Abstract

The “new, new trade theory” argues that firm-specific attributes such as size explain why large firms predominantly engage in foreign direct investment (FDI) and thus reap most of the rewards of globalization. However, studies have neglected the importance of firms’ political influence over core financial institutions. I argue that large firms engage in greater FDI in part because of their political connections, which allow them to receive government loans in support of FDI. Using a unique, hand-coded dataset that includes 4936 directors of South Korean firms and these firms’ FDI announcements, I show that firms that place elite financial officials on their boards engage in greater FDI than firms without such board-member connections. Therefore, the outsized gains that large firms receive from globalization are dependent on their political ties to their home government.

Foreign Direct Investment (FDI) can be very lucrative for firms. Halliburton, a US-based oil company, received a $7 billion contract to reconstruct Iraq’s oil infrastructure after the Iraq war. 1 Skypower, whose headquarters are in Canada, concluded a $1.3 billion contract with Uzbekistan in 2018 to build 1000 MW of solar energy production facilities throughout the country. 2 Global firms can benefit not only from being awarded investment contracts, but also operating the resulting facilities, which increases long-term revenues.

However, FDI involves significant costs (Foley & Manova, 2015, 125–126). Most of these are up-front, fixed costs that often go toward building production or service facilities. Likewise, various non-economic factors, such as unstable political situations or weak property rights, can raise the risk of FDI projects. 3 Most FDI projects only become profitable several years after the project is completed. Therefore, the significant up-front costs of FDI, and the long time horizon of its profitability, prevent many firms from entering the global market.

Political economy models show that only the most profitable firms can afford to bear the costs of FDI (Antràs & Helpman, 2004; Helpman & Yeaple, 2004; Melitz, 2003). Large firms are often best able to do so. They can provide differentiated products or deliver skill-intensive services at low prices because they are able to leverage economies of scale. By contrast, many smaller firms cannot take advantage of economies of scale and so must sell similar products at higher prices (Bernard et al., 2003). Ultimately, large firms can monopolize the market for certain products by undercutting their competitors with low prices, allowing them to further increase their profits in both foreign and domestic markets. Consequently, it is believed that only the largest firms that generate the most profits are able to serve foreign markets through costly FDI.

FDI research has not fully explored the political power of large firms. 4 Firms are not apolitical actors that are insulated from governments (e.g., Fisman, 2001). Instead, they frequently lobby their government to obtain preferred policies (Grossman & Helpman, 1994). In turn, many governments incentivize domestic firms to engage in FDI to boost national economic performance (Kalinowski & Cho, 2012; Shi, 2015). One of the common methods of doing so is by making credit easily available through state-owned banks (Danzman, 2019).

I argue that state-subsidized financing acts as a financial incentive for certain firms to engage in FDI. Beyond just directly reducing the immediate financial burdens of FDI, state-subsidized financing also functions as risk insurance. Political events, such as contractual breaches and expropriations by host governments, degrade the value of firms’ foreign assets. The home government can directly cover these losses with access to cheap credit or cash payments. This insurance reduces the political risks of FDI and thereby ensures its long-term profitability. Therefore, I expect firms, particularly large ones, to enhance their government lobbying efforts to secure such state-subsidized financing. Specifically, I hypothesize that they will place retired bureaucrats on their boards who served previously in top-ranking positions at important state financial institutions. The idea is that these board members will help firms to obtain larger bank loans through existing personal networks.

I combine unique project-level FDI announcement data with firm-level board connection data to investigate the relationship between firms’ ability to secure state-subsidized financing and their ability to pursue more FDI projects. I capture board-member ties to state-owned banks by hand-coding a political career dataset of 4936 board members of 732 firms in South Korea. Examples of these financial institutions include the Korean Development Bank, the Export-Import Bank of Korea, and the Financial Supervisory Commission, all of which have authority over the distribution of state-subsidized financing. The empirical results reveal that firms that hired former financial executives at state financial institutions pursued more FDI projects than firms who did not hire such executives. The results also show that the strength of this effect is positively associated with firm size.

This study builds on recent scholarship, but is unique in several ways. It has its origins in the recent research on the political economy of large firms. So-called “new, new trade theory” suggests that firm-specific attributes, such as size, explain why it is predominantly large firms that engage in international markets (e.g., Helpman & Yeaple, 2004) and thus reap most of the rewards of globalization (Baccini et al., 2017). However, this study hypothesizes that the outsized gains that large firms receive from globalization are also dependent on their links to their home governments (e.g., Allee & Peinhardt, 2014). Moreover, a large body of studies in comparative politics often focuses exclusively on capital importing countries (Jensen, 2008). Previous studies highlight capital importing countries’ efforts to attract FDI (Jensen et al., 2015) and show how such capital inflows can affect their electoral consequences (Owen, 2019), corruption (Pinto & Zhu, 2016), and political stability (Bak & Moon, 2016). However, this study provides fresh insight by highlighting capital exporting countries’ interests in promoting FDI. Finally, this study’s analysis of the role of corporate board members complements the literature on political lobbying by firms (Vidal et al., 2012; Bertrand et al., 2014; Shepherd & You, 2020). Political science scholars recently have begun to focus on the value of corporate board members in lobbying activities (Palmer & Schneer, 2019). This study shows how firms can increase their international operations through the hiring of former governmental officials.

Political Economy of FDI Promotion

FDI is an essential part of global firms’ activities, but is not without cost. Recent studies that analyze micro-level firm data have argued that firm-level attributes explain firms’ engagement in international markets, regardless of industry competitiveness or country-level factor endowments (Melitz, 2003). 5 The consistent finding of these studies is that there is a size threshold that explains why some firms can afford the costs of engaging in international business. The largest firms, which are often the most competitive at selling products at the lowest price, are sufficiently profitable to afford the costs of FDI. Their competitiveness also enables them to engage in different modes of the production, such as allocating their production networks across different countries or establishing export platforms. Small and medium-sized firms may be unable to bear the fixed costs of FDI and instead may export their products to target markets instead of producing them there directly. The smallest firms are unable to make profits in the face of international competition, and typically drop out from the global markets (Helpman & Yeaple, 2004).

FDI studies have largely overlooked the role that home governments play in promoting FDI. Firms are active in the domestic political process and governments are often receptive to their demands (Grossman & Helpman, 1994). Therefore, home governments often provide domestic firms with various forms of support when they engage in FDI, such as international investment agreements (Allee & Peinhardt, 2010; Kim, 2020) and trade rules that favor their products (Baccini et al., 2017; Manger, 2012).

Subsidies are an effective domestic tool for home governments that past FDI studies have tended to ignore. Governments can mobilize financial resources to support domestic firms’ FDI projects if they have sufficient control over domestic banks (La Porta et al., 2002). For example, Japan is notable for providing state-subsidized financing for Japanese firms’ foreign ventures (Solis, 2003, 153). Likewise, since the 2000s, the Chinese government has been facilitating FDI by state-owned enterprises through financing from state-run banks (Gallagher & Irwin, 2014; Shi, 2015). Ample evidence suggests that banks are subject to political capture (La Porta et al., 2002). Banks have been found to increase their lending specifically during election years (Cole, 2007), and politicians can exploit bank lending to purposefully increase employment in politically attractive regions (Carvalho, 2014).

