Abstract

The centrality of home equity to the balance sheets of American households, and the oppressive legacy of racial exclusion from mortgage markets, compel the design of intentionally anti-racist housing policy capable of building lasting wealth for Black families. In this study, we compare the home-mortgage terms offered to middle-income Whites in the New Deal era, with a contemporary New York City policy offered in formerly redlined districts. The city's Housing Development Fund Corporation policy is for limited-income households but does not limit down payments nor qualify for federal home loans. Using mined listing data and the 2017 Panel Study of Income Dynamics, we find more than 80% of income-eligible urban Black households lack the wealth to purchase the median listing, versus 51% of Whites. Moreover, the policy's market exclusions preclude access to what is now substantial accumulated equity. Unit owners face wide-scale housing-code violations and property seizure, highlighting the limitations of “limited equity” ownership, which counteracts wealth creation. We draw two primary lessons. First, anti-racist policy cannot demand substantial financial assets. Second, financing schemes for building improvement or climate-responsive adaptation, in addition to initial purchase, should be well-tailored to family budgets and designed to deliver equity to the formerly excluded.

Introduction

Federal housing policy in the twentieth century expanded homeownership to lower- and middle-income White families, largely for the first time, while explicitly excluding Black families from the same opportunity. Home equity continues to comprise a majority of these White households’ wealth, while their Black counterparts continue to lack a comparable stock of assets, despite the excision of explicit racism from federal housing policies in the 1960s. This paper traces the evolution from that era to today, through the lens of a low-income homeownership policy instituted in the city of New York during the aftermath of redlining. We evaluate the limitations of this program's “limited equity” approach in contrast to preceding policies designed to maximize equity for White families.

For most Americans, especially lower- and middle-income Americans, the lion's share of household wealth is held in home equity. Among households below the median, approximately 75% of net worth is held in home equity. 1 As this paper will outline, the federal government expanded the population for whom home equity could serve as an avenue for wealth building by encouraging the design of home mortgage terms built around the means of middle-income families and by promising to back banks that expanded into this frontier. The National Housing Act of 1934 created the Federal Housing Administration (FHA) and instituted the 20- to 30-year home mortgages we see today. The legislation was hugely successful—resulting in lasting wealth for future generations of American families. This policy formed a pillar of the New Deal, the collection of Depression-era economic relief and recovery policies enacted by President Franklin D. Roosevelt.

Despite the immense success of federally insured mortgages among families who were able to make use of them, the FHA's mortgage underwriting practices of the 1930s and 1940s were explicitly racially exclusionary. As a result, the practices’ legacy of generational wealth is highly racialized. As of the end of 2019, 74% of white American households owned their homes, while only 44% of Black American households did (FRED St. Louis Fed 2022). The median white family has approximately 10 times the wealth of the median Black family—much of it held in housing.

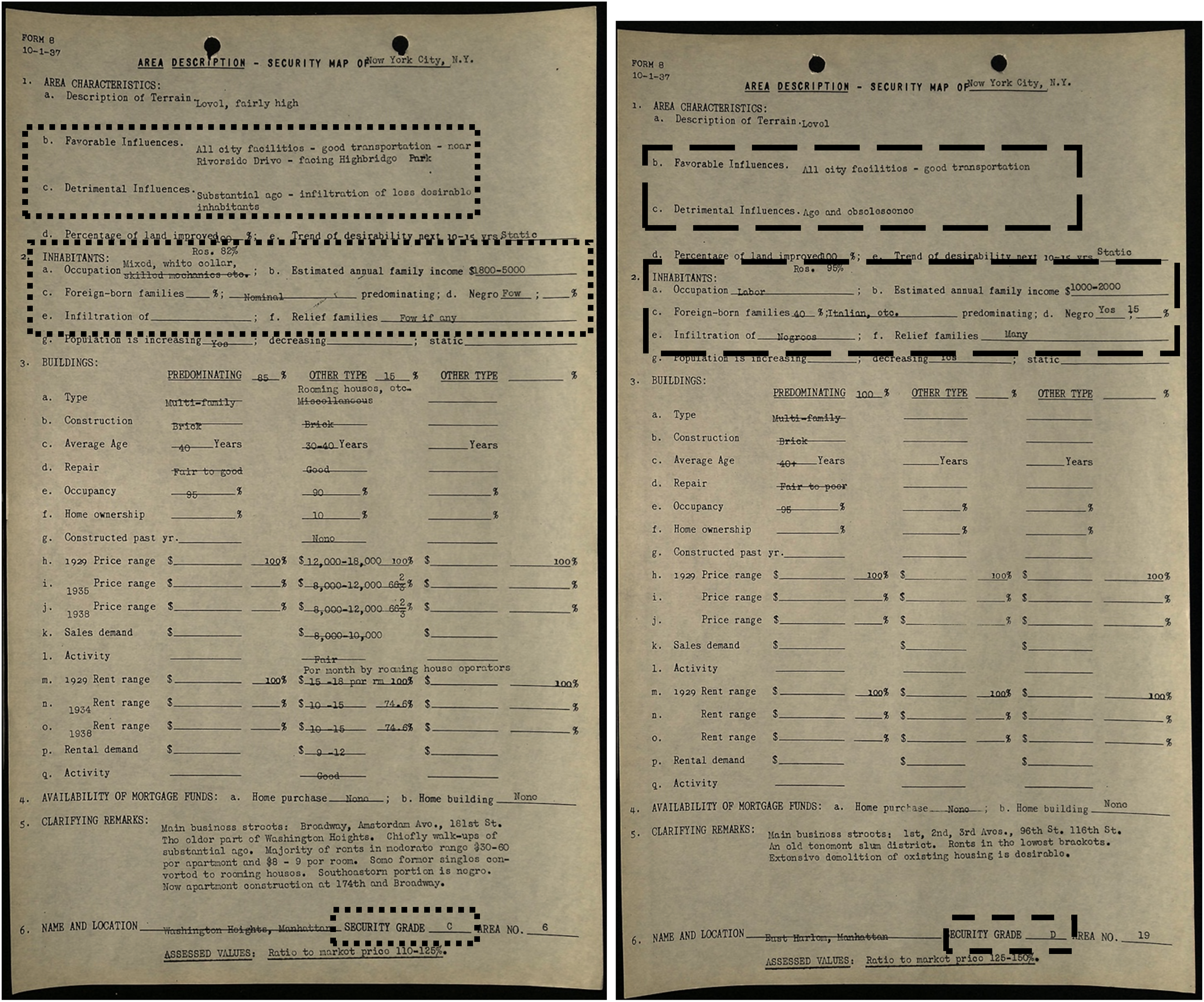

The original instrument of racial exclusion in federal housing policy was called redlining. During the New Deal–era of the 1930s and 1940s, this process of racial exclusion was highly formalized: Federal housing authorities used four colors to delineate a neighborhood's desirability as a function of residents’ race (see Figures 1 and 2). Federal bureaucrats would appraise neighborhoods, noting the percent “Negro” and infiltration of any other non-white inhabitants, and encircling majority non-white or integrating areas in red, to denote a “hazardous” area, or in yellow to designate the area as “definitely declining” (Robert Nelson et al. n.d.; Figures 1 and 2). The practice was seemingly crude and banal, due to its imprecise measures and highly bureaucratic process, but was nonetheless effective in maintaining residential segregation.

Examples onf federal housing administration forms describing “declining” and “Hazardous” areas. Note. Documents developed by the federal government's Home Owners’ Loan Corporation (HOLC) describing demographic characteristics of two neighborhoods in northern Manhattan. Based on these characteristics, most notably the racial composition of the population, neighborhoods were assigned security grades and outlined in corresponding colors on HOLC's “Residential Security Maps.” Provided by the University of Richmond Mapping Inequality project (Robert Nelson et al. n.d.). (Highlighted boxes added to show the neighborhood influences and inhabitant characteristics leading to the final determination of Security Grade.).

