Abstract

While COVID-19 has caused significant short-term disruptions in global value chains (GVCs), in the longer run, the pandemic will not be the primary catalyst in GVC evolution. As GVCs recover from the initial shock, managers will make GVC restructuring decisions guided by long-term strategic considerations. This article describes barriers that lead firm managers may encounter when rethinking location/control decisions for value chain activities and suggests that, in addition to structural changes, managerial governance adaptations are instrumental in enhancing GVCs’ long-term resilience. Lessons learned from responding to the pandemic can help managers enhance GVC efficiency in the increasingly uncertain global environment.

Keywords

Adopting internalization theory as our conceptual lens, we posit that lead firm managers will—in the long term—select, adjust, and retain GVC configurations that are the most efficient. 4 Importantly, shorter-term transient effects should not be mistaken for longer-term trends. As they recover from the initial shock caused by the sudden onslaught of the pandemic, managers are likely to make decisions about GVC restructuring guided by long-term strategic considerations. GVCs consist of a constantly evolving network of actors, and GVCs survive when they are continually able to adapt to multiple socio-economic environments and market conditions. The pandemic represents an admittedly significant and globally pervasive shock, but the key advantage of a GVC over a vertically integrated firm is that the network involves a multitude of different actors, and it is therefore designed with a certain degree of resilience to overcome exogenous events, even in instances where individual firms within the GVC (be it the lead firm or its suppliers) may not be so resilient.

Large-scale global crises and disruptions are not uncommon and have included earthquakes, tsunamis, nuclear disasters, and global financial meltdowns. However, COVID-19 has delivered a broader, more intense, and prolonged shock to today’s GVC economy and has created acute awareness that future crises are unpredictable, yet inevitable. As a result, we expect that lessons learned from responding to the pandemic can be useful for addressing a more generic set of future challenges and that much of the post-COVID governance adaptations will be aimed at building resilience into GVCs to safeguard against future shocks.

We analyze the prevailing GVC trends, which have been either intensified or induced by COVID-19, with the objective of identifying managerial responses that are likely to generate the most value for GVCs and increase longer-term GVC resilience to external shocks. Our core argument builds on distinguishing between structural GVC governance, such as the ownership, control, and location of GVC activities (i.e., the what, where, and who decisions) and managerial governance—namely, “more fine-grained mechanisms within a broader governance structure, some of these being relational in nature, that encourage repeated, observable patterns of behavior by targeted units and individuals” (i.e., the how decisions). 5 To date, most of the scholarly discussion on GVC’s response to the pandemic has focused on large-scale changes in location and control of value chain activities; however, finer-grained governance changes that do not involve these two dominant GVC variables are equally important. The raison d’être of the GVC requires the continual refining of strategies in intra-GVC collaboration with suppliers and other stakeholders, the sharing of knowledge, and maintaining the flexibility needed in order to upgrade GVC competences—in other words, activities that belong to the domain of managerial governance. The emphasis on managerial governance represents a dynamic take on GVC reconfiguration and the essential interdependence between the lead firm and suppliers, whose role continues to evolve.

Internalization Theory and GVC Governance

Internalization theory posits that economic actors select and retain the most efficient governance mechanisms to organize economic exchange. 6 In the context of a GVC, this means that, over the long term, lead firm managers and their strategic partners will make decisions about the structure and strategy of the network in a way that results in the most efficient, economizing mix of internal and external contracts and locations. Efficiency 7 is achieved by aligning governance decisions with attributes of transactions (such as micro-level attributes, including individual characteristics of decision makers involved, as well as macro-level attributes, including technological, institutional, geographic, cultural characteristics of relevant environments, and industry features). Efficient governance is defined as a system that is comparatively superior at allowing the lead firm to: economize on bounded rationality of all actors involved in transactions 8 ; economize on bounded reliability 9 ; and create a context conducive to value creation in the network. 10

Importantly, GVC efficiency is served through both structural governance decisions—that is, decisions on who performs which transactions, who owns or controls activities, where activities are performed, and how the network is organized—and managerial/strategic governance decisions, namely, decisions pertaining to learning and knowledge transfer in the GVC, relationship management, resource recombination, contractual details, coordination and monitoring, and other managerial routines/practices deployed within the GVC. The latter are less observable, more difficult to measure, and, consequently, less prominently featured in international business literature 11 —however, we argue that it is the managerial governance responses that are likely to be instrumental in enhancing GVCs’ long-term resilience.

From an internalization theory perspective, the pandemic triggered macro-level shifts in both home and host countries, requiring lead MNEs to adapt their governance choices to respond to new internal and external drivers and constraints, including resource constraints, work environment changes, supply disruptions, demand fluctuations, regulatory restrictions, and home country pressures for supply chain sovereignty. However, as the long-term impact of the pandemic unfolds, the efficiency of extant governance tools will be tested. If the adjustments prove inefficient—that is, if they restrict information flows (create bounded rationality challenges), fail to secure commitments (create bounded reliability challenges), and inhibit innovation and value creation in the network—lead MNEs will correct them by engaging in further governance adaptation and by introducing comparatively more efficient governance practices. 12 That is, governance adaptations (both structural and managerial ones) implemented to deal with the immediate disruptions associated with COVID-19 will only be retained if they continue to be aligned with the lead MNE’s and suppliers’ internal and external contexts.

