Abstract

Marketing to investors—especially when seeking funding for startups—is unique, with investors facing extreme uncertainty. This study uses foundational work in marketing, economics, management, finance, and psychology, as well as theories-in-use development with angel and venture capital investors, to build a business-to-investor marketing theory. The theory proposes that investors rely on marketing signals from startups, whether they are costly (financial, social, human, and intellectual resource endowments) or costless (verbal passion and concreteness). Results of a large quantitative field study of 5,334 written proposals from startups show that costly and costless signals have interactive effects on investor acceptance. The natural entrepreneurial tendency to compensate for a lack of costly signals with the use of passionate language backfires, reducing investor acceptance. Only when costly signals are communicated does a greater use of passion increase investor acceptance. Further, written proposals should be moderately concrete when they lack costly signals and should be formulated abstractly when plenty of costly signals can be offered. These contingencies provide insights into costly–costless signal interdependence in business-to-investor marketing and suggest how startups can optimize their written proposals for investor acceptance.

Keywords

How marketing assets create financial value is well known, but how do nascent firms use marketing to acquire financial resources in the first place? This is a significant marketing question; despite the fact that new ventures are key engines of value creation (Schumpeter [1911] 1934), 99% of them die prematurely (Homburg et al. 2014), with the lack of financial resources being a primary reason for said failure (Shane 2003). Therefore, new ventures, from inception, actively engage in a unique form of marketing activity to secure financial resources, which we label business-to-investor (B2I) marketing. Little is known about how to effectively implement such marketing, despite its economic and societal importance.

Therefore, the purpose of this article is to develop a new theory for B2I marketing in the context of new venture signaling theory (Colombo 2021) and investor “gut feeling” (Huang 2018). Relying on a combination of foundational work in economics, finance, management, communications, and psychology, as well as inductive theories-in-use development (Zeithaml et al. 2020), we propose a new theory for B2I marketing. We then test this theory with a large quantitative dataset consisting of new ventures’ marketing attempts to gain acceptance by investors.

Understanding how to market to investors is critical for a number of reasons. Foremost, startups are the engine of value creation, a core construct in marketing, yet we know very little about how new ventures can use marketing to attract early-stage investors and persuade them to provide financial resources. This focus on investors is key because without adequate capitalization, a new venture's odds of survival are extremely low (Smith, Smith, and Bliss 2011). Research insights that improve the marketing of new ventures therefore promise to help the economy plus demonstrate marketing's value more generally.

Further, the unique circumstances of marketing to early-stage investors necessitates bespoke theory. Investing in new ventures is unlike any other consumption or investment decision because it is characterized by extreme uncertainty, even compared with the general risks of most other investments (Ueda 2004). As heretofore argued and demonstrated, early-stage investors are not only a unique stakeholder group; they also undergo an investment decision-making process that is distinct from decision-making in B2B and B2C contexts (Huang 2018; Huang and Knight 2017; Huang and Pearce 2015). Finally, although research in finance and management (Cook, Kieschnick, and Van Ness 2006; Martens, Jennings, and Jennings 2007) touches on some marketing activities to secure financial resources, persuasive value exchange between market participants is quintessentially a marketing topic. Accordingly, and alongside calls for boundary-spanning and strategy-relevant marketing research (Kohli and Haenlein 2021; Moorman et al. 2019; Palmatier 2018), there is a need for marketing theory to explain exchanges with critically important stakeholders such as early-stage investors.

The contribution of this research study is threefold. First, it complements the B2C and B2B marketing domains with a novel approach regarding B2I marketing. While some may think marketing is either B2C or B2B, investors are a crucial marketing audience as well. New venture investors are a unique stakeholder group to market to, just as the new venture marketplace is unique due to the extreme uncertainties startups and investors face (DeKinder and Kohli 2008; Ueda 2004). We therefore propose a new B2I theory, building on multidisciplinary foundations. We suggest that the B2I marketing process includes both substantive costly signals to systematically influence decision-making as predicted by normative economics (Colombo 2021) as well as costless, heuristic signals that, following behavioral science, interact with systematic processing—even when the decision-makers (investors) are highly rational (Drover, Wood, and Corbett 2018).

Second, we respond to calls for research on the role of actual, word-level communication in marketing (Berger et al. 2020). Theories-in-use interviews with 13 angel and venture capital (VC) investors suggest two primary costless signals at the granular level of word use in startups’ communication: passion (i.e., the degree to which entrepreneurs describe their venture using intense, positive, and high-arousal emotions, such as enthusiasm; Cardon et al. 2009) and concreteness (i.e., the degree to which entrepreneurs describe their ventures in a perceptible, precise, specific, or clear manner; Brysbaert, Warriner, and Kuperman 2014). Adding to the first insights into the use of these costless signals (Huang et al. 2021; Parhankangas and Renko 2017), we use a proprietary dataset of written proposals to investors from the Creative Destruction Lab (CDL) to assess the preconceived relations between these signals and investors’ acceptance of startups.

Third, integrating signaling theory with research on investor decision-making (DeKinder and Kohli 2008; Homburg et al. 2014; Huang 2018), we investigate the interplay between systematic costly signals and heuristic costless signals (passion and concreteness). Using a response surface approach and a polynomial regression (Kim et al. 2022), we find that the effects of concreteness and passion in startups’ written proposals on investors’ acceptance are indeed contingent on the level of costly signals a startup possesses: When costly signals are high, excessive concreteness backfires, but passion has a positive linear effect. Conversely, when costly signals are low, concreteness improves the probability of investor acceptance (but with diminishing returns that become negative, i.e., an inverted U-shaped effect), whereas passion lowers it. Thus, we offer both startups and investors a fine-grained perspective on how to strike a balance between costly and costless signals when engaging in (or processing) B2I marketing.

The remainder of the article proceeds as follows: First, we build a new theory for B2I marketing. To complement our deductive theorizing, we report an inductive theories-in-use study, conducted with angel and VC investors. Second, we develop specific hypotheses on costly and costless signals, which we then test in a large quantitative field study of 5,334 written startup proposals and their investor evaluations. Finally, we derive the implications of our work.

Theoretical Background

The principle of marketing orientation (Kohli and Jaworski 1990) suggests that strategy formulation is rooted in an in-depth understanding of the market and its key stakeholders: in our case, crucially, early-stage investors. Early-stage investors and the new venture investment market are unique (distinct from B2C, B2B, and even later-stage equity investments), for the following three main reasons.

First, new ventures are burdened with a heavy liability of newness (DeKinder and Kohli 2008) and require investors to invest based on extremely uncertain, incomplete, and asymmetrically distributed information (Colombo 2021). Therefore, early-stage investors face the nonquantifiable risk of adverse selection when contemplating investment. This is unlike B2B or B2C contexts, where marketers and their target audiences (counterparty firms or end consumers) have at least some understanding of the exchange risks involved, and thus are able to mitigate risks to some degree during decision-making. In contrast, early-stage investors “face decisions with such extreme uncertainty that the risk qualifies as unknowable” (Huang and Pearce 2015, p. 635).

Second, new ventures, by default, lack marketing assets commonly present in B2C and B2B markets. They commonly lack a strong brand or established distribution network, due to their brevity (or complete lack) of operating history and limited (or completely absent) market success. They typically have not had the opportunity or ability to invest in advertising, sales, or customer relationship management, or to build innovative product portfolios (there may only be prototypes or conceptual plans). Many new ventures may not have any customers at all (Blank 2013). This reality is in stark contrast with established firms, which can (and do) rely on brand equity (Rego, Billett, and Morgan 2009), advertising outlays (Cheong, Hoffmann, and Zurbruegg 2021), customer satisfaction and orientation (Moon, Tuli, and Mukherjee 2023; Srivastava, Kashmiri, and Mahajan 2022), and innovative product portfolios (Cillo, Griffith, and Rubera 2018; Warren and Sorescu 2017) to achieve their market goals—thereby, in turn, also reducing B2B or B2C counterparty risk. Clearly, most early-stage investors lack the advantage of relying on marketing assets and capabilities to guide their decisions to engage with or pass on new ventures, making the B2I domain distinct.

Third, despite these extremely high uncertainties, investors still do invest in early-stage ventures. Research in management and finance shows that (1) the decision-making strategy of early-stage investors is not so much to mitigate extreme uncertainty, but to embrace it, because the investment objective is to achieve asymptotic returns (“home runs”) rather than average high returns (which routine risk mitigation is tasked with achieving; Sahlman 1990), and (2) early-stage investors use what they describe as “gut feeling” to actually make the investment decision, which, given the unknowability of home-run probabilities, a rational investor would avoid (Huang and Pearce 2015).

Thus, the conceptualization of marketing in the B2I domain needs to accommodate a set of considerations that are distinct from those of established firms and the world of B2B and B2C marketing.

Classic Costly Signaling in B2I Marketing

In reevaluating marketing for the B2I context, we first rely on the foundations of classic signaling theory. Next, we review newer developments inspired by research in psychology (applied to management), which, though fragmented, serve as a strong critique of classic signaling theory. Finally, we take on the challenge of integrating these fragmentary developments into a more comprehensive model.

