Abstract

Considering China's green credit policy (GCP) as a quasi-natural experiment, this study discusses the effect of GCP on enterprise green innovation (GI) using a difference-in-difference method based on data from Chinese listed companies from 2009 to 2020. The results indicate that green credit enhances the strategic GI of heavy polluters while significantly inhibiting essential GI, thus suggesting the nonexistence of the Porter effect. In addition, the inhibition effect is attributed to an increase in financing constraints and a reduction in government subsidies, firm research and development investment, and employment scale. This disincentive effect is particularly pronounced in privately owned firms, small cities, and capital-intensive low-profitability firms. Resource misallocation caused by the GCP fails to stimulate the green transformation of heavily polluting industries through the Porter effect. Hence, governments should establish a diversified green financial system, integrate green venture capital and GI elements, and guide the flow of social capital toward green industries.

Introduction

The utilization of fossil fuels in agricultural and industrial production systems results in extreme climate change,1–3 which adversely affects both human health and the natural environment.4–6 Inefficient energy consumption increases emissions, which ultimately degrades the ecology. China's extensive growth has resulted in rapid economic progress. To achieve a green economy, the Chinese government has subsidized abundant green investments in environmental governance. Overexploitation has created a significant ecological deficit, which occurred due to untimely intervention. Green technologies are vital for conserving resources, reducing pollution emissions, and achieving a circular economy.7,8 Guidance for green technology development will be emphasized in long-term human research, as this technology determines whether more than 60% of the carbon reduction targets can be achieved. Green innovation (GI) promotes the green transformation of companies and enhances productive capacity and competitive advantage. 9 In addition to government policies, the business financing environment is a critical driver of GI. 10 Firms engaged in technology research and development (R&D) must assume high risks associated with unknown return cycles and returns. 11 However, the GI generates environmental externality through reduced environmental costs. This externality triggers severe market failure, thus resulting in conflict between economic and ecological interests. 12 Meanwhile, financial instruments are essential for eliminating environmental pollution. 13 Under financial resource constraints, green investments will trigger a “crowding-out effect” on productive investments. Green finance can address the lack of incentives for microentities to innovate by relying on the advantages of capital, markets, and credit. Green finance, which is a financial support tool for green development, has piqued the interest of governments and scholars worldwide in their quest to pursue long-term, healthy, and sustainable economic development.

Green finance is a financing activity that expands or provides environmental benefits through green financial bonds, banks, carbon market tools, fiscal policies, financial technology, community green funds, and other financial tools and policies. The 27th Conference of the Parties highlighted that climate finance has been emphasized in climate summits. The Paris Agreement must be implemented urgently through legislation, policies, and projects to mitigate and adapt to extreme climatic damage. Currently, green finance policies are being implemented to accelerate the green transition. As the largest developing country, China presents a loan balance that has increased from RMB 5.2 trillion in 2013 to RMB 15.9 trillion in 2021, which represents an average annual growth rate of 14.99%. In 2021, direct and indirect green loans from financial institutions for carbon emission reduction projects are 7.3 trillion yuan and 3.36 trillion yuan respectively, which constitute 67% of the total green credit. Compared with general financial approaches, green finance exhibits certain peculiarities. The green finance policy stipulates more explicit requirements for the operation of financial institutions and emphasizes that factors such as conserving resources, controlling pollution, protecting the environment, promoting national health, and maintaining biodiversity should be important for making banking credit decisions.14,15 In terms of implementation effectiveness, the results of numerous studies showed that the green credit policy (GCP) is effective for environmental management. Green credit significantly contributes to the innovative performance of green firms and limits the flow of credit to heavy polluters.16,17 Through fund allocation, green credit restructures heavily polluting industries, thus allowing heavy polluters to escape credit constraints by increasing their investments in environmental management. 18 However, some scholars believe that green credit fails to achieve the expected results and may even impose adverse effects. This is attributed to the decrease in investment efficiency of renewable energy companies in green finance and the failure to improve firms’ technology and optimize the industrial structure by reducing loan amounts and maturities.17,19 Clearly, the policy effects of green finance are diverse due to differences in research methods, perspectives, and time horizons. Additionally, the effect of green finance on the GI of heavy polluters remains an active topic of discussion.

