Abstract

Can political parties, social movements and governments influence market outcomes and shape the functioning of a capitalist economy? Is it possible for social democratic parties, and the labour movement in general, to promote a significant redistribution of income in favour of labour? According to proponents of the structural dependence thesis, the answer to both questions is negative, because the structural dependence of labour upon capital severely constrains feasible income distributions. This article provides a long-run analysis of the UK, which casts doubts on the structural dependence thesis. There is some evidence of a short-run profit-squeeze mechanism, but income shares are much more variable in the long-run than the structural dependence argument suggests, and the power resources available to social classes are among the key determinants of distributive outcomes.

Introduction

A foundational question in political economy concerns the nature of the interaction between politics and markets. To what extent can political parties, social movements and governments influence market outcomes and shape the functioning of a capitalist economy? More specifically, given the inherent tendency of unfettered markets to yield major income and wealth inequalities, is it possible for social democratic parties, and the labour movement in general, to promote a significant redistribution of income in favour of labour?

According to a prominent tradition comprising both neo-pluralist (Lindblom, 1997, 1982; Stone, 1980) and neo-Marxist authors (Block, 1977; Coates, 1975; Offe, 1984), the margins of intervention are extremely narrow, due to the unique power of business in capitalist economies. Capitalists do not need to organize and lobby in order to influence decisions: they enjoy a structural power which derives from their control over investment. If governments try to implement any policies or reforms that damage capitalist interests and undercut profitability or business confidence, profit-maximizing capitalists respond by reducing investment and thus economic activity. To the extent that economic activity matters for electoral outcomes, this severely reduces the margins for reforms, and it is why the market might be characterized as a prison. For a broad category of political/economic affairs, it imprisons policy making, and imprisons our attempts to improve our institutions. It greatly cripples our attempts to improve the social world because it afflicts us with sluggish economic performance and unemployment simply because we begin to debate or undertake reform. (Lindblom, 1982: 329)

In the last two decades, the structural power of business has played a key role in explanations of the declining ambitions and influence of social democratic parties. As Glyn (2001: 1) remarked, ‘At the turn of the century more parties of the Left were in government in advanced capitalist countries than ever before, including, for the first time ever, those of the four largest West European countries’ and yet this only brought ‘modest shifts in economic policy’. This persistent ineffectiveness, compounded by the electoral decline of socialist parties across Europe, has led even prominent social democratic theorists to emphasize the structural limits that capitalism places on redistributive policies and reforms (Streeck, 2014). But the structural power of business has also played a central role in analyses of financialization and globalization (Bell, 2012; Krippner, 2011; Panitch and Gindin, 2014; Roos, 2019; Starr, 2019). ‘Indeed, the financial crisis revived the structural power debate’ (Woll, 2016: 375).

However, the structural power of capitalists does not constrain only government actions. In a series of seminal contributions, Przeworski (1985, 1991), Przeworski and Sprague (1986) and Przeworski and Wallerstein (1988) have argued that there is an irreversible tendency that makes it impossible in capitalist democracies in the long-run to promote significant changes in the distribution of income in favour of labour, let alone any socialist objectives. While the immediate interests of capitalists and workers are in conflict in the short-run (higher profits lead to lower wages, and vice versa), this is not true in a dynamic context, because in a capitalist system profits are the engine of growth, and growth delivers (at least potentially) higher welfare in the future. It is this mechanism that is the material basis of workers’ consent to capitalism and thus of capitalist hegemony, since it explains why, faced with the likely high costs of transition to socialism, self-interested rational workers will support capitalism: capitalism promises continued welfare growth.

Furthermore, when socialist parties and the labour movement forsake revolutionary strategies, they inevitably enter into an economic logic of class compromise. In order to gain the future benefit of returns to investment, they must forego any significant expropriation of profits today. Both high levels of taxation imposed by a sympathetic government and the promotion of working-class militancy through class struggle are counterproductive, because each will generate a profit-squeeze mechanism: low profits lead to a reduction in investment, which implies lower employment today and lower production and wages in the future. Changes in the distribution of income, either via a welfare state or via bargaining and conflict, are severely constrained. The working class is, therefore, structurally dependent upon capital, an argument summarized as ‘the structural dependence thesis’ (SDT).

Przeworski’s theory is extremely influential, and his conclusions widely debated. It is difficult to underestimate the theoretical and policy implications of the idea that the structural features of private ownership economies severely constrain the range of attainable distributions of income.

Przeworski has formalized some key intuitions of the neo-pluralist and neo-Marxist literature, extending the analysis of the structural power of capital beyond policy-making stricto sensu, but the basic idea is shared by many authors belonging to very different traditions. It also lies at the heart of neoliberal approaches and provides the foundations for criticisms of social democratic parties, the welfare state and Keynesian policies.

Furthermore, SDT has strongly influenced policy debates and the elaboration of political programmes. German chancellor Helmut Schmidt famously remarked, ‘The profits of enterprises today are the investments of tomorrow and the investments of tomorrow are the employment of the day after’ (quoted by Glyn, 2001: 16). More recently, Wickham-Jones (1995, 2003) has shown that during the 1990s and 2000s, the UK Labour Party (first in opposition and then in government) formulated policy programmes explicitly on the basis of a belief in SDT.

Yet there is little empirical evidence that definitively supports the idea that income distribution in capitalist economies is severely constrained, for empirical analyses of SDT are few and inconclusive. Existing studies focus in the main on redistributive policies in order to ascertain the existence of limits to government policies either by examining differences in choices under different governments, 1 or by considering the limiting cases of governments elected with radical programmes (e.g. Allende’s Chile or Manley’s Jamaica). According to Przeworski and Wallerstein (1988), such empirical analyses of SDT are uninformative because they ‘cannot speak to the issue of limits and possibilities’ (Przeworski and Wallerstein, 1988: 14). On the one hand, differences in policies would not prove much about ‘the existence of structural constraints that bind all governments. We cannot know whether the observed differences exhaust the realm of possibility’ (Przeworski and Wallerstein, 1988: 14). On the other hand, the issue of ‘possibilities cannot be determined on the basis of limited historical experience’ (Przeworski and Wallerstein, 1988: 14).

Those doubts about empirical tests of SDT that cannot distinguish between actual and possible choices are cogent. Trying to test choices generally involves counterfactual statements about what could have been done, and these are notoriously difficult to pin down. Yet to move from these problems to advocating a purely theoretical analysis of SDT, by constructing ‘a formal model with which the internal logic of the theory can be explored’ (Przeworski and Wallerstein, 1988: 14) is both doubtful and unwarranted. It is doubtful because while SDT is a theoretical construct to explain the empirical world, the claim by Przeworski and Wallerstein suggests that it cannot be subjected to empirical scrutiny. Taken literally, this claim would place SDT in the realm of metaphysics. It is unwarranted because the examination of isolated historical episodes and of government choices does not exhaust the content of possible empirical tests. Indeed, although limiting cases of radical redistributive policies are interesting, it is the ‘more routine political–economic interactions that serve as a crucial test of the generalized form of [SDT]’ (Swank, 1992: 39).

This article analyses the core claims of SDT empirically. In order to circumvent the above objections, the empirical analysis proposed does not focus on actual or possible choices of the actors in the economy, but tries to trace the effects of the structural dependence of labour upon capital on income distribution. We investigate whether there is indeed a basic distributive trade-off and what its characteristics are. Instead of evaluating whether policy choices co-vary with the partisan orientation of cabinets in a cross-sectional context, we analyse the dynamics of distributive conflict by focusing on the time series of UK data from the end of the nineteenth century in order to understand the behaviour of the pre-tax functional distribution of income.

There are two main reasons to focus on the functional distribution of income in the context of our analysis. First, SDT focuses primarily on the income distribution between classes, and emphasizes the central role of profits, and of the share of income accruing to capitalists, in private market economies. Although not all aspects of the relations between employers and employees should be viewed as a zero-sum conflict (Korpi, 2006; Wright, 2000), empirically a focus on the functional distribution of income allows us to derive some precise testable propositions and to examine the conflictual dimension of the interaction between classes, and the existence of the distributive trade-offs postulated by SDT, in the starkest possible form. 2

Second, SDT is a theory of the constraints that private control of investment imposes on any attempts to change the distribution of income: markets act as a prison leaving little margin to politics. This includes, but is not limited to, redistributive policies: taxation policy and welfare state provisions are only some of the means that can be used to alter market outcomes. Our focus on the pre-tax income distribution underlines a much broader set of policies and institutional factors – product and labour market regulations, trade union laws, restrictions on capital flows, regulation of the financial sector and so on – with significant distributive implications. Changes in the functional income distribution should be considered – we shall argue – as a fundamentally political phenomenon.

In the context of our analysis, the key difference between different types of policies is the time scale at which they operate. Changes in tax rates and welfare state provisions can be seen as short-to-medium run policies, whereas transformative political decisions involving the basic legal and institutional framework in which economic actors operate have long-term effects. SDT has relevant, but distinct, implications for both types of political interventions on markets. This motivates our longitudinal approach and, unlike the existing empirical literature on SDT, we shall draw a fundamental distinction between short-run dynamics and long-run tendencies.

