Abstract

The COVID-19 pandemic shocked the global economy, laying bare the coordination challenges and vulnerabilities of global value chains (GVCs) across sectors. Governments, consumers, and firms alike have called for greater GVC resilience to ensure critical products are delivered to the right place, at the right time, and in the right condition. This article investigates whether GVC reconfiguration through the adoption of redistributed manufacturing (RDM) in local production can deliver greater resilience against unexpected, disruptive global events. It proposes actionable steps for managers to ensure more resilient GVCs in the face of global shocks.

Keywords

Firms can address vulnerabilities and risks in GVCs using buffer stocks and multiple sourcing strategies with in-built supplier redundancies. Alternatively, they could look to reconfigure their GVCs through “Redistributed Manufacturing” (RDM) 6 —small-scale local production that enables decentralized design and manufacture through geographically unconstrained value chains to address urgent needs. 7 RDM builds on the convergence of innovative technologies, such as additive manufacturing (AM) 8 and microfactories, supporting moves toward customized delivery of products at point of use. 9 The pandemic has generated greater recognition of the untapped potential of RDM, particularly its impact on complex GVCs through a shift toward more localized production. A case-in-point is the automobile firm Jaguar Land Rover (JLR) harnessing the agility offered by its AM and computer-aided design (CAD) capabilities to quickly develop and ramp up production of reusable face visors in the United Kingdom. 10

Against this backdrop, our central question asks whether adopting and implementing RDM-led GVC reconfiguration can deliver greater resilience against disruptive global events. Many drivers for GVC reconfigurations were evident pre-COVID-19 as re-shoring of manufacturing garnered renewed interest following changed social attitudes toward climate and environmental concerns, 11 greater scrutiny of value system resilience, sustainable forms of value and ethical trading, 12 as well as increasing awareness of the reputational and financial risks of GVCs. Although these have arguably led to relatively incremental changes, catastrophic events such as economic and humanitarian crises (including COVID-19) radically impact the way firms do business, 13 requiring firms to “do things differently.” 14 We provide an analysis of the opportunities and challenges for reconfiguring GVCs using RDM at a local level by drawing on insights from the literature on GVCs and RDM, setting the scene for our empirical exploration of the potential for RDM-led GVC reconfiguration across three health care GVCs: medical devices, diagnostic technologies, and pharmaceuticals.

COVID-19 highlighted GVC vulnerability and risk in health care. For instance, in specialized PPE (e.g., N95 respirators), China accounted for 41% of the world’s exports and around 90% of such masks used in the United States. 15 Yet, during the pandemic, China required more masks than it could initially supply domestically, reflecting a supply-side disruption. The Organisation for Economic Co-operation and Development (OECD) highlighted the core supply-side bottleneck was the availability of melt-blown polypropylene that the Chinese government addressed by adding over 100 new manufacturers. Supply constraints also occurred as some nations imposed export bans and authorizations, making it impossible for health care organizations to urgently source required products. Against this background, the Director-General of the World Health Organization argued for countries to increase local production of PPE by 40%. 16

These factors demonstrate risks associated with depending on the geographically concentrated supply of a critical good and the need for resilience planning. As our research demonstrates, complexities in GVCs are apparent in other valuable health care products, such as medical devices, diagnostic technologies, and pharmaceuticals. Although our focus is on health care, we highlight the transferability of GVC issues to other industries. More broadly, the OECD 17 highlights the importance of addressing risk (including upstream dependencies on a few suppliers, especially when geographically concentrated) to build greater resilience across GVCs because of the COVID pandemic. Although traditional approaches to GVCs have been predicated on cost-competitiveness seeking advantage through globally disaggregated production, resilience requires firms to focus on approaches with risk as a central factor. The next section introduces the core concepts of GVCs and RDM, before positioning our methods and cases. We collected rich primary and secondary data sets, and our research was undertaken before and after the first wave of lockdown in the UK (March and July 2020). This setting provided us with a natural experiment, investigating different scenarios for reconfiguring GVCs pre-pandemic and experiences of the effects of the first wave to assess the potential for RDM in this reconfiguration. We then present our findings by mapping healthcare GVCs to uncover drivers and barriers for GVC reconfiguration. Our work reveals that opportunities for reconfiguration utilizing RDM can be framed in the context of two key dimensions of urgency and risk affecting sourcing and supply. From this, we offer an actionable framework for business leaders in any sector to navigate the minefield of disrupting existing GVCs. The framework provides insights, clear steps, and questions to guide managers seeking to reconfigure more responsive and resilient GVCs and evaluating how RDM can contribute to this.

Theory Background

Leveraging GVCs

The GVC concept explains how value 18 is created, distributed, and captured as globally connected organizations work together to bring products to market 19 and sustainability for local communities. 20 Popularized as the global factory, 21 GVCs have been a widely adopted framework for analyzing the geographical footprint, role, and influence of global lead firms in interactions between multiple actors, 22 such as suppliers and nongovernmental organizations (NGOs), in shaping the governance of these GVCs. 23

In most health care GVCs, front- and back-end (knowledge-intensive) activities are generally located in more advanced economies. Firms in developing economies are often concerned that they are trapped in low value-added activities and locked out of higher value-added activities in design, key technological inputs, and marketing. It has been argued that in developing countries, involvement in GVCs may benefit the entire population through expanded trade and faster growth, but this development often does not benefit all GVC members equally. 24 In health care, this is evidenced by the European Federation of Pharmaceutical Industries and Associations 25 that identified vulnerabilities in traditional GVCs, and the need for investment in capabilities to strengthen the higher value-added activities such as R&D and services that anchor either end of the so-called “smiling curve” (particularly against global competitors).

Recent studies highlight the possible impact of technology (Industry 4.0) on shortening GVCs through re-shoring routine labor-intensive activities from developing countries back to developed countries. 26 Such technology advances may make undertaking aspects of the production in high-wage countries more profitable by reducing the amount of labor required, and thus the reliance on low-cost labor from developing countries. 27 As a consequence, the World Trade Organization (WTO) has highlighted the potential negative impact on developing countries but has also identified opportunities associated with technological advances for small firms to participate in complex GVCs, especially those in higher value-added knowledge-intensive sectors.