Classic signaling theory (Spence 1973, 2002) is a form of rational choice theory (Gilboa 2012), which aims to explain how utility maximization can and should happen for rational actors when reliable information is very hard to come by. Thus, the theory is designed for environments with high uncertainty, where parties involved in an exchange are asymmetrically endowed with information and have incentives to cheat (Connelly et al. 2011). Under such circumstances, recipients are advised to rely on “costly” signals, that is, signals that incur real and high costs for signal senders. The classic example (Spence 1973) is a job market interview, wherein the cost of high-quality education is prohibitively expensive for some candidates but is believed by many recipients to be critical for selecting employees with high job performance outcomes (a decision mired in high risk otherwise). Therefore, candidates who can legitimately showcase their “costly” education credentials are identified as high quality and selected. This sole focus on a costly resource endowment (education, in this example) rather than the entirety of available information thus enables receivers to efficiently resolve both contextual uncertainty and counterparty information asymmetry.

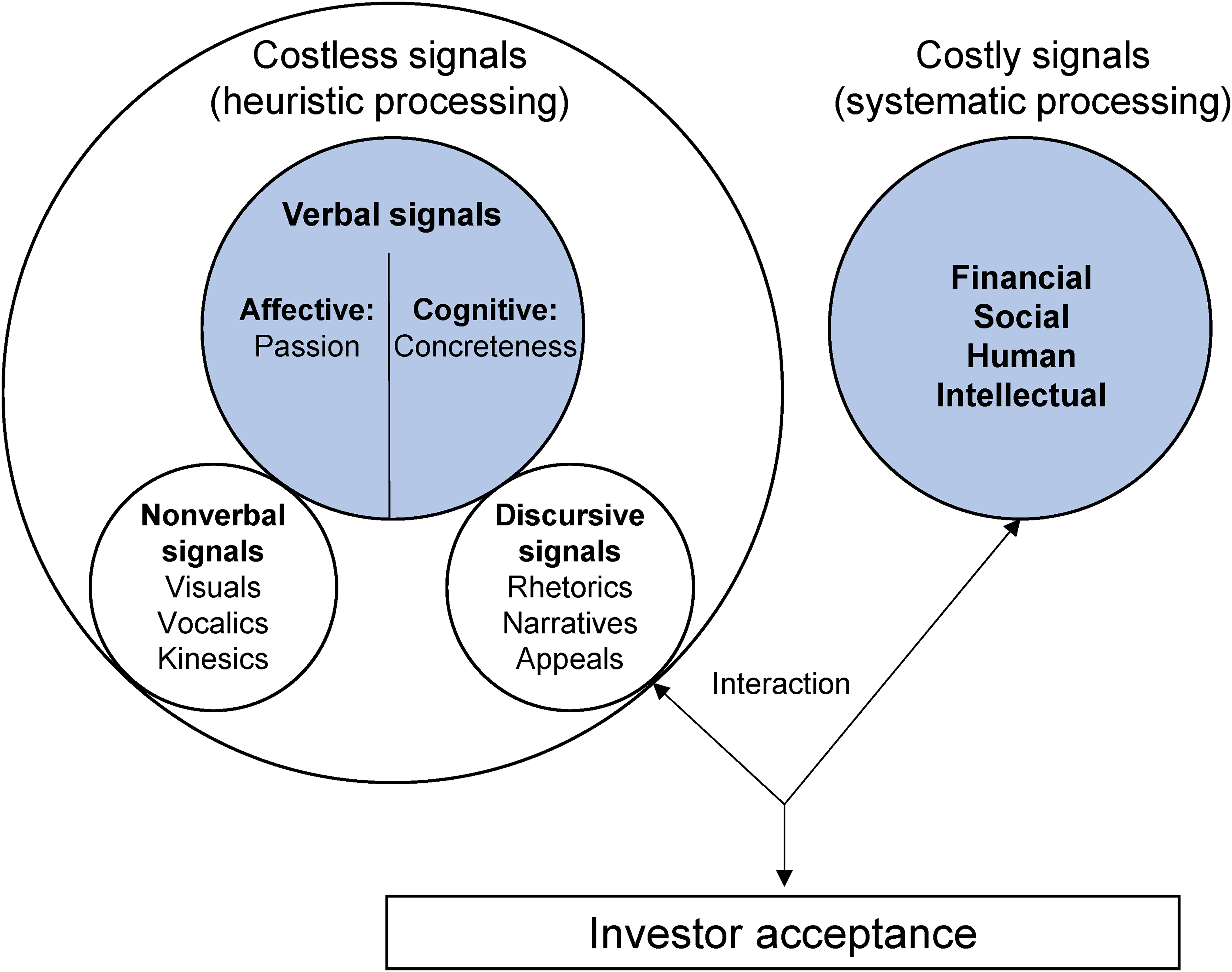

Marketing, management, and finance research have employed the concept of costly signaling in B2I contexts with great success (for a summary of costly signaling, see Web Appendix A). This considerable body of research has operationalized costly signals as entrepreneurial resource endowments and categorized them into four key groups: financial, social, human, and intellectual signals (Clough et al. 2019; see also our adaptation of this fourfold typology in Figure 1, which shows our theoretical model). For example, the financial capital already invested in the venture has a positive impact on subsequent VC funding because it is costly to acquire, and low-quality ventures would not have it; therefore, it reduces information asymmetry (Ko and McKelvie 2018). Similarly, social capital, in the form of the quantity (Baum and Silverman 2004) and quality (Carter and Manaster 1990) of relevant business or institutional relationships, results in higher resource acquisition for the new ventures showcasing it. Human capital such as prior training, knowledge, and experience of the founders also has a positive impact (Delmar and Shane 2004). Finally, intellectual capital (e.g., a patent) also reduces information asymmetry (Audretsch, Bönte, and Mahagaonkar 2012). Marketing research has shown that the four categories of costly signals—financial (Luo 2008), social (Saboo, Kumar, and Anand 2017), human (Homburg et al. 2014), and intellectual capital (Cao et al. 2023) signals—have a positive impact on investor decision-making (for a summary, see Panel A of Web Appendix A).

An Integrative Model of B2I Marketing.

Costless Signaling, Multiple Signals, Receiver-Focus, and Heuristic Processing

Costly signaling's success notwithstanding, it has become increasingly clear that it is still incomplete. Advances in psychology, most importantly in the area of heuristics and biases, highlight that rational information processing has severe limits (Gilovich, Griffin, and Kahneman 2002). Highly rational venture capitalists process information they are not supposed to (Franke et al. 2006). Costly signaling theory has evolved in three ways, with relevance for our B2I marketing theory: (1) through the study of a new type of signals: costless signaling, (2) by allowing for the synchronous impact of multiple signals, and (3) by emphasizing receivers in the signaler–receiver dyad, who often engage in heuristic cognitive processing.

Costless signaling

First, new evidence suggests that investors process costless signals, defined as any signals that lack the assumption of costliness (Colombo 2021). A core tenet of classic signaling is that the value of a signal under information asymmetry lies in its cost to the sender (incurred in outlays of money, time, and/or energy). In contrast, costless signals are “cheap talk” because, by definition, they lack the hard costs giving them their informational value (Farrell and Rabin 1996). They constitute the stylistic form (verbal and nonverbal) of startups’ B2I marketing (as opposed to its costly content). Yet, investors rely on them.

While the analysis of stylistic form is new to signaling theory, it is not new to marketing and communications research. To structure this vast literature and provide a new frame for how investors rely on costless signals, we adapt a signal typology widely used in communications and management theory (Bonaccio et al. 2016; Littlejohn, Foss, and Oetzel 2017; Powers 1995; see Figure 1). The typology organizes communicative signals into three groups, ranging from the smallest possible units to the largest: (1) nonverbal signals, which are the smallest units and contain “relatively independent physical signs” (Powers 1995, p. 194) such as visual images, sounds (“vocalics”), and human bodily signals (“kinesics,” such as posture or facial expressions; Bonaccio et al. 2016); (2) verbal signals, which are formal linguistic codes, such as patterns in word use (semantics); and (3) discursive signals, which are the “larger segments” of signaling structure (Littlejohn, Foss, and Oetzel 2017, p. 105), including rhetorical tropes, narratives, and argumentative appeals (Powers 1995, p. 198). Marketing research has long studied the consumer (albeit not the investor) effects of each of these costless signal types: verbal signals (Berger and Milkman 2012), nonverbal signals (Sevilla and Meyer 2020), and discursive signals (Van Laer et al. 2019).

Even more relevant for our B2I domain, empirical studies (conducted primarily in management and finance) have begun to investigate the impact of these various types of costless signals on early-stage investors’ decision-making (Kalvapalle, Phillips, and Cornelissen 2024). Recent work in marketing shows that certain vocal pitch tones result in higher crowdfunding likelihood (Wang et al. 2021), while emotional (vs. informational) appeals have mixed effects on the number of crowdfunding supporters (Xiang et al. 2019; for a review of B2I costless signaling, see Web Appendix B).

Multiple signals

Second, in parallel to the introduction of costless signals, researchers have realized that classic startup signaling literature often limits itself to isolated, singular signals—yet in reality, investors consider many signals at once (Vanacker et al. 2020). While several studies empirically estimate a range of signaling predictors, the theoretical focus is commonly on a single costly signal type. Importantly, few studies consider the interaction of costly and costless signals (e.g., Anglin et al. [2018] report that the use of a psychological capital rhetoric boosts the positive impact of human costly signals).

