Abstract

High-quality development represents a fundamental shift in China’s economy from scale and speed to quality and efficiency. In this transition, environmental, social, and governance (ESG) practices are not only closely integrated with China's development strategy but have also become a core standard for measuring development quality. Nevertheless, research on how ESG practices specifically promote high-quality development in Chinese enterprises remains limited. Based on the environmental Kuznets curve (EKC) theory framework, this study uses data from the Huazheng ESG Index from 2009 to 2022 and employs fixed effect models, mediation effect models, and heterogeneity analysis to examine the specific impact of China's ESG practices on corporate high-quality development from multiple dimensions. The results show that there is a “U-shaped” relationship between the ESG practices of Chinese listed companies and green total factor productivity (GTFP). Initially, improving ESG practices may temporarily suppress GTFP, but as ESG levels further improve, they exhibit a significant positive impact on GTFP. Corporations significantly boost productivity by alleviating financing constraints and promoting green technological innovation, although the direct impact on technological advancement remains relatively limited. In China's western regions and industries such as manufacturing, electricity, heat, gas, and water production and supply, wholesale and retail, and information transmission, software, and information technology services, the positive effects of ESG on GTFP are particularly evident. Based on these findings, it is recommended that governments and financial institutions collaborate to promote green credit policies and increase support for the research and development of green technologies. Additionally, environmental education and resource use optimization should be strengthened, especially in industries such as agriculture, forestry, animal husbandry, and fisheries, and the exchange of ESG technologies and experiences between industries should be encouraged.

Keywords

Highlights

Utilizing the framework of EKC theory, there is a U-shaped relationship between ESG practices and firms’ GTFP.

Alleviating financing constraints and fostering green technological innovation mediate the relationship between ESG and GTFP.

ESG's positive impact on GTFP is significantly enhanced in China’s western enterprises, notably within manufacturing, utilities, wholesale, retail, accommodation, and catering sectors.

Inter-industry ESG practices have spillover effects.

Introduction

With the advancement of economic globalization and sustainable development goals, China urgently needs to transition from a traditional scale-and-speed economic model to one focused on quality and efficiency. This strategic shift aims to address inefficiencies and resource wastage inherent in the traditional development model while optimizing the economic structure. High-quality development emphasizes the quality and efficiency of economic growth rather than its speed, aiming to achieve this through innovation-driven growth, coordinated development, green practices, open cooperation, and shared benefits for all. 1 This model seeks to foster technological and managerial innovation, driving balanced development across the economy, society, and the environment, ensuring that development benefits are equitably shared among all members of society and effectively meeting the global demand for sustainable development.

Environmental, social, and governance (ESG) standards are widely recognized globally as key indicators of corporate sustainability and are closely aligned with China’s high-quality development goals. These standards require companies to enhance environmental protection, social responsibility, and governance structures while pursuing economic benefits. ESG practices have shown positive impacts on decent work and economic growth (SDG 8), responsible consumption and production (SDG 12), and climate action (SDG 13), all contributing to China’s high-quality development strategy. By promoting technological innovation and management reforms, ESG practices strengthen interactions between enterprises and employees, communities, and stakeholders, drive energy conservation and emission reduction, and emphasize sustainable resource management. 2 Additionally, they highlight the importance of global responsibility and international cooperation. These activities aim to enhance corporate economic efficiency and promote social and environmental harmony, ensuring that development benefits are widely and fairly shared among all members of society, thus providing robust support for China’s high-quality development strategy. 3

Currently, according to data from the International Index Industry Association (IIA), the number and investment scale of ESG indices are rapidly increasing globally, demonstrating the global expansion and deepening of ESG practices (see Figure 1).

Expected average future share of asset portfolios that will contain ESG elements.

However, in China, despite significant attention and progress in specific areas, ESG development is still in its early stages compared to the more mature ESG systems. As shown in Figure 2, although the number of A-share listed companies issuing independent ESG reports continues to increase and these companies are paying more attention to ESG regulatory policies and their own ESG management, the proportion of all listed companies actively disclosing ESG information remains low. Additionally, the guideline on “Comprehensively Promoting the Construction of a Beautiful China” issued by the Central Committee of the Communist Party of China and the State Council in December 2023 mentioned the need to explore the development of corporate ESG evaluations, indicating strong government support for ESG development. Therefore, given that ESG is still in its preliminary development stage in China and the need to consider localized high-quality development requirements, it has become an urgent and critical research topic to study how ESG can help enterprises achieve high-quality development in China.

Disclosure of new-year independent ESG/social responsibility reports of all A-share listed companies in 2023.

Theoretical framework.

Given that the environmental Kuznets curve (EKC) theory is widely applied in studying the complex relationship between economic development and environmental pollution, this paper adopts this theoretical framework to explore the interaction between corporate ESG practices and high-quality development. The core hypothesis of the EKC theory posits that the relationship between economic growth and environmental impact is nonlinear, typically taking the form of an inverted U-shaped curve. This study aims to examine whether a similar nonlinear dynamic exists in corporate ESG practices. Additionally, considering the holistic nature of green total factor productivity (GTFP) and its critical role in measuring sustainable development, this study selects GTFP as a representative indicator of high-quality development. 4

Although the importance of ESG practices has been widely researched, there is limited literature on the specific impact of ESG practices on corporate sustainability and productivity at different stages of economic development through the EKC theory, and there is still a lack of understanding of the specific mechanisms, such as the study of this impact through mediating variables such as financing constraints and green technological innovations, as well as a lack of research on the impacts of this impact on different industries and regional differences are less well studied. To further improve the existing research, this paper empirically analyzes the impact of ESG on GTFP using data from the Huazheng ESG Index from 2009 to 2022 through the EKC theoretical framework (see Figure 3). By incorporating financing constraints and green technological innovation as mediating variables, the study deeply explores the mechanisms underlying the impact of ESG on GTFP. Through heterogeneity analysis, it investigates the differences in these impacts across various industries and enterprise sizes, thereby providing scientific evidence for the government and enterprises to formulate effective ESG policies. This aids high-quality development and offers strategic references for addressing global environmental and social challenges.

The potential contributions of this study to the existing literature are highlighted in the following areas:

First, this paper applies the EKC theory to analyze the relationship between corporate ESG practices and GTFP, offering a new theoretical perspective on the impact of ESG on GTFP in Chinese enterprises. Second, by introducing financing constraints and green technological innovation and employing a mediation effect model, this study explores into the specific mechanisms through which ESG impacts corporate GTFP, providing a deeper understanding of this relationship. Third, through heterogeneity analysis, this study investigates the impact of ESG practices across different industries and enterprise sizes, providing tailored insights and recommendations for the government and enterprises to formulate targeted ESG policies.

The remainder of this paper is organized as follows: Literature review section briefly reviews the literature related to ESG and GTFP. Mechanism analysis section conducts a detailed mechanism analysis. Methodology section provides the methodology and data used in the study. Empirical analysis section presents all the empirical results. Finally, Conclusions and policy implications section concludes and offers policy recommendations.

