Abstract

Corporate social responsibility (CSR) initiatives targeting primary stakeholders are recognized for their potential to increase shareholder value (i.e., value enhancers). In contrast, CSR initiatives aimed at secondary stakeholders, such as local communities, are often regarded as value stabilizers—reducing variability in value without significantly boosting it. Drawing on instrumental stakeholder theory, we argue that community development initiatives (CDIs), an important CSR practice directed at secondary stakeholders, can enhance shareholder value when combined with effective engagement strategies. We posit that firms can strengthen positive shareholder value by engaging in long-term or business-related CDIs. Additionally, we propose that firms with strong social management capabilities can achieve greater increases in shareholder value through CDIs. Our findings suggest that secondary CSR, traditionally seen as a stabilizer, can be developed into an enhancer through effective stakeholder engagement strategies, providing clear and actionable guidance for managers to engage in secondary CSR in a financially effective way.

Keywords

Ethics and economics are not independent realms. Individuals and firms characterized by honesty, integrity, and trustworthiness can achieve and maintain a real competitive advantage in the marketplace.—Thomas Jones (Professor of Management, University of Washington)

Corporate social responsibility (CSR) refers to corporate actions that are not required by law to promote social good and go beyond the firm’s explicit transactional interests (McWilliams & Siegel, 2001). Over the past few decades, CSR has evolved from a discretionary choice to a global imperative, prompting extensive research into its impact on shareholder value (Havlinova & Kukacka, 2021). Given the often-diverging empirical findings regarding the business case of CSR, scholars have emphasized the importance of distinguishing between primary and secondary stakeholders when examining CSR’s effect on shareholder value. Primary stakeholders—shareholders, employees, suppliers, customers, and the natural environment—are integral to a firm’s viability. In contrast, secondary stakeholders include those “who influence or affect, or are influenced or affected by, the corporation, but they are not engaged in transactions with the corporation and are not essential for its survival” (Clarkson, 1995, p. 107). Under this definition, media, local communities, and diverse special interest groups (regulatory agencies, nongovernmental organizations [NGOs]) can be classified as secondary stakeholders (Eesley & Lenox, 2006; Thijssens et al., 2015). Compared to the large body of work on the business value of CSR efforts aimed at primary stakeholders, studies focusing on CSR directed at secondary stakeholders are still relatively nascent, presenting a promising area for future research.

CSR literature has predominantly focused on primary stakeholders (investors, employees, customers, suppliers) who engage in direct transactions, mainly through formal contracts, with the focal firm (C. Kim et al., 2024; Mattingly & Berman, 2006; Vasi & King, 2012). This focus stems from the perception that primary stakeholders are pivotal in formulating CSR strategies because of their direct financial impact on firms through various economic transactions (Clarkson, 1995). However, despite their potential influence, secondary stakeholders, such as communities, have received far less attention because their interactions with firms lack direct economic exchanges. As a result, CSR initiatives targeting these groups are often seen as less strategically relevant in terms of financial benefits (Hillman & Keim, 2001; Thijssens et al., 2015; Van der Laan et al., 2008; Vogel, 2010). Some researchers have highlighted the challenges that firms face in leveraging CSR aimed at secondary stakeholders to enhance firm value (Chang et al., 2014; Lu et al., 2023). As Lu et al. (2023) concluded, whereas CSR targeting primary stakeholders (primary CSR) can be regarded as a value enhancer, CSR targeting secondary stakeholders (secondary CSR) primarily acts as a value stabilizer for firms by mitigating risks and reducing value variability. Despite this, secondary CSR is increasingly recognized as essential for firms. In this research, we aim to identify effective stakeholder engagement strategies that can transform secondary CSR from a “stabilizer” to an “enhancer.” Specifically, we ask, how can firms’ CSR initiatives targeting secondary stakeholders yield financial benefits?

Instrumental stakeholder theory, a common theoretical foundation in the CSR literature, argues that ethical relationships with stakeholders can enhance firm performance (Jones, 1995). Although insightful, this theory offers little guidance on how firms should engage different stakeholder groups in their pursuit of social responsibility. This highlights the importance of understanding CSR engagement strategies—specifically, how firms engage with stakeholders to address social issues. Tang et al. (2012) emphasized the role of path dependence in CSR, noting that when a firm engages in CSR gradually and consistently, focusing on related CSR dimensions and starting with internal CSR practices, its financial performance improves (p. 1274). Drawing upon Tang et al. (2012) and related studies (Al-Dah, 2019; Bocquet et al., 2017), we argue for the significance of path dependence in developing secondary CSR strategies. We propose that three key elements jointly capture path dependence in secondary CSR engagement strategies: relatedness to the firm’s core business, long-term orientation, and social management capability. Specifically, we argue that firms can strengthen shareholder value by engaging in secondary CSR that is long-term oriented or closely aligned with their core business. Furthermore, firms with high social management capabilities can generate higher shareholder value through secondary CSR.

In this study, we focus on community development initiatives (CDIs) as an important type of secondary CSR, exploring how firms can engage in CDIs while simultaneously generating shareholder value in the U.S. context. U.S. firms, particularly in urban areas such as Los Angeles and San Francisco, have been addressing pressing community challenges such as homelessness (Anthony et al., 2019). Companies such as Google and Apple have responded with initiatives ranging from housing solutions to funding (Evans, 2019). U.S. firms are expanding their community initiatives to encompass education and infrastructure. The U.S. Securities and Exchange Commission has emphasized the importance of environmental, social, and corporate governance (ESG) commitments, particularly post-COVID-19, as seen in the rapid vaccine production by Pfizer and Moderna. This context makes the United States an ideal setting for examining the synergy between secondary CSR, community development, and shareholder value.

