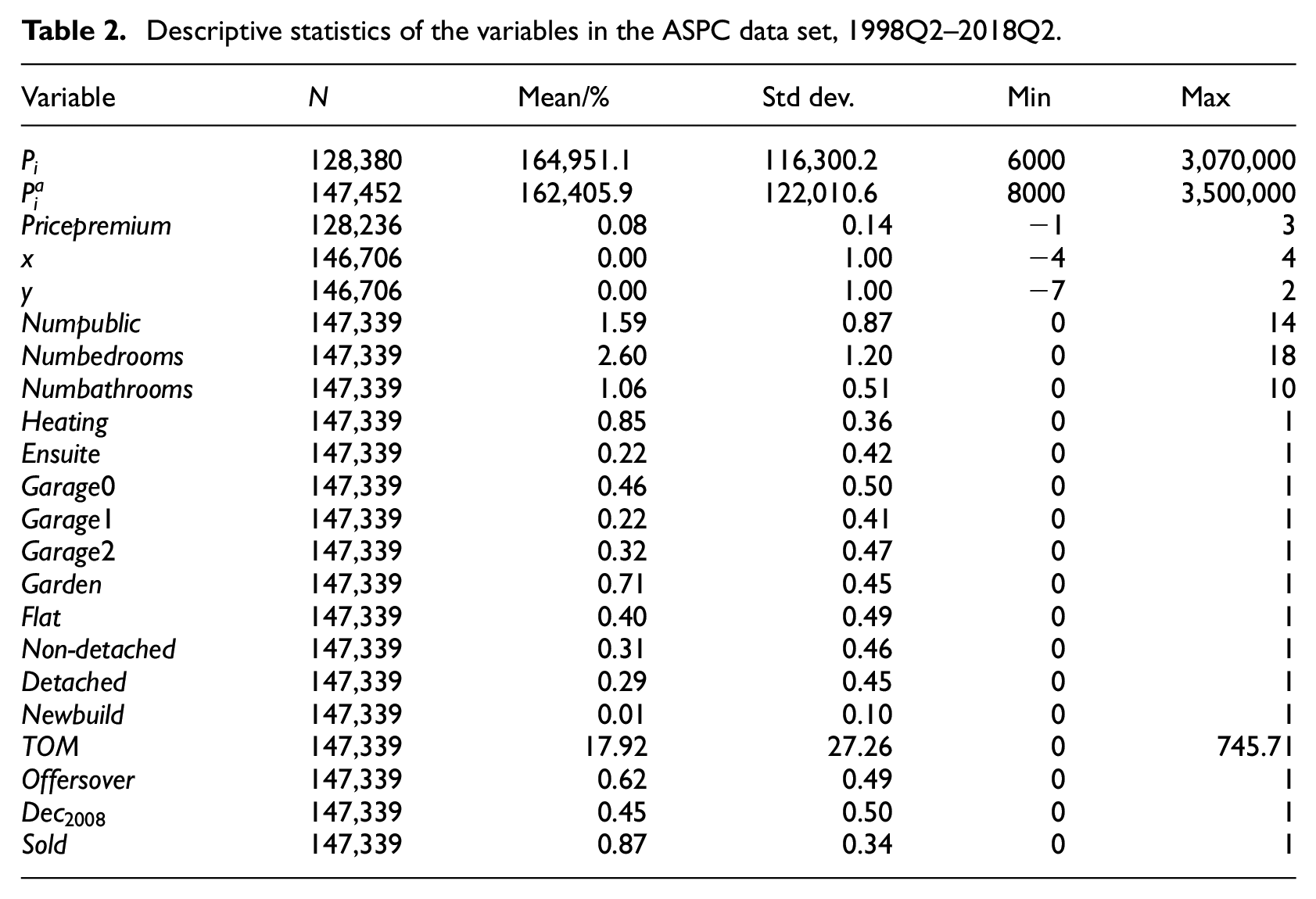

Descriptive statistics of the variables in the ASPC data set, 1998Q2–2018Q2.

