Abstract

The aim of this work is to analyze the factors that help companies avoid liquidation following the spirit of the Spanish insolvency law. This work focuses on the phase starting when companies file for bankruptcy and ending with the completion of the common phase. We apply the agency theory to explain how insolvency administrators and court characteristics influence the outcome of the bankruptcy process (liquidation or reorganization). We analyze unique accounting data from 2,627 companies that filed for bankruptcy during the period 2008–2014. The findings reveal the significant roles played by the liquidation trustee, Big 4 administrators, and higher remunerations, along with the type of court in charge. Processes are more likely to result in reorganization if they are handled by specialized courts, managed by the Big 4, and if the insolvency administrator has longer experience in bankruptcy filing and receives a higher remuneration. These findings have important implications for all the agents involved. It is necessary to rationalize the filing process, foment better training for insolvency administrators, provide courts with more funds, and create more specialized courts. The principal contribution of this article is to examine the role played by insolvency administrators and the courts, and their influence on the outcome of the insolvency process.

Introduction

In this article, we analyze the factors influencing the likelihood of reorganization within the Spanish bankruptcy law framework. Concerning low levels of reorganization in Spain, previous papers (Celentani et al., 2010; García-Posada Gómez and Vegas Sánchez, 2018) have reported that between 2004 and 2008, only 5% of bankrupt firms reached a reorganization agreement with their creditors. According to Van Hemmen Almanzor (2014), between 2006 and 2012, the annual percentage of reorganizations ranged between 5% and 10%. As stated by the Insolvency Proceeding Annuary, of all the companies involved in insolvency procedures, 6% of them were restructured in 2016, which is a similar percentage to that of the previous 10 years. These levels are extremely low compared to other countries, as pointed out by Arruñada (2021, p. 29), who argues that the low number of filings makes “Spain an anomaly at the international level.” In the Spanish context, the number of bankruptcies and the unemployment rate are closely related. In fact, these two variables evolve in the same way. While in 2008, the number of bankruptcies was 3,298, and the unemployment rate was 13.78%, in 2014, when bankruptcies increased to 6,564, the unemployment rate was 25.9% (INE, Instituto Nacional de Estadística: Spanish National Statistics Institute). Thus, in the short term, firm insolvencies account for significant job loss. Given the statements made by lawmakers and the statistics on insolvency procedures, the aim of the law has not been fulfilled.

Understanding how insolvency laws and their agents work is relevant because, as pointed out by Fu et al. (2020), insolvency recovery rates positively affect entrepreneurial activities and, consequently, a country’s wealth. Therefore, bankruptcy law is far from being a marginal subject, and it is not without academic debate. Some authors argue that crises can be beneficial, as they bring about Schumpeter’s creative destruction process. The two dominant theoretical schools in this field are Traditionalist and Proceduralist (Baird, 1998). Traditionalists, such as Korobkin (1992), defend that the aim of insolvency law should be to reorganize a financially distressed company and avoid liquidation to preserve the going-concern value of the company. However, proceduralists advocate for a market-determined process that avoids prolonging the life of unhealthy companies. Baird (1986) justifies that corporate reorganizations should take place if investors agree to a hypothetical sale of assets before the fact instead of a real one. Therefore, this author considers that the set of conditions making corporate reorganization preferable to corporate liquidation is extremely limited. Dou et al. (2021) quantify the efficiency of bankruptcy in the United States, identifying problems related to excessive liquidation, excessive reorganization, and problems of delay. While these authors do not give much importance to excessive liquidation, other authors, such as Antill (2022), advocate that excess liquidation plays an important role when it comes to bankruptcy efficiency.

In this article, we analyze the factors influencing the likelihood of reorganization within the Spanish bankruptcy law framework. The spirit of the law was “to decrease the duration of bankruptcy procedures and to increase the percentage of successful reorganizations” (García-Posada Gómez and Vegas Sánchez, 2018, p. 71). In Spain, companies with severe economic or financial problems can file for bankruptcy under the umbrella of the 2003 Bankruptcy Law. Filing for bankruptcy is a court-driven decision, as opposed to an out-of-court solution (voluntary liquidation, Mergers and Acquisitions (M&A), informal agreement, or an arrangement through the mortgage system). Filing for bankruptcy can be initiated with a petition filed by the debtor, which is the most common occurrence, or on behalf of creditors. Corporate governance is affected once the bankruptcy process begins, as management is controlled by an insolvency administrator appointed by the judge. This process is subject to special legislation with two possible outcomes determining different ownership rights: liquidation or reorganization (the equivalent to chapters 7 and 11, respectively, in US bankruptcy law) (Baird, 1986).

The current Spanish Bankruptcy Law (2003) merged the former Insolvency and Bankruptcy Laws that were in effect until 2004. This new law is intended to improve the efficiency of the whole process by incorporating a preventive phase called “prebankruptcy,” thereby avoiding process costs and delays. According to Urquía Grande et al. (2011), efficiency is achieved when economically viable debtors can reorganize, or economically unviable ones can liquidate, in the shortest time and at the least cost possible. Efficiency is lost due to two types of errors. Error I refers to the situation where companies that should be liquidated are allowed to continue. Error II appears when companies that should be reorganized are liquidated. Both type I and II errors occur frequently, as Bulow and Shoven (1978) illustrate in their work. Moreover, Dou et al. (2021) show that apart from excess liquidation and excess continuation, there can be another problem: excess delay. The spirit of the law seems to favor reorganization, avoiding unnecessary liquidations caused by delay.

This new law came into effect a few years before a terrible financial crisis broke out that affected all companies, both good and bad. This scenario seemed to verify the law’s utility. The failure of one firm could lead to the failure of those who supplied it with raw materials and those who acquired its finished products (García-Marí et al., 2016). Some authors believe that preventing this contagion is worth the cost of trying to keep a firm alive and justifies placing some costs on the firm’s secured creditors (Baird and Jackson, 2007). Buehler et al. (2012) find that bankruptcy rates are higher in regions with unfavorable business conditions. These adverse conditions could produce a domino effect and result in a massive type II error when the economic crisis is long and deep. Indeed, a recent article proposes increasing the number of bankruptcy judges to guarantee that they have enough time to treat each case appropriately (Iverson et al., 2021). When there are a large number of bankruptcy cases, courts are overwhelmed and cannot handle all the filings. This short-term, generalized type II error is what the 2003 law, and specifically its 2009 and 2012 amendments try to avoid.

Many authors have proposed theoretical models to justify improvements to the bankruptcy law (Aghion et al., 1992). Since the 2003 law came into effect, several studies have analyzed its efficiency (Aysun, 2015; López-Gutiérrez et al., 2011; Urquía Grande et al., 2011). They conclude that the law is inefficient due to an inappropriate definition of legal deadlines; refinancing agreements (Ara, 2014); the way insolvency is defined (Camacho-Miñano et al., 2013); a lack of creditor protection (Celentani et al., 2010); and inefficiencies that occur before, during, and after filing for bankruptcy (ex-ante, interim, and ex-post inefficiencies). More than 90% of the filings ended up in liquidation (Van Hemmen Almazor, 2016). This article adds to the previous literature about the analysis of the law’s outcome by incorporating variables that control for the insolvency administrator and the court where the company files for bankruptcy.

García-Posada Gómez and Vegas Sánchez (2018) for the Spanish case and Cepec et al. (2017) for the Slovenian case illustrate the important role that insolvency administrators play in the outcome of the bankruptcy process. Morrison (2007) highlights court characteristics in the US case, revealing that a shortage of funds and lack of economic expertise do matter when courts decide which firms should be liquidated or reorganized. In this work, we analyze the roles played by the insolvency administrator and the court assigned to carry out bankruptcy proceedings. There is a gap in the research about these two actors who play such important roles in this process due to their legal functions. According to Spanish law, once the insolvency process is initiated, the firm manager loses control of the company, as approval for any decision (i.e., payments) must be given by the court-appointed insolvency administrator. When it comes to property sales or layoffs, additional court approval is required. This article investigates the role of this special type of governance that goes into effect when filing. The literature about agency costs, beginning with Jensen and Meckling (1976), represents a huge body of research, but little has been studied about the implications stemming from the agency costs that may appear in this process.

Agency costs may play a determining role in the two possible outcomes of filing for bankruptcy: reorganization or liquidation. We focus on the court-driven process, hypothesizing that potential adverse selection and moral hazard costs (in addition to other indirect agency costs, like the agent’s lack of skill or effort) may influence the outcome. We consider the interest and characteristics of two key players (insolvency administrators and judges/courts). Our research questions are as follows: Does the type of insolvency administrator and their remuneration affect the likelihood of a company reorganizing? Does the rate of reorganization depend on the court to which the filing is assigned?

These two questions represent the novelty of this study. To answer them, a unique database has allowed us to gather information about the types of insolvency administrators, their remuneration, and the court where each specific procedure is held. The data also provide an economic and financial snapshot of the filing companies. Our database comprises companies that have filed for bankruptcy and have ended up either in reorganization or liquidation. The sample used in the regressions is made up of 2,627 companies, considering accounting information for the period 2008–2014. The years comprised in our database are in a homogeneous recession period. It is precisely in this type of period when the efficiency of this legislation is put to the test.

We find that both the type of insolvency administrator and their remuneration are important variables that affect the outcome of the whole process. The specific court in which the filing is considered also appears to be relevant in determining how the process will end. These findings are meaningful for both lawmakers and companies facing difficult times. Our study is part of the bankruptcy literature dealing with insolvency procedures and basing the phenomenon on the agency cost theory. We add to the limited number of studies focused on two main drivers of process outcomes: insolvency administrators and the courts. Ours is the only study incorporating variables related to these two factors concurrently.

The rest of the article is structured as follows. Section “Institutional setting and hypotheses development” deals with the theoretical framework and research hypotheses. Section “Sample, variables, and methodology” reports on the methods and the measurement of variables. Section “Results” shows and discusses the results of the statistical tests, and section “Discussion, conclusions, and limitations” concludes the article and gives indications for future research.

Institutional setting and hypotheses development

Spanish Bankruptcy Law 2003

The expressed objectives of the Bankruptcy Law are to preserve the economic activity, either completely or partially, of the company in question and maintain the company’s assets to maximize compensation to the creditors involved in the insolvency process. However, in reality, companies do not use the bankruptcy process to survive their crises (González Pascual and Gimeno Losilla, 2017). Empirical evidence shows there are fewer bankruptcy proceedings in Spain than in other countries. Therefore, a substantial number of insolvency proceedings are resolved outside the courts. The ratio of bankruptcy proceedings to companies in 2015 in Spain was 0.1%, compared to 2.1% in France (González Pascual and Gimeno Losilla, 2017).