We first collected announcements of U.S.-listed firms’ CDIs from the LexisNexis and Factiva news databases as well as data on the social management capabilities of these firms from the Refinitiv ESG scores (formerly known as ESG ASSET4) database. Next, we gathered firm-level financial data for U.S.-listed firms with CDI announcements from the COMPUSTAT database. We conducted an event study to estimate the shareholder value of 434 CDI announcements. Additionally, we performed a regression analysis to estimate the impact of the three proposed engagement strategies on the shareholder value of CDIs. Our results show that CDIs are associated with a significant increase in shareholder value, with an average abnormal return of 0.66% within 3 days of the announcements.

Our study contributes to the CSR literature in two major ways. First, to the best of our knowledge, this is the first systematic study of path dependence in secondary CSR engagement strategies. Although considerable research has focused on primary CSR (Tang et al., 2012), studies on secondary CSR remain relatively scarce (Chang et al., 2014; Fu et al., 2022; Lu et al., 2023). Our findings offer several novel insights. Specifically, whereas Tang et al. (2012) found that relatedness positively influenced the financial value of primary CSR, we observed the opposite effect regarding secondary CSR. This difference may stem from the fact that primary and secondary CSR influence firm value through different mechanisms. Moreover, we found that a firm’s engagement in primary CSR, as reflected in its social management capability, can amplify the financial impact of secondary CSR. In other words, primary and secondary CSR are not entirely disconnected; rather, they mutually reinforce each other. Second, our findings challenge the notion that secondary CSR merely stabilizes value without contributing to firms’ shareholder value (Lu et al., 2023). Our results suggest that secondary CSR can serve as a “value enhancer” when an effective engagement strategy, recognizing path dependence in CSR is applied. In complementing prior studies, such as Tang et al. (2012), our research provides robust empirical evidence highlighting the importance of path dependence in CSR.

Theoretical Foundation

In this section, we introduce the most relevant concepts and theories to understand secondary CSR and shareholder value. In the first subsection, we provide a brief overview of CSR research, explaining core concepts and highlighting key differences between primary and secondary CSR. In the second subsection, we synthesize the literature on the relationship between CSR and shareholder value. Finally, the third subsection describes two theoretical perspectives on CSR engagement strategies, aiming to explain the boundary conditions of the relationship between secondary CSR and shareholder value. Overall, our goal is to establish a solid theoretical foundation for developing our hypotheses.

Primary and Secondary CSR

McWilliams and Siegel (2001) defined CSR as corporate actions not required by law that aim to further a social good and extend beyond the explicit transactional interests of the firm. CSR encompasses four general components: economic responsibility to investors and consumers, legal responsibility to government and law, ethical responsibility to society, and discretionary responsibility to the community (Carroll, 1979). Essentially, CSR means that, in addition to serving the interests of shareholders, firms must also serve the interests and well-being of various stakeholder groups, including employees, customers, suppliers, and communities.

CSR activities can be classified as either primary or secondary, depending on the stakeholders targeted by these activities. Primary stakeholders are those without whose participation the firm cannot survive. These stakeholders include shareholders, employees, suppliers, customers, and the natural environment (Clarkson, 1995; Starik, 1995). Primary CSR includes employee-oriented activities such as funding opportunities for further education (Mirvis, 2012) and supplier-oriented activities such as offering training and guidance on sustainable operations (Villena et al., 2021). In contrast, secondary stakeholders are those “who influence or are influenced by the corporation but are not engaged in transactions with the firm and are not essential for its survival” (Clarkson, 1995, p. 107). Examples of secondary stakeholders include the media, local communities, and special interest groups, such as NGOs (Eesley & Lenox, 2006; Thijssens et al., 2015). CDIs represent an important form of secondary CSR through which firms address pressing social and environmental issues in communities. Despite extensive research on the business value of primary CSR, studies on the value of secondary CSR, particularly in terms of its impact on firms, remain relatively limited (Aguinis & Glavas, 2012; C. Kim et al., 2024).

CSR and Shareholder Value

Since CSR emerged as a relevant management concept in the 1950s, debates have continued regarding its implications for shareholder value. On the one hand, scholars like the American economist Milton Friedman have argued that CSR represents a misallocation of corporate resources, which would be better used to serve shareholders’ interests: “The business of business is business.” On the other hand, CSR proponents, such as Thomas Jones, have argued that firms can accumulate valuable and nonsubstitutable intangible assets—such as employee commitment, reputation, and stakeholder trust—through engaging in various types of CSR activities. These assets can be crucial and indispensable to a firm’s long-term success (Jones et al., 2018). The instrumental stakeholder theory succinctly summarizes the arguments supporting CSR’s contribution to shareholder value (Jones, 1995; Jones et al., 2018). Since the 1970s, scholars from multiple disciplines have conducted hundreds of empirical studies to examine the relationship between CSR activities and corporate financial performance. Meta-analyses of these studies (Havlinova & Kukacha, 2021; Margolis et al., 2007; Orlitzky et al., 2003) have revealed an overall positive relationship between CSR and shareholder value, supporting the instrumental stakeholder theory.

It is also clear that the relationship between CSR and shareholder value is influenced by various factors. In particular, evidence has suggested that primary and secondary CSR can have significantly different implications for shareholder value (Chang et al., 2014; Godfrey et al., 2009; Hillman & Keim, 2001; C. Kim et al., 2024; Lu et al., 2023; Van der Laan et al., 2008). Compared to primary CSR, secondary CSR appears to have a more limited potential to boost shareholder value. For example, Hillman and Keim (2001) found that using corporate resources to address social issues unrelated to primary stakeholders cannot create value for shareholders. Similarly, Van der Laan et al. (2008) concluded that CSR performance related to secondary stakeholders is unlikely to contribute significantly to a firm’s financial performance. More recently, Chang et al. (2014) and Lu et al. (2023) found contrasting performance implications for primary versus secondary CSR: Primary CSR acts as a value “enhancer” by increasing shareholder value, whereas secondary CSR serves as a value “stabilizer,” reducing the variability in a firm’s shareholder value without significantly increasing it (Lu et al., 2023). How can firms transform a “stabilizer” into an “enhancer”? In other words, how can firms strategically engage in secondary CSR in a way that also contributes to shareholder value? This is the core question we aim to address in this study.