Receiver-focus and heuristic processing

Third, classic signaling theory focuses on the sender; it does not empirically demonstrate how signals are received. It simply assumes that investors promptly attend to costly signals and process them because doing so would reduce information asymmetry (Bergh et al. 2014). However, new evidence suggests that investors encode signals from startups only selectively; indeed, some signals do not have functional utility to receivers because they are exogenous to the receivers’ goals (Drover, Wood, and Corbett 2018). The theoretical implication for B2I theory of this refocusing on the recipients is that the normative economics-driven signaling logic needs to be complemented by theorizing how signals are processed. Relatedly, advances in signaling theory supplement utility maximization and rational choice with heuristic processing (Cumming et al. 2023). This latter extension presents a puzzle for classic signaling theory since it involves two, seemingly irreconcilable claims: Investors act rationally out of their own interest to reduce information asymmetry (costly signaling), yet they may process irrelevant information heuristically (costless signaling).

B2I Marketing Theory: Hypothesis Development

To reconcile costly and costless signaling in a comprehensive theoretical model, we rely on the work of Huang and colleagues on gut feeling (Huang 2018; Huang and Knight 2017; Huang and Pearce 2015), which suggests that early-stage investors rely on both systematic and heuristic processing simultaneously. This research shows that early-stage investing is so ridden with chronic and extreme uncertainty that even costly signals cannot effectively remedy information asymmetries between startups and investors (Huang and Knight 2017). Further, early-stage investors’ goals differ from those of other investors (such as ones in public markets) in that risk management is subordinated to the quest for home runs—investments with outsized returns of the “power law” type, which are expected to compensate for other losses (Huang and Pearce 2015). Gut feeling theory also highlights that, as a result of this contextual uniqueness (characterized by extreme uncertainty, but also outsized possible returns), these investors process information differently (Diebold, Doherty, and Herring 2010; Foss and Klein 2012). Finally, the reliance on gut feeling provides much-needed confidence in investment decisions that otherwise simply would not be made (Huang 2018). These observations do not mean that early-stage investors only rely on their subjective intuition; instead, these investors take elements of costly signals (whatever their worth is in the given situation) and combine them with what we call costless signals to form a holistic assessment.

To illustrate our theory at work (and subsequently test it with a large dataset), we have to limit its scope at this point. To this end, we focus on verbal costless signals, for three main reasons. First, as our literature review shows, while discursive and nonverbal signals have been studied extensively in costless signaling, verbal signals have received less attention (Web Appendix B). Second, focusing on verbal signals is especially relevant for marketing scholarship, as calls for word-level analysis of marketing phenomena strongly argue (Berger et al. 2020). Third, we expect verbal signals to be easily manipulable yet highly consequential in B2I marketing practice, as our empirical findings will corroborate.

While providing useful insights, gut feeling theory leaves at least two key research questions unanswered. First, what verbal costless signals do investors consider (RQ1)? Gut feeling theory generally points to costless signals as important complements to costly signals. It also suggests that gut feeling likely carries an affect–cognition duality. However, it does not specify costless signals’ substantive content, much less at the granularity level of verbal signals (Huang 2018). Even the typology we relied on for costless signals (see Figure 1) identifies only broad buckets for these signals, referring to their modality of appearance, not their substantive content. Therefore, specific theory development is needed in the B2I context to solve this puzzle.

Second, how do investors use verbal costless signals (in combination with costly signals) when deciding whether to invest (RQ2)? Again, while the foundations of gut feeling theory are helpful in suggesting that investors do combine costly and costless signals in a holistic manner, details are lacking as to how exactly this “holistic” combination occurs (Huang and Pearce 2015). Is the joint reliance on costly and costless signals merely additive, or instead multiplicative (interactive)? While gut feeling theory hints at the possibility that costly and costless signals interact (in the sense that costless signals may be compensating for the lack of hard evidence costly signals could provide; Huang 2018), no specific hypotheses are developed regarding how investors use costly and costless signals in interaction.

To answer the first broad research question, we rely on theories-in-use development (Zeithaml et al. 2020) with angel and VC investors (our methodology is described in Web Appendix C). To answer the second research question, we use insights from this exploratory study to develop specific hypotheses, which we subsequently test in a large-scale field study.

RQ1: What Verbal Costless Signals Do Investors Consider?

The VC and angel investors we interviewed unequivocally expressed their reliance on verbal costless signals in addition to costly signals. Investors indicated that they pay attention to such verbal input, partly due to a natural human tendency, but, more importantly, because such input is particularly relevant for early-stage investing. As one noted, referring to costless signals: “I actually don’t think they’re ‘costless.’ But let's call them intangibles” (Interview 3). This self-admitted reliance on costless signals does not diminish the importance of costly ones. Rather, these investors suggested that their holistic assessment of startups includes both: “I very much do think stylistics matter. […] It's viewed as one, you know, big factor, for sure. Not the only factor. So, I don’t ever see, just look at, you know, obviously, at stylistics. But it's huge” (Interview 8).

Investors suggested the most important verbal signals they relied on were passion and concreteness: “I want your passion, and I want to hear competency […] And the competency is conveyed with, you know, the classic, […] some very concrete examples” (Interview 3). The first costless signal, passion, was both anticipated and keenly attended to by investors—the consensus being that this signal is a necessary (if not sufficient) condition for evaluation: “And so passion I find really sells me as an investor” (Interview 9). These investors highlighted that they indeed look for verbal signals of passion, which can be clearly conveyed through language: “And I want to see… In their writing, I want to see someone talk about something they’re excited about” (Interview 3).

In the entrepreneurship literature, passion is defined as entrepreneurs’ intense, positive, and high-arousal emotions (such as enthusiasm) regarding their ventures (Baum and Locke 2004; Cardon et al. 2009; Chen, Yao, and Kotha 2009; Robinson et al. 2004). Passion, therefore, is more than mere positivity; it is an intensely aroused positivity that indicates a high level of activation, energy, or enthusiasm (Russell 2003).

Investors noted, however, that entrepreneurial passion is not boundlessly favorable with respect to investment decisions; in fact, at extremely high levels, it may backfire. A complete lack of passion was interpreted as low entrepreneurial motivation and a violation of the tacit expectation that entrepreneurs are always in “selling mode.” At the same time, excessive passion was either viewed as an indication that the content of communication was untrue (“There will be natural skepticism, some skepticism, as there always should be”; Interview 3) or grounds for an unfavorable entrepreneurial character assessment (“It's kind of like, you know, when you watch a movie. For you to really like a character, they can’t be perfect. That was the problem with Superman. There has to be some flaw for you to really like that character”; Interview 2).

The second core verbal costless signal investors pointed to was concreteness: “I like the concreteness a lot. I think that, that gets me excited!” (Interview 13). Concreteness in linguistic research is defined as “the degree to which the concept denoted by a word refers to a perceptible entity”; communicating with greater concreteness means describing something in a perceptible, precise, specific, or clear manner (Brysbaert, Warriner, and Kuperman 2014, p. 904).

Investors in our interviews suggested that they rely on the verbal costless signal of concreteness because it increases believability amid the extreme uncertainty of early-stage investing: “Are you talking in concrete terms or abstract terms?” […] If something has been done, you will tell me concrete things, right? You will tell me a dollar amount, right? We’ve got “$10,000 in revenue” versus we’ve got “lots of revenue.” If you say “we’ve got lots,” I don’t believe you, right? (Interview 7)

Given the strong and somewhat counterintuitive reliance on “costless” signals (both passion and concreteness) by rational financial professionals, we further probed the underlying reasoning. Investors claimed that they rely on passion and concreteness because they are able to draw character inferences about the entrepreneurs from these signals: “When someone can explain that same problem that they’re just passionate about solving, in a very straightforward, clear manner that someone without that subject matter expertise could at least partially understand. That to me is the sign of intelligence” (Interview 3). Passion, in particular, is a sign of entrepreneurial drive, which investors consider an essential quality in an environment where most newly established businesses fail. Concreteness, in turn, was also read as a signal of character—but in this case, a marker of competence and trustworthiness. Since all information in early-stage investing is considered suspect and is treated with skepticism by investors (“I think a lot of the companies are actually frauds,” as one of them posited; Interview 6), concrete, tangible communications serve as an assurance that the sender (the entrepreneur) is both capable and trustworthy.

These character heuristics, however, are not ends unto themselves; the main reason investors draw such inferences is to make another inference regarding the underlying startup's quality. Indeed, these investors weigh character attributes and skills while evaluating how successful the venture will be in the future: “Because how a person utilizes language to me indicates how well they are able to grasp an idea and share it with others. Which is an important part of scaling a company” (Interview 4). The importance of this entrepreneur-to-venture transfer is underlined by these investors’ beliefs about how verbal signals such as passion and concreteness are indicative of venture quality: Because you also have to show that passion, enthusiasm to your customers, right, not just to investors, eventually. […] There's, I think, there's got to be correlation with the quality of their business. Because if you can’t tell me what you do in a very short period of time, like, how are you going to do that with a customer? (Interview 8)

RQ2: How Do Investors Use Verbal Costless Signals Interactively with Costly Signals?

In addressing our second research question (and setting up formal hypotheses to test it), we note that the empirical literature in entrepreneurship, management, and finance provides little guidance. This is because rather than investigating how investors combine these costless and costly signals for investment decisions, most prior literature considers them a dichotomy (Martens, Jennings, and Jennings 2007). Accordingly, some research sets costly signals up against costless signals directly, to see which one “wins” in influencing investors (Chen, Yao, and Kotha 2009); other research focuses on either exclusively costly (Xiong and Bharadwaj 2011) or costless (Parhankangas and Renko 2017) signals.