Firms employ political strategies to receive such state financial support. Khwaja and Mian (2005) show that Pakistani firms that hired boards of directors who previously ran in state or national elections took out twice as many loans from state-owned banks than other firms. Using the same political connection data, Khwaja and Mian (2008) also show that firms with political connections can avoid financial distress caused by unanticipated bank liquidity shocks by borrowing with financially preferential terms, while firms without political connections experienced significant declines in overall borrowing. Charumilind et al. (2006) show that Thai firms that placed politically influential people on their boards of directors, or that were owned by wealthy families could more easily engage in long-term borrowing from government-owned banks than their competitors without political connections. Relatedly, Danzman (2019) provides compelling evidence that politically connected firms lobby for FDI liberalization when they lose access to state financing as a result of financial repression or banking reforms. Therefore, a great deal of empirical evidence exists to support claims of politically influenced lending by state banks (Claessens & Laeven, 2008).

Bank lending is an important source of funding for FDI (Ma & Cheng, 2005; Milesi-Ferretti, Tille & Tille, 2011; Contessi & De Pace, 2012; Cetorelli & Goldberg, 2011; Düwel et al., 2011; De Maeseneire and Claeys, 2012). For example, Klein, Peek and Rosengren (2002)’s seminal study shows that the negative financial shocks suffered by Japanese banks in the 1990s reduced the amount of FDI in the U.S. by Japanese firms, indicating that firms relied on bank loans as their primary source of financing. Difficulties in securing loans from banks deter firms from making investments, even if they have alternative sources of funding, such as access to equity markets (Amiti & Weinstein, 2018). 6

State financing might play a key role at different stages of FDI. Given that investments in fixed assets often involve large sunk costs, firms need to secure sufficient financial resources for their future FDI projects during the preparation stage. Firms also may need to demonstrate their ability to finance their projects when they try to win an investment contract from a foreign government. Thus, state financing helps firms to demonstrate that they can defray the up-front costs of FDI.

State-backed financing also can act as a financial safeguard when firms engage in FDI. Studies on international investment agreements commonly assume that global firms want their future FDI projects to be covered by investment protection (e.g., Allee & Peinhardt, 2010). Various policy choices by the host governments can harm these firms’ significant foreign assets. These policy choices, which include breach of contract, regulatory measures, taxation, or out-right expropriation, can lead to dispute settlement procedures that may take five or more years to complete (Raviv, 2015, 654). In such cases, state financing serves as insurance by covering financial losses through direct cash payments. Home governments can relax firms’ monetary budget constraints from various future investment uncertainties. 7

There are many reasons why governments want to promote their firms’ FDI by providing financial support, and this is particularly true with regard to large firms. Whether political leaders remain in office is often determined by national economic performance, and large firms are the largest individual contributors to this performance (Bernard et al., 2012). Relatedly, better FDI performance can increase large firms’ stock prices and thus foster the development of a home country’s financial markets, which in turn promotes overall economic growth (Levine & Zervos, 1996; López-Duarte & García-Canal, 2007). Large firms are also a significant source of political campaign contributions, which can significantly improve politicians’ chances of being re-elected (Samuels, 2001).

Political Connections and FDI Financing in South Korea

Legislators and other government employees are concerned about their careers after leaving the government, which gives rise to a revolving door phenomenon. 8 The lobbying literature shows that a significant number of government officials have chosen to become lobbyists or corporate board members after they leave their government positions (Vidal et al., 2012; Bertrand et al., 2014; Palmer & Schneer, 2016). Retired legislators tend to receive higher salaries than other types of lobbyists because they have more influence over their former colleagues through their personal networks than those who have not served as legislators before (Vidal et al., 2012).

Firms can increase their political clout by placing important ex-politicians on their boards (e.g., Goldman et al., 2009). Former officials can tap into their personal networks, which help firms to create important links with incumbent political leaders and potentially influence government policy. 9 Indeed, policies about issues such as government procurement contracts and tax rates have been found to be influenced by firms’ board-member ties (Goldman et al., 2009; Faccio, 2010). 10

Relatedly, bureaucrats at state banks often look to corporate board positions with high compensation to provide for themselves in retirement. They reasonably believe that they can join corporate boards when they see that their colleagues have previously done so. These former bureaucrats who go on to sit on corporate boards can pressure current bureaucrats by implying that they may be employed on the board in the future if they extend credits. Thus, state banks may become more submissive to these firms’ demands.

The role of corporate political ties in increasing firms’ economic strength is well-evidenced in South Korea (Korea hereafter). Korea’s developmental state produced rapid economic growth in the 1960s and 1970s (Johnson & Mitton, 2003; Amsden, 1992; Evans, 1995). The developmental state assumes direct control over the economy through close coordination with their firms. The Korean government has maintained a great deal of control over the economy since then (Kang, 2002). Interviews that were conducted among Korean multinational firms during the period 2000–2006 indicate that seeking government favor is “a fact of Korean business life” (Siegel, 2007, 629). The corruption scandal that toppled the Park Geun-hye administration in 2017 revealed that the state had retained strong authority over powerful family owned conglomerates, or “Chaebol” (Jäger & Kim, 2019).

Korean firms can receive greater access to state-subsidized financing by strengthening their relationships with the government. Foreign firms have pursued joint ventures with local Korean firms, and prefer working with Korean firms that have ties to the government because banks tend to provide those firms with “cheap finance” (Siegel, 2007). Moon and Schoenherr (2022) show that banks’ lending to firms whose executives were linked to Lee Myung-bak increased after he was elected president (24).

Korean firms seek to use board positions for lobbying in part because of corporate governance reforms following the 1997 Asian Financial Crisis. One such reform required that at least 25% of board seats go to outside, independent directors (Chang, 2003). 11 Since then, Korean firms have sought to recruit former politicians, government officials, and creditor bank executives to fill these slots, and thus such board ties have become prevalent for Korean firms, especially large ones. 12

Two recent Korean corruption scandals have revealed that placing former government officials on corporate boards can create important back channels to access state-subsidized financial resources. Despite being one of the largest Korean shipbuilders, STX Offshore and Shipbuilding (STX) filed for court-led restructuring in 2016 after becoming seriously debt-ridden (Yonhap, 2016). The Korea Development Bank (KDB) appeared to be the main source of this debt, having granted the company KRW 900 billion (USD 883.6 million) in loans. STX used these loans to build production facilities in foreign countries, over-extending itself. It was alleged that the company’s access to KDB’s loans was a product of its political ties (Chung, 2014; Suk, 2014) in the person of Song Jae-yong, a former vice-chairman of KDB and STX board member. KDB also appeared to be responsible for another financial scandal at Daewoo Shipbuilding and Marine Engineering (DSME), the world’s second-largest shipbuilder (Lee, 2016). DSME provided fake audit reports by not including possible costs associated with building 40 overseas production facilities. KDB was the company’s largest creditor and was responsible for overseeing its financial status. Not coincidentally, Kim Yul-jung, a member of DSME’s board, was a former head of KDB. KDB ignored the company’s growing financial difficulties until the fraud debacle stood out. In fact, the vast majority of former top-ranking bureaucrats at state financial institutions, such as KDB, were hired to join corporate boards soon after retiring from public service because of the political connections that they bring with them (Lee, 2013). In sum, these major scandals in Korea reveal that firms can engage in FDI using financing secured through their board-member linkages with the government.

Other corruption scandals have revealed that state bank officials indeed extended credit in return for future employment opportunities. These scandals show that KDB made contracts with borrowers to “hire a board member that KDB recommends” to them (Lee, 2016). Thus, the borrower was contractually required to hire a KDB bureaucrat on the board to receive state financing. A report on the employment of former KDB employees further shows that 29 former KDB bureaucrats had been hired at 12 firms that had received about $902 million (about 1.2 trillion South Korean won) in financing from KDB in the 2013–2018 period (Shim, 2018).

A systematic analysis of bank loans in South Korea also indicates that lending is indeed influenced by political ties. Moon and Schoenherr (2022) collect information about South Korean firms’ loans by analyzing the annual reports they submitted to South Korea’s Financial Supervisory Services.

13

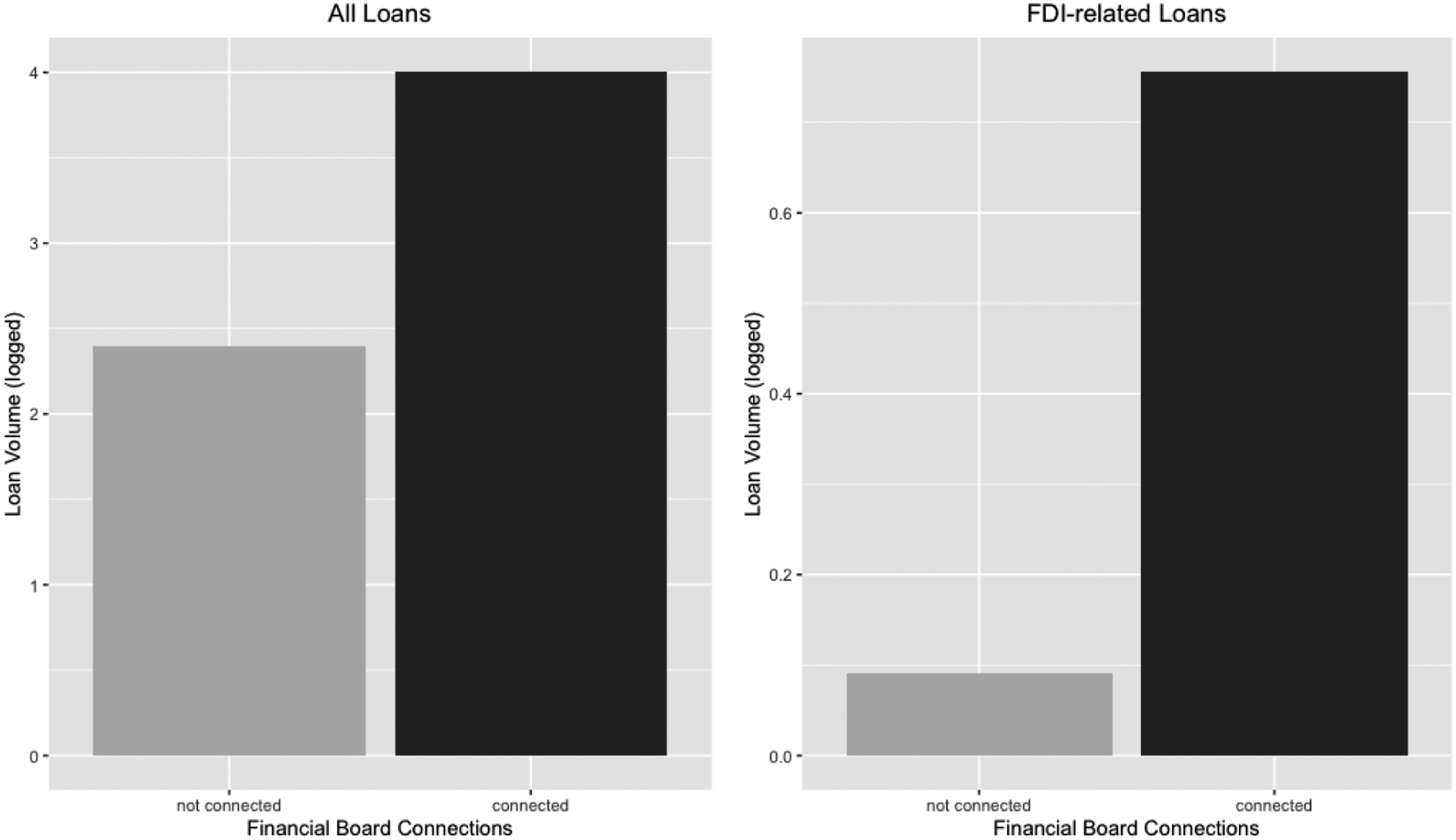

I match Moon and Schoenherr (2022)’s loan information with all publicly listed firms used in this study and classify firms as either “connected” or “not connected” based on their connections with state-owned banks. Figure 1 shows the volume of banks loans obtained by firms that hired former financial bureaucrats and those that did not. Loan Distribution (among large firms).

The left graph in Figure 1 compares the average volume of loans between large firms with and without financial board ties. 14 As the graph shows, on average, firms that had former state-bank officials on their boards received large loans than firms that did not. A simple t-test indicates that this difference is statistically significant at the 99% confidence level. To further understand the link between bank loans and FDI, I also only consider FDI-related loans. One of the merits of Moon and Schoenherr (2022)’s loan data is that it contains information on the use of bank credits. 15 Based on this usage information, I include loans that were taken out to promote FDI, namely, loans taken out for constructing general and energy facilities in other countries. The right graph in Figure 1 shows the average volumes of FDI-related loans taken out by firms with and without financial board connections. As the graph shows, the relationship between financial board connections and FDI-related loans is even stronger than the relationship between financial ties and general loans. A simple t-test shows that this difference is statistically significant at the 95% confidence level. Therefore, the results show that more bank loans were allocated to firms with financial board connections and this relationship was stronger when the loans were taken out to promote FDI.

The historical record shows that the Korean government has been successful in promoting firms’ FDI activities. Korean companies in the manufacturing, finance, transportation, and communications sectors have become internationally competitive after receiving the government’s financial backing (Jones, 1975). The Korean government used “an extensive network of specialized state banks,” such as KDB and the Export-Import Bank of Korea (KEXIM), to direct most credit to select firms to support their international investments (Frieden & Rogowski, 1996, 428). 16

State-subsidized financing in South Korea has desirable qualities that make it particularly attractive to firms that engage in FDI. KDB offers 100% financing with a 10-year repayment period for FDI projects. KEXIM will lend up to 90% of the required capital and offer repayment periods of up to 30 years, depending on the purpose of the loan. Access to this type of financing allows large firms to hedge against FDI risks. In fact, the Korea Trade Insurance Corporation guarantees that firms will be compensated if their assets are lost due to war or host country bankruptcy. KEXIM even guarantees that Korean firms do not carry any financial liability for resource development failures.

Board member ties can be particularly valuable for select, large Korean firms because they are the main participants in international business. A small group of Korean conglomerates accounts for the most offshore production and sales, so it is likely that board member ties producing state financial backing would bring greater benefits to large firms than smaller ones. Moreover, large firms tend to undertake sizeable FDI projects with significant up-front costs. These capital-intensive projects often require big loans that may not be available through private sources because the projects are often too risky and do not become profitable for a long time.