While a focus on the functional distribution of income allows us to capture the core mechanism linking private control of investment, economic activity and distributive outcomes in SDT, it is important to stress at the outset that we do not provide a comprehensive empirical evaluation of all aspects of the privileged position of business in capitalist societies. Theories of the structural power of capitalists are arguably much richer and include, for example, a strong ideational dimension, which is not captured in our analysis. 3

SDT: Two Testable Propositions

Consider a stylized account of class conflict over distributive shares in the process of capitalist accumulation. Investment increases employment, which in turn increases the bargaining strength of the working class, and increases the wage share in value added. The corresponding falling profit share reduces investment, hence employment and hence the bargaining strength of the working class. This recreates the profitability conditions necessary for renewed accumulation, investment rises and the cycle repeats. This is the mechanism originally analysed by Przeworski (1985) and it can be considered as the canonical model of the profit-squeeze cycle underlying SDT.

There are many possible ways of formalizing this mechanism by considering specific causal links between the variables, thus deriving different versions of the profit-squeeze cycle. 4 For example, Block (1977) emphasizes the role of labour-saving technical change in restoring profitability, while Offe (1984) focuses on Kalecki’s notion of ‘business confidence’ in determining investment decisions. However, we do not wish to analyse a specific formalization of SDT, and so we keep our analysis at a general level. Indeed, the stylized account above identifies the two key variables of the analysis, the wage share (in value added) and the employment rate (employees to workforce), postulating a cyclical interaction between them, and is sufficient to formulate our hypotheses.

At a general level, if SDT is correct and relevant, the range of income distributions attainable in capitalist democracies should be narrowly circumscribed.

No government . . . can reduce the share of income that owners of capital consume. Any additional income for wage earners, whether it consists of wage gains won at the bargaining table or as transfer payments won through election, reduces total investment, dollar for dollar. (Przeworski and Wallerstein, 1988: 16; see also Lindblom, 1982: 327)

Attempts to redistribute income should therefore only yield short-run temporary effects. Two issues are thus of considerable interest in evaluating SDT: first, whether there has, in fact, empirically been a profit-squeeze mechanism; and second, the behaviour of the long-run income distribution.

Consider the first issue. A scatter plot of the employment rate (on the vertical axis) against the wage share (on the horizontal axis), with scatter points considered sequentially in time, should generate a clockwise path if it is to represent a profit-squeeze mechanism. In the wage share (WS) – employment rate (ER) space, we call these clockwise movements WSER cycles. Thus, focusing on the short-run, a first simple test of SDT can be formulated.

The latter pattern would derive from attempts to redistribute income by trade unions or social democratic parties when in power; the former would emerge in the absence of such attempts (for example, because of an awareness of their futility, given SDT).

It is less immediate to derive precise, testable propositions concerning the behaviour of the long-run income distribution according to SDT. Both neo-pluralist and neo-Marxist accounts of the structural power of capital focus on changes in distributive variables due to government policies or labour militancy, but do not provide an explanation of the long-run equilibrium distribution. Thus, according to Lindblom (1977: 170–175), the key criterion for businessmen’s decisions is whether the rate of return on investment is sufficient or not. Similarly, Przeworski (1985: 43) posits a mechanism whereby ‘if profits are not sufficient then eventually wages or employment must fall’. Lacking a proper definition of ‘sufficient’ profits, however, the explanatory power of these claims is limited, as they are consistent with an infinity of values of ‘sufficient’ profits. In the absence of an explanation of capitalists’ expected or ‘normal’ profits, SDT is at best underdetermined. 5

From the viewpoint of empirical testing, this omission would not be excessively problematic if actual distributive shares varied within a narrow range. Indeed SDT can be interpreted as predicting that ‘within a very narrow range . . . all [distributive] outcomes are equally possible, outside of this range they are nearly impossible’ (Przeworski, 1985: 162).

If, however, long-run income shares were not constrained ‘within a very narrow range’, then the question would be whether an explanation of the determinants of long-run income distributions (i.e. of the level of ‘sufficient’ profits, or of ‘business confidence’) can be provided which is consistent with the key insights of SDT. For even if Hypothesis 1 were shown to be true, and a profit-squeeze mechanism were operating at any point in time, this would not provide decisive support to SDT. Profit-squeeze cycles are consistent with an infinity of equilibrium income shares and if governments, or unions, could significantly alter the long-run income distribution, then SDT would be false – or at best correct but irrelevant. For SDT to be correct, and relevant, one needs a theory of long-run changes driven (entirely or mostly) by forces that are completely independent of government policies and distributive conflict (such as exogenous technical change or some Malthusian population mechanism).

The previous observations help us formulate the second testable hypothesis.

Empirical Strategy

We test Hypotheses 1 and 2 focusing on the UK as our case study. As a canonical example of a ‘liberal market’ or ‘pluralist’ economy (Hall and Soskice, 2001; Korpi, 2006), 6 and given the influence of SDT on policy-making mentioned above, the UK should be an excellent test for the theory; indeed, it is so analysed in much of the literature (King and Wickham-Jones, 1990; Wickham-Jones, 1995, 2003). Given the key distinction between short-run changes and long-run trends, it is obviously desirable to obtain as long a run of data as possible; and so we examine the period 1892–2018.

We use a mixed-methods approach. In the section ‘Distribution and Conflict in the UK: Descriptive Analysis’, we provide a detailed descriptive analysis of the co-movement of the wage share and employment rate in the UK over the period 1892–2018. The wage share variable is the ratio of total employee compensation to gross domestic product. The employment rate variable is the ratio of employees in employment to the sum of total employment and unemployment (the latter based on standardized international definitions and not on the administrative criteria of the claimant count). 7 In order to distinguish short-run movements from long-run trends, we use a Hodrick–Prescott filter. If trend values are interpreted as proxies for the long-run values of the two variables, this allows us to check whether the income distribution has remained ‘within a narrow range’ (Hypothesis 2). Analysis of deviations from the trend allows us to track short-run changes in income distribution and check for the existence of profit-squeeze cycles (Hypothesis 1).

In the section ‘Power, Conflict and Distribution: A VECM Approach’, we develop a formal econometric analysis of the long-run variability of distributive outcomes for the UK. The aim is not to provide an exhaustive explanation of the determinants of the wage share and the employment rate, which have been the subject of a vast debate (see, e.g. Kristal, 2010 and the literature therein). Rather, our purpose is to test SDT, and in particular its predictions concerning the long-run movement of distributive shares (Hypothesis 2). To be specific, contrary to the key tenets of SDT, and in line with a long-standing tradition in social theory, 8 we suppose that the power resources available to social classes in the economic and political spheres are important determinants of distributive outcomes, and that different equilibria correspond to different configurations of the balance of power between the two classes.

In the empirical power resources literature, various measures of working class power in the labour market (unionization, labour law, collective bargaining institutions), in the workplace (work councils, co-determination), and in the political sphere (strong labour parties, participation of the Left in government) explain a significant part of cross-national differences in the structure and development of welfare states (Bradley et al., 2003; Esping-Andersen, 1985; Korpi, 1983, 2006) and even important macroeconomic outcomes, such as inflation and unemployment (Cameron, 1984; Korpi, 1991). But a power resources approach also provides a general framework in which to analyse class relations and distributive conflicts (Korpi and Palme, 2003). From this perspective, the main actors in the economy are ‘expected to organize for collective action in political parties and unions to modify conditions for and outcomes of market distribution’ (Korpi, 2006: 173). That is, classes use their power both to alter income distribution in the short-run, given a certain structure of trade-offs, and to modify that structure of trade-offs in the long-run.

We consider trade union density as the primary empirical measure of the bargaining strength of the working class. From a theoretical viewpoint, the key dimension of workers’ power lies precisely in their ability to act collectively as a class, and unionization is the most basic form of workers’ collective organization both in the labour market and in the workplace (Korpi, 1991; Korpi and Palme, 2003; Rothstein, 1984; Wright, 2000). Trade union density captures working class strength better than indices of strike activity: there is no clear relation between conflict and organizational strength, because strength or power is a property, not an act, and powerful actors might not need to exercise it. Unionization is a causally important variable in the analysis of distribution and class conflict in a number of approaches across the social sciences (see, for example, Jaumotte and Osorio, 2015; Pontusson, 2013, and the literature therein). 9 Indeed, in empirical studies of pre-tax income distribution, other measures of working class power often turn out to be insignificant after controlling for unionization (see, e.g. Bradley et al., 2003: 216ff). Finally, and pragmatically, for most of the variables used in cross-national studies – such as collective bargaining coverage, employment protection or the existence of work councils – there exist no reliable data covering the entire historical period. 10

We suppose that increases in the power resources of one class have positive, long-lasting effects on the share of income that goes to that class. In particular, and contrary to SDT, we expect union strength to be positively associated with the wage share. We use a vector error correction model (VECM) to investigate the long-run dynamics of income distribution and test whether there exists interaction and a common dynamic between wage share, employment rate and trade union density in the UK since 1892.

