Abstract

We investigate how age diversity on corporate boards affects their monitoring performance. Despite the critical importance of the monitoring function of the board, previous studies focus mainly on the advisory role of age-diversified boards. Our emphasis is on banks where the opacity in their complex operations poses a challenge for external stakeholders to assess performance and thus they heavily rely on the board for monitoring managerial activities. We examine how age diversity affects one of the primary monitoring roles of corporate boards – a responsibility over the provision of high-quality financial reports. Using a large panel data of banks in the United States (N = 7005) our findings suggest that age-diversified boards are associated with less earnings management, indicative of higher-quality reporting. Our results still hold for different indicators of the monitoring performance of the board in other areas, such as loan risk. Further analysis reveals that, as age diversity increases, the strength of the board’s monitoring effectiveness also increases. Overall, our findings suggest that age-diversified boards are more effective at monitoring managerial decision making.

Keywords

Introduction

Corporate governance codes and regulations around the globe emphasise the importance of diversity for board effectiveness. For instance, the Securities and Exchange Commission (SEC) in the United States (US) requires listed companies to disclose their diversity strategies (Securities and Exchange Commission, 2009), while Australia requires listed companies to disclose a diversity policy (Australian Securities Exchange, 2010). Banking regulators also emphasise the importance of diversity. The Basel Committee on Banking Supervision (2015) explicitly specifies that the complex nature of banking operations calls for banks’ boards to include a diverse set of directors. While much attention from academics and regulators has been directed towards gender and ethnic diversity, other forms of diversity have often been overlooked. For instance, although age diversity could significantly impact firms’ boards, we are not aware of any regulation or governance code emphasising its importance. This is despite the fact that nearly 90% of directors of firms in the Standard and Poor’s 500 (S&P 500) consider age diversity important, while only 6% of S&P 500 firms have directors younger than 50 years old (PricewaterhouseCoopers, 2019). Given this, we examine how age diversity affects one of the primary roles of corporate boards – a responsibility over the provision of accurate and timely financial reports to shareholders.

Our focus in this study is on the banking industry for a number of reasons. First, the opacity and complexity of bank operations makes it challenging for external stakeholders to monitor bank activities (Acharya and Ryan, 2016). Hence, bank boards have an even more significant monitoring role than boards of non-financial firms. Second, governments pay specific attention to the banking industry owing to its substantial impact on the economy. Banks facilitate borrowing by acting as intermediaries between borrowers and lenders and, as such, policymakers have been particularly interested in ensuring the safety and soundness of banking systems. It is no wonder that board characteristics – the first line of defence against industry instability – are also receiving increasing attention from researchers (Adams and Mehran, 2012; Laeven and Levine, 2009).

Age diversity, as a salient board characteristic, and its impact on banks’ reporting quality can be of particular importance. US banks are facing extended scrutiny on issues related to diversity and inclusion, as suggested by a recent investigation on the matter by the US Congress (Committee on Financial Services, 2020). The banking sector is also facing challenges related to diversity in other settings, for example in Turkey (Taser-Erdogan, 2022). We consider the quality of reporting as one important indicator of the overall monitoring performance of banks’ boards. Since banking operations are complex and opaque (Bratten et al., 2019; Cetorelli et al., 2014), financial reporting plays a vital role in communicating information to external stakeholders (Bushman and Williams, 2012). Following banking literature, we use loan loss provision (LLP) as our measure of earnings management, indicative of the quality of reporting (Bushman and Williams, 2012; Fan et al., 2019; Kanagaretnam et al., 2005, 2014).

Prior literature seems to overlook the effect of age diversity on board effectiveness in monitoring, while it directs its attention towards the board’s advisory role, yielding mixed results (Ali et al., 2014; Hagendorff and Keasey, 2012; Kim and Lim, 2010; Talavera et al., 2018). Our study fills this research gap by exploring the relationship between boards’ age diversity and the board’s monitoring role, providing evidence that age-diversified boards monitor bank managers more effectively. Board diversity studies widely use two theories to explain why and how diversity improves board effectiveness, namely social identity theory and information processing theory. Social identity theory suggests that differences in beliefs and values reflected in age differences increase the tendency for conflicts to appear among board members. We propose that this tendency makes the board more independent and thus improves its monitoring capabilities. Additionally, information processing theory suggests that age-diversified boards mix different experience and knowledge, which improves the quality of discussions on the board. Notably, we provide evidence that this latter theory might be less relevant to the age diversity-based monitoring performance of the board and could only help indirectly explain board monitoring effectiveness.

Our results are consistent with the notion that board age diversity improves board performance: we find that age diversity improves the board’s monitoring effectiveness, which is reflected by reduced earnings management in banks. Specifically, we find that the effect of age diversity on improving board monitoring activities is only prevalent at moderate and high levels of age diversity. Using quantile regression analysis, we find no association between age diversity and earnings management in banks with a low level of age diversity. In contrast, we find a negative relationship between age diversity and earnings management in banks with moderate and high levels of age diversity. Interestingly, we also find that the relationship becomes stronger in banks with the most diverse boards. These results suggest that well-diversified boards can secure the full benefits of age diversity. We find this result intuitive because, in a well-diversified board, no single group can control the board’s discussion, allowing out-of-group thinking and enhancing decision-making quality. Finally, we also show that age diversity reduces loan Charge-off, non-performing loans and idiosyncratic risk.

Overall, our study generates new insights and provides some first empirical evidence on the association between age diversity and the board’s monitoring performance. The findings are robust to a variety of controls and specifications, including fixed effects and propensity score matching. Overall, our evidence supports the recent calls for more diverse boards and emphasises the importance of age diversity.

The remainder of this article is organised as follows. Next, we review the related literature and develop our hypothesis. The third section presents our methodology, while section four reports the results. We discuss our findings in section five. Limitations and directions for future research are available in section six. Finally, we conclude in section seven.

Background and hypothesis development

Age diversity and board effectiveness: Theory and empirical evidence

The impact of diversity on boards’ operations and decision making can be approached from a number of theoretical lenses. Information processing theory suggests that diverse boards would increase overall board effectiveness through having a wider spectrum of diverse expertise and perspectives. Directors from different demographic backgrounds transmit different experience and knowledge to the board (Hillman et al., 2000). Consistent with this argument, McLeod et al. (1996) find that diverse groups are more likely to produce higher-quality ideas than homogenous groups, while both Miller and Del Carmen Triana (2009) and Bernile et al. (2018) find that firms with diverse boards are more innovative.

In the context of age diversity, older and younger people tend to differ significantly in terms of their interests, work biographies, education, use of technology and membership of social networks (Aggarwal et al., 2008; Hatfield, 2002; MacCrimmon and Wehrung, 1990). As a result, an age-diverse team may blend a variety of resources and add to the overall richness of knowledge and information processed by the organisation (Harrison and Klein, 2007). In addition, research shows that age-diverse groups tend to be more creative and more adaptive to change as they are less prone to the effects of groupthink (Janis, 1972), because they tend to generate more diverse and meaningful discussions across the different perspectives represented in the group. Other empirical research shows that age diversity can contribute to performance in cases of complex and non-routine information processing and decision-making tasks. Wegge et al. (2008) and Wegge et al. (2012) report that in cases of highly complex tasks, age diversity is positively related to group performance. These findings are also supported by Backes-Gellner and Veen (2013), who show that age diversity has a positive effect on performance when the tasks are creative and non-routine. This literature, overall, indicates that more age-diverse boards are likely to address challenges from executives on the board more effectively, as the former would have more knowledge and experience at their disposal, contributing to better decisions, but also to better monitoring and scrutiny of proposals from the executives.

It has to be noted that other theories propose that increasing levels of diversity can have negative outcomes on performance-related factors in social groups, such as higher levels of conflict and lower levels of social cohesion. In particular, it is suggested that highly diverse groups may be prone to breaking down to subgroups along social identification faultlines, thus making decision making costlier in terms of time and effort. In the case of age-diversified groups, breaking down into smaller groups may happen along the lines of different ages, as people prefer to interact with others who have similar values, attitudes, experiences and interests to them. In particular, psychological theories tend to show that an age differential is likely to be a strong promoter of separation within groups. Byrne’s (1971) similarity-attraction theory proposes that actors tend to affiliate selectively with others who are similar to themselves and age is regarded as one of the factors according to which actors select their associations. Social identity theory (Tajfel, 1981; Turner et al., 1987) also supports this effect, proposing that individuals regard age as an important component of their social identity and so tend to form and maintain social groups following age differences.

More pertinent to our setting, empirical research about the impact of age diversity on the performance of top-management teams provides some mixed evidence. Kilduff et al. (2000) find a positive association between age diversity of top management and performance. Similarly, Kim and Lim (2010) examine the effect of age diversity of the independent directors on Korean firms’ valuation. They find that age diversity is associated with an increase in firm valuation. Li et al. (2011) find that age diversity is associated with improved performance in Chinese and western firms. Nevertheless, they do not find similar evidence for East Asian firms. Ali et al. (2014) suggest that the effect of age diversity on firm performance is non-linear. They find that age diversity has an inverted U-shaped relationship with firms’ return on assets.

Bunderson and Sutcliffe (2002) report no significant association between age diversity and performance, while Ellwart et al. (2013) show that age diversity has a negative effect on knowledge exchange. Hagendorff and Keasey (2012) find that banks with age-diverse boards tend to have a decreased stock market performance after mergers and acquisitions investments. They argue that shareholders prefer experience to diversity in contexts of complex decision making such as acquisitions. In the same vein, Talavera et al. (2018) examine the association between age diversity of the board and bank performance in China. They find that age diversity of the board has a negative effect on bank return on assets and return on equity, and no effect on bank risk. However, and inconsistent with Talavera et al.’s (2018) findings, Zhou et al. (2019) find that the larger the age gap between the chairman and the chief executive officer (CEO) the lower is the bank risk taking. They attribute their findings to the cognitive conflict between the CEO and the chairman, inducing the chairman to be more independent.

