Abstract

For manufacturers, remaining competitive depends on their ability to digitalize their business models (i.e., offer digital and digitally enhanced products and services). To achieve this, they must engage with new digital partners and help their existing suppliers, partners, and other stakeholders to digitalize. Orchestrating this growing ecosystem is challenging. Manufacturers struggle with this endeavor because of specific barriers associated with their existing legacy business model and related to their lack of digital vision, product-centric value chains, and a bias toward firm-centered profit formulas. To overcome these barriers, leading manufacturers have developed new approaches to ecosystem orchestration.

Data is the new oil, fueling novel sources of value creation. Industrial manufacturers are increasingly transforming their business models, 1 so they can use digital technology to create, deliver, and capture greater value. 2 Investment in digital technologies (e.g., industrial data platforms and analytics) has allowed leading providers such as Komatsu and ABB to create new revenue streams from innovative digital services—for instance, fleet management and site optimization—to improve the performance of connected equipment and production sites for their customers. 3

Yet, many such initiatives have fallen short of realizing their potential because of a “do it yourself” approach. 4 Leading manufacturers are now learning that they must extend their ecosystems 5 to gain access to digital infrastructure, data, and capabilities 6 to catalyze the development of new digital offerings, 7 and to ensure their delivery across global markets. 8 This requires a multitude of new collaborations with new and existing actors—for example, new digital infrastructure providers, software and application providers, connectivity providers, and specialized Small and Medium Sized Enterprise (SMEs)—as well as existing local sales and service partners (e.g., distributors) and competitors who need to align for a focal value proposition to materialize. 9 For instance, a global automation and control system provider, ABB, has established dedicated digital partnerships with technology providers (e.g., Microsoft, IBM, and Ericsson), SMEs, and startups (e.g., the Synnerleap program), while driving digitalization with customers and existing service partners.

Orchestrating this expanding and evolving ecosystem to ensure the joint development and execution of digital business models is a highly complex and challenging undertaking. 10 A key challenge is that the very nature of a traditional manufacturing company’s product-centric business model and existing ecosystem partners may conflict with the new ecosystem partnerships needed to develop and commercialize digital solutions. 11 As a result, manufacturers need to take radical steps to redefine value creation, value delivery, and value-capture activities, while aligning ecosystem incentives, roles, and responsibilities. 12

Existing research on business and innovation ecosystems provides few recommendations on how manufacturers can achieve this complex undertaking. 13 Moreover, in the business model literature, very few studies address the question of how best to manage ecosystem collaboration to achieve business model innovation, 14 especially when this involves entirely new or changing ecosystems. 15 There is, in consequence, a need to develop a deeper understanding of ecosystem orchestration through a business model lens so that the set of deliberate, purposeful actions and activities conducted by a focal firm pursuing digitalization can be illuminated.

Digital Business Model Innovation and Ecosystem Orchestration

Digital business model innovation is crucial for industrial manufacturers. 16 This is reflected in their heightened sense of urgency to engage in new ecosystem partnerships to drive the digitalization of their business models. 17 An (innovation) ecosystem represents the “alignment structure of the multilateral set of partners that need to interact in order for a focal value proposition to materialize.” 18 Accordingly, understanding appropriate ecosystem collaboration starts with a value proposition and seeks to identify the activities and set of actors that need to interact for the value proposition to materialize. For example, Volvo Group has begun to design and commercialize construction site optimization solutions with “digital native” ecosystem partners (e.g., connectivity, analytics) while coordinating the transformation of their existing distributors responsible for delivery to construction industry customers. Thus, successful ecosystems involve partners that co-evolve capabilities around a new innovation. They work cooperatively and competitively to support new offerings, satisfy customer needs, and eventually develop the next round of innovation. 19 For that reason, companies in an ecosystem rely on each other’s contributions to a greater degree than in traditional value chains 20 where partners can more easily be replaced. 21 Due to this interdependence, there is arguably a need for the focal manufacturer to consider involving ecosystem actors in all business model elements.

A business model represents the “design or architecture of the value creation, delivery, and capture mechanisms” of a company. 22 A closer look at each of the business model elements helps to assess the potential that (digital) ecosystem partnerships can offer. First, value creation concerns what is offered to the customer—for example, the type of (digital) product or service. The involvement of ecosystem actors with digital skills (e.g., digital startups, cloud analytics providers) can supply missing pieces and innovative applications to spark higher value creation and more advanced digital offerings (e.g., artificial intelligence [AI]-enabled site optimization) for incumbent manufacturers. 23 Yet, existing ecosystem partners with established customer contacts may also hold vital market knowledge that could customize digital offerings for specific customer needs. Second, value delivery concerns how activities and processes are employed to deliver the promised value—for example, what specific logistical resources and capabilities are needed. Involving new ecosystem actors can innovate delivery processes by adding sophisticated digital applications (e.g., predictive maintenance, route optimization), but it may also require changes in the roles and capabilities of existing delivery partners (e.g., distributors) to leverage digital potential. Finally, value capture is concerned with the financial viability of the revenue model—in other words, what is the balance between the possible revenue sources and corresponding costs? The involvement of new digital actors and digital infrastructure may fundamentally change existing cost structures and revenue models (e.g., subscriptions, pay per use) and introduce a more comprehensive sharing of revenues and risk among partners.

The theory and practice of digital business model innovation, while continuing to evolve, is in need of further development. 24 Indeed, prior research has not adequately investigated the involvement of ecosystems in business model innovation. 25 There are a number of crucial theoretical and empirical questions that remain unresolved, such as, How does the involvement and orchestration of ecosystem partners in digital business model innovation unfold? What are the barriers, processes, and key activities that mark out the journey? Thus, a key focus for digital business model innovation is understanding how a focal company can orchestrate an ecosystem of interdependent actors to create and commercialize digital solution offerings for the benefit of the end customer.

Indeed, innovation ecosystems do not evolve on their own. 26 An essential and distinguishing feature of an ecosystem is the presence of a central orchestrator (in our case, the manufacturer) who sets the system-level goal, defines the hierarchical differentiation of members’ roles, and establishes standards and interfaces. 27 To orchestrate an ecosystem, manufacturers “need to engage in deliberate, purposeful actions for initiating and managing innovation processes in order to exploit marketplace opportunities.” 28 For example, this can relate to forging and sustaining partnerships, 29 managing the technology infrastructure, 30 governing the ecosystem, 31 and orchestrating value-creation and value-capture activities 32 across the ecosystem. Managing the orchestrator role is, therefore, critical for manufacturers in their efforts to provide more efficient digital solutions. For example, there is a need to promote the use of data and digital technologies to enable digital service innovations and consciously manage collaboration among different ecosystem actors. Indeed, without adequate coordination in the ecosystem, innovations often fail. 33 In addition, a time perspective on ecosystem evolution and orchestration has been recognized but not fully understood in the academic literature. 34 For example, during the early stages of ecosystem orchestration, orchestrators may need to focus on forming new partnerships whereas, at a later stage, they may need to focus on exploiting digital opportunities with partners. Thus, a crucial area where further knowledge needs to be developed is how digitalizing manufacturers orchestrate their ecosystems for digital business model innovation. In particular, the linkages between ecosystems and deliberate orchestration activities through changes in value creation, delivery, and capture can carry important implications.