There are also several reasons why the board ties of big businesses are more effective from a lobbying standpoint than those of smaller firms. Political leaders are more likely to represent large firms’ interests because of their economic importance. The Korean government’s historical favoritism toward big businesses is an example of this phenomenon. 17 The ties between the Korean government and large Korean companies have been characterized as a mutual hostage situation because the large Korean companies’ role in the national economy makes them too big to fail (Kang, 2002). There are also many more small firms than big firms, meaning that their interests are more diverse, making collective bargaining with the government difficult (J. Bennett, 1998). Consequently, small firms’ lobbying efforts through board-member ties are likely to be overshadowed by large firms’ efforts.

This study hypothesizes that firms’ political power arising from their corporate boards is closely linked to their FDI ability. Having former heads of state banks or financial supervisory institutions on their boards will serve as effective means for subsidized financing. Firms can use the connections provided by these board members to exert pressure on state banks to receive greater loans, even if their financial status may not qualify them for those loans.

With such extensive financial backing, large firms are particularly well-placed to pursue more FDI projects. As discussed earlier, large firms tend to have more potential opportunities to pursue FDI projects and greater means to secure financing for those projects. In contrast, the chances for small or medium firms to pursue FDI projects are more limited.

Data and Methods

To test these two hypotheses, I analyze the FDI decisions of the 732 Korean firms that were listed in the Korea Composite Stock Price Index from 2012 to 2016. 18 The unit of analysis is the firm level, and this includes all publicly traded firms engaging in FDI for which data is available. 19

The dependent variable in this study is the logged volume of FDI projects (in millions of US dollars). The firm-level FDI data analyzed in this study was drawn from the fDi Markets database provided by The Financial Times. The fDi Markets database contains information about multinational firms’ announcements of greenfield investment projects in which firms planned to build all project facilities. The volume of FDI projects is analyzed instead of the number of projects because pursuing a greater number of FDI projects would require substantial resources and so might obscure the effects of board-member connections on FDI. FDI volume is thus a more conservative metric for measuring the value of board connections.

Although a drawback of the fDi Markets database is that it does not contain information about mergers and acquisitions, it does have several advantages, the most relevant of which is that it contains project-level FDI information, an example of which is Samsung Electronics’ semiconductor production facility in Shaanxi, China. This project-level information, then, is matched with investing firms’ financial data to create unique firm-level FDI data. Because firms can start building entire facilities some years after planning their FDI projects, FDI announcement data allows one to estimate the direct impact that the board ties have on firms’ ability to plan their future FDI. The data also involves a quality check process to confirm the validity of announcements of FDI by searching them from various language sources. As a result, prominent studies in business and political science have begun to use the fDi Markets dataset (Albino-Pimentel et al., 2018; Owen, 2019; Jung et al., 2021).

The first primary independent variable, “Board Ties to State Banks,” measures whether a firm maintained any board-member connections to state banks. 20 To create this variable, I coded data on 4936 members of boards of directors provided by the Korean Listed Companies Association (KLCA), which annually surveys all publicly listed Korean firms. The main argument of the study is that firms that establish ties with state banks via their boards are more likely to engage in FDI given their great political access to financial resources. Thus, I analyzed board members’ political profiles to determine the financial institutions with which they were employed previously. These banks included the KEXIM, the KDB, and the Korea Trade Insurance Corporation (KSURE). Firms were also identified as politically affiliated if at least one member of their board of directors had worked in the leadership position at lending supervisory institutions, such as the Financial Supervisory Service, the Fair Trade Commission, the Financial Services Commission, or the Ministry of Finance. Ninety-five companies were identified as having political connections to the core, state financial institutions. 21

The second independent variable is firm size. The largest firms are generally the only firms that can compete internationally (Osgood et al., 2017), so this study analyses whether size affects a firm’s ability to pursue more FDI projects. I use market capitalization (in millions of USD) of firms to capture their size and this data is drawn from the Worldscope database.

I also include a variable that multiplies firm size times board connections. This interaction term examines whether the effect of board connections on FDI is contingent on firm size. I hypothesize that firm size shapes the extent to which board ties increase the volume of FDI firms can pursue. I argue that large firms have the motivation and resources to dominate lobbying efforts to secure FDI financing. As predicted by my theory, data on board membership shows that the likelihood of firms forming board ties to state banks was positively associated with firm size. Among the largest 10% of firms, which have the highest potential for creating FDI projects, the chances of employment for former financial executives are high: about 46% (33 out of 72) of firms employed at least one board member with experience of serving at state financial institutions or the government’s supervisory body. In contrast, among the smallest firms, which range from 0% to 10% or 10% to 20%, these rates of employment were lower than 2% of firms. 22

Various control variables are added to account for other individual firm characteristics that have been found to correlate with firms’ market performance. Debt ratio, defined as the ratio of total debt to total capital, and profitability, defined as return on equity, are included in all models as control variables. A chaebol dummy is included to account for the perceived political prominence of this group of firms, separate from any board-member ties they might have. Finally, I added sector dummy variables based on the Standard Industrial Classification codes. Data on all these individual firm characteristics are drawn from the Worldscope database, which is based on annual corporate reports. Summary statistics are reported in the Supplemental appendix.

