Abstract

This article revisits the macroeconomic foundations and political economy of national growth models. It argues that the neo-Kaleckian model, which inspired the emergent growth model perspective and focuses primarily on the functional income distribution, can be usefully complemented by theories of private household consumption that focus on the personal distribution of income. The examples of the export-led and debt-led growth models of Germany and the United States, respectively, show how institutional differences help to explain why different countries developed different patterns of income distribution and how income distribution and institutions interacted to generate financial imbalances in different sectors of the economy (i.e., the private household sector, the private corporate sector, and the government sector).

Keywords

In this article, we revisit the macroeconomic and political economy foundations of national growth models. We contrast the export-led growth model of Germany, traditionally considered the classic example of a coordinated market economy (CME), and the debt-led growth model of the United States, the archetypical liberal market economy (LME). The article thus contributes to recent debates about the relationship between macroeconomic growth models and varieties of capitalism. 1

As noted by Lucio Baccaro and Jonas Pontusson, 2 comparative political economy (CPE) scholars currently are split into two camps: on one side are those who argue that all capitalist economies embarked on an essentially similar, socially regressive trajectory of neoliberal transformation from the 1970s onward; on the other side are those who emphasize the resilience of national models and cross-national diversity. Baccaro and Pontusson offer a new “growth model perspective” as an alternative to the established varieties-of-capitalism (VoC) approach inspired by Peter Hall and David Soskice. 3 Unlike the VoC literature, the growth model perspective emphasizes the link between income distribution and aggregate demand. Like the VoC approach, the growth model perspective focuses on cross-national diversity, but it does not see different national growth models as rooted in the institutional equilibria of the kind analyzed in the VoC literature (CMEs vs. LMEs).

We argue in this article that there are still large cross-country differences in some domains typically associated with different VoCs, including industrial relations institutions, financial arrangements, gender relations, employment mobility, corporate governance, and social policy regimes. In our view, these institutional differences contribute to explaining, first, why different countries have experienced rather different patterns of income distribution (despite superficially similar trends in simple summary indicators such as the Gini coefficient of household income) and, second, how changes in income distribution contributed to the emergence of different growth models. It is especially instructive to compare the export-led and debt-led growth models, respectively, of Germany and the United States.

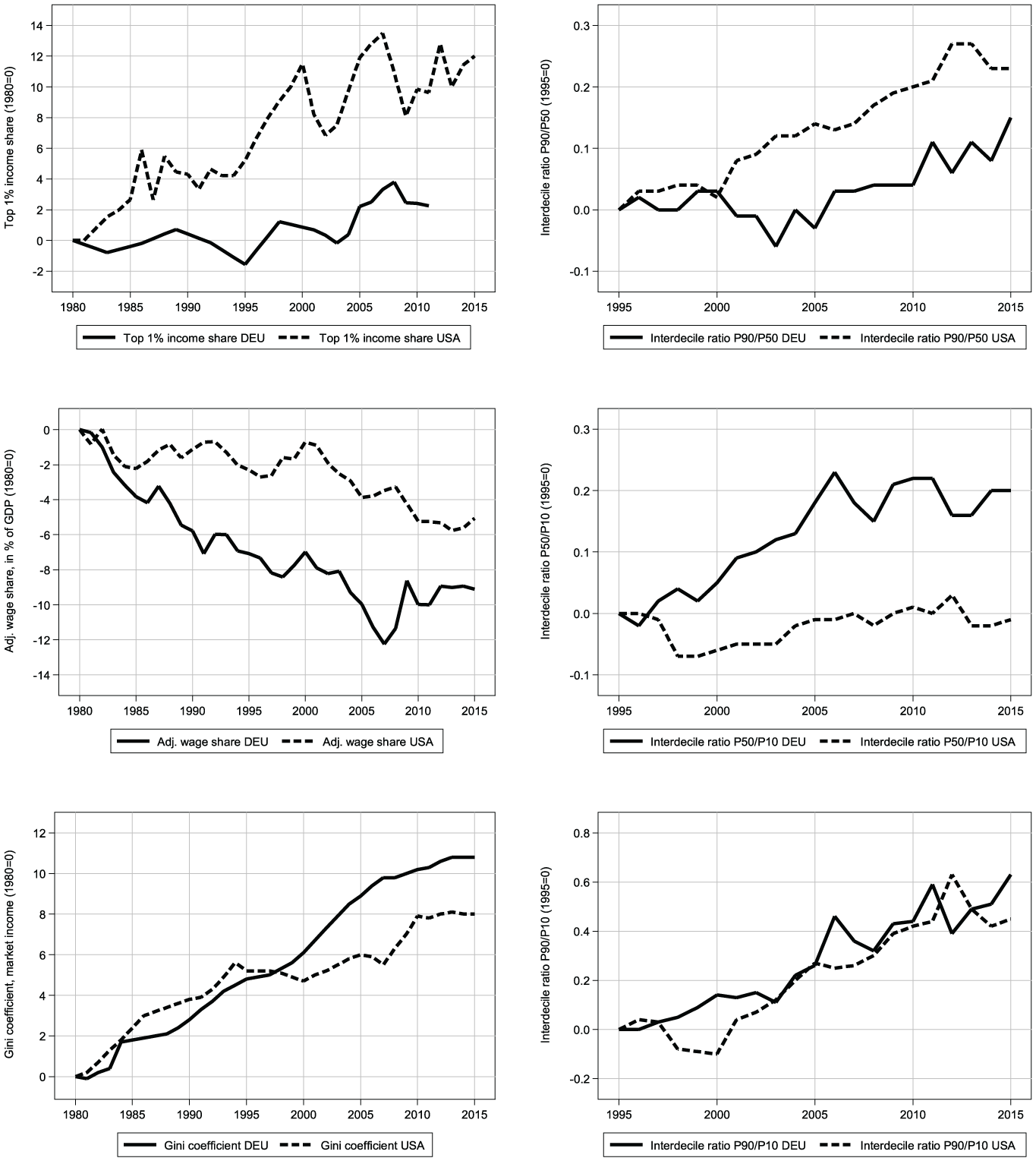

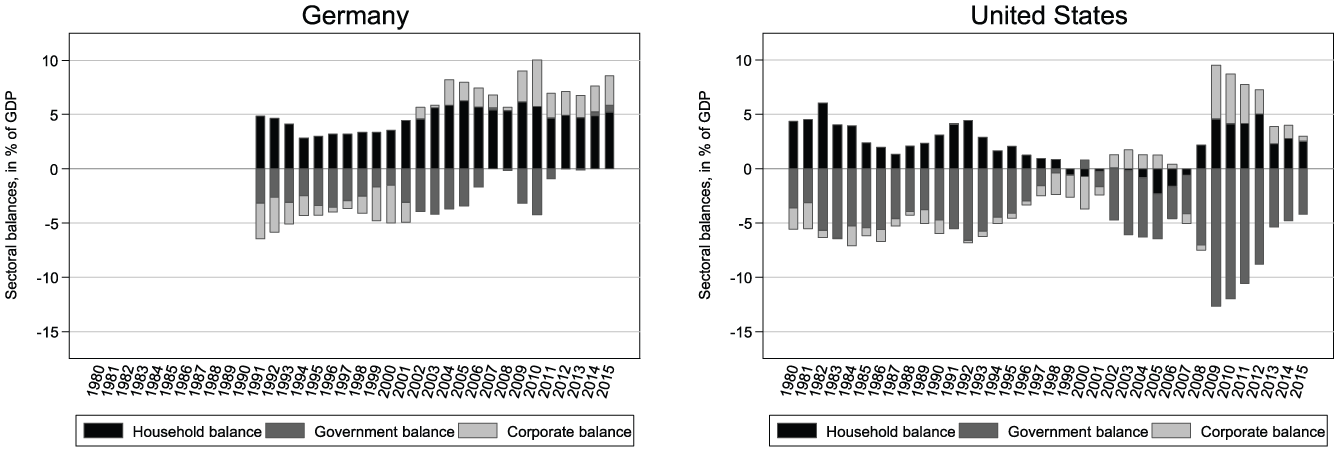

In particular, we examine trends in income distribution and the importance of different sectors of the economy (households, corporations, government) to the emergence of national growth models, which were linked to the widening of current account imbalances during the run-up to the global financial crisis starting in 2008. Although income distribution has played a central role in recent debates about growth models, 4 most existing analyses fail to address the following questions clearly. First, why have some countries (e.g., Germany) experienced only small changes in top-end income inequality but a dramatic fall in the share of wages in national income whereas others (e.g., the United States) featured an explosion of top household income shares but relatively little variation in the wage share (Fig. 1)? And second, how are these trends in income distribution related to the emergence of current account surpluses and deficits, which have been driven primarily by the corporate sector in Germany and by the private household sector in the United States (Fig. 2)?

Different Measures of Income Distribution.

Sectoral Balances.