It is important to stress that contemporary internalization theory does not equate efficiency with the least sum of transaction costs at a given moment in time. Efficient governance refers to a system of structural and managerial tools that allows the GVC to operate in a cost-effective, reliable, and value-enhancing way. This means that, in order to achieve long-term GVC efficiency, certain short-term sacrifices to cost effectiveness may need to be made, for example, by investing in supplier development and capability upgrading, sharing an equitable proportion of value with partners, and/or maintaining slack resources. 13 The disruptions associated with the pandemic have shined a spotlight on reliability as a particularly salient factor of the efficiency bundle. GVC governance adaptations will therefore include structural changes and managerial routines to enhance lead firms’ economizing and value creation capacity. 14 These adaptations, however, started over a decade ago, as a response to a “new normal” 15 business environment resulting from socio-political, institutional, and technological developments.

GVC Reconfiguration Trends: A Brief History

In the past few years, we have witnessed significant restructuring and reshaping of the global economic system, 16 with a number of interrelated macro-level forces affecting GVC governance. These forces have been identified in recent GVC research as geopolitical tensions, renewed protectionism, growing costs of doing business in emerging markets (i.e., increasing labor and transportation costs, as well as costs of compliance), increased pressure for social and environmental regulation compliance/full chain responsibility, and digitization and automation. 17 Together, these trends have created substantive risks to GVCs, whose very existence was enabled by liberalization and deregulation of international trade. 18 However, these macro-level developments also presented new opportunities for coordination and control of dispersed activities through continued technological transformation. 19

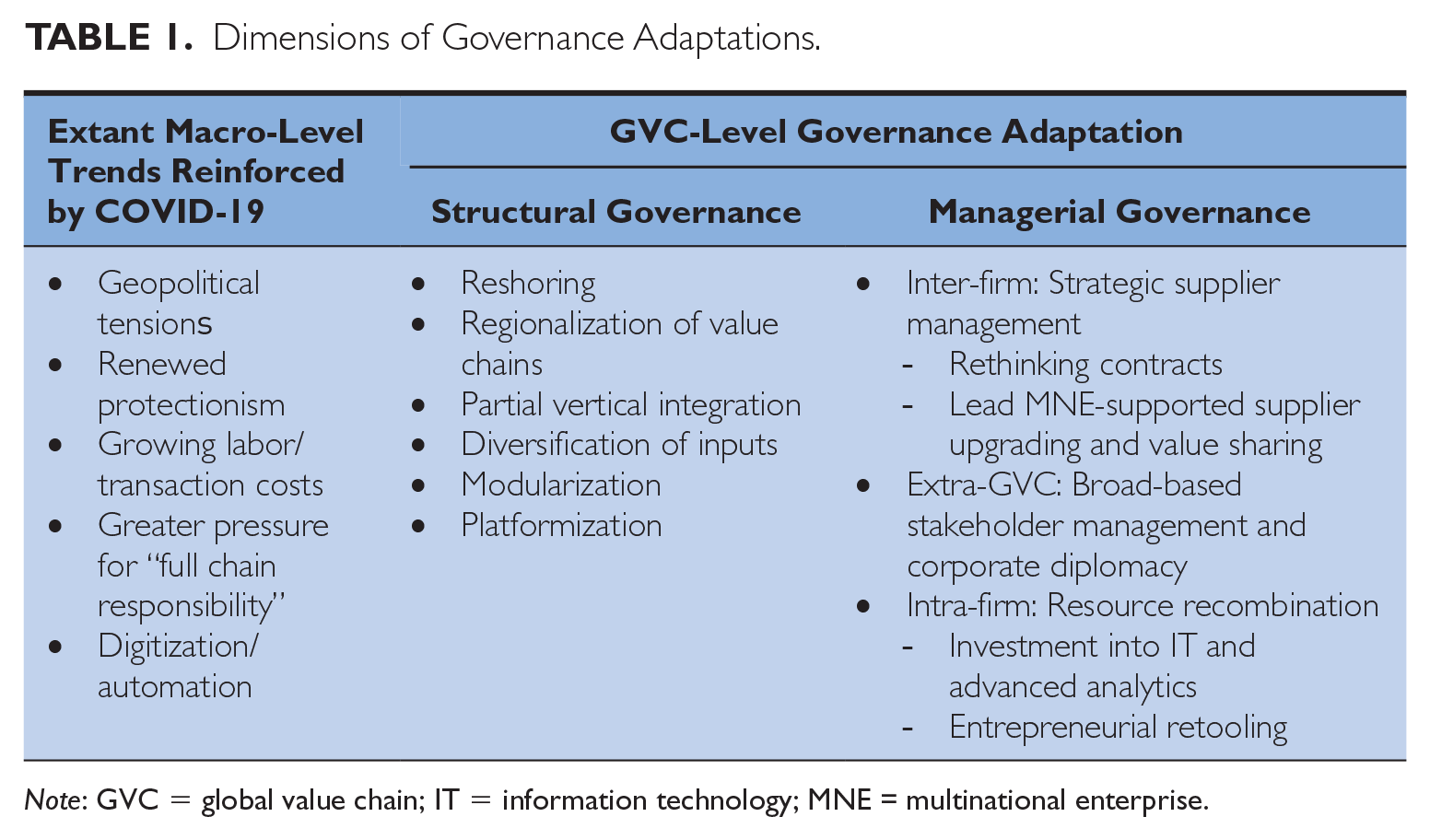

Over time, lead firms have responded by structural changes to their GVCs so as to maintain efficiency in the face of macro-level shifts: reshoring and retreating from global to regional geographic scope 20 ; vertically integrating (at least partially) in an effort to control quality and ensure compliance with sustainability requirements 21 ; and diversifying manufacturing locations to lessen dependence on markets such as China. 22 These reconfigurations have been partially enabled by technological advances and data sharing. Advanced labor-saving technologies acted to change the locus of production and permitted lead MNEs to substitute capital for labor, leading to production shifts away from low-wage countries. 23 Enhanced connectivity made GVCs more localized, fragmented, modularized, and closer to end users. 24 New technologies also facilitated platformization, whereby lead MNEs rely on digital technology for their business models. 25 Dominant macro-level forces and associated GVC responses are summarized in Table 1.