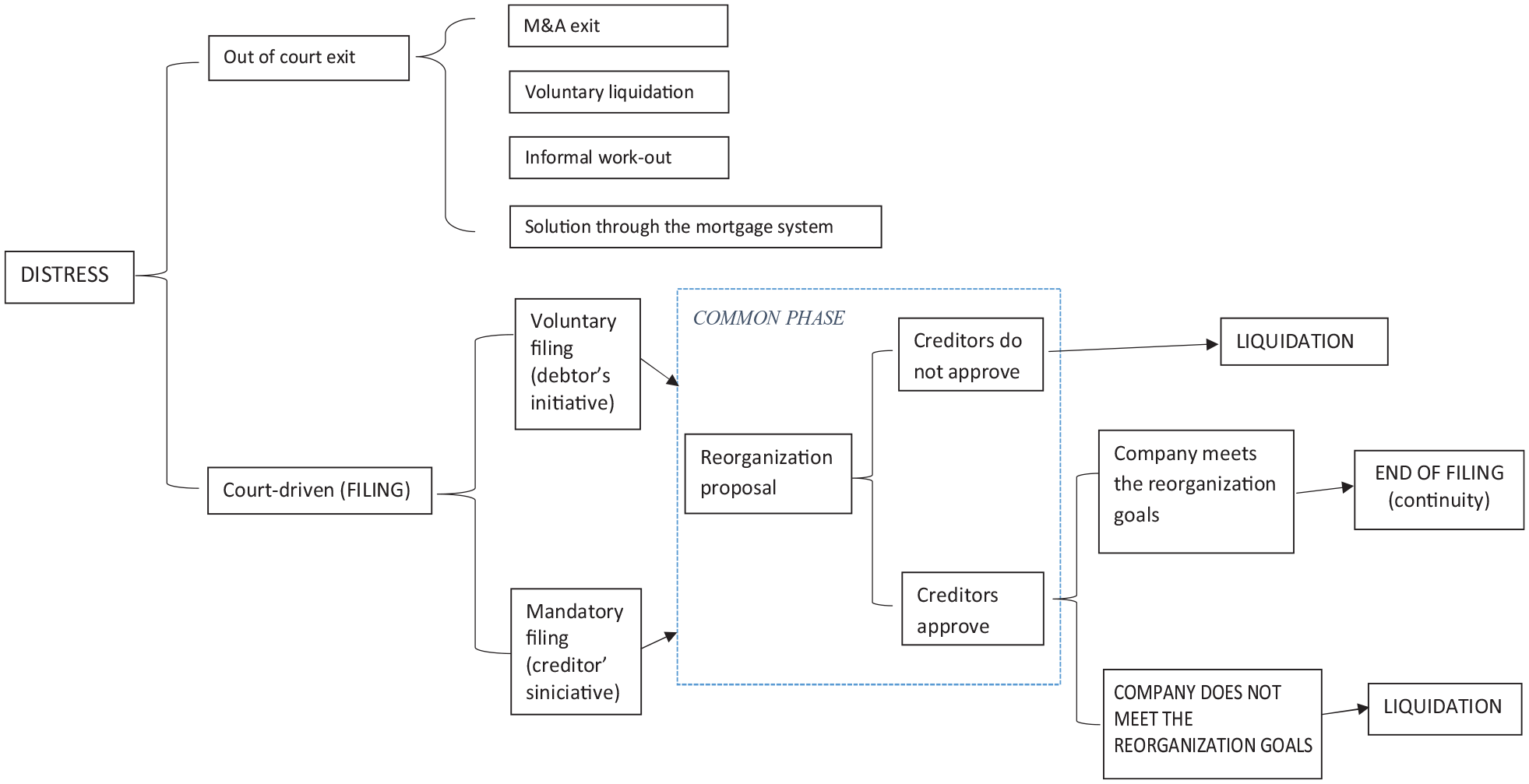

In Figure 1, we summarize all the potential routes that a troubled company can take. The latest major revision to Spanish bankruptcy legislation occurred in 2003 with the Bankruptcy Law that entered into effect at the end of 2004. The most important aspect of this legislation is the legal unity it establishes. This is to remedy the dispersed nature of the former bankruptcy legislation. With the new law, the same commercial court judge can manage the entire insolvency process in some regions, thereby avoiding the confusion and lack of knowledge that often occurred when a different judge managed each part of the process (claims, implementation, and seizure of companies’ assets) in civil procedures. This new legislation arose from the need for a regulatory framework that would make the processes of business failure simpler, quicker, more flexible, more modern, and more efficient (Fernández, 2004). After the law went into effect, the most important amendments were made in 2009 and 2012. The simplified procedures—cheaper and quicker legal processes—that were initially intended solely for small and medium-sized enterprises (SMEs) were expanded to all types of companies by these two reforms. However, neither the 2003 law nor its later amendments have achieved their objective since only 5% of companies have managed to avoid liquidation (Celentani et al., 2010).

Potential routes that a troubled company can take.

Paying attention to the court-driven roadmap, there are filings initiated by the debtor (voluntary) and initiated by creditors (mandatory). These two types of filings mark the beginning of the common phase. Mandatory filing is possible when there are two or more unpaid creditors. Voluntary filing is undertaken by the debtor when there is imminent or foreseeable insolvency. It must be requested by law, although it is usually applied for only when claims by creditors begin to appear. This type of filing considers that the insolvency administrator controls but does not substitute the company’s former management. Foreclosures are paused, and companies are entitled to reorganize. The difference between voluntary and mandatory filing is that when the latter enters the common phase, the insolvency administrator substitutes the company’s former management.

A more detailed explanation of the possible ways to initiate liquidation is given in Appendix 1, along with the interests and competencies of the rest of the stakeholders under the new law: creditors and debtors, who are not the key actors in our analyses.

Filing procedure agency costs

A company is an organization with different economic agents associated with its activity, and these agents may have different interests (Jensen & Meckling, 1976). An agency relationship exists when an economic agent, called the principal, requires the participation of another agent to fulfill their interests (Stucchi & Raygada, 2011). Many scenarios arise where the economic incentives for each of the parties differ as a result of the way companies are managed. In these situations, the literature about agency relationships mentions the agency costs or inefficiencies that may decrease company value. An example of an agency cost in the context of the bankruptcy process is when shareholders are reluctant to file for bankruptcy or liquidate a firm due to legal priority of claims (Cámara Turull, 2015). The same thing happens with managers, who may advocate for company’s continuity to avoid losing their jobs. These circumstances increase the probability of committing a type I error, favoring the continuation of a failed company when it should be liquidated. Franks and Loranth (2014) find that many bankrupt Hungarian firms were maintained as going concerns despite significant operating losses and low recovery rates. This occurred because of the specific allocation of control rights, which turned out to be crucial to the outcome of the process. Bernstein et al. (2019, p. 6) state that “conflicts of interests among claimholders, information asymmetry, and coordination costs in reorganization may lead to inefficient continuation and, in turn, to inefficient asset allocation.”

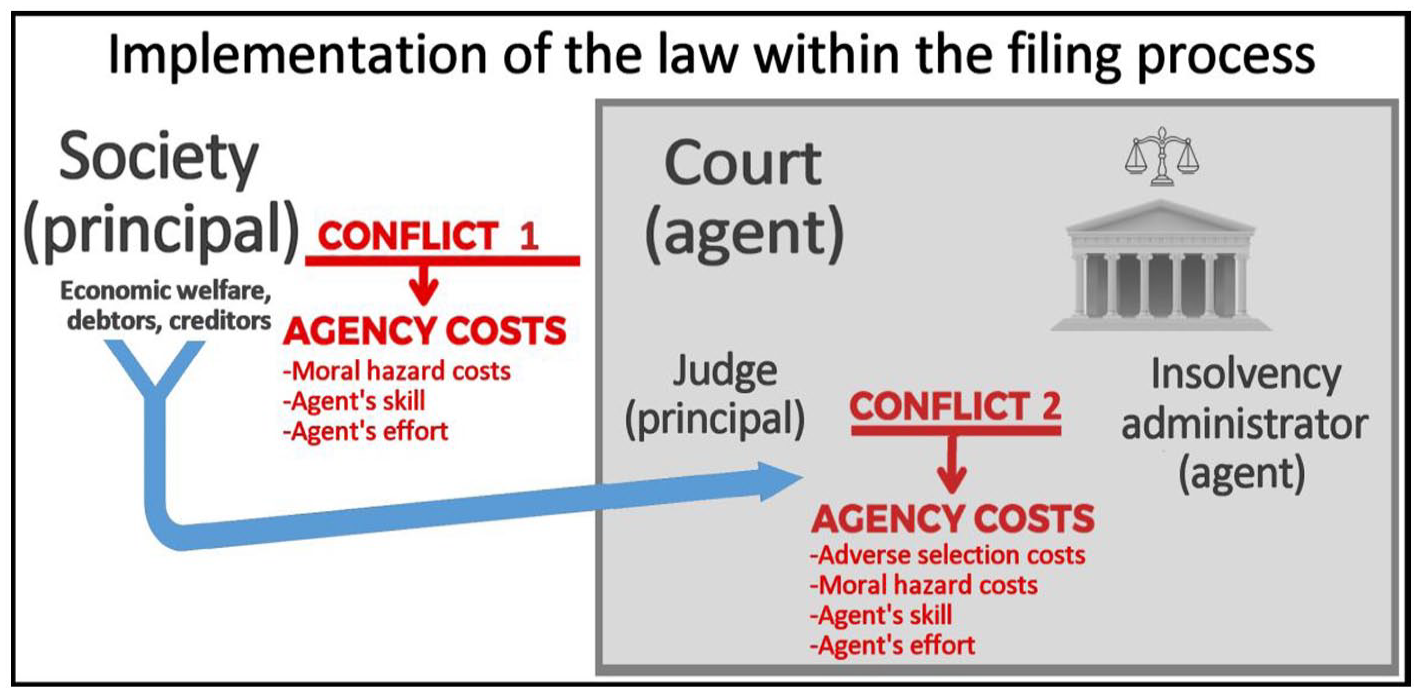

As mentioned in the previous section, in insolvency procedures in Spain, there is an unusual governance dictated by law a court-appointed insolvency administrator supervises or takes control of the firm from the beginning of the procedure. Consequently, a whole new scenario emerges, as illustrated in Figure 2. In terms of the agency relation framework, this process resembles the agency problems that can arise inside a company, as there are potential costs stemming from the agency conflicts between the managers and owners. However, other conflicts, with their respective costs, can emerge, such as those between the company and external investors, as in the case of banks (Stiglitz & Weiss, 1981).

Agency conflicts in the filing process under the bankruptcy law framework.

We will refer to judges and courts indiscriminately, as the first one directs and represents the second, and the inefficiencies and shortfalls of courts directly impact the work of the judge. The court/judge is a delegate responsible (agent) for enforcing the law in agency relationship 1 (Figure 2). The goal of the judiciary system is to enforce the law and safeguard the welfare of society. Specifically, commercial law aims to serve the needs of the commercial community and facilitate commercial activity (Irvine, 2001). This could mean liquidating companies that should be liquidated to avoid wasting limited resources or trying to restructure firms that merit this effort to maintain economic activity and employment. The insolvency administrator is clearly the agent, and the court or judge is the principal in agency conflict 2 (Figure 2). Among the parties in this process, we include debtors and creditors, who may influence relationship 2 (for example, when their approval is necessary to propose reorganization in the common phase).

The two parties we are focusing on are those who are agents in Conflicts 1 and 2 in Figure 2. In terms of the judge/court, the judicial system suffered from crippling backlogs during the entire period analyzed, as evidenced by a constant delay in proceedings (Defensor del Pueblo, 2016). This circumstance was worsened by the fact that not all jurisdictions have commercial courts. Some provinces employ civil courts for commercial cases instead of creating commercial courts. Out of 50 Spanish provinces, 16 have commercial courts (Madrid, Barcelona, Valencia, Cádiz, Málaga, Sevilla, Oviedo, Palma de Mallorca, Las Palmas de Gran Canaria, Santa Cruz, Alicante, La Coruña, Pontevedra, Murcia, San Sebastián, and Bilbao). The courts want the procedures to follow the letter of the law and legal precepts scrupulously. A short process with as few incidents (lawsuits deriving from the process), complaints, and opposition as possible is in the court’s interest. In contrast to the United States, debtors cannot choose the court in charge of bankruptcy proceedings in Spain. The company’s legal address determines the court where the proceedings will take place. Debtors can choose their lawyers, but the insolvency administrator takes control of the company decisions once the process begins.

The insolvency administrator is the judge’s delegated deputy. They should be exclusively concerned with the best outcome of the process to try to save economically viable companies and, in the case of liquidation, maximize the resources obtained in the process. However, given their lack of autonomy and legal guarantees, along with the courts’ interest in finishing the proceedings as quickly as possible, these agents have strong incentives to terminate processes and avoid any incidents or disfavor arising from formal or procedural issues. They increase the probability of being appointed in future proceedings if they rapidly and efficiently resolve the process. In Spain, judges are responsible for appointing insolvency administrators from a list of eligible candidates. Appointing an insolvency administrator is discretionary (Arruñada, 2021), and, as defined in Article 27 of the 2003 bankruptcy law, candidates are chosen from a pool. These candidates only need to register and meet certain requirements to become insolvency administrators. These requirements are being an economist, auditor, or lawyer, with more than 5 years of experience and with specific filing training/courses. The 2003 law dictates that the appointment decision should be made based on the candidate’s experience and the complexity of the specific filing procedure. In section 4 of the law, a mandatory ranked list based on insolvency administrators’ experience was laid out, and it was stressed that appointments should be objectively made, considering all the potential candidates in the pool and distributing appointments proportionately among them. In practice, however, this scheme has never been entirely developed, and it has never been more than a recommendation. Currently, courts rely on a basic list of candidates who meet the minimum requirements established by law; the appointment decision still resides solely with the judge. There are, however, some incompatibilities established to guarantee independence and objectivity. The insolvency administrator cannot have been disqualified from handling administration, cannot be related to the debtor, and cannot manage more than three filings in 2 years in the same court.

As in any other agency relation, adverse selection and moral hazard problems can arise. An adverse selection problem arises when an inefficient insolvency administrator is chosen due to information asymmetry and the judge’s lack of skill or expertise. Insolvency administrators should manage the filing in the most competent way, which implies acting in good faith and following the law (Implicit in Article 204, since it urges the insolvency administrator to preserve the value of the total assets in the most efficient way for filing). They are responsible only for acts or omissions contrary to bankruptcy law and the legal system in general (Article 94.1). The law can take action when insolvency administrators excessively delay reports, do not adequately respond to the information creditors or third parties require, unjustifiably extend the process, or clearly undervalue the debtor’s assets (Article 37). In these cases, judges can withdraw part or all of the insolvency administrator’s remuneration or even fire them and appoint a new one (Article 38). This firing may result in temporary or permanent disqualification. In practice, judges usually control delays and only reduce administrators’ remuneration or dismiss them when a creditor has filed a formal complaint about the insolvency administrator’s modus operandi.

