Abstract

Does having more women on a committee matter? Interestingly, answers to this question are unknown, despite a significant push toward greater gender diversity on committees and boards. This article uncovers the mechanism of if and how committees’ gender diversity impacts its deliberations and decisions. We utilize a unique dataset that matches detailed meeting transcripts of the Federal Reserve’s Federal Open Market Committee (FOMC) spanning over 30 years, with member characteristics and economy-wide conditions, allowing us to effectively compare committees with the same member resources and economy-wide conditions but different gender diversity. We find that deliberations are more thorough and engaged in more gender-balanced committees, wherein both men and women talk more about wider topics in depth. Unlike findings from other studies, women in the FOMC participate as active members, whereby they are more likely to voice formal disagreement and less likely to be dismissed by an interruption. Finally, we find that member resources and the economy-wide conditions explain the committee’s decision, where gender diversity exhibits no explanatory power by and in itself. With the high correlation between gender diversity and member resources, we demonstrate that gender composition affects committees via two channels; deliberation qualities and member resources.

Keywords

Introduction

Business committees, including business boards, serve critical roles in directing and overseeing important affairs of the committee’s organization. Given that a committee typically consists of a small number of highly select people, its composition would likely impact how the committee functions. Whether the gender makeup of a business committee/board, specifically whether having more women members, affects board effectiveness has been an ongoing debate in research and media. It is argued that female representation in boards improves their functions, governance, and, ultimately, the organizations’ performance (Adams and Funk, 2012; Cook and Glass, 2018; Cook et al., 2019; Farrell and Hersch, 2005).

One of the rationales for this claim is that having female members allows the board to access more and superior resources. The resource dependency theory (RDT) postulates that by attracting a broader pool of talent, a gender diverse board would benefit the organization by bringing in different but complementary resources, such as information, skillsets, relational capital, values, preferences, and temperaments (Hillman et al., 2002; Kim and Starks, 2016; Miller and Triana, 2009). Another rationale for better board effectiveness, and increased shareholder value, is through improved monitoring, as posed in the agency theory (AT) (Fama and Jensen, 1983; Jensen and Meckling, 1976). The AT theorizes the fundamental issue underlying the alignment/misalignment of interest between the principal (e.g. owners, stockholders) and agents (chief executive officers (CEOs), managers). According to AT, monitoring is an essential function of business boards to ensure that the management group’s actions remain aligned with owners’ interests. Women not being a part of the “club” makes them better suited for monitoring the board activities, as found by Adams and Ferreira (2009) and Chen et al. (2021).

There are numerous studies investigating the link between board gender composition and firm characteristics/performance, such as: financial performance (Isidro and Sobral, 2015; Post and Bryon, 2014), risk profile (Adams and Funk, 2012; Eckbo and Ødegaard, 2020; Faccio et al., 2016; Sila et al., 2016), ethical and social behavior (Bear et al., 2010; Glass et al., 2016; Post and Bryon, 2014), business strategy (Chen et al., 2016; Fondas and Sassalos, 2000; Matsa and Miller, 2013; Torchia et al., 2011), and the firm’s overall gender diversity (Cook and Glass, 2014; Cook et al., 2019; Matsa and Miller, 2011; Stainback et al., 2016). Despite the substantial research attention, the overall results are inconclusive, with mixed positive, negative, or no effects (Kirsch, 2018). Work by Adams (2016) and Kirsch (2018) argues that the inconsistent results, and therefore a significant gap in the literature, come from a lack of a clear explanation and sound empirical evidence on how and when gender composition matters. In particular, the aforementioned studies are based on externally observable characteristics and do not address the mechanisms through which gender composition influences the board. Instead, these studies attribute traits found in the general population of women, such as attitudes toward risk and negotiation and other-regarding preferences (see Bertrand, 2011 and Hyde, 2014 for review), to observable differences in boards.

This empirical approach presents two challenges. First, gender is an imperfect and perhaps noisy proxy for these traits, especially among woman directors who may be quite different from typical women in the population (Kirsch, 2018). Very few studies directly measure these traits, and when they do, these women are indeed found to have traits different from the stereotypical women (Adams and Funk, 2012). Second, the previous empirical approach generates an endogeneity problem (Adams, 2016) whereby the variable of interest is correlated with other important variables that are left out of the model. In such instances, the effect found on the variable of interest is contaminated with the effect from the omitted/uncontrolled correlated variables, leading to empirical findings that are biased, unreliable, and misleading. For example, the link between women directors and higher company performance may be explained by high-performing companies tending to be larger, and in turn, larger companies tending to be more conscious of gender diversity (Grosvold et al., 2007; Hillman et al., 2007; Marquardt and Wiedman, 2016). When the firm size is not properly accounted for in an empirical model, the effect of women directors may be inflated as it is confounded with the effect of firm size.

Uncovering the mechanism of if and how board gender diversity impacts the organization, therefore, requires (1) data that reveal the inner-workings of the board that goes beyond the gender proxy; and (2) an empirical strategy that addresses the endogeneity issue. A few studies do investigate committee inner-workings (Huse and Solberg, 2006; Krawiec et al., 2013; Nielsen and Huse, 2010); however, they use surveys and interviews, which do not utilize verbal communication that took place in the actual deliberation. For instance, Krawiec et al. (2013) interviewed board participants about board gender diversity, finding that board members believe it has a positive impact, but they are unable to articulate the reason for the positive impact. We are aware of only one study that examines the business committees’ actual deliberation and links to its strategic outcomes (Schwartz-Ziv, 2017); however, it does not consider the economic/business conditions in place at the time of the committee’s discussion. While there are studies incorporating wider economic contexts in their examination of committee decisions (Cook and Glass, 2018; Nielsen and Huse, 2010), these studies typically do not have a long enough time span to cover sufficient variation (e.g. entire business cycle).

In this study, we overcome the data and endogeneity challenges by utilizing the meeting transcription of the Federal Open Market Committee (FOMC) of the US Federal Reserve, comprising 330 meetings from 1978 to 2014. Our approach has several advantages over the existing literature. First, the FOMC has a clear mandate (stabilizing inflation and maximizing employment) with a fixed organizational structure, creating a stable environment for an investigation. Second, the transcripts provide the complete deliberation record, including voting patterns, so the details of the deliberation processes and the decisions are observable. Third, the primary policy decision made by the committee is whether to change the federal funds rate, which can be simplified to three possible outcomes; tighten (higher rate), ease (lower rate), or stay (status quo). The committee’s policy decision is public knowledge and comparable across time. Fourth, the transcripts provide complete lists of participants’ names. The FOMC is a well-known committee so that member information can be gathered from publicly available sources. This allows us to match the transcript data with member characteristics. Fifth, the relevant contextual economy-wide information is available as official statistics from public sources and can be matched to each meeting.

From RDT and AT perspectives, we conceptualize that gender diversity affects the committee by enriching the available member resources (e.g. expertise and values), as well as by altering deliberation qualities (e.g. the range of topics covered, meeting length, depth of the discussion, and the degree of disagreement). By utilizing the unique dataset, we empirically investigate both channels simultaneously, along with concurrent economy-wide conditions to address the endogeneity problem.

Additionally, for the committee to fully benefit from the unique resources that women possess, it is necessary that “gender stereotypes do not cast a shadow on the space female directors have to voice opinions, initiate ideas and gain recognition on boards” (Sidhu et al., 2021: 1679). In committees, women may be deterred by other members from speaking and/or unable to assert themselves in the conversation (Heath et al., 2014), which can severely reduce their contribution and influence (Carli, 2001). 1 This is owing to the gender stereotype that puts women into subordinate positions within the committee (Agars, 2004; Eagly and Karau, 2002; Rudman et al., 2012). As our empirical investigation relies on one institution, it is important to consider if such culture prevails in the FOMC. Our strategy is to identify whether incidents of interruption and inaudible speech in the transcripts exist as evidence of undermining a member’s impact and influence.

Our empirical results are consistent with RDT and AT, showing that deliberations are more thorough and engaged with more gender-balanced committees, as documented by higher average word counts per member, more topics discussed, and more in-depth discussions by both men and women. These effects exist after controlling for the member resources, commensurate with the unique contribution of women beyond their professional expertise. We also find that female members are more likely to voice formal disagreement. We do not find evidence that women’s contribution and influence are actively repressed, as our results show that women are less likely to be interrupted. Finally, we find that the committee’s policy decision is explained by both member resources available to the committee and the current economy-wide conditions, with gender composition providing no explanatory power after controlling for the former conditioning variables.

This study contributes to the literature in several ways. First, we refine the RDT and AT and provide a theoretical argument identifying the mechanisms through which gender diversity impacts the committee—one by affecting the deliberation quality (more comprehensive and engaged discussion) and the other by affecting available committee resources (the policy stance, education, and professional expertise). Second, we provide strong empirical support for the two theorized processes by utilizing unique unbalanced panel data spanning over 30 years. Third, and related to the first two, we delineate the impact of specific resources contributed by committee members, such that member resources impact the committee’s policy decisions, whereas gender impacts how the committee reaches these decisions. Fourth, we demonstrate the importance of addressing the endogeneity issue by explicitly accounting for members’ expertise and relevant monetary policy orientations as sources of heterogeneity between male and female members at each meeting, as well as concurrent economy-wide conditions. We show that failing to account for both could result in misleading findings. Finally, we employ a novel methodology based on Natural Language Processing to utilize the committee’s transcript data, which contains close to 10 million words.