Dimensions of Governance Adaptations.

Note: GVC = global value chain; IT = information technology; MNE = multinational enterprise.

While these trends pre-dated the pandemic, it has been argued that COVID-19 has created significant supply and demand disruptions, accelerated de-globalization of trade, and, consequently, will precipitate the above-mentioned pre-existing GVC reconfiguration trends geared toward greater risk aversion, supply chain sovereignty, and, more generally, limited globalization. 26 There are, however, caveats associated with this prediction.

First, the ability of lead MNEs to implement efficiently such ownership and location changes is tempered by a number of significant barriers. Efficient reshoring, for example, requires access to specialized knowledge and manufacturing infrastructure, which may not be readily available. In fact, few locations possess the right combinations of skill, infrastructure, low wages, and scale capabilities. Learning from the examples of organizations that have tried to make structural GVC changes and failed is important. For instance, when Apple Inc. announced its plan to move some of the manufacturing and assembly of computers out of China and back into the United States around 2012, the company—very soon after going forward with partial reshoring—found that skill shortages and infrastructure limitations made reshoring ultimately inefficient, particularly for differentiators such as Apple, which often rely on the ability of suppliers to quickly produce vast quantities of custom parts. 27 Sustained industry-wide outsourcing to lower-wage locations over a long period of time has seen a reduction in home market capacity, which is difficult to reverse in the short term.

Second, the magnitude of risks created by macro-level shifts differs across industries, as does the lead MNE’s ability to adapt its GVC structure in response. These risks are particularly salient in labor-intensive manufacturing GVCs, where lead MNEs rely on efficiencies of offshore operations in low-cost countries. Lead MNEs in these industries, such as textiles and apparel, have been gradually shifting production away from China to countries such as Bangladesh, Vietnam, Ethiopia, and Turkey, 28 in response to rising labor costs 29 in China, and the emergence of skilled low-cost suppliers outside of the Chinese market. However, geographic reconfiguration can be financially prohibitive in capital-intensive GVCs, which are characterized by significant, irreversible capital investments made over a number of years. Relocation is also challenging in knowledge-intensive GVC activities (e.g., R&D, marketing) tied to specialized skills residing in particular suppliers and/or locations providing differentiated outputs that are not so easily replaced. Similarly, GVCs operating in extraction or natural resource-intensive industries will find relocation difficult given the location-boundedness of the resources sought. 30 GVCs tied to product markets in host countries are also difficult to reconfigure. For instance, lead MNEs in automotive GVCs are bound by “obligated embeddedness” 31 in fast-growing emerging markets (notably, China), whereby governments pressure MNEs to set up local operations in order to serve these markets. 32

Admittedly, the pandemic reinforced the ongoing macro-level shifts and introduced new, immediate shocks. Restrictions on travel and transportation, along with the physical closure of businesses, led to sudden and severe supply bottlenecks. Global demand patterns shifted, partially reinforcing supply-side shocks. 33 Demand for non-essential consumer goods and services that require in-person contact fell, while demand for essential everyday commodities, from food and cleaning supplies to toilet paper, rose dramatically. 34 Shortages in medical and personal protective equipment also ensued. Yet, GVC-level barriers to structural reconfiguration remain even in the face of these unique disruptions. Simply put, factory closures in China due to COVID unsurprisingly led to supply disruptions for many companies; yet, despite these disruptions, companies such as Apple, for instance, do not have the capability to efficiently reshore production in 2020 any more than they did in 2012 when first attempting to reshore.

Policy reactions by home and host governments—such as new trade and investment restrictions or incentives to localize production of strategic supplies—do not remove barriers to efficient changes in ownership and location of activities. In strategic industries—renewable energy, dual-use (military and civil) technology, computing and artificial intelligence, as well as pharmaceuticals and medical equipment—some vertical integration and reshoring may be attempted, following national security requirements of lead MNEs’ home countries. But structural reconfigurations are costly, and thus they beg the all-important question of “who” is going to cover the additional costs. 35 For example, repatriation and internalization of geographically dispersed pharmaceutical GVCs are hardly feasible, despite pressure and incentives by governments to increase domestic production of key pharmaceuticals and medical equipment. 36 Where relocation and internalization are costly and lengthy—such as in pharmaceutical GVCs—vertical integration and reshoring may stall and disrupt the supply of critical goods to the domestic economy and thus fail to serve the greater “common good” purpose it was meant to accomplish. Case in point, PhRMA, an association of American pharmaceutical researchers and manufacturers, is pushing back against the pressure to shorten and localize pharmaceutical value chains, citing tremendous cost and time requirements for setting up new pharmaceutical facilities, which would likely result in inefficiencies. PhRMA puts forward a strong argument that attempting to reconfigure well-established, technologically complex pharmaceutical GVCs may in fact disrupt, rather than secure, the supply of medicine to the United States and to the rest of the world. 37

Lead MNEs may seek to safeguard against large-scale future bottlenecks by lessening their dependence on dominant suppliers or locations. GVCs that are not tied to particular supplier capabilities will likely become even more fragmented. This fragmentation will, in turn, create orchestration challenges. Fragmented and specialized GVCs are often more efficient but may also be more fragile in times of crisis, particularly when challenges to cooperation are posed. From an internalization theory perspective, only efficient structures are sustained over time: if predicted reconfigurations offset the gains derived from operating a GVC, they will not last. How, then, can lead MNEs increase the robustness and resilience of their GVCs to prepare for likely future disruptions and to respond to increasingly nationalist government policies?