Given the close oversight of insolvency administration and the severe consequences of malpractice, insolvency administrators are motivated to perform their duties effectively. In addition, since insolvency administrators are interested in gaining a reputation for efficiency to obtain future restructuring appointments, those perceived as skilled will be appointed more often. In spite of the regulatory sanctions and the reputational costs, moral hazard issues may appear when appointed insolvency administrators pursue their own interests instead of prioritizing public welfare (Arruñada, 2021). This is a problem because insolvency administrators are difficult to control once appointments have been made. Their power is greater than could appear from the strictly judicial point of view. In practice, when insolvency administrators recommend liquidation in their viability reports (common phase), the company is generally liquidated and the filing terminated. Moreover, the lack of cooperation with former managers in the case of mandatory filings means that insolvency administrators usually decide that companies should cease their activities. This nearly always results in liquidation. Another sort of moral hazard cost comes from the fact that an insolvency administrator’s remuneration when liquidating is preset. They are only paid for 12 months and only receive 50% of the remuneration during the last 6 months. Procedures that last longer are at the expense of the insolvency administrator’s time and effort. Thus, the insolvency administrator may be anxious to carry out a quick liquidation instead of considering a potential reorganization.

Previous literature coincides in pointing out the interest insolvency administrators have in earning the highest possible remuneration (Stucchi & Raygada, 2011) as one of the bases of the moral hazard problem. When an insolvency procedure is in course, the law should propitiate negotiation between the different parties to avoid the liquidation of economically viable firms (López-Gutiérrez et al., 2011). The moral hazard issue becomes more evident when this does not happen because bankruptcy laws either allocate significant control rights to third parties, such as judges or insolvency administrators, or allow them to mediate in allocating these rights to debtors and creditors (Ayotte & Yun, 2009), and these actors do not always pursue the same goal.

Insolvency administrator’s remuneration and type

As argued above, a relevant factor is the administrator’s remuneration, determined by Royal Decree 1860/2004. This remuneration is variable and depends on a percentage of the debtor’s assets and liabilities. Certain correction coefficients are applied to these percentages depending on, for example, the number of creditors (Articles 33 and 34). The insolvency administrator’s effort and, thus, the outcome of the filing process can be affected by this retribution (Moreno Serrano, 2010). The higher the remuneration, the greater the incentive to fulfill the commitments of the procedure and the more funds available to face the administrative costs of the insolvency proceeding. This is so because some of the costs have to be paid by the insolvency administrator, not by the company. Insolvency administrators have a series of responsibilities that oblige them to incur professional liability insurance costs, training, software and database purchases, travel expenses, extra employee costs, and commissioning other professionals to carry out appraisals, guard assets, respond to lawsuits, and prepare valuation and intermediation reports for asset disposal (Articles 78, 216, and 278 of TRLC [Royal Decree 1/2020, 5 May]). As with any activity, a well-paid professional is able to allocate economic and financial resources for better training/education, travel expenses, asset safekeeping and administration, more precise valuations, and asset disposal at the best price.

This is especially relevant in micro and small companies, as they usually lack a consolidated administration department and skilled staff to take charge of these tasks. Therefore, administrators have to carry out more tasks during the process, significantly affecting the relationship between effort and remuneration. Spanish law makes reorganization a more expensive and drawn-out process than liquidation. We believe that, from a moral hazard point of view, a higher remuneration diminishes the probability of mismanagement by the insolvency administrator and better aligns all the stakeholders’ interests. This discussion is also supported by the long-established argument in the agency relation literature (Akerlof, 1982; Fehr et al., 1993), where an emphasis is placed on the mutual exchange of a bigger reward to the agent in exchange for more non-contractual effort. This bigger reward will depend not only on the agent’s work but also on their skills. Consequently, our hypothesis is the following:

Hypothesis 1a: Higher retributions for insolvency administrators increase the probability of reorganization.

Considering the types of insolvency administrators, the existing literature evidences a different quality standard in Big 4 companies (PricewaterhouseCoopers, Ernst & Young, KPMG, and Deloitte), overall in auditing services (Defond & Zhang, 2014). Big 4 auditors improve the quality of the accounting information, and this reduces asymmetry information problems between the company and its creditors. One explanation for the negative relationship between Big 4 insolvency administrators and the probability of liquidation is that a high-quality insolvency trustee is a sign of credibility. If creditors are on the verge of refinancing or extending the terms of their debt contracts, they could lose trust in an administrator who is regarded as inferior since this could endanger their potential cash flows. The possibility of cheating creditors is greater if a company has been audited by a low-quality auditor (Sundgren, 2009). Big 4 administrators are more skilled and better able to anticipate future problems before filing for bankruptcy, thus converting the audit report into a valuable tool for insolvency evaluation (Muñoz Izquierdo et al., 2017).

We contend that the reputation, authority, and trustworthiness of Big 4 firms also hold true for insolvency management activities. If this is the case, filing companies administrated by the Big 4 could undergo fewer liquidations than those managed by non-Big 4 administrators. Specifically, for the case of bankruptcy procedures, Big 4 companies have more specialized staff, and they can often work exclusively on bankruptcy procedures. This could lead to greater professionalism and specialization. They most likely have more financial and administrative resources, allowing them to better carry out their activities as insolvency administrators from the very beginning. It is interesting to note that a company’s auditing firm can never be appointed as its insolvency administrator (Article 28 of the 2003 Law).

Although it could be argued that all professionals, individuals, or companies, large or small, are eager to preserve or increase their prestige, we contend that Big 4 insolvency administrators are particularly keen on preserving their reputation (to protect their professional standing and to be appointed again in similar procedures). In the auditing literature (a process similar to this that shares many actors, as argued before), some authors have found that large audit firms are more concerned about their reputation, and this has an impact on their relationship with the auditee (Cook et al., 2020). Moreover, the reputation of Big N auditors results in better conditions for the auditee in terms of borrowing (Ma et al., 2019). We argue that if the Big 4 have better reputations, they also have more to lose when intervening in insolvency filings. Moreover, the Big 4 wish to avoid the potentially high litigation costs provoked by these procedures (Aguiar-Díaz and Díaz-Díaz, 2015). Reputation acts, in this case, as a unifying factor that aligns different stakeholders’ interests. This quest for respectability should serve as a deterrent to potential opportunistic behavior, like unnecessarily lengthening the procedure. Based on these arguments, we propose the following hypothesis:

Hypothesis 1b: When the insolvency administrator belongs to a Big 4 firm, the probability of reorganization increases.

Role played by the judge/court

In the United States, debtors can choose where to file for bankruptcy, and bankruptcy outcomes vary greatly among bankruptcy judges. Some favor debtors, while others give preference to creditors (Bris et al., 2006; Chang & Schoar, 2013). This leads companies to file in pro-debtor courts named forum shops. Overall, 60% of large bankruptcy processes in the United States have been classified as forum shopping (LoPucki, 2005). Although debtors do not have such freedom when filing in Spain, what occurs in the United States shows that even when judges apply the same law, the specific court managing the bankruptcy process makes a difference. Judges, and the insolvency administrators they appoint, manage soft information about the company (e.g., the recent evolution of cash flows). Thus, their ability to make sound business decisions determines the efficiency of the process. Celentani et al. (2010) argue that with able third parties, there should be proportionally more reorganizations.

In search of greater specialization and professionalization, the 2003 law created commercial courts as a division of civil courts. This did not materialize homogeneously throughout Spain. Most likely due to resource allocation, said commercial courts were not created in some provinces. Instead, one of the existing civil courts was empowered to handle commercial court cases. What was instigated as a temporary arrangement is not likely to be the optimal solution. Lack of efficiency could be another agency cost, analogous to an agent’s lack of effort. Moreover, not appointing suitable insolvency administrators (because the judge/court is not skilled enough or does not spend enough time managing the filing) influences the possibility of a rapid solution and resolution in the different phases of the process. In fact, according to Wang (2012), judiciary efficiency is a major determinant in the outcome of the proceeding. This outcome can also be affected by the judge’s desire to finish the filing as soon as possible to alleviate court backlogs, thus creating a moral hazard cost. Inefficiency indirectly affects creditors, as it tends to discourage them from seeking reorganization. In our work, we hypothesize that the specific court in charge of the bankruptcy procedure may influence outcomes. The Consejo General del Poder Judicial (Spain’s General Council of the Judiciary, n.d.) statistics 1 point in this direction and find that the efficiency of the courts varies among provinces and from one court to another. Our hypothesis is defined as follows:

Hypothesis 2: Different courts result in different filing process outcomes.

Sample, model, and methodology

Sample

The sample of companies that have filed for bankruptcy has been obtained from the Infoconcursal database, which provides specific information about insolvency procedures. It includes information about the courts in charge of the procedures, insolvency administrators, date of filing, date of reorganization approval, date of liquidation, and identity of the distressed company. This last piece of information helps gather accounting information from the database provided by Bureau Van Dijk: SABI (Sistema de Análisis de Balances Ibéricos de Informa, S.A.).

To control for industry effects, we use industry-adjusted variables in some analyses. To do so, a large random sample of companies from SABI was used. With a balanced percentage of each of the sectors, we calculate the industry median. We take industry as the two-digit NACE-2009 code. The year previous to filing (t − 1), or 2 years previous to filing (t − 2) if there are no data for year t − 1, is used to compute the value of accounting ratios. This is to avoid some accounting operations related to filing, such as the conversion of all current liabilities to long-term debt. Incorrect data have been eliminated in most of the variables: for example, leverage ratio values higher than one, negative cash ratios, and so on. To avoid outliers, we have winsorized at the 95% level in some cases, for instance, the profitability ratios.

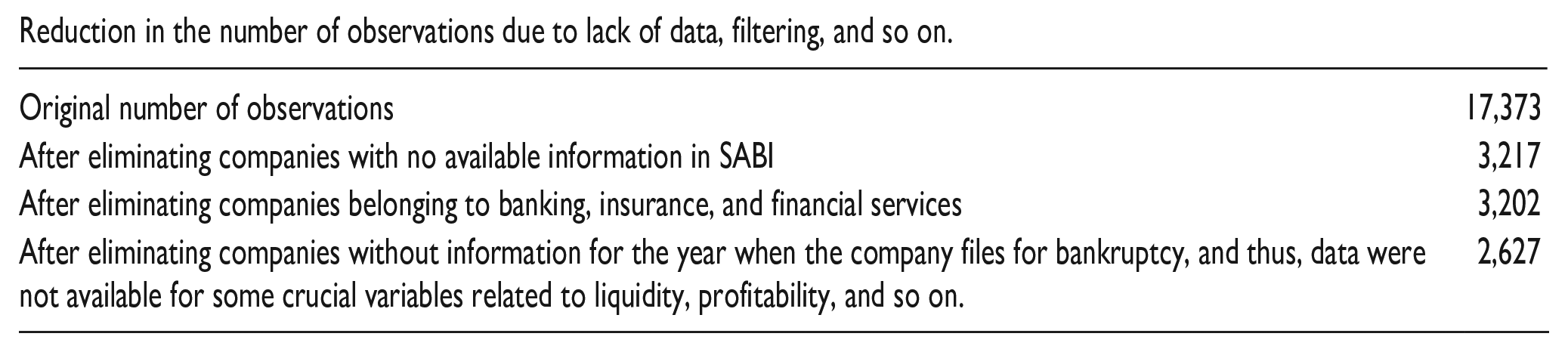

An initial dataset of 17,373 observations is reduced to 3,217 because not all the companies could be traced in SABI (see a summary of the applied reductions in Appendix 2). The total Spanish population for the analyzed period consists of 42,122 cases, according to the annual data supplied by the Instituto Nacional de Estadística 2020.