We offer answers to these questions that bring together elements from a number of complementary literatures: first, neo-Kaleckian macroeconomics, which focuses on the functional distribution of income between wages and profits and underpins the growth model perspective proposed by Baccaro and Pontusson; 5 second, the relative income hypothesis of consumption, which focuses on personal income inequality between top income groups and other households; and third, the VoC literature, which can be extended to explain why and how in some countries the emergence of a particular growth model is related to shifts in the functional income distribution, whereas in others it is shaped mainly by trends in the personal income distribution. The starting point of our sectoral balances approach is the accounting identity that the current account balance is equal to the sum of the financial balances of the private household, the corporate, and the government sectors of the economy. We then ask through which institutional channels the different sectors of the economy have contributed to the emergence of national growth models and the related macroeconomic imbalances, in a context of changes in income distribution. In particular, we argue that the functional income distribution and the personal income distribution can have rather different implications for the different sectors of the economy.

Our contribution is rooted in a structuralist approach to macroeconomics that has a long tradition in the analysis of sectoral balances 6 and national growth models. 7 We here seek to engage with the CPE literature, which has developed a more sophisticated analysis of the key role of institutions and social conflict in the evolution of capitalism. A number of influential recent contributions to CPE have challenged the view that capitalism can be analyzed in terms of neatly identifiable and stable “varieties.” Instead, it has been argued that “the time has come to think, again, about the commonalities of capitalism.” 8 Wolfgang Streeck challenges the view that Germany’s political economy still represents a CME in view of recent sectoral changes in Germany’s political economy, “all toward disorganization.” Collective bargaining coverage and union density have declined; social policy has been retrenched; the once-organized German company network, based on cross-shareholdings, relational banking, and government support, has largely disintegrated; and German banks have increasingly changed from providers of patient finance for national firms to players on the international financial markets. 9 Streeck does not, however, analyze the macroeconomic implications of Germany’s “reforming capitalism.” He does not ask how far the emergence and persistence of Germany’s export-oriented growth model is linked to what he describes as the liberalization of its political economy.

In another influential recent contribution, Lucio Baccaro and Chris Howell argue that “a careful examination of contemporary capitalist political economies reveals a common liberalizing tendency in the trajectory of industrial relations institutions, as everywhere employer discretion has expanded and the balance of class power has shifted against labor.” 10 Lucio Baccaro and Chiara Benassi consider the macroeconomic consequences of the liberalization of German industrial relations, borrowing from post-Keynesian macroeconomics (in its neo-Kaleckian variety) and focusing on the role of income distribution. 11 They argue that the German economy has shifted from a model of growth simultaneously led by net exports and household consumption to an almost exclusively export-led model. And they show how this process was to a large extent caused, or at least facilitated, by the liberalization of the German labor market. First, export-oriented firms have reduced wage costs to improve their international export competitiveness by withdrawing from sectoral collective bargaining, using opening clauses, and outsourcing. Second, the weakening of collective bargaining institutions has led to stagnant wage growth both overall but especially in the lower half of the wage distribution. According to Baccaro and Benassi, the dampening of household spending that resulted from rising income inequality contributed to the one-sided dependence on net exports. Baccaro and Pontusson as well as Baccaro and Benassi highlight the unstable and destabilizing nature of Germany’s export surplus model.

We agree with Streeck and with Baccaro and Howell that Germany’s political economy has undergone significant changes, including substantial shifts in income distribution, throughout at least the past two decades. However, from a comparative perspective, an important open question arises: If the advanced high-income countries, including Germany and the United States, share so many commonalities of capitalism, and if they are characterized by institutional convergence along a neoliberal trajectory, then why have they developed such different growth models? Baccaro and Howell emphasize that their argument about neoliberal convergence is compatible with the emergence of different accumulation regimes across countries. Although it is therefore true that they should not “be accused of treating liberalization as the night in which all cows are black,” 12 the question remains why different cows look so different (e.g., export-led growth in Germany vs. debt-led growth in the United States) if they are all fed in the same way (liberalization and rising inequality)?

We attribute a key role to income distribution interacting with institutions in affecting sectoral financial balances and hence the pattern of aggregate demand. We focus primarily on the top-end inequality of household income and on the respective shares of wages and profits in national income. The cross-country differences apparent in these measures of income distribution are perfectly consistent with very similar trends in summary indicators such as the Gini coefficient of household income or the D9/D1 earnings ratio, which are often used to argue for cross-national convergence (see Fig. 1).

We argue, in particular, that the strong rise in top-end personal income inequality in the United States has contributed to the fall of the household saving rate and financial balance (and to the rise in personal debt) during the decades before the global financial crisis. This argument is supported by empirical evidence and is broadly consistent with theories of consumption grounded in the notion of upward-looking status comparisons, in the tradition of the relative income hypothesis. 13 Theories of “expenditure cascades” 14 or “trickle-down consumption” 15 can explain why the US middle and upper-middle classes have reacted to their falling relative incomes by reducing financial savings in an attempt to keep up with households higher on the income distribution ladder, who have increased their expenditures on positional goods in line with their strongly rising incomes. Such consumption externalities can be expected to be especially pronounced in LMEs, where such important positional goods as housing or education are allocated via competitive markets; 16 where the precautionary saving motive of households is relatively low because of fluid labor markets with relatively short job tenures and workers with general (rather than industry-specific) skills; 17 and where, before the financial crisis, largely deregulated credit markets allowed households to maintain consumption despite falling incomes. 18 An important driver of the rise in top household income shares in the United States was the pronounced shareholder-value orientation and the explosion of top management salaries in the context of the corporate sector’s strong stock market orientation.

In Germany (and other CMEs), by contrast, relative income effects on consumption due to upward-looking status comparison were less pronounced: top household incomes increased far less, families who depend more strongly on the male breadwinner (with specific skills) have a higher demand for precautionary saving, credit markets are more regulated, and important positional goods are provided through government funding. Meanwhile, the German corporate sector, characterized by a large share of family-owned businesses (the Mittelstand) and correspondingly weaker shareholder-value orientation, has paid lower dividends and top management salaries to the household sector than its US counterpart. Although those are important reasons for the lower top-end personal inequality and weaker trickle-down consumption effects in Germany, the surge in corporate profits led to higher corporate saving and thus constrained the increase in household incomes and consumption demand.

In short, we hope that this article can help bring together the VoC approach to CPE, neo-Kaleckian macroeconomics, and the emergent growth model perspective. In our view, a blind spot of the VoC approach is the interaction of income distribution and aggregate demand, but it can be readily extended by the growth model perspective to address this important link. Neo-Kaleckian macroeconomics, on the other hand, places income distribution center stage in its theory of aggregate demand, but it fails to distinguish the effects of changes in the functional income distribution (wage income vs. profit income) and personal income inequality. It also lacks a political economy explanation for why different countries display different patterns of income distribution and how income distribution and institutions combine to produce different growth models. The emergent growth model approach to CPE has the potential of bringing these traditions together and of developing an interdisciplinary analytical framework for the analysis of distribution and growth from a comparative international perspective. To live up to the challenge, we argue, the growth model perspective should adopt a flexible macroeconomic framework that allows for a joint analysis of the aggregate demand effects of both the functional and the personal distribution of income.

The remainder of the article is organized as follows. We first review the neo-Kaleckian distribution and growth model and the relative income hypothesis with upward-looking status comparisons. We then sketch the sectoral balances approach as a flexible macroeconomic framework that highlights the importance of income distribution for understanding trends in sectoral financial balances and national current account balances. In a following section, we discuss how income distribution and institutions have affected the financial decisions of the household, corporate, and government sectors in Germany to produce a growth model that has been strongly dependent on persistent export surpluses. We contrast the German growth model with the debt-led growth model of the United States, which has featured persistent current account deficits. The final section offers some concluding remarks.

Income Distribution and Aggregate Demand

The Neo-Kaleckian Model: The Functional Income Distribution and Aggregate Demand

The analyses by Baccaro and Pontusson and by Baccaro and Benassi of national growth models in general, and of Germany’s export-led growth model in particular, are strongly inspired by neo-Kaleckian macroeconomics. As noted by Baccaro and Benassi, neo-Kaleckian macroeconomists, following the seminal article by Amit Bhaduri and Stephen Marglin, 19 generally distinguish between two types of growth models: “wage led” and “profit led,” depending on the effect of a change in the share of wages in national income on aggregate demand, that is, the sum of consumption, investment, and net exports. It is argued that a rise in the wage share has a positive effect on private consumption, ceteris paribus, because the propensity to consume out of wages is higher than the propensity to consume out of profits. However, a higher wage share is expected to reduce private investment, ceteris paribus, by deteriorating firms’ profitability expectations and their ability to self-finance investment expenditures. Similarly, it is expected that net exports will be negatively affected by a rise in the wage share, ceteris paribus, owing to a decrease in price competitiveness. In a wage-led growth regime, a rise in the wage share has overall positive effects on aggregate demand, owing to a strong partial effect of a higher wage share on private consumption and relatively weak partial effects on investment and net exports. By contrast, in a profit-led regime, a rise in the wage share has a negative total effect on aggregate demand if either investment spending is highly sensitive to firms’ profit margins, or net exports react strongly negatively to a higher wage share via the price competitiveness channel, or both (see App. B for a technical summary of the neo-Kaleckian model).