In addition to the geocodes and postcodes, the data set includes 80 geographical areas, which are neighbourhoods and towns defined by the ASPC. Potential buyers can filter their search by these areas on the ASPC’s website, and they are used as the predefined submarkets in this study. 7

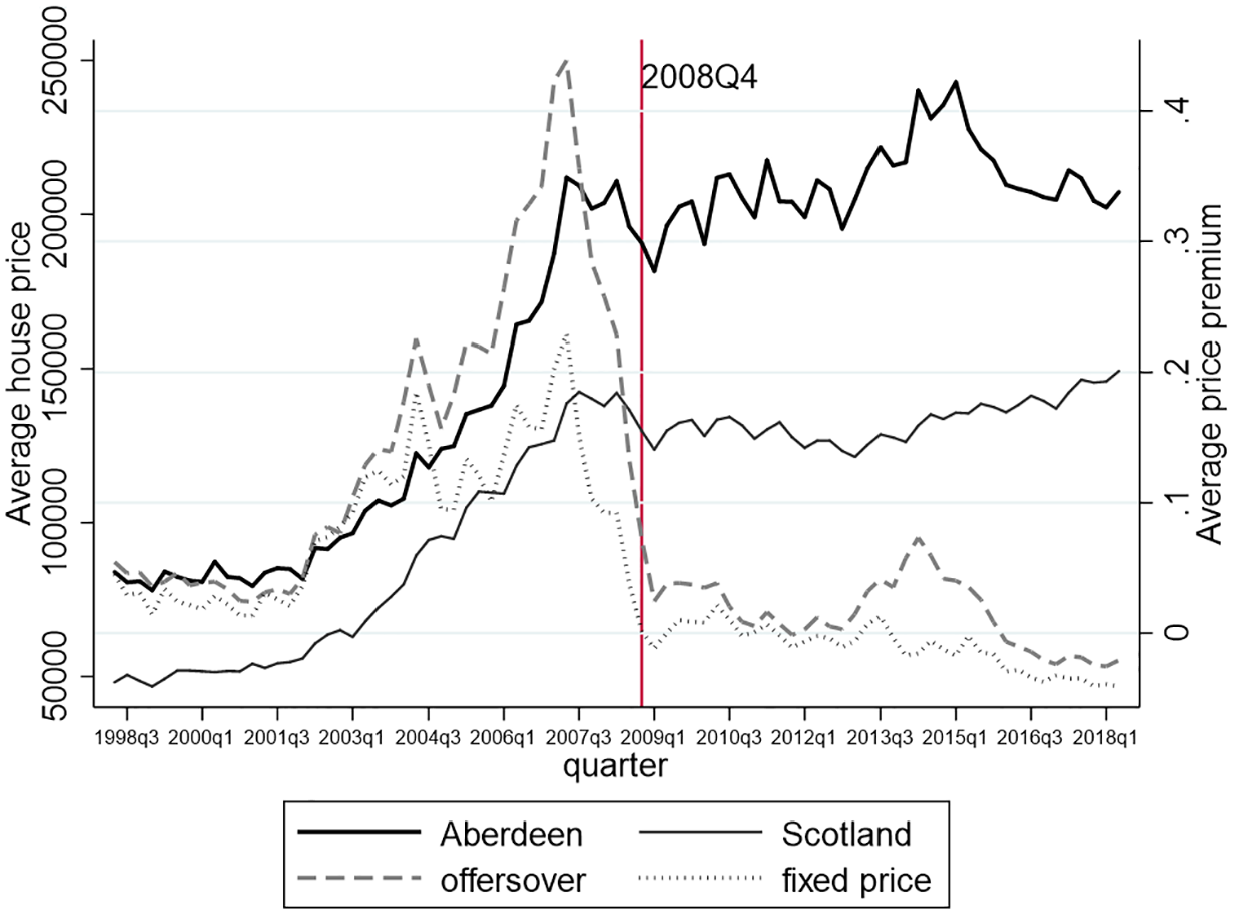

When the Home Report was introduced in December 2008, most UK housing markets were experiencing a dramatic downturn as a result of the global financial crisis. However, house prices in the study area were less affected by the financial crisis because the region’s economy is predominantly influenced by the oil and gas sectors. As shown in Figure 1, compared with house prices at the national level, prices in the Aberdeen housing market (measured by the left-hand side vertical axis) recovered relatively quickly after the 2007 financial crisis and reached another noticeable peak in 2015. Subsequently, prices in the Aberdeen area started to decrease as a result of the significant fall in oil prices in late 2015, while prices in the rest of the country continued to increase. This shows the peculiar nature of the Aberdeen housing market given its independent market cycle associated with the oil industry. The case study area allows pricing strategy to be compared before and after the introduction of the Home Report without the concern of the potential simultaneous effect of a market slump. The data set also covers a relatively long period with more than one property cycle, which is useful for investigating the effect of market buoyancy on pricing strategy.