GVCs have not only made it possible to buy and offer products at affordable prices through exploiting economies of scale and scope, 28 but have created opportunities to increase economic value and bring about technological advancements. 29 An oft-cited benefit of integrating multiple actors, including customers, into GVC configurations is firms’ increasing ability to engage in value co-creation. Well-known examples exist in the consumer experience space (e.g., Airbnb) but are also evident in the health care sector (e.g., serving an end-user with computed tomography [CT] and magnetic resonance imaging [MRI] scanners for hospitals). 30 Global markets, alongside new technologies, provide new ways of value co-creation, leading to value chain reconfigurations. As firms adopt an integrative approach to creating value, the organizational architecture (or boundaries between GVC actors) begins to shift, requiring a rethinking of the GVC structure. However, while GVCs offer benefits, they also have inherent coordination challenges and vulnerabilities that must be navigated. 31

Coordination Challenges and Vulnerabilities in GVCs

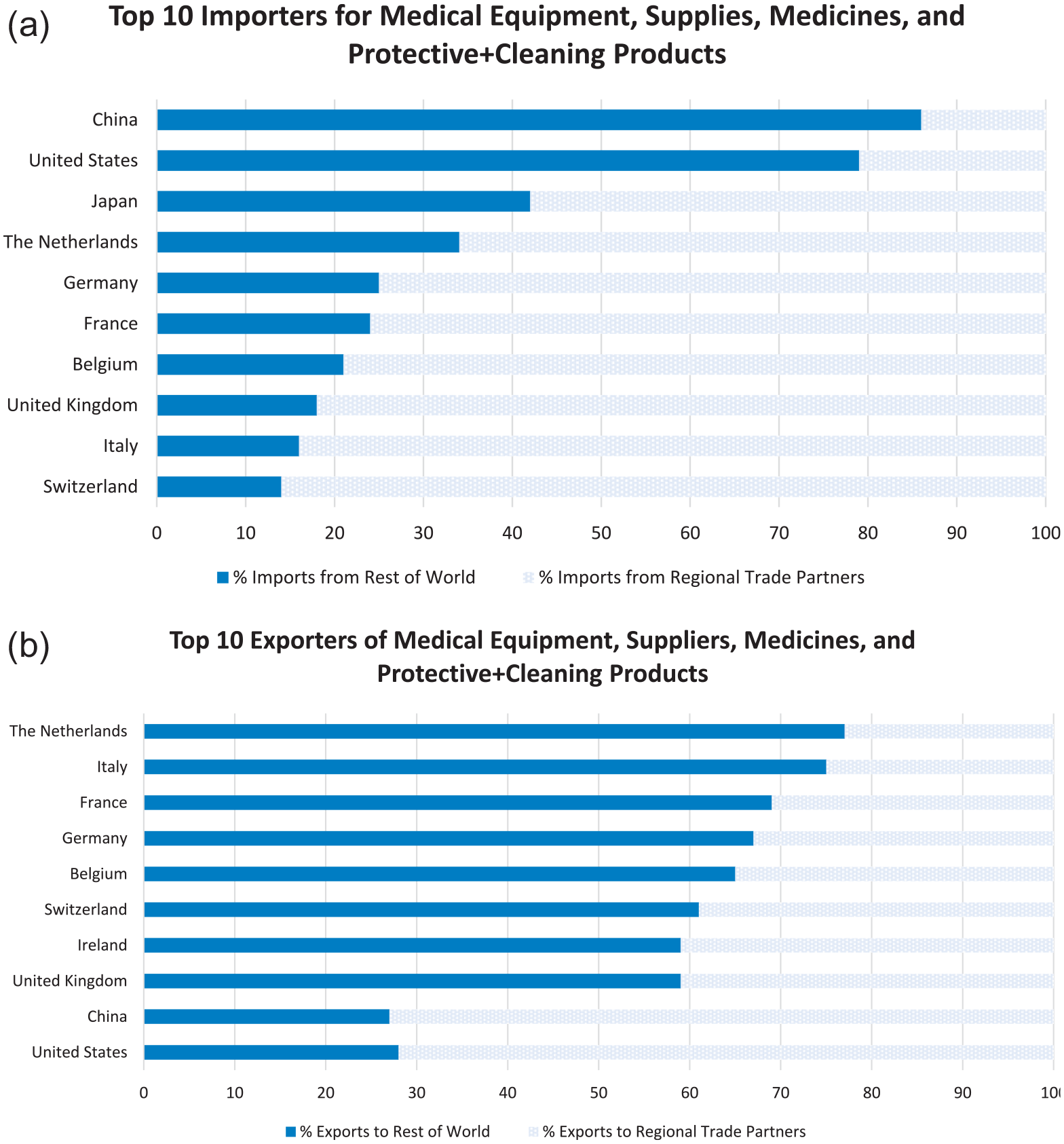

According to WTO data (Figure 1), the United States predominantly relies on imports from the “rest of the world” (vs. regional agreements) for medical equipment, supplies, medicines, protective equipment, and cleaning products. 32 Data also show around $26.8 billion of medical technology was imported into China in 2019, representing a fourfold increase over a decade, whereas the United States imports around £29.5 billion in medical instruments and $79.5 billion in packaged medicines. 33 COVID-19 is likely to exacerbate short-term dependencies on such imports, notwithstanding ongoing reported shortages of PPE, laboratory kits, ventilators, and non-COVID-related medicines. 34 For EU member states, Figure 1 implies reliance on imports from regional trading partners, yet this did not entirely insulate member states from high-stakes behavior in competing for limited resources—hence calls for improved coordination and a sharper focus on so-called “health sovereignty” within the European Union. 35

(a) Top importers for medical products; (b) Top exporters for medical products.

An exemplar GVC is vaccine manufacture that is both complex and requires specialized production capacity, much of which is supplied by U.S. and EU firms. Production can draw on raw materials and components from over 300 suppliers in 30 countries, and for which global shortages were noted in April 2021 for around 100 components and ingredients, ranging from lipids to tubing and single-use reactor bags used in the vaccine production process. 36 In sourcing raw materials and parts, similar challenges have occurred for other high-demand medical products such as ventilators. 37

Vaccine production reflects highly interdependent relationships honed over time and concentrated on relatively few firms and countries. For example, trade interdependencies among major vaccine-producing countries (such as India, China, Brazil, the European Union, the United States, and the United Kingdom) for key ingredients for vaccine production sourced mainly from other major producers 38 allow little leeway for GVC failure. The system is dependent on (and must deal with risks from) not only suppliers, but an array of subcontracting, transport, and logistics firms, and the constraints of shipping, especially airfreight and cold chains. For instance, vulnerabilities in cold chain distribution, which affect a range of pharmaceutical GVCs, are estimated to contribute wastage of 15% to 25%. 39 Furthermore, there are inherent risks associated with government policies, for example, variations in national regulatory frameworks for vaccine production and the threat of “Vaccine Nationalism.” 40 Vulnerabilities in such complex systems quickly surface; while global demand for vaccines rose to 3.5 billion doses by 2018, 68 countries suffered stockouts of at least one month’s vaccine supply due to manufacturing issues or procurement delays. 41 This hinders urgent responses to sudden outbreaks in both developed and developing countries, as the case of stocks of Yellow Fever vaccine depletion demonstrated. 42

Integration across complex GVCs presents risks as well as opportunities. Confronted with disaggregated production and supply, coordination of economic activities in GVCs varies in the complexity of roles and relationships among the actors required to mobilize value creation. Governance of activities can be orchestrated along a continuum: from simple market transactions to in-house management. Coordinating activities depend on the complexity of the value chain transaction, codifiability of the production task, and suppliers’ competences. 43 The GVC concept provides insights into how firms can create greater value through GVC reconfiguration. Lead firms not only have to consider the geographical location of GVC activities, 44 but they also need to consider how to coordinate them and make decisions about what activities need to be undertaken in-house versus elsewhere. Consideration of key decisions include time/urgency of delivery, costs of production and logistics, product quality considerations, risks involved in the GVCs, and the various relationships between GVC members that may hinder speedy scaling up/down of production. Increasingly, exposure to vulnerabilities and the potential for shared value creation is reshaping GVCs. 45 A natural progression is to consider the role of RDM in future GVC reconfigurations.

Why RDM?