Method

Research Approach and Case Selection

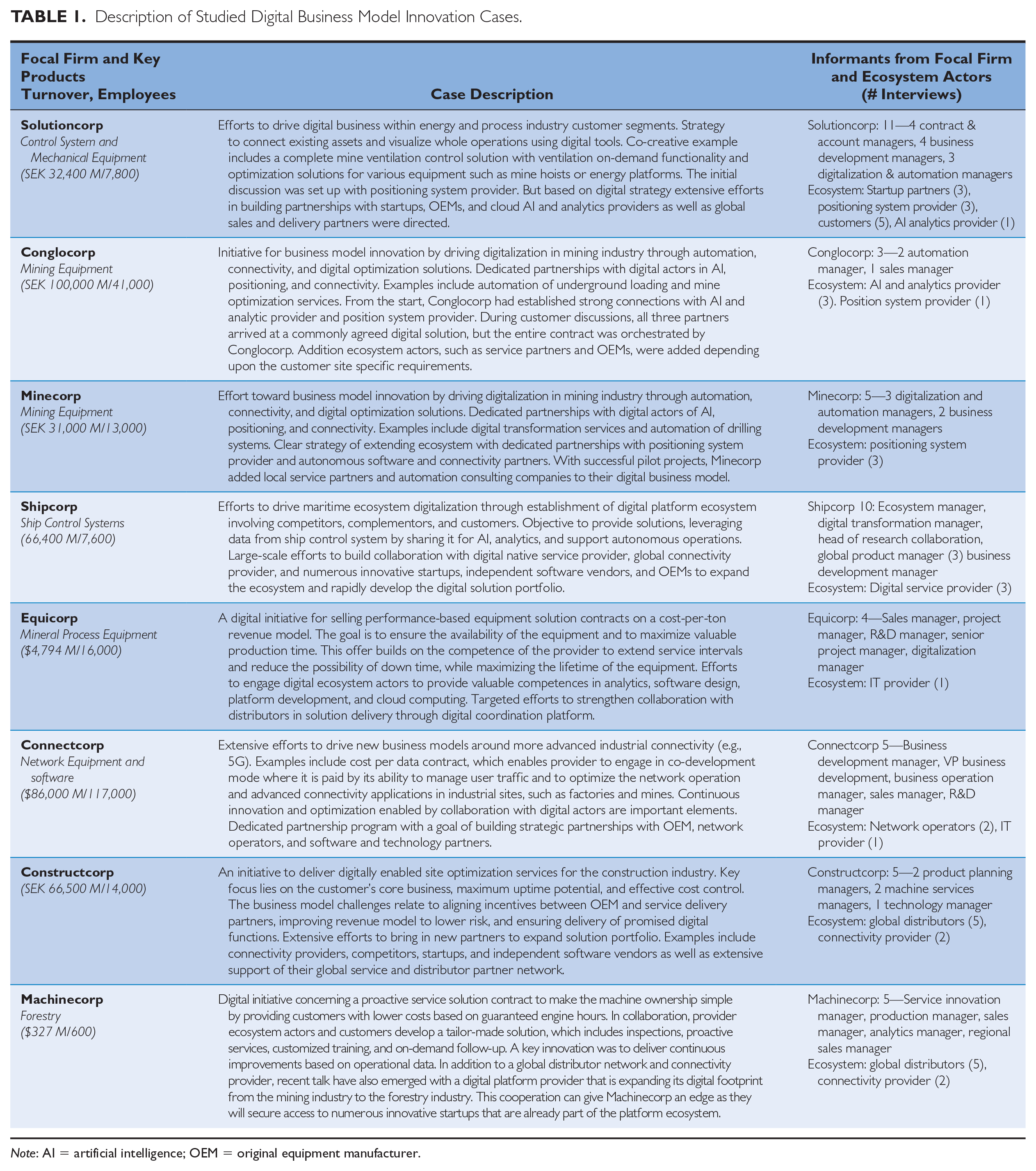

This article presents an exploratory multiple case study to investigate how manufacturers orchestrate ecosystems for digital business model innovation. The sample consists of eight globally active Scandinavian B2B providers and their ecosystem partners engaged in digital business model innovation (i.e., digital servitization). Each was generally regarded as a market leader within their industry segment (e.g., top three in sales). Provider cases from diverse industries (manufacturing, shipping, construction, and mining) were selected to enhance the generalizability of our findings.

Several factors underpinned our selection of these cases. First, the providers were actively working with digital business model innovation (e.g., customer site/process optimization offerings) and had several successful collaborations with customers. For example, Solutioncorp had a solid record of delivering digital services that have optimized machine operation by up to 25%. (Note: Here and throughout, the names of the companies have been anonymized by using “industry + corp” as pseudonyms.) Second, these firms had been working to involve ecosystem actors in digital business model innovation for some time, with notable developments in routines and processes, which have been incorporated into their business models. This background meant that we could learn from the experiences of leading companies. For example, Shipcorp described a comprehensive approach to identifying and onboarding ecosystem partners in order to develop new digital services. Third, we selected cases where we had established good contacts with stakeholders in the firms. These positive contacts enabled us to collect detailed descriptions of their attempts at ecosystem orchestration and business model innovation and obtain in-depth information on how they unfolded.

Data Collection

Data were gathered primarily through individual, in-depth interviews with participants from manufacturers and ecosystem partners that were active in ongoing digital business model innovation. In total, we conducted 82 interviews with key informants. The informants were selected because they were actively involved in orchestrating ecosystem partnerships to drive business model innovation for the focal manufacturer. Interviewees were identified by snowball sampling, where key informants were asked to recommend people with experience of and insight into the research question. We interviewed various participants exercising different organizational functions to capture a multifaceted view of the process. The interviewees included roles such as digital business developers, R&D managers, platform managers, project managers, product managers, and service delivery staff. Table 1 provides a brief description of each case, the companies involved and their roles (supplier, customer, or ecosystem actor), and the focus of digital business model innovation in each case.

Description of Studied Digital Business Model Innovation Cases.

Note: AI = artificial intelligence; OEM = original equipment manufacturer.

The respondents were asked open-ended questions with the support of an interview guide. This guide was developed from themes on barriers and practices relating to digital business model innovation, business model elements, and ecosystem orchestration/involvement. For example, respondents were asked to consider questions relating to broad themes such as, How do you drive digital business model innovation in your organization? How do you involve ecosystem actors to support digital initiatives? What are the key barriers and challenges in managing an ecosystem for digital business model innovation? Which activities are critical to enabling successful ecosystem involvement? and How are different roles involved in the process? Follow-up questions were used to clarify points and obtain further details, which enabled further exploration of relevant cases. All interviews were recorded and transcribed, and the transcripts provided the basis for the data analysis.

Data Analysis

We followed a thematic approach to data analysis. 35 The first step in our data analysis was an in-depth examination of the raw data (i.e., the interview transcripts) for each case. This analysis consisted of reading every interview several times and highlighting phrases and passages related to the overarching research purpose of understanding how manufacturers orchestrate ecosystems for digital business model innovation. By coding the common words, phrases, and terms mentioned by respondents, we identified first-order categories of codes that reflect the views of the respondents in their own words. The second step of the analysis was to further examine the first-order categories across cases to detect links and patterns among them. Here, we combined insights from the literature and data in an iterative process, which yielded second-order themes representing theoretically distinct concepts created by combining first-order categories. These themes relate to key ecosystem orchestration activities and barriers relating to the business model elements (i.e., value creation, value delivery, and value capture). We performed this step in the data analysis together, which allowed us to thoroughly discuss and refine the data structure. The next step involved the generation of aggregate dimensions that represented a higher level of abstraction in the coding. Thus, the aggregate dimensions built on the first-order categories and second-order themes to present a theoretically and practically grounded categorization.