The contributions of this study are as follows: First, by evaluating the effect of the GCP on corporate innovation, our findings enrich the literature regarding the effects of environmental and economic policies. The effectiveness of the GCP has been discussed in some studies from the perspectives of enterprise investment and financing; however, few studies delve into enterprise technological innovation. Second, we attempt to reveal the inhibitory mechanisms of green credit on GI. We conclude that green credit will be similar to the cost effect, which results in a decrease in incorporated investment toward R&D and hence ineffective innovation compensation. A rigorous empirical test was conducted to provide conclusive evidence regarding the relationship between the GCP and corporate GI. Third, we investigate the effect of heterogeneity and discovered that the effects of the GCP are constrained by firm ownership attributes, profitability, and geographic location. This finding allows us to identify differences in the effects of policy implementation, thus allowing the GCP to be further improved. Green credit is a financial activity that promotes environmental protection and sustainable social development and is crucial in promoting green economic development. This study clarifies the role and effect of the GCP on corporate GI. The effect of green finance policy is verified in this study, which provides a basis for whether green finance promotes social green transformation. Additionally, our findings provide a reference for improving green financial systems, promoting social transformation, and achieving carbon neutrality.

Literature review and theoretical mechanisms

Literature review

Literature study regarding green credit

The GCP is defined as sustainable financing. 20 In the credit issuance process, the economic profit indicators and environmental factors are comprehensively investigated by financial institutions to realize appropriate loan decisions. 21 Therefore, the GCP refers to a policy instrument in which financial institutions provide preferential loan support to enterprises engaged in new energy, circular economy, and green manufacturing in accordance with relevant national policies, and restrict investment projects through punitive interest rates. 17 Additionally, most studies indicate that the effects of the GCP are positive.18,22 The GCP effectively increases the innovative productivity of green corporates and reduces new loans to high polluters. Additionally, through support from bank and commercial credits, heavily polluting enterprises are expected to significantly increase their investment in environmental treatment, thus accelerating industrial restructuring and improving the environment significantly. However, based on different findings, the GCP does not yield the anticipated results and may result in negative consequences in some cases. Through adjustments in the amount and terms of loans, the GCP cannot sufficiently influence enterprises to upgrade their production technology and restructure the industry. Once the GCP is not effectively implemented, the investment efficiency of renewable energy firms decreases. 17 The GCP effects depend on the legal environment, and the envisioned policy effects may not be realized once the legal system vanishes. In addition, the effect of financing on the R&D investments of firms has been emphasized in academia. Scholars argue that convenient external financing effectively promotes the R&D investment of firms.23,24 Commercial banks will improve credit thresholds and specify eco-friendly levels as the basic criteria for granting loans, which may increase corporate financing costs and reduce corporate long-term loans. 25 In addition, green bond pricing and its effect on corporate value and performance have triggered discussions among scholars.26–28

Literature study regarding GI

Research pertaining to green technology comprises three main aspects. First, the concept of green technology is applied. Technological innovation refers to the implementation of a new or modified product, service, marketing approach, or management style in business practice. GI technologies enable the economical use of resources, the effective reduction of raw material inputs, and ecological protection. Kemp and Pearson 29 explained GI from a broad perspective and suggested that technological innovations that benefit the environment can be named GI. It includes the innovation of the environmental management system, with the government serving as the main body, and the innovation of production and consumption systems, such as the renewable energy system. GI comprises two primary aspects, that is, green process innovation and green product innovation. 30 GI cannot be measured precisely because of the complexity of technology used in the industry. In addition, because a unified measurement standard for the reduction of pollutants does not exist and improvements in resource utilization are insufficient, corporate green patents have become a key criterion for portraying corporate GI in numerous cases.

GI is considered a key factor affecting economic growth and eco-friendly sustainable development. 31 GI-focused companies are more likely to earn a good reputation and social recognition, as well as achieve product premiums and sales growth. 32 Additionally, GI is an important tool for achieving cost reduction and quality improvement. Therefore, scholars have attempted to clarify the motivation for GI in firms and discovered that it mainly comprises external factors, internal factors, and the organizational structure of firms.33–35 Specifically, the external factors include subsidy policies, ambient regulations, the monitoring of energy consumption, the expansion of green markets, and the proliferation of carbon finance markets.36–38 The internal factors include the technical capabilities and resource availability of the enterprise. The organizational structure of a firm comprises corporate governance mechanisms, green awareness, ecological quality management, and ecological pressure from stakeholders.39–41 The dual role of credit policy in GI increases the stress of survival, which motivates firms to engage in GI to fulfill environmental supervision standards. Meanwhile, introducing a series of policies, such as tax exemptions and green subsidies, would encourage enterprises to strive toward technological innovation. 42 Yang and Yang 43 suggested that human capital accumulation, R&D investment intensity, and knowledge stock of enterprises are key factors that promote GI. However, compared with conventional innovation activities, human capital, and R&D investments contribute less to GI, thus necessitating more knowledge and information from exterior parties. 44 Regarding internal factors, Sanni 45 argued that organizational capabilities and the availability of knowledge resources affect the green technologies of firms. Using survey data from 442 firms in China, Cai and Li 46 discovered that competitor pressure and market incentive-based environmental regulations contribute significantly to GI.