We propose that, in instances where structural GVC reconfigurations are not economically feasible, lead firms can engage in managerial governance adaptations, which provide a “countervailing force” 38 to GVC disruptions introduced by exogenous trends and reinforced by the pandemic. Such adaptations target managerial processes associated with intra- and extra-GVC economic exchange and may include, inter alia, rethinking of contract details, upgrading of competences, redirection of knowledge flows, entrepreneurial initiatives, and changes in relationship management. 39 Unlike structural changes—whose feasibility depends on various external factors, including institutions, industry structures, and supplier capabilities—managerial governance adaptations are within lead firm managers’ control, are potentially equally efficient in various types of GVCs, and may prove instrumental in reducing disruptions and increasing GVC resilience.

GVC Governance Post-Pandemic: Managerial Governance Adaptations

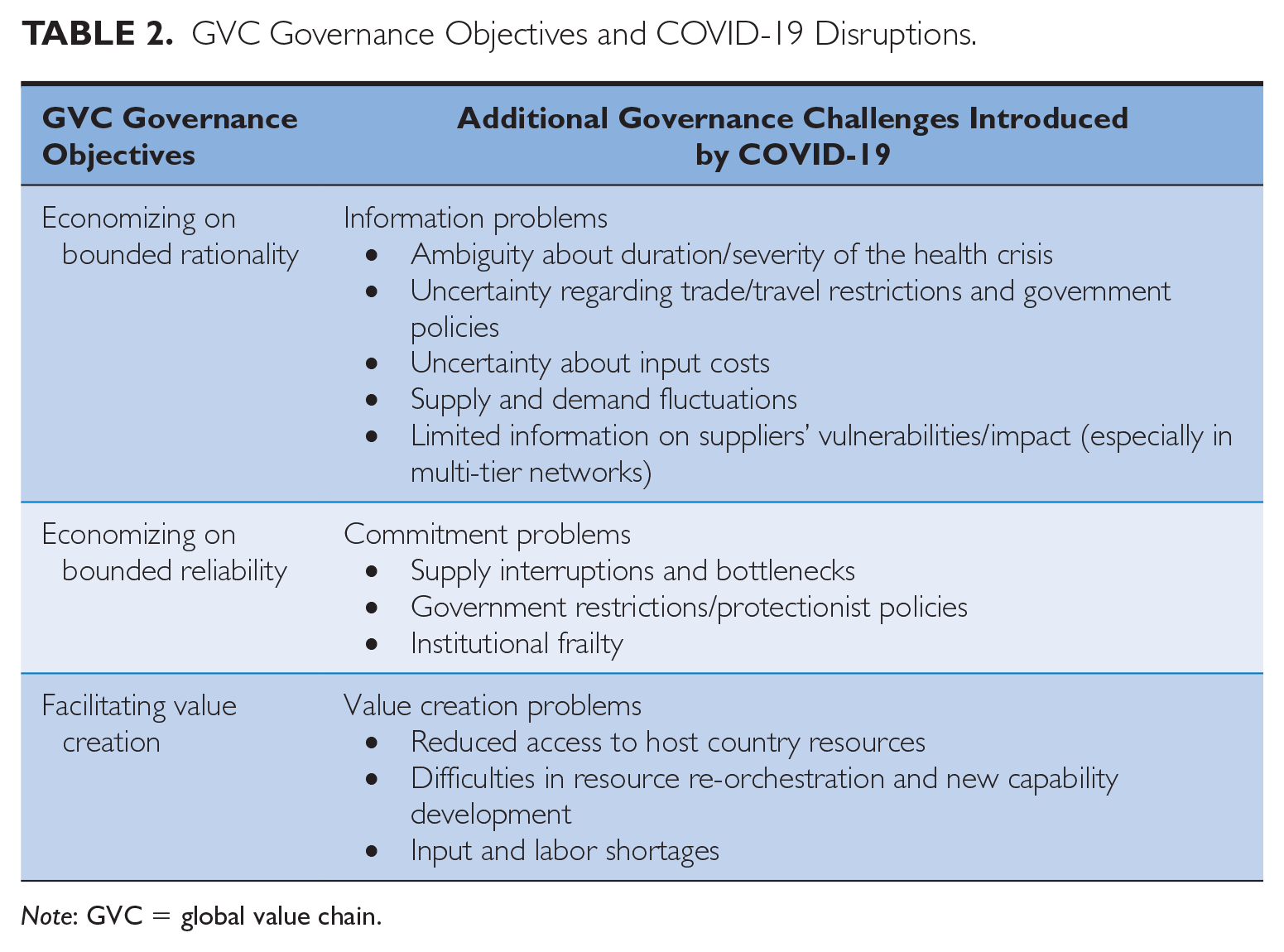

As mentioned above, efficient GVC governance is defined as a set of routines and practices that reduce bounded rationality and reliability and facilitate value creation in the network. The pandemic has introduced additional governance challenges that can be characterized along these three dimensions of efficiency: information problems (continued ambiguity about the global health situation, uncertainty regarding trade and travel restrictions); commitment problems (supply bottlenecks, protectionist policies of governments, increasing institutional frailty); and associated value creation problems (reduced access to resources outside of home country, inability to deliver value to customers due to trade interruptions and labor shortages, lack of capabilities to address shifting demand). 40 Lead firm’s governance objectives and associated governance challenges introduced by the global pandemic are summarized in Table 2. We propose that in order to build resilient GVCs, lead MNEs need to implement governance adjustments that best address these new efficiency challenges.

GVC Governance Objectives and COVID-19 Disruptions.

Note: GVC = global value chain.

