Abstract

Analysing the financial sustainability of local governments is of great interest, as they offer a wide range of services and are close to citizens. Various organizations have pointed out the need to analyse the determinants of financial sustainability, and recent research has focused on several European countries, using adjusted income as a dependent variable. To fill the research gap in the context of German local governments, we conduct an empirical analysis with 5 years of data from 363 local governments from North Rhine–Westphalia to analyse the impact of socio-demographic and financial-economic factors on financial sustainability, focusing on the adjusted income. Our results indicate that financial sustainability is influenced by factors on which the local governments have no impact or at least only a limited impact. Specifically, the debt level and the level of population are identified as risk factors, whereas own taxes, rate support grants and the net cash surplus serve as drivers of financial sustainability.

Points for practitioners

Understanding the determinants of financial sustainability is important for politicians and public managers in order to improve their risk management and decision-making processes and to prevent future sustainability problems. This paper identifies several socio-demographic and financial-economic determinants of FS, on which the local governments have only a limited impact. Considering that the financial sustainability of German local governments in North Rhine–Westphalia largely depends on external factors might be of great interest for policymakers with regard to future financial crises.

Introduction

Local governments (LGs) offer a wide range of services, such as water disposal, energy supply and cultural entertainment, which affect citizens’ lives in a basic way (Gardini and Grossi, 2018) and are close to citizens (López-Subires et al., 2019). A lack of financial sustainability (FS) might prevent these entities from delivering their services and reduce citizens’ quality of life (Cuadrado-Ballesteros et al., 2014). Therefore, analysing LGs’ FS is of great interest. Taking into account the recent international financial crisis, austerity policies, budget cuts in the public sector and financial problems of several governments around the world, international bodies have started to pay particular attention to FS in the public sector (Bisogno et al., 2017; European Union (EU), 2012; Navarro-Galera et al., 2016).

International bodies such as the EU (2012) and the International Federation of Accountants (IFAC, 2013) have outlined that demographic and financial–economic factors have an essential influence on public sustainability, which has also been confirmed by relevant public sector research (Navarro-Galera et al., 2021; Rodríguez-Bolívar et al., 2021). Recent European research on influential factors in LGs’ FS based on the adjusted income focuses mainly on Spain and recently on England and Italy (for an overview, see Gardini and Grossi, 2018). German literature mainly analyses FS while focusing on debt grades, net cash surpluses and primary balances (see e.g. Bogumil et al., 2014; Seuberlich, 2017). In this context, we want to contribute to relevant research by shedding some light on the financial–economic and socio-demographic factors that might influence the FS of German LGs in North Rhine–Westphalia (NRW) based on adjusted income. FS, focusing on the adjusted income, is a broader concept than considering debts or net cash surplus, as it includes non-liquid elements like provisions and depreciations and is a measure for intergenerational equity. Using this broader concept, we tend to expand the understanding of the impact of socio-demographic and financial–economic factors on FS.

Our findings make several contributions. First, our study is the first to analyse the determinants of FS in the German LG setting, relying on adjusted income. Second, we reveal an impact of variables on which the LGs have only a limited or no actual influence. Although bailouts helped LGs to consolidate and to reduce cash credits on an aggregated level, various NRW LGs in structurally weak regions still face financial problems. Against this backdrop and with regard to expected rising interest rates, which burden the adjusted income (due to a still persisting high number of LGs’ old debts), federal states and government might be challenged to find solutions. Third, these findings are important for politicians and managers since knowing the determinants of FS can help them take measures to ensure a stable future financial condition and to provide sustainable public services.

The remainder of this paper is structured as follows: the following section describes the German context of LGs. The third section introduces the concept of FS, reviews the relevant literature and derives our hypotheses, and the fourth section defines the methodology, while the fifth section presents the results. The last section contains the discussion and conclusions, including limitations and further research opportunities.

German local government

Germany is characterized by LGs that are relatively strong in the European context (Grossi et al., 2016). Whereas LGs in Germany traditionally applied the cash-based accounting system, in 2003 the federal states agreed on implementing new public management guidelines at the local level, resulting in the application of accrual accounting elements. In 2016, almost two-thirds of German LGs adopted accrual accounting (Frintrup and Hilgers, 2018).

The German federal system consists of three layers: the federal level, the 16 states and the local level, with approximately 11,000 municipalities (Christofzik, 2019). German LGs are subject to monitoring by the fiscal supervisors of the respective federal states, although the LGs are quite autonomous with regard to business and property taxes and spending and borrowing (Roesel, 2016).

German LGs provide various public services, such as waste disposal, child care and cultural institutions (Ruge and Ritgen, 2021), although the range of services varies among different states.

Following the financial crisis and the extraordinary economic downturn in 2008, the average financial situation of German LGs has significantly improved in recent years, accompanied by growing taxes and investments and declining debt (Boettcher et al., 2021). Nevertheless, persisting and even growing disparities in municipal finances on several financial indicators have become apparent (Boettcher et al., 2021).