Based on a literature review, we discovered that the concept, economic benefits, and driving factors of technological innovation have been discussed in previous studies. In general, several aspects can be improved. However, whether existing studies analyzing GI from a GCP perspective disregard heterogeneity due to differences in research methods, perspectives, and time horizons remains unclear. The effect mechanism of GI, particularly on heavy pollutants, must be further investigated. However, to address deteriorating resources and environmental problems via a new financial product, systematic empirical evidence does not exist that demonstrates whether the GCP is effective in improving the GI of heavy polluters. Nonetheless, the aforementioned literature provided inspiration and perspectives for this study. Therefore, in this study, a quasi-natural experiment was conducted using the GCP introduced in China and the difference-in-difference (DID) method was employed to empirically investigate the effect and mechanism of GCP enforcement on corporate GI in China.

Theoretical development

GCPs offer different credit lines and interest rates to businesses as well as provide financial support at the macro level. Environmentally friendly businesses will receive credit support, whereas heavy polluters will be adversely affected by low credit lines. 47 Under the GCP, heavily polluting enterprises are affected by strict credit restrictions and cannot easily secure funds to maintain normal production and operation. Owing to increasing financing costs and difficulties, the marginal production costs of polluting firms have increased, which may adversely affect other types of investments and reduce the production scale. 48

Companies engaging in GI facilitate green transformation. GI not only facilitates credit limits but also provides enterprises with an environmentally friendly option that allows access to capital markets and alleviates capital pressure.

49

GCPs aim to internalize the externalities of corporate environmental pollution and motivate enterprises to develop GI and reduce pollution through front-end prevention and control/end-of-pipe treatments. Notably, two main types of corporate GI exist: essential innovation and strategic innovation. Essential innovation promotes green technological progress through higher-quality GI inventions that increase a firm's competitive advantage and improve its environmental performance. Strategic innovation seeks other benefits by pursuing the quantity and speed of innovation to satisfy the requirements of the government system and achieve creditor tolerance. The GCP affects corporate GI in the following manner:

Financing constraints. Essential GI exerts a significant catalytic effect on corporate pollution control. However, the process of patent acquisition for GI is affected by long R&D cycles, high risks, and uncertain returns.

50

By contrast, green strategic innovation offers the advantages of low cost, easy imitation, and short cycle time. Companies can obtain several green patents for utility models via small capital investments. Firms tend to respond to GCPs through strategic innovation instead of essential innovation, which features uncertain inputs. Thus, the financing constraints caused by the GCP encourage heavy polluters to engage in strategic GI instead of essential GI. Government subsidies. Through the implementation of GCPs, local governments subsidize the GI of enterprises through financial allocations, tax rebates, or exemptions. This form of financial support allows enterprises to overcome financing constraints, reduce the capital costs of their GI activities, and enhance their GI performance.51,52,53 Moreover, it effectively promotes the green transformation of enterprises and industrial structure optimization. The GI performance of enterprises is an important indicator that enables governments to assess the effectiveness of subsidies. Companies that achieve green transformation are more likely to receive green subsidies. Some enterprises receive government financial support through GI activities. Meanwhile, the purpose of R&D innovation by enterprises may not be to improve production processes and reduce emission levels, but to satisfy the policy requirements of government subsidies and pursue the quantity and speed of innovation. This adverse selection further increases the crowding-out effect of green credit policies on enterprises’ essential innovation, thus encouraging them to pursue strategic innovation. R&D investment and employment scale. Strategic GI requires lower R&D investments and higher returns on government subsidies. Companies affected by financial constraints will reduce their R&D investment and downsize their R&D staff to ease the financial pressure, thereby resulting in the crowding-out effect on corporate R&D investment.

54

Consequently, the overall green R&D investment and R&D staff investment of the companies will continue to decrease.

Methods and data

Model settings

To verify the theoretical analyses in this study, a DID model was formulated as follows to evaluate the effectiveness of green financing on corporate GI:

Method for measuring control variables.

The sample data range in this study includes Shanghai and Shenzhen A-share listed companies from 2009 to 2020. Corporate green patents were obtained from the Green Patent Research Database of the Research Data Service Platform. Data for firm-level control variables were extracted from the Wind database and the China Stock Market and Accounting Research Database.54,55 Based on previous studies, this study addresses the original data as follows: (1) Samples from the financial and real estate industries were excluded. (2) ST and PT samples were excluded. (3) Delisted samples were excluded. (4) Samples that included incomplete financial data were excluded. (5) The 1% and 99% quantiles of all continuous variables in the sample were identified to eliminate extreme values (Table 2). The analysis flow performed in this study is as follows: First, we analyzed the direct effect of GCPs on green technological innovation; subsequently, we comprehensively discuss the heterogeneous effects between them. Finally, we analyze the effect mechanism of green credit on GI from the perspectives of financing constraints, government subsidies, R&D investment, and employment scale.

