Abstract

The question of foreign direct investment (FDI) and socio-political development is debated heavily. Liberals believe that FDI brings economic opportunities and/or increased incentives for peace and security among host societies. Critics suggest that FDI is exploitative, leading to conditions that increase the risk of violence. We take a political economy perspective that views FDI as problematic depending on how FDI affects politically powerful local interests. As such, all forms of FDI should meet domestic opposition, but only FDI in the extractive sector, where domestic political actors have little at stake, escalates to major war. Building on recent work which examines this question pertaining to extractive sector FDI, we introduce sub-national, geo-referenced data on FDI in all sectors for evaluating local conflict using combined data from four distinct geo-referenced conflict databases. Using site-period fixed effects with a difference-in-difference like approach, we find that FDI in all sectors increases local conflict. Conflicts induced by most FDI sectors fall short of becoming civil war, except for extractive sector FDI.

The government will also address all other matters that relate to the creation of an attractive investment climate for both domestic and foreign investors, conscious of the fact that we have to compete with the rest of the world in terms of attracting, in particular, foreign direct investment. (Nelson Mandela. Newly elected President of South Africa. The State of the Nation Speech, 24 May, 1994.)

1

Lack of managerial skills and capital among Botswana will lead to a situation where the economy will be in the hands of foreigners which will ultimately impact on the policy of the country…. It is like a man who marries a rich woman. He will lose control over the affairs of his house. (Former leader of the opposition in Botswana, Kenneth Koma. Cited in Moss, Ramachandran & Shah (2004: 342).)

Introduction

The quotations from Nelson Mandela and a prominent Botswanan politician, Kenneth Koma, above feed into a long and contentious debate between liberal/modernization theorists and dependency and other critical theorists about the desirability of foreign direct investment (FDI) from transnational corporations (TNCs) for economic and socio-political progress (Seligson & Passé-Smith, 1998). The quotations highlight the tensions between domestic and foreign economic interests, and illustrate how such tensions spillover into politics, affecting the economic futures of countries (Moss, Ramachandran & Shah, 2004). The modernization school argues that FDI promotes economic growth and development because TNCs bring much-needed investment, new ideas and technology, and they open up richer markets for developing countries (Asiedu, 2006; Lipsey, 2000). The neo-Marxist/dependency theorists argue that FDI is simply monopoly capitalism that exploits the poor and undermines local institutions, placing profits over the interests of poor people (Léonard et al., 2014). Liberals counter that very little FDI flows to poor countries because weak institutions, political instability and other risks dissuade TNCs from investing among the poor (Moran, Graham & Blomström, 2005; Asiedu, 2006; Vadlamannati 2012). As some suggest, the problem with FDI is that there is too little of it in the poor world, not too much (Lipsey, 2000; Bhagwati, 2004). Yet, as Mandela's quotation above suggests, governments pursue FDI because they lack capital for generating growth, which brings jobs and tax revenues, particularly following the disastrous failure of import substitution industrialization (ISI) policies.

Critics of FDI argue that investments from TNCs bring negative externalities, such as political instability and civil war. A recent study by Kishi, Maggio & Raleigh (2017) suggests that African conflicts can be explained by the degree to which states are dependent on FDI because finance from TNCs encourages states to ‘securitize,’ or seek military solutions, rather than make reforms. Their argument is that FDI provides revenues to states for pursuing military options, reducing incentives to make concessions. Similarly, Pinto & Zhu (2022), using a global sample, find that FDI increases the risk of a civil war onset. They argue that FDI increases market concentration, producing high rents over which states and challengers fight, which is particularly likely within weak states (Pinto & Zhu, 2022). Others focus specifically on natural resource extraction, assessing disaggregated data on FDI in mining activity, where conflict is driven by the extortion of companies by ‘loot seeking’ rebels, or issues pertaining to disagreements between foreign companies and host communities (Berman et al., 2017; Wegenast & Schneider, 2017; Mihalache-O’Keef, 2018; Christensen, 2019; Vadlamannati et al., 2020).

We expand on these studies in several distinct ways. First, we argue that focusing only on mining activity is unnecessarily restrictive because FDI, in any form, is potentially ‘lootable’ because of the ‘obsolescing bargain,’ where FDI projects become vulnerable due to sunk costs post hoc. Where state institutions guaranteeing security are weak, FDI projects in Africa are likely to be politicized simply because they are large and visible. Accordingly, we examine the impact of all types of FDI, not just mining, on the risk of proximate conflict. If weak state arguments are correct, then FDI’s impact on conflict should not be sector dependent since any foreign finance, regardless of sector, should matter for weakening states and securitizing politics. If the mechanism to conflict is the availability of ‘lootable’ rents due to market concentration, then all forms of FDI should matter.

Secondly, our theoretical argument broadens Christensen’s (2019) logic of bargaining failure under imperfect information and uses information on FDI projects in all sectors using geo-referenced, project-level, FDI data from the Financial Times’ ‘fDi Markets’ database. We suggest that FDI causes local level conflict because FDI is a threat to the monopoly rents enjoyed by local capital. FDI potentially displaces powerful local economic actors and is conflict prone when its ‘displacement’ effects threaten powerful local interests. Some sectors should be more important for powerful local interests than others, but industrial and service projects should be more enticing for domestic elites to squabble over than mining, which is often very capital intensive and oligopolistic. Comparatively, an agro-business or tourism project is likely to displace well-placed domestic actors with access to political power, but these same actors should have very high opportunity costs for organizing large-scale violence. As some argue, domestic capitalists/governments own the largest share of the capital stock, which would make large-scale violence very costly for domestic commercial interests (de Soysa, 2020). Thirdly, we use new aggregation techniques developed by Donnay et al. (2019) to merge conflict data from four distinct conflict databases: the Armed Conflict Location and Event Data Project (ACLED) (Raleigh et al., 2010); the Georeferenced Event Dataset (GED) (Croicu & Sundberg, 2017); the Global Terrorism Database (GTD) (START, 2022); and the Social Conflict Analysis Database (SCAD) (Salehyan & Hendrix, 2017). These data allow us to examine gradations of violence from non-fatal to fatal conflicts as well as civil wars based on established battle-death thresholds. We also add methodological innovations by more directly addressing the modifiable areal unit problem (MAUP) that can introduce bias into spatial studies and by directly accounting for spatial–temporal autocorrelation.

Unlike the broader studies focusing on FDI and civil war, which mostly use country-level data with aggregated FDI, we use disaggregated FDI at the sub-national level, as domestic political economy arguments, such as de Soysa’s (2020), assume that powerful domestic actors have the same incentive for challenging FDI. In most instances, these actors will likely be responding to local rather than national FDI and thus the empirical linkage between local FDI and local conflict is a more convincing empirical approach. Thus, like Christensen (2019), we study the relationship between FDI and conflict by utilizing local, geo-referenced data that allow us to employ location-period fixed effects in a spatial–temporal, difference-in-difference like, approach which allows us to mitigate some of the endogenous selection effects of both conflict and FDI. However, whereas Christensen (2019) focused exclusively on mining concessions, we focus on all FDI with refined theoretical expectations about how different types of FDI might have heterogeneous impacts on different types (fatal, non-fatal and major) of conflicts. Using a panel of five-minute grid cells, we find strong evidence that the arrival of local FDI exacerbates subsequent local conflict, when defining both FDI and conflict broadly. However, we find that this relationship is more pronounced for fatal conflicts short of civil war, although this is also conditional on the FDI sector. While the results are generally in line with Christensen’s (2019) findings, suggesting broad replicability using a full spectrum of FDI projects, they also add a degree of nuance. Extractive FDI is the only type that is associated with major conflict. Likewise, FDI in the real estate and service sectors appear only to incite violent (fatal) conflicts, while FDI in the extractive and industry sectors prompts both fatal and non-fatal conflicts. Why violence under these circumstances does not escalate to civil war level needs to be explained, which we theorize is dependent on the incentives of local elites for maintaining stability due to their high opportunity costs. Our findings are robust to many different estimators, spatial capture distances and spatial correlation concerns.