RDM represents a shift away from large-scale GVCs toward small-scale, localized, and flexible manufacturing, offering reduced lead times and increased product personalization. 46 Time/urgency is particularly important in crises, 47 such as a global pandemic, when vital products are needed to deliver health care services. RDM has the potential to disrupt existing GVCs from a “current state” of a high-volume, centralized model (with a focus on “scaling-up” production) to a “future state” of geographically distributed operations located close to the market (or scale-out of production). 48 Some health care products are already produced in a decentralized manner, but these tend to be low-volume/high-margin products such as radioactive pharmaceuticals for nuclear medicine, personally titrated anticancer agents, and blood and platelet supplies. 49 In contrast, until COVID-19, it made economic sense to centralize the production of low-cost, standardized products such as PPE. Yet, from a risk and resilience perspective, the business case for RDM has become much stronger through the various waves of COVID-19, whereby the scale-out of manufacturing closer to the point of need could complement, or replace, existing supply arrangements, facilitating an improved response to peaks in demand. 50

In the ongoing battle to keep ahead of recurrent waves of COVID-19, we observe governments and commercial buyers actively reviewing their local sourcing strategies for critical products such as PPE and medical equipment, as well as placing export bans on some products. 51 Such changes are already catalyzing manufacturers to do things differently by proactively experimenting with new strategies, such as embracing advances in digital transformation or applying their technical skills to meet new demand through cross-sectoral innovation. For example, in the United Kingdom, due to a lack of international supply, there was a critical need to rapidly increase the production of medical ventilators. The VentilatorChallengeUK initiative—a consortium of organizations from the aerospace, automotive, and motorsport industries—worked with medical device firms to solve the supply problem, rapidly designing and producing critical care and mobile medical ventilators. 52 Similarly, in Germany the “Maker vs. Virus” movement linked-up end-users with manufacturers and logistic providers to support the production and supply of protective masks, face shields, and ear defenders. 53

In health care, new technologies such as machine learning and robotics, advanced CAD, and big data analytics are supporting convergence toward more distributed, intelligent, and seamless forms of manufacturing, enabling production of health care products close to the point of need. In the emerging area of personalized medicine, leading-edge cell and gene therapies are particularly well suited to localized manufacturing due to patient specificity and the instability of biological materials and processes. These technological shifts are fundamentally altering the assumptions underlying many traditional GVC configurations—namely, scale economies and market share for achieving productivity gains, lower costs, and competitive positions. The rise of RDM is supported by AM, where unit costs do not vary substantially with scale. Consequently, as the technology improves, the cost of AM becomes more competitive, 54 substituting the labor-intensive manufacturing underpinning many GVCs. An eroding cost differential, reliance on fewer component parts combined with an expanding range of applications for AM, presents numerous opportunities for small firms’ participation in GVCs, helping to realize the “scale-out” of production stated earlier.

Switching to more local sourcing and production systems with a reduced global footprint is increasingly salient due to growing political and social pressures for more environmentally sustainable “green” products and the reduction of resource inputs and waste. 55 Pre-COVID-19, the benefits of RDM were identified as particularly pertinent for complex manufacturing systems such as health care, 56 bringing production of devices, medicines, and therapies closer to the point of need and the delivery of patient-specific treatments. In the COVID-19 era and beyond, RDM might be recognized as having wider potential to address shortages of commodities and assisting front-line services in a range of challenging operational environments. 57

In summary, our study combines GVC and RDM to address challenges in GVC reconfiguration (such as coordination, risks, and urgency), 58 and while prior GVC studies have looked at economic crises and their impact on GVCs, our study investigates the role, coordination challenges, and vulnerabilities of GVCs during a pandemic. The COVID-19 pandemic provides an important context to continue exploring challenges faced by GVCs and offers invaluable managerial insights.

About This Research

To gain insights into the potential for RDM-led GVC reconfiguration, we draw on our in-depth study of the U.K. health care sector. The study provides insights before the pandemic and continues throughout the initial phase of the COVID-19 response. Given the scale of the challenges facing the sector prepandemic, from globally recognized issues such as an increasingly aging population, massively overstretched budgets, unpredictable availability of medical products, and sudden threats from climatic events and conflict/terrorism, the need for breakthrough solutions and disruptive innovation was apparent. As such, this sector was purposefully selected as key players sought to understand how RDM could play a critical role in solving these challenges. Our pre-COVID-19 workshop examined a manufacturing case from the following three areas: medical device and diagnostic technologies (worth $470 billion globally in 2018; expected to grow to $595 billion by 2024); advanced therapy medicinal products (ATMPs), including cell therapy and gene therapy (worth over $3 billion globally in 2019 with strong expected growth potential); and vaccines (worth over $26 billion globally in 2018, up 25% from the previous year). 59

Triangulating different data sources (see the Online Appendix), we collected and analyzed data using a two-stage recursive strategy:

Stage 1 (prepandemic) drew on the transcripts and visual materials from an expert academic and business leader workshop with 50 participants. The workshop employed value chain mapping 60 techniques to explore current (traditional) and future (RDM-led) value chain configuration and scenarios. After careful analysis of data collected in stage 1, we sought to establish how health care GVCs were affected by the pandemic and the role that RDM could play in addressing key challenges.

Stage 2 involved 15 in-depth interviews with senior front-line managers from public and private organizations during the COVID-19 first lockdown phase in England (March 2020), and then during emergence from this lockdown (June-July 2020). We also analyzed over 50 policy and industry reports published during this period. Interviewees were asked to draw on their recent experiences of sourcing critical medical components to analyze the potential of RDM-led GVC reconfiguration in light of the ongoing crisis of COVID-19. To obtain an accurate picture of the health care GVCs, we undertook a systematic mapping of key processes before delving deeper into interview and secondary data sources.