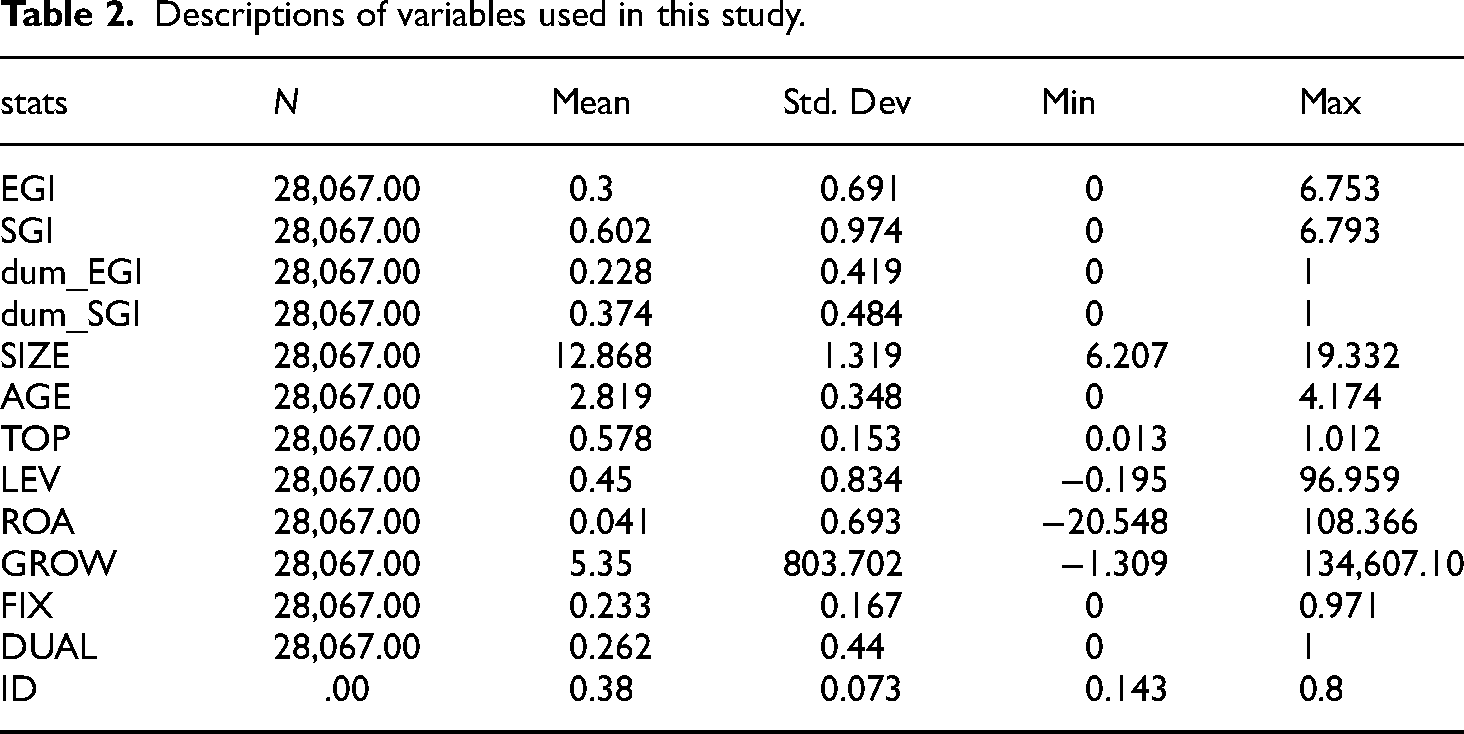

Descriptions of variables used in this study.

Results and discussion

Benchmark model

We regressed Equation (1) and obtained the benchmark regression results (Table 3). The dependent variables were the EGI and SGI. The regression model considers the control variables of firm-, year-, and industry-level fixed effects. Based on the GCP evaluation model shown in Column (1), the estimated coefficient of the interaction term (pollution*post) is −0.082, which is statistically significant at the 5% level. This indicates that the GCP reduces the GI of enterprises in restricted industries but not in non-restricted industries. Thus, the crowding-out effect of green finance policies is validated. As an environmental economic policy, the GCP urges financial institutions to consider the environmental performance of enterprises as an important criterion for granting loans, which may reduce the scale and performance of polluting enterprises. Additionally, by obstructing the financing channels of heavy polluters, the GCP reduces financial support to GI and deters corporate GI behavior.