Theory

Modernization theorists argue that FDI offers an opportunity for poor countries to obtain the capital and technology needed for joining global markets (de Mello, 1999; de Soysa & Oneal, 1999; Adams, 2009). Expanded economic contact with companies and markets abroad exposes poor countries to best practices of governance, potentially boosting the legal institutions and business practices (Becker & Sklar, 1999). Indeed, recent work using sub-national data has found that local FDI can reduce local individual experiences with corruption (Brazys & Kotsadam, 2020). Thus, a broad strand of literature generally suggests the more FDI the better for social outcomes because all the processes mentioned above can reduce the risks of costly armed conflict by raising the opportunity costs of people for engaging in violence. Moreover, the presence of foreign companies increases the audience costs for governments to make reforms rather than use repressive tactics against opposition because bad press abroad can harm future flows of FDI (Vadlamannati, Janz, & Berntsen, 2018).

Many argue that FDI avoids bad governance, poor infrastructure, political instability and low productivity of labour, which might explain why Africa receives very low levels of FDI (Asiedu, 2006). However, an often ignored, but critical, reason as to why FDI has been reluctant to flow to poor countries was largely because of the hostility of parochial elites reluctant to encourage change and accept competition. Modernization undermines the position of the parochial economic and political elites, who often reap monopoly rents (Krasner, 1985; Asiedu, 2004). Indeed, FDI experienced high rates of ‘expropriation’ in newly-decolonizing countries (Vernon, 1971). The ‘obsolescing bargain’ gave host governments all the power after the investment is made because of high sunk costs, which often resulted in a change in the terms of entry post hoc, increasing risks for FDI. Since the end of the Cold War, however, developing countries have clamoured for FDI, and the share of FDI going to poor countries has steadily increased, with some of this increase coming from new sources of FDI, such as India and China (Asiedu, 2004; Sumner, 2008).

Contrary to the liberal/modernization view, dependency/critical theories suggest that FDI corrupts local processes, increasing the chances of political failure and violence (Boswell & Dixon, 1990; Léonard et al., 2014). These theorists see local militant actions against FDI as ‘heroic resistance’ (Cramer, 2002). A recent study on FDI and armed conflict in Africa provides evidence in support of the pessimistic arguments on FDI (Kishi, Maggio & Raleigh, 2017). They suggest that states dependent on outside sources of unconditional finance are likely to be weak states motivated to please these foreign sources of finance. As a result, FDI incentivizes these ‘bad’ states to ‘securitize’ rather than reform, ending in social resistance and violence. They present evidence, at the country level, showing that larger stocks of FDI increase conflict events, which they interpret as support for their state ‘securitization’ thesis. Apparently, states are less willing to negotiate and more willing to use force when FDI is a larger source of revenue. Indeed, both the liberal and the weak state/securitization arguments expect uniform effects of all types of FDI.

While acknowledging the possibility that FDI might promote violence in two ways – (A) as a ‘honey pot’ for rebels, and (B) by incentivizing securitization – Kishi et al. (2017) interpret their statistical tests as support for the latter possibility. They conclude that: The proposed link between FDI and securitization violence is that regimes may use access to external financial resources to further their power and longevity through intervention in conflict and repression, where violence against both challengers and citizens remains an effective way for regimes to secure control (Kishi et al., 2017: 19).

Many others focus on FDI and conflict from the standpoint of FDI as ‘lootable income.’ Berman et al. (2017) and Christensen (2019) focus only on extractive activity, or mining FDI, at the sub-national level because such activity apparently is more vulnerable due to high sunk costs and capturability by either rebels or organized local interests. The former, focusing on all extractive activity, finds that a commodity price increase raises the risk of violence in a mine area, and that controlling a mining area increases the risk of conflict spreading outside to areas adjacent to mines. They interpret these findings as support for the view that mines offer increased sources of finance for rebels. These findings support a larger literature on civil war suggesting that, rather than political and other grievances, conflict is organized by groups that find fighting feasible due to the availability of ‘lootable’ income (Collier et al., 2003; Ross, 2004). Some also report that the increased risk of conflict is dependent on the type of corporation engaged in the mining activity and the nature of the host country’s institutions (Wegenast & Schneider, 2017).

Christensen (2019), utilizing data specifically on FDI in mining activity finds, however, that the risk of conflict is explained almost entirely by a spike in riots and protest, but that the risk of more severe armed conflict remains low. He attributes the violence associated with mining to artisanal mines easily controlled by rebels rather than to more capital-intensive projects typical of FDI-based activity. Christensen’s carefully constructed study first eliminates competing grievance-based explanations for why there might be higher protest at FDI sites, such as labour unrest, in-migration and displacement effects, health and environmental conditions, inequality issues, and local corruption. Finding no support for such explanations, he offers a theory based on bargaining under incomplete information.

Since a local community’s expectations rise about what they hope to gain from mining projects, protest and small-scale violent events erupt when the companies and the local community are unable to find mutually acceptable solutions. Companies, which already have some idea of what their risks and rewards are likely to be before investing, will be reluctant to, or unable to, meet the expectations of a community post hoc. Communities, in turn, with little access to information about the true profitability of projects, will be reluctant to be ‘low-balled’ by the company, resorting to protests, strikes and other activity to stop the activities of the company, or hurt the company economically for ascertaining how far the company will go. Low-level violence, thus, is a bargaining device. We use this theory of bargaining under imperfect information, which is often invoked as a general theory for the failure of peace agreements and the continuation of civil war, to argue that all FDI projects, not just in mining, are likely to be affected similarly (Fearon, 1995; Blattman, 2022). Why, for example, would a hotel project (compared with a mine) not elicit similar responses from local populations? Also, if FDI weakens state resolve for reforming over securitizing (militarizing), why mining alone should matter is not entirely defensible – rents are rents! Indeed, if Pinto & Zhu (2022) are correct in their argument about market concentration driving FDI conflicts, then all FDI projects should matter. Thus, we examine all FDI sectors and go a step further to explain why FDI projects may not impact the incidence of civil war measured by the standard of battle-related deaths, even if FDI projects increase political unrest.

More than in mining, the information problem is likely to be as severe in manufacturing, or even services. In the Christensen (2019) schema, bargaining occurs between the local community and the mining company, and it is assumed that the local community’s interests are represented by leaders. In many poor countries, political unrest is orchestrated by higher authorities and well-placed elites, and such events are rarely, if ever, spontaneous, or bottom up, representing the true interests of those who suffer the costs (Chenoweth & Ulfelder, 2017; Blattman, 2022). The power of local and national political authorities to use force is generally unimpeded by institutional and political concerns, which are hallmarks of weak states. Poor communities, thus, must contend with potentially facing the full force of a state’s apparatus of coercion. A community, particularly those finding direct employment from the firm and other goodies in terms of corporate social responsibility projects, etc. are also likely to be hurt directly if the company decides to halt its activities, even temporarily. If mining activity is not protested due to wide-spread grievances, which would justify assessing how an entire community transacts (bargains) with a company, it is more reasonable to assume that such movements are orchestrated by a leadership, whether political or economic in nature, for whom extorting a company has concentrated benefits.