Asking–selling price premiums and average real house price in Aberdeen housing market and Scotland 1998Q2–2018Q2.

Figure 1 also shows the average

Empirical models

As highlighted in section ‘Conceptualising pricing strategy in the sealed-bid context’, this paper has the following empirical objectives:

to test if the introduction of the Home Report has a significant impact on sellers’ pricing strategy; and

to examine the influence of the Home Report on the trade-off between the selling price and selling time.

Estimating the price of a property

Pryce (2011) suggests that ‘perhaps buyer/seller beliefs about a property’s value are based on simple rules of thumb that are best approximated by a fairly rudimentary hedonic model … valuers’“professional judgement” may in fact boil down to a fairly simple set of intuitive rules’ (p. 775). The paper starts with a baseline log-linear hedonic specification presented in Model (1):

where

The use of geocodes does not necessarily fully capture the locational effects concerning neighbourhood qualities. Some house price studies conceptualise the location of a property using fixed locational attributes (Orford, 2002). For example, Bracke et al. (2017) include fixed effects at the street level in their hedonic model. In this paper, Model (2) captures the fixed locational effect at submarket level:

where

Many also argue that housing market dynamics operate at different spatial levels and hedonic models should allow for the differences in prices caused by such locational externalities (Gelfand et al., 2007; Goodman and Thibodeau, 1998; Jones and Bullen, 1993; Leishman, 2009; Leishman et al., 2013; Liu and Roberts, 2012; Liu et al., 2018; Orford, 2000). These studies propose multilevel models, in which house prices are modelled using property-level attributes and higher spatial-level attributes to allow for the potential differences in the intercept term and housing attributes at different spatial scales. Using neighbourhood as an example, the multilevel model assumes that neighbourhoods in the data set are a random sample of larger population neighbourhoods, and the coefficients for the neighbourhood effects vary randomly around an overall mean (hence referred to as the ‘random effect’).

Model (3) illustrates such hierarchical specification for the ASPC data: at the individual property level (level 1), price is assumed to be determined by physical attributes and location (measured by

where

At level 2, the random intercepts and slopes are expressed as:

and

where

By the same token, the random intercepts and slopes at level 3 are:

and

where

This first stage of selling prices modelling is important because misspecifications could result in misleading estimates of the pricing strategy variable in the next stage (Pryce, 2011). The multilevel model recognises the potential locational structure of the data; thus it has the capacity to improve predictive power, reduce spatial dependence, capture heteroscedasticity and allow explicit modelling of the influence of submarkets (Leishman, 2009; Leishman et al., 2013; Orford, 2000, 2002). However, the model does not account for sellers’ heterogeneity, which could cause unexplained residual in the hedonic specifications (Glower et al., 1996). Furthermore, the group-level effects may simply reflect the misspecification of or unaccounted for individual-level predictors (Diez-Roux, 2000; Gelman, 2006), and this limitation is particularly relevant to this study, as omitted variable bias can be present at the property level. Indeed, many have argued that multilevel models are unable to fully capture all spatial processes in house price data (Chaix et al., 2005; Chasco and Le Gallo, 2012; Hu et al., 2019). Another potential issue with multilevel models is that the interrelationships between variables at different levels are not fully examined; for instance, it is possible that property-level attributes may influence group characteristics; and vice versa (Dedrick et al., 2009; Diez-Roux, 2000).