Model and methodology

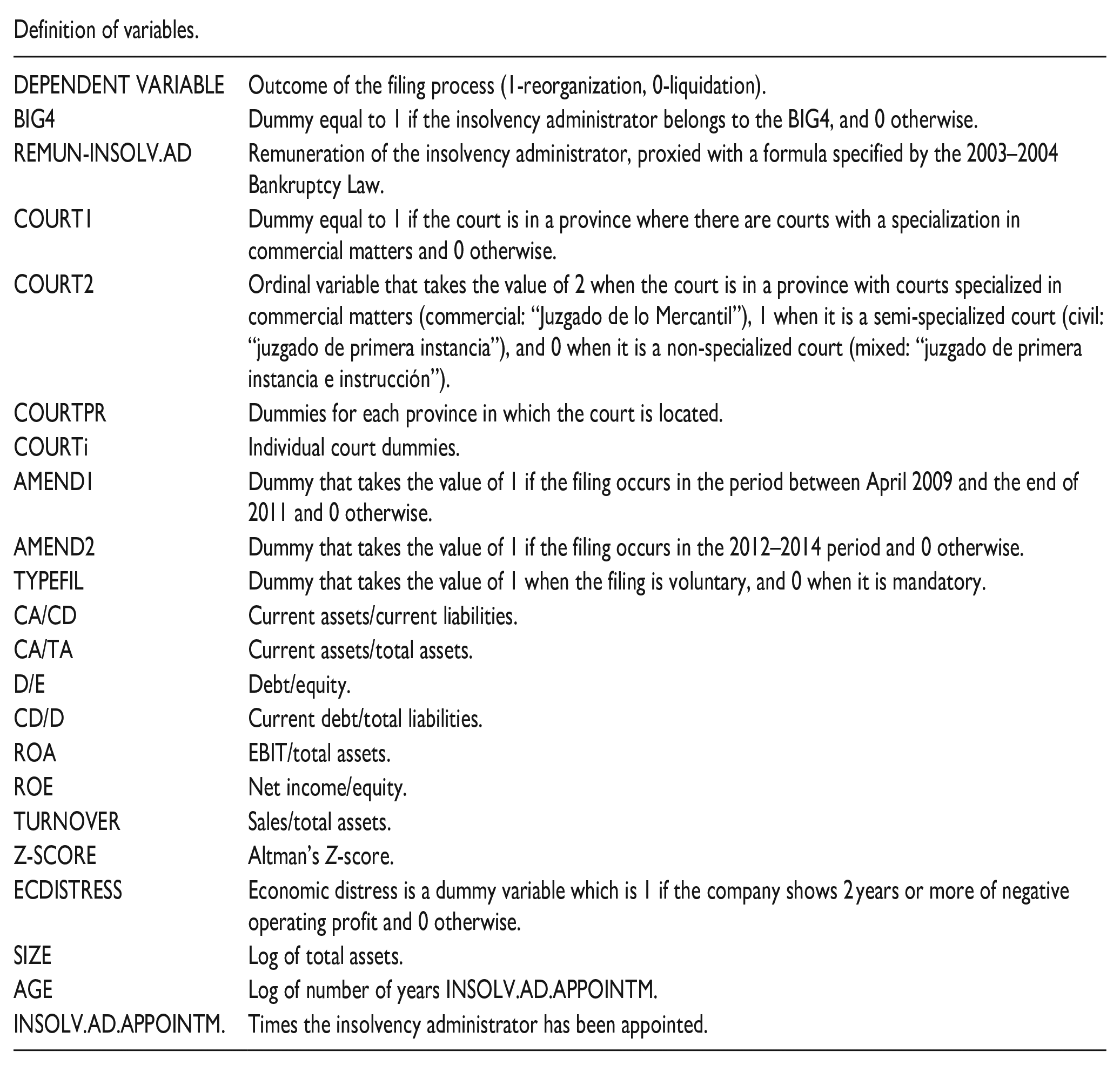

The dependent variable is the outcome of the filing process, which takes the value of 1 when the company restructures and 0 otherwise (definitive liquidation). In our database, a company is considered restructured when there is a date of approval for the reorganization plan and 0 otherwise (see the details of how this and the rest of the variables were computed in Appendix 3).

To contrast Hypothesis 1a, we have calculated the variable Remuneration of the insolvency administrator (REMUN-INSOLV.AD), proxied with a formula that takes legal specifications (Royal Decree 1860/2004) into account using the values of total assets and liabilities (in €1000) to determine a proxy for that remuneration. Regarding Hypothesis 1b, we have computed the dummy variable BIG4, which is 1 if the insolvency administrator belongs to one of the following firms: PWC (Pricewaterhousecoopers), EY (Ernst & Young), KPMG Lawyers, or Deloitte, and 0 in any other case.

Hypothesis 2 is verified with four sets of variables. Thus, our first variable (COURT1) is a dummy that takes the value of 1 if the court is in a province with courts specialized in commercial matters and 0 otherwise. The second variable (COURT2) is a more sophisticated version of COURT1 and is based on the name of the court. The “Juzgado de primera instancia” is exclusive to civil matters, so it is more specialized than “Juzgado de primera instancia e instrucción,” which is a general court that handles both civil and criminal cases. These more general courts are thought to lack specific knowledge in insolvency and commercial matters. The “Juzgado de primera instancia” may have little specific knowledge about bankruptcy matters, but these courts are considered to be knowledgeable about commercial and financial matters. This ordinal variable has three levels: specialized court (commercial: “Mercantil” takes the value of 2 when the court is placed in a province with courts specialized in commercial matters), semi-specialized court (civil: “Juzgado de primera instancia”) takes the value of 1, and non-specialized court (mixed: “Juzgado de primera instancia e instrucción”), which takes the value of 0. The third set of COURT variables considers dummies for each province (COURTPR), and the fourth group of variables consists of individual court dummies (COURTi).

Control variables

As we commented previously, this law has been amended several times. The two most important amendments were passed in 2009 and 2012. They aimed to make the whole process more efficient mainly by shortening the duration of its different phases. Consequently, AMEND1 and AMEND2 are two dummies that take the value of 1 if the filing takes place during the period the respective amendments went into effect: April 2009–end of 2011 and 2012–2014, respectively. According to the previous arguments regarding the law, an important distinction should be made depending on who initiates the bankruptcy filing. Thus, we include a dummy, TYPEFIL, which is equal to 1 if the filing is voluntary (voluntario), or 0 if it is mandatory (necesario).

Several studies have analyzed insolvency procedures in Spain, trying to identify the variables that best predict a firm’s probability of survival through the use of accounting ratios (Camacho-Miñano et al., 2015, among others). Ex-ante and interim efficiency are probably a reflection of the different economic and financial situations between companies that reorganize and those that end up in liquidation. Balcaen et al. (2012) state that the fact that companies had already experienced economic difficulties before filing can condition the outcome of the bankruptcy process. Moreover, the sample is probably a mixture of companies in very different circumstances, some more solvent than others. It may include profitable firms that are underperforming compared to their industry counterparts and unprofitable firms under threat of liquidation (Schweizer & Nienhaus, 2017). This heterogeneity should be reflected by a company’s financial status quo and thus has an impact on our dependent variable too.

The variables used to define a company’s economic and financial situations are grouped by factors reflecting the liquidity, solvency, profitability, and turnover of each company. Each of these factors, except for turnover, is summarized with two variables. Liquidity is established with the ratios of current assets/current liabilities (CA/CD) and current assets/total assets (CA/TA) (Brédart, 2014 and Camacho-Miñano et al., 2015). Solvency is proxied with the ratios of debt/equity (D/E) and current debt/total liabilities (CD/D) (Camacho-Miñano et al., 2015; Tian et al., 2015). The ratios of EBIT/total assets (ROA) and net income/Equity (ROE) are used to account for profitability (Altman, 1968; Camacho-Miñano et al., 2015). TURNOVER is represented as sales/total assets (Altman, 1968). We have included the Z-SCORE to control for the fact that even with insignificant individual ratios, what could matter is a company’s global situation. In addition, we have calculated the same variables adjusted by the industry median for robustness.

Based on the work by Balcaen et al. (2012), we proxy economic distress (ECDISTRESS) with a dummy variable of 1 if the company shows 2 years or more of negative operating profit and 0 otherwise. We use size and age, as these two variables are generally associated with the levels of information asymmetry (Sánchez-Vidal and Martín-Ugedo, 2012) or with the ability to grow (Jovanovic, 1982). They are proxied with the log of total assets for size and log of years since the creation for age (Bigelli et al., 2014; Giordani et al., 2014).

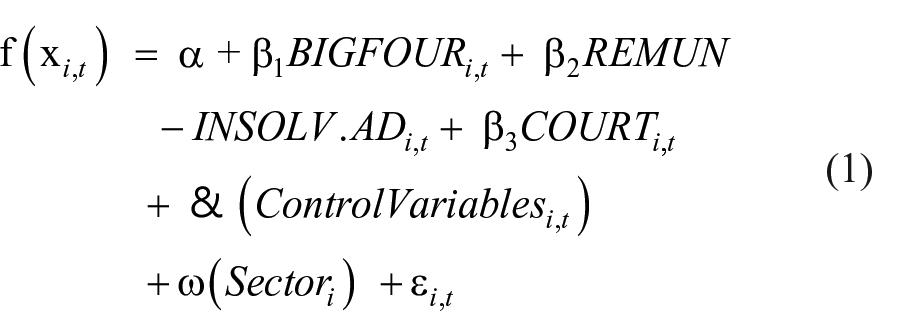

The formula of our omnibus model is:

As the dependent variable is binary, either the company goes to reorganization or to definitive liquidation, the analyses were done with a logit, which allows us to identify the important determinants of each particular outcome. Although we work with panel data, the outcome is a one-day-off event, which makes the data a cross-section database in practice. The analyses were carried out with Stata Software.

Results

Univariate analysis

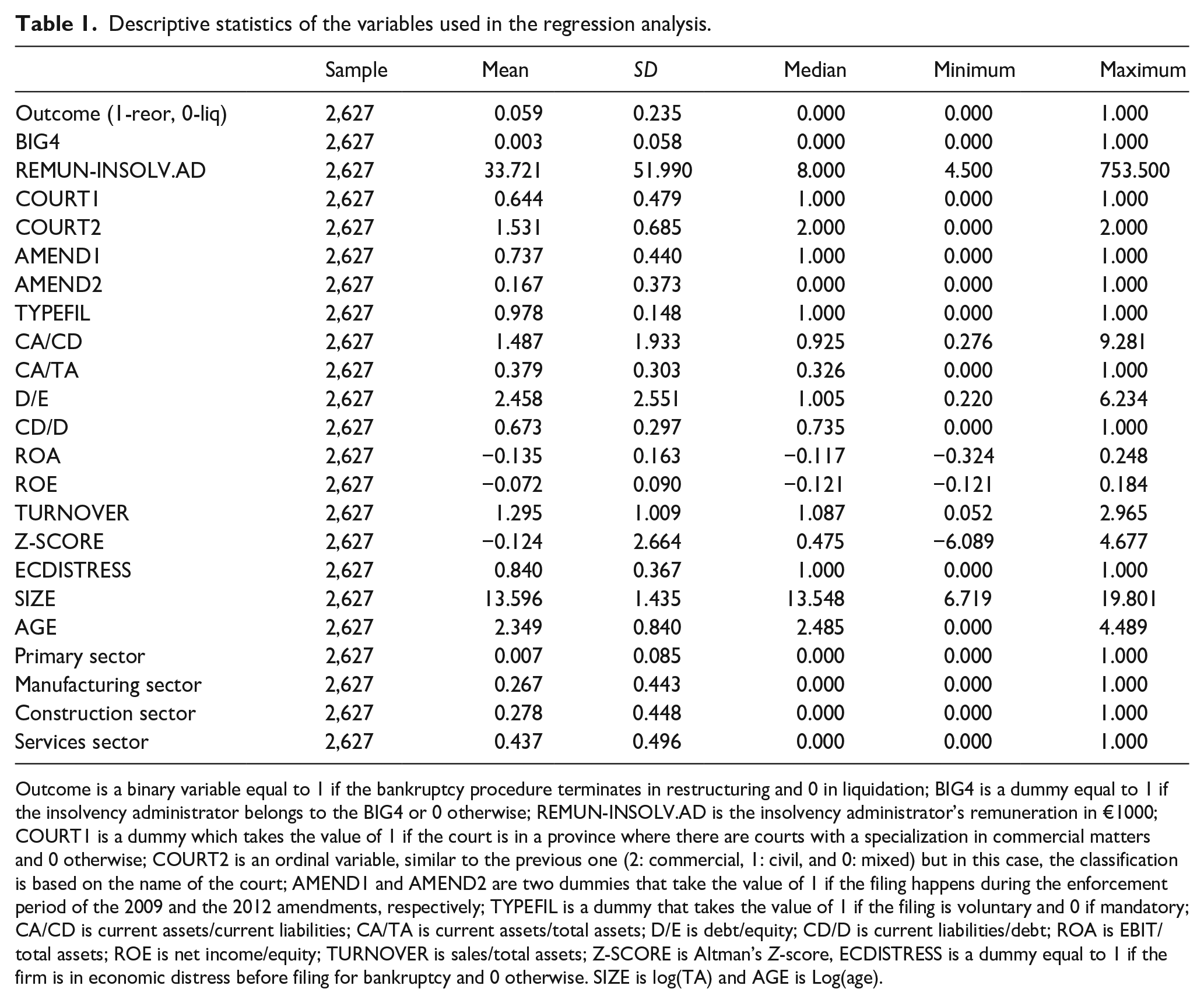

Table 1 reports the descriptive statistics of the variables used in the regression analyses. The first thing that draws our attention is the low number of filings ending in reorganization in the dependent variable of our analysis. Only 5.9% of the filings resulted in reorganization, which is similar to Celentani et al. (2010), whose database showed that in 11% of the cases, reorganization plans were presented, and only 5% of them were approved. There are other similar cases in nearby countries, such as Italy, with 4% of filings ending in reorganization (Celentani et al., 2010).