Empirical Results

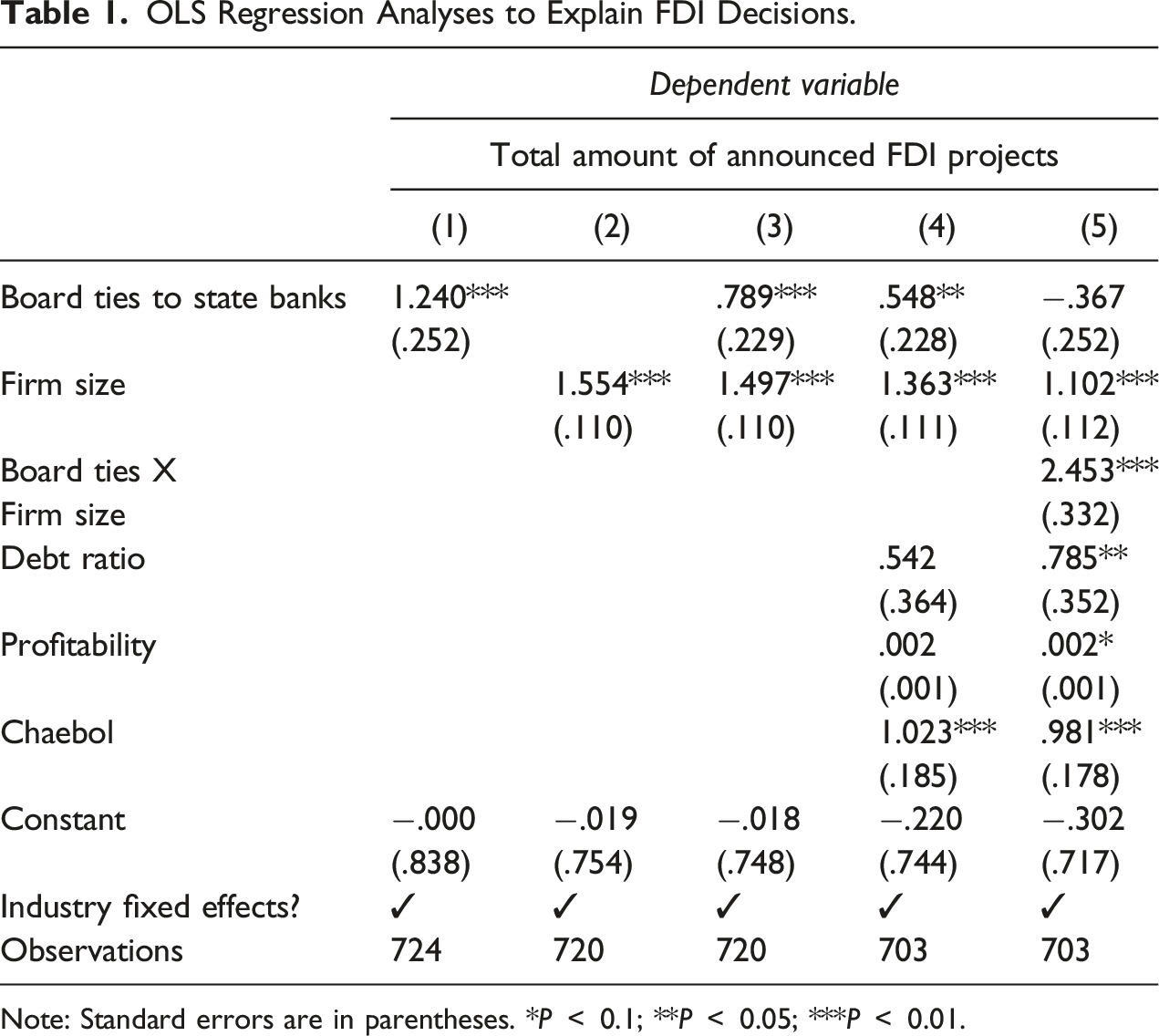

OLS Regression Analyses to Explain FDI Decisions.

Note: Standard errors are in parentheses. *P

The statistical results in Table 1 show that both board member connections and firm size exert strong effects on the volume of FDI projects. The coefficients for board connections and firm size for Models 1–4 indicate that they both have positive and statistically significant effects on firms’ ability to pursue FDI projects. Model 1 shows that the board member connection variable individually has positive effects on FDI promotion. Model 2 shows that the effect of firm size is also independently strong, supporting the conventional wisdom that large firms are better at engaging in FDI. Model 3 shows that these relationships remain significant when these two variables are included in the same model. Model 4 shows that the results are robust after accounting for basic firm characteristics. The findings from Models 1, 3, and 4 provide strong empirical support for the first hypothesis that political ties with state-owned financial institutions have a significant effect on firms’ ability to extend their global businesses. All of the results are robust to industry fixed effects.

Model 5 shows that the strength of the effect of board ties on the value of FDI projects is positively associated with firm size (Table 1). 23 This result reveals a dynamic that importantly alters the way that the effect of board ties on FDI should be thought of. The effect of the board connection variable in Model 5 is no longer statistically significant when the interaction term is accounted for. However, the interaction term between board connection and firm size is statistically significant at the 99% confidence level. Put differently, the board connection effects presented in Models 1, 3, and 4 are mostly driven by large firms. Thus, this result supports the second hypothesis of this study that firm size conditions the effect of board member linkages on FDI. Large firms with board connections have a particular advantage in promoting their FDI projects because of their political dominance in domestic lobbying.

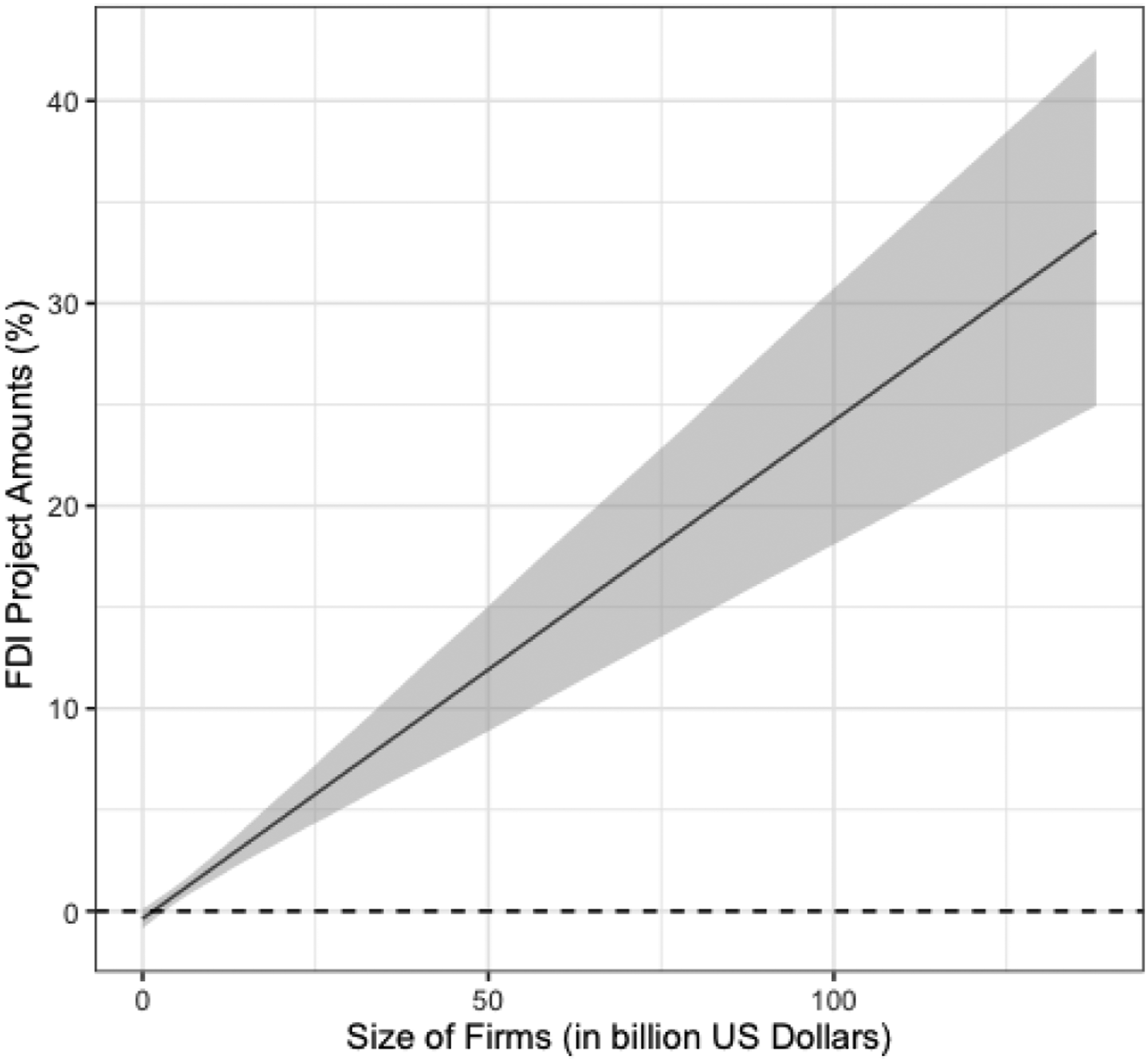

Figure 2 graphically shows the marginal effect of board connections on planned FDI volume conditional on firm size. The shaded area contains the 95% confidence interval for the marginal effect. Specifically, the figure shows that the marginal effect of hiring board members who had previously served in important positions at core financial institutions is notable, particularly for the largest firms. The strength of this effect is positively linked to firm size, demonstrating that board connections had a greater impact on the volume of FDI projects for larger firms. These substantive effects are large. For the largest firm with a market capitalization of USD $137 billion (i.e., setting size equal to Samsung Electronics), board ties to state-run banks increased the volume of FDI projects by 33%. However, for the smallest firm with a market capitalization of USD $4 million (i.e., setting size equal to the Kukdong Corporation), board ties actually had very little effect on the volume of FDI projects. Marginal Effects of Financial Board Ties on FDI Project Amounts. Note: The shaded area gives 95% confidence interval.

