Abstract

(Dutch) veterinarians have increasingly been confronted with conflicting accountability regimes, related to data-driven, networked accountability systems, to decrease the use of antibiotics in veterinary practices. Based on our longitudinal ethnography (2012–2020), we propose a conceptual model that illustrates how professionals intra-actively become positioned in different accountability regimes, yet which is continually diffracted by the recalling of their responsibilities to proximal and distant others. By taking an agential realist approach, we contribute to recent critical perspectives on accountability by showing how veterinary professionals become positioned as specific accountable subjects and yet how such positioning simultaneously produces the ‘borderlands’ – a space of indeterminacy in which the accounting practices of the professional are continuously weighed in light of incommensurable responsibilities. Based on our results, we show how conflicting accountability regimes are—as often argued—not to be ‘fixed’ through commensuration, nor are they dysfunctional. Rather, they create the very condition of indeterminacy, opening up the possibility for professional responsibility. We offer suggestions for how to further investigate this appreciation of the borderlands, for example, by focusing on how the account holder can draw from other responsibilities to counter a dominant accountability regime, and how governing authorities can become positioned as responsible for keeping professionals in the borderlands.

Keywords

Introduction

Where there is social relationality with others, there is normally some form of accountability practice expected (e.g., Frey-Heger and Barrett, 2021; Messner, 2009). As such, accountability practices have been a topic of interest within a variety of disciplines ranging from institutional-theory-based studies (e.g., Courpasson, 2000; De Bree and Stoopendaal, 2020; McGivern and Ferlie, 2007; Pas et al., 2021; Reay and Hinings, 2009; see also Andersson and Liff, 2018 for an overview), to critical accountability literature (e.g., Fenwick, 2016; Joannides, 2012; Kamuf, 2007; McKernan, 2012; Roberts, 2017, 2021), to public governance literature (e.g., Bovens et al., 2014). There is much diversity and some unity in how to define accountability and account for its enactment (e.g., Mulgan, 2000; Sinclair, 1995). In terms of this diversity, such approaches can be divided, roughly, into structural approaches and personal approaches to accountability. The structural approach tends to take a representationalist, objectivist view on accountability; in the personal approach—deployed more by critical accountability scholars—accountability is normally discussed in terms of a moral/ethical expression of responsibility (Dillard and Vinnari, 2019; Sinclair, 1995). In terms of unity, both approaches are concerned with explaining how professionals cope with the expectations emanating from the multiplicity of ‘accountability regimes’ 1 (the structural) within which they find themselves related to different proximal and distant human and non-human others (the personal) (Bovens, 2007; Keevers et al., 2012; Kurunmäki and Miller, 2011; Power, 1997; Strathern, 2000; Vosselman, 2016). It is in the intersection between these two orientations that our article is located, and where it seeks to make its contribution.

In this regard, we situate our work in the critical accounting literature. Critical accountability scholars have addressed the importance of a relational understanding of accountability to counter the predominance of the structural approach with its objectivist (representationalist) instrumental understanding of accountability—which tends to be mostly based in principal–agent theoretical understandings of the (distant) other (power holder) (Ahrens and Chapman, 2002; Barad, 2007; Frey-Heger and Barrett, 2021; McKernan, 2012; Roberts, 2021; Vosselman, 2016). A much-addressed concern in the literature is the apparent disconnect between accountability practices and responsibility that seems to be prevalent in representationalist approaches and tends to transform accountability—as a response(ability) to the other—into something in which the other is lost and the accountability practices become an end in and of themselves (Fenwick, 2016; Solbrekke and Englund, 2011). As McKernan (2012) argues, along with some others drawing on Levinas (e.g., Butler, 2005; Joannides, 2012; Messner, 2009; Shearer, 2002), without the anchor of responsibility, accountability practices can paradoxically produce quite the opposite, namely irresponsibility.

Some recent theoretical arguments have been offered for how accountability regimes should include a space for responsibility, ideally with relative power symmetry between the power holder (e.g., regulator) and account holder (Vosselman, 2016), or by developing ‘accountability-based’ accounting systems that provide information and criteria relevant to the relational responsibility network (Dillard and Vinnari, 2019; Tanima et al., 2020). As much as we support a relational ontology of accountability, including its associated notion of performativity of accountability systems, these current suggestions lack explanatory power in how subjects become positioned by, and position themselves in, already existing relational accountability (power) regimes. In other words, what is missing is empirical illustrations of the messy way in which the enactment of accountability regimes can performatively both deprive and enhance professional responsibility simultaneously. Moreover, despite good suggestions on how to ‘fix’ representationalist or accounting-based accountability systems, it seems somewhat idealistic to expect that current predominant representationalist accountability regimes can be excluded from the responsibility meshwork, partly due to the seductive nature of commensuration (Redden, 2019; Sauder and Espeland, 2009) and existing deeply rooted power asymmetries.

We would argue that what remains to be further investigated, especially empirically, is how to somehow secure an appropriate relationship between the responsibility for self and all others (human and non-human alike) as the very condition of possibility for responsible action (e.g., Frey-Heger and Barrett, 2021), and in particular, the role of incommensurable accounting regimes in producing such a responsible professional. This article aims to contribute to such a critical perspective in which accountability is to be understood as an inherently relational material-discursive practice, as it relates to our responsibilities to both proximal and distant human and non-human (e.g., animals) others. By taking a relational ontological (agential realist, Baradian) approach to accountability, we take both ways of understanding accountability into account: we do not simply reject (or try to fix) the structural, representationalist understanding of accountability by addressing its limits, nor do we simply ascribe to the personal responsibility approach, which has been argued for by Roberts (2009; 2018, 2021) and Messner (2009). Rather, we argue for, and illustrate empirically, how the conditions of possibility for responsibility are produced through the way in which incommensurable material-discursive accountability regimes intra-actively enact the professional as responsible (or not). From this perspective, two interconnected preoccupations or concerns emerge that are relevant to us.

Once responsibility is brought back into our understanding of accountability, a concern then emerges regarding the nature of different, possibly conflicting, accountability regimes and their perceived hybridity—or commensurability. It is often argued that professionals tend to find themselves in ‘hybrid accountability’ that ‘results from the blurring and shifting of boundaries between accountability regimes, mixing actors, logics, norms, and mechanisms’ (Benish, 2020: 295). ‘Hybrid accountability’ assumes that professionals can somehow respond to the often-contradictory demands of these accountability regimes, in terms of their specific accountability claims, as a more or less skilful bricoleur deploying strategies such as compartmentalization, assimilation, blending, blocking, and so forth (e.g., Skelcher and Smith, 2015). Although hybrid accountability might seem to resolve issues related to the conflicting demands of accountability regimes—through a process of commensuration (Espeland and Stevens, 1998) that renders equal that which is unequal (e.g., Benish, 2020; Skelcher and Smith, 2015)—we argue that the notion of hybrid accountability paradoxically functions to hide the irreconcilable responsibilities to the self and different others, which can indeed result in irresponsibility.

A second concern relates to what critical accountability scholars have highlighted as the anthropocentric nature of representationalist or objectivist understanding of how accountability regimes function as governing technologies (e.g., Vosselman, 2016). The prevailing assumption in objectivist representational approaches to accountability regimes is one in which the human is portrayed as a pre-existing more or less autonomous actor, who can act and be made accountable (e.g., Benish, 2020). We suggest, drawing on the work of Barad (2007), that accountability regimes are material-discursive ensembles that involve a multiplicity of entangled human and non-human (technological) agencies (Scott and Orlikowski, 2012), which circulate in ways that are fluid and performative (e.g., Keevers et al., 2012; Vosselman, 2016). That is, accountability regimes, with their technologies of representation, not only reflect the assumed accountability of the accountee but also simultaneously produce what such practices assume: that is, the subject that can be made accountable (Butler, 2005; Messner, 2009). Importantly, this subject becomes enacted through the circulation of a multiplicity of material-discursive agencies in which the accountee acts and is simultaneously enacted, often situated and contingently (Hultin et al., 2021; Introna, 2019). However, what needs to be further explained is how the conditions of possibility for responsibility are enacted in the space in which the accountable subject is always and already positioned—and in a multiplicity and contradictory manner. In short: in what way can the subject be said to be responsible—to all other others—when they are always and already enacted specifically through a multiplicity of contradictory accountability regimes?

This article aims to rethink and contribute to our current understanding of professional accountability by (1) reconnecting accountability to responsibility to proximal and distant others; (2) in doing so, arguing for a different understanding of accountability regimes, and thus, the inherent impossibility of ‘hybrid accountability’, as often presented as a solution in more structural approaches to accountability; and (3) by taking the material-discursive and performative nature of accountability, and thus, the limits of accountability, seriously by calling for an appreciation of the ‘borderlands’ (Barad, 2014). As such, the question we aim to answer in this article is: How does the position of the responsible/ethical subject become enacted within conflicting material-discursive accountability regimes?

To do this, we engaged in an ethnographic study of Dutch veterinarians over a period of nine years (2011–2020). Dutch veterinarians, until about a decade ago, were granted professional autonomy and allowed self-regulation. However, due to public and political pressure, their work has increasingly been recognized as a public health issue (Geenen et al., 2001). This pressure stemmed from their abundant use of antibiotics and the emergence of antimicrobial-resistant bacteria such as MRSA in livestock (Bondt et al., 2009). The particularity of veterinary work, which is already characterized by ambiguities and contradictions (e.g., Clarke and Knights, 2018, 2021), is now a source of even more tension for veterinarians as it can be difficult, if not impossible, for them to adequately account for professional conduct according to often-conflicting accountability demands by an expanding host of proximal and distant others.