Pricing strategy

In the following equation, the asking price is compared with the estimated prices from the hedonic models to indicate pricing strategy or the degree of overpricing (DOP): 11

where

Section ‘Conceptualising pricing strategy in the sealed-bid context’ highlights that the sellers’ pricing strategy is influenced by market conditions, the locational convention of a submarket and selling mechanisms. First, to control market conditions, variable

A small

where

It is unlikely that equations (4) and (5) can fully model the determinants of sellers’ pricing strategy. As pointed out by previous studies, sellers’ motivation and behaviours also play a critical role in housing market dynamics (Anglin et al., 2003; Genesove and Mayer, 2001; Yavas and Yang, 1995). Studies have shown that factors such as the expectation of capital gain (Ong and Koh, 2000), sellers’ characteristics (Springer, 1996), sellers’ motivation (Glower et al., 1996) and sellers’ original purchase price (Genesove and Mayer, 2001) can all have an impact on pricing strategy. As the ASPC data have no further information on the sellers, it is impossible to include such measures in Models (4) and (5). Such limitations are further discussed in conjunction with the empirical results in section ‘Empirical results’.

Testing the effect of the Home Report

To indicate the introduction of the Home Report, a dummy variable

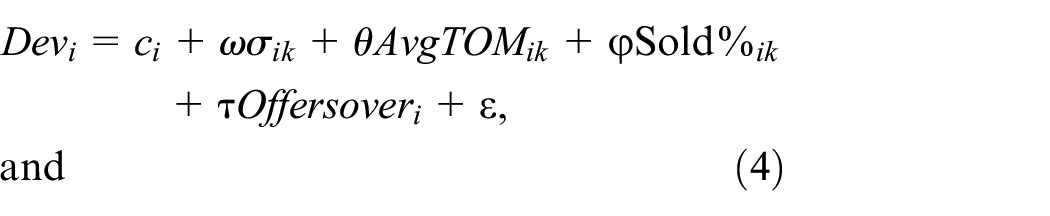

The trade-off between selling price and selling time

The second empirical objective of this paper is to examine the influence of the Home Report on the trade-off between the selling price and selling time. In the selling price Models (8)–(10),

The final stage is to examine

where

Overpriced properties are expected to have a longer TOM. However, the more buoyant the market, the shorter TOM is expected to be. If the Home Report has changed the liquidity of residential properties, the magnitude of

