Abstract

Despite recent expansion in its population covered by public-funded insurance, a large section of India’s population remains at major financial risk from health shocks. This segment of the population, sometimes referred to as the ‘missing middle’, typically consists of population groups that are, or have been, engaged in informal sector work, and are not poor enough to be eligible for state-subsidised contributions to insurance premiums; and potentially includes many even among those who satisfy the eligibility criteria. We estimate that the missing middle number is at least 300–350 million in India, with large variations in their economic circumstances. Using extensive international and India-based evidence, we assess two approaches to cover the missing middle: an expansion in public sector health delivery and a contributory demand-side financing system, that is currently popular in India. We conclude that a mix of the two approaches appears to be the most feasible in the short run, given limited regulatory and management capacity and resource constraints, with a longer-run emphasis on integrated systems. The approach proposed in the paper is also likely to help address the problem of shallow coverage of existing health insurance coverage that concerns large numbers of people extending beyond the group comprising the missing middle.

1. Introduction

Over the last two decades, countries across the world have been working towards achieving universal health coverage (UHC), broadly taken to be the aspiration that populations have affordable access to good quality healthcare services (Sachs, 2012). China, Mexico, Indonesia and Thailand have extended health insurance coverage to almost their entire population, and others, such as Ghana, are making progress, with significant shares of their populations also covered by national health insurance (Wagstaff & Neelsen, 2020).

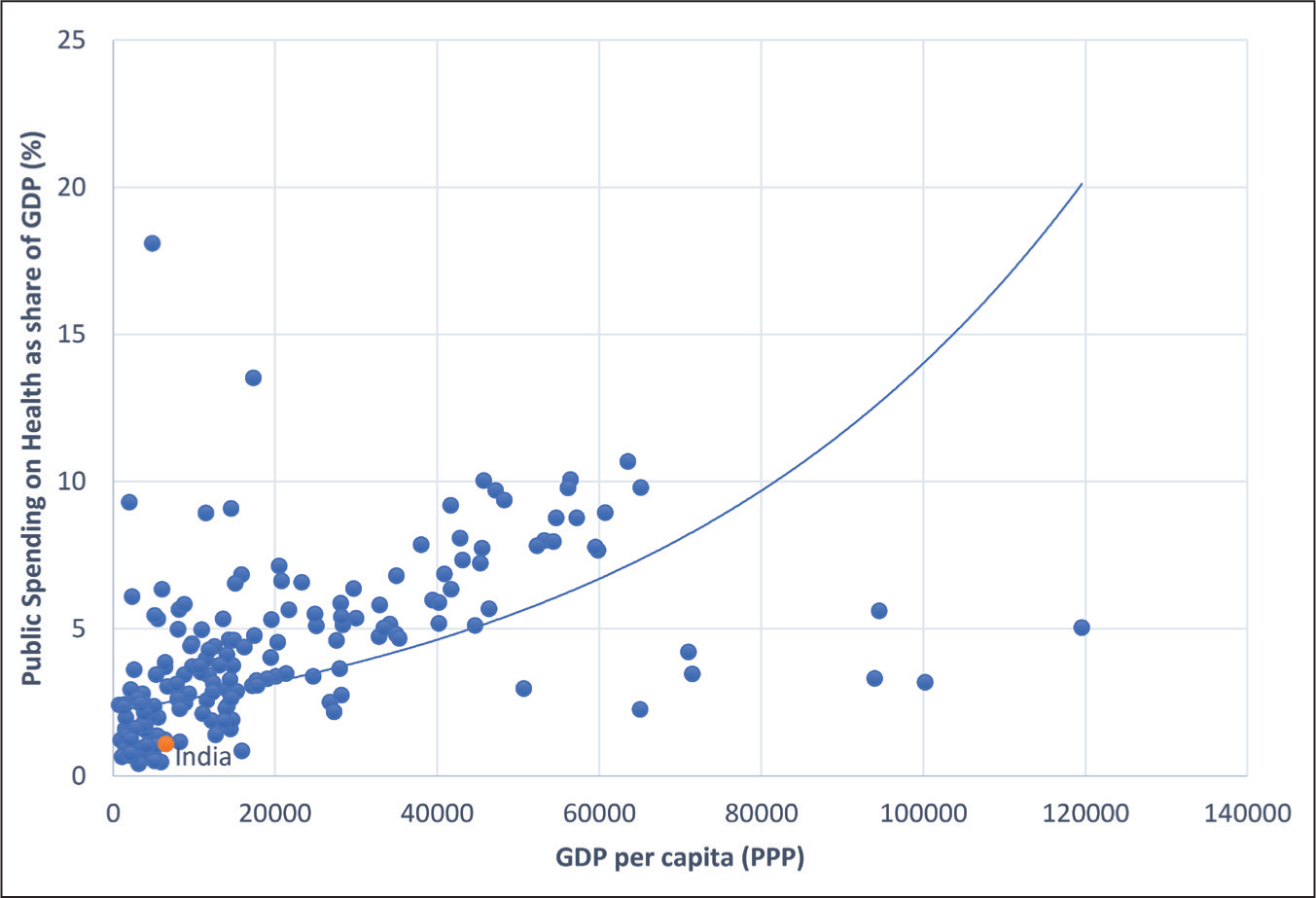

Consistent with the above vision, there is a long-standing policy commitment in India to provide affordable healthcare services to its population (Bhore, 1946; Ministry of Health and Family Welfare (MOHFW), 2017), which policymakers have sought to meet in four main ways, each with its challenges. The first approach involved strengthening the subsidised public sector healthcare delivery system, through a mix of increased government spending and organisational reform (Peters et al., 2002). With public spending on health in India currently at about 1.1 per cent of gross domestic product (GDP) amongst the lowest in the world and certainly below levels that would be predicted by its income per capita (Figure 1), this approach has had limited traction in the Indian context.

With a history of low spending, public services in India can at best be considered only superficially providing ‘universal cover’. Public sector health services in India are characterised by care of inadequate quality, one consequence of which has been a rapid growth in private sector services, a major driver of out-of-pocket (OOP) spending (Hooda, 2015).

A second strategy has been to expand mandated insurance coverage to a segment of the population—the formal sector—through social insurance, including the Employees State Insurance Scheme (ESIS) for the private formal sector, the Central Government Health Scheme (CGHS) for central government employees and other schemes for the armed forces, para-military organisations, railways and various public sector agencies. Many operate their own facilities, although ESIS has known problems with the quality of its health services (Ministry of Labour and Employment, 2018). With formal sector employment at less than 10 per cent of India’s workforce, social insurance has obvious limitations as a mechanism to expand population health coverage (Mehrotra, 2019).

Third, there is voluntary health coverage through private insurers. Private insurance holders, however, are concentrated among richer households, either as group policies (of employers) or individually held policies (Insurance Regulatory and Development Authority of India (IRDAI), 2022).

Publicly funded (and often publicly managed) health insurance for population sub-groups perceived to be needy constitutes a fourth strategy adopted by central and state governments in India (Niti Aayog, 2021). Initial efforts, going back to the 1970s, took the form of chief ministers’ relief funds in various states to support recovery from natural disasters and medical treatments for the needy (Patnaik et al., 2018). More recently, large national- and state-level schemes have emerged, including the Rashtriya Swasthya Bima Yojana (RSBY), launched in 2008 by the Ministry of Labour and Employment, for the poor and informal sector workers across India, with premiums fully subsidised by the centre and the states (La Forgia & Nagpal, 2012; Sood & Wagner 2018). RSBY was replaced in 2018 by the Pradhan Mantri Jan Arogya Yojana (PM-JAY) aimed at providing subsidised hospital cover with larger benefits and targeted to groups experiencing high levels of deprivation, as well as informal sector workers deemed vulnerable. These national-level schemes have been complemented by state-funded health insurance programmes that have sometimes offered more generous benefits and extended benefits to additional population sub-groups.