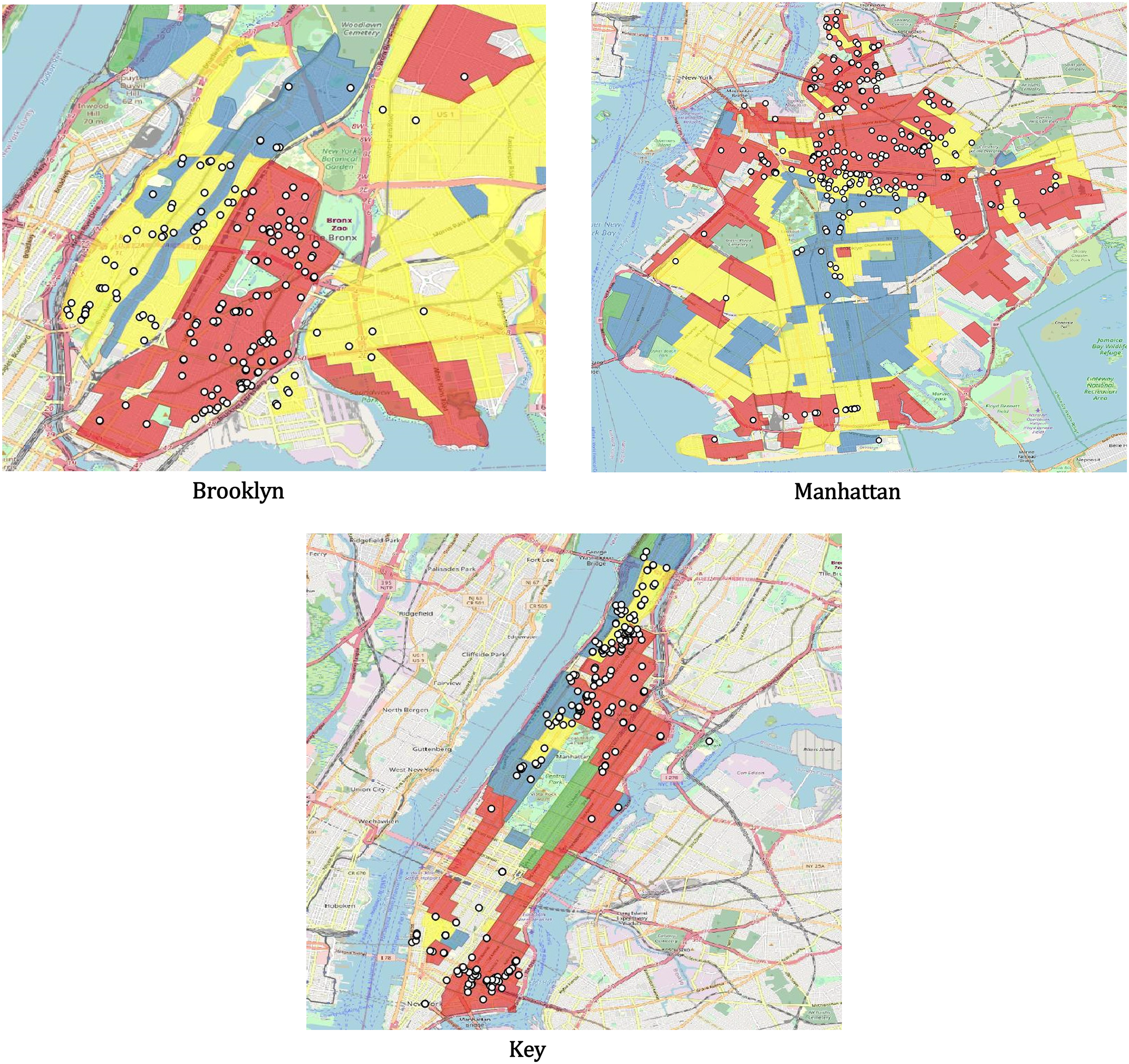

Federal housing administration districts and housing development fund corporation co-op locations. Note. These maps show the overlap of the FHA's neighborhood grading system for three New York City boroughs with HDFC locations. As depicted, HDFC units were largely concentrated in the yellow (“definitely declining”) and red (“hazardous”) zones. Maps were created by Timothy Gilman using data on HDFC addresses from ACRIS and Home Owners’ Loan Corporation neighborhood grades from the University of Richmond Mapping Inequality project (Robert Nelson et al. n.d.).

The Fair Housing Act of 1968 marked the official end of redlining, but real estate segregation lived on. Exclusionary lending practices became less conspicuous but remained persistent, as did the racism and profit motives underlying real estate segregation. After the end of redlining, and in the wake of the Great Migration of Black Americans, urban centers nationwide lost wealthy residents who fled to racially homogenous suburban developments, home equity intact (Boustan, 2010). These urban centers fell into disrepair, leaving the abandoned buildings in the custody of cities with already overextended budgets and leaving remaining inhabitants with the safety hazards of neglected buildings.

This paper connects the dots from that era to today. It explores a limited-income homeownership policy in New York City that grew out of the aftermath of redlining, and draws lessons for the contemporary design of intentional anti-racist housing policy that can redress past harm. Like many urban centers in the 1970s, New York City had its share of abandoned buildings, which were disproportionately located in segregated, formerly redlined districts from which the middle class had fled. One way New York dealt with its abandoned buildings was through a policy that allowed the remaining tenants to form limited-equity co-operatives called Housing Development Fund Corporations (HDFCs). HDFCs operate under the purview of a local nonprofit, then transition to the joint ownership of the tenants. Under the policy, low- and middle-income households could collectively purchase their abandoned apartment building at a low price, and if a household eventually decided to sell their unit, would do so at restricted prices to other low-income buyers. The goal was to build (limited) equity for the tenants of the abandoned buildings, while also creating affordable housing in perpetuity for disinvested communities.

Today, however, HDFCs’ combination of equity restrictions, income rules, and limited mortgage options prevent the program from achieving its intended purpose of true affordability. We estimate that buyers must pay $93,000 as a down payment but cannot earn more than $95,520 in income annually to purchase the median-priced home under this policy. We also find that the impacts of these financing terms are racially disparate. More than three-quarters of income-eligible Black households will not have the wealth for such a down payment, according to our estimate, compared with about 4 in 10 white households. This asset-centric design negates the purpose of HDFCs—to help historically disadvantaged families build home equity—though the policy itself is ostensibly colorblind. Indeed, one local real estate law expert with whom we spoke referred to the program as the “trust fund baby housing act” (Roberts, Esq. 2020).

What's more, the income- and price-restricted structure of the policy limits the equity that co-op owners can retain for themselves and their families or that they can access for repairs. Over time, as residents have lacked the capital to keep up with maintenance investments, thousands of apartment units have been seized by the city and sold to third parties to pay off taxes and to pay down debts for repair and maintenance, once again failing to build housing wealth for the formerly redlined co-op owners.

This paper highlights key lessons for anti-racist home financing policies moving forward. First, programs to expand homeownership cannot expect purchasers to bring large quantities of financial assets to the table, an approach that effectively excludes Black participation. The New Deal–era FHA that expanded homeownership to lower-income white Americans targeted down payment levels of as little as 5% of the buyer's annual income (Taylor 2019, 33–34), a figure far more attainable than the 97% of annual income mandated in today's New York City co-op policy.

Second, an intentional policy design should ensure adequate funding for home repairs and improvements, which will not naturally emerge when low-income households retain limited equity. Historically, white working-class families were more likely to move into homes in new developments, so once a home needed repairs, its owners had had time to build up equity. Today, many new homeowners will purchase existing homes with maintenance needs, such as repairs to boiler rooms, pipes, and building facades. In urban centers in particular, the housing stock tends to be older and in need of more intensive investment. Financing schemes for both the initial purchase and for physical improvements should be well-tailored to family budgets and designed to deliver equity over the long term. Future investments in housing, for example, to adapt housing stock to changing climate needs, can be designed to intentionally build equity that is retained by the household (Hendricks et al. 2021).

The following section discusses ways in which wealth and homeownership are important for household financial stability and how federal agencies in the twentieth century established a pathway to home equity for white middle- and low-income families—but not Black families. Next, we describe the goal and the design of the New York City co-op policy, and its overlap with the legacy of New Deal–era redlining. We present evidence mined from real estate listings showing the income restrictions and required down payments for co-op purchases, relative to a typical family's budget. We find that the New York City co-op policy is racially exclusionary due to the demands it places on buyers to have modest income and substantial assets. Finally, we conclude with lessons for building anti-racist policy, including designing parameters (like down payment assistance) around the capacity of low-income and Black residents and designing municipal actions that funnel federal dollars and infrastructure support to historically excluded communities.

Background

Wealth is a key driver of a family's financial stability. For most American families, homeownership is the primary route to building wealth. Unlike the income used to meet immediate needs, wealth enables households to plan for and invest in major life decisions, like moving to a new city, continuing higher education, or starting a business (Braga et al. 2017). The role that wealth plays in households’ financial wellbeing has grown in importance as real wages have been outpaced by expenses like housing and education (Emmons and Ricketts 2015; FRED St. Louis Fed 2019; 2023).

Homeownership can be a practical tool for building wealth, especially among lower- and middle-income households that lack the ability to set aside savings with each paycheck. Housing already constitutes a major component of most household budgets, at one-third of households’ total spending on average. Retaining that expenditure through purchasing housing rather than renting, it can be a practical way to accumulate savings. By contrast, the next largest components of household budgets are food and transportation, and cannot be retained as savings as readily (Bureau of Labor Statistics 2020).

In addition to allowing for the retention of savings, home values tend to appreciate over the long term as real incomes rise and total land availability remains fixed. This holds true on average in both larger and smaller cities, and among Black and white homeowners. While Black homeowners often receive smaller rates of equity appreciation on average relative to their white counterparts, they nevertheless have net positive returns (Bogin, Doerner and Larson 2019; Fesselmeyer, Le and Seah 2013; Herbert, McCue and Sanchez-Moyano 2013).

This trend of long-run appreciation contains short-term volatility in prices that poses risks to households who may want to liquidate their asset at a given point in time. Still, evidence suggests these risks are not prohibitive to realizing equity gains for most householders (Goodman and Mayer 2018). For example, Wainer and Zabel (2020) find that low-income households who purchased a home in a stable market realized substantial increases to net worth, while those that bought just prior to the housing crash realized no net change in wealth over a 10-year period. Given that, 2008 to 2012 were the only years since 1940 in which home prices depreciated on average (Federal Housing Finance Agency, n.d.), purchasing an appropriately financed home offers a reasonable level of risk and an appropriate entry point for households looking to gain equity and accrue assets over time while circumventing the cost of rent (Herbert, McCue and Sanchez-Moyano 2013; Ding et al. 2011).

In addition to the wealth returns associated with homeownership, a longstanding body of economics literature examines the non-financial benefits gained both privately by the homeowner as well as by the neighborhood and community in which the household is located. Rental leases are typically defined over one year or occasionally over two or more years, while homeownership has no associated time limit. Longer tenure in one home, which is facilitated by homeownership, is tied to favorable educational and social outcomes for children (Hanushek, Kain and Rivkin 2004; Green and White 1997; Aaronson 2000). Children of low-income homeowners in urban centers have shown longer-term economic gains into adulthood than their peers in families that rent (Harkness and Newman 2002).

Beyond benefits to individual households, homeownership incentivizes the formation of stronger ties and more community investment. Homeowners are more likely to vote (Harding, Miceli and Sirmans 2000; DiPasquale and Glaeser 1999), and urban low-income homeowners show greater awareness of local politics, increased participation in community activities, and more informally bonded networks (Brisson and Usher 2007; Roskruge et al. 2013). These households report a greater sense of control and trust in their neighbors, and fewer adverse mental health outcomes than matched renters (Manturuk 2012). 2 They have a greater incentive to invest in home maintenance and beautification, which evidence suggests translates into higher home prices. Owner-occupied dwellings and neighborhoods with more owner residents appreciate in value more quickly (Coulson and Li 2013) than otherwise similar rented units. 3

Because of the importance of housing for household well-being, the large proportion of a household's budget it often accounts for, and the positive spillover effects of homeownership for society, all levels of government have been deeply involved in financing housing. Most prominently, during recovery from the Great Depression, the federal government created the Federal Housing Administration. During the 1930s and 1940s, this agency shored up a new kind of mortgage contract in which debt could be gradually and incrementally paid off over decades (a process called amortization), supplanting the volatile 5- to 10-year interest-only mortgages of the pre-FHA era. The FHA-instituted practice of amortization has continued to be the standard even into today's housing market (Federal Housing Administration 1940, 8; Rose and Snowden 2013). Additionally, under the FHA, the federal government could protect lenders against the risk that borrowers might default on their long-term amortized mortgages by insuring the loans.

