Abstract

This article analyses situated uses of digital payment platforms, contributing to the sociology of money, and digital sociology. Our data are video recordings of 256 small-scale transactions, gathered from across four Chinese cities, at grocery stores, supermarkets, street markets, restaurants, and cafes. Our focus is the visibility of money in particular circumstances associated with some WeChat payments. In these cases, payment is made visible via a confirmation screen only seen by the customer. We argue that payment applications provide a good empirical site for understanding how digital media reconfigure ‘the social’ by shaping how monetary information is seen and heard. Rather than eliminating trust, reducing transactions to impersonal semi-automated affairs, we show how mobile payments generate new and complex patterns of economic action. A nuanced language game is described that requires sellers to trust customers are acting in good faith. We show how ‘the social’ is imprinted on this contemporary monetary medium.

Keywords

Introduction

In recent years, ‘the surge of new currencies and payment systems has transformed how we use money and how we think about it’ (Bandelj et al., 2017: 5). Monetary media have changed throughout history, taking such forms as shells, leather pieces, liquor and gold dust (Hart, 2001: 237). But at present, money is changing at an unprecedented rate (Maurer, 2015). One change has been the ‘monetary revolution’ (Birch, 2017: 95) brought about by the mobile phone, described as ‘the least noticed and yet perhaps most important development in modern financial history’ (Ferguson, 2019: 444). There were seven mobile money services in the world in 2006, and 227 by 2016 (GSMA, 2016: 28). This trend is nowhere more visible than in China, where the market share of mobile payment has grown from 3% in 2011 to 83% in 2018 (Statista, 2019: 15). The ‘future of money maybe under construction’ in China, where many cities are now virtually ‘cashless’ (Ferguson, 2019: 446).

Sociological studies have started to consider these changes at the macro level, describing the ‘new sociability of money’ (Guseva and Rona-Tas, 2017). We analyse these tumultuous changes by zooming in to understand how they are ‘embedded in everyday life’ (Fussey and Roth, 2020: 660), exploring how buyers and sellers in Chinese cities use mobile payment applications. The data are video recordings of 256 everyday transactions, where people use WeChat Pay and Alipay in supermarkets, hairdressers, taxis, shops, street markets and restaurants. Videos are analysed by drawing on ethnomethodology and conversation analysis, where prior studies have also analysed money ‘changing hands’ (Clark and Pinch, 1992; Llewellyn, 2016; Mondada et al., 2020). Our dataset provides unprecedented access to contemporary monetary media, how ‘money is shaped from the inside by the social practices of its users’ (Dodd, 2017: 231).

Our central focus is the visibility of digital monies and how people ‘see data’, such as numbers on a phone screen, in interaction (Kennedy and Hill, 2018: 834). Monetary media have always varied in terms of visibility, for example, subterranean informal monies have circumvented constraints placed upon official currencies (Carruthers and Ariovich, 2010: 47). But mobile money adds an intriguing new dimension to this problem. Cash is symmetric, from its material form buyers and sellers see the same thing changing hands, but with mobile payment applications, on occasion, only the customer may ‘see the data’ (Kennedy and Hill, 2018) and know whether money has ‘changed hands’. Rather than neutral, payment applications configure ‘the social’ in particular ways, creating new problems. We investigate one – whether, when and how customers are obligated to demonstrate they have paid. We find mobile payment is not a semi-automated process, but a thoroughly social one, posited upon the ability of buyers and sellers to navigate an intriguing language game that to differing degrees requires sellers to trust that customers are acting in good faith.

The Visibility of Digital Money

Sociological literature is addressing how the transformation of material objects into digital information is shaping everyday activities and social relations (Brownlie and Shaw, 2019; Kennedy and Hill, 2018; Fussey and Roth, 2020; Wood et al., 2019). We add to this work, analysing how people use mobile payment platforms in the context of small-scale everyday transactions. Our central focus is the visibility of immaterial digital money. While material money configures transactions so parties see the same information, mobile payment applications disturb this easy line of sight.

The visibility of money has been a recurrent theme in sociology. Zelizer’s (1989, 1994) meso-level analysis is a good place to start. It has motivated much contemporary sociological interest in money, and visibility is a recurrent theme. In relation to the management of domestic money, Zelizer (1989) shows how in middle-class households, men typically passed only a proportion of their wages to their wives as ‘dole’ and then ‘allowances’. What remained was private and unseen. Women might be trusted with credit, the uses of which could be supervised and observed by the husband (Zelizer, 1989: 359), but not cash, the uses of which are less visible. In working-class households, in contrast, men passed all of their wages to their wives who then allocated them an ‘allowance’, putting what remained to household needs. Wives saw all the money coming into the house, although men might finesse the arrangement; when passed, the ‘envelope’ containing the husband’s earnings was not ‘necessarily in-tact’ (Zelizer, 1989: 364). These household problems mirrored problems at the level of the state. Zelizer (1994: 131) explores how welfare agencies made visible how the poor used money, describing restricted currencies, such as food orders. Welfare workers developed technologies and educational interventions to make family expenditure visible, creating budget books and account ledgers (Zelizer, 1994: 124).

So, Zelizer analyses how money is made visible in situ, and how third parties observe monetary actions at a distance. These problems have been explored subsequently by studies of firms and auditors (Higdon, 2011), priests and the devout (Parry, 1989), husbands and wives (Zelizer, 1994), money launderers and the police, and individuals and the tax authorities (Carruthers, 2010). This body of research considers how actors make material money visible; we explore the visibility of immaterial digital money.

Sociological work addressed to the ‘new sociability of digital monies’ (Guseva and Rona-Tas, 2017: 204) has largely emphasised the traceability of digital transactions. For example, Dodd (2014: 294) notes how digital platforms allow private and state actors to see, not only ‘the amount changing hands and the flow of funds involved, but also the preferences and routines of transactors themselves’. There is now a market for this information, which once mined, can be sold. Rona-Tas and Guseva (2014) describe how Union Pay, the national payment card issued by the Chinese state, is not a consumer product per se, but a tool to control and improve citizens’ behaviour.

Alongside this work, recent studies have explored how digital payment platforms shape everyday life. McDonald and Guo (2021) consider how factory workers store money on Alipay and Yu’e bao. Two aspects of monetary visibility are considered. Yu’e bao encourages individuals to save and engage with banking regularly, to view the ‘ascending bar charts’ that depict daily interest payments, ‘a clear example of the superior visibility of money on Yu’e bao’ (McDonald and Guo, 2021: 724). Others maintain material anchors. For them, ‘the visibility of money was experienced not through figures displayed on a smartphone, but instead materialised and “made safe” through concrete infrastructures of traditional banks’, such as owning a ‘thick fold open wallet’ containing credit and debit cards (McDonald and Guo, 2021: 726).

Perry and Ferreira (2018) analyse ‘money work’, situated practices of handling and negotiating digital and analogue money. They consider how people come to ‘agree on and verify an exchange of value’ (Perry and Ferreira, 2018: 1) when using digital payment platforms, describing ‘transactional visibility’ and ‘sharing’. They found using the Bristol Pound, at one point the largest local analogue currency in the UK, to be especially accountable, and highly visible. Rather than frictionless, payment took time and effort, becoming a topic of conversation and impression management. Users were encouraged to make payment visible beyond the situation, by sharing on social media platforms such as Twitter, via practices such as ‘first to spend’, where users unlock ‘achievements’.

The present article aims to extend our understanding of ‘money work’ (Perry and Ferreira, 2018), by exploring how digital payment platforms alter lines of sight, making in situ money harder to observe. We recover a distinctive language game (Wittgenstein, 1953) through which buyers and sellers establish whether, when and how digital money has changed hands.

Typically, money use is taken for granted. People do not have to ‘think’ about relevant social rules or how they are ‘imposed, negotiated and readjusted’ in practice (Mondada et al., 2020: 720). Only following various shocks and troubles, do we even notice the fact that money handling is socially organised. For example, Mondada et al. (2020) explore the implications of COVID-19 for the way money is handled. We think digital payment platforms are having just such a disruptive effect, by sometimes preventing synchronic information sharing. While Coleman equates the demise of cash with a retreat of the social, since ‘sellers no longer have to trust buyers, but depend instead upon impersonal, central, electronic clearinghouses’ (Coleman, 1990, in Zelizer, 1994: 206), we argue a new micro-sociability of digital monies is emerging centred on the problem of trust (Guseva and Rona-Tas, 2017: 204).