The remainder of the article is organized as follows. The next section provides the background and contextual information about the FOMC, followed by a discussion of our conceptual framework and hypotheses and a section describing the data. The following two sections lay out our empirical strategies and results. Lastly, we provide a discussion of the results, conclusions, and limitations of the study.

Background: The Federal Open Market Committee

The FOMC is responsible for setting and implementing monetary policy for the United States economy. The FOMC consists of a board with 12 voting members, where the Board of Governors holds seven standing board positions. The president of the Federal Reserve Bank of New York has a permanent voting position, and the remaining four seats have a yearly rotation of voting rights between the remaining 11 Federal Reserve Banks. Appointments to the Board of Governors are made by the US president, while the Federal Reserve district presidents are appointed internally within their respective districts. The FOMC holds eight regularly scheduled meetings per year in addition to ad hoc conference calls. Each meeting consists of a review of economic and financial conditions both nationally and by district, a presentation of the staff forecasts, deliberations, and a formal vote regarding the appropriate monetary policy action. The decision is based on the majority voting (yes/no) on the suggested action to either tighten monetary policy, maintain the status quo, or ease monetary policy.

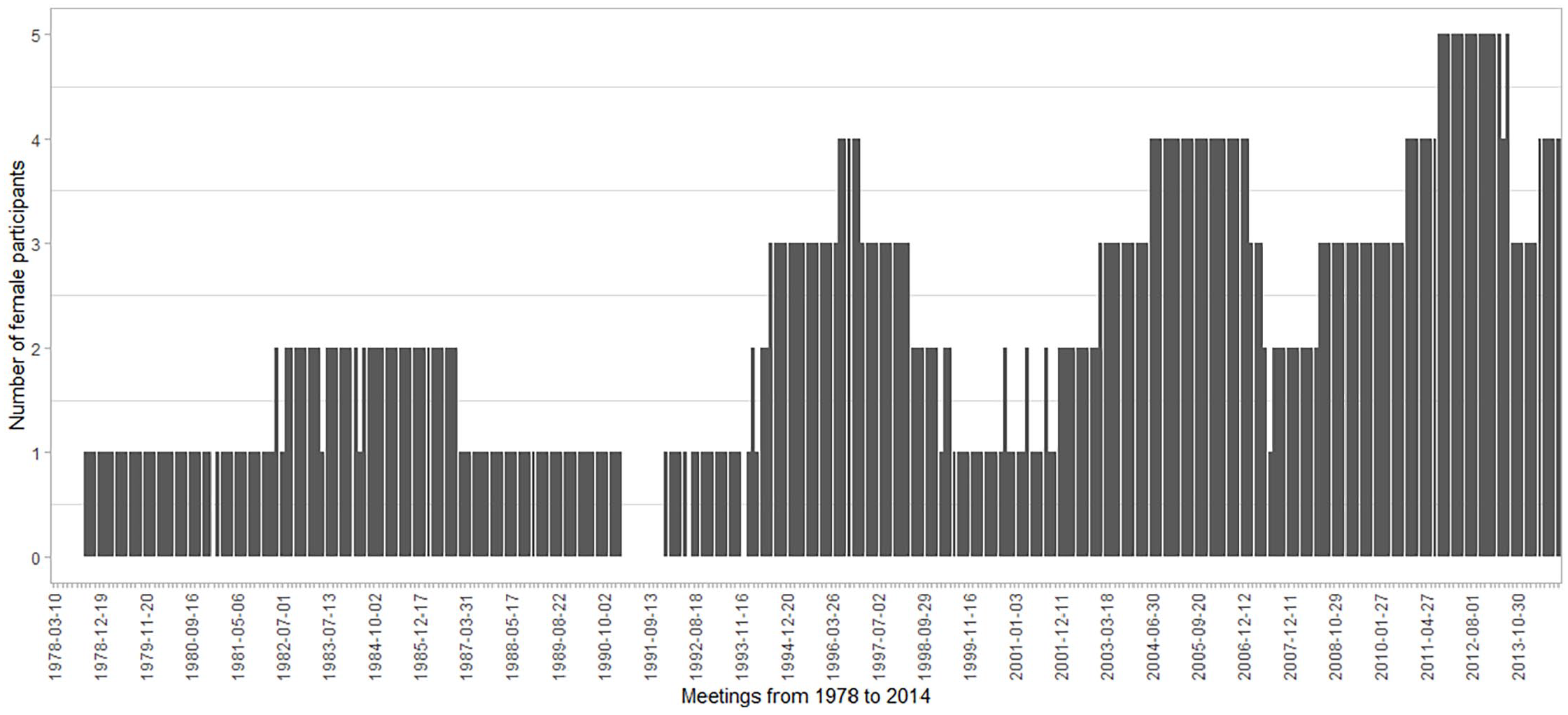

Three important details about the FOMC directly impact our analysis and its interpretation. First, the fundamental objective of each FOMC meeting, set by the US Congress, is to “promote price stability and maximum sustainable employment”. This objective, known as the “dual mandate”, is constant across meetings, providing a consistent environment for the investigation. The two criteria—price stability and maximum sustainable employment—are often in a trade-off relationship, and the crucial role of the FOMC is to deliberate on the optimal balance by setting the appropriate course of action for monetary policy. Second, an important policy change, known as the “transparency rule”, was implemented in November 1993, whereby transcripts of the FOMC meetings were to be released to the public at a five-year lag. Thus, prior to the transparency rule implementation, what was said in FOMC meetings was private information, and after the policy change, FOMC members understood that what was said would be released to the public, reviewed, and potentially scrutinized. The third is the history of women’s membership within the FOMC. While men have always outnumbered women, women’s membership has been increasing since 1978, when Nancy Teeters, the first woman to serve on the FOMC, joined the board. Since then, four women have held standing positions on the FOMC, two on the board and two as district presidents. Figure 1 displays the number of women at each meeting, varying up to five women in a 12-member committee. Despite having no mandate or quota, it demonstrates increasing, albeit slow and uneven, movements toward gender balance on the FOMC.

Number of female board members of the FOMC.

Conceptual framework and hypotheses

The potential benefits of more gender diverse committees can be argued through both RDT and AT. According to RDT, having more women can allow boards to access diverse sets of resources in the forms of information, skillsets, relational capital, values, preferences, and temperaments (Hillman et al., 2002; Kim and Starks, 2016; Miller and Triana, 2009). Having more women can also enhance the monitoring function of the board (Adams and Ferreira, 2009; Chen et al., 2021), as argued by AT (Fama and Jensen, 1983; Jensen and Meckling, 1976). From these perspectives, we conceptualize two possible mechanisms that gender diversity affects the committee—by altering the deliberation qualities and available member resources.

Deliberation qualities

Both RDT and AT imply women bring unique resources to committees. However, how exactly these resources materialize to benefit the committee’s decision making is not well understood. We argue that women influence how the committee’s discussions are formulated and delivered. Several qualitative studies (Baskaran and Hessami, 2019; Konrad et al., 2008) find that women tend to bring up topics different from men in committees, so it is possible that higher gender diversity increases the breadth (number of topics) of the discussion. Furthermore, women are found to be better at facilitating and monitoring discussions, as postulated in AT, ensuring that all aspects are addressed before reaching a decision (Adams and Ferreira, 2009). It would suggest that the depth of the committee’s discussion would also be increased with more female committee members. Given the FOMC’s dual mandate and specific policy considerations, there is a standard set of topics typically discussed in the committee meetings (e.g. inflation, employment, prices, money supply, exchange rates). While one might expect the committee to discuss all the economic implications of the suggested policy decision, the reality is that the committee may focus its discussion on some topics more than others. Higher gender diversity may lead to a more balanced and thorough discussion. Finally, with the potential for increased breadth and depth of the discussion, it is also plausible that having more women makes the committee discussion longer. Aggregating all conjectures above, our first hypothesis is stated as follows:

H1: Higher gender diversity is associated with more comprehensive coverage in deliberation in breadth, depth, thoroughness, and length.

Disagreement

Another way having more women can affect the deliberation is through the level of disagreement. On the one hand, if women have a higher desire to be a part of unanimity in congruence with their female communal gender characteristics (Eagly and Karau, 2002), the committee might experience less disagreement. On the other hand, if women contribute unique vantage points that are different from men, this could increase disagreement. In the FOMC, disagreement can be tracked by the dissension votes. The FOMC has a long tradition of valuing unanimity to demonstrate a united front as a monetary policymaker; thus, dissension votes can be considered a strong sign of disagreement and a gesture of exerting influence. Women might also be less willing than men to publicly demonstrate their formal disagreement. A notable contextual factor that can provide richness to our analysis is the introduction of the 1993 transparency policy. Hansen et al. (2018) found a general tendency toward conformity among all members after the transparency policy, but a higher frequency of dissension by women was found up to 1993 (Lähner, 2018). Combining the results of Hansen et al. (2018) and Lähner (2018) might suggest that the confirmatory pressure was higher among women. We hereby formulate our second hypotheses:

H2a: Women are less likely to cast dissension votes.

H2b: Transparency policy reduces the propensity to dissent more for women than men.