Structural and personal approaches to accountability regimes

The structural governing of the accountable subject

Accountability presupposes a particular implicit or explicit agreement about what constitutes a legitimate account, according to a particular discourse of justification (Sinclair, 1995). In the structural approach, accountability refers to a technical property, a role or contract, a structure, or a system, in which boundaries are clear and demarcated and more or less uncontested (Sinclair, 1995). According to the established set of definitions and concepts, accountability has become a general term for any mechanism that makes actors responsive or ‘answerable’ to those that they work with or for (Acar et al., 2008; Mulgan, 2000). From such a perspective, accountability is thus perceived as a regulatory phenomenon that is imposed on actors and to which actors are required to respond (Ezzamel et al., 2007; Hallett, 2010; Yang, 2011). The structural approach employed in much of the accounting literature is characterized by quantified language in which context is conflated into abstract, detached, and rational terms (Sinclair, 1995). Here, an ‘account’ can and has to be delivered, mostly for the sake of control for some other(s)—typically based in principal–agent theory (Vosselman, 2016), where senior management, regulators, auditors, etc. (the principal) act on behalf of beneficiaries or distant others in need (Frey-Heger and Barrett, 2021). Other terms related to such a ‘representationalist’ understanding of accountability are ‘accountability as transparency’ (Roberts, 2009), ‘instrumental accountability’ (Vosselman, 2016), ‘accounting-based accountability’ (e.g., Dillard and Vinnari, 2019), and ‘hierarchical accountability’ (Frey-Heger and Barrett, 2021).

Accounting for distant others through representationalist accountability regimes is often mediated through technology (e.g., Frey-Heger and Barrett, 2021)—enacting what Foucault (1997) might call a ‘regime of governmentality’ (Faÿ et al., 2010). We would argue that increasingly technologically mediated, data-driven, and networked accountability systems rely heavily on processes and practices of commensuration. Although Espeland and Stevens (1998) define commensuration as a social process, we would instead define it as a material-discursive process that transforms ‘different qualities into a common metric [or measure]’ (p. 314). In short, it is a set of material-discursive practices that reproduces that which is incomparable into that which is comparable, of which counting is the paradigmatic example but in essence stretches beyond it—such as other valuing systems: ranking preferences, benchmarking, etc. Commensuration transforms qualities into quantities and difference into sameness, reducing and simplifying disparate information into numbers that can be easily compared (Espeland and Stevens, 1998), stored, and exchanged. As such, accountability regimes—through substantive commensuration—tend to govern the most intimate minutia of professional life, bringing the distant other into the here and now (Faÿ et al., 2010).

Scholars using a structural approach to accountability, for example, institutional-theory-based work in public accountability literature, have pointed to professionals currently being confronted with conflicting accountability regimes. This highlights how global public management reforms and changes in governance have stimulated the emergence of a plurality of ‘rationalizations’, referred to as ‘institutional logics’ (e.g., Pache and Santos, 2013; Skelcher and Smith, 2015), or in the context of accountability practices, ‘accountability logics’ (Benish and Mattei, 2020). Without going into detail about how ‘hybrids’ are theorized in this stream of literature (see, for example, Skelcher and Smith, 2015, for a more elaborate foundation for the term ‘hybrid’ from an institutional perspective), in essence, the term ‘hybrid accountability’ refers to ‘the blurring and shifting of boundaries between traditional accountability [mixing] actors, logics, norms, and mechanisms from public, market, and social accountability regimes by applying two or more of these differing regimes to the same situation at once (Skelcher and Smith 2015)’ (Benish, 2020: 293). Hybridity is created when two or more accountability regimes are integrated, assimilated, or blended; and is characterized as ‘blocked’ when there is an inability to resolve tensions between different accountability regimes, causing organizational dysfunction (Benish and Mattei, 2020; Heinzelmann, 2017; Skelcher and Smith, 2015). Hybrid accountability practices, then, are achieved, for example, by broadening the responsibility logic with new criteria (approved and checked by certifying bodies), which then enable actors to assimilate and articulate their hybrid performance objectives and actions (Baudot et al., 2020). Despite the fact that hybrid accountability practices might offer discursive ‘tactics’ to deal with conflicting demands for accountability, they still leave the question of how conflicting ‘felt’ responsibilities to different others are dealt with by professionals in situ.

A personal relational grounding of accountability in responsibility

Critical accountability scholars stress that responsibility, accountability, and subjectivity are relational enactments as they are already grounded in the self’s responsibility for and toward others (Roberts, 2009, 2018, 2021; Fenwick, 2016). For example, Roberts (2009) calls for a reconstitution of accountability as a vital social practice: ‘an exercise of care in relation to self and others, a caution to compassion in relation to both self and others, and an ongoing necessity as a social practice through which to insist upon and discover the nature of our responsibility to and for each other’ (Roberts, 2009: 969; 2017).

Based on a relational, ethical understanding of accountability, it is argued that representationalist accountability regimes open up the possibility of the alienation of the professional by others (Roberts, 2021), due to the commensuration of the complexity of the situations by transforming it into a quantity; and from others, due to the commensurating practices of performance indicators positioning the professional in a competitive relationship with other others, rivalling over the recognition that each craves. As such, these accountability regimes ‘create a permanent preoccupation with the defence or the promotion of the self, in which one is casted as the entrepreneur of the self’ (Roberts, 2021: 4)—that is, governing practices that produce a specific kind of self-disciplining accounting self (Knights and Clarke, 2018).

Most critical accountability scholars (e.g., Joannides, 2012; McKernan, 2012; Messner, 2009; Roberts, 2021) who discuss the relationality of accountability and responsibility tend to refer to the work of Levinas (1985), Butler (2005), and Foucault (1977) to highlight the limits and/or impossibilities of accountability. Drawing on the ideas of Levinas (1985), McKernan (2012) makes a distinction between singular and general responsibilities, each governed by different accountability demands and accountability practices. With singular responsibilities, McKernan refers to the responsibilities arising at the level of the individual (between the self and the other facing her, the proximal other). Such responsibility (and accountability) is primordial, infinite, and inexhaustible rather than being intelligible in terms of any specific social norm or rationale (Levinas, 1985). In situated professional practice, the professional tends to be accountable to the proximal (e.g., client, patient, peer) through a multiplicity of relatively implicit accounting practices such as treating them as a singular case, displaying appropriate functional knowledge, and enacting a ‘service ethics’ (Noordegraaf, 2007).

However, it is not just the opposite other to which one has to account, which is why McKernan also refers to general responsibilities, referring to one’s responsibility toward all other others (distant others, not present here and now)—what Levinas (1985) calls ‘the third’. The enactment of general responsibilities toward all others is governed by a demand for equality of access and conduct, which tends to lead to ‘an attempt to codify right behaviour, and to impose order and rationality on responsibility’ (McKernan, 2012: 266). As such, general accountability demands tend to aim for universality and require that we establish unambiguous rules for distinguishing between proper and improper conduct. Consequently, we find that accountability to distant others is often expressed in terms of norms, rules, and codes of conduct and is often enacted through quantification.

Our study particularly addresses what is indeed at the heart of accountability problematics as discussed in the literature (Joannides, 2012; McKernan, 2012), namely the (im)possibility (Roberts, 2021) of accounting for both singular and general responsibilities to proximal and distant others, simultaneously. For example, in responding to the general accountability demands of distant others—in accordance with rules, norms, standards, etc.—a professional might be hampered in responding to the very specific situated and singular demands of the one facing them, here and now. Similarly, responding to the legitimate singular demands of the other (here and now) might indeed in some way contravene the general accountability rules, norms, and standards imposed, reasonably, by distant others. Hence, McKernan (2012) claims that responsibility and accountability are paradoxical and aporetic.

However, this is not yet the complete picture of the relationality of our responsibility network. What about the responsibility the self has for itself (surely the self is also another to itself) (Butler, 2011)? For the self to respond to the other and the third, it needs to take care of itself—as has been argued by Foucault (1998). Of course, taking responsibility for the other and the third is in some way, though not entirely, taking responsibility for the self (Haker, 2004). For Foucault (1998), contra Levinas, the ethical subject only becomes possible through practices of freedom, the self actively making itself. Only such a self can be responsible—and so we can go to and from, endlessly, without firm ground (Haker, 2004). Thus, we see in responsibility a set of paradoxical and aporetic relationalities: the self to itself (the professional identity), the self to the more or less proximal, visible other (the client, the colleague(s), the animal), and the self to the invisible third (the regulator, the public).

Fixing accountability: Grounding accountability in responsibility, somehow

More recently, critical accountability scholars have started to address this aporetic incommensurable tension by trying to bring back responsibility to accountability regimes—albeit mostly theoretically. Vosselman (2016), for example, emphasizing how to understand and improve the personal positioning, suggests a duality frame in which accountability and responsibility are simultaneously addressed, by backgrounding the instrumental accountability regime and foregrounding the relational response-ability frame—a decentred frame that originates from the interconnected intentions of individuals at local positions. ‘It encourages and channels intrinsic motivation, enhances committed behaviour and self-realization and it pushes purely economic and opportunistic interests to the periphery. What it creates can be characterized as a moral community reflecting and constructing a performance management regime through which individuals benefit from open communication’ (Vosselman, 2016: 617/618). Dillard and Vinnari (2019) have a similar intention by offering a critical dialogic understanding of accountability, explicitly recognizing the presence of incommensurable ideological orientations (radical negativity) and asymmetrical power relationships (hegemonic regimes, power difference between power holder and account holder) associated with accounting, accountability, and responsibility relationships (p. 22). These elements can provide a framework for motivating and engaging in dialog and debate regarding accountability systems in which the responsibility network and the accounting system are brought together, by regarding the accountability system as an interface between representations of actions/outcomes and criteria for evaluation delivered by constituents of the responsibility network.

