Abstract

Rare watches, fine wines and spirits, sports cars, designer sneakers, and many other luxury goods create massive enrichment opportunities for consumers if they resell them on secondary markets. This trend is part of the enrichment economy, a novel form of market arrangement wherein consumers use iconic goods to increase their capital. However, it creates challenges for brands, such as preserving their primary market desirability and avoiding cannibalization. To understand how brands can navigate the enrichment economy, the authors conducted an ethnographic study of the luxury watch industry. They draw on market system dynamics to theorize market processes that sustain a market within the enrichment economy, and they explain the shared discourses, norms, and practices that make the enrichment economy function. This research makes four contributions. First, the authors theorize primary–secondary market dynamics as a novel class of market dynamics. Second, they theorize the new role of luxury brands as enrichment curators. Third, they discuss the ethics of enrichment by highlighting inequalities and risks it creates. Fourth, this research introduces the enrichment strategy as a novel brand strategy that capitalizes on the market dynamics of enrichment. The authors offer recommendations for luxury and nonluxury brands on product portfolio management, customer relationship management, and ethical innovation.

Keywords

A smattering of markets has recently created unprecedented opportunities for consumers to make significant financial returns. Take, for example, the “Carhartt x Eminem x Air Jordan 4 Retro” sneakers, initially gifted to loyal fans in 2015. Within three years, their value soared to $10,000 per pair (Tesema 2018) and by 2024, they were priced over $30,000 each (StockX 2024). Similarly, in 1987, 40 bottles of “The Macallan 1926 Fine & Rare” whisky were sold for around $20,000 per bottle. Today, each bottle commands about $1.5 million in resale value (Squires 2021). And, in 2022, 170 Tiffany Blue Nautilus watches from Patek Philippe were sold to the brand’s lifelong clients for $50,000 each. Today, they fetch an astonishing price of around $3 million each on the secondary market (Chrono24 2024). Similar phenomena can be observed in other markets that deal in highly singular goods, ranging from luxury (e.g., sports cars, high jewelry, and leather goods) to artworks and antiques and NFTs.

Such markets belong to the rapidly expanding enrichment economy, a novel economic arrangement based on enrichment goods that can potentially increase the financial capital of their owners (Boltanski and Esquerre 2020). They stand in stark contrast to conventional markets, where goods typically lose monetary value, status, and desirability when transferred from primary to secondary markets (Fontaine 2008; Gregson and Crewe 2003). Moreover, such markets are quickly emerging as primary value drivers within their respective industries. For instance, the market for preowned luxury watches is expected to reach $29 billion to $32 billion in sales by 2025 (McKinsey & Company 2021), surpassing half of the primary luxury watch market’s value (Dupreelle et al. 2023).

However, the expansion of the enrichment economy poses significant challenges for brands accustomed to operating in the primary market alone. In the enrichment economy, the value of brands is increasingly connected to their secondary market performance, which seemingly falls beyond the brands’ control. How can brands navigate this challenge to avoid potential cannibalization from the secondary market, preserve their primary market desirability, and leverage their equity in secondary markets to enhance their position in the primary market?

To address these emerging business challenges, we embraced the market system dynamics (MSD) approach (Giesler 2008, 2012; Giesler and Fischer 2017) and conducted an ethnographic investigation of the luxury watch market, which is one of the most prominent examples of the enrichment economy at work (see Saxena 2024). Recognizing the processual nature of markets (Vargo et al. 2017), we ask the following research question: “What are the processes that sustain a market within the enrichment economy?” We aim to understand the intertwined discourses, norms, and practices (Reay and Jones 2016) that unite the market actors within the enrichment economy, such as the primary market, the secondary market, and consumers navigating between the two markets.

Our research makes four contributions to marketing literature. First, we contribute to the MSD literature (Giesler 2008, 2012; Giesler and Fischer 2017) by investigating the primary–secondary market dynamics that explain the circulation of goods between primary and secondary markets. We do so in markets that deal in both “standard” and enrichment goods. For each market, we theorize the nature of goods circulation, primary–secondary market interdependencies, and dominant market logics.

Second, we identify an emerging role for luxury brands as enrichment curators that goes beyond status maintenance for both brands (Dion and Arnould 2011; Dion and Borraz 2017; Kapferer 2015) and consumers (Bellezza 2023; Humphreys and Carpenter 2018). We demonstrate that accessing enrichment goods is a form of enrichment privilege carefully curated by luxury brands. In enacting this role, luxury brands create a complex network of social interdependencies that reinforce their power while prompting consumers to court them in pursuit of better enrichment privileges.

Third, we prominently discuss the ethical dimension of the enrichment economy (Boltanski and Esquerre 2020). We highlight the social inequalities and externalities that the enrichment economy may foster and suggest public policy remedies. We also show the paradoxical effect of secondary market consumption increasing primary market consumption, which undermines circularity (Machado et al. 2019), and suggest strategies to mitigate it.

Fourth, we introduce the enrichment strategy as a brand strategy that leverages the market dynamics of enrichment. Central to this strategy is the transformation of goods into enrichment privileges and brands into enrichment curators, enabling luxury (and select nonluxury) brands to increase their revenues and desirability in a unique way. We offer advice on product management, customer relationship management, and ethical innovation to make the enrichment economy more democratic, egalitarian, and transparent.

Theoretical Framework

Primary and Secondary Markets

The literature on secondary markets and their interaction with the primary markets rests on several interrelated assumptions. The first assumption has to do with the nature of secondary market actors. The first type is decentralized actors that thrive on festivity, such as flea markets (Belk, Sherry, and Wallendorf 1988; Sherry 1990). The second type is organized actors that thrive on thrift, such as secondhand shops (Fontaine 2008; Gregson and Crewe 2003). In these secondary markets, consumers seek affordable alternatives, shop for inexpensive memorabilia, and look for sustainable options that reduce resource use (Hansen and Le Zotte 2019; Machado et al. 2019).

The second assumption addresses the circulation of goods between primary and secondary markets. Most goods are assumed to see their standing, monetary value, and desirability decrease when they are transferred from primary to secondary markets (Fontaine 2008; Gregson and Crewe 2003). Since each transaction only contributes to an item’s deterioration, the latter is assumed to eventually reach a “rubbish” state (Thompson 1979). In this paradigm, secondary markets are assumed to deal in unwanted, used, and cast out goods that are no match for primary market goods (Belk, Sherry, and Wallendorf 1988; Fontaine 2008; Sherry 1990).

The third assumption concerns the interdependencies across primary and secondary markets. Secondary markets are assumed to cannibalize primary markets (Yrjölä, Hokkanen, and Saarijärvi 2021; Zhao and Jagpal 2006; Zhao, Zhao, and Deng 2016). This is fueled by thrifty consumers who artfully mediate between the two markets to “bargain hunt” (Guiot and Roux 2010). In response, brands focus on the continuous substitution of current goods with new goods to resist cannibalization.

However, a growing number of emerging secondary markets are actively challenging these assumptions. For instance, select vintage goods are sold by highly specialized main street resellers (Veenstra and Kuipers 2013), and the prices of these goods tend to appreciate over time (Abdelrahman, Banister, and Hampson 2020). This trend is also observable in art markets, where some works of art appreciate dramatically over time (Thompson 1979; Velthuis 2005). Moreover, art and vintage goods do not always cannibalize the primary market. For instance, when an artist’s work garners interest on the secondary market, it will likely benefit them in the primary market. As described in the introduction, we observe a similar phenomenon in many luxury markets (i.e., fine wines and spirits, sports cars, luxury watches, and leather bags). To understand such markets, we turn to the sociology of the enrichment economy (Boltanski and Esquerre 2020).

Enrichment Economy

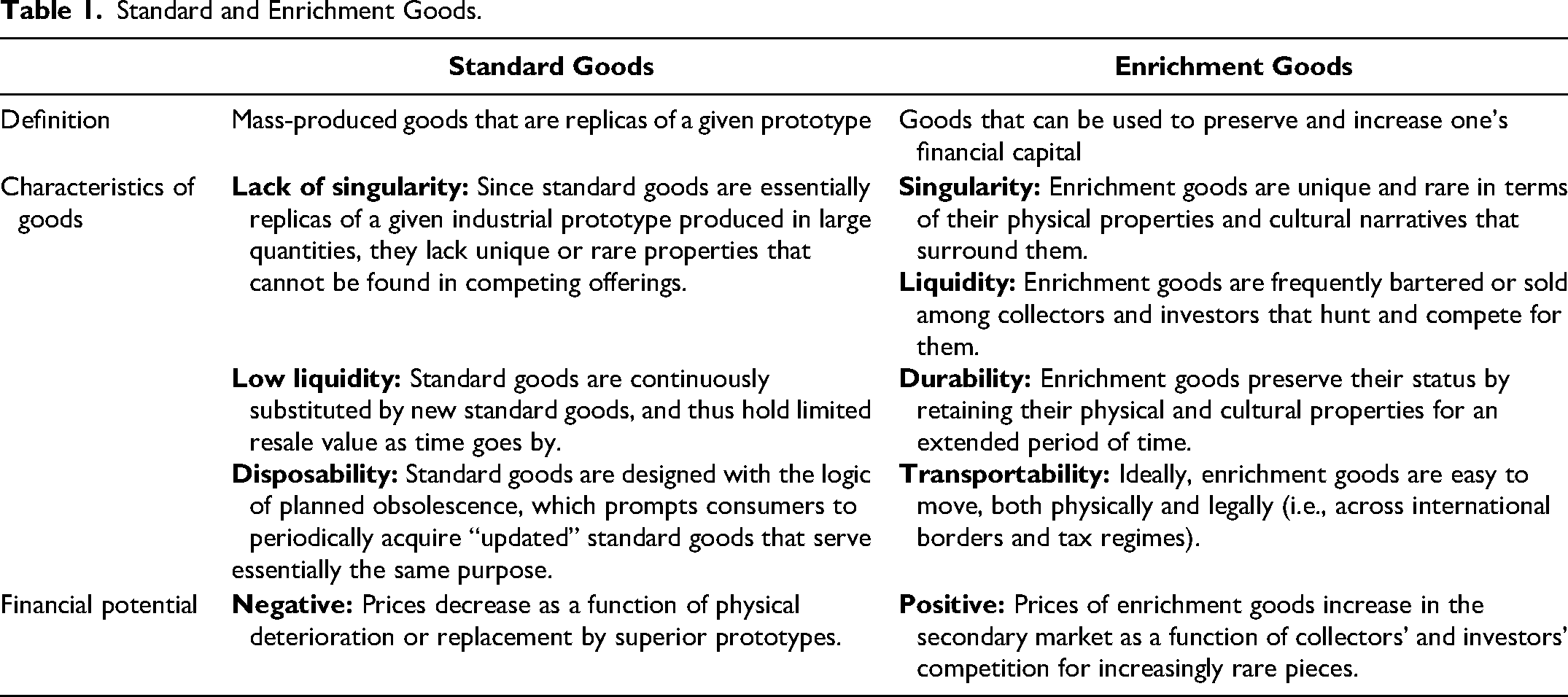

Boltanski and Esquerre (2020) posit that deindustrialization has led to the emergence of new models of value creation. One of them is the enrichment economy, an economy based on small-scale production of enrichment goods. Enrichment goods can be used to preserve and increase one’s financial capital. They tend to be singular, liquid, durable, and transportable (see Table 1 and Web Appendix W1 for additional details). Some of the most enduring examples of enrichment goods are artworks and antiques. Also, select luxury goods often become enrichment goods (e.g., sports cars, fine wines and spirits, or luxury watches). Even mass-market goods can evolve to become enrichment goods if they are singular enough, which is usually the function of their limited or irregular supply, as seen in trading cards or toy collectibles. Thus, enrichment goods differ from standard goods, which are typically nonsingular and interchangeable goods that tend to depreciate when a new iteration is introduced (Boltanski and Esquerre 2020; see also Karpik 2010; Reckwitz 2020).