In particular, the state of NRW was one of the first German states to implement accrual accounting at the LG level before 2010 and represents Germany's largest state by population and economic size (De Widt, 2017). LGs in NRW regions seem to show a long-term debt problem. Of the 10 LGs exhibiting the highest expenditures for social services in Germany, 7 LGs are in NRW (Boettcher et al., 2021). Additionally, 60% of the nationwide municipal cash credit stock is concentrated in NRW (Boettcher et al., 2021). NRW has a long history of bailouts, starting in the 1980s to support old industrial cities suffering from socio-economic decline going over to the global financial crises with the pact for strengthening cities in 2011 (Person and Geissler, 2021). In 2018, as the cash credits still remained on a high level in NRW, the federal state started a discussion on a major bailout of cash old debts, which was postponed due to the large amount of credits and is still discussed (Person and Geissler, 2021).

Considering the prevailing debt problems in this region, we especially focus on NRW LGs.

Literature review and hypotheses development

The concept of financial sustainability

Triggered by recent economic and financial crises in the public sector, international bodies have begun to focus on the concept of FS to evaluate when a public sector entity faces financial problems (EU, 2016; IFAC, 2013). This concept refers to information about future financial years instead of current financial figures and is therefore broader than other financial indicators (Rodríguez-Bolívar et al., 2016).

FS, defined as the ability to meet service and financial commitments and to apply and maintain current policies without rising debt (IFAC 2013), is deeply connected to the concept of intergenerational equity (IFAC, 2012). Although there is no universal definition on how to measure FS with regard to intergenerational equity, the income statement is considered a good indicator, as it mirrors an LG's ability to provide the same level of public services and goods in the future and the respective needed resources (IFAC, 2012). Furthermore, it covers the three dimensions of the concept as defined by the EU (2016): services, revenues and debt (Navarro-Galera et al., 2016). More concretely, the income statement covers two dimensions directly: revenues, on the one hand, are included in the income statement, and the service component can be measured through service commitments, which are part of expenses (Rodríguez-Bolívar et al., 2016). Additionally, by means of interest expenses, the debt level is indirectly connected to the income statement.

In recent international literature, there is a growing body of studies that analyse the determinants of FS focusing on adjusted income. Knowledge of these determinants might improve public managers’ and politicians’ decision making (Bisogno et al., 2017). Some authors solely examine the influence on FS of socio-demographic factors (López-Subires et al., 2019; Rodríguez-Bolívar et al., 2021), and identify risk factors such as population size and unemployment rate. Others focus on the influence of financial–economic factors such as debt level and different types of expenditures (Navarro-Galera et al., 2016). Finally, other researchers integrate socio-demographic and financial–economic factors to analyse their influence on FS (Navarro-Galera et al., 2016, 2021; Rodríguez-Bolívar et al., 2016,), showing mixed evidence.

There is a certain body of German literature which analyses FS of LGs in a quantitative way. These studies can be distinguished with regard to dependent variables. A lot of studies, using the balance sheet, focus on debts as an indicator of FS (e.g. Boysen-Hogrefe, 2014; Junkernheinrich and Wagschal, 2014), while others focus on the net cash position (Seuberlich, 2017). Net cash surpluses only consider in- and outgoing cash flows, whereas they do not include non-liquid elements like provisions and depreciations. LGs might use current net cash surpluses to repay and reduce debts (Junkernheinrich and Micosatt, 2022), while the adjusted income could be negative. Consequently, LGs might run the risk of creating a hidden indebtedness. The (accrual-based) adjusted income as a broader concept is the basis for intergenerational equity (IFAC, 2012), as it adequately ensures the consideration of resource consumption and resource availability. Intergenerational equity itself is closely linked to the concept of FS (Rodríguez-Bolivar et al., 2016). Therefore, focusing on the adjusted income is highly important also for German LGs, as it is a broader concept than merely considering debts or net cash surplus.

However, studies on drivers and risk factors for FS based on adjusted income are mostly focused on the US and Spain (Gardini and Grossi, 2018). We therefore want to contribute to existing FS research by analysing the drivers and risk factors associated with German LGs’ FS. To the best of our knowledge, our study is the first to focus on adjusted income as a measure for FS in German LGs. In the following, we derive our hypotheses, divided into socio-demographic and financial–economic variables.

Influential factors on FS

International and German literature differs between internal and external conditions which might have an impact on LGs’ FS (Bogumil et al., 2014; Gardini and Grossi, 2018). Whereas external conditions mostly concern socio-economic and demographic factors, internal conditions focus on managerial and political settings like partisan and political cycles (Bisogno et al., 2017; Gardini and Grossi, 2018). Recent literature states that external and internal factors determine FS (Bogumil et al., 2014). However, since international bodies (EU, 2012; IFAC, 2013) emphasize the importance of demographic and financial–economic factors with regard to public sustainability, and recent public sector research confirms this importance (Navarro-Galera et al., 2021; Rodríguez-Bolívar et al., 2021), we focus on socio-demographic and financial–economic factors. This is especially timely and relevant with regard to the demographic change and the financial challenges which LGs have to face in view of the COVID-19 pandemic and the Ukrainian war.

Socio-demographic factors

Socio-demographic variables are external factors that are not controllable by LGs. Most recently, international organizations have emphasized the role of the population structure as an important external factor of FS (IFAC, 2013) and the demographic change poses a great challenge for LGs (Starke, 2021). Typical demographic factors in public finance studies are population size, dependent population share and the importance of a place of work within the LG.