Both studies provide frameworks and suggestions to ‘fix accountability’ by (1) somewhat acknowledging the issue of incommensurability between plural, conflicting accountability regimes and (2) explicitly addressing the problematics or limitations regarding the relationship between accountability regimes and relational responsibility networks. However, both frameworks lack empirical grounding for how professionals become positioned, and position themselves, in and through accountability regimes when providing accounts to all human and non-human others. Moreover, they seem to ignore the matter and importance of indeterminacy to produce the possibility of being responsible. It is here that an agential realist or relational ontological approach can enhance our understanding, which we will explore in further detail below.

Accountability from a relational ontological perspective

Accountability regimes as material-discursive apparatuses

Taking a relational ontological approach to accountability regimes and systems implies important reworking of materiality, discursive practices, agency, and causality, among others (Barad, 2007). Such a relational understanding of accountability opens up the possibility to acknowledge how phenomena such as accountability come into being in and through relationality and do not pre-exist such relationality (Barad, 2007; Vosselman, 2014). Instead of merely regarding accountability regimes as socially agreed discourses of justification, embodied in socio-technical systems, accountability regimes should rather be understood as material-discursive apparatuses—that is, ongoing material-discursive (re)configurations through which ‘objects’ and ‘subjects’ are produced (Barad, 2007: 148), or come into being. Taking Barad’s elaboration of apparatuses (2007: 146), here, we define accountability regimes as specific material-discursive practices that produce differences that matter, relationally to the self and others. Specifically, they both enact what counts as meaningful/legitimate discourses of justification and simultaneously produce the subject of which they speak. As Barad suggests (1998: 98), apparatuses are not passive measuring instruments that mirror reality. Rather, they are ‘productive of (and part of) phenomena’, simultaneously enacting and organizing the phenomena—the norms, the account, the accountee, etc.—that they supposedly reflect. That is to say, they are performative (Orlikowski and Scott, 2014).

The relational and material-discursive enactment of accountable subjects in entangled accountability regimes

Drawing on the agential realist perspective of Barad (2007), we want to more closely consider the manner in which accounting subjectivity is performatively produced, in and through material-discursive accounting practices. Barad suggests that we replace the ‘actor-centric’ notion of interaction (which assumes pre-existing actors) with intra-action, which she defines as ‘relations without pre-existing relata.’ She is not saying that there is nothing and that then relations somehow magically produce something. Rather, she is suggesting that in the ongoing relational becoming of the world, a dynamism of forces or processes encounter each other intra-actively, thus enacting specific subject positions in the moment and duration of the intra-acting forces. Being positioned ‘specifically’—as an accountable subject, for example—means that in such positioning, specific ways of being accountable come to be understood (by the one positioned) as possible, obvious, meaningful, and appropriate to do (and others not), within the intra-active ongoing flow of action itself. Differently stated: the professional is not a specific accountable subject as such, but rather becomes enacted as one by being positioned in and through the situated relational flow of material-discursive practices of a particular accountability regime. As Barad (2007) puts it, responsibility requires an accounting of the larger material-discursive arrangements (i.e., the full set of intra-actions) that participate in the performative enactment of the phenomenon being investigated or produced, including the enactment of specific boundaries of mattering and meaning. For Barad, ethics is therefore not about a correct response to a radically exterior(ized) other but about responsibility and accountability for the lively relationalities of becoming, in which we are always and already entangled (Barad, 2007: 393). If accountability regimes—as material-discursive apparatuses—enact the accountability demands and the accountable subject specifically and differently, how then does the responsible professional respond legitimately within the multiplicity of different, often contradictory, regimes in which they are always and already positioned, simultaneously?

To explore this question, we want to engage with Barad’s notion of diffraction. Barad (2014) proposes the notion of diffraction as a non-binary conception of entangled difference. This diffraction is not the forcing together—as is suggested through the idea of ‘hybrid accountability’—of seemingly opposing responsibilities or accountability regimes, nor is it a flattening out or erasure of their difference. Rather, it is a relationality of ongoing differencing within the ongoing accounting practices itself—ongoing differencing that is formed through intra-activity, in the very enactment of accountability attuned by incommensurable responsibilities and accountability regimes, within their inseparability (or entanglement) as such. As Barad suggests: [E]ntanglements are not the intertwining of two (or more) states/entities/events, but a calling into question of the very nature of twoness, and ultimately of one-ness as well. Duality, unity, multiplicity, being are undone. ‘Between’ will never be the same. One is too few, two is too many . . . [E]ntanglements require/inspire a different sense of a-count-ability, a different arithmetic, a different calculus of response-ability. (2014: 178)

What Barad wants to highlight is that in the entanglement of these responsibilities (drawing on quantum theory), there is a ‘a different arithmetic, as different calculus of responsibility’, one that has at its root in essential indeterminacy—an indeterminacy that allows responsibility to become worked out in practice, intra-actively and in its very singularity (as opposed to commonality, as suggested by commensuration). This situated indeterminacy is what she calls the borderlands. The indeterminacy of the borderlands is an ongoing dynamic wherein that which has been excluded (be that responsibility to the proximal or distant other) always returns to interrupt because there is no absolute outside—for example, the needs of the invisible, distant other (Frey-Heger and Barrett, 2021) is always already also the ‘inside’. Barad suggests that confronting such indeterminacy is like acting or being in the ‘borderlands’, which ‘is a vague and undetermined place created by the emotional residue of an unnatural boundary. It is in a constant state of transition . . . Boundaries don’t hold; times, places, beings bleed through one another’ (Barad, 2014: 179). We would suggest that it is this experience of indeterminacy—which is at the heart of the so-called accountability problematics—that is the condition of possibility for the becoming of the responsible professional, as we hope to reveal in and through the empirical material below.

Research methods and approach to analysis

Case description and data collection

Our case study was conducted among Dutch veterinarians. This professional field has undergone several governance issues in the past decade, particularly with regard to the use of antibiotics (AB). In terms of governance and the enforcement of new regulations, the sector still heavily relies on self-regulation, even after it was much contested, resulting in additional legislation in 2014 (Pas et al., 2021). Under Dutch law, only veterinarians are allowed to practice veterinary medicine and to prescribe, sell, and administer veterinary drugs. They play an important role in monitoring animal health and well-being but also in safeguarding public health. In January 2020, in total, 8657 veterinarians were registered in the CIBG Veterinary Medicine register, of which 1,030 veterinarians are employed in the farm animal sector (cattle, pigs, goats, sheep, poultry), for whom antibiotics regulation is more (cattle, poultry) or less (goats, sheep) relevant. Approximately 80% of veterinarians in the Netherlands are women and approximately 30% of veterinarians in the Netherlands are self-employed, while the remaining 70% work in small- to medium-sized clinics, governmental organizations, universities, or businesses (e.g., pharmaceutical companies) (Bergevoet et al., 2020).