Standard and Enrichment Goods.

Boltanski and Esquerre (2020) theorize two ways in which brands can turn goods into enrichment goods. Physical enrichment bestows goods with singular physical properties that are hard to match or imitate (e.g., a leather bag made with exotic skin). In contrast, cultural enrichment involves embedding goods in compelling storytelling that endures over time, often featuring the narratives of outstanding events and celebrities (e.g., a watch brand offering its watches for a lunar mission).

According to Boltanski and Esquerre (2020), enrichment goods attract two major consumer segments: wealthy collectors and investors. For collectors, enrichment goods offer a chance to create a unique portfolio of rare and personally meaningful objects (see Belk 1995; Pearce 1998). For investors, enrichment goods are a way to preserve and increase one’s financial capital. They complement standard investment instruments such as stocks and spur the interest of those who want to diversify their portfolios.

The most significant difference between enrichment and standard goods is their financial potential. The prices of enrichment goods are constantly increasing due to the heightened competition among collectors and investors. Consequently, access to these goods is increasingly restricted to wealthy individuals, making the enrichment economy “a supplementary source of [personal] enrichment for the wealthy” (Boltanski and Esquerre 2020, p. 2). In contrast, standard goods depreciate over time, as the introduction of each new version diminishes the value of the older one (e.g., Toyota Corolla).

Boltanski and Esquerre’s treatment of the enrichment economy is goods-centered (2020, p. 112). They capture the outcome of the enrichment economy, which is the growing prevalence of enrichment goods as a novel class of commodities whose circulation generates enrichment opportunities for wealthy consumers. However, they do not explore the actual functioning of the enrichment economy. For instance, the supply side of the enrichment economy is left unexplored, for “production does not play a determining role [in the enrichment economy]” (Boltanski and Esquerre 2020, p. 161). The same applies to the demand side. At the same time, the authors acknowledge that the enrichment economy is a novel and thus fragile economic arrangement, similar to what the standard economy was at its origins during the Industrial Revolution. Thus, it is imperative to investigate the fundamental supply and demand forces (Alderson 1965; Alderson and Cox 1948) that make this economy possible.

For this, we turn to market system dynamics (MSD), which investigates how markets function at the intersection of both supply and demand (Giesler 2008, 2012; Giesler and Fischer 2017). The MSD tradition considers the vast array of actors, including consumers, producers, influencers, and policy makers, who jointly shape how supply and demand interact both within and across markets. It explores the arrangements among market actors and the ways in which they shape various market processes. In drawing on MSD, we shift attention from the existence and growing prevalence of the enrichment economy (Boltanski and Esquerre 2020) toward understanding how the supply and demand for enrichment goods originate and function.

Market System Dynamics

The central tenet of MSD is that markets are complex and ever-evolving social arrangements that are inherently dynamic (Giesler 2008, 2012; Giesler and Fischer 2017; see also Alderson 1965; Alderson and Cox 1948; Vargo and Lusch 2004). MSD research theorizes how markets emerge, stabilize, and dissipate (Humphreys and Carpenter 2018; Jafari, Aly, and Doherty 2022; Nøjgaard and Bajde 2021; Pedeliento et al. 2023). MSD regards markets as continuously (re)constructed by a vast array of actors, ranging from consumers and producers to governments and societies (Giesler and Fischer 2017). The MSD tradition has addressed many dynamics as they relate to space (Castilhos, Dolbec, and Veresiu 2017), time (Parmentier and Fischer 2015), and competition (Ertimur and Coskuner-Balli 2015), among others.

Vargo et al. (2017) propose four interrelated principles to analyze markets. First, markets shall be studied holistically, since “the systemic properties [cannot] be reduced to those of the smaller parts” (p. 262). Second, the locus of analysis shall be relationships between market actors and not mere objects of exchange. Third, the emphasis shall lie on processes that make structures function, since “a system is more than [a] static configuration” (p. 262). Fourth, research shall focus on mapping recurring patterns inherent to a given market at a given time.

In following these, two concepts are fundamental: market logics and circulation. Market logics are “principles that direct thoughts, decisions, and behaviors of people and organizations” (Ertimur and Coskuner-Balli 2015, p. 40). They are shared understandings expressed in discourses (verbal, visual, or written), norms (behaviors), and practices (symbolic and material) inherent to a given market (Reay and Jones 2016; see Thornton, Ocasio, and Lounsbury 2012). Frequently, a dominant market logic, which organizes exchange and bestows each actor with a unique role, may arise. Such logics reveal processes and relationships that sustain a market (Giesler 2012; Jafari, Aly, and Doherty 2022; Pedeliento et al. 2023). For instance, Giesler (2012) captures the sequence of dominant logics on the music distribution market, each representing a compromise between key market actors (i.e., music publishers and consumers). Alternatively, Ertimur and Coskuner-Balli (2015) capture the coexistence of several dominant logics in the American yoga market, each represented by different market segments. Similarly, we need to understand the logic of enrichment markets and highlight the broader discourses, norms, and practices in which enrichment goods and market actors are embedded.

Equally important is the notion of circulation, or the transfer of objects among market actors. It reveals how and why actors assign value to goods (Appadurai 1988; Graeber 2001). As Figueiredo and Scaraboto outline, “a focus on circulation brings [forth] the role of objects in fostering interdependencies that occur as objects are transferred” (2016, p. 510). Such interdependencies further highlight the dominant logic that organizes exchanges in a market. For instance, Figueiredo and Scaraboto (2016) outline how the circulation of objects in the context of geocaching unites enthusiasts by allowing them to add unique value to objects despite geographic distances. In another article on religion, Scaraboto and Figueiredo (2017) describe how the circulation of mini-chapels fosters communal bonds between the church and its various stakeholders. With regard to enrichment markets, the focus on circulation brings forth a more complete picture in which enrichment goods circulate concurrently on both primary and secondary markets and across various market actors.

In sum, MSD is a promising approach to understand enrichment markets. It moves us beyond the properties of enrichment goods to consider their circulation and the marketwide processes that support it. We ask the following research question: “What are the processes that sustain a market within the enrichment economy?” To this end, we conducted an ethnographic study of the luxury watch market.

Context and Research Design

Context

The history of watches goes back to the 16th century, when spring-powered clocks were sized down into portable devices resembling the watches today. Swiss companies dominated the market until the 1960s, when the “quartz revolution” introduced electronic timekeeping (Donzé 2011, 2020). In response, Swiss brands repositioned themselves as purveyors of luxury goods, emphasizing their role as status symbols (Donzé 2011, 2020). Today, the luxury watch industry is valued at $42 billion and is expected to grow to $50 billion by 2026 (Grand View Research 2022). The market is dominated by legacy Swiss brands such as Rolex, Patek Philippe, and Audemars Piguet. More and more, they are challenged by innovators (e.g., F.P. Journe, MB&F) and adjacent luxury brands (e.g., Louis Vuitton, Chanel).

One of the biggest trends on the luxury watch market is the rise of the secondary market, which is projected to reach $32 billion in sales by 2025 (McKinsey & Company 2021), accounting for more than half of the primary market (Dupreelle et al. 2023). Today, it is sustained by three types of actors: auction houses, online marketplaces, and peer-to-peer clubs. The most singular pieces are sold exclusively at elite auctions, such as Christie’s. However, the majority of sales occur on online platforms (e.g., Watchfinder, Chrono24), which have seen double-digit growth in the past few years (Robinson 2021). Additionally, enthusiasts can trade watches directly through peer-to-peer clubs, such as Moda Watch Club, a private group of more than 60,000 members. It is a collective of experienced dealers and collectors that thrives on exclusivity. All of this makes the luxury watch market the perfect context to understand the enrichment economy, which is characterized by a large number of enthusiasts increasingly dealing in unique and precious goods (Boltanski and Esquerre 2020) (see Web Appendix W2 on the history of the secondary luxury watch market).

