Abstract

In this study, we develop a model to examine the dynamics of the insolvency and bankruptcy code (IBC) processes in the aftermath of Covid-19. We use the model to study the impact of the pandemic on the following aspects of the financial disputes and their implications: number of disputes between debtors and their creditors in the aftermath of Covid-19; frequency of these disputes coming to the National Company Law Tribunal (NCLT); impact of the pandemic on the frequency of ‘out of court’ settlements; the nature of disputes settled amicably and those adjudicated under the corporate insolvency resolution process of the NCLT; and the recovery rates in the settled versus litigated disputes. We show that while the number of disputes will go up, the frequency of settlements will come down in the post-Covid world. Moreover, the post-pandemic legal changes made to the IBC are detrimental to the interest of the micro, small and medium enterprises and also for the formal and informal sector employees. We offer suggestions for promoting out-of-court settlements to save time and costs of the parties involved. Our suggestions related to public policy can help mitigate the macroeconomic costs of the pandemic.

Introduction

The Covid-19 pandemic has unleashed a spate of commercial disputes. The pandemic and the lockdowns have inflicted heavy losses on sales and incomes of many businesses—big or small, formal or informal. Consequently, many companies and enterprises are finding it difficult to meet their contractual obligations. Given the severity problem, the Reserve Bank of India (RBI) has issued a moratorium on repayment of all term loans. Similarly, in an effort to ameliorate the liquidity crisis faced by the debtors, the Government of India has suspended initiation of insolvency and bankruptcy proceedings under the insolvency and bankruptcy code (IBC). So far, these moratoria have helped the companies and other debtors defer servicing of their debt obligations.

Once the moratorium on IBC proceedings ends, many debtors will find it difficult to service the debt. Therefore, the number of disputes between debtors and creditors is bound to explode. Already there are reports of borrowers expressing inability to service the debt. Many employers have refused the promised wages and employment benefits, consequently triggering litigation by the counterparties for compensation. 1 As to the disputes between debtors and their creditors, they are adjudicated by the National Company Law Tribunal (NCLT) set up under the IBC, 2016. For details about the procedural issues and the legal changes brought about by the IBC, 2016, see, for example, Chadha and Gangopadhaya (2019), Chatterjee et al. (2017) and Gupta (2019).

In this study, we examine the effect of Covid on the following aspects of disputes between corporate debtors and their creditors: frequency of disputes in the aftermath of Covid-19; frequency of the disputes coming to NCLT before and after the pandemic; and effect of the pandemic on the number of ‘out-of-court’ settlements (OCSs) of these disputes. In addition, we examine the nature of disputes settled in OCSs with those being adjudicated by the NCLT under the corporate insolvency resolution process (CIRP). We compare the recovery rates in OCSs with the recovery rates under the CIRP.

For this purpose, we develop a model that captures the essential aspects of functioning of the IBC process. The model serves to provide an analytical framework and also to make predictions about the OCS and the CIRP. Our model predicts that the probability of OCS is higher if the dispute is with an operational creditor rather than the financial creditor. Ceteris paribus, probability of litigation (CIRP) increases with the value of outstanding debt. Moreover, the recovery rate is higher under OCS compared to litigation. These predictions are tested using the empirical evidence available on the issues mentioned above.

Our analysis shows that the number of debt and payment-related disputes will explode after the moratorium in IBC proceedings end. However, the 2020 amendment to the IBC code will make the situation worse. The amendment has increased the case filing threshold from ₹ 1 lakh to 1 crore. As a consequence of this legal change, the frequency of OCSs of debt and payment-related disputes will come down significantly. In other words, a larger proportion of post-Covid disputes will remain unsettled for a longer duration. On one hand, this will increase frequency of socially wasteful litigation and on the other hand, resolution of distressed assets will be prolonged. Therefore, the balance sheet of debtors and their lender banks will be stretched leading to decline in recovery rates and increase in non-performing assets (NPAs).

Finally, we show that the effect of the increase in filing threshold is detrimental to the interest of the micro, small and medium enterprises (MSMEs). In the post-Covid world, the small businesses and employees will not be able to bring their claims to National Company Law Apellate Tribunal (NCLT). We show that the small businesses will suffer from the double whammy of fall in business income as well as non-recovery of their dues.

The amendments to the IBC have implications for employees of the formal and informal sectors. Employees are considered as operational creditors under the IBC. In the past, they have been able to recover their salary from fraudulent or insolvent employers by filing a case before NCLT. However, due the increase in threshold affected by the amendment, they will not be able to and will be left uncompensated for their due wages.

We offer suggestions for promoting OCSs to save time and costs of the parties involved. Our suggestions related to public policy can help mitigate the aggregate costs of the pandemic. This work adds to the existing literature that mostly focuses on procedural and legal aspects of the Code. Some of the works on the topic examine implications of the IBC on NPAs and the banking sector in general. See, for example, Anant et al. (2019), Ayilyath (2019), Durga Priya et al. (2018), Rajoria (2018), Sane (2019) and Tandon (2019).

The second section of the study describes the processes of insolvency, bankruptcy and OCS under the IBC. The third section presents a model to formally capture the dynamics induced by these processes. The model is used to make predictions about the likelihood of OCSs and litigation for different types of creditors and their recovery rates. In the fourth section, we test predictions of the model using the data available on IBC related cases. The data analysis in this section also helps us make predictions about the outcomes in the post-Covid world. In the fifth section, we discuss the outcomes in the post-Covid world for different stakeholders including MSMEs, employees and banks. We offer suggestions for reducing litigation and mitigating the adverse effects of the pandemic.

Settlement and Resolution Processes under IBC

The IBC 2016 is based on principles of resolution with or without the intervention of the Adjudicating Authority (NCLT/NCLAT). The Code provides ‘Corporate Insolvency Resolution Process’ (CIRP) leading to resolution with the support of Interim Resolution Professional (IRP) or Resolution Professional (RP). The RP takes care of the operation of the company as going concern in place of the previous debtor in possession model.