According to a common interpretation, 20 aggregate demand in most industrialized countries was driven by rising wages during the “Golden Age of Capitalism,” that is, the three decades or so following the Second World War. However, the Fordist model of wage-led growth ground to a halt as wage growth decoupled from productivity growth in the 1970s and 1980s. Since then, different countries have developed new growth models that illustrate “different solutions to the problem of finding a replacement for the faltering ‘wage driver.’” 21 Whereas the United States and the United Kingdom were characterized by debt-led growth, in which consumption by working-class families with stagnating real wages was increasingly financed through higher indebtedness, 22 Germany “came to rely on export-led growth, repressing wages and consumption to boost the competitiveness of the export sector.” 23

In our view, the neo-Kaleckian model in its simple formulation 24 does not offer a fully convincing explanation of why different growth models developed in different institutional environments of individual countries. The neo-Kaleckian model provides a good starting point for the analysis of the links between export-led growth in Germany and a strongly falling wage share, rising corporate net lending, and weak consumption demand since the early 2000s (see Figs. 1 and 2). It is, however, less useful for understanding the debt-led growth model of the United States, because the only distributional variable in the neo-Kaleckian model is the wage share, which was roughly constant in the United States during the period 1980–2000, for example (see Fig. 1). Moreover, because the neo-Kaleckian model takes the (functional) income distribution as an exogenous variable, it is of limited help in understanding why the decline in the wage share has been so much stronger (and the rise in top household income shares so much weaker) in Germany than in the United States since the 1980s. And because the neo-Kaleckian model has no explicit theory of household consumption, it cannot establish any link between changes in personal income inequality and household consumption and saving; hence it cannot account for the divergent trends in the household financial balance in Germany and the United States since the 1980s.

The Relative Income Hypothesis: Personal Income Distribution and Household Consumption

We argue that the neo-Kaleckian model can be usefully complemented by theories of private household consumption that focus on social status comparisons in a context of rising personal income inequality. According to those theories, it is not generally to be expected that “shifts within the distribution of wage income, for example, redistribution from super-managers to low-wage workers, would have similar effects to a redistribution from profits to wages.” 25

Rather, according to different variants of the relative income hypothesis in the tradition of James Duesenberry, 26 an increase in income inequality may increase aggregate consumption demand in specific institutional and historical circumstances, if consumption externalities due to upward-looking status comparisons are large and lead to falling saving rates in the lower segments of the income distribution (see App. B for a technical summary of a variant of the relative income hypothesis). In such circumstances, the propensity to consume will still vary negatively with income, and rich individuals will still save more than poor individuals relative to their incomes, but a rise in personal income inequality leads to a decline in the aggregate personal saving rate and an increase in the consumption-to-income ratio. 27

The “expenditure cascades” model, according to Frank, Levine, and Dijk, captures what are perhaps the two most robust findings from the behavioral literature on demonstration effects: (1) the comparisons that matter most are highly localized in time and space; and (2) people generally look to others above them on the income scale rather than to those below. 28

To the extent that many consumption goods are perceived as positional goods (indicating social status), a rise in income inequality may provide incentives for households below the top of the income distribution to sacrifice nonpositional goods (including leisure and saving) in an attempt to maintain relative status in consumption.

Clearly, the extent to which expenditure cascades are triggered by rising inequality can be expected to depend crucially on the country-specific institutional environment. Expenditure cascades can be expected to be stronger in countries with, among other factors, a stronger shareholder-value orientation of firms and a more competitive market for managers, which lead to higher shareholder and top management income and hence higher top household income shares. Moreover, expenditure cascades will be more pronounced with a less strictly regulated financial system (and hence access to credit easier for households below the top of the income distribution), a larger share of private financing of health care and education (giving rise to positional arms races), more general skills of workers, and higher female labor force participation (reducing the precautionary saving motive of families). 29 We will discuss the empirical relevance of these theories of “trickle-down consumption” or “expenditure cascades” below, as an important explanation of the fall in household net lending and the decrease of the current account in the United States since the early 1980s (see Figs. 1 and 2).

A Sectoral Balances Approach to the Political Economy of Growth Models

In this section, we briefly describe our general approach to the analysis of growth models, before applying it to the German and US growth models in the next section.

We see the financial balances approach as a flexible analytical framework that encompasses both the neo-Kaleckian model and theories of household consumption. To see more clearly how the different approaches are linked, it may be useful to consider the macroeconomic accounting identities underlying them more explicitly. The neo-Kaleckian model focuses on the expenditure equation (GDP = gross domestic product):

where household and government demand consist of consumption and investment spending and corporate demand is corporate investment. The financial balances approach combines the expenditure equation with the income equation (GNI = gross national income):

The financial balances equation results from equating the expenditure and the income equation while making the necessary adjustment for the difference between the gross national income and the gross national product:

where the financial balances are defined as the difference between the income and expenditure of each sector.

One advantage of the financial balances approach is that it directly addresses the question of current account imbalances, a widely agreed indicator of macroeconomic instability. Whereas in the Kaleckian model the total aggregate demand effects of a fall in the wage share can be compatible with either an increase or a decrease in net exports or the current account balance in both a wage-led and a profit-led economy (see App. B), the sectoral balances approach asks how the different sectors of the economy have contributed to the observed changes in the current account balance. Clearly, if the current account increases, perhaps as a result of a lower wage share, then there must be a corresponding increase in the financial balance(s) of the corporate sector, the household sector, or the government sector. In particular, the financial balances approach seeks to understand how the institutional settings in different countries affect the net lending positions of different economic sectors and how these are related to national growth models.

It may also be useful to recall that both the neo-Kaleckian and the sectoral financial balances approaches differ from the individualist tradition of neoclassical economics, in which macroeconomic outcomes such as the current account balance are determined largely by household preferences. If, for example, the corporate sector raises or lowers its retained profits, rational shareholders will see through the “corporate veil,” according to simple neoclassical models based on rational agents. They will always be able to offset any unwarranted changes in corporate saving by opposite changes in personal saving so that the aggregate amount of saving remains at the discretion of households. Similar arguments apply to the government sector, based on the notion of Ricardian equivalence. If, for example, the government increases its deficit (lowers its saving), rational households may anticipate future tax hikes and adjust their current saving upward.