11

In the profit-squeeze mechanism, economic activity plays a key role in linking distribution (the wage share) and the employment rate. Therefore, in our analysis, we also include the logarithm of Gross Domestic Product,

Distribution and Conflict in the UK: Descriptive Analysis

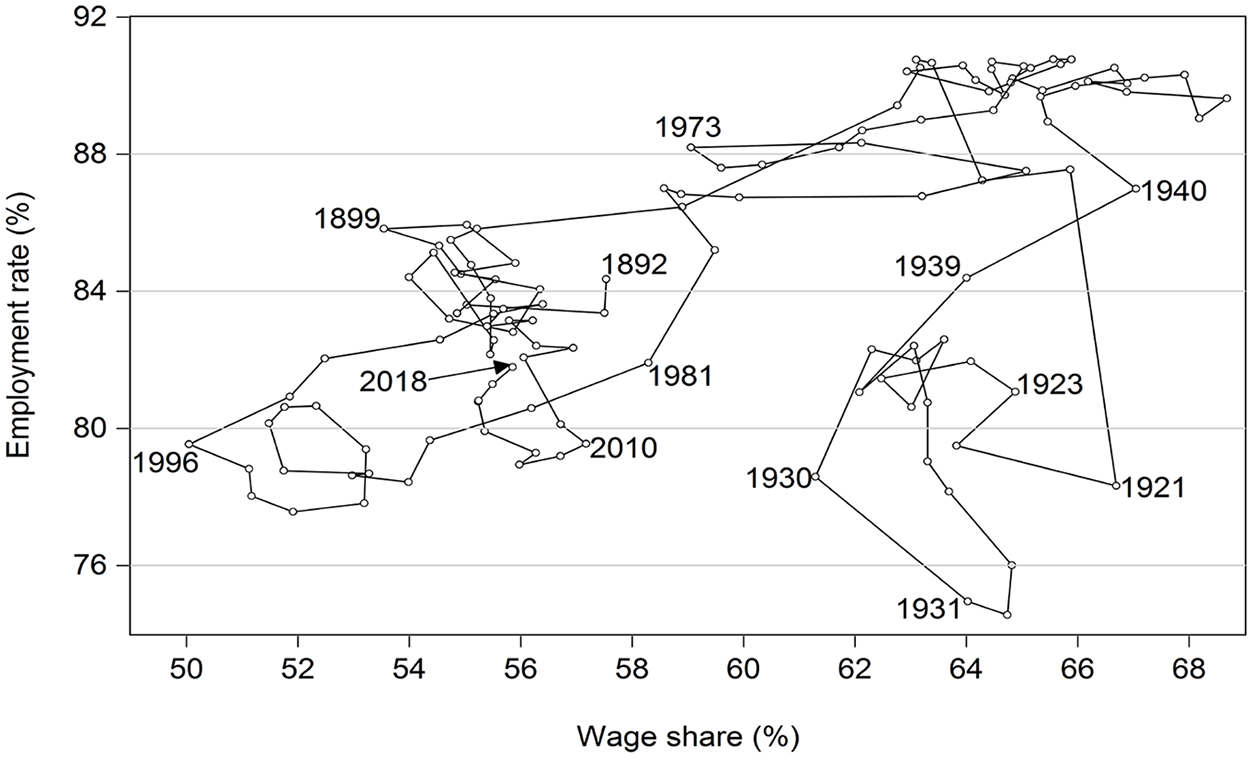

Figure 1 plots the annual values of the wage share and the employment rate in the UK. 12 On the face of it, this evidence is not encouraging for SDT: there is no tightly determined income distribution and the wage share is rather variable, a well-known empirical finding (Kristal, 2010). The wage share varies between 50% (in 1996) and 68.7% (in 1947); the employment rate between 74.6% (in 1932) and 90.8% (in 1955). Although the data do not accurately describe a uniform profit-squeeze cycle, some have interpreted them as describing an erratic long-run cycle (see for example, Flaschel, 2008). This interpretation is unconvincing: a single cycle of over 100 years is not a periodic motion, and if a profit-squeeze mechanism is at work, it is not plausible that it takes six generations to complete. Besides, this would not rescue SDT: if profitability is only restored after some 125 years, worker gains could hardly be considered ephemeral.

Employment Rate Against Wage Share, UK, 1892–2018.

This is however a rather crude test. As argued in the section ‘SDT: Two Testable Propositions’, a clear distinction should be drawn between the long-run and the short-run. In the long-run, the wage share and the employment rate may vary because of long-run processes – such as technical change and institutional changes – that continually modify the political–economic equilibrium. The WSER cycles are then the shorter-run cycles that appear around the long-run motion, and are subject to continual displacement. If SDT is valid, then either random deviations or stable WSER cycles should be visible in the short-run (Hypothesis 1), and most of the variability in the data should derive from these short-run movements around (reasonably) constant long-run values of the two variables (Hypothesis 2).

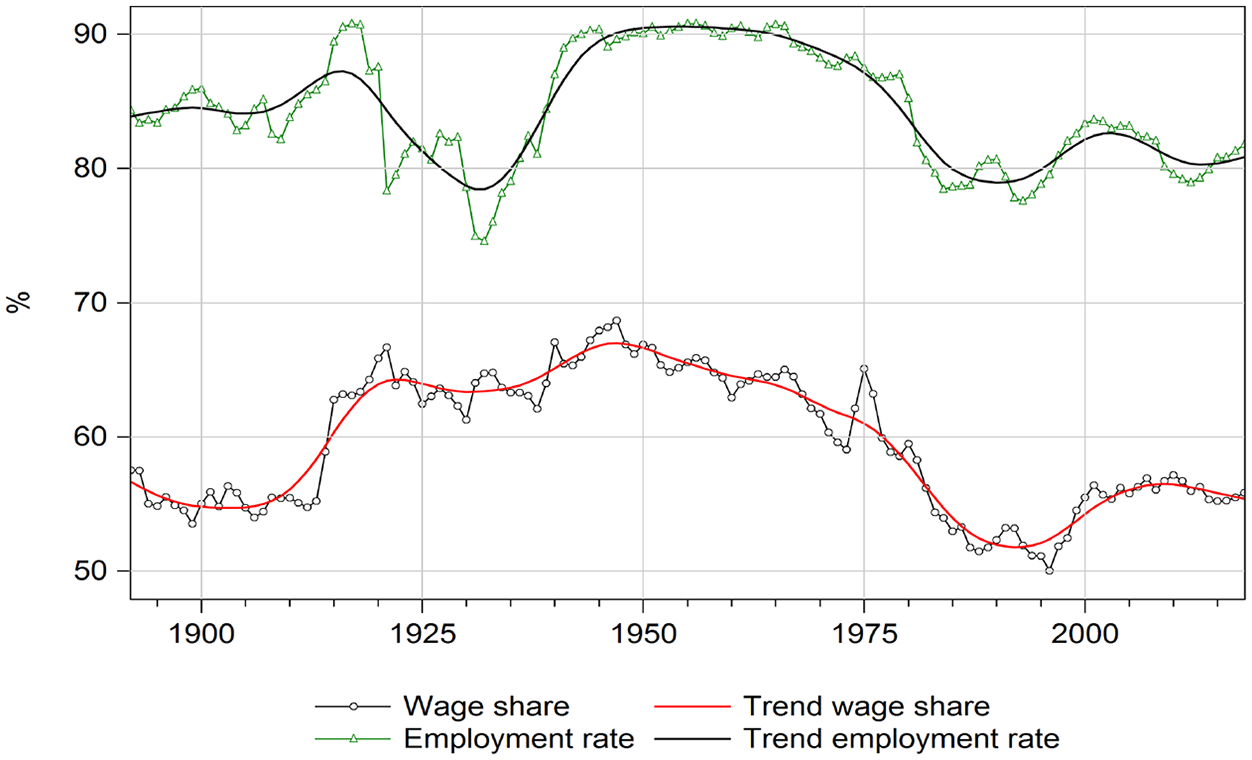

In order to evaluate SDT in these terms, we filter the data to distinguish between short-run fluctuations and long-run changes. We use the Hodrick–Prescott filter with a value of 100 for the smoothing parameter. The time paths of the annual values of the wage share and the employment rate (total and trended) are shown in Figure 2.

Wage Share and Employment Rate, UK, 1892–2018.