Descriptive statistics of the variables used in the regression analysis.

Outcome is a binary variable equal to 1 if the bankruptcy procedure terminates in restructuring and 0 in liquidation; BIG4 is a dummy equal to 1 if the insolvency administrator belongs to the BIG4 or 0 otherwise; REMUN-INSOLV.AD is the insolvency administrator’s remuneration in €1000; COURT1 is a dummy which takes the value of 1 if the court is in a province where there are courts with a specialization in commercial matters and 0 otherwise; COURT2 is an ordinal variable, similar to the previous one (2: commercial, 1: civil, and 0: mixed) but in this case, the classification is based on the name of the court; AMEND1 and AMEND2 are two dummies that take the value of 1 if the filing happens during the enforcement period of the 2009 and the 2012 amendments, respectively; TYPEFIL is a dummy that takes the value of 1 if the filing is voluntary and 0 if mandatory; CA/CD is current assets/current liabilities; CA/TA is current assets/total assets; D/E is debt/equity; CD/D is current liabilities/debt; ROA is EBIT/total assets; ROE is net income/equity; TURNOVER is sales/total assets; Z-SCORE is Altman’s Z-score, ECDISTRESS is a dummy equal to 1 if the firm is in economic distress before filing for bankruptcy and 0 otherwise. SIZE is log(TA) and AGE is Log(age).

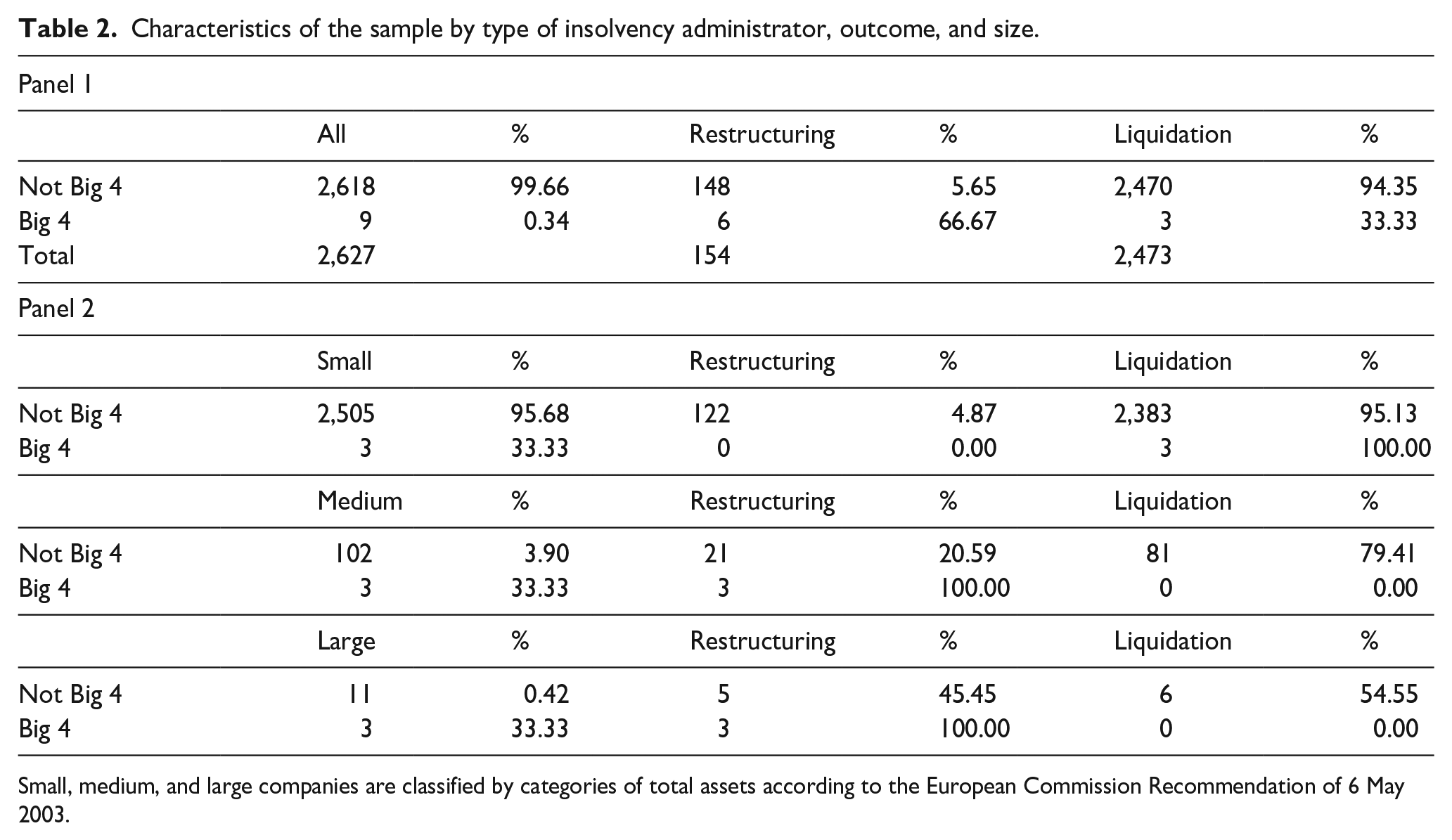

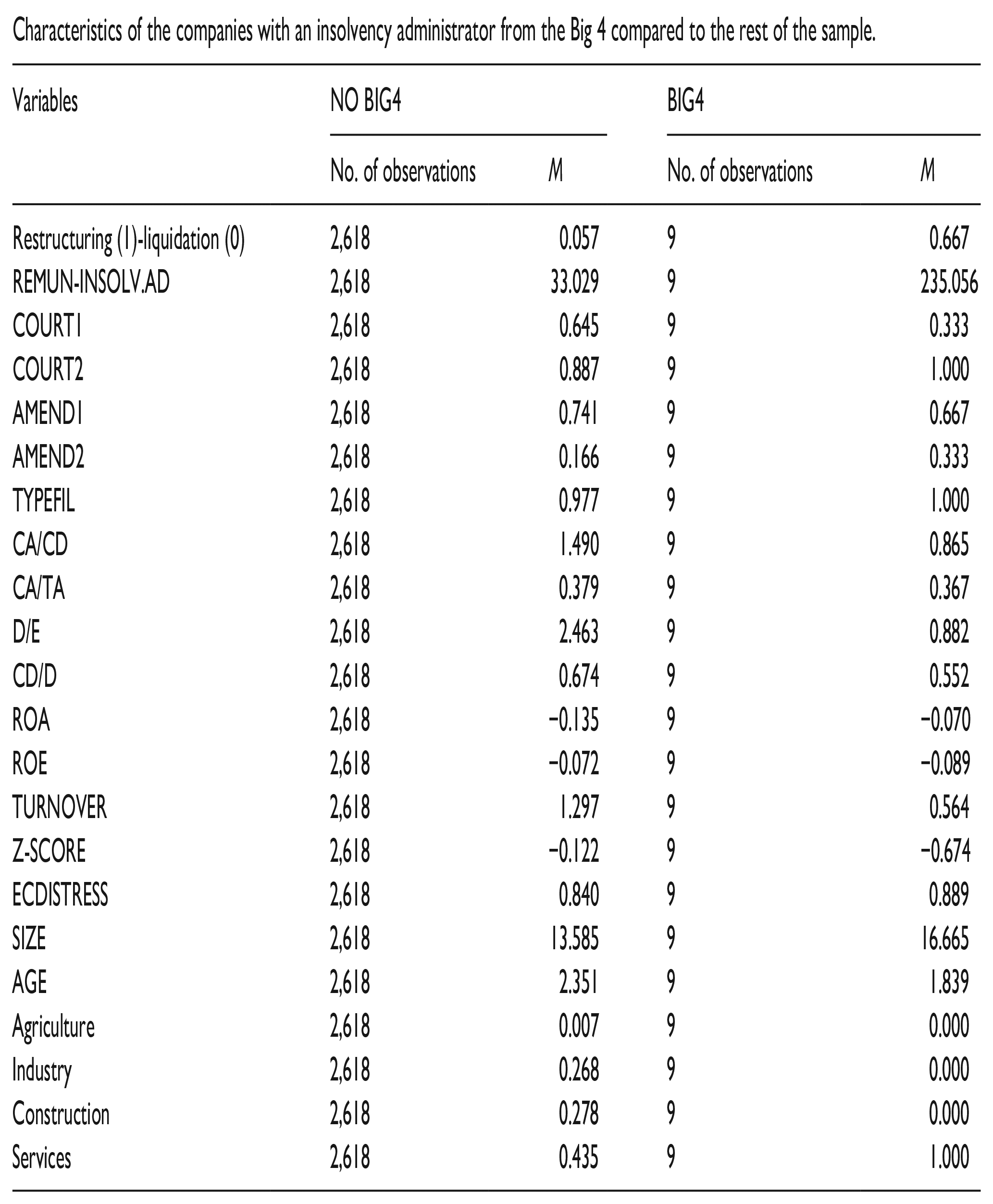

There are very few companies administered by the BIG4; the administrators’ remuneration shows a wide range of values, and more than half of the courts are specialized in commercial law, according to the two different proxies, COURT1 and COURT2. Few filings were initiated by the creditors, as can be seen from TYPEFIL. Due to low denominators, some ratios related to liquidity, solvency, and profitability show extreme values in some cases, even after winsorizing the more problematic values at 5%. These extreme values are typical in bankruptcy studies (López-Gutiérrez et al., 2015). The mean and median values for the CA/CD ratio show that, on average, companies have approximately the same level of CA as CD, and the mean suggests a positive value for working capital. Approximately 38% of the assets are current assets. D/E is quite high, showing that the companies are saddled with debt, primarily short-term liabilities (ratio CD/D). ROA and ROE show that, on average, filing companies have economic and financial problems. The Z-SCORE shows a negative value on average, which is logical for these unhealthy companies. The value for ECDISTRESS confirms that the majority of enterprises suffer from economic distress. Companies in the service sector are the most common; industry and construction each make up approximately one quarter of our sample, and roughly 1% of the companies belong to the primary sector. Concerning size, we find that the vast majority of our companies are small (95% of the sample). As in Park et al. (2010), we do not exclude large companies. These companies have some distinctive features that make them interesting for comparative reasons, as we shall see in the empirical evidence. From this information, it is clear that this study is focused on small and medium companies. Given that the BIG4 represents a small percentage of our sample, we consider it timely to explore how having a Big 4 firm running the insolvency administration interacts with the size factor and the different outcomes of the procedure in further detail. This information is in Table 2.

Characteristics of the sample by type of insolvency administrator, outcome, and size.

Small, medium, and large companies are classified by categories of total assets according to the European Commission Recommendation of 6 May 2003.

Even after considering the very low number of observations for companies represented by Big 4 insolvency administrators, their surprisingly high percentage of restructurings rather than liquidations implies that this is a factor worth considering. Filings by Big 4 administrators seem to involve much larger companies. This is indirect evidence that Big 4 companies have the reputation, resources, and skills to face large filings, as they are more likely to be appointed to larger firms filing for bankruptcy. A deeper analysis of the companies administrated by the Big 4 when they filed for bankruptcy is given in Appendix 4. The results show that the insolvency administrator’s remuneration is remarkably higher since the companies are much larger. They are all voluntary filings, have fewer current assets and less debt, but their Z-score is worse, and they are all from the service sector.