Basic regression results.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

As shown in Column (2), the estimated coefficients (pollution*post) are significantly positive, thus indicating that the GCP increases the strategic innovation of firms. Under the constraints of the GCP, enterprises do not receive much financial support from financial institutions and can in fact be charged by severe pollution penalties. Enterprises expect to increase their number of green patents by approving simple utility patents, escaping pollution punishments, and obtaining more subsidies and tax incentives. Thus, these firms pursue the quantity of innovation and then disregard the quality of innovation.

Meaningful findings were obtained from the results of the control variables. The larger the enterprise scale, the more conducive it was to the GI. The coefficient of firm age is significantly positive, indicating that long-established firms have a higher capacity for GI. This might be because these firms have accumulated many innovative elements that facilitate GI activities. The regression coefficient of stock ownership concentration is significantly negative, thus implying that corporate equity concentration is detrimental to corporate GI. The effect of the asset–liability ratio on corporate GI is significantly positive, thus demonstrating that companies with high debt repayment capacities are imposed by fewer financing constraints. A higher fixed assets ratio implies that firms have more collateral, which enhances their financing abilities. The regression coefficients of return on assets, position overlap, and independent directors do not pass the significance test.

To prevent the findings above from being affected by different GI indicators, GI applications are used as explained variables for the regression analysis in Columns (3) and (4). The estimation results show that, under different GI measures, the value and significance of pollution*post are essentially the same. Therefore, the conclusions of this study are convincing.

Column (5) of Table 3 lists the number of patents obtained from firms for all types of GI. The regression coefficient is insignificant, thus suggesting that firms consider both EGI and SGI when affected by financial pressure. However, the quality of innovation is considered as well, and the results in Column (6) show that GCPs significantly reduce the portion of essential innovation. This implies that the GCP increases the quantity of GI but reduces the quality of innovation, thus resulting in the f “good money replacing bad money” phenomenon. This finding is consistent with those of Wang et al. and Su et al.56,57 Their findings indicate that the GCP inhibits green technology innovation among heavily polluting firms. By contrast, Zheng et al. and Chen et al.58,59 suggest that a GCP can significantly promote technological innovation by increasing R&D investment and management efficiency.

Robustness test

Table 4 presents the results of a series of robustness tests performed to obtain convincing estimation results. The regression coefficients in the models listed in Columns (1) and (3) are insignificant, thus indicating that the GCP does not promote EGI activities among heavy polluters. Severe financing constraints have restricted the incentives for companies to undertake green technology. Under the GCP constraints, high polluters pursue SGI to offset the decline in EGI inputs and volumes. As shown in Columns (2) and (4), the coefficients (pollution_post) are statistically significantly positive at the 1% level, thereby demonstrating that the GCP motivates constrained firms to invest scarce factors in SGI projects for short-term policy support funds.

Robustness test results (1).

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

The city- and firm-level fixed effects are listed in Table 5. The regression results in Columns (1) and (2) show an increase in the significance of the coefficients (pollution*post) compared with the baseline regression, thus suggesting that the results remained robust and reliable after the fixed effects were excluded. Moreover, the clustering of standard errors to industry-year levels presented in Columns (3) and (4) did not change the robustness of the results. Therefore, in the “cost crowding out” effect of the GCP, heavy polluters allocate resources to SGI as opposed to EGI.

Robustness test results (2).

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

Other environmental policies introduced in China between 2008 and 2020 may have affected the industrial structure and production patterns of firms, which consequently resulted in changes in their GI behavior. Hence, the effects of these factors on the GCP must be eliminated. In this regard, we used the cost of pollution control in each province to eliminate the effects of competing environmental policies. Columns (1) and (2) of Table 6 show that the coefficient of the effect of the GCP on corporate GI is consistent with the basic regression results after disturbances from environmental regulatory factors were excluded. In addition, after controlling for potentially missing variables (such as the operating cash flow, Tobin's Q, capital intensity, financial expense ratio, and profit margin), the results remained convincing.

Robustness test results (3).

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

Parallel trend test and expected effect test

The prerequisite assumption for adopting the DID model is that the treatment and control groups satisfy the same trend assumptions prior to industrial policy enforcement. The event analysis method was used to examine mutual trends in the treatment and control groups, with Post in Equation (1) replaced by a dummy variable for each year. Columns (1) and (2) of Table 7 reveal that the coefficients were not significantly different before the implementation of the GCP, thus confirming the parallel trend hypothesis. After the GCP was implemented, the absolute value and significance of the coefficients increased steadily despite the time lag from the effect of the GCP on GI. We concluded that the GCP inhibited EGI among heavy polluters but accelerated their strategic SGI.