In reality, however, this is not an either-or choice. All startups, those with relatively few (or many) costly signals, still have to communicate their venture to investors. In addition, recent marketing research highlights that dualities (in our case, costly and costless signals) may exert both “combining” (synergistic) and “balancing” (antagonistic) effects on outcomes; moreover, these effects may co-occur simultaneously, conditional on the level of either of the signals (Kim et al. 2022; a “multidimensional” approach to theorizing the effects of dualities).

The interplay between passion and costly signaling

Relying on the broad foundations of gut feeling theory, which suggest that costless and costly signaling are used conjointly for investor decisions (Huang 2018), we propose that the usefulness of passion as a signaling strategy for startups is dependent on the available costly signals on offer. While gut feeling theory does not specify how exactly passion and costly signals interact, our theories-in-use interviews provide strong hints as to the nature of this interplay.

Passion was judged very differently when costly signals were low versus high. Given the background of low costly signals, investors’ default judgment was skepticism. Because of both the high volume and generally inflated nature of startup pitches they encounter on a daily basis, most investors defaulted to this outcome if there were no strong costly signals to reverse the skepticism. Investors colorfully described overinflated proposal attempts as “lipstick on a pig” (Interview 5), “hot air” (Interview 9), or “sizzle (not the steak)” (Interview 10). You know, passion is good, but passion really is … it opens the door, but it doesn’t get you through the door. Passion gets you that chance for someone to listen to you. But if you’re, if you’re just talking frivolous data that you cannot back up … Passion isn’t, I mean, it just gets you so far. It's just lipstick on a pig. It's still a pig. (Interview 5)

Thus, following the qualitative interview insights, we argue that when a startup has little to offer in terms of costly signals, passion does not compensate for or mitigate the fact that the startup in effect has nothing substantial to show. In this circumstance, the use of passion is indeed perceived as mere “cheap talk” (Farrell and Rabin 1996), discounted, or even viewed as dishonest—with detrimental effects. In contrast, when costly signals are high, passion is more likely to bolster those costly signals (consistent with a synergistic, combining logic), given that passion should not be interpreted as baseless boasting in this context, but perhaps as an entrepreneur's keen understanding and excitement regarding what the substantive evidence is worth. Formally:

The interplay between concreteness and costly signaling

Both gut feeling theory (Huang et al. 2021) and our theories-in-use exploration suggest that concreteness exhibits a similar conditionality on costly signals, but in the opposite direction. Specifically, when costly signals are low, investors expect concrete communication about any aspect of the venture that the startup can position as an achievement. Indeed, with few costly signals, investors face greater uncertainty and their natural reaction is skepticism (MacMillan, Zemann, and Subbanarasimha 1987). In this scenario, concreteness implies much needed tangibility to compensate (at least heuristically) for the lack of costly signals, and vagueness leads to investor judgments of low investment value: “If there was sort of concrete words used […] then, you know, I think that would offset some of those lack of costly signals” (Interview 8).

However, high concreteness is not an unqualified advantage. When costly information is high, concreteness can become a negative signal and as such suggest inadequate focus on long-term growth, the “future horizons” of the venture: This company is not thinking long-term and big enough. They’re not thinking about horizons. So, if I have a company that's just generating a lot of revenue, and then they only talk about next month: “I wanted to make, you know, another X next month… I want to increase another 30%.” Someone could say, “No! You’re not thinking about, you know, next year or five years… You should think about an IPO!” (Interview 12)

Testing B2I Marketing Theory with a Large-Scale Quantitative Field Study

Setting and Sample

To test our theory, we utilized a proprietary dataset from CDL (https://creativedestructionlab.com). CDL is a global startup program for seed-stage, science-based companies with a mission to enhance the commercialization of science for the betterment of humankind. It operates locations in 13 leading business schools around the world. Selected CDL partners include the venture investment teams from Amazon, Barclays, General Motors, Microsoft, and Novartis. The program employs an objectives-based mentoring process with a highly selective group of accomplished entrepreneurs, angel investors, economists, and scientists. To date, CDL has facilitated venture funding to enhance the commercialization as well as funding opportunities for the selected startups, thereby creating more than USD 21 billion in equity value. In addition, CDL's mentors include venture capitalists, who often invest in some of the participating startups. To receive CDL's investment (and the potential investment from the mentoring venture capitalists), startups need to be accepted into the CDL program. To apply, startups must submit a business proposal in written form, which is then evaluated by a panel consisting of several mentors. Importantly, this written proposal is the only information that the panel receives to inform their decision. The startups do not give a presentation; hence, any influence is derived from the words used in the proposal, excluding the effects of visual presentation style and other nonverbal signals. 1

The dataset includes information on 5,334 submitted business proposals and subsequent investor decisions made between 2012 and 2019 in seven different geographic locations, for a total of 23 decision groups. Applicants were required to provide essential information about their ventures, such as financial, social, human, and intellectual capital they already possess (which serve as costly signals). The proposals were submitted as free-text entries, which allowed startups to shape their verbal signaling in any manner they chose. The average proposal length was 538.40 words (SD = 302.22 words).

Measurement

Dependent variable

We employed CDL's acceptance decision as our dependent variable, which measured the binary outcome as whether a startup was “accepted” into the accelerator program (coded 1) or “not accepted” (coded 0). The acceptance decision is directly and indirectly linked with several investment decisions, including CDL's, as well as the mentors’ investment of time and resources and the potential funding from venture capitalists participating in CDL.

Costly signals

We drew on the model by Clough et al. (2019) to measure costly signals in the submitted business proposals. This model posits that startups can signal the quality of their ventures to potential investors through investments in various types of capital (financial, social, human, and intellectual). Financial capital represents the cash or credit that has already been invested in the venture (Parhankangas and Ehrlich 2014). In our study, CDL measured financial capital by asking startups to report the amount of money they had spent developing their venture. 2 We converted foreign currency to U.S. dollars at the mid-market rate on the date of proposal submission. Social capital refers to the preexisting social connections of the startup; we measured this construct via startups’ indication of the number of affiliations they had with other programs or institutions (Baum and Silverman 2004). Human capital encompasses the prior skills, knowledge, and experience of the founders, acquired through investments in schooling and other types of experience (Becker 1964). We operationalized human capital in two ways: by documenting the highest educational degree of the main founder (Unger et al. 2011) and by counting the number of cofounders (Gompers and Lerner 1998). Intellectual capital refers to intellectual property that can be used to create wealth (Stewart 1999); we measured intellectual capital by noting if patents were indicated as a means of protecting the idea from competitors and imitators (Hsu and Ziedonis 2013). The four costly signals had only low to moderate correlations (r ranging from .04 to .19). We thus used the standardized financial, social, human, and intellectual capital measures and combined them to a formative construct (Jarvis et al. 2003), in line with the formative composite index of costly signals from Clough et al. (2019). We report the effects of each measure separately in the “Robustness Tests and Additional Analyses” section.

Passion as a costless signal

Passion is defined as entrepreneurs’ intense, positive, and high-arousal emotions (such as enthusiasm) toward their ventures (Baum and Locke 2004; Cardon et al. 2009; Chen, Yao, and Kotha 2009; Robinson et al. 2004). There is no existing text-mining approach to derive the passion of a text. So, using the Affective Norms for English Words (ANEW) word list, which includes a 1–9 rating of both the valence (the pleasantness of a stimulus) and a 1–8 rating for arousal (the intensity of emotion provoked by a stimulus) of 13,916 English lemmas (Warriner, Kuperman, and Brysbaert 2013), we first removed all negatively valenced words. Only words with a valence score greater than the mean score across all 13,916 words (i.e., greater than 5.133) were kept. Next, we used the arousal scores of the remaining positively valanced words (e.g., in descending order of arousal: “spectacular” [positivity score of 7.5; arousal score of 6.65], “terrific” [positivity score of 7.12, arousal score of 5.46], “superb” [positivity score of 7, arousal score of 4.33]). We then mined our texts, employing this refined word list to arrive at an aggregate arousal score for all positively valenced words used in each startup text.

Concreteness as a costless signal

Concreteness is defined as “the degree to which the concept denoted by a word refers to a perceptible entity”; communicating with greater concreteness means describing something in a perceptible, precise, specific, or clear manner (Brysbaert, Warriner, and Kuperman 2014, p. 904). To operationalize this concept, we used Paetzold and Specia’s (2016) perceived concreteness ratings. This database contains over 85,000 modern English words, scored on a scale from 100 to 700 per their perceived level of concreteness. Higher scores indicate greater concreteness, with words referring to more tangible and specific objects, people, processes, or relationships receiving higher ratings. For instance, “funding” was rated as 366.59, “money” as 442.23, and “dollar” as 546.64. Research has demonstrated that this score is a reliable and valid method for measuring concreteness (Packard and Berger 2021). To capture the level of concreteness expressed in each proposal, we computed the average concreteness score of all the words in the given proposal. Both passion scores and concreteness scores were calculated using automated text mining.