Findings

Mapping Health Care GVCs

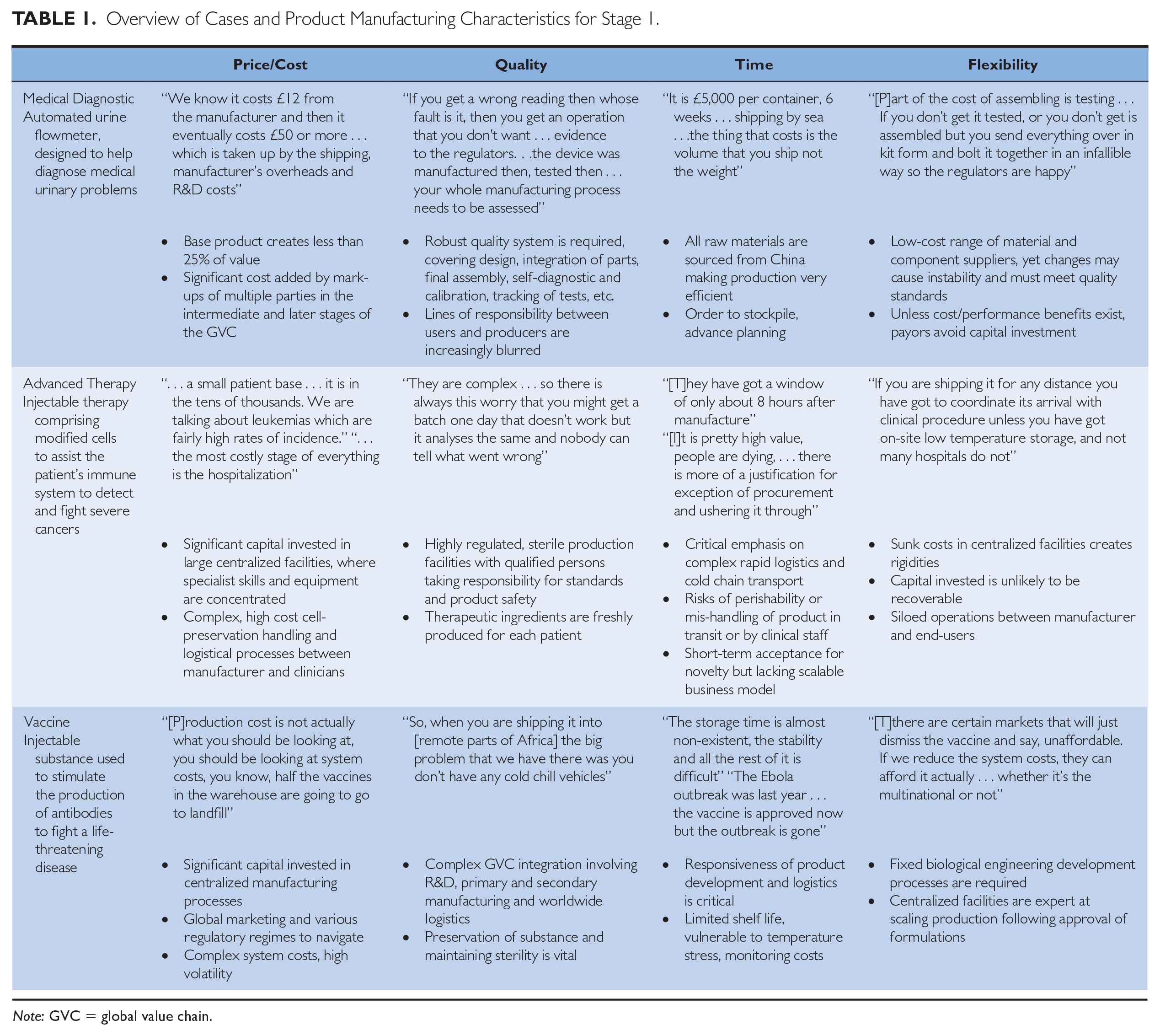

Using four dimensions of manufacturing firm priorities 61 (price/cost, quality, time, and flexibility), we compare and contrast features of the traditional manufacturing model for each case (see Table 1). GVC challenges across all three cases highlighted major risks around ensuring production system quality from basic to regulated and clinical-grade standards. All cases relied on centralized production sites to capitalize on efficient operations, economically favorable access to raw materials, and concentration of skills/labor; yet this fixed approach does not easily lend itself to achieving operational flexibility or value co-creation. For example, a Medical Diagnostic Executive noted a GVC had been extended to China to source a $1 substitute for a component costing $90. The only alternative would be to redesign the product so that the $1 component was no longer required. The Medical Diagnostic and Vaccine cases could be considered volume-based procurements, where product availability would be dependent on stockpiling and inventory management. In contrast, ATMPs reflect a lower volume batch approach with a relatively shorter GVC and a faster timeline between production and use.

Overview of Cases and Product Manufacturing Characteristics for Stage 1.

Note: GVC = global value chain.

In all three cases, a range of international environmental dependencies exists with varying degrees of logistical concerns, such as the correct handling and integrity of biological materials in transit, raising questions around the efficacy and performance of the end-to-end quality system between end-users (clinicians) and manufacturers. For ATMPs and Vaccines, an audit trail was cited as critical in ensuring cold storage up to the point of use, yet transport distances and conditions, from the production site to eventual use, were considered costly and wasteful (see Table 1). One ATMP professional highlighted the scale of the problem: “for some of the replacement skin therapies, they were losing up to 70% of their product just in shipping.”

Arising from issues of quality and logistics, interorganizational coordination mechanisms across the GVC were vital in all three cases, particularly for ATMPs and Vaccine products. A disconnect between manufacturing and service use was discussed by an ATMP expert who suggested the need for greater coordination to overcome the siloed operations to “better predict when [cell therapies] are going to be harvested, and when they are going to be ready, and when it is going to arrive.” Workshop discussions also explored the potential of a more sophisticated collaborative relationship if both sides took advantage of real-time information and communications technology (ICT) and analytic technologies to ensure a two-way flow of critical information on medicines’ use or patient health being fed back to manufacturers and R&D.