We have no quarrel with Christensen’s (2019) explanation, which is convincing, but by identifying the organized nature of the small scale protest and violence, we are able to show that such projects are unlikely to spawn bigger conflicts (civil wars) because the leaderships of these communities and central government authorities that might initially ignore protest have higher opportunity costs if indeed these conflicts are not resolved short of deadly violence. Consider that, according to the World Bank’s World Development Indicators online database, in 2020, the annual FDI inward flows to the whole of Sub-Saharan Africa amounted to a paltry 1.8% of gross domestic product on average. 2 It is hard to believe that FDI influences states to greater degrees than domestic capitalists given this ratio. Thus, a state’s willingness and effort to protect FDI and resolve conflict is likely to be greater the higher the stakes in the FDI–local community disputes. Moreover, the effect of FDI on conflict is unlikely to be uniform, but sector dependent, based on the nature of political opposition to FDI, which we term the ‘displacement’ effect.

As suggested above, the attitudes of host countries to FDI began to change around the mid-1980s because many countries, particularly in Africa, were facing massive debt crises and structural problems in their economies (Srinivasan & Baghwati, 2001; Asiedu, 2004). These countries shed their ideological commitments to ISI strategies and approached the multilateral lending institutions, such as the International Monetary Fund and the World Bank for help (Ranis, Vreeland & Kosack, 2006). At the same time, countries began to sign bilateral investment treating (BITs) with the United States and other powerful economies, binding these countries to a host of multilateral rules, often with the Multilateral Investment Guarantee Agency (MIGA) underwriting these investments (Ramamurti, 2001). The MIGA is aimed particularly at addressing questions arising from civil disturbances and political conflict (Collins, 2015). The BITs bind the host country to following international laws governing economic relations and contravening these agreements would have high costs for host governments in terms of their relationships with powerful markets, particularly for trade and other partnerships. Consider that the incidence of expropriations, for example, had reached a high of as much as 80 incidents per annum before the 1990s, which dropped to less than a handful by the late 1990s. As many suggest, the multilateral track by which poor countries have seen a massive gain in FDI has also come with much greater multilateral control over the bargaining power of host countries (Ramamurti, 2001). For these reasons, we argue that government incentives to protect FDI have been raised to new levels, reducing the chances that bargaining failure in FDI–community conflicts and powerful local actors escalate to levels reaching civil war, even if such projects are likely to generate high levels of contention. Indeed, the effect of FDI in poor countries highly dependent on this form of capital is one reason that scholars argue that FDI’s effects are likely to be problematic in poor countries and not in rich ones where state dependence on external capital is likely to be low and where societal actors have high opportunity costs for organizing large-scale violence.

A central government is likely to authorize projects, largely bound by the multilateral rules and bilateral treaty agreements governing the host government–FDI relations. A company also wields most of the power relative to a government at this stage because it can change its mind about where to locate. Once invested, however, the company has sunk costs and community–company bargaining failure is likely, particularly because FDI is easily extorted by local political forces. The nature of these conflicts, however, are likely to be heterogeneous given the differential impacts of the different types of FDI, particularly on powerful local interests. The most powerful local interests are likely to be occupying the ‘commanding heights’ of an economy, such as industry and services, where local capital (and labour) potentially earn monopoly rents. In these circumstances, TNCs are in direct competition with local capital, for example, by competing over inputs to production, such as land and labour (Moss, Ramachandran & Shah, 2004). Or it might be political in that FDI may displace employment (organized labour) in highly protected state enterprises. Many of these conflicts might, in fact, not be ‘societal’ or ‘community-related’ but largely orchestrated by powerful domestic actors that hope to scare off FDI or raise costs on them.

Under these conditions, companies can appeal to the multilateral rules and request central government assistance, or they could cease operations. Given both the real costs from tax revenues forgone and reputation costs of the multilateral spotlight, central government authorities and elites have very high incentives to avoid the conditions of costly high-level conflict. State capacity from increased revenue and willingness to end costly violence, thus, increases the possibility that these low-level disputes end short of war. The economic elite too have a massive interest in avoiding disruptive war because they own the largest share of a country’s capital stock. If our argumentation is correct, then we should be able to replicate Christensen’s (2019) finding with all FDI projects, rather than just mining. We should also find that FDI-related conflict stops short of major civil war except in the case of the extractive sector, where local elites have little control over distant mining projects (weak state capacity), have very little invested in such projects and thus low stake in this sector (weak effort), and these distant rebel-led insurgencies (civil wars) often do not threaten the broader capital stock (low losses).

If our reasoning that powerful domestic interests in opposition matter for predicting FDI-related conflict, then FDI in a sector such as mining should have the least opposition given that mining very rarely has organized domestic interests due to very low labour intensity in mining and low domestic interest due to the highly concentrated ownership structures in the global mining business. It is also interesting to note that extractive industries make up less than 5% of projects and 21% of investment assessed in dollar terms in the data we use. This fact alone tells us that lumping all FDI together in analyses of conflict as well as lumping all conflict as major violence over some battle-death threshold might only provide partial pictures. In short, we believe that the FDI–conflict relationship should be examined for all FDI and assessed according to its impact across sectors, across conflict types, and assessed by the displacement effects of FDI on powerful local interests. If FDI is uniformly beneficial or detrimental, then the political economy argument would be weak. Contrarily, if the effects of FDI are heterogeneous on political conflict, then it is highly likely that conflict occurs when the losers from FDI are well placed. For these reasons, we believe that FDI in sectors other than the extractive sector also generate conflict, but these conflicts are likely not to escalate to full blown civil wars.

Methods and data

To test our expectation, we use data from multiple sources. There are several different geo-referenced conflict datasets for the Africa region. Specifically, the Armed Conflict Location ACLED, the SCAD, the GED, and the GTD contain geo-referenced coverage of protest and violent conflict events. As discussed in Donnay et al. (2019), there are strong reasons to use data from all these datasets when analysing conflict. Each of these datasets have strengths in terms of their coverage, yet none is complete. These datasets contain different types of events which we will utilize to create several outcome measures based on conflict characteristics. The ACLED dataset focused primarily on armed conflict events (military attacks, sexual violence and violent demonstration) while the SCAD dataset considers a broader range of social conflict events. The GED dataset is a geo-referenced version of the Uppsala Conflict Data Program database which primarily tracks armed conflict and civil war. Finally, the GTD is focuses exclusively on (violent) domestic and international terrorist events. Accordingly, omitting events from any of these datasets potentially leads to biased analyses (Donnay et al., 2019).

Accordingly, we follow Donnay et al. (2019) by using the Matching Event Data by Location, Time and Type algorithm used in that paper to combine the four datasets along temporal and geographic dimensions. Full details can be found in Table A2 in the Online appendix, but starting from 551,641 input observations, the algorithm finds 64,016 duplicates, leaving a total of 487,625 unique conflict event observations globally. To create our outcome variable, we use 303,453 five-minute grid cells compiled by the International Food Policy Research Institute as our unit of analysis. Our empirical approach largely follows Christensen (2019), with a few notable exceptions. We first spatially join the conflict events data to the grid cells. We use this information to create our primary outcome variable, a binary indicator coded ‘1’ if a grid cell-year had any conflict within the grid cell from any of the datasets. We then create binary sub-measures which we code as ‘1’ if the grid-cell year had any fatal conflict, no fatal conflict, or major conflicts if the grid-cell year had 25 or more deaths. In the robustness checks, we employ a measure that utilizes the count of conflicts in the grid cell-year.