Multivariate analysis

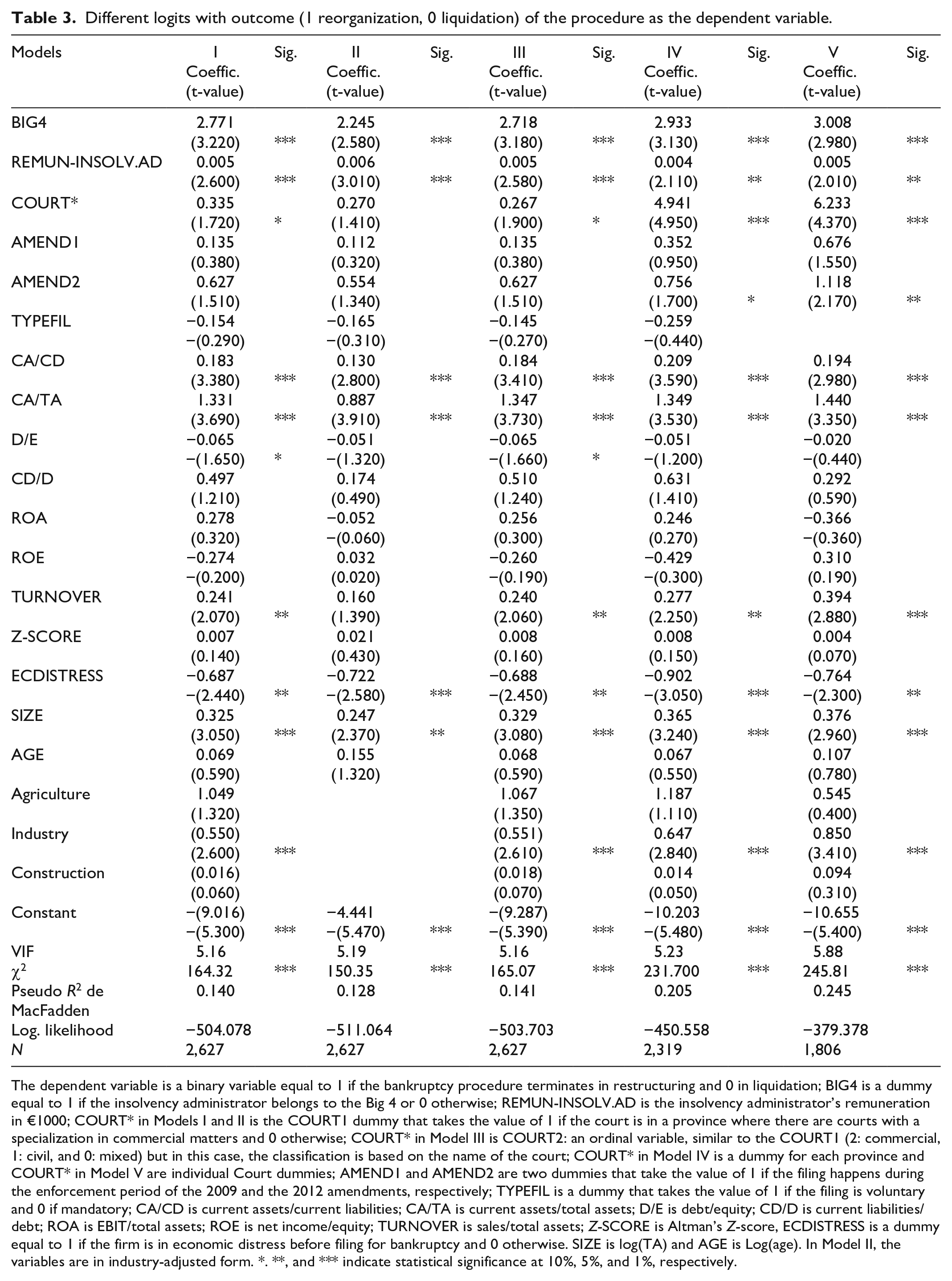

Table 3 shows the leading model with all the variables: those related to agency costs of insolvency administrators and judges/courts, the type of filing, the two dummies that account for the two amendments of the law, the ratios that define the financial conditions of the enterprise, Altman’s Z-SCORE, the dummy for economic distress, SIZE, AGE, and the industry dummies (which are typical in studies about company failure; Balcaen et al., 2012), leaving the service industry as the base dummy. In Model I, we incorporate all the variables along with the court dummy: COURT1. As some of the variables, especially all the firm-specific variables, can suffer from strong industry influence, we take industry-adjusted variables in Model II. Both Models I and II control for the problem of multicollinearity, as the variance inflation factor (VIF) is well under the critical value of 10 and very near the more prudent upper limit of 5.

Different logits with outcome (1 reorganization, 0 liquidation) of the procedure as the dependent variable.

The dependent variable is a binary variable equal to 1 if the bankruptcy procedure terminates in restructuring and 0 in liquidation; BIG4 is a dummy equal to 1 if the insolvency administrator belongs to the Big 4 or 0 otherwise; REMUN-INSOLV.AD is the insolvency administrator’s remuneration in €1000; COURT* in Models I and II is the COURT1 dummy that takes the value of 1 if the court is in a province where there are courts with a specialization in commercial matters and 0 otherwise; COURT* in Model III is COURT2: an ordinal variable, similar to the COURT1 (2: commercial, 1: civil, and 0: mixed) but in this case, the classification is based on the name of the court; COURT* in Model IV is a dummy for each province and COURT* in Model V are individual Court dummies; AMEND1 and AMEND2 are two dummies that take the value of 1 if the filing happens during the enforcement period of the 2009 and the 2012 amendments, respectively; TYPEFIL is a dummy that takes the value of 1 if the filing is voluntary and 0 if mandatory; CA/CD is current assets/current liabilities; CA/TA is current assets/total assets; D/E is debt/equity; CD/D is current liabilities/debt; ROA is EBIT/total assets; ROE is net income/equity; TURNOVER is sales/total assets; Z-SCORE is Altman’s Z-score, ECDISTRESS is a dummy equal to 1 if the firm is in economic distress before filing for bankruptcy and 0 otherwise. SIZE is log(TA) and AGE is Log(age). In Model II, the variables are in industry-adjusted form. *. **, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

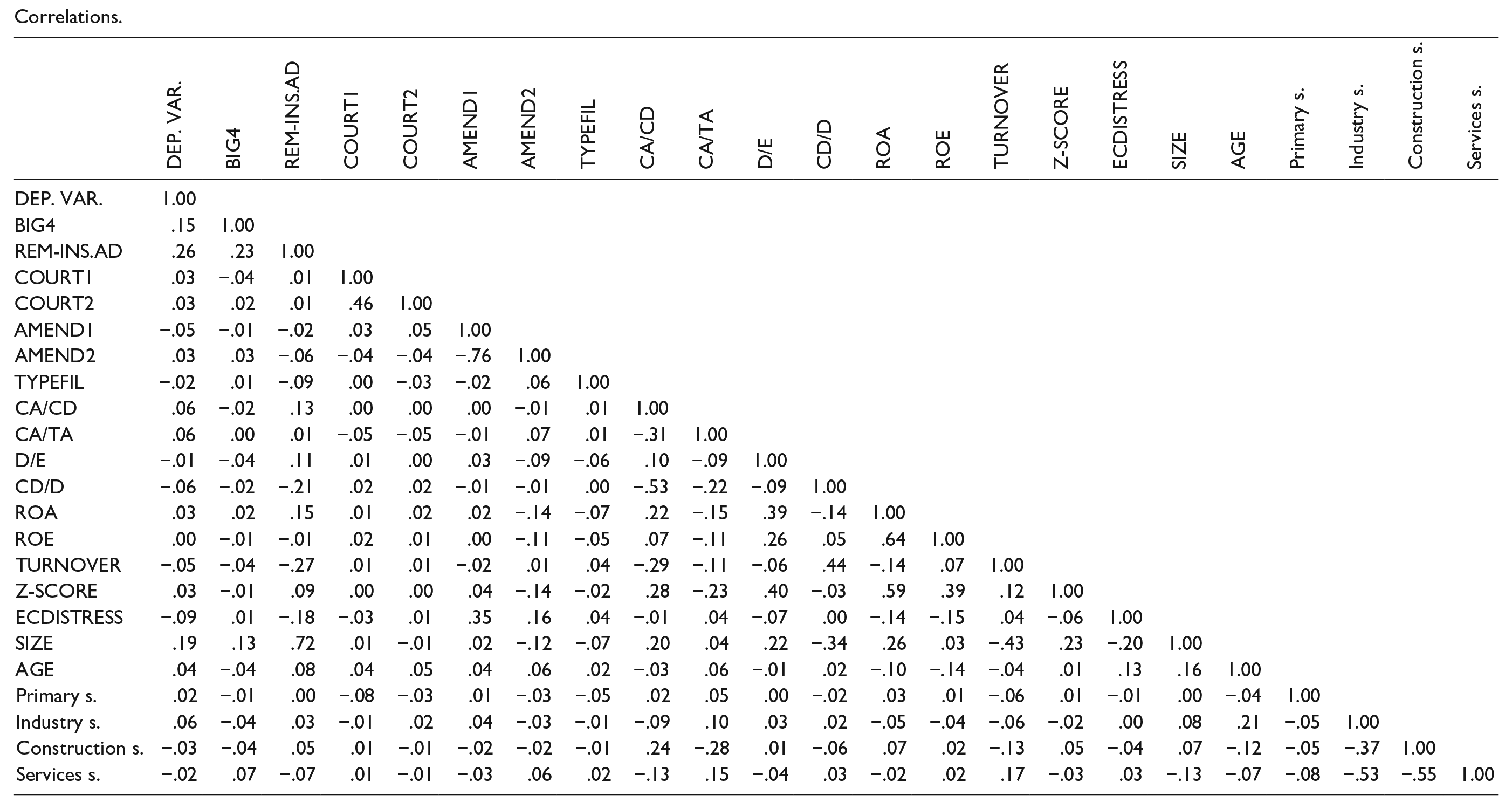

An overall look at the two models reveals that the results in terms of coefficient values and significance are quite stable. A potential higher standard deviation of the estimated coefficients is the most problematic consequence of multicollinearity. These results suggest this issue is not that important. The Big 4 and remuneration dummies are very significant. Remuneration and Big 4 are related to large companies (see the correlations table in Appendix 5), but in spite of these correlations and the fact that Big 4 administrated observations are quite low, when we run the regressions, all three variables are significant on their own, and the regressions do not have remarkable multicollinearity problems. This means that each variable contributes individually to the explanation of the model, and thus, even if we think that Big 4 companies may choose to manage the insolvencies of larger companies, that is, cherry-picking, remuneration still plays a role in this case. Nevertheless, given the small number of Big 4 companies in our study, our results concerning this group of insolvency administrators should be taken with caution, and further research should investigate this issue with a more representative sample.

The fact that these variables strongly influence the outcome makes these features desirable for small companies if policymakers are interested in increasing survival rates. The significance of size is also of interest. It suggests that small and medium companies are likely to end up in liquidation due to factors such as emotional pricing, meaning that small companies delay filing more than they should, which makes restructuring more difficult (Yamakawa and Cardon, 2017). Another cause of delay could be the social stigma SME managers face when filing (García-Alamán et al., 2016). Small companies are also more opaque, so insolvency administrators have to make greater efforts to do their job efficiently. Without all these barriers, more processes could end in reorganization instead of liquidation. Court characteristics reach 10% significance in Model I, which means that classifying according to the provinces with specialized courts makes sense and that this specialization is positive. The type of filing is surprisingly non-significant.

We can observe that the liquidity measures are significant: companies with proportionally more current assets than current liabilities and companies with more current assets than total assets are more likely to reorganize. These results are in line with Bisogno’s (2012), who found that the ratio that best differentiated between failed and non-failed firms was current assets to total assets. The combined result of these two ratios shows that it is better to have more working capital and fewer fixed assets. The negative sign for fixed assets could be explained by the fact that these assets are very probably associated with more operational risk and result in little room for maneuverability. However, fixed assets may serve as better collateral, and this should make the coefficient less negative (or more positive). Moreover, this collateral is only useful when liquidating; it is irrelevant for restructuring. This is very probably the reason why the combined effect is significantly negative. These results are robust after controlling for industry (with either dummies or using industry-adjusted variables).

Surprisingly, although the debt ratio (liabilities/equity) shows the expected sign, it is not highly significant (only at a 10% level), and the proportion of current liabilities to total liabilities is not significant. ROA and ROE are unexpectedly non-significant, indicating that in the event of filing for bankruptcy, profitability does not seem to influence the outcome of the procedure. One could think a priori that it should. The indirect costs of bankruptcy could erase any previous advantage on profitability, but, as explained in subsection “Sample,” the financial accounting ratios are calculated the year before the filing, so these ratios should not be affected by these costs. This conclusion is robust across the different models, and it probably indicates that when the insolvency procedure has started, there are other more important variables coming into play. This is the point of this article.

Higher turnover seems to push companies into restructuring, but we should take into account that this is probably a very industry-influenced ratio. When running Model II, the non-significance obtained for industry-adjusted turnover is not surprising. This evidence, combined with the significance of the industry dummy in most of the regressions, points to sector influence. This result is very similar to that found by Rico and Puig (2021), who show that belonging to the manufacturing sector is relevant. Size is always very significant, but age is not, and thus, the bigger the company, either young, mature, or old, the higher the probability of restructuring. Altman’s Z-score at the moment of filing for bankruptcy is not significant, which means that a global measure of insolvency is not important. However, some of its components, such as liquidity or solvency to a lesser extent, are significant. Camacho-Miñano et al. (2015) also find that sector, size, and the liquidity ratio are the leading variables that forecast insolvency.

The dummy for economic distress shows a logical sign for its coefficient. Companies with two or more years of economic distress usually end up in liquidation. The few companies for which this dummy is 0 would have probably been good candidates for the former suspension of payment filing before the current legislation merged this type of insolvency with bankruptcy in Spain. These candidates would also have had more likelihood of reorganizing.