Parallel trend test and expected effect test.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

The GCP can be regarded as quasi-experimental as policy shocks are exogenous, that is, companies in various industries cannot predict the implementation of this policy. To verify the premise of the parallel trends, we added poll_post10 and poll_post11 to Column (1) to test the expected effects in 2010 and 2011. Columns (3)–(6) show that the coefficients (pollution_post10 and pollution_post11) of the expected effect are insignificant. Therefore, prior to the implementation of the GCP, the expected effects of implementing the policy in different industries were unclear. This further supports the adequacy of the model in fulfilling the requirements of the parallel trend assumption.

Effects of other unobservable characteristics: placebo test

A placebo test was conducted, and the results are shown in Figure 1. A randomized setting was used to construct a dummy treatment group via random sampling. In this study, several companies with similar numbers of firms to the original experimental group were randomly selected as the virtual experimental group. We regressed Equation (1) using the DID model and repeated the placebo test 500 times to assess the robustness of the test results, which are shown in Figure 1. The regression coefficients were distributed around zero, thus conforming to a normal distribution. The coefficients (0.078 and 0.094) were outside 99% of the coefficients estimated from 500 repetitions, which excluded the possibility that the regression results were caused by unobservable factors.

Placebo test.

Heterogeneity analysis

City heterogeneity

The listed companies in China are mainly distributed in large cities, such as Beijing, Shanghai, Guangzhou, and Shenzhen. A large disparity exists between large and small cities in terms of bank credit facilities and access to financing. Green financing is more readily available to companies in metropolitan areas, which feature mature credit markets and diverse financing channels. Therefore, we categorized cities into large and small cities in this study to examine the heterogeneous effect of the GCP on the GI of enterprises at different city scales. Columns (1) and (2) of Table 8 show the heterogeneity in large cities and other cities, respectively. In the large cities, the effect of the GCP on EGI was insignificant, whereas it was significantly negative in the small cities. This implies that highly polluting companies in large cities are imposed by fewer credit constraints. Therefore, firms in large cities possess sufficient funds to offset the unfavorable consequences of the GCP on EGI.

City heterogeneity and ownership heterogeneity.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

Ownership heterogeneity

Based on extensive studies, SOEs, instead of private enterprises, dominate the loan market. Under the GCP, SOEs can still access sufficient funds for green transformation. However, under credit restrictions, private enterprises are affected by the “crowding-out effect” arising from technological innovation capital investments. Columns (3) and (4) of Table 8 show that the effect of the GCP on EGI in SOEs is insignificant, whereas its effect on private enterprises is significantly negative. This suggests that the GCP adversely affects the EGI of private enterprises and reduces the quality of green investments.

Heterogeneity of capital intensity

To identify whether the GCP imposes different effects on capital-intensive firms, we categorized industries into two groups, that is, capital-intensive and labor-intensive industries, based on the average industry intensity in the year prior to the policy implementation. Column (1) of Table 9 shows that the GCP inhibits GI among capital-intensive heavy polluters. This is attributable to the fact that capital-intensive enterprises rely significantly on credit. Therefore, the GCP imposes a severe “crowding-out effect,” which reduces the input and output of EGI in capital-intensive enterprises. Column (2) shows that the effect of the GCP on labor-intensive firms is insignificant. This is attributable to the fact that labor-intensive firms are more severely constrained by labor costs than by financial disincentives.

Heterogeneous results on capital-intensive and profitability level.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

Heterogeneity of profitability

The credit constraints encountered by enterprises with different profitability levels differ. We used the average profitability to classify companies into high- and low-profitability companies. Column (3) of Table 9 shows that the GCP substantially affects the EGI of high-margin firms. This is attributable to the fact that high-profit enterprises have better development prospects and diverse financing channels, which render their EGI behaviors unaffected by the GCP. The results in Column (4) indicate a significant adverse effect on low-profit enterprises. The cost-crowding effect reduces the total EGI expenditure in firms with lower profitability. In this case, low-margin firms tend to reduce their R&D expenditures and EGI activities to reduce operating costs when presented with uncertain business risks and financing constraints.