Research Design

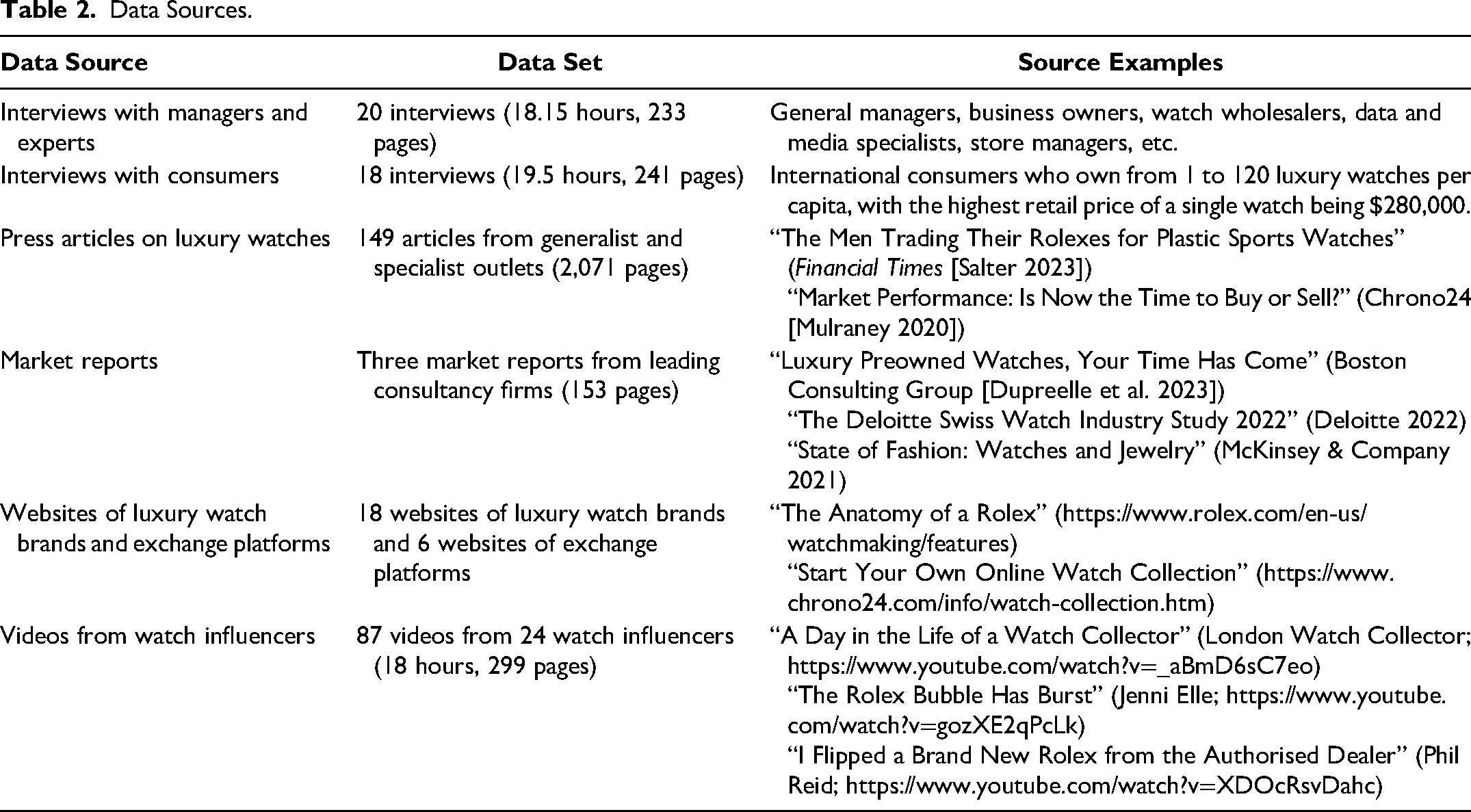

To explore the luxury watch market, we used an ethnographic approach that captures the market from the perspective of its key actors (Dion and Borraz 2017; Dolbec, Arsel, and Aboelenien 2022; Humphreys and Carpenter 2018). We immersed ourselves in the industry, conducted 38 interviews, and built an extensive archival dataset (see Table 2).

Data Sources.

To engage with our context, we selected the peripheral membership approach (Adler and Adler 1987), which implies a close and frequent engagement with the field without directly engaging in its central activities (i.e., buying and selling luxury watches). This choice is informed by personal, structural, and research considerations (Adler and Adler 1987). We came into the context as neophytes, making direct engagement in central activities impossible. Thus, our priority was to understand our informants’ practices without becoming direct participants (see Becker et al. 1961). This approach has paid off because informants have shown visible pride in proselytizing to us as outsiders. Structurally, our context is highly elite and secretive. Hence, we relied on focused interviewing as the most feasible and nondisturbing pathway into informants’ lives. We embraced the critical streak of Boltanski and Esquerre’s (2020) treatment of the enrichment economy. It implied maintaining an analytical distance to understand the field beyond informants’ lived experiences (see Adler and Adler 1987). To further our engagement, we immersed ourselves in the field as researchers and individuals. We watched influencer videos, discussed watch trends among ourselves, visited watch boutiques whenever possible, read up on the topic, and discussed it extensively with colleagues and friends.

To obtain a marketer’s perspective, we conducted 20 interviews with managers, business owners, and market experts (see Web Appendix W3). The primary market is represented by high-profile managers (e.g., general managers, marketing directors, key account managers) who work or have worked for leading watch brands such as Rolex, Patek Philippe, Audemars Piguet, Fabergé, Cartier, Van Cleef & Arpels, Zenith, and Vacheron Constantin. The secondary market is represented by high-profile informants who work or have worked for leading secondary market actors such as Bob’s Watches, among others. In addition, we reached out to experts at Indochine Media (luxury media), Digital Luxury Group (luxury consulting), and Data&Data (luxury big data). Thanks to the professional and alumni connections we have cultivated over the years, we earned the trust of our corporate informants, enabling them to share their insights despite the industry’s high level of secrecy. During the interviews, we explored topics such as luxury watch retailing, customer relationship management, and the secondary luxury watch market.

To obtain a consumer’s perspective, we interviewed 18 luxury watch enthusiasts. We found the first several informants through our professional and personal networks. We secured enough trust with them to get interview referrals. Their occupations range from business consultants to executives and entrepreneurs. They own from 1 to 120 luxury watches per capita, with the highest price of a single watch exceeding $280,000. In addition, two informants are graduate students securing their first luxury watch (see Web Appendix W4). During the interviews, we discussed informants’ passions, favorite watch models, and shopping experiences.

In addition, we have constructed an extensive archive of secondary data (see Table 2). We collected 149 press articles on the luxury watch industry from generalist (e.g., New York Times) and specialist (e.g., Hodinkee) publications to construct a broad picture of the industry. We also studied three market reports from leading consultancies (Boston Consulting Group, Deloitte, and McKinsey & Company) to elicit statistics and consumer insights. We then studied the websites of luxury watch brands and exchange platforms (see Web Appendix W5). On brand websites, we sought information on models and product lines. Regarding platforms, we were interested in how the trades are conducted. For both, we took notes that catered to our emerging theorization. Finally, we transcribed 87 YouTube videos from 24 watch influencers. We included all influencers mentioned by our informants and reached out to select informants for help. We sampled at least three videos per influencer (see Web Appendix W6). Here, we strived to learn how the industry tastes are shaped by the community leaders (see Humphreys and Carpenter 2018).

Our data analysis proceeded in parallel with data collection. We constantly moved back and forth between data collection, analysis, and theorization to develop codes that capture our data (Gioia 2021). We relied on the three-stage analytical procedure outlined by Corbin and Strauss (2014) (see Web Appendix W7). In the first stage (open coding), we focused on practices and representations of key market actors (i.e., brands, consumers, platforms, influencers) as well as the key properties of the goods. They have served as the basis for initial category development (i.e., buying and selling watches). In the second stage (axial coding), we sought interconnections between categories by grouping them on the basis of (dis)similarities. It allowed us to elicit the core “marketplace drama” (Giesler 2008) between the primary and the secondary markets for luxury watches. In the third stage (selective coding), we further refined our category groupings. This procedure was iterated several times in light of new data, emerging ideas, and engagement with existing literature. Eventually, we elicited the idea of enrichment privilege as the central organizing principle. It enabled us to reconstruct the enrichment process in its entirety and unite all market processes into a single theoretical framework.

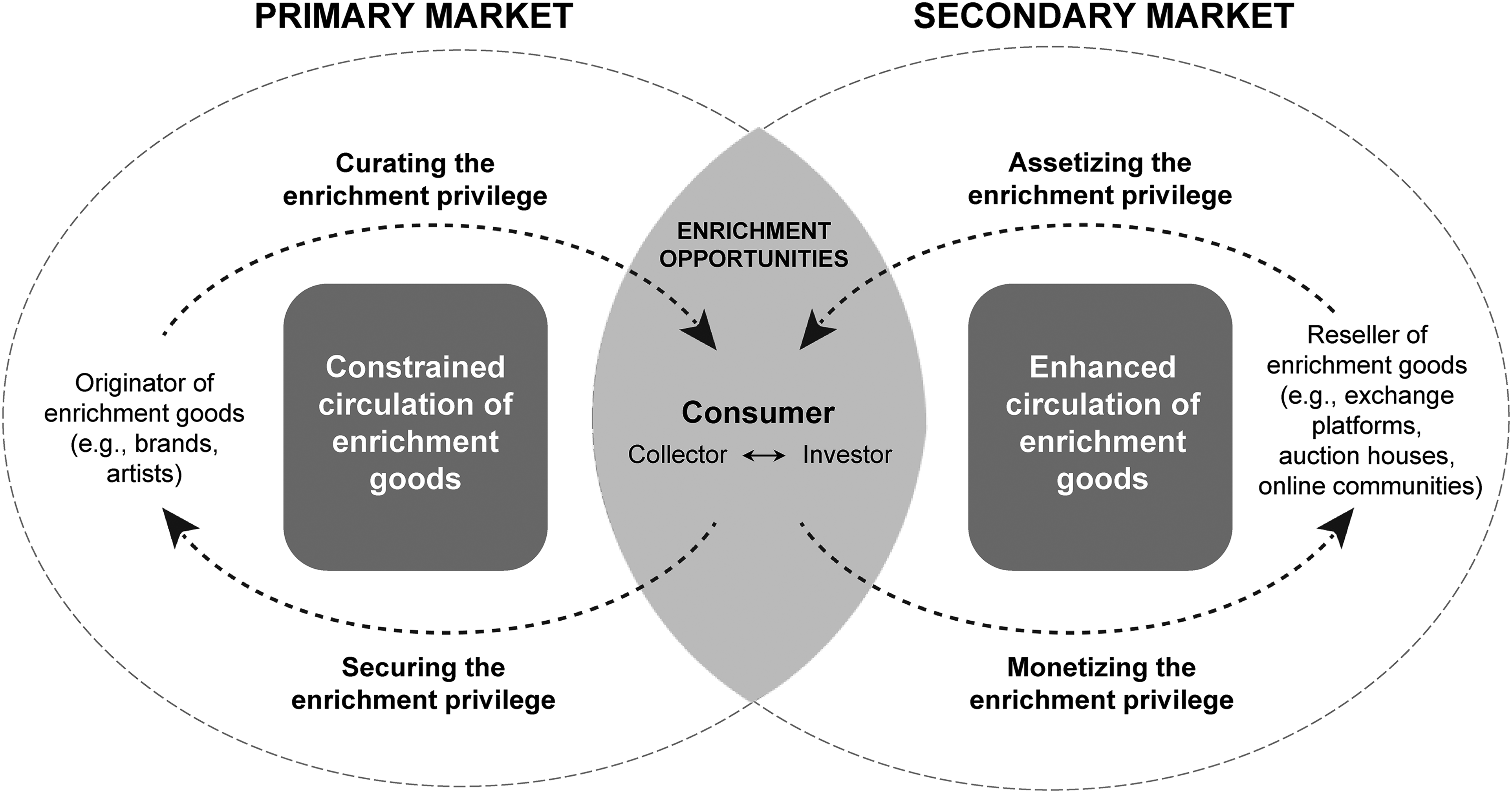

In our findings, we first outline the massive enrichment opportunities in the luxury watch market, and we introduce the idea of the enrichment privilege to capture the differential access to such opportunities. We then focus on the four market processes that sustain a market within the enrichment economy: curating, securing, monetizing, and assetizing the enrichment privilege.