Validation of the Findings

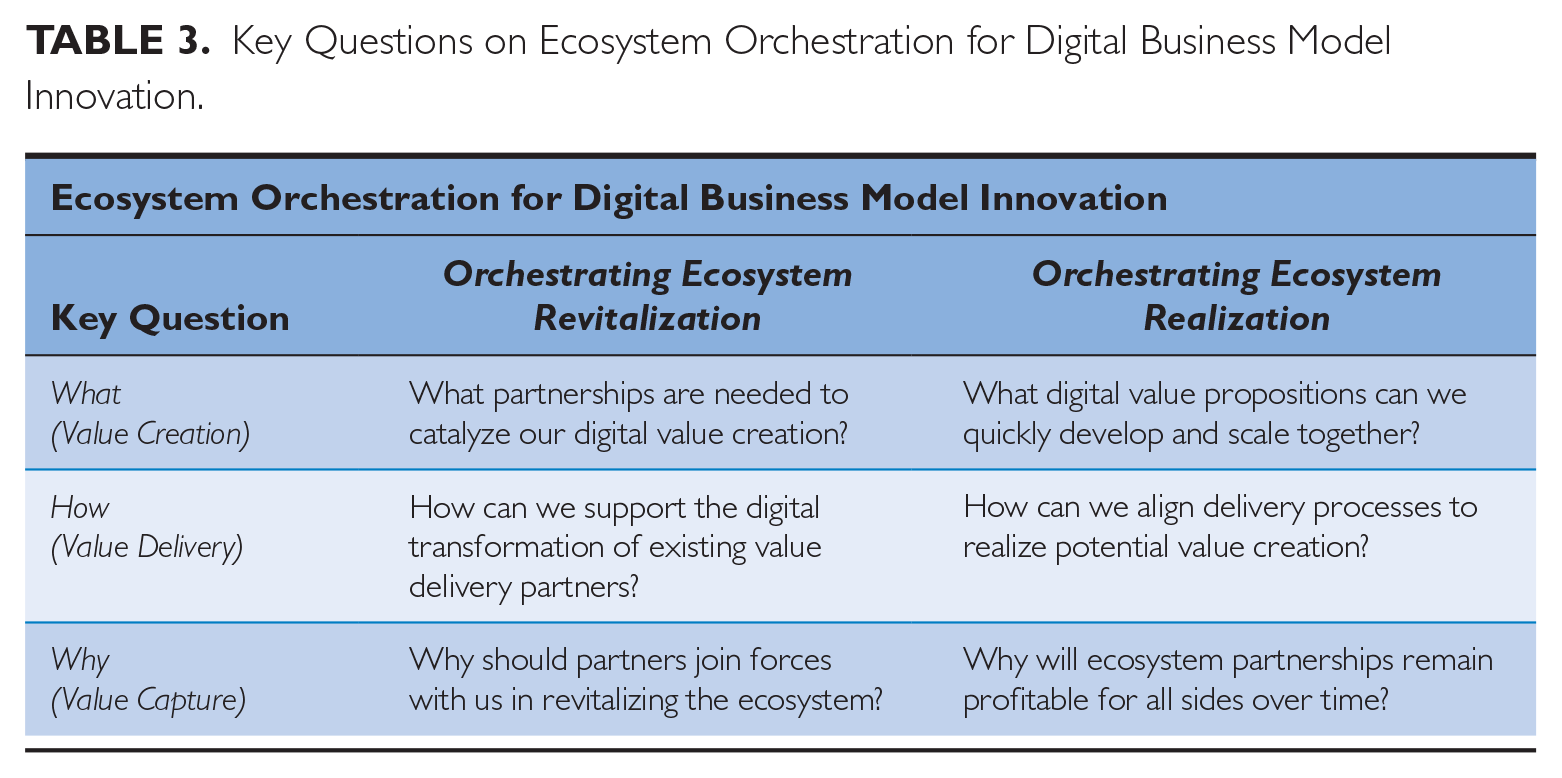

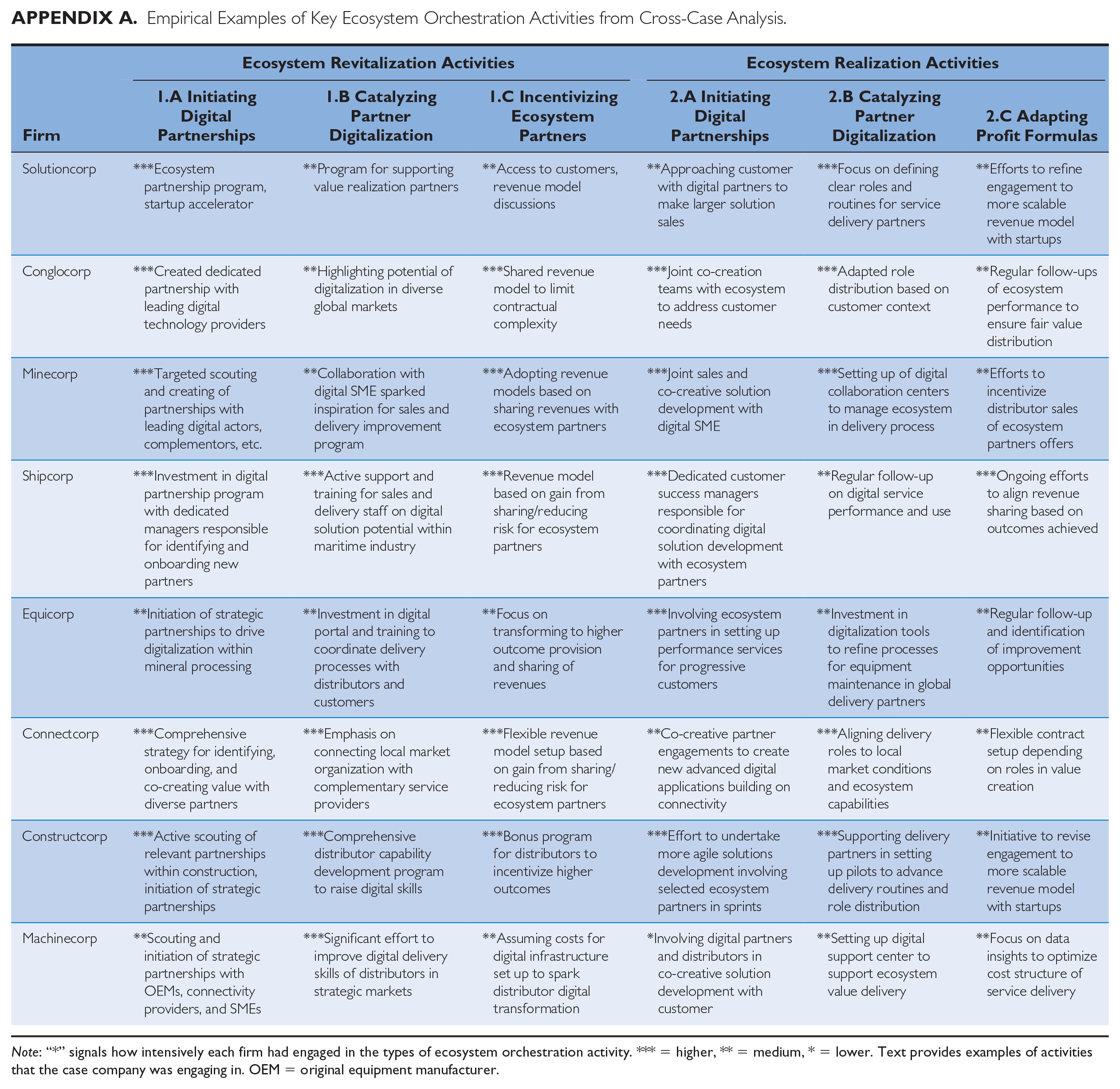

The identification of themes across the cases enabled us to develop a framework on how manufacturers orchestrate ecosystems for digital business model innovation. We compared our first draft with the processes described in the literature. We further validated the framework by means of multiple workshops with companies. In the final instance, it was discussed extensively with our research team and revised several times. Appendix A provides case examples for our core dimensions of revitalization and realization activities. To summarize our findings to progress with ecosystem orchestration for digital business model innovation, business leaders must address the business model questions of what, how, and why (see Table 3). If they do not, then the chances of breaking down their legacy business model barriers and succeeding with digital business model innovation will be low.

Barriers and Ecosystem Orchestration Activities for Digital Business Model Innovation