Interruption and not being heard

For the committee to benefit from gender diversity, it is necessary that women on the committee are able to fully contribute to the discussion. If there are mechanisms in place that stifle, shut down, or actively deter women from contributing (Heath et al., 2014), it could severely reduce women’s contribution and influence (Carli, 2001). To assess whether such mechanisms exist in the FOMC, we count the number of interruptions (an abrupt ending to someone’s speech delineated by “–” followed immediately by another member’s speech) and incidences of not being heard (inaudible speech, denoted as [unintelligible] in the transcripts). Admittedly, these are not direct measures of members’ attitudes or values toward gender equality, but they do provide empirical evidence if women’s speech is actively being undervalued in the committee. Accordingly, we state our third hypothesis:

H3: Women are more likely to be interrupted/not be heard than men in the deliberation.

Member resources and policy decisions

Finally, we examine if gender diversity plays a role in explaining the committee’s policy decisions. In particular, we hypothesize that gender diversity influences the committee through the pool of member resources that the committee accesses, but after controlling for the available resources, gender in and of itself has no impact on the policy decision. We seek a set of member characteristics that accurately reflects the resources available to the committee because of its membership. Within the monetary policy decision-making literature, of central importance is how members interpret the current economy-wide conditions, such as inflation, unemployment rate, and so on, and any economic or political crisis. Members tend to focus their attention more on one side of the dual mandate (inflation versus unemployment) than the other. See Bordo and Istrefi (2018) and Chappell et al. (2000) for studies that explore gender and monetary policy stances. Given the setting of our study, we define the relevant set of member resources as members’ inflation/employment-focused policy stance, as well as education and professional expertise.

H4: Gender diversity does not affect the committee’s policy decisions when the committee’s pool of member resources and economy-wide conditions are accounted for.

Data and methods

The central dataset for our investigation is an unbalanced panel data containing the transcripts of the FOMC discussion, 2 together with the committee’s policy decisions, from March 1978 (the first available individual voting record) to December 2014, resulting in 330 meetings. The data are organized longitudinally by members within each meeting. The total number of words spoken in all meetings by FOMC members is 9,705,512. To process a large amount of text in an efficient and consistent way, we utilize the Natural Language Processing used increasingly in business/social science fields, such as marketing (Humphreys and Wang, 2018), psychology (Tausczik and Pennebaker, 2010), and economics (Athey and Imbens, 2019). 3

The meeting data are supplemented with background information on committee members collected from bibliographies, Wikipedia, and the past literature, including; gender, date of birth, year of entry to the FOMC board, highest degree earned, university of the highest degree earned, a field of study, profession before joining the FOMC, political affiliation, if known, and a monetary policy stance (inflation/employment-focused). 4 The macroeconomic data associated with the FOMC congressional mandate, collected from the Federal Reserve Bank of St Louis FRED database, provide the economy-wide contexts for each meeting. Specifically, the data include the consumer price index (CPI), the civilian unemployment rate (CUE), the slope of the yield curve, measured as the difference between 10-year and one-year Treasury yield, the federal funds rate, and the return of the Wilshire 5000. We also include an indicator for crisis periods and recessions (Arora et al., 2020). 5 The dataset contains 14 and 79 unique female and male members, respectively, from when Nancy Teeters served as the first woman board member of the FOMC until the first year that Janet Yellen was the first chairwoman.

Dictionary

After a standard text cleaning procedure of tokenization and stemming are applied, we employ a dictionary approach utilizing the FOMC dictionary developed by Arora et al. (2020) to reduce the dimensionality of the data. A dictionary is a predetermined set of words used to categorize the text. The FOMC Dictionary captures the text information representing topics related to the FOMC mandate, such as inflation, employment, credit, equity and foreign exchange markets, monetary aggregates, reserves, federal funds, and long/short horizons. The dictionary contains 21 categories with 28 subcategories and 524 terms. The dictionary approach is effective but also sensitive to the construction of the dictionary; thus, we supplement with an alternative method discussed below.

Distance of conversation

Conversation distance is a novel way of quantifying how far a conversation travels in terms of topics discussed. It is captured by the distance between word vectors, wherein each word vector represents the content of one segment of the conversation (Kusner et al., 2015). In particular, we partition the meeting discussion into “windows”, measure the distance between the windows, and then sum the total distance traveled for each meeting. By construction, if a meeting covers a wider range of topics, the conversation distance measure will be larger.

The cleaned text data are processed by the word2vec procedure in Python, where each word in the text is represented by pre-trained 300-dimensional content vectors

and each meeting is represented by an average distance the meeting conversation travelled.

Empirical models

For our first hypothesis, the dependent variables for conversation breadth are the topic counts from the FOMC dictionary (Arora et al., 2020), regressed on gender diversity, member resources, and macroeconomic measures. For meeting i and member k, we specify:

where

The conversation depth is examined by comparing the distribution of the standard deviations of Euclidean distances by women and men. The smaller overall variability of the Euclidean distance measure is consistent with a more in-depth discussion of topics. The significance of the distributional difference is tested via the Kolmogorov-Smirnov test of distribution equivalence. The length of the meeting is measured simply by the average words spoken by members, with the same specifications as in Equations (2) and (3).

The probability of member

where

Finally, the committee’s policy decisions are estimated by aggregating all data to the meeting level and running a multinomial logit model, where