As Keeanga-Yamahtta Taylor (2019) describes in her authoritative book Race for Profit, the FHA of the 1930s and 1940s challenged lenders to make homeownership possible for low-income families. An FHA leader contended that offering “reasonable terms” for home buying was a “direct responsibility of business and government,” (Taylor 2019, 33) and the federal government would be ready to assist by insuring those mortgages. In turn, lenders designed reasonable terms based on their knowledge of consumers’ expenditures. If families with annual incomes below $2,000 were buying cars and refrigerators, they should be able to buy homes, too. Lenders boasted about being able to offer terms with only $100 down and monthly mortgages equal to 15% of the buyer's income over the mortgage life.

The bulk of the federally insured mortgages did, in fact, have reasonable enough terms. In 1945, about a quarter of all FHA-insured homes were sold to households making between $2,000 and $2,500 annually, with another 6% going to families earning under $2,000 (Federal Housing Administration 1946, 85). This represents the 35th percentile of (non-farm) household income for that year (US Census Bureau 1948a, 8). These households on average would purchase a house worth four or five thousand dollars at a 10% down payment (Federal Housing Administration 1946, 24–25). In terms of their earnings, buyers put down 20% of annual income and paid 16% of monthly income over a 30-year mortgage. If the same terms were available today, this would mean that families making $42,000 could buy a home for approximately eighty thousand dollars, put $8,400 as a down payment, and pay $560 a month, including taxes and fees, to own their home. Instead, the average mortgage payment for this income group is approximately $2,000 a month according to the 2021 American Housing Survey. The chasm in affordability reflects both the increase in real housing prices relative to incomes and the inability of mortgage-assistance terms to keep apace of these market realities.

Though well-designed to bring low-income Americans into homeownership, these terms were explicitly exclusionary. The United States as a whole—not just the officially segregated South—excluded Black Americans and other non-white Americans from much of public life. The federally structured and federally backed mortgage program of the 1930s and 1940s was no different (Hannah-Jones 2020; Jackson 1980). Racism and racial segregation were explicitly and intentionally constructed through such strategies as reducing the score of a loan application if the home was in a neighborhood with racial heterogeneity, as well as entirely excluding redlined neighborhoods with substantial non-white populations (Taylor 2019).

To the architects of these “residential security” maps and the lenders that relied on them, a few non-white people living in a neighborhood was an issue, but many in one area was insurmountable. Any new non-white residents would jeopardize a neighborhood's standing with banks. Racial integration risked barring future buyers from accessing federally insured mortgages for home purchases in the neighborhood, making it difficult to sell property there and potentially forcing down home prices. The key result was that the design of federal policy predicated home values in White neighborhoods on the exclusion Black families.

Moreover, segregation was profitable. Suburban developers could sell whiteness at pure profit, whereas an extra bathroom would cost time and materials to build (Taylor 2019). Conversely, residents redlined into segregated, poor communities were—and continue to be—a captive audience for tenant exploitation (Desmond and Wilmers 2019; DuBois, Anderson and Eaton 1996). In these communities, landlords were (and still are) able to rent sub-par housing in poor condition at high prices with little threat of competition.

For those households eligible to participate (that is, white households), the newly liberalized loan amortization program of the New Deal was hugely successful. By 1960, over 60% of Americans were homeowners, up from about 44% in 1940 (“US Historical Homeownership Rate” 2014). FHA-insured mortgages are largely credited with building out the (white) middle class (Hannah-Jones 2020). But only 2% of these loans were given to non-white families (Hannah-Jones 2020), despite at least 40% of non-white households having incomes as high as $2,000 in 1945 (US Census Bureau 1948b).

While these discriminatory lending practices were solidified 80 years ago, their racialized legacy continues today. White American families have housing wealth that acts as a source of intergenerational support, while Black families reside in a stock of housing in which no program has invested at scale, the vestige of the exploitative segregated market that morphed from de jure redlining into a period of “predatory inclusion” that failed to open access to New Deal–era terms (Taylor 2019).

The next section maps out redlining and the ensuing co-op policy in New York City neighborhoods. We examine the ways in which its current financing structure, which relies on high down payments, and its insufficient planning for quality improvement acts to recreate racial disparities in housing wealth.

Case Study: New York City

New York City's Housing Development Fund Corporation (HDFC) policy grew out of the aftermath of redlining. Urban centers nationwide suffered during the post-redlining 1970s era as the tax base fled neighborhoods where integration was occurring, leaving abandoned buildings in their wake. In a 1978 study conducted by the US Comptroller General, 113 of 149 cities that responded to the survey reported having an abandonment problem (Reiss 1997; Comptroller General of the United States 1978). New York City lost 114,000 residential units between 1965 and 1968, in the early days of the crisis. The city and its advisors carefully assessed the range of landlord incentives at its disposal, primarily various levels of tax abatement and low-interest municipal loans, and concluded that the asset values of buildings, measured in rents received, needed to increase (Rydell 1970; Clapp 1976). In 1970, the city enacted a law to sunset its policy of rent control. However, the move was largely unsuccessful in preventing abandonment and outmigration: New York City lost 800,000 residents over the following decade (Chall 1983).

Although it was the well-off who were fleeing, and fleeing from the most desirable neighborhoods, residents of the poorest and most stigmatized areas suffered most from abandonment. When the wealthy fled, those for whom the most desirable neighborhoods had previously been just out of reach swooped into the now cheaper apartments in these more desirable locations. Those in the next highest economic rung filled their spots in turn, and this continued until the process filtered all the way down to the least desirable neighborhoods (Reiss 1997), which, in the US real estate market, meant the poorest and most racially segregated (Taylor 2019). Though many fled these neighborhoods, inevitably some lacked the resources to leave and got stuck with the hot potato of abandonment. Once landlords were unable to fill a building, it was often financially advantageous to recoup as much of the initial investment as possible by continuing to collect rent without investing in any maintenance or paying any taxes until the building was foreclosed. One or more abandoned buildings on a block could reduce the value of other nearby properties, ultimately pulling down entire neighborhoods as investments gradually appeared to be “financially hopeless” (Rydell 1970). Ultimately, the city foreclosed on over 100,000 abandoned apartments by 1979, making it the largest landlord in the New York market (Furman Center for Real Estate and Urban Policy 2006).

But here is where New York City diverged from other urban centers of the era. Beginning in the late 1970s, tenants in these abandoned buildings organized a social movement that, through protest and negotiation, allowed them to gain control over their buildings at affordable rates (Starecheski 2019). Though initially wary of prohibitive prices, and understandably skeptical of future real estate values, tenants organized and lobbied to ensure affordable terms when rental buildings converted to co-operative ownership (Holtzman 2017). What emerged was Article XI of New York State's Private Housing Finance Law. Under the law, the city sold derelict apartments to residents for $250 each—well below the New York City average for the decade, which was $65,000 (Miller 2012). 4 The buildings, collectively owned and operated by residents, were termed Housing Development Fund Corporations (HDFC), a nod to the former tenants’ new roles as joint shareholders. The co-ops were concentrated in non-white areas deemed in the New Deal–era to have been “declining” or “hazardous” (see Figures 1 and 2, below), which were those most vulnerable to abandonment.

For the first several years of cooperative ownership, residents would gain access to incentives similar to those designed to entice private landlords, like tax abatement and municipal loans, at the comptroller's discretion (Private Housing Finance Law 2021). The law establishing HDFCs also established a fund that would advance money to residents for immediate repairs when they assumed ownership. That fund was to be replenished by co-op residents over time and thus made available for future HDFCs (Private Housing Finance Law 2021). When residents initially sought ownership, they entered into a collective agreement with the city over the specific terms for repaying up-front building investment costs, needed to address the neglect, which usually comprised some combination of installment payments and dedicating a share of any profits realized upon resale, though each individual building's agreement varied. When agreement terms ended, residents would either continue operating the building or, in the event that they had failed to pay off investment costs in full, would enter into a new agreement to restructure remaining debts.

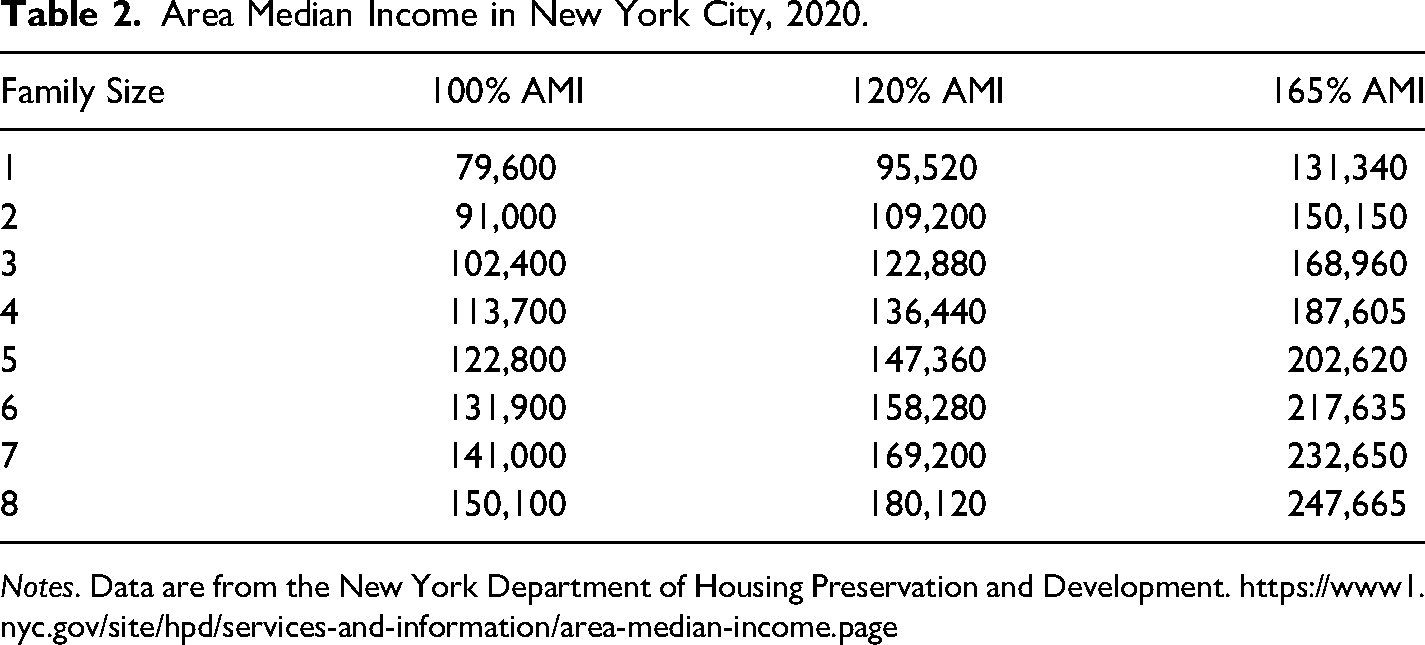

While the incentives resembled municipal tactics developed for private landlords, HDFCs were established as affordable housing, rather than as asset-building tools. At the time of purchase, all future co-op purchasers would be subject to income restrictions. Buyers could make no more than 165% of the Area Median Income ($131,340 in 2020 [New York City Department of Housing Preservation and Development n.d.]), though buildings could choose to go lower. The income limit was not heavily restrictive, given that more than half of households in the area would always be eligible under a cutoff that exceeds 100% of the area median. However, the resale restriction would apply to the building in perpetuity. These same resale restrictions, along with the majority of other HDFC regulations, currently remain in effect.