We explore this by drawing upon study policies from ethnomethodology and conversation analysis to extend the ‘language analogy’ in the sociology of money (Ganβmann, 1988: 297) through the analysis of ‘everyday digital interactions’ (Brownlie and Shaw, 2019: 117). Authors such as Braudel (1981) and Parsons (1967) argue money is akin to a ‘language, which every society speaks after its fashion, and which every individual is obligated to learn’ (Braudel, 1981: 477). The visibility of money is central to the language analogy, where monetary media are analogous with words spoken in conversation: ‘Like language, monetary symbols must be visible and interpretable by the relevant audiences if they are to convey their meaning effectively. Tokens cannot function as money if people do not recognize them as such’ (Carruthers, 2010: 52).

But the emergence of digital payment platforms raises new questions about the visibility of money, and trust between buyers and sellers (Beckert, 2006), because monetary transfer is now indexed by fleeting digital signs. Camera et al. (2013) suggest money engenders trust precisely on the basis of its materiality, so what happens when the material symbol is removed? Mobile payments can be recognised from diverse media, including phone screens and loud-speakers, which can be hard to see, hear and read. The visibility of money may now hinge on ‘where you stand’ (Husserl, 1989: 177), the availability of mobile data and even noise and light in the ambient environment. Buyers and sellers may no longer share the same ‘view of the object’ and additional work may be required for them to recognise they are participating in an ‘ongoing intersubjective experience’ (Rettie, 2009: 435). Below, we recover a new financial language that has emerged to combat this, which over a billion people have thus far been ‘obligated to learn’ (Braudel, 1981: 477); new ways of collectively showing, hearing and seeing that money has changed hands.

Accessing Mobile Payments

We analyse ‘everyday engagements with data’ (Kennedy and Hill, 2018: 830) and ‘the part played by visual phenomena in the production of meaningful action’ (Goodwin, 2000: 158). To capture these processes, video recordings were selected as data. These provide a vivid, permanent record of the situated uses of technology (Heath et al., 2010).

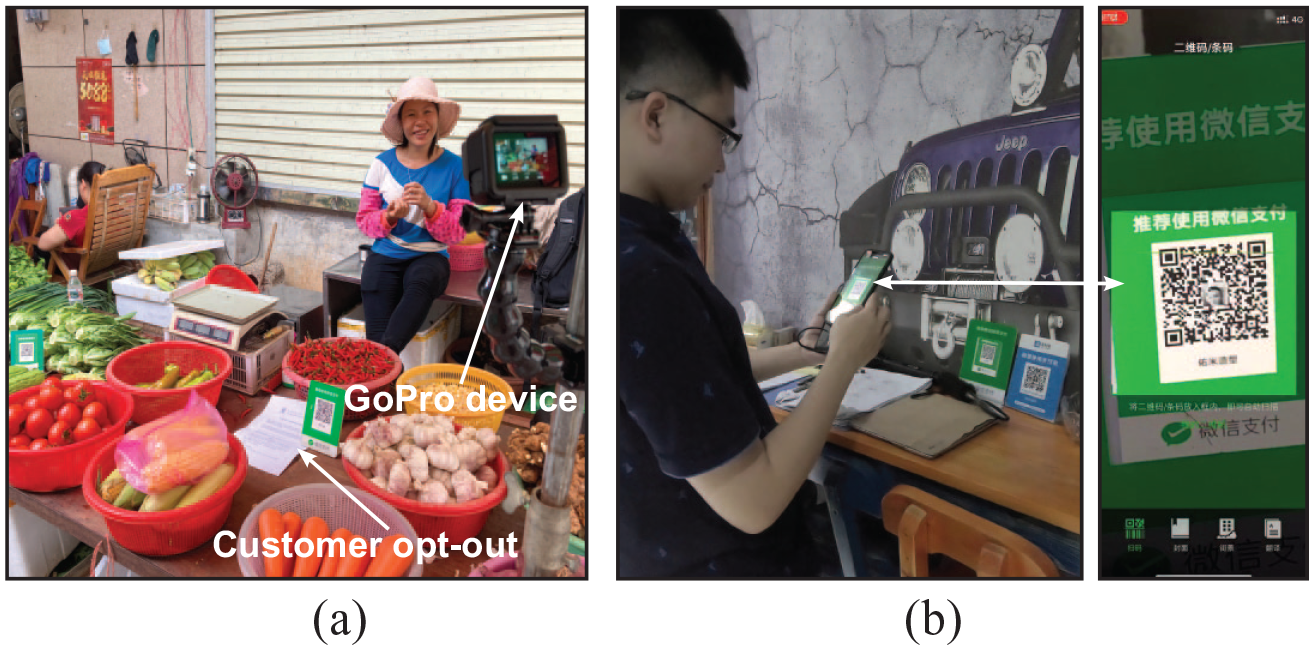

The visibility of mobile payment is a problem for buyers and sellers, and also for researchers. We had to make phone use visible, accessing what buyers and sellers could see, without disrupting the flow of commercial activities. Addressing these challenges, we developed a dataset consisting of 256 video recordings of people paying for goods and services in street markets, supermarkets, restaurants and cafes, across four Chinese cities of varying sizes, Shenzhen (Guangdong province), Xiamen (Fujian Province), Nanning and Guigang (Guangxi province). Of these, 211 involved WeChat Pay and 45 Alipay. The scope of the article is limited to understanding the organisation of relatively small-scale transactions, where WeChat Pay is used most often – rather than interactions where large sums are involved (which may involve alternative payments methods).

There are two main ways of paying using WeChat Pay. In one, the customer generates a QR code on their phone, which the seller scans. The phone acts like a bank card. We focus on a second method where the customer scans the seller’s QR code (see Figure 1, image b). They open the application, press ‘scan’, scan the QR code, input the price, press ‘pay’, authenticate payment with a six-digit code, fingerprint or face scan and then press ‘finish’. The daily limit is 500 Yuan (about £60 or US$80) for payments made in this way. This practice is striking because the customer controls much of the process; they enter the price and progress payment through to confirmation. In some cases, sellers are informed money has ‘changed hands’ via a broadcast message, in others they depend entirely on the customer for information. We recorded 130 transactions where payment was organised in this way; 120 involved WeChat Pay.

Data collection techniques: (a) static use of GoPro and (b) roaming video and phone recording.

Two approaches to data collection were used, following approval from our University’s Survey and Behavioural Research Ethics Committee. In one, static GoPro cameras were located in situ (see Figure 1). A notice was placed in a prominent position, informing customers about the study, and the use of images in publications, and offering them an opt-out (Heath et al., 2010: 30). This would have involved permanently deleting encounters; several customers examined the notice, but none opted out. In a second approach we recruited individuals through personal networks and advertisements, to film their actions as they made purchases. An information sheet was used to obtain informed consent. Participants agreed to record their phone screens, capturing real-time phone usage. It was possible to synchronise phone screen and video recordings for 49 transactions.

To complete transactions, people draw upon multiple resources. We therefore employed ‘multimodality transcription’ (Mondada, 2018), which incorporates grammar, lexicon, prosody, gesture, gaze, body postures, movements and the manipulations of artefacts.

Our analytic interest in the visibility of mobile money was first piqued by transactions where it was unclear whether money had ‘changed hands’. Garfinkel (1967: 36) argues that many routine activities are ‘seen but unnoticed’, and this seemed to be true for payment. We see that payment has happened, but fail to notice the work of producing the activity precisely so it is observable. We argue payment is always accomplished through ‘the practices that participants in a variety of settings use to construct the events and actions that make up their lifeworld’ (Goodwin, 2000: 179). Guided by these ideas, we began by searching for the methods through which actors make monetary transfer ‘visible’ and ‘accountable’ (Garfinkel, 1967) to one another. We considered obvious cases, where payment appears completely visible, and cases where payment work became noticeable to participants, typically owing to various hitches. Over time, the analysis revealed three main practices for making monetary transfer visible – namely ‘showing’, ‘telling’ and ‘doing payment without showing or telling’. We recovered practical ways customers came to recognise which practice was in operation, whether they should ‘show’ rather than ‘tell’, or whether neither was required.

Findings

Showing Rather than Telling

We start by considering simple cases where the transfer of digital money is rendered entirely visible through showing. Customers do not leave, with goods in hand, when they see they have paid. Rather, they enable the seller to see that money has ‘changed hands’.