The coefficient of interest is

Results

Member resources

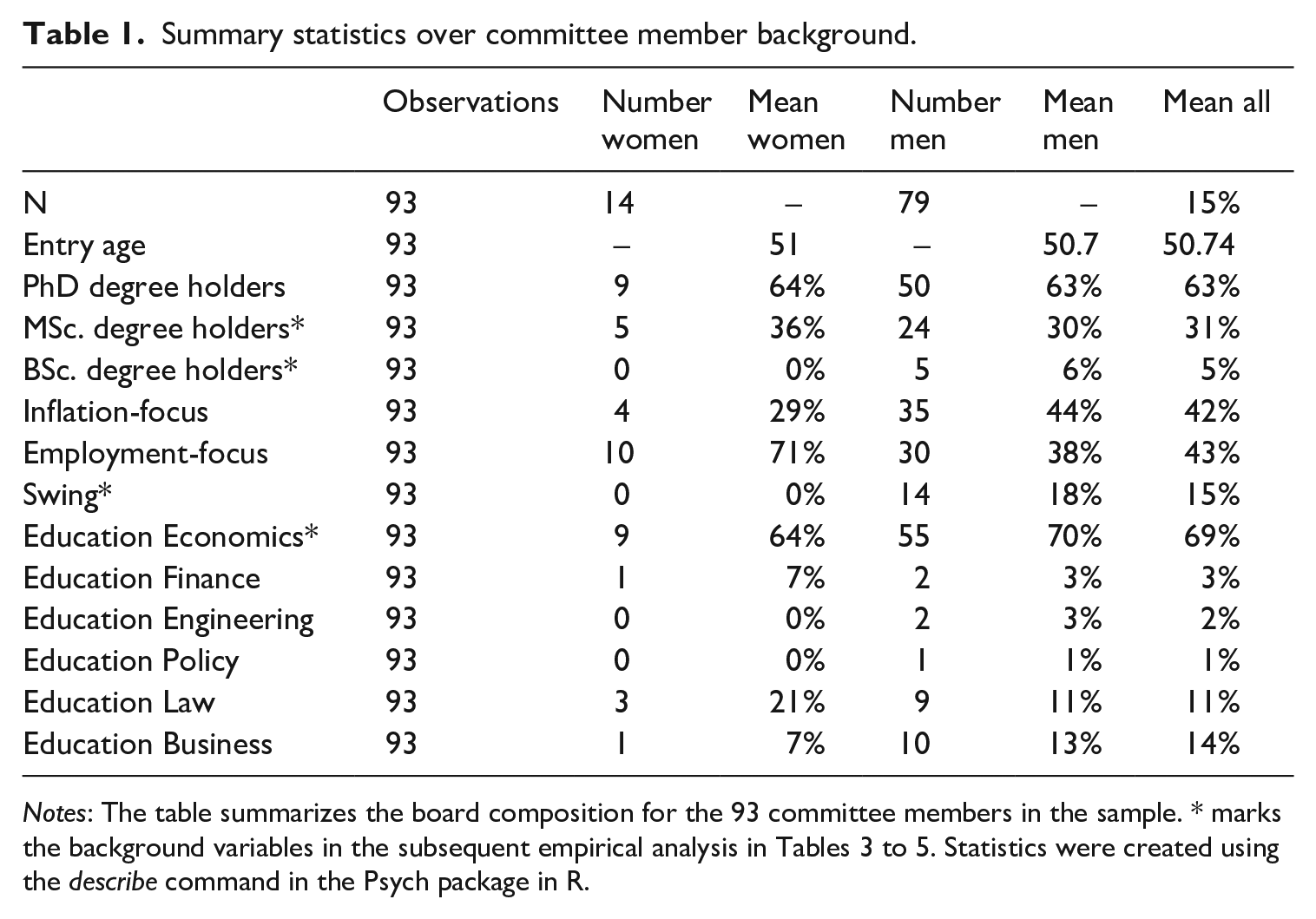

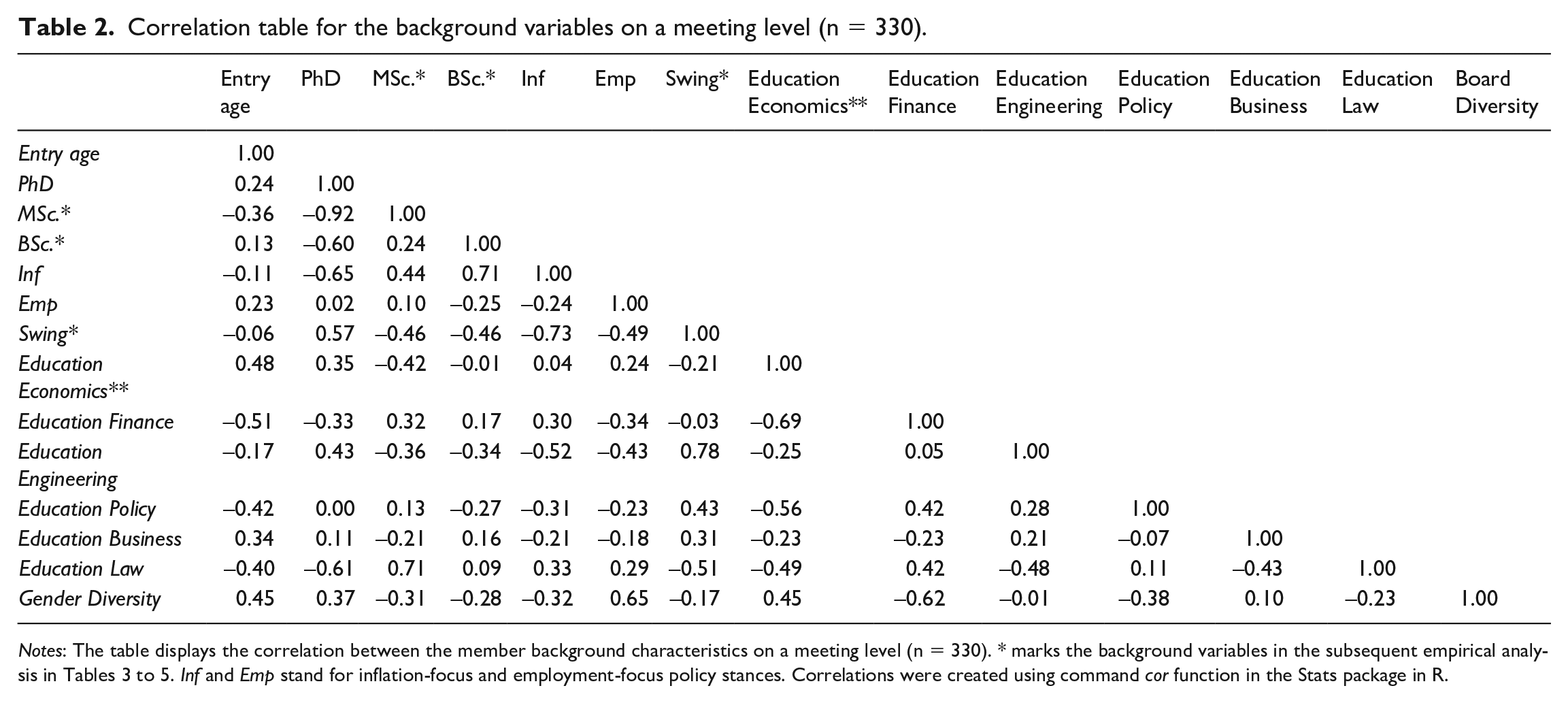

A summary of member resources by gender is provided in Table 1, and the correlation among these variables and gender diversity measures at the meeting level is shown in Table 2. 7 As expected, a number of characteristics found in FOMC members are distinct from business boards (Ahern and Dittmar, 2012; Chattopadhyay and Duflo, 2004; Matsa and Miller, 2013). Most members have PhD degrees (63%) in economics, finance, or business fields. The most pronounced difference between men and women comes from their monetary policy orientation. Seventy-one percent of women are considered employment-focused compared with 38% of men. While men and women are strikingly similar from a resource diversity perspective, women in the FOMC are more homogeneous in characteristics with the “standard” background and career path (PhD degrees and economist backgrounds) compared with men. At the meeting level, the gender diversity measure ranges from 0 to 0.42, with an average level of 0.20. Meeting-level correlations shown in Table 2 reveal that gender diversity is correlated with a number of member resources, particularly with entry age (0.45), the proportion of employment-focused members (0.65), economics education (0.45), and finance education (–0.62). Thus, gender composition does seem to affect the member resources that the committee has access to at each meeting.

Summary statistics over committee member background.

Correlation table for the background variables on a meeting level (n = 330).

Notes: The table displays the correlation between the member background characteristics on a meeting level (n = 330). * marks the background variables in the subsequent empirical analysis in Tables 3 to 5. Inf and Emp stand for inflation-focus and employment-focus policy stances. Correlations were created using command cor function in the Stats package in R.

Topics discussed (breadth)

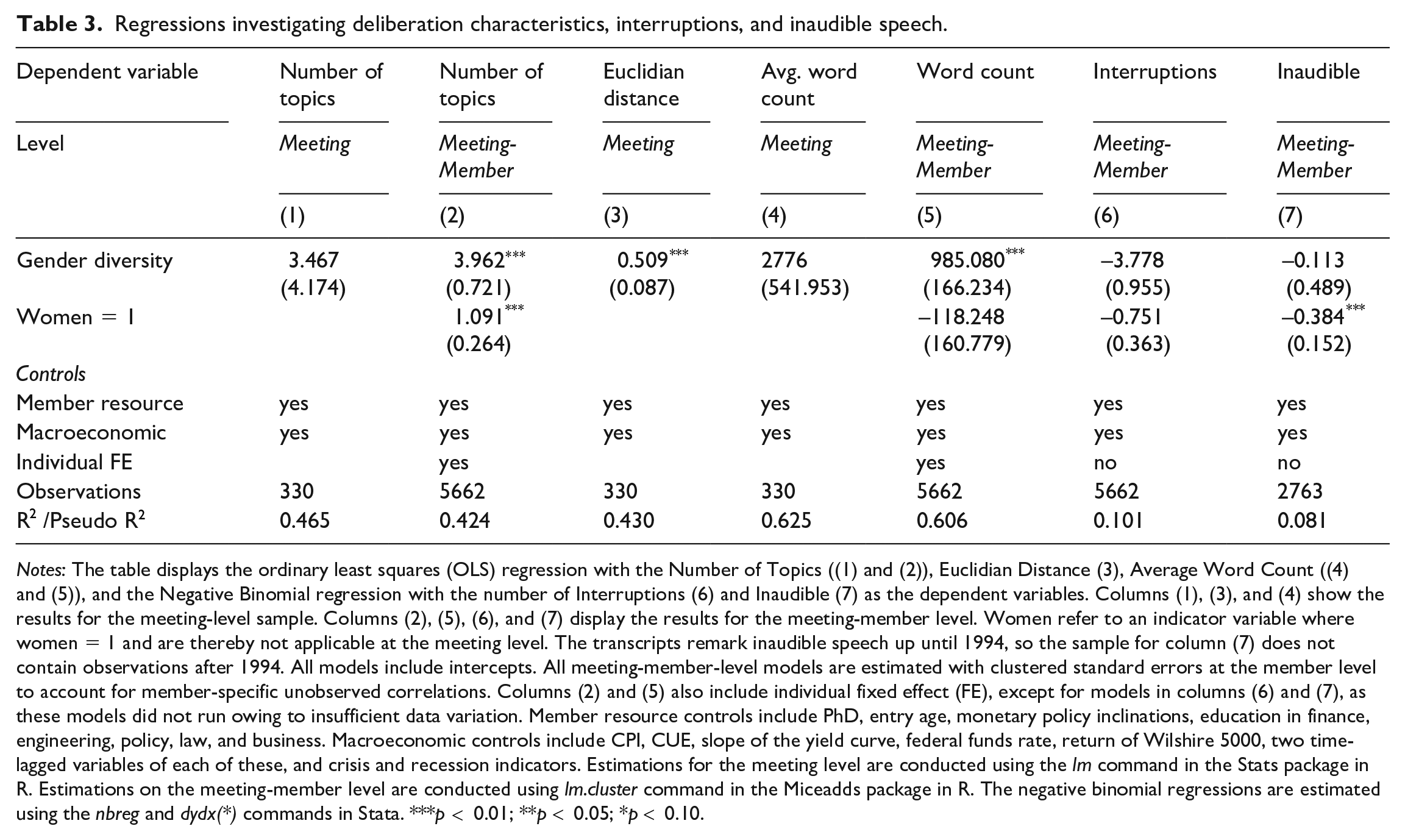

Among the 34 potential topics in the FOMC library (Arora et al., 2020), approximately 25 topics are covered in each meeting on average, but the number varies from eight to 33. To investigate if gender diversity affects the discussions, we first examine whether gender diversity changes the number of topics addressed in the meeting (Equation (2)). The corresponding results are displayed in column 1 of Table 3, where we see that gender diversity does not impact the number of topics at the meeting level. It might be that the meeting-level aggregate counts are not at a fine enough scale to address more subtle changes in the meeting discussion. For instance, it is possible that, even if the total number of topics addressed is unchanged, each topic could be mentioned by more members, which may indicate a more active dialogue. We investigate this possibility with our meeting-member-level analysis (Equation (3)). The results displayed in column 2 of Table 3 show a significant positive relationship between gender diversity and the number of topics addressed at an individual level. It is estimated that when gender diversity increases from zero (no women) to 0.20 (overall average level), each member addresses one additional topic on average.