Critically, the HDFC plan set no limit on buyers’ assets nor on the down payments required for purchase, which left a gaping hole in the pathway to affordable homeownership. While monthly mortgage costs must be affordable relative to income—no more than 30% of monthly earnings—sellers can easily meet this restriction and then ask for a large down payment. Some even ask for full cash up front. In other words, low- and mid-income buyers are asked to pay tens of thousands or even hundreds of thousands of dollars in cash in order to own a supposedly “affordable” HDFC co-op.

Even among the majority of co-op sales that ask for only the standard down payment of 20% of purchase price, buyers have limited access to financing, including being barred from applying federal first-time homebuyer grants, as we enumerate in our analysis below. Though most co-ops allow for the buyer to obtain external financing for the purchase of an HDFC apartment, mainstream banks are unfamiliar with the byzantine municipal and state rules outlined in Article XI, and are wary of the limited equity imposed by resale restrictions and municipal repayment agreements. Additionally, co-operative apartment buildings, where residents own shares in a building as a whole and lease their individual apartment unit, are not eligible for federal home loans or the down payment assistance these loans offer (unlike condominiums, where each resident owns their apartment outright, which are eligible). This leaves income-limited buyers to finance mortgages without assistance on the down payment and with only a small pool of specialty banks potentially able to help—or they must find the cash themselves. By requiring a limited income, a substantial down payment, and few financing options, the HDFC policy effectively privileges intergenerational wealth, summed up by a local real estate expert who referred to the Article XI policy as the “trust fund baby housing act” (Roberts, Esq. 2020).

The next section evaluates this policy in practice by scraping the HDFC homes for sale from the housing site StreetEasy. No similar study of affordable homeownership programs has been conducted in New York or any other major U.S. city, that we are aware of. We ask: Are the homes affordable? Are they affordable for Black families? And how might a different design be more empowering?

Empirical Methods

Data

We collected the data on home prices and income restrictions from the website StreetEasy, a subsidiary of Zillow that lists homes for sale and for rent in New York City. To identify the income-limited co-operative units, we filtered for co-ops with the word “HDFC” or “income” anywhere in the unit description. We mined the search results for the listing's URL, the listing address, asking price, and textual description of the listing, including the sales pitch and any advertised financing terms. Our search returned a total of 217 active listings, spanning three New York City boroughs: 155 from Manhattan, 41 from Brooklyn, and 21 from the Bronx. We excluded listings with incomplete information on the income threshold for eligibility, which left a total of 164 listings (118 in Manhattan, 34 in Brooklyn, and 12 in the Bronx).

Price Verification

Before running analyses, we verified our sample against public records of home sales. These records report the address and sale price of each unit sold in New York City. However, because they do not report on the income restrictions or down payment terms, we removed these listings prior to conducting the final empirical analyses, as described below. The sale records were retrieved from the New York City Automated City Register Information System (ACRIS), which lists property records. We then matched ACRIS records, using their addresses, to a list of known HDFC co-op buildings compiled by the Department of Housing Preservation and Development and provided to us by the nonprofit Urban Homesteading Assistance Board (UHAB). We subset the ACRIS home-sale data to include only those matching the HDFC list of addresses.