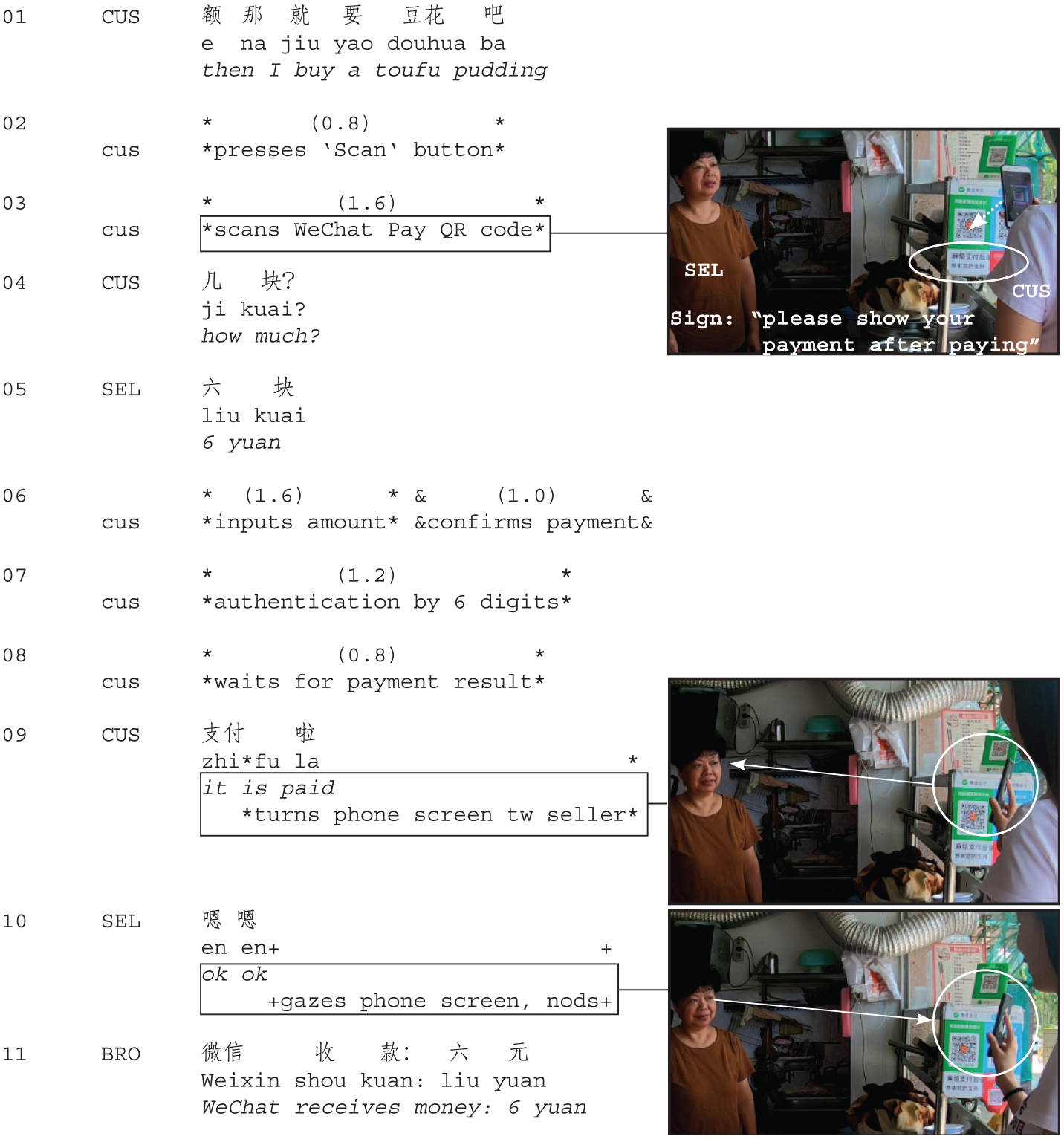

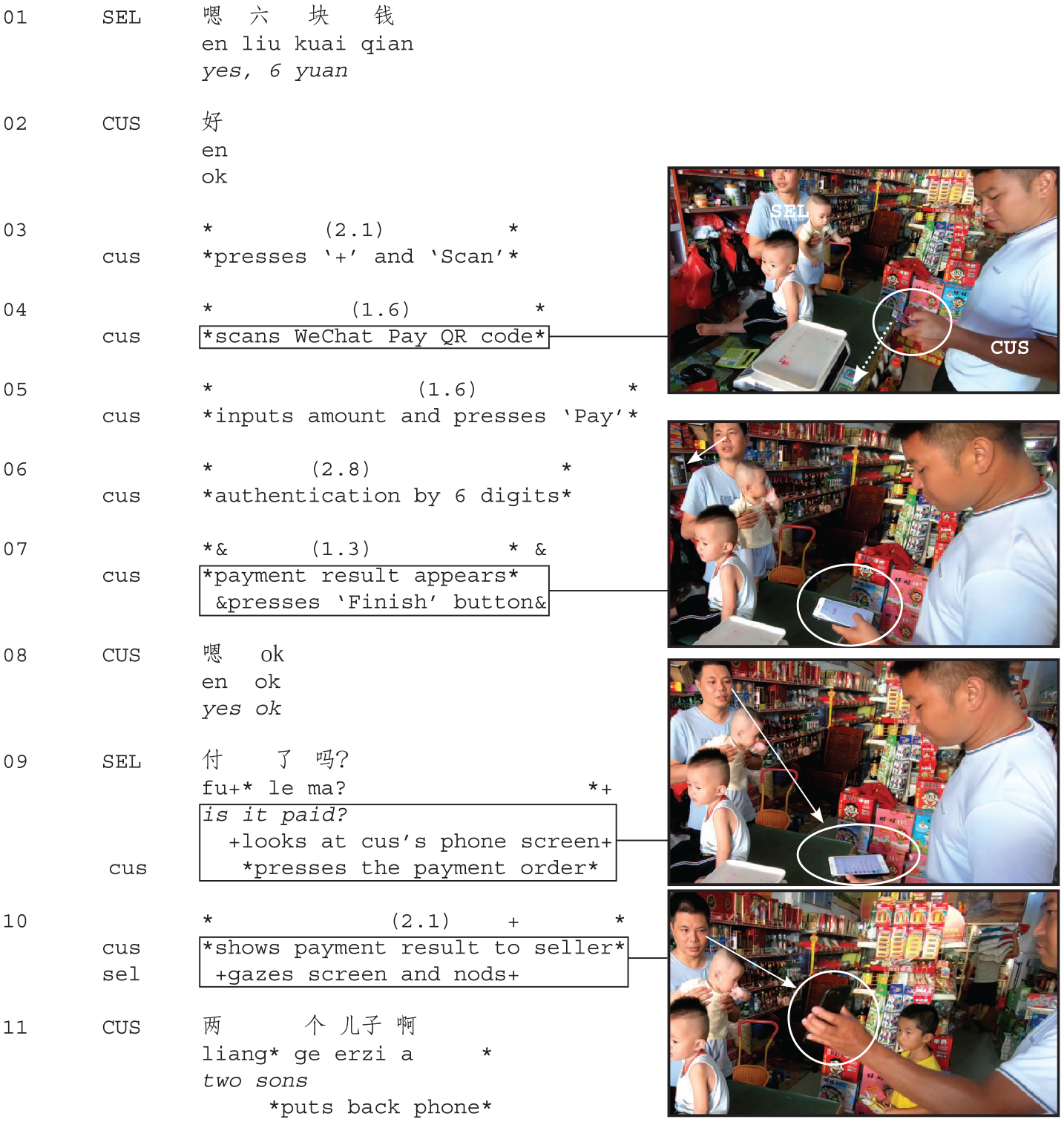

In extract 1, a customer is buying tofu pudding from a small food outlet. ‘Monetary expectations’ (Dodd, 2017: 234) are communicated via a sign located by the QR code; the customer should ‘show payment after paying’.

As the customer (CUS) approaches the counter, she has her phone out and is talking with the seller while simultaneously opening WeChat. When she comes to order, she is ready to scan the QR code (lines 2&3). But she has ordered without knowing the price. She is prompted to check the price by the application itself (line 4); having scanned the QR code, the next step is to input price. WeChat is guiding her actions.

Rather than busying herself with other activities, the seller (SEL) remains still, her gaze cast towards the customer’s phone. She seems to be doing little, but is overseeing payment. After the customer enters her authentication code, she raises the phone up, perhaps ready to show once payment is confirmed. The seller attends to this, raising her gaze; she is awaiting showing. When payment is confirmed via WeChat, the buyer does not simply reach over and take the goods, but enables the seller to enter the same monetary lifeworld. Following the rule, she turns her phone-screen and shows (line 9).

They both then orient to a further requirement, not described by the written rule. The seller publicly exhibits her subjective understanding, through a brief nod (line 10). Moreover, the customer, who is looking directly towards the seller, removes her phone from the seller’s gaze only once she has seen her nod. While fleeting, they fashion an ‘ongoing intersubjective experience’ (Rettie, 2009: 435). The rule for monetary usage is ‘negotiated and readjusted’ in practice (Mondada et al., 2020: 720). The fully explicated rule might read, ‘show your phone after paying and continue to show it until the seller has confirmed payment’.