Progress towards UHC is typically associated with a reduction in OOP spending for healthcare (World Health Organization (WHO), 2010). However, OOP spending on healthcare remains high in India, at about 52 per cent of national health expenditures (MOHFW, 2023). High levels of OOP are underpinned by two features of the coverage gap in India: the absolute numbers of people who are not covered by any insurance scheme (other than low-quality public services) and the limited financial risk protection available to those who are covered (Karan et al., 2017; Niti Aayog, 2021). Addressing these coverage gaps is a key issue confronting Indian policymakers on the pathway to UHC.

The primary focus of this article is on the group, sometimes referred to as the ‘missing middle’, who are not covered under any insurance scheme, although they do have access to subsidised but low-quality public services. Regarding this group, this article explores the following questions: What is the composition of the missing middle and what are the potential benefits of extending coverage to members of this group? What policy alternatives are available to improve financial protection against health shocks to the missing middle, and how do the potential solutions stack up, based on the international and Indian experiences on their effectiveness? Because OOP spending is high even among those ostensibly covered by existing schemes, we also examine strategies to expand the depth of coverage for the Indian population.

2. The ‘Missing-Middle’ in India: Magnitude and Composition

The National Health Authority estimates that PM-JAY covers 120 million households, or about 550 million people (

Next, there is the population eligible for social insurance, enrolled in ESIS, public sector employee schemes and schemes for the armed forces (Ministry of Statistics and Program Implementation (MOSPI), 2023; Niti Aayog, 2021). The number of workers covered by social insurance can be roughly estimated to be 32 million, based on data from covered employees under ESIS, the number of central government employees who are covered (whether by CGHS or under department-specific schemes) and members of the armed forces. Assuming a family size of 4.4, this translates into 141 million covered. We estimate an additional eight million retired personnel (and their spouses) who have health coverage from these and related schemes, following retirement.

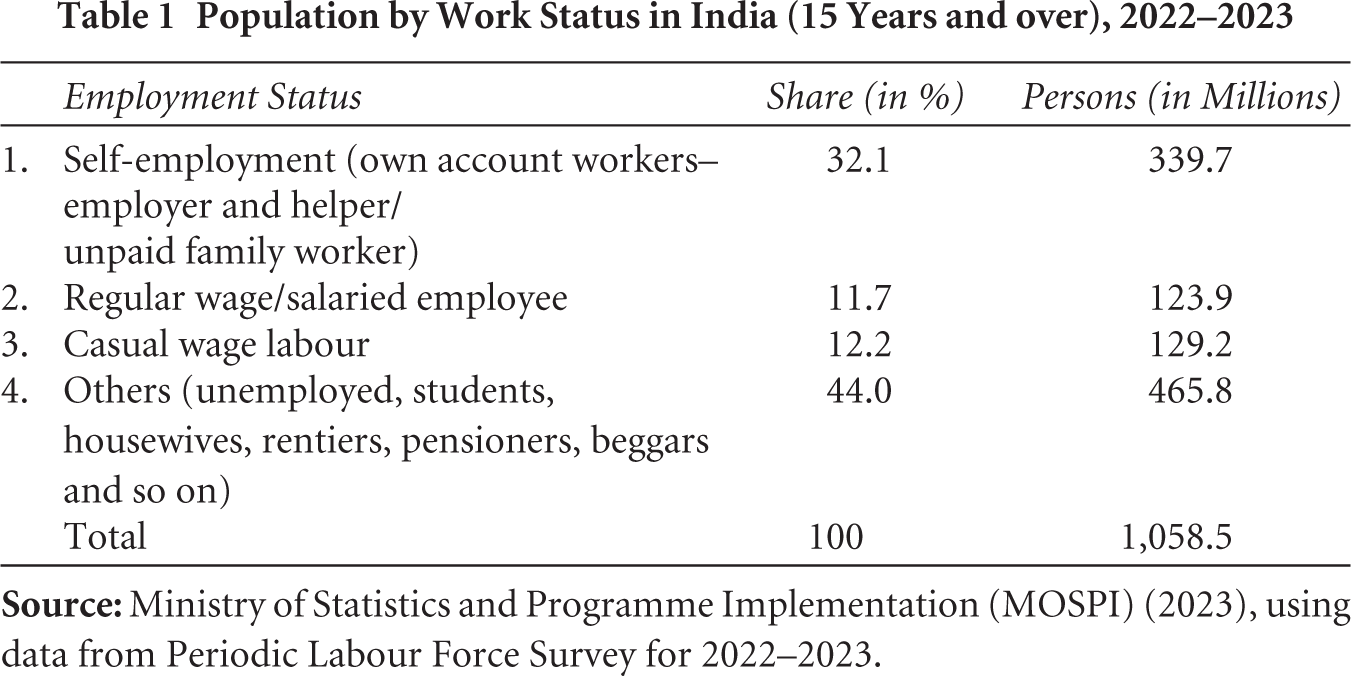

The large number of people covered by social insurance notwithstanding, a substantial number of formal sector employees remains uncovered. Table 1 reports the share of workers falling into different employment categories, by self-employed status, casual work and by regular salary from labour force survey data. Of the estimated 592 million workers aged 15 years and over, nearly four-fifths (or 468.9 million) were engaged in self-employment and casual wage work, mostly in the informal sector. Even among regular wage/salaried employees, there is a large element of informality: with 58.6 per cent reporting no written job contract, 54 per cent reporting not being eligible for paid leave and 54 per cent not eligible for any social security benefit (MOSPI, 2023). These data suggest that 57 million people may be formally employed, defined as workers with regular wages and salaries who do not report any of the elements of informality. Comparing this with an estimated social insurance coverage of 32 million, as many as 25 million formal sector workers may not have social insurance cover, including individuals in the private sector who earn above the ESIS threshold and are thus ineligible for its coverage. Retired personnel belonging to this group are also ineligible for social insurance. Some sections of state and local government employees would not be covered if their salaries exceed ESIS thresholds, although they usually benefit from medical reimbursement schemes with shallow coverage; and some states (e.g., Telangana and Andhra Pradesh) also recently introduced publicly funded insurance for their serving and retired (government) employees.

Population by Work Status in India (15 Years and over), 2022–2023

Taken together, publicly funded insurance and social insurance covered almost 900 million people in 2023. Private insurance schemes covered about 252 million people in the most recent year for which data are available (IRDAI, 2023), including both group cover and individual cover. Group coverage schemes cater to private formal sector employees with earnings above ESIS thresholds and their families (employer–employee groups), but also non-employer–employee groups, such as groups within a specific occupational category and members of cooperatives (IRDAI, 2022). However, there are considerable numbers of people with dual coverage, as individuals can hold multiple private health insurance policies (Sanghvi, 2020). In addition, CGHS enrolees can claim from private insurers as well as CGHS, creating incentives for the purchase of private cover, so that dual membership of private and public plans is also likely (CGHS, 2021). With a population of 1.43 billion in 2023 then, the number of people uncovered by some form of health insurance is likely to exceed 300 million, possibly closer to 350 million.