Recent literature on German FS identifies population size as a risk factor. On the revenue side, a shrinking population might decrease LGs tax revenues with regard to the share in income taxes (Starke, 2021). Focusing on the expenses, LGs might face remnant costs. In case of a population decrease, due to technical, political and economic remnant costs, LGs might not be able to reduce expenses for infrastructure services proportionally to the population size (Starke, 2021). Technical remnant costs occur in the area of road network and disposal services (e.g. waste water) (Lenk et al., 2012), whereas political remnant costs concern museums, theatres and schools. The common problem of these costs lies in the rising average expenses per capita. We therefore propose the following hypothesis:

International organizations have expressed worries about the rising share of the dependent population, as it is expected to have a significant impact on public sector FS (EU, 2016). Generally, a shift in age structure changes the demand of citizens for public services, which in turn influences the expenses within the municipal tasks, since a lot of tasks are performed for specific age categories (Starke, 2021). Young people require a lot of public services without contributing through tax payments (Santis, 2020), as the share of income tax is depending on age structure. Therefore, the share of income taxpayers should be lower in the young and old age groups (Seuberlich, 2017). Older people necessitate a lot of services but contribute with a smaller tax amount on their pensions (Santis, 2020). Consequently, the income tax revenues might be lower in LGs which offer a higher share of dependent population. Recent German literature states that the old-age dependency rate increases cash credits (Junkernheinrich and Wagschal, 2014) and significantly reduces the net cash position (Bogumil et al., 2014). We therefore propose the two following hypotheses:

Recent literature analyses the importance of an LG as a place of work as a measure for workplace centrality. This variable is calculated by setting the employees at the workplace in relation to employees at the place of residence. A value higher than one means that more employees work than employees live in the LG and there are more ingoing than outgoing commuters (Bogumil et al., 2014). This variable is a measure of economic power of an LG. Recent literature concludes that the importance as a place of work has a significant negative relation to LGs’ cash credit rate of change (Junkernheinrich and Wagschal, 2014) and a significant positive impact on the net cash position and the primary balance (Bogumil et al., 2014). Relying on the positive effects of a commuter surplus on the net cash position and the primary balance, we propose the following hypothesis:

Financial–economic factors

Another important group of variables with an influence on LGs’ FS are financial–economic factors (IFAC, 2013). In our analysis, these include the level of indebtedness, the net cash position, the level of own taxes and the level of rate support grants.

International organizations such as IFAC (2013) state that increasing debt requires higher revenues for repayment and comes at the expense of resources required for public service provision. To ensure FS, evaluation of debt is necessary (Navarro-Galera et al., 2021). Additionally, analysing the debt level is highly important since NRW LGs account for 60% of all nationwide municipal cash credits (Boettcher et al., 2021) Whereas 10 LGs own one-third of all nationwide municipal cash credits, other LGs exhibit absolutely no cash credits (Boettcher et al., 2021), showing a regional disparity. German literature finds a negative influence of the debt level on the primary balance (Bogumil et al., 2014; Seuberlich, 2017) and the net cash position in district-free cities (Seuberlich, 2017). The negative influence on FS was also stated on an international level (Navarro-Galera, 2016; Santis, 2020). We therefore propose the following hypothesis:

Another factor that might influence FS is the in- and outgoing cash flows. In our analysis, we use the net cash position, which is the surplus or deficit in cash receipts and cash payments and which provides information on the financial capacity of an LG and its room for planning and implementing the budget. In contrast to the adjusted income, the net cash position is focused on liquidity and shows the cash in- and outflows. A positive net cash position might be used to reduce debts and guarantee balanced spending and revenues (Rodrìguez-Bolìvar, 2016) We therefore propose the following hypothesis:

FS involves providing and maintaining public services without increasing taxes and debt levels (Bisogno et al., 2017). In our analysis, we focus on own taxes, which are the trade tax and property taxes A and B. Property tax A especially refers to agriculture and forestry properties, whereas property tax B concerns developed and undeveloped properties. Trade tax especially is very sensitive to the general economic situation, which has been criticized in recent literature (Seuberlich, 2017). The own taxes can be seen as a measure for economic power of an LG (Junkernheinrich and Wagschal, 2014). Bogumil et al. (2014) find a negative relationship between the amount of trade tax and the debt level of an LG, whereas Seuberlich (2017) shows a positive influence of the amount of trade tax on the primary balance. As higher tax revenues might reduce debts and increase the primary balance, we assume a positive effect on financial sustainability, proposing the following hypothesis:

Each German state implemented a fiscal equalization system in order to ensure a need-based financial basis (Person and Geissler, 2021), which consists of dedicated (from federal states and federal government) and general allocations (from federal states only) (Seuberlich, 2017). The central element of the fiscal equalization system is the rate support grants as part of the general allocations, which consider the financial need in relation to the financial power of an LG (Seuberlich, 2017). LGs’ financial flexibility is significantly influenced by fiscal equalization systems (Bogumil and Holtkamp, 2013). Gröpl et al. (2010) state that the change rate of cash credits is negatively correlated with rate support grants, as LGs might compensate for a reduction in grants with an increase in cash credits. Analysing grants for NRW and English LGs, De Widt (2016) states that total grants are positively related to debt per capita, as LGs with a high dependence on grants tend to borrow more money. Nevertheless, in his study, for general grants the results for NRW lack significance. Assuming that decreasing rate support grants increase an LG’s debt level, we therefore propose the following hypothesis:

Methods and data

This section provides an overview of the data collection and the sample and describes the variables used for the analysis.