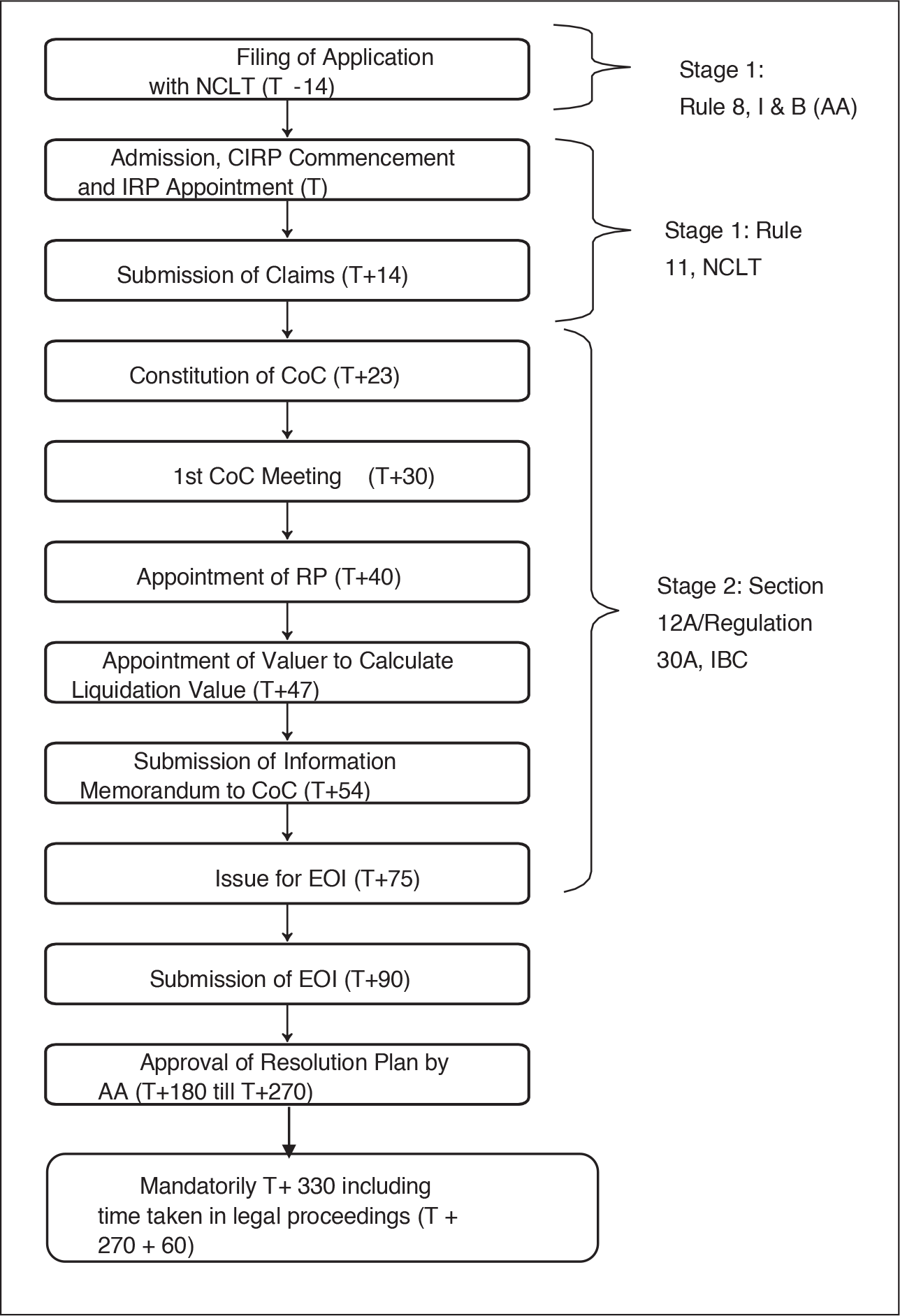

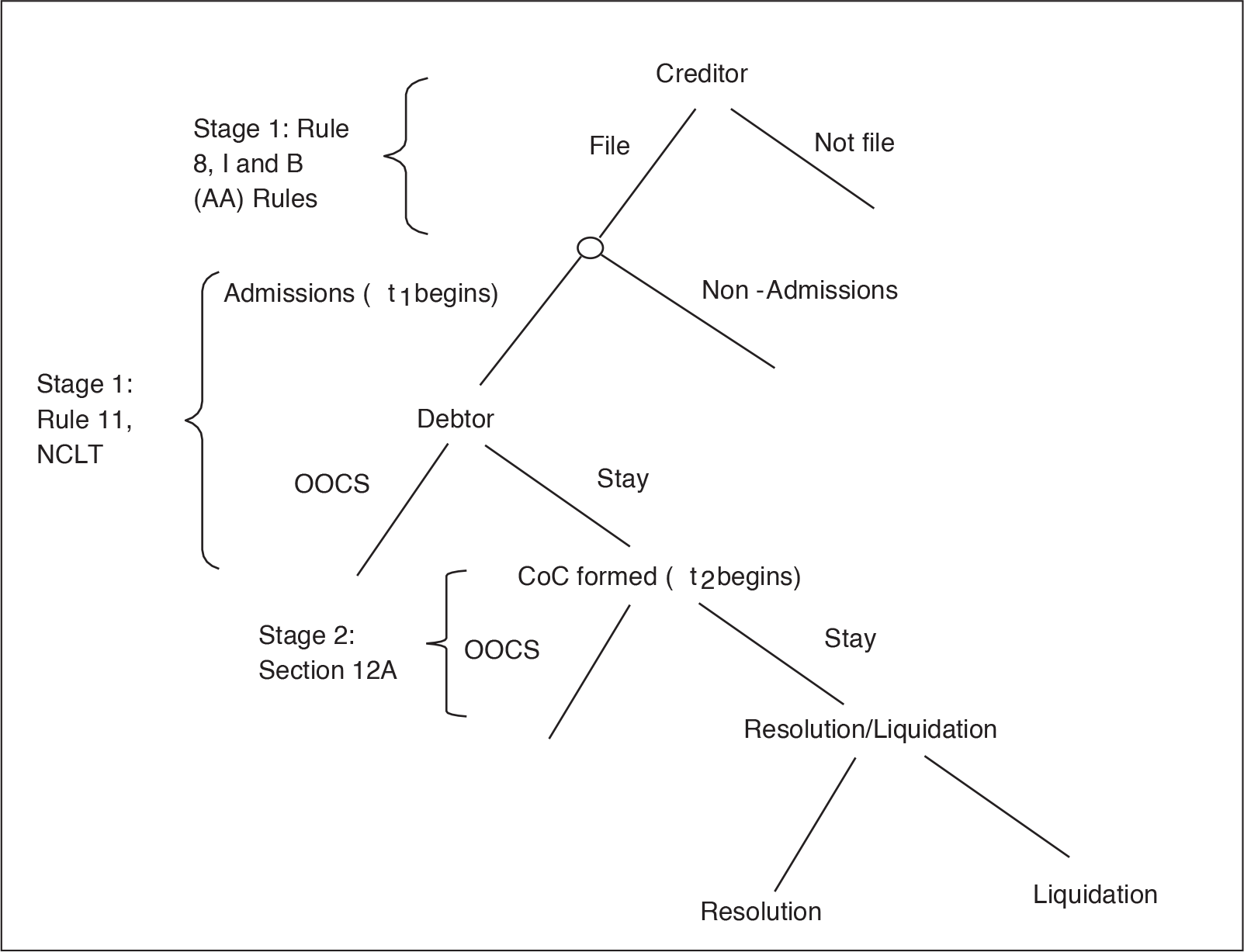

Here we present the process of settlement and resolution under the IBC. First, the default or non-payment of debt (minimum threshold of 1 lakh previously and currently 1 crore based on amendment 2020) leads to the problem of insolvency. The creditors file application before NCLT. The NCLT admits the application and appoints an IRP to commence the CIRP process. The IRP declares public announcement and invites claims from other creditors. After receiving the claim, the IRP constitutes a Committee of Creditors (COCs). Stage 1 is the period between filing of an application to NCLT and just before the constitution of COCs. Stage 1 is determined in accordance to Rule 8 of IBC 2 and Rule 11 of NCLT. 3 In Rule 8, IBC relates to the period between the filing of an application and before its admission of application. Whereas, in Rule 11 NCLT relates to the period between the admission of application and before the constitution of COCs which is reflected in Figures 1 and 2.

In the first meeting of COC, IRP can be appointed as RP or any other RP can be appointed based on the recommendation of COC. The appointment of the valuer calculates the liquidation value. The RP prepares information memorandum and invites expression of interest (EOI). Therefore, Stage 2 is period after constitution of COC and issuance of EOI as determined under ‘Section 12A of IBC 2016 4 read with Regulation 30A of IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016’ which is reflected in Figures 1 and 2. Finally, based on EOI from resolution applicants, the COC approves or rejects the resolution plan (go for the liquidation). Also, the liquidation may be due to the lapse of time period from T +180 days till T + 270 days or T + 330 days including the time taken for the legal proceeding as described in Figure 1.

Therefore, the OCS evolves from Rules 8 and 11, and post amendment under Section 12A. The Rule 8 allows withdrawal before the admission of application. Whereas, the Rule 11 of NCLT allows withdrawal before COC is constituted after the appointment of IRP, a party can approach NCLT said in Swiss Ribbons Pvt Ltd. v UOI. 5 However, there was no provision for an OCS post constitution of COC, so Section 12A was inserted via amendment. Also, the Regulation 30 A (1) is not mandatory but directory which means that in exceptional cases, even after issue for EOI in accordance with Regulation 36A the withdrawal may be accepted as said in Brilliant Alloys Pvt Ltd v S Rajgopal. 6