2.1 Who Are the Uncovered?

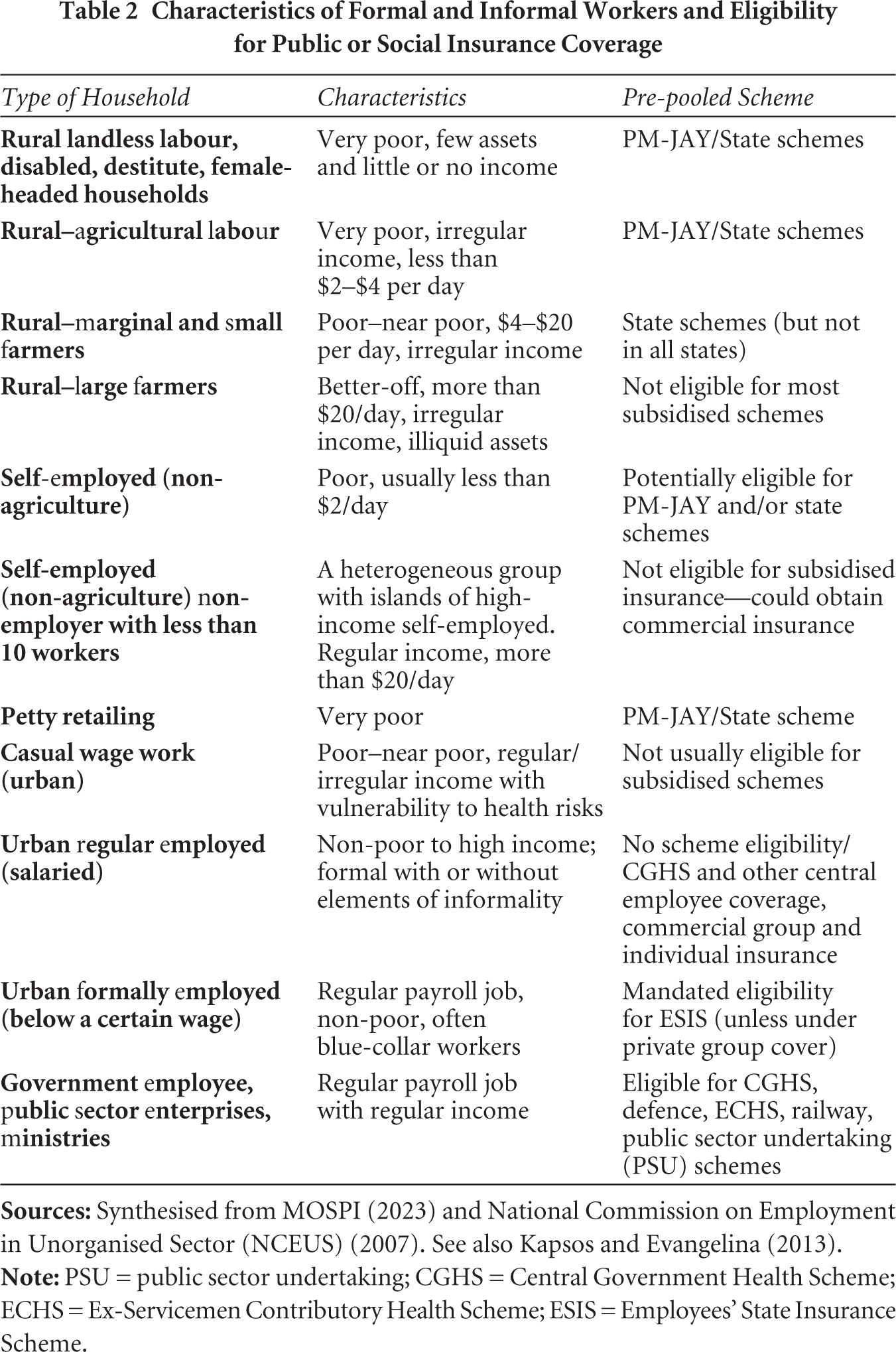

Given the eligibility criteria for publicly funded insurance, individuals who are not working in the formal sector nor (officially) poor enough to be in the BPL list (plus older individuals from this group) are disproportionately likely to be ineligible for public coverage. Another group likely to be uncovered are current and former employees of state and local governments in states that do not provide publicly funded insurance coverage for this group. Labour force surveys can help provide additional understanding of the socio-economic and occupational characteristics of the missing middle. In Table 2, we map work status into BPL status and other indicators of vulnerability commonly used for determining eligibility in public insurance schemes in India. We acknowledge these links are approximate and potentially characterised by significant inclusion and exclusion errors (Bajpai et al., 2017; Krishna, 2007; Krishna & Shariff, 2011; Sahu & Mahamallik, 2011; Saxena, 2015). An examination of Table 2 suggests that households in the farm sector (with medium and large farm holdings) are likely to constitute one major uncovered group. A second group is likely to be households where individuals are self-employed in the non-agricultural sector with sufficiently large incomes, ranging from small enterprises to high-earning professionals (doctors, lawyers, etc.). Casual wage workers in the urban sector and marginal farmers may also be uncovered, although this may vary by the eligibility criteria used in states. Finally, certain slices of formal sector workers (including retirees) may be left uncovered, such as state government employees or former private sector employees previously covered by group insurance.

Characteristics of Formal and Informal Workers and Eligibility for Public or Social Insurance Coverage

One way to think of the ‘missing middle’ is that it comprises the groups mentioned in the previous paragraph, that is, those who are neither eligible for subsidised public insurance nor covered by some other insurance scheme. However, this assumes that all individuals eligible for subsidised public insurance can be accurately identified and enrolled. In practice, subsidised insurance schemes are likely to be characterised by significant exclusion and inclusion errors, on account of mistakes in assessing eligibility status at the time of initial enrolment, or due to the insurer not accounting for changing economic status of households over time. The National Family Health Survey for 2019–2021 suggests that only about one-third of the poorest 40 per cent households reported being covered by public insurance, suggesting large exclusion errors. Inclusion errors also appear to be large, with the richest two quintiles of rural households reporting 40 per cent enrolment in public insurance schemes, and almost a quarter of the top two quintiles in urban households also reported being enrolled (Mohanty et al., 2023). Assuming the overall number of covered households under PM-JAY is 550 million, these survey findings have implications for the composition of the uncovered middle, and for policies intended to promote coverage, as discussed below.

Aside from certain categories of retired personnel and dependents, there is no obvious reason why the age and gender characteristics of the missing middle population are likely to be very different from the covered population. However, as shown above, there is likely to be considerable economic variation within the population of the missing middle, suggesting that if programme targeting is necessary given its size and limited resources, it will be important to distinguish between people eligible for subsidised premiums and others. Moreover, the more inaccurate the targeting, the greater will be the resource challenge of reaching the poor.

We also wish to underline that even for the group covered by public and social insurance in some form, almost 900 million, the depth of coverage varies considerably across states and schemes, with inpatient cover being common, and outpatient cover being somewhat uncommon. In addition, insurance policies in the private sector are characterised by high administrative expenses and shallow coverage. Although the population has access to subsidised public facilities for outpatient care, access and quality vary considerably across states and across rural and urban areas. Together with the missing middle, populations with shallow coverage account for a large share of OOP spending in India, much of it on drugs and outpatient services.

2.2 Rationale for Covering the Missing Middle

There is a strong case for expanding the coverage of health insurance programmes to the missing middle group. Expanding coverage could contribute to improved equity in financing in two ways. First, given that the missing middle are a mix of upper-income populations, alongside the middle-income and the near-poor and poor, expanding coverage to at least some (of the poorer) sections of this group would improve their access to affordable healthcare. Moreover, including the economically better-off and healthier sections of the missing middle could additionally contribute to cross-subsidisation of poorer groups, including political support for additional government funding, provided the added resource costs of covering this group are not too high. This cross-subsidisation could occur in one of two ways, depending on the strategy adopted. If coverage is financed from additional government resources, the progressive structure of the tax system will be the main mechanism to do so. It could also be theoretically achieved if coverage is mandated via private contributions based on the ability to pay, although this latter approach is harder to implement, as discussed further below. This equity-enhancing argument also assumes that on average the health expenditure needs of the economically better-off are less than what they would likely contribute by way of taxes and/or premiums, all else being the same.