The Enrichment Privilege

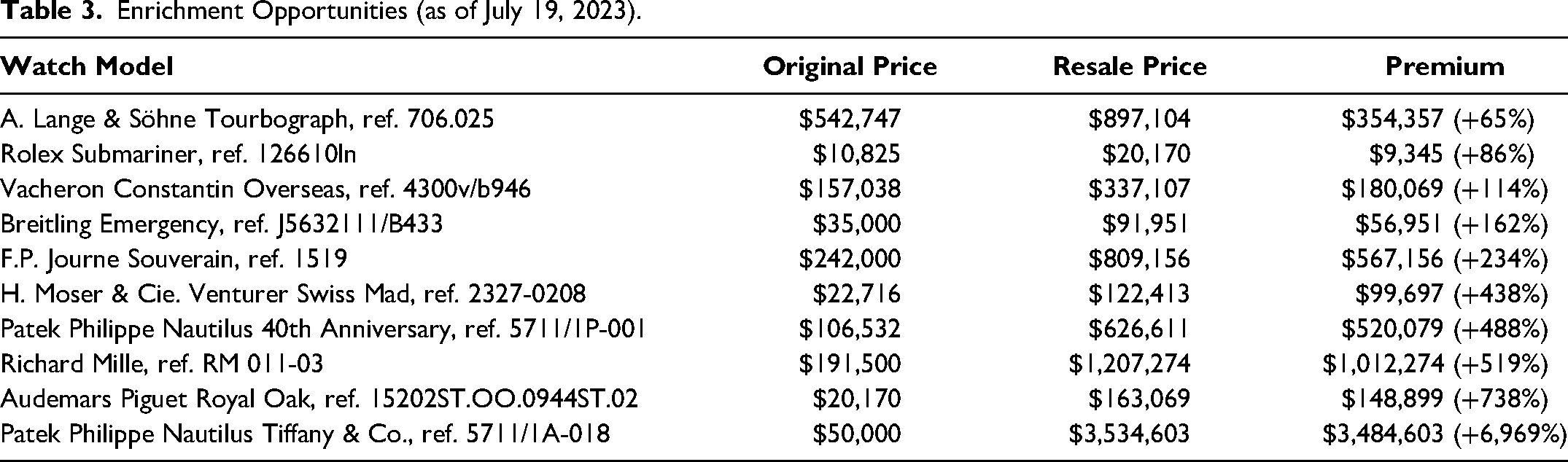

Recently, preowned luxury watches have emerged as hypergrowth investments, consistently outperforming other assets (Deloitte 2022; McKinsey & Company 2021). For instance, in the past five years, average secondary market prices for top models of Rolex and Patek Philippe have increased at an annual rate of 20%, compared with 8% for the S&P 500 (Dupreelle et al. 2023). As a result, the owners of luxury watches can realize substantial and often immediate gains in the secondary market. Table 3 highlights some of the most notable examples (see also Web Appendix W8).

Enrichment Opportunities (as of July 19, 2023).

Such price discrepancies have inverted the commonly assumed depreciation flow (whereby secondary market goods lose standing, monetary value, and desirability; Fontaine 2008; Gregson and Crewe 2003; Thompson 1979) into an appreciation flow, whereby secondary market goods have become more expensive and desirable than primary market ones. The appreciation flow has dramatically changed the consumer behavior of luxury watch clientele. First, the promise of massive financial returns in the secondary market has attracted a large pool of consumer-investors. As Anson, a manager at a watch brand, explains: One of the shifts I’ve seen in the last 15 years is when the finance guys started getting into watches. That represented a big shift, because suddenly the conversation was not just about technicality. Suddenly, it became about resale value. And then it became about research: who could get the hottest watch and who could get the best deal. And then, perhaps, in a few years, they could make a nice profit if they resell it.

The enrichment opportunities have also changed the practices and discourses of traditional watch collectors. Historically, and akin to other collectors (Belk 1995; Pearce 1998), they have been driven chiefly by personal taste. Contemporaries, however, increasingly tie their purchase decisions to financial performance. As Michael, a watch enthusiast, explains: The secondary market is like the stock market. When a watch comes out, you don’t know its real worth until it’s on the secondary market. For example, if [a brand] is selling it for $10,000, and then you see that people are selling it for $20,000, then you know that watch is worth [something]. But if [it] is being sold for half the retail price, then you know that [the brand] is putting a higher premium than what the watch is really worth.

Consequently, the secondary market price (and the corresponding enrichment opportunities) has become a leading indicator of a watch brand’s desirability. Consider Don, a watch enthusiast, as he explains the explosive rise of a particular independent watchmaker brand: There’s a vaccine for coronavirus, but there is no vaccine for the [brand F] virus. We are totally encapsulated by it. And the proof is in the money. Again, the increase in the market value is the highest for [brand F] even more than [other desirable brands]. That’s why a lot of experts think this brand will overtake [brand B] in the future.

Thus, the exploding trade in preowned luxury watches has led to the formation of a novel dominant market logic (Giesler 2008, 2012) that we call the logic of enrichment. A shared understanding (Reay and Jones 2016; Thornton, Ocasio, and Lounsbury 2012) among all market actors is that luxury watches should appreciate (or at least not lose value) on the secondary market and enable consumers to make financial gains in the long run. This logic has transformed the practices, norms, and discourses of both luxury watch brands and luxury watch enthusiasts.

However, securing “hot pieces” that would enable one to make massive financial gains in the secondary market is not easy. As Ben, a watch enthusiast, explains: I think [luxury watch] consumers are completely powerless. Even the VIPs. Because there’s literally millions of people who want the same watch. So, consumers have to work hard to foster that relationship, which is very bizarre. I see people literally begging them to let them buy, let them spend hundreds of thousands of dollars.

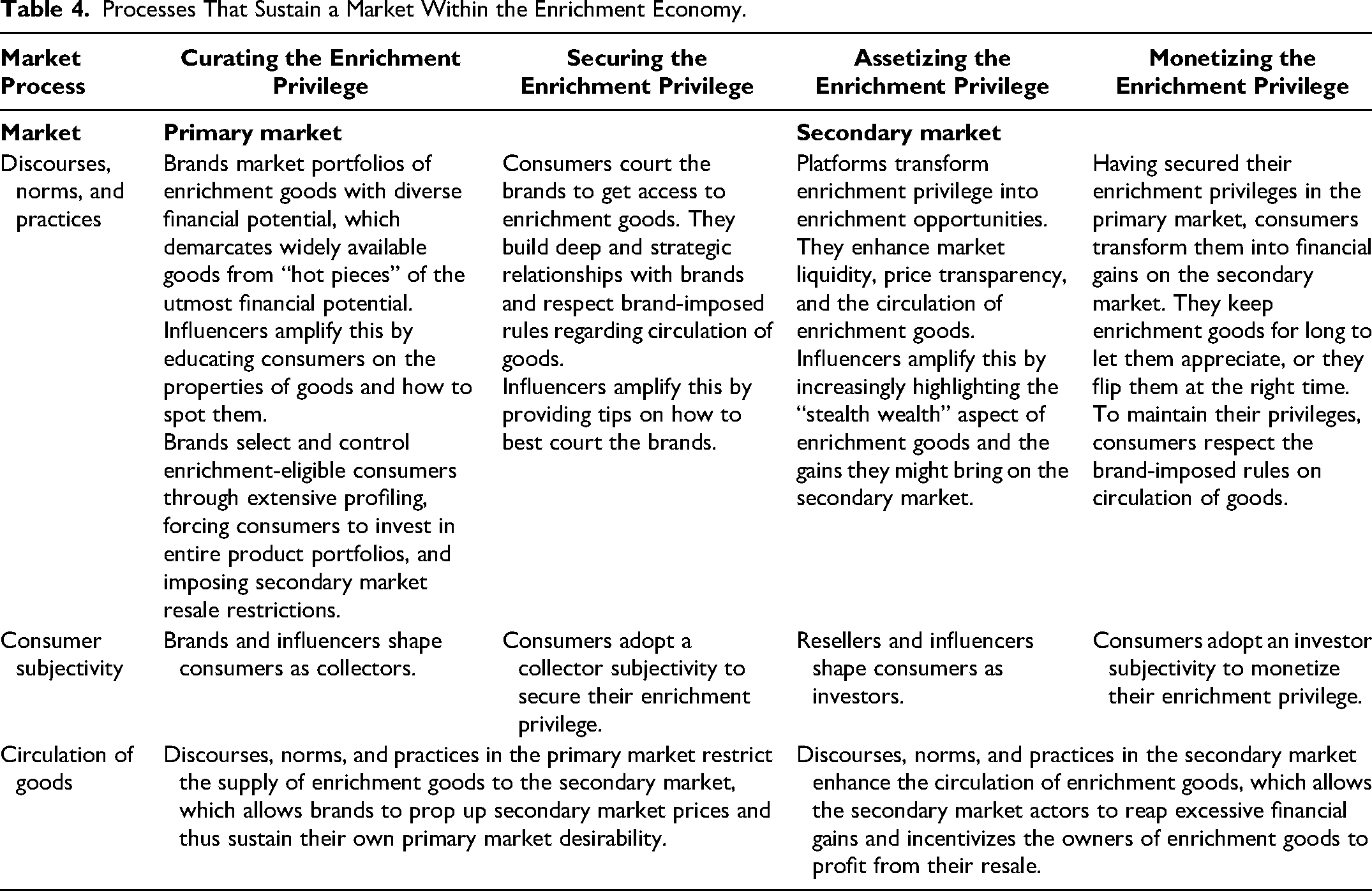

In the following sections, we explain how the enrichment privilege shapes the dynamics of an enrichment market through four key market processes: curating, securing, monetizing, and assetizing the enrichment privilege (see Table 4).

Processes That Sustain a Market Within the Enrichment Economy.

Curating the Enrichment Privilege

Brands curate the enrichment privilege by marketing portfolios of diversely enriched goods, selecting enrichment-eligible consumers, and controlling them across both primary and secondary markets.

Marketing Portfolios of Enrichment Goods with Diverse Financial Potential

Luxury watch brands physically enrich their goods by incorporating unique features. Apart from striking designs and precious materials, these brands develop unique “complications”—functions of a watch beyond time display, such as a tourbillon or a world timer. This greatly adds to the singularity (Boltanski and Esquerre 2020; see also Karpik 2010; Reckwitz 2020) of luxury watches, elevating them above mere time-telling devices.

Luxury watch brands also enrich their goods culturally by embedding them in singular narratives that elevate them above everyday “disposability” (Boltanski and Esquerre 2020, p. 211). They tie their models to iconic personalities, places, and events. Among many others, Rolex Milgauss is emblematic of this. It is a unique antimagnetic watch initially designed for the laboratory. Over the years, it has become an archetypal embodiment of scientific endeavor. Such narratives become entrenched over time, contributing to the iconic status of luxury watches. They embed watches in a timeless narrative that links the present with a glorified heritage (see Arnould and Dion 2023; Dion and Mazzalovo 2016).

Drawing on physical and cultural enrichment (Boltanski and Esquerre 2020), luxury watch brands market portfolios of goods with diverse financial potential. Most luxury watch brands carry small product portfolios with just a few product lines. Yet, each line features a vast number of “references,” or particular variations of the same model enriched to varying degrees. The presence of numerous references does not result in market fragmentation, where each segment largely pursues a specific product (Dolbec, Arsel, and Aboelenien 2022; Ertimur and Coskuner-Balli 2015). Instead, it greatly stimulates enthusiasts, who feel that owning just one reference is not sufficient and that they must continuously acquire “better” ones. As Wilson, a watch enthusiast, explains: [Brand X] changes a few things and then limits the supply. So, the original version of this [watch] is in white gold. And then, a steel version came out, on the Jubilee bracelet. But then, last year, they relaunched this version with an oyster bracelet similar to the white gold version. It’s just these very weird things where they just make you continuously purchase it.