Withdrawal Process Under IBC, 2016.

Moreover, Section 12A is based on strong fundamental prudential practice. In Bank of Baroda (as COC), Veda Biofel Ltd. v Mr. Sisir Kumar Appikatla, 7 under Section 29A, the resolution plan was approved with 96.39% majority but NCLAT noted that Mr Madhusudhan, one of the resolution applicants and Mr. P. Vijay Kumar, who is erstwhile promoter and MD of the CD entered into a settlement agreement under Section 12A. The NCLAT noted that the former MD was seeking a backdoor entry under the restructuring plan and they did not meet the requirements of Section 30(2). NCLAT declined to approve the resolution plan. Whereas in Maharashtra Seamless Ltd v Padmanbhan Venkatesh & Ors, 8 the approved Resolution Plan went on appeal to the NCLAT. The NCLAT directed to the applicants to increase the upfront payment to an average liquidation value. The NCLAT ruling was also appealed before the SC. The SC decided that there is no provision in the Code that prescribe matching the liquidation value and once COC approved the resolution plan, the NCLT/NCLAT ought to verify commercial wisdom of creditors. Also, Section 12A is not applicable to successful resolution applications.

The above cases discuss the threshold of ‘Out-of-Court Settlement’ in Stage 1, where the corporate debtor (CD) has full opportunity to settle or withdraw under Rules 8 and 11 and Stage 2 (Section 12A). However, after matters go beyond Stage 2, the corporate debtor (promoter, MD or original CD) misses the opportunity to take benefit under Section 12A. Moreover, the CD has put the company in such a distress situation, so beyond Stages 1 and 2, CDs willing to offer a bid look like a clear case of ‘willful default’ or ‘corporate fraud’. Therefore, the post Stage 2 clearly deterred the CD to settle dues. Therefore, the probability of settlement is higher in Stage 1 as detailed in the model section. Whereas, Stage 2 threshold of ‘Out of Court Settlement’ is after the constitution of COC till Issue of EOI as reflected in Figures 1–3. Therefore, the settlement or withdrawal under Section 12A post EOI issue is subject to the wisdom of the Adjudicating Authority and also depends upon circumstantial evidence. The cost of bidding process is high post-EOI stage or post Stage 2 (recovery amount + litigation cost) and the probability of succeeding in post Stage 2 is low. Finally, Section 12A ends at issue of EOI and there is no scope of using Section 12A after the approval of resolution as discussed in the above case.