There are efficiency arguments for coverage expansion as well. For instance, extending coverage to this group could enable additional economies of scale benefits arising from a larger enrolee base, including benefits from the increased viability of strategies that lead to the integration of preventive care and health promotion with curative services.

Expanding coverage via strategies discussed later in this chapter could also help address the well-known problem of market failure in the private insurance sector, underpinned by issues of adverse selection among potential enrolees and risk selection by insurers as a response. Shallow benefit packages offered by private insurers are often the result, and along with high administrative costs, discourage households who could otherwise benefit from and could afford health insurance from voluntarily purchasing their policies. Essentially, the available products end up being viable only for healthier segments of the population, with lower healthcare expenditure needs. But market failure could also take the form of inadequate access of the population to information about health insurance products, inability to predict health risks, and ‘waste aversion’ as when households do not plan on using the cover to fund healthcare up until the point when they need it (Suter et al., 2017). The high levels of OOP expenditure for healthcare in India, especially for the non-poor, suggest some mix of these explanations is potentially relevant (MOHFW, 2023; Sekhri & Savedoff, 2005). Devising effective means to expand coverage to such households will enhance their financial risk protection and contribute to improved social well-being.

3. Covering the Missing Middle in India: Alternative Strategies

Many countries, including low- and middle-income countries (LMICs), have been in a situation like India. The strategies adopted by these countries to cover their missing middle offer important lessons to policymakers in India and other countries planning to expand coverage. The experience of India’s own states, with their differing benefits packages and population eligibility criteria, offers lessons of its own. We draw upon these lessons, along with those of other countries to assess how to expand coverage to this group in India.

The available literature and India’s own experience point to two broad policy approaches to cover the ‘missing middle’ in India: (a) expansion of subsidised public services and (b) contribution-based cover, provided (or mandated) either by the government or by private insurers, with or without public subsidies. These are not necessarily either–or options, and combinations across these options are also possible. We shall consider each in turn, focusing on their implications for effectiveness, efficiency, equity, cost and feasibility.

3.1 The Public Service Delivery Option

The Bhore Committee report (Bhore, 1946) laid out a vision for health service delivery and financing for India with the public sector as the major provider (and funder) of care. With low levels of income per capita and a small private sector at the time of India’s independence, this strategy seemed appropriate. The experience of the state of Kerala, where health outcomes have been strong historically, is a successful example of this model with long-standing public sector investments in health (Kutty, 2000). At least two other states, Himachal Pradesh and Tamil Nadu, have invested significant resources in their public healthcare delivery systems in recent decades (Dasgupta & Rani, 2004; MOHFW, 2023; Sharma & Kapila, 2019).

Cross-state and micro-studies for India suggest that improved public sector services are associated with health improvements, equity in health service use, and sometimes, efficiency improvements as well. Increased public sector spending on health services was found to lower infant and adult mortality (Bhalotra, 2007; Farahani et al., 2010). In Chhattisgarh state’s government primary health centres, improved doctor competence and availability in clinics were associated with fewer patient bypassing of public primary care facilities (Rao & Sheffel, 2018). Increased spending on public services was also associated with greater use of public sector outpatient services by the poor and lowered use of private (informal) providers (Mulcahy et al., 2021). Bowser et al. (2019) found that government services tend to be pro-poor for outpatient care, although not for inpatient care. Mulcahy et al. (2021) suggest that even a small increase in public spending—of ₹100 per capita—could lead to large increases in health care utilisation by the poor, and away from informal providers. Moreover, high social (as against private) returns from investments in health also justify larger public spending on health.

Collectively, these studies support the view that expanded public service provision could enable progress towards UHC. Because identification of economic status is not critical when subsidised services are available to all, the costs of separating out the near-poor and the poor from wealthier groups are also avoided.

Ignoring for the moment arguments against public delivery of services, can India fund a major expansion of public services? Long-running fiscal deficits were a key factor in constraining the government’s health sector investments in Kerala beginning in the 1980s, and India’s fiscal crisis in the 1990s led to a lengthy period of reduced public spending on the social sector (Kutty, 2000). However, the recent expansion of publicly subsidised insurance suggests that fiscal constraints may not be that tight, especially given that some schemes have eligibility criteria that allow coverage of populations beyond the poor. The states of Rajasthan and Andhra Pradesh use relatively loose definitions of poverty to cover large shares of their total population with full premium subsidies and offer universal free access to essential medicines (Selvaraj & Mehta, 2014).

The experience of Sri Lanka and Malaysia is pertinent even if fiscal constraints are assumed to be binding. Malaysia’s public spending on health has hovered around 2 per cent of GDP, with OOP spending of about one-third of aggregate health spending. Because OOP spending in Malaysia is concentrated among the better-off, its health system has produced outcomes consistent with the UHC goal of affordable and good quality services being accessible to all (Rannan-Eliya et al., 2017). Inpatient and outpatient use rates in Malaysia are comparable with high-income countries and catastrophic spending rates are extremely low. At around 2 per cent of GDP, the Malaysian public sector services can achieve reasonable quality but are not as attractive to high-income households, who end up choosing to pay for private care, not because they have no choice, but because they can afford to. The identification issue—separating out the rich who can pay more for care, from the rest—is resolved by their self-selecting out of public services (Besley & Coate, 1991). A roughly similar strategy has been adopted by Sri Lanka where, despite an OOP share in national health expenditures of almost 50 per cent, medical impoverishment due to health expenditures is low (Rannan-Eliya & Sikurajapathy, 2009).

Both Sri Lanka and Malaysia have also invested heavily in primary care, especially in rural areas where many poor live, effectively self-selecting richer groups (who tend to be urban-based) out of parts of the publicly funded health system. The Indian state following a similar strategy is Tamil Nadu (Dash & Muraleedharan, 2011). By focusing on primary care and secondary services interventions and scaling up immunisation, Tamil Nadu has greatly improved health outcomes for its rural population (World Bank, 2019).

Relying on the richer groups to self-select themselves out of the public system, effectively limiting the fiscal burden of public sector services, can also be observed in Australia, a high-income country. In Australia, higher marginal tax rates on richer households that forgo private health insurance cover incentivise better-off groups to purchase private health insurance and services (Stoelwinder, 2014). Because private insurance also funds care in public hospitals, private resources help finance public services in this model, albeit with some risk selection issues, with patients with more severe health conditions more likely to be transferred from private to public hospitals (Cheng et al., 2015). Nonetheless, because even these patients are funded by private insurers, the public system can access resources which they otherwise would not have.