The thirst of watch enthusiasts for references old and new is amplified by watch influencers, who take on the role of product experts (see Humphreys and Carpenter 2018). With titles such as “How to Tell If a Watch Is Well-Made” and “How Watch Brands Cut Corners” (influencer Teddy Baldassarre [2021, 2022]), consumers are taught to pay attention to the smallest of elements (e.g., case brushing) and how to spot the difference within and across brands.

Eventually, some references achieve iconic status among enthusiasts due to their scarcity and the unique combination of physical and cultural enrichment. Thus, they steadily increase their financial potential on the secondary market. As Luna, a manager at a watch brand, explains: The hardest one to get is probably our concept watches. It's basically from our dream factory. And these pieces are very limited—if not “1 of 1,” [then] “1 of 15.” It really depends on the edition. And those are pretty hard to get. Last year, we launched the first ever watch that has the highest percentage of recycled materials, almost 100%, which was a game changer. … If you have it in your collection, it means “OK, you're quite important.” And I believe—you know, many, many years from now—to have the first ever watch in the industry with this kind of mostly sustainable components … we will have a very good, you know, longevity in terms of value.

In sum, luxury watch brands market diverse portfolios of enrichment goods. The most singular ones, characterized by their rarity and their physical and cultural enrichment, often hold the highest financial potential. In doing so, luxury watch brands establish the foundation for curating the enrichment privilege by marketing enrichment goods with differentiated financial potential.

Selecting Enrichment-Eligible Consumers

Only a small number of consumers get the privilege of acquiring enrichment goods with the highest financial potential. To select such enrichment-eligible consumers, the brands practice extensive consumer profiling and force consumers to invest in the entire product portfolio.

Consumer profiling

Luxury watch brands are very selective in choosing customers who get access to the “hot pieces” with the highest financial potential. In playing their role as curators of enrichment privileges, they look for enthusiasts who value long-term ownership, and they avoid speculators who flip watches the next day. Unrestricted and quick speculation may damage the secondary market performance of enrichment goods by preventing them from appreciating, which in turn negatively impacts the primary market desirability of these goods. As Matthias, a sales manager at a leading luxury watch brand, explains: Since I’ve been with [Brand A], I no longer have the same job. Because when I was at [Brand B], I tried to sell. Today, I am selecting the client to whom I want to sell to, and I avoid clients who are going to buy a watch just to resell it and fuel speculation. So, it’s really trying to understand the profile and psychology of the person.

Therefore, luxury watch brands normatively and explicitly engage in extensive consumer profiling to identify trustful watch enthusiasts and weed out speculators, such that only the most trustworthy ones are granted the enrichment privilege. As Paul, a manager at a luxury watch brand, explains: It’s our job to identify the people we want to sell our watches to. … You should be interested in the brand, the partnership, and our history. The first question we ask is, “Why do you want it?” It’ll be like an interview. They ask you questions about the watch: design, movements, the history. But of course, the most important is the understanding of having to wait. We know who you are, we know your values and strengths, and one day, we want to sell to you. … We don’t want to make it easy.

Forcing consumers to invest in the entire product portfolio

The more financial potential a given watch has, the more exclusive the allocation list. To get access to the “hot pieces,” consumers are forced to invest in the brand’s entire product portfolio, including the enrichment goods of lower financial potential. As Dominic, a manager and an enthusiast, explains: [At brand K], the first watch you buy is [watch C, an entry-level model]. The second watch must be a complication watch, [like] a chronograph. … There’s a hot watch that I want. They’re telling me I can get it as my third watch. Then I ask, “What about the other hot pieces?” The [watch N], right? So, [it] will be like my fifth or sixth watch. [With brand K], you have to spend money on watches you didn’t really like to get the one you want. [At brand F], you have to spend almost €200,000 just to buy a €30,000 watch because that’s the piece everyone wants. In the most blatant sense, that is how you prove you’re a good customer.

In sum, luxury watch brands carefully select consumers who get the privilege of acquiring enrichment goods of the highest financial potential. To grant this privilege, brands engage in consumer profiling and force consumers to invest in low-potential enrichment goods first. In doing so, they restrict the circulation of enrichment goods, which contrasts with other contexts where companies strive to increase goods circulation to expand their customer base (see Figueiredo and Scaraboto 2016).

Controlling Enrichment-Eligible Consumers

Besides selecting enrichment-eligible consumers, watch brands strive to control their activities in the secondary market. This further limits the supply of “hot pieces” on the secondary market, which allows brands to sustain both the secondary market prices and their own primary market desirability. Brands control enrichment-eligible consumers by shaping the subjectivity of consumers as collectors and by enforcing secondary market resale restrictions.

Shaping the subjectivity of consumers as collectors

Luxury watch brands strive to shape the subjectivity (or self-understanding based on experience; see Hall 2004) of their clients as collectors, because collectors tend to hold on to the goods for extended periods of time (Belk 1995; Pearce 1998). Brands invest in extensive education to cultivate consumers as collectors. The sales staff is trained to explain each model’s origins and heritage. It is essential, as collectibles thrive on storytelling (Thompson 1979). As Yohan, a manager, explains: There is much storytelling around each piece. As a brand, you have to edit books about your history, because collectors need complete information. If you look at the brand with the biggest base, it is [brand K]. How many books have been written about each piece with every little detail? These resources are useful. You need to write that history and make it available. Without strengthening our past and our icons, it’ll be difficult for us to get it right.

By educating watch enthusiasts in this way, the industry makes a long-term investment that pays off over time. As Fabio, the CEO of a watch auction house, explains: The goal of auctions is to raise the level of collectors, because the more educated he is, the more sensible he is. And the more willing he is to spend money. Because he learned what to look at on the watch. … When you spend time on educating people, it’s not a 100% loss, because it is an investment. You get it back a long, long time after. Maybe they don’t spend at your auctions, but that is important.

In addition, brands elevate the memorial power (the capacity of objects to evoke strong memories; Boltanski and Esquerre 2020) of enrichment goods they sell. The memorial power of collectibles is already strong, since collectors often connect their purchases with life’s precious moments (Belk 1995; Pearce 1998). Yet, we find that luxury watch brands strive to elevate it even further. As Don, a watch enthusiast, explains: [This watch] came through an auction in partnership with [a well-known museum]. The winner would get a unique piece from [a leading brand]. We’d get to pick any artwork, and they would engrave it. So, my father and I won. We’ll spend the first two days at [the brand’s HQ] [with] the head of client management. He’ll show us [around]. We'll get a tour of the manufacturing and the private salon. We’ll also meet the man who’ll be making our piece. We’ll have the entire museum to ourselves with a curator, and we’ll spend the day picking the artwork. It will be so in demand that we will probably just flip it immediately.

While Don’s experience represents an extreme case, we find his testimony emblematic of the informants’ experiences. At luxury watch boutiques, customers are immersed in a microcosm of high-end watchmaking that features a highly knowledgeable sales force, crisp service, and spacious environments. Should consumers profess interest in rare pieces, they are immediately ushered to a more exclusive area and served fine champagne. There, they are privy to rare references not showcased in the main area. All of this creates memorable experiences for enthusiasts that strongly contribute to their passion for long-term ownership. In turn, this reduces the secondary market supply of enrichment goods, bolsters the brands’ primary market desirability, and makes consumers yearn for their enrichment privileges.

Enforcing secondary market resale restrictions

Beyond the point of sale (see Dion and Arnould 2011; Dion and Borraz 2017), the power of luxury watch brands extends to the secondary market. Brands carefully monitor it to ensure that recently acquired watches with high financial potential are not being flipped. As Kayden, a market expert, explains: A lot of brands will dedicate resources to look at the secondary market to make sure that their pieces are not being resold because they do not want to be known as the brand that is just making pieces, hyping them up, and then no one actually loves them. That is the wrong progression for a watch brand to grow. They want people [who] really love it, and they are loyal, and they look forward to buying the next [piece].

The chief “punishment” for betraying the brand’s trust is the loss of the enrichment privilege. As Dominic, a manager at a leading luxury watch brand, explains: I was doing an audit for some [of our] pieces, and I saw one of our limited-edition watches [online]. Usually, when this model has popped up before, the poster has done a good job of covering the serial number. But in this listing, the number was revealed. So, I was instructed to report this to the commercial team [to] investigate. [So, the customer was blacklisted?] Yes. But that depends. Some brands have very strict blacklist rules. Some brands are more tolerant. So, it really depends, but it is safe to say that the [brands] love it. There is no first chance. You do not get a warning. It is an immediate blacklist. It is like the Mafia. Let’s say you’re friends with a Mafia member, and let’s say that he says good things about you. You might be happy that, oh, you are getting complimented, but you are kind of scared because it is someone of that reputation that is speaking about you. That is kind of what the atmosphere is, like, between [brands] and [consumers].

Still, luxury watch brands prescribe grace periods, after which it is safe to resell watches without losing enrichment privileges. The average period is three to four years, although it may go up to ten years (and more) for the most enriched pieces. After that, a given watch has generated enough enthusiasm to essentially guarantee its financial potential and the brands’ resulting desirability.

In sum, luxury watch brands curate their customers’ enrichment privileges. First, they market diverse portfolios of enrichment goods that clearly differentiate enrichment goods of lower (easy to access) and higher (hard to access) financial potential. Second, they select enrichment-eligible consumers by profiling them and prompting them to invest in the brand’s entire product portfolio before they get access to the “hot pieces.” Third, they control enrichment-eligible consumers by shaping their subjectivities as collectors and enforcing secondary market resale restrictions. It allows luxury watch brands to control the entire enrichment process, since they are in a position to control the distribution of the enrichment privilege and restrict the circulation of enrichment goods. It also contributes to the maintenance and growth of prices on secondary markets, since the supply of enrichment goods is tightly controlled by the brands. In turn, this props up the primary market, the desirability of which is increasingly tied to the secondary market performance.

Securing the Enrichment Privilege

Consumers play the “enrichment game” and navigate strategically between primary and secondary markets. The goal is to secure the enrichment privilege and then capitalize on it by reselling the watch or keeping it as an asset. However, securing “hot pieces” is not easy. This creates an inverted selling relationship where luxury clients are no longer kings (see Bhatnagar et al. 2023), but mere prospects who fight for their enrichment privilege. This privilege includes the purchase itself. But it also includes access to information (i.e., which references will be available shortly), getting on allocation lists, and even “jumping the line.”

Thus, luxury watch enthusiasts engage in extensive courting behavior that brings them closer to obtaining the enrichment privilege. As Kayden, a watch industry expert, explains: Once in a while, you drop in and say “hi.” You say: “Well, what do you have?” And they say: “Okay, here are some pieces.” And then you just buy that as well. And then, you obviously behave well. You know, I think they also want people who are not nasty people who will just troll their way around. They want nice customers.