Extract 1 (MP004)

Just as the phone is withdrawn, a broadcast message plays, further confirming the transfer of funds (line 11). These broadcast messages also give buyers and sellers shared access to the same information. While it would be possible for buyers and sellers to concertedly hear broadcast messages, this does not happen in our materials. Moments of shared or intersubjective understanding were fashioned around the phone only.

Extract 2 (MP135)

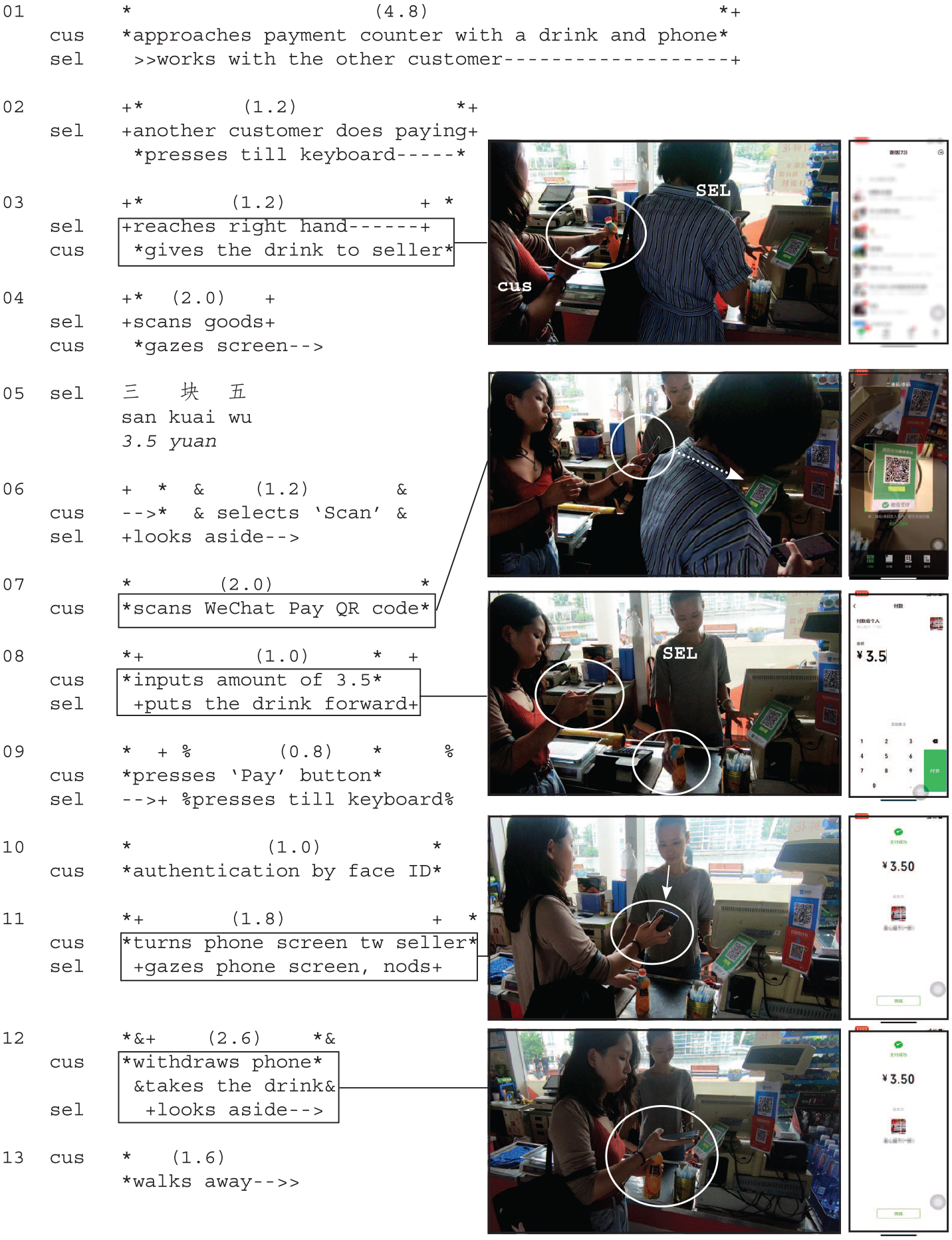

Extract 2 is a second simple showing example. It takes place in a small convenience store, where a customer is purchasing a drink. There is no sign describing the rule in this case. As she approaches the counter the seller is in the midst of a prior transaction. The seller reaches over, and the customer passes her the drink, which is scanned to determine price (‘3.5 yuan’, line 5). The employee is multi-tasking, completing one transaction, while beginning the next. Prior studies have noted that naming price can be an indirect way of soliciting payment (Mondada et al., 2020). But something different is happening here. Through the seller’s actions, the customer can now start to progress the payment. Moreover, she now has both hands free and can access her phone. The seller places the bottle down, rather than returning it, while the customer opens WeChat and scans the sellers QR code.

One problem for transactors is the order in which money and goods change hands. Do sellers demand confirmation of payment before releasing goods; should customers demonstrate payment before taking goods? In this case, the seller slides the bottle towards the customer. But it is left unclaimed. The customer presses pay and authenticates payment via a face scan.

When the seller has finished her work at the till, rather than beginning some other task, she maintains her gaze steadily and only slightly beyond the customer. Hers is a studied form of inattention, she remains in the same moment as the customer, she is overseeing payment.

When payment is confirmed on the phone, the customer does not simply take the bottle and leave the shop. In the absence of a written rule, with her free hand, she reaches towards the bottle, but only so she is touching, rather than holding it. She shows her phone to the seller, so she can see the payment confirmation screen. Together they build a shared social world. As the phone is presented, the seller looks towards it and nods, offering a brief perfunctory smile (line 12). Once more, the phone is withdrawn by the customer only after the seller’s response. This happens very quickly. The phone is shown for less than a second. It is only at this point that the bottle is claimed. Buyer and seller do not speak, or catch the other’s eye, but nevertheless fashion mutual understanding.

We have started with two simple cases where social relations at the point of consumption have been re-ordered by new monetary technologies. Now, the customer enters the price and processes the payment. This produces an intriguing information asymmetry; the customer may alone know that money has ‘changed hands’. We have analysed a simple practice through which actors overcome this asymmetry, how sellers make monetary rules relevant, by overseeing payment, and how customers await confirmation of the seller’s perspective before departing with the goods. The language game appears very simple at this stage, and could be codified by a single rule; that is, ‘show, and await confirmation’. We have seen buyers and sellers orienting to social considerations beyond written rules, and how rules are made practically relevant through the overseeing actions of sellers.