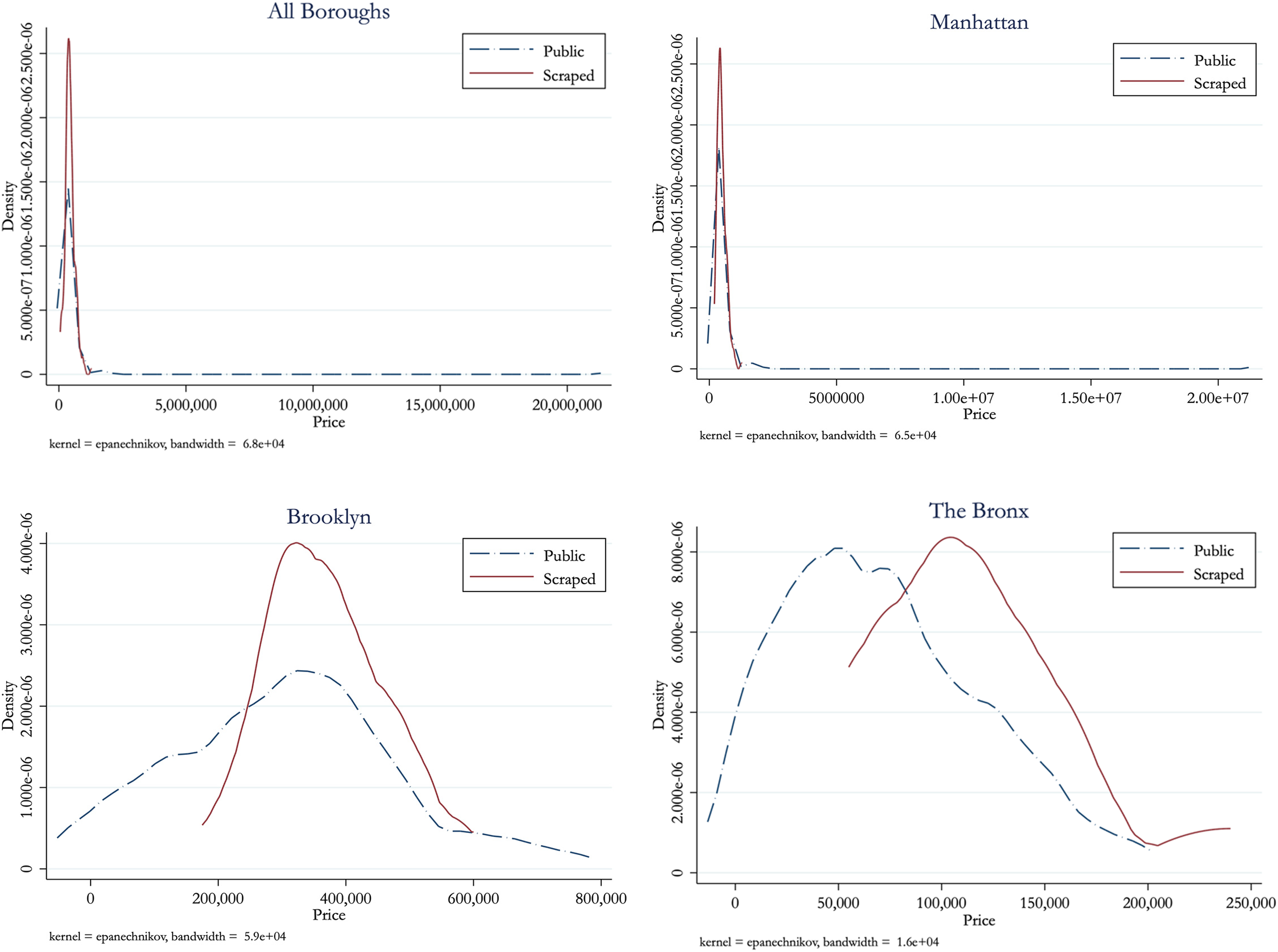

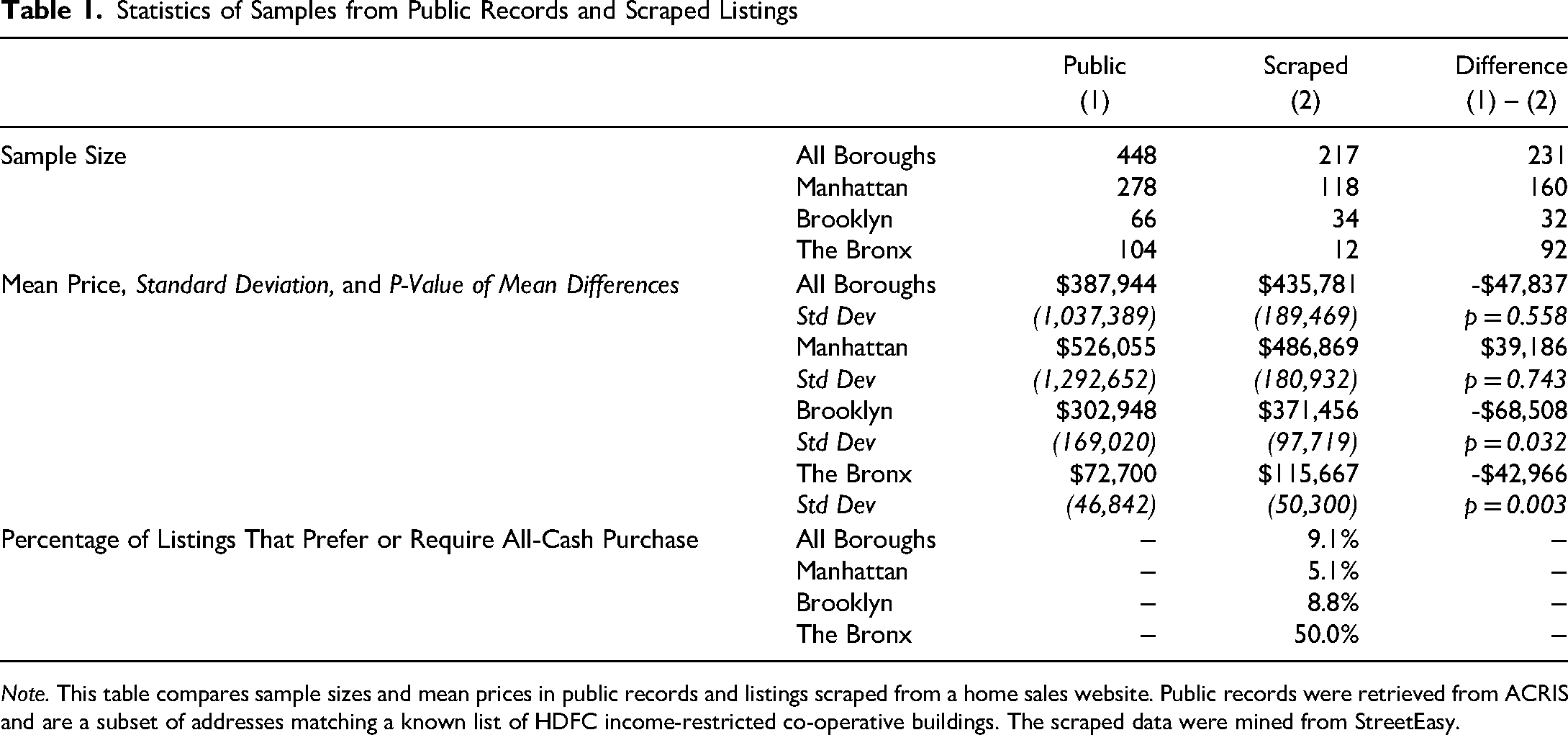

Finally, we compared the public and scraped datasets, and found that our scraped data represented only a subset of those that are publicly available. We gathered approximately half of the overall listings—roughly half in Manhattan and Brooklyn, but only 12 of 104 total listings in the Bronx. We then performed a simple t-test to assess whether the prices of our scraped listings were representative of the larger public records sample. We were unable to find a statistically significant difference in mean price between the public and scraped samples for all boroughs combined and for Manhattan (see Table 1). However, we did find significant differences in Brooklyn and in the Bronx, despite having smaller sample sizes in these two boroughs. Below, we show density plots of the price distribution by data source for each borough (see Figure 3). Means overlap in the overall and Manhattan plots. In Brooklyn, the public data distribution shows a node at a lower price—approximately $175,000—that does not appear in the scraped data. In the Bronx, the public data mean falls below the scraped mean by between $25,000 and $50,000.

Visual comparison of public and scraped data.

Statistics of Samples from Public Records and Scraped Listings

Note. This table compares sample sizes and mean prices in public records and listings scraped from a home sales website. Public records were retrieved from ACRIS and are a subset of addresses matching a known list of HDFC income-restricted co-operative buildings. The scraped data were mined from StreetEasy.

As a result, we used only the data from Manhattan for the study. A majority of listings were from Manhattan, both in our scraped sample and in the public records. Additionally, our data appear sufficiently representative within that borough. The listings in Manhattan have higher prices on average than do the listings in the other boroughs. Nevertheless, the phenomenon we describe in this study, wherein the income-restricted listings require high levels of cash contributions relative to income, does not appear to be confined to Manhattan. HDFC listings in each borough can require substantial assets at purchase. For example, the final panel of Table 1 shows that approximately 5% of scraped listings in Manhattan mentioned that the seller either requires or prefers a full cash purchase; the same is true for 9% of listings in Brooklyn and 50% in the Bronx. These listings thus require low-income households to put down tens or even hundreds of thousands of dollars or more to purchase one of these units. Because we used only samples from Manhattan, we do not conclude that listings in other boroughs are definitively more likely to require a cash deal. However, the evidence also does not suggest that the practice is more likely in Manhattan.

Income Restrictions

Using our sample of 118 scraped Manhattan listings, we manually identified and then standardized the income restrictions from within the text descriptions. While the city requires some income limit be set, and imposes a cap at 165% of the area median income (AMI), each building can set a lower limit. Table 2 below lists the income amounts in dollars associated with % AMI benchmarks by family size.

Area Median Income in New York City, 2020.

Notes. Data are from the New York Department of Housing Preservation and Development. https://www1.nyc.gov/site/hpd/services-and-information/area-median-income.page

Difference Between Assumed and Reported Down Payment.

This table shows differences between the down payment noted in the listing, available for only 27 of the 118 Manhattan listings, and the down payment assumed in this study (20% of asking price) as well as other alternative down payment assumptions we could have made (25% or 15%). The difference is reported as assumed minus noted, and is thus a positive number when the assumption is larger than the noted amount on average.

To find income-restricted listings, we searched for the terms “income” and “AMI” in the website's listing description, then manually checked each listing URL to verify. We then standardized listings to show the income restrictions as a percent of AMI. For example, if a listing imposed an income limit of $79,600 for a single adult or $131,340 for two, we converted both to 100% AMI in our data.

Down Payments

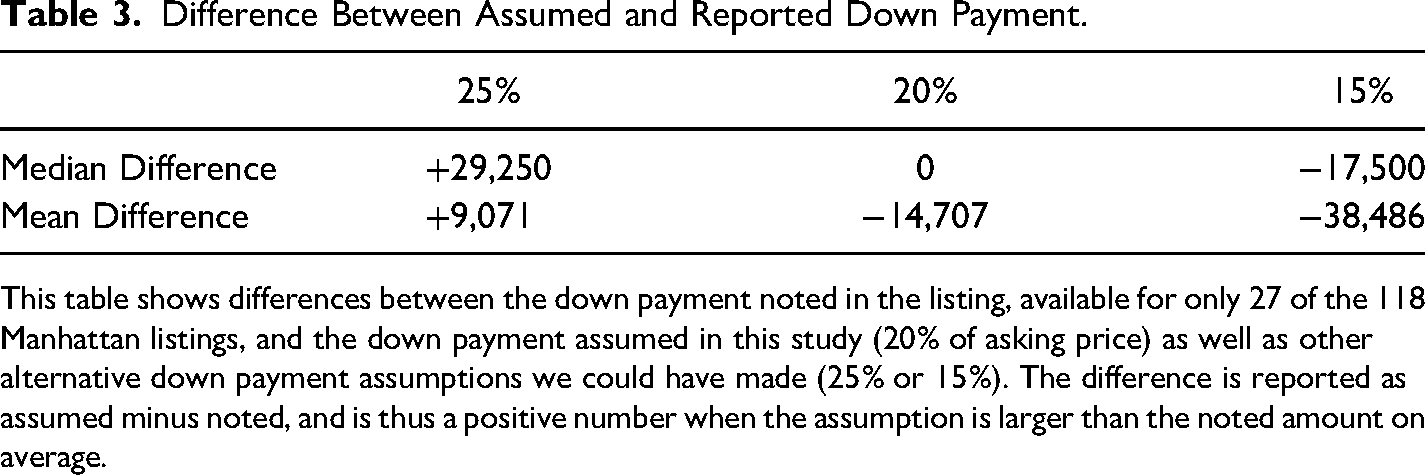

We similarly identified listing-specific down payment requirements from the description text. However, most listings (77%) did not specify a required down payment. We assumed a down payment of 20% and validated the assumption in two ways. First, we asked several experts on NYC real estate 5 , and examined available documentation. Each expert suggested a 20% down payment would be standard. Next, we compared our assumption to the actual down payments required in those listings that specify an amount and found that the 20% assumption was closest to the listed down payment. When we assumed a 20% down payment, we found a $0 difference at the median between that assumed amount and the actual down payment where noted. We found a mean difference of -$14,707, which suggests that our assumption was approximately $15,000 lower than the listed down payment at the mean. By comparison, the 25% assumption appears too high with a median difference of +$29,250 and a mean difference of +$9,071, and the 15% assumption appears too low, with the median difference of -$17,500 and a mean difference of -$38,486. Given some form of error with any assumption, we selected 20%, which aligned with expert advice, had a $0 median difference, and appears to slightly understate the mean difference and thus will not overstate the down payment required.

Home Financing

Black Families’ Exclusion from Entry into HDFCs

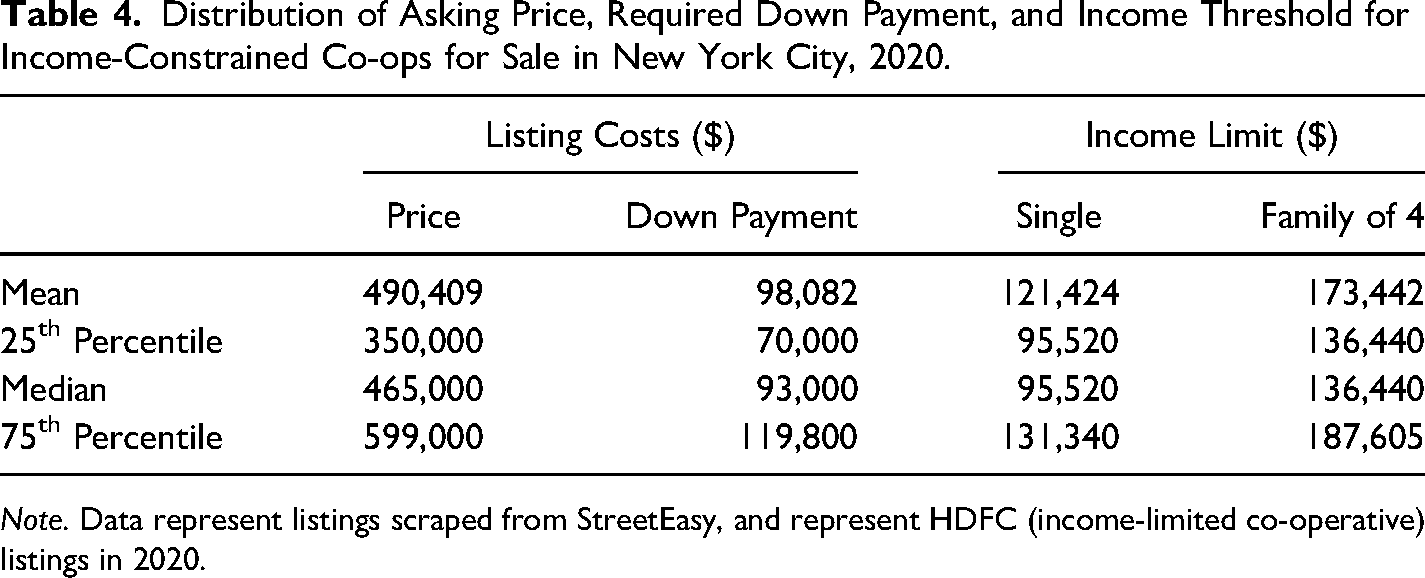

Among the homes for sale in Manhattan through this income-limited New York City policy, the median price was $465,000, shown below in Table 4. This amount is somewhat higher than the median home price in the United States for 2020 ($333,975) (US Census Bureau and US Department of Housing and Urban Development 2021), but much lower than the median for Manhattan ($999,000 in 2018 [Vasquez 2019]).