Data collection and sample description

The present study focuses on LGs in the state of NRW, with its 396 LGs. The study sample is composed of 363 LGs with data for the period 2014–2018, as we could not obtain data for every LG. The data were drawn from the statistical office of NRW (adjusted income as dependent variable) and from the ‘Wegweiser Kommune’ project (the independent variables) (Bertelsmann-Stiftung, 2022). ‘Wegweiser Kommune’ is an information system for the municipal practice. As the largest German state by population size and density and economic size, NRW is assumed to be representative of the intergovernmental regulation of LG finance (De Widt, 2017). Taking further into account that several LGs in NRW seem to have a long-term debt problem and that regional disparities prevail, our analysis is based on NRW. Furthermore, NRW LGs are characterized by a great diversity of population sizes. In contrast to recent previous research, we focus on LGs of all population sizes and choose not to focus only on larger LGs (Santis, 2020; Rodríguez-Bolívar et al., 2021).

Dependent variable

In our empirical analysis, FS is the dependent variable. To measure LGs’ FS, our study focuses on information from income statements, as suggested by international organizations (EU, 2016; IFAC, 2013) and recent research (Navarro-Galera et al., 2021; Rodríguez-Bolívar et al., 2021). The income statement is considered a good indicator because it mirrors an LG's ability to provide the same level of public services and goods in the future and the respective resources needed (IFAC, 2012). We therefore use (published) income statements from LGs as our data source and measure of the dependent variable FS. According to previous research, the income statement must be adjusted because it contains extraordinary revenues and expenses that will likely not be repeated in the future (Rodríguez-Bolívar et al., 2016). Excluding these extraordinary items makes income a better indicator in terms of intergenerational equity and of the measurement of FS (López-Subires et al., 2019). We therefore use the accrual-based annual income statements adjusted for extraordinary items (see Figure 1).

Financial sustainability. Source: López-Subires et al. (2019).

Independent variables

With regard to the independent variables (Table 1), we include socio-demographic and financial–economic variables that might influence German LGs’ FS. The socio-demographic variables include population size (POP), dependent population under 18 (DP18), dependent population over 65 (DP65) and the importance as a place of work (IPW). As financial–economic variables, we choose debt level (DL), net cash position (NC), own taxes (OT) and rate support grants (SG). From the independent variables, we choose to use the logarithm only in the case of the population size in order to normalize this variable. All other variables are expressed in their relative values.