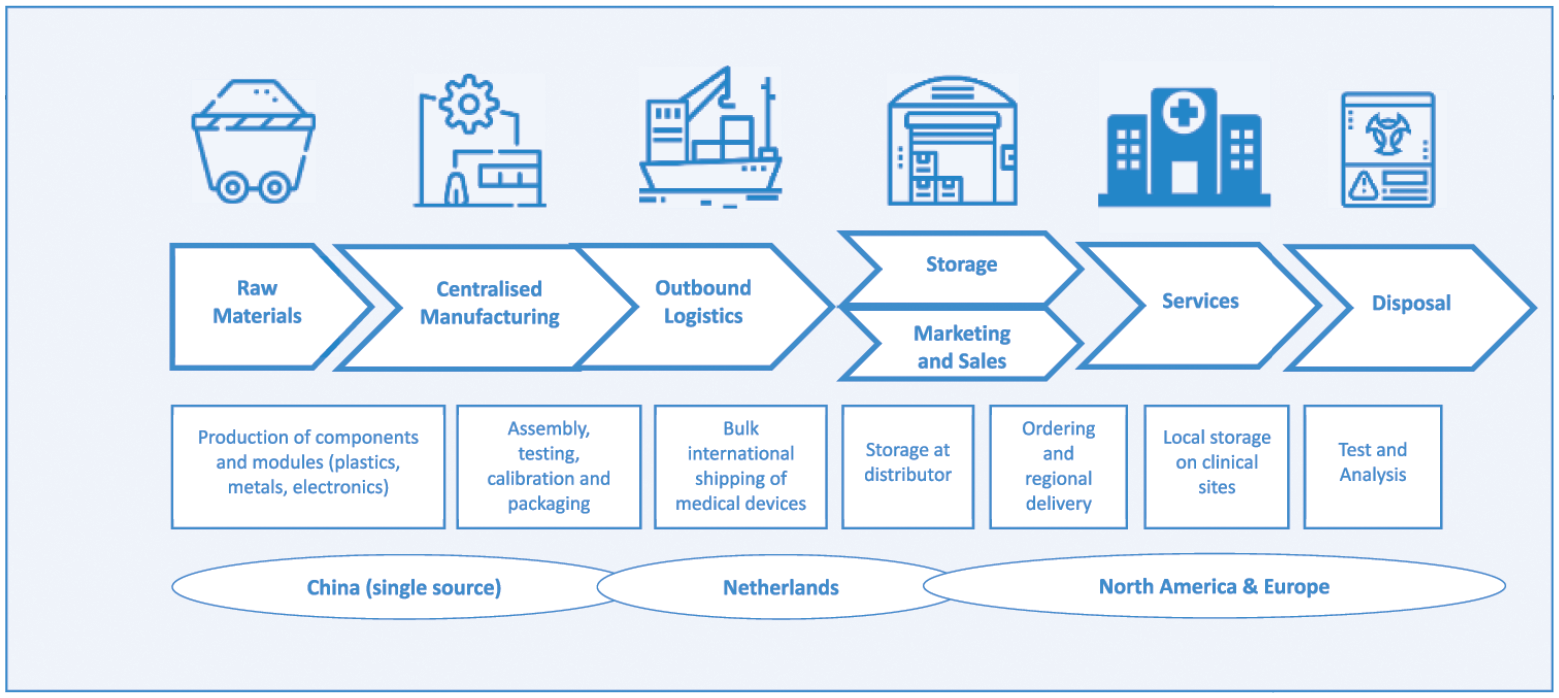

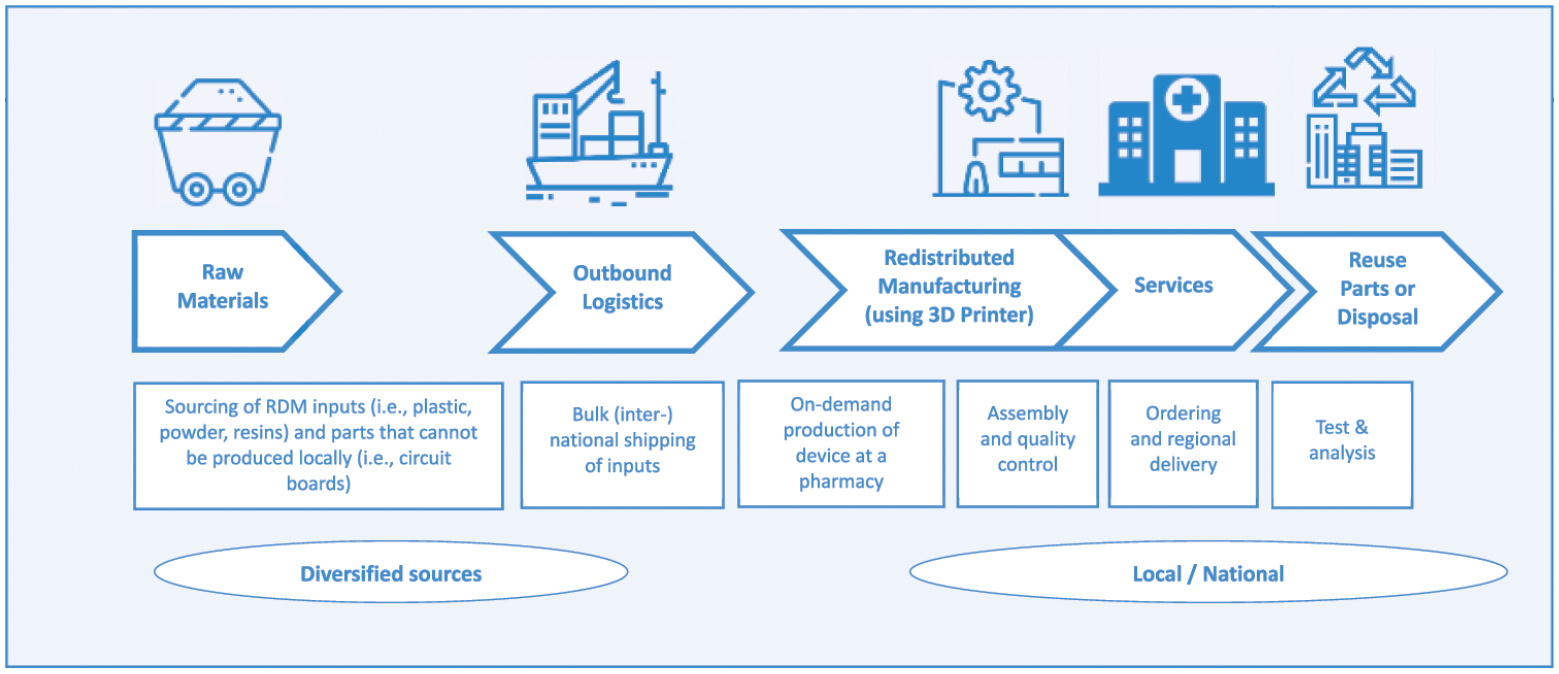

Figure 2 and 3 provide stylized illustrations of the journey from raw materials to final use for a medical diagnostic device, comparing traditional manufacturing and a reconfigured GVC, based on applying RDM through the introduction of a commercially available desktop 3D (3-dimensional) printer located in a hospital pharmacy near to patients.

Medical diagnostic case, traditional GVC.

Medical diagnostic case, RDM-led GVC.

The traditional GVC in Figure 2 represents the typical long GVC found in a range of medical device products originating from lower cost production in Asia. In this case, the first stage of the GVC, electronics, and plastics are contract-manufactured and assembled in China, where components are sourced, assembled, tested, and packaged. Postmanufacture, the products are shipped to specialist warehousing and logistics providers in the Netherlands. Typically, at this stage in the GVC, shipping hubs provide cost- and/or tax-efficient locations for repackaging and forwarding to distributors serving major customer locations in North America and Europe. With multiple steps and actors in the GVC, a significant proportion of the product’s final cost is added during the intermediate and later storage, assembly, and shipping stages. The RDM-led GVC in Figure 3 shows how RDM presents an opportunity to produce, on-demand, most of the medical device parts but in a new design favoring 3D printing rather than mass production. In this scenario, GVCs are still important for sourcing so-called “feed” material for the 3D printer and electronic parts that are not easily printable locally at a reasonable cost. Over time, as 3D printers become more commonplace, our workshop experts expected raw inputs will be sourced closer to production or will employ circular economy practices that will allow local waste to be melted down into raw material for new products.

The expert workshop provided insight into the feasibility of RDM-led GVC reconfiguration, highlighting some drivers (including risks) and cost reductions over geographical distances and across firm boundaries, as well as the economic and clinical benefits of manufacturing responsiveness to demand and ensuring product quality. Pre-COVID-19, the transition toward RDM was still considered a niche activity, at best a small-scale complementary operation alongside established centralized manufacturing until such time as the business case became more compelling.

Drivers for GVC Reconfiguration

Drawing across our research stages, we highlighted the impact of the pandemic on health care GVCs and issues arising for RDM-led GVC reconfiguration. Our research revealed major risks in all areas of product manufacturing characteristics highlighted in Table 1 (price/cost, quality, time, and flexibility) related to reliance on established GVC configurations during the pandemic (i.e., traditional GVC in Figure 2). Paramount was the lack of global production capacity for critical health care products, restricting the ability of health care organizations to respond flexibly to the rapid spike in demand. The situation was further compounded by individual governments focusing on their own citizens’ best interests. Our findings center on three core issues, reflecting increasing risks in the GVCs in response to the urgent need to source supplies:

delivery assurance—reliable delivery of orders to the right place, at the right time, and in the right condition;

procurement capabilities—the knowledge, skills, and experience health care managers had to manage the supply issues confronting managers during the COVID-19 pandemic; and

product integrity—assurance that a product meets a customer or end-user requirements for performance, quality, durability, and safety.