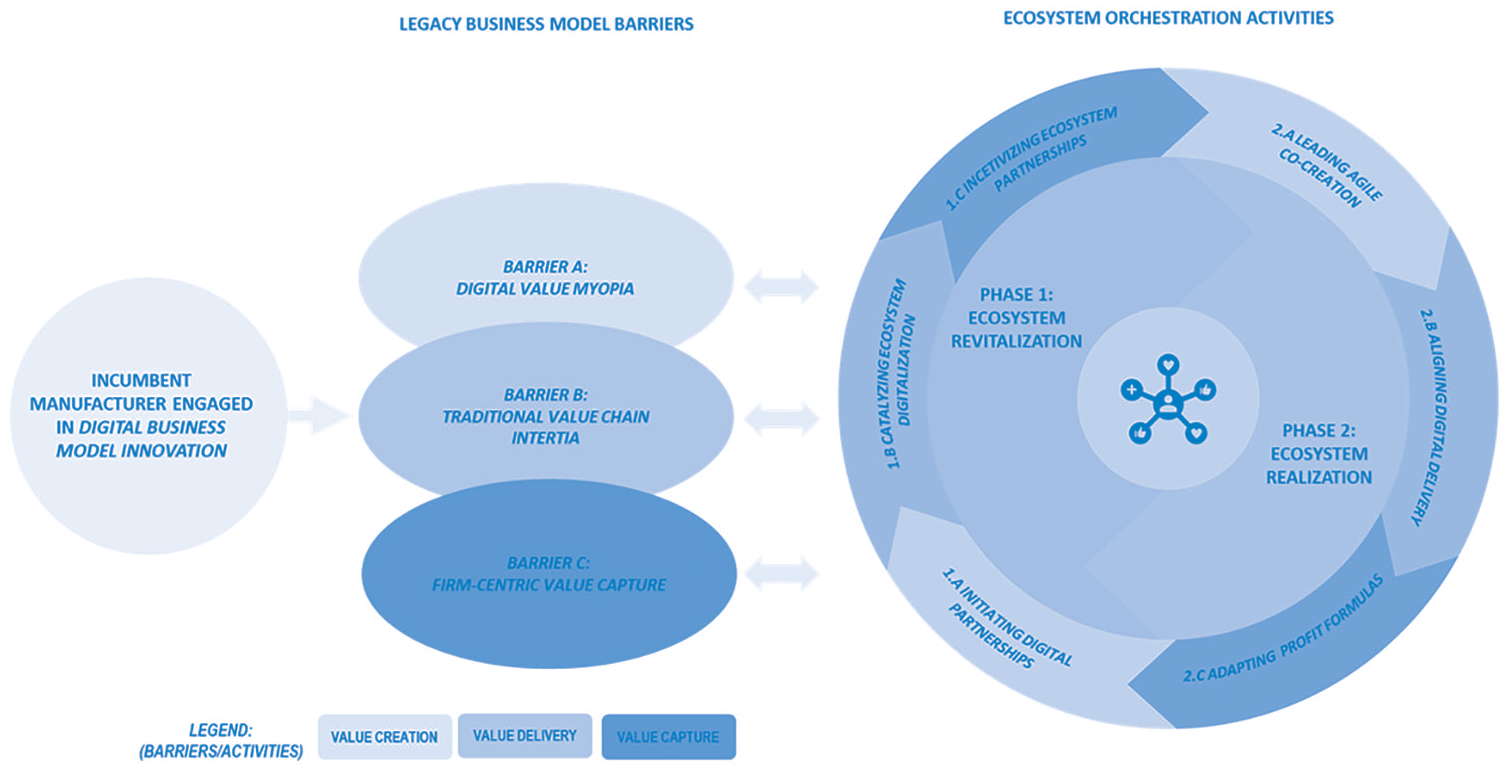

Our case studies offered relevant insights into how a manufacturer can orchestrate its ecosystem for digital business model innovation. We present these insights in an ecosystem orchestration framework for digital business model innovation depicted in Figure 1. Specifically, the framework identifies three legacy business model barriers that hamper manufacturers in their efforts to digitalize, which we label digital value myopia, traditional value chain inertia, and firm-centric value-capture logic. To break down these barriers, a manufacturer must progress through two distinct phases of ecosystem orchestration, revitalization and realization, each including specific activities. The revitalization activities relate to engaging new digital partners and supporting the digitalization of existing non-digital partners in order to begin the process of creating new digital business models. The realization activities consist of bringing these new digital business models to fruition—namely, developing, commercializing, and scaling novel digital offerings—in collaboration with ecosystem partners.

An ecosystem orchestration framework for digital business model innovation.

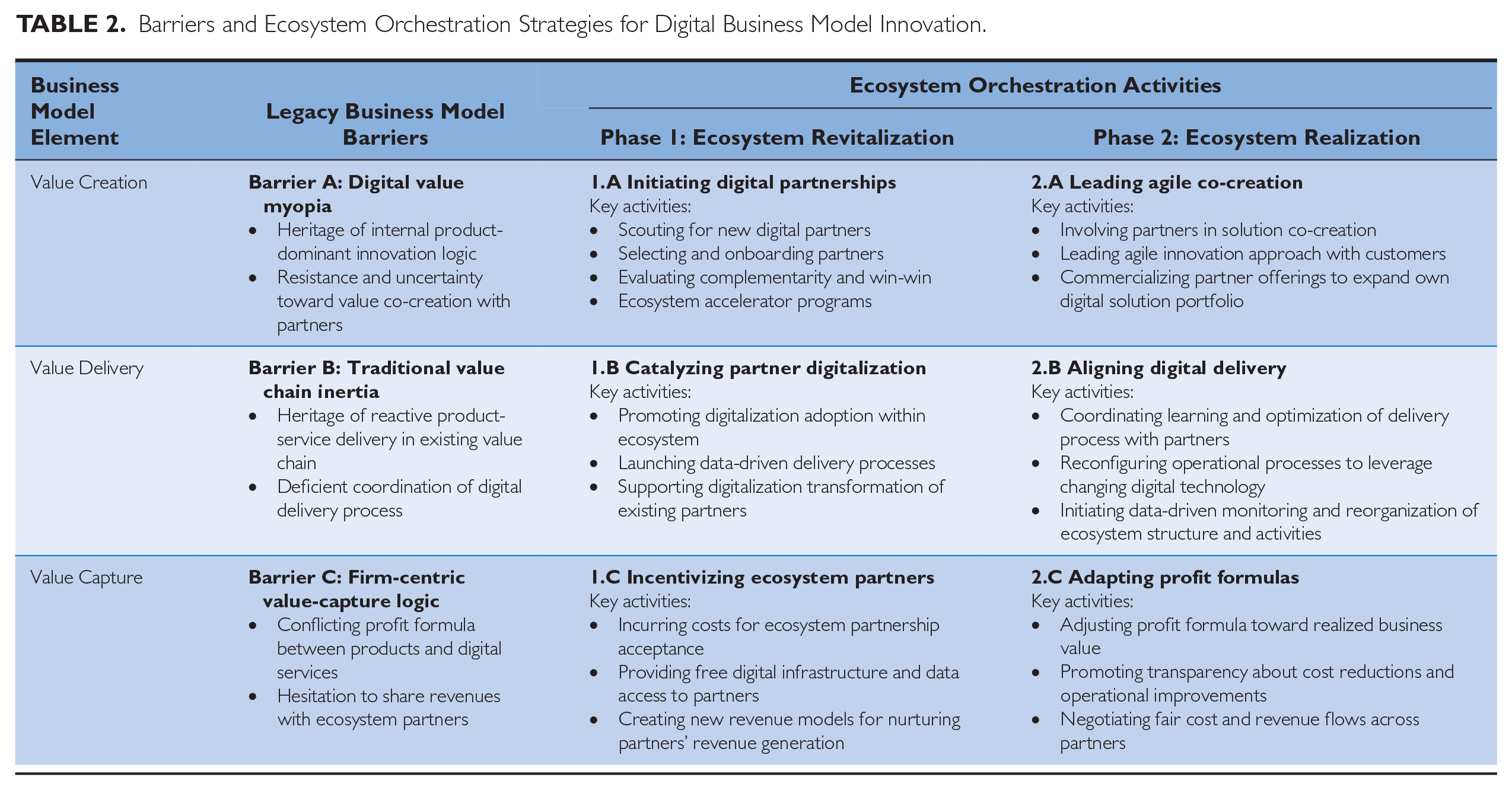

As further demonstrated in Table 2, each of the barriers relates to a specific element of the business model—value creation, value delivery, and value capture—and has corresponding revitalization and realization activities. For example, addressing traditional value chain inertia (barrier B related to value delivery) requires manufacturers to first engage in catalyzing partner digitalization (revitalization activity 1.B) and then to progress to aligning digital delivery processes across multiple ecosystem actors (realization activity 2.B).

Barriers and Ecosystem Orchestration Strategies for Digital Business Model Innovation.

Key Questions on Ecosystem Orchestration for Digital Business Model Innovation.

Legacy Barriers for Digital Business Model Innovation

A central barrier for manufacturers is digital value myopia. At the root of this barrier is a heritage of product-dominant innovation logic. The essence of how these companies have been successful is product leadership and technological sophistication, where digital components have been an enabler for products rather than new digital value propositions. Thus, many manufacturers lack the foresight to visualize the scope and logic of digital offerings. In addition, a heritage of internally focused development and commercialization means that manufacturers often face internal resistance to, and uncertainty over, value co-creation with partners. Specifically, incumbent manufacturers often have cultural issues such as “not invented here” or “not sold here” that prevent an unbiased view of the value of new digital partnerships. For example, a global product manager responsible for digital transformation at Constructcorp described the challenge of knowing how to engage with ecosystem partners on digital solutions that extend beyond their traditional competences: It seems everyone is scrambling for these new types of partnerships. We need analytics, we need to structure our data, and we need to transform our business . . . Yet, how we will set this up and work together is less clear . . . We have a strong and proud engineering culture built on mechanics and understanding material properties and our development processes are built around this. Developing software and services is something radically different, so we need to change our development approach . . . and there is an understanding that we can’t do this alone.