Regressions investigating deliberation characteristics, interruptions, and inaudible speech.

Notes: The table displays the ordinary least squares (OLS) regression with the Number of Topics ((1) and (2)), Euclidian Distance (3), Average Word Count ((4) and (5)), and the Negative Binomial regression with the number of Interruptions (6) and Inaudible (7) as the dependent variables. Columns (1), (3), and (4) show the results for the meeting-level sample. Columns (2), (5), (6), and (7) display the results for the meeting-member level. Women refer to an indicator variable where women = 1 and are thereby not applicable at the meeting level. The transcripts remark inaudible speech up until 1994, so the sample for column (7) does not contain observations after 1994. All models include intercepts. All meeting-member-level models are estimated with clustered standard errors at the member level to account for member-specific unobserved correlations. Columns (2) and (5) also include individual fixed effect (FE), except for models in columns (6) and (7), as these models did not run owing to insufficient data variation. Member resource controls include PhD, entry age, monetary policy inclinations, education in finance, engineering, policy, law, and business. Macroeconomic controls include CPI, CUE, slope of the yield curve, federal funds rate, return of Wilshire 5000, two time-lagged variables of each of these, and crisis and recession indicators. Estimations for the meeting level are conducted using the lm command in the Stats package in R. Estimations on the meeting-member level are conducted using lm.cluster command in the Miceadds package in R. The negative binomial regressions are estimated using the nbreg and dydx(*) commands in Stata. ***p < 0.01; **p < 0.05; *p < 0.10.

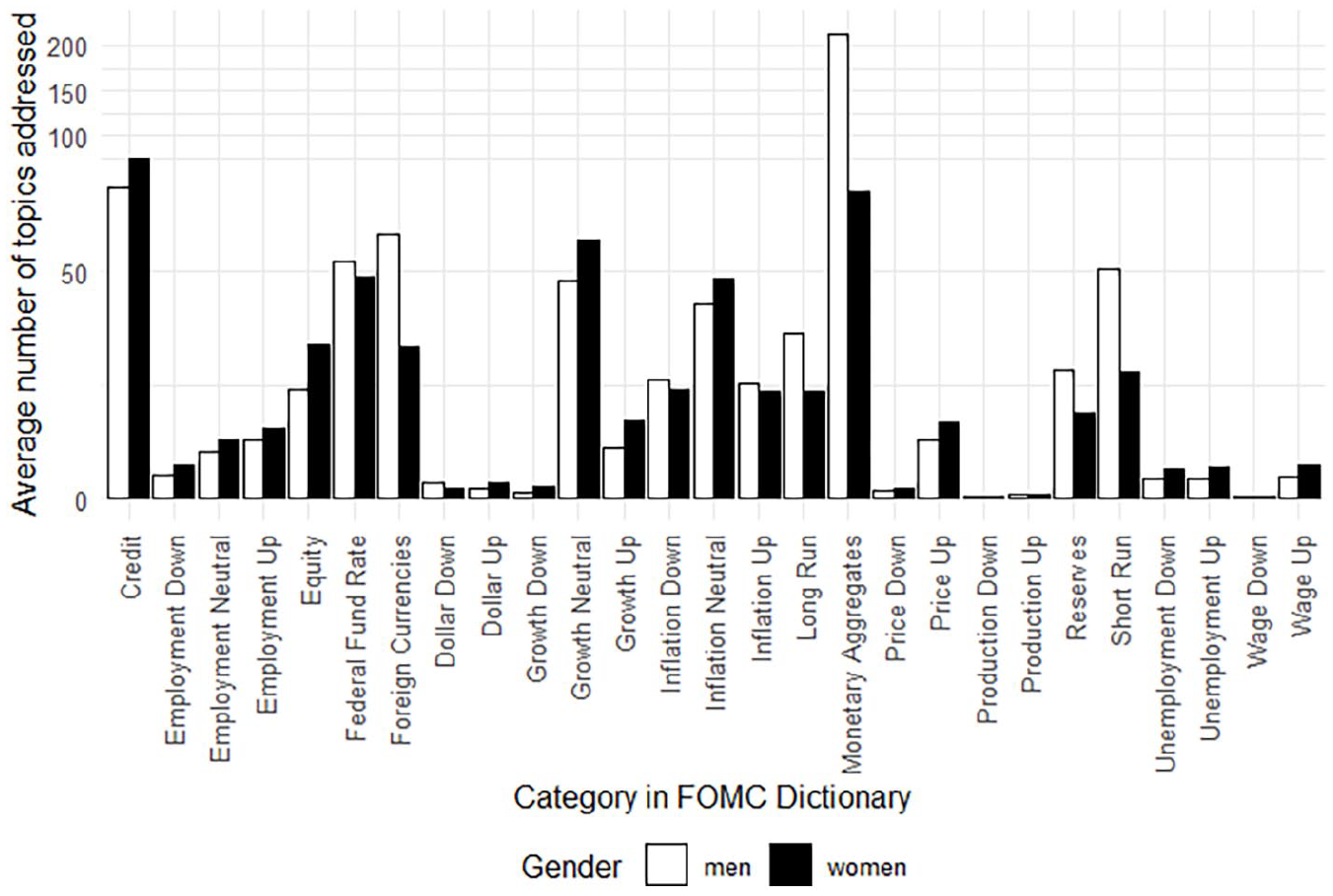

Figure 2 shows the average number of times each FOMC dictionary topic is addressed by each gender. Women members mention both employment and inflation more than men, suggesting that they address the two topics fundamental to the FOMC mandate regardless of their particular policy stances. 8 As shown in Figure 2, women address relevant topics that are generally overlooked by men.

Topics addressed by men and women.

Regression results for Equations (2) and (3) are reported in Table 3. Comparing the meeting-level results (column 1) with those of the meeting-member level (column 2) reveals that, while the meeting-level aggregate topic counts are not significantly influenced by gender diversity, higher gender equality significantly extends what each member discusses in the deliberation. These findings align with RDT, AT, and the literature, suggesting that women contribute different expertise and perspectives, enriching the conversation and increasing board effectiveness (Kim and Starks, 2016; Kirsch, 2018; Schwartz-Ziv, 2017).

Conversation distance and variability (distance and depth)

To further investigate the thoroughness of the discussion, we measure how far the conversation traveled using Euclidean distance (Equation (1)). Intuitively, a smaller measure means a shorter distance, implying that the conversation does not move and topics do not change, wherein a higher number implies a wide-ranging discussion where the topics are more heterogeneous. 9 We estimate the regression model specified in Equation (4), and the results are shown in Table 3, column 3. Higher gender diversity is significant and positively associated with a longer conversation distance, suggesting that meetings with a higher gender diversity tend to cover more ground/topics. 10

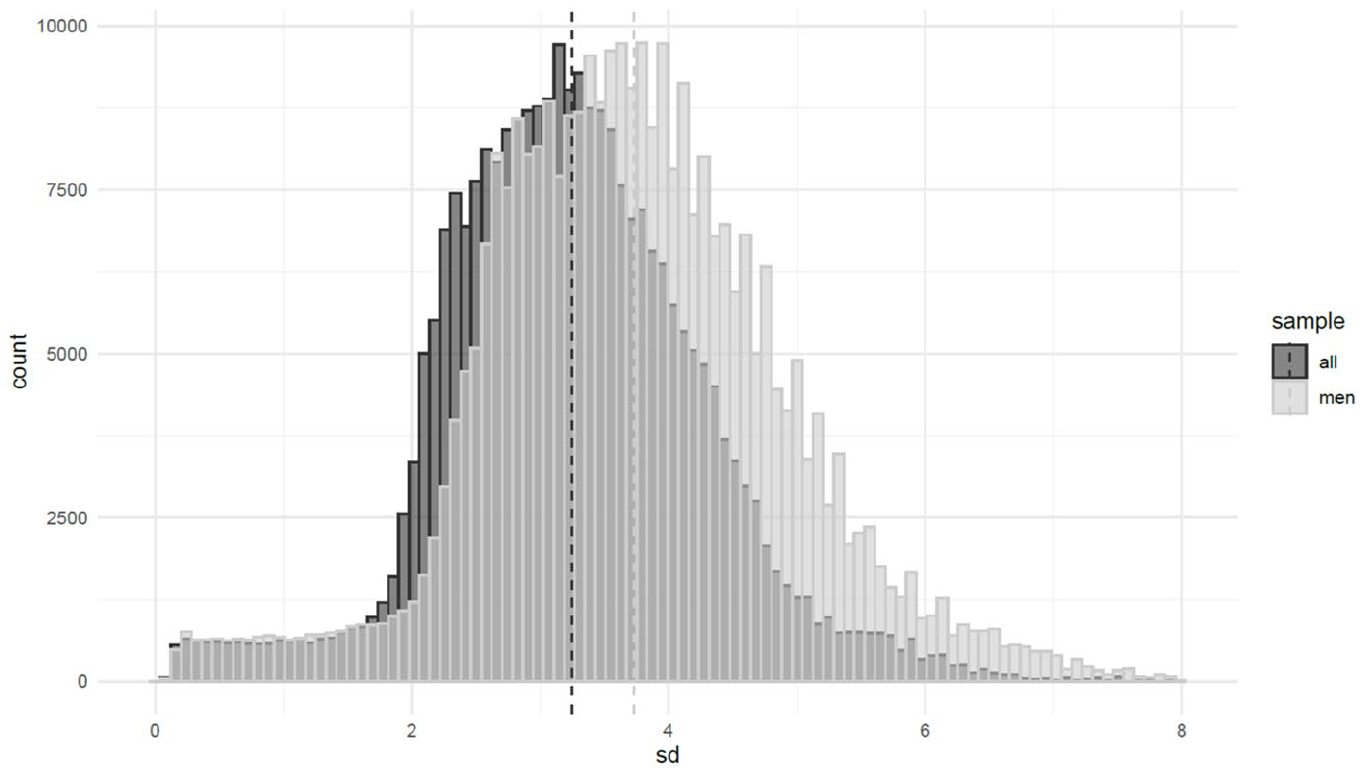

Conversation depth is examined by comparing the distribution of standard deviations of Euclidean distance by gender (Figure 3). We find that conversation variability is higher among men, indicating that men tend to have lower conversation depth when women are not included. The Kolmogorov-Smirnov test shows a significant difference in the two distributions (p-value < 0.001), suggesting women not only broach more topics, but their topics are discussed by all members. Overall, our results show that women contribute both in breadth and depth to the committee discourse.