Delivery assurance

At the outset of the COVID-19 pandemic, urgency in ensuring a supply of critical health care products meant delivery assurance was vital due to last-minute changes to availability arising from pressures on suppliers by their national governments to redirect orders. Furthermore, delivery times were unpredictable as airfreight and shipping became severely affected by COVID-19. Our interviewees recounted how suppliers could not deliver on contracts since “all-of-a-sudden a manufacturer in China cannot cope . . . The French bought . . . a whole factory capacity . . . that supply that you knew was shut down” (private health care provider). A European Head of Sourcing felt that “Some of the problems we have . . . are from USA firms prioritizing stock for themselves and not releasing to us.” These experiences mirrored concerns elsewhere, such as the proposed U.S. Medical Supply Transparency and Delivery Act (H.R.6711) seeking to avoid competition between states, introducing transparency in managing the national stockpile, and compelling firms to produce critical medical equipment. The European Commission actively intervened to restrain national governments’ efforts to restrict cross-border supplies of PPE, creating joint procurement across European member states, forcing Germany to issue export licenses for PPE to countries such as Italy and Austria. 62 Despite government efforts, one private health care provider reflected the uncertainty around distributors “basing promises on anticipated supply from China . . . being almost like the Wild West.”

Procurement capabilities

Prior to COVID-19, most participants were reliant on U.K.-based distributor networks; when these networks were unable to deliver on their contracts, managers had to step away from traditional sourcing arrangements and engage directly with the overseas manufacturers. To meet the urgent requirements for critical medical supplies, managers had to identify new, unfamiliar suppliers with no background information. As highlighted in the press, 63 this resulted in costly (life-threatening) and irreversible mistakes running into hundreds of millions of dollars. In a rush to secure a supply of 50 million face masks for U.K. health care workers, insufficient due diligence on safety standards meant these masks could not be used. Lacking procurement capabilities in dealing with overseas suppliers, many managers relied on working with firms with existing logistics arrangements: “We were tactically buying, with the need to pay high prices and commit large minimum orders to secure supply” (Head of Procurement). We discovered that even organizations with built-in redundancies and backups (with appropriate suppliers, stockpiles, or sourcing alternative products) were still subjected to unfavorable terms and conditions, artificially high prices for commodities, and dysfunctional bidding wars as regional procurement hubs prioritized their own hospitals or care systems.

Product integrity

Even when distributors had the logistical arrangements in place, they often had little expertise in medical product regulations and quality standards and were working with an overly opportunistic marketplace: “As demand completely outstripped import supply, a number of UK distributors seemed to lower standards, chasing the sales” (private health care provider). Counterfeit goods were a real threat, compounded by difficulties in securing testing facilities to ensure specifications were met. A Head of Sourcing expounded, We received fraudulently accredited PPE via a more trusted supplier . . . information was provided in Chinese only. We also had a problem with the translation of specifications for one product resulting in products being produced-to-order that did not meet our specifications.

While, in the short term, governments may be focusing on fixing legacy procurement and GVC structures, the pandemic raises urgent questions around more sustainable long-term investments and solutions. It has provided an opportunity to reflect on how best to coordinate GVCs and work toward a more effective response to such future global events. A procurement manager suggested the situation prompted firms to look at alternative sourcing arrangements, increasingly with local suppliers, since “The local supply chain and providers have been the ones that got us out of trouble.”

Our findings revealed increasing awareness of the advantages for patients and end-users in shifting production closer to the point of need (or care). The immediate challenges of managing GVCs during the height of the pandemic presented a strong rationale for RDM toward more localized production. Managers cited benefits such as lead-time reduction resulting in less inventory at point of use, the potential to purchase tailored service offerings, risk mitigation in terms of improved availability of critical medical supplies, and a reduced dependency on large overseas manufacturing sites.

Barriers to RDM-Led GVC Reconfiguration

Despite the support for RDM-led GVC reconfiguration, our study highlights barriers to adopting RDM, such as difficulties in locally sourcing raw materials and ensuring quality control across multiple locations. Even during the pandemic, efforts to manufacture PPE locally gave rise to problems. As a Head of Procurement noted, “local production using 3D printers was used . . . there were quality control issues . . . access to raw materials also became an issue. It was again difficult to get CE (quality standard) accredited products.” Our study revealed five main barriers to replacing global sourcing with local production systems:

Organizational inertia—Having previously invested in centralized forms of production and sophisticated logistical and purchasing arrangements, we found some concerns about changing business models to accommodate RDM. As summarized by a representative from Vaccines, “There is huge organizational inertia at the institutional level, corporate level, it is not that they do not know how to do it—they may not be skilled enough to do it.”

Lack of systemic perspective—Without a holistic perspective of the risks and benefits, it is challenging to set out the business case for change. As one Medical Device expert stated, “The view you will get from the [UK health service provider] purchasing people will be very short term . . . it is the systemic cost that people do not factor in. They factor in just the short-term costs.” He went on to suggest, “Hospitals do not want to lay out for a very expensive piece of equipment, but they are quite happy to lock themselves into paying for disposables.”

Cost-benefit—Our research highlighted the assumption that digital advances may help the transition to RDM adoption. As explained by an ATMP participant,

Automation lets you guarantee a good process at a local level rather than centralizing . . . but then you stop and do the math . . . if I build an automated platform, it is pretty expensive, and I would need to be quite sure it was working 24/7.

From the purchasing organizations, there is concern regarding potentially increased management costs if multiple suppliers need to be managed.

GVC coordination—RDM proffers opportunities to change organizational configurations. An ATMP workshop expert noted, “The ideal case would be to coordinate delivery with use because if you can do that . . . you have got the minimum chance of things going adrift.” Given the requirement for significant investment in manufacturing assets associated with such developments in RDM, a shift to long-term relationships and contracting would be necessary, potentially by more than one user or customer organization. Greater coordination would be required to ensure all regulatory and quality assurance standards were met, necessitating investment in adequate testing, certification, and regulatory arrangements across multiple sites.

Design control and IPR—Moving to RDM-led GVCs raises both opportunities for enhanced value co-creation and design improvements, but also raises questions related to potential IPR issues, such as who “owns” the final assembled product, especially if something goes wrong. As stated in Table 1 (Medical Diagnostic), manufacturers and end-users (i.e., clinicians) need to ensure that risk is managed collaboratively, from design integrity to usage protocol compliance, providing a reliable audit trail for regulators.

In summary, our findings highlight that RDM should not be considered a panacea for all inputs to a finished product and organizations are likely to require a portfolio of approaches to managing their GVCs. For example, many raw materials and some components may not be available locally and this will limit the extent to which GVCs can be reconfigured.