CSR Engagement: Two Complementary Theoretical Perspectives

Path dependence theory (Sydow et al., 2009) offers a valuable framework for answering this question. Among the factors that influence the relationship between CSR and shareholder value, path dependence is a central concept. It captures the idea that a firm’s historical development and decisions shape its current and future CSR practices (Bansal & Roth, 2000; Lins et al., 2017; Lockett et al., 2006). Path dependence theory emphasizes the importance of a firm’s historical trajectory and learning process in shaping future choices and outcomes (Garud et al., 2010). This suggests that the knowledge and investments a firm accumulates from CSR activities can constrain future options and influence the effectiveness of CSR engagement. In this context, Tang et al. (2012) provided systematic support for the significance of path dependence in firms’ CSR engagement strategies. They found that “firms [financially] benefit more when they adopt a CSR engagement strategy that is consistent, involves related dimensions of CSR, and begins with aspects of CSR that are more internal to the firms” (p. 1274). Building on this body of research, we propose that a CSR engagement strategy recognizing path dependence can help firms transform from a “stabilizer” into an “enhancer.”

Based on a review and synthesis of studies on path dependence in CSR engagement, we identified three factors that together reflect path dependence in CSR targeting secondary stakeholders: relatedness, consistency (long-term orientation), and social management capability. First, path dependence theory suggests that the similarities and differences among the involved activities can determine the extent of the complementary resources required and the complexity of coordination among activities (Sydow et al., 2009). When a firm engages in CSR activities closely related to its core business, it can use or reuse existing resources efficiently to conduct these activities. This phenomenon is particularly evident in so-called exploitation activities, where firms strive to maximize the use of existing resources and capabilities to develop new products or services (Cohen & Levinthal, 1990). Tang et al. (2012) found that relatedness is a key element of an effective CSR engagement strategy: Firms financially benefit more when they engage in CSR dimensions closely related to their businesses. Second, consistent CSR engagement means that a firm systematically and regularly participates in CSR activities (Vermeulen & Barkema, 2002). Path dependence theory suggests that “firms that adopt CSR engagement strategies with consistent involvement can accumulate and absorb CSR knowledge in an incremental manner, build complementary resources more systematically, and convey to their stakeholders the image of serious and persistent CSR” (Tang et al., 2012, p. 1281).

A third key concept in path dependence theory is that history matters (Sydow et al., 2009). A firm’s CSR engagement history can significantly shape its social management capability, which reflects “the skills, practices, relationships, and processes that enable a firm to improve its performance on human safety, welfare, and community development” (Huq et al., 2016, p. 20). Accumulated experiences, resources, and knowledge constitute a firm’s social management capability and can be leveraged to conduct other related activities, such as secondary CSR. In summary, we argue that an engagement strategy that recognizes these three elements of path dependency can help transform secondary CSR from a value stabilizer into a value enhancer.

Although path dependence theory provides a useful framework for understanding CSR engagement strategies from an internal resource optimization perspective, it does not sufficiently account for how external stakeholders—who lack full visibility into the firm’s internal processes, capabilities, and motivations—perceive and react to these engagement strategies. To address this gap, we integrate signaling theory to offer a complementary lens, focusing on how firms communicate their intentions and values through different path-dependent CSR strategies to influence stakeholder responses.

Signaling theory provides a valuable framework for understanding how firms convey information to external stakeholders, particularly when information asymmetry exists (Spence, 1978). In the context of CSR, signaling theory suggests that firms use CSR initiatives to signal their commitment to ethical behavior, long-term sustainability, and corporate integrity (Connelly et al., 2011). This is particularly relevant in scenarios where external stakeholders—such as investors, customers, or regulators—lack complete information about the firm’s internal processes or its genuine motivations for engaging in CSR (Eccles et al., 2014). For example, CSR reports and disclosures can serve as signals to establish trust and reputation among investors who would otherwise face uncertainty and ambiguity about a firm’s long-term ethical and financial performance. These signals help reduce information asymmetry between a firm and its stakeholders such as investors and regulators (Connelly et al., 2011; Eccles et al., 2014). Tang et al. (2012) suggested that firms adopting a CSR strategy that begins with internal dimensions and gradually expands to external ones are perceived as more authentic by the public compared to firms that adopt an external-to-internal approach. This perception leads to improved financial performance. Ioannou and Serafeim (2015) further developed this argument, suggesting that investors—who often lack direct access to internal corporate governance and sustainability practices—use CSR activities as cues to assess a firm’s risk profile and ethical standing. Consistent and credible CSR engagement signals responsible management, which improves investor confidence and potentially enhances shareholder value.

Signaling theory also emphasizes the importance of signal credibility (Santos et al., 2024) in influencing perceptions and responses from external receivers. This highlights that merely “doing good” by engaging in CSR activities, even when done well, is insufficient if stakeholders perceive these actions as disingenuous or merely symbolic (Pontefract, 2016; Yoon & Lee, 2016). To reduce skepticism and build trust, firms must convey authentic signals—demonstrating that their CSR efforts align with their values and are not superficial actions aimed solely at improving their public image, a practice often criticized as “greenwashing.” Greenwashing refers to the gap between overstated CSR communication and limited substantive efforts to address significant environmental and societal issues. By exploiting information asymmetry, firms may resort to greenwashing in an attempt to signal positively and improve their reputation, legitimacy, and financial performance (Berrone et al., 2017; S. Kim, 2019). However, scholars have warned that stakeholders may react negatively to symbolic CSR initiatives, potentially undermining the firm’s financial performance (Walker & Wan, 2012), especially when local environmental regulations and media coverage reduce information asymmetry (Li et al., 2023).