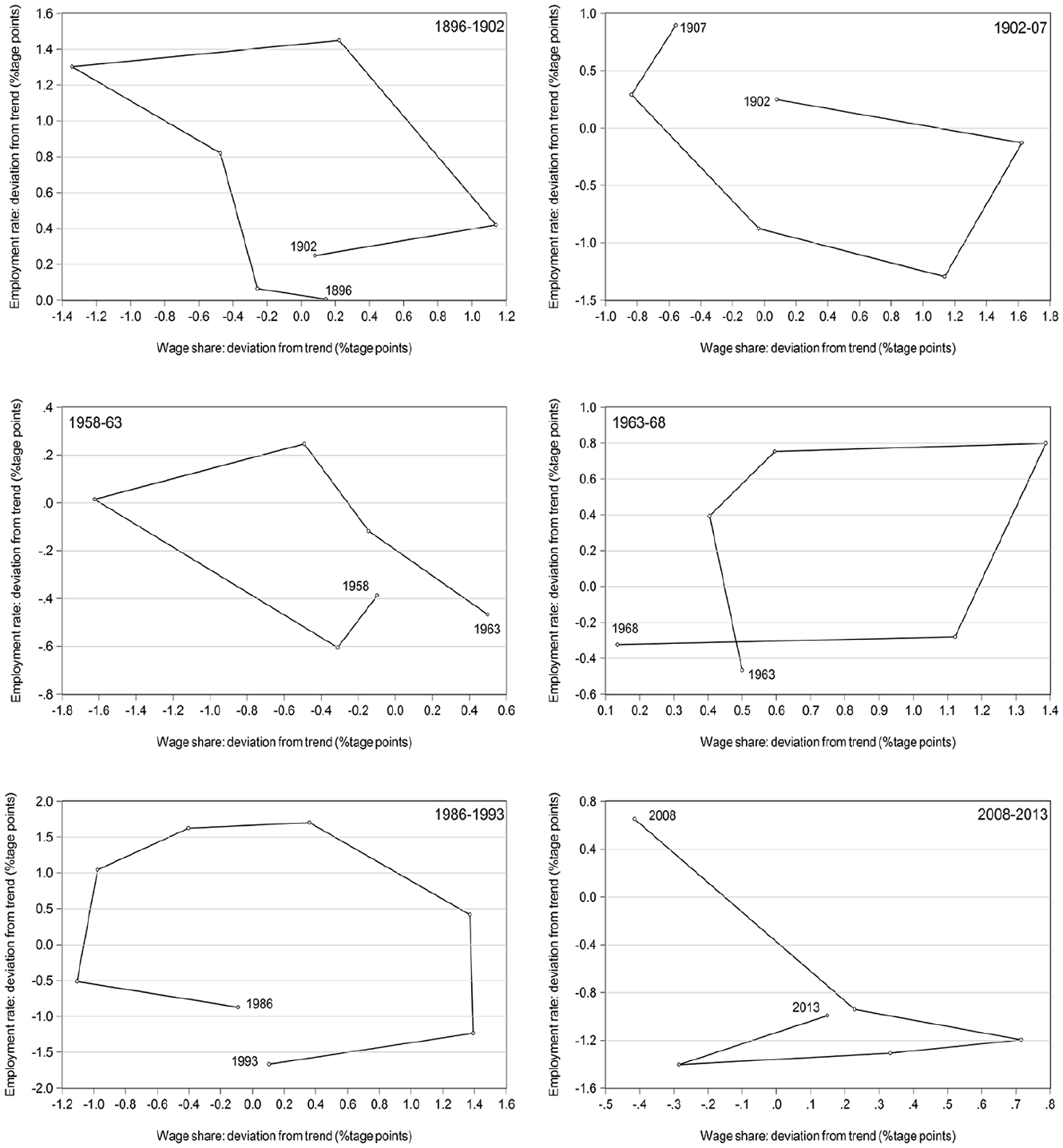

First, we investigate visually whether the scatter plots of deviations from trend display a cyclical motion. For each variable, its cyclical value is the percentage points difference between the raw data and its trend value. Figure 3 displays illustrative examples of such short-run cycles, two from the pre-1914 era, two from the 1945–1973 (‘golden age’) period and two from the neoliberal era after 1979. 13 Over the whole period, there are 21 cycles, of which 15 display clockwise movements (covering the years 1892–1914, 1925–1930, 1947–1981, 1986–2002 and 2008–2018); five display anti-clockwise movements (covering the years 1914–1924, 1930–1947 and 2002–2008); and one is just erratic (1981–1986). So the pattern is mixed. For about 30% of our sample, SDT appears not to work. But visual inspection suggests that for about 70% of the sample, the data do indeed describe a repetitive (clockwise) cyclical process, yet with cycles that are very variable in both amplitude and periodicity (witness the different axis scales in Figure 3). Data of these years are broadly in line with the basic intuitions of SDT; at any given time, an increase in the wage share triggers a profit squeeze, and after an increase in unemployment weakens workers’ bargaining power, profitability is restored.

UK WSER Cycles: Some Examples.

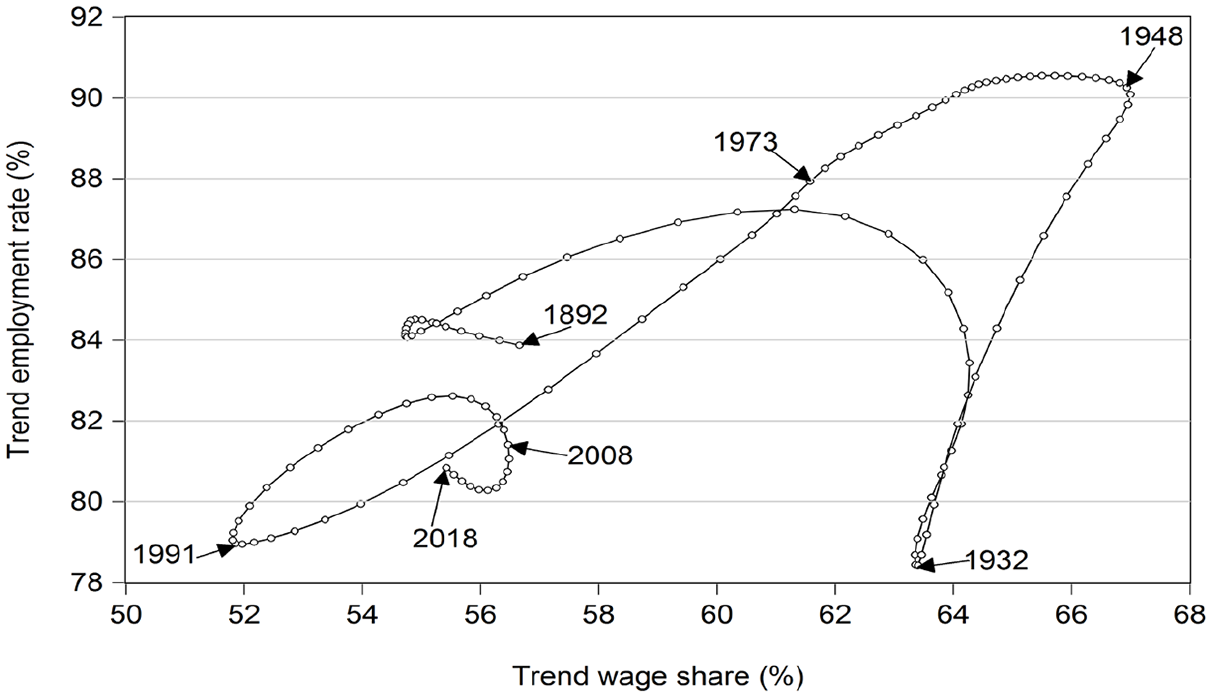

However, this provides only a partial picture of distributive conflict. As noted above, SDT is not just about short-run trade-offs: it is primarily a theory of the constraints on feasible long-term equilibrium distributions. The long-run dynamics of the wage share and the employment rate are shown in Figure 4, which depicts a connected scatter of their trend values.

Trend Employment Rate Against Trend Wage Share, UK, 1892–2018.

The long-run movement of the variables can be thought of as depicting changes in their equilibrium values, after purely erratic or cyclical fluctuations are purged from the data. The short-run WSER cycles of the type shown in Figure 3 move along a long-run trend, and it is this trend that has to be interpreted by SDT, for visual inspection shows that the set of attainable equilibrium values of the wage share and employment rate are by no means ‘within a very narrow range’, even after all temporary and cyclical movements have been eliminated.

Indeed, rather than a single mechanism determining an equilibrium income distribution over the whole period, Figure 4 shows several periods reflecting significant changes in the political–economic equilibria of UK capitalism. The last years of the nineteenth century saw a falling trend wage share, followed by a rising trend wage share to the early 1920s, both with only a slowly rising trend employment rate. The 1920s saw falling trend wage shares and employment rates till 1931 followed by rising trend wage shares and employment rates till 1947. The ‘golden age’ divides into two phases, 1947–1960 with a gently rising trend employment rate and a falling trend wage share, and 1960–1973 with a falling trend employment rate and wage share. Following the collapse of the ‘golden age’, 1974–1991 sees much steeper falls in the trend wage share and employment rate; both of which then rise through the 1990s to 2004, and then fall thereafter. These changing patterns are much more challenging for SDT to interpret.

In summary, there is indeed some evidence of a short-run profit-squeeze mechanism as predicted by SDT but there is significant variability of the long-run income distribution that is prima facie inconsistent with SDT. While eyeballing the data is not encouraging for SDT, the question arises as to whether a satisfactory explanation of this empirical evidence can be provided which is broadly consistent with SDT. This is addressed in the next section.