Rethinking Your GVC

Our research has distilled two overarching factors impacting the pressing need for GVC reconfiguration. These are “risk” and “urgency.” Risk is a characteristic of strategic decisions for GVC reconfiguration 64 and captures the dimensions of outcome uncertainty (such as variability in possible outcomes, and the extent to which organizations have some or no control), outcome expectations (or the gap between aspirations of anticipated and realized outcomes), and outcome potential (that the outcome is significant enough to require managerial attention). In our study, all three forms of risk were evident. The urgency of a strategic issue driving the GVC reconfiguration relates to time sensitivity such as immediacy and duration, reflecting managers’ evaluation of the importance of addressing this issue. 65 In the response to COVID-19, this was paramount in the health care sector as high visibility both within primary care providers and from external stakeholders, translated into urgency in response by managers who perceived their organizations to be responsible. Urgency in this context is associated with a heightened sense of threat and perceptions of the real cost of failing to act. Thus, in the context of varying degrees of risk and urgency, we suggest four models of GVCs relevant in the postpandemic era, as illustrated in Figure 4. While the main guiding principles of GVC design (e.g., the search for economic efficiency) are less likely to change for many products, components, or materials, we show partial RDM-based GVC reconfiguration is vital in three of the four models in our framework.

Models of manufacturing and GVC reconfiguration.

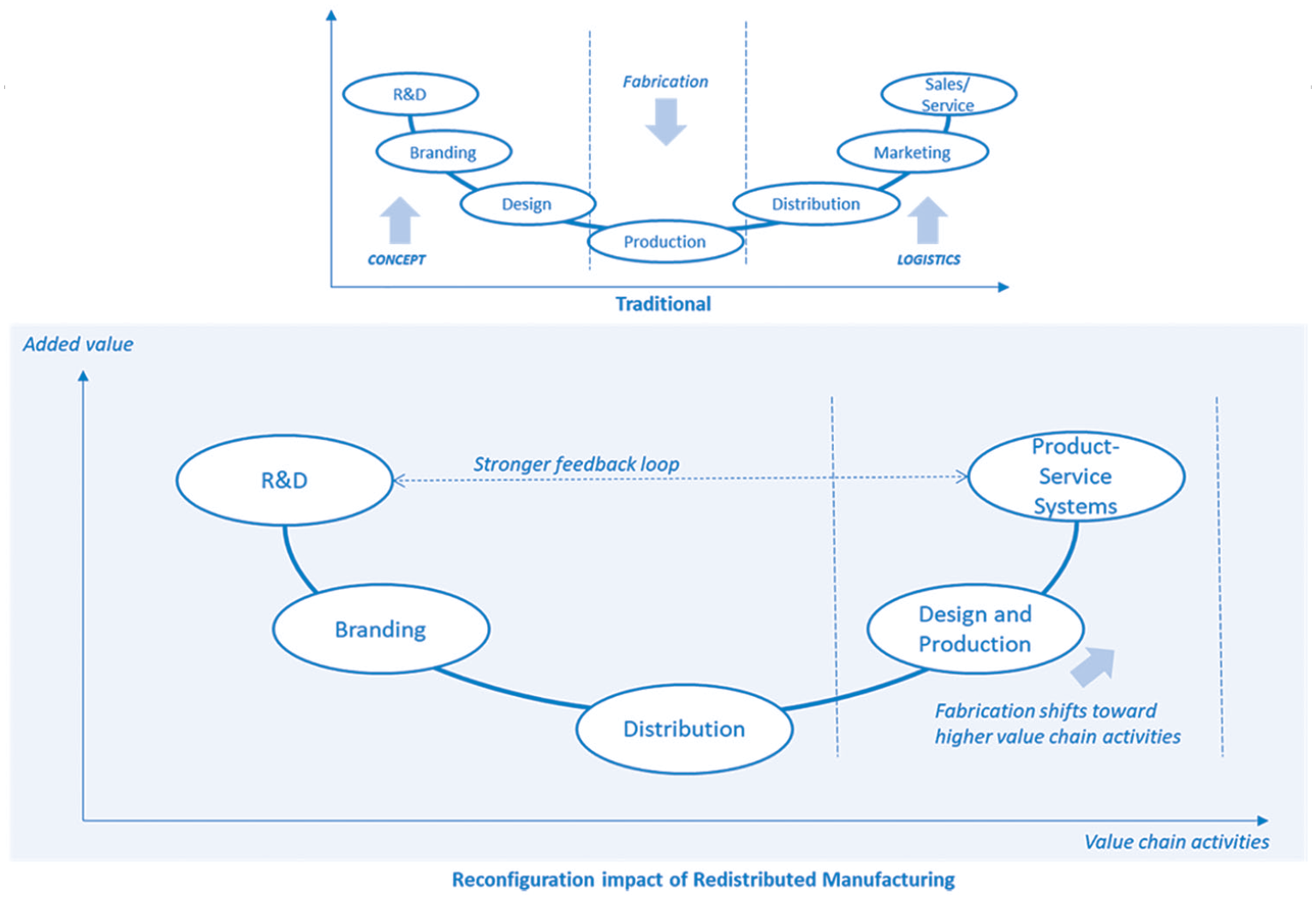

The “Global Standardizer” reflects the traditional health care GVC, and likely for other sectors with similar product profiles. The Global Standardizer is optimized for mass production and therefore limited in its ability to respond on either axis, whereas the “Local Customizer” provides a dedicated, or complementary, solution to high-risk and high-urgency demands, underpinned by an RDM strategy. These two models differ significantly in where value is created in their GVCs, as conceptualized in Figure 4. The Global Standardizer is more associated with the traditional diagram in the top half of Figure 5 with a “smiling curve” on which R&D and services are located at the top ends of higher value-added activities. Notably, “production” is overlooked in this diagram as a potential valuable driver of innovation or a critical component of a responsive manufacturing capability. When shifting toward the Local Customizer model, formerly siloed activities gain new value from a more cohesive RDM approach such as personalized design, development, production, and tailored products that are a seamless part of an integrated service solution to deliver clinical outcomes. This is conveyed by the reconfigured “smiling curve” diagram in the lower half of Figure 5. Servitized manufacturer business models may become a strong feature of the “Local Customizer” approach, as clinical communities seek day-to-day operational design and engineering support of production equipment installed within or near to a clinical setting.

Traditional versus RDM smiling curve: Value-added along the (global) value chain (modified from Berden, 2020a—EFPIA).

We observed rapid adoption of both the “Local Contractor” and the “Global Stockpiler” in a reactive attempt to deal with the lack of medical product availability during the initial peak of the pandemic. For example, Local Contractor interventions resulted in urgent repurposing of local assets and infrastructure from other sectors, while Global Stockpiler interventions resulted in frequent attempts to secure new international contracts to build or stockpile essential supplies while simultaneously experimenting with new technologies. For some, a portfolio approach to hedge the risk of overreliance on a particular model may provide increasing redundancy and switching capacity in a complex system, but may also drive up costs. Looking beyond the immediate response to the crisis and business continuity pressures, we argue against the continuation of short-term fixes in favor of the Local Customizer RDM profile, which offers greater resilience and other strategic long-term benefits such as mitigating environmental challenges.