Model Development and Model Specification

Model development

Using our conceptual framework, we specify a binary logistic regression model to disentangle the effects of costly and costless signals on investor acceptance for startup proposals (i.e., accepted or not accepted into CDL). To test the effects of costly signals, passion, and concreteness, we used a main effects model (with linear and squared terms). Crucially for our tests of H1 and H2 (and thus answering RQ2), we added interaction effects between passion and costly signals, and between concreteness and costly signals, with respect to acceptance, enabling us to simultaneously examine the “combining” or “balancing” effects of costly and costless signals on proposal success at varying levels of these variables (in line with Herhausen et al. 2023). We used the following base equations to test our hypotheses:

Correlated observables

We incorporated several covariates that could potentially be correlated with our focal measures and influence securing acceptance. The complete list of variables for our study, including their conceptualizations and operationalizations, is given in Web Appendix D. First, we controlled for recommendations originating from within the CDL program. Specifically, applicants were asked to self-report regarding whether former participants had encouraged them to seek out CDL; we coded submissions as 1 if they had received such encouragement and 0 otherwise. We treated this as a control variable, given that it does not indicate a costly signal of investability as such, and is an artifactual measure compared with more generalized constructs of social capital (i.e., social capital not specific to applying to CDL). Second, we controlled for the presence of at least one female cofounder, as prior research shows that female entrepreneurs are less likely to receive funding (Huang et al. 2021). Third, we controlled for proposal length (word count) because a higher volume of information may make the recipient feel more informed, and specific topics stemming from some projects may be more appealing to investors (Xiang et al. 2019). We measured the length of the proposal by counting the total number of words. Fourth, we controlled for impression signals in the proposal because impression management affects the likelihood of securing funding (Parhankangas and Ehrlich 2014). Specifically, we measured the use of pronouns since they have been linked to impression management strategies (e.g., Bazarova et al. 2013). Fifth, we controlled for imagery in the proposal, defined as the vivid portrayal of communication content, measured by the Toronto Word Pool (Van Balen, Tarakci, and Sood 2019). This pool includes 1,080 words, rated according to the ease with which they arouse a mental image. We included this variable because communicated imagery can be evoked in investors’ minds, which may in turn positively influence investor acceptance. Sixth, we controlled for competitive awareness in the proposal, which is the strategic consideration of existing or potential competitors that could threaten the new venture (Porter 1979). Applications were coded as 1 if they contained acknowledgment of competition in the corresponding field and 0 otherwise. While not a costly signal in and of itself, this information could favorably predispose investors. Seventh, we controlled for topic breadth in the proposal, as this indicates the startups’ capacity to deliver on more potential outcomes (Steigenberger and Wilhelm 2018). As detailed subsequently, each proposal document contains a mixture of ten possible topics. We operationalized the breadth of topics in each proposal as the number of topics covered in excess of 10% among all topics. We chose this cutoff because it represents the minimum proportion to which a proposal can focus on a topic, if it were to cover all ten topics equally (Blei 2012). Eighth, the startups self-selected into one of six venture development stages in their application (1 = concept stage, 2 = technology stage, 3 = prototype stage, 4 = validation stage, 5 = early-revenue stage, 6 = profitable stage). These stages are widely recognized as common venture development milestones, and are consistent with existent categorizations (Gompers and Lerner 2004). While startups applying to CDL are generally early stage, there is still heterogeneity within the early stage. We control for these stages given their potential impact on investor decisions (Ruhnka and Young 1987). We employ fixed effects to more accurately capture the nuances of a company's stage of development and its potential impact on investor acceptance. Web Appendix E presents means, standard deviations, and correlations.

Correlated unobservables and omitted variables

In addition to the observed covariates, there may be unobserved factors that influence acceptance decisions. For example, the expectations or level of skepticism among different decision-making panels may differ. Consequently, securing acceptance may be more challenging in some decision groups. The acceptance decisions were made over eight years (2012–2019) across different locations, with one location in the first four years, two locations in the fifth year, five locations in the sixth year, and six locations in the seventh and eighth years. We included fixed effects for all 23 decision groups to remove from our model any impact specific to the decision panel. Web Appendix F presents the distribution of proposals according to venture development stages and decision groups.

Moreover, certain topics may be more attractive to investors, making them more likely to be accepted. To control for the similarity of topics, we followed the topic modeling approach of Blei and Lafferty (2007) to identify distinct topics within proposal descriptions (Swaminathan et al. 2022). We first dropped all common stop words and eliminated all adverbs, prepositions, conjunctions, and punctuation. We allowed for word collocations to identify popular phrases and terms, stemmed all words, and used bigram collocations as single tokens. We then trimmed the resulting document-feature matrix by removing any terms occurring less than ten times or in fewer than .1% of all documents. This yielded 2,543 unique words/phrases, which we classified using k-means. Based on the Akaike information criterion, we determined that ten was the optimal number of topics for the startup descriptions, which also had the highest semantic coherence. We report more details in Web Appendix G. We used fixed effects for membership in the most likely topic to remove the potential preference of the investor for any specific topic.

We present model-free evidence in Web Appendix H. The distributions of the acceptance rates for both costly signals and concreteness hint at inverted U-shaped effects. However, the acceptance rate seems to drop when more passion is evident.

Strategic behavior of startups

Although the threat of endogeneity in terms of selection effects (i.e., we sampled all proposals during the study period), reverse causality (i.e., temporal separation between proposal and decision), and omitted variables (the written proposals are officially the only available information for the decision-makers) is rather low, we still must acknowledge that some startups may decide to use a certain amount of costly and costless signals in their proposals in anticipation of investor acceptance. The reasons driving these choices may potentially influence the outcome, and are unobservable for us. For example, very passionate entrepreneurs may not only use passion in the proposal but also speak publicly about their ideas. Further, startups high on costly signals such as human capital may have existing informal connections to people within CDL (both scenarios may increase acceptance).

Thus, we cannot claim on theoretical grounds that the effects of costly and costless signals are uncorrelated with the error term in Equation 1. To correct for the potentially endogenous regressors, we use the control function approach (Petrin and Train 2010), which is recommended for binary dependent variables such as ours (Ebbes, Papies, and Van Heerde 2022). However, we need to find instruments that correlate with the costly and costless signals, but not with the unobserved determinants of the outcome (that form part of the error term); that is, we must find instruments that meet the relevance and exclusion restrictions (e.g., Hughes, Swaminathan, and Brooks 2019). We use the startups’ peers—startups that operate in the same industry or industries—as sources to instrument the focal startups’ communication (Germann, Ebbes, and Grewal 2015).

3

In terms of relevance, we argue that the focal startup faces similar market conditions as the peer startups, given that they all operate in the same industry or industries. Thus, similar proposal conditions should make the instruments relevant. We further argue that the instruments meet the exclusion restriction because other startups’ proposals are not publicly available, and it is unlikely that competitors would share the outcome of their proposals with each other. Therefore, the instrument should be uncorrelated with the omitted variables related to the strategic behavior of startups. The first-stage equations are specified as follows:

Model specification

We included the residuals from the first stage as control variables in our model, and used robust standard errors (Papies, Ebbes, and Van Heerde 2017). To ensure the robustness of our model, we included the control variables and fixed effects for VC stages, decision groups, and proposal topics. The updated equation is as follows:

Findings

We present the base models without controls and the full models including all control variables and endogeneity corrections in Table 1. To ease the interpretation of effects, we report the odds ratios (ORs). We rerun all models with bootstrapping: All results are fully in line with the results using robust standard errors. Additional models that exclude the endogeneity correction, use the subdimension of costly signals, use alternative conceptualizations of passion for robustness, use a nonlinear measure of venture development stages, and include venture development stage interactions are discussed in the “Robustness Tests and Additional Analyses” section.

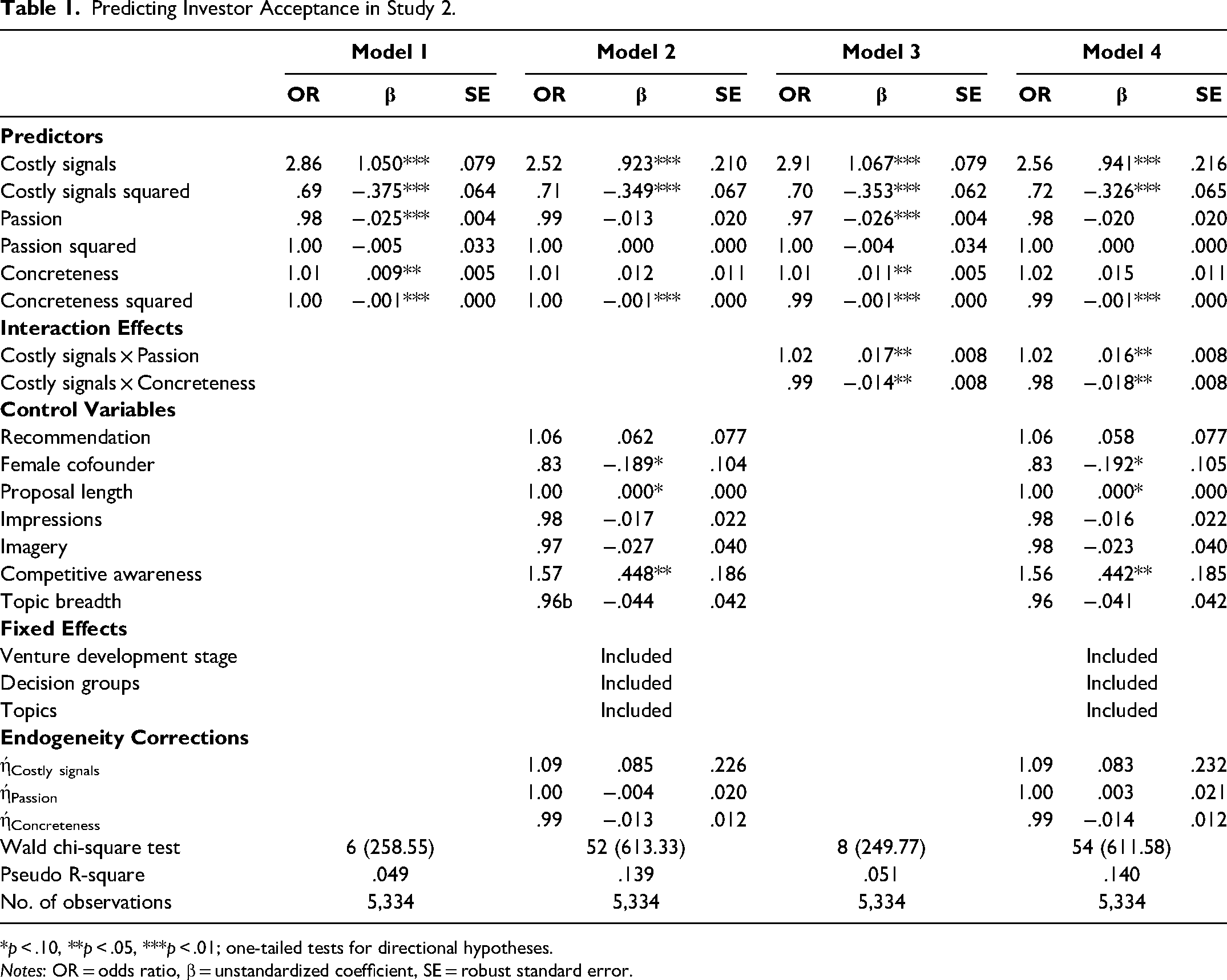

Predicting Investor Acceptance in Study 2.

*p < .10, **p < .05, ***p < .01; one-tailed tests for directional hypotheses.

Notes: OR = odds ratio, β = unstandardized coefficient, SE = robust standard error.

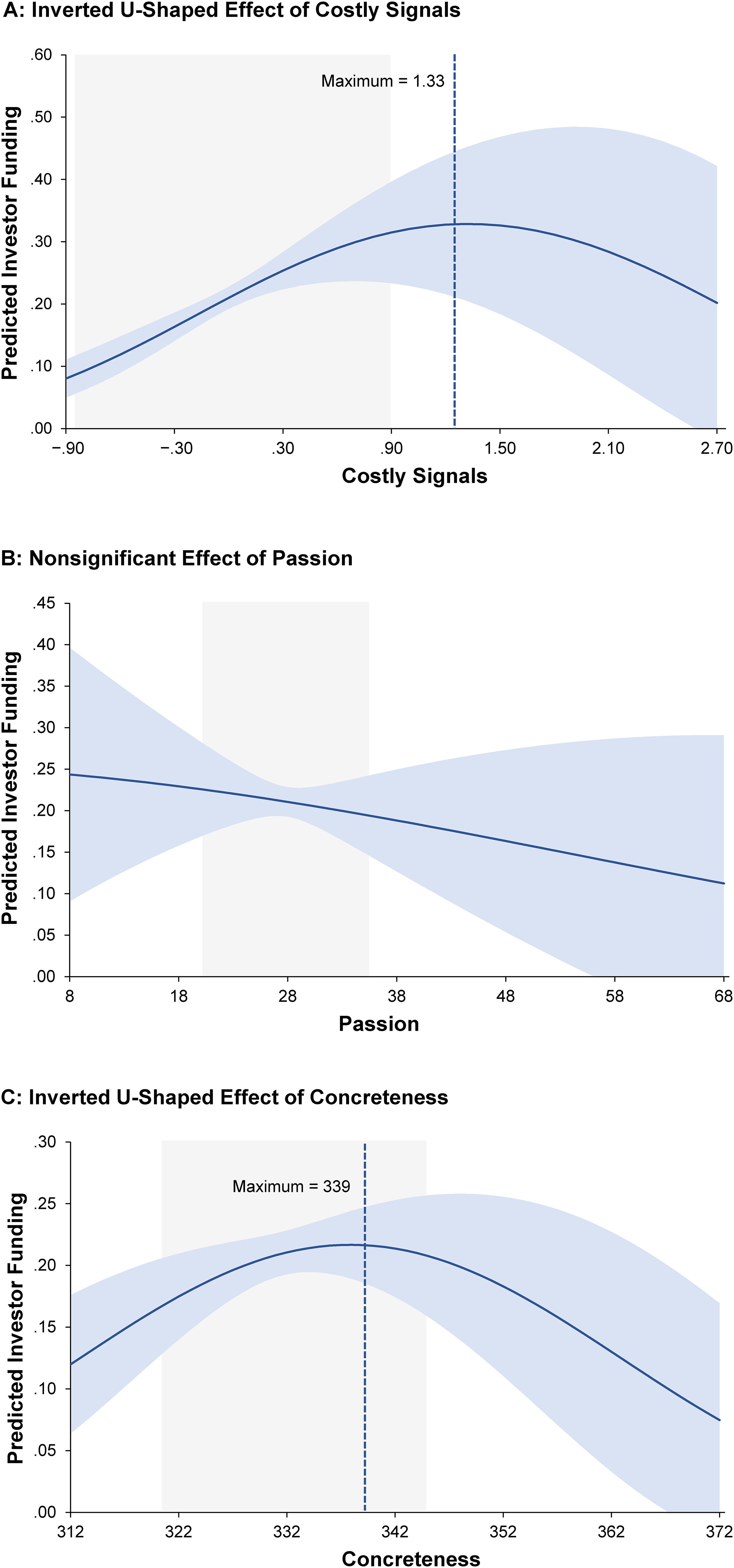

Models 1 and 2 report main effects, whereas Models 3 and 4 test H1 and H2. Results are robust across models with and without control variables. The costly signals demonstrate a positive linear effect (OR = 2.52, p < .01) and a negative quadratic effect (OR = .71, p < .01). As illustrated in Figure 2, Panel A, the turning point for this inverted U-shaped relationship is at 1.33 standard deviations above the mean. Passion shows a negative but nonsignificant linear effect (OR = .99, p = .53) and a nonsignificant quadratic effect (OR = 1.00, p = .64; see Figure 2, Panel B). Concreteness has a nonsignificant linear effect (OR = 1.01, p = .26) and a negative quadratic effect (OR = .99, p < .01). The turning point for this inverted U-shaped relationship occurs when the concreteness of the proposal equals 339 (Figure 2, Panel C).

Main Effects of Costly and Costless Signals on Investor Acceptance.