We draw a general observation from our review of the extant empirical research. The majority of previous studies focus on the effect of age diversity on firm performance or, in other words, on the efficiency of the advisory role played by the board. Indeed, none of the previous studies we reviewed investigates specifically the effect of age diversity on the monitoring function of the board, as it is reflected in the quality of financial reporting. Crucially, given that the monitoring and scrutiny functions of boards are centred around non-routine socio-cognitive tasks, where age-diverse boards are shown to perform better, and the centrality of board independence for effective monitoring, we believe that age-diverse boards are likely to perform better in their monitoring role. Additionally, low degrees of social cohesion and conflict arising from board diversity will not necessarily have only negative effects on the monitoring function of the board. Although such conflicts may contribute to slower and less efficient decision making (Berger et al., 2014; Chrobot-Mason et al., 2009; Forbes and Milliken, 1999), diverse boards are likely to be more independent as they are less likely to establish strong in-group social ties. Taken together, our reading of the relevant literature leads us to suggest that diverse boards are more likely to encourage useful challenging of managerial decisions, leading, overall, to improved decision making and monitoring activities (Bernile et al., 2018; Fan et al., 2019).

Hypothesis development

Bank operations are complex and LLP reporting is based on private information about the loan portfolio of the bank (Acharya and Ryan, 2016; Beatty and Liao, 2014). This explains why LLP is one of the widely used methods of managing earnings in banks (Beatty and Liao, 2014; Cohen et al., 2014; Fan et al., 2019). LLP is highly discretionary because it depends on the managers’ estimation of future credit losses. While managers have access to private information related to loan quality, it is challenging for external stakeholders to access such information (Bushman and Williams, 2012). Thus, managers can take advantage of this information asymmetry and misreport LLP (Richardson, 2000). However, effective boards should preclude managers from this, by challenging managers over their judgements and hence deter them from fraudulent activities.

As discussed earlier, we expect age diversity to promote a lower degree of social cohesion on the board (Berger et al., 2014; Chatman and Flynn, 2001; Talavera et al., 2018), but also to encourage more independence (Adams and Ferreira, 2007; Fan et al., 2019) and a wider knowledge among its members; all these characteristics are associated with more effective monitoring. Thus, we expect age-diversified boards to be more effective in scrutinising managers’ judgements on LLP reporting, leading to improved quality of reporting.

Main hypothesis: Age-diversified boards are more effective monitors.

Sub-hypothesis: Age-diversified boards are associated with a higher financial reporting quality in banks.

Methodology

Sample and data

We use COMPUSTAT to collect LLP-related data, along with other accounting data. We obtain directors’ ages, along with other board characteristics, using Institutional Shareholder Services (ISS). The data available on ISS starts in 1996. Therefore, our sample consists of US banks for the period between 1996 and 2018. We also use ExecuComp to collect data on CEO compensation. We merge the databases using six-digit CUSIP. Then, we omit observations with missing LLP, age diversity, bank or board characteristics data. Our final sample consists of 7005 bank-year observations. The total number of banks included in our study is 232. Owing to some missing CEO characteristics data, our sample size drops to 5915 observations (188 banks) when we include CEO control variables. Therefore, owing to the substantial loss of observations, we exclude the CEO controls from our base model but include them in an extended analysis.

Dependent variable: DLLP

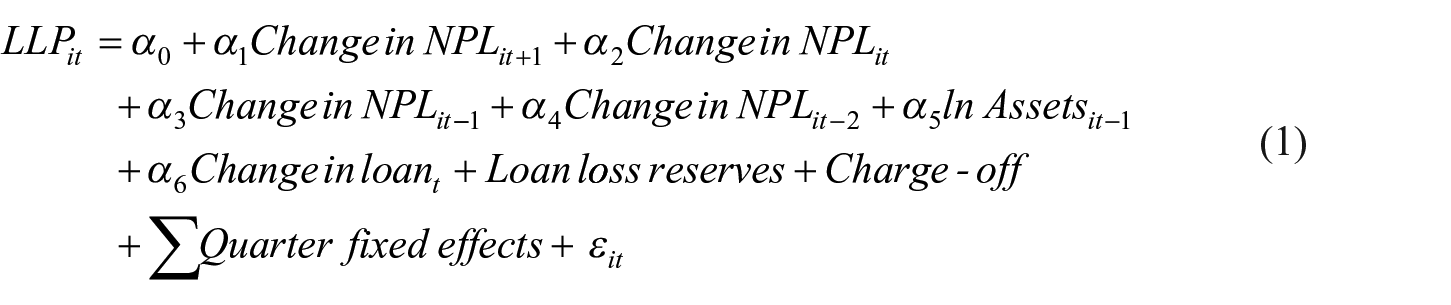

Banking studies normally use discretionary loan loss provisions (DLLP) as a measure of discretionary earnings management (Beatty and Liao, 2014; Fan et al., 2019; Kanagaretnam et al., 2010, 2014; Tran et al., 2020). To distinguish between the discretionary and non-discretionary component of LLP, we implement Beatty and Liao’s (2014) model. In the first stage, this model regresses LLP on variables that are known to affect loan losses, while the second stage uses the first-stage estimates to calculate the residuals from the model estimates. The calculated residuals are regarded as the discretionary component of the reported LLP. Greater (lesser) residuals, in absolute terms, indicate a greater (lesser) degree of earnings management. The following model is used:

where LLP is the loan loss provision of bank i at quarter t. Change in NPL is the change in non-performing loans over the quarter. NPLs are loans for which the borrower fails to make interest payments for a defined period of time, normally 90 days. The model uses Change in NPL in the periods t+1, t, t–1 and t–2 to control for the fact that banks use future, current and past information to estimate LLP (Bushman and Williams, 2012). ln Assets is the natural log of the book value of assets. Larger banks are scrutinised more by regulators as they are ‘too big to fail’. Change in loan is the change in total loans over the quarter. This variable captures the increase/decrease in the lending activities of the bank as LLP is expected to increase with an increase in loans (Kim and Kross, 1998). The model also uses Loan loss reserves to control for managers’ adjustment to LLP over-reporting in previous periods (Beaver and Engel, 1996). Finally, Charge-off is used as it is an important loan metric that managers use to estimate LLP (Liu and Ryan, 2006). All variable definitions are provided in Appendix A. We run model 1 on the entire set of bank accounting data available on COMPUSTAT. Then, we generate our DLLP variable as the absolute value of the residuals estimated from model 1.

Main explanatory variable: Age diversity

The objective of this study is to investigate the effect of age diversity on monitoring financial reporting decisions in banks. Thus, our key explanatory variable measures the age diversity of the nonexecutive directors of the board. We are particularly interested in the age diversity of nonexecutive directors because they are the ones carrying the monitoring role of the board.

An age-diversified board should have higher discrepancy in the age of its nonexecutive members. We follow Hagendorff and Keasey (2012) and Talavera et al. (2018) and measure age diversity as follows: the standard deviation of nonexecutives’ ages, divided by their mean age. Then, we assign a value of one for observations with an age diversity coefficient above the sample median and zero otherwise.

Research design

Base model

A fixed effects estimator is used to measure the effect of an age-diverse board on earnings management. An advantage of the fixed effects estimator is that it controls for unobserved time-invariant heterogeneity at the bank level, which allows us to attenuate the effect of endogeneity related to omitted variable bias. The fixed effects estimator captures the net effect of age diversity on DLLP, after removing the effect of those time-invariant characteristics. To control for heteroskedasticity, we use Huber-White standard errors. We also cluster the standard errors at the bank level to control for potential estimation bias owing to within-bank correlation. Our baseline model is as follows:

where DLLPt is the absolute value of the residuals estimated using model 1 in period t, and Age diversity of NEDt is a variable that takes the value one if the age diversity of the nonexecutives is above the sample median and zero otherwise, as described in the previous section. We include the following bank-level controls. First, we use pre-managed earnings (EBDLLPt) to control for the motivation to carry out earnings management. Previous studies show that managers are motivated to manage earnings when their pre-managed earnings are low (Bushman and Williams, 2012). We also use Tier one capital %t-1, to control for banks using LLP to manage their regulatory capital, a behaviour that is specific to the banking industry (Ahmed et al., 1999). We control for bank size using the lagged natural log of total assets (ln Assetst-1). Large banks are likely to have highly sophisticated internal controls (Doyle et al., 2007), and are subject to scrutiny from regulators (Michelson et al., 1995), lessening the managers’ ability to manipulate earnings. Diversity in operations is also an important attribute that might affect banks’ tendency to manage earnings. Diversification increases information asymmetry between insiders and outsiders, and hence increases the monitoring costs of the firm. Consistent with this argument, Tran et al. (2019) find that diversified banks are more likely to use LLP to manage earnings. We consider a bank to be diversified when it is less reliant on its lending activities. Therefore, we use the ratio of loans over total assets to control for bank diversification (Loan concentrationt). Also, relative to mature firms, growing firms have a higher propensity to manage earnings (Tran et al., 2019). We follow previous studies and control for the effect of bank growth using Assets growth (Fan et al., 2019; Tran et al., 2020).

As to our board-level controls, we use Board sizet to control for board effectiveness. The direction of the relationship between board size and board effectiveness is unclear. Some studies suggest that large boards are more likely to have diversified experience and skills, which enable them to better monitor bank activities (Adams and Mehran, 2012; Coles et al., 2008). Audit committee size is also used as a control variable as it can reduce earnings management (Yang and Krishnan, 2005). We also control for board independence using Nonexecutive directors %t, CEO/chairman dualityt and Gender diversity %t. Nonexecutive directors are not involved in day-to-day operations; hence, they are viewed as independent from executives and in a bank their main duty is to monitor the bank executives (Jensen, 1993). We also control for CEO/chairman duality as powerful CEOs may compromise board independence (Tuggle et al., 2010). The chairman sets the board agenda and facilitates the debate in the board. Therefore, executive chairmen can sway the board discussion in their favour. Chairmen also have considerable influence over directors’ re-appointments (Carcello et al., 2011). Thus, directors will be discouraged from challenging their views. Finally, recent studies show that gender diversity increases board independence. Women directors are not considered part of the ‘old boys’ network’ and do not have the tendency to form social ties with executives, so their presence ultimately enhances board effectiveness (Gul et al., 2013; Gull et al., 2018). Fan et al. (2019) show that bank boards with more women are associated with less earnings management, as measured by DLLP.

To alleviate the effects of omitted variable bias, we use bank fixed effects. Bank fixed effects control for unobservable characteristics related to time-invariant factors. We also use a vector of time dummies to control for time-variant characteristics that affect LLP reporting. Finally,

Extended model

In an extended model, we control for CEO characteristics that might affect reporting quality. CEOs have a significant effect on financial reporting decisions (Dechow and Shakespeare, 2009; Hribar and Yang, 2016; Kim et al., 2011). We specifically control for CEO compensation, CEO age and CEO gender. Compensation plans might persuade CEOs to alter reported earnings, especially when their pay is more performance-sensitive (Laux and Laux, 2009). We use the natural log of CEO compensation (ln CEO compensation) to account for exponentiality in the relationship between compensation and earnings management. In addition, we control for CEO age and CEO gender because previous studies suggest that these factors could affect firms’ financial reporting decisions (Ho et al., 2015; Huang et al., 2012).

Results

Univariate analysis

Dependent variable

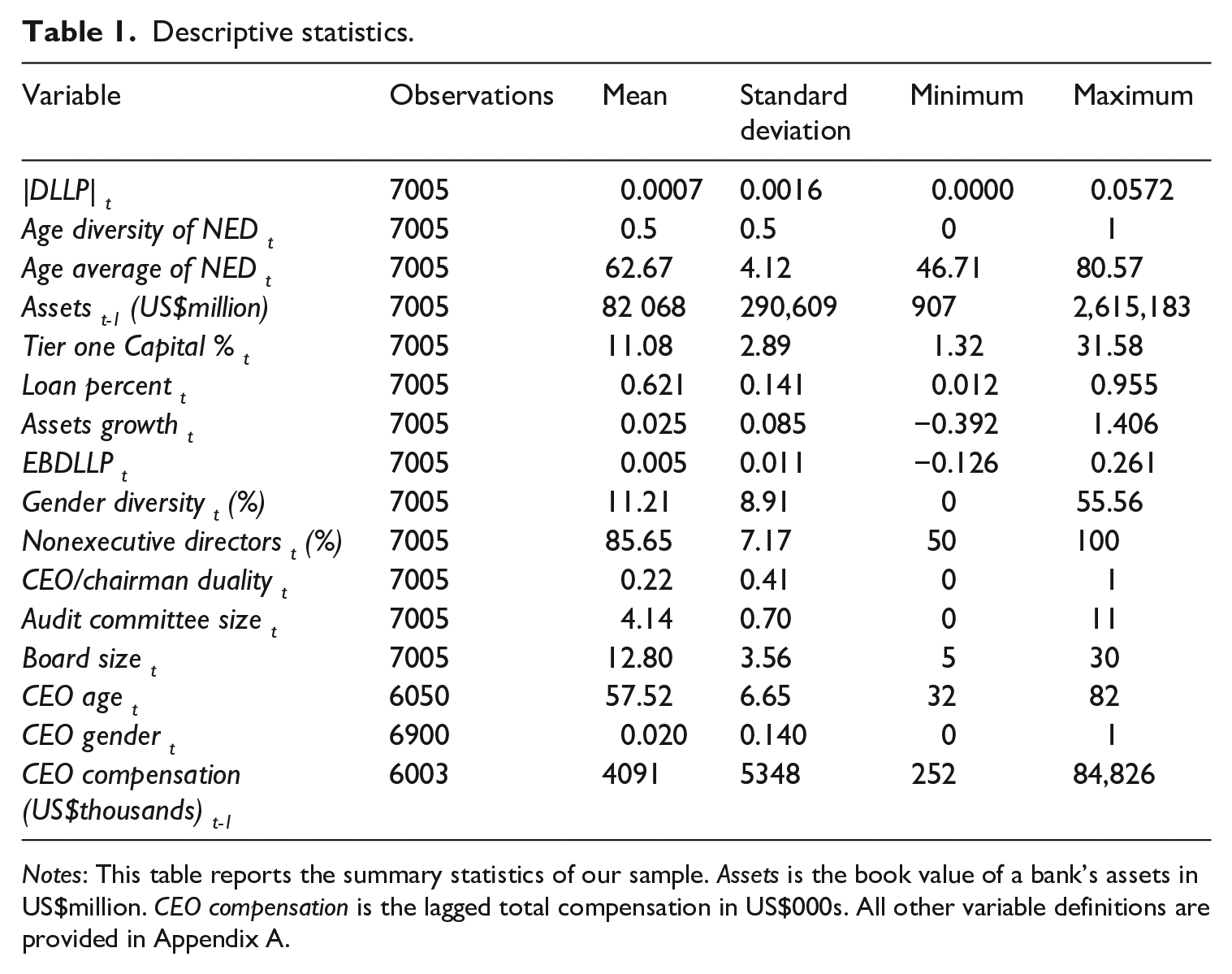

Table 1 reports our descriptive statistics. With regards to our earnings management variable, the average |DLLP| in our sample is 0.0007, whereas the maximum is 0.0572. Note that DLLP represents the discretionary component of LLP deflated by lagged total loans. To make more sense of the actual size of our |DLLP|, we multiply the |DLLP| of each bank by its corresponding lagged total loans. In actual numbers, the average |DLLP| is US$27m and the maximum is US$6b. We believe that these numbers are material in size in comparison to earnings and LLP. Earnings before extraordinary items in our sample average at nearly US$196m, while the average LLP is approximately US$94m. Tables 1A and 2A in the online appendix report the correlation matrix and differences in means, respectively.

Descriptive statistics.

Notes: This table reports the summary statistics of our sample. Assets is the book value of a bank’s assets in US$million. CEO compensation is the lagged total compensation in US$000s. All other variable definitions are provided in Appendix A.

Age diversity

Based on the descriptive statistics reported in Table 1, we find that bank boards are older and less diversified than boards in non-financial industries. Our descriptive statistics show that the average age of bank directors is 62 years. This is three years higher than in non-financial firms as reported by Bernile et al. (2018), who look at non-financial firms listed in the S&P1500 for the period between 1996 and 2014. 1 Table 1 also shows that the standard deviation of the directors’ age is 4.12, indicating a lack of age diversity in general.

With regards to our proxy for age diversity, our mean (median) is 0.109 (0.115), while the mean (median) in S&P1500 non-financial firms is 0.14 (0.14), as reported by Bernile et al. (2018). This demonstrates that, as with gender diversity, banks are lagging behind other industries in terms of the age diversity of their boards. Finally, we construct our Age diversity of NED variable as a dummy variable that equals one if the age diversity of the bank’s nonexecutive directors is greater than or equal to the median (0.115), and zero otherwise.

Multivariate analysis

Base model

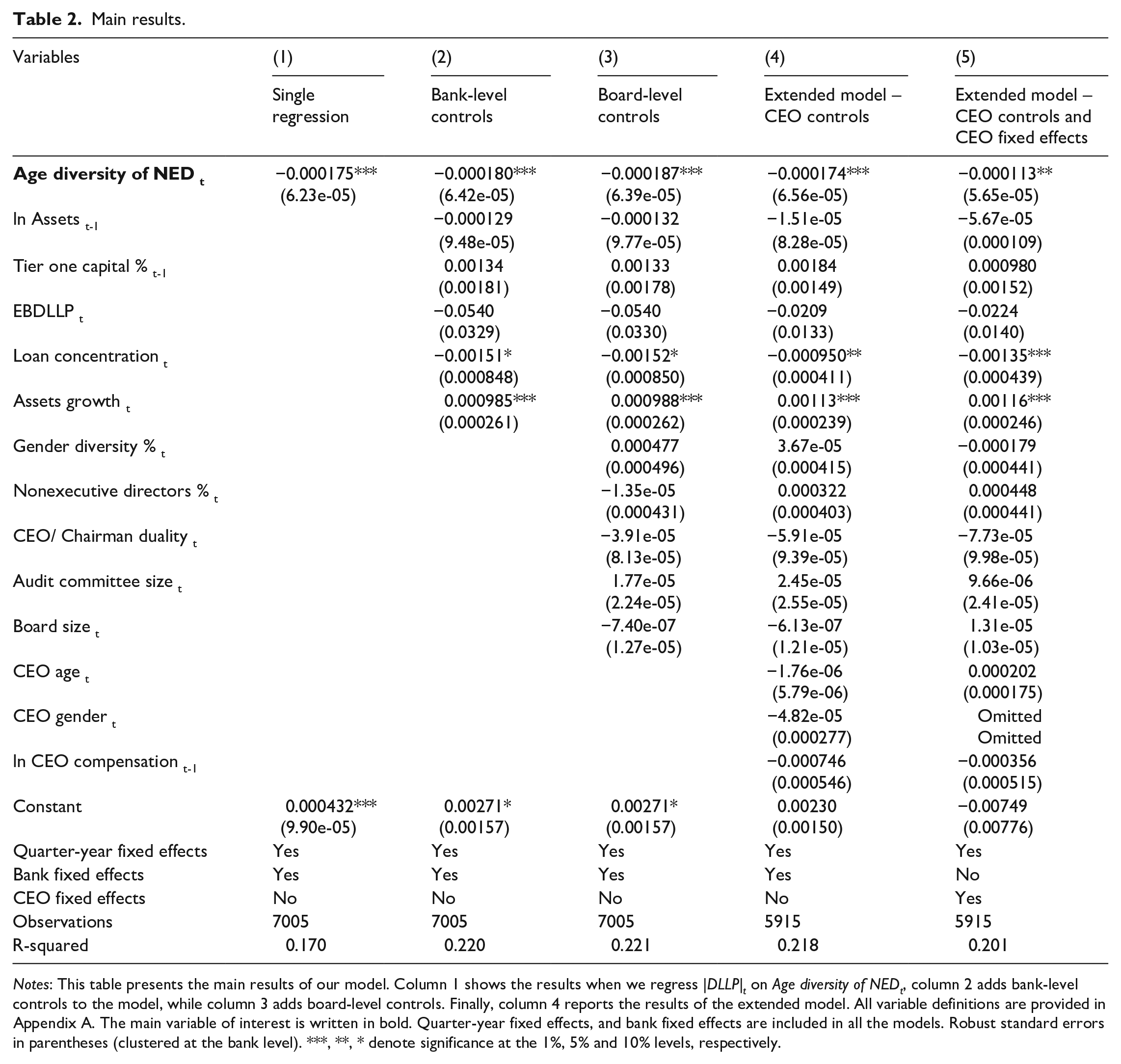

Table 2 reports our main results on the relationship between age diversity and earnings management in banks. We begin by regressing our earnings management measure against age diversity. The results show a negative association between Age diversity of NED and |DLLP|, significant at the 5% level (column 1). Then, we run the regression including bank-level controls. The results of this regression, which are reported in column 2, show that the coefficient of age diversity is still positive and significant. In untabulated analysis, we replace our Loan concentration and Assets growth variables with other proxies for bank diversification and firm growth, and our results still hold. 2 Column 3 reports the results after the inclusion of board-level controls. The results confirm our earlier findings. We use bank fixed effects and quarter-year fixed effects in all models’ specifications. Our baseline model shows that the coefficient on Age diversity of NED is negative and significant at the 1% level. The estimated magnitude of the coefficient is −0.000187. Finally, we find a significant positive association between Loan concentration and earnings management, consistent with the notion that diversified banks tend to manage earnings (Tran et al., 2019). In addition, and consistent with Park and Shin (2004), we find a positive association between bank growth and earnings management.