Standard deviation of Euclidean distance.

Number of words spoken (length)

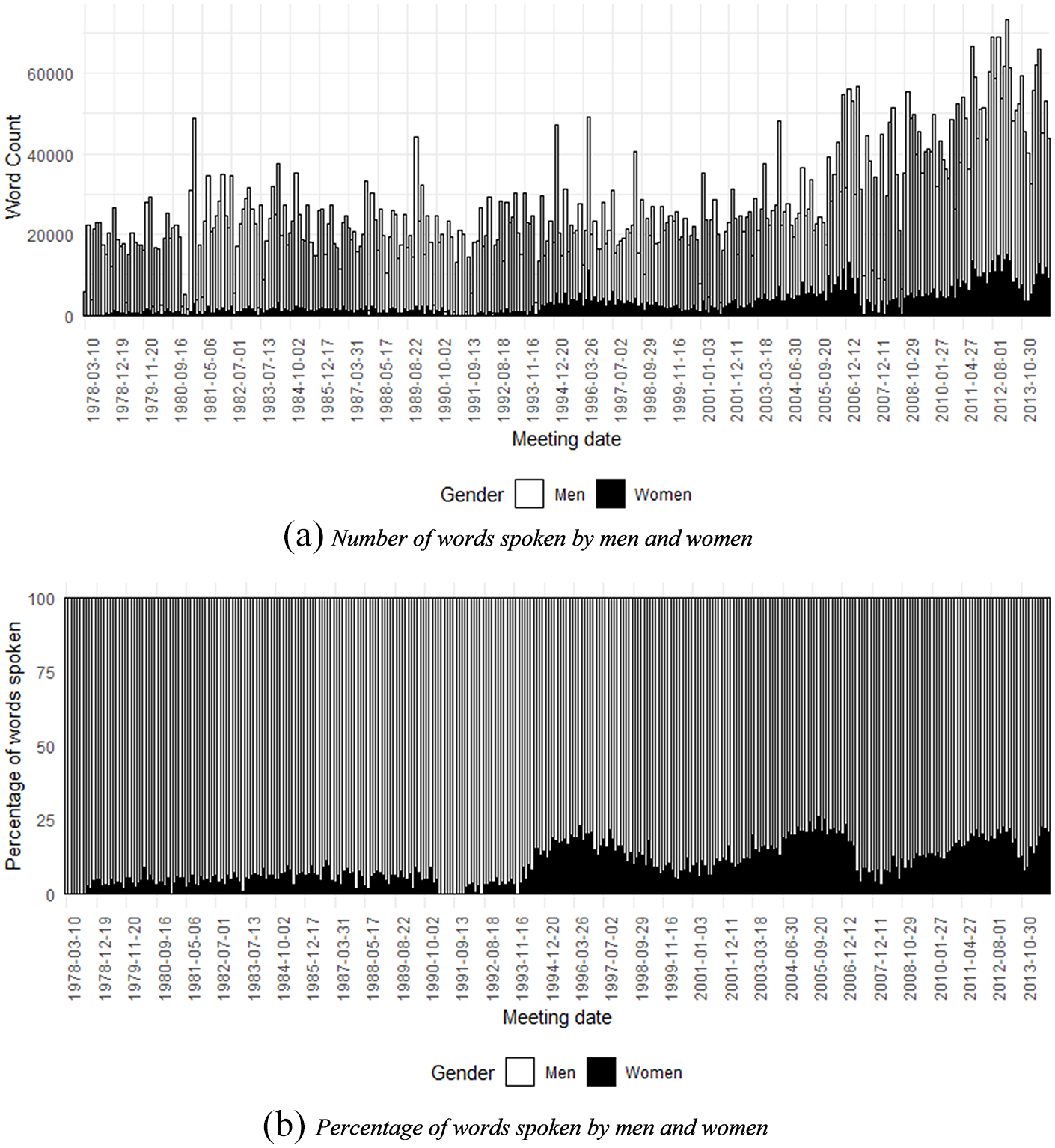

Figure 4 Panel (a) displays the number of words spoken by men and women per meeting. While the number of words spoken has an upward trend over time, there has been a substantial increase since the 2008 financial crisis for both men and women. Figure 4 Panel (b) shows the percentage of words spoken by each gender. Over the sample period, women make up an increasing fraction of the discussion, demonstrably so after 1993. Furthermore, comparing Figure 4 and Figure 1, the increased word counts are not simply coming from changes in the number of women on the committee.

Words spoken by men and women.

Table 3, column 4 shows the regression results of average word counts at meetings. The estimated coefficient for gender diversity is positive but not statistically significant, indicating that we do not find support that the meetings are significantly longer when there is higher gender diversity. When estimated at the meeting-member level, we find that participants speak significantly more when the committee is more gender-balanced (Table 3, column 5). 11

In summary, we find support for H1. In particular, we find that members in meetings with higher gender diversity have more active discussions, address a broader range of topics, cover wider distances in conversation, have a more in-depth discussion by women, and have a more engaged discussion overall.

Disagreement

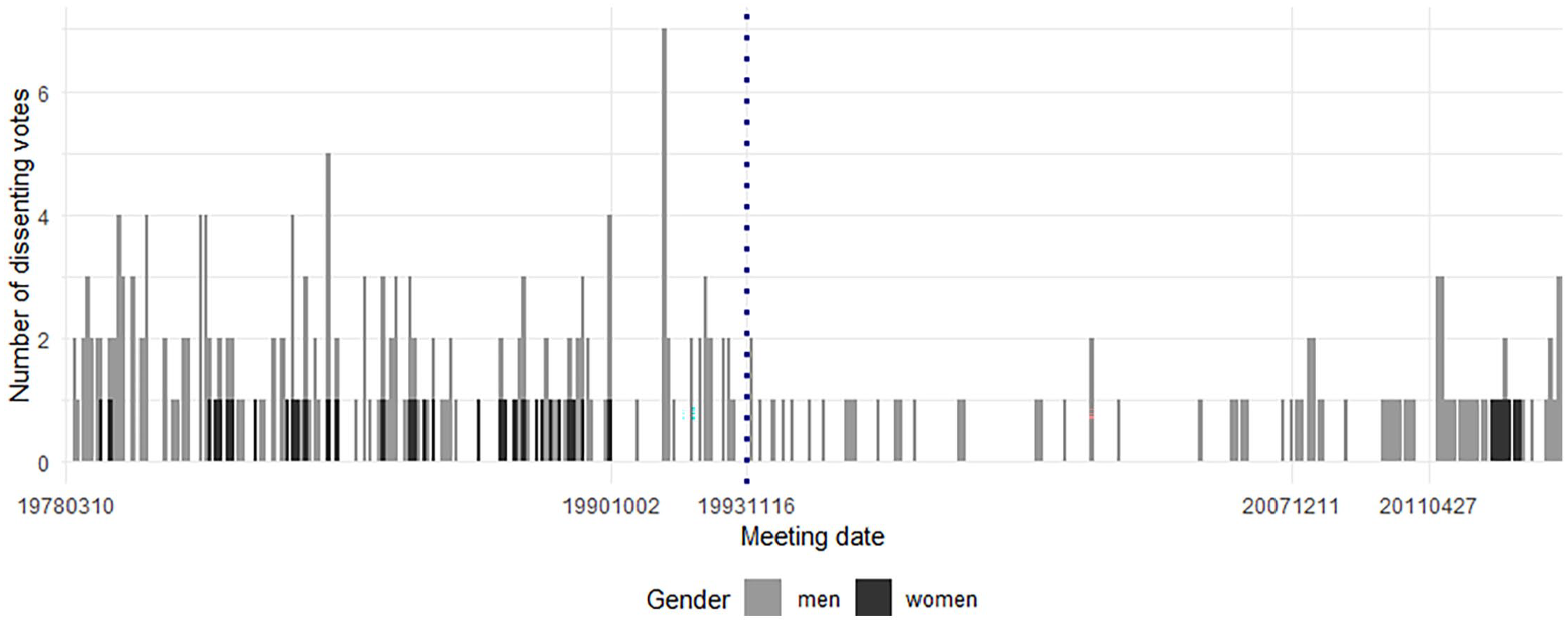

Within the sample, there are a total of 260 dissenting votes, of which 17 (6.54%) were cast by women. Figure 5 shows that the dissenting votes have declined over time. As in Lähner (2018), the 1993 change in the transparency policy produced a visible and abrupt change to the number of dissenting votes.