Pursuing Showing

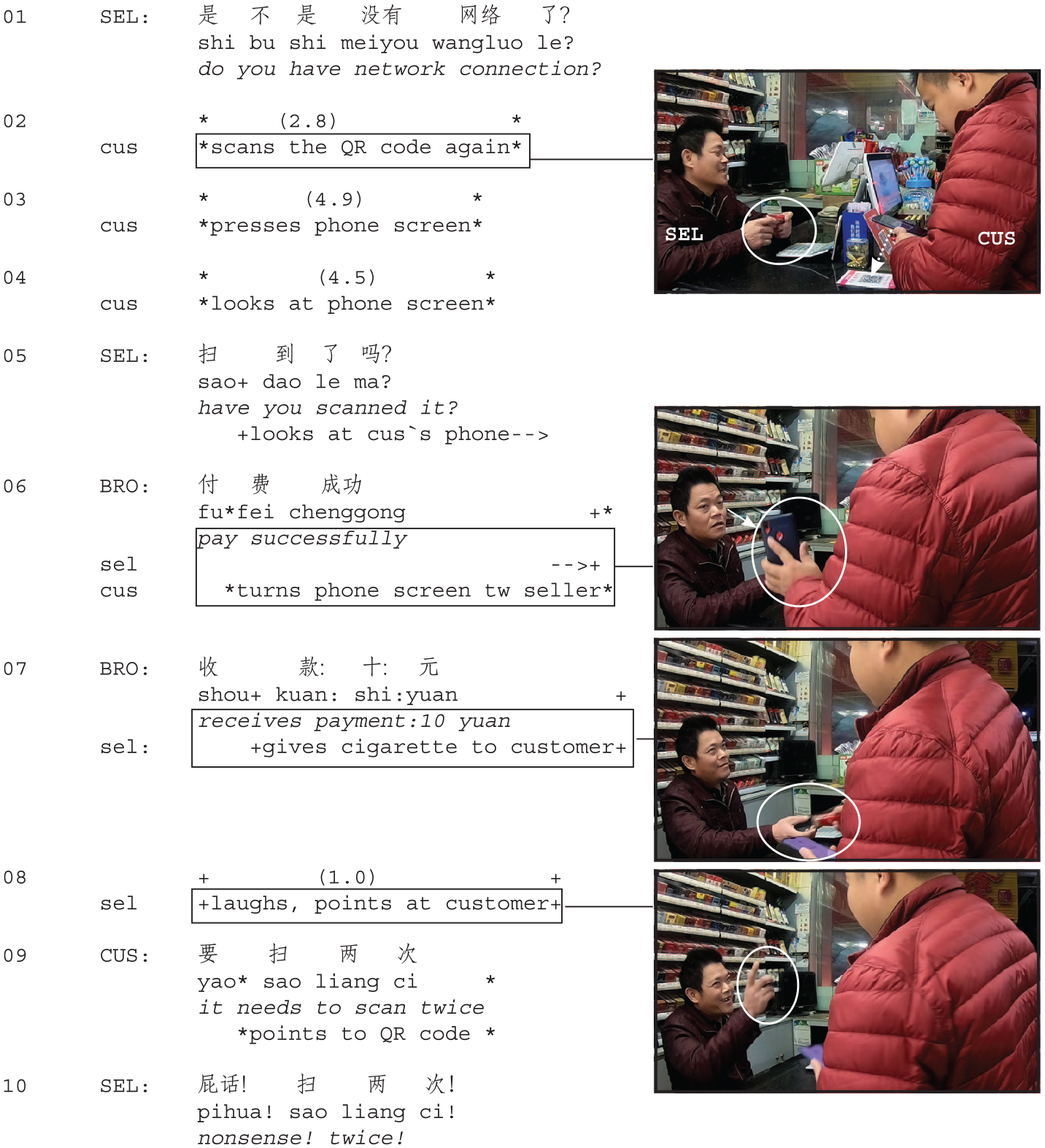

We now consider cases where sellers perform additional work to elicit showing. In extract 3, we are in a convenience store. The customer is buying cigarettes, positioned behind the seller. The customer has ordered, but is struggling to scan the QR code. He questions whether the ‘payment works’ and is told ‘it works’. Somewhat defensively perhaps, the seller suggests the fault lays with the customer, perhaps he scanned the code incorrectly, or has no network connection (line 1). Technological features, such as QR codes, give rise to new patterns of accountability and blame.

As the customer tries again, the seller is holding the goods in his right hand; the cigarettes are not passed to the customer, ready for him to take. Moreover, the seller is no longer overseeing payment, his gaze is drawn towards the back of the store.

As the seller’s gaze moves back to the customer, he inquires whether he has ‘scanned it’ (line 5). He pursues information. At this moment, payment is confirmed on the customer’s screen and he immediately shows, rather than tells, the seller that payment has gone through. The broadcast message plays (line 6), but neither party orients to this. The seller looks to the phone, as the customer looks to the seller. Rather than nodding to display understanding, the goods are exchanged, which serves the same function. The customer’s right hand, now free from operating the phone, reaches towards the cigarettes, which the seller passes.

Extract 3 (MP008)

Payment has a distinctive set of meanings in this instance (Zelizer, 1994). It is taken as validation of the seller’s argument, that he was not responsible for the troubles. For him, the screen carries two meanings, that money has ‘changed hands’, and that blame has been allocated. The customer maintains his account that the seller’s QR code is faulty (line 9). As the goods change hands, the seller fixes the customer’s gaze, produces an ironic laughter particle ‘huh’ and a knowing smile before pointing to the customer and wagging his finger.

Above, the seller poses a question that elicits a showing. But he is not suggesting the customer has been remiss. In the next case (extract 4), in contrast, the rule is not followed and both parties orient to a requirement for reparatory action. We are in a convenience store this time, with a customer buying ice creams.

The seller starts by establishing the price (‘6 yuan’, line 1) and the customer scans the seller’s QR code (line 4). The goods are already held by the customer and do not need to be scanned. We see vividly how the transfer of payment work to the customer may leave sellers free to engage in non-work activity, childcare in this case.

As the customer works through the transaction (pressing ‘+’ and ‘scan’, scanning the QR code, entering the amount, pressing ‘pay’ and finally entering the authentication code) the seller is not overseeing payment (line 7). As payment is visually confirmed on the customer’s phone, the seller is looking away, interacting with a colleague. For the first time in the data presentation, buyer and seller are out of synch. Presenting the phone to the seller might be interruptive. Rather than doing this, the customer verbally confirms payment through a telling (‘yes, okay’, line 8), which immediately draws the seller’s attention back to him.

But, at this point, the seller has no visual evidence money has ‘changed hands’, he has been told rather than shown payment has happened. New problems of trust come into play. Should he take the customer’s word? The moment of payment has passed and the customer has exited WeChat.

The seller shifts his gaze back and solicits evidence of payment, asking ‘is it paid’ (line 9), while looking directly to the customer’s phone. He wants more than verbal confirmation. Independently, and before the question (‘is it paid’, line 9), the customer starts to access his recent ‘payment orders’, akin to receipts. He orients to a minor error, namely exiting WeChat too soon, and improvises. The interaction reveals new practices, bound up with gaze in this case, for making payment rules accountable. Step by step the language game is becoming more complex and subject to contingencies, such as what the seller is doing as payment is confirmed, and subtleties, such as how questions can be designed to solicit showing, and how mutual understanding can be displayed, by nodding or passing objects.

With the actors back in synch, the checking sequence unfolds in the now familiar way. With the payment order screen open, the phone is presented to the seller (line 10). The customer looks at the seller, who looks at the phone. The seller’s confirmatory nod is produced for the customer but directed at the phone. Again, the phone is removed only once the seller publicly exhibits their understanding through a confirmatory nod to the phone.

Extract 4 (MP099)

We have continued to map the language game through which mobile payments are achieved, considering practices through which sellers actively pursue showing. The relationship between showing and telling has also been considered, through a case where telling was insufficient.

Telling Rather than Showing

We now add further layers of complexity. In some cases, buyers do not need to show, and can merely tell the seller that payment has gone through. Payment thus does not involve following a simple rule. Rather, actors have to deploy local reasoning to determine which rule, from a number of alternatives, is relevant.

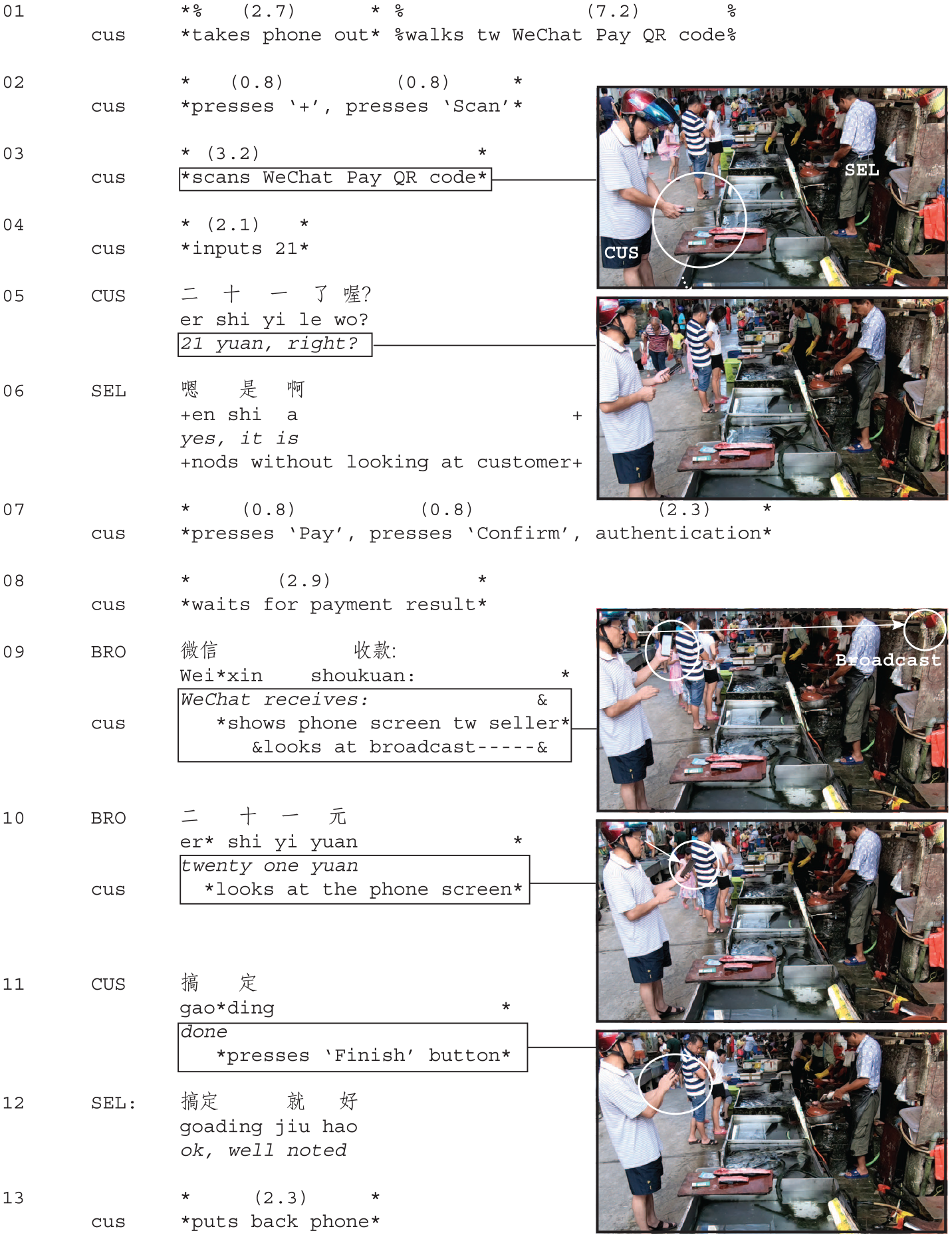

In extract 5 we are in a street market, with a customer purchasing fish from a stall. He has ordered and the fish have been weighed and the price is identified as 21 yuan.