Empirical results

Results for estimating property prices

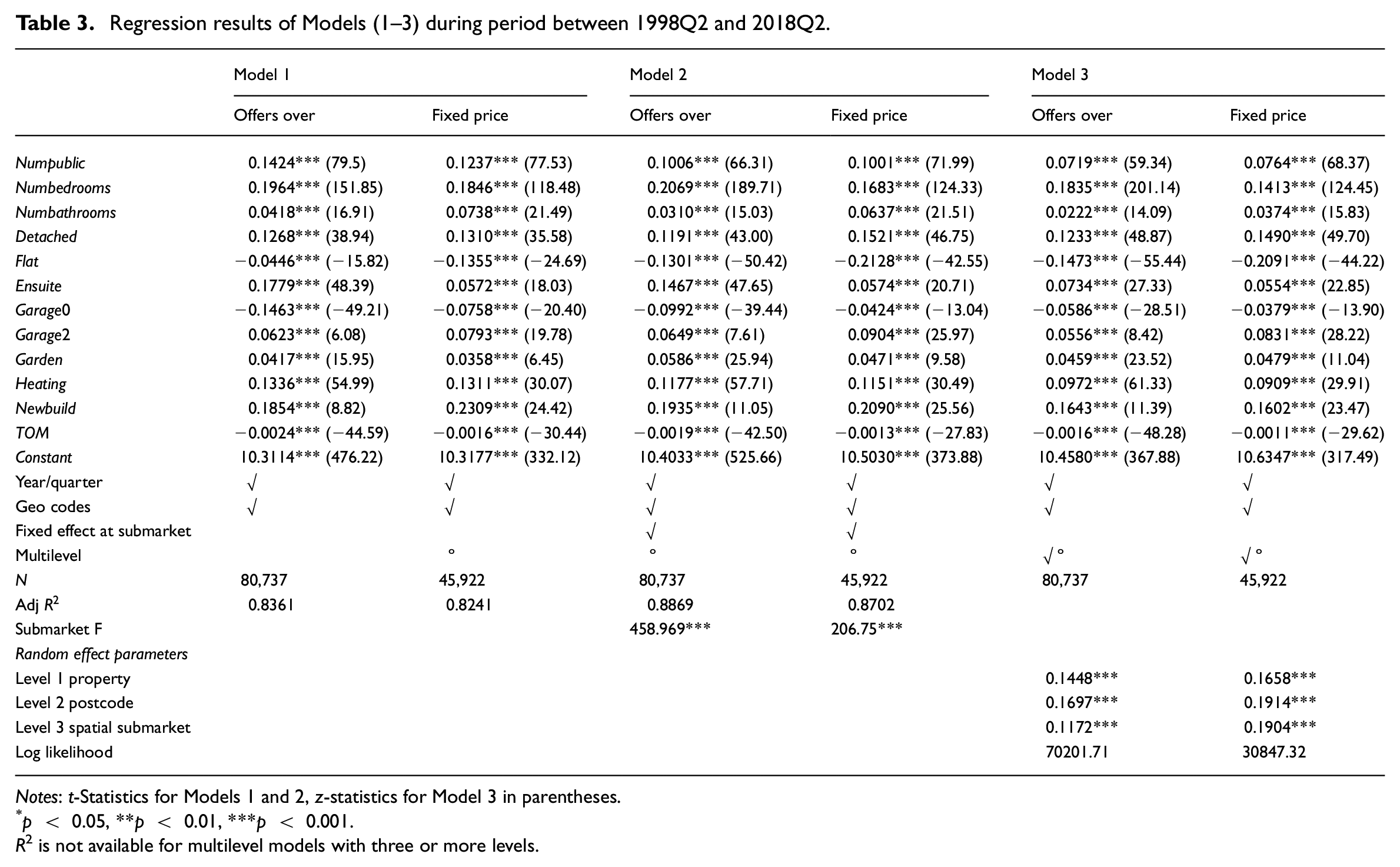

The performances of Models (1)–(3) are presented in Table 3. The adjusted

Regression results of Models (1–3) during period between 1998Q2 and 2018Q2.

Notes: t-Statistics for Models 1 and 2, z-statistics for Model 3 in parentheses.