We add Models III, IV, and V to explore the possibility that court specificities could be better approached with other proxies. Model III is the same as Model I, but the proxy for court is now an ordinal variable (COURT II) that takes the denomination of the court into account. The results of the regression are very similar to Model I, and the dummy for type of court is still significant at 10%. Proxying with province dummies explores different judiciary characteristics at a regional level in Model IV. As the number of dummies is high in this case, the statistical software omits some of them for multicollinearity reasons. We further eliminate one province: Madrid, which becomes the base case, to make the VIF lower. We only show the results for the most significant province (Seville). Other provinces that show highly positive significant coefficients are (in order) Barcelona, Soria, Pontevedra, and Lleida.

The results are again persistently stable both in the significance and signs of the coefficients. Using province dummies increases the explanatory power of the model remarkably. This increase is again confirmed in the last model, where we create an individual dummy for each court. Again, several dummies are omitted to control for multicollinearity, and we only show the most significant dummy, 64 (Juzgado de lo Mercantil nº 2 of Seville). Other courts that show remarkably positive coefficients are (in order) as follows: Juzgado de lo Mercantil nº 8 de Barcelona, Juzgado Mercantil nº 2 de Alicante, Juzgado de lo Mercantil nº 3 de Barcelona, and Juzgado de lo Mercantil nº 2 de Valencia. Other courts that do not participate in the regression of Model V due to their low number of filings (making them less representative) but with high reorganization percentages (more than a 45%) are as follows: Juzgado de lo Mercantil nº 1 de Toledo, Juzgado de lo Mercantil nº 2 de A Coruña, Juzgado de lo Mercantil nº 3 de Salamanca, Juzgado de lo Mercantil nº 6 de Barcelona, and Juzgado de primera instancia y mercantil nº 7 de Tarragona. All of them but one are Juzgados de lo Mercantil and, therefore, courts of provinces with specialization, with a value of COURT1 = 1 and COURT2 = 2.

The results are again constant for the rest of the variables. The 2012 amendment is the only one that seems to make a difference in Models IV and V. The type of filing is omitted from the analysis for multicollinearity reasons in Model V. When looking at the internal financial situation of a company, the ratios of solvency and, overall, liquidity are the ones that matter. Thus, some results are worth mentioning. Profitability is stubbornly insignificant, which is surprising. The D/E ratio is also insignificant, which means that overleverage (an especially serious problem for SMEs during these years, Lawless & McCann, 2011) is not an issue. Larger companies tend to restructure more than smaller ones. AGE is not relevant, as in Rico et al. (2021), nor is Altman’s Z-score. The dummy for economic distress serves to predict the outcome. Taking a general overview, we observe that the gain of overall significance reflected in χ2 is exclusively due to different definitions of the variable COURT, and we notice that remuneration tends to lose significance when COURT gains it

The results for the most important variables of this work show that the BIG4 dummy and the remuneration of the insolvency administrator confirm that there are agency costs in insolvency procedures. The different dummies that have proxied for court characteristics are significant and raise the overall significance of the model. This implies that the luck and randomness of the court assigned for the bankruptcy proceeding could determine a company’s possibility of survival. The most appealing result lies in the fact that in Models IV and V, which show a rise in overall significance, some variables, such as administrator remuneration, lose quite a lot of significance. This means that the dummies that reflect court characteristics in more detail, such as COURTPR and COURTi, steal part of the limelight from these variables. The only variable that gains significance is AMEND2, which means that this variable is more powerful when more detail is included in the court definition (thus, some judges/courts make better use of the Bankruptcy law amendments than others).

The overall results show that once the procedure is initiated, the profitability of the company when beginning the procedure does not matter. Only the liquidity and solvency ratios are important, which is shocking. This implies that to achieve a positive outcome (restructuring), not only economic factors are important. There are factors that depend on managers’ decisions, but there are others that are totally out of their control.

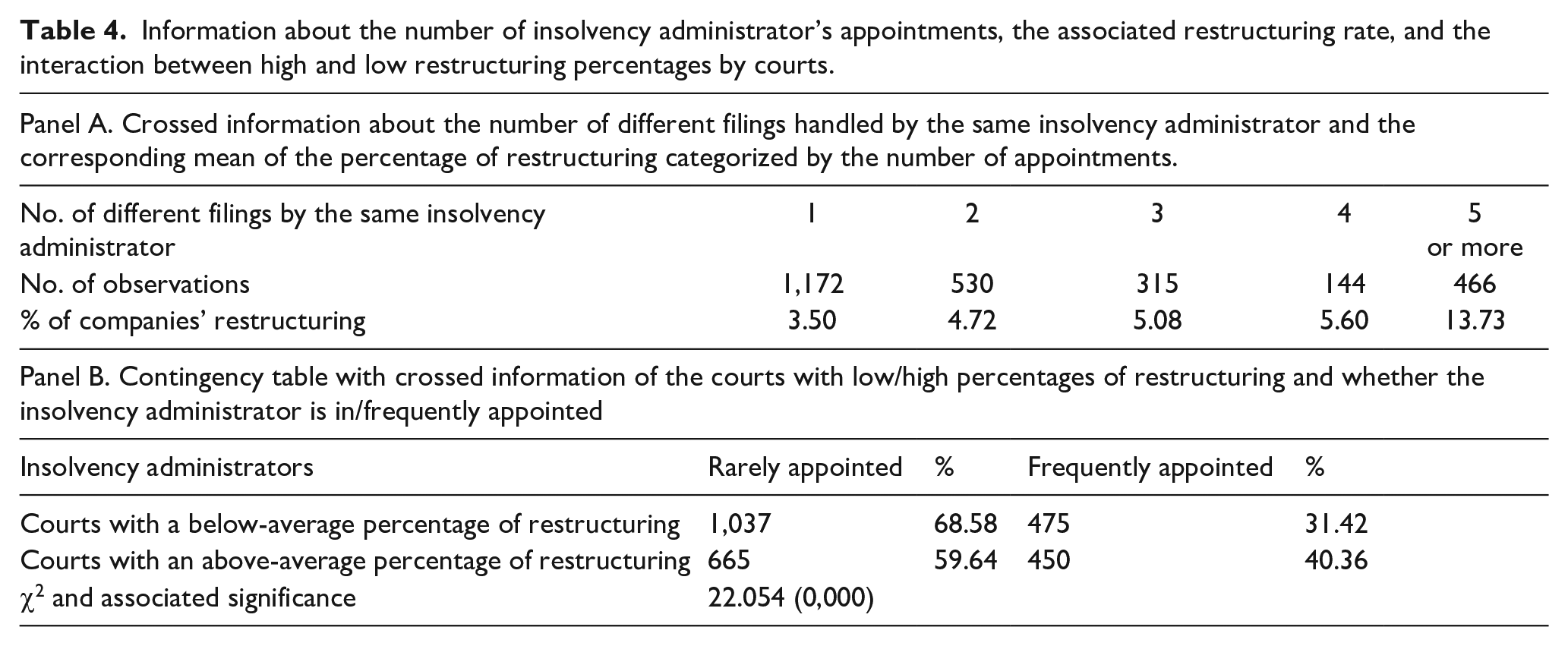

Frequency of insolvency administrator’s appointment and the adverse selection problem

Given the importance of the results on insolvency administrators, we have decided to further examine this issue as far as the data allow it. The choice of the insolvency administrator and the framework in which this decision is made is explained in section “Spanish Bankruptcy Law 2003.” The information about the number of times the same insolvency administrator has been appointed is crossed with the mean of the main dependent variable in Panel A of Table 4.

Information about the number of insolvency administrator’s appointments, the associated restructuring rate, and the interaction between high and low restructuring percentages by courts.

The results hint at a positive relation between the experience of the insolvency administrator and restructuring, which is at the core of the law. Particularly, the percentage of restructuring when the insolvency administrator has been appointed five or more times is impressively high. We create a dummy of many appointments (value of 1: 3 or more appointments, and 0: 1 or 2) and the information provided by another dummy, which takes the value of 1 if the mean of a specific court’s restructuring is higher than the overall mean and 0 otherwise. Panel B shows the crossed information of these two dummies in a contingency table along with the χ2, whose significance implies these two variables are related. The results show that the imbalance between less-appointed and more-appointed insolvency administrators is not pronounced in successful courts.

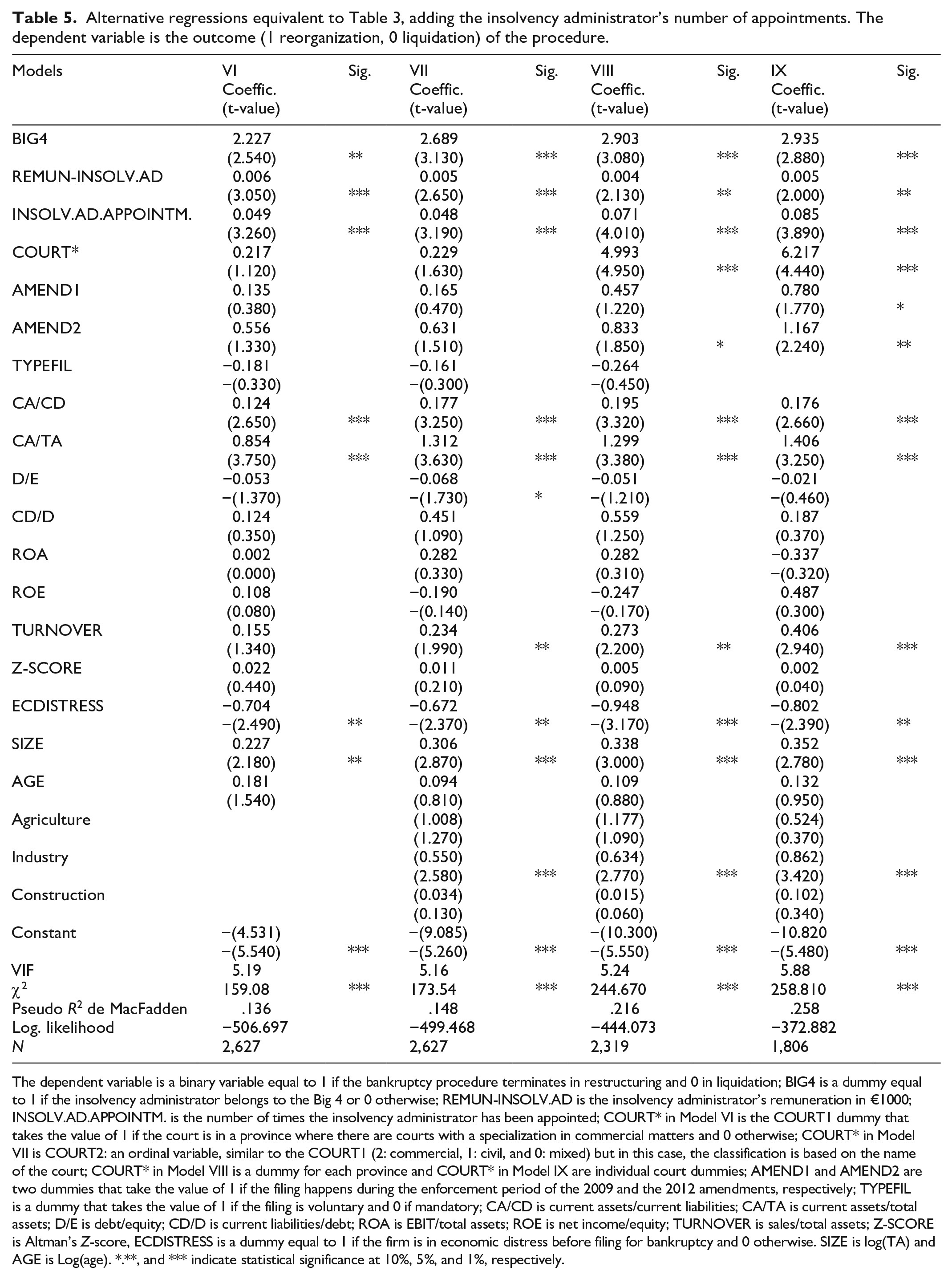

When managing insolvency filings, an adverse selection cost may appear (see Figure 2). In this case, we think the number of previous appointments handled by the same insolvency administrator is an excellent instrument to reduce this cost. We add the variable: number of appointments (INSOLV.AD.APPOINTM.) for the panel database period of the same insolvency administrators and rerun regressions I, III, IV, and V of Table 3 with this new variable in Table 5.

Alternative regressions equivalent to Table 3, adding the insolvency administrator’s number of appointments. The dependent variable is the outcome (1 reorganization, 0 liquidation) of the procedure.