Extract 5 (MP103)

The transcript begins with the customer being directed to the WeChat QR code. As he opens the application, the seller prepares the fish. For the first time in the data presentation, the transfer of funds occurs while the seller is engaged in other work, some way from the small phone screen.

As the customer scans the QR code, the seller looks up from his work, and towards him. Having scanned the code, the customer catches the seller’s eye, and confirms the price (‘21 yuan right?’, line 5). The seller returns his gaze to the fish, confirms the price (‘yes, it is’, line 6) and nods. The customer may have forgotten, given the initial confusion, but his inquiry makes his payment activity publicly accountable.

As payment is announced, via a broadcast message, the customer looks towards the seller, and raises his phone upwards, and towards him. He attempts to show payment, but is ‘left hanging’. The seller does not look to the phone and the customer abandons the showing.

Evidentially, for the customer, the problem is not resolved by the broadcast message. He does more work to evidence payment. As he presses the finish button, the customer says ‘done’ (line 11), publicly indexing the transfer of funds through talk that invites the seller to confirm payment, which he does (‘okay, well noted’, line 12). A shared understanding is publicly exhibited, via a telling.

In this case, the customer came to see that it was sufficient to ‘tell’ rather than ‘show’ payment has happened. This seemed to rub somewhat. He wanted to show the phone, and in the absence of being able to do so, struck up a verbal contract with the seller, that supplemented the impersonal broadcast message. The example also suggests that the customer might have neither shown nor told, but relied more fully on trust. After all, he was the only customer being served and had rather obviously been engaging in payment activities.