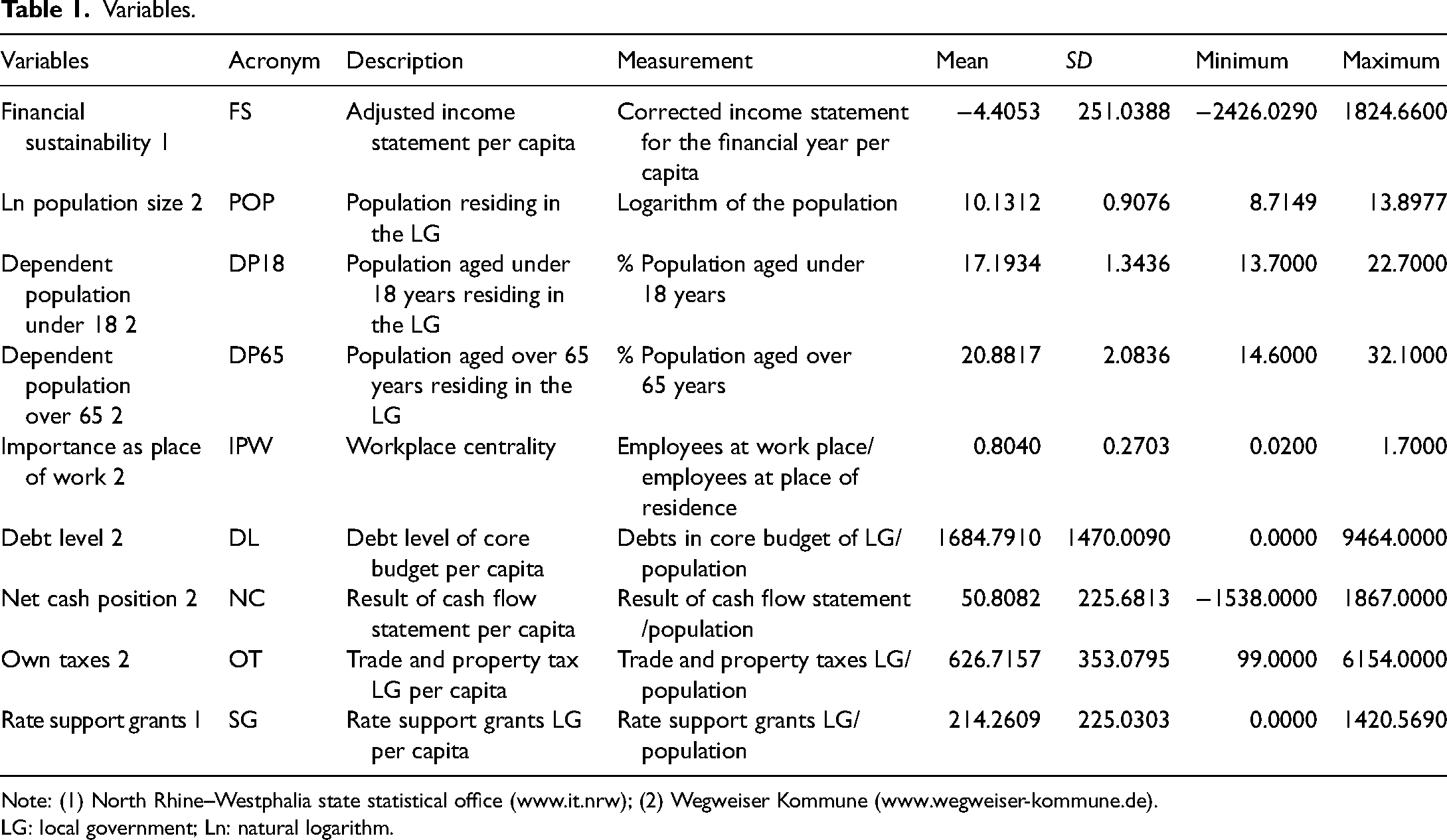

Variables.

Note: (1) North Rhine–Westphalia state statistical office (www.it.nrw); (2) Wegweiser Kommune (www.wegweiser-kommune.de).

LG: local government; Ln: natural logarithm.

Statistical model and methodology

To analyse the influence of the independent variables on FS, we collect data for 363 NRW -LGs for a 5-year period (2014–2018) and then apply a panel data technique. This technique is the most common tool in public finance research (Rodríguez-Bolívar et al., 2016) and, by pooling different time series, increases the number of observations (Zhu, 2013). Accordingly, our model contains a vector of variables for n units (363 LGs) over T periods of time (5 years, 2014–2018), resulting in the following equation model:

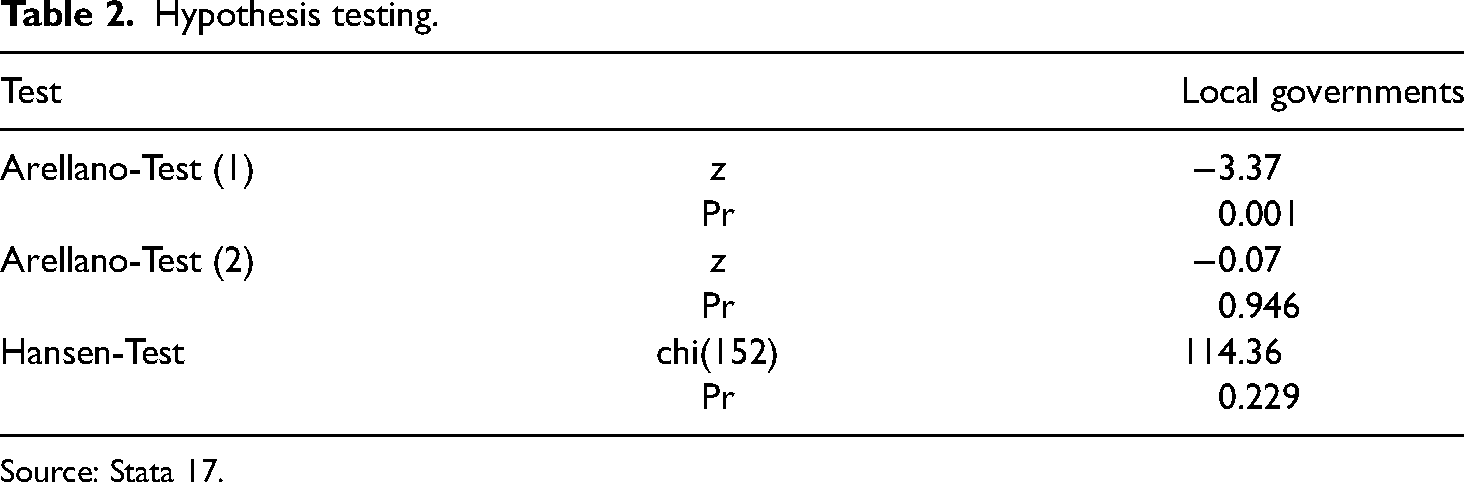

Anticipating the possible existence of endogeneity, we use the system generalized method of moments (SGMM) to estimate our model. SGMM is appropriate to control for possible endogeneity between endogenous variables and the error term (Prillaman and Meier, 2014), as it uses lagged levels of the endogenous regressors as instrumental variables (Roodman, 2009). Furthermore, due to the small sample, we apply a two-step estimation including the Windmeijer correction to make the model asymptotically more efficient and robust to any patterns of heteroscedasticity and cross-correlation (Windmeijer, 2005). To check for the existence of serial correlation and to analyse if the instruments adequately control for endogeneity, we perform the Arellano–Bond test and the Hansen test (Arellano and Bond, 1991), which confirm the consistency and robustness of our model (Table 2).