A central barrier for manufacturers is traditional value chain inertia. It is critical to acknowledge that, even in the digital era, manufacturers are working in existing value chains (e.g., distributors) built around sales of products and after-sales services. These actors would still exercise key roles within emerging digital business models because they maintain deep customer relationships and local delivery capabilities. Yet, shifting to increasingly digital offerings (such as predictive maintenance or machine optimization) requires fundamental changes in value chain roles and capability requirements. A key change required is the shift from a more reactive mind-set (e.g., servicing customers when they call) to a proactive one (e.g., monitoring data and analytics for signals of required action). However, this shift can often face resistance and inertia because sales and service personnel are used to working in a certain manner and may be unwilling or slow to change their ways. In addition, since the existing product-service business would still remain dominant, there is often deficient coordination in the digital delivery process. For example, while real-time analytics of the performance of connected products can deliver significant value, it is often unclear whose role it is to monitor these systems, take preventive actions, and be responsible for the realization of operational goals (e.g., the back end of the customer, distributor, or manufacturer). A product manager from Machinecorp explained the predicament of transforming the way of working in its existing value chain: If you think of our ecosystem. I think we are used to being reactive both from the distributor’s and customer’s side. When a machine breaks down, a service technician goes out and fixes it and he is the “hero.” With our digital fleet management solution, the idea is that [the technician] should monitor the machine and do the service before we have a breakdown, saving downtime and making operations predictable. But then he is no “hero,” more of a disturbance, and that is something that both distributors and technicians have had a hard time to adjust to. It’s frustrating since this is the value of our solution getting lost.

A final barrier relates to a heritage of firm-centric value-capture logic. Manufacturers are striving to increase their returns from digitalization but often fail to consider its impact on their ecosystem. For example, digital offerings often result in a value-capture logic conflict with their existing ecosystem (e.g., distributors, service partners), which is set up to derive profits from the sale of products and after-sales services (e.g., maintenance, spare parts). Specifically, digital offerings with the purpose of optimizing the use of products and reducing maintenance needs may conflict with the profit formulas of distributors, making them reluctant to actively engage in the commercialization of such offerings. In addition, many manufacturers disclosed that they, because of their heritage, had challenges perceiving how increased digital revenues should be split to construct a profit formula that would incentivize existing and new ecosystem partners. For example, several manufacturers described how their heritage of being a dominant player in their ecosystem led them to believe that new partners would conform to being paid as sub-suppliers (e.g., cost plus) rather than partners (e.g., share of revenue). This represents a key challenge because lacking an appropriate revenue model for emerging digital solutions that does not take into account the ecosystem perspective is doomed to fail. In the absence of such clarity, there is a risk of manufacturers imposing their existing business models rather than sharing revenues appropriately and fairly with existing and new ecosystem actors. This may derail efforts to get manufacturers’ ecosystems to work together in driving new profits from digital business model innovation. A digital transformation manager at Minecorp described the uncertainty over how the company and its ecosystem partners would make money from novel digital solutions: There is definitely a risk of cannibalizing our existing product business as we go for digital business models. We are geared towards sales of products and spare parts, and our digital offerings contradict this logic as the value proposition is typically about optimizing machine usage to reduce breakdowns and getting more out of existing equipment. So there is an inherent conflict here, especially as digital offerings would often entail a larger degree of profit-sharing with new ecosystem partners.

Ecosystem Revitalization Phase

As a start to the process of addressing the legacy barriers, we observed conscious efforts of incumbent manufacturers toward orchestrating ecosystem revitalization. The focus is on creating the foundations for designing digital business models by infusing digital components within the ecosystem through engagements with new and existing ecosystem partners. Key activities include initiating digital partnerships, catalyzing partner digitalization, and incentivizing ecosystem partners.

Initiating Digital Partnerships

Incumbents who seek to spark the value creation potential of digitalization dedicate immense efforts to initiating digital partnerships. This involves efforts to find ecosystem partners who can support the manufacturer’s digitalization initiatives and address the internal digital capability gaps (e.g., AI algorithm development) so that greater customer value can be created. All the manufacturers we studied have been systematically scouting for new ecosystem partnerships related to digital technologies and software (such as big data analytics, machine learning, and AI applications) to catalyze digital value creation. For example, Shipcorp had carried out a comprehensive mapping of all digital solution providers active in the maritime industry to identify potential partners. A central component is the development of an ecosystem strategy to select which partners to engage with and how to involve them in value-creation activities. This requires an additional focus on how to onboard partners by, for example, reaching an agreement on the scope of the partnership and the rules of engagement. For example, Connectcorp had created a comprehensive process for identifying, engaging, and onboarding ecosystem partners to extend their digital footprint in the industry. Indeed, manufacturers described the importance of identifying the appropriate breadth and depth of partners for the purpose of co-creating an extended portfolio of new digital value propositions. This onboarding is not limited to complementary actors, such as technology providers, but often includes partnering with other original equipment manufacturers (OEMs) or even competitors. A portfolio manager from Constructcorp described its approach to formulating a strategy for ecosystem co-creation: We have invested a lot of resources into mapping potential ecosystem configurations. We are investigating how customers are working with different players to identify opportunities and different value propositions. Then we need to connect to our strategy and see where we should partner or invest in promising startups. This is super critical for us, but also so [. . .] complex.

Informants emphasized that the best partnerships are built on identifying complementarities that can create win-win partnerships. Incumbent manufacturers hold a strong position in creating new value-creation partnerships due to their significant installed bases of equipment that provide access to data and long-term customer relationships globally. Yet, they often lack the digital infrastructure, applications, and capabilities to reap the benefits. On the other side, independent software vendors and global IT and analytics providers offer complementarities because they need access to the data, and they want to gain an understanding of customer operating conditions so that they can make use of their competencies (e.g., AI, analytics) and co-create new digital offerings. This will expand the scope of value creation beyond the capacity of any actor to achieve on its own (i.e., value expansion partnerships). A global product manager involved in digitalization at Minecorp described his company’s focused efforts to understand complementarities and the win-win potential of bringing partners into the value-creation process.

One of the most important factors is the holistic understanding of existing and potential actors on what is the win-win for each of the actors in the relationship, so that everybody knows what they are expected to do and what will be their gains, and then everybody acts accordingly.

In addition, many manufacturers had created programs to engage with innovative startups and new ventures (e.g., accelerators, hackathons) that could leverage partnerships with the manufacturer to secure access to data and customers, and to establish legitimacy in the marketplace. These initiatives offer manufacturers considerable potential for innovation and learning, but they also pose demands on speed and flexibility. For example, a strategy manager at Constructcorp described the critical importance of engaging with innovative ecosystem partners to revitalize their business model and the ecosystem as a whole: We can accelerate our learning by partnering with ecosystem partners . . . How the industry works, how the offerings works, how to offer, what the business models should be, revenue models, etc. . . . But we need to accelerate our internal processes to engage with these actors.

Catalyzing Partner Digitalization

Revitalizing the ecosystem also requires orchestrating value delivery by catalyzing the partner digitalization of actors who engage in direct contact with customers. The key focus here is promoting the adoption of digitalization within the existing ecosystem of incumbent manufacturers, such as customers, distributors, and complementors. To build a commitment to digitalization and change product-focused cultures within the existing ecosystem, manufacturers affirmed the need to exploit the competitive potential that digital solutions contain to drive a shift in the mentality and culture of the existing ecosystem and advance the digital maturity of delivery processes. For example, many companies had comprehensive programs to raise awareness of the potential of digital solutions directed at their distributors. A digital business development manager in Shipcorp recounted: We have invested heavily in promoting the need for digitalization and change in the whole shipping industry. I think the ecosystem is moving, and they see the potential of digital, but there is also a lot of skepticism as to what value can be achieved. We realize that we need to take a more active role in driving this change through initiatives, such as customer success teams and involving the whole ecosystem, even competitors, in making this happen.