We observe that watch enthusiasts are highly strategic about how they secure their enrichment privileges, because not playing the game “just right” may severely damage their chances of getting a brand new enrichment good. For instance, consider Brian, a young enthusiast, who had recently attempted to purchase a highly enriched watch: [The sales rep] knew right away I’m not here by accident. I wasn’t a kid who wanted to get something flashy. So, we’re talking about movements, [etc.]. We’re vibing a little bit. We spent like an hour talking. It’s just easier when you are familiar with the brand. [And], the first thing they look at is your watch. So, I wore a watch that looked expensive. That was the hook. They wanted to talk to me.

Watch influencers play a crucial role as they often post tips on how to behave when buying a luxury watch. With titles such as “How to Buy a Rolex Watch at Retail Price from ADs (5 Tips)” (influencer KC Time Share [2022]), consumers are taught to “play the game” by “showing interest,” “spending time with the sales associate,” and “being genuine,” among others.

Client–brand relationships in our context are highly instrumental. The degree of the enrichment privilege bestowed by the brand is proportional to the amount of personal courtship and spending on consumers’ behalf. As Yohan, a manager, explains: Of course, the more you buy, the closer you get to the salesperson. And then you have a personal relationship, which is, you know, “how much time do you spend [developing it]?” But this relationship is always in relation to how much you have spent in that boutique to acquire a VIP [status] or to get to the head of the queue or to jump the queue and things like that. It’s always either because you know the person or you are a friend of the owner.

As Yohan mentions, the most exclusive relationships are with the “owner” or other top managers of the brand. In terms of privilege, this is akin to lords who are personal friends with the king (Elias 1983). Such relationships take years of spending and courting to build, but they guarantee access to enrichment goods of the utmost potential. They also highlight the social inequalities inherent to the market system of enrichment, since they may often follow a path of corruption and cronyism. Consider an anecdote from Andrew, a watch enthusiast: [My friend] was buying a [watch from a brand], and he could not get it. So, he called our friend, who called the CEO of [the brand]. And the CEO had to make the call to get that particular watch. He can [also] give him a discount, right? But, the privilege was not the discount. The privilege was getting it. Because if he did not have that connection, you are probably on, like, a two-year waiting list.

In sum, because luxury watches of the highest financial potential are almost impossible to get, consumers engage in extensive courting behavior. It is an inverse selling relationship in which consumers are mere prospects fighting for their enrichment privileges. They strategically build deep relationships with brands. Knowing this, luxury watch brands scale the degree of the enrichment privilege they bestow with their customers’ involvement. Consumers have to court brands to get access to the enrichment goods of increasingly higher financial potential.

Assetizing the Enrichment Privilege

The secondary market assetizes the enrichment privilege by transforming it into enrichment opportunities. It enhances the liquidity and transparency of the preowned watch trade and shapes the subjectivity of consumers as investors, which greatly expands the circulation of enrichment goods on the secondary market and prompts enthusiasts to capitalize on their possessions.

Enhancing Market Liquidity and Transparency

Due to their physical properties, luxury watches make perfect assets. Made mostly with precious and durable materials, they are not easily damaged. And they are easy to transport discreetly, both physically and legally.

However, the secondary watch market further assetizes the enrichment privileges by presenting itself as a liquid marketplace akin to a stock exchange. First, it has greatly enhanced market liquidity. Historically, preowned luxury watches have been traded privately (Donzé 2011). Today, a growing number of dedicated sites offer a chance to buy and sell watches across the globe. The secondary luxury watch trade has become its own industry, with thousands of preowned watches traded each year (McKinsey & Company 2021). Furthermore, the secondary market contributes much to price transparency. As Alan, a watch market expert, explains: [Platform C, a leading exchange platform for preowned luxury watches] was a major change in the industry, because it made its pricing transparent, and it became an index for secondhand [watch] values. And that was a catalyzing factor in the industry. It is very similar to the [diamond business]. In the ’70s, they started creating indexes for diamond prices, and it made the market very transparent.

In addition to that, the secondary luxury watch market has drastically reduced the quality uncertainty commonly associated with secondary markets (see Fontaine 2008; Sherry 1990). It has done so by offering a range of services that foster a safe trading environment, including escrow, watch authentication by professional watchmakers, and insured shipment.

All these developments have imbued preowned luxury watches with qualities of liquidity and transparency characteristic of assets. This platform’s practices have two effects on the secondary market. First, it creates an infrastructure necessary to transform enrichment privileges into enrichment opportunities. Second, it greatly enhances the circulation of preowned enrichment goods, turning them from dormant collectors’ goods into liquid and trade-friendly assets.

Shaping the Subjectivity of Consumers as Investors

To further assetize enrichment privileges, the secondary market constructs the subjectivity of consumers as investors. It provides performance indexes and portfolio management tools that mimic financial markets and prompt consumers to make investment-like decisions. Consider WatchCharts, a service offering “market insight for watch collectors”: WatchCharts Market Ratings are measurements of a watch’s performance relative to the overall market. Each rating is represented on a scale of 0–99. For each watch, we provide four market ratings: Overall, Growth, Liquidity, and Predictability. Each Market Rating indicates if the watch is outperforming, aligned with, or underperforming the secondary watch market, or with respect to the specific category. It is entirely data-driven and serves as a quick indication of how “hot” a watch is compared to the market at large. (WatchEnthusiasts 2022)

This assetization is also reinforced by influencers that increasingly act as market gurus. For instance, consider Kevin O’Leary, the star of Shark Tank and a prominent watch influencer: I’ll tell you something really interesting about this watch. It’s very hard to find, but again, when you're building a collection, that’s not what you care about. … Why? Let’s look at the economics that’s driving this. The purchase price of this watch is $31,373. It’s a lot, but it is a good investment. Oh yes my friends, what are these trading for right now in the open market? $72,295. That's a 123% appreciation. That’s what I’m talking about: you can build your collection and, at the same time, make great investments. (O’Leary 2019)

In sum, the secondary market has transformed the preowned luxury watch trade into a marketplace akin to a stock exchange. It has done so by greatly enhancing the liquidity of preowned luxury watches, fostering price transparency, and providing analytical services that prompt consumers to trade watches as financial instruments, all of which greatly contribute to enhanced circulation of enrichment goods on the secondary market.

Monetizing the Enrichment Privilege

The few consumers who manage to secure their enrichment privileges can expect a multitude of personal gains. They can get access to an exclusive club of high-net-worth watch enthusiasts, which contributes to their social distinction struggle. They can position themselves as wealthy individuals with “expensive” taste. And they can simply let their watches appreciate and pass them on as inheritance. Consider the words of Gustav, an enthusiast: I started looking at higher-end stuff. I went into Patek Philippe, and then Audemars Piguet, and now I’m more focused on Rolex. So basically, I ended up restraining myself to watches that are quite valuable, interesting historically and, you know, from a market perspective, without trading at the [retail] price.

Most directly, though, enthusiasts can adopt a more speculative subjectivity and make massive gains by flipping the watches at the right time. Consider the words of influencer and professional “watch flipper” Phil Reid: The guy I’m meeting has already made $1 million off of his watches. He’s invested around $1.5 million. But, where else can you invest $1.5 million and get $1 million back [in 6 months]? If the salespeople like you, they will give you watches. Buying watches from an A.D. [authorized dealer] is not cheap, but it’s a cheaper way to do it. … Don’t go into the A.D. saying “I want a Pepsi” [a nickname for a Rolex reference]. They’ll take you a lot more seriously if you actually say the reference number and explain the reasons why you’re interested in that watch and how it fits your lifestyle. Play the game, guys. (Reid 2022)

Discussion

Our ethnography of the luxury watch market shows the four processes that sustain an enrichment market. Brands curate access to enrichment goods on the primary market. They grant the privilege of acquiring the best enrichment goods to a small and well-vetted group of consumers who are incentivized not to resell their watches. Doing so, they constrain the circulation of enrichment goods to secondary markets. In the meantime, the secondary market actors assetize enrichment privileges by highlighting their worth as assets and fostering market transparency and liquidity, which enhances their circulation. In turn, consumers of enrichment goods adopt a collector–investor subjectivity and navigate between the two markets to build their portfolios. They secure their enrichment privileges in the primary market by strategically courting the brands, and then monetize them on the secondary market as both short-term speculators and long-term investors. These processes contribute to a complex circulation of enrichment goods that turn enrichment privileges into enrichment opportunities (see Figure 1). This research makes four contributions to marketing literature.

The Market System of Enrichment.