Literature review

EKC and ESG practices

ESG are key indicators for measuring a company’s performance in environmental protection, social responsibility, and corporate governance.5,6 ESG encompasses three dimensions: ESG. 7 Environmental factors involve a company’s efforts to reduce pollution emissions, conserve resources, and protect the environment, such as lowering carbon emissions and improving resource utilization efficiency. 8 Social factors focus on a company’s performance in labor rights, community relations, and product responsibility. 9 Good social performance not only enhances the company’s image but also strengthens social capital, reduces social conflicts, and lowers legal risks. 10 Governance factors include board structure, shareholder rights protection, and transparency. A sound corporate governance structure can improve management efficiency, enhance investor confidence, and promote the company’s long-term sustainable development. 11

Existing research on ESG typically explores aspects such as information disclosure, corporate adaptive behavior, risk management, financial performance, and corporate reputation. 12 Transparent ESG disclosure not only significantly reduces firm-specific risk 13 but also positively impacts financial performance,14,15 such as reducing litigation risk and mitigating the idiosyncratic volatility of listed company stocks.16,17 Additionally, ESG disclosure effectively alleviates information asymmetry between companies and their stakeholder and enhances corporate reputation through sustainability reports. 18

Research by Li et al. 19 reveals a U-shaped relationship between ESG information disclosure and green innovation in heavily polluting enterprises, aligning with the relationship between economic growth and environmental quality proposed by the EKC theory. 20 This finding suggests that changes in ESG practices may represent adaptive adjustments made by enterprises according to different stages of economic development. 21 This indicates that the EKC theoretical framework provides a solid basis for analyzing the effects of ESG practices at various stages of economic development.22,23 At different stages of economic development, enterprises may prioritize ESG practices differently. In the early stages of economic development, companies might focus more on economic growth; however, as economic development progresses and public environmental awareness increases, companies are likely to pay more attention to ESG practices and performance.24,25

ESG practices and corporate GTFP

In recent years, the relationship between ESG practices and corporate GTFP has garnered significant attention. As global environmental challenges intensify and social responsibility becomes more prominent, companies are increasingly recognizing that continuous ESG practices are not only a reflection of their social responsibilities but also crucial for enhancing competitiveness and achieving sustainable growth. 6 Scholars have utilized various econometric methods, such as fixed effect (FE) models, random effect (RE) models, and generalized method of moments (GMM), to delve deeply into the relationship between ESG practices and GTFP,26,27 significantly enriching existing economic theories and practical applications.

FE models and RE models have advantages in addressing data endogeneity issues and handling explanatory variables that remain constant over time. 28 Utilizing these models allows researchers to more accurately estimate the impact of ESG practices on corporate production efficiency. For instance, Singh et al. 29 found that corporate social responsibility activities significantly enhance the total factor productivity (TFP). Deng et al. 1 employed a dynamic panel data model to examine the relationship between ESG ratings and corporate production efficiency, discovering that companies with higher ESG ratings generally demonstrate greater production efficiency. This suggests that robust environmental governance, social responsibility, and transparent corporate governance structures contribute to improved operational efficiency and market image, giving companies a competitive edge.

Wang and Chu 27 used the GMM to analyze how ESG standards promote TFP growth by improving the information environment. Their study highlights the critical role of information transparency in corporate management, showing that strong ESG practices enhance information transparency, reduce information asymmetry, and attract more investors and partners, thus fostering technological innovation and efficiency gains. Using a RE model, they confirmed that ESG practices play a crucial role in encouraging companies to adopt more environmentally friendly and sustainable production models.

Although ESG has been widely studied, there is limited literature analyzing the specific impact of ESG practices on corporate sustainability and production efficiency at different stages of economic development through the lens of the EKC theory. 30 Moreover, while ESG impacts the corporate production efficiency, existing research study has a limited understanding of the specific mechanisms, particularly in exploring this impact through mediating variables such as financing constraints and green technological innovation. 31 Although the literature notes that ESG practices vary across different industries, detailed analysis of these differences is still lacking, which hinders the ability to develop targeted ESG strategies for specific industries or regions.32,33

To further refine existing research, this paper introduces the squared term of ESG practices, combined with the EKC theory, to explore the impact of ESG practices on corporate sustainability and production efficiency at different stages of economic development. Additionally, this paper introduces financing constraints and green technological innovation as mediating variables in the baseline model, examines the mechanisms of ESG impact, and through industry heterogeneity analysis, uncovers the variability in ESG practices, providing customized ESG strategy recommendations for specific industries and regions.

Mechanism analysis

This study aims to delve into the direct and indirect impacts of ESG practices on the GTFP of firms, considering the mediating roles of financing constraints and green technological innovation, along with the moderating effects of industry and regional heterogeneity.

Direct impact of ESG practices on corporate GTFP

The direct impact of ESG practices on corporate GTFP can be elucidated through three theoretical frameworks. The Porter Hypothesis suggests that when firms enhance their environmental performance, they achieve productivity gains through more efficient utilization of human resources, facilities, and capital. 5 Resource-based theory emphasizes that the effective allocation of resources fosters technological and managerial innovations, enabling firms to optimize the combination of production factors to meet market demands and enhance the production efficiency. 34 The theory of market failures indicates that by fulfilling social responsibilities, such as charitable donations, firms improve public image, reduce stock price volatility, 35 focus on enhancing product and management quality, and promote green productivity. Social exchange theory highlights the establishment of effective employee management mechanisms, investment in employee protection, gender equality, and skills training to motivate skills enhancement, 36 attract talent, increase employee sense of belonging and responsibility, 37 improve labor productivity, and facilitate the enhancement of GTFP.

According to the EKC theory, in the early stages of economic development, environmental pollution increases with the rise in per capita GDP, but after reaching a certain threshold, the pollution levels begin to decline. 38 This theoretical assumption also applies to ESG practices: in the initial stage of implementing ESG practices, companies face increased capital investments, such as equipment upgrades and enhanced environmental standards, which may reduce production efficiency in the short term. At the same time, adjustments in operational models to comply with ESG standards, such as supply chain management reforms and the adoption of new production processes, and the learning adaptation of employees and management, temporarily affect work efficiency and productivity. As time progresses, firms improve efficiency through energy-saving and emission-reduction technologies and resource management. ESG practices stimulate corporate innovation; enhance brand image, attracting customers and investment, improving market performance; successful ESG practices lower legal and environmental risks, reduce compliance costs, and increase sustainability. 21 Therefore, with long-term dedication to ESG, corporate GTFP experiences a trend of initial decline followed by an increase, achieving enhancement.

Based on the aforementioned analysis, the following hypothesis is proposed:

H1: There is a U-shaped relationship between ESG practices and corporate GTFP.