Power, Conflict and Distribution: A VECM Approach

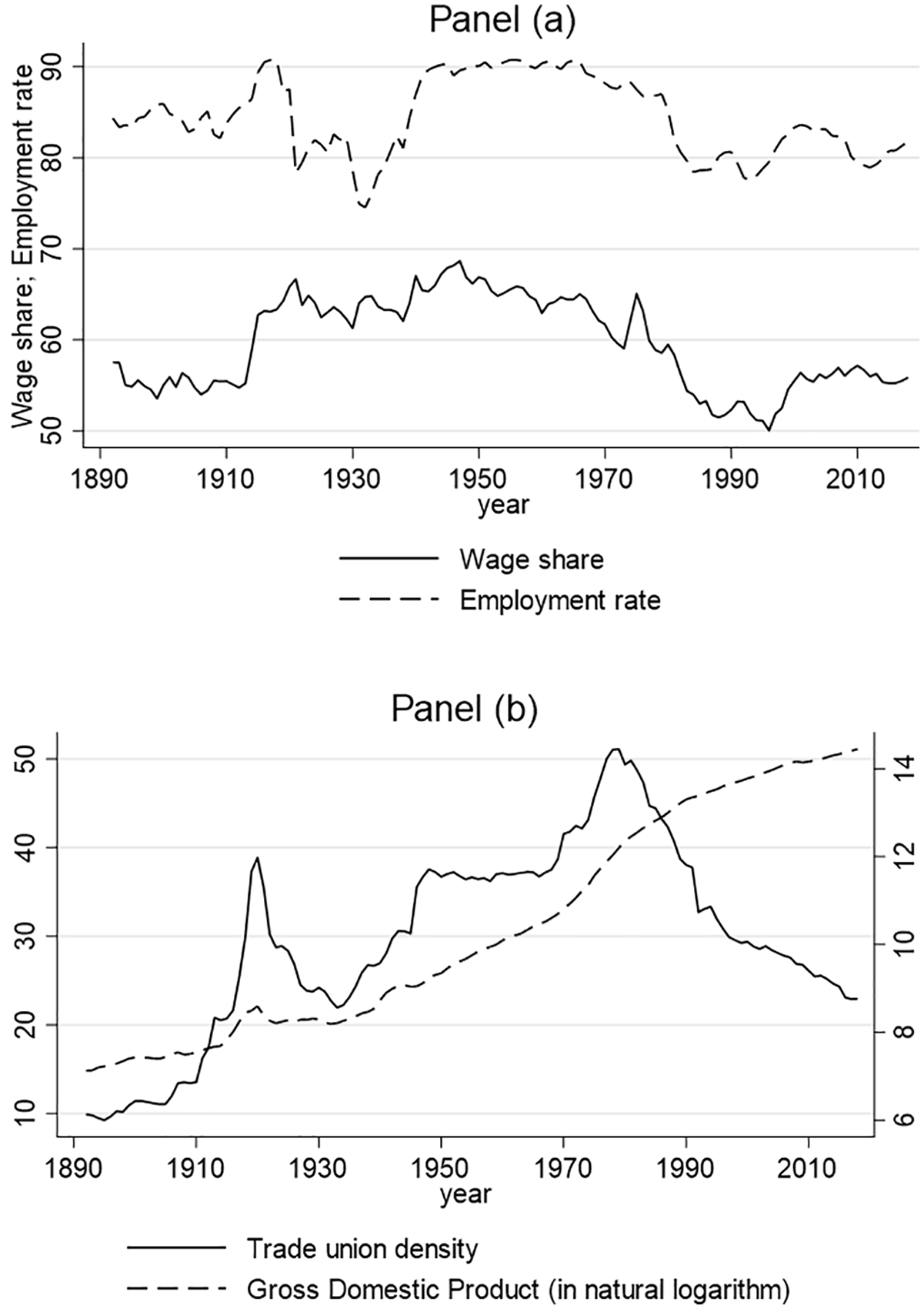

We use a VECM to test whether there exists an interaction and a common dynamic between wage share, employment rate and trade union density in the UK since 1892. Our annual data comprise 127 yearly observations from

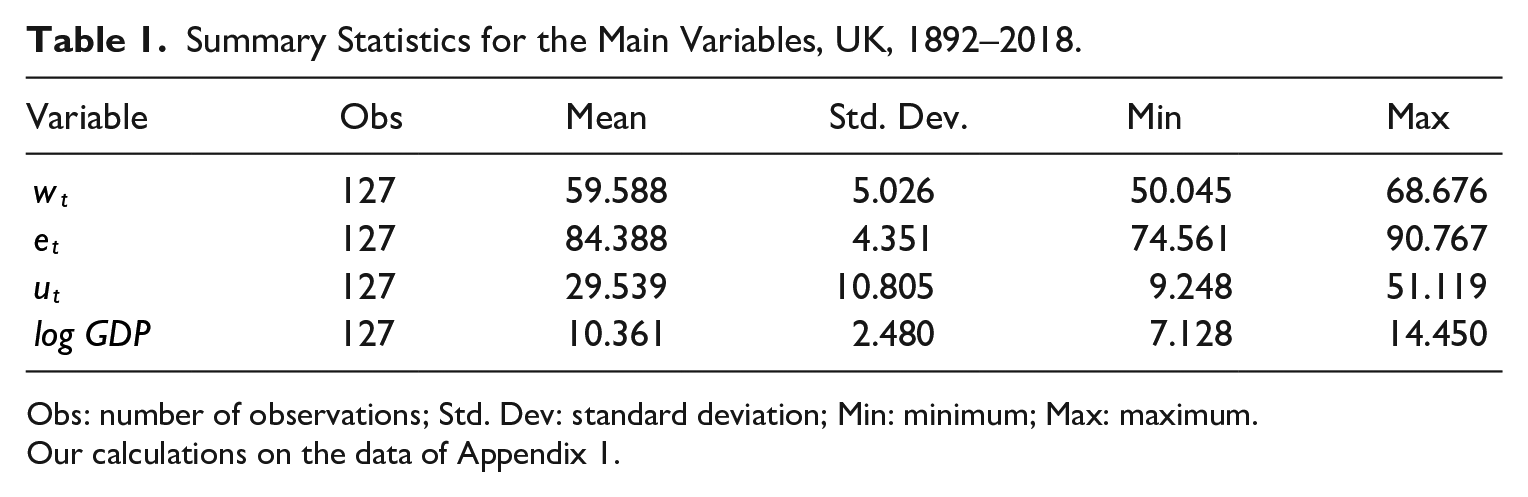

Basic summary statistics of all variables are provided in Table 1. The time paths of the wage share (

Summary Statistics for the Main Variables, UK, 1892–2018.

Obs: number of observations; Std. Dev: standard deviation; Min: minimum; Max: maximum.

Our calculations on the data of Appendix 1.

The Pattern of the Main Variables, UK, 1892–2018.