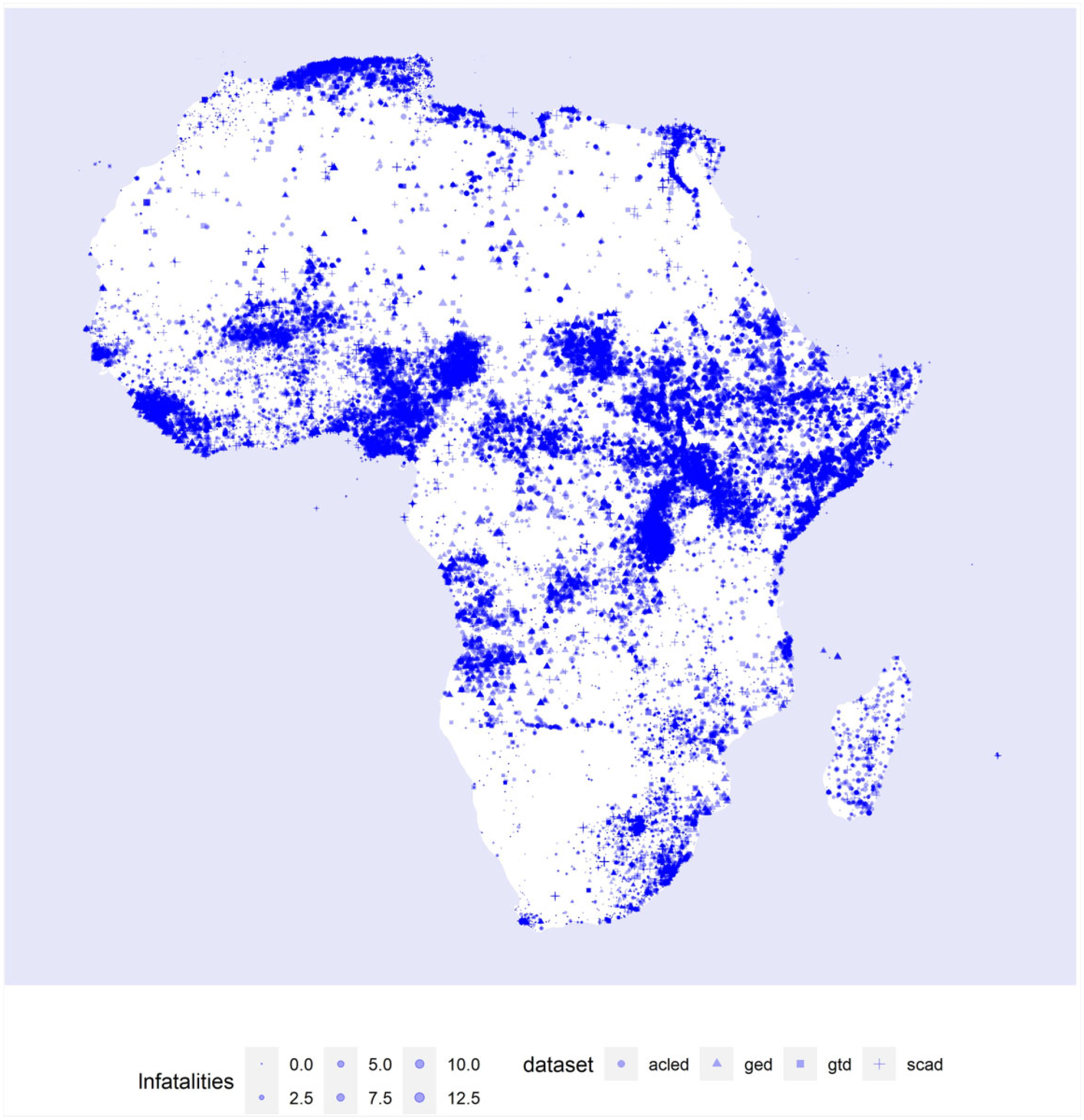

Our main explanatory variable is greenfield and expansion FDI projects sourced from the Financial Times’ ‘fDi Markets’ database. This database includes nearly 10,000 green-field, expansion, and co-location, FDI projects in 56 African countries from 2003 to 2017. While these data undoubtedly miss some FDI projects, we believe they are reasonably complete and they have been employed in several recent studies and are used as foundational data for investment statistics compiled by the World Bank, the United Nations Conference on Trade and Development and more than 100 national governments (Gil-Pareja, Vivero & Paniagua, 2013; Owen, 2019; Saltnes, Brazys, Lacey & Pillai 2020). To the extent that there is missing FDI, this is likely to bias any results toward the ‘null’ of a non-finding as it will result in ‘treated’ units being classified as ‘untreated.’ Like Brazys & Kotsadam (2020), we utilize the geographical information in these data, namely the city-names which are available for 5,701 of the projects. Of these projects, 5,203 are greenfield investments, 437 are expansions and 61 are co-location projects. Using the city centroid coordinates, we spatially join these projects to grid-cells in order to create our primary explanatory variable of active FDI, a binary indicator that equals ‘1’ for the current and subsequent years of the first FDI project in the capture radius of a given grid cell. These data also have information on FDI sector. Accordingly, we group FDI projects into four broad types: extractive; industrial; service-oriented; and real estate. The full listing of sectors, and which category we assigned them to, is available in the Online appendix. We plot the location of both FDI projects (black diamonds) and conflict events (blue shapes) in the map in Figure 1.

Our identification strategy employs location-period fixed effects in a manner like the most conservative estimations in Christensen (2019). Our sample of grid cells includes those that will receive FDI at some point and their neighbouring cells. As discussed in Christensen (2019), when employed with site-period fixed effects, this allows for a difference-in-difference like comparison wherein we compare the grid cell-years with active FDI to the years in those grid cells prior to the FDI becoming active and to neighbouring cells which received no FDI. The assumption underlying the inclusion of neighbouring cells as comparators is that they should be reasonably like the ‘active’ cells on all other potential time-varying confounders. The comparison of grid-cell years after FDI to years at the same sites before FDI, accounts for unobservable, time-invariant, ‘site type’ characteristics that may correlate with both FDI and conflict. 3 Finally, the inclusion of cell-period fixed effects should at least mitigate any site-specific, time-varying confounders. We utilize a 5-year period for these fixed effects, although we test this by using other period lengths in the robustness checks below.