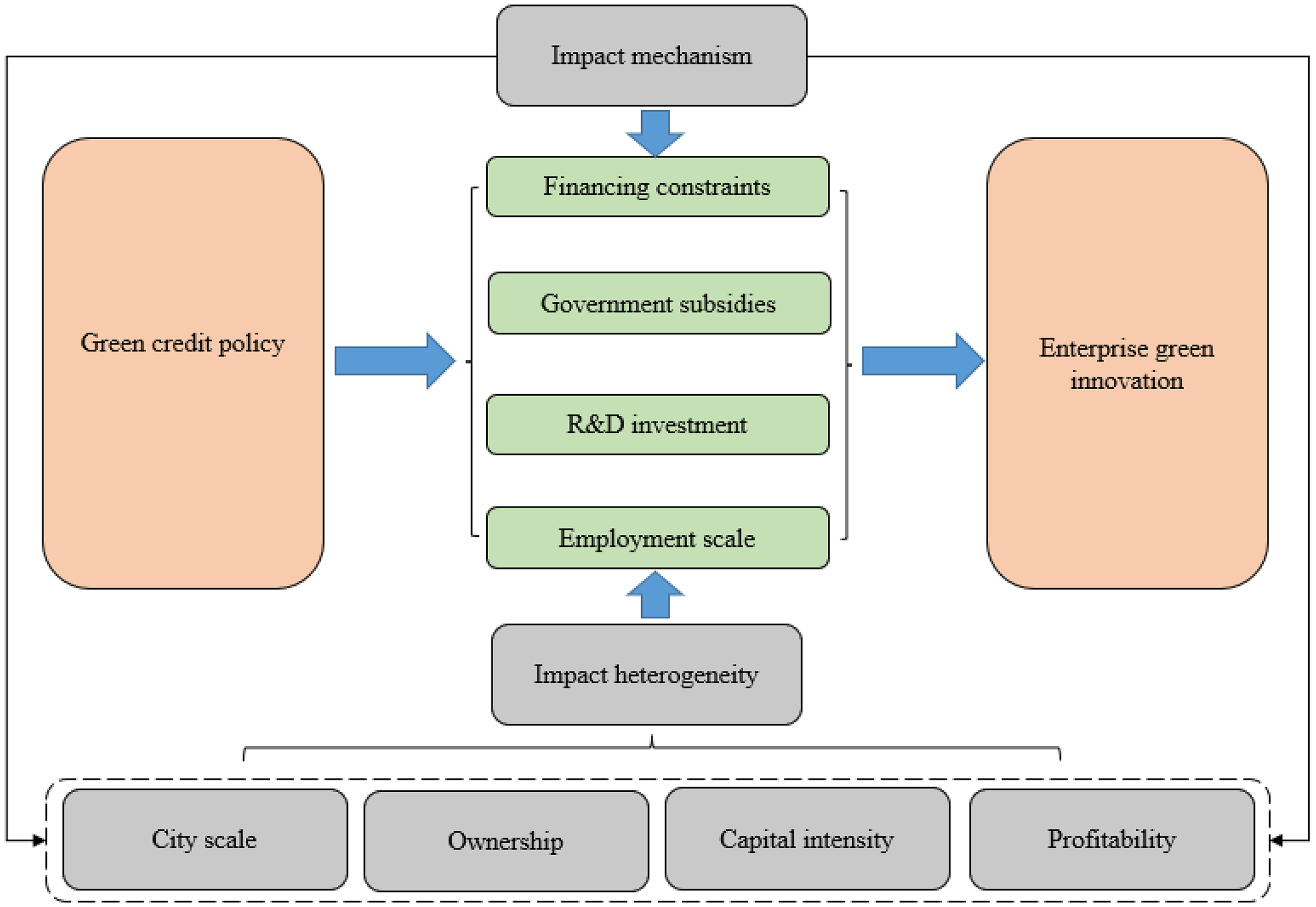

Effect mechanism analysis

This study interprets the effect mechanism of the GCP in terms of credit facilities, government subsidies, R&D investments, and employment. We argue that owing to GCP constraints, high-pollution industries may gradually reduce their expenditures on R&D funding and labor employment. Second, when affected by various environmental regulation constraints, firms may consider an apparent green transition by allocating more funds to SGI.

First, we verified whether the GCP limits capital access to heavy polluters through credit constraints. Specifically, we considered two aspects: financing constraints and government subsidies. The simulated annealing indices were adopted to capture corporate financing constraints. Column (1) of Table 10 shows that the GCP significantly increases the financing constraints of firms. The regression results in Column (2) show that firms in high-pollution industries receive significantly fewer government subsidies after the implementation of the GCP. For a relatively long duration, government subsidies were based primarily on the number of patents instead of their quality, which prompted enterprises to pursue SGI with low costs and high returns, instead of EGI with large investments and long reporting cycles.

Mechanism analysis results.

Note: *p < 0.1, **p < 0.05, ***p < 0.01.