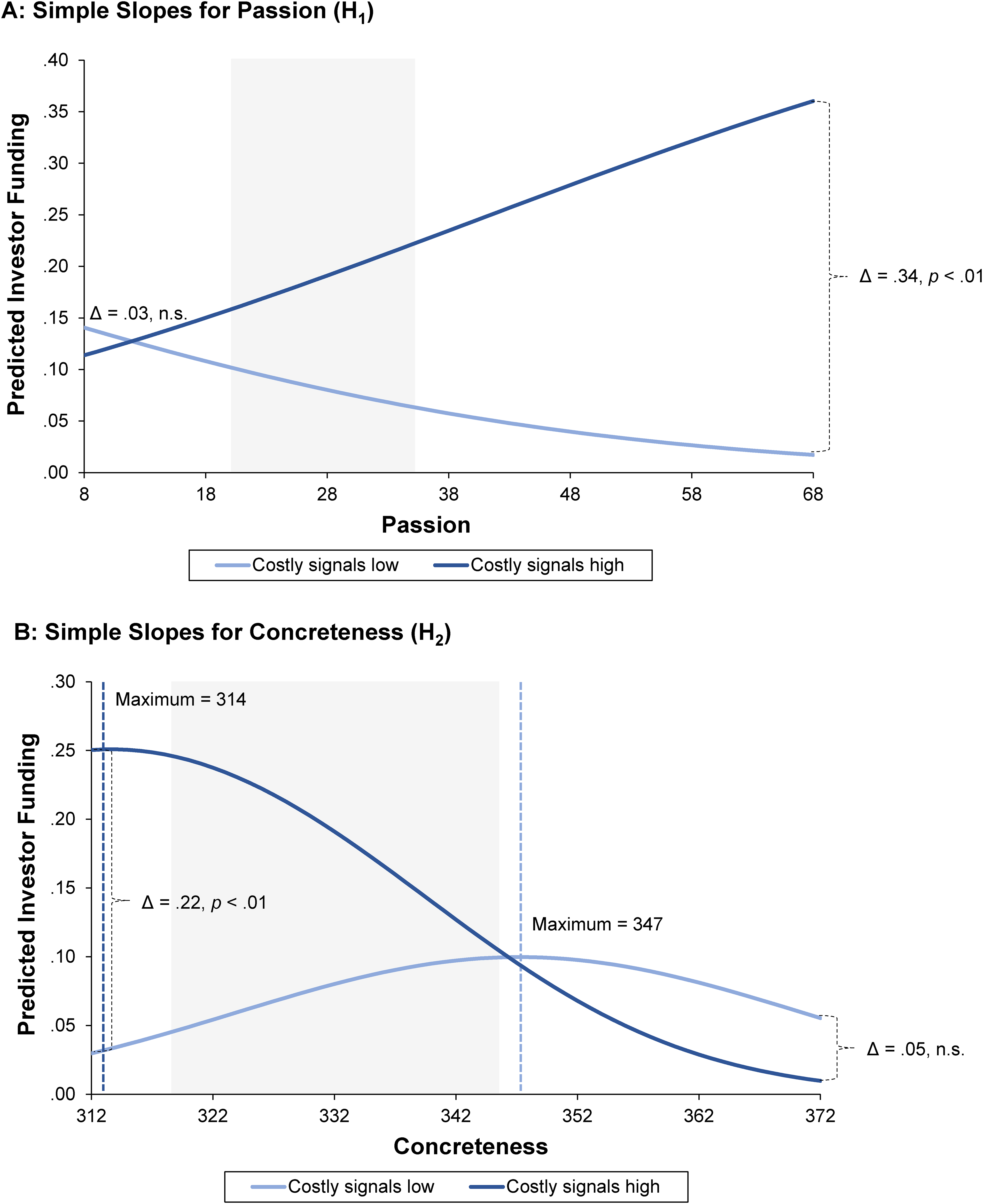

Web Appendix J presents the coefficients for the three-dimensional surfaces, and provides the two-dimensional simple slopes that test the effect of “combining” versus “balancing” costly signals with either passion or concreteness, respectively. When a small number of costly signals are provided, passion has a negative effect on investor acceptance (linear effect: OR = .97; quadratic effect: OR = 1.00). When a large number of costly signals are provided, passion has a positive effect on investor acceptance (linear effect: OR = 1.03; quadratic effect: OR = 1.00). We plot this relationship in Figure 3, Panel A. The pattern aligns with our expectations. Moreover, when a very low level of passion is provided, predicted investor acceptance does not significantly differ between low and high costly signals (Δ = .03, n.s.). Conversely, when a high level of passion is provided, high costly signals outperform low costly signals (Δ = .34, p < .01). Thus, these findings support H1.

Simple Slopes for Investor Acceptance.

Turning to concreteness, we find that when few costly signals are provided, concreteness has a positive linear effect on investor acceptance (OR = 1.03), which is qualified by a negative quadratic effect (OR = .99). When a large number of costly signals are provided, concreteness has an inverted U-shaped relationship with investor acceptance (linear effect: OR = .96; quadratic effect: OR = .98). These findings indicate that the interaction between costly signals and concreteness is more nuanced than the theory would suggest, as illustrated in Figure 3, Panel B. When a very low level of concreteness is provided, high costly signals outperform low costly signals (Δ = .22, p < .01), whereas low and high costly signals do not significantly differ when a very high level of concreteness is provided (Δ = .05, n.s.). This pattern aligns with H2. Nevertheless, the positive effect of concreteness when costly signals are low tapers off for higher levels of concreteness (above 347), and its negative effect when costly signals are high manifests when concreteness is higher than 314.

Robustness Tests and Additional Analyses

Several additional models are used to test the robustness of our findings. First, in Web Appendix K, we estimate a model that excludes the endogeneity corrections, but includes all controls. Such a robustness test is important because endogeneity corrections could potentially backfire if instruments are not strong enough (Rossi 2014). The only difference that we find relative to our main models is a significant, negative linear effect of passion (OR = .99, p < .01), while the results with interaction effects are fully in line with the model including endogeneity corrections.

Second, for robustness, we use an alternative conceptualization of passion and measured positivity. For this alternative conceptualization of passion, we repeat our steps to refine the entire ANEW word list, this time choosing a different cutoff score for the valence rating and keeping only the words in the top quartile range of said ratings (i.e., valence rating greater than 5.95). For positivity, we use the valence score from ANEW. While positivity and passion are highly correlated as expected (r = .83, p < .01), they nevertheless capture different nuances in the business proposals (as documented previously in the methods section “Passion as a costless signal”).

Instruments are similar to the main analysis (passion [robustness variant]: ΔR2 = .40 and positivity: ΔR2 = .05; passion [robustness variant]: β = 7.70 and positivity: β = .33, both p < .01; passion [robustness variant]: F = 1,327.02 and positivity: F = 350.08, both p < .01). Web Appendices L and M display the results, fully in line with our conceptualization of passion.

Third, we use the four subdimensions of costly signals and estimate their individual effects in Web Appendix N. Notably, we are unable to estimate a squared effect for the intellectual capital dummy (patents: 1 = yes, 2 = no). In line with the main findings for costly signals, we find inverted U-shaped effects for financial capital (positive linear effect: OR = 1.35, p < .01; negative quadratic effect: OR = .97, p < .01) and social capital (positive linear effect: OR = 1.27, p < .01; negative quadratic effect: OR = .93, p < .01), a positive linear effect for human capital (OR = 1.34, p < .01)—qualified by a significant negative squared effect in the model without controls (OR = .95, p < .05)—and a positive effect of the intellectual capital dummy (OR = 1.25, p < .01). These effects are displayed in the figure in Web Appendix N. In addition, all interaction effects are directionally in line with the main analysis.

Fourth, in Web Appendix O, we include a nonlinear measure of venture development stage instead of costly signals, and interaction effects with passion and concreteness. While venture development stage demonstrates a positive linear effect (OR = 1.22, p < .01) and a negative quadratic effect (OR = .86, p < .01), both its interactions with passion (OR = 1.00, p = .81) and concreteness (OR = 1.00, p = .40) are nonsignificant. This effect is shown in the figure in Web Appendix O. Finally, we control for the nonlinear effect of venture development stage in our original model, instead of including fixed effects for the stage. Results for the hypotheses in Web Appendix P are fully in line with the main analysis.

Discussion of Quantitative Field Study Findings

The study aimed to examine the impact of costly and costless signals on the likelihood of investor acceptance by testing two interactive hypotheses. Using a proprietary dataset from CDL, the study finds that when few costly signals are provided in a startup proposal, passion has a negative effect, whereas concreteness has a positive effect (with diminishing returns) on investor acceptance. When a large number of costly signals are provided, however, passion has a positive effect, while concreteness has a negative effect on the likelihood of investor acceptance. These findings are all in line with H1 and H2. The study contributes by showing the interplay of costly and costless signals on investor acceptance and by providing insights for startups regarding the optimal combination of signals to secure acceptance.

General Discussion

Theoretical Contributions

We offer three main theoretical contributions. First, we build new theory for B2I marketing, thereby complementing the familiar B2C and B2B domains. We build our theory on two pillars derived from foundational literatures: costly signaling (based on normative economic logic) and costless signaling (based on heuristic processing in behavioral science). We unify these theoretical streams to suggest that both costly and costless factors have a role to play within early-stage investors’ holistic “gut feeling” assessments. In so doing, we bring together two broader streams of theorizing that can explain the effects of B2I marketing. In the dyad of signaling startups and recipient investors, signaling theory has largely focused on the sender (Colombo 2021), while theories of investor decision-making (Huang and Pearce 2015; Shepherd, Zacharakis, and Baron 2003) have focused on the recipient. In reality, and as evident for marketing scholars, both sender and recipient perspectives need to be considered in order to adequately understand this dyad. Our theorizing sets out to do just that, and thereby joins these paradigms.

Second, we map out a comprehensive typology for both costly and costless signals; we then test our theory with a focus on verbal signals with a large proprietary dataset. Thus, we respond to calls for research on word-level communication (Berger et al. 2020). To our knowledge, we are among the first to do so in the domain of B2I marketing. We uncover positive but curvilinear (inverted U-shaped) effects of concreteness in written proposals on investor acceptance, which helps reconcile the two available (but contradictory) findings in the management literature showing both positive (Parhankangas and Renko 2017) and negative (Huang et al. 2021) effects. Our deductive (as well as theories-in-use) theorizing with venture capitalists explains this curvilinear effect by suggesting that investors expect an optimum (not too high, not too low) level of concreteness, given that this results in impressions of both initial success probability and long-term growth. Once we account for a number of startup and proposal characteristics, passion in the written proposal, a heuristic that we expected (in line with prior research; Parhankangas and Ehrlich 2014) to be linked to successful B2I communication outcomes, was not shown to have a significant direct effect. While prior research could not account for such detailed background data, it does acknowledge that the effectiveness of costless heuristics is likely dependent on the investor context (Parhankangas and Ehrlich 2014). In CDL, a global startup program for seed-stage, science-based companies focused on high tech and high growth, passion's influence is contingent on the costly signals a startup possesses, as we discuss next.

Third, we assess interdependence between costly signals and each of our costless verbal signals (passion and concreteness). We find that the effects of concreteness and passion are indeed contingent on the level of costly signals a startup possesses: When costly signals are high, excessive concreteness backfires whereas passion has a positive linear effect. Conversely, when costly signals are low, concreteness improves the probabilities of investor acceptance but with diminishing returns that become negative (i.e., an inverted U-shaped effect), while passion simply lowers investor acceptance. These findings corroborate our core theoretical argument that, to understand B2I marketing, both costly signaling's economic logic and costless signaling's heuristic logic are needed. This is because both processes interdependently influence investor judgment. Thus, our work extends both signaling theory (DeKinder and Kohli 2008; Homburg et al. 2014) and understanding of investor decision-making (Huang and Pearce 2015), while also providing novel managerial insights.

Managerial Implications

Our research offers practical insights for entrepreneurs trying to market their startups and for investors presented with such marketing. Any research insights in the B2I domain are important, given the size of the VC industry ($288 billion in 2021, not counting corporate VC, angel, and crowdfunding involvement; Teare 2021).