In addition, we observed an increased focus on gathering, analyzing, and using extensive data sets from customer operations. This digital layer enables ecosystem partners to improve activities related to the delivery process. For example, the digitalizing manufacturing firm can, in collaboration with delivery partners, design routines for a more effective maintenance and uptime schedule. Another key aspect of ecosystem revitalization is setting up digital transformation programs for distributors and other value realization partners. Specifically, manufacturers described a need to become actively involved in developing the digital capabilities of existing ecosystem actors. For example, Machinecorp described a comprehensive program for nurturing the development of digitalization capability in local service delivery partners (e.g., distributors). More specifically, key activities that help to build digital capabilities in the ecosystem include investing in intelligent and connected digital technology, building skills in the advanced analysis of customer usage data in front-end units, and automating basic data analysis and support for service delivery. Similarly, a portfolio manager from Constructcorp explained, Our distributors can make or break many of our digital services. It does not matter how sophisticated we make our digital infrastructure or the potential value we can create. If they can’t use the systems and deliver concrete [value] to customers, we will fail . . . So a lot of attention is devoted to advance digital capabilities of our global network of distributors.

Incentivizing Ecosystem Partners

As the firms that we studied argued, a new logic for value capture is at the crux of orchestrating ecosystem revitalization. A common theme among the manufacturers studied was the need to incentivize ecosystem partners. Our informants revealed that incentivizing the ecosystem may require the manufacturer to share a disproportionate level of revenue, cost, and risk with ecosystem partners to motivate them to partake in revitalization. For example, to incentivize new value-creation partners (e.g., app providers, analytics, competitors) to join, Shipcorp was offering free access to data and infrastructure and recouping the investment from a share of the revenue generated from that data. Similar approaches were described by all the manufacturers in our study, who took on cost and risk to revitalize the ecosystem through digital investments in the first instance, and then looking to make a profitable return further down the line. A portfolio manager from Constructcorp described how the company had assumed significant cost to revitalize the existing ecosystem and create a digital foundation for new partnerships: We have taken on quite a high cost for setting up this [digital infrastructure] and connecting all of our machines to have operational data readily available free of charge for our distributors and customers . . . On the other hand, we need this data to provide a foundation for our [digital offerings] and the larger transformation of our ecosystem.

A second area of incentivizing relates to revenue models. The shift to digital offerings can enable new revenue or pricing models based on “pay per use,” achieved outcomes, or similar payment structures where the end customer pays for the value created. Manufacturers can leverage shared revenue models, such as sharing a percentage of the use/outcome revenues with partners to tie ecosystem actors more closely to their business models. These revenue models connect manufacturers and their ecosystems more closely to the actual value created for customers and necessitate increased customization and shifts in responsibility. In practice, ecosystem partners can agree on what each partner will bring to the value proposition and how the resulting revenue should be divided so that all actors are incentivized to contribute. For example, Constructcorp had experimented with a bonus system in which the distributors’ share of revenues would increase when they achieved certain outcome levels for customers. Conversely, Minecorp had designed a revenue model with a digital SME that gave higher initial sales revenue to the SME and a higher proportion of running revenues to Minecorp itself. Managers described a shift away from transactional partnerships to more relational partnerships—that is to say, highly collaborative business relationships in which all parties are equally committed to each other’s success. A sales manager from Conglocorp explained this thinking: We have found that it simplifies negotiations when we can go to the customer as a team and focus on solving their problems rather than discussing contractual details. We have built a solid relationship with [Positioning provider] and [AI and Analytics provider] and we know where we stand with broad agreements on who gets what . . . The key to me is that our model ensures that, as long as we are successful in creating value for the customer, everyone profits.

Ecosystem Realization Phase

Once the ecosystem is revitalized, the crucial challenge for incumbent manufacturers is to orchestrate ecosystem realization (i.e., realizing the value of digitalization). The focus is on developing, commercializing, and scaling digital business models by aligning ecosystem partners in customer-facing processes. Key activities include leading agile co-creation, aligning digital delivery, and adapting revenue-sharing mechanisms.

Leading Agile Co-creation

Orchestrating the realization of value creation in the ecosystems was largely ensured by manufacturers taking action in leading agile co-creation. Central to this approach is getting both existing and new ecosystem partners to work with customers on co-creation processes to quickly develop and commercialize customized digital solutions. For example, Conglocorp described how it would meet customers jointly with key digital and service partners, and how together they would identify key customer pain points for the creation of a digital transformation roadmap, which would include the co-creation of customized solutions. All the manufacturers described similar examples where partners would be involved in an agile innovation approach to make incremental digital investments (e.g., infrastructure, applications) in solving specific customer issues. For example, Solutioncorp described how the parties, instead of developing a complete mine optimization solution (solving multiple needs), would divide the solution envisaged into discrete needs and then seek to progressively solve the most pressing needs by developing specific solutions. The full mine optimization solution would, therefore, emerge flexibly over several cycles of solution development, incorporating solutions from both partners and the manufacturer, each adding a distinct value proposition to the overall solution. A digital lead at Solutioncorp described his company’s approach to developing a platform that integrated customers, distributors, and digital ecosystem partners: The objective of [our] digital journey is to solve real-world customer problems . . . We need to pinpoint customers’ problems and show that we can address them one by one over time . . . Agile development is the only way to go when delivering large-scale solutions in the new, digital world.

Incorporating an agile innovation approach into the ecosystem ensures customer focus and solution adaptability. Working jointly with an agile approach to customer problems ensures that trust develops steadily between the ecosystem partners involved, which makes it possible to address more complex problems as the relationships and digitization capability mature. For example, Shipcorp described working with an independent software startup to assess the environmental footprint of customer operations. This solution was refined over multiple sprints and was ultimately integrated and scaled as a more comprehensive solution for other customers. A common theme among the manufacturers we studied was a focus on how to maximize the use of ecosystem-partner capabilities and applications to deliver digital solutions quickly so that internal digital business model innovation efforts are catalyzed. In addition, a dedicated focus on commercializing ecosystem partners’ digital solutions allowed incumbent firms to expand their digital solution portfolios to customers and, in the process, create comprehensive digital solution footprints in the industry. Thus, a digital transformation partnership that is focused on achieving concrete results is established between all the actors involved. A digital business manager from Minecorp explained, The potential value propositions from adopting digitalization in mining are incredible. To me, it’s clear that we can never succeed by doing everything ourselves. So, we have decided that we want to be open and involve partners in value creation and promote joint offerings. This allows us to rapidly expand our solution portfolio, maintain complementary solutions, and remain flexible towards the future.

Aligning Digital Delivery

To orchestrate ecosystem realization in value delivery, manufacturers focus on aligning digital delivery. As the scope and sophistication of digital solutions increase, manufacturers will need to ensure productive collaboration internally across diverse units and with ecosystem partners to accomplish value delivery. A chief digital officer from Equicorp described how the company had been prioritizing learning so that it could actually deliver value from digitalization in collaboration with a key digital partner: Together, we’re learning how to best deliver IoT and digital offerings to help organizations improve process and performance and create data-driven businesses.

Informants noted that orchestrating the ecosystems requires revising operational processes, roles, and activities for value delivery to diverse and geographically distributed customers. For example, Solutioncorp had set up an internal service level agreement (SLA) involving ecosystem partners, defining who was responsible for which functions (e.g., data monitoring), information flows, and service levels (e.g., how frequent) to ensure clear role distribution among partners. Since the ecosystem is constantly faced with new technologies and system upgrades, the manufacturer must ensure that its own processes are updated and that the various elements of the ecosystem will complement each other over time. Indeed, a common theme among the manufacturers studied was that getting the ecosystem to work demands continuous improvement in routines and role distribution related to information flow, integration of service activities, and centralized monitoring of service processes across ecosystem actors. For example, digital solution contracts could run for two to three years and, over this delivery time, the role between actors can change and be revised. A digital transformation manager from Minecorp remarked, To truly deliver value from digitalization, we need to be more collaborative, transparent, and connected with our ecosystem partners to convert data into action.