A central argument against this option is that public services cannot be effectively delivered in India, due to poor state capacity to manage service provision. Some researchers have argued that additional health resources for the public sector are akin to affixing ‘band-aid on a corpse’ (Banerjee et al., 2008). Challenges related to the management of funding flows, such as delays in the availability of funds and poor resource utilisation, have remained an ongoing concern, alongside governance and oversight challenges related to the public sector. Studies demonstrate high rates of absenteeism among healthcare workers in public facilities (Muralidharan et al., 2011), low quality among government (and private) healthcare providers, a significant ‘know-do’ gap (Dash & Muraleedharan, 2011; Mohanan et al., 2017), inequities in access to inpatient care in public hospitals (Mahal, 2005) and a lack of strong governance structures to improve provider accountability (Banerjee et al., 2008). These findings would suggest that added spending on public sector delivery in India could be both inefficient and inequitable. However, there is also evidence of excellent public health sector performance of some Indian states, such as Tamil Nadu and Kerala (Dash & Muraleedharan, 2011), and a track record of government underinvestment in the public sector that is likely to have hamstrung its long-term performance. And service delivery in the private sector is also poor. More recently, the counterargument that giving up on the public health sector is akin to ‘throwing the baby out with the bathwater’ has been made (Kane et al., 2022, 2023). This research highlights why investing in public health services is important and necessary in the Indian context, and how even small investments can make a significant difference (Mulcahy et al., 2021), particularly to those most vulnerable. Given these arguments, at the very least, one can say that demand-side financing implicit in the PM-JAY is not the only option to cover the missing middle. In a decentralised polity such as India, a mix of strategies might be appropriate, including expanding investments in public services.

3.2 The Contributory Scheme Strategy

Countries have taken different routes to ensure ‘buy-in’ from the missing middle population for insurance. In the Republic of Korea and China, uncovered populations ‘voluntarily’ pay premiums to join, but with an element of arm-twisting (as in China where local political leaders were pressured to increase enrolment) and premium subsidies (Hsiao et al., 2014; Kwon, 2009). In Vietnam, the government issued a mandate to enrol in social health insurance (Mao et al., 2020). In Thailand, the government fully subsidises premium contributions to public insurance for individuals not covered by existing schemes catering to the formal sector (Tangcharoensathien et al., 2007). In several European Union countries (e.g., the Netherlands), a combination of mandatory participation with individuals being able to choose insurers has been adopted (Saltman & Dubois, 2004).

In India, strategies adopted by state governments mirror those internationally, although there is considerable cross-state variation. The Arogyasri scheme of Andhra Pradesh (AP) uses a loose definition of economic hardship (e.g., not owning car, having less than 35 acres of land, annual income less than ₹500,000 (or $7,000)) for fully subsidised premiums. The AP state government offers the Arogya Raksha scheme to households that do not satisfy the economic eligibility criteria, to voluntarily enrol with premium payments ranging from ₹1,200 ($15) to ₹62,500 ($800), depending on the benefits package. In Rajasthan, government-funded insurance fully subsidises premiums for the poor; the rest have the option of voluntarily enrolling themselves at a premium of ₹850 ($11) annually per family, with an enrolment incentive in the form of a free smartphone (Mint, 2021). In Himachal Pradesh, the government combined three population groups into a single pool—individuals eligible for PM-JAY (full premium subsidy), highly vulnerable groups (people over 70 years, disabled, women-headed households and street vendors) who pay an annual premium of ₹365 ($4.50) per household to enrol, and the rest who can enrol at an annual premium of ₹1,000 ($12) per household, well below premiums for private cover in India. In Chhattisgarh, the government does not charge a premium for people above the poverty line, but the health insurance cover offered to this group is smaller relative to that offered to people below the poverty line (₹50,000 versus ₹200,000). Nationally, the PM-JAY scheme is exploring the idea of private voluntary insurance to increase enrolment among the missing middle (Niti Aayog, 2021).

3.3 Should Premiums Be Subsidised?

To summarise, the international literature suggests that in LMIC contexts, large government subsidies are required to enrol the missing middle group into health insurance, irrespective of who the insurer (public or private) is, and irrespective of whether the coverage is voluntary or mandated.

The evidence on the impact of subsidies on insurance enrolment is compelling. As of August 2021, Indonesia’s national health insurance scheme covered about 83 per cent of its population, about one-half being poor with fully subsidised premiums (Asante et al., 2023). One-third of this group was covered through contributions based on work in the formal sector or contributions from a mix of pensions/government for retirees. The remaining enrolees were non-poor, with the option of contributing to premiums on a sliding scale, matched to a benefits package. With most non-enrolees in national insurance also belonging to the last group, the coverage rate for the non-poor in the informal sector was slightly more than one-fifth. Even this involved considerable self-selection, with high claims ratios (6.5:1) among those enrolled (Banerjee et al., 2019; Dartanto, 2017). Surveys suggested their non-enrolment stemmed from problems in getting registered, lack of information about the scheme, and perceived costs of coverage outweighing the benefits. Although only one-fifth of the surveyed individuals mentioned affordability as a problem, subsidies mattered: high levels of premium subsidies (amounting to 50–100 per cent of the premium) led to an almost 8-fold increase in enrolment (Banerjee et al., 2019).

In Vietnam, beginning with a compulsory contributory scheme for government employees and pensioners in 1993, and voluntary participation for family members, coverage progressively expanded (over 5 reform stages) to cover almost 87 per cent of Vietnam’s population by 2018 under a single national scheme (Lê et al., 2019; Teo et al., 2019). One-quarter of the covered population consisted of government and enterprise employees with premiums financed by employer and employee contributions. About 40 per cent of the poor and near-poor, plus children aged six years or less and the elderly population, were fully covered by tax-financed premium contributions. The remainder could be termed the missing middle. With population coverage hovering around 60 per cent as recently as 2010, the government mandated the participation of households not covered under the employee or fully subsidised schemes in 2014. Partial subsidisation of premium contributions across a broad swathe of this previously uncovered population is likely to have been key to increased coverage. Even so, there is evidence of adverse selection in this last group, with much higher rates of health care use and claimed expenditures relative to the average enrolee (Lê et al., 2019).

The Republic of Korea started with a relatively small-sized informal sector at a time (about one-quarter of the work force) when its national health insurance was extended to the self-employed in the late 1980s (Kwon, 2009). The government strategy involved classifying insurance pools by sub-groups within the self-employed population (referred to as ‘insurance societies’) to save on the effort to disentangle incomes, instead using group-specific information from other sources to determine income-based contributions. The insurance societies were essentially quasi-public bodies, tightly regulated and did not compete for members. Despite an autocratic polity in the country at the time, high levels of premium subsidy (44 per cent of total contributions) were needed to ensure the support of self-employed groups. Subsidies were also needed because mandated levels of benefits were regulated to be identical across insurance societies (including societies catering to the formal sector), but incomes among self-employed populations were inadequate to support premiums required to finance mandated benefits packages. Nevertheless, the societies remained deficit prone, a factor that led to a single pool of national health insurance in 2000, with partial premium subsidies for the self-employed and full subsidies for the poor, with poverty being continually (annually) assessed by a measure of income and property held by a household (Kwon, 2009).

Subsidies also influenced the growth of China’s health insurance coverage, now at almost 100 per cent (Li & Li, 2019). China’s risk pools can broadly be classified into two categories, the UEMBI (Urban Employee Basic Medical Insurance) and the Urban–Rural Resident Medical Insurance (URRMI) (Wang et al., 2020). The former covers about 300 million urban workers, with one billion being covered under URRMI, comprising non-workers in urban areas and rural residents. Within UEMBI, there are differences in premiums and coverage, and separate pools both geographically and across groups, for formal sector workers, the self-employed and retirees. Premium contributions for the self-employed are based on the average salary in the area, with lower premiums for retirees. All schemes under UEMBI receive government subsidies. The URRMI is heavily subsidised by governments (typically 80 per cent of the premium), although the extent of the subsidy varies by the fiscal capacity of local governments. Additionally, local leaders were incentivised by the party leadership to increase enrolment by linking expanded coverage to their future career prospects (Hsiao et al., 2014). Apart from high levels of enrolment, benefit limits and co-payments limit the impact of adverse selection under UEMBI and URRMI.