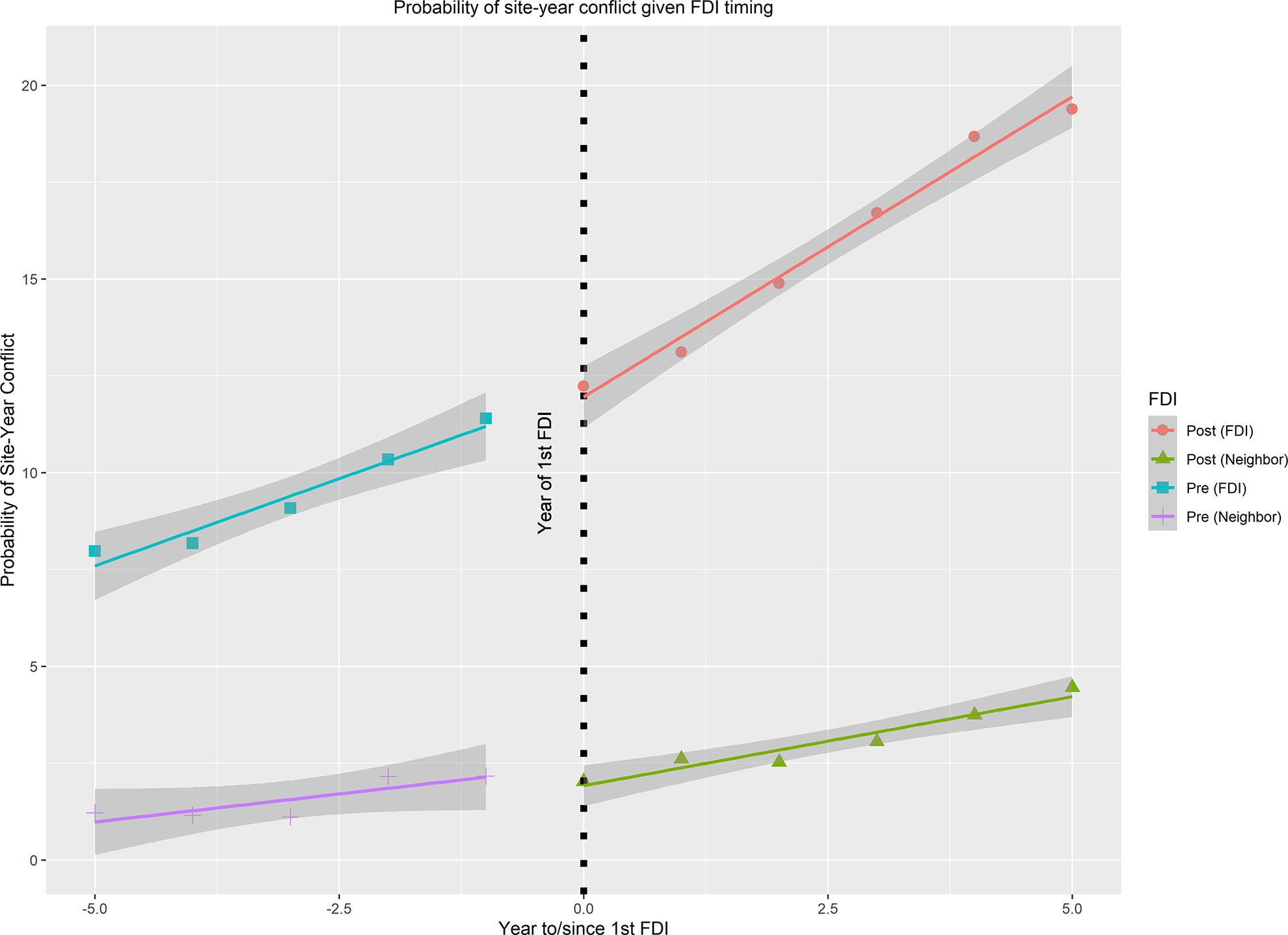

To evaluate the suitability of comparing the ‘active’ sites to their neighbours, the inclusion of neighbour sites as comparators necessitates that we make a parallel trends assumption about the likelihood of conflict. As seen in Figure 2, both FDI and neighbouring non-FDI sites see an upward trend in conflict relative to the timing of FDI opening, but the absolute probability of conflict in FDI sites is higher both pre-FDI and post-FDI. However, we do also observe that the upward trend becomes more pronounced only in the FDI sites following arrival of the FDI. Thus, it appears that our parallel pre-trends assumption is reasonable, but the Conflict and foreign direct investment sites

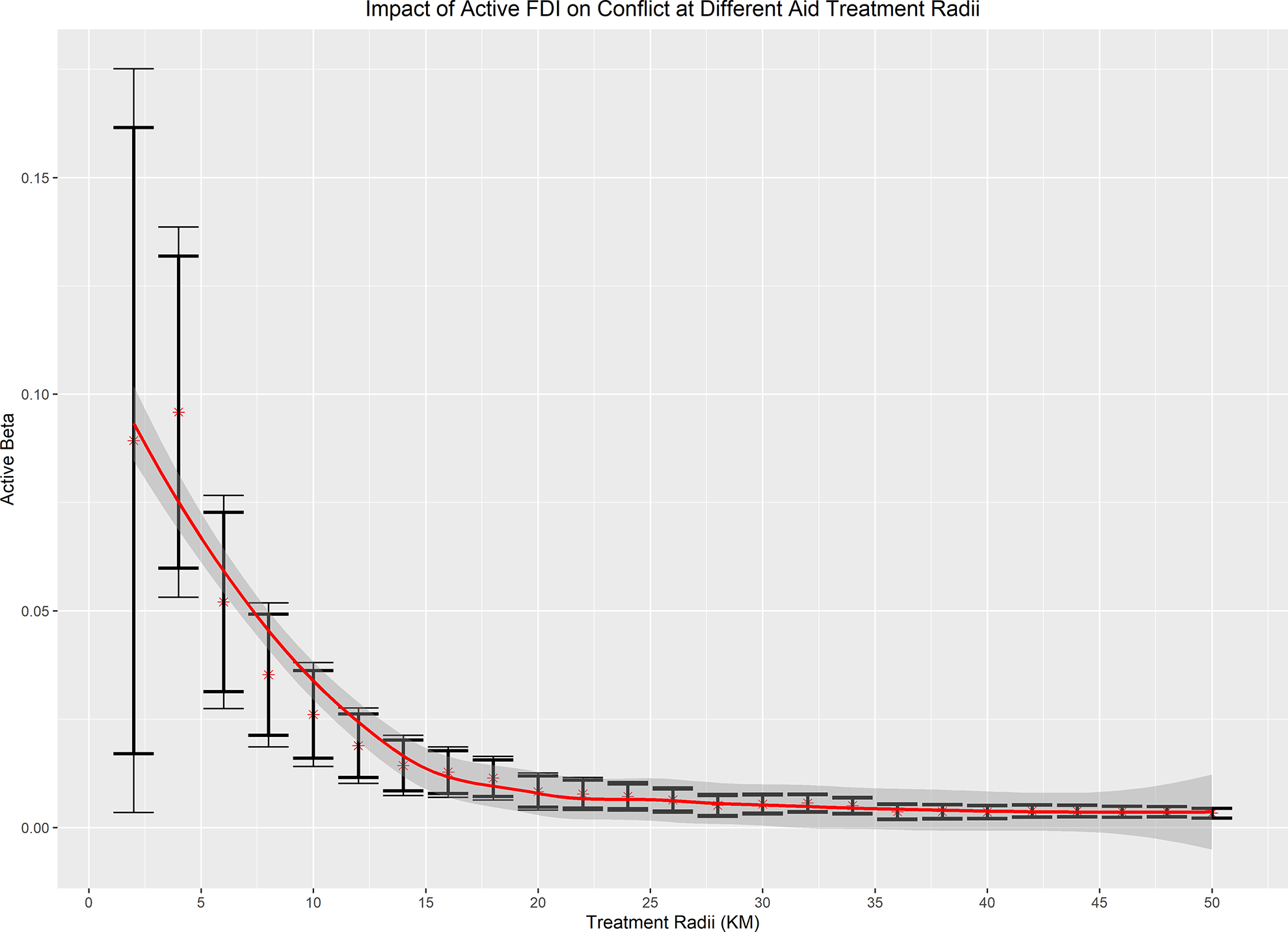

Our base analyses use all conflict events. However, in order to test the contention that the impact of FDI on conflict is heterogeneous with respect to the level of violence, we create a measure of grid cell-year conflict deaths to create indicators of conflict that include non-fatal, fatal, or ‘major’ conflict events, respectively. In assigning ‘major’ events we use the standard convention of a cut-off of 25 deaths. In calculating the reach of our FDI ‘treatment’ area, we face the same problem as other research that employs similar spatial techniques in that we assume the geographical ‘treatment’ reach of a given FDI project. Ultimately this is an empirical question that involves a trade-off between the spatial precision of the data, the diffusion range of the treatment, and unnecessary noise. We use a 10 km capture radius in our base analyses as our FDI data are precise to roughly this level.

Impact of FDI on Conflict at Different Treatment Radii

However, using any discrete spatial capture radius potentially introduces the MAUP of aggregating which may bias estimates (Fotheringham & Wong, 1991). The essence of the MAUP is that an arbitrary delimitation of spatial boundaries may include/exclude observations at the margin which results in biased estimates. One method of tackling this problem is using a range of differently sized areal-units (Zhang & Kukadia, 2005). Accordingly, in the robustness checks, we also run our baseline specification using all capture radii from 2 km to 50 km at 2 km intervals. Concerns about the MAUP problem diminish if the estimates do not vary widely based on the incremental boundary change. That said, we would expect larger, but less precise, effects at smaller capture distances and more precise, but smaller, effects at larger distances given the increased size of the ‘treated’ area which will capture both more conflicts and FDI projects.