The dependent variable is a binary variable equal to 1 if the bankruptcy procedure terminates in restructuring and 0 in liquidation; BIG4 is a dummy equal to 1 if the insolvency administrator belongs to the Big 4 or 0 otherwise; REMUN-INSOLV.AD is the insolvency administrator’s remuneration in €1000; INSOLV.AD.APPOINTM. is the number of times the insolvency administrator has been appointed; COURT* in Model VI is the COURT1 dummy that takes the value of 1 if the court is in a province where there are courts with a specialization in commercial matters and 0 otherwise; COURT* in Model VII is COURT2: an ordinal variable, similar to the COURT1 (2: commercial, 1: civil, and 0: mixed) but in this case, the classification is based on the name of the court; COURT* in Model VIII is a dummy for each province and COURT* in Model IX are individual court dummies; AMEND1 and AMEND2 are two dummies that take the value of 1 if the filing happens during the enforcement period of the 2009 and the 2012 amendments, respectively; TYPEFIL is a dummy that takes the value of 1 if the filing is voluntary and 0 if mandatory; CA/CD is current assets/current liabilities; CA/TA is current assets/total assets; D/E is debt/equity; CD/D is current liabilities/debt; ROA is EBIT/total assets; ROE is net income/equity; TURNOVER is sales/total assets; Z-SCORE is Altman’s Z-score, ECDISTRESS is a dummy equal to 1 if the firm is in economic distress before filing for bankruptcy and 0 otherwise. SIZE is log(TA) and AGE is Log(age). *.**, and *** indicate statistical significance at 10%, 5%, and 1%, respectively.

The results in Table 5 are quite similar to those of the analogous regressions in Table 3, but the variables Court1 and Court2 do not reach 10% significance. From Table 4, we learn that successful courts tend to appoint successful insolvency administrators, and the number of appointments seems a good proxy for this feature. The significance of this new variable makes the variables representing the courts non-significant for regressions VI and VII, which makes sense as these two variables are obviously related. Another point that deserves mentioning is the increase in χ2 and the pseudo-R2 and log. likelihood when adding this new variable. The results suggest that adverse selection is an important issue in the filing process, and courts try to offset it by appointing skilled insolvency administrators with proven experience in managing these filing processes.

Discussion, conclusions, and limitations

Economic crises catalyze the fall of many companies, quite a lot of them economically unviable. Notwithstanding, the spirit of the Spanish Bankruptcy Law passed in 2003 was to increase the number of companies that restructured and could consequently continue, compared to the number of firms ending up in liquidation. This law was justified based on inefficiencies and delays throughout the procedure, which were thought to be the reason why allegedly viable companies failed.

Wang (2012) suggests that a reasonable percentage of reorganizations would result from good legislation combined with court efficiency. In countries with more pro-creditor legislation, liquidation is favored over reorganization. Filing processes in Spain are considered to be creditor-oriented and framed in the context of poor court efficiency (Wang, 2012).

Filing for bankruptcy is usually the most demanding alternative for companies, as many costs arise from the filing procedure. According to Djankov et al. (2008), Spain is one of the most expensive countries in Europe in terms of bankruptcy filing costs (court, attorney, liquidation/auctioneer, government fees, and inefficient decisions), along with Italy. This inefficiency tends to discourage creditors from seeking reorganization (Wang, 2012).

Insolvency regulations have been modified to increase reorganizations in countries other than Spain. López-Gutiérrez et al. (2012) report on the reforms carried out in Australia (1993), Germany (1999), and the United Kingdom (2003). Unexplained factors remain that affect the efficiency of these laws. Specifically, the result of the process does not depend solely on the ability of the company in difficulties but on other outside agents that have power granted to them by the regulation. These agents are insolvency administrators and the courts. In this article, we study the role of third parties in the outcome of insolvency proceedings through the perspective of the agency theory. Judges/courts and insolvency administrators have specific characteristics and may have interests other than maximizing the value of a company immersed in insolvency.

Although there are many works about insolvency and bankruptcy laws in the field of comparative law, there is still a need for empirical studies in economic research to analyze the outcomes/implications of such laws. This work aims to add a theoretical and empirical contribution to this gap by taking an innovative approach to the agency costs of the filing process. Using a database of 2,627 filing processes in Spain during the 2008–2014 period, we run a logit analysis and find that many of the variables that the literature finds relevant do have an impact on the outcome of the process, such as ratios of liquidity, solvency, size, sector, and so on. The most interesting result is the importance of the type of court in which the filing process takes place, and certain insolvency administrator characteristics, such as their quality and remuneration. These findings are in line with Celentani et al. (2010), who argue that with able third parties, there should be proportionally more reorganizations. Although other works have already pointed out the role of courts and insolvency administrators, this is the first work that integrates them from the agency cost point of view and incorporates ad hoc variables related to these costs. Another interesting result from our analyses is that judges/courts faced with the potential costs of adverse selection learn from previous cases and tend to appoint experienced insolvency administrators. Courts behaving this way show a higher proportion of reorganizations.

However, in spite of the spirit of insolvency law, it is not clear whether closing a company is bad or good for economic welfare. Authors have found advantages (the elimination of a player) and disadvantages (contagion) for competitors, which suggests that both substitution and spillover effects are present (Baird, 1986; Lang & Stulz, 1992). In this context, our results have important implications, especially when talking about short-term effects. These effects can be evaluated by taking, for example, Model I and calculating the logit marginal effects (not reported) of the variables of interest. We can observe that the fact that the insolvency manager belongs to the Big 4 increases the probability of restructuring by 13.56%; this means that if in 2014, 7,280 companies filed for bankruptcy in Spain (INE, n.d.), having a more specialized insolvency administrator would have saved 987 companies more. If an average company in our sample has a mean of 17 employees, this would have implied saving 16,782 jobs. If the remuneration increased by €10,000, the probability of restructuring would have increased 0.2%. This would have implied nearly 15 more companies restructuring and 247.5 job positions maintained; finally, having more specialized courts would have saved 119 companies and 2,030 jobs. Therefore, we have identified the need for legislators to ensure a high enough remuneration to the insolvency administrator to make it a motivating element. This would avoid the perverse effect that can lead viable companies to liquidation. Likewise, it is necessary to develop protocols that ensure the quality of insolvency administrators, promoting multidisciplinary work between lawyers and economists, thus ensuring that this type of situation is managed with sufficient economic knowledge.

The appointment of the insolvency administrator should be taken from the most objective criteria possible, based on their skills and previous work, thus creating an efficient and competitive market of insolvency managers. From our results, it is clear that insolvency administrators acquire experience that increases the probability of reorganization. The characteristics of this expertise should be analyzed and shared with younger insolvency administrator candidates. Finally, although we are aware that governments suffer from budget constraints since the courts have a significant effect on the probability of reorganization, it is necessary to provide them with more resources and prioritize their specialization. These findings contribute to the open debate about the power endorsed to courts and insolvency administrators on the normative’s efficiency. In this sense, Arruñada (2021) advocates for a more balanced design of the procedure, decreasing the power of third parties and increasing the role played by the main actors (creditors and debtors), promoting private solutions, and decreasing state intervention.

This work is not without limitations that, in turn, present opportunities for future research. First, it would be advisable to check whether the results of this work apply to other countries with similar legislation. A noteworthy limitation of our research is the reduced number of observations of filings administrated by the Big 4, and thus, future research should use databases with more cases involving this type of administrator. Another strand of research could analyze whether the legislation, which seems to favor reorganization, contributes to the welfare of society in the long term. As our results have stressed size as a relevant factor, it would be interesting for future research about the outcomes of filing processes to incorporate factors particular to small enterprises, such as excessive delays in liquidation (Yamakawa and Cardon, 2017), late payment problems (see EU Directive 2011/7/EU), and social stigma (García-Alamán et al., 2016). All these issues are more likely to appear in a local context when managing an SME.

Our research has stressed the important role that insolvency administrators play and how their expertise and previous experience increase the probability of restructuring. Future research should investigate whether specific characteristics of insolvency administrators, such as age, background, and previous experience, explain the outcomes of insolvency procedures, along with analyzing past successes (reorganization) and successive appointments. Similarly, future research could involve investigating whether the characteristics of judges, their expertise, experience, skill, and specialization play a role in the filing process in other countries. In addition, emphasis should be placed on investigating the factors that influence the use of the filing process and its outcomes: court backlog, management qualifications, and the overall reliability of the judiciary system, as opposed to the out-of-court processes that take place before filing for bankruptcy. Given that Spain seems to have a high rate of pre-agreements/arrangements, it would be useful to apply the model by Daigle and Maloney (1994), who propose a scheme that encourages creditors and shareholders to agree on informal reorganization before filing.

Footnotes

Appendix 1

Appendix 2

Reduction in the number of observations due to lack of data, filtering, and so on.

| Original number of observations | 17,373 |

| After eliminating companies with no available information in SABI | 3,217 |

| After eliminating companies belonging to banking, insurance, and financial services | 3,202 |

| After eliminating companies without information for the year when the company files for bankruptcy, and thus, data were not available for some crucial variables related to liquidity, profitability, and so on. | 2,627 |

Appendix 3

Definition of variables.

| DEPENDENT VARIABLE | Outcome of the filing process (1-reorganization, 0-liquidation). |

| BIG4 | Dummy equal to 1 if the insolvency administrator belongs to the BIG4, and 0 otherwise. |

| REMUN-INSOLV.AD | Remuneration of the insolvency administrator, proxied with a formula specified by the 2003–2004 Bankruptcy Law. |

| COURT1 | Dummy equal to 1 if the court is in a province where there are courts with a specialization in commercial matters and 0 otherwise. |

| COURT2 | Ordinal variable that takes the value of 2 when the court is in a province with courts specialized in commercial matters (commercial: “Juzgado de lo Mercantil”), 1 when it is a semi-specialized court (civil: “juzgado de primera instancia”), and 0 when it is a non-specialized court (mixed: “juzgado de primera instancia e instrucción”). |

| COURTPR | Dummies for each province in which the court is located. |

| COURTi | Individual court dummies. |

| AMEND1 | Dummy that takes the value of 1 if the filing occurs in the period between April 2009 and the end of 2011 and 0 otherwise. |

| AMEND2 | Dummy that takes the value of 1 if the filing occurs in the 2012–2014 period and 0 otherwise. |

| TYPEFIL | Dummy that takes the value of 1 when the filing is voluntary, and 0 when it is mandatory. |

| CA/CD | Current assets/current liabilities. |

| CA/TA | Current assets/total assets. |

| D/E | Debt/equity. |

| CD/D | Current debt/total liabilities. |

| ROA | EBIT/total assets. |

| ROE | Net income/equity. |

| TURNOVER | Sales/total assets. |

| Z-SCORE | Altman’s Z-score. |

| ECDISTRESS | Economic distress is a dummy variable which is 1 if the company shows 2 years or more of negative operating profit and 0 otherwise. |

| SIZE | Log of total assets. |

| AGE | Log of number of years INSOLV.AD.APPOINTM. |

| INSOLV.AD.APPOINTM. | Times the insolvency administrator has been appointed. |

Appendix 4

Characteristics of the companies with an insolvency administrator from the Big 4 compared to the rest of the sample.

| Variables | NO BIG4 | BIG4 | ||

|---|---|---|---|---|

| No. of observations | M | No. of observations | M | |

| Restructuring (1)-liquidation (0) | 2,618 | 0.057 | 9 | 0.667 |

| REMUN-INSOLV.AD | 2,618 | 33.029 | 9 | 235.056 |

| COURT1 | 2,618 | 0.645 | 9 | 0.333 |

| COURT2 | 2,618 | 0.887 | 9 | 1.000 |

| AMEND1 | 2,618 | 0.741 | 9 | 0.667 |

| AMEND2 | 2,618 | 0.166 | 9 | 0.333 |

| TYPEFIL | 2,618 | 0.977 | 9 | 1.000 |

| CA/CD | 2,618 | 1.490 | 9 | 0.865 |

| CA/TA | 2,618 | 0.379 | 9 | 0.367 |

| D/E | 2,618 | 2.463 | 9 | 0.882 |

| CD/D | 2,618 | 0.674 | 9 | 0.552 |

| ROA | 2,618 | −0.135 | 9 | −0.070 |

| ROE | 2,618 | −0.072 | 9 | −0.089 |

| TURNOVER | 2,618 | 1.297 | 9 | 0.564 |

| Z-SCORE | 2,618 | −0.122 | 9 | −0.674 |

| ECDISTRESS | 2,618 | 0.840 | 9 | 0.889 |

| SIZE | 2,618 | 13.585 | 9 | 16.665 |

| AGE | 2,618 | 2.351 | 9 | 1.839 |

| Agriculture | 2,618 | 0.007 | 9 | 0.000 |

| Industry | 2,618 | 0.268 | 9 | 0.000 |

| Construction | 2,618 | 0.278 | 9 | 0.000 |

| Services | 2,618 | 0.435 | 9 | 1.000 |

Appendix 5