Thailand’s approach varies from previous country examples by its explicit reliance on general revenues to cover the missing middle. Prior to 2001, health coverage in Thailand broadly fell into four main groups. The civil servant scheme offered generous benefits to government employees (and their dependents) financed by general revenues; a social security scheme covered employees in the formal sector (but not their dependents); a ‘low-income scheme’ covered poor individuals, elderly and young children with 100 per cent premium subsidy to about one-third of the population; and a voluntary card scheme covered individuals in rural areas on a contributory basis for another 20 per cent. This left uncovered dependents in the private formal sector, and various categories of non-poor, including informal sector workers in urban areas, amounting to some 30 per cent of the population (Tangcharoensathien et al., 2007). In addition, the ‘low-income scheme’ with 100 per cent subsidy was poorly targeted, reflecting the challenge, of identifying the poor in a large informal sector. Although a 50 per cent premium subsidy helped increase the proportion of people covered under the voluntary card scheme, from 1 per cent in 1991 to almost 21 per cent in 2001, there was evidence of adverse selection (Supakankunti, 2000). The ‘universal’ coverage scheme introduced in 2001 covered the poor, the uninsured and the informal sector worker population in one pool and was fully financed from general revenues, leading to a rapid scale-up of the scheme. Thailand has achieved this high level of coverage with a public spending on health of about 2.8 per cent of GDP, as in China, and with a more generous benefits package. This achievement though was underpinned by the rapid growth of the Thai economy, by a favourable political climate and prime ministers consistently backing the state-subsidised coverage of informal sector workers.

Many Indian states have followed a ‘premium subsidy’ model alongside voluntary enrolment. Starting in 2018, a mix of HIMCARE (Himachal Pradesh state public insurance scheme) and PM-JAY was intended to cover all individuals in the state of Himachal Pradesh. Poor individuals, whether classified as such by PM-JAY or under state guidelines, had their premiums fully subsidised. For other vulnerable groups, enrolment premiums were well below the cost of coverage in most private insurance plans in India, but with comparable benefits. The Arogyasri scheme of AP state, when launched in 2007, also had a loose definition of household poverty and provided a 100 per cent premium subsidy. The state of Rajasthan is also moving in this direction. The Megha Health Insurance Scheme of Meghalaya provides a 100 per cent premium subsidy for all, except employees of the state government. Although enrolment rates are high as a share of the population among subsidised groups, evidence on the enrolment rates among non-subsidised populations is unavailable for states, although the experience of the Yeshasvini scheme, discussed next, is instructive.

Karnataka’s Yeshasvini scheme was launched in 2002 and was targeted at members of the registered co-operative societies—mainly agricultural sector workers—comprising 70 per cent of the state’s population. Enrolment was voluntary initially, and effectively automatic by virtue of co-operative societies paying premiums on behalf of members, enrolling them in the scheme. Evaluations of the scheme revealed improved utilisation of healthcare and lowered OOP spending, although these effects were more pronounced for better-off households (Aggarwal, 2010). While it was recognised at the time of the launch of the scheme that member contributions would be insufficient to cover the costs of benefits and government subsidies would be required, not everybody in the government saw the rising use of services and costs of the scheme as desirable. The cost to the government rose from ₹28 ($0.40) per capita in 2003–2004 to ₹393 ($5.50) per capita in 2016–2017. Simultaneously, many members chose not to renew their membership (Kuruvilla et al., 2005). Over the period from 2003–2004 to 2016–2017, members as a proportion of the eligible population fell from 13.9 per cent to 5.7 per cent.

3.4 Implications

The significance of subsidies for increasing coverage among individuals in the missing middle suggests that progress in enrolment will have fiscal implications if the informal sector is large, as in India. Moreover, there remains a high risk of adverse selection, even when enrolment is deemed ‘mandatory’. Although it is generally desirable that a person receives care when in need, even with adverse selection, the benefit so obtained could be deemed inequitable if regular contributors or taxpayers subsidise this individual, especially if they are non-poor. Thailand’s early experience with enrolling low-income groups suggests that poor groups might end up being excluded from coverage if the poor cannot be readily separated from the non-poor when fiscal constraints limit extending coverage to all, and as noted previously, survey data for India suggest that targeting errors may be excluding significant numbers of eligible poor from coverage (Mohanty et al., 2023). Without a strategy to limit eligibility-related errors, and continually identifying changes in economic status over time, the choice appears to be between high levels of subsidy to enrol the missing middle, as in Thailand, which gets around the selection and equity issue altogether, or to adopt a longer-term strategy to wait for the formal sector to become large as a share of the economy, perhaps with voluntarily added coverage in the interim. This latter strategy is what India is currently pursuing in most states, via a mix of private and public insurers.

3.5 Private Versus Public Sector Insurers

The argument in favour of private insurers is their greater responsiveness to incentives and that if sufficiently incentivised, high rates of enrolment will result. Of course, this discussion presupposes that premium contributions are heavily subsidised since voluntary (or even mandated) participation without subsidies does not seem to increase coverage irrespective of insurer type. Recognising the incentives involved, some publicly funded health insurance schemes at the national and state levels in India have engaged private insurers with management and enrolment responsibilities at pre-negotiated premium rates with the overall premium income dependent on the number of eligible people enrolled. A study of the rollout of the RSBY programme in Karnataka that involved private insurers in enrolment found that 85 per cent of the eligible households in four sampled districts were aware of the scheme, and 68 per cent were enrolled within one year of the rollout of the programme (Rajasekhar et al., 2011).

The private insurer (or administrator) of the public sector RSBY scheme in Karnataka was incentivised to enrol, as it triggered premium revenues fully subsidised by the government, but not incentivised to increase utilisation, which would have increased claim payouts. Thus, ‘smart cards’ that could help facilitate access to services were handed out to only two-thirds of the enrolees, the process of empanelling hospitals under RSBY was delayed, as were insurance reimbursements to empanelled hospitals. In AP, a state that experimented with both the private insurer–intermediary model to manage the enrolments and claim payouts and a ‘Trust’ model (essentially an autonomous agency with substantial government and other stakeholder involvement), administrative costs were higher and claims ratios lower for private administrators, compared to the Trust (Nagulapalli & Rokkam, 2015). Other researchers concluded that private insurers and the firms they contract to enrol (under RSBY) ‘economize their enrolment process in terms of village selection, …’ (Palacios et al., 2011, p. 23). The schemes in AP and Karnataka were both characterised by a 100 per cent premium subsidy and no pre-existing condition exclusions, so selection into the scheme by sicker populations (as in Indonesia and Thailand’s voluntary health card scheme) should have been limited, although risk selection by insurers during enrolment could still occur.

Incentives for enrolees and insurers can change dramatically when contributions are not subsidised, enrolment is voluntary, and insurer profits depend on who they enrol, as when the missing middle are targeted via private insurers, with two key implications. First, poor individuals who, for whatever reason, are misclassified as being ineligible for the 100 per cent subsidy under the PM-JAY or state health insurance schemes would likely fall through the cracks for lack of ability to pay. Second, individual policy holders would be more expensive to enrol than groups, owing to adverse selection and corresponding risk selection by insurers, and even left out altogether from coverage (Malhotra et al., 2018). Thus, group insurance is preferable, ideally with compulsory enrolment for the group’s members. Even then, the ability to pay among group members will likely determine the benefits package, as in Korean insurance societies prior to 2000. Without subsidies for premiums, there will be cross-group inequities (Kwon, 2009). And, unless competition for the insured across risk pools is tightly restricted as in Korea and China, private insurers may generate inefficient competition aimed at attracting groups with lower claims ratios in India.