An engagement strategy for secondary CSR that incorporates the three elements of path dependence—relatedness, consistency (long-term orientation), and social management capability—can send different signals to shareholders and influence shareholder value. Although signaling theory asserts that consistency (long-term orientation) and strong social management capabilities positively signal genuine, long-term commitment, it diverges on the issue of relatedness. From the signaling theory perspective, unrelated secondary CSR efforts may be perceived as evidence of a firm’s genuine commitment to societal good rather than as symbolic actions solely aligned with business interests and reputations. This perception could help build an image of true social responsibility and ethical integrity, potentially increasing shareholder value. In short, path dependence theory and signaling theory offer different predictions regarding the impact of various secondary CSR engagement strategies on shareholder value. We will draw on these two perspectives to develop hypotheses for CSR engagement strategies.

Community Development Initiatives

CDIs are designed to address societal challenges, such as poverty and education deficits, within communities (Eweje, 2006; McLennan & Banks, 2019). Although CDIs do not directly target primary stakeholders, recent studies, such as those by Jones et al. (2018), have suggested that CDIs may have substantial implications. This form of secondary CSR could strengthen firms’ relationships with primary stakeholders and generate intangible assets, such as trust, reputation, and goodwill. These assets cultivate valuable relational bonds that are not directly available in the market (Sharma & Vredenburg, 1998). In this regard, Godfrey et al. (2009) found that secondary CSR was more effective than primary CSR in enhancing firms’ financial performance.

Another stream of literature has emphasized strategic partnerships among firms, governmental entities, and nonprofit organizations as an emerging trend in corporate responses to social challenges. Shaikh and Levina (2019) and Eweje (2006) discussed how these collaborations help address poverty, education, and health care gaps while fostering conditions for economic growth. The increasing support of local enterprises by large firms suggests that CDIs can effectively catalyze sustainable community development.

Recent literature has also highlighted the growing emphasis on CDIs in the United States. Gunawan et al. (2020) documented the increasing practice of disclosing community development activities in firms’ annual sustainability reports. In the wake of the COVID-19 pandemic, corporate efforts to support local health care, education, and economic infrastructure have noticeably increased. Margherita and Heikkilä (2021) suggested that this intensified involvement could significantly affect corporate performance metrics, including financial performance. Collectively, these developments offer a robust theoretical and empirical foundation for our research, further elucidating the relationship between CDIs and the creation of shareholder value. In the next section, we use CDIs as a representative form of secondary CSR to develop our hypotheses.

Hypotheses

CDIs and Shareholder Value

Instrumental stakeholder theory (Barnett, 2007; Jones, 1995) is one of the main theories regarding the business case of CSR, including both primary and secondary CSR. This theory posits that the primary value of CSR practices lies in cultivating effective, cooperative relationships with key stakeholder groups, which can lead to valuable intangible assets crucial for gaining and maintaining a long-term competitive advantage. Therefore, using corporate resources to address social issues that are not directly related to primary stakeholders may not create such a competitive advantage (Hillman & Keim, 2001; Van der Laan et al., 2008). Because CDIs typically address social issues such as poverty, underemployment, and lack of educational resources in the firm’s local community (Eweje, 2006; McLennan & Banks, 2019), their connections to the firm’s primary stakeholder groups appear weak. This weak connection may explain the lack of significant relationships between secondary CSR and firm (financial) performance.

However, Jones et al. (2018) recently extended instrumental stakeholder theory to propose that a firm’s relationships with secondary stakeholders, such as the local community, can potentially become a source of competitive advantage. Unlike a firm’s relationships with primary stakeholders, which are typically characterized by high levels of contract specificity and formality, relationships with secondary stakeholders tend to be more relational than contractual (Jones et al., 2018). Consequently, cultivating close relationships with secondary stakeholders can be a challenging but ultimately rewarding endeavor. The intangible assets embedded in these relational bonds—such as trust, goodwill, and cooperation—cannot be directly obtained from the market. These intangible assets are largely path-dependent because they can only be developed through close collaboration over time (Jones et al., 2018; Sharma & Vredenburg, 1998).

The CSR literature has provided limited evidence of the strategic value of secondary CSR. For example, Godfrey et al. (2009) found that CSR practices benefiting primary stakeholders did not lead to improvements in corporate financial performance; however, altruistic CSR directed toward secondary stakeholders significantly contributed to financial performance. Recently, researchers (C. Kim et al., 2024; Lu et al., 2023) have described secondary CSR as a “value stabilizer” that can reduce the variability of a firm’s shareholder value in the face of negative events. Considering recent developments in instrumental stakeholder theory and emerging empirical evidence, we argue that shareholders are likely to view a firm’s CDIs as a valuable use of resources because these initiatives strengthen relational bonds with the local community. In other words, a value stabilizer can evolve into a value enhancer, a process that requires an effective CSR engagement strategy. Thus, we hypothesize the following:

CDIs: Long-Term Versus Short-Term Orientation

An effective CSR engagement strategy must account for path dependence in stakeholder interactions. A firm cannot expect to cultivate strong, trusting relationships with stakeholders in a short period through ad hoc initiatives. This raises the issue of consistency in CSR engagement, specifically the temporal dimension of path dependence (Tang et al., 2012). The umbrella of CSR includes a broad range of activities aimed at addressing complex social and environmental issues such as pollution, inequity, and human rights violations (Cheng et al., 2014; Van Tulder et al., 2009). CSR initiatives range from ad hoc donations and small projects to long-term environmental programs, employee benefits, and community activities. Among these, CDIs stand out. These initiatives often cater to the developmental aspirations of impoverished and marginalized communities struggling with issues such as poverty, inadequate employment, and poor educational resources (McLennan & Banks, 2019). Ad hoc donations by individuals or firms may not contribute to the fundamental resolution of these issues, even if they offer short-term relief. In contrast, long-term engagement with secondary stakeholders, including firms with sufficient slack resources, is essential for addressing long-term community issues (McLennan & Banks, 2019; Servaes & Tamayo, 2013).