Hypothesis testing.

Source: Stata 17.

Empirical results and discussion

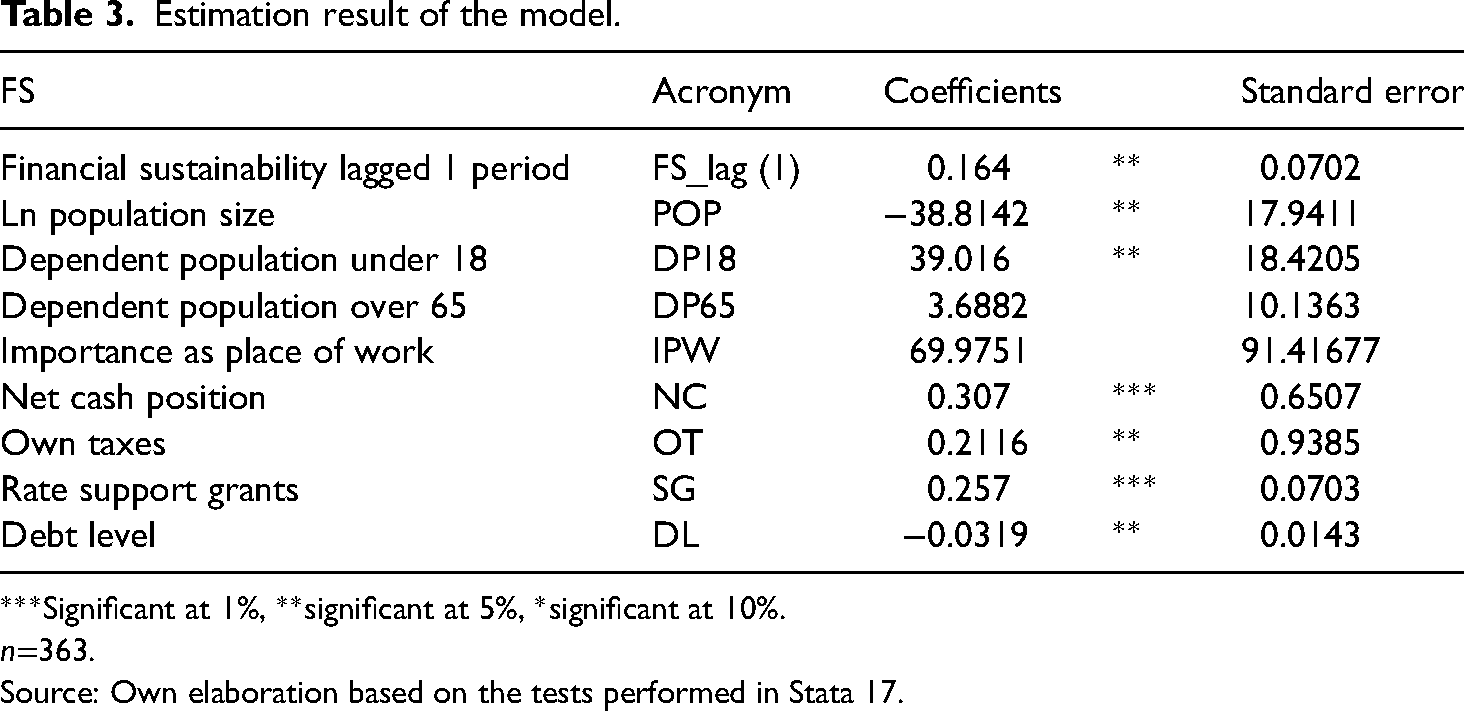

The empirical results of our analysis are shown in Table 3. With regard to FS, we identify drivers (+β; when they rise, FS increases) and risk factors (−β; when they rise, FS decreases).

Estimation result of the model.

***Significant at 1%, **significant at 5%, *significant at 10%.

n=363.

Source: Own elaboration based on the tests performed in Stata 17.

As shown in Table 3, our results produce two negative factors for FS, population size (β = −38.8142) (H1 is accepted) and debt level (β = −0.0319) (H5 is accepted). An increase in these factors conclusively worsens an LG’s FS. In addition, we find other factors with a positive influence on FS; that is, the dependent population under 18 (β = +39.016), the net cash position (β = +0.307), own taxes (β = +0.2116), and rate support grants (β = +0.257).

With regard to socio-demographic factors, we identify population size as a risk factor for FS, corroborating findings from German (Boettcher, 2013; Boysen-Hogreve, 2014) and international literature (Navarro-Galera et al., 2021; Rodríguez-Bolívar et al., 2021). This might be due to cost remnant effects, as in the case of shrinking population size, expenses for existing infrastructure services cannot be reduced proportionally to the population trend (Lenk and Starke, 2015). On the other hand, despite economies of scale, a rising population might raise the demand for public services but not necessarily be accompanied by a corresponding increase in tax revenues.