Finally, it should be noted that our FDI data are temporally censored in 2003. As such, we do not know which grid-cells may have been ‘active’ before that date. While this is not likely to be a substantial number of grid cells given the fact that FDI to Africa has only accelerated since the mid-2000s, in the robustness checks below we drop the first six years of the data such that ‘inactive’ sites will have not had an FDI project for at least the preceding six years.

We use linear estimators for our main models for ease of interpretation and due to including site fixed effects in panel logit models can introduce the incidental parameter problem (Lancaster, 2000). Nevertheless, we also check our results to the use of non-linear estimators in the robustness checks. The reduced form specification of our baseline model is:

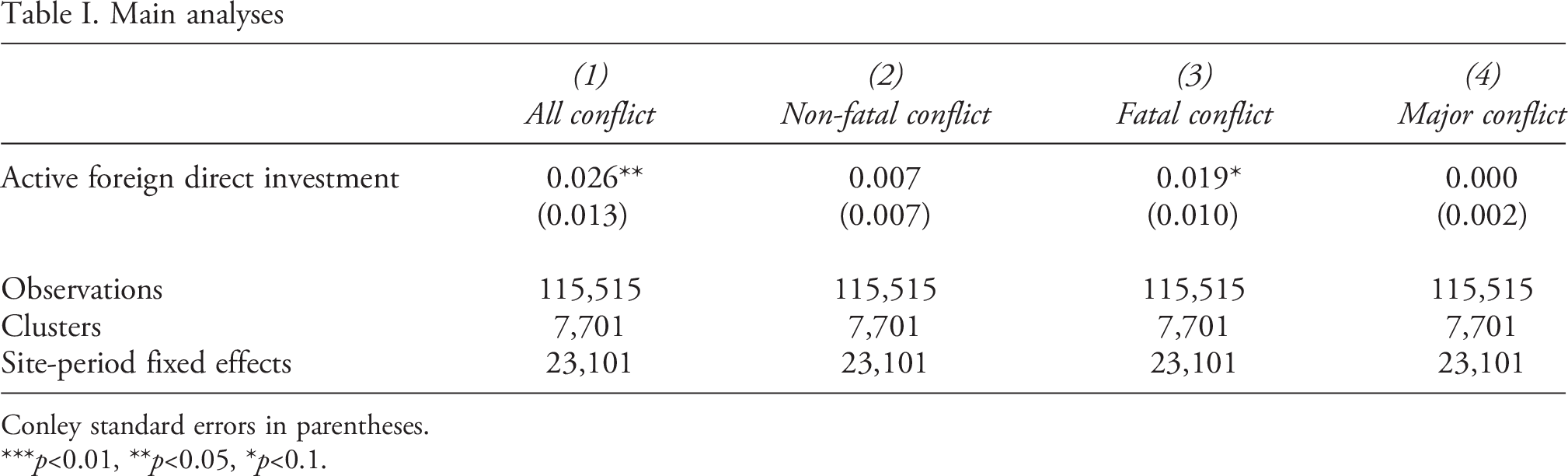

Main analyses

Conley standard errors in parentheses.

***p<0.01, **p<0.05, *p<0.1.

Results

Our main regression results are presented in Table I. In short, we find that active FDI sites increase proximate local conflict using all identification strategies. Furthermore, we find that, when considering all types of FDI, this positive impact only holds for fatal conflict events (Model 3). There is no effect on either non-fatal conflict alone (Model 2) or major conflict (civil war) (Model 4). These results support the view that all FDI generates conflict, potentially because local elites and communities contend with multinationals on diverging interests, but these conflicts do not escalate to war. Substantively, our base model (1) suggests that ceteris paribus, an FDI active grid cell-year increases the absolute probability of any conflict in that grid cell-year by 2.6%. This is an impact equivalent to an increase of 68% on the underlying probability rate of conflict of 3.8% at inactive and neighbouring FDI site-years. When examining different types of conflict, we see that the overall effect appears to be driven primarily via an increase in fatal conflict. 4

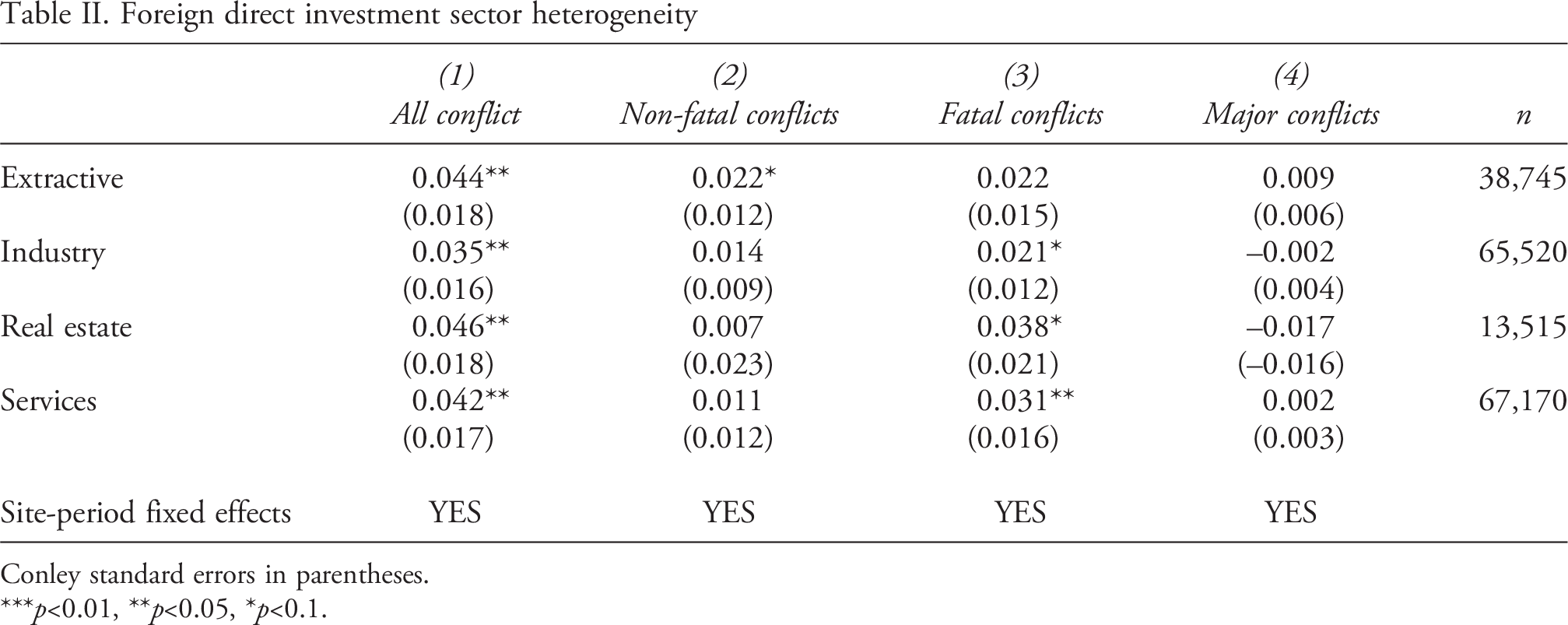

We next consider FDI sectoral heterogeneity. Results presented in Table II indeed suggest that some heterogeneity exists when we consider the impact of a given type of FDI on conflict. Fatal conflict appears to be a driver of the overall impact of FDI on conflict in all sectors. However, notably, only FDI in the extractive sector has a positive coefficient on major conflict, although this result is not significant at statistical levels. However, this may be due to the fact that the paucity of major conflicts means these models are underpowered. Substantively, while the point estimate is only a 0.9% increase, as the risk of major conflict in the inactive site-years and neighbours is only 0.16% this finding represented a risk that is 560% larger than the underlying baseline. In the other sectors, FDI does not appear to have any impact on the occurrence of major conflict. This former result is very much in line with Christensen’s (2019) finding, while the latter result is consistent with findings that extractive industries can promote major conflicts due to looting rebels and the absent incentives of governments (elites) to contain them (Fearon, 2005; Collier, Hoeffler & Rohner, 2009).