Following path dependence theory, we argue that the impact of CDIs on shareholder value depends on their time-based orientation—whether they focus on long- or short-term goals. A long-term orientation toward CDIs represents a deliberate, strategic investment in comprehensive, enduring community development projects aimed at securing sustainable social advancement. In contrast, a short-term orientation often leads to sporadic and immediate actions that prioritize quick benefits or reputational enhancement over a structured strategy for lasting community impact. We contend that a long-term orientation is crucial for an effective CDI engagement strategy because such an approach is necessary to address persistent local community issues (McLennan & Banks, 2019). In this regard, Tang et al. (2012) found that consistency is a key characteristic of effective CSR engagement strategies that can help firms benefit financially from CSR. They suggested that firms should engage in CSR activities systematically and regularly. Additionally, Tang et al. (2012) argued that a long-term orientation toward CSR strategies enables firms to gradually build CSR knowledge, systemically accumulate related resources, and demonstrate commitment to CSR, compared to inconsistent or spur-of-the-moment efforts (Husted & Salazar, 2006; Vergne & Durand, 2010). From the signaling perspective, ad hoc, inconsistent CDIs may signal that firms are engaging in unplanned, random, or opportunistic actions. Inconsistency may suggest that a firm’s CDI engagement is merely window-dressing or a response to external pressure following a negative event (Tang et al., 2012; Vermeulen & Barkema, 2002).

We argue that short- and long-term CDIs have different effects on a firm’s relationships with stakeholders, following both path dependence and signaling theories. Long-term CDIs deliver stronger signals to the firm’s stakeholders, who are more likely to trust and cooperate with the firm. Compared to short-term CDIs, long-term CDIs are more effective in leveraging experience and existing resources to boost stakeholder confidence in a firm’s credibility and authenticity in community development. Taken together, we argue that a long-term orientation is a key characteristic of effective CDI engagement strategies that can trigger positive shareholder responses.

CDIs: Relatedness to the Firm’s Core Businesses

Path dependency theory (Sydow et al., 2009) provides a useful framework for understanding the implications of maintaining established practices and routines versus exploring unfamiliar and experimental activities. This theory suggests that the similarities between the activities a firm engages in and its core businesses may determine the required complementary resources and the complexity of coordinating those activities. CDIs can be categorized based on resource requirements and targeted interest groups: (a) job creation, (b) education, (c) health care, and (d) social investment (Meade, 2021). However, a firm may also undertake a CDI initiative that requires resources and capabilities that are not readily available within its core business. Tang et al. (2012) defined “relatedness” as “the similarities in the resources, skills, and knowledge required by different CSR dimensions in which a firm engages” (p. 1280). We argue that the degree to which CDIs are related to a firm’s core business plays a crucial role in influencing their effects on shareholder value.

To some extent, a firm can be seen as a bundle of resources that can generate various outcomes (Wernerfelt, 1984). If CDIs can be grouped based on the similarities and differences in their resource requirements, it would be more resource efficient for a firm to engage in CDIs closely related to its core business and utilize similar resources (Tang et al., 2012; Vermeulen & Barkema, 2002). According to path dependence theory, CDIs that align with a firm’s core business resources are more likely to create synergies, leading to more efficient use of those resources. When a firm’s CDIs are closely connected to its core business, they can leverage the tacit knowledge accumulated from experiences. This enables the firm to engage in CDIs in a more resource-efficient manner, using both tangible and intangible resources (Kor & Mahoney, 2000; Teece et al., 1997). From a path dependence perspective, CDIs closely related to a firm’s core businesses are likely to trigger positive shareholder responses because shareholders will view these initiatives as efficient uses of firm resources that generate broader social value. This leads to the following hypothesis:

Whereas path dependence theory emphasizes resource efficiency and synergy by engaging CDIs closely related to the core business, signaling theory offers a different perspective on the impact of the closeness of CDIs on shareholder value. Signaling theory posits that firms use visible activities, such as CDIs, to communicate their values and long-term commitments to external stakeholders, particularly in situations where there is information asymmetry (Spence, 1978). In other words, shareholders, customers, and other external observers cannot easily observe a firm’s internal motivations or processes, so they rely on visible actions (e.g., CDIs) to assess the firm’s authenticity and ethical standing (Connelly et al., 2011). From the signaling perspective, CDIs that are less closely related to a firm’s core business may have a more positive effect on shareholder value because they send a stronger signal of authentic social responsibility commitment, even if they are not the most resource-efficient. In contrast, CDIs that are closely related to a firm’s core business are likely to be seen as symbolic actions or greenwashing—where firms engage in activities that appear environmentally or socially responsible but are primarily designed to create a misleading impression of the firm’s commitment to these values (Bothello et al., 2023). Greenwashing is often done to appeal to stakeholders such as customers, investors, and the public without making substantive efforts or investments to address broader issues. Therefore, CDIs that are closely related to a firm’s core business might be perceived by investors as low-investment, low-effort initiatives that avoid addressing broader societal concerns, which could demonstrate a firm’s lack of genuine concern for broader environmental and societal issues (Fu et al., 2022). As a result, shareholders may lose confidence in the firm’s long-term ethical stance and commitment. Accordingly, we propose the following competing hypothesis for H3a:

CDIs: The Role of Firm Social Management Capabilities

The historical dimension of path dependence manifests in a firm’s social management capability, which refers to “the skills, practices, relationships, and processes that enable a firm to improve its performance on human safety, welfare, and community development” (Huq et al., 2016, p. 20). The development of social management capability requires a more hands-on approach because of the complexity and path dependency of most, if not all, social issues (Huq et al., 2016). As a result, firms develop their social management capabilities mainly through direct participation and gaining firsthand experience and knowledge. As such, these capabilities are mostly path-dependent and competitively valuable because competitors cannot easily imitate them within a short time (Aragon-Correa & Sharma, 2003; Sharma & Vredenburg, 1998). Because CDIs fall squarely within the social dimension of CSR (Meade, 2021), we contend that a firm’s knowledge and capabilities accumulated through participation in addressing social issues can be instrumental in shaping an effective CDI engagement strategy. By engaging in social issues, a firm develops its social management capability, which can help it leverage issues specifically related to community development more effectively.