Turning to the dependent population under 18 and over 65, our results do not identify these variables as a risk factor for FS in German LGs (H2 und H3 rejected). A change in an LG’s age profile could change the demand behaviour of a population, since different age groups demand different services. Furthermore, a rising share of old and young people might lower tax revenues and raise expenses. German literature focusing on old age dependency ratio shows a negative influence on net cash position (Bogumil et al., 2014) and a positive relation to cash credit volume (Junkernheinrich and Wagschal, 2014). Our analysis, however, shows no significant influence of the dependent population over 65 on FS. This is in line with findings from Starke (2021), who states that the expenses for people over 65 such as benefits from pensions and nursing care are mainly born by state and federal government. With regard to the dependent population under 18, our results show a positive significant impact on FS. Nevertheless, the interdependence of local age structure on LGs’ financial power is rather difficult to determine, since the potential effects might be overperformed by social conditions (Boettcher, 2013).

Turning to the financial–economic variables, our results reveal debt level as a risk factor for FS (H5 is confirmed). This is in line with our expectations and recent findings from international literature on adjusted income (Navarro-Galera et al. (2016) and German literature on primary balance (Bogumil et al., 2014; Seuberlich, 2017). These results are highly decisive with regard to the recent debt situation, as several NRW LGs face severe financial problems. Despite fiscal equalization systems and strict budgetary frameworks, many cities had and still have to face fiscal problems (Person and Geissler, 2021), due to structural changes and inadequate funding. Accordingly, higher debt levels may negatively impact FS and therefore endanger the provision of public services by LGs. With regard to the still prevailing high amount of cash credits in NRW LGs, the debt problem for certain LGs still lacks a solution. Additionally, given the possibility of rising interest rates, the high number of old debts might cause relevant interest expenses, which would have to be borne by the following generations.

A variable with a positive influence on FS is net cash surplus (H6 is confirmed), corroborating findings from the EU (2012) and Rodríguez-Bolívar (2016) and meeting our expectations. Net cash surplus renders information on the financial capacity of corresponding LGs and therefore is a driver of FS. LGs which achieve positive net cash surpluses might contribute to intergenerational equity and financial sustainability, whilst balancing spending and revenues (Rodriguez- Bolívar, 2016). Nevertheless, this variable only considers in- and outgoing cash flows and no provisions, which limits its explanatory power.

Our analysis identifies own taxes as a driver of FS, showing a positive coefficient (H7 is confirmed). This is in line with recent findings from German studies, which identify trade tax as a driver of the primary balance (Seuberlich, 2017), state a dampening effect of trade tax on debts (Bogumil et al., 2014) and find a negative relation of total taxes and debts (De Widt, 2016). Our findings are intuitive, since next to the share of income taxes, trade taxes are the most important municipal taxes, making up to 40% of local tax revenues (Sidki, 2014). However, own taxes show two conflicting characteristics. On the one hand, LGs have the freedom to set the assessment rates for trade and property taxes, which is based on German Basic Law (Article 106 (6) of the Basic Law). Against this backdrop, own taxes can be seen as a key element for adjusting local finances (Seuberlich, 2017). On the other hand, trade taxes are very sensitive to the economic situation (Sidki, 2014) and therefore rather volatile. Consequently, LGs run the danger of being burdened by declining tax revenues due to an unfavourable global economic situation (Junkernheinrich, 2010).

Our results identify rate support grants as a driver of FS (H8 is confirmed), corroborating findings from Bogumil et al. (2014) and Gröpl et al. (2010). Rate support grants are a central element of the municipal equalization scheme in order to strengthen fiscally weak LGs (Seuberlich, 2017). In our empirical analysis, there is some evidence that the financial support of an LG within the framework of the municipal equalization scheme is decisive for its financial results based on published accrual financial statements. Since LGs cannot directly influence the scheme of municipal equalization, they depend on institutional settings, which shows in some sense the responsibility of the federal states for the financial setting of respective LGs (Gröpl et al., 2010). Rate support grants are part of the institutional explanatory factors of LGs’ FS and, through the design and amount of fiscal equalization schemes, determine the financial flexibility of LGs (Bogumil and Holtkamp, 2013).

Additionally, our results indicate that the one-period-lagged FS has a positive effect on FS, which corroborates recent findings in international (Navarro-Galera et al., 2021) and German literature (Bogumil et al., 2014). In the sense of path dependency theory, an LG might face some difficulties in achieving positive FS in the following year once it is trapped in negative FS values.

Conclusions and implications

Conclusion

This study's aim is to shed some light on drivers and risk factors that might influence German LGs’ FS in NRW. With regard to still prevailing financial problems and high debt grades of several NRW LGs and the ongoing political discussion on how to handle old debts, achieving FS is highly relevant and timely. We therefore conducted a panel analysis to measure the impact of socio-demographic and financial-economic factors on FS.