Mandating a common package across groups, no individual risk rating (that is, premiums are based not on the individual’s own claims experience but that of a larger group—sometimes referred to as community risk rating), and the use of ‘risk equalisation’ approaches offer a way out of incentives favouring risk selection. Risk equalisation typically involves reallocating premium subsidies, if the government or national insurance agency subsidises premiums, to different insurers depending on their claims experience relative to the community risk profile of their members, as in many European countries. In Australia, resources are reallocated from insurance companies that have a more favourable claims experience, compared to others that have a less favourable one, at the end of each year (Stoelwinder, 2014). But this requires considerable regulatory capacities, which are sometimes lacking even in high-income countries—and are certainly a major constraint in India.

Can public and private insurers exist side by side? A public insurer, such as the National Health Authority in India, can regulate by competition, offering a guaranteed product to members of the uncovered middle. The Chilean experience, though, suggests a situation whereby the public insurer ends up with individuals with high claims expenses, with private insurers carrying out extensive risk selection to enrol the healthiest population segments (Roman-Urrestarazu et al., 2018). Following reforms in 1980, the Chilean insurance system consisted of FONASA (Fondo Nacional de Salud), the public insurer, and ISAPREs (Instituciones de Salud Previsional), a collection of private insurers. The poor were covered by FONASA, and civil servants were covered under a separate scheme. The rest could either access FONASA with premiums pre-set at a share of the wage; or, if they chose ISAPRE, they could use the same wage-based contribution, along with a top-up, since the premiums were typically greater than the wage-based contribution rate. The ISAPRE practised individual risk rating in setting premiums. Individuals with low incomes or those with a history of illness typically ended in FONASA, so the share of social insurance contributions received by ISAPRE was substantially higher than their share in health spending (Holst et al., 2004), with adverse implications for both equity and efficiency. Recent health insurance reforms in Chile have tried to address these concerns by lowering incentives for risk selection by setting a base premium for a standard benefits package and establishing limits on how far ISAPRE premiums could move away from this standard, introducing risk equalisation funds to compensate insurers with higher claims ratios and limiting individual risk rating.

The preceding discussion has implications for progressing contributory health insurance in India for the missing middle. Given that government policy documents (e.g., Niti Aayog, 2019) often discuss the role of public insurers (such as the ESIS or the National Health Authority) in progressing the coverage of the missing middle, three key challenges are apparent. First, public insurers such as the ESIS are likely to require considerable enhancement of their capacity for managing an insurer role, including ways to enhance accountability to its enrolees, by improving the healthcare services it funds, and paying attention to equity objectives. A key capacity constraint relates to the insurer’s ability to purchase services aligned with priorities, to negotiate prices with service performance guidelines, and to be able to monitor and evaluate the performance of providers of services. Effective price negotiations often require good costing data, and this is often lacking as the recent Supreme Court judgment attests (Tiwari et al., 2024). Second, relying on private insurers in this environment will mean directing attention to multiple regulatory issues, including standardisation of benefits packages, incentives to promote group coverage, and perhaps risk equalisation. Finally, relying on mandatory enrolment without large premium subsidies to limit adverse selection and increase enrolment is unlikely to work, given the experience of Vietnam, Indonesia and elsewhere, as potential enrolees in the informal sector may discontinue their premium contributions if their incomes are uncertain, or choose to selectively insure themselves when sick.

4. Implications on Ways Forward for India

Countries that have been able to address the burden of OOP spending, including LMICs, have done so only through successfully implementing some form of population-level risk pooling. Thailand’s universal coverage scheme helped reduce the incidence of catastrophic spending from 6 per cent in 1996 to 2 per cent in 2015; the number of people falling into poverty due to health-related causes also decreased significantly (Tangcharoensathien et al., 2020). Similarly, Vietnam’s social health insurance increased its population coverage from 47 to 70 per cent between 2008 and 2014; in this period, Vietnam saw a reduction in catastrophic spending from 5.5 to 2.3 per cent and a reduction in health-related impoverishment from 3.5 to 1.7 per cent (Lêet al., 2019). How might one do this in India given the large number of people who are likely to be left uncovered under existing schemes?

As noted above, one possibility is increased investments in public sector health provision leading to a strengthened public sector that provides subsidised services to all could yield improved health outcomes and improved protection against financial risk among the poor and informal sector populations while avoiding potentially high costs of identifying the poor. Good-quality public services could also offer competition to private sector providers and an element of choice to users of health services.

In contrast, one can take the view that the proverbial ‘ship has sailed’, given the large and growing central and state government investments in publicly financed insurance for the poor that support both public and private inpatient care, with financial incentives driving performance. At the very least, given the added funding for hospital cover that existing public programmes provide, further supply-side financing for public sector hospital services is unlikely to be directly available.

How about supply-side investments in the public primary care sector? Primary sector investments could also help address a major driver of OOP spending in India, namely, outpatient services, and thus help address risk protection concerns raised by a relatively shallow private insurance coverage and public sector insurance that emphasises hospital-based care. The ‘Ayushman Bharat’ is the latest in a series of national- and state-level initiatives to try to improve public sector primary care in India, which has tended to be pro-poor. Investments in public primary care services in rural areas of India, where a large share of the poor population and informal sector workers reside, can improve utilisation and lower private provider use by the poor. While serious questions have been raised about the public provision of health services in India, private provision of primary care also has its own problems, including a vast number of unqualified providers, weak regulatory oversight and few checks over the quality of care and fees charged. There is a track record of good service delivery at the primary care level in at least a few states, which could serve as a model for others. Given that there is already an infrastructure, including that supported by the National Rural Health Mission, additional financial investments in the primary sector to improve service quality might be manageable.

If investments in public sector delivery are not forthcoming, another primary care option might be a model that permits access to public and private outpatient services, for example, in Australia (and some other countries), with all providers satisfying certain qualifying standards being reimbursed by a central payer or public insurer at the state level. In Australia, though, due to a long-standing constitutional provision, general practitioners can independently set fees above the reimbursement rate, resulting in high OOP payments. In India, where large numbers of individuals pay OOP for private outpatient care, it will be difficult for insurers to set provider payment rates, without addressing private providers’ access to an alternative market-health services for individuals with direct OOP payment. Thus, harnessing (pooling of) OOP payments is potentially a key step to the effective engagement of private primary care providers for serving UHC objectives, a challenging assignment in the short run, but likely feasible in the longer run. In the interim, subsidised public sector primary care services will likely be key to addressing the healthcare needs of the less well-off among the missing middle and the poor. The proposed heavy investments in infrastructure for public healthcare delivery in India, labelled the ‘Ayushman Bharat Health Infrastructure Mission’ (MOHFW, 2021), are aligned with this strategy.

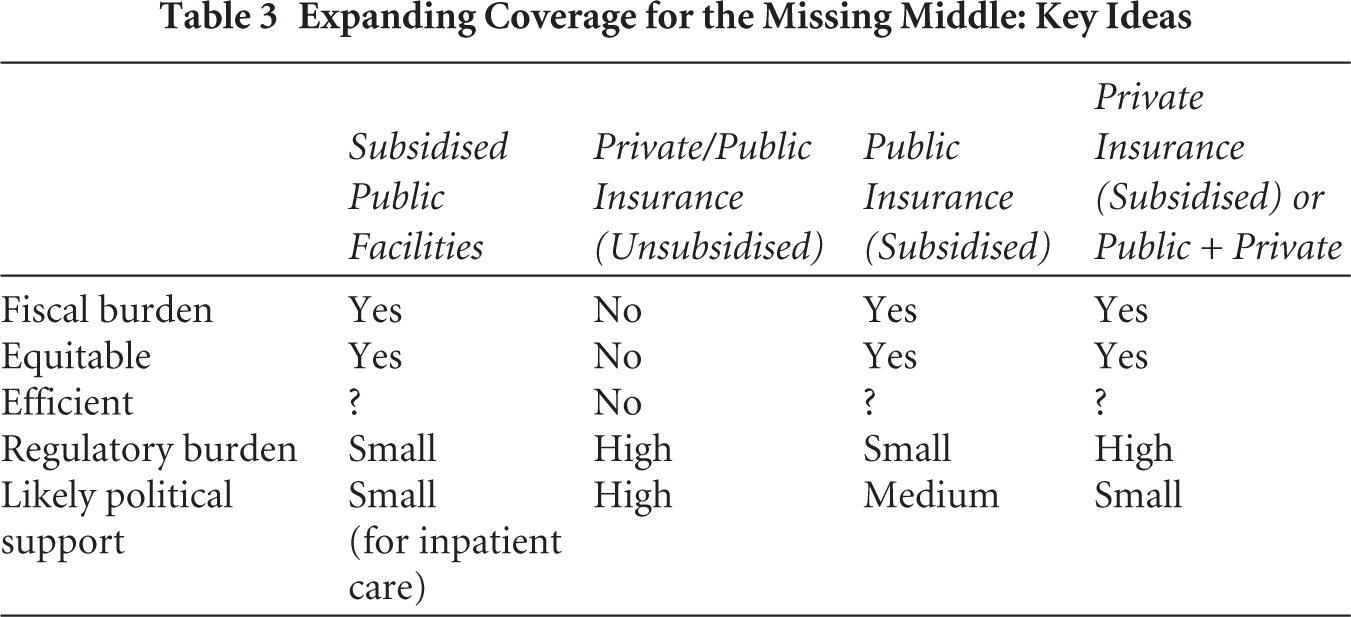

For inpatient services, the message from the literature is broadly that if public resources are sufficient, the most effective mechanism is providing highly subsidised cover for all. Some Indian states are moving in this direction. The alternative, suggested in a government policy paper (Niti Aayog, 2021), that members of the missing middle mostly pay their own premiums will result in a smaller fiscal burden on governments (Box 1). However, the consequence is likely a slow expansion in coverage and inequitable outcomes. Leaving the responsibility of covering the missing middle to private insurers is likely to be even less successful than via publicly funded insurance, and even then, the strategy would need to be centred around insurance of groups. Strong regulatory oversight would also be needed to manage insurer competition, which the IRDAI and the states currently lack (see Table 3 for key ideas emerging from this article).

Box 1. Pros and Cons of Premium-based Inpatient Coverage for the Missing Middle in India

Sidesteps governance and accountability challenges of public service provision and builds on existing programme experience at the state and national levels. Adds resources to the health sector, including to public facilities. Introduces accountability among providers as funding tracks patients.

Without publicly subsidised contributions, enrolment rates remain low, and adverse selection risks high. Limited oversight and management capacity for regulation if there is competition among insurers. If resources are limited, will incur costs on identification of poor and vulnerable segments of the missing middle for equity.

Expanding Coverage for the Missing Middle: Key Ideas

4.1 Longer-term Prospects

Thus far, we have stressed two relatively unlinked strategies to progress towards universal coverage in India: an approach that relies on public service investments to provide universal access to primary care, and a strategy of subsidised premiums to provide hospital coverage. The emphasis on the delivery of primary sector services suggests two important caveats about this approach that may need careful attention. First, the demand-side (insurance-driven) model for access to good quality inpatient care relies on the availability of such services in proximity to the covered population. One might suppose that effective demand for services will generate supply, and perhaps it will do so in the long run, but in the short run, there are likely to be service delivery gaps, with consequences for equity, efficiency and the credibility of such schemes. Second, this model can be financially costly without strong two-way referral linkages or inpatient gatekeeping functions. Currently, third-party hospital coverage insurers, such as the National Health Authority of India or the state-level insurers, do not have the capacity to execute or exercise oversight of referral linkages. Concerns about patients bypassing primary care and heading directly to specialists (and associated inefficiency) are well recognised in India and elsewhere and are an important reason for integrated service provision by organisations such as Kaiser Permanente in the United States, and more recently, insurance-funded integrated provision of healthcare services in Thailand.

The approach adopted by the Netherlands (and some other Northern European countries) to achieve UHC is instructive here. In the Netherlands, health insurance is mandatory, and the standard benefits package includes primary care delivered by general practitioners (Faber et al., 2012). All Dutch residents need to register with a (usually local) general practice (GP) which they can choose (and change if needed). The GP is the gatekeeper to all hospital-based and specialist care and access to higher levels of care (except emergencies) must be initiated and coordinated by the GP. While there is some co-payment for specialist care, GP visits attract no co-payments. In practice, this means that more than 90 per cent of all new health problems presenting at the primary care level are managed at that level. The service integration across levels of care and the broader financial integration are such that they enable the efficient deployment of financial and human resources across the health system by supporting the return of patients from higher centres back to GPs; they also support the delegation of tasks within GP practices from physicians to practice nurses. Thailand is also moving towards such a model, emphasising that, ‘primary care needs to move from its traditional role of providing basic disease-based care, to being the first point of contact in an integrated, coordinated, community-oriented and person-focused care system’ (Sumriddetchkajorn et al., 2019).

How might one approach the challenge of service delivery gaps confronting insurance-funded demand for care and integrated care in India? While a detailed response to these questions is a separate article by itself, it is worth noting that Thailand’s expanded insurance coverage benefited from extensive public investments in health facilities in the decades preceding. Instead of relying solely on private sector responses, governments in India could selectively strengthen access to public sector facilities in areas that lack an adequate supply of hospital services. More generally, we also contend that India requires to formulate a contextualised framework for the provision of integrated, coordinated and responsive services, perhaps involving an initial process of experimentation and learning, given the limited experience with such models. The integration and coordination are about the financing of services and the delivery of services across all levels of care. An initiative that can operate at scale and can thus serve as a living learning lab which yields macro (policy and design)-, meso (institutional and managerial arrangements)- and micro-level (implementation and service provision) insights on what will work, for whom, how and why, is required at this stage, rather than wholesale reforms whose outcomes may be hard to predict. While some of the state schemes discussed earlier could play this role, the countrywide ESIS is perhaps optimally placed to serve this function (Prasad & Ghosh, 2020). While the ESIS has its issues too, it has all the features and building blocks for an integrated system to be initiated and kickstarted quickly—and is well placed to overcome the key bottleneck of fragmented care provision (Niti Aayog, 2019). This is because it functions at a large enough scale, being the largest contributory risk pooling system in India, covering more than 100 million workers and their dependents with an existing mandate to provide health insurance coverage to all formal sector workers (earning less than ₹21,000 ($300) per month) and their dependents. The ESIS provides coverage through funding a network of dispensaries (primary care level providers) and hospitals. One possible extension of its responsibilities could involve ESIS expanding its coverage to include the informal non-poor in a contributory health insurance, although this would first need strengthening ESIS functioning in health service delivery (Niti Aayog, 2019). ESIS’s recent opening of its hospitals and services to PM-JAY beneficiaries, and (implicitly) raising the opportunity to include the non-poor in the informal sector, presents a timely opportunity to attempt a potentially insightful natural policy experiment.

Footnotes

Acknowledgements

We are grateful to Dr Jack Langenbrunner for comments on a previous draft of this paper.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was partly supported by a grant from the Health Systems Transformation Platform.