Therefore, Rules 8 and 11 and Section 12A discuss the withdrawal of cases, which ultimately provide hope of recovery without court intervention and without compromising crore prudential principles of commercial wisdom.

To mitigate the stressed balance sheet problem caused by the Covid-19, on 5 June 2020, the government issued the IBC (Amendment) Ordinance, 2020. Two of the changes brought about in the amendments are relevant to our study. First, the moratorium on filing of cases under IBC and secondly, increase in the threshold from ₹1 lakh to ₹1 crore for filing a case.

In this section, we develop a model to analyse the dynamics of dispute settlement and adjudication under the IBC. The model offers several testable predictions.

Consider a creditor and a debtor. Creditors can be a ‘financial creditor’ or an ‘operational creditor’. The debtor can be a corporate, company or limited liability partnership firm. The debtor runs a business and has an outstanding debt, D, to the creditor. Let the monetary worth of business as an ongoing concern be denoted

Even if the business has high worth, the debtor can renege on the debt repayment schedule on account of some exigencies such as liquidity constraints or cyclical demand depression, or he could stop repayment guided by fraudulent considerations. While the debtor knows the strength of his business and his intentions, it is realistic to assume that the creditor does not have full information about the business’ worth. Formally, while the debtor knows his type—low value type or high value type—but the creditor does not know this. The level of debt

In the context of IBC-related disputes, we are interested in a situation where the debtor has reneged on the debt contract. Specifically, assume that the debtor still has an outstanding debt equal to

Therefore, the net expected gains for the creditor from adjudication will be

Plausibly,

The expected cost to the debtor of the adjudicated dispute will be at least

To keep the model simple, we consider two recovery scenarios. One, where

However, after an application has been filed under CIRP, the two parties can opt for OCS or withdrawal of application from the CIRP. The OCS can take place before as well as after a case has been accepted under IBC, for details see Rule 8, I & B (AA) and Rule 11, NCLT as discussed in Section 2. Recall, the creditor is not 100% fully sure about the repaying capacity of D. So, during the OCS, while the debtor is fully aware of the worth of business, the creditor has only a rough idea of the value of the business.

Following the mainstream models of negotiations under asymmetric information, we assume that the creditor makes a take it or leave it (TIOLI) demand from the debtor. Assume that the creditor knows the probability of full repayment by the debtor. Let,

In other words, C thinks that if the CIRP is completed, he will be fully repaid with probability

Of course, ability of the debtor to fully repay also depends on relative values of

During this stage, if creditor makes a TIOLI demand equal to

By definition the maximum possible recovery is

In view of the above, it can be seen that only plausible demand by the creditor are equal to

Recall, from the perspective of the creditor

Therefore, the creditor will prefer to demand

This means that as the probability

That is, we get the following result:

Recall, creditor’s estimate of

Plausibly, if the debtor’s business is of low-value type, the assessment will lead to the conclusion that

Argued as above, it can be shown that the creditor will still make demand for full recovery iff

Note when

Therefore, the inequality in Equation (3) will continue to hold. Hence, the belief of the creditor that they are dealing with a high-type debtor will be strengthened. So, the creditor will continue with his demand for

However, in case of low-value business, since

So, the above inequality in Equation (3) may not hold, even though Equation (2) holds. In that case, even though the creditor demanded full repayment at Stage 1, he will be better off lowering his demand to partial recovery. To see why, note that when

It should be noted that as long as assessment is imperfect, the probability of negotiations failing will be positive. That is, some cases will surely go unsettled.

In addition, we get the following result.

As discussed above, for given value of business

To see why, the recovery rate is higher for the OCS, note that during the OCS the settlement happens if the debtor complies with the demand for full recovery. Indeed, a debtor who can repay fully would like to settle the case because if he does not settle before the case is admitted then information about the disputes gets public and the creditors other than the one who has filed the case will also join to demand their dues. Therefore, the recovery demands will add up making it difficult for the debtor to meet them all. In case, he fails to meet these demands for recovery, the debtor faces the real risk of losing control of his business.

However, the low-type debtors cannot comply with the demand of full repayment. So, most of the unsettled disputes that go for litigation will involve debtors of low (insolvent) types, for whom

Based on predictions of our model, we can propose the following hypotheses:

H1: The probability of settlement decreases with the outstanding D. H2: The probability of OCS settlement is higher for operational creditors than for financial creditors. H3: The recovery rate is higher under OCS compared to the adjudication (resolution and liquidation).