Social issues often have complex causes rooted in social, economic, and institutional environments (Bansal et al., 2014; Villena et al., 2021). Direct participation in addressing these salient social issues is an effective and even necessary approach to gaining an in-depth understanding of the root causes of issues such as poverty and underemployment. More importantly, working with relevant stakeholder groups enables firms to gain insights and knowledge that would otherwise be inaccessible to outsiders (McLennan & Banks, 2019). To some extent, the concept of social management capability, as Huq et al. (2016) defined, provides a concise and accurate reflection of a firm’s maturity in addressing broad social issues. A firm’s social management capability reflects its accumulated experience, knowledge, insights, and skills related to social issue participation. These capabilities are largely path-dependent and socially complex because they cannot be readily obtained from the labor or resource market (Huq et al., 2016). If a firm has developed a high level of social management capability through experience, it will likely engage in CDIs more efficiently and effectively. As a result, shareholders are likely to respond more positively to such CDIs because they may have greater confidence that firms with adequate social management capabilities can pursue CDIs in a resource-efficient and effective way.

From the signaling theory perspective, a firm’s social management capability serves as a strong signal of its credibility and commitment to social issues. Given that shareholders often face information asymmetry, they cannot directly observe how efficiently a firm manages its CDIs or the motivations behind them. However, firms with a high level of social management capability, developed through prior engagement in social issues, can signal their expertise and ability to address complex social challenges effectively and resourcefully. Shareholders and other external stakeholders may interpret a firm’s established social management capability as an indicator of authentic and committed CSR engagement, reducing concerns about potential greenwashing or symbolic CSR actions. When firms demonstrate a long history of successful engagement in social and environmental causes, they signal genuine dedication to community development, enhancing their reputations and trustworthiness (Eccles et al., 2014; Tong et al., 2018). Furthermore, the accumulation of skills, knowledge, and stakeholder relationships in addressing social issues reflects the firm’s ability to manage these complex issues effectively, signaling that the firm can be trusted to implement CDIs successfully. Taken together, path dependency and signaling theory predict that a firm’s social management capability enhances the relationship between CDIs and shareholder values.

Methods

Sample and Data

In this study, we explore the financial impact of CDIs as an important form of secondary CSR. Therefore, we employed the event study method to estimate the stock market reaction to CDI announcements. The foundation of the event study is the efficient market hypothesis, which assumes that a firm’s stock price will quickly adjust in response to new market information (Bilgili et al., 2017; El Nayal et al., 2020; Slangen et al., 2017). A firm’s stock price will increase (or decrease) if the market perceives information that may positively (or negatively) affect the firm’s future cash flow (Fan et al., 2020). Changes in stock prices, in turn, will affect shareholder value.

Our event study began by collecting news announcements related to CDIs. We first obtained a list of publicly traded U.S. firms from the COMPUSTAT database. We focused on publicly traded firms because stock prices and firm-level financial information were available only for these companies. Following previous studies (Konchitchki & O’Leary, 2011), we used the academic LexisNexis and journalistic Factiva databases to identify CDI-related news announcements.

Compared with other well-recognized dimensions of CSR, such as environmental sustainability and employee well-being, CDI is an emerging concept (Muthuri et al., 2012). We followed the ISO 26000 definition—a standard developed by the International Organization for Standardization (ISO) that provides guidance on social responsibility for all types of organizations—and developed a preliminary set of keywords to collect CDI announcements from various publications. Specifically, based on the four high-level dimensions of CDI (education, health care, social investment, and job creation) outlined in ISO 26000, we identified valid news announcements related to corporate CDIs. We carefully reviewed these announcements, identifying additional keywords and valid phrases commonly used to describe CDIs. We iterated this procedure and eventually created a comprehensive list of keywords that covered all CDI dimensions described in ISO 26000, including useful subdimensions under each of the high-level dimensions. This approach helped us capture a broad range of relevant CDI news. We searched the headlines and lead paragraphs of news announcements (Jacobs et al., 2010), consistent with prior studies that used the same identification approach for event studies (Cheung, 2011; Hendricks et al., 2015; Orzes et al., 2017; Podrecca et al., 2021). The full list of keywords used in the search is provided in Supplemental Appendix Table A.

We downloaded all the news announcements from the databases after completing the keyword search and carefully reviewed the full text of each announcement to verify its alignment with the CDI definition. We also hired and trained three postgraduate students to assist with double-checking the content validity of the identified sample. In addition, we eliminated the following types of announcements: (a) announcements made by privately held firms and (b) multiple announcements released by the same firm within a time frame of five trading days (we retained only the earliest announcement in the sample). We eliminated these announcements because the event study results could have been confounded with multiple announcements. We also eliminated duplicate announcements in multiple publications. In such cases, we retained only the earliest announcement. The final sample consisted of 434 valid announcements from 212 publicly traded firms. An overview of the sample collection procedure is provided in Supplemental Appendix Table B.

The sample covered a 17-year period (2007–2023) and included firms with 44 unique two-digit Standard Industrial Classification (SIC) codes. Supplemental Appendix Table C displays the year distribution, and Supplemental Appendix Table D shows the top 10 industries from which the announcements originated. No single year or industry comprised more than 15% of the announcements, ensuring that the samples were not heavily concentrated in any particular year or industry.