Foreign direct investment sector heterogeneity

Conley standard errors in parentheses.

***p<0.01, **p<0.05, *p<0.1.

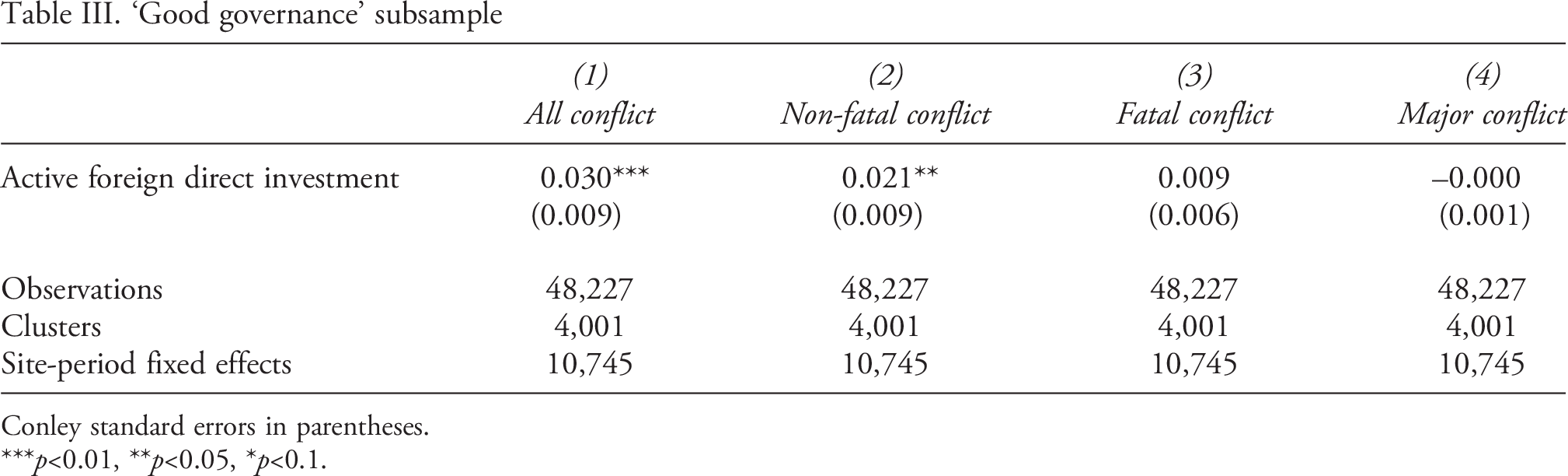

‘Good governance’ subsample

Conley standard errors in parentheses.

***p<0.01, **p<0.05, *p<0.1.

Extension and robustness checks

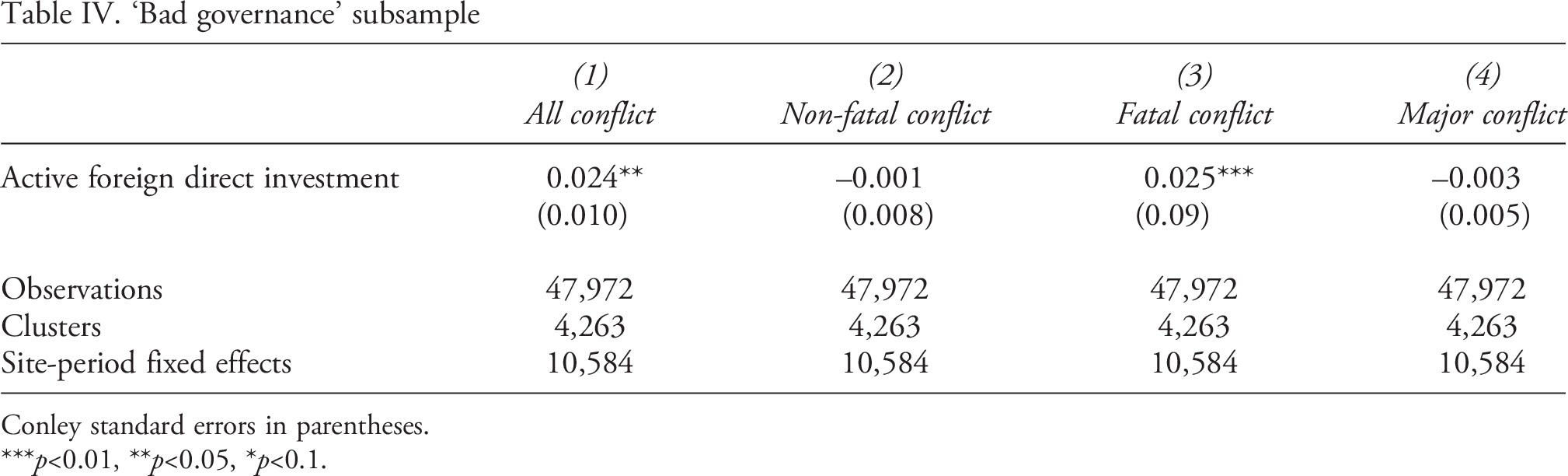

While we have explored sectoral heterogeneity above, it is possible that other types of heterogeneity also condition the impact of FDI on conflict. In particular, we would expect the quality of governance to impact the relationship between FDI and conflict. Accordingly, while we do not have access to governance measures at a subnational level, we can split our sample of grid-cells depending on if they are in a country with good governance. Using five of the six measures from the World Bank’s ‘World Governance Indicators,’ 5 we generate a composite value for each country-year and then split our sample based on the median value, coding a binary variable ‘1’ for any country-years in the upper half of the index. We run the models in Table I for both the ‘good governance’ and ‘bad governance’ subsamples in Tables III and IV, respectively.

‘Bad governance’ subsample

Conley standard errors in parentheses.