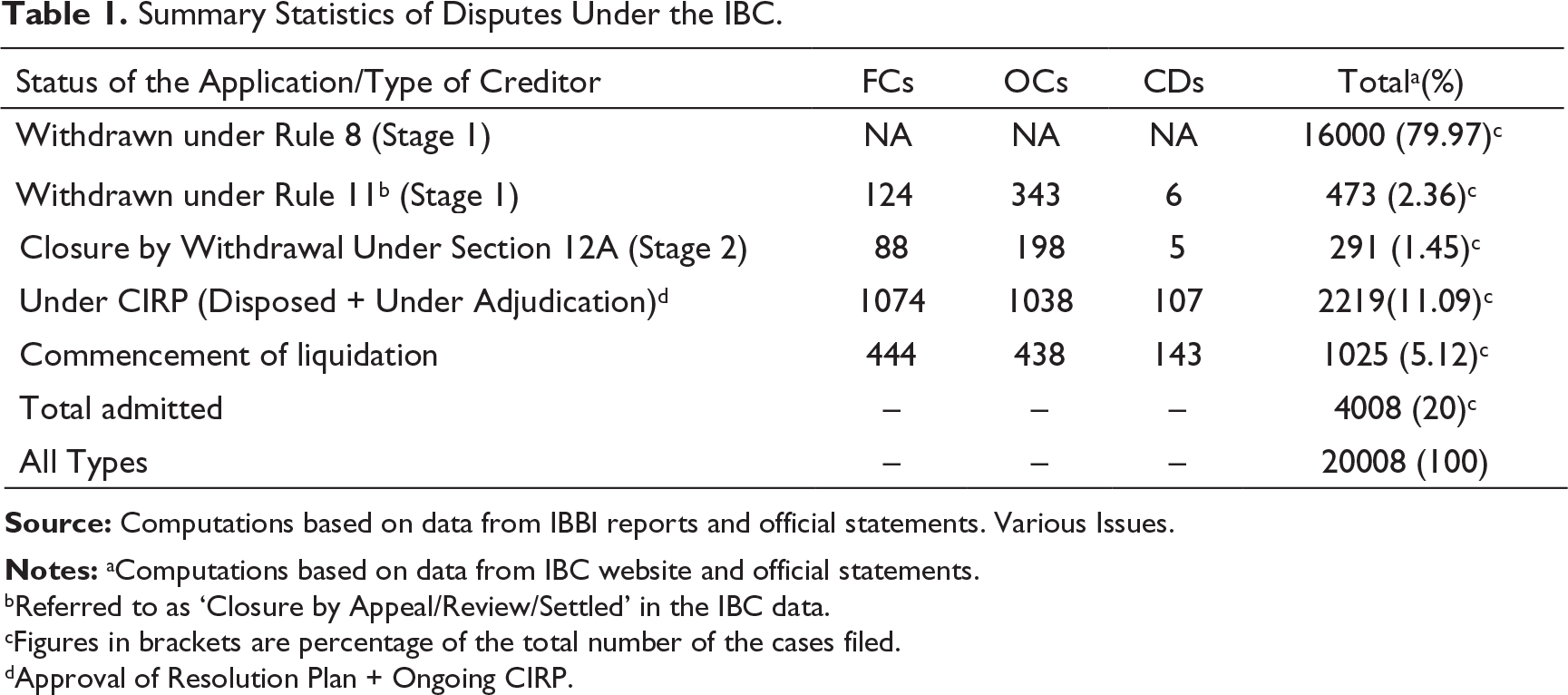

Summary Statistics of Disputes Under the IBC.

Summary Statistics of Disputes Under the IBC.

Source: Computations based on data from IBBI reports and official statements. Various Issues.

Notes: aComputations based on data from IBC website and official statements.

bReferred to as ‘Closure by Appeal/Review/Settled’ in the IBC data.

cFigures in brackets are percentage of the total number of the cases filed.

dApproval of Resolution Plan + Ongoing CIRP.