Main results.

Notes: This table presents the main results of our model. Column 1 shows the results when we regress |DLLP|t on Age diversity of NEDt, column 2 adds bank-level controls to the model, while column 3 adds board-level controls. Finally, column 4 reports the results of the extended model. All variable definitions are provided in Appendix A. The main variable of interest is written in bold. Quarter-year fixed effects, and bank fixed effects are included in all the models. Robust standard errors in parentheses (clustered at the bank level). ***, **, * denote significance at the 1%, 5% and 10% levels, respectively.

Extended model: CEO characteristics

In this section, we extend our base-level analysis by including CEO controls in the regression model. Owing to data availability, our sample size drops to 5915 observations and 188 banks. The advantage of this specification is that it accounts for CEO characteristics that may also affect DLLP reporting. Previous literature demonstrates that CEOs have a substantial effect on earnings management. Our results might therefore be biased if banks with higher age diversity among their directors have CEOs that encourage the management of earnings. To alleviate this concern, we control for CEO characteristics that might affect earnings management practices. The results of this extended model are reported in column 4, and show that our age diversity variable is still negative and significant at the 1% level, consistent with our previous findings. The coefficient of Age diversity of NED becomes −0.000174. Finally, we use CEO fixed effects to control for CEO time-invariant characteristics and CEO change. The results are reported in column 5. Our results hold under all these specifications.

Robustness checks

Tenure diversity

It is plausible that tenure diversity may be highly correlated with age diversity since older directors are more likely to have longer tenures than younger directors. The absence of a tenure diversity variable in our models might lead the residual term to be correlated with age diversity, which would invalidate the model assumptions. Thus, we control for tenure diversity in our model to exclude this possibility.

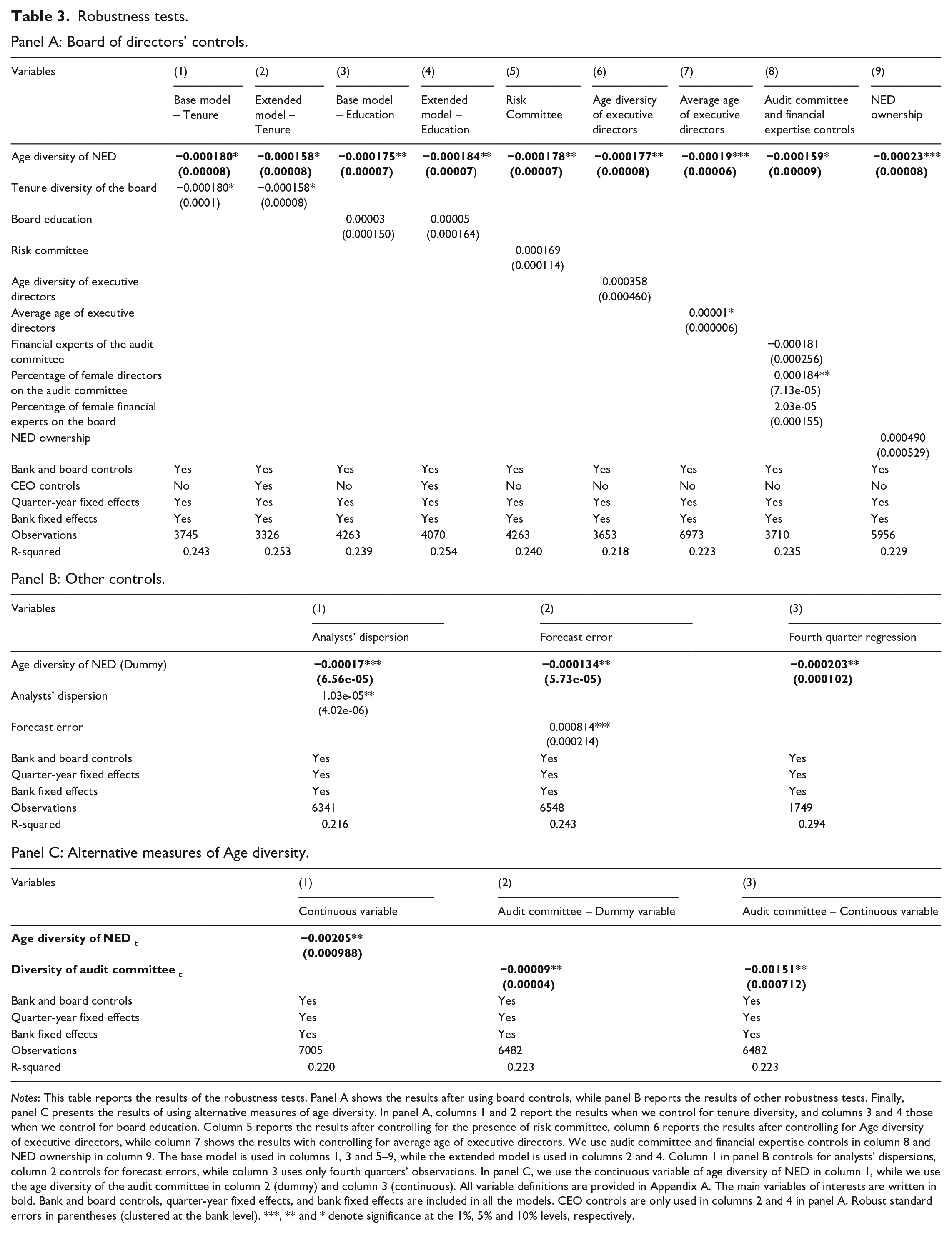

We first collect information on director tenure from BoardEx. Our data collection starts from 2003 because the availability of board data before this year in BoardEx is limited. We follow Hagendorff and Keasey (2012) and calculate tenure diversity as the standard deviation of directors’ tenures on the board. Then, we manually trace every bank in BoardEx to the same bank in the ISS database using the bank name. Columns 1 and 2 of Table 3 report the results of this analysis. Our observations drop to 3745 (3326) when we use the base model (extended model). However, our age diversity variable is still negative and significant, confirming the robustness of our findings.

Robustness tests.

Panel A: Board of directors’ controls.

Notes: This table reports the results of the robustness tests. Panel A shows the results after using board controls, while panel B reports the results of other robustness tests. Finally, panel C presents the results of using alternative measures of age diversity. In panel A, columns 1 and 2 report the results when we control for tenure diversity, and columns 3 and 4 those when we control for board education. Column 5 reports the results after controlling for the presence of risk committee, column 6 reports the results after controlling for Age diversity of executive directors, while column 7 shows the results with controlling for average age of executive directors. We use audit committee and financial expertise controls in column 8 and NED ownership in column 9. The base model is used in columns 1, 3 and 5–9, while the extended model is used in columns 2 and 4. Column 1 in panel B controls for analysts’ dispersions, column 2 controls for forecast errors, while column 3 uses only fourth quarters’ observations. In panel C, we use the continuous variable of age diversity of NED in column 1, while we use the age diversity of the audit committee in column 2 (dummy) and column 3 (continuous). All variable definitions are provided in Appendix A. The main variables of interests are written in bold. Bank and board controls, quarter-year fixed effects, and bank fixed effects are included in all the models. CEO controls are only used in columns 2 and 4 in panel A. Robust standard errors in parentheses (clustered at the bank level). ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

Board education

Younger directors are arguably better educated than older directors (Hatfield, 2002), and this might add to their monitoring ability. Since age-diversified boards are more likely to have younger directors, board education may drive our results. If age-diversified boards are highly educated, then the argument that age diversity leads to less earnings management can be disputed. Thus, we extend our model and control for board education.

Following Fan et al. (2019), we assign a value of one to directors with bachelor degrees, two to directors with master’s degrees, three for directors with doctoral degrees and zero otherwise. Then, we calculate the average of the directors’ education level for a given board. We collect data on directors’ education using BoardEx. We follow the same procedure as was used in the previous section to match the BoardEx data to our dataset. Columns 3 and 4 of Table 3 report the results of this analysis. Because our data start from 2003, our observations drop to 4263 (4070) in the base (extended) model analysis. Our results corroborate the results of the main analysis. The coefficient of Age diversityt is still negative and significant at the 5% level in both columns. The coefficients are also similar in magnitude to those reported in the main analysis.

Other sensitivity checks

We perform a battery of sensitivity checks to confirm the robustness of our findings. The results are reported in Table 3. In panel A of Table 3, we control for the presence of a separate risk committee (or other committees related to loan management) in the board, and executive directors’ average age and executive age diversity. We also control for nonexecutive directors’ stock ownership, percentage of financial experts in the audit committee and percentage of female financial experts on the board. 3 Panel B of Table 3 reports the results after controlling for analysts’ forecast error and the dispersion of analysts’ forecasts as proxies for the quality of the information environment of banks (Armstrong et al., 2010). In addition, we restrict our observations to the fourth quarter only to control for the fact that there are more incentives for managers to manage earnings in the fourth quarter (Liu et al., 1997). Overall, our main results remain unaffected.

In addition, as there is no consensus on which LLP-related model better estimates DLLP, we repeat our analysis using other LLP models, as suggested by Beatty and Liao (2014). Table 3A in the online appendix reports the results of this analysis. Our results remain robust under all LLP models.

Alternative measures of age diversity

The main analysis uses a dummy variable instead of a continuous variable to measure the effect of age diversity on earnings management in banks. A continuous variable would allow us to instead measure the effect of an incremental increase in age diversity on earnings management. Thus, we repeat our analysis using a continuous variable to measure the age diversity of nonexecutive directors. This variable is the standard deviation of director ages divided by their mean age. Panel C of Table 3 reports the findings of this analysis. Column 1 shows that the coefficient of age diversity (continuous) is −0.002 and significant at the 5% level. In economic terms, a one-standard-deviation increase in age diversity leads to a decrease of US$0.72m in DLLP in real terms. 4 This is a high decrease in earnings management given that the median DLLP in our sample is US$3.2m and the median earnings are US$32m.

We also use different measures of age diversity to confirm the robustness of our findings. We use the age diversity of the whole board (i.e. not only of the nonexecutive board members) and the number of decades represented in each board. Our inferences remain the same. The results of these models are reported in Table 4A in the online appendix.