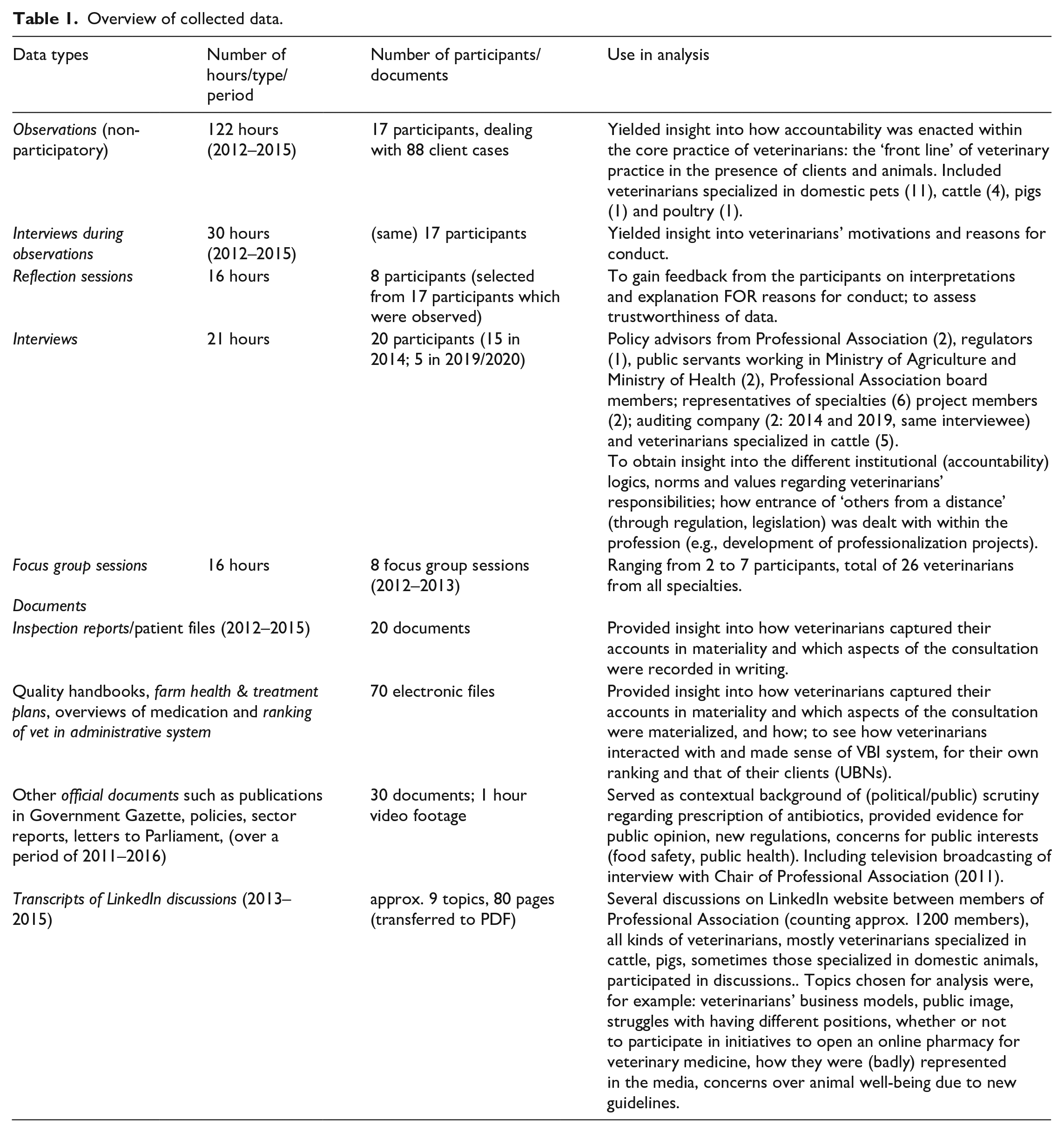

The data collection was initially based on grounded theory sensibilities (Charmaz, 2006), with the intention of understanding the professional accountability practices of veterinarians. The data were collected over two different time periods. Our first set of data was collected between 2012 and 2015 and covered observations and interviews with all types of veterinary specializations. To describe, document, and understand these practices in situ, our main and initial method of data collection was (video, when possible) observation of interactions between veterinarians and their clients (122 hours). Additionally, we collected documents such as advisory reports, inspection reports, quality handbooks, and farm health and animal treatment plans, whether in printed or digital form. Sometimes, we asked veterinarians follow-up questions to explain what they were saying and doing, and why. We also further interviewed policymakers, board members of the professional association, regulators, auditors, and veterinarians. The latter were interviewed both individually and in focus group sessions (for an overview, see Table 1). This enabled us to perform a ‘multimodal analysis’ in which the practices of giving accounts could be related with material configurations (Vesa and Vaara, 2014).

Overview of collected data.

In our data stemming from 2012 to 2015, we noticed that veterinarians and farmers in particular were still insecure and resistant regarding the additional administrative tasks that the increased accountability demands required. We wondered how this had evolved since the last field work and decided to return to the field. We then conducted another five interviews, retrieved additional documents, and observed the now-operating VBI system (2019–2020) to understand how the initial launch of new legislation and a networked, data-driven accountability system to support this new legislation back in 2014 was transforming veterinary and farming practice, especially with regard to accountability.

Approach to data analysis

Based on literature from a performative perspective grounded in a relational ontology (Barad, 2007; Introna, 2019), our initial round of analysis—based mostly on the material gathered between 2012 and 2015—was to understand how accounts for veterinary care were produced and made sense of in material-discursive practices. We progressively moved toward a poststructuralist analysis to go beyond an obvious relational view that relates actors, accounting practices, and responsibility as if these were all grounded in pre-existing subjects (vets) that needed to somehow be made responsible. Not because the professional’s responsibility was not important, as such, but because the intra-active processes through which accountability and the accountable subject become produced require an analysis far more sensitive to the phenomena involved: the other, including the animal, the other others, regulations, accountability regimes, technology, and so forth (Højgaard and Søndergaard, 2011). For example, based on the additional interviews and observations conducted and documents collected in 2019 and 2020, we noticed how, among others, technology (e.g., Cow Compass, MediCow, the VBI system) had intra-actively enacted a particular ‘care for accounting’ regime (and associated subject positionings), different than other accountability regimes we had so far encountered in our empirical material. We were particularly keen to take note of how accounts produced in veterinary practices were transformed intra-actively by practices, regulation, discourse, materiality, etcetera. As our analysis developed, we increasingly connected with the literature on performativity in which accountability is understood through the doings of situated practices as part of heterogeneous sociomaterial assemblages within which they are embedded (Introna, 2016). Doing accountability is thus not simply the execution of instructions as determined by the interface of an accountability/management system; their intra-relational actions (Barad, 2007) also enact the objects they are supposed to represent. This allowed us also to notice how different responsibilities were hard to clearly distinguish. We therefore started to code instances in which veterinarians (directly or indirectly) referred to responsibility toward the self, related others, the proximate other, and distant others, and which accountability regimes seemed to prevail in such instances, but also how other responsibilities and accountability regimes quickly disrupted such prevalence.

We applied Barad’s (2007) diffractive methodological approach in which the researcher obtains insights through attending and responding to the details and specificities of relations of difference and how they matter (Barad, 2007). For example, in an interview in which a vet expressed increased concern when having to register a third preferred medicine, the vet commented: ‘and then you use it, and I already feel my stomach crunch thinking “how am I going to register that in the system [without making mistakes], inducing an extra audit?” and then you have a discussion with your colleagues in the clinic who also ask “how could you do that, using that, registering that?” [fearing extra audits as well]’ (Veterinarian N, February 2020); this can be seen as the ‘care for accounting’ regime, yet this was then immediately ‘disrupted’ by the ‘accounting for care’ regime enacted by the same veterinarian who expressed concern for the animal’s well-being when not prescribing that particular medication: ‘but it [the third preferred medication] was my last resort. . . and so I thought, when it comes to trial, so be it . . . I know what I’m doing is right [for the animal]’.

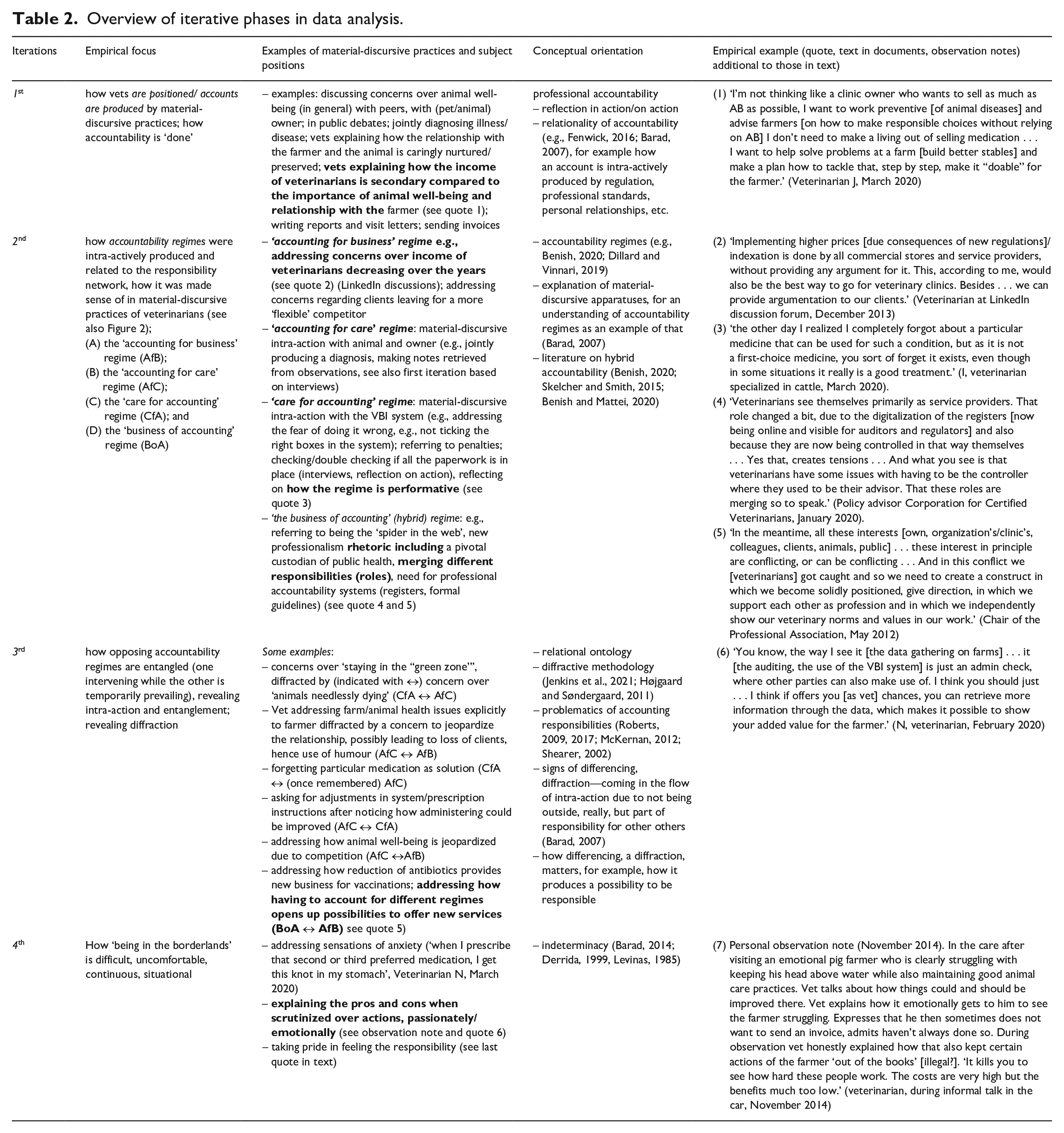

Importantly, our use of material-discursive vignettes—which, in our study, were parts of recorded observations of intra-actions—was helpful in preventing us from falling into the trap of taking our vignettes as a ‘means of producing authentic reflections of participants’ lived experiences’. Rather, for us, they revealed the processes of intra-action through which the ‘veterinarian’, ‘farmer’ (human), ‘cow’ (non-human), and ‘ultrasound device’ (material) are mutually co-constituted in the flow of daily practices (Jenkins et al., 2021: 984). Finally, we became aware of the affective expressions of veterinarians of ‘being in the borderlands’—that is, not referring to one particular regime but addressing the difficulty in deciding what to do, how to appropriately account, how it leaves an emotional residue. The main iterations in our data analysis are summarized in Table 2.