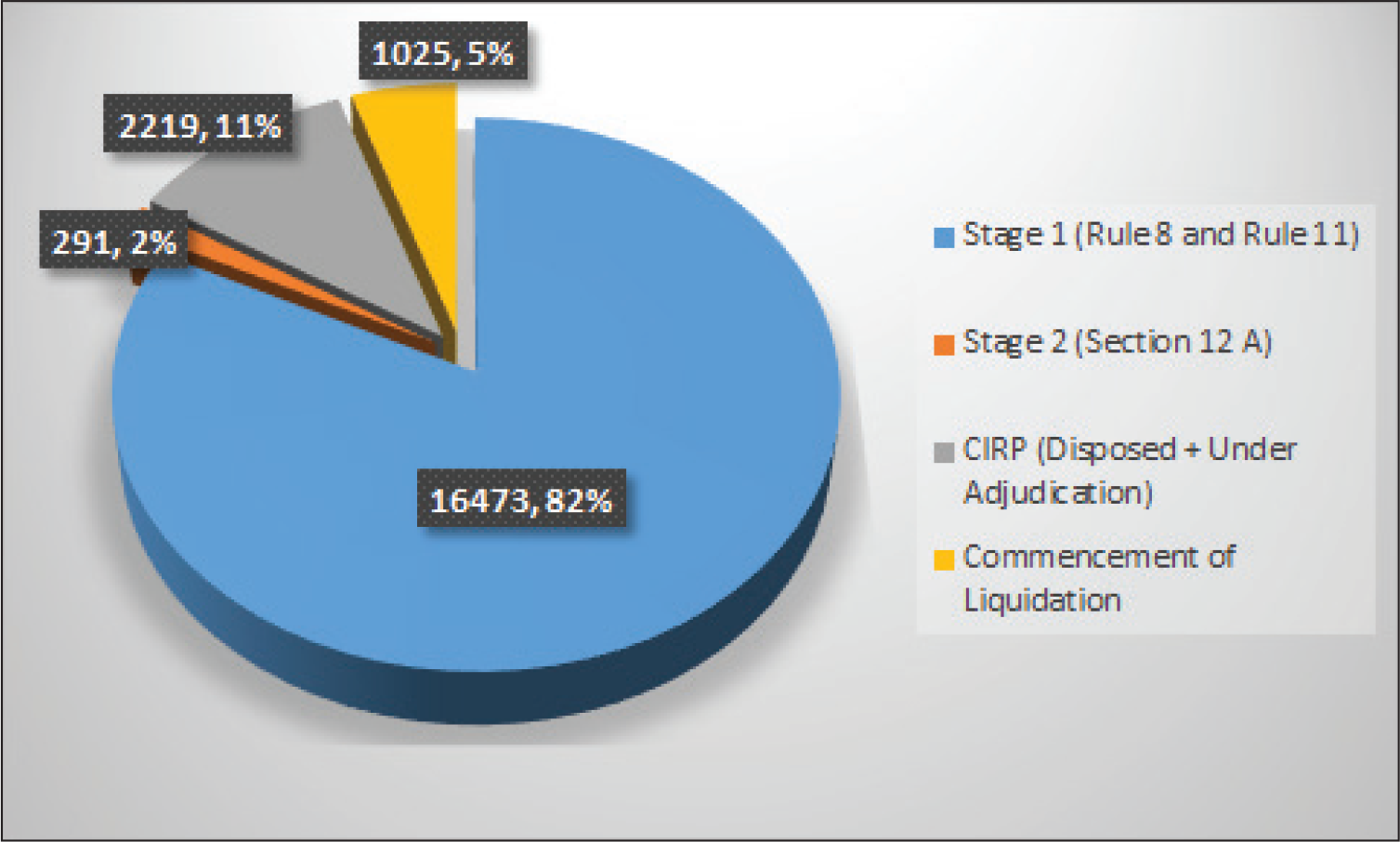

According to the Chairman of the Insolvency and Bankruptcy Board of India (IBBI), a total of 20,008 cases were filed of which 16,000 were withdrawn before they reached the admission stage (The Economic Times, 18 February 2021). 15 Therefore, only 4008 CIRPs had been admitted and initiated by the end of September 2020, as presented in Table 1. Of these, 473 have been closed on appeal or review or settled; 291 have been withdrawn; 1025 have ended in orders for liquidation and 277 have ended in approval of resolution plans. The rest are under adjudication. In other words, a really large number of applications under the IBC have been withdrawn under (Rules 8 and 11). An application is withdrawn if the parties reach a mutually agreed settlement of the disputes. In the terminology of our model, it means that about 80% of all disputes coming to NCLT have been settled through OCSs during Stage 1. 16 Some of the admitted disputes are also settled under Section 12A, that is, Stage 2 of our model. Together, in Stages 1 and 2 more than 80%of the applications are withdrawn owing to OCSs.

Summary Statistics of Disputes Under the IBC.

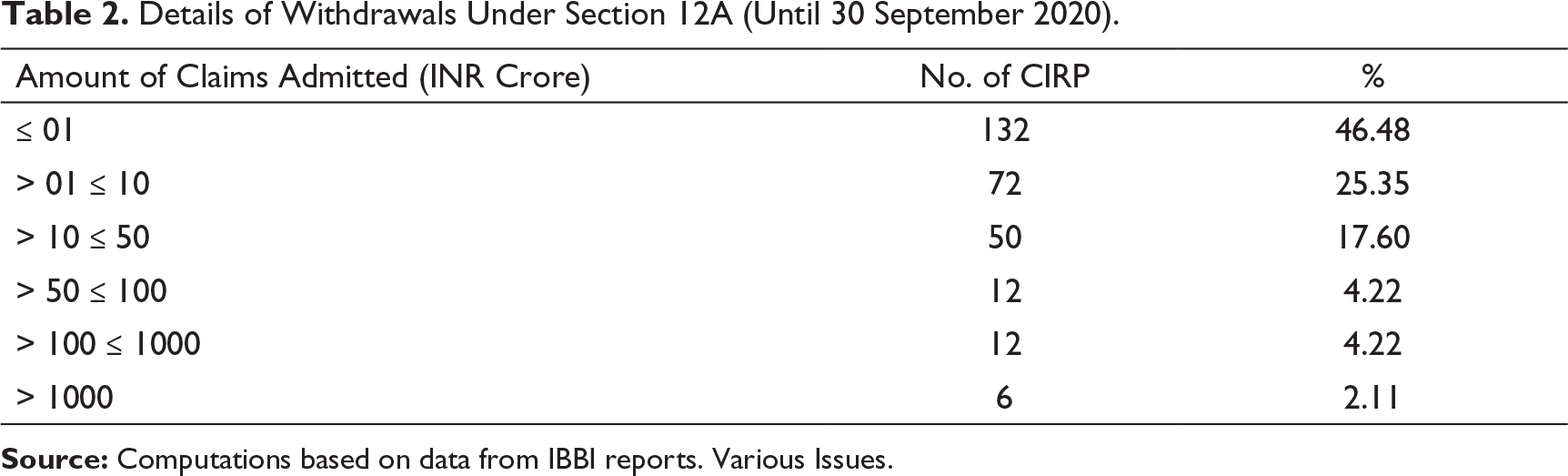

Details of Withdrawals Under Section 12A (Until 30 September 2020).

Source: Computations based on data from IBBI reports. Various Issues.