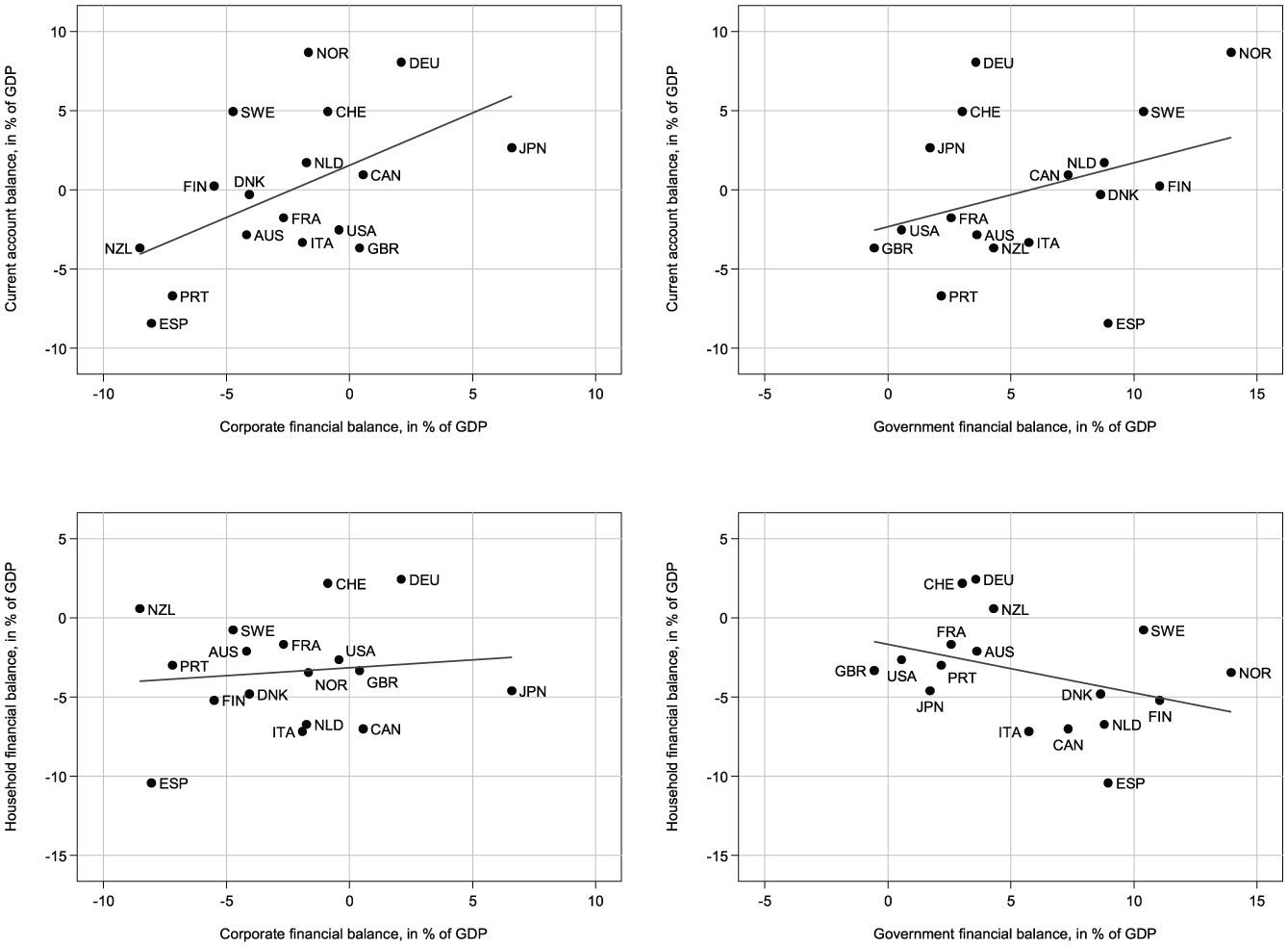

Despite their formal appeal, the notions of a fully transparent corporate veil and of Ricardian equivalence are difficult to reconcile with empirical evidence that suggests that the financing positions of the nonhousehold sectors do affect the current account. 30 To illustrate, Figure 3 shows that changes in the current account balance correlate positively with changes in the corporate financial balance, but there is no negative correlation between changes in the corporate financial balance and changes in the household financial balance in a sample of seventeen high-income countries for the period 1995–2007. Although the picture is less clear for the government financial balance, multivariate estimations of current account determinants consistently show that a higher (lower) government deficit contributes to a lower (higher) current account balance. 31 In the light of the empirical evidence, we can thus confidently conclude that sectoral balances do matter for macroeconomic outcomes.

Changes in Sectoral Balances, High-Income Countries.

As can be seen in Figure 3, Germany’s shift from a small current account deficit in the 1990s to a persistent and unprecedentedly large current account surplus since the early 2000s was in large part due to the shift of the corporate sector from a net borrowing position to a net lending position. In addition, the government turned from a persistent deficit position to a balanced budget. The financial balance of the household sector remained roughly stable over time. In the United States, by contrast, the bulk of the decrease of the current account from the 1980s through the outbreak of the financial crisis was reflected in a large decrease of the private household financial balance. Corporate and government net lending, by contrast, showed no pronounced secular changes (despite some cyclical variation).

The next question is how these changes in the sectoral balances are related to shifts in the distribution of income both between and within sectors. The neoclassical rational expectations model leaves little room for income distribution to affect aggregate demand. But the neo-Kaleckian model, as outlined above, is clearly non-neoclassical, in the sense that the distribution of income between the corporate and the household sector does have saving and aggregate demand effects, because the economy can be either wage-led or profit-led. The relative income hypothesis with upward-looking status comparisons also deviates from the standard neoclassical assumption of exogenous individual preferences, as it assumes that the satisfaction households derive from certain consumption goods depends on the consumption of such goods by other households above them in the income distribution ladder. It thus predicts a negative effect of a rise in income inequality on household net lending. This effect is expected to be especially large when households in the middle and upper-middle part of the income distribution lower their saving in response to a rise in the share of total income going to the very top. Other non-neoclassical theories of consumption, such as traditional Keynesian theory, predict a positive link between income inequality and household net lending based on relatively stable saving propensities across income quantiles. Previous quantitative research, using panel analyses for high-income countries, suggests that a fall in the wage share tended to raise the corporate financial balance and the current account (consistent with wage-led growth in the neo-Kaleckian sense), whereas a rise in top household income shares tended to lower the private household financial balance and the current account (consistent with the relative income hypothesis) during the run-up to the global financial crisis. 32

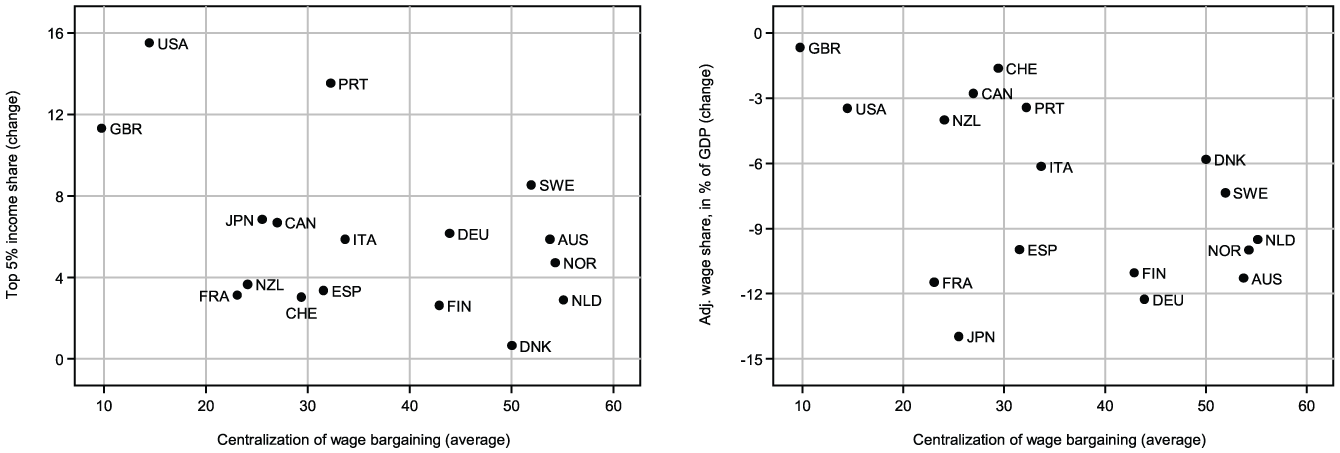

Finally, we ask how the observed changes in income distribution and their macroeconomic effects, through their impact on sectoral balances, can be explained from a political economy perspective, taking into account the institutional environment in specific countries. In so doing, we borrow extensively from the VoC literature and argue that, despite a common trend toward a more inegalitarian society, important institutional differences associated with CMEs and LMEs in the literature have largely remained in place and shaped both income distribution and growth models. Results from multivariate panel analysis suggest that countries with different degrees of wage coordination, despite confronting similar paths of technological change, globalization, and financial and labor market liberalization, experienced rather different patterns of income distribution, with top-end personal income inequality increasing more strongly in countries with less coordinated labor markets and wage shares decreasing more strongly in countries with more coordinated labor markets. 33 Figure 4 gives a bivariate illustration of the relationship between wage centralization and income distribution. In the next section, we attempt to dig deeper into the political economy underpinnings that may help explain why Germany and the United States have experienced such different patterns of income distribution and how these are related to the two countries’ divergent growth models.

Income Distribution and Centralization of Wage Bargaining, High-Income Countries.

Export-Led versus Debt-Led Growth: The Cases of Germany and the United States

The Corporate Sector

An important building block of the analysis by Baccaro and Pontusson of Germany’s export-led growth model is based on the view that German exports have become increasingly price-sensitive and that the German corporate sector has managed to improve its international export competitiveness by reducing wage costs since the early 2000s. The empirical evidence for the price elasticity of German exports is highly contested; 34 we do not need to take a stance on the sources of Germany’s recent export successes. Rather, in terms of the financial balances perspective, our main question of interest is why the receipts from higher exports were not channeled back into domestic demand but retained by corporations.

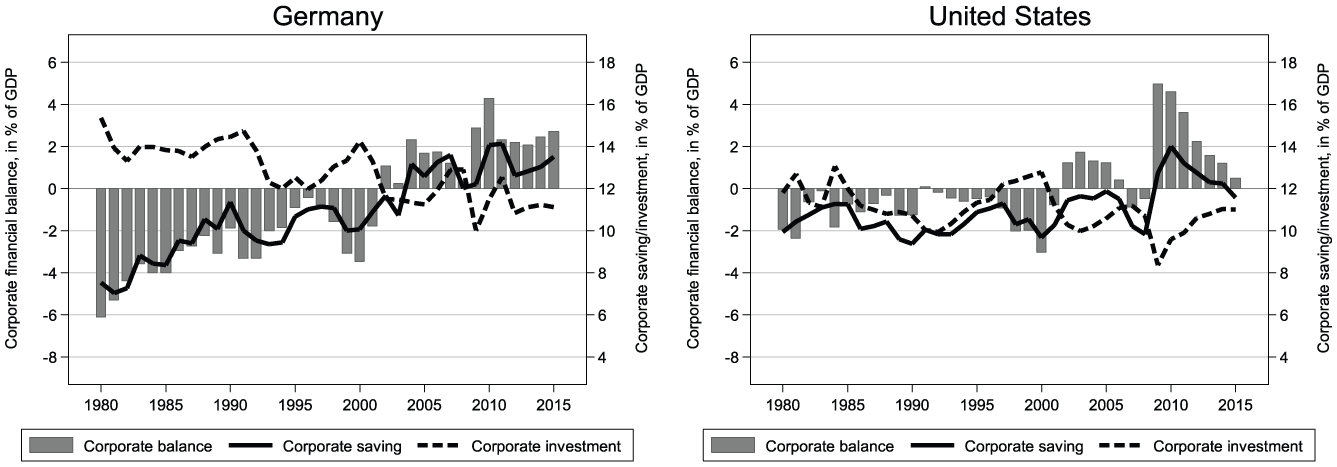

Figure 5 shows the evolution of corporate saving and investment in Germany and the United States since 1980. A striking observation from Figure 5 is the strong rise in corporate saving as a percentage of GDP in Germany, leading to persistently positive corporate net lending since the early 2000s. By contrast, in the United States corporate saving has remained roughly constant as a percentage of GDP, and corporate net lending has turned positive only in response to the financial crisis of 2008.