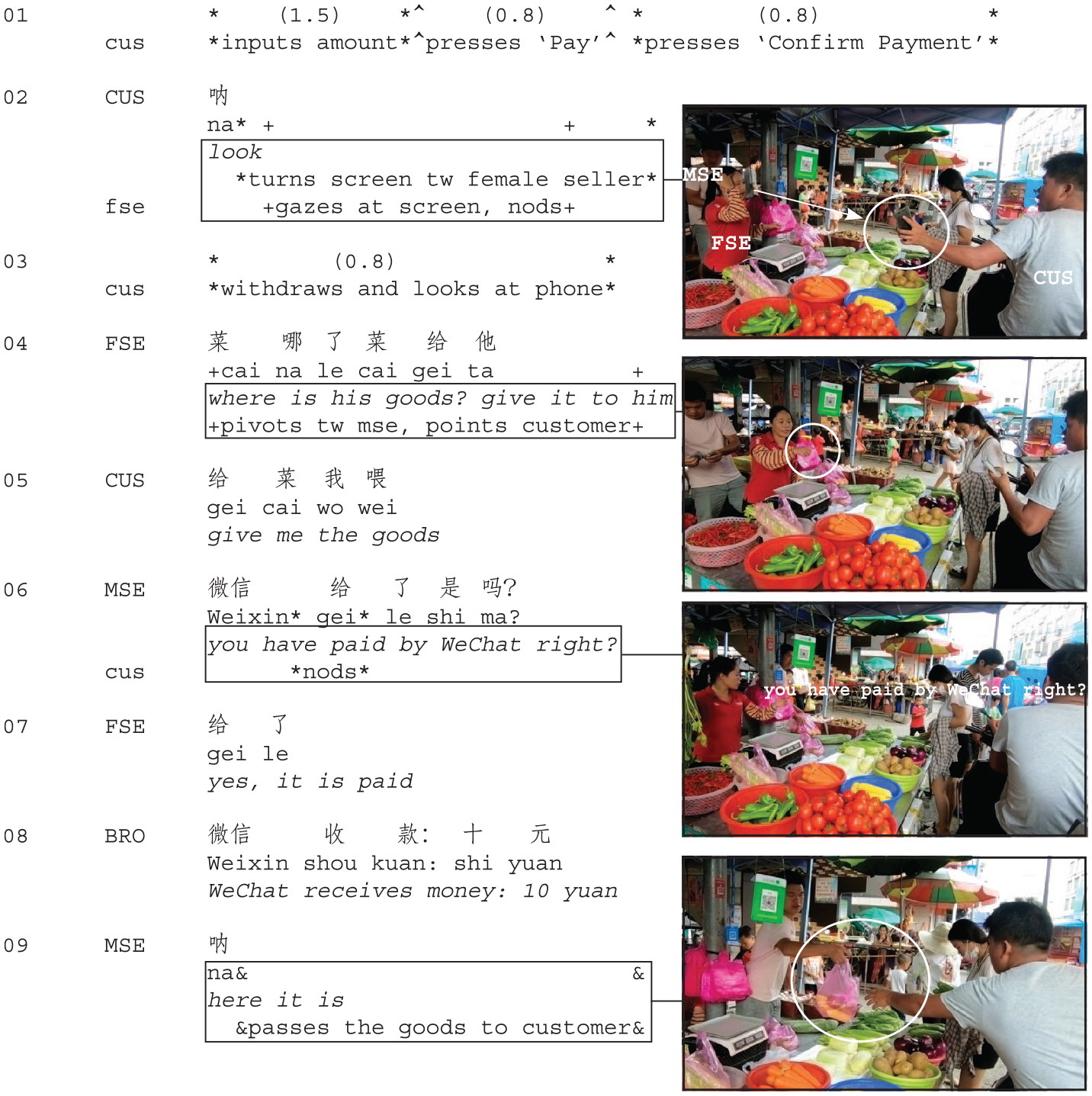

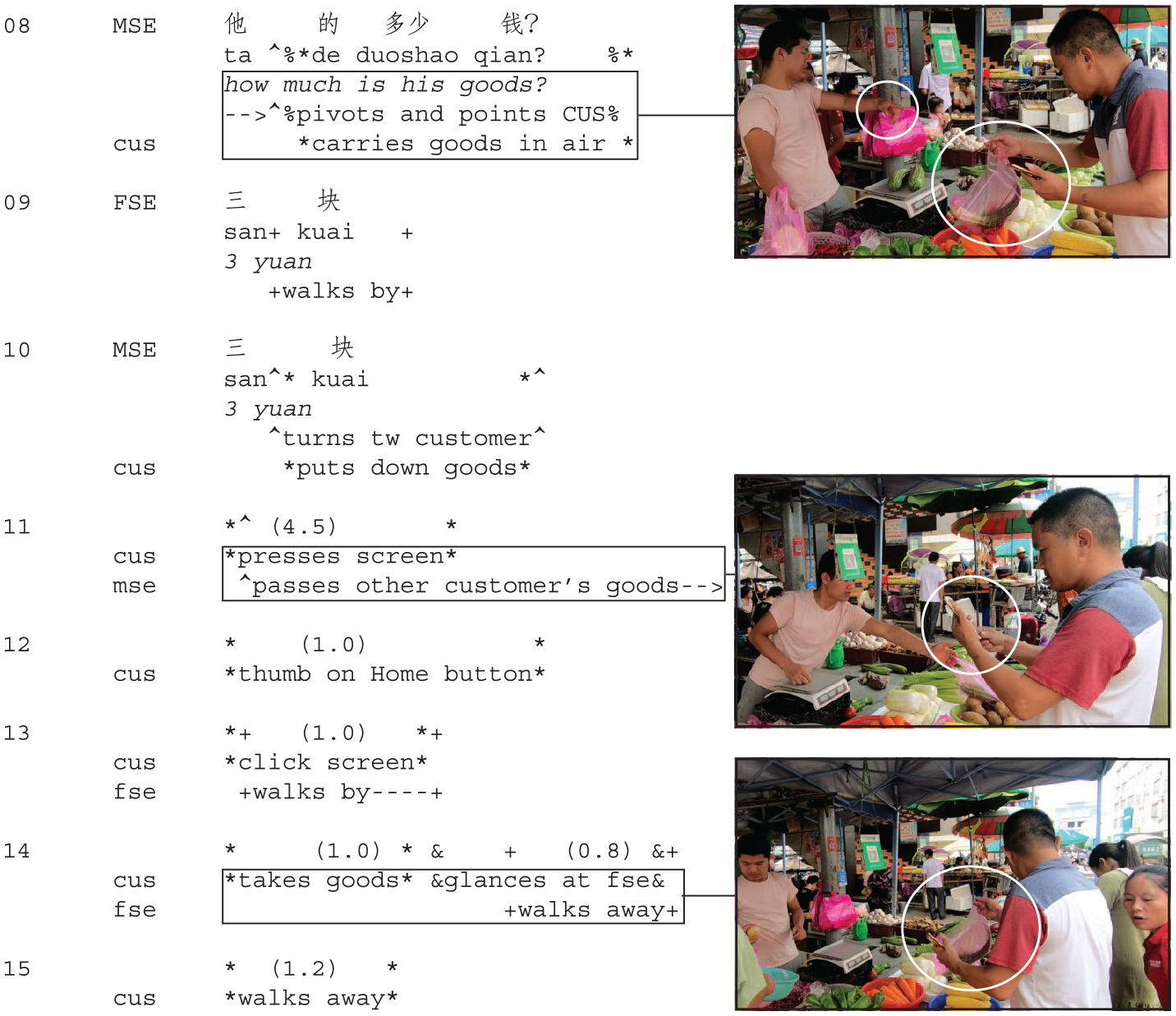

The relationship between showing and telling becomes additionally nuanced in extract 6, where an individual customer at a busy market where two servers – one male, the other female – are simultaneously participating in four separate transactions. The broadcast speaker is re-booting. Our focus is on the customer (CUS), seated on the motorcycle to the right of the still images.

With one hand, the other steadying his bike, the customer places potatoes in a bag, which he lifts and moves towards the male seller, before placing them down. He then picks out three sweetcorn cobs, somewhat precariously. Seeing his difficulties, the male seller (MSE) leans over to receive the goods, placing them in a bag, and confirms the overall price of 10 yuan.

The male seller then breaks from this transaction. He moves to the back of the stall to deal with another customer, who is paying in cash. The customer has both hands free and starts the business of paying via WeChat. As payment is confirmed, the female seller (FSE) at the front of the stall is bagging up celery for a female customer who then orders carrots; she is not overseeing his payment. The customer finds an interactionally sensitive way of showing the phone, just as the female seller turns and looks away to the carrots, in the customer’s broad direction. The female seller pauses, scans the screen and nods, before continuing with her task. So, in this case, the male seller took the order, but the female seller was shown the payment. The actors confront the problem of who should be shown; the customer orients to the sellers as a ‘team’ (Sacks, 1992).

Extract 6 (MP060)

The female seller, dealing with another customer, actively pursues the transit of goods to the customer who has just shown payment, instructing the male seller to pass them (‘where is his goods, give it to him’, line 4), but of course he has not personally seen the payment. A further problem arises, for the male seller. Does the instruction ‘give it to him’ mean she knows that money has ‘changed hands’?

We can see that he does not interpret it this way, but questions the customer (‘you have paid by WeChat right’, line 6). Thus far, we have seen a clear preference for showing over telling in light of such questions. But the rule is nuanced in this case, because the customer has already shown. This is the only example in our corpus where the customer does not show in response to such a question. He tells the server he has paid, by nodding.

So, those playing this language game have to see, not only which rule is in play, but also circumstances where rules can be waived or finessed. The female server supplements the customer’s response, telling her colleague ‘yes, it is paid’ (line 36).

Doing Payment without Showing or Telling

Finally, we consider a third practice, already alluded to above. Rather than showing or telling the seller they have paid, the customer publicly and accountably engages in payment activities, often drawing the seller into their payment work, and expects to be trusted. We have already seen that customers not only pay, but publicly engage in activities that are ‘category bound’ (Sacks, 1992: vol. 1, Lecture 8) to paying. They ask the seller questions about the whereabouts of QR codes, double check prices and variously produce commentaries on their activities. They make the work of paying visible, and in some cases, this is all that happens; neither party initiates a checking sequence. Payment work establishes a distinctive basis for trusting the customer; the seller has to trust the customer is not performing an elaborate fraud and pretending to pay with their phone.

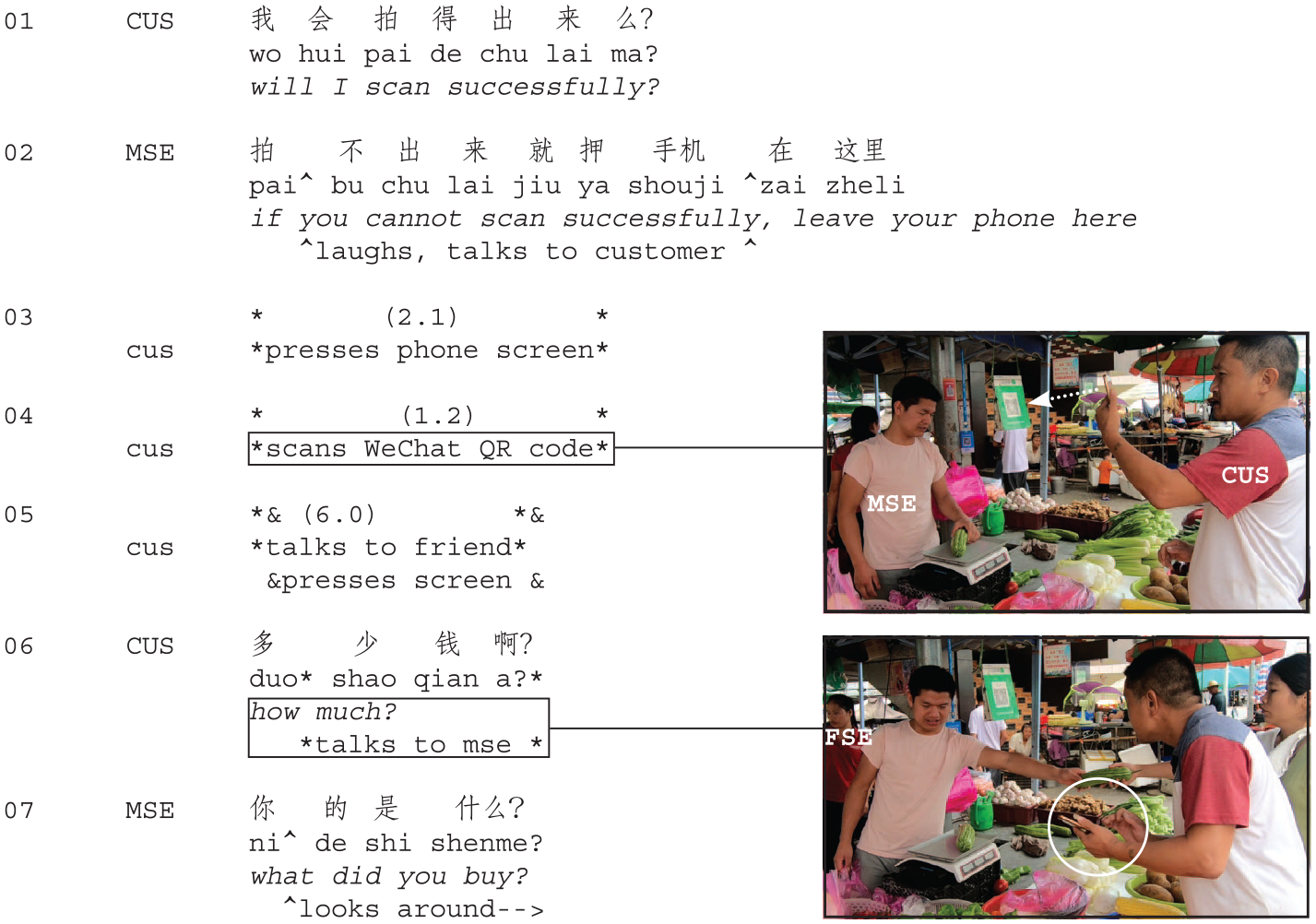

Extract 7a (MP039)

In this final example (extract 7) we return to the fruit and vegetable stall and a case where a customer begins to pay in an avuncular fashion. He draws attention to the act of scanning (‘will I scan successfully?’, line 1), which the seller turns into a joke (‘if you cannot . . . leave your phone here’, line 2). After establishing the price (lines 6–10), the customer places the goods down and works on his phone (lines 11–13).

Extract 7b (MP039)

In the absence of screen recordings, we have to infer the customer is entering the price followed by his six-digit authentication code. Engaging seeing practices ourselves (Goodwin, 2000), we can see he moves his thumb as he would to authenticate payment, readjusting how the phone is held. As he appears to pay, the male seller is dealing with four customers, each at different stages of the transaction. He is not overseeing payment. The customer does not try to get his attention. He simply recovers his goods, and slowly moves away from the stall. Neither party initiates a confirmation sequence and the broadcast message does not sound. Either the speaker is rebooting, turned off or he has not paid.

Sellers sometimes demand evidence that money has ‘changed hands’, and even hold the customer’s phone until this is shown. Above, we have no idea whether the customer has paid, but neither party orients to any troubles. The movement of money is left to trust. Perhaps, to call after the customer would be to accuse him of an elaborate fraud, given he was so publicly doing paying.

Sellers may be both in a moral and practical bind at such points. Practically, it is difficult for them to check payments independently of the customer. For small-scale settings, payment may become less, rather than more, visible overtime. To check, the seller would have to stop serving, find a device, open their WeChat account, and scroll through to find a ‘missing entry’ of 3 yuan. This may be very difficult. The list may show many hundreds of transactions each hour, completed by different sellers, for similar sums. Each transaction is identified only by an account number, and an amount; the user may add a photograph only at their discretion.

Discussion

We have considered the enmeshing of online platforms and everyday situated interaction (Fussey and Roth, 2020). The fact mobile money requires interpretation and reasoning to function can seem strange (Perry and Ferreira, 2018); money appears to ‘work’ independently of social actors. We recovered three different practices through which users of mobile money accomplish small-scale everyday transactions, ‘showing’, ‘telling’ and ‘doing payment without showing or telling’. These form part of the monetary language that users of mobile payment applications are ‘obligated to learn’ to participate in a common economic culture (Braudel, 1981: 477). When Parsons (1967) equated money with language, he was not seeking to elaborate how money is actually used. The analogy was more limited. In contrast, we have analysed how actors build social actions using visual depictions of financial data, revealing a complex language game that binds buyers and sellers.

We found appropriate money handling is not a matter of following a priori ‘rules’ (Zelizer, 1989: 368), but ‘knowing how to go on’ (Wittgenstein, 1953: §151). Even in a culture where mobile payment is massively prevalent, buyers and sellers do not simply follow a script. Rather, the use of money is reliant upon in situ adaptations and improvisations (Clark and Pinch, 1992; Mondada et al., 2020). From their embodied conduct, the customer recognises the seller is overseeing payment (extracts 1 and 2); following an initial attempt at a showing, the customer switches to a telling (extract 5); when asked whether they have paid, following an initial showing, the customer switches to a telling (extract 6). Monetary rules are not fixed features of payment cultures. The customer has to recognise that when a seller asks, ‘is it paid?’ (extract 4) but looks to their phone, they are obligated to show, rather than tell, that payment has been confirmed. Monetary competence is apparent in the ways that people navigate, and guide others to understand, competing rules and expectations.

The practices we have considered attend to an information asymmetry brought about by digital payment technologies, which take the form of interpersonal networks based on trust (Wood et al., 2019: 932). In relation to money, Simmel’s (1900/2004: 177) well-known treatment of trust speaks to a different set of troubles, the willingness of parties to honour the convention that worthless tokens will be taken as money. With mobile money, sellers still have to trust ‘real money’, which they can claim upon, is somewhere behind the confirmation screen. But such concerns are nowhere apparent in our data. For all practical purposes, people trust the platform entirely. The case of mobile money is intriguing because new interpersonal dynamics arise. Customers and sellers have to resolve whether customers have paid. We have shown how trust in market relations is negotiated live, ‘in the situation itself’ (Beckert, 2006: 320).

We analysed a specific circumstance, that arose in around half of the encounters we recorded (130 from 256), where the customer, the ‘trust taker’ (Beckert, 2006: 319), alone sees payment has been confirmed. In these, customers often tried to eliminate the need for trust, in 55 cases, by showing evidence money had changed hands. Having done the right thing, perhaps they wanted their honourable conduct recognised, or to release the seller, the ‘trust giver’ (Beckert, 2006: 319), from the burden of having to trust them. Sellers likewise structured conditions in ways that eliminated the need for trust, playing an overseeing role that made showing relevant. But in 75 transactions, trust remained fundamental. Sellers accepted tellings or doing payment as sufficient evidence money had changed hands, in 16 cases without a broadcast message. We have produced an analysis of trust as a ‘performative act’ (Beckert, 2006: 319).

Zooming out from the video data, and speculating somewhat, trust may become prevalent in more informal economic settings, where customers scan the QR codes of sellers who lack the expensive infrastructure used, for example, in supermarket chains, where phones work more like credit cards, and printed receipts evidence the transfer of funds. In small-scale settings, sellers may be performing payment and service work, with multiple customers. Here, the transaction costs associated with low trust rise. Checking the customer’s phone takes time. Sellers may also have an interest in maintaining a lack of monetary visibility. Expensive payment systems make money visible in situ and to the tax authorities (Carruthers, 2010). Many sole traders accept payments into their personal WeChat Pay accounts, and may risk that some customers dodge payments, for lower levels of cost and scrutiny. These are questions for future research. We have produced an interactional analysis of visibility in situ. But there are clearly important questions about visibility at the macro-level. Perhaps WeChat allows a midway position between traceable cards and untraceable cash. A digital trace is produced, but one that is hard to connect to economic practice, for overseers and traders alike.

By exploring how buyers and sellers negotiate payment rules in situ, the current study contributes to literature that has analysed how the social imprints itself on apparently fungible units of money. Prior research has not explored the kinds of mundane transactions analysed above. Instead, settings have been considered where there is a ‘more durable social relation’ (Zelizer, 1996: 482) and where meanings are imprinted on money as a result of broader political and cultural processes. The meanings we have analysed are of a different order, but hopefully inform this literature. We have revealed meanings that are comparatively fleeting, through which anonymous buyers and sellers determine what they owe the other. We have not analysed general meanings, but how actors exhibit meaning to one another, crafting shared lifeworlds (Rettie, 2009).

In a similar way, Mondada et al. (2020) consider, not general meanings pertaining to COVID-19, but how actors orient to new restrictions upon the transit of coins and cards. We have analysed how actors communicate meanings to each other, because it is on this basis that they assemble the actions that comprise economic exchange. When the seller stands, visually attending to the customer, the buyer sees the meaning of this, and that drives the action. When the seller asks, ‘has it paid?’, while looking at the customer’s phone, the customer can see the meaning of this, and act on that basis. The social was clearly imprinted on the 10 yuan in extract 3; the seller took that 10 yuan as evidence against the customer and in his defence. Through such reflexive processes, buyers and sellers are bound together. This was apparent even where customers produced simple showings. They showed but waited for the seller to display their understanding of the situation before removing the phone. We see a strong and continuing preference for mutuality (Rettie, 2009: 435), rather than automation and depersonalisation, in the organisation of economic activity.

Conclusion

With around one billion daily users, WeChat Pay is part of a global change in the way households use money. Rather than a neutral monetary technology, the platform assembles the social in intriguing ways, showing further how ‘digital forms of interaction are embedded in everyday life’ (Fussey and Roth, 2020: 660). Our central analytic focus has been just one aspect of WeChat’s performativity, how it configures monetary information held by buyers and sellers, and how this has led to the creation of a subtle language game. Outlining how monetary rules and expectations relevant for mobile payment are negotiated, our study further elaborates how ‘money is shaped from the inside by the social practices of its users’ (Dodd, 2017: 240). We have recovered ‘micro-foundations’ that secure what is now a global financial network, through which actors determine whether and how they should be trusted to engage in exchange (Wood et al., 2019).

We have shown that when mobile money is transferred in interaction, its meaning arises from within a language game that consists of rules, practices for occasioning rules, knowledge of circumstances where rules might be wavered and re-ordered and so forth. In the data we have considered, money may have many other meanings. It may be gendered in ways that reflect the social organisation of households. But whatever else it means, when it is used in interaction, meanings will also be imprinted on money that are altogether more local, through which buyers and sellers determine what they are owed and what they are prepared to take on trust.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: this research was supported through a Direct Grant for Research (4052241) from the Faculty of Social Sciences, The Chinese University of Hong Kong.

Ethics Statement

We received approval from the Survey and Behavioral Research Ethics Committee (SBRE-19-503) from The Chinese University of Hong Kong.