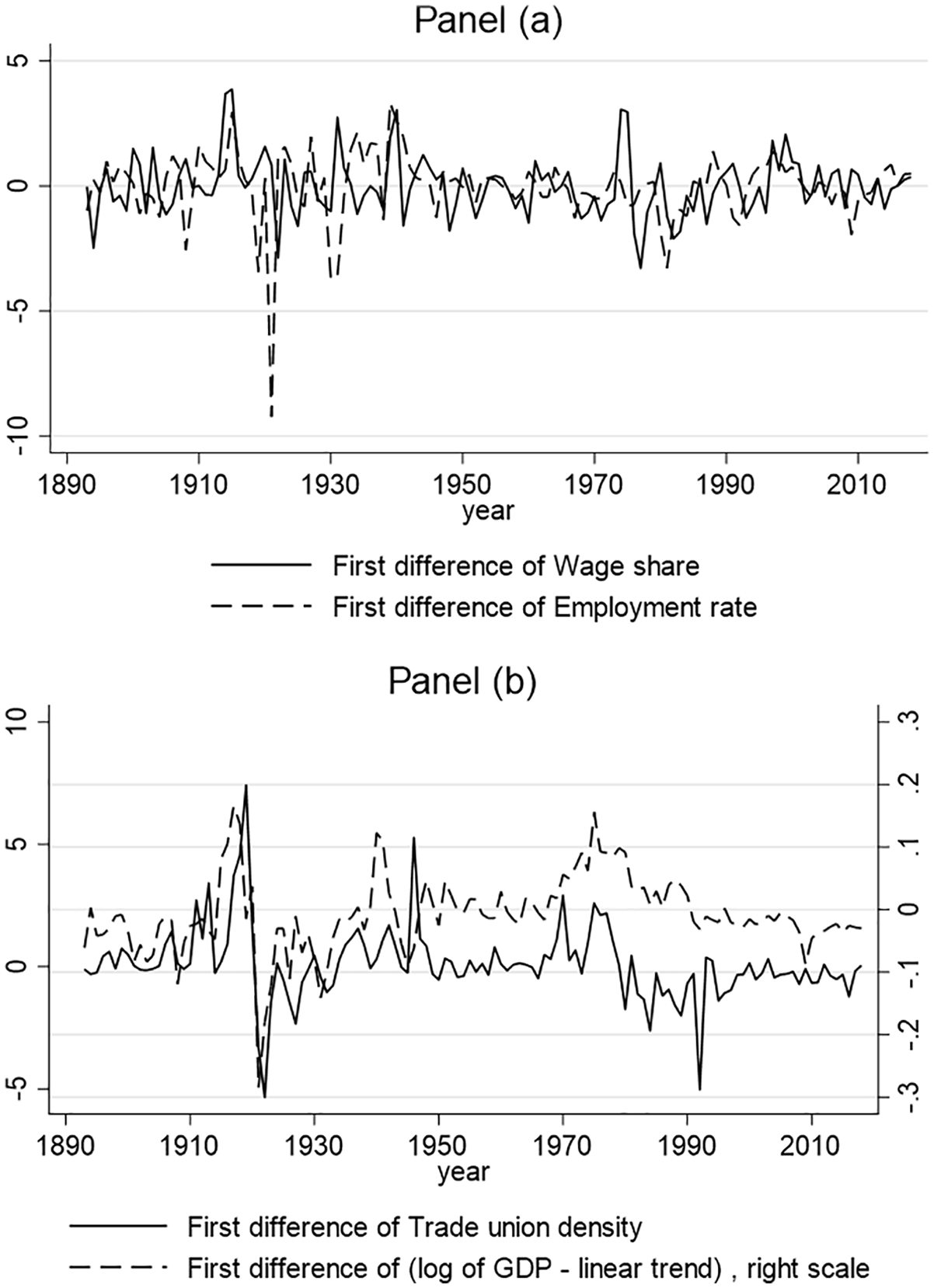

Visual inspection suggests that all four variables are nonstationary. We investigate whether the single processes have a unit root by using the modified Dickey–Fuller

The Main Variables in First Differences, UK, 1892–2018.

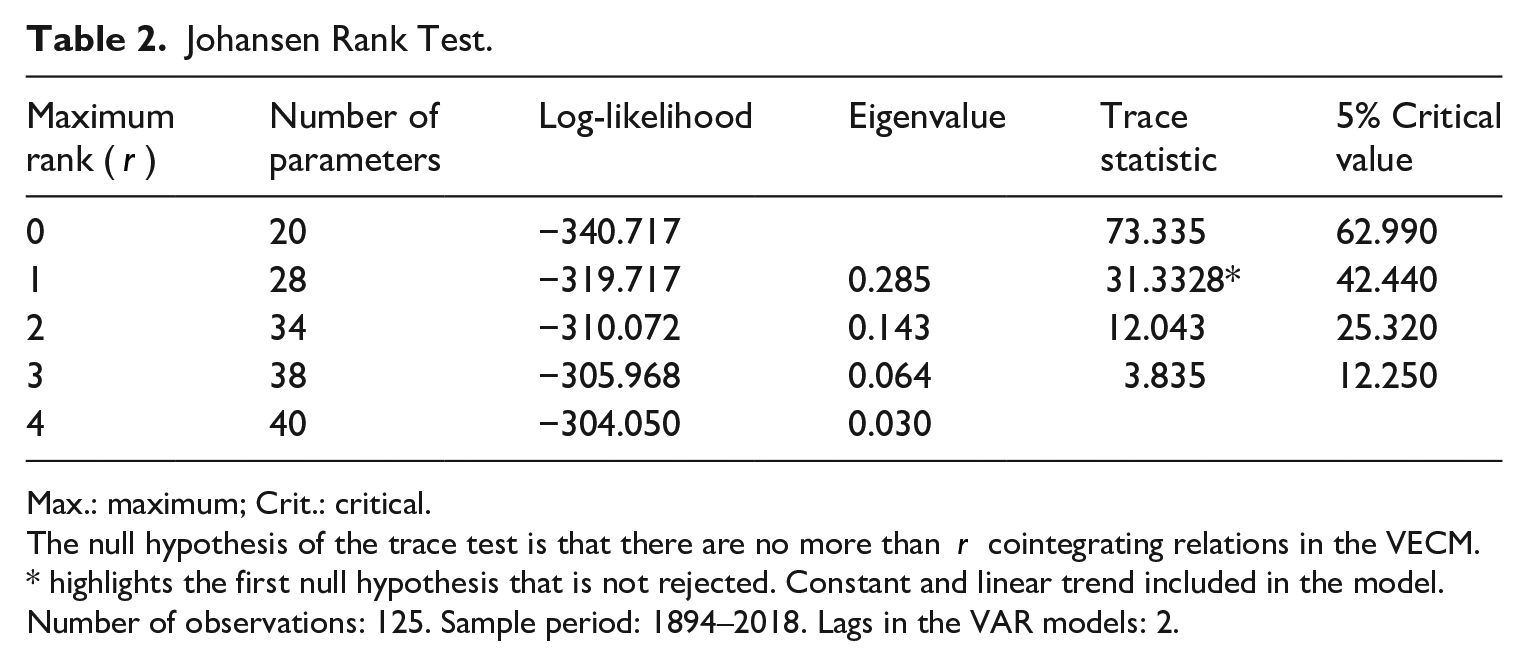

Given our interest in detecting the long-run interaction between the four variables considered, we estimate a cointegrated vector auto-regressive model with finite lag

where

Consistent with the pattern of the series under analysis, we assume a model with only a constant and a deterministic trend in the cointegrating equation, to account for the linear trend of

Johansen Rank Test.

Max.: maximum; Crit.: critical.

The null hypothesis of the trace test is that there are no more than

Assuming the presence of one cointegrating equation, we have checked that the residuals of the estimated VECM are not subject to significant heteroskedasticity. Letting

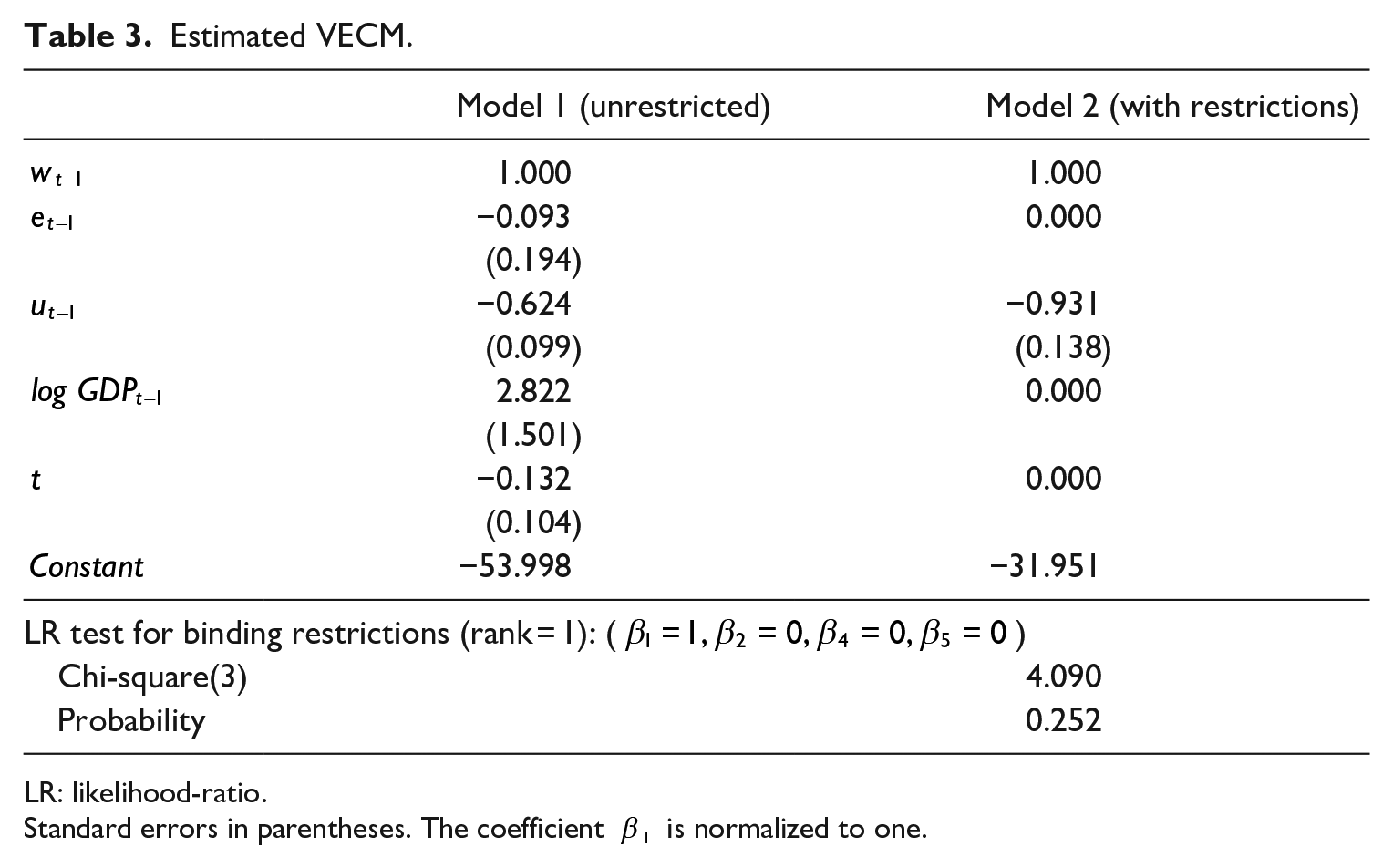

Table 3 gives the estimate of the cointegrating equation

Estimated VECM.