Corporate

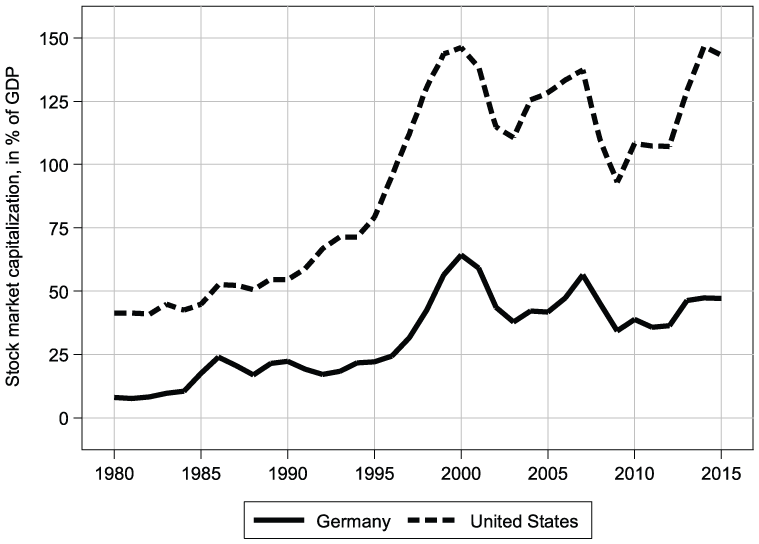

In our view, the different institutional settings and different strategic objectives in the corporate sector are key to understanding the diverging patterns of income distribution and the different growth models of Germany and the United States. Although Streeck emphasizes the growing shareholder-value orientation and the increasingly competitive and fluid market for corporate managers, 35 it can be seen from Figure 6 that stock market capitalization as a share of GDP in Germany is still quite small compared to the United States. More important, although a view of the largest listed companies may convey the impression that “as in other countries, German executives’ salaries have gone through the roof in recent years,” 36 top household income shares have increased only moderately since 1980, especially in comparison with such countries as the United States or the United Kingdom (see Fig. 1).

Stock Market Capitalization.

An important peculiarity of the German corporate sector is the large share of family-controlled businesses, the so-called Mittelstand. 37 Note, to begin with, the macroeconomic importance of the Mittelstand. The Mittelstand comprises practically all small and medium-sized enterprises (SME) but also many large companies. SMEs in Germany account for 35 percent of all sales and for 59 percent of all employees covered by social security. According to the German Institut für Mittelstandsforschung (IfM), roughly 65 percent of all German firms belong to the Mittelstand, defined by the IfM as made up of all firms in which at most two natural persons hold more than 50 percent of the firm’s equity while also actively involved in the firm’s management. Beyond this formal definition, as many as 77 percent of all firms are perceived by their executives as being part of the Mittelstand. Even among large companies with annual sales exceeding 50 million euros, 41 and 91 percent of all firms belong, respectively, to the definitional and the self-proclaimed Mittelstand. 38

An important characteristic of the Mittelstand is that the principal-agent problem between the owners and the managers of the company is less pronounced than in publicly listed joint-stock companies. Owner-managers can be expected to have more long-term objectives than hired managers with a much shorter average job tenure. Owner-managers therefore have less incentive than hired managers to extract as much cash as possible from their firms in as short a time as possible. This fact is especially true when the ownership and management is passed from one family generation to the next. In Germany, business wealth enjoys a preferential tax treatment compared to other forms of bequests. Moreover, retained profits are taxed less than distributed profits. According to Eric Ruscher and Guntram Wolff, the tax law in Germany therefore provided “an incentive to use corporations as piggybank.” 39 And Andre Pahnke and his colleagues point out that the stricter equity requirements of Basel I and II may have led to an even stronger desire of Mittelstand companies to make themselves independent from the banks. 40 Hence, these new regulations may have further increased firms’ saving motive. Pahnke and his colleagues show that equity ratios have strongly increased in SMEs, but not in large companies, and that the retained earnings of SMEs also strongly increased throughout the 2000s, to exceed 80 billion euros, or almost 3 percent of GDP, just before the start of the financial crisis in 2008. 41

It is important to realize that the corporate sector’s policy of profit retention is directly linked to the relative constancy of top household income shares (Fig. 1). Clearly, if German corporations had behaved more like their counterparts in the United States and paid higher salaries to top management, corporate retained earnings would have been lower but top household income shares higher. On the other hand, the rise in corporate saving is also linked to the fall of the economywide wage share in Germany (Fig. 1). One explanation of the relative constancy of the wage share in the United States, perhaps paradoxical at first sight, is the explosion of top management wages that compensated for the much more sluggish wage trends in the bottom 90 percent or so of the wage distribution.

The developments mentioned above can also be discussed in the context of the “dualization hypothesis”: that the German economy is increasingly characterized by a dual labor market in which self-confident and well-protected core workers coexist with precarious low-pay workers. In that regard, we agree with Streeck: Rising competitive pressures . . . have not made German firms seek relief in radical individualization of the employment relationship. . . . Instead the dominant strategy was to build a coalition between shareholders and core employees.

42

As can be seen in Figure 1, the brunt of the strong fall in the German wage share has been borne by workers in the bottom half of the wage distribution, while the earnings distribution has remained relatively stable in the upper part of the distribution. However, the main beneficiaries of recent changes in the distribution of income in Germany clearly have been corporate owners (rather than salaried top managers as in the United States).

In a nutshell, we argue that the very different financial policies and strategic orientation of the corporate sector in Germany and the United States help explain why the common trend toward a more inegalitarian distribution of income has taken rather different forms and why these were linked to different macroeconomic outcomes in the two countries. In Germany, the strong fall in the wage share and the concomitant rise in corporate retained earnings largely prevented an increase in top household income shares but also held back domestic demand by pushing the corporate sector into a persistent net lending position. In the United States, the corporate sector paid much higher incomes to top earners, implying lower corporate saving but also a stronger rise in top-end income inequality.

The Household Sector

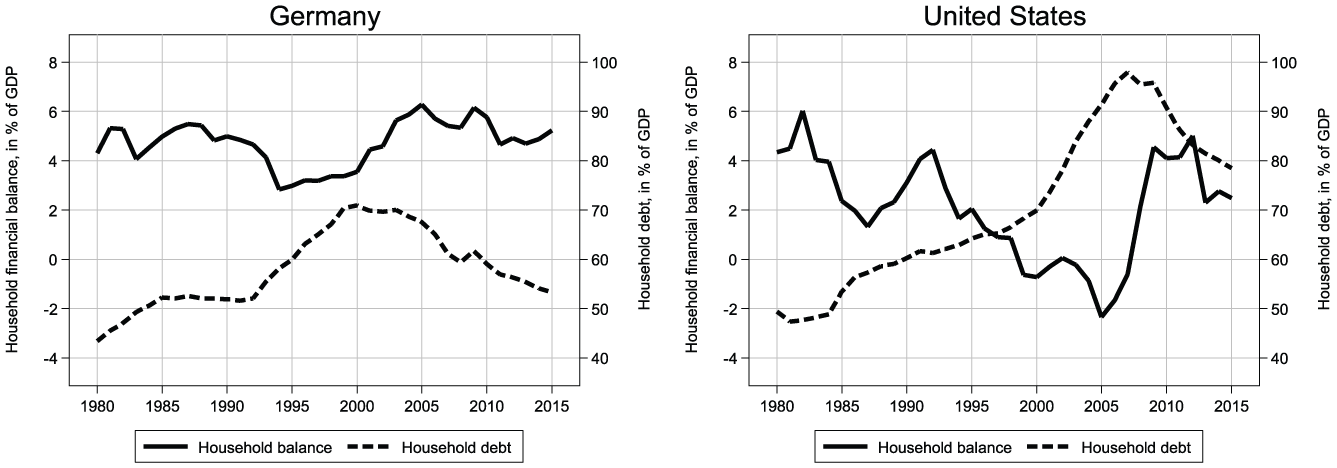

Figure 7 shows the relative constancy of the private household financial balance in Germany since the 1980s. The ratio of personal debt to GDP increased during the 1990s, only to fall back to its 1990 level of slightly more than 50 percent today. In stark contrast to this, in the United States private household net lending fell from more than 6 percent of GDP in the early 1980s to around −2 percent just before the financial crisis, while personal debt to GDP skyrocketed from less than 50 percent in the early 1980s to almost 100 percent just before the crisis.

Household Balance and Debt.