Distribution of Asking Price, Required Down Payment, and Income Threshold for Income-Constrained Co-ops for Sale in New York City, 2020.

Note. Data represent listings scraped from StreetEasy, and represent HDFC (income-limited co-operative) listings in 2020.

In order to be eligible to purchase one of these “affordable” homes, a buyer cannot make more than the income limit. These vary somewhat, as co-op boards are allowed to set lower income limits. Few go below 120% of the area median, or $95,520 for a single adult, which is both the median and 25th percentile income requirement. Other co-ops exceed that amount, up to $131,340 at the 75th percentile, which represents the maximum allotment of 165% of Area Median Income. These amounts translate to between $136,440 and $187,605 of income allowed for families with four persons. In effect, the co-ops function as middle-income, rather than low-income, housing.

More striking, at the median, a buyer would have to put down $92,900 in order to purchase a unit in one of these income-constrained co-operative buildings in 2020. What's more, the $70,000 down payment at the 25th percentile indicates that while 25% of the listings have down payments below that amount, 75% of listings require more than a $70,000 down payment to make the purchase. Unlike its income and mortgage payment rules, the HDFC policy puts no limit on buyers’ assets or on the required down payment.

The required down payments nearly reach the level of income allowed (Table 3). For example, at the median, income cannot exceed $95,520 for a single adult, while the down payment reaches $93,000. By contrast, the New Deal–era FHA, which was designed to bring white working-class families into homeownership, afforded its lower-income homebuyers a down payment at 20% of annual household income. Here, the down payment reaches approximately 97% of annual income at the median.

Given the racial disparity in wealth, which holds across different levels of income, we anticipate that Black families who are income-eligible, whose earnings do not exceed the income limit, may be less likely to have the assets to meet the down payment required to buy into this homeownership policy. To examine this, we compared listing prices and down payments to publicly available data on the household incomes and wealth of city dwellers by race. We assessed whether households in the 2017 Panel Study of Income Dynamics who live in a metropolitan area and who fall below the income threshold for a given listing would have the assets needed to make the down payment. 6 To be generous in our interpretation, we allowed any form of asset to be used to contribute to the down payment, including, for example, retirement accounts and vehicle equity, which in theory could all be liquidated.

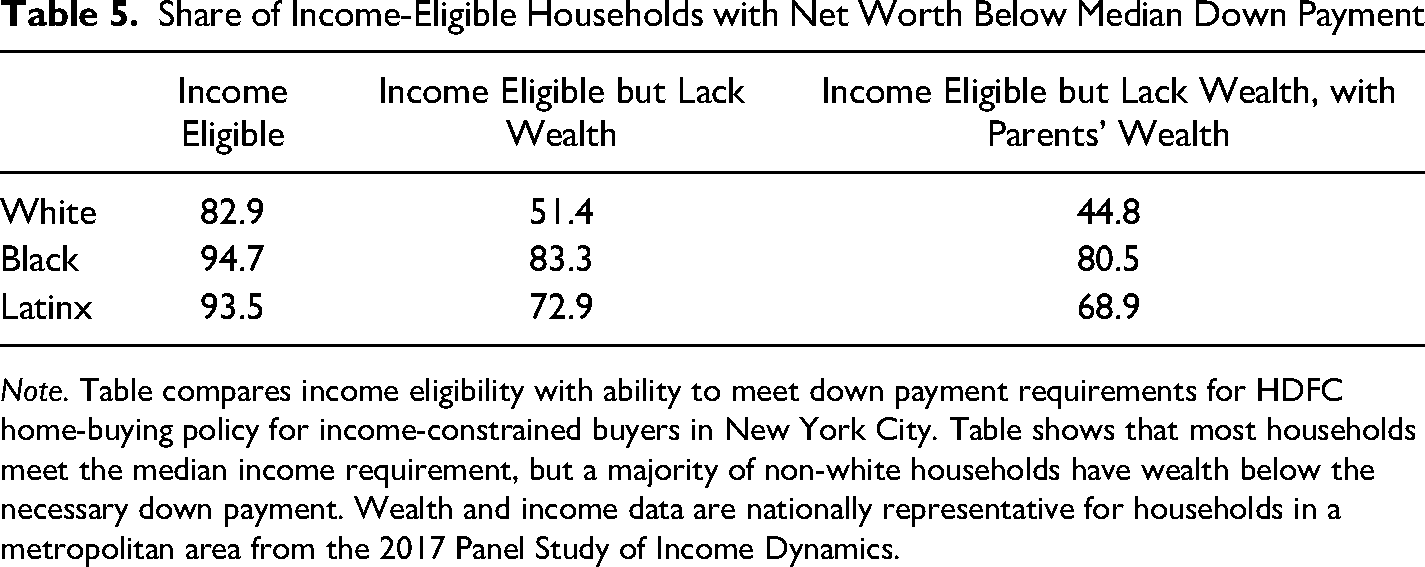

As suspected, we find that Black families are the most likely to be excluded from purchasing an HDFC co-op due to down payments in excess of household net worth. The down payments of HDFC co-op listings exceed the total net worth of 83% of income-eligible Black families in US cities (Table 5). More than 7 in 10 Latinx households will be excluded from participation on the basis of wealth. By comparison, just over half of income-eligible white families will lack the wealth needed to buy a co-op apartment.

Share of Income-Eligible Households with Net Worth Below Median Down Payment

Note. Table compares income eligibility with ability to meet down payment requirements for HDFC home-buying policy for income-constrained buyers in New York City. Table shows that most households meet the median income requirement, but a majority of non-white households have wealth below the necessary down payment. Wealth and income data are nationally representative for households in a metropolitan area from the 2017 Panel Study of Income Dynamics.

Given the potential for disparate access to parental financial support through monetary gifting and other forms of intergenerational financial assistance (Charles and Hurst 2002), we additionally examine disparities after accounting for parental wealth. We sum the value of assets held by the household's living parents and the value of assets held by the household itself, and reassess whether families are then able to meet the down payment requirements. To find parental wealth, we first obtain identifiers of the biological and adoptive mother and father of each sample member; find the wealth of mothers and fathers; remove one parent if within the same household to avoid duplication; then merge the parents’ wealth value back on to sample members.

We find a small change in the expected direction (Table 5). Six additional percentage points of white families become able to afford one of the HDFC co-op units, making a majority of income-eligible white people capable of participating. But only 3% points of Black households are pushed over the edge by parental wealth. Even incorporating parental assets, 80.5% of listings for which Black families are income-eligible will still exclude them from participating on the basis of down payment, while only 44.8% of listings for which white families are income-eligible will require down payments that are prohibitively expensive to the family.

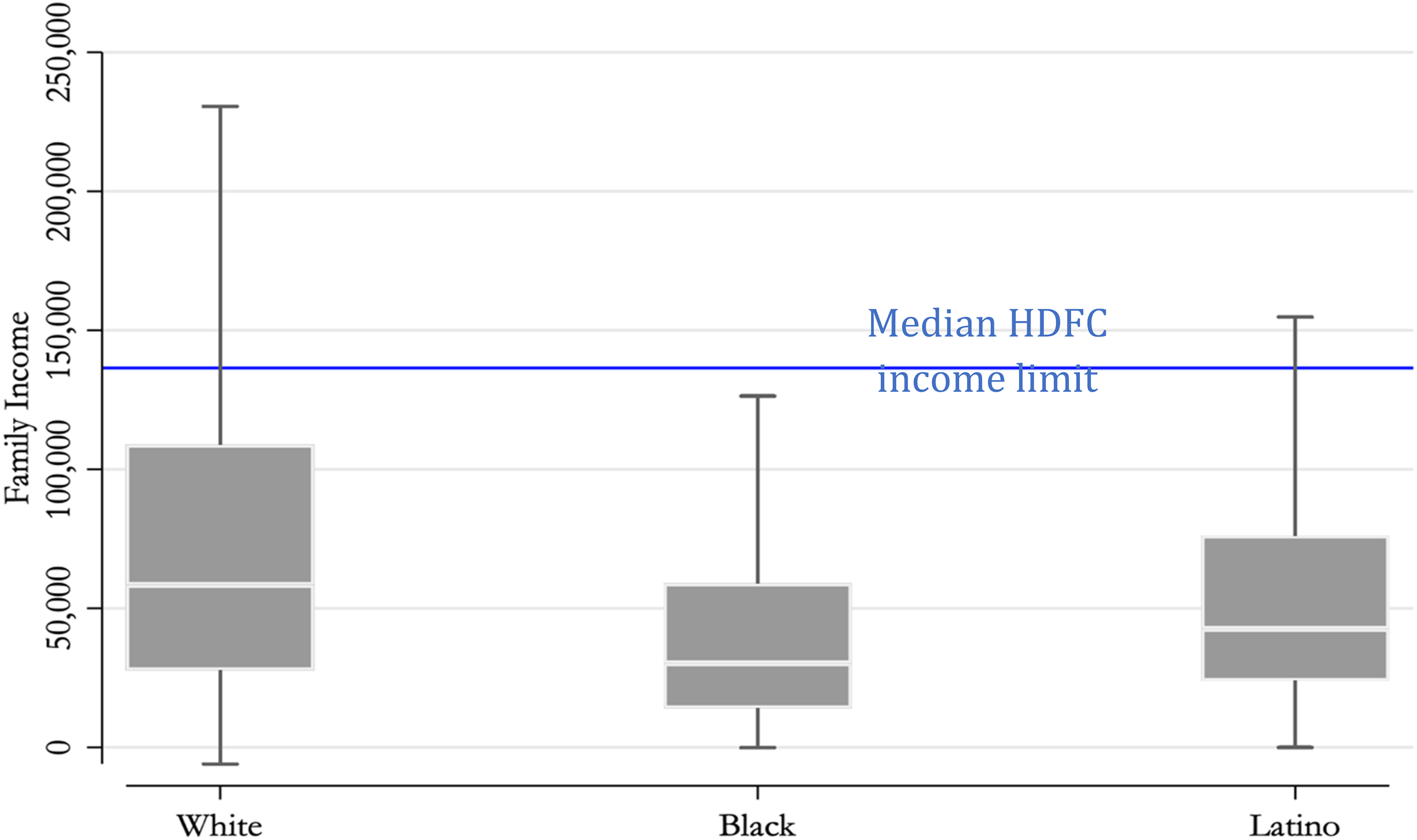

The figures below illustrate these findings. As shown in Figure 4 a majority of households meet the income eligibility threshold for the median HDFC listing. Nearly every Black family has income below the maximum allowed, as do a substantial majority of Latinx and white households. For all three groups, the 75th percentile of the income distribution, illustrated by the top of the shaded gray box, falls below the median income threshold. This means that at least 75% of the population has income below the constrained level imposed by the policy, reflecting the way in which the policy functions more effectively as middle- rather than low-income housing. This contrasts with New Deal–era FHA-insured mortgages, which were designed for lower-income households, specifically those at 35th percentile of the income distribution.