It should be noted that managerial governance adaptations are not specific to crisis situations. Lead firms in GVCs are tasked with choosing the most suitable governance mechanism for each fine-sliced value chain activity. Here, decisions on requisite changes in location and control are necessarily accompanied by managerial adaptations that best support each activity set and allow the head office to effectively coordinate, monitor, and integrate internalized and outsourced activities. It has been argued that managerial routines that facilitate knowledge sharing, collaborations, entrepreneurial resource orchestration, and flexibility are critical for the GVC’s sustainability over time and for the lead firm’s ability to maintain its central position in the network. 41 These managerial routines become particularly important in the post-pandemic environment, where links connecting various dispersed GVC actors are disrupted. The value of managerial governance is further amplified when responding to disruptions through structural reconfigurations (i.e., ownership and location changes) is not feasible.

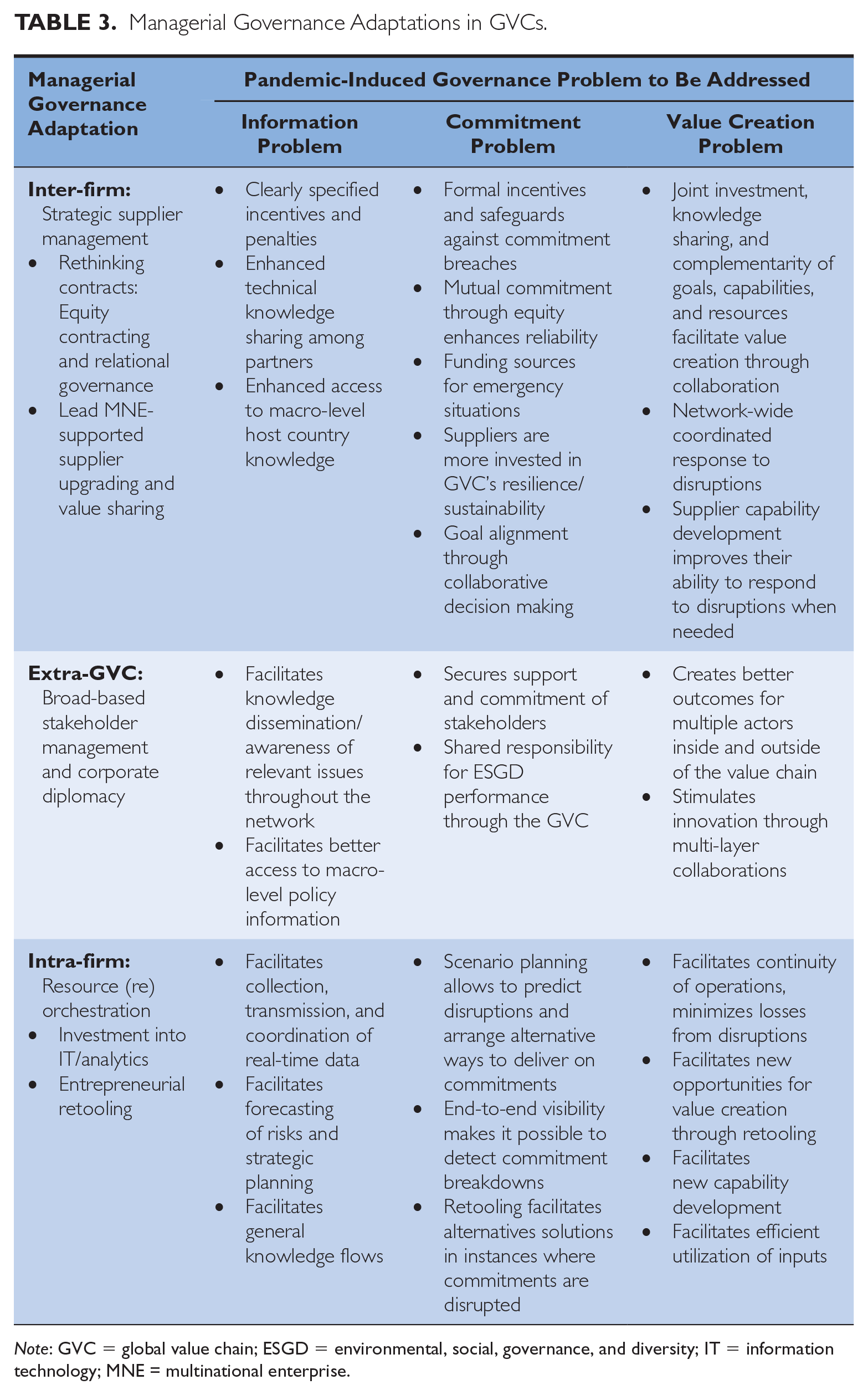

We discuss proposed managerial governance mechanisms relevant for post-pandemic GVC orchestration below. Our process for identifying these managerial government adaptations was twofold. First, we surveyed extant research on GVC governance, with a focus on identifying managerial governance routines deployed by lead firms for network orchestration. 42 Second, we assessed these governance mechanisms based on their capacity to address efficiently the information, commitment, and value creation problems introduced by the global pandemic. We classified the resulting managerial governance mechanisms into three groups: inter-firm adaptations (those pertaining to relationships among GVC actors); extra-GVC adaptations (those pertaining to relationships with actors outside of formal GVC boundaries); and intra-firm adaptations (those pertaining to routines, processes, and decision rules inside the lead firm). 43 The results of this analysis are summarized in Table 3 and presented below.

Managerial Governance Adaptations in GVCs.

Note: GVC = global value chain; ESGD = environmental, social, governance, and diversity; IT = information technology; MNE = multinational enterprise.