These observations are intriguing, not least from a traditional Keynesian point of view. As noted above, some authors argue that “rising inequality has, other things equal, a negative effect on consumption expenditures and thus on aggregate demand” 43 and that “shifts within the distribution of wage income . . . would have similar effects to a redistribution from profits to wages.” 44 Hence, an interesting question to ask is, Why did private consumption take such different paths in Germany and the United States, despite the increase in inequality that those authors see as the main reason for the emergence of debt-led and export-led growth models? Engelbert Stockhammer notes in passing that “financial institutions as well as industrial relations and industrial policy play a role,” and he points to “a strong aspect of historical continuity on the side of the export-led models.” 45 Baccaro and Howell indicate that debt-led growth may result from the interaction of rising inequality and financialization and that “a debt-led economy needs to attract international financial capital to cover its endemic current account deficit as a result of excessive consumption.” 46

The relative income hypothesis with upward-looking status comparisons offers a direct theoretical explanation of the divergent paths of household consumption in Germany and the United States. In particular, it can explain why the decrease of the aggregate US household saving rate 47 was driven largely by the decrease in the saving rates of households below the top 1 percent of the wealth distribution and why the rise in personal debt was concentrated in the bottom 95 percent of the distribution. 48 It is interesting that saving and debt-to-income ratios remained roughly constant at the top of the distribution. The basic intuition here is that the middle and upper-middle classes in the United States have reduced their saving to try to keep up with the spending patterns of households at the top. This, in turn, may have increased the pressure on the lower-middle and lower classes to increase spending relative to their incomes. Ultimately, therefore, the rising standard of living at the top of the distribution has affected the consumption norms of the entire income distribution. 49 There is considerable evidence that middle- and upper-middle-class households in the United States have traded off their retirement savings for the purchasing of positional goods such as education, housing, or health care, which are allocated through largely unregulated markets especially in the United States. 50 Meanwhile, the rise in the personal debt-to-income ratio was facilitated by the largely deregulated credit markets in the United States, that is, a high degree of “financialization.”