Event Analysis

We defined day 0 as the event date when a firm announces a CDI. We aimed to capture the change in stock prices following the announcement. Specifically, we used a 4-day window (day 0–3) to estimate the stock price change, which was sufficient for the information to reach the shareholders. However, a firm’s stock price can also be affected by unsystematic market fluctuations. For example, an advanced market index may drive an individual stock’s price to increase. To account for this confounding effect, we applied a market model to calculate the abnormal returns associated with CDI announcements (Lee & Park, 2016). This market model offers a robust estimation of the relationship between the stock market index and firm returns (Brown & Warner, 1985; Moses et al., 2018). Specifically, we calculated the abnormal return of firm i on day t (AR it ) as follows:

where Rit and Rmt represent the actual returns of firm i and market index m on day t. We collected these data from the Center for Research in Security Prices (CRSP) database. We estimated ai and bi based on the regression coefficients of αi and βi from:

where Ri(−210, −11) is the return of firm i, and Rm(−200, −11) is the return of market index m from day −210 to day −11. Previous researchers have commonly used the 200-day estimation window (Jacobs et al., 2010; McWilliams et al., 1999). The estimation window ends on day −11, allowing a distance between the estimation window (day −210 to −11) and the abnormal return window (day 0–3), which can mitigate concerns regarding estimation bias (i.e., the announcement may confound the estimation when two windows overlap or are too close to each other). We then calculated the cumulative abnormal return (CAR) by adding all the daily abnormal returns from day 0 to 3. The mean abnormal return for day

where

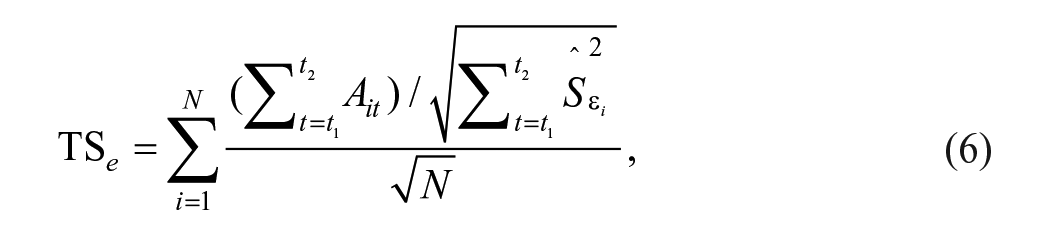

We used a t-test to determine the statistical significance of the mean abnormal return. CAR for a given time period

The test statistic

One might argue that information on CDI could leak through informal channels prior to the focal firm’s official announcement of the CDI. We addressed this concern by examining CAR from day −10 to −1 and found that the CAR is not statistically different from zero (p > .1), suggesting that information leakage was not a serious concern. We also examined the alternative CARs by including the days prior to the announcement (i.e., day −3, −2, and −1) to account for any information leakage.

In separate analyses, we used the market-adjusted model and the Fama–French three-factor model as alternative estimation methods for testing the CAR. The results remained unchanged, further showing that they were insensitive to different estimation models.

H2 to H4 propose that the impact of CDI announcements on shareholder value (captured by abnormal CAR in the estimation) can be influenced by three characteristics of CDIs: long-term oriented, related to the firm’s core business, and the focal firm’s social management capability. The regression analysis used the CAR from day 0 to 3 as the dependent variable. We measured the three variables as follows:

Long-Term-Oriented

We coded this variable based on the full description in the announcement. Specifically, if the CDI explicitly indicated that the focal firm would invest long-term (e.g., over several years) effort to implement a specific CDI practice, we considered the CDI to be long-term oriented and coded it as 1; otherwise, we coded it as 0 (i.e., a CDI that is short-term oriented, e.g., one-off donation). The rationale is that long-term orientation in CDI increases stakeholders’ perceptions of the credibility and level of engagement in the initiative (Flammer & Bansal, 2017). Examples of long-term-oriented CDIs include the following:

“In 2014, GE Announced a $20MM Commitment to Maternal and Child Health Programs in Africa to Demonstrate Long-Term Commitment to Advancing Millennium Development Goals 4 (Reduce Child Mortality) and 5 (Improve Maternal Health).”

“In 2012, Lear Corporation Teamed Up With Detroit Public Schools for a Comprehensive New Three-Year Student Tutoring Program to Strengthen Educational Pathways and Lifelong Learning.”

Relatedness to Core Business

We coded this variable as 1 if the specific CDI was related to the focal firm’s core business, and as 0 otherwise. In doing so, we carefully read the description of the CDI and identified the major activities (e.g., equipment donation and skill training) involved in the CDI announcement. Moreover, we downloaded the focal firm’s 10-K annual report to understand its core business. Thereafter, we compared the major activities in the CDI announcement and decided whether they were related to the focal firm’s core business or not. Specific examples in which the CDI announcements are relevant to the focal firm’s core business include the following:

“In 2010, Microsoft Was Donating Grants for Purchasing Computer Hardware and Software to Two Schools in the U.S.”

“In 2007, QUALCOMM Was Providing Communication Devices and Services to Schools in Guatemala.”

Social Management Capability

We measured the sample firm’s social management capability using the social pillar score developed by the Refinitiv ESG (previously known as the Thomson Reuters ASSET4 database). This indicator, which reflects a firm’s historical social management capability, has been widely used in previous literature (Fan et al., 2021; Luo et al., 2015). We used the 1-year lag of this variable to mitigate the reverse causality issue in our analysis.

Control Variables

We included several control variables to increase the robustness of our analysis. We controlled for firm size using total assets (natural logarithm transformed). We then measured firm performance using return-on-assets (ROA). We also included annual sales growth to control for firm growth as well as firm age to control for firm inertia. In addition, we included the quick ratio to control for a firm’s liquidity and its ability to finance CDI without compromising operational stability. These firm-level factors may relate to the firm resources that affect the effectiveness of CDIs.

Furthermore, we included the score of board independence (collected from Thomson Reuters) to control for the firm’s board governance and the percentage of institutional ownership to control for the ownership structure. We also included the gender diversity score to control for the diversity of the top management team. We included executive education, measured by executives with postgraduate degrees (collected from COMPUSTAT), as a proxy for managerial ability (Wiersema & Bantel, 1992). These governance factors may influence the quality of the planning and implementation of CDIs.

We also controlled for the CSR committee, which indicates whether the firm had a dedicated committee for managing social responsibility activities. Additionally, we controlled for the sample firm’s CSR transparency by including the variable CSR reporting, which measures the level of detail and transparency of the firm’s published CSR report. We collected data on CSR committees and CSR reporting from the Thomson Reuters ESG database, which standardizes these two variables according to the firm’s industry and converts the variables into a score ranging from 0 to 100. These CSR practice factors may enhance investor confidence when CDIs are implemented.

Unless otherwise noted, all control variables are lagged for 1 year to mitigate possible reverse causality. In addition, we included the event year to control for potential confounding effects (e.g., macrolevel economic policy changes) caused by time. We created a set of dummy variables for the four types of CDI discussed earlier: education, health care, social investment, and job creation. We clustered the firms based on their industry (using the four-digit SIC code) in the regression estimation to control for industry-specific factors and ensure robust standard errors. A summary of the variables is presented in Table 1.

Summary of Variables.

Note. CDI = community development initiatives; IPO = initial public offering.

One may argue that the significant impacts captured in our regression analysis could be due to selection bias. For example, firms led by managers with a strong sense of social responsibility may be more likely to initiate CDIs, and these firms may also be longer-term oriented, resulting in better social performance. To mitigate these concerns, we performed Heckman’s two-stage analysis. Specifically, we included the inverse Mills ratio, estimated in the first stage of Heckman’s model, as an additional control variable to correct for potential selection bias. The steps for generating the inverse Mills ratio variable are provided in Supplemental Appendix E. Our regression model for testing H2 to H4 is as follows:

where

Results

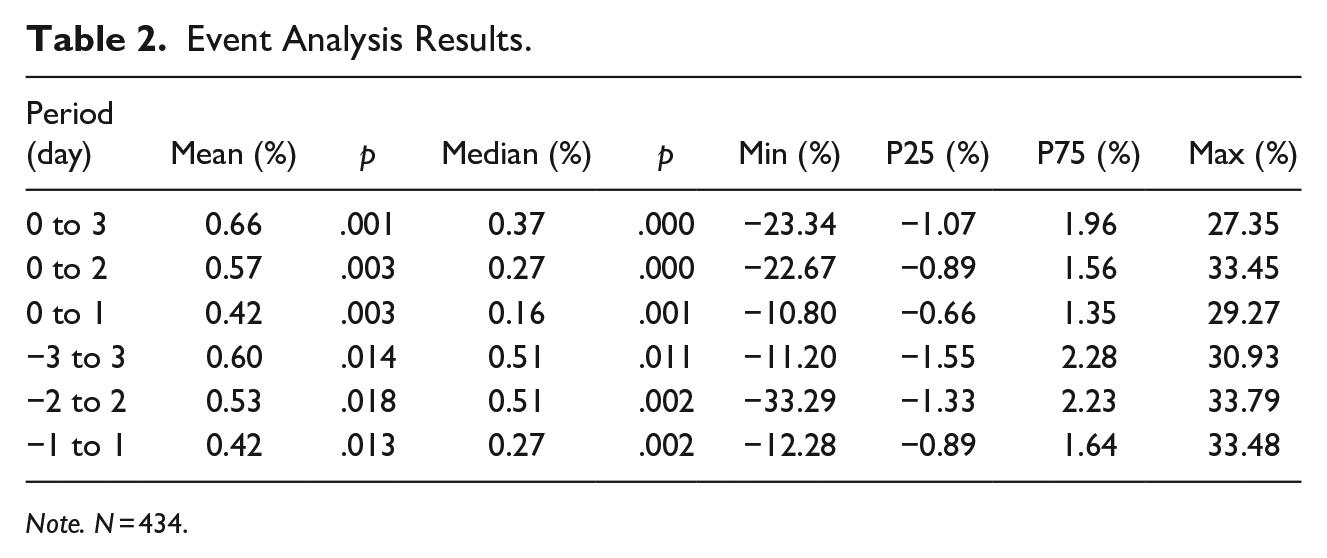

We present the event analysis results for testing H1 in Table 2. The parametric paired t-test showed that the mean CAR from day 0 to 3 was significant and positive (0.66%, p = .001). To check the robustness of these results, we also performed the nonparametric Wilcoxon signed-rank (WSR) test. Although the WSR test has lower statistical power, it does not assume a normal distribution, which is common for event study variables (Corbett et al., 2005). The WSR test shows that the median CAR from day 0 to 3 is also statistically significant and positive (0.37%, p < .001), indicating that the results are robust for both parametric and nonparametric statistical analyses. The average market capitalization of the sample firms is 75.071 million USD, and the mean (median) abnormal increase in firms’ value from day 0 to 3 is 495.47 (277.76) thousand U.S. dollars, underscoring an economically significant impact. The results also show that the effects of CDI announcements can be captured as early as 1 day after the announcement (see the results in the row for period 0–1), and the mean CAR from day 0 to 1 is statistically significant and positive (0.42%, p = .003).

Event Analysis Results.

Note. N = 434.

When including the days prior to the announcement, we found that the CAR from day −3 to 3 was statistically significant and positive (0.60%, p = .014). In addition, significantly positive impacts can be captured in alternative event windows, including day −2 to 2 and day −1 to 1 (mean CAR = 0.53% and 0.42%, p < .05). Table 2 also presents a description of the key percentiles of the CARs. These results strongly support H1. The economic magnitude of our findings is comparable to the stock market reactions observed in studies on green product development (0.45%; Ba et al., 2013), corporate environmental initiatives (0.11%; Jacob et al., 2010), and green supply chain management initiatives (0.37%; Bose & Pal, 2012). These comparisons demonstrate that our results align with established findings in similar contexts, showing that the observed CARs are economically meaningful.