As a robustness test, I employ the number of announced investment projects as the dependent variable, instead of the amounts of those projects. Previous studies point out the possible measurement error when using data on the amounts of planned FDI projects due to the estimated values (e.g., Albino-Pimentel et al., 2018). 24 The robustness tests using the FDI project numbers are reported in Table A6 in the Supplemental appendix. Model 1 shows that board member connections have a positive and significant effect on the number of FDI projects. Model 2 shows firm size alone has a positive and significant effect on the number of FDI projects. Models 3 and 4 show that these relationships remain significant when these primary variables are included in the same model and after controlling for firm-level characteristics. Finally, Model 5 confirms that the significant effect of board connections is positively associated with firm size. 25

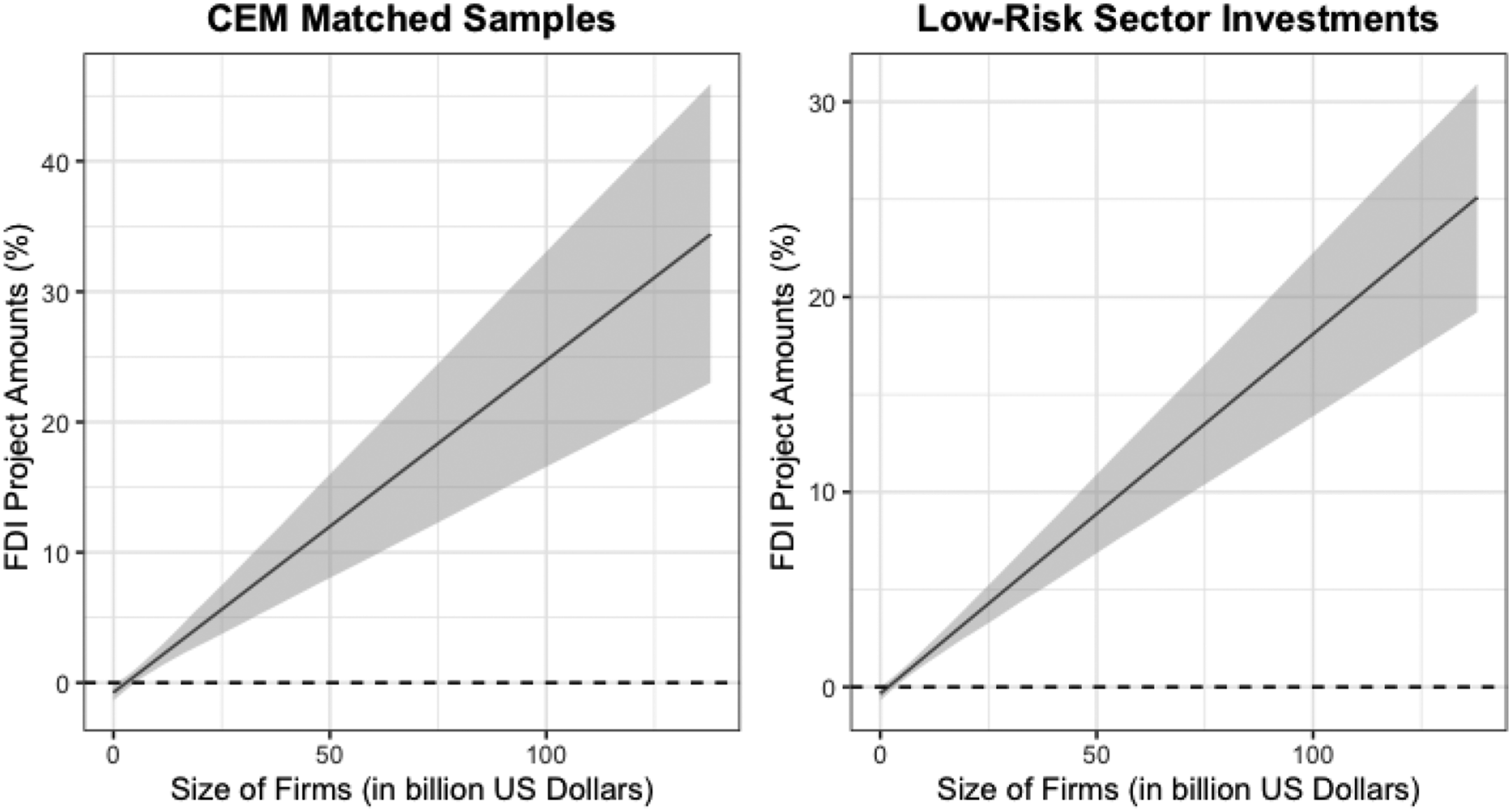

I conduct two additional tests. First, I conduct one in consideration of endogeneity bias. Firms that had financial board ties may have been systematically different from those that did not. An ideal estimate would compare firms with financial board ties to those without financial board ties, but which are otherwise identical. Thus, I use coarsened exact matching (CEM) methods to reduce the imbalance between firms with and without board ties by specifying confounding factors and matching firms with similar covariate vectors (Iacus et al., 2012).

Second, I try to alleviate concerns about reverse casualty, which in the context of this study is that the risk of FDI projects motivates firms to form board-member ties. Investment risks vary across sectors, and are greatest in those that tend to incur large sunk costs or are vulnerable to negative public sentiments. Colen & Guariso (2016) find that FDI in the natural resource extraction, utilities, agriculture, and real estate sectors are politically risky based on the fact that most investor-state dispute settlement cases brought to international dispute resolution bodies are in these sectors. Thus, it is plausible that within these sectors, firms are likely to form board membership ties to guard against these risks. By contrast, we are less likely to see such strategic board-stacking behavior in low-risk sectors.