Dissenting votes.

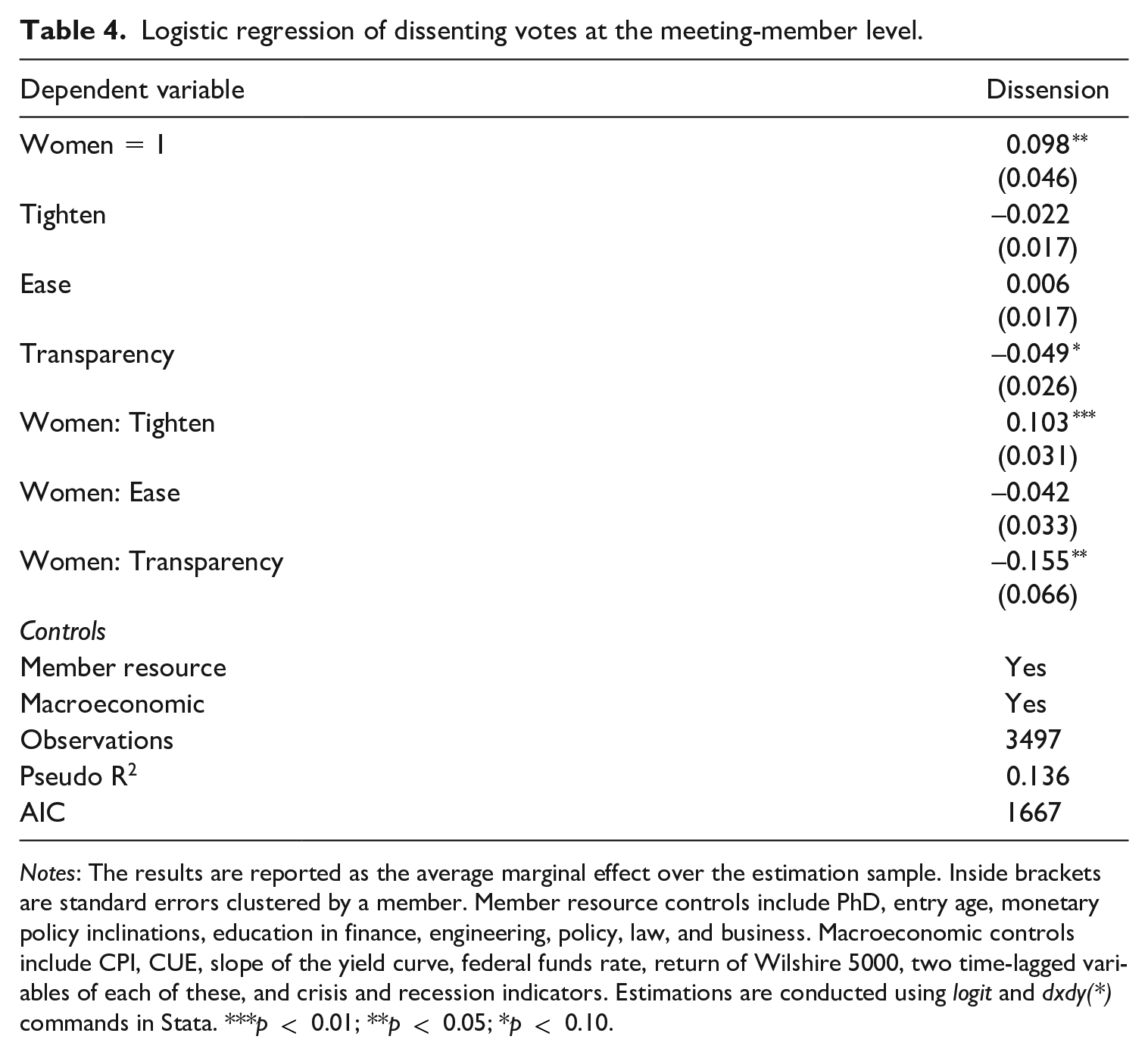

Table 4 displays the results of the logit model as specified in Equation (5), showing that women are more likely to cast a dissenting vote, as seen by the positive and significant effect of the women indicator. Further, women are more likely to cast dissenting votes if the policy action is to tighten, as shown by the positive and significant interaction term (Women: Tighten). We find no change in the probability of dissent when the policy outcome is ease for both men and women, based on the insignificant coefficients for Ease and Women: Ease.

Logistic regression of dissenting votes at the meeting-member level.

Notes: The results are reported as the average marginal effect over the estimation sample. Inside brackets are standard errors clustered by a member. Member resource controls include PhD, entry age, monetary policy inclinations, education in finance, engineering, policy, law, and business. Macroeconomic controls include CPI, CUE, slope of the yield curve, federal funds rate, return of Wilshire 5000, two time-lagged variables of each of these, and crisis and recession indicators. Estimations are conducted using logit and dxdy(*) commands in Stata. ***p < 0.01; **p < 0.05; *p < 0.10.

We find that the transparency policy has a marginally significant and negative effect on dissension for both men and women. However, the interaction between women and transparency is negative and significant, showing that women are less inclined to cast a dissenting vote when individual voting records are published. Our results indicate that women are more likely to dissent (H2a rejected), with an even greater likelihood when the outcome is tightening policy. However, the transparency policy reduced women’s propensity to dissent more than men (H2b supported).

Interruption and not being heard

Table 3, columns 6 and 7, display the results of the interruption and inaudible speech. Women indicators are negative and statistically insignificant for the interruption, showing that women are not interrupted more than men. The coefficient for the inaudible speech by women is negative and statistically significant, showing that women are significantly less likely to be not heard by the members. This analysis indicates that women are able to contribute to the discussion without being interrupted or by not being heard. Moreover, gender diversity did not significantly affect the degree of interruptions or inaudible speech.