Income distribution of US households versus median income threshold. Note. HDFC purchasers must have income below the limit, with the median shown in Figure 4, and a net worth above the down payment, also shown at the median in Figure 5. While income eligibility is common for all races, net worth is particularly unlikely to lie above the median down payment line for Black and Latinx American households. Data on HDFC income restrictions and down payments are scraped from Street Easy for HDFC listings in 2020. Household income and wealth are nationally representative of households in a metropolitan area from the 2017 Panel Study of Income Dynamics.

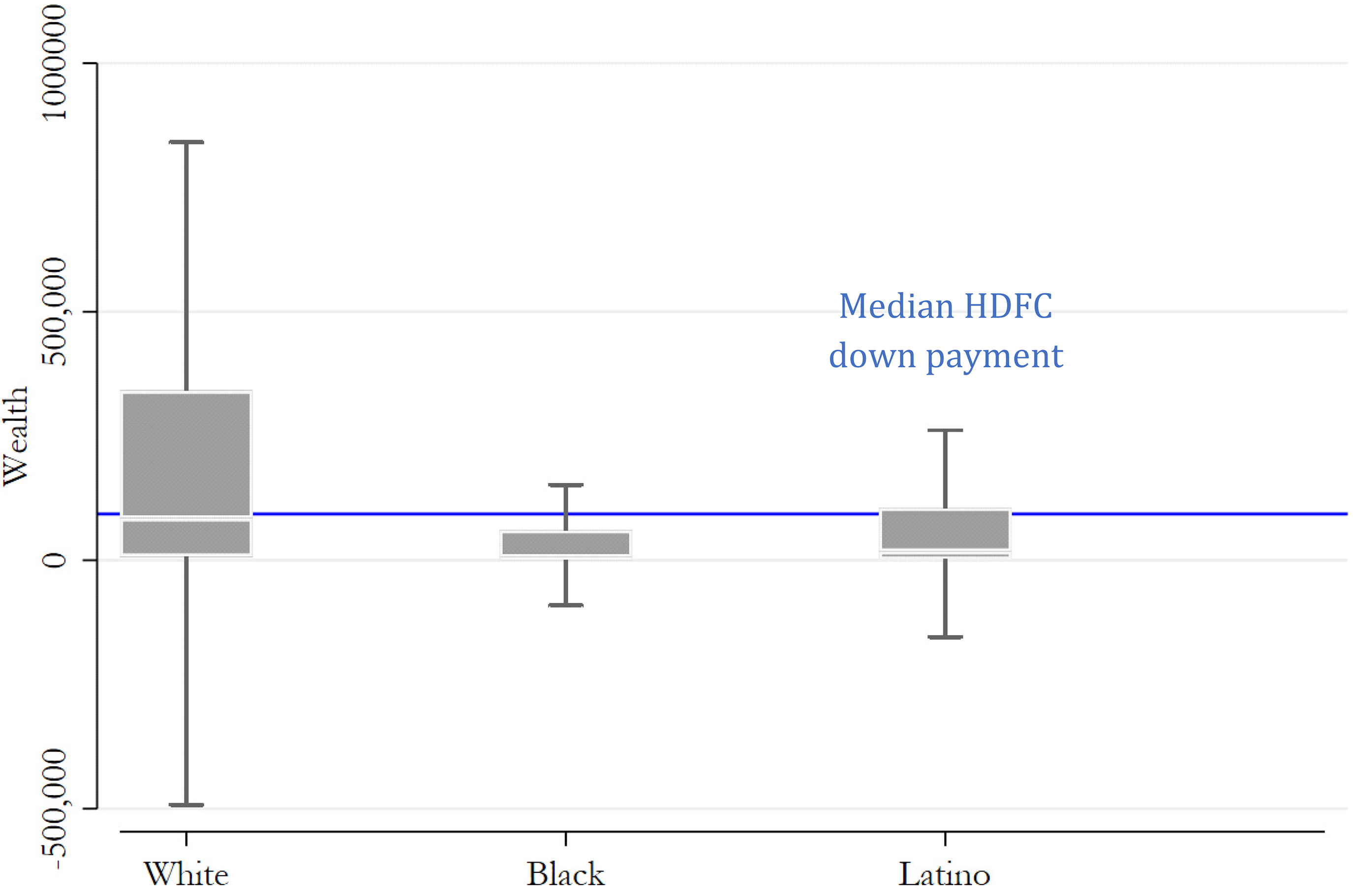

In order to purchase one of these homes, a household's income must therefore fall below the income threshold (most do), while at the same time its wealth must exceed the needed down payment. As shown in Figure 5, very few Black families have the wealth that HDFCs require. The median listing, again, in a policy considered a pathway to affordable homeownership for formerly redlined communities, requires families to have $93,000 in cash to put down on the purchase, thereby excluding the vast majority of non-white families from Article XI's purview without ever referencing their race.

Wealth distribution of income-eligible households versus median down payment. Note. HDFC purchasers must have income below the limit, with the median shown in Figure 4, and a net worth above the down payment, also shown at the median in Figure 5. While income eligibility is common for all races, net worth is particularly unlikely to lie above the median down payment line for Black and Latinx American households. Data on HDFC income restrictions and down payments are scraped from Street Easy for HDFC listings in 2020. Household income and wealth are nationally representative of households in a metropolitan area from the 2017 Panel Study of Income Dynamics.

Maintenance Challenges

The HDFC housing policy started in response to the problem of abandoned and unmaintained apartment buildings—those left in disrepair by owners who had stopped investing in ongoing maintenance. After federal funds for home buying went almost exclusively to white families in segregated neighborhoods in the early twentieth century, formerly redlined residents were left with blighted buildings, safety hazards, and infrastructure sorely in need of habitability investment.

However, the co-op ownership policy left the issue of habitability largely unresolved. The state has made available a sum of funds from which HDFCs could draw, which would be replenished by ongoing payments or upon resale by a share of any profits that may have accrued within the limited-equity strictures. Usually, habitability loans were set up to be paid off collectively over time. Because the buildings were set up as co-operatives, the cost of taxes, capital investments, ongoing maintenance, and debt repayment would have to be divided among each of the families in the co-op. Yet if a household lacks the capacity to contribute to these costs (often the case among limited-income residents without ready access to their equity), the financial stability of the whole co-op can be jeopardized.

The result is that many HDFCs have been, or are currently in danger of being, in arrears or financially unmanageable disrepair, amassing hundreds of thousands of dollars in unpaid bills, fines, and taxes. In 2018, the average HDFC pending disclosure had accrued 78 violations and owed $972,000 in unpaid debt (Stewart 2018). Eventually, the city seizes these indebted properties and transfers ownership to a third party whom they charge with creating affordable rental housing. From 1996 to 2008, the city seized 1,669 HDFC units. 7 This process entirely divests co-op owners of even the limited equity that would have been available to them under the policy's strictures.

The financial stakes are high and growing: Most of the HDFCs facing third-party transfer of ownership are located in rapidly gentrifying neighborhoods (Swarts 2019). And co-op owners often lack the resources for independent representation, given their limited incomes and lack of access to wealth. As a result, the problem of “deed theft” has grown in the HDFC sector, with private developers aggressively pursuing third-party ownership transfer (Frost and Abruzzese 2019; Montgomery 2019; Partnow 2019).

This process thus creates another avenue whereby ownership of HDFC co-ops transitions over time from the tenant organizers to the individuals and organizations with wealth. Furthermore, the failure to address building distress, evidenced by accrued code violations, continues a legacy of the racial wealth and income disparities and housing discrimination that has historically placed Black families in unmaintained homes of poorer quality.

Alternative Local Strategies

Given the difficulty of financing large-scale investments among low-income homeowners with restricted equity, the need for capital investments is a shared issue across affordable-housing programs. Some state and local organizations have attempted to implement solutions. For example, Detroit's Make it Home program began in 2017 to address foreclosures associated with the sub-prime mortgage crisis. Their program offered occupants of tax-foreclosed properties the right of first refusal to purchase (or re-purchase) their home, which would otherwise be headed to auction, with a loan at 0% interest. It served a largely low-income population. In 2020, users of the program, 9 in 10 of whom were Black or mixed-race, had an average household income of $25,000, or 40% AMI.

While the program successfully halted displacement for at least 1,000 households in the its first 2-years, it initially left unaddressed the hardships associated with home investments. The city's next move was to initiate the Make it Home Repair Program in 2019, providing $5,000 interest-free loans and $6,000 grants towards plumbing, foundations, rooves, and other major repairs, in addition to smaller grants for utilities and electrical items such as furnaces and refrigerators.

Ultimately, the grants and loans helped but were not large enough to cover all necessary repairs and costs. According to a 2021 external analysis of the program, two-thirds of participants still needed major repairs following the financing. However, 92% of participants reported that the program “improved” or “greatly improved” their housing conditions and one quarter reported that they would have had to leave their homes had they not received MIH Repair support.

Perhaps a more comprehensive and visionary solution is found through MassHousing, a self-funded quasi-public organization in the state of Massachusetts. For decades, the organization ran a program similar to the HDFC of New York, with permanently income-restricted housing that enabled low purchase prices but prevented the intergenerational wealth associated with full equity. Correspondingly, administrators identified a trend in which newer purchasers were primarily White.