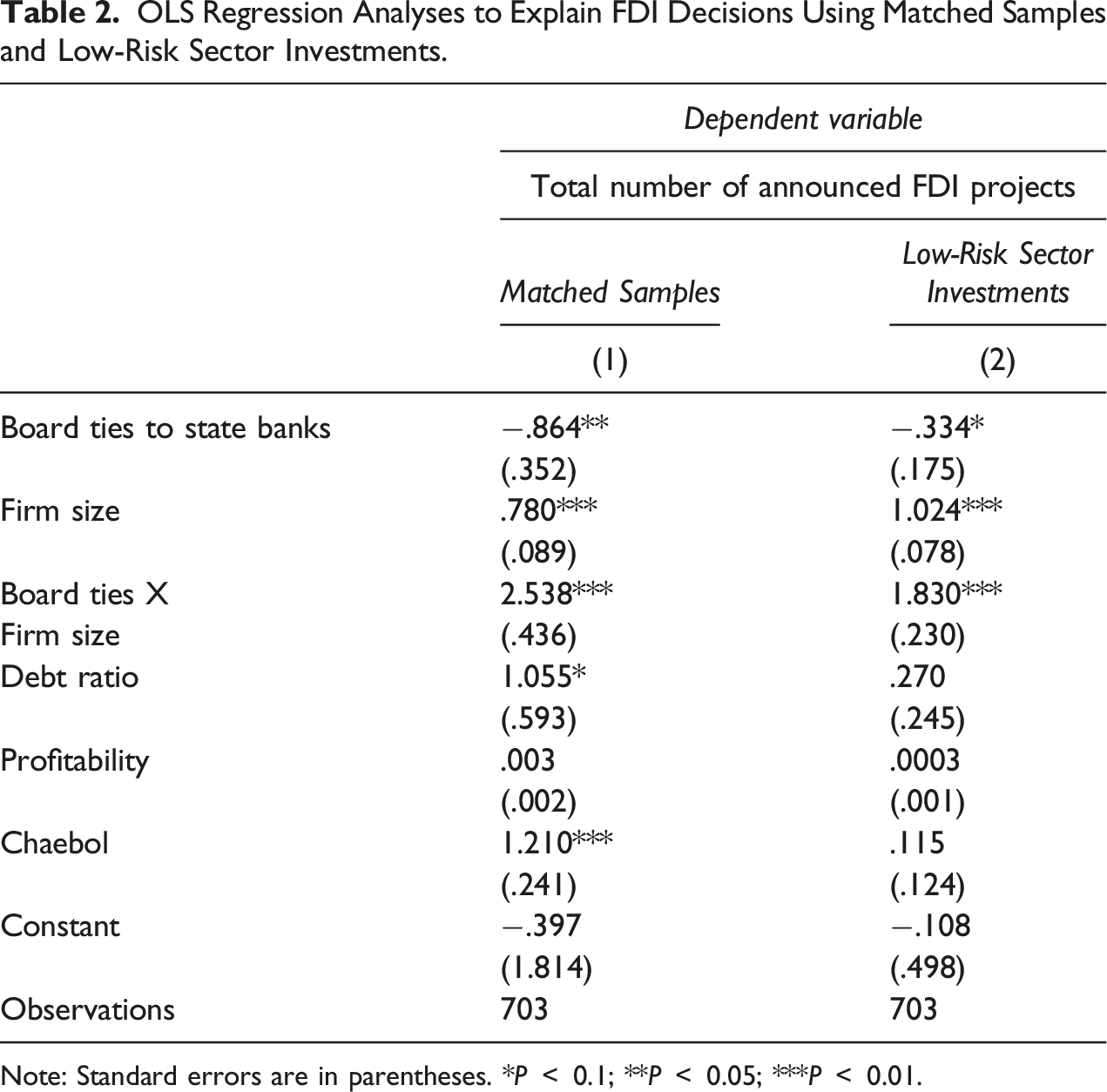

OLS Regression Analyses to Explain FDI Decisions Using Matched Samples and Low-Risk Sector Investments.

Note: Standard errors are in parentheses. *P

Figure 3 shows the marginal effects of the interactive terms between financial board ties and firm size in Models 1 and 2 (Table 2). The graphs show patterns similar to those observed with the main models. The left graph in Figure 3 shows that the marginal effect of board ties on FDI decisions is near zero for the smallest firms when analyzing matched samples. However, this effect becomes significantly positive and larger as firm size increases. Similarly, the right graph in Figure 3 also shows that the marginal effect of board ties is statistically different from zero and positive for large firms when analyzing investments in low-risk sectors, but approaches 0 for the smallest firms. The results confirm that larger firms are better positioned to increase their FDI volume by employing board ties than smaller firms. Marginal Effects of Financial Board Ties on FDI Project Amounts Using Matched Samples and Low-Risk Sector Investments. Note: The shaded area gives 95% confidence interval.

As further robustness checks, I probe for evidence of alternative political explanations. If other forms of political connections allow firms to get better access to state financing without having direct board ties to state banks, we would observe the same positive relationship between different measures of political ties and firms’ FDI volume. If it did not, then we would not observe that relationship, which would strengthen my argument that firms’ enhanced ability to engage in FDI was possible as a result of their board ties with state banks.