Second, we analyzed the “crowding-out effect” of the GCP on heavy polluters from the perspective of R&D. Column (3) shows a negative coefficient (pollution_post) at the 1% level, thus demonstrating that the implementation of the GCP aggravated credit constraints on heavy polluters and reduced the necessary R&D investments. Finally, we examined the cost effects of enterprises from the perspective of employment size. Column (4) shows that highly polluting firms reduced their number of employees significantly after the policy was implemented. This suggests that highly polluting firms reduce the adverse effect of credit restrictions by reducing the employment scale, which consequently adversely affects their EGI. A graphical representation of all regression results is shown in Figure 2.

Graphical presentation of regression results.

Conclusion and policy recommendations

In this study, the driving forces and constraints of enterprise GI under the effect of the GCP were examined. The empirical results showed that the GCP imposed a crowding-out effect on EGI and a resource-misallocation effect on SGI. The GCP inhibits enterprise EGI, which is mainly attributed to the fact that the GCP increases financing constraints and reduces government financial subsidies, R&D investment, and employment labor. Furthermore, GCPs reallocate the R&D resources of firms, thus prompting firms to shift to SGI activities to avoid environmental regulations and seek government subsidies. The GI of heavy polluters exhibited the “bad money replacing good money” phenomenon. Suggestions to accelerate the GI of heavy polluters through green finance policy incentives were proposed in this study.

First, we established a robust GCP and strengthened the implementation of environmental policies. The government should establish more precise GCPs, comprehensive risk compensation, and an incentive mechanism for green loans. To promote GI among heavy polluters, the government should introduce R&D funding and innovation incentive policies such that large-scale energy-saving and near-zero carbon demonstration projects can be realized.

Second, in terms of credit authorization, financial institutions should strengthen their internal organizational capacity and risk management and improve information disclosure to provide sufficient positive guidance to enterprises under the GCP. Enterprises should strengthen information exchange with environmental protection departments and provide credit support to enterprises with R&D funding demands and green transformations. Additionally, enterprises must establish environmental information disclosure and carbon emission mechanisms. When implementing green financial policies, financial institutions should adopt lenient financing policies to improve energy efficiency, reduce carbon emissions, and combat environmental pollution. The combination of technological innovation and GI can diversify the green financial product supply, thus resulting in the green transformation of the manufacturing industry.

Third, achieving the “double carbon” goal requires enterprises to actively implement green transformation and low carbon transformations. Enterprises should balance between social responsibility and economic benefits as well as accelerate technological transformation, management transformation, development transformation in procurement and production, and functional management. Moreover, enterprises should not only focus on environmental risks but also on technological innovation initiatives and actively invest green credit funds in enterprise R&D to pursue industrial transformation. Additionally, technology R&D should avoid overreliance on bank loans, introduce venture capital funds, fully utilize the capital market, and expand financing channels.

In this study, the effect path of green finance on GI was analyzed from five perspectives. However, green finance may affect green technological innovation through other channels (e.g., capital mismatch efficiency and resource mismatch). Therefore, the effect mechanisms between these channels must be investigated in future studies. In addition, we used green financial policies as a quasi-natural experiment for empirical analysis and disregarded the specific measures of green financial indicators. In general, a green financial system includes green credit, securities, investment, insurance, and carbon finance. Therefore, a comprehensive measurement of green finance indicators will enrich investigations pertaining to green finance. Thus, we conclude that green financial development reduces GI. However, green finance in China is still in the early development stage, and as the government introduces more green finance policies, their relationship with GI must be further verified to obtain more convincing conclusions.

Footnotes

Abbreviations

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Key Projects of the National Social Science Foundation of China (21AJL009), Fujian Innovation Strategy Research Project (2022R0050), Fujian Social Science Youth Foundation (FJ2022C094), Funding for the National First-Class Undergraduate Majors Construction Sites (Economics, C166136), and Project of Research Start-up Foundation of Jimei University (Q202209).

Author biographies

Tao Lin is an associate professor in School of Finance and Economics, Jimei University, China. His main research focus on the green finance, green transformation, sustainability, was well as the trade and foreign investment.

Wanwan Wu is a student in School of Finance and Economics, Jimei University, China. Her research interests include industrial economic theory economics and economic policy.

Mingyue Du is a PhD student on economics at School of Economics, Beijing Technology and Business University, China. She has published some articles in international journals on resident consumption, industrial transformation, labor economics, eco-investment and environmental governance.

Siyu Ren is a PhD student on economics at School of Economics, Nankai University, China. His research interests include energy economics, energy policy, applied energy, energy efficiency, green finance, energy finance.

Yangping Huang is a professor in School of Finance and Economics, Jimei University, China. His main research focus on the macroeconomic policies, labor economics, industrial organization, was well as the digital economy.

Javier Cifuentes-Faura is professor in Faculty of Economics and Business, University of Murcia, Spain. He has published many papers on green development, industrial transformation, and renewable energy consumption.