p < 0.05, **p < 0.01, ***p < 0.001.

R2 is not available for multilevel models with three or more levels.

The Home Report and pricing strategy

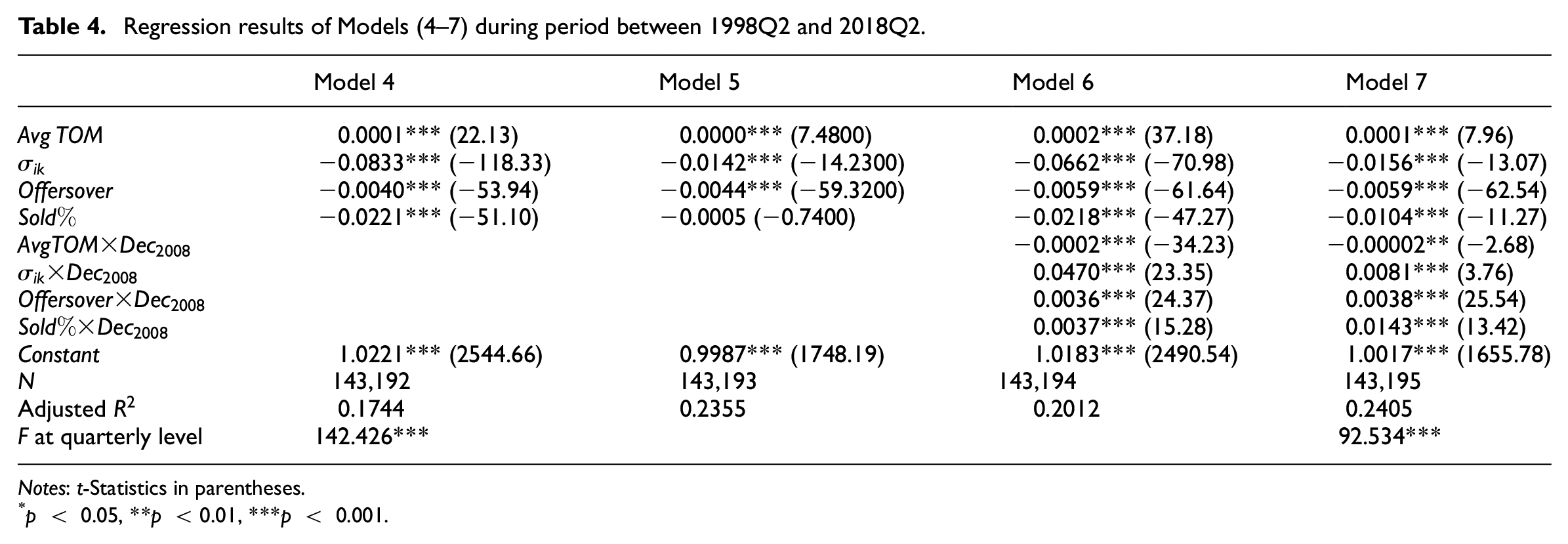

Table 4 displays the results of Models (4)–(7) and shows that market conditions, locational convention and selling mechanisms are significantly correlated to