***p<0.01, **p<0.05, *p<0.1.

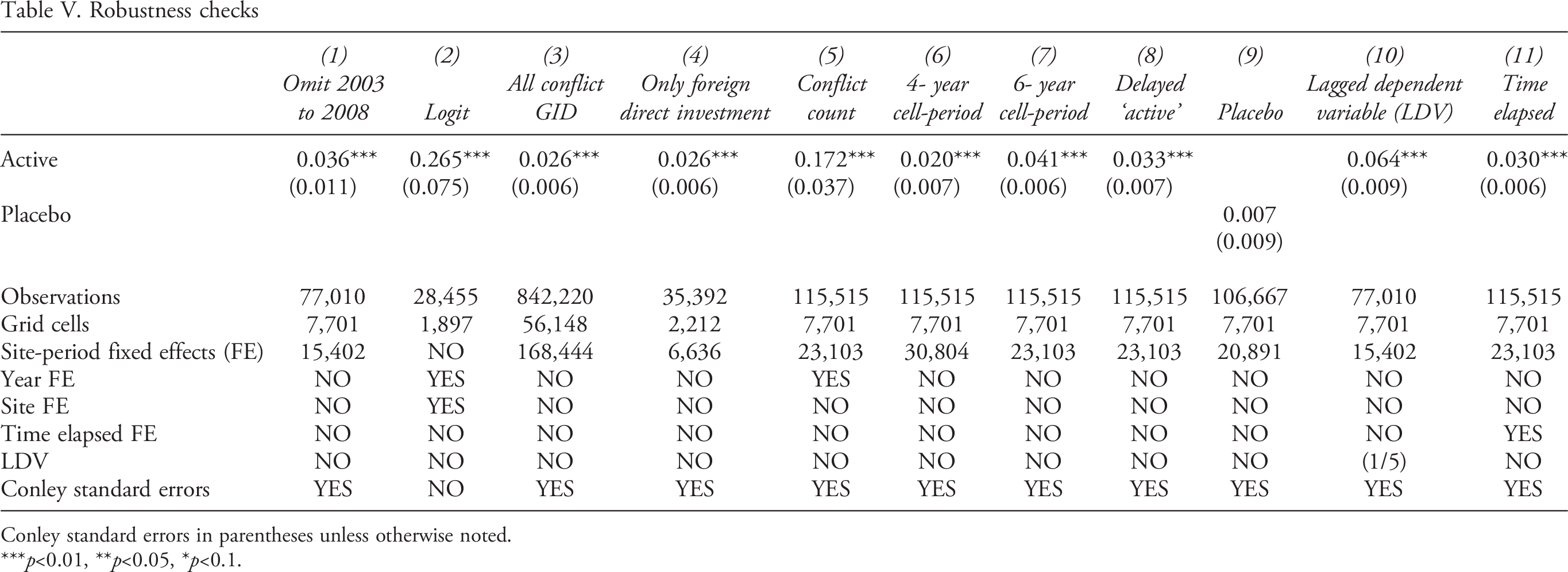

We consider several robustness checks. As discussed above, our FDI data are truncated in 2003. Accordingly, we omit the first six years to help ‘burn in’ inactive site years in Table V, Model 1. Also, in the main analyses we used linear estimators for ease of interpretation. However, to see if our results are robust to the use of non-linear estimators, we employ a logit model with year fixed effects in Table V, Model 2. Our substantive results are maintained using both these approaches. In Models 3 and 4 we include all sites which had conflict in at least one year and only the sites which hosted FDI in at least one year, respectively.

This is an event-study plot that displays the probability of conflict in the years before and after the arrival of the first FDI project.

Results are robust to these changes in sample. In Model 5 we use an alternative outcome measure, namely we use the natural log of the count of conflict events in a site-year rather than the binary indicator. 6 In Models 6 and 7 we adjust the time period of the site-period fixed effects from five-year periods to four-year and six-year periods, respectively. Next, the FDI data we use are based on FDI project announcements. While we think it is reasonable that (local) conflict can erupt because of these announcements in a bid to halt the FDI, it is also possible that the conflict only erupts when the project is underway/completed. As such, in Model 8 we only turn a site ‘active’ 3 years after the project announcement. The results are robust to these changes. Like Christensen (2019), we conduct a placebo test to investigate if FDI is selecting into areas of increasing conflict in Model 9. Indeed, a recent study using the same sub-national FDI data as ours, finds precisely this latter result (Jamison 2019). As in that approach, we create a placebo that turns ‘active’ on for a period of five years prior to active FDI. The coefficient on the placebo is statistically insignificant, suggesting a lack of evidence for any selection effect. Finally, we control for past conflict at the site in two ways. First, in Model 10, we include a distributed lag of the dependent variable for the previous five years. Second, in Model 11, we include a count variable for the years since the first conflict at a site, as conflict relapse is a duration-specific risk. In both instances, the main substantive result is maintained.

Robustness checks

Conley standard errors in parentheses unless otherwise noted.

***p<0.01, **p<0.05, *p<0.1.

Event-study plot of conflict pre-post FDI arrival at grid cell and neighbours

The results largely conform with what we would expect from a spatial process, with noisy but generally larger substantive effects at lower capture distances, and more precise but smaller effects at larger distances. The largest substantive effect of 0.025 is at a capture distance of 4 km. As the distance increases, the point estimate gets progressively smaller, as one would expect from attenuation bias whereby ‘untreated’ units are being considered as ‘treated.’ This issue, combined with the absence of abrupt changes in the point estimates, suggests that our results are not sensitive to a particularly sized areal unit and that the MAUP is not likely to be a source of major bias in our results.

Conclusions

There is a durable debate across many fields about the effect of FDI on conflict in the developing world. Several recent studies address the issue of FDI and conflict, using disaggregated data. Many of these studies assess the effects of FDI in mining and extractive activity, which we argue is unnecessarily restrictive given the arguments linking FDI to conflict. Using spatial–temporal identification approaches and FDI projects aggregated across all sectors, our results suggest a strong correlation between the arrival of any local FDI project and subsequent local small-scale conflict but only FDI projects in the extractive sector show any effect on the risk of civil war. All FDI types, however, show increased conflict activity, including small-scale fatal conflict, showing that FDI generates violent contention. We suggest that these conflicts stop short of large-scale armed conflicts because local elites have a strong interest to prevent their escalation. These results are robust to several different estimation techniques, spatial considerations, and fixed-effects approaches. There are, however, two caveats to these findings. First, the evidence is that this FDI effect comes primarily via an increase in small-scare fatal conflicts, consistent with country-level studies showing that FDI increases societal conflict due to protests, riots, strikes, etc. Our finding for all FDI, thus, supports the theoretical mechanism for increased protest offered by Christensen (2019), who examines only FDI projects relating to mining company–community conflict due to bargaining failure under imperfect information. Yet, our results also speak to the debate on FDI and serious armed violence, and they suggest, like others, that only extractive FDI is susceptible to generating battle deaths that meet the threshold for civil war (Mihalache-O’Keef, 2018). These results are also generally in line with findings based at the country level showing no relationship between the level of FDI and the onset of civil war (de Soysa, 2020).

Yet, upon further interrogation of our data disaggregated by FDI sector, we find additional nuance, suggesting strongly that the effects of FDI on conflict are not as uniform as extant theory based on weak states predicts. It seems that unrest can occur due to FDI related to industrial, real-estate or service-sector projects, potentially due to the displacement of well-placed domestic agents capable of fomenting anti-state/FDI dissent but these same elites have very strong incentives to resolve the disputes short of armed war. Nevertheless, only extractive FDI appears to have a larger relative impact on both non-fatal conflict and major conflict defined in terms of 25 battle deaths and above. Elites that dissent thus have higher opportunity costs for enlarging conflicts to reach civil war levels. Likewise, a preliminary extension suggests that FDI is more likely to lead to violent protests in more poorly governed countries in contrast to inciting more non-violent protest in better governed locales. The results taken together in our highly disaggregated, place-specific analysis of African conflict, thus, do not support the wider argument that FDI increases civil war risk by ‘securitization’ of states, or by weakening state strength due to dependence on FDI, or arguments based on rent capture alone.

While our heterogeneous results are suggestive of some types of causal mechanisms being more likely than others, our research design does not allow us to directly detect or evaluate exact mechanisms that may cause small conflicts to escalate to civil war levels. Future qualitative, or mixed-methods investigation, that can more directly explain why different types of FDI appear to have differential impacts on local conflict would be a useful extension of our work. We suggest that such focus pay particular attention to how powerful domestic actors are either displaced or co-opted by specific forms of FDI, and how such elite interests navigate the negotiating stage between governments and FDI projects that either lead to the intensification of, or the cauterization of, serious conflict post hoc.

Footnotes

Replication data

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank the European Union’s Horizon 2020 research and innovation programme under grant agreement number 693609 (GLOBUS) for generous funding support for this project.