Overview of iterative phases in data analysis.

Analytical presentation of the empirical data

The ‘accounting for business’ regime: The positioning of the competitive professional

Around 2011, Dutch veterinarians were publicly criticised for prescribing too many antibiotics and having a ‘perverse business model’ (NRC newspaper, Dohmen, April 2011). In a report that the Ministry of Agriculture, Nature, and Food Quality assigned a consultancy firm to draw up regarding the position of veterinarians, the economic business position of the veterinarians was described as problematic in terms of public health goals to reduce the use of antibiotics: First, a veterinarian has a monopoly on prescribing antibiotics . . . Veterinarians’ income depend on the farmer (s)he advises and to whose animals (s)he prescribed and administers veterinary medicine . . . For farmers, the use of antibiotics is still the most cost efficient (on the short term) . . . Veterinarians are therefore (too) much attuned to the wishes of the farmers. This causes a [problematic] combination of public responsibility and a commercial business model. (Report by Berenschot, February 2010)

Before monitoring was increased through data-driven networked technology, a neoclassical economic ‘accounting for business’ regime was how most veterinarians were positioned and positioned themselves. Here, the professional exercised her own considered will to allocate her resources in such a way to maximise her profit in pursuit of financial returns commensurate with her investment (of time and resources) (Shearer, 2002). That is, to care for the business of her enterprise (and ultimately those related others such as her partners and family).

In our focus group sessions, some veterinarians admitted they feared some clinics would encounter financial trouble due to the increased regulations, for example, when they knew they had many farmers as clients who would threaten to take their business elsewhere (a competitor). Veterinarian A: ‘Listen . . . we [have to] admit that we perhaps made a bit too much money on our pharmacies’ (focus group session with four veterinarians specialized in household pets, March 2012). In the ‘accounting for business’ regime, professionals clearly struggled with the required commensuration—fitting the quality of their professional service, which now had to rely less on selling medication, in line with prevailing market prices for veterinary practices. Due to the (at that time upcoming) new regulation regarding antibiotics and preferred medication, we noticed a diffraction in how ‘vetting’ was to be done. Veterinarians spoke of increased additional administrative work but also of how the intra-active entanglement of increased regulation, announced networked, data-driven accountability systems, negative publicity, and so on produced new understandings of veterinary practice. It now not only includes the treatment of sick animals but also requires veterinarians to be trustworthy advisors regarding how to improve farming practices in such a way that they align with future regulations. It was often expressed that it was tricky to ‘sell’ advice instead of a physical service (in the form of treatment/the prescription of medication) to their customers, also because it could jeopardize their competitive position toward other (cheaper) veterinarians, as the excerpt of a conversation below shows: Veterinarian specialized in poultry: ‘in our line of work, we benchmark for use of AB for chicks already for years, we have a fixed price, which includes our fee for advice and service, clients know this, that is no longer a dispute’. Other (equine) veterinarian: ‘I think you are pretty unique in that [working with fixed prices]’ . . . ‘In my line of work, it is important that you show them [clients] what you offer them in exchange for your price, in terms of service. There are of course clients who say “but there is another veterinarian who is cheaper, who does not bill me for only dropping by [with advice]” so yes, there are vets who do that, so that means these vets then probably sell medication for higher prices because otherwise, I don’t know how else you could keep your business going.’ (Focus group, April 2012)

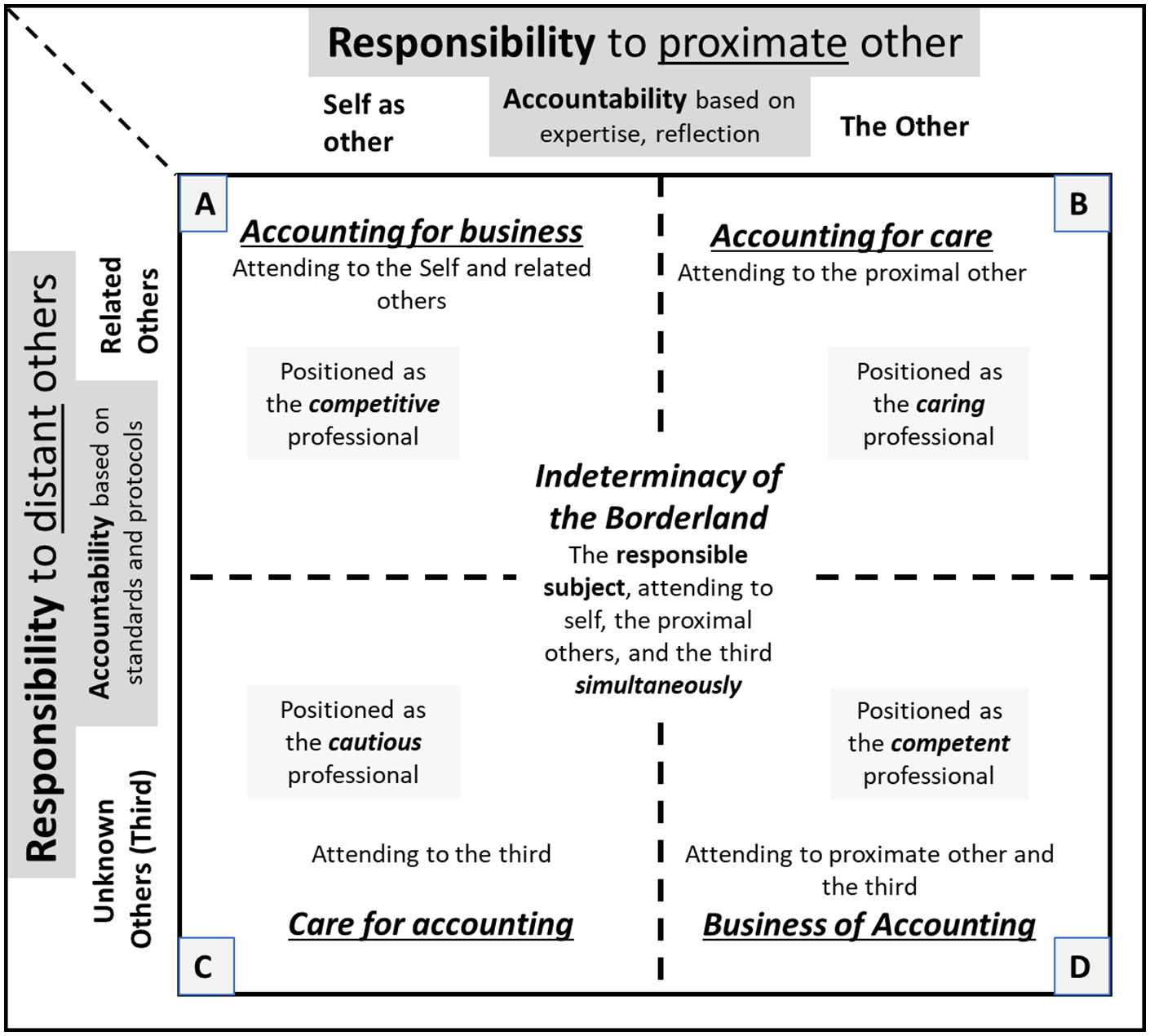

What is illustrated above is how the ‘accounting for business’ regime performatively positions the veterinarian as a competitive professional who is responsible for producing income for the clinic—her responsibility to the self and related others (colleagues, the profession, etc.) (see also Quadrant A in Figure 2).

The ‘accounting for care’ regime: The positioning of the caring professional

Veterinary practices inherently represent an intra-active material-discursive apparatus that enacts subject positions, specifically. In the vignette below, we want to show how the vet intra-actively becomes positioned as a caring professional, the cow as the ‘cared for’ animal, and the farmer as both the ‘caring’ and ‘cared for’. Being positioned as the caring professional mostly requires some form of balancing act (through commensuration or otherwise) between the well-being of the animal and the (financial) well-being of the farmer (the proximate others), as well as adhering to professional standards and protocols (related others, e.g., professional association): On Friday morning, Linsey visits Patrick to examine his cattle. The visit mainly consists of ‘pregnancy checks’. Every visit, Patrick selects particular cows for these checks because he wants to know whether these cows are (still) pregnant or whether they can be inseminated. This particular morning, Patrick has selected cows for pregnancy control as usual. Linsey puts on a latex shoulder-length glove on her right arm. With this arm she rectally examines the cow and brings the ultrasound scanner close above the uterus. On her left arm she wears a little screen on which she can see the sonographic image. Together with Patrick, Linsey walks through the stables and during the examination of the third cow Linsey refers to the two cows she checked some minutes before: ‘The manure of the last two cows I examined is really. . .’ [remains quiet but looks at Patrick’s face]. Patrick: ‘Yes, in my opinion, some cows do have very thin, poorly digested manure.’ Linsey nods with a ‘yes’ and to illustrate this she also takes a little manure from the cow to show to Patrick. She turns to Patrick and slowly lets the manure pass through her fingers and says: ‘Look.’ Patrick responds: ‘Yes, there are a number of cows which I think . . . their manure is way too thin.’ Meanwhile, Linsey is already walking toward the next cow and begins examining it: ‘This one is pregnant.’ Patrick responds and says: ‘Does it correspond to 44 days?’, which is confirmed by Linsey: ‘Yes.’ Patrick writes down the findings on a paper he is holding and together they walk to the next cow. (Observation, farm visit veterinarian Linsey, specialized in cows, October 2014)

From a relational perspective, we can see, in the vignette above, how the cow becomes positioned (or enacted) as a healthy and pregnant (or not) cow, where non-human actors (e.g., the ultrasound scanner) and human actors intra-act in the flow of the ongoing professional ‘accounting for care’ regime. The image of the ultrasound, the bodily sensation of running the manure through her fingers. . . these are all part of a joint intra-active choreography of the veterinarian, the farmer, the ultrasound scanner, and the cow, to account for the well-being of the animal and to produce an account (diagnosis). During the flow of this accountability choreography, Linsey notices an irregularity regarding the cows’ manure. This is revealed in her saying ‘the manure of the previous two cows I examined is really. . . [does not finish her sentence]’. Her pause functions to position the farmer as the responsible actor that must produce an account (to explain this deviation). Moreover, the lack of a descriptive account of the manure positions the farmer as the knowledgeable expert who is indeed able to complete the sentence with an appropriate account of the status (and possible explanation) for the deviation. Positioned as the accountable subject, Patrick seemingly feels compelled to account for the situation by stating: ‘yes, in my opinion, some cows do have very thin, poorly digested manure’. Patrick’s statement is confirmed by Linsey’s nodding and showing the manure, slowly passing it through her fingers.

In this vignette, we demonstrate how the material-discursive practices are performative—by positioning and enacting the vet and the farmer as accountable subjects, what we call caring professionals. Being positioned or enacted as such, the farmer and the vet act in ways that are meaningful and appropriate: Patrick responds, writes the relevant information down on a piece of paper, etc. Linsey makes claims, runs the manure through her fingers, proceeds to the next cow, and so forth. These care-oriented accountability practices are not directed at anyone specifically or exclusively; they are either to the proximate other (the farmer, the animal, the ‘future self’) or a possible related other such as a locum tenens or professional body who provides standards, guidelines, and criteria for ‘good veterinary practice’ (see also Quadrant B in Figure 2). Importantly, these responsibilities become enacted intra-actively within the flow of ongoing material-discursive practices called vetting and farming—they do not exist outside of it.

The ‘care for accounting’ regime: The positioning of the cautious professional

As of 2014, cattle farmers and veterinarians specialized in livestock have to be registered in a sector-specific register (database) in which the amount of antibiotics per herd sold has to be registered by the veterinarian and the amount of antibiotics per herd administered has to be registered by the farmer. These regulative control measurements spurred administrative practices which quickly became more and more automated through online databases. Much of these data-driven regulative control practices have been automated and centralized since 2014. For example, if the veterinarian sends out an invoice for a particular treatment of antibiotics, ‘this information is automatically uploaded in the database of the auditing company’ (Manager at Kiwa Verin, January 2020).

One of the benchmarks used in this intensified, data-driven regulative accounting regime is the Veterinary Benchmark Indicator (VBI). The VBI, established by the Authority for Veterinary Medicine (SDa) in 2013, is based on a framework for monitoring patterns of antibiotic sales by veterinarians and antibiotic use by farmers based on pre-defined associated benchmark values for different types of animals. These benchmark values are based on antibiotics sales/use by a particular vet/farmer relative to all other vets/farmers for a particular type of animal (pig, cattle, etc.). In other words, it is an indication of variance from the norm (by the vet or farmer) in that farming sector, which is a particular form of commensuration (Sauder and Espeland, 2009).

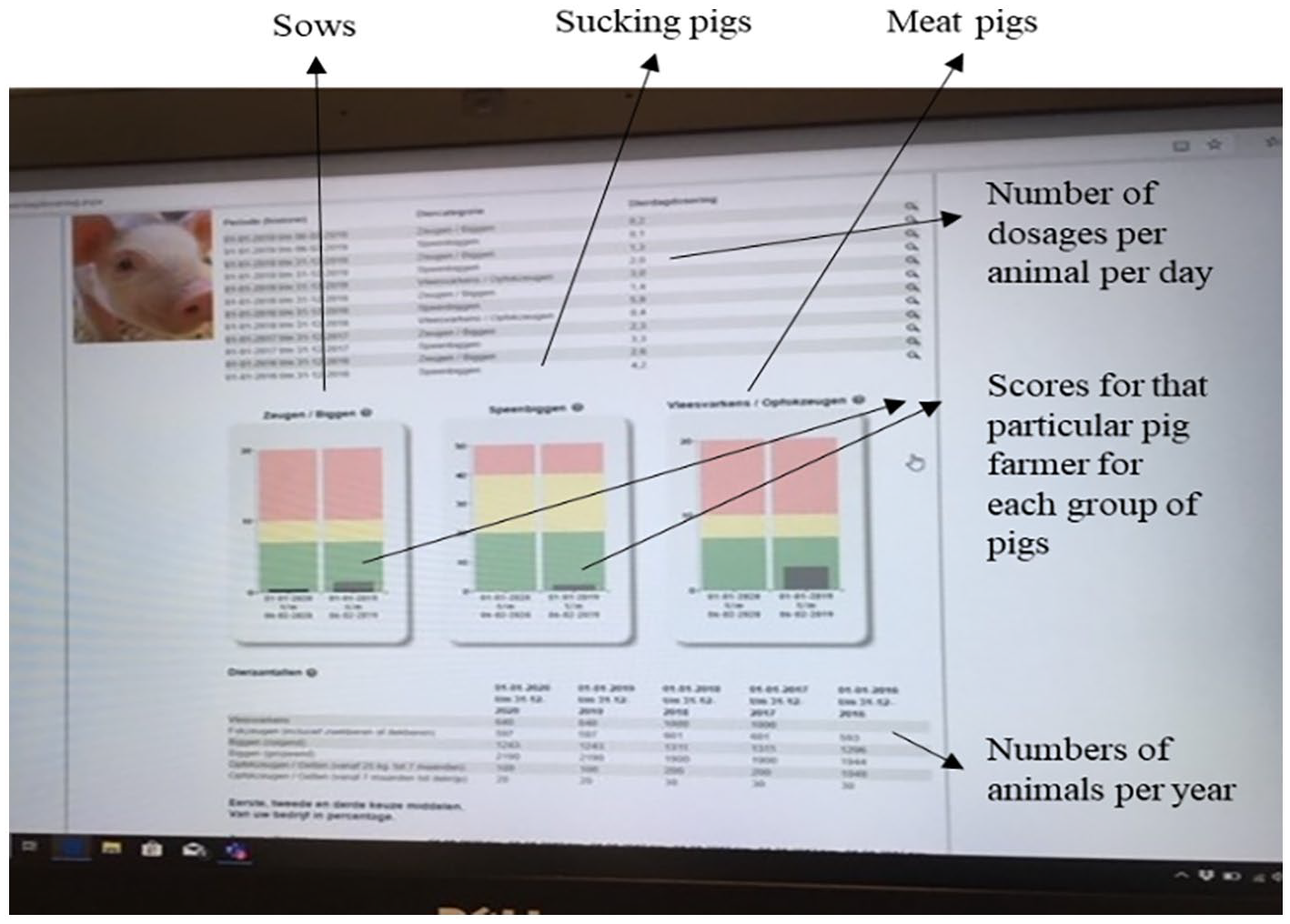

A VBI of 0.30 or higher indicates that the responsible veterinarian has one in three farms within the ‘action zone’, or the so-called ‘red zone’. This means that at one out of every three farms, they are prescribing more antibiotics than the norm (i.e., other vets responsible for similar farms). The SDa expert panel considers this to be ‘a substantial systematic deviation from target (normal) prescription patterns requiring immediate action’ (SDa Report, 2014: 8). A veterinarian whose farms have animal-defined daily dosages at the higher part of the action zone will be assigned a higher VBI than a veterinarian with the same number of farms in the action zone but whose farms have animal-defined daily dosages closer to the threshold value. Being in the ‘yellow zone’ (signalling zone, 0.10<VBI⩽0.30) is regarded to be seen as a warning, whereas being in the ‘green zone’ is good (‘target’ zone, under threshold value for VBI ⩽0.10) (SDa Report, 2014). When in the ‘red’ or ‘yellow’ zone, the veterinarian is obliged to take action toward the farmers under her responsibility—that is, to address and discuss the excessive use of antibiotics or medication identified and draw up agreements with the farmer to reduce the use of antibiotics and take preventive actions (Manager at Kiwa Verin, January 2020). The veterinarian, the auditor, and the farmers that contracted the particular veterinarian can see the VBI of the veterinarian. Figure 1 shows a screenshot of how a VBI is visualized for the farmer and veterinarian.

Screenshot of Veterinary Benchmark Indicator (VBI) system visualizing the score of a particular UBN (pig farm) for which this particular veterinarian is responsible.

The grey bars show that this particular farm is in the green zone. Finally, there are also regulatory restrictions on which antibiotics can be selected and prescribed for use when treating certain conditions. For any specific condition, veterinary medicine is classified into three main groups: first-, second-, and third-choice medications. There is always a legal requirement to justify the use of all antibiotic treatments.

The accounting regime, as a material-discursive apparatus, with its VBI indicator (and coloured zones) and regulatory prescription protocols, functions to enact a subject (vet and farmer) that ‘cares for accounting’ to distant others (e.g., regulators and public health officials, as representatives of the public). Through the intra-actions of the VBI, they are enacted as ‘good’ (green), ‘needing help’ (yellow), or ‘bad’ (red) farmers or vets. The ‘benchmark threshold is expected to stimulate veterinarians to mirror their prescription pattern to their colleagues and to trigger discussions between veterinarians. These discussions should lead to reflection and feedback on prescription patterns within veterinary practices and within the veterinary sector, but also between farmers and veterinarians’ (Bos et al., 2015: 2424). As this quote from an article on the VBI indicator shows, the subjects are expected to internalize their VBI scores and prescription patterns in order to become self-governing subjects (a process Foucault (1991) calls governmentality). The VBI thus produces what such a regime already assumes (that there are good and bad veterinarians/farmers).

When comparing interview transcripts between 2014 and 2020, we noticed how the vocabulary of the material-discursive apparatus of the accounting regime has entered the language of veterinarians. For example, some veterinarians introduced themselves in ways such as ‘Yes, I have 30 UBNs [registered farms’ unique codes in the system] . . . and I have ‘m from green farms to red farms, I have ‘m all’ (E., veterinarian, specialized in cattle, February 2020). The ‘green’ and ‘red’ clearly refer to how these farms score in terms of their VBIs in the system.

As the system became embedded in the practices of farmers and vets over the last six to seven years, we noticed how many veterinarians became increasingly attentive when doing their accounting for their veterinary work, to fill in the boxes ‘right’ (see also the example provided in the method section). According to our interviewees, working with the standardized regulatory systems in which prescribed medicine and treatment plans need to be selected, clicked, explained, and provided with additional digital documents (e.g., consultation reports) produces in them a certain awareness of how they became enacted or intra-acted through the regulatory data: What I do experience, especially when you prescribe a third-choice medicine, is the number of things we have to register and take down; it sometimes really creates a sort of Sword of Damocles hanging over your head as you’re thinking ‘o my, I’m absolute sure they [auditors] will pick this one out, am I sure I filled in the right animal tracking number? Did I click the “off-label” box?’ . . . and being so stressed about this, well, you’re practically turned into such a person [by the system]. (J, veterinarian specialized in cattle, March 2020).

When positioned in the ‘care for accounting’ regime, the professional can account to distant unknown others (represented by an auditor, the regulator, technologically mediated through material/accountability system) and to the self and related others, as making mistakes can result in sanctions (fines) for the clinic (see also Quadrant C in Figure 2). This accountability regime—with its intensified administrative work—made the veterinarians very cautious and even afraid. That is, it caused ‘commensuration stress’ in trying to fit qualities of the contextual doings and sayings into one metric in a particular way which, when it does not neatly fit, causes stress as it could invoke intensified audits and sanctions contained within the regulatory apparatus. Veterinarians are afraid not so much of making the wrong veterinary decisions regarding treatment or medication but more of making administrative mistakes that would affect themselves and their related others (colleagues at the clinic). This accountability regime means that caring for accounting to distant others becomes something that not only leads to the internalization of the regime and a self-disciplining subject but also enacts a particular flow of professional practice, in which a particular ‘account’ becomes the only logical, meaningful, accurate one. ‘I always make pictures of the animals’ ear tags I euthanize, so that I can accurately account for that in the management system by the end of the day, because, you know, you remember a lot, but mistakes happen’ (J, veterinarian specialized in cattle, March 2020).

Subject positions produced by entangled material-discursive practices and prevailing accountability regimes.

The ‘business of accounting’ regime: The competent professional

As of 2014, as part of the increased regulations, veterinarians and farmers have to jointly draw up the yearly farm health and animal treatment plans in order to remain registered as a certified veterinarian (or farmer). Our vignette below documents an intra-action between John, a recently qualified veterinarian (specializing in cattle), Peter, a cattle farmer (registered in a sector-specific quality register), the health and treatment plans, the VBI, and much more besides. John is required to develop (or review) the two plans once a year together with his client Peter (which they both signed off on). They drew up these plans for the first time in 2013; hence, this was a fairly new activity for them at the time: Today, John visits Peter, a cattle breeder and the owner of a modern farm. John has made a special appointment with Peter specifically to discuss, evaluate and draw up plans regarding farm conditions to improve animal health and animal treatment. They need to evaluate the past year and make agreements for the year(s) to come. In order to prepare for this appointment, John has already asked Peter to collect the necessary data (for example, the number of new-born calves that died within 24 hours). John himself also has to read through previous plan(s) in preparation for the appointment. At the farm, John and Peter sit down together at the coffee table and John opens his laptop to complete the specific details in the standard plan format. Peter is prepared and has printed out the necessary documents. Evaluating the plans usually takes between 90 and 120 minutes. During the meeting, John compares this year’s numbers of animals at the farm and animal diseases with those from the previous year. As Peter prepared himself well and as John frequently visits the farm, a lot of questions and answers are already familiar to both of them. Yet, John is obliged to answer all the questions required by the standard plan.

‘The death rate of stillborn calves or within the first 24 hours is seven? And navel inflammation zero?’

‘Yes (looks at his printed files)’

‘And diarrhoea ten?’

‘Yes, but that number is based on intuition. I don’t know the exact number’

‘This (point to the computer screen) is good to keep it on five percent. Navel inflammation. . . what is “too much”? We will note “4 percent” (typing). And diarrhoea “ten calves” is not an extremely high number’

‘It is more diarrhoea caused by food then something else’

‘And last year you agreed with Betty [former veterinarian and John’s colleague] to vaccinate the calves this year. . .’

‘Yes, but I thought we were already vaccinating the calves at that time. Or maybe we quitted, I don’t know. Anyway, it [the number of sick calves] is now decreasing [compared to last year]. It’s better than ever’

‘I don’t know, because I just recently became your veterinarian. I can look it up though, but it is not that important’

‘No indeed’

‘I think it is ok if you have ten [calves with diarrhoea] on a yearly basis’

The conversation between Peter and John reveals how they negotiate their now temporally shared responsibility to distant others (the public, the regulator) and to the proximate other (the cow, the farmer). What became particularly apparent in our analysis is how Peter and John mostly seem to negotiate two possibly conflicting accountability regimes in which they are already positioned: the ‘care for accounting’ regime and the ‘accounting for care’ regime. John asks a quantitative accounting type of question ‘And diarrhoea ten?’ The plan, like many regulatory mechanisms of distant others, is based on quantity. Peter replies ‘Yes, but that number is based on intuition. I don’t know the exact number’. He indicates that his number is based on intuition—that is, on a certain sense of being with the animals on a daily basis. As a person that cares for the animals daily, he ‘knows’ the level of diarrhoea instinctively (that is, qualitatively rather than quantitatively)—his account refers to his ‘accounting for care’ regime. Peter senses this re-entry of a different accountability regime and accounts for his professional care, stating: ‘. . . And diarrhoea “ten calves” is not an extremely high number’. In doing this, he also simultaneously translates what is being ‘said back’ by the regime of ‘care for accounting’, which reveals how the distant others are already implicated in the process. Similarly, although none of Peter’s calves have died from navel inflammation, they still have to specify a target in the animal health plan for the following year. ‘Navel inflammation . . . what is “too much”? We’ll say four percent (typing)’. In this way, Peter and John foreclose possible future interference by distant others, as they do not need to give a detailed explanation to distant others such as auditors regarding the number of calves dying from navel inflammation in the following year, as long as it falls in the range they just decided on (between zero and four percent). However, these remarks are quickly followed by statements such as ‘It is more diarrhoea caused by food then something else’, which again reflects how the ‘accounting for care’ regime diffractively causes Peter to refer back to his ‘accounting for care’ regime and responsibility to the animal. Peter, mindful of the need for ‘care for accounting’ (he needs to upload a filled-in farm health and animal treatment plan at a certain point), pushes the conversation forwards to the next element in the plan—and so forth.

What we see in the conversation between John and Peter is that although the accountability regimes are entangled from within—they continuously invoke and disrupt each other and enact different positionings—they are treated as somewhat separate from their felt responsibilities, as regimes which need to commensurate. Both John and Peter are aware that what they are doing is somewhat unrealistic, yet that for ‘competent accountability’s sake’ requires an act of commensuration. For example, for diarrhoea, the number is ‘ten’ (‘care for accounting’ (CfA in Table 2)), but it is ‘based on intuition’ (‘accounting for care’ (AfC in Table 2)), ‘which is not a high number. . . “I think it is ok if you have ten [calves with diarrhoea] on a yearly basis. . .”’ (commensurating two regimes in one sentence while filling in a number in the system). While intra-acting, they are both positioned as competent professionals—both ‘caring’ (attuned by AfC regime) and ‘cautious’ (attuned by CfA regime)—in that moment being seen by the proximal and distant other(s) as ‘responsible’. In a sense, John is positioned, by a collaborating farmer, by a clinic that works with certified veterinarians only, by a well-organized back office, by recently taking an additional course to become more aware of the public responsibility veterinarians have. John, according to the ‘business of accounting’ regime, is a competent veterinarian.

Together, sharing responsibility to the proximate other (each other, the animals) and the distant other, they attempt a reconciliation between opposing regimes, locally and situated, related to their responsibilities to the distant (animals, the farmer, the auditor, the regulator, the public—basically everyone but the self and related others) and proximal other (the farmer, for whom it has to remain ‘doable’) (see also Quadrant D in Figure 2). However, its reconciliation, the commensuration, is only superficial. Underneath, different responsibilities remain irreconcilable but seem to be pushed to the background. Ultimately, the well-being of the animal and the farmer cannot be weighed as more or less important than that of public health (in the long run)—they are ethically equally important and entangled: both sick animals and/or bankrupt farmers jeopardize public health, although something could be said for the current scale of cattle farming practices which puts unequal strains on our climate. Additionally, there is the backgrounded responsibility to the self, and related others (colleagues) when positioned in the ‘business of accounting’ regime—although considered ‘competent’ by the proximate and distant other, the responsibility to oneself, to one’s business, is also what is still at stake. As the vignette shows, John had to take a certain ‘leap of faith’ in making decisions based on educated guesses regarding numbers of sick animals per year, which, if wrong, could put his responsibility to the vet clinic (and himself) in jeopardy.

Coping with entangled irreconcilable accountability regimes: The borderlands

While trying to find a solution between opposing regimes, what remains is a disruptive indeterminate space between these two regimes. This disruptiveness—where multiple responsibilities enacted through different accountability regimes produced boundaries and differences in what matters (or not), intra-actively—was noticed in all the accountability regimes presented above. More examples are provided in Table 2. It shows that it is not a matter of temporal or perpetual commensuration of possibly conflicting accountability regimes but rather of ongoing differencing, that is, allowing for the transformation of one regime (‘accounting for care’) through the other (‘care for accounting’), creating possibilities to become positioned differently, and as such, opening up different possibilities for acting responsibly. However, what always remains is what also matters, for which one is also responsible yet for which one cannot account, simultaneously. It is this indeterminate space that we call the ‘borderlands’ (Barad, 2014). A space that can be regarded as the emotional residue produced by being positioned and positioning oneself to account according to a particular regime, yet where one’s responsibility for the other others is not and cannot be laid aside.

The borderlands are a tense, intersubjective space, which, during interviews, veterinarians only gradually started to reveal. For example, all of our interviewees brought up that the relationships between veterinarians and their clients are often long term and considered them to be very personal. Enacting their professional position (as veterinarians that care for the well-being of the animals) meant that they often had to discuss delicate issues such as poor animal health or farm conditions, extensive use of antibiotics, and so forth. Traditionally, this is done by, for example, ‘using humour’, which is seen as an important skill in keeping rapport with the farmer while also indicating a serious need for change in farming practices (E, certified veterinarian specialized in cattle, March 2020). Some veterinarians indicated that the increasing prevalence of the ‘care for accounting’ regime provided them with opportunities to enact their ‘accounting for care’ regime through the former—that is, by invoking the distant others as the ones demanding accountability from both the veterinarian and the farmer. They indicated that they can now blame ‘the system’ for expecting reductions in the use of antibiotics to be addressed, even though they had ‘wanted to do so for a long time but [I] did not know how to do it without jeopardizing the relationship with the client’ (N, veterinarian, March 2020). This disruption of one regime through the invoking of the other (the distant others in this case) might be a useful example of how this tension of being entangled—not two and not one either—and the uncertainty that it creates represents exactly the sort of indeterminacy that creates the conditions of possibility for the professional to become responsible.

It is, however, also possible for one accounting regime to unintendedly start to dominate and transform the other. Veterinarians as well as farmers are increasingly attuned to what the numbers tell them, how certain actions produce certain outputs in productivity and in their VBI scores. These entangled regimes, where a ‘care for accounting’ regime starts to dominate, can also transform the attunement of other subjects involved in the accountability practices. For example, farmers might see particular actions as more appropriate and legitimate to do than the veterinarian, as this veterinarian explains: You sometimes have a farmer that carries on a bit too far, who says ‘yeah, but we’re not going to treat this cow anymore because then I get into trouble with my animal-day-dosage ratio’ [jeopardizing the ‘green zone’ position]. And then I have to step in and explain that we cannot let animals die which we can easily cure. (J, veterinarian, March 2020)

What we see here is what happens when one regime is prioritized over the other. The farmer suggests that it is better to let the animal die than risk their VBI scores. This is absolutely not what the vet, more attuned to the ‘accounting for care’ regime, would want to happen, but that is what happens when the two accountability regimes and related responsibilities are treated as if they are commensurable, in which the farmer believes that he somehow has to choose one at the expense of the other. All the interviewed veterinarians talked about the difficult place of feeling forced (positioned) to choose between conflicting accountability regimes, always at the expense of some other. They experience a lot of tension (what we might call indeterminacy) that is very much affectively felt when faced on a daily basis.

Some veterinarians seemed to make sense of these performative changes by adjusting how they see themselves more as: guardians of public health. We’re the bio-industry’s lubricant, we’re like a spider in a large web and we’re in the centre. Not because we are vets. But because we have particular tasks and when performing them, we are expected to continuously perform a balancing act. We hear this all the time, but you really feel it the moment when you’re standing there [at a farm] and you have to make a decision in that moment. (E, veterinarian specialized in cattle, March 2020).

As this quote illustrates, there is a delicate difference between becoming positioned through material-discursive practices as the competent, accountable ‘hybrid’ professional ‘doing accountability’ (in the ‘business of accounting’ for conduct); and continuously (re)positioning yourself to remain or become the responsible professional. Whereas the first backgrounds and denies irreconcilability by emphasizing accountability through some form of commensuration, the latter acknowledges the irreconcilability by her awareness of the weight of his decision, for all others (Levinas, 1985)—as indicated in the last sentence: ‘but you really feel it the moment when you’re standing there [at a farm] and you have to make a decision in that moment’. It reveals her positioning in the borderlands. That is, feeling the sheer weight of the incommensurable responsibilities to all others, the impossible ‘balancing act’ in which she has to ultimately decide, responsibly. We will elaborate on this further in our discussion below.

Discussion: Becoming a responsible professional in the borderlands

Entangled responsibilities: Professional responsibility in the borderlands

Our empirical material particularly revealed how a fundamental indeterminacy disrupted and haunted all attempts at reconciling or commensurating accountability regimes, and in doing so, revealed the emotional residue, the weight on the shoulders of the account holder (the borderlands in the centre).

We argued in the introduction and theoretical section that there are two different approaches to accountability—the structural and the personal/relational (e.g., Sinclair, 1995)—and how the aim of many accountability scholars is to explain how professionals cope with the expectations emanating from a multiplicity of ‘accountability regimes’ (the structural) within which they find themselves related to different proximal and distant human and non-human others (the personal) (e.g., Frey-Heger and Barrett, 2021; Kurunmäki and Miller, 2011). We concluded that although recent theoretical suggestions have been made by critical accountability scholars for how accountability (regimes) and responsibility can and should be reunited (e.g., Dillard and Vinnari, 2019; Fenwick, 2016; Solbrekke and Englund, 2011; Vosselman, 2016), two interrelated concerns remained to be further investigated.

First, the material-discursive intra-active performativity of multiple accountability regimes needs to be considered more seriously. As we argued, our main concern is the way in which conflicting accountability regimes are problematized within the structural approach, especially in terms of the belief that they can be hybridized through some form of commensuration. We argued, drawing on the work of Barad and our data, that the accountable subject is not constituted ‘outside’ these irreconcilable regimes—which would enable it to somehow reconcile them—but rather becomes performatively enacted in and through the very material-discursive apparatuses constitutive of the regimes as such. Consequently, the image of hybrid accountability is deeply problematic. Indeed, a limited number of critical accountability scholars noticed the risk of just ‘adding a bit more’ criteria to existing accountability systems. They argue that any addition should ensure that the needs of all stakeholders are incorporated and safeguarded (Dillard and Vinnari, 2019), that participatory accountability is created (Komporozos-Athanasiou et al., 2018), or that a space for responsibility is created through appropriate power symmetries (Vosselman, 2016). These suggestions are indeed commendable. However, as we saw in our results, when the force to respond to a single other (the regulator) becomes dominant, the equal demands of all others (such as the animals) can easily be pushed to the background. Additionally, being forced to account regardless of whether it produces highly speculative, unrealistic accounts (‘business of accounting’ regime) might jeopardize the responsibility for the self (‘can I still live with myself if this is what I as a professional do? How do I bill the time spend on it to a client not willing to do this either?’). Hence, we suggest that any attempt to ‘fix’ a regime or accountability process should recognize that any transformation of indeterminacy into determinacy might indeed underplay, hide, or even eliminate that which is the fundamental condition of possibility for the responsible professional to become enacted. More specifically, our study shows how a subject can and should remain able to draw from its responsibility to others to counter any dominating accountability regime of a power holder (e.g., regulator).

Our second, related concern regarded the subject positioning of the professional enacted in and through accountability regimes. We argued that such a subject is often taken as a pre-existing autonomous subject that must be made responsible/accountable through such regimes. In contrast, we argued and showed that accountability regimes, with their material-discursive technologies of representation, function to produce what such practices assume—the subject that can be made accountable (Butler, 2005). We showed that such a professional, positioned in multiple and conflicting subject positions, can easily internalize the dominant accountability regimes and be seen to be accountable but might actually be irresponsible. On the other hand, by internalizing all these regimes, as entangled, the subject becomes acutely aware of their equal responsibility to all, which is indeterminable. Hence, as we argue, there is a need for an appreciation for ‘the borderlands’ (Barad, 2014).