Regression results of Models (4–7) during period between 1998Q2 and 2018Q2.

Notes: t-Statistics in parentheses.

p < 0.05, **p < 0.01, ***p < 0.001.

The trade-off between selling price and selling time

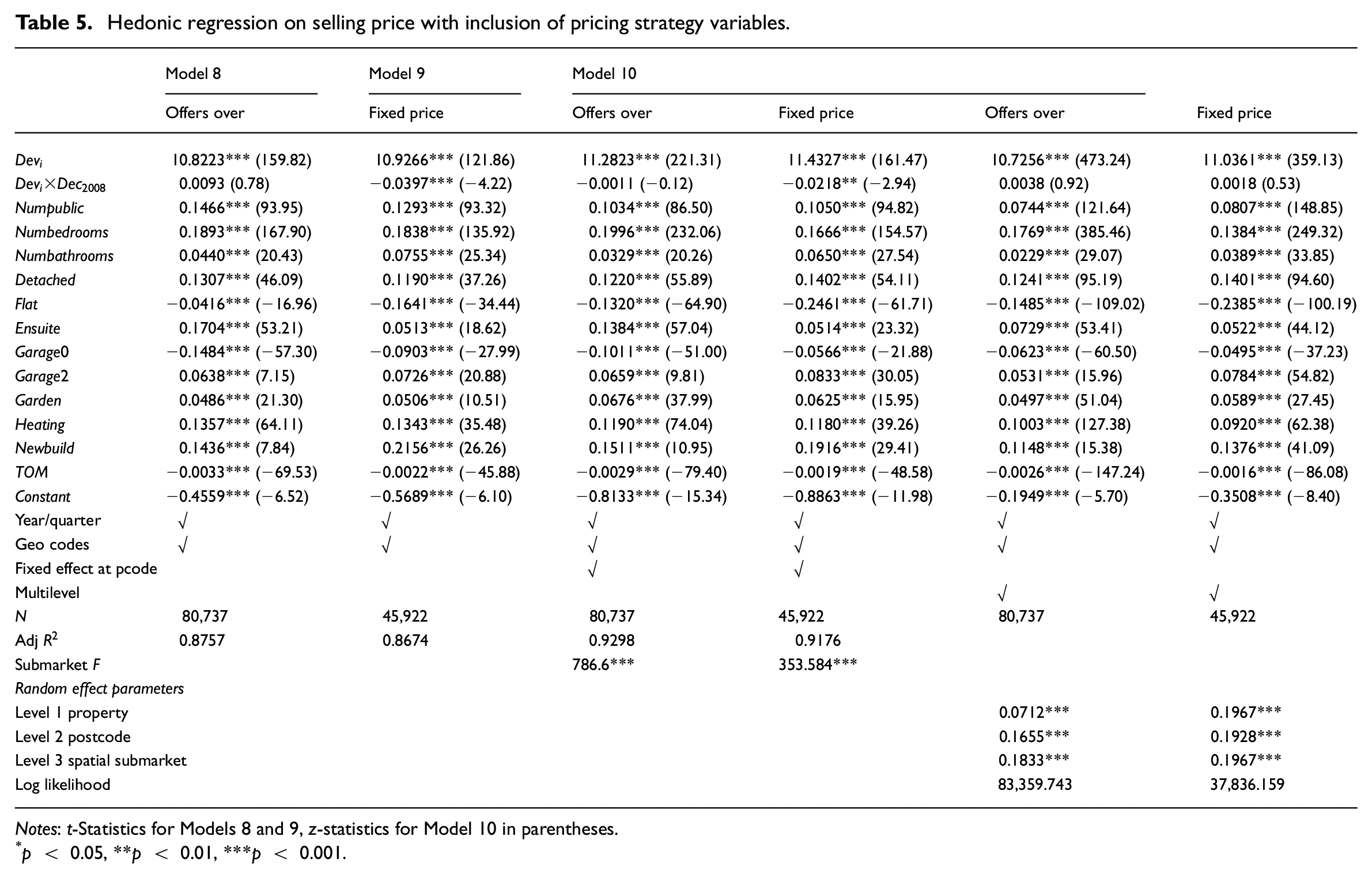

Consistent with previous studies such as Anglin et al. (2003), Arnold (1999) and Springer (1996), results of the price Models (8)–(10) in Table 5 show positive and significant coefficients of

Hedonic regression on selling price with inclusion of pricing strategy variables.

Notes: t-Statistics for Models 8 and 9, z-statistics for Model 10 in parentheses.

p < 0.05, **p < 0.01, ***p < 0.001.

There are four possible explanations for such ‘puzzling’ results. First, this paper implicitly assumes that agents are rational and that they use current market price as the reference point; but it does not consider behavioural biases that can affect exchange behaviour (Gallimore and Wolverton, 1997; Paraschiv and Chenavaz, 2011). An example of a behavioural factor is illustrated in Genesove and Mayer (2001) and Einiö et al. (2008), when a seller’s reluctance to realise a housing loss can help explain their choice of an asking price. In addition, factors such as Loan-to-Value (LTV) put ‘an institutional constraint on sellers’ behavior’, and ‘its effect does not diminish with learning or exposure to market conditions’ (Genesove and Mayer, 2001: 1252), it is also possible that such institutional constraint has not changed with the Home Report. Second, publicly available information may not be adequately considered by buyers (Pope, 2008) and improvement of such information symmetry may not affect the final selling price. Third, the Home Report does not disclose all the information (for example, there is no information on the neighbours or nuisance) and information asymmetry can still exist. Finally, as mentioned before, there might be misspecifications of the hedonic models that misrepresent sellers’ bargaining power (Anglin et al., 2003).