Inter-Firm Managerial Governance Adaptations: Strategic Supplier Management

We know by now that a lead firm’s GVC network is multi-tiered and can consist of hundreds of Tier 1 suppliers (which have a contractual relationship with the lead firm), as well as hundreds or even thousands of sub-tier suppliers that Tier 1 firms manage. Beyond Tier 1 (and to a degree, Tier 2 suppliers), lead MNEs rarely know who their sub-tier suppliers are, how resourceful they are, and, implicitly, how reliable they are in times of disruption. The pandemic highlighted that lead firms did not have reliable information as to where their Tier 1 suppliers sourced the critical parts or materials from, whether those suppliers were clustered in a single affected area, and whether there were even viable substitutes for current suppliers in other locations. 44 Some lead firms in buyer-dominated GVCs may indeed opt to become more vertically integrated to reduce the risks associated with loss of value chain control. When vertical integration is not feasible, lead firms may achieve easier coordination and monitoring by re-evaluating contractual relationships with suppliers, strengthening relationships among strategic partners, and investing in key strategic suppliers’ capabilities and resources.

Rethinking contracts: Equity contracting and relational governance

Presently, most offshore production is managed through non-equity contracts. 45 While non-equity contracting will likely continue, firms may need a greater reliance on equity and the associated use of formal orchestration tools—such as contracts that clearly specify price incentives and penalties—to incentivize suppliers and safeguard against potential commitment breakdowns in case of external shocks. Equity-based contracts provide lead firms and their strategic partners with clearly specified and legally enforceable options for monitoring and controlling GVC relationships. Equity investment also signals a deep commitment to the relationship and thus enhances partners’ reliability. Importantly, equity contracting implies partners’ commitment to contribute funding in emergency situations in case of future disruptions.

While equity-based contracts provide an attractive incentive for commitment fulfillment and productive collaboration, we recognize that they are not 100% efficient under conditions of high uncertainty—for example, in institutional environments where contracts are poorly enforceable despite the lead firm’s best efforts, 46 and/or in situations where external ambiguity and task complexity make elaborate contracting highly complicated. It would therefore be difficult for lead firms to design contracts when there is ambiguity and uncertainty around the nature of the relationship between the firm and its partners (which explains the vague contract language often used between lead firms and their partners). 47

Here, relational governance can act as either a substitute or complement to formal contracting. Scholars have argued that relational contracting will play a prominent role in the post-pandemic environment, fueled by increased institutional frailty, perceived volatility of commitments, and associated need for greater safeguards. 48 Lead MNEs can engage in informal relationship building throughout the network to a greater extent to secure commitments and increase the amount and quality of knowledge exchanges, thus stimulating innovation and flexibility. Deeper and more meaningful relationships among partners 49 may also help the lead firm close information gaps related to changing trade and investment environments in host countries. Close relationships within the GVC can be particularly helpful when quick, coordinated action is needed in response to disruptions. For example, Procter & Gamble created cross-functional teams to engage in “joint innovation” with several of its suppliers 50 ; the rationale was to generate value by leveraging the skills of employees as well as partners, in order to develop new ideas, identify other external partnership opportunities, and create more interaction between business strategy and the operational activities of the company.

Lead MNE-supported supplier upgrading and value sharing

Supplier upgrading refers to the development of branding capabilities, technological catch-up, and/or progression from original equipment manufacturing (OEM) to original design manufacturing (ODM) and own brand manufacturing (OBM) by peripheral GVC actors typically located in emerging economies. 51 New supplier capabilities, such as moving into manufacturing of more sophisticated product lines and using superior technologies to transform inputs into outputs, can potentially benefit lead firms, especially those competing on quality rather than cost. Yet, to date, the main drivers behind supplier upgrading have been related to macro-level forces such as market conditions and institutional environments, 52 with lead firms playing a secondary role in spurring supplier upgrading initiatives (with several notable exceptions, e.g., lead firms in automotive industries purposefully facilitating auto parts supplier upgrading). 53 Part of the reason for lead firms’ passive role in supplier upgrading is their reluctance to relinquish control over critical knowledge, generally out of fear that suppliers may use that knowledge to move up the value chain and challenge the dominant position of the lead MNE, either displacing the lead firm or, over time, becoming its direct competitor. 54

The COVID-19 pandemic has shown that suppliers may be inertial and path-dependent when responding to the crisis, mainly because they lack the technological capabilities and orchestration know-how needed to efficiently deal with unpredictable disruptions. 55 In the post-COVID era, a lead firm may benefit from adopting a “developmental” GVC governance structure 56 to avoid the inefficiencies that come with supplier inertia and lack of competence to manage disruptions. In the manufacturing industry, late deliveries can mean that lead firms have to pay additional overtime or credit customers for delays experienced (if lead firms are to enact penalties, as often suggested, 57 that would probably bankrupt some of the suppliers in the developing world). Hence, a more active role in facilitating supplier learning entails investing in common use of technology, active knowledge transfer and training, assigning MNE staff to offer support to suppliers in a similar manner in which the lead MNE would support its own units, and promoting collaborative decision making. Some lead firms have been successfully invested in collaborative supplier strategies for many years. For instance, IKEA managers share business intelligence, managerial practices, and business policies with their network of suppliers located in China and South-East Asia in order to stimulate technological upgrading and innovation in their value chain and help less-efficient and less-experienced partners become more competent. 58 These adjustments have proved efficient because they increased value creation within the company’s supplier network.