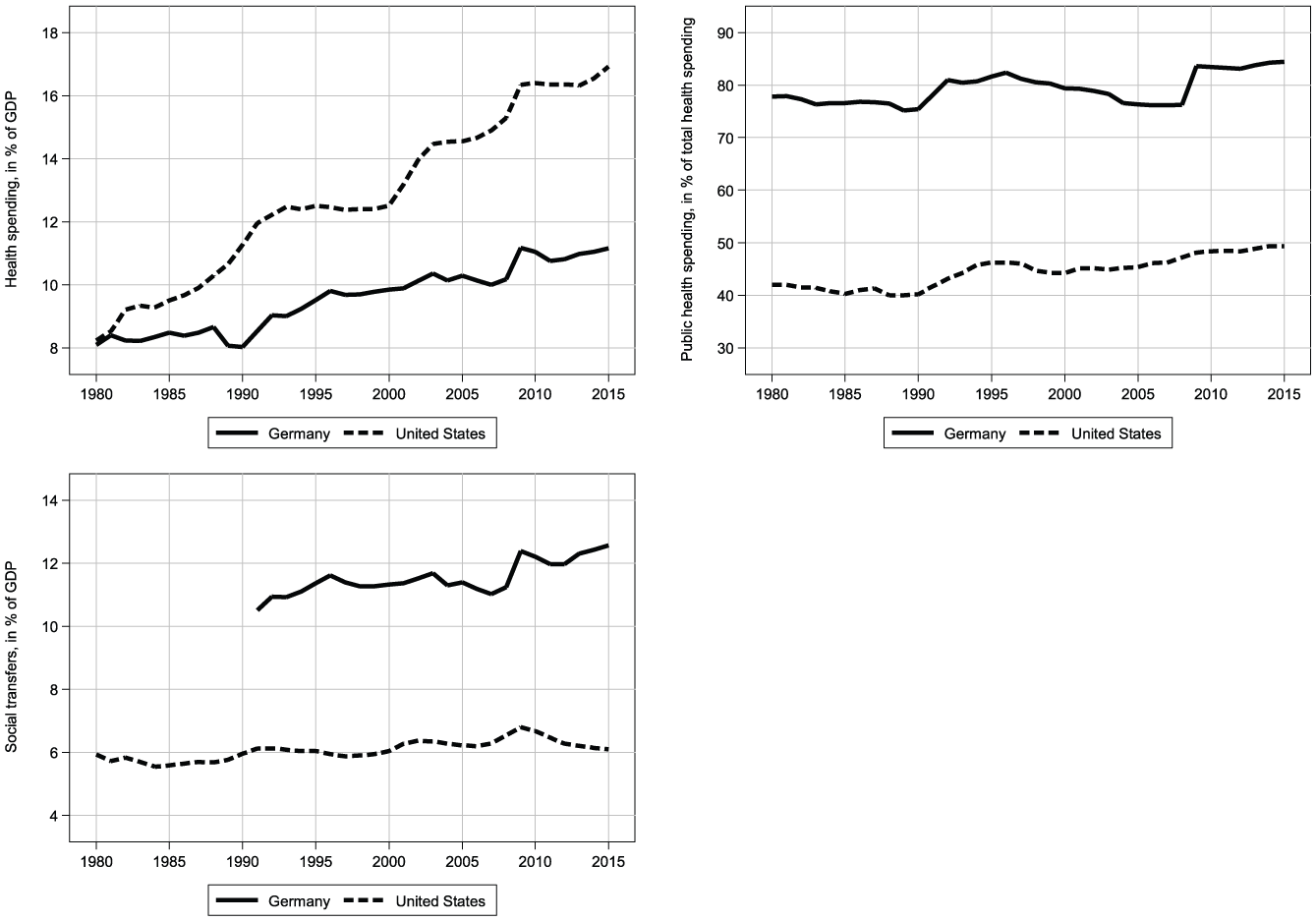

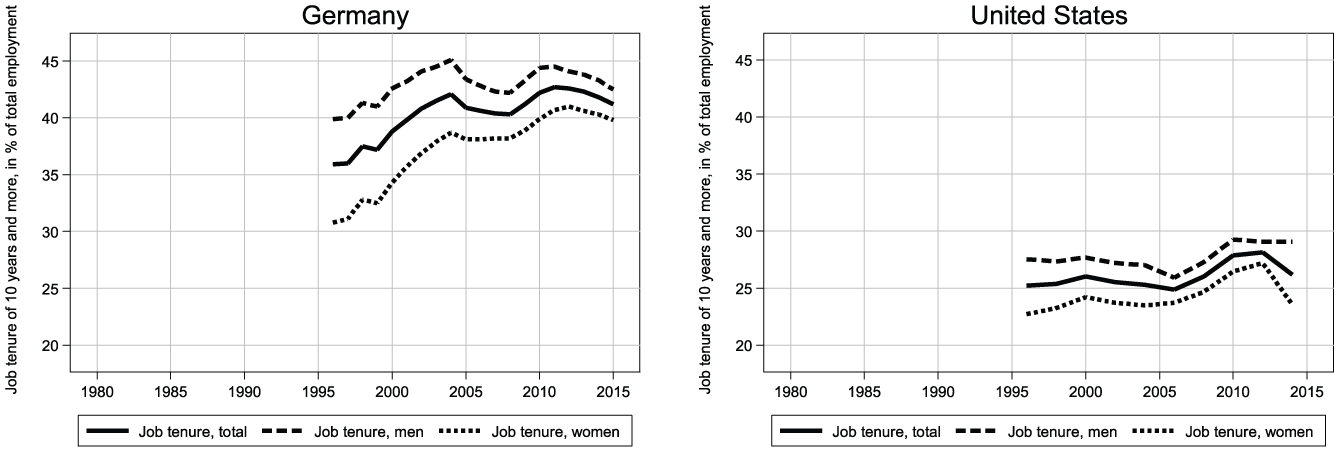

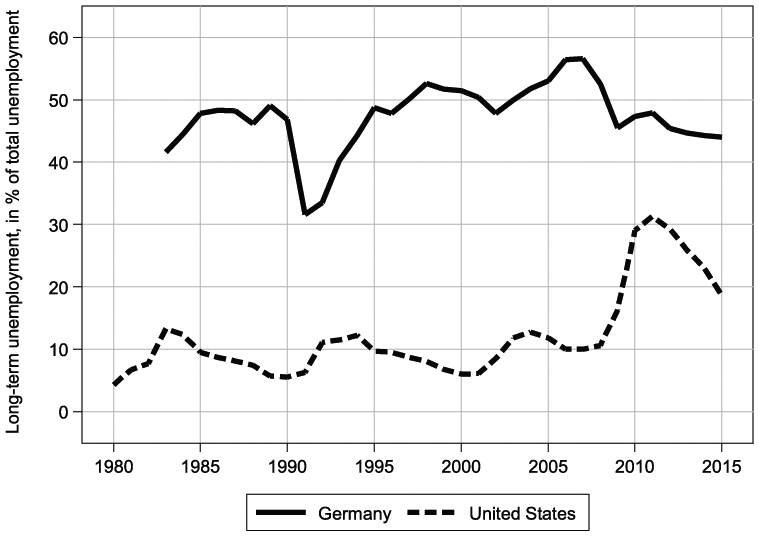

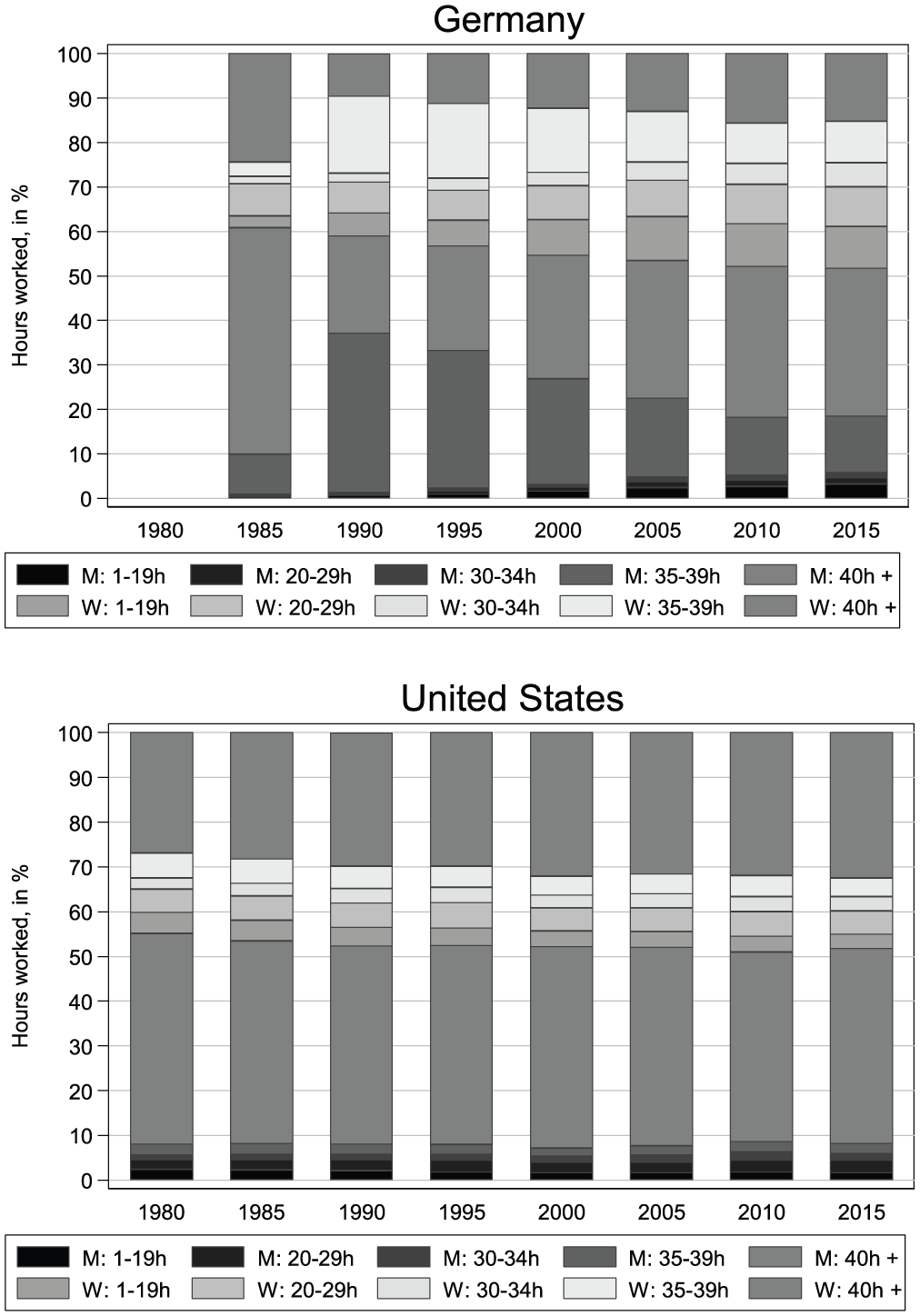

It is unlikely, however, that differing degrees of financialization are the main explanation for why household net lending and household debt developed so differently in the United States and Germany. Certainly household demand for goods and services in Germany was held back not primarily by supply-side constraints (in the credit market) but by household demand for consumption and credit. Note that the saving rate of the bottom three income quartiles actually decreased slightly since the early 2000s, when these groups saw their incomes decrease relative to the top quartile of the distribution, 51 as the relative income hypothesis would predict. The main difference compared to the United States was that households just below the top of the distribution (in fact, those who are least likely to face credit constraints) did not lower their saving rates. In our view, potential reasons for this are the following: First, income inequality did not change as much at the very top of the distribution so that middle- and upper-middle-class households felt less pressure to trade off saving for positional goods to keep up with the rich (Fig. 1). As argued in previous sections, the subdued rise in top-end income inequality (and hence of consumption trickle-down effects) was due to the fact that a large part of rising profits was retained by corporations. Second, the public health and social systems are more developed in Germany (see Fig. 8), reducing the need of households with declining relative income to finance health and other expenditures through lower saving and higher debt. Third, German households have a stronger precautionary saving motive in part because of more industry-specific skills, reflected in longer job tenure (see Fig. 9) and higher long-term unemployment (see Fig. 10), and because the division of paid labor within households is less equal (see Fig. 11), which taken together reduce households’ ability to self-ensure against unforeseen spells of unemployment. 52

Health and Social Spending.

Job Tenure.

Long-Term Unemployment Rate.

Hours Worked.

The inequality-consumption nexus in the household sector can also be interpreted in the context of recent debates about the dualization of the German labor market. Clearly, the rise in the Gini coefficient and the D9/Dl earnings ratio in Germany was in large part due to higher earnings inequality in the bottom half of the distribution and to a much lesser extent to higher top-end income inequality (see Fig. 1). Against that background, part of the VoC literature argues that the manufacturing core of Germany’s industrial relations remains fundamentally coordinated and that core workers remain protected from the liberalization and deregulation in the growing low-pay sector. 53 In contrast, others argue that liberalizing reforms pressure core workers to agree to concessions and that unions increasingly view agency work as a way to replace stable employment with precarious employment. 54 See Baccaro and Howell for a fuller discussion. 55 In terms of the inequality-consumption nexus considered here, both views contain important truths. On the one hand, the German middle class still fares relatively well economically, especially relative to top-income households. The middle class therefore had no need to reduce their saving or go deeper into debt to afford basic middle-class wants such as decent health care, education for their children, or housing. On the other hand, the implementation of reforms since the 2000s to make the labor market more flexible and to establish a growing low-pay sector may have interacted with the behavior of workers with specific skills to increase precautionary savings and thus may have contributed to depressed domestic demand. 56

The Government Sector

Beyond our main focus here on the corporate and household sectors, the government can influence national growth models in several important ways. To begin with, the government regulates, taxes, and pays transfers and subsidies to the corporate and household sectors.

For example, the fact that in Germany credit markets are more strictly regulated and important (positional) goods such as education and health care are provided to the household sector through government funding certainly go far to explain why expenditure cascades have been less pronounced in Germany than in the United States. As shown in Figure 8, neoliberal transformation notwithstanding, public spending on health and social benefits in kind has been relatively constant in Germany over time and orders of magnitude higher than in the United States. Similarly, the German education system is almost fully government-funded from the primary school to the postgraduate level; it thus stands in stark contrast to the largely private education system in the United States. From the perspective of the relative income hypothesis, the German system of public goods clearly reduces the need for middle-class families aspiring to a good level of education for their children and decent health care, for example, to bite into their savings and go into debt as their relative incomes decrease.

In Germany, there is a long tradition of preferential tax treatments for retained profits and inherited business wealth. Unlike in the United States, the (re)introduction of a wealth tax or a more substantive inheritance tax is a political taboo in Germany, partly because both would meet the resistance of the Mittelstand. Germany’s tax policy thus favors the “retain and save” strategy of the corporate sector in a context of a rising profit share.

As highlighted in the discussion of the sectoral balances approach, above, the government may also affect macroeconomic outcomes in a more direct way, that is, through the government financial balance (see also Fig. 2). Torben Iversen and David Soskice cite a number of studies suggesting that higher wage centralization is associated with more conservative monetary and fiscal policy. 57 The basic argument is that with high union centralization, each union is large enough to know that a high wage settlement will push up inflation. This in turn provides incentives for monetary and fiscal policy to be conservative and for the trade unions to implement nominal wage restraint, with the result of lower price inflation and higher export price competitiveness. In line with this argument, Hamzeh Arabzadeh presents empirical evidence that higher wage centralization is typically associated with a lower budget deficit and hence with a higher current account. 58 A less functionalist but more political explanation of Germany’s fiscal conservatism would be that, as the German corporate sector has become increasingly export oriented since the early 2000s, it has lobbied against more expansionary fiscal policies which may have increased the tightness of the labor market and pushed up wages.