For example, Constructcorp described how an AI-generated warning signal (e.g., risk of breakdown) from customer usage data could immediately flow through the entire system and trigger the necessary changes in spare-part levels, service staff scheduling, and automated re-routing of service plans across multiple actors in the ecosystem. A digital lead from Solutioncorp further elaborated on this point: We and our ecosystem partners have made investments in upgrading and interconnected systems to ensure that critical information and job tasks can automatically be shared when a service request is generated by customers. Our customers don’t want to interact with different actors to get their operational problems solved; we are the coordinators and need to ensure that equipment works and performance guarantees are fulfilled.

Adapting Profit Formulas

In their efforts to orchestrate realization in value capture, manufacturers described the need for adapting profit formulas with their ecosystem. Since the scope of value creation is evolving, the contributions and roles of different ecosystem actors may change, necessitating different revenue models and risk-sharing agreements to manage complex interdependencies in the ecosystems. There is, therefore, a need to continuously adapt the foundations of the partnership to maximize business value for customers and partners as necessary. For example, changes in the underlying technology could introduce significant changes in the previously agreed profit formula. Other examples demonstrate that varying customer sites and requirements influence the value creation and delivery activities, and, in turn, the value-capture conditions. For example, when Constructcorp set up its site optimization solution, the company soon realized that the digital infrastructure was underdeveloped in many customers’ sites, and so it had to significantly increase the role and revenue share for IT and connectivity providers in those particular cases. Thus, the increased uncertainty needs to be handled, and new risk-reward sharing approaches must be required. Accordingly, manufacturers are likely to spend considerable time on realigning incentives among ecosystem actors over time.

A key benefit of digitalization comes from creating transparency in ecosystem relationships and for customers by providing real-time data insights. This affords the opportunity to more closely monitor the outcomes achieved, where revenue distribution is tied to the real value. For example, Conglocorp regularly adjusted the cost and profit formula with the AI and analytics provider and position system provider based on one year of operation. Thus, such shifts require totally new negotiations on how ecosystem partnerships should be set up to create and capture value fairly and for the mutual benefit of partners. Informants stated that orchestrating ecosystem realization for the purpose of capturing value required a flexible mind-set and an ability to adapt to current realities so that fair mechanisms to capture value over time are put in place. This transparency would provide opportunities for both sides to work fairly and achieve common goals. As the head of business development at Compucorp (ecosystem actor) explained it, Business-to-business relationships are not naïve, and there is a need for transparency and fairness . . . How are you going to design revenue models when people are not willing to share the data? Ecosystem business models would need to demonstrate a clear win-win for all actors. To summarize our findings to progress with ecosystem orchestration for digital business model innovation, business leaders must address the business model questions of what, how, and why (see Table 3). If they do not, then the chances of breaking down their legacy business model barriers and succeeding with digital business model innovation will be low.

Implications for Digitalizing Business Models

This study offers several lessons for leaders in the manufacturing industry looking to digitalize their companies. Our first key message is that a simple acquisition of digital technology is not sufficient. Instead, successful digitalization is accomplished when a manufacturing company innovates its business model. This digital business model innovation consists of introducing novel ways of creating, delivering, and capturing value with the help of digital technology. Our second key message is that success with digital business model innovation can only be achieved if a company involves its ecosystem partners in the process. This involvement is neither automatic nor easily accomplished, and manufacturing companies need to consciously plan how to orchestrate the ecosystem in relation to digital business model innovation. Our study, based on the experiences of eight manufacturers and their ecosystems, proposes two progressive phases and six interdependent activities that break down three barriers to successful ecosystem orchestration (see Figure 1 and Table 2 for a quick overview).

We find that the three barriers to successful ecosystem orchestration and, consequently, to successful digital business model innovation are associated with the manufacturer’s existing or legacy business model. Each of these legacy business model barriers is deeply entrenched in the manufacturer’s existing approach to create, deliver, and capture value. The six ecosystem orchestration activities that successful manufacturers use to break down these barriers can be conveniently classified into three pairs of value creation, delivery, and capture activities, where each pair tackles one of these barriers. We further identify a temporal separation of ecosystem orchestration activities into progressive phases of revitalization and realization, where each phase ensures alignment between activities and the developing ecosystem business model. The first phase and activity in the pair, which we label revitalization activities, relates to engaging new digital partners and supporting the digitalization of existing non-digital partners in order to start creating a new digital business model. The second phase and activity in the pair, labeled realization activities, consists of bringing it to fruition—that is, developing, commercializing, and scaling this new digital business model with ecosystem partners. The three legacy business model barriers are digital value myopia, traditional value chain inertia, and firm-centric value-capture logic.

Digital value myopia is the barrier to digital value creation that represents the struggle that manufacturers face in seeing beyond the physical product design approach to which they are accustomed. A revitalization activity of initiating digital partnerships with digital natives can help manufacturers acquire digital skills and mind-sets and, therefore, break through the myopia. As they learn to “think digitally,” manufacturers can then progress to nurturing agile co-creation with digital and non-digital partners and realize the creation of an ongoing stream of new digital solutions.

The barrier to digital value delivery of traditional value chain inertia is closely related to digital value myopia. Whereas myopia is caused by the lack of digital skills in the focal manufacturing company, traditional value chain inertia refers to the lack of digital skills among existing value chain partners, which impedes implementation of the digital solution. Revitalization of the traditional value chain can be accomplished by catalyzing the digitalization of ecosystem partners or, more specifically, facilitating the digital learning of customers, distributors, complementors, and other partners through various activities and investments on behalf of the manufacturer. As the scope and sophistication of digital solutions increase, the manufacturer needs to continue to align digital delivery in order to ensure that all partners maintain the progress so that proficient delivery of new digital solutions continues to be realized.

The barrier to digital value capture of firm-centric value-capture logic is probably the least understood and yet the most salient among the legacy business model barriers. Firm-centric value-capture logic refers to the legacy value-capture system that is established to derive profits from the sale of “tangible” products and services, which conflicts with the development of an appropriate profit formula for the digital service within the ecosystem. The manufacturing company should actively revitalize its value-capture systems by incentivizing ecosystem partners in novel ways, such as “paying them with data” or creating outcome-based contracts where all partners can obtain their share of revenues and profits. Moreover, this “setting of incentives” cannot remain a one-time activity. As the digital solution evolves, the contributions and roles of different ecosystem actors may change, calling for the manufacturer to continue adapting profit formulas in order to maintain fairness in allocating returns from value realization in the ecosystem.

Theoretical Implications

These findings hold several theoretical implications. By combining the perspectives of business model innovation and ecosystem orchestration, we have shed light on how digitalizing manufacturers can overcome the barriers and orchestrate the revitalization and realization of their ecosystems. Our findings carry broad implications for research on business model innovation, 36 innovation ecosystems, 37 and digitalization. 38 First, we contribute to the literature on innovation ecosystems by highlighting the business model as an important sensemaking device for conceptualizing ecosystem orchestration activities. 39 Adopting this perspective allows for the detailing of micro-foundational orchestration activities related to how value is collaboratively created, delivered, and captured in an ecosystem context. In particular, it may advance knowledge on how a focal firm approaches the alignment of partners and secures its role in competitive ecosystems by delineating the interrelationships in key business model activities. 40 Second, we demonstrate the need for ecosystem orchestration activities to simultaneously align all business model elements in order to make ecosystems successful over time. We contribute by delineating the gradual and iterative phases of ecosystem orchestration and their corresponding logics and key activities for ensuring alignment. Essentially, this means co-evolving existing and new ecosystem relationships to ensure the “appropriateness” of the various elements of value creation, delivery, and capture in relation to one another. 41 For example, creating greater value by integrating the applications of new digital partners into advanced digital solutions (e.g., site optimization) but failing to ensure appropriate ecosystem processes for delivering that value may lead to unprofitable businesses or customer dissatisfaction. Indeed, if manufacturing companies fail to assure alignment across the dimensions of the business model within an ecosystem context, they will incur the risk of value co-destruction. 42

Managerial Recommendations

Our findings carry several implications that are relevant to both academics and practitioners, particularly senior managers who are charged with the digitalization of large incumbent firms. We offer some direct suggestions:

Revitalize your existing ecosystem to create a foundation for digital business model innovation. Focus on forming new partnerships with digital natives while guiding the digital transformation of the existing (non-digital) ecosystem. A critical, yet often overlooked, factor in achieving this involves finding new ways to incentivize key ecosystem actors. For manufacturers, this means not only identifying and onboarding appropriate partners capable of driving the innovation of digital solutions, but also finding ways to ensure they are appropriately rewarded. For instance, involving existing actors (e.g., distributors) and new (e.g., digital) ecosystem actors may require the leading manufacturer to bear the initial costs of transformation. Bearing these initial costs may be critical in order to provide novel partners (e.g., startups) with a clear path for growth and old partners with the digitalization capabilities they need, thereby providing the entire ecosystem with a digital growth path.