Policy decisions

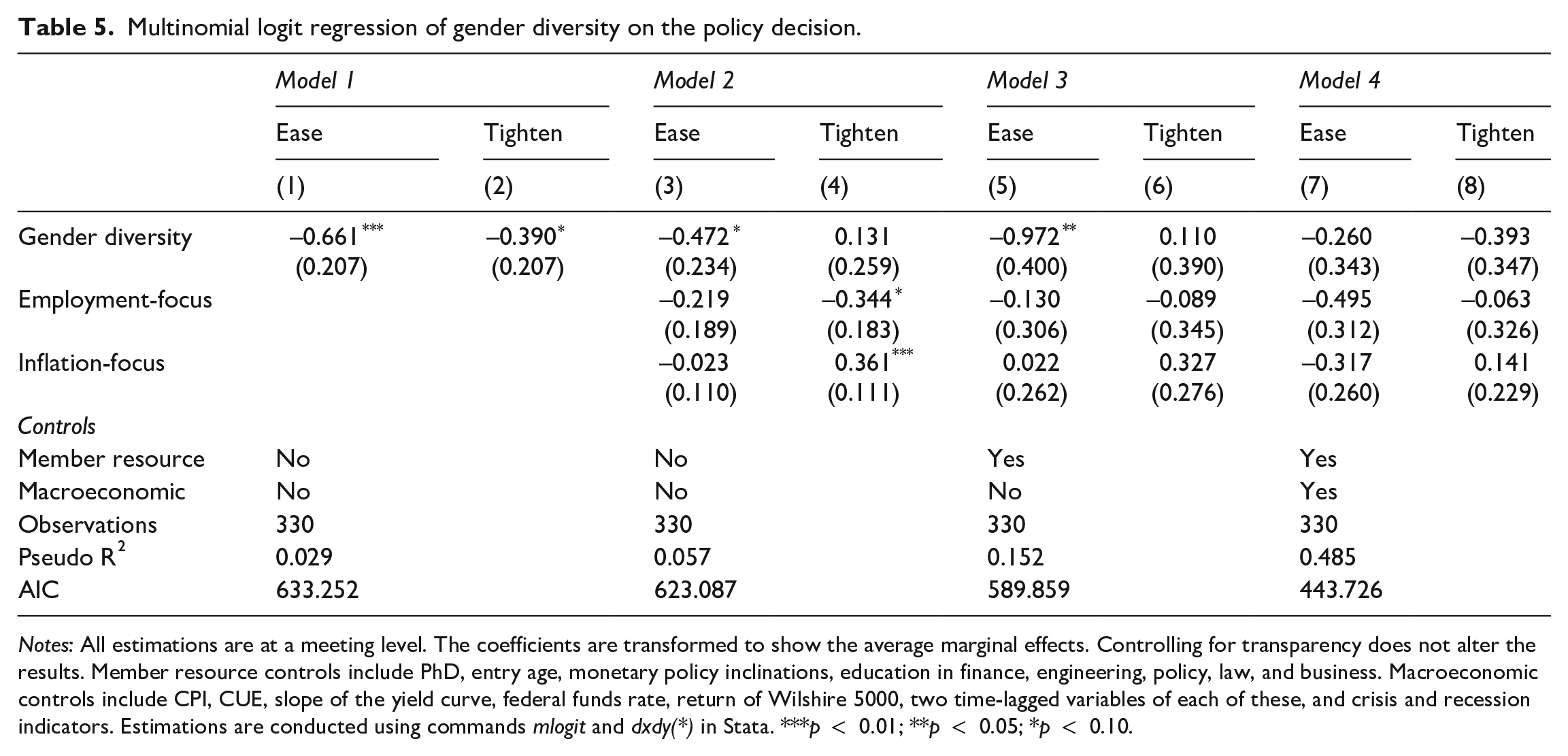

How gender diversity affects the committee’s decisions is investigated via the logit model specified in Equation (6), where the results are shown in Table 5. We show the results stepwise to clearly demonstrate the endogeneity issue. Model 1 in columns 1 and 2 shows the baseline model with the gender diversity at the meeting as the only independent variable. In this regression specification, we find that higher gender diversity is significantly negatively associated with both ease and tighten monetary policy. However, without the appropriate controls, we do not know if this effect is driven by the macroeconomic conditions (economy-wide trends that happen to coincide with gender diversity measures) and/or gender diversity acting as a proxy for member resources. Model 2 in columns 3 and 4 shows results when the monetary policy stance is added to the baseline model, as these traits influence monetary policymaking (Chang, 2001). As expected, employment-focus is negatively and marginally significantly associated with tighten, and inflation-focus is positively and significantly associated with tighten. Gender diversity is still negatively associated with ease with a marginal significance but no longer significant in affecting tighten. Next, we add all the member resource variables (Model 3 in columns 5 and 6) and find that gender diversity is still negatively associated with ease. It might be because the period with higher gender diversity tends to coincide with periods experiencing economic expansion. 12 It is also worth noting that the monetary policy stance is no longer significant. This is probably owing to the high correlation with other member resources (Table 2). Finally, when both member resources and economy-wide conditions are added (Model 4, columns 7 and 8), the coefficient for gender diversity for both ease and tighten outcomes are not significantly different from zero, suggesting that gender diversity does not explain the committee’s policy decision when other relevant factors are properly controlled. As discussed earlier, gender diversity is correlated with many member resources, which explains why gender diversity loses its significance when member resources are added to the model.

Multinomial logit regression of gender diversity on the policy decision.

Notes: All estimations are at a meeting level. The coefficients are transformed to show the average marginal effects. Controlling for transparency does not alter the results. Member resource controls include PhD, entry age, monetary policy inclinations, education in finance, engineering, policy, law, and business. Macroeconomic controls include CPI, CUE, slope of the yield curve, federal funds rate, return of Wilshire 5000, two time-lagged variables of each of these, and crisis and recession indicators. Estimations are conducted using commands mlogit and dxdy(*) in Stata. ***p < 0.01; **p < 0.05; *p < 0.10.

Discussion and conclusion

Firms face substantial pressure to better comply with Environment, Social, and Governance (ESG) standards and meet stakeholder expectations. Well-functioning committees are a necessary condition to address this pressure, and greater gender diversity has been viewed as a way to improve committees’ effectiveness. However, the research on the effects of gender diversity on committees and organizational performance has not sufficiently addressed the mechanism—if and how gender diversity affects the committee and the organization. This article contributes to the literature via the resource dependency and agency theories by identifying two channels where gender diversity affects committees: deliberation quality and member resources. We then provide empirical support for these two processes by utilizing a unique dataset comprised of the transcripts of the Federal Open Market Committee of the US Federal Reserve from 1978 to 2014, matched with member resources and economy-wide contextual factors.

We find that a higher female representation influences how the committee deliberates. First, higher gender diversity is associated with more comprehensive coverage of topics, both by breadth and depth. Women tend to address a broader range of issues than men, which is in line with Konrad et al. (2008) and Schwartz-Ziv (2017). Second, more gender-balanced meetings are associated with both men and women talking more. Thus, these results are not solely driven by what women say at the meeting; but also by how the presence of women impacts male members’ behavior. Men talk about broader topics with women present, and that effect increases with gender diversity. These results are consistent with research comparing same-sex and mixed-sex group dynamics (Aries, 1976) and the idea that women are better facilitators (Konrad et al., 2008; Nielsen and Huse, 2010).

Third, higher gender diversity is associated with more dissenting votes, particularly by women on tightening policy outcomes. This reflects their monetary policy stances tending to focus on employment (Bordo and Istrefi, 2018; Chappell et al., 2000). While a higher likelihood of dissension among women goes against the general female trait of avoiding conflict (Bertrand, 2011; Hyde, 2014), it does conform to the view that women in these competitive and male-dominant environments (e.g. monetary policy committees) are different from women in the general population (Adams and Funk, 2012; Eckbo and Ødegaard, 2020). This also implies that the increased gender diversity may be associated with more disagreement. Still, thorough discussion is precisely what this committee is mandated to perform, and having more women seems to enhance that function. That said, we also find that the policy to release transcripts to the public lowers the propensity to dissent more for women than men. It may indicate that confirmatory pressure was higher among women, but further investigation is needed for a better understanding. Finally, when we examined the effect of gender diversity on the committee’s policy decisions, we did not find any direct effects. Instead, gender diversity works through altering the member resource pool, shown by the high correlation with member resources.

By theorizing and testing two channels, we detailed the impact of specific resources contributed by committee members. In particular, members’ monetary policy stance, education and professional expertise impact the committee’s policy decision, whereas gender impacts how the committee functions. This delineation is a new insight that enriches our understanding of how gender balance influences committees. We also note that the high correlation among member resources at the meeting level implies that member resources are interrelated and require caution when included in an empirical investigation. Another important factor that we control for is the economy-wide conditions. The committee’s decisions are not made in a vacuum—they are considered within the current and expected business environment. Omitting such a contextual factor, especially when they are (systematically or by chance) correlated to gender diversity, delivers results that are misleading.

We are cognizant that our results could be interpreted as women are not influential enough to affect policy decisions. Being in an important committee and speaking up would be seen as incongruent with communal gender norms (Agars, 2004; Eagly and Karau, 2002; Rudman et al., 2012). If that is the case, women may be shut down or interrupted and/or not able to assert themselves in the conversation (Heath et al., 2014). However, our results are inconsistent with such a stifling environment, as women are not more likely to be interrupted or speak inaudibly. These results, our own readings of the transcripts, and the finding that women are more likely to cast dissension votes, together suggest that women in the FOMC are able to contribute equally to the deliberation.

Why are women in the FOMC able to speak up, dissent, and engage in conversation, whereas in other committees, women do not seem to exert sufficient influence? We offer several possible reasons related to the specific FOMC context. First, the FOMC is mandated to make extremely high-stake policy decisions that are speculated, watched over, and scrutinized by the world. Given that the committee is relatively small, the FOMC may not be able to afford to dismiss the member resources endowed by each member regardless of gender. Second, these are elite women appointed to serve in the highly influential committee with no mandatory gender quota. When women achieve very high-status positions – despite the difficulty they may face in many professional situations, for example, double-standard and backlash (Rudman and Phelan, 2008) – they are viewed as extra competent (Rosette and Tost, 2010). It might also be relevant that these women seem to go through a more “standard” career path for FOMC members (PhD degrees in economics/finance or law followed by a career as an economist either in academia or within the Federal Reserve). These conditions could provide additional credentials, legitimacy, and relational capital for female FOMC members. Third, the procedural custom of the FOMC where the chair ensures each member has opportunities to offer their professional knowledge and opinions may be relevant. This point responds to what is discussed in Sidhu et al. (2021), calling for an investigation of how the companies’ wider culture, systems, and practices moderate the effect of gender diversity.

Although the FOMC context provides many advantages, it also limits generalizing the findings. The members of the FOMC certainly do not represent a random sample, and the member characteristics may not be representative of other business committees. We also note that our setting did not provide enough variation to identify the effect of critical mass (Kanter, 1977), 13 although it could be important for gender quota argument and requires further research. From a methodological perspective, we took a quantitative approach using Natural Language Processing of transcript data. While this approach may miss subtle nuances in conversation that a qualitative approach may uncover, it has produced results that heretofore have not been demonstrated in a committee’s deliberation. It is also worth noting that even in a situation where women could be considered similar to men in their credentials and capabilities, we still document that women contribute uniquely to the committee.

In terms of a practical implication of this research, we demonstrate that gender diversity impacts the thoroughness and legitimacy of discussions and enhances the committee’s monitoring and governance functions, which are important for stakeholders. Therefore, creating a balanced committee composition that allows members to participate and impact the deliberation is crucial to ensure its effectiveness.

Supplemental Material

sj-pdf-1-hum-10.1177_00187267221135846 – Supplemental material for Effect of gender composition of committees

Supplemental material, sj-pdf-1-hum-10.1177_00187267221135846 for Effect of gender composition of committees by Erika Christie Berle, Kenneth Kavajecz and Yuko Onozaka in Human Relations

Footnotes

Acknowledgements

For helpful comments and suggestions, we thank seminar at the University of Stavanger, of the ICGR 2022: 5th International Conference on Gender Research and the Norwegian Bank Investment Management Group. We acknowledge Stefan Andrew Aase for providing expert coding help. In addition, the authors are most grateful to Chidiebere Ogbonnaya, Associate Editor, Human Relations, and four anonymous referees whose insights and patience made this a much better article. Any remaining errors are our own.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.