Our analysis focuses on the adjusted income as a broader concept of FS, which, in contrast to other financial indicators such as debt grades and the cash-flow-based net cash position, provides financial information on the coming years rather than explaining only current figures. By including future costs and consumption of capital investments, the income statement offers a more comprehensive approach to FS (Navarro-Galera et al., 2016). Additionally, as it is closely connected to intergenerational equity, it allows not only the evaluation of LGs’ capacities to currently deliver public services without increasing debts, but also to discover whether they own adequate resources to do so without burdening future generations (Rodrìguez-Bolìvar et al., 2016). We expand the understanding of German LGs’ FS, being the first to use adjusted income in the German context, offering insights on current and future FS. Below, we discuss the key findings of the study.

Although the financial setting of an LG is depending on various socio-economic, institutional and political factors and reveals itself as highly complex, we offer some interesting findings. Our results indicate that in the German setting in NRW, population size as a socio-demographic variable has a negative impact on FS, corroborating recent international and German literature and confirming the existence of remnant costs. Since LGs have no direct and timely influence on their population size, this variable turns out to be an exogenous risk for LGs.

With regard to financial–economic factors, we identify debt level as a significant potential risk factor, whereas net cash surplus, own taxes and rate support grants are significant drivers of FS.

The negative influence of debts on FS might be intuitive. Nevertheless, with regard to the regional disparities and prevailing financial problems of some NRW LGs, especially those from the Ruhrgebiet, focusing on debts is of great importance. On the one hand, the high number of older debts poses a risk in the case of an increase in interest rates, burdening the adjusted income and future generations and resulting in a vicious circle. On the other hand, sound FS in the form of adjusted income might prevent further cash credits and ensure the provision of public services. Although the decision to borrow lies in the hands of the respective local management and politicians, LGs might be pushed into borrowing to ensure the provision of their public services.

In our analysis, the net cash surplus serves as a driver of FS. Whereas on a nationwide basis, LGs show positive net cash surpluses in recent years, the allocation shows immense regional disparities. Nevertheless, it renders information on the financial capacity of an LG.

Our results reveal own taxes as a driver of FS. LGs possess a certain degree of autonomy with regard to the assessment rates. However, the benefit of raising assessment rates is limited and poses certain risks. NRW LGs participating in the bailout ‘pact for strengthening cities’ significantly raised their assessment rates, without strengthening their equity or reducing older debts (Holtkamp and Garske, 2020). In the aftermath of the financial crises, the municipal bailout programme was implemented in 2011 and foresees annual grants with the intention of achieving a balanced budget (Person and Geissler, 2021). Raising assessment rates additionally influences the fiscal attractiveness of locations and LGs might enter into a fiscal competition. Furthermore, trade taxes show a high volatility with regard to the economic situation on a global and national level, whereas the expenses of an LG might remain stable.

Rate support grants show a positive influence on FS. Distributed to equalize fiscal disparities, these grants are rather exogenous to LGs and belong to the institutional setting. Our results reveal that rate support grants are generally adequate to strengthen an LG’s FS. Nevertheless, the amount and distribution of rate support grants and bailouts could not solve the prevailing debt problems of some LGs in NRW and is continuously debated.

Theoretical and practical implications

Our findings offer some important theoretical and practical implications. First, knowledge of the determinants of FS is important for helping politicians and public managers improve their risk management and decision-making process and ultimately prevent FS problems. Our findings indicate that in the German setting, LGs have a limited impact on the analysed variables. Although they can set assessment rates for own taxes and decide upon borrowings, they depend heavily on the institutional setting (throughout rate support grants) and the global economic situation (throughout the volatile character of trade taxes). Nevertheless, socio-demographic and financial–economic factors do not solely determine LGs’ FS. Recent research shows the significance of political competition as an endogenous factor on LGs’ debt situation (Bogumil et al., 2014). Consequently, political factors like the size of communal parliament and the configuration of municipal constitutions also influence FS.

Furthermore, our study might be of interest to international readers of public sector accounting literature, as LGs will have to respond to future challenges that will certainly affect FS, such as migration flows from the Ukraine war and the coronavirus pandemic. Shedding some light on socio-demographic and financial–economic factors is of great interest in recent research. As the first authors to analyse determinants of FS in Germany while focusing on adjusted income, we show that the financial setting of an LG largely depends on external factors. With regard to the problems of older debts and the upcoming challenges, federal states and government are required to find solutions.

Limitations and future research

Our study is not free of limitations. Although NRW is Germany’s largest federal state by population and economic size, our findings might not be generalizable to all German LGs, and the sample size is limited. Further research could expand the analysis to different German federal states, or – once accrual accounting has been applied in all German LGs – to all German LGs. Furthermore, it would be interesting to analyse drivers and risk factors by LG size to determine whether our findings can be applied to LGs of all sizes. According to recent literature, FS is not solely determined by external factors (Bogumil et al., 2014). Therefore, our results on FS should be interpreted with caution. Consequently, further research on the FS based on adjusted income of German LGs could focus on another group of internal variables: political factors. Recent research has identified political ideology and competition as well as political strength as determinants of FS (Gardini and Grossi, 2018). These findings could be expanded on the concept of FS. Last, against the backdrop of the COVID-19 pandemic and the recent war in Ukraine, which might result in refugee flows to several European countries and present the local public sector with new challenges, analyses of FS should be replicated and updated.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article