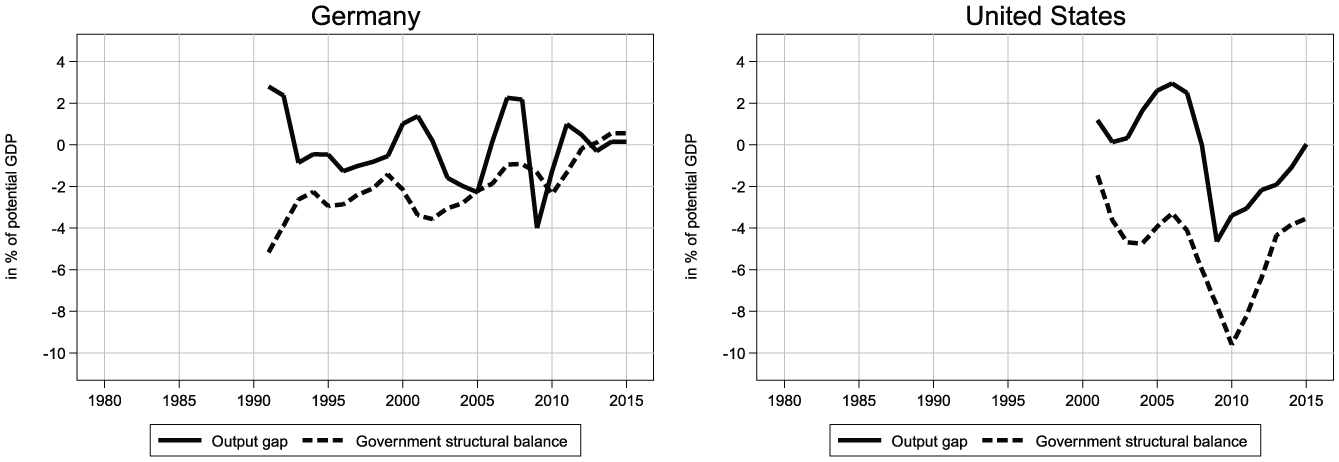

Figure 12 shows the cyclically adjusted government balance and the output gap for Germany and the United States. In the presence of a countercyclical discretionary fiscal policy, the structural government balance should be expected to move in the same direction as the output gap. While this has been largely the case in the United States, Germany has conducted either less strongly countercyclical or even procyclical discretionary fiscal policies, especially since the early 2000s. These have further contributed to the weak domestic demand and to the increasing export dependence of the German growth model.

Structural Government Balance and Output Gap.

Concluding Discussion

In this article we have reconsidered the export-led and debt-led growth models, respectively, of Germany and the United States from a financial balances perspective. The article thus seeks to contribute to recent attempts at “bringing macroeconomics back into comparative political economy (CPE).” 59 We do agree with proponents of the growth model perspective that the VoC approach tends to neglect the importance of income distribution as a determinant of broad macroeconomic trends. At the same time, we try to show that the growth model perspective can benefit from distinguishing more clearly between the potential macroeconomic implications of the functional distribution of income (wages vs. profits), on the one hand, and the personal distribution of income (top-end income inequality in particular), on the other hand. In particular, although we agree, for example, with Stockhammer and with Baccaro and Benassi that the neo-Kaleckian model provides a useful analytical framework for explaining the link between the strong fall in the wage share and the weak domestic demand and persistent current account surplus of Germany, the standard neo-Kaleckian model has less to say about the macroeconomic effects of income distribution in the United States (at least before the financial crisis) because it has no role for the personal distribution of income.

We argued above that the weak domestic demand in Germany was the result not so much of the increase in income inequality in the household sector but rather of the profit-retention policy applied by the corporate sector, which constrained household income and hence consumption demand. More generally, we argue that corporate sector behavior is crucial to an understanding of trends in income distribution and aggregate demand in different countries. We hypothesize that the institutional differences between, simply put, the family-controlled German Mittelstand firm and the shareholder-value-oriented US stock company go a long way to explain why top household income shares have exploded in the United States but not in Germany since the 1980s, whereas the wage share has fallen substantially in Germany but not in the United States, although both countries confront similar technological change and globalization as well as financial and labor market liberalization. As they affect the income and hence the net lending positions of the household and corporate sectors, the financial decisions of the corporate sector are crucial to the analysis of aggregate demand regimes.

An important weakness of the financial balances approach is that it does not say much about the determinants of growth per se. Because the financial balances of the household, corporate, government, and foreign sectors must always, by definition, sum to zero, any level of sectoral net lending or borrowing in principle can be consistent with any growth rate. In this article, therefore, we do not have a stance, for example, on the debate over whether nominal wage restraint has boosted German exports, as argued by Baccaro and Benassi, or whether wage suppression has actually been damaging to Germany’s aggregate performance, as suggested by Servaas Storm and Ro Naastepad. 60 Rather, we have looked at how Germany’s positive net exports (associated with a current account surplus and net capital exports) were reflected in the financing positions of the household, corporate, and government sectors.

From a macroeconomic perspective, both the export-led growth model of Germany and the debt-led growth model of the United States, important contributors to the global current account imbalances, were also important contributing factors in the global financial crisis of 2008. It is quite likely that the trickle-down consumption hypothesis has ceased since the outbreak of the crisis to be an accurate description of the saving behavior of households in the United States. The rise in household debt has turned out to be unsustainable, and it seems unlikely that private consumption will once again become the main driver of aggregate demand growth without a stronger growth of middle-class incomes. 61 Similarly, Germany’s current account surplus will not be compatible with macroeconomic and political stability at the European and global level. As Baccaro and Pontusson put it, growth regimes are “numerous and unstable” 62 and contingent on specific historical circumstances. Future research needs to analyze the macroeconomic conditions for more stable growth models.

A further important avenue for future research has been highlighted by Baccaro and Pontusson: politics needs to be introduced into the growth model perspective in a more systematic fashion. 63 The basic intuition is that growth models are supported by clearly identifiable coalitions of social forces (“social blocs”) that defend particular growth models in the name of the “national interest.” We certainly agree with Baccaro and Pontusson that in the case of Germany, export-oriented manufacturing firms and what is left of the worker aristocracy of skilled workers constitute a cohesive and dominant social bloc in this sense. That view is also consistent with the income distribution data reported in this article, that is, the relative constancy of top household income share and the D9/D5 earnings ratio and the strong fall in the wage share and rise in the D5/D1 earnings ratio. More generally, the comparison of income distribution trends in Germany and the United States shows how much (corporate) elites can shape social and macroeconomic outcomes. Put bluntly, in the United States top corporate management elites have used their increased bargaining power to maximize their own individual incomes and, as consumers, put pressure on the rest of society to reduce saving and go deeper into debt by raising consumption norms. In Germany, the influential group of owner-managers, faced with a similar increase in bargaining power, have renounced ostentatious individual lifestyles but accumulated financial wealth for their family-owned businesses and thereby restrained the development of domestic demand. An important question for future research is, How are cross-country institutional differences, as emphasized by the VoC literature, in such areas as the public provision of positional goods and credit market regulations, systems of skill formation, and the shareholder-value orientation of corporations related to the interests of dominant social blocs in different countries? As this article has shown, such institutional factors, which persist despite similar neoliberal trajectories in most countries, are crucial to an understanding of both country-specific patterns of income distribution and macroeconomic growth models.

Footnotes

Appendix A

Description of Data.

| Variable | Definition | Source |

|---|---|---|

| Top income share | Top income share of fiscal income | WID |

| Adjusted wage share | Adjusted wage share of the total economy in percentage of GDP at total factor cost | AMECO |

| Gini coefficient | Gini coefficient of equivalized household market income | SWIID |

| Decile ratios | Earnings ratios ninth (P90), fifth (P50), and first (P10) upper decile limits of gross earnings, full-time dependent employees | OECD |

| Current account balance | Current account balance in percentage of GDP | AMECO |

| Household financial balance | Household financial balance in percentage of GDP | AMECO, OECD |

| Corporate financial balance | Corporate financial balance in percentage of GDP | AMECO, OECD |

| Government financial balance | Government financial balance in percentage of GDP | AMECO, OECD |

| CENT | Summary measure of centralization of wage bargaining | ICTWSS |

| Corporate gross saving | Gross saving in percentage of GDP | AMECO |

| Corporate gross capital formation | Gross capital formation in percentage of GDP | AMECO |

| Stock market capitalization | Stock market capitalization in percentage of GDP | WDI |

| Household debt | Household debt in percentage of GDP | BIS |

| Job tenure | Job tenure of ten years and more, in percentage of total employment | OECD |

| Long-term unemployment rate | Long-term unemployment rate (twelve months or more) | OECD |

| Hours worked | Average usual weekly hours worked in percentage of total hours worked | OECD |

| Health spending | Health spending in percentage of GDP | OECD |

| Public health spending | Public health spending in percentage of total health spending | OECD |

| Social transfers | Social transfers in kind in percentage of GDP | AMECO |

| Government structural balance | Government structural balance in percentage of potential GDP | WEO |

| Output gap | Output gap in percentage of potential GDP | WEO |

Appendix B: The Neo-Kaleckian Model and the Relative Income Hypothesis

Acknowledgements

We would like to thank participants at the annual conference of the Forum for Macroeconomics and Macroeconomic Policies in Berlin, at the workshop “Rethinking German Political Economy” in San Francisco, and at the annual conference of the Society of the Advancement for Socio-Economics in Kyoto for helpful comments on previous versions of this research.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.