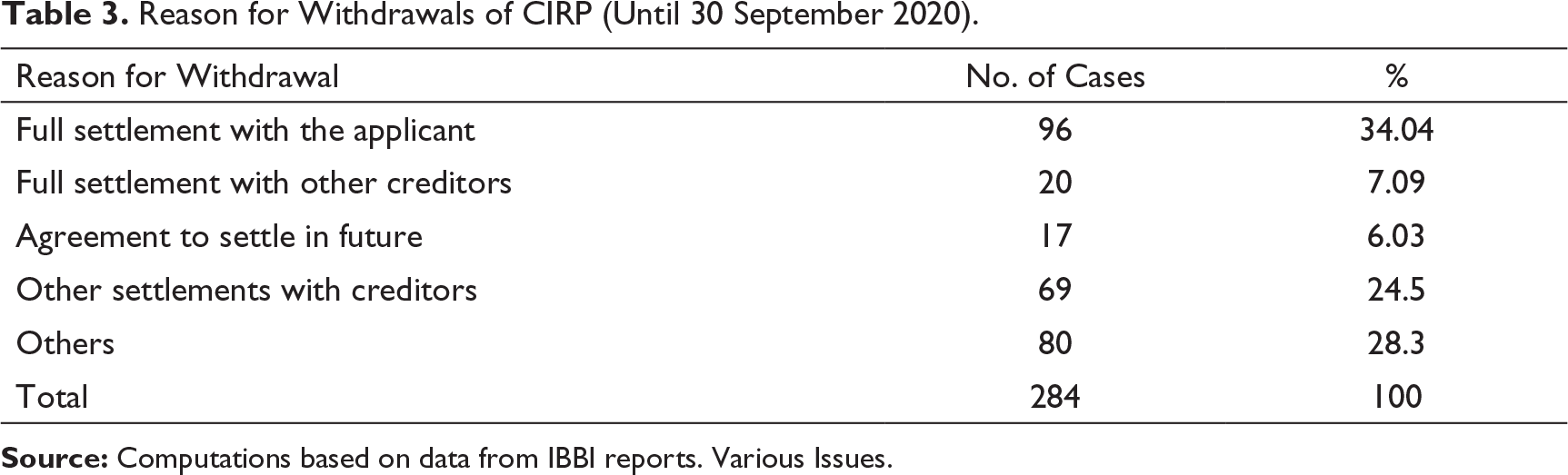

Reason for Withdrawals of CIRP (Until 30 September 2020).

Source: Computations based on data from IBBI reports. Various Issues.

Therefore, as is predicted by our model, it can be seen that the operational creditors with relatively small claims are able to use Rules 8 and 11 of NCLT and Section 12 A of IBC to recover their dues simply by filing cases and then settling the dispute under OCSs. In other words, in the pre-Covid world the NCLT has given significant bargaining power to operational creditors, who are mostly SMEs supplying inputs to bigger companies. This inference is also corroborated by the available information on this issue.

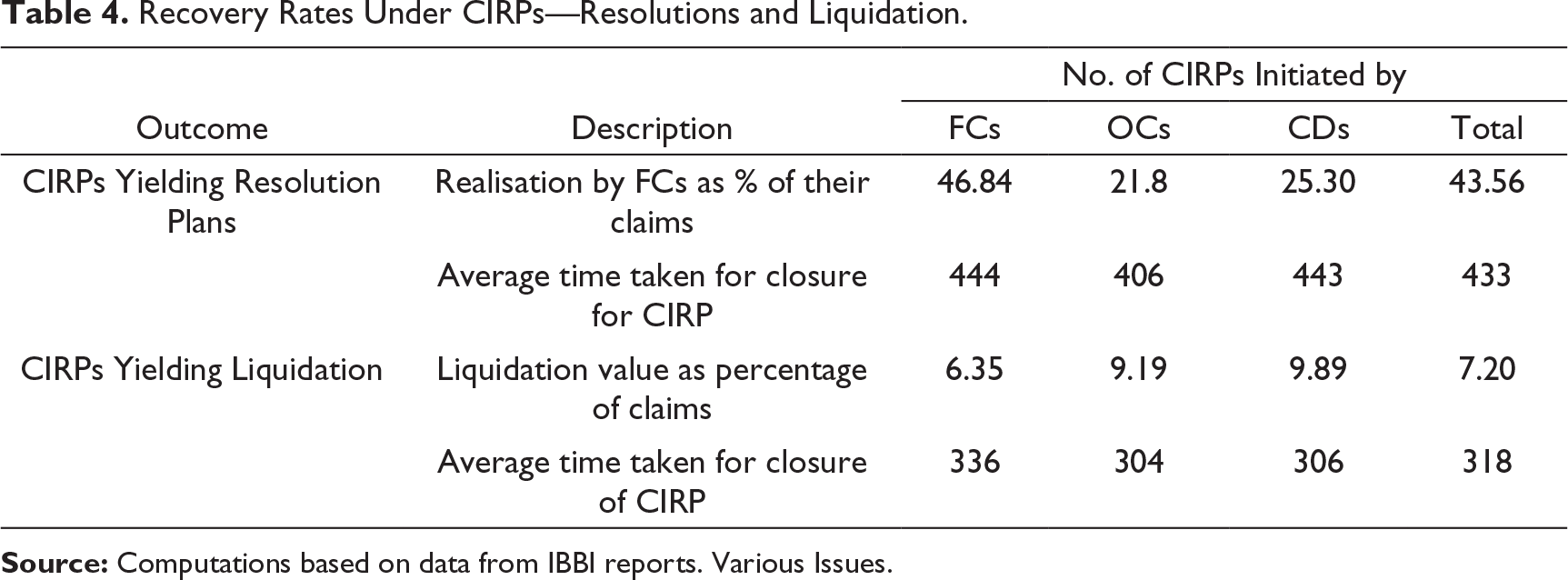

Recovery Rates Under CIRPs—Resolutions and Liquidation.

Source: Computations based on data from IBBI reports. Various Issues.

The Covid-19 has adversely affected many businesses. It has taken a heavy toll on business income of firms and companies, especially the SMEs and other small enterprises in the industry and service sectors see Leo & Singh (2020) and Singh & Leo (2021). 17 Many debtors—big as well as small—find themselves unable to service their debt. Given the severity and extent of impact of the pandemic, the RBI has issued a moratorium on equated monthly instalments and repayment of all term loans. Similarly, in an effort to ameliorate the distress situation of the debtors, Government of India has suspended the IBC. However, once these moratoria are lifted, the debtors will have to deal with piled up debts along with cumulative interest costs. Therefore, the number of debt and payment-related disputes are going to increase.

Our analysis suggests that compared to the pre-Covid period, the frequency of OCSs of debt and payment-related disputes are going to be much smaller in the post-Covid world. This will happen on two counts. First reason is related to the benefit of negotiations/settlement in the shadow of the CIRP. As explained earlier, one of the main benefits of the threat of the CIRP under IBC is that it incentivises many parties to settle their disputes at Stage 1 or Stage 2 discussed above. As is argued in the previous section as much as 75% of the cases seem to get settled through this channel. In the post-Covid world, however, due to the increase in the case filing threshold from ₹1 lakh to ₹1 crore, 18 a significant proportion of the disputes is not going to be filed before NCLT. Available indicators suggest that the SMEs and companies in catering, hospitality, tourism and many others are not going to be in a position to service their debt contract and/or make promised payments to their suppliers. This means that many disputes will not benefit from the negotiations in the shadow of the threat of the CIRP and hence will not be settled.