Coordinate the realization of digital value across the entire ecosystem. While ecosystem revitalization provides the foundations for value creation within the ecosystem, it is not enough. Manufacturers need to consciously work with their ecosystems to ensure that novel digital offerings become profitable for all parties involved. Our informants emphasized that the agile co-creation of digital solutions and joint delivery are key to ensuring a string of “small wins” so that trust and scalability can be built progressively across the ecosystem. As these small wins mount up, there is a need to align value creation and capture so that a recurring flow of revenue across ecosystem actors is assured. Thus, realizing value in ecosystems concerns not only creating new offerings but also ensuring their delivery and commercialization in an effective way. Hence, it is critical that issues of fairness, such as the sharing of revenue, are addressed early on. In fact, the manufacturers we studied referred to many failed digital initiatives arising simply from a lack of ecosystem coordination.

Create dedicated roles for coordinating ecosystem orchestration. Putting ecosystem orchestration strategy into action requires leading manufacturers to create new roles, such as “ecosystem manager,” that are responsible for developing blueprints and relationships for ecosystem revitalization and realization. For example, many of the firms we studied had created such roles with specific responsibilities concerning either existing (e.g., distributors, competitors, complementors) or new (e.g., startups) ecosystem actors. Indeed, considering the roles, incentives, and transformational properties of ecosystem partners is key. In addition, ecosystem managers hold important gatekeeping roles between the ecosystem and internal business model innovation activities. For example, as business model activities related to value, creation, delivery, and capture are shared by multiple units within incumbent firms, the ecosystem manager can serve as an important integrator and catalyst for digitalization.

Ecosystem orchestration is an ongoing and iterative process. While we have described ecosystem orchestration in two distinct phases, it is important to highlight the ongoing nature of this development cycle. Manufacturers need to progressively revitalize and realize the potential of their ecosystems in recurring loops of activity in step with ongoing developments in digital technology. For example, we have yet to fully see the large-scale implications of AI in industry. However, as the technology gains maturity, manufacturers will need to monitor potential AI partners and how they can revitalize their ecosystems to drive next-generation business model innovation. Accordingly, orchestration activities are continuous and evolving as the technology and the potential for novel digital services develop.

What are the gains to be made from ecosystem orchestration for digital business model innovation? Of course, financial and competitiveness gains are evident—our case firms are testament to these benefits. But, more importantly, having a conscious ecosystem orchestration strategy offers the additional gain of projecting to customers a progressive nature and a willingness to co-develop and co-innovate in order to maintain relevance in the future. As most customers are fearful of lock-in effects, a collaborative ecosystem approach can smooth the passage across the threshold of customer adoptions when introducing digital business models. However, the transformational needs should not be taken lightly because the “identity” of the product-centric firm built on traditional, transactional relationships has to change radically into a more software-oriented, service-oriented, and externally oriented relational-centric firm. This must be placed at the top of all manufacturing firms’ agendas—to change the focus of the organization toward leveraging ecosystems and exploiting the potential of digital business models. Thus, creating a dedicated unit with profit/loss responsibility for digital business model innovation and ecosystem orchestration may be more effective in securing the future competitiveness of the organization than merely installing an overarching digital transformation manager.

Conclusion

To succeed with digital business model innovation, manufacturers must take the lead in the revitalization and realization of their ecosystems. This article provides a framework for how best to achieve this by delineating the key barriers and how to overcome them. The framework underscores the need for ecosystem collaboration and provides recommendations for how best to proceed.

Footnotes

Appendix

Empirical Examples of Key Ecosystem Orchestration Activities from Cross-Case Analysis.

| Firm | Ecosystem Revitalization Activities | Ecosystem Realization Activities | ||||

|---|---|---|---|---|---|---|

| 1.A Initiating Digital Partnerships | 1.B Catalyzing Partner Digitalization | 1.C Incentivizing Ecosystem Partners | 2.A Initiating Digital Partnerships | 2.B Catalyzing Partner Digitalization | 2.C Adapting Profit Formulas | |

| Solutioncorp | ***Ecosystem partnership program, startup accelerator | **Program for supporting value realization partners | **Access to customers, revenue model discussions | **Approaching customer with digital partners to make larger solution sales | ***Focus on defining clear roles and routines for service delivery partners | **Efforts to refine engagement to more scalable revenue model with startups |

| Conglocorp | ***Created dedicated partnership with leading digital technology providers | **Highlighting potential of digitalization in diverse global markets | ***Shared revenue model to limit contractual complexity | ***Joint co-creation teams with ecosystem to address customer needs | ***Adapted role distribution based on customer context | **Regular follow-ups of ecosystem performance to ensure fair value distribution |

| Minecorp | ***Targeted scouting and creating of partnerships with leading digital actors, complementors, etc. | **Collaboration with digital SME sparked inspiration for sales and delivery improvement program | ***Adopting revenue models based on sharing revenues with ecosystem partners | ***Joint sales and co-creative solution development with digital SME | ***Setting up of digital collaboration centers to manage ecosystem in delivery process | **Efforts to incentivize distributor sales of ecosystem partners offers |

| Shipcorp | ***Investment in digital partnership program with dedicated managers responsible for identifying and onboarding new partners | ***Active support and training for sales and delivery staff on digital solution potential within maritime industry | ***Revenue model based on gain from sharing/reducing risk for ecosystem partners | ***Dedicated customer success managers responsible for coordinating digital solution development with ecosystem partners | **Regular follow-up on digital service performance and use | ***Ongoing efforts to align revenue sharing based on outcomes achieved |

| Equicorp | **Initiation of strategic partnerships to drive digitalization within mineral processing | **Investment in digital portal and training to coordinate delivery processes with distributors and customers | **Focus on transforming to higher outcome provision and sharing of revenues | ***Involving ecosystem partners in setting up performance services for progressive customers | **Investment in digitalization tools to refine processes for equipment maintenance in global delivery partners | **Regular follow-up and identification of improvement opportunities |

| Connectcorp | ***Comprehensive strategy for identifying, onboarding, and co-creating value with diverse partners | ***Emphasis on connecting local market organization with complementary service providers | ***Flexible revenue model setup based on gain from sharing/reducing risk for ecosystem partners | **Co-creative partner engagements to create new advanced digital applications building on connectivity | ***Aligning delivery roles to local market conditions and ecosystem capabilities | **Flexible contract setup depending on roles in value creation |

| Constructcorp | ***Active scouting of relevant partnerships within construction, initiation of strategic partnerships | ***Comprehensive distributor capability development program to raise digital skills | ***Bonus program for distributors to incentivize higher outcomes | ***Effort to undertake more agile solutions development involving selected ecosystem partners in sprints | ***Supporting delivery partners in setting up pilots to advance delivery routines and role distribution | **Initiative to revise engagement to more scalable revenue model with startups |

| Machinecorp | **Scouting and initiation of strategic partnerships with OEMs, connectivity providers, and SMEs | ***Significant effort to improve digital delivery skills of distributors in strategic markets | **Assuming costs for digital infrastructure set up to spark distributor digital transformation | *Involving digital partners and distributors in co-creative solution development with customer | **Setting up digital support center to support ecosystem value delivery | **Focus on data insights to optimize cost structure of service delivery |

Note: “*” signals how intensively each firm had engaged in the types of ecosystem orchestration activity. *** = higher, ** = medium, * = lower. Text provides examples of activities that the case company was engaging in. OEM = original equipment manufacturer.

Acknowledgements

The authors would like to thank the editors of CMR and three anonymous referees for their constructive comments.

Authors Note

Vinit Parida is also affiliated from University of South Eastern Norway and University of Vaasa, School of Management. Ivanka Visnjic is now affiliated with ESADE Business School, Ramon Llull University.

Funding

The author(s) disclosed the receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by The Swedish Governmental Agency for Innovation Systems (Vinnova), Formas, Norwegian Research Council and the Spanish Ministry of Science, Innovation, and Universities.