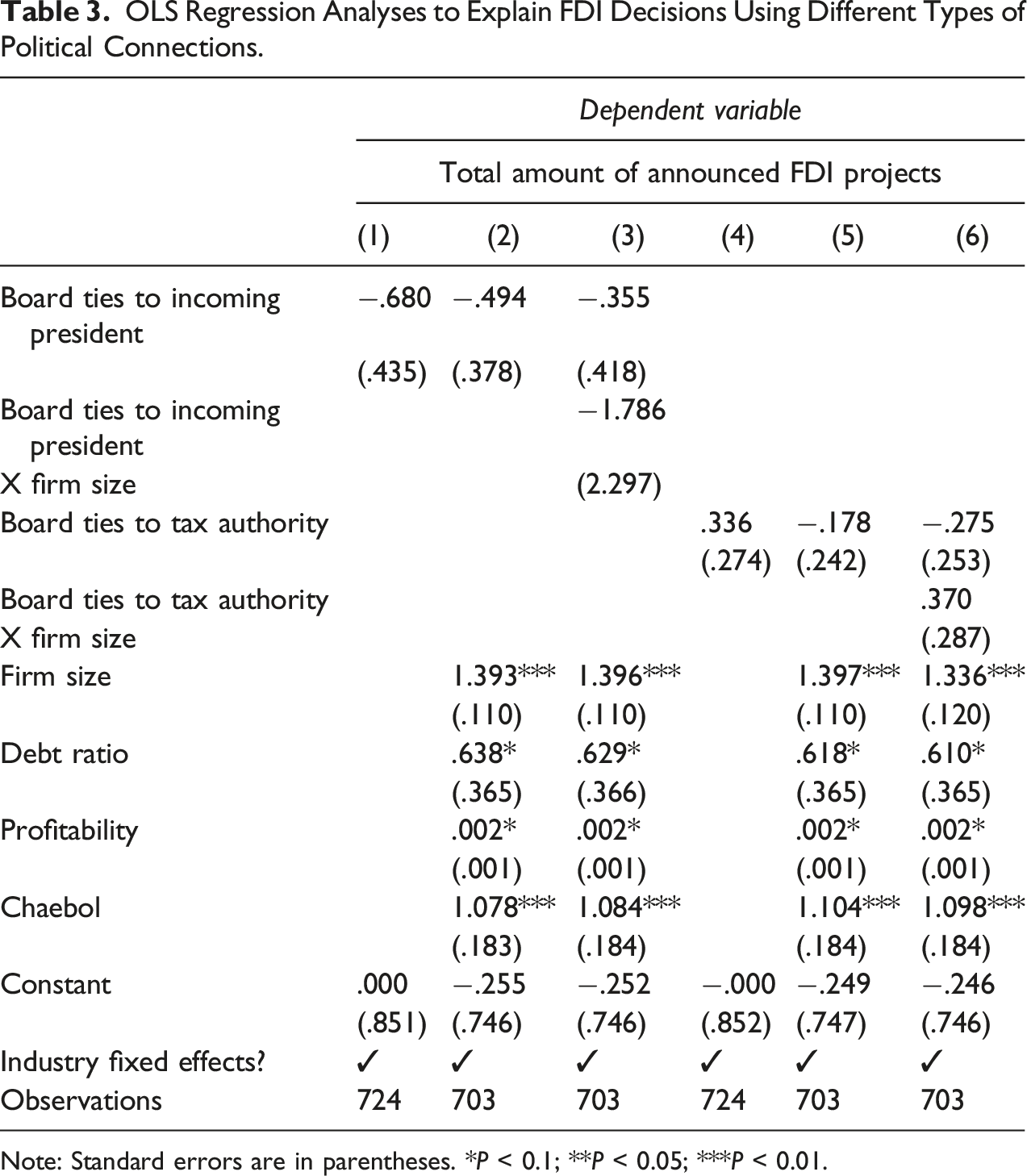

Thus, I design placebo tests by employing two different types of political connections. First, a major Korean election in 2012 resulted in the conservative New Frontier Party gaining the presidency with its candidate Park Geun-hye. Empirical evidence suggests that firms with political ties to the incoming president influence government policy (Jäger & Kim, 2019). Thus, the variable, “Board Ties to Incoming President” measures whether a firm had any political, social, or familial connections specifically with NFP candidate Park Geun-hye. For instance, Lee Hoon Kyu, a director of SK Innovation, was a member of the NFP party and Park Geun-hye’s close political ally. Furthermore, I capture firms’ board ties to the tax authority. Tax research shows that firms with political connections to tax authorities can escape government oversight or underreport their tax liabilities (Desai, Dyck & Zingales, 2007), which may improve their financial status. Thus, firms with such connections might be more qualified for getting bank loans. The variable, “Board Ties to Tax Authority,” captures whether a firm hired former tax officials onto its board. For instance, Kim Ki-joo is a director of Dongbu Corporation and he was previously a commissioner of a regional tax office. Overall, there were 24 and 65 firms, respectively, that were either connected to the NFP presidential candidate or the tax authorities. 26

OLS Regression Analyses to Explain FDI Decisions Using Different Types of Political Connections.

Note: Standard errors are in parentheses. *P < 0.1; **P < 0.05; ***P < 0.01.

In addition, I conduct robustness tests using different outcomes to alleviate concern over the fact that, if certain firms self-select into having financial board connections, then they may also be more likely to have better economic outcomes than other firms. Appendix Table 7 shows the results of regression analyses employing the same financial board connections variables but replacing the dependent variable with the rate of return on investments during 2012–2016. Similarly, Appendix Table 8 shows the regression analysis results when substituting income tax rates as the dependent variable. All of the results presented in Appendix Tables 7 and 8 show that the statistically significant effects of firms’ financial board ties disappear when using measures of firms’ return on investment and their income tax rates as dependent variables. These results suggest that firms’ financial board ties are not systematically related to firms’ economic outcomes, thus, further alleviating concerns about selection bias.

Although these sets of robustness checks alleviate concerns about endogeneity arising from reverse causality and selection bias, it should be acknowledged that firms may be strategic in the nature and timing of board-member placements. In other words, there may still be firms that place former officials on their boards because they plan to expand their FDI projects. Even if there is some reverse causal logic, the empirical reality is that firms with financial board connections engage in more FDI than those without such connections. The strong association between firms’ financial board connections and their increased ability to engage in FDI is striking because it is very consistent under different model specifications.

Conclusion

A growing number of studies reveals that there are clear winners and losers in globalization because the benefits of globalization are concentrated in the largest firms (Osgood et al., 2017; Osgood, 2017; Kim, 2017). We see the power of large firms under globalization via their promotion of trade liberalization (Baccini et al., 2017; Manger, 2012), frequent pursuit of trade disputes before the World Trade Organization (Davis, 2012; Ryu & Stone, 2018), influence over the World Bank’s lending decisions (Malik & Stone, 2018; Lim & Vreeland, 2013), and effective advocacy for strong international investment agreements (Allee & Peinhardt, 2010). This study shows that the largest firms can also increase their presence in global markets by gaining access to domestic financial assistance.

The empirical results of this study show that political and economic power is linked. Political connections that large firms have with the government provide these firms with greater access to financial resources, which allows them to pursue more FDI projects than other similarly sized firms without such connections. In short, the largest firms become more dominant in global markets by out-competing domestic rivals using political influence. Therefore, the beneficiaries of globalization may be even more highly concentrated than previously thought.

This research has an important implication for the FDI literature. Multinational corporations have been key actors in the growing fragmentation of production. When establishing supply chains across multiple countries, global firms decide whether to manufacture intermediate goods in house or to acquire them from other unaffiliated firms. The latter is less costly, but reduces firms’ bargaining power with the companies that they buy from. Thus, multinational firms’ organizational strategies may be driven by their domestic political ties. As discussed in this article, firms that are better able to reduce the costs and mitigate the risks of doing international business by cultivating domestic political ties may be more able to integrate their production processes and establish total control over their supply chains.

This study also makes several contributions to the comparative political economy literature. Developmental state model research has shown that strong government control over the financial sector can facilitate rapid economic growth (Kang, 2002). This study’s finding that the South Korean government provides financial support for FDI suggests that there is still a legacy of the developmental state in the South Korean political economy. The governments of other countries in East Asia that developed rapidly, such as Taiwan, Japan, and China, exhibit similar dynamics and could have a similar pattern of state financial backing for FDI. For example, Taiwan developed similar effective bureaucracies that maintain a strong control over economic planning (Cheng et al., 1998). We see a parallel revolving door appointment phenomenon in Japan, as exemplified by Amakudari (“descents from heaven”) (Colignon & Usui, 2018). Recent studies also show that Chinese bureaucrats have strong motivation to join corporate boards (Li, 2021) and Chinese firms’ FDI targets have been strongly influenced by the government (Stone et al., 2021).

Another of this study’s unique contributions is that it evaluates different types of political connections. Other studies have evaluated the value of specific ties such as familial, social, and political ties—but these studies generally focus on only one type (Acemoglu et al., 2016; Fisman, 2001; Goldman, 2008). However, firms may diversify their political strategies across institutional settings to mitigate political risks or increase the effectiveness of their lobbying (Hillman & Hitt, 1999; Hall & David, 2001). This study’s findings suggest that financial board-member ties are more effective at securing state financial resources than other types of political connections.

Future research building on this study might evaluate whether corrupt political connections can ultimately be harmful to a nation’s economy (Holcombe & Castillo, 2013). When firms without political connections realize that government support is not available to them, they may give up on seeking international business opportunities. In such an environment, firms would likely engage more in rent-seeking than improving elements of their competitiveness, such as innovation.

Supplemental Material

Supplemental Material - Personal Networks, State Financial Backing, and Foreign Direct Investment

Supplemental Material for Personal Networks, State Financial Backing, and Foreign Direct Investment by Seungjun Kim in Comparative Political Studies.

Footnotes

Acknowledgements

I am grateful to my advisor, Todd Allee, for his generous guidance. I thank Vincent Arel-Bundock, Inho Choi, Yoonbin Ha, Rebecca Hann, Virginia Haufler, Kai Jäger, Scott Kastner, Paul Lagunes, Jaehyun Lee, Erik Peinert, William Reed, and Sondre Solstad for their comments. The paper benefited from suggestions at the 2019 Midwest Political Science Association and the 2019 American Political Science Association annual meetings. I thank David Schoenherr and Terry Moon for their loan data.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: University of Maryland; Robert H. Smith business school, research funds.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.