Masshousing advanced three important design solutions. First, they subsidize new construction of affordable housing. The Common-Wealth Builder program, which launched in 2019 provides a $150,000 subsidy for newly-constructed affordable units. Buyers must have incomes between 70% and 120% of the area median, and homes must be located in “Gateway Cities,” economically distressed areas of the state, which have some of the highest concentrations Black and Brown residents and some of the oldest housing stock.

Second, affordability restrictions are now dissolved at 15 years, leaving the family with long-term equity intact. Combined with the subsidy of new construction, new home owners are unlikely to require major renovations until after they have realized full equity.

Finally, to avoid down-payment disparities, MassHousing insures mortgages itself, and requires no down-payment at all from households with incomes at or below the area median. Since 2018, MassHousing's down payment assistance program has increased the rate of home purchase loans to buyers of color by nearly 47%. 8

The programs in Detroit and in Massachusetts both began relatively recently, within the past 5 years, and will not have data comparable to our New York evaluation until the units begin to change hands. Nevertheless, they offer potential solutions for affordable homeownership approaches that address both the supply of housing, by providing new homes or subsidizing their repairs, and on the demand side, with purchase-financing programs that do not demand extensive financial assets. These approaches may channel an essential component of antiracist housing policy that promotes sustainable, not merely attainable, homeownership.

Policy Lessons

This legacy of US housing policy—historically, and in New York contemporaneously—illustrates two key principles in the design of anti-racist housing policy.

Principle One: Purchase Financing

First, purchase financing is indispensable to the process of sustainably expanding access to homeownership. Financing must be intentionally designed to meet the needs of low- and middle-income households—those who are able to pay rent on a monthly basis and thus would likely be able to pay a monthly mortgage, if only the financing were within the means of a typical family's budget.

The FHA offered mortgage terms to the white middle class that amounted to about 20% of annual income as a down payment, and 15% of monthly income as the mortgage payment, for households at the 35th percentile of income. The corresponding family today makes $42,000 9 , and would put $8,400 down and pay $560 each month. However, housing costs have far outpaced increases in income since 1945; the median renting household today that earns between $40,000 and $50,000 spends, on average, $860 on housing monthly. Median net worth among all renting households in this income range is $9,750, and $6,770 among Black renting households in that income range. A reasonable expectation for a down payment may begin with these figures, perhaps using the corresponding percentiles within a particular municipality. Surely allowing the market to demand over $90,000 is no reasonable person's understanding of an affordable housing policy. An anti-racist homeownership policy, one aimed at redressing the exclusion of Black, Hispanic, and other non-white persons from the creation of wealth, will not require hefty assets as an entry ticket. Even as most municipal governments 10 lack the capacity to directly redress the racial asset gap, their home-buying policies can nevertheless find ways to avoid perpetuating racial inequality by opting to channel funds made available by better-resourced federal or state mechanisms and should, in the least, be monitoring existing home-buying policies for de facto racial discrimination.

Principle Two: Habitability Financing

The experience of purchasing and living in a home is governed in large part by the quality of that housing, yet this issue has for decades been left unaccounted for (American Archive of Public Broadcasting n.d.). Just as a policy planner can foresee the need for affordable and sustainable home financing, they can also foresee that the cumulative effects of housing disinvestment in redlined neighborhoods will require financial assets to repair over and above the cost of purchasing the unit. The New York City case evidences the outcome of a homeownership policy with inadequate habitability financing: the seizure of tens of thousands of HDFC buildings for which tenant-owners were unable to meet the costs of repair. Ultimately, one cannot expect to hand over buildings in disrepair to low-income families and consider it a job well done, particularly if they are explicitly barred from realizing equity through special “limited-equity” financing strictures.

When the federal government bolstered the white middle class, the majority of homes for purchase were newly built on land made newly accessible due to recently created, federally funded highways (Nall 2015; Federal Housing Administration 1946, 9). In this case, the problem of building investment would not be felt as acutely for the owner of a new home. In the eventuality that the home required investment, the family would have built up some equity that can be funneled toward the expense. By contrast, an older home in a chronically disinvested neighborhood may require new pipes or a new roof within the year.

Whereas infrastructure growth in the early era of federal housing policy was one of freeway and suburb construction, today it lies in stemming the tide and impacts of climate change. Our housing stock will need to be repaired and retrofitted nationwide, from fortifying pipes and foundations against cracks caused by extreme temperatures to fortifying walls and basements against hurricanes, floods, and wildfires, and upgrading windows and insulation for energy efficiency. An intentionally reparative approach will establish sustainable financial terms for purchase while keeping the cost of maintenance and adaptation within community members’ budgets. Data on household income, in collaboration with residents themselves, can inform key design features like the selection of subsidy levels and the choice between offering grants versus loans for capital improvements (Hendricks et al. 2021). The funds can be made to improve habitability in formerly redlined districts even while allowing for the income-limited homeowners residing there to realize greater financial equity as the quality and value of their homes rise.

Policy Principles in the New York City Case Study

The design of the New York City housing co-operatives falls short on these policy principles. The design fails to channel critical federal dollars or to otherwise establish affordable purchase terms, all while actively limiting the wealth realizable for households to retain or reinvest in their homes.

First, the federal government does not ensure “co-operative” multi-unit buildings, only those considered “condominiums.” In a co-op, residents share ownership of the whole building and then permanently lease the unit in which they live. In a condo, residents own their own unit outright. Beyond that, the regulatory structures do not differ dramatically. Co-ops tend to exercise more oversight over building matters including over potential buyers, but condo boards can, and do, carry rules as well (Schill, Voicu and Miller 2007). What differs dramatically is financing access. Federal mortgages with longer amortization periods (30 11 rather than 15 12 years) and access to federal down payment assistance requiring only 3%–5% of the home price, are available only to condominiums.

Second, income restrictions, which act as the policy's instrument for ensuring affordability, are less than sufficient for that goal. The city's policy intends to contain the overall price of the home by requiring that a new buyer's monthly mortgage not exceed 30% of their household's monthly income. Yet at any given price, paying a larger portion as a down payment reduces the amount paid through the mortgage loan. With no cap on down payments, this acts to incentivize large down payments and undermines the goal of affordable home ownership. Most require the standard 20% down payment, but as we saw, this translates to over $92,000 down at the median, largely upending the notion of affordability.

Finally, to the extent that income restrictions do reduce the price of the home, it will counteract the goal of building equity. In contrast with unrestricted housing wealth offered exclusively to white Americans, this model recreates patterns of racialized access. Co-op owners are made to bear the costs of repairs and capital investments but are barred from reaping the wealth.

The New York City policy, under the umbrella of the “shared equity” real estate sector, privileges community wealth (in the form of permanently affordable homeownership) over private wealth (in the form of homeowners’ acquisition of equity) (Davis 2010; Hannah 2015). In other words, co-op owners cannot retain their equity privately because they must leave the unit affordable for the next generation of homebuyers.

Affordable housing is a critical building block of a well-functioning society, and therefore a matter of public policy interest. But perhaps these particular homeowners are not responsible for sacrificing their equity in service of our collective interest in housing affordability. Instead, we can turn to universal policies that broadly mitigate housing speculation and make housing more universally affordable without sacrificing the wealth of those communities already so long excluded.

Such policies could affect the demand side through universal rent stabilization laws carefully designed to temper the future expectations of income generation that drive up housing prices (Teresa 2016). This would have the added effect of promoting housing tenure among renting households. Policies could also affect the supply side by increasing the number of affordable units for sale. For example, voters in Berlin approved a ballot-measure that would expropriate apartments from large landlords—units in excess of 3,000—purchasing them at cost and renting them out as affordable housing (The Economist 2019). Political hurdles remain, even after passage of the referendum in September 2021. The referendum only requires that the local government develop and vote on a bill, not that they implement it. Nevertheless, this movement illustrates a supply-side approach aimed directly at the problem of affordable housing without sacrificing wealth on behalf of low-income families.

Rather than arguing in favor of one demand or supply side initiative over another, the critical distinction here is that we can make housing more affordable through policies that shoulder the burden of progress more broadly as an alternative to systematically limiting the realization of home equity for any segment of householders. Just as the New Deal policies facilitated the creation of private wealth through affordable housing, we can create anti-racist policies that do the same in majority Black and formerly redlined neighborhoods. We do not strictly need to pinpoint formerly redlined communities for lower wealth realization. At the very least we should offer these homeowners a choice: contribute to the social good of future affordability (assuming such affordability is in fact present) or realize the private benefit of housing wealth. If they choose not to share, we needn’t force them (Sørvoll and Bengtsson 2018, 135). An anti-racist approach to affordable housing should first be sure to establish true affordability and second spread the costs of progress universally. In order to more effectively redress the racialized legacy of housing wealth, we can provide Black and Latinx and formerly redlined persons access to wealth-building through homeownership, build access to deeply affordable public rental housing for communities lacking sufficient shelter, and mitigate housing speculation through universally shouldered legislation. This way, we achieve affordable housing without requiring Black and Latinx families’ home equity to suffer in that pursuit.

Conclusion

Federal housing policy helped create a circumstance wherein the median Black household has a fraction of the net worth of the median white household, whose wealth is primarily held in home equity. Today, we are more aware of, reckoning with, and attempting to correct for collective historical wrongs. New York City's co-op policy illustrates the importance of strategic and intentional planning in anti-racist initiatives. Creating an effective policy, one that builds lasting economic security for Black and other non-white families excluded from the last century of wealth creation, requires affordable and sustainable purchase financing terms based on the typical family's budget. Further, even after they gain ownership, these families will require public funds that build a climate-prepared urban housing stock of habitable quality, to attempt to correct for decades of disinvestment. By designing financing terms for purchase and habitability around Black households’ budgets, public policies can finally spur the generational wealth afforded to white working-class homeowners 80 years ago.

Footnotes

Acknowledgements

The authors would like to thank Sophia House and Susan Saegert for their comments on the manuscript and Ellen Gould, Alanna McCargo, and Kilolo Kijakazi for their feedback on the study design. Redlining maps of New York City overlaid with HDFC co-op units were produced by Timothy Gilman, MS candidate at Northeastern University, and Vicky Bu at the City University of New York mined real estate data for the project. Alexander Roesch and Samantha Kattan at UHAB, Cea Weaver at Housing Justice for All, Jonathan J. Miller, Dean M. Roberts, Esq. were interviewed for the project.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Roosevelt Institute.