LR: likelihood-ratio.

Standard errors in parentheses. The coefficient

As we have no a priori theoretical restrictions to impose, we test the model with all variables included. In order to apply Johansen’s (1995) maximum-likelihood estimation methods, we normalize to unity the coefficients of the wage share as this allows a straightforward economic interpretation of the relations.

19

The estimated cointegrating equation reported in the first column of Table 3 suggests that, in the long-run, trade union density and wage share are positively correlated (if

In other words, in the long-run, the dynamics of the wage share is significantly correlated with the dynamics of unionization: an increase in the power resources of workers, proxied by the union density measure, is correlated with a long-run increase in the wage share. These results both support a power resources approach and raise serious doubts about SDT: an increase in the power resources of the working class tends to modify the long-run income distribution in favour of workers. This conclusion is further supported by an analysis of Granger-causality, which suggests that

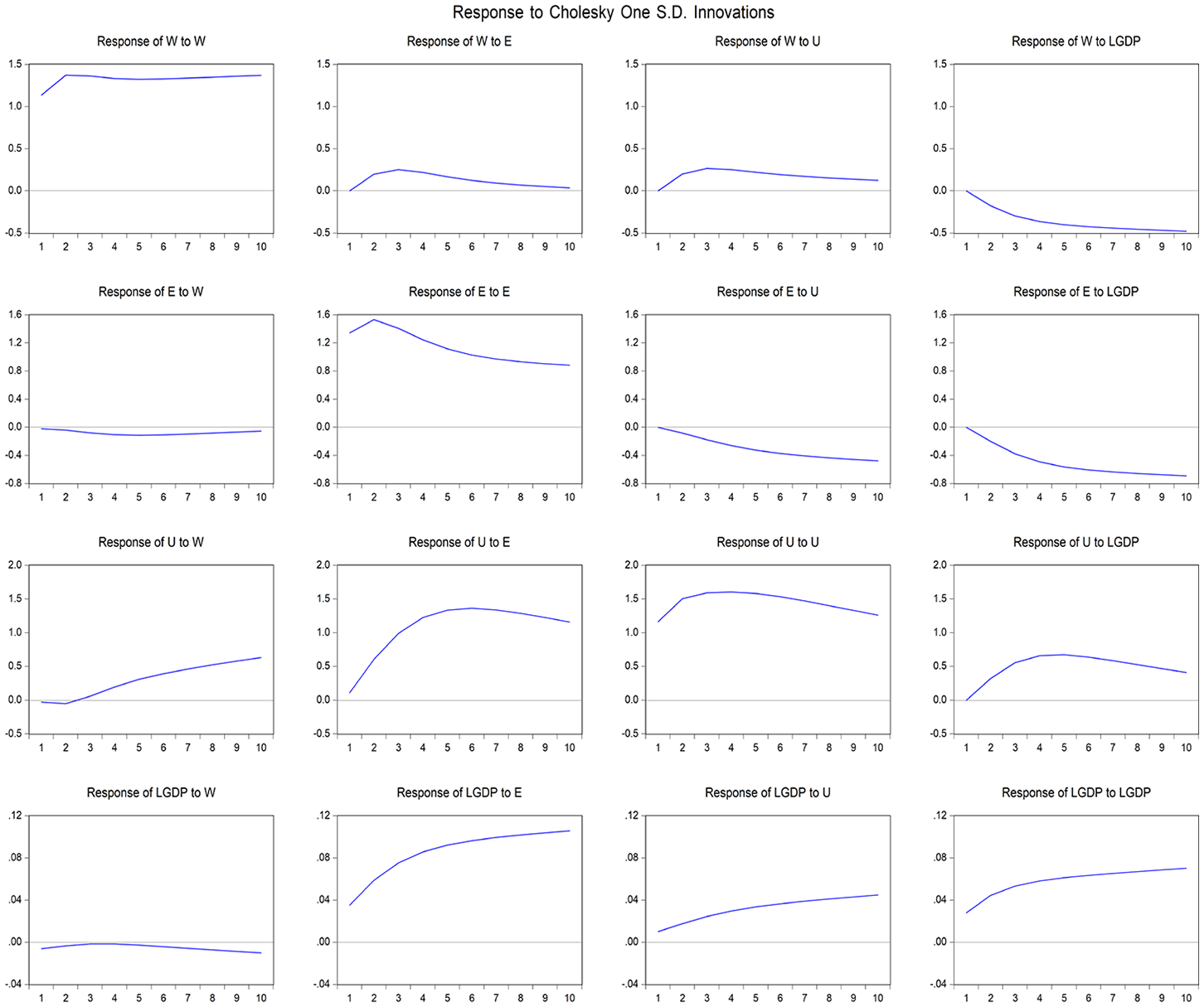

As all variables are endogenous, we analyse long- and short-run dynamics jointly, simulating the orthogonalized impulse response function (IRF), which traces out the response of current and future values of each of the variables to a one unit increase in the current value of one of the errors at a time, holding everything else constant. We use the Cholesky factorization of the residuals covariance matrix to orthogonalize the impulses. Figure 7 plots the response of each variable,

Impulse Response Functions of the Restricted Model. Cholesky Decomposition, Shocks of 1 Standard Deviation.

Summing up the main findings, Figure 7 shows that a one standard deviation shock on union density has a positive, permanent effect on the wage share (panel in first row, third column). The employment rate is gradually negatively affected by increases in union density (panel in second row, third column). Figure 7 may be seen as providing also some evidence consistent with the short-run profit-squeeze mechanism identified in the section ‘Distribution and Conflict in the UK: Descriptive Analysis’, for a one standard deviation shock on employment has a positive transitory effect on the wage share. Moreover, a one standard deviation shock on the wage share has a temporary negative effect on employment. Yet, both effects are comparatively rather small. In general, however, a shock in one of the variables has a permanent effect on the others.

Robustness

We assessed the robustness of our results in several ways. 22

Consider first the analysis in the section ‘Distribution and Conflict in the UK: Descriptive Analysis’. The Hodrick–Prescott procedure is sometimes considered ad hoc because it relies on the choice of smoothing parameter,

Consider next the econometric analysis in the section ‘Power, Conflict and Distribution: A VECM Approach’. To begin with, we have analysed the two key variables of our model, the wage share and the employment rate, in isolation and the results are unambiguous and in contradiction with SDT: quite strikingly, there exists no long-run cointegrating relationship between

First, our results are robust to alternative definitions of the main variables, including alternative measures of union density and the employment rate. For example, if we use claimant count unemployment rather than the standardized international definition, in the denominator of the union density variable and of the employment rate variable, our conclusions remain unchanged.

Second, we have considered collective bargaining coverage as an alternative measure of workers’ power. The lack of a continuous long-run series of the coverage of collective pay-setting institutions in the UK makes it impossible to formally estimate our VECM. However, we have reconstructed various time series starting in 1895 based on (incomplete) historical data and compared them with the union density variable: the correlation coefficient ranges between 0.92 and 0.96.

Third, theoretically, in the profit-squeeze mechanism underlying SDT, it is arguably economic activity in general, rather than investment, that provides the link between distribution (the wage share) and the employment rate, and

Fourth, it may be argued that if the long-run dynamics of income distribution (and employment) are – at least partly – the product of class struggle, then what matters is the relative power of both classes. On the other side of our two-class framework, the primary power resources of employers are economic assets or capital. Therefore we have estimated our model using the log of total non-dwellings capital stock as a proxy of capitalist power. The results confirm our conclusions and provide support to the power resources approach: an increase in union density has a positive, long-run effect on the wage share, while an increase in the stock of productive capital has the opposite effect.

Yet, the capital stock may be an imperfect proxy of the employers’ power resources, because the extent to which ownership of economic assets translates into power depends on a number of factors, and in particular on capitalist control over investment. Assets can be divested and transferred (Korpi, 2006), but the actual mobility of capital depends both on technological factors and on the broader legal, political and institutional framework. From this perspective, the openness of an economy may be deemed a better proxy of the power of employers (Beramendi and Rueda, 2007; Bradley et al., 2003; Korpi and Palme, 2003; Kristal, 2010; Wright, 2000). Increased capital mobility tends to increase the capacity of capitalists to control investment and the allocation of capital, and provides an indirect measure of the extent to which, in their relation to workers (and the nation state), capitalists can choose ‘exit’ as opposed to ‘voice’. Hence it measures their incentive to find a compromise in distributive conflicts.

Two sets of measures of openness are used in the literature: de jure measures of openness – such as the indices constructed by Quinn and Inclan (1997), Fernandez et al. (2016) and Ilzetzki et al. (2019) – capture the legal restrictions on capital movements or foreign exchange transactions. De facto measures capture instead the actual movements of capital across borders. While insightful for cross-national comparative analysis, de jure measures suffer from some major shortcomings in our context as they cover only a small part of the period under investigation and provide a rather coarse classification with limited room for variation. 24 Furthermore, the legal framework of a given country is only one of the determinants of capital mobility and can only partially capture capitalists’ ability to exercise the exit option.