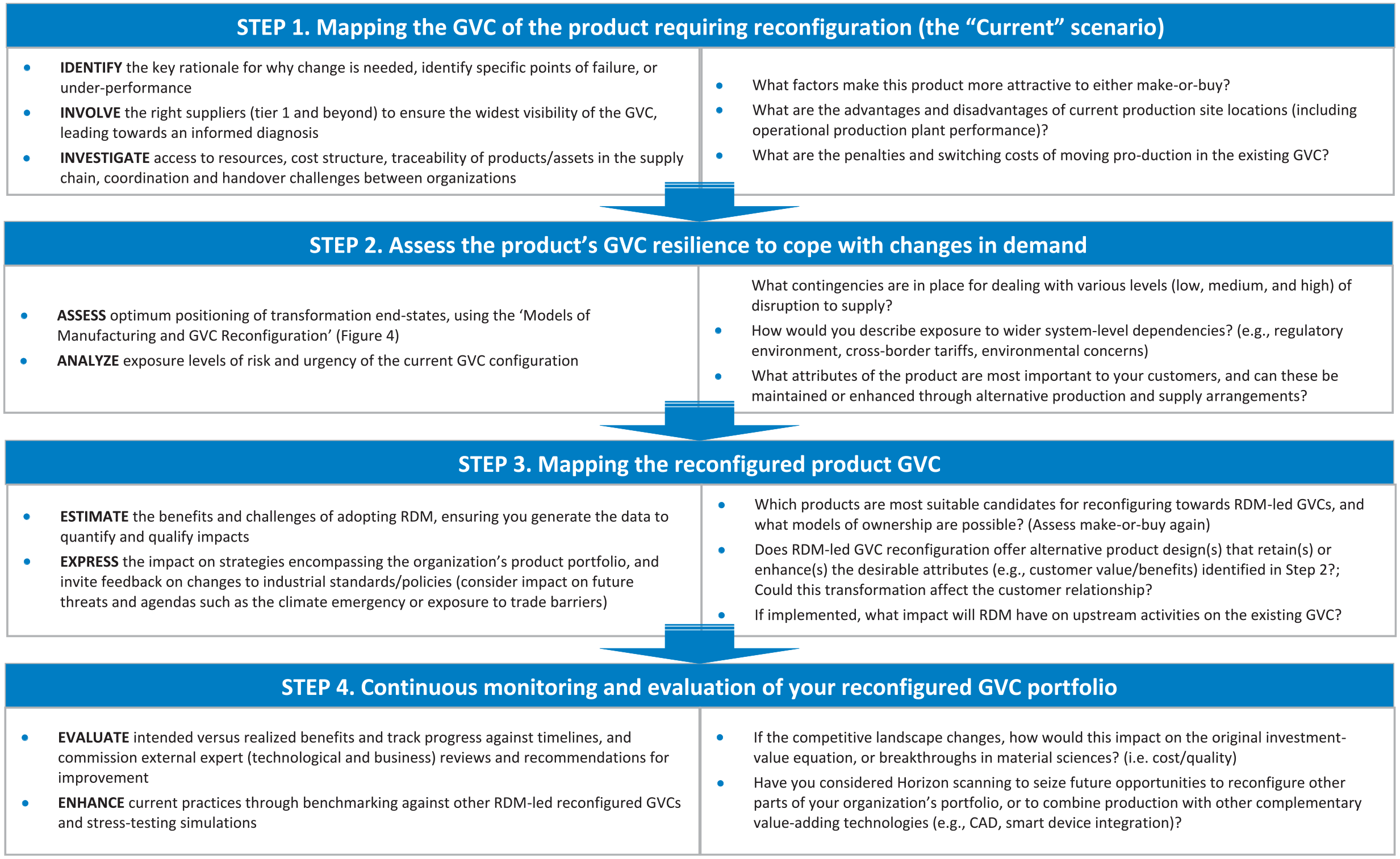

In a post-COVID-19 era, managers will need to quantify risk and urgency differently when developing new strategies to mitigate future crises. We recognize that substantive changes to GVCs will often be a long-term process and may involve experimenting with dual business models or working with new innovators involved in R&D and manufacturing. Our framework (Figure 4) helps organizations to better understand their current positioning and is designed to trigger further analysis of future strategic options. Depending on the product, we recognize that the GVC reconfiguration process may be complex. Therefore, we recommend breaking down the process into four steps as outlined in Figure 6. Step 1 involves scoping the rationale, involving key parties, and compiling the evidence base for further analysis. Step 2 draws on Figure 4 to stimulate a critique of current performance and future directions. Step 3 brings together the business case for GVC transformation, setting out ways to mitigate potential challenges. Finally, Step 4 involves tracking and evaluating progress with a view to maintaining a competitive position.

Steps to reconfiguring your GVC portfolio.

Our study is informed by prior work on GVCs and offers actionable, practical insights on how RDM-led GVC reconfiguration in health care can offer a solution to crisis situations. Although the focus of this research is medical product GVCs, our findings should be of interest to other sectors that recently faced similar challenges and are actively considering GVC reconfiguration. Exciting developments may emerge where RDM supports, or is integral to, other pressing agendas, such as meeting carbon reduction targets, adopting circular economy policies, increasing personalization to customer needs, incentives for local employment (covering design, production, and support), and more responsive relationships with buyers.

Conclusion

The uncertainty generated by the ongoing global pandemic has forced organizations to reconsider risk and urgency as critical factors in the context of GVCs; entire sectors of the economy can shut down, disrupting GVCs without advance warning or negotiations. Against this backdrop, firms are actively seeking insights for achieving innovative restructuring of their GVCs, taking advantage of existing technological innovations such as AM to overcome the challenges. Reconfigurations during (and post) COVID waves may help GVCs to reap the benefits not only of value co-creation but also open innovation. 66 Conditions are ripe for changes that will create and shape reconfigured GVCs and markets. Overreliance on traditional GVCs has strengthened demand for more localized, resilient, and agile value chains to manufacture products customized to local needs and with smaller environmental footprints.

The COVID-19 pandemic has highlighted the saliency of redistributed models of production, but there are important challenges that must be addressed if the potential benefits are to be realized and a transformative shift made. The complex nature of these challenges underlines the need for commissioning further multidisciplinary R&D into RDM and horizon-scanning for opportunities to acquire or collaborate with early adopters, exploratory pilot ventures, and university spinouts. With the emphasis on building greater systemic resilience for the rapid delivery of critical supplies, such as medical products, RDM should be considered as a potentially powerful entrepreneurial solution to meet future challenges.

Supplemental Material

sj-pdf-1-cmr-10.1177_00081256211068545 – Supplemental material for Global Value Chain Reconfiguration and COVID-19: Investigating the Case for More Resilient Redistributed Models of Production

Supplemental material, sj-pdf-1-cmr-10.1177_00081256211068545 for Global Value Chain Reconfiguration and COVID-19: Investigating the Case for More Resilient Redistributed Models of Production by Wendy Phillips, Jens K. Roehrich, Dharm Kapletia and Elizabeth Alexander in California Management Review

Footnotes

Funding

The author(s) disclosed the receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the United Kingdom’s Engineering and Physical Sciences Research Council (EPSRC) under Grant EP/M017559/1 and EP/T014970/1.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

Wendy Phillips is Professor of Innovation at Bristol Business School UWE, UK (email:

Jens Roehrich is Professor and HPC Chair in Supply Chain Innovation at the University of Bath, School of Management, UK (email:

Dharm Kapletia is a Senior Research Fellow at Bristol Business School UWE, UK, and is a Fellow of the Schumacher Institute for Sustainable Systems, UK. He holds a PhD from the Engineering Department at the University of Cambridge, UK (email:

Elizabeth Alexander is a Reader in International Management at Newcastle University Business School, UK, and has a PhD from the George Washington University School of Business, Washington, D.C., USA (email:

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.