Indirect impact of ESG practices on corporate GTFP

The indirect impact of ESG practices on corporate GTFP within the domain of financing constraints is illustrated by research showing that financing constraints reduce the total productivity gains firms can obtain from trade liberalization. 39 Financing barriers hinder firms’ expansion and reproduction activities, affecting the effective integration and allocation of resources, and becoming a major factor constraining corporate development. 40 The social responsibility advocated by ESG helps enhance corporate legitimacy, promote resource acquisition, ease financial constraints, and meet funding needs. Good ESG performance attracts customers and investment through reputational effects, 41 increasing cash flow, relieving financing pressure, creating better production conditions for firms, promoting effective resource allocation, and enhancing the GTFP.

The impact of green technological innovation on corporate GTFP can be explained from three aspects. Firstly, enterprises seeking profit maximization reduce environmental costs through green innovation, improving production efficiencency,42,43 and enhancing GTFP. Green technological innovation motivates firms to continuously optimize products and production processes, promoting a positive cycle. 44 Secondly, government sustainable development policies consider corporate environmental performance as a basis for investment and credit allocation, 45 supporting firms with more green R&D, 46 strengthening their financing capability and productivity. Lastly, due to the externality and high investment risks of green technological innovation, firms may avoid green technological innovation activitie. 47

Based on the above analysis, the following hypothesis is proposed:

H2: Financing constraints and green technological innovation play mediating roles in the impact of ESG practices on the growth of corporate GTFP.

Industry spillover impact of ESG practices on the GTFP

The impact of ESG performance is significantly influenced by industry and regional differences. Recently, green credit and financial policies implemented by the government aim to direct capital towards environmentally aware and resource-efficient businesses, 48 significantly increasing financing costs for highly polluting industries. This change makes it difficult for high-pollution industries to pass on costs; attempting to do so may compress the profit margins and resource efficiency of downstream industries, thereby reducing corporate GTFP. In this context, by improving ESG performance, high-pollution industries may promote GTFP enhancement in other industries through inter-industry spillover effects.

Regional differences are equally critical to the relationship between corporate ESG performance and GTFP. 49 Due to limitations in the legal environment, economic resources, and regulatory strength, businesses in western regions have significant room for ESG performance improvement. Under the latecomer advantage effect, ESG-related measures may lead to significant improvements and marginal effects. In contrast, the eastern region, with its mature economic development, well-established institutional environment, and strong public social responsibility awareness, places higher demands on corporate environmental responsibility and internal governance, prompting businesses to pay more attention to ESG performance.

Based on the above analysis, the following hypothesis is proposed:

H3: ESG can impact GTFP through industry spillover or regional heterogeneity.

Methodology

Model specification

Benchmark regression model

To measure the impact of ESG practices on corporate GTFP, this paper employs FE and RE models. The FE model controls for unchanging heterogeneity within firms, improving the accuracy of the estimated results. However, when individuals in the study sample share similar characteristics, the RE model may be more effective. To determine which model is more suitable, we conducted a Hausman test. If the Hausman test results are significant (p-value <0.05), we reject the RE model and select the FE model as the primary model.

Based on the EKC theory, which posits a potential nonlinear relationship between ESG and GTFP, this paper incorporates a quadratic term of ESG into the baseline regression model as follows:

Instrumental variable model

This paper employs the number of ESG-related corporate holdings as an instrumental variable for ESG to mitigate the endogeneity issue in the model. The model for the instrumental variable regression is:

Intermediate effect model

To test the mediating effects of financing constraints and green technological innovation, this paper establishes the following models and employs a three-step approach to assess the mediation effects. Based on Model (2), the following regression models are specified:

Variable selection

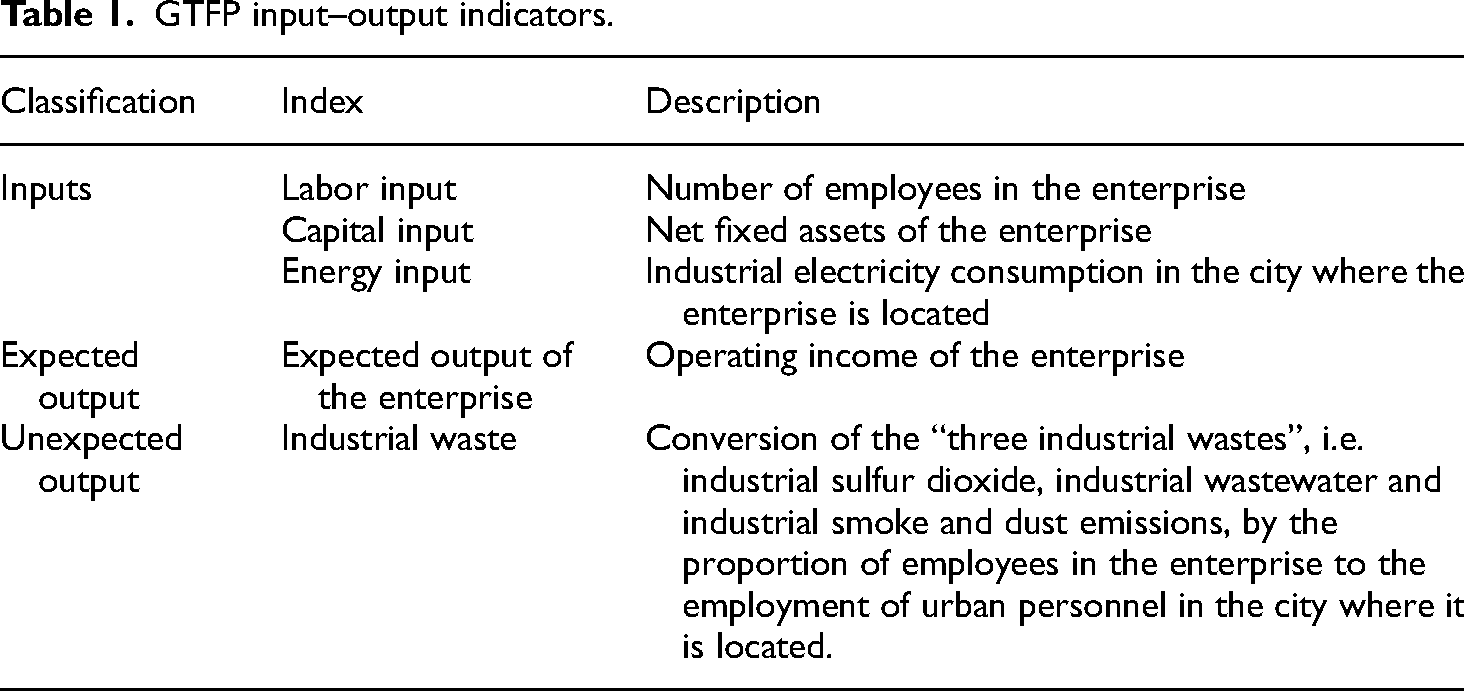

Explained variable

This paper adopts the directional distance function that accounts for undesirable outputs and the Malmquist–Luenberger (ML) productivity index to measure the GTFP of listed companies.

50

Following the approach of Chung et al.,

51

this study calculates the GTFP of listed enterprises. Drawing on Xia andXu,

50

input and output indicators for corporate GTFP were selected, as illustrated in Table 1. The calculation method is described as follows. Factor input:

Labor input takes the number of employees as a proxy variable; Capital input takes the net fixed assets of enterprises as proxy variable. The energy input is converted from the industrial electricity consumption of the city where the enterprise is located to the proportion of the employees of the enterprise in the employment of urban people as a proxy variable. Expected output: Business income is taken as the proxy variable of expected output. Nonexpected output: The “three industrial wastes,” namely industrial sulfur dioxide, industrial wastewater and industrial smoke and dust emissions, are converted according to the proportion of employees in the employment of urban personnel in the city where the enterprise is located.

GTFP input–output indicators.

Assuming a system consists of n decision-making units (

The directional distance function is defined as:

Figure 4 presents the average GTFP values across different industries, with the education sector showing the highest values and the service industry displaying the lowest.

Average value of GTFP by industry.

Total number of green patents of listed companies in China.

Explanatory variable

This study, following the approach of Shen et al., 52 employs Huazheng ESG rating data for measurement. Since 2009, the Huazheng Index has assessed the ESG performance of A-share and bond issuers among other securities issuers, covering all A-share listed companies to date, and has been widely recognized by both the industry and academia. The Huazheng ESG rating includes assessment indicators in three aspects: environmental (E), social (S), and governance (G).

Environmental (E): Measures the company’s environmental management capabilities, including energy use, pollution emissions, resource management, and environmental protection investments.

Social (S): Assesses the company’s social responsibility performance, including employee welfare, community relations, product responsibility, and social welfare.

Governance (G): Evaluates the company’s corporate governance structure and management level, including the board composition, shareholder rights, management transparency, and compliance.

Each aspect’s indicators are derived through a combination of specific quantitative data and qualitative assessments, forming a comprehensive ESG score. Listed companies’ ESG ratings are assigned values from 1 to 9, with higher numbers representing better ESG performance. This method ensures that the Huazheng ESG rating comprehensively covers the three aspects of environmental, social, and governance, and guarantees the scientific and fair nature of the ratings.

In the baseline regression analysis of this paper, to improve the interpretability and comprehensibility of the results, we scaled down the explanatory variables ESG and ESG squared (ESG2) by a factor of ten, naming the variables ESG_10 and ESG2_10. Specifically, this treatment method ensures that the regression coefficients are within a reasonable magnitude range, thereby enhancing the interpretability of the results.25,53 This method is common and reasonable in academic research, providing a more intuitive reflection of the relationships between variables. 54 ESG2 represents the squared term of ESG, used to capture the nonlinear relationship between ESG and corporate GTFP.

Intermediate variable

This paper identifies two mediating effect variables, following the methods of Kaplan & Zingales

55

and Guo and Xia:

56

Financing constraints Green technological innovation

Control variables

Drawing from the existing literature,57,58 this paper selects the following control variables. To reduce data skewness and ensure the robustness of the regression results, we take the natural logarithm of each control variable after adding one.

Stock Ownership Concentration

Leverage Ratio

Return on Assets

Intangible Net Asset Value

Tobin’s Q

Beta

Table 2 presents the descriptive statistics of all variables selected in this study. The results indicate that the data exhibit good stability, with no outliers present, and the standard deviation is less than the mean. The mean value of corporate ESG ratings is 0.458, indicating that, based on the Huazheng ESG Index ratings, most listed companies have ESG ratings ranging from C to BBB.

Descriptive statistics.

Data sources

The ESG rating index data for 1017 companies listed on the Shanghai and Shenzhen stock exchanges from 2009 to 2022 comes from the Wind Financial Terminal. Data on corporate financing constraints and other financial indicators are from the China Stock Market & Accounting Research Database (CSMAR); green patent data is sourced from the China Research Data Services Platform (CNRDS). Data on companies’ GTFP is derived from the China Urban Statistical Yearbook, China Environmental Statistical Yearbook, China Environment Status Bulletin, China Statistical Yearbook, China Regional Economy Statistical Yearbook, and China Energy Data Statistics.

To ensure data accuracy, companies in the special financial and insurance industries, “special treatment” (ST) companies, and those from industries with fewer observations in some years were excluded, resulting in a total of 14,238 firm-year observations. For data on industrial sulfur dioxide, industrial wastewater and industrial soot emissions, a linearly interpolated version of the data was obtained by using linear interpolation to fill in the missing parts in the middle of each year. The GTFP of each firm from 2009 to 2022 was calculated by MAXDEA. This paper processes the data using Stata18 and tests the impact of ESG practices on corporate GTFP through the baseline model.

Empirical analysis

Benchmark regression

Result

To measure the impact of ESG practices on corporate GTFP, the model incorporates core explanatory variables and control variables, performing FEs and ordinary least squares (OLS) regression while controlling for firm FEs. The baseline regression results are presented in Table 3. The findings indicate a U-shaped relationship between corporate ESG and GTFP, with the coefficient of ESG2 being significantly positive at the 1% level, specifically 0.0916. This result confirms the applicability of the EKC theory in ESG practices, showing that as ESG practices deepen, corporate GTFP first decreases and then increases. This discovery aligns with the research of Shi and Xu, 62 who both noted that environmental quality initially deteriorates and then improves with economic development.

Benchmark regression results.

Note: Robust standard errors are in parentheses; **, and *** denote statistical significance at the 5%, and 1% levels, respectively.

Specifically, the ESG coefficient in both models is −0.654, significantly negative at the 1% level, indicating that ESG initially suppresses the growth of corporate GTFP. This aligns with the EKC theory, which posits that in the early stages of economic development, companies face increased costs or challenges in the short term as environmental protection measures may increase costs and reduce production efficiency. Initially, improvements in ESG lead to a decrease in GTFP, but after reaching a certain threshold, further improvements in ESG begin to positively impact GTFP. Analyzing the number of green patents as a proxy for ESG inputs, a steady increase in the number of green patents from 2009 to 2022 indicates increasing investment in green technologies and environmental management. This suggests that over time, as ESG practices deepen, these investments will enhance efficiency, brand reputation, or reduce legal risks, thereby positively impacting GTFP. Aminu et al. 22 also noted that while environmental protection measures may initially increase corporate costs, in the long term, environmental management and innovation can lead to higher production efficiency and economic benefits.

The marginal effect of ESG varies with its level. At lower ESG levels, increases negatively impact productivity, while at higher levels, incremental increases bring significant positive effects. This is consistent with the inverted U-shaped relationship between economic development and environmental pollution described by the EKC theory. Apergis et al. 23 found that ESG practices significantly impact corporate financing costs and production efficiency, further supporting the findings of this paper.

As can be seen in Figure 6, the average ESG scores of SOEs are consistently higher than those of non-SOEs, suggesting that in China, large firms (e.g. SOEs) are significantly better at investing in and performing ESG practices than small and medium-sized firms (e.g. non-SOEs). This implies that SMEs with poorer ESG performance may simply meet minimum compliance requirements rather than proactively improving their ESG practices. This pattern of behavior may lead to a “U”-shaped relationship that applies more to large firms that have the resources and incentives to invest in ESG than to all firms. Therefore, there is a need for further research on the differences in ESG practices among different types of firms to better understand the relationship between ESG and GTFP.

Comparison of the mean ESG scores of state-owned and nonstate-owned enterprises, 2009–2022.

Therefore, Hypothesis 1 of this paper is validated, further supporting the relationship between the impact of ESG practices on corporate production efficiency at different stages of economic development and the EKC theory.

The results for the control variables validate existing research. 63 The estimated coefficients for equity concentration, financial leverage, corporate growth capability, and net profit margin of total assets are mostly significantly negative at the 1% level, while the estimated coefficients for net intangible assets and BETA are significantly positive. Bruna et al. 12 noted that high equity concentration and financial leverage increase governance pressure on companies, thereby affecting production efficiency.

In the FEs and OLS models, the ESG coefficient is −0.654, while the ESG squared coefficient is 0.0916, both significant at the 1% level. This indicates that while initial ESG investments reduce a company’s GEC, the negative impact gradually turns positive as ESG levels increase. Specifically, ESG measures such as improving energy efficiency, reducing waste, and enhancing resource utilization directly promote the technical efficiency, whereas advancements in green technology rely on long-term investments in innovation and technology development. Dempsey et al. 64 highlighted the long-term benefits of ESG practices in improving resource utilization efficiency and corporate image, aligning with the findings of this paper.

The GEC, as a measure of efficiency, is influenced by corporate operations and management practices, which are closely related to ESG measures. Conversely, GTC is affected by factors such as R&D investment, innovation policies, and industry dynamics, which may not directly correlate with the short-term effects of ESG. This aligns with the studies by Chen et al. 7 who noted that ESG practices enhance long-term production efficiency and competitiveness by promoting technological innovation and management optimization.

Robust test

To ensure the robustness of the conclusions, this study applied winsorization to all variables and verified the continued validity of the research hypotheses through regression analysis (Table 4). The results revealed a significant linear relationship between ESG practices and corporate GTFP and GEC, while ESG did not show a significant relationship with GTC. This finding aligns with the research by Xie et al. 60 indicating that ESG practices play a crucial role in enhancing corporate environmental performance and production efficiency. In contrast, the low R2 values for GTC and the control variables suggest their limited role in explaining the variability of the dependent variables. This supports the view of Castellacci and Zheng, 32 who argued that the impact of technological innovation takes longer to manifest and may not be evident in the short term.

Indentation test results.

Note: Robust standard errors are in parentheses; **, and *** denote statistical significance at the 5%, and 1% levels, respectively.

Specifically, the higher R2 values for the relationship between ESG practices and corporate GTFP and GEC demonstrate that ESG practices have greater explanatory power in accounting for the variability of GTFP and GEC. The purpose of winsorization is to reduce the influence of extreme values and ensure the robustness of the estimation results. After winsorization, the significant relationships between most variables and the dependent variables are maintained, thereby validating the robustness of the research conclusions. This aligns with the findings of Li and Tanna (2019), 62 who noted that ESG practices can enhance corporate performance by optimizing resource allocation and improving the management efficiency.

Since the introduction of the new development concept, significant changes have occurred in China’s ESG sector. In response, this paper selects data from 2016 to 2022 for robustness testing, and the regression results presented in Table 5 confirm the robustness of the research conclusions. The results show that the U-shaped relationship between corporate ESG and GTFP persists over different time periods, validating the continued effectiveness of the research. This finding is consistent with the EKC theory, which suggests that as ESG practices deepen, corporate GTFP first decreases and then increases. 38

Sensitivity analysis results.

Note: Robust standard errors are in parentheses; *** denote statistical significance at the 1% level.

Mediation effect analysis

Financing constraint

Financing constraints significantly limit the improvement of corporate GTFP. ESG practices shift corporate goals from purely maximizing economic profits to enhancing both economic and social value, helping companies gain the trust of financial institutions and secure necessary innovation funds. This study uses the KZ index to assess the degree of corporate financing constraints.

The regression analysis results in Table 6 show that ESG performance is positively correlated with financing constraints at the 1% significance level, indicating that good ESG performance may be associated with increased financing constraints. This result suggests that although companies with good ESG performance may have increased capital needs due to adopting more sustainable measures, this increased financing constraint does not necessarily hinder the company’s long-term performance. In fact, the full sample analysis further confirms that despite the increased financing constraints, corporate GTFP is still improved at the 1% significance level. Particularly in terms of GEC, the presence of financing constraints is significantly associated with an improvement in corporate GEC. This result is consistent with the study by Zhang and Vigne, 65 which noted that the presence of financing constraints positively promotes the growth of GTFP, especially in terms of environmental efficiency. Similarly, Apergis et al. 23 found that although companies with good ESG performance face higher financing needs, this does not hinder them from obtaining financing and may actually promote their production efficiency.

The intermediary effect of financing constraints.

Note: Robust standard errors are in parentheses; *** denote statistical significance at the 1% level.

Additionally, by introducing financing constraints as a mediating variable, we find that it partially mediates the impact of ESG on GTFP and GEC. In Table 6, the coefficients of ESG and ESG2 remain significant after adding financing constraints, but their absolute values decrease, indicating that financing constraints play a partial mediating role between ESG and corporate performance.

Green technology innovation effect

Table 7 reports the regression analysis results for the effect of technological upgrades. The coefficient of corporate ESG performance is negative at the 1% significance level, while its quadratic term coefficient is significantly positive, indicating that improvements in ESG performance have a long-term positive impact on corporate green technological innovation. In the full sample, the coefficient of ZL (corporate green technological innovation) is 0.0135, significant at the 1% level, indicating that technological upgrades significantly enhance corporate GTFP. This result aligns with existing research, such as the Porter Hypothesis proposed by Porter and Van der Linde, 66 which suggests that environmental regulations and ESG standards can stimulate corporate innovation capabilities, thereby improving productivity.

The intermediary effect of green technology innovation.

Note: Robust standard errors are in parentheses; *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

In the sample focused on green technological efficiency, ZL is significantly positive, while it is not significant in the green technological progress sample, indicating that corporate green technological innovation has enhanced green technological efficiency. This finding aligns with Chen et al., 7 who found that green technological innovation improves production efficiency. Chen et al. noted that companies directly promote technical efficiency by improving energy efficiency and reducing waste, while green technological progress relies on long-term investments in innovation and technology development.

In response to environmental policies, companies increase investments in environmental protection, purchase clean equipment, and develop and introduce green technologies, promoting green technological innovation. This reduces environmental costs and improves the GTFP. This finding is consistent with Li and Tanna, 67 who found that green technological innovation significantly reduces corporate environmental costs while improving production efficiency.

In summary, Hypothesis H2 of this paper is supported. This finding supports the view that ESG practices enhance corporate GTFP through green technological innovation. 6

Endogeneity analysis

The above research indicates that companies with high ESG scores usually have higher GTFP, but there may be potential reverse causality, where higher productivity could encourage companies to fulfill environmental and social responsibilities. Although the baseline regression model controls for multiple influencing factors, the empirical results may be affected by unobserved factors. 68 To address potential endogeneity issues, such as reverse spillover effects, this study constructs an instrumental variable for ESG. Existing literature often uses industry or regional ESG levels as instrumental variables. While these variables easily meet the relevance requirement, there are concerns about their compliance with the exclusion restriction hypothesis. 23

This study uses the number of ESG fund holdings as an instrumental variable due to its role in alleviating corporate governance externalities and enhancing the ESG performance of listed companies, despite the lack of direct evidence. 8 The establishment and size of ESG funds are determined by fund companies and have no direct connection to corporate GTFP. Additionally, ESG funds rarely intervene directly in the daily management of companies. Instead, they promote ESG performance through active shareholder strategies such as private engagement with company executives. 69

Table 8 shows that the proportion or market value of ESG fund holdings is positively correlated with corporate ESG performance, and the effectiveness of the instrumental variable has been validated through various statistical tests. The F-value of the first-stage regression is 13.49, well above the critical value of 10, ruling out the weak instrument variable problem. The Cragg–Donald Wald F-statistic is 26.6465, significantly exceeding the threshold of 10, indicating the strength and applicability of the instrumental variable.

Endogeneity test results.

Note: Robust standard errors are in parentheses; *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

The number of ESG fund holdings is positively correlated with corporate ESG performance, and after addressing endogeneity issues, corporate ESG performance continues to promote GTFP improvement in the long term. These findings support the positive relationship between ESG practices and corporate productivity enhancement and confirm the validity of using the number of ESG fund holdings as an instrumental variable. 16

Furthermore, the results of this study are consistent with existing literature, indicating that ESG practices can enhance a company’s social responsibility and environmental awareness, thereby improving its long-term production efficiency. 70

Heterogeneity test

Regional heterogeneity

When analyzing the impact of corporate ESG performance on GTFP, the importance of regional differences must be considered. Accordingly, this study divides the sample into three regions based on the geographical location of the companies’ registration: eastern, central, and western, to conduct subgroup regression analysis.

The results in Table 9 show that the estimated coefficients of ESG squared are generally significantly positive, with the estimated coefficient for ESG squared in the western region surpassing those in the eastern and central regions. This indicates that the ESG performance of companies in the western region is most effective in enhancing the GTFP, followed by the eastern region, with the central region showing the weakest effect. This finding is consistent with existing research, which suggests that companies in relatively underdeveloped areas can significantly enhance resource efficiency and environmental management levels when adopting ESG practices. 71

Regional heterogeneity results.

Note: Robust standard errors are in parentheses; *** denote statistical significance at the 1% level.

Further analysis of the decomposed items of GTFP reveals that ESG performance mainly improves green technological efficiency, while its impact on green technological progress is not significant. This aligns with the existing literature, which suggests that ESG primarily enhances corporate operational efficiency rather than directly promoting technological progress. 27

Specifically, the improvement in the western region is most pronounced, followed by the eastern region, and the central region is the weakest. This could be because the western region, being relatively behind the eastern and central regions in terms of infrastructure and economic development levels, experiences more noticeable improvements from the introduction of ESG practices, especially from a long-term perspective. The higher environmental sensitivity of the western region, such as its rich natural resources and ecological environment, along with its latecomer advantage in ESG performance, may lead to more significant improvements and marginal effects from adopting ESG measure. 69

Industry heterogeneity

This paper analyzes the industry heterogeneity in the impact of corporate ESG on GTFP, conducting separate tests for 18 major industries, with results presented in Table 10. The coefficients for manufacturing, electricity, heat, gas and water production and supply industries, wholesale and retail trades, and information transmission, software, and information technology services are 0.762, 0.727, 0.784, and 0.701,respectively, significant at the 1% level. This indicates that in these sectors, enhancing ESG levels significantly promotes GTFP. In contrast, the coefficient for agriculture, forestry, animal husbandry, and fishery is −0.746, significant at the 10% level, indicating that improving ESG levels does not significantly enhance GTFP in this industry.

Industry heterogeneity test.

Note: Robust standard errors are in parentheses; *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

In the manufacturing industry, improving the environmental performance, such as enhancing energy efficiency and reducing waste emissions, directly reduces production costs and improves efficiency. This is consistent with existing research, which indicates that environmental management practices can enhance the competitiveness and productivity of the manufacturing industry by improving the resource utilization efficiency and innovation capability. 70

ESG focuses on stimulating innovation, such as developing environmentally friendly technologies and improving design, which is crucial for enhancing competitiveness and productivity. 15 In high-energy-consuming industries such as electricity, heat, gas, and water production and supply, effective environmental management, such as emission reduction and improving energy efficiency, can significantly improve production efficiency and reduce costs, thereby enhancing GTFP. This result is consistent with Li and Tao, 72 who found the critical role of environmental regulation and energy-saving measures in high-energy-consuming industries.

In the wholesale and retail industry, which is close to the consumer end, improving ESG performance can attract environmentally conscious consumers, and supply chain management is crucial for ESG performance. Existing literature indicates that by improving the environmental and social performance of the supply chain, companies can enhance the overall operational efficiency and market competitiveness. 69

In the information transmission, software, and information technology services industry, energy-saving technologies and innovation can effectively enhance the resource utilization efficiency and operational management levels. With the rapid development of digitization and information technology, ESG practices in this industry not only improve corporate image and customer trust but also significantly enhance the market competitiveness and operational efficiency. 26

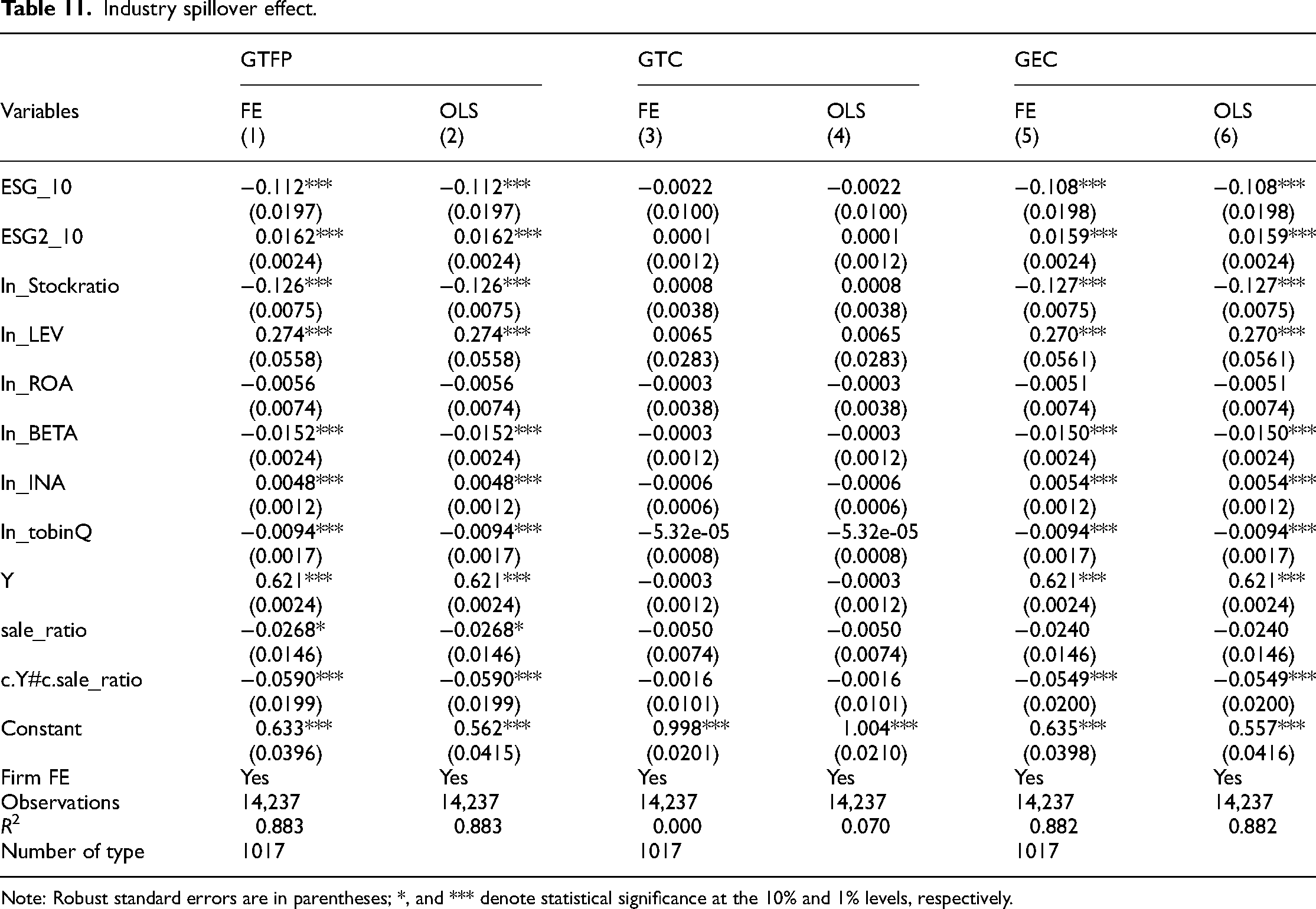

Industry spillover effect

Building upon the study by Zheng and Li,

73

this paper incorporates interaction terms into the empirical model to explore inter-industry spillover effects. The specific model is formulated as follows:

Industry spillover effect.

Note: Robust standard errors are in parentheses; *, and *** denote statistical significance at the 10% and 1% levels, respectively.

The increase in the direct consumption coefficient may lead to rising production costs. The rise in product prices due to ESG factors can increase production costs, driven by factors such as product scarcity, increased transportation costs, or heightened environmental requirements. 15 In competitive and price-sensitive market environments, firms may struggle to pass on cost increases to consumers. Price hikes may lead to reduced demand and profit margins, implying that net profits may decrease even when sales volume remains constan. 26 Considering that the evaluation of GTFP assesses both the efficiency and environmental impact of enterprises, the increase in production costs and decrease in profit margins imply a reduction in resource use efficiency, reflected in the decline of GTFP. 74

Although the initial costs of environmentally friendly materials or technologies may be high and may lead to short-term cost increases, in the long run, these investments are beneficial for a firm’s sustainable development. By gradually adopting green technologies and optimizing resource allocation, companies can improve production efficiency and environmental benefits in the long term. 27

Conclusions and policy implications

Conclusions

This study selects nonfinancial listed companies on the Shanghai and Shenzhen stock exchanges from 2009 to 2022 as the research subjects, using fixed and effects and OLS models to analyze the impact of corporate ESG performance on GTFP after controlling for firm FEs. Through mediating effect models, this study delves into how ESG specifically affects green productivity and examines the spillover effect of ESG across different industries by introducing interaction terms. The main findings are as follows:

In the short term, corporate ESG performance suppresses GTFP growth, while in the long term, it contributes to GTFP enhancement, specifically reflected in the positive impact of the ESG squared term on corporate GTFP (coefficient of 0.990, significant at the 1% level), with no significant impact on technological change. This finding is consistent with the EKC theory, which suggests that companies may face high costs and operational adjustment challenges during the initial stage of ESG investment, thereby suppressing GTFP in the short term.

38

However, as companies gradually adapt to and optimize these ESG practices, these investments will enhance corporate efficiency and sustainable development capabilities in the long term.

66

The mitigation of financing constraints and green technological innovation play mediating roles in enhancing GTFP. The alleviation of financing constraints significantly promotes GTFP growth, especially in terms of environmental efficiency.

5

This indicates that when companies can obtain more financial support, they are better able to invest in environmental technologies and sustainable development projects, thereby improving GTFP. Green technological innovation also has a significant impact on improving GTFP (coefficient of 0.126 at the 1% significance level), indicating that technological innovation primarily enhances green technical efficiency.6,7 This finding supports the Porter Hypothesis, which suggests that environmental regulations and ESG standards can stimulate corporate innovation capabilities, thereby improving productivity. From a regional perspective, the ESG performance of companies in the western region contributes more significantly to GTFP enhancement. This result may be related to the relatively underdeveloped economic level in the western region, where these areas have a greater need to improve corporate production efficiency and environmental sustainability through ESG practices.

67

Industry analysis reveals that manufacturing, electricity, heat, gas and water production and supply, wholesale and retail, and information transmission, software, and information technology services significantly promote the growth of GTFP by improving ESG performance. Especially in the manufacturing and energy industries, ESG practices can significantly reduce pollution and resource waste, thereby improving production efficiency and environmental benefits.

75

Although this study reveals the impact of ESG practices on corporate GTFP and its internal mechanisms, there are still some limitations. First, the data of this study are limited to nonfinancial listed companies on the Shanghai and Shenzhen A-share markets in China. Future research could extend to companies in other countries and regions to verify the universality of the research results. Second, as corporate ESG standards and policies continue to evolve, future research should update data and analytical methods to reflect the latest developments. Third, while many variables in the model are statistically significant and the R2 values are high, indicating strong explanatory power, the R2 value is not the sole evaluation standard. Future research should further refine the model to improve its explanatory power and predictive ability.

Policy implications

This study reveals that proactive ESG practices by corporations significantly enhance GTFP, providing a theoretical foundation for sustainable economic development. Based on these findings, the following policy recommendations are proposed:

The government should further improve the ESG-related policy system of China’s financial market and incorporate the construction of sustainable development goals into the top-level design of ESG. Considering the phased characteristics of enterprise ESG performance and the long-term trend of ESG rating, the government should establish a dynamic ESG evaluation system. By incorporating sustainable development values into formal institutional frameworks and making them concrete and mandatory, effective short-term constraints can be created. The quality, reliability and transparency of ESG rated products also require unified government supervision and management. At present, domestic mainstream rating agencies have their own evaluation methods and frameworks, but the transparency is not high. It is difficult for investors to understand the detailed calculation process and basis of rating results. In order to reduce the diversity of the ESG rating system, the government should improve the transparency of the rating agencies’ rating methods and data. By disclosing rating methods and data sources, investors can greatly increase their understanding and trust in rating results. For enterprises with excellent ESG performance, the government should support them by means of tax relief and green credit. Enterprises with poor ESG performance will be punished in the form of administrative notification and negative list. The government should improve the ESG information disclosure system and improve the quality of information disclosure. Under the influence of insufficient policy constraints and weak internal motivation, the scope of ESG information disclosure of Chinese enterprises is relatively small, the content is relatively single, and the quality is uneven, which directly affects the credibility and influence of ESG values. In this regard, we propose to first strengthen the mandatory information disclosure through policy constraints, clearly require enterprises to disclose ESG information through the introduction of relevant laws and regulations, regulate the disclosure behavior of enterprises, and improve the transparency and credibility of information. Punishments shall be given to enterprises that do not disclose environmental information in accordance with the provisions of the Measures, or that disclose environmental information that is untrue and inaccurate. Secondly, it is necessary to build an information disclosure system that is suitable for Chinese enterprises and fully reflects the characteristics of the industry. When formulating the information disclosure system, the characteristics and actual situation of different industries should be fully considered, and targeted disclosure standards and norms should be formulated to improve the quality and relevance of information disclosure and better reflect the actual situation of enterprises. Strengthen the regulatory system, establish third-party audit disclosure reporting requirements, and ensure that all publicly available ESG information is audited and verified by third-party auditors. Taking into account the characteristics of different regions and industries in China, adopt a differentiated ESG evaluation system for industries. There are significant differences in ESG disclosure across sectors, with finance, steel, transportation, real estate and mining leading the way in both the number and rate of reports published. The information disclosure rate of agriculture, forestry, animal husbandry and fishery, pharmaceutical, electronics and telecommunications industries is low. Accelerating the establishment of ESG information disclosure standards that are in line with China’s national conditions and for the characteristics of listed agricultural and fishery companies in China, ensures the comparability of data in different industries and regions, and enhances the consistency and scientific rigor of ESG ratings. The government should unify the disclosure framework, clarify the disclosure caliber, and standardize the relevant elements. In the form of disclosure, reduce the subjective qualitative description, enrich and improve the quantitative indicators, and facilitate the horizontal and vertical comparison between enterprises and industries. In terms of disclosure content, take the initiative to disclose negative information, respond reasonably and appropriately, and ensure the authenticity and integrity of disclosed information; Combined with the characteristics of listed agricultural and fishery companies in China, we focus on the disclosure of food safety, environment and social responsibility. Given the economic, infrastructure, and environmental differences between China’s regions, a tailored ESG rollout strategy is critical. The government should focus on supporting the western region through financial assistance, tax incentives and technical assistance, especially to improve the efficiency of green technologies. The eastern region should use its economic and technological advantages to advance green practices, while the central region needs to strengthen ESG investments to improve GTFP outcomes.

Supplemental Material

sj-pdf-1-sci-10.1177_00368504241288782 - Supplemental material for How green governance empowers high-quality development: An EKC framework-based analysis of ESG and green total factor productivity

Supplemental material, sj-pdf-1-sci-10.1177_00368504241288782 for How green governance empowers high-quality development: An EKC framework-based analysis of ESG and green total factor productivity by Zhe You, Dandan Chen, Chuandi Fang, Mengjie Gao and Jinhua Cheng in Science Progress

Footnotes

Acknowledgments

We gratefully acknowledge the financial support received from the National Natural Science Foundation of China (No. 71991482, No. 72104189, and No. 72204235); The Ministry of Education of Humanities and Social Science project: No. 23YJC790021, Hubei Provincial Department of Education Philosophy and Social Sciences Research Project.

Authors’ contribution

Zhe You contributed to writing—original draft, conceptualization, methodology, formal analysis, visualization, and software. Dandan Chen contributed to writing—review and editing, conceptualization, methodology, and supervision. Chuandi Fang contributed to writing–review and editing, conceptualization, formal analysis, and visualization. Mengjie Gao contributed to writing–review and editing, methodology, and software. Jiahao Chen contributed to writing–review and editing, conceptualization, and formal analysis.

Data availability statement

In compliance with the journal’s requirements, this manuscript includes a Data Availability Statement to ensure transparency and reproducibility of our research findings. All data supporting the conclusions of this study are openly available as follows:

The authors confirm that the data supporting the findings of this study are available within the article and its supplementary materials.

Where applicable, source data for figures and other evidences in this manuscript are provided as supplementary materials.

Any additional information required to reanalyze the data reported in this paper is available upon request from the corresponding author.

Restrictions apply to the availability of some data, which were used under license for the current study. Data are however available from the authors upon reasonable request and no third-party permissions are required for the availability of the data used in this study.

This statement is intended to provide transparency and support the replication of our research findings, adhering to the principles of open science.

Declaration of conflicting interest

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article. No conflict of interest exits in the submission of this manuscript, and manuscript is approved by all authors for publication. I would like to declare on behalf of my co-authors that the work described was original research that has not been published previously, and not under consideration for publication elsewhere, in whole or in part. All the authors listed have approved the manuscript that is enclosed.

Ethical statement

This research adheres to the ethical standards for research involving human participants and/or animals, ensuring respect, integrity, and responsibility toward all participants. Ethical approval was obtained from Wuhan Institute of Technology’s Ethical Review Board (ERB), where applicable. Informed consent was secured from all participants, and their anonymity and confidentiality were guaranteed. No animals were used in this study. Any potential conflict of interest has been disclosed, and all funding sources are acknowledged. This work is committed to upholding the highest standards of integrity and ethical conduct in academic research.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge the financial support received from the National Natural Science Foundation of China (No. 71991482, No. 72104189, No. 72204235); The Ministry of education of Humanities and Social Science project: No. 23YJC790021, Hubei Provincial Department of Education Philosophy and Social Sciences Research Project.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.