The second reason pertains to the effect of Covid-19 on the balance sheet of debtors. As mentioned earlier, many debtors across sectors have experienced a deterioration in the worth of their business and accumulation of the interests. In other words, the value of D relative to V has gone up. In view of Proposition 3, this means that even for the cases that will come to NCLT, the average probability of settlement is going to be smaller in the post-Covid world. This, in turn, has implications for the recovery rate for the creditors. Our analysis shows that the rate of recovery through CIRP is rather low, as under CIRP stressed companies are kept running for longer and costs of resolution get compounded. This problem is acute for firms engaged in engineering, procurement and construction (EPC) services as they lose the value of their assets fast. The pandemic has made the situation worse; therefore, the average recovery rate is expected to fall in the aftermath of the pandemic-induced moratorium. This will be true for operational creditors as well as the financial creditors.

In contrast, an OCS has the advantage of saving time and costs for the parties. It is partly for this reason that the rate of recovery is higher under the OCSs. Therefore, there is a strong case for encouraging OCSs by providing legal sanctity to the ‘pre-packaged deals’ or the ‘pre-packs’. A pre-pack is a restructuring plan agreed upon by the debtor and its creditors prior to filing of insolvency but the plan is meant to be sanctioned by a court of law or a tribunal. Under a pre-pack focus is on saving the business under the incumbent management until the agreement gets legal sanctity.

International experience from USA, Singapore and UK suggests that the informality of the process under pre-pack can help in a faster resolution of distressed businesses. Being informal in approach, a pre-pack provides flexibility to the stakeholders to work out a consensus-based plan for maximisation of business value, something that does not happen under the formal CIRP as can be seen from our analysis in the fourth section.

However, for the pre-packs to succeed as an effective vehicle for OCSs, it is crucial that pre-packs deals do make the unsecured creditors feel disenfranchised. This calls for transparency of the entire process, especially the valuation process so that the outcome is acceptable to all stakeholders. The legal and judicial certainties are going to be critical for the success of pre-packs For implications of legal uncertainty see (Singh, 2003 & Singh, 2004a). 19

Finally, our results imply that the increase in filing threshold is going to be detrimental to the interest of the small businesses. True, this legal change will provide temporary relief to some small businesses but will harm many others. For SMEs and small businesses, the debt levels tend to be small—less than 1 crore. Therefore, they will not be sued before NCLT. However, as a matter of fact, many small businesses serve as suppliers of goods and services to large companies and government agencies. In other words, the many small businesses are operational creditors to large companies and government departments. The credit claims of small businesses against big companies tend to be small (in a few lakhs). Media reports about on how the big companies and government agencies are withholding payments due to small vendors. The small businesses can do very little vis-a-vis the government. More importantly, because of the increased thresholds, these small businesses will not be able to bring their claims to NCLT. As discussed earlier, in the past NCLT has served as an effective instrument for recovery by small businesses from large companies. Unfortunately, this option will not be available to them now. The alternative channels of recovery are costlier and less effective. 20 Hence, the small businesses will suffer from the double whammy of fall in business income as well as non-recovery of their dues; the threat of their accounts turning NPAs is looming large.

The amendments to the IBC have implications for employees as well. There are reports of partial and substantial salary cuts by employers. Employees are considered as operational creditors under the IBC. In the past, they have been able to recover their salary from fraudulent or insolvent employers by filing a case before NCLT. However, under the increased threshold, they will not be able to do so and will be left uncompensated for their due wages.

Steering the economy through such large-scale toll taken by the Covid will require coordinated measures—fiscal, monetary and legal. As such, compared to legal processes, the public policy is better suited to deal with large-scale losses due to Covid. The litigation including the CIRP makes the losses a zero-sum game between debtors and creditors. In contrast, a suitably designed public policy can help balance the interests of the two sides and mitigate the general economic costs of the pandemic. Unsurprisingly, several countries have come out with public policy responses. For instance, the USA has enacted the Pandemic Risk Insurance Act, 2020 to establish a system of shared (public and private) compensation for business income losses during a pandemic. The government has undertaken to compensate losses exceeding a threshold amount fixed by the policy.

Similarly, the Danish Parliament has passed a law on salary compensation for companies affected by Covid-19. The government policy offers a temporary wage-funding scheme that prevents Covid-related layoffs in private companies. Besides, the government has offered a rescue package for companies losing at least 35% of their turnover due to Covid-19.

Singapore’s Covid-19 Temporary Measures Act, 2020 is another case in point. The Act provides for targeted protection to individuals and businesses unable to perform contractual obligations due to Covid-19. The public policy aims to balance the interest of all participants. It offers rental relief to eligible SMEs through government assistance and helps property owners facing cash-flow constraints through deferment of loan payments and waiver of property tax of up to 100%. Another good example of public policy approach is from the Republic of Germany. The Covid-19 Mitigation Act offers comprehensive protection to companies affected by the pandemic and offers them an opportunity to overcome insolvency. At the same time, it protects lenders from going insolvent.

In India, the moratoria issued by the RBI and the Centre have provided a temporary and partial cushion to the debtors and MSMEs. The subordinate debt scheme for stressed MSMEs has disbursement of only 28.3 crore against the target of 20,000 crore. For instance, the emergency credit-line guarantee scheme announced by Finance Ministry on 13 May 2020 has resulted in partial offtake by the MSMEs. However, the fiscal support to small businesses has left much to be desired. Clearly more can be done and should be done.

Footnotes

Acknowledgment

We are thankful to the referees and the editor for very helpful comments and suggestions. Nikita Gupta, Meghna Jain and Anchal Garg provided excellent research assistance. The institutional support by the Centre for Development Economics at the Delhi School of Economics and University of Delhi are gratefully acknowledged.

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship and/or publication of this article.