Another example is ASML, a lithography equipment manufacturer for the semiconductor industry, which developed what the company refers to as a “value-sharing” mechanism with its suppliers. 59 The company allows suppliers to maintain healthy profit margins (which act as a volatility buffer), finances part of the infrastructure required to produce new products, and offers purchase guarantees. The strategy to value-share with suppliers led to suppliers prioritizing the lead firm’s business, reduced costs and lead times, and offered stability in an industry where product lifecycles are relatively short and demand is unstable. We would therefore expect benefits from an increase in such supplier management practices in situations when GVC resilience is threatened (i.e., during and after the pandemic), particularly in markets that are of key strategic importance for the lead MNE. This requires further commitment from the MNE and its suppliers, who may then take more formal and informal responsibilities to ensure the long-term resilience and sustainability of their GVCs.

Extra-GVC Managerial Governance Adaptations: Broad-Based Stakeholder Management and Corporate Diplomacy

Lead firm MNEs are under tremendous pressure from a variety of stakeholders—NGOs, international organizations, regulators, consumers, the media, and the general public—to enhance GVC performance in terms of environmental, social, governance, and diversity (ESGD) parameters. 60 The pandemic has exacerbated these pressures by drawing the public’s attention to societal issues in different locations and shining a spotlight on MNEs’ potential wrongdoings, such as unfair working conditions and discrimination. We note that the COVID-19 pandemic has had a disproportionately negative effect on workers in less-developed countries, where lead firms and their Tier 1 suppliers already experienced issues with environmental and labor standard violations. One particularly notable example is Bangladesh, where many garment factories were closed until further notice, as retailers (e.g., Gap, Zara, and Primark) canceled or suspended their orders and stopped placing new orders to avoid further losses from sales decline. 61 In these locations, the pandemic has triggered either mass unemployment, rising inequality, or exposure to the virus due to poor working conditions. 62 Labor groups and local institutions will expect companies to keep at least some of their investment in these factories, and to adhere to strict safety protocols once reopened.

The pandemic may well become a catalyst for achieving better working conditions throughout the GVC. Research 63 suggests that social restructuring brought about by crises offers an opportunity for MNEs to become more strategically involved with local actors and contribute to recovery efforts, thereby building legitimacy and consolidating local market acceptance.

In fact, an independent study conducted by Morgan Stanley Capital International also found that, all else considered, firms with stronger ESGD practices suffered less during periods of crisis. 64 Perception of social irresponsibility in any part of the GVC may damage the reputation of the lead MNE, which is increasingly seen as accountable for the behavior of the entire network. 65 On the other hand, lead MNEs will benefit from positive reputation effects if they and their partners are seen as contributing, in a meaningful way, to pandemic-fighting efforts and post-pandemic social and economic recovery. Sustained goodwill achieved through positive engagement with stakeholders can also help during difficult times, whereby communities and customers rally behind a firm seen as a good corporate citizen.

What does this mean for the lead MNE management? This implies that a GVC must be managed in a way in which activities align with the interests of all affected stakeholders, beyond the lead firm and its subsidiaries. 66 Lead firms should employ targeted, systematic, and professional corporate diplomacy strategies to engage relevant stakeholders, 67 including government, research, educational, political, financial, and social institutions. Historically, close links to non-market stakeholders have helped lead firms respond to policies around social and economic development in host countries, promote innovation, develop new capabilities, and build local market legitimacy and reputation. 68 These connections will remain highly valuable post-pandemic, particularly ties with home and host country regulators who have the relevant information and the power to shape local, national, and international responses to external shocks (i.e., through lock-downs, restrictions on travel and trade, as well as business subsidies/support packages). 69

In certain cases, cooperation with non-market stakeholders outside of the MNE’s immediate value chain can lead to large-scale, multi-layer collaborations with significant, positive global outcomes. For instance, the global efforts to fight the pandemic have already resulted in international R&D collaborations to accelerate the development of medical equipment, therapies, and vaccines. 70 Such collaborations involve multiple layers of stakeholders, including lead MNEs, hospitals, research institutes, and various levels of governments, with the World Health Organization acting as a global hub to centralize and properly channel relevant knowledge. Ultimately, collaborations facilitate the use of underutilized resources and efficiently redirect knowledge, which is critical in times of crisis and disruption. We therefore propose that large-scale cooperation and knowledge sharing, if replicated and taken onboard by lead firms in a variety of industries, may enhance GVC resilience in the long term.

Intra-Firm Managerial Governance Adaptations: Resource Recombination

GVCs’ raison d’être, as stated in our introduction, is the continuous re-evaluation of governance, with the goal of achieving maximum efficiency for the entire network of fine-sliced activities. This means that lead firms must simultaneously allocate and recombine resources across product and geographic space, while reconciling global pressures with local priorities, and macro-level dynamics with internal resources and capabilities. 71 The pandemic has highlighted the role of resource recombination and has shown that GVCs with lead firms that were able to quickly reallocate resources to address sudden supply and demand shifts experienced less disruption than GVCs with lead firms adopting “wait and see” strategies. 72 Furthermore, lead firms that invested significantly into advanced technology were (and will remain) in a better position to implement successfully such resource shifts. 73