We also investigate the association between age diversity of the audit committee and earnings management in banks. Given that the audit committee is the one primarily responsible for reporting quality, we expect the diversity of the audit committee to affect financial reporting quality in banks. We construct our audit committee age diversity variable in a similar way that we construct our main variable, whereby we divide the standard deviation of the directors in the audit committee over their age average. Then, we assign a value of one if the value of age diversity is above the sample median and zero otherwise.

Panel C of Table 3 reports the results of this analysis. Our observations drop to 6482 owing to missing data on audit committees. The results show that banks with age-diversified audit committees have lower |DLLP| than banks with less age-diversified audit committees. Column 1 reports the results using the dummy variable measure of age diversity, while column 2 reports the continuous variable results. Both results are consistent with our main findings and significant at the 5% level. We repeat this analysis using the extended model, and our conclusion remains unchanged (Table 5A, columns 1 and 2 – online appendix).

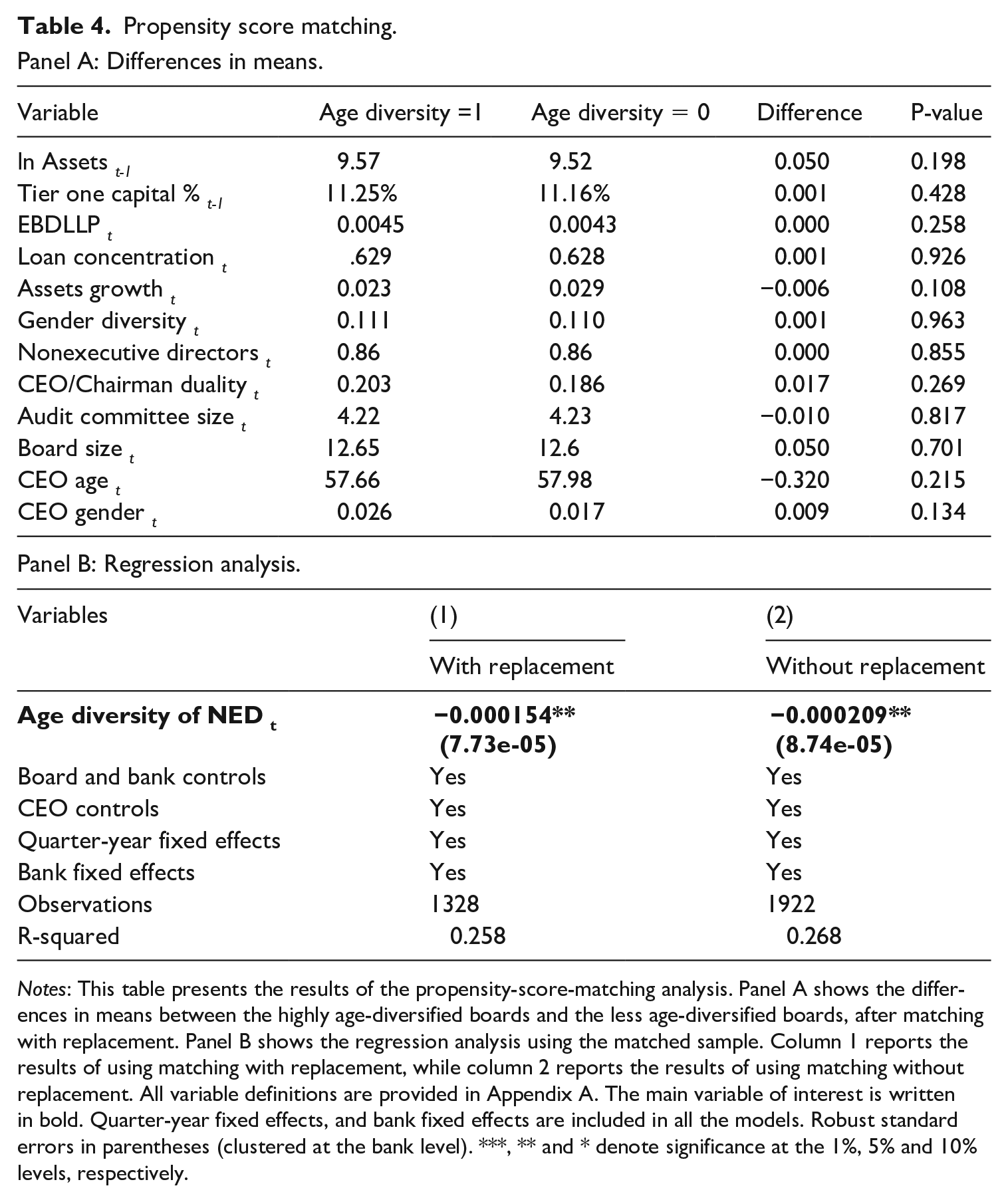

Propensity score matching

Directors are possibly not randomly selected into banks. If banks that aim to improve their financial reporting quality simultaneously increase the diversity in their boards, it will be difficult to conclude that age diversity affects earnings quality. Table 2A (online appendix) confirms this, showing that there are significant differences between banks with high age diversity boards and banks with low age diversity. We thus utilise propensity score matching to attenuate this effect. Propensity score matching consists of two stages of analysis. The first stage uses observable bank characteristics to predict the likelihood that a bank will choose to have an age-diversified board (i.e. treated sample). The second stage matches each treated bank with another bank that has a very similar likelihood of being treated but is not treated (i.e. control sample).

In our context, we split our sample into banks with high-age diversity boards (treated) and banks with low-age diversity boards (control). Next, we calculate the probability of a bank being in the treated group (i.e. banks with high age diversity) using the control variables from the extended model as the determinants. Then, we match each treated observation with a control observation that has the closest propensity score. To improve the matching quality, we allow each observation to appear more than once (i.e. matching with replacement) and impose a caliper of 0.005%. Our final dataset comprises 1328 observations. Table 4, Panel A reports the difference between the means of our control variables after matching. The results show that propensity score matching succeeds in eliminating the differences between the treated and control groups. After matching, age diversity is the only characteristic by which the two groups can be distinguished.

Propensity score matching.

Panel A: Differences in means.

Notes: This table presents the results of the propensity-score-matching analysis. Panel A shows the differences in means between the highly age-diversified boards and the less age-diversified boards, after matching with replacement. Panel B shows the regression analysis using the matched sample. Column 1 reports the results of using matching with replacement, while column 2 reports the results of using matching without replacement. All variable definitions are provided in Appendix A. The main variable of interest is written in bold. Quarter-year fixed effects, and bank fixed effects are included in all the models. Robust standard errors in parentheses (clustered at the bank level). ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

Finally, we run our extended regression to find the association between age diversity and earnings management. The results are reported in Panel B of Table 4, confirming our previous findings and showing that the age diversity of NED is associated with a reduction in earnings management, as measured by DLLP. The coefficient of Age diversity of NED is negative and significant at the 5% level. We perform our matching again but without replacement and obtain similar results. We also perform the propensity score matching again on our base model but leave those results (which remain the same) untabulated for brevity reasons.

Additional analyses

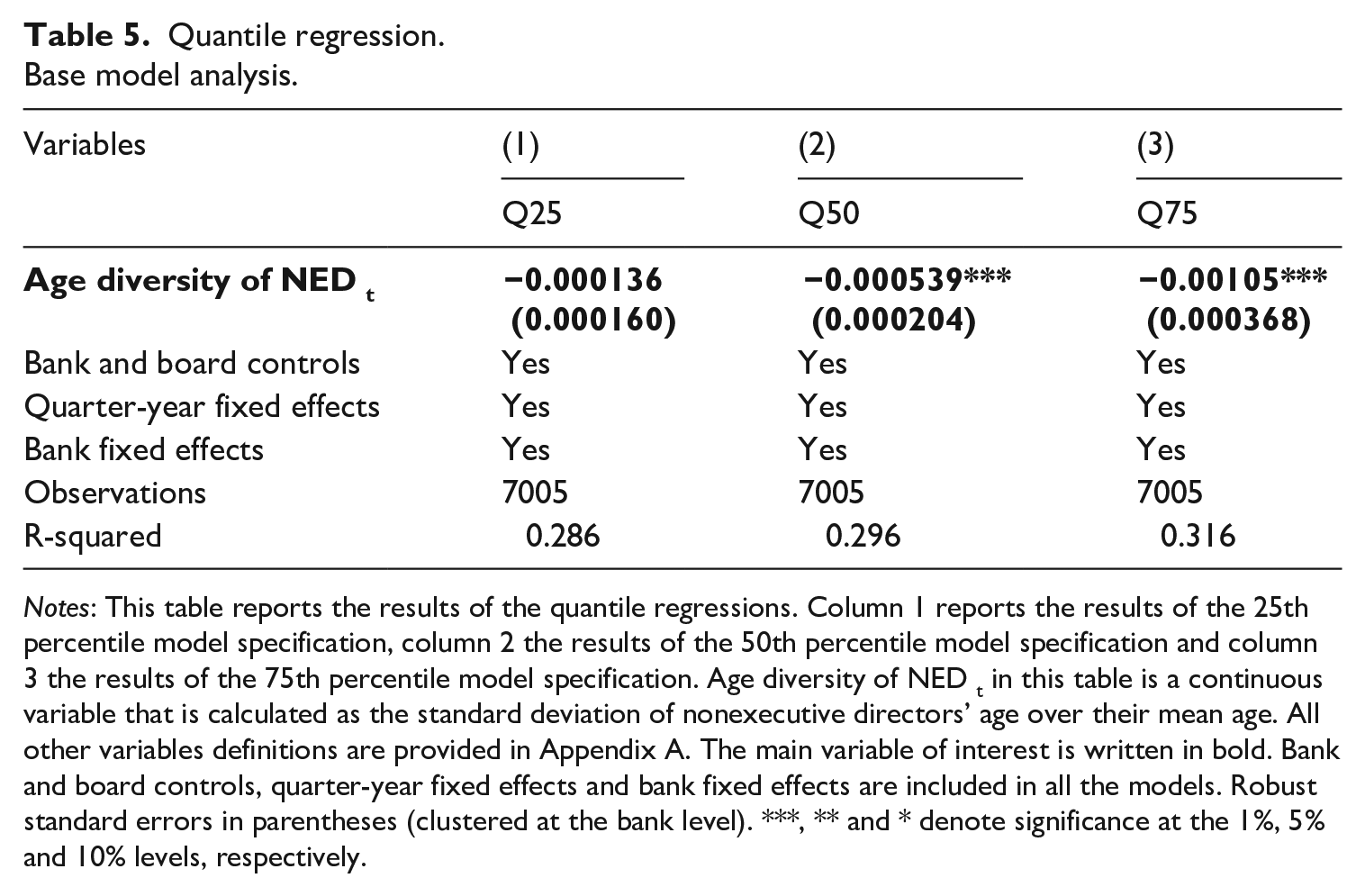

Quantile regression analysis

Next, we use quantile regression analysis, employing Parente and Silva’s (2016) method in calculating clustered standard errors. This analysis has two advantages over fixed effects analysis. The fixed effects estimator assumes that the magnitude of the relationship between age diversity and earnings management is consistent across different quantiles of the data. On the other hand, the quantile regression allows us to investigate whether, at lower versus higher levels of age diversity, a slight increase in age diversity affects earnings management or not. Another advantage of the quantile regression over the fixed effects estimator is that it does not make any assumption about the distribution of the residuals, thus ensuring the validity of our results.

Table 5 reports the results of the 25th percentile (column 1), 50th percentile (column 2) and 75th percentile (column 3). The reported results suggest that the relationship between Age diversity of NED and |DLLP| is not homogeneous across the sample. The effect of age diversity on earnings management becomes stronger with an increase in age diversity. The results of the quantile model suggest that the coefficient of age diversity, conditional on the 25th percentile, is insignificantly different from zero. However, the coefficient increases in both magnitude and significance as the level of age diversity increases. In the 50th percentile regression, the coefficient of Age diversity of NED is −0.0005 (p-value < 0.05), whereas it increases to –0.0013 (p-value < 0.01) in the 75th percentile regression. Table 6A (online appendix) reports the results of this analysis using the extended model, including CEO characteristics, and our findings remain the same. Overall, the results of the quantile regression confirm our earlier findings. They also show that the effect of age diversity on |DLLP| is not consistent across our sample, revealing that the strength of the relationship is increasing with the increase in age diversity.

Quantile regression.

Base model analysis.

Notes: This table reports the results of the quantile regressions. Column 1 reports the results of the 25th percentile model specification, column 2 the results of the 50th percentile model specification and column 3 the results of the 75th percentile model specification. Age diversity of NED t in this table is a continuous variable that is calculated as the standard deviation of nonexecutive directors’ age over their mean age. All other variables definitions are provided in Appendix A. The main variable of interest is written in bold. Bank and board controls, quarter-year fixed effects and bank fixed effects are included in all the models. Robust standard errors in parentheses (clustered at the bank level). ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

To ensure robustness of the findings from the quantile regression, we also use fixed effects estimators with dummy variables to measure the level of age diversity. Specifically, we introduce Age diversity Q25, Age diversity Q50 and Age diversity Q75 variables to our fixed effects model. Age diversity Q25 is a dummy variable that takes the value of one if the age diversity of the board is between 25th and 50th percentiles and zero otherwise. Age diversity Q50 is a dummy variable that takes the value of one if the age diversity of the board is between 50th and 75th percentiles and zero otherwise. Age diversity Q75 is a dummy variable that takes the value of one if the age diversity of the board is more than the 75th percentiles and zero otherwise.

Our results are similar to those reported in the quantile regression and show that Age diversity Q25 has no effect on |DLLP|, while both Age diversity Q50 and Age diversity Q75 have a significant negative effect on |DLLP|. In addition, the effect of Age diversity Q75 is stronger than that of Age diversity Q50, confirming our earlier findings that the efficacy of age diversity increases with the increase in the level of age diversity. Table 7A in the online appendix reports the results of this regression.

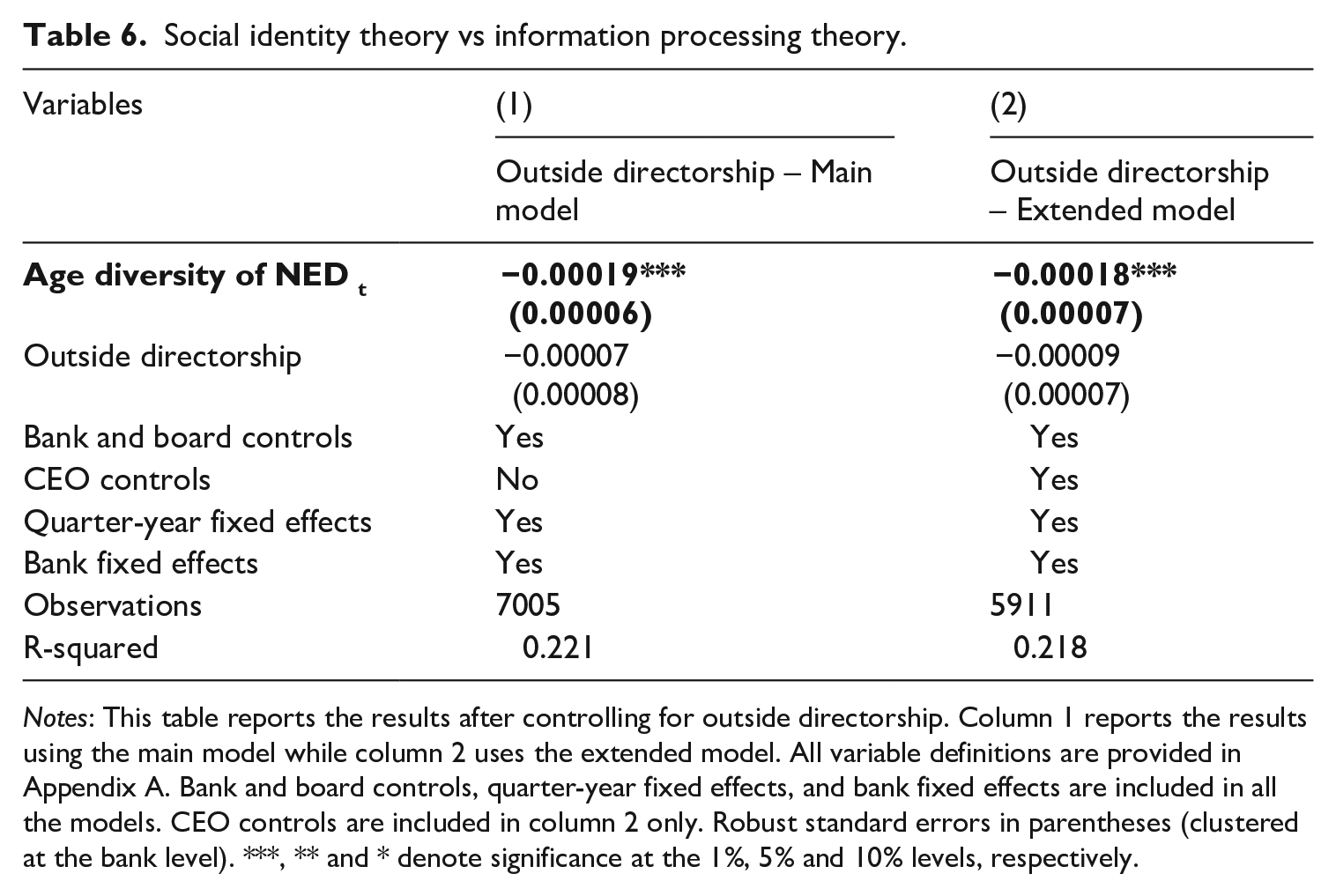

Social identity theory versus information processing theory

Our review of the literature suggests that both social identification theory and information processing theory can help us explain our results. Information processing theory suggests that board diversity brings verities of experience and knowledge to the board. As a result, this will improve the board’s ability to process complex information and better interrogate managers’ decisions. Although we emphasise that information processing theory provides an indirect or, probably, weak explanation of the relationships we examine, we cannot rule out its role in our discussion.

To further investigate whether information processing theory is relevant to our setting, we examine whether outside directorship affects financial reporting quality in banks. The assumption is that directors with more directorship positions are more experienced and have access to different knowledge and expertise (Fama and Jensen, 1983; Masulis and Mobbs, 2011). Thus, we use outside directorship as a proxy of board quality, hence, of its ability to process and solve complex business problems. We expect boards with a higher proportion of outside directorships to be able to better process information.

We follow previous literature and consider a director with more than two outside board seats to be busy (Ferris et al., 2003; Jiraporn et al., 2009). Then, we construct a dummy variable that takes the value of one if the board’s percentage of busy independent directors is in the top quartile of the sample distribution of the percentage of busy independent directors. Column 1 of Table 6 reports our results. The results fail to show that outside directorship affects |DLLP|, indicating that information processing theory might not be relevant to our main findings. Column 2 of Table 6 also shows a similar result for the extended model. This is also in line with our analysis presented in Table 3, as board education can be another proxy for board ability and its quality to process complex information. However, we caution the reader against over-interpreting our findings in this section.

Social identity theory vs information processing theory.

Notes: This table reports the results after controlling for outside directorship. Column 1 reports the results using the main model while column 2 uses the extended model. All variable definitions are provided in Appendix A. Bank and board controls, quarter-year fixed effects, and bank fixed effects are included in all the models. CEO controls are included in column 2 only. Robust standard errors in parentheses (clustered at the bank level). ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

The relationship between age diversity and bank risk

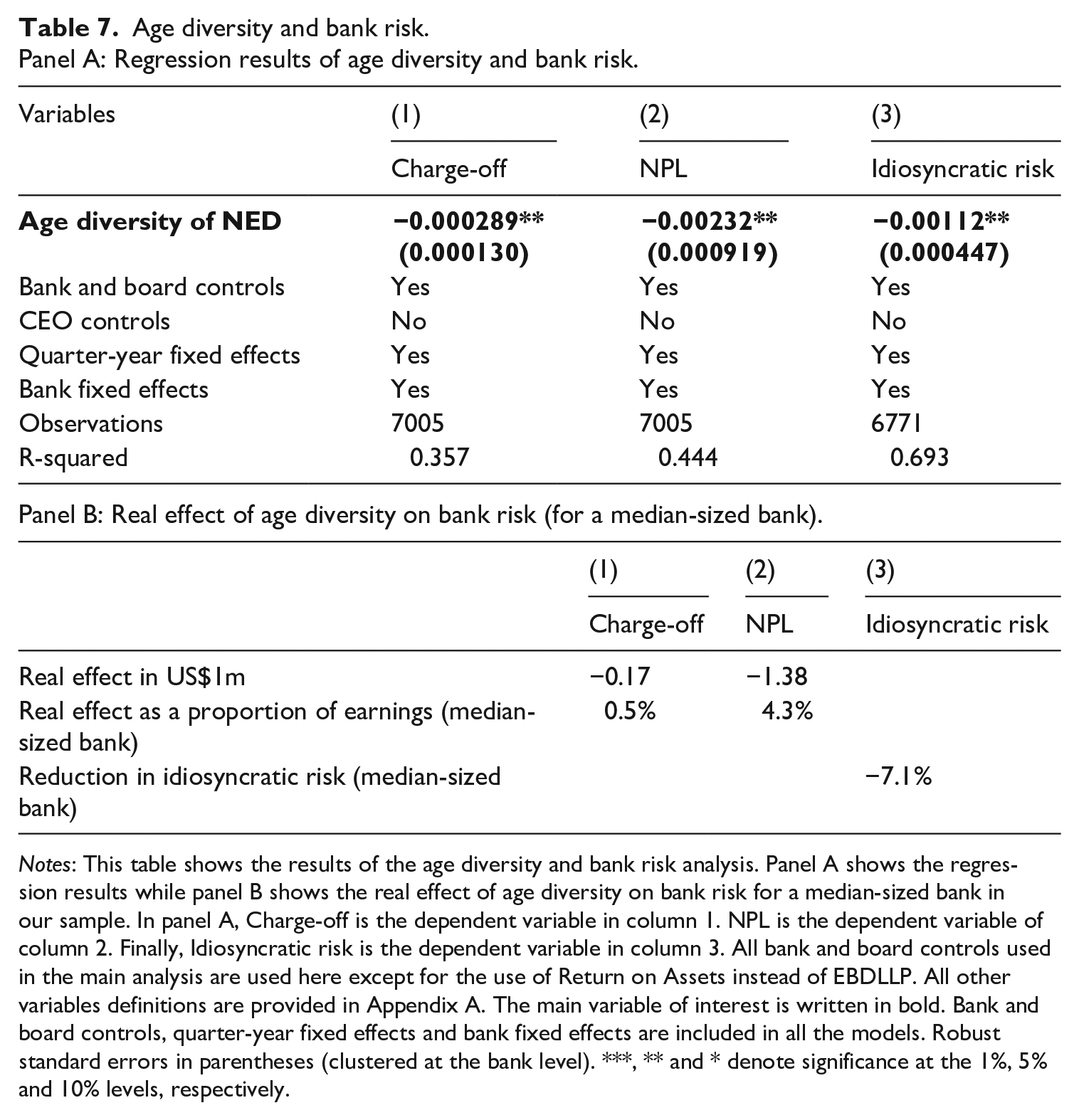

This section investigates how age diversity can affect the monitoring performance of the board in areas of activity beyond financial reporting, and in particular bank risk. Previous studies suggest that banks that do not manage earnings and report timelier LLP are associated with decreased loan risk (Beatty and Liao, 2011; Bushman and Williams, 2012; Cohen et al., 2014). For instance, Beatty and Liao (2011) show that banks that report timelier LLP are associated with lower corruption in loans because their timelier reporting leads to timelier correction. In addition, Bushman and Williams (2012) find that banks that do not manage earnings are less risky. They argue that this is because earnings management dampens earnings quality and thus inhibits external stakeholders from disciplining banks over risk taking. Cohen et al. (2014) document that banks that managed earnings before the financial crisis had higher tail risks, as measured by stock price crashes.

Therefore, given that our main analysis shows that banks with age-diversified boards are less likely to engage in earnings management, we postulate that these banks will also be associated with decreased loan risk. Banks have lower loan risk when they lend exclusively to borrowers who can repay. We use NPL, Charge-off and idiosyncratic risk to measure bank risk. Thus, we expect banks with age-diversified boards to be associated with lower NPL, Charge-off and Idiosyncratic risk.

To construct our idiosyncratic risk measure, we first use the following market model:

Where Stock returnit is the stock return on day t for bank i, and Market returnt is the return on the Center for Research in Security Prices (CRSP) value-weighted market index on day t. The lagged and lead market return variables are used to account for non-synchronous trading (Dimson, 1979; Kim and Zhang, 2016).

We report the results in Table 7. All the control variables used in our |DLLP| model are used here except for the use of return on assets instead of earnings before LLP. The association between Age diversity of NED and Charge-off, NPL and Idiosyncratic risk is negative and significant, at the 5% level. We also use the extended model and find that our conclusions do not change (Table 8A – online appendix). Panel B of Table 7 shows the economic effect of age diversity on bank risk. Our results show that for a median-sized bank in our sample, age diversity reduces Charge-off by US$0.17 million (0.5% of earnings), NPL by US$1.38m (4.3% of earnings) and idiosyncratic risk by 7.1%.

Age diversity and bank risk.

Panel A: Regression results of age diversity and bank risk.

Notes: This table shows the results of the age diversity and bank risk analysis. Panel A shows the regression results while panel B shows the real effect of age diversity on bank risk for a median-sized bank in our sample. In panel A, Charge-off is the dependent variable in column 1. NPL is the dependent variable of column 2. Finally, Idiosyncratic risk is the dependent variable in column 3. All bank and board controls used in the main analysis are used here except for the use of Return on Assets instead of EBDLLP. All other variables definitions are provided in Appendix A. The main variable of interest is written in bold. Bank and board controls, quarter-year fixed effects and bank fixed effects are included in all the models. Robust standard errors in parentheses (clustered at the bank level). ***, ** and * denote significance at the 1%, 5% and 10% levels, respectively.

In untabulated analysis, we also use lead NPL, Charge-off and Idiosyncratic risk to reflect the fact that it takes time for the board to affect loan quality. We use one, two, three and four quarters lead periods. 5 Our results hold under all these specifications.

Discussion

Academic research on boards’ diversity focuses primarily on the effect of gender and ethnic diversity and little attention is paid to the effect of age diversity on boards’ effectiveness. Moreover, the relatively little empirical evidence on the effect of age diversity on boards examines the board’s advising role. To the best of our knowledge, our research is the first to examine the impact of age diversity on the monitoring role of the board, with a particular focus on the impact of age diversity on the quality of financial reports.

Empirical evidence on the effect of age diversity on firm performance is mixed owing to the fact that different theories predict different impacts of age diversity on group performance. Information processing theory predicts that age diversity of the board will have a positive impact. This theory suggests that directors from different age groups bring varieties of experience and knowledge to the board, which will enhance the board capability in processing information and solving complex business problems (Harrison and Klein, 2007; Wegge et al., 2008). On the other hand, social identity theory predicts that age diversity will increase conflict and communication difficulties between directors, which may distort the quality of decision making on the board (Chatman and Flynn, 2001; Talavera et al., 2018). We argue that age diversity is likely to have an overall positive impact on the board performance as a monitor of the executives’ decision making. Specifically, we argue that the increased propensity to disagreement and conflict may improve board independence and result in better monitoring (Cumming et al., 2015; Zhou et al., 2019). In addition, in an age-diverse board, it is less likely that any age group would dominate the board’s internal communication, thus improving the quality of discussion and allowing for better scrutiny of managerial decisions.

Our results overall suggest that age diversity reduces earnings management in banks. We observe that banks with age-diversified boards, holding everything else equal, report lower discretionary LLP. Specifically, we find that age diversity is associated with a decrease of 0.0187 percentage point in |DLLP|. For a median-sized bank, this is equivalent to a reduction of US$1.6m in DLLP. We believe that this is a significant change in economic terms, given that the median LLP in our sample is US$6.52 million and median earnings are US$32m. Our results hold even after we control for CEO characteristics. For a median-sized bank, we find that an age-diversified board will reduce DLLP by approximately US$1.5m, not significantly different from our earlier finding. In order to deepen our understanding of the effect of age diversity on DLLP, we use a continuous variable to measure age diversity. We find that a one-standard-deviation increase in age diversity leads to a decrease of US$0.72m in DLLP in real terms. In sum, these findings are consistent with our hypothesis that age-diversified boards are more effective in monitoring managers and limit earnings manipulation in banks.

Among many robustness tests, we control for tenure diversity and the education level of the board. It is reasonable to assume that older directors have higher tenure while younger directors are better educated. Since old directors are those with high tenure, it might be tenure diversity driving our results. In addition, because diverse boards consist of young and old directors, it is possible that the input of younger directors, who are arguably better educated, drive our findings. Thus, we account for these two factors to ensure that our age diversity measure does not actually capture tenure diversity or board education. Still, our results hold. Our findings emphasise that age diversity of the board’s independent directors reduces earnings management in banks, not tenure diversity or board education.

The use of various firm-, board- and CEO-level controls, fixed effects estimator and propensity score matching add to the robustness of our findings. We are confident that our analysis addresses concerns related to selection bias and omitted variable bias. Fixed effects estimator accounts for omitted variable bias related to time-invariant characteristics such as firm culture. On the other hand, propensity score matching deals with selectin bias compared with treated banks and similar non-treated banks. The concept behind this analysis is to maintain that all observable characteristics other than the age diversity of the board are virtually similar. Thus, we can conclude with confidence that the variations in earnings management in banks are exclusively explained by the variation in the age diversity of the board.

We also examine whether the relationship between the board’s age diversity and earnings management in banks is non-linear. We deploy a quantile regression analysis; this specification allows us to capture the effect of the change in age diversity on earnings management at low, moderate and high levels of age diversity. Our results reveal that at low levels of age diversity, a slight increase in age diversity will not affect earnings management. However, we find that the strength of the relationship increases with the increase in age diversity. At moderate levels of age diversity, we find a positive association between a slight increase in age diversity and earnings management. We find that the relationship becomes even stronger at high levels of age diversity. This indicates that banks may only grasp the benefits of age diversity with moderate and high diversity levels. In other words, boards with limited age diversity have to make significant changes to their board structure to capture the full benefit of age diversity. The quantile regression findings also confirm our earlier suggestion that in a well-diversified board, no single group can control the board discussion.

Previous studies suggest that financial reporting has a significant effect on banks’ risks (Bushman and Williams, 2012, 2015; Cohen et al., 2014). Thus, we investigate what effect age diversity has on bank risk. It is known that transparent LLP reporting reduces loan risks through accelerating corrective actions against bad loans and enabling external stakeholders to monitor banks (Akins et al., 2017; Bushman and Williams, 2012). Our results suggest that age diversity reduces bank risks as observed by reducing loan Charge-off, non-performing loans and idiosyncratic risks. These findings are consistent with our main results that board diversity improves its monitoring performance.

Generally, our findings are consistent with the notion that age-diversified boards are more effective at monitoring managerial decision making. Our results are consistent with Zhou et al. (2019), who find that the generation gap between the CEO and the Chairman improves risk monitoring. On the other hand, our results contradict Talavera et al. (2018), who find the age diversity is associated with weakened performance and not linked with risk monitoring. We attribute this conflict in results for two possibilities. First, their study investigates risk taking in Chinese banks. As the corporate governance structure and mechanisms in China are significantly different compared with the United States (Becht et al., 2011; Lin and Zhang, 2009), we cannot generalise their results to the US setting. Second, we use a slightly different measure of age diversity. While Talavera et al.’s (2018) diversity measure includes executive and nonexecutive directors, our measure excludes executive directors. We believe that excluding executive directors makes the measure more relevant in a monitoring context.

While previous research focuses mainly on the effect of board diversity on firm performance (i.e. the advisory role of the board), our study sheds more light on its effect on the board’s monitoring role. Interestingly, we find stronger monitoring performance for age-diversified boards. We attribute our results to the notion that diversity improves board independence, based on social identity theory. Using the same theory, some previous studies view that diversity increases conflict in the board and has a destructive effect on the advisory role of the board. However, we counter-argue that it has a constructive effect on its monitoring role. In addition, our results might be driven by the fact that diversity improves discussion in the board (information processing theory) and allows it to understand complex business issues better. This would eventually, though indirectly, improve the monitoring performance of the board. However, our early evidence fails to show a link between information processing and the monitoring ability of the board. Following recent calls on the need for further interdisciplinary research on diversity issues and the role of identities in organisations in general (Brown, 2022), we also highlight the need for further interdisciplinary studies on the importance of social identification issues for the board and their impact on corporate decision making.

To the best of our knowledge, our article is also the first to show that age diversity of the board improves financial reporting quality in banks. Previous research on board diversity focuses mainly on the effect of gender (Cook and Glass, 2018; Cook et al., 2019; Fan et al., 2019), while other forms of diversity are overlooked. We also contribute to the banking literature. As banks’ financial reports are opaque (Acharya and Ryan, 2016; Beatty and Liao, 2014; Yue et al., 2022), both academics and policymakers examine the factors that affect financial reporting transparency in banks. This literature reveals that board independence (Cornett et al., 2009), ownership structure (Bushman et al., 2017), managerial overconfidence (Black and Gallemore, 2013), competition (Jiang et al., 2016) and operational diversification (Tran et al., 2019), among other characteristics, affect financial reporting quality in banks. We extend this literature and show that age diversity of the board reduces earnings management practices and hence improves financial reporting transparency in banks.

In addition, our study has at least one practical implication. The Basel Committee on Banking Supervision (2015) states that the complex nature of bank activities should encourage banks to consider diversifying their boardrooms. Our results support this call for diversifying boards and suggest that age diversity improves the financial reporting quality. Our findings are particularly important for banks, as they show that age diversity improves transparency in an opaque industry. In addition, the 2007–2009 financial crisis shows that excessive risk taking by banks may be costly to the economy as a whole. Thus, our findings are crucial in this perspective as we show that risk taking is reduced under the supervision of an age-diversified board.

Limitations and directions for future studies

Our study is not without limitations. Although we control for endogeneity and omitted variable bias, we cannot rule out the possibility that they may still influence our results. Second, we use models widely used in the bank accounting literature to estimate earnings management levels. Thus, our results are highly dependent on the reliability of our estimations. However, there is no reason to suggest that age diversity systematically correlates with the estimation error; hence, we are confident in our findings’ reliability. Future studies might extend our findings to different industries, as different industry characteristics can provide managers with different earnings management opportunities.

Another limitation of our study is that our setting does not allow us to clearly establish which theory explains our results. We build our hypotheses on information processing and social identification theories. While both theories predict the same outcome, they suggest different mechanisms. Information processing theory predicts that age diversity will improve the monitoring ability of the board because a diverse board is better at solving complex problems. On the other hand, social identity theory attributes the improvement in boards’ monitoring performance to the improvement in board independence. Unfortunately, our setting does not allow us to clearly establish whether both or only one of these theories can explain our results. However, we attempt to distinguish between the two theories by investigating whether outside directorship or board education, as a proxy of directors’ broad knowledge, can improve the monitoring ability of the board. We do not find evidence of an association between outside directorship or education and the board monitoring effectiveness, indicating that information processing is less relevant to our setting. However, we still urge future studies to further distinguish between the two theories in a monitoring setting and to examine through which mechanisms board monitoring performance can be improved or deteriorated. This could entail the use of primary data (e.g. interviews, surveys), which could help identify any social identification issues and the emergence of respective board faultlines.

Finally, we warn the reader against over-interpretation of our results. Although our study finds that age diversity improves financial reporting quality, we do not believe that imposing regulations on age quota would necessarily yield the same outcome. Our study uses a sample of US banks, where there is no requirement for quotas. In other words, banks in our sample voluntarily diversified their boards. Thus, we cannot assure policymakers that imposing mandatory requirements for age diversity will improve banks’ performance. Banks may diversify their banks by hiring under-qualified directors, who would rubber-stamp boards’ decisions. Previous studies on regulatory effects on firms show that regulations do not always produce their intended outcome (Kim and Klein, 2017; Lennox, 2016).

Conclusion

This article examines the association between age diversity and financial reporting quality in banks. We use LLP as our accrual-based earnings management proxy, the most significant single accrual for commercial banks. Our sample covers US banks for the period between 1996 and 2018. Controlling for various firm and board characteristics, and bank fixed effects, we find that age diversity is negatively related to the absolute value of DLLP. We also address heterogeneity in the association between age diversity and earnings management using a quantile regression estimator. The results suggest the relationship increases with the increase in age diversity. We also control for board tenure diversity and board education to rule out the possibility of omitted variable bias affecting our results. Finally, we use propensity score matching to attenuate the effect of self-selection bias. Our results remain robust under all these tests.

To the best of our knowledge, our study is the first to show that the age diversity of the board improves its effectiveness in monitoring the quality of financial reports. Specifically, we show that the age diversity of the board improves the transparency of financial reports in banks. In addition, amid increasing calls to make corporate boards diverse, policymakers might find our results useful. Our evidence supports regulatory bodies’ inducement of companies to increase diversity in their boards.

Supplemental Material

sj-pdf-1-hum-10.1177_00187267221108729 – Supplemental material for Age diversity and the monitoring role of corporate boards: Evidence from banks

Supplemental material, sj-pdf-1-hum-10.1177_00187267221108729 for Age diversity and the monitoring role of corporate boards: Evidence from banks by Mohamed Janahi, Yuval Millo and Georgios Voulgaris in Human Relations

Footnotes

Appendix

Variable definitions.

| |DLLP| | The absolute value of discretionary loan loss provision scaled by lagged total loans. We calculate DLLP as the estimated residuals from Model 1. |

| Age diversity of NED | A dummy variable that takes the value of one if the level of age diversity of the nonexecutive directors is above the sample median and zero otherwise. The level of diversity of the board is calculated as the standard deviation of the age of nonexecutive directors over their age average. |

| Assets growth | The percentage of increase of assets over the quarter. |

| Audit committee size | Total number of directors in the audit committee. |

| Analysts’ dispersion | The standard deviation of analysts’ forecasts prior to a quarterly earnings announcement. |

| Board size | Total number of directors on the board of directors. |

| CEO age | The age of the CEO as provided by ExecuComp. |

| CEO gender | A dummy variable that takes the value one if the CEO is a woman and zero otherwise. |

| CEO/chairman duality | A dummy variable that takes the value one if the same person holds the CEO and chairman roles, and zero otherwise. |

| Change in loan | The change in loans over the quarter scaled by lagged total loans. |

| Change in NPL | Change in non-performing loans (NPL) over the quarter scaled by total loans. |

| Charge-off | Net Charge-off as a percentage of total loans. |

| Loan concentration | Total loans over total assets. |

| EBDLLP | Earnings before extraordinary item plus DLLP scaled by lagged total loans. |

| Board education | For all nonexecutive directors, we assign a value of one to directors with bachelor degrees, two to directors with master’s degrees, three for directors with doctoral degrees and zero otherwise. Then, we calculate the average of the directors’ education level for a given board. |

| Gender diversity % | Percentage of female independent directors in the board. |

| LLP | Loan loss provision as a percentage of total loans. |

| ln Assets | The natural log of the book value of the bank’s total assets. |

| ln CEO compensation | The natural log of CEO total compensation, comprising the following: salary, bonus, other annual, total value of restricted stock granted, total value of stock options (using Black-Scholes), long-term incentive payouts and all other total. |

| Loan loss reserves | Allowance for loan loss provision as a percentage of total loans. |

| Nonexecutive directors % | Percentage of nonexecutive directors on the board. |

| Outside directorship | A dummy variable that takes the value of one if the proportion of busy directors in the board is among the top quartile in our sample. A director is considered busy when they hold two or more outside directorships. |

| Return on Assets | Earnings before extraordinary item divided by total assets. |

| Tenure diversity of the board | The standard deviation of nonexecutives’ tenures on the board. |

| Tier one Capital % | Tier one capital divided by risk-weighted assets. |

| Forecast error | The mean of the absolute value of analysts’ forecast error. Forecast error is calculated as the difference between the actual earnings reported by the bank and the analyst’s earning forecast. |

| Diversity of audit committee – dummy variable | A dummy variable that takes the value of one if the level of age diversity of the audit committee is above the sample median and zero otherwise. The level of diversity of the audit committee is calculated as the standard deviation of the age of nonexecutive directors over their age average. |

| Diversity of audit committee – continuous variable | The standard deviation of the age of nonexecutive directors over their age average. |

| Age diversity of executive directors | The level of diversity of the audit committee is calculated as the standard deviation of the age of executive directors over their age average. |

| Average age of executive directors | Average age of the executive directors. |

| Financial experts of the audit committee | Total number of financial experts on the audit committee over audit size. |

| Percentage of female directors on the audit committee | Total number of female directors on the audit committee over the audit committee size. |

| Percentage of female financial experts on the board | Total number of female financial experts over the board size. |

| NED ownership | Number of independent directors that own more than 1% of the bank shares divided by the total number of directors on the board. |

| Risk committee | A dummy variable that takes the value of one if the board has a separate risk committee, an asset quality or similar committee. |

Acknowledgements

We gratefully acknowledge comments from the associate editor and three anonymous reviewers, Konstantinos Bozos, Zulfiqar Shah and seminar participants at Alliance Manchester Business School and Warwick Business School.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.