Primary–Secondary Market Dynamics

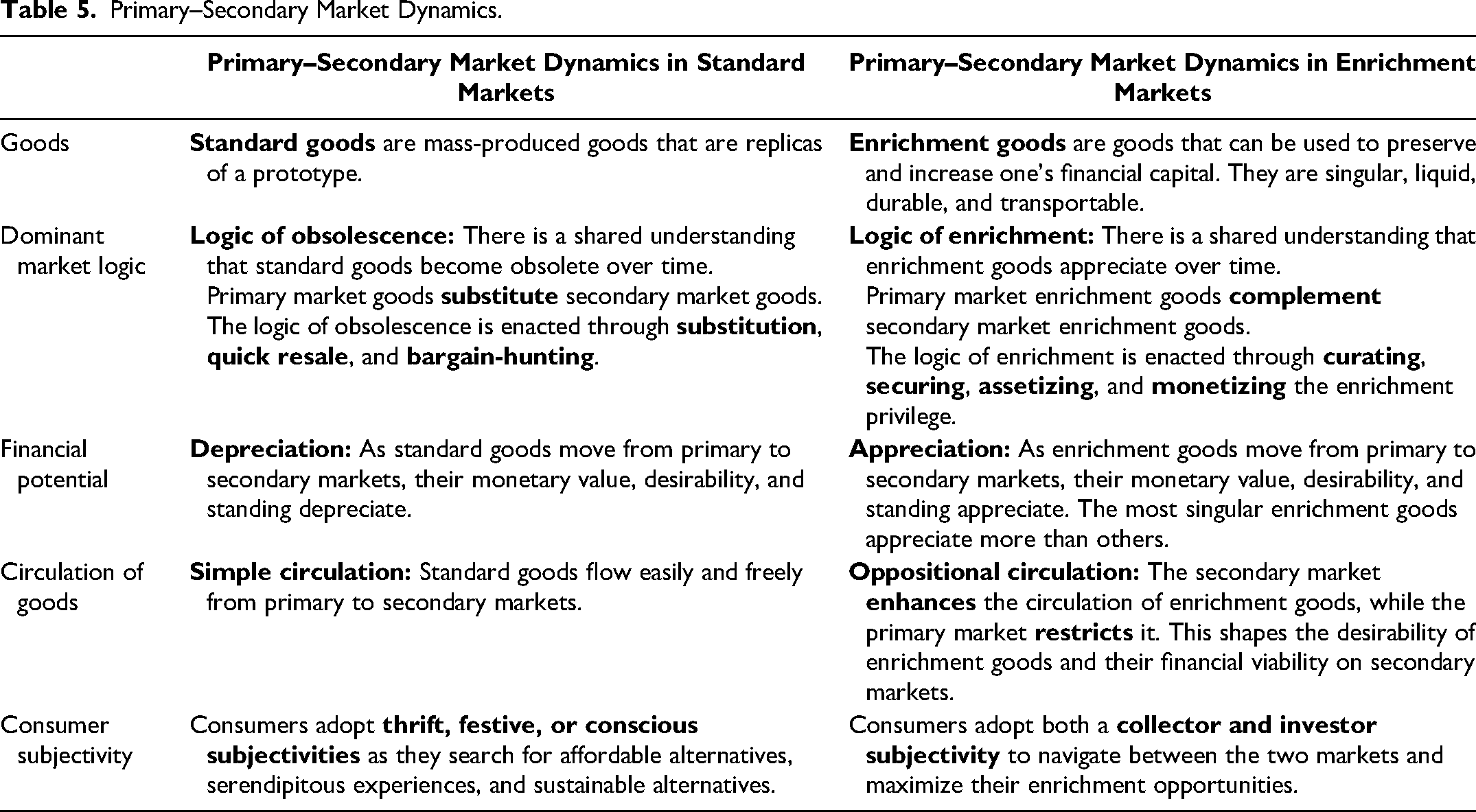

Over the years, the MSD tradition (Giesler 2008, 2012; Giesler and Fischer 2017) has explored various market dynamics as they relate to space (Castilhos, Dolbec, and Veresiu 2017), time (Parmentier and Fischer 2015), and competition (Ertimur and Coskuner-Balli 2015), among others. We contribute to the MSD literature by highlighting primary–secondary market dynamics—that is, the dynamics that structure the exchange across primary and secondary markets. We demonstrate that the exchange across primary and secondary markets is governed by dominant market logics and performed through interrelated market processes that are informed by discourses, norms, and practices shared by key market actors. It impacts the nature of circulation of goods across the two markets, the subjectivity of consumers that populate them, and, consequently, the financial and symbolic values on secondary markets (see Table 5).

Primary–Secondary Market Dynamics.

Standard markets

Standard markets deal in standard goods, or mass-produced and exchangeable goods that are replicas of a prototype (Boltanski and Esquerre 2020). The secondary market actors in standard markets thrive on festivity (Belk, Sherry, and Wallendorf 1988; Sherry 1990), thrift (Fontaine 2008; Gregson and Crewe 2003), and sustainability (Hansen and Le Zotte 2019; Machado et al. 2019).

The dominant market logic that captures the primary–secondary market dynamics on standard markets is the logic of obsolescence. A shared understanding (expressed in discourses, norms, and practices; Reay and Jones 2016) among all market actors is that standard goods become obsolete over time because of new technology, design, fashion, and so forth. Thus, brands focus on the continuous substitution of existing goods by new and more advanced goods. Secondary market actors realize that their window of opportunity is small and ever-shifting, because the goods are rapidly substituted. Thus, they focus on the quick resale of goods at a discount. Consumers adopt thrift, festive, or conscious subjectivities and mediate between the primary and the secondary market to bargain-hunt in search of affordable alternatives, serendipitous experiences, and sustainable alternatives, respectively.

Therefore, goods in standard markets follow a depreciation flow in terms of their financial potential, where the transfer of goods from primary to secondary markets lowers their monetary value, standing, and desirability (Fontaine 2008; Gregson and Crewe 2003; Thompson 1979). The circulation of standard goods from primary to secondary markets is easy and free, in the sense that it is unrestricted in any way by any of the market actors, which contributes to their depreciation on secondary markets. However, most standard goods become obsolete and depreciate so fast that they do not even move to the secondary market.

Enrichment markets

Enrichment markets deal in enrichment goods, that is, goods that can be used to preserve or increase one’s financial capital. They possess exceptional singularity, liquidity, durability, and transportability (Boltanski and Esquerre 2020). The secondary markets of the enrichment economy resemble a stock exchange in terms of their presentation and functionality (e.g., Chrono24). They enable owners of enrichment goods to transform their enrichment privileges into personal enrichment opportunities.

Thus, the dominant market logic that captures the primary–secondary market dynamics on enrichment markets is the logic of enrichment, a shared understanding expressed in discourses, norms, and practices (see Reay and Jones 2016) that enrichment goods appreciate over time, including after their transfer from primary to secondary markets. Performed through the interrelated processes of curating, securing, assetizing, and monetizing the enrichment privilege, the logic of enrichment creates a symbiotic relationship that sustains a market within the enrichment economy. Thus, enrichment goods on both primary and secondary markets do not cannibalize each other. Instead, they complement each other, since both are singular enough, and both are used concurrently by consumers to maximize their enrichment opportunities.

Therefore, enrichment goods follow an appreciation flow: They gain in standing, monetary value, and desirability long after the original purchase. This flow is sustained by the continuous interest of enthusiasts who compete for increasingly rare enrichment goods. This flow is oppositional. On the one hand, secondary market players enhance goods circulation by fostering the liquidity and price transparency of enrichment goods and highlighting their worth as assets. On the other hand, brands produce enrichment goods with the highest potential in limited quantities and impose restrictions on the resale of enrichment goods. This oppositional circulation of goods between markets creates shortages in the secondary market, which triggers their desirability and long-term financial viability.

Arguably, the logic of obsolescence is present in most standard markets. The logic of enrichment, however, depends on two additional conditions. First, it depends on the presence of a highly organized, continuous, and centralized secondary market that fosters liquidity and transparency and eliminates the challenges of quality uncertainty and fraud associated with preowned goods (Fontaine 2008; Sherry 1990). Thus, it may not appear in contexts with disorganized and opaque secondary markets prone to fraud and uncertainty.

Second, it depends on the power of brands in the industry. By their desirability and their status and the nature of their distribution network (proprietary stores and tightly controlled authorized dealers), luxury brands have enough power to effectively control the entire enrichment process. This may not apply in other industries where brands do not enjoy the same level of power and control over other stakeholders.

Transferability

Enrichment goods tend to be singular (i.e., unique in terms of their physical and cultural properties), liquid (i.e., easily convertible into cash), highly durable, and transportable (i.e., easy to move across borders and tax regimes) (Boltanski and Esquerre 2020). Thus, the market dynamics of enrichment can appear, to a different extent, in markets that deal in similar goods.

Following mass media reports about skyrocketing secondary market sales across a range of categories such as luxury leather goods (e.g., the infamous Birkin bag by Hermès), elite wines and spirits (e.g., Macallan 1926 Fine & Rare whisky), and sports cars (e.g., 1955 Mercedes-Benz 300 SLR Uhlenhaut Coupé), we believe our findings to be fully transferable to other luxury markets. The singularity of luxury goods is based on their rarity, heritage, and craftsmanship and the iconicity of brand founders and creative directors (Arnould and Dion 2023; Kapferer 2015). Today, many of them trade prominently on secondary market platforms such as Vestiaire Collective and The RealReal. We observe similar dynamics on such markets, where consumers strive to secure and monetize their enrichment privileges, which brands curate and the secondary market assetizes.

Artworks and antiques are the most enduring examples of enrichment goods (Boltanski and Esquerre 2020). Ultrawealthy consumers are always looking for ways to preserve and increase their wealth, of which artworks and antiques seem an obvious choice for many (Boltanski and Esquerre 2020). Artworks and antiques are singular in essence (Karpik 2010; Reckwitz 2020), and some appreciate for centuries (Velthuis 2005). The logic of enrichment is present in such markets, since there is a shared understanding among all market actors involved (e.g., ultrawealthy consumers, museum and gallery curators) that the goods do and should appreciate. Similarly, the notions of monetizing and assetizing fully hold, since we observe extensive and dynamic secondary markets for artworks and antiques. At the same time, the curation and securing of enrichment privileges are likely to take a different shape. Museums, artists, or gallery curators may not be able to impose resale restrictions in such “behind closed doors” settings. Except for highly celebrated artists, they may not be able to select enrichment-eligible consumers. Thus, while the general logic of enrichment is present in art and antiques markets, the particular supply-side mechanics of such markets may be different.

Last, mass-market goods can also become enrichment goods if they are singular enough, which is usually the function of their limited or irregular supply. For example, the “Cloud City” Lego set was released in 2003 in limited quantities at $80 apiece. In 2023, it was reselling for around $10,000, signifying a 11,200% premium (BrickEconomy 2023). Other examples include trading cards, toy collectibles, or limited-edition sneakers from mass-market brands. Based on this and similar observations, the enrichment economy within standard markets is sporadic and infrequent. Furthermore, enrichment goods in standard markets are allocated either on a “first come, first served” basis or randomly (e.g., in the case of trading cards). Thus, the notion of securing enrichment privileges may not be as salient. At the same time, given the explosive growth of certain standard goods with a strong enrichment effect (e.g., select Lego sets), the notions of monetizing and assetizing enrichment privileges are fully applicable.

Luxury Brands as Enrichment Curators

The most salient challenge for luxury brand management is status maintenance, for both brands and their clients (Bellezza 2023; Dion and Borraz 2017; Humphreys and Carpenter 2018). We show, however, that the enrichment economy brings forth a new challenge for luxury brands. They have to allow consumers to make financial gains in the secondary market while enhancing their own primary market revenues and desirability.

We show that luxury brands successfully meet this challenge by becoming enrichment curators. They create a complex network of interdependencies that reinforce their own market power while prompting consumers to continuously court them in pursuit of their enrichment privileges. This resembles the distribution of royal privileges at royal courts, especially at the Palace of Versailles in the 17th and 18th centuries. The term “royal privilege” refers to the special rights and advantages that the French kings granted to their courtesans. Elias (1983) demonstrates that courtesans who lived at Versailles were entrapped in a web of social and financial obligations before the king. It fostered a highly competitive, stratified, and rigid environment. Thus, the courtesans’ status depended fully on the king’s favor, and courtesans were constantly compelled to gain such favors, competing with each other for the king’s attention. This culture transformed Versailles into a golden prison, which enabled the king to maintain his power over his subjects (Elias 1983).

First, as enrichment curators, luxury brands originate highly desirable and status-signaling enrichment goods. By marketing diverse portfolios of goods enriched to various degrees and by carefully monitoring their supply to the primary market, they foster the perception that some goods are more desirable than others. In turn, this fosters the idea among luxury consumers that attaining a higher status means attaining increasingly exquisite goods that, by design, come in increasingly shorter supply.

Second, luxury brands make enrichment goods increasingly harder to obtain by screening their customers for enrichment eligibility. They distribute the enrichment privilege unevenly, such that only a small proportion of the luxury clientele gets it. To be successful, customers first have to invest in a brand’s entire product portfolio to signal their material wealth. They must also signal a deep knowledge of the brand. This ties customers to the brand from an experiential and emotional perspective, as they are prompted to perpetually refine their understanding of and commitment to the brand in order to impress the brand’s sales force enough to secure and maintain their enrichment privileges.