Implications for startups

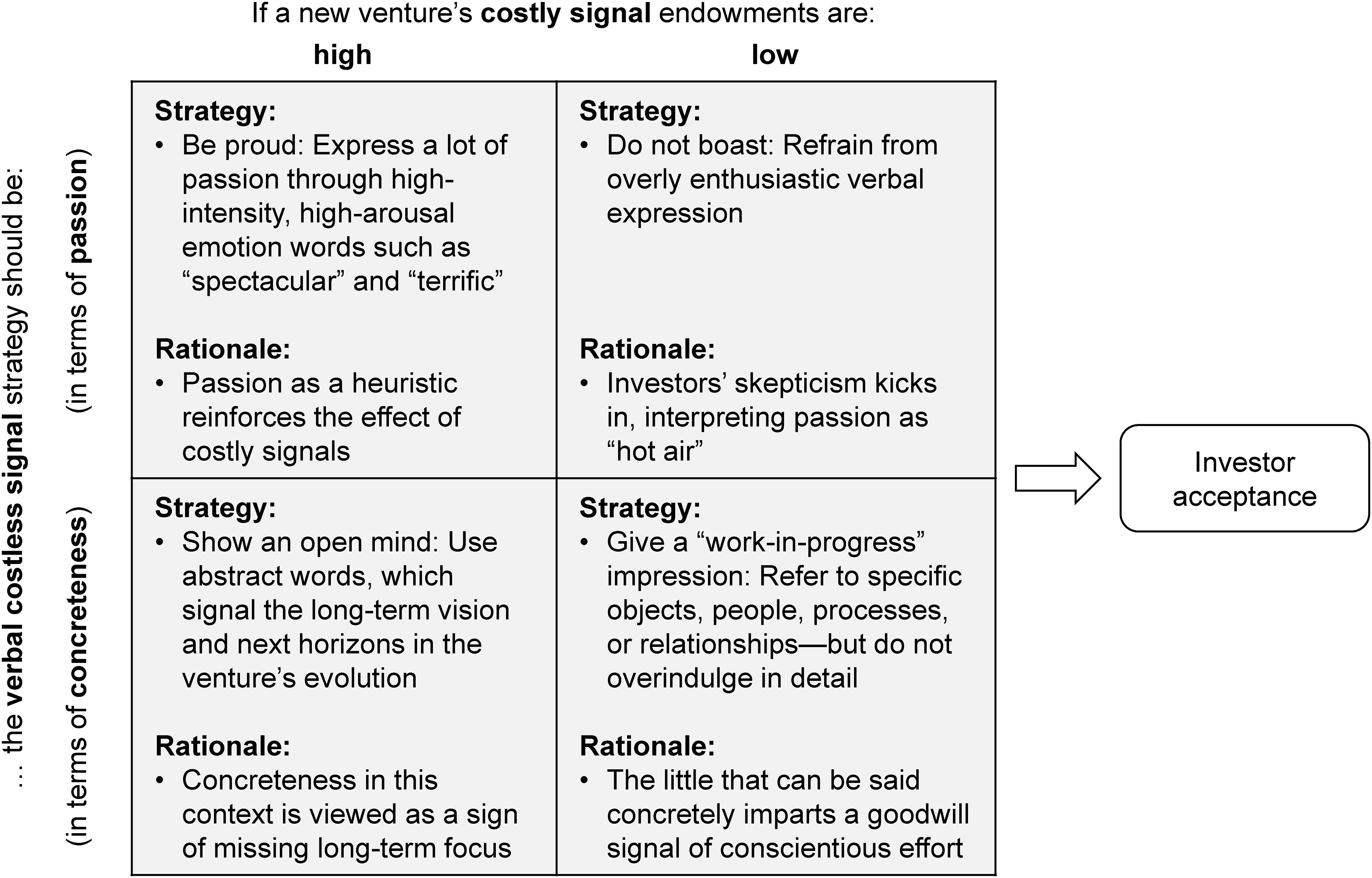

Given the complexity of entrepreneurial marketing to investors (and the general uncertainty of a startup's environment), our study provides clear guidance on how startups should formulate the all-important proposal. Our key implication for startups is that their formulations depend on the magnitude of costly resources they are able to showcase. We summarize these recommendations in a 2 × 2 matrix (Figure 4).

Implications for Investor Acceptance.

Passion may be a strong motivator for the entrepreneur, but displaying it to investors when there is scarcely anything else to show will not help. What does help is to be moderately concrete about what little there is to say. Conversely, when the venture has costly resources, being passionate in proposals is the optimal B2I marketing strategy. Startups with plenty of costly signals are also more successful when they refrain from overly concrete language while sharing a broader outlook on the possible future.

Implications for investors

Our findings have implications for investors, too. Investors expect the startup's proposal to be a strong marketing push, which they will need to mentally discount and cross-check. We find further validation for the investors’ understanding that the effects of passion and concreteness are dependent on the costly resources showcased. Indeed, our account of these conditional effects confirms the rationality of investors, even when handling supposedly “costless” signals. After all, looking for concreteness where there is no substantive, costly signaling—and, conversely, allowing passion to have its due effect when there is—may be just the right approach to take as an investor.

However, there are also risks. Startups divulging excessively concrete details about their costly resources are not necessarily narrow-minded, lacking the ability to imagine broader horizons; they may only appear so. In reality, startups may indeed have a grand vision but may simply think it more appropriate to be concrete instead of chasing “pies in the sky” (i.e., abstractness). Similarly, showcasing passion, when there is no underlying costly value, is not necessarily a sign of vacuousness or dishonesty; it may only appear so. In reality, some startups are able to succeed on passion alone. Therefore, investors are advised to seek more information specific to the signals we investigate here.

Finally, investors need to be aware of the effects that excessive costly resources seem to have on other investors (and themselves). While excessive resources may signal resource waste and inflated valuations, it is also possible that investors have simply encountered entrepreneurs with an exceptional ability to secure important resources (what's not to like?). Again, investors are advised to specifically probe for additional information on coachability, strategic flexibility, and underlying value.

Limitations and Directions for Further Research

First, our quantitative dataset contained only written proposals. While this is beneficial in terms of ruling out the confounding effects of any nonverbal signals, it is also an important limitation, given that our broader typology shows that nonverbal signals in the form of visuals, vocalics, and kinesics are all important structural elements of pitches. Indeed, our structured review of the literature (Web Appendix B) finds that each impacts early-stage investors. Future research should investigate these costless signals, not in isolation, but in interaction with costly signals. Further, future studies could specifically target the entirety of our typology with a feasibly rich dataset to compare the effect sizes of each type of costless signal.

Second, our data contained decisions on investors’ acceptance into the CDL accelerator. While we believe acceptance decisions are both directly and indirectly related to actual investment decisions these same investors may make later in the process, we acknowledge this limitation of the data. Future research can corroborate our findings with different datasets that include dollar investments.

Third, we had no data on the characteristics of the investor decision-makers and the fit within the entrepreneur–investor dyad. While prior research has demonstrated the influence of such congruence (i.e., homophily effects; Franke et al. 2006), future studies could investigate whether fit in the dyad moderates our findings. Further, and irrespective of homophily effects, investors may differ in many ways, which may in turn impact how they appraise the same proposal information—with downstream consequences for funding decisions. For example, given the uncertainty of the startup marketing context, it is not clear what passion may mean to different groups of investors. As hinted previously, excess passion without costly signals may indicate vacuousness to the average investor, but a subset of the investing community may appraise such information differently (for example, as a positively judged, devil-may-care attitude, signaling a startup that will force its way through any obstacle by sheer will). Similarly, while the average investor may conclude that concreteness combined with costly signals means lack of vision, others may presume that extreme focus will pay dividends over the long term.

Fourth, we tested our B2I marketing theory on early-stage investors, specifically angel and VC investors. While these groups are of great importance in providing capital to startups, other investor groups also deserve research attention. Crowdfunding, for example, has become an important research target in marketing (Herd, Mallapragada, and Narayan 2022). Crowdfunders are, arguably, a unique investor group, closer to consumers in many ways than professional investors. Future research could extend our B2I theorizing and test whether marketing to crowdfunders represents a type of hybrid between B2C and B2I marketing, with unique predictors fitting this target alone (some initial research by Xiang et al. [2019] seems to support this possibility).

The “selling” of IPOs may also represent a particular subtype of B2I marketing, given the highly formalized, somewhat later-stage and multistakeholder nature of the marketing efforts contained therein (Bahadir, DeKinder, and Kohli 2015). Indeed, B2I theorizing could even be extended to post-IPO, public-market investor marketing. As part of this extension work into later stages, future research could test which emerging marketing assets (e.g., brand equity, customer equity) are the most effective costly signals and why.

Future studies may also seek to directly target the whole range of different investor groups enumerated previously, and test the comparative effects of B2I theory-derived predictors on them. This could potentially further enrich marketing research and also help with managerial segmentation decisions. Finally, CDL's industry sector focus is high-tech, high-growth entrepreneurship, which, though a perfect fit for angel/VC contexts, cannot cover the entire gamut of everyday entrepreneurial activity (e.g., family or small businesses). Hence, we encourage more research pertaining to these additional domains.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429241288464 - Supplemental material for Business-to-Investor Marketing: The Interplay of Costly and Costless Signals

Supplemental material, sj-pdf-1-jmx-10.1177_00222429241288464 for Business-to-Investor Marketing: The Interplay of Costly and Costless Signals by Greg Nyilasy, Shangwen Yi, Dennis Herhausen, Stephan Ludwig and Darren W. Dahl in Journal of Marketing

Footnotes

Acknowledgments

The authors acknowledge the research support provided by the Creative Destruction Lab and thank the JM review team for their thoughtful guidance and support throughout the review process.

Coeditor

Vanitha Swaminathan

Associate Editor

Caleb Warren

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.