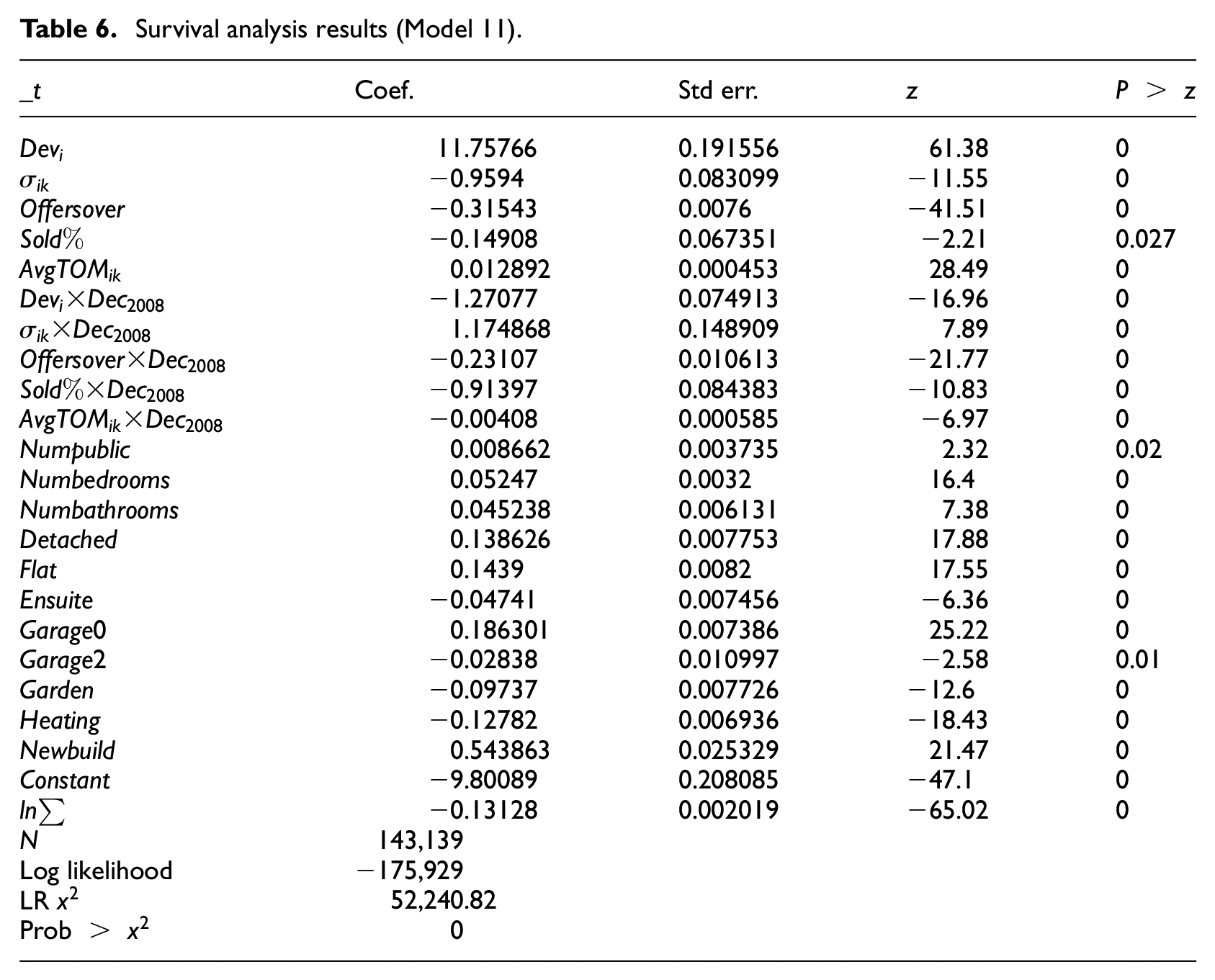

Results in Table 6 confirm the anticipated positive correlation between overpricing and TOM, which is in line with previous studies (Pryce, 2011; Yavas and Yang, 1995). Also as expected, properties are more liquid in a buoyant market and ‘offers over’ properties sell faster than ‘fixed price’ properties. The highly significant coefficients of the interactive terms

Survival analysis results (Model 11).

Conclusion

There has been a global trend in improving information transparency in housing markets at an institutional level and this paper set out to investigate the impact of such institutional changes on the trade-off between selling price and selling time in the sealed-bid context. The empirical results support the view in the existing literature: improvements in information symmetry appeared to influence sellers’ pricing strategy. However, while the results suggest that the Home Report reduces the effect of pricing strategy on selling time, this study did not find conclusive evidence to support the view that the scheme could reduce the influence of overpricing on the final selling price. This finding implies that although sellers bear the costs of the Home Report, potentially they could benefit from increased liquidity.

The paper has a wider implication for policymakers globally. It highlights that institutional factors do influence the behaviours of market participants. Both sellers and buyers can benefit from a higher level of information symmetry. Policymakers should compare the monetary and social cost of improving information transparency with the benefits of such schemes and further assess the usefulness of such schemes in bringing market stability.

Inevitably, the study has some shortcomings. First, there might be specification issues surrounding the computation of predicted selling price, which in turn could misestimate the pricing strategy variable. The study attempted to address the problem using a multilevel model in order to consider the unobservable neighbourhood effects. Despite the limitations of the OLS and multilevel model, the models yielded reasonable goodness to fit and the results appear to be robust. Nevertheless, the limitations of the models should not be ignored. Second, the pricing strategy is modelled using a simple OLS regression with limited control over sellers’ characteristics, so the prediction level of the model was relatively low. This is an area where further research is needed. There is also more work to be done in the trade-off between selling price and selling time. Particularly, the study can be extended to examine the behavioural factors of both sellers and buyers. Third, there is a need to further understand the role of TOM as a determinant of equilibrium price in a ‘caveat emptor’ context (Pryce, 2011). The process of shifting from one selling mechanism to another and the role played by TOM was not explicitly examined in this paper. From an institutional perspective, future research should consider the implications for the total information costs under the two distinct legal regimes (caveat emptor and caveat venditor).

Supplemental Material

sj-pdf-1-usj-10.1177_0042098021991784 – Supplemental material for Market buoyancy, information transparency and pricing strategy in the Scottish housing market

Supplemental material, sj-pdf-1-usj-10.1177_0042098021991784 for Market buoyancy, information transparency and pricing strategy in the Scottish housing market by Nan Liu in Urban Studies

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.