Third, luxury brands control their customers’ enrichment privileges beyond the point of sale. They enforce strict resale restrictions that scale with the level of a given item’s physical and cultural enrichment. The most enriched pieces are the hardest to resell: Consumers have to wait for longer periods (often in excess of ten years), and some of our informants even recalled calling the brand’s sales associates to make sure that the resale is allowed. The “violators” are swiftly punished, and their enrichment privileges are taken away. This type of control further ties customers to the brand, since they are perpetually afraid of losing their hard-earned enrichment privileges.

Some informants are frustrated with the inner workings of the enrichment economy. However, we observe that most of them still enjoy playing the enrichment game because of the sheer number of perks that it may bring them if they play it right. Thus, in surviving the ordeals of securing and maintaining their enrichment privileges, many enrichment-eligible consumers resemble the courtesans who would go out of their way to serve the king. And luxury brands resemble the king himself, who entraps his subordinates in a perpetual cycle of (increasingly harder to fulfill) obligations (Elias 1983).

In serving as enrichment curators, luxury brands effectively control the enrichment economy within their markets, such that other market processes within the enrichment economy become dependent on them. Getting access to enrichment goods of increasingly higher financial potential is impossible without courting the brand in just the right way imposed by the brands. In turn, enduring the ordeals of securing one’s enrichment privileges prompts consumers to monetize them on secondary markets, which thrive by prompting consumers to sell and resell their possessions in a manner akin to stock exchange.

By serving as enrichment curators, luxury brands also perpetuate the enrichment economy and prevent it from failing. Indeed, some quasi-enrichment markets (e.g., NFTs) are sporadic, unorganized, and prone to sudden crashes. This is because such markets are based on unrestricted secondary market speculation that falls beyond anyone’s control. In contrast, luxury markets in enrichment goods are highly organized and tightly controlled by brands as enrichment curators. Their stability and growth depend on the ability of brands to impose hard-to-challenge discourses, norms, and practices on other market actors.

All of this puts luxury brands in a position of strength. Previous research on the power of luxury brands highlights their ability to shape consumer tastes (Dion and Arnould 2011; Humphreys and Carpenter 2018) and subjectivities (Dion and Borraz 2017) to their standards. In contributing to these findings, we show that luxury brands further reinforce and legitimize social inequalities by originating, distributing, and controlling the enrichment privileges of their customers. These actions create a vicious (yet highly profitable) cycle of exclusivity, where consumers are prompted to court and spend more and more to get access to the latest enrichment goods of the highest financial potential. This is the essence of the emerging role of luxury brands as enrichment curators.

Ethics of the Enrichment Economy

Following Boltanski and Esquerre (2020), we discuss the ethical dimension of the enrichment economy. We highlight the social and environmental externalities that the enrichment economy may foster. We suggest public policy remedies that address them.

Tax evasion

Boltanski and Esquerre’s (2020) original treatment of the enrichment economy is critical in nature. They capture its existence and growing prevalence, but their principal aim is to expose the enrichment economy as an exclusive club for the super-wealthy that generates secret transactions that cannot be taxed or traced. Consequently, they see it as an unjust economy that stands on the backs of countless workers (i.e., artisans) while actually enriching only those at the very top (i.e., consumers that resell artisans’ work at massive premiums). They suggest redistributing the wealth generated by the enrichment economy by taxing enrichment transactions and compensating the relevant workers at a higher level.

We join Boltanski and Esquerre (2020) in calling for a more efficient taxation of the enrichment economy. We observe that many consumers purchase enrichment goods as alternative investments and, sometimes, for the sole purpose of hiding their wealth in seemingly insignificant objects that can be easily moved to tax havens. The goods are then resold privately, providing opportunities for massive tax evasion.

We also believe that a public system that keeps track of enrichment goods is warranted. Such a system will make it more difficult to trade in enrichment goods behind closed doors. Among others, it may prevent a situation where a prominent individual passes away, but transfers some of their wealth into enrichment goods and then passes them on stealthily, so that the heirs are able to avoid paying the inheritance tax. Therefore, policy makers could develop a system to track enrichment goods. This can be managed by blockchain certificates that preserve one’s purchase record and that can be sent to authorities when the goods are resold.

In addition, policy makers should reinforce customs surveillance to prevent enrichment goods from navigating secretly across borders. For instance, Arnold Schwarzenegger was recently detained in Austria for failure to declare a one-of-a-kind “Terminator” Audemars Piguet watch at customs (Slow 2024). This particular watch was destined for a charity fundraising event, but it is easy to imagine that enrichment goods (especially small and seemingly inconspicuous ones) can cross borders to achieve more nefarious goals, such as tax evasion or illicit wealth transfer. Thus, a tighter customs control over enrichment goods is necessary. Blockchain certificates could be checked when crossing borders and enable customs administrations to prevent tax evasion.

Consumer protection

Our analysis highlights the potential for unethical retailing practices when it comes to the enrichment economy. For instance, Rolex has been recently fined $100 million by the French Competition Authority for preventing its authorized dealers from trading certain references freely (Graff 2024). In addition, there is currently a class-action lawsuit underway in the United States against Hermès, which prompts consumers to purchase ancillary goods before they get access to much-coveted Birkin and Kelly handbags (Danziger 2024).

In their outlets, luxury watch brands often display enrichment goods that are not actually for sale. In other words, these are mere exhibits designed to spur consumers’ interest. This may amount to coercion that exploits consumers’ emotions of seeing a better product, but not being able to buy it right away. Policy makers around the world can adopt laws that prevent goods from being used solely as display pieces and that force providers to have the product in stock if it is promoted to the general population. This echoes bait-and-switch advertising laws in the United States. Bait-and-switch advertising involves brands deceptively advertising a good deal on a certain product knowing that none of the orders will be possible to fill, with the intent to make consumers purchase something else. Implementing similar legal initiatives would greatly enhance consumer protection in the enrichment economy.

Rebound effects of the circular economy

We invite readers to consider the counterintuitive lesson the enrichment economy provides with regard to the circular economy. The circular economy aims at decoupling value creation from waste generation and resource use (Camacho-Otero, Boks, and Pettersen 2018) by closing the loop between production and consumption. Thus, circularity research typically encourages secondary markets as a viable way to reduce resource use (Machado et al. 2019).

However, our investigation of the enrichment economy identifies a significant rebound effect that demonstrates how the expansion of some secondary markets can backfire against circularity. In the enrichment economy, secondary markets can create massive enrichment opportunities. In turn, this prompts consumers to invest in the primary market in search of goods to resell. The vicious cycle continues as consumers keep reinvesting their earnings in a casino-like fashion. This echoes the growing evidence for the dark side of circularity (Lloveras et al. 2022). Given that circularity is becoming a dogma in global business circles (Parker 2023), we encourage all stakeholders to explore alternative methods to alleviate resource use, such as degrowth (Rémy et al. 2024), and explore how (and if) other secondary markets actually contribute to economic circularity.

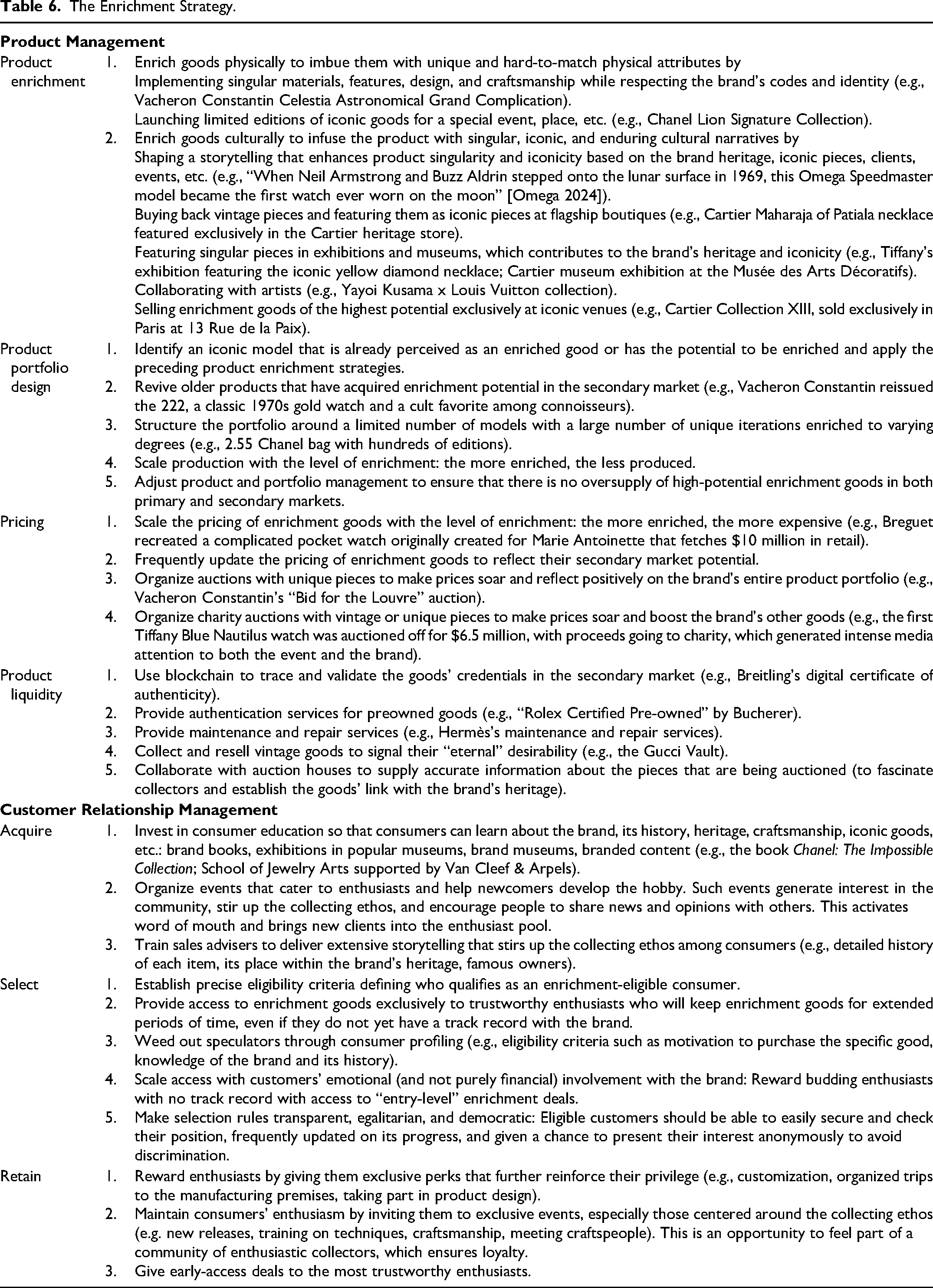

The Enrichment Strategy