Therefore, we have experimented with a de facto measure, focusing on property income from overseas as a percentage of the sum of property income from overseas, total domestic profits and an estimated profits component of mixed income as our main measure of openness and proxy of capitalist power. The estimated VECM replacing

Finally, it may be objected that SDT concerns the wage share as a class share, and that is not what is captured in our empirical analysis. For employee compensation includes the labour income of the highest paid executives on the same basis as the labour income of the most lowly paid unskilled worker. Ideally, a much narrower definition of wage share would be appropriate to throw light on SDT. This objection is pertinent but it does not question our conclusions, because a focus on all employees puts our assumptions concerning the relevance of power resources, and our critique of SDT, to a stronger test. It is all the more remarkable that the empirical evidence and econometric analysis support our theoretical hypotheses despite the data limitations. Moreover, the available data for the UK that distinguish different categories of employees provide strong support to our conclusions. Census of production data provide a continuous series for manufacturing for the years 1971–1995, and for the production industries (mining, manufacturing and utilities) for the years 1974–1995. These data are too limited to use the econometric techniques above. Yet the pattern of the data for manual workers in production industries is strikingly similar to that for all employees: over the period for which there are data, short-run cycles are visible around a sharply declining trend.

Discussion

Both the descriptive analysis in the section ‘Distribution and Conflict in the UK: Descriptive Analysis’ and the VECM suggest that a profit-squeeze mechanism may be operating in the UK, for at least part of the sample. This provides some (limited) support for Hypothesis 1. However, the econometric analysis shows that there exists a robust long-run relation between distributive outcomes and the power resources of the two classes. Hence while a short-run profit-squeeze mechanism may be operating at any given time, this hardly provides support to SDT. Hypothesis 2, the core SDT proposition, is false: the long-run equilibrium values are much more variable than required by SDT and they are correlated to the power resources of economic classes, consistent with power resources theory.

These results point to a key conceptual limitation of SDT: the mechanism underlying SDT operates at a very high level of generality, and is based only on the most basic institutions of capitalism, namely ‘the laws of private property’ (Lindblom, 1977: 172) and the control over investment decisions that they afford, together with profit maximizing behaviour. In this sense, SDT operates in a sort of institutional vacuum. Yet, ownership comprises various rights, powers, claims and immunities, not all of which must be vested in one agent, including in capitalist economies. The exact allocation of these rights depends on political decisions, institutions, social norms and so on, and it determines the degree of control that capitalists have over investment. Thus, although capitalists do enjoy structural power, this power is mediated by institutions, which ‘shape the mechanisms and forms of business power’ (Quinn and Shapiro, 1991: 855), and is limited by the power of other actors, starting from the working class. Power relations and institutional rules affect ‘the rights and powers accompanying private ownership of the means of production’ (Wright, 2009: 111) and the boundaries of feasible income distributions, and tend to change over time. Contrary to Hypothesis 2, the structural features of class conflict – including the political, economic and institutional framework – are central determinants of distributive outcomes. For this reason, there is no cointegrating relationship between wage share and employment rate taken on their own. A focus on class struggle requires, as we have seen, additional variables capturing the power resources of the main classes in the economy.

Conclusions

That an increase in the power resources of one class has a positive, long-lasting effect on the share of income that goes to that class does not imply that any income distribution is feasible at any moment of time. Nor does it imply that the prospects for an electoral socialism/social democracy pursuing redistributive class policies are good. For there certainly are structural limits to attainable distributions within capitalist institutions, and the empirical evidence suggests that some form of profit squeeze may be operating at any given time. It does suggest, however, that strong versions of SDT based on a profit-squeeze mechanism, such as Przeworski’s, do not explain the actual choices and trade-offs faced by the labour movement. In contrast, our analysis provides novel empirical support for power resources theory and the relevance of class in the determination of distributive outcomes.

It may be objected that the evidence in favour of the power resources approach – and against SDT – is inconclusive, for the power resources of the two classes may themselves be exogenously determined. This objection is not entirely convincing, for it is theoretically very difficult to find some long-run explanatory mechanism that is completely independent of power resources, distributive conflict and government policies. This includes long-run changes in the institutional and legislative framework, and in the basic structural features of the economy (including long-run trends in technological progress, labour supply, skills and so on). There is robust historical evidence that political actors intentionally act to modify the structural and institutional features of the economy in order to change the balance of power between classes (Korpi, 2006; Rothstein, 1984). Indeed, ‘institutions are created with the object of giving the agent . . . an advantage in the future game of power’ (Rothstein, 1984: 35). The dynamics of unionization in the UK, for example, has been largely driven by political and institutional factors (Dunn and Metcalf, 1996). Although technical innovations may affect trade unions, technical change itself is a site of class struggle and is often introduced in order to alter power relations (Kristal, 2010, 2013). Changes in the degree of openness of an economy are anything but exogenous. In general, assuming the existence of a set of completely exogenous explanatory variables would imply the endorsement of a crude economic determinism, which Przeworski (1985) himself has convincingly rejected.

In summary, power resources matter, and therefore institutions and politics matter. They matter for their short-run effect on market distribution, but also – and perhaps more importantly – for their long-run effect on the conditions for market distribution. Therefore, going back to our opening questions, the social democratic model is more undetermined than that suggested by SDT, especially from a long-run perspective because the political and class struggles are not just about choosing the optimal position in a given structure of trade-offs, but first and foremost about altering those trade-offs themselves. This can, and should, be the starting point for a renewal of the social democratic project.

Supplemental Material

addendum_2020_04_16 – Supplemental material for Class, Power and the Structural Dependence Thesis: Distributive Conflict in the UK, 1892–2018

Supplemental material, addendum_2020_04_16 for Class, Power and the Structural Dependence Thesis: Distributive Conflict in the UK, 1892–2018 by Carlo V Fiorio, Simon Mohun and Roberto Veneziani in Political Studies

Footnotes

Appendix 1

Acknowledgements

Special thanks go to Emanuele Bacchiocchi, Bob Hepple, Fabrizio Iacone, John Kelly, David Soskice, Nicholas Vrousalis, Mark Wickham-Jones and three anonymous referees for long and detailed comments. We are indebted to Bilge Erten, Antu Murshid, Dennis Quinn and Carmen Reinhart for sharing their data with us. We also thank Jim Boyce, Dick Bryan, Alex Bryson, Firat Demir, Meghnad Desai, Jerry Epstein, Jonathan Goldstein, Geoff Harcourt, Florence Jaumotte, Arjun Jayadev, Peter Kriesler, Valentino Larcinese, Peter H. Matthews, Tom Michl, Ron Ratti, John Roemer, Peter Skott, Naoki Yoshihara and participants in the Manchester Workshops in Political Theory, the MPSA Conference, the PSA Conference, the Progressive Economy conference, the WINIR conference, the FMM-IMK conference, the London Analytical Political Economy Workshop, the European Association of Labour Economics conference, the annual meeting of the September Group and seminars at the New School for Social Research, UMass Amherst, Queen Mary University of London, University of Sydney, Colgate University and University of Western Sydney for comments and suggestions on earlier versions of the article. The responsibility for any remaining errors is our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplementary Information

Additional Supplementary Information may be found with the online version of this article.

Figure A1: Four WSER Clockwise Cycles, UK, 1892–1951. Figure A2: Four More WSER Clockwise Cycles, UK, 1951–2002. Figure A3: Five WSER Anti-Clockwise Cycles, UK, 1914–2008. Figure A4: One Period With No Clear Cyclical Pattern, UK, 1981–1986. Figure A5: One Incomplete Clockwise Cycle, UK, 2013–2018. Table A1: Granger-Causality Analysis. Figure A6: Granger-Causality Scheme. Figure A7: Collective Bargaining Coverage and Union Density, UK, 1892-2018. Table A2: Estimated VECM, with an Alternative Measure of ut and Impulse Response Functions of the Restricted Model (Cholesky Decomposition, Shocks of 1 Standard Deviation). Table A3: Estimated VECM, with an Alternative Measure of et and Impulse Response Functions of the Restricted Model (Cholesky Decomposition, Shocks of 1 Standard Deviation). Table A4: Estimated VECM, Using the Percentage Change of Total Nominal Non-Dwellings Capital Stock, i, Instead of log GDP and Impulse Response Functions of the Restricted Model (Cholesky Decomposition, Shocks of 1 Standard Deviation). Table A5: Estimated VECM, Using the Log of Total Nominal Non-Dwellings Capital Stock, log K, Instead of log GDP and Impulse Response Functions of the Restricted Model (Cholesky Decomposition, Shocks of 1 Standard Deviation). Table A6: Estimated VECM, Using Property Income from Overseas, k, Instead of log GDP and Impulse Response Functions of the Restricted Model (Cholesky Decomposition, Shocks of 1 Standard Deviation). Figure A8: Three WSER Cycles, UK Operatives, 1976–1993. Figure A9: Production Industries: Operatives’ Wage Share (Raw Data and Trend), UK, 1974–1995.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.