Investment in Information and Analytics

Lead firms can manage risks associated with external shocks by increasing investment into advanced analytics (e.g., AI, natural language processing) so as to predict disruptions, anticipate impacts on value chain activities, and map out responses (e.g., identify potential bottlenecks, replace high-risk suppliers, reroute supply and distribution channels, re-organize logistics, and/or build additional capacity into operations). There are examples of firms whose GVCs have proved more resilient as a result of having predictive analytics mechanisms in place. For instance, General Motors invested significant resources over the years in mapping its GVC in order to understand how and when inputs turn into outputs, and where each supplier and each activity is located. 74 When disruptions take place, the company has greater visibility of its value chain and is therefore better able to understand in real time which areas are likely to be affected and how the end product may be influenced. Furthermore, with this information, a lead firm is much more flexible, because it is able to establish inventory; book alternative locations for production and assembly; effectively communicate with onsite workers, suppliers, and carriers; and offer substitute products to customers quicker than its competitors, thus overcoming potential bounded reliability issues. In the same vein, Toyota invested in improving supply chain resilience by creating a database that can be used to visualize supply networks for each component. 75 In turn, Procter & Gamble has what the company refers to as a control tower system, which offers comprehensive information about its geographies and products; this system integrates real-time data on lead firm and partner locations, including any disruptions associated with road delays, weather conditions, and inventory levels. 76 When disruptions do occur, the system can rapidly analyze the data and find alternative solutions to supply disruptions in a matter of minutes and hours. In fact, empirical evidence indicates that when the pandemic struck, lead firms with superior analytics systems gained timely access to relevant information, efficiently moved activities from affected cities in China, and experienced fewer losses than competitors. 77

While the use of advance analytics to optimize GVCs is not particularly new (although few companies invest in advanced logistics control as significantly as the MNEs discussed above), the pandemic has highlighted its tremendous potential for managing risks and disruptions under conditions of volatility, uncertainty, complexity, and ambiguity (VUCA). 78 Beyond real-time data analysis, lead firms can rely on predictive analytics such as AI to forecast various types of disruptions, from supply and demand fluctuations to political, weather-related, and socio-cultural risks. 79 A recent study by Bain and Company 80 found that advanced analytics can improve forecasting accuracy by 20% to 60%.

Entrepreneurial Retooling

Advanced analytics offer information necessary for managing GVC risks; however, effectively utilizing this information requires considerable flexibility and entrepreneurial judgment on behalf of the lead firm management. A number of entrepreneurial lead firms were able to quickly reroute their supply chains and repurpose their production lines at the onslaught of the pandemic so as to address urgent changes in demand while providing employment to an idle workforce. 81 For instance, brewers, gin distilleries, and perfume producers used their existing ethanol supplies to make hand sanitizer; telecom companies leveraged their technologies to develop thermo-scanners and physical distancing bracelets. Manufacturers with 3D printers made personal protection equipment; luxury designers (e.g., Armani, Gucci, Prada, and Burberry) repurposed their factories to produce masks, medical overalls, and gowns; Dyson used its competencies in vacuum cleaners to manufacture portable ventilators. Supermarket chains partnered with restaurants and their suppliers to make use of restaurants’ inventory while addressing the shortage of groceries. Many services were forced to expand their digital presence, reroute distribution toward online delivery, and become more innovative in the manner in which they use technology to interact with customers. Achieving these results required that lead MNEs rapidly source raw materials, design new products, test and distribute them in a short time span.

For entrepreneurial retooling to occur, past routines had to be unlearned, new knowledge developed, personnel retrained and redeployed, new technologies adopted, and new partnerships entered. 82 In order to recover from the crisis and thrive under VUCA conditions, lead firms will need to take an active entrepreneurial role in managing GVC resources. Entrepreneurial abilities, sophisticated managerial skills, and orchestration know-how of lead MNE managers will become critical ingredients of post-pandemic success.

Conclusion

Without a doubt, the impact of COVID-19 will continue to unfold for years to come. In the long-term, responding to the risks associated with crises and disruptions will become an integral part of business-as-usual. It is therefore the responsibility of scholars to accurately portray specific implications of the pandemic for researchers, managers, and regulators.

We explain how lead MNEs can take this increased complexity and supply chain disruption and potentially turn it into meaningful change. We specifically propose that, instead of focusing on short-term responses to immediate disruptions, lead MNEs should structure and orchestrate their GVCs based on long-term governance considerations. Long-term governance implies regularly evaluating costs, risks, and value creation potential of extant structural and managerial governance mechanisms and making the necessary adjustments. We predict that an exclusive focus on cost, while certainly influencing any potential changes in governance, may be less determinative of GVC governance decisions than pre-pandemic. Other considerations, such as facilitating timely and reliable access to information, safeguarding commitments, and, more generally, ensuring continuous capability development and value creation in the GVC, may be of greater importance. 83

Our overarching point is that while there are pre-COVID trends pushing GVCs toward structural reconfiguration, it is the managerial governance responses that are likely to be instrumental in reducing information costs, increasing efficiency, and enhancing GVCs’ long-term resilience. The short-term restrictions on trade and transportation will be lifted once the pandemic is under control, and the flow of goods and services will resume once the global economy restarts. The COVID-19 pandemic may not radically change the governance of GVCs, but, we predict, will provide an impetus for changing the manner in which firms use managerial tools at their disposal to (re)organize, develop, and control their GVCs.

The global pandemic has presented a set of serious challenges to the global community, but we may be faced with even bigger global problems in the coming years, 84 including continuing climate change, food security, extreme poverty in some parts of the world, and major global health issues. These issues are certain to have implications for MNEs, GVCs, and broader stakeholders, yet the exact nature of these implications is difficult to predict. Managers, therefore, need to continue to develop and refine tools for efficiently managing their GVC in the increasingly volatile and unpredictable global environment.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to thank the Haskayne School of Business at the University of Calgary for funding the research of this article through the Transformative Research Grant and the Corporate Longevity Research Grant.

Notes

Author Biographies

Liena Kano is an Associate Professor of Strategy and Global Management, and the McCaig Family Future Fund Professor of International Family Business at the Haskayne School of Business, University of Calgary, Canada (email:

Rajneesh Narula is the John H. Dunning Chair of International Business Regulation at the Henley Business School, University of Reading, UK (email:

Irina Surdu is an Associate Professor of International Business Strategy at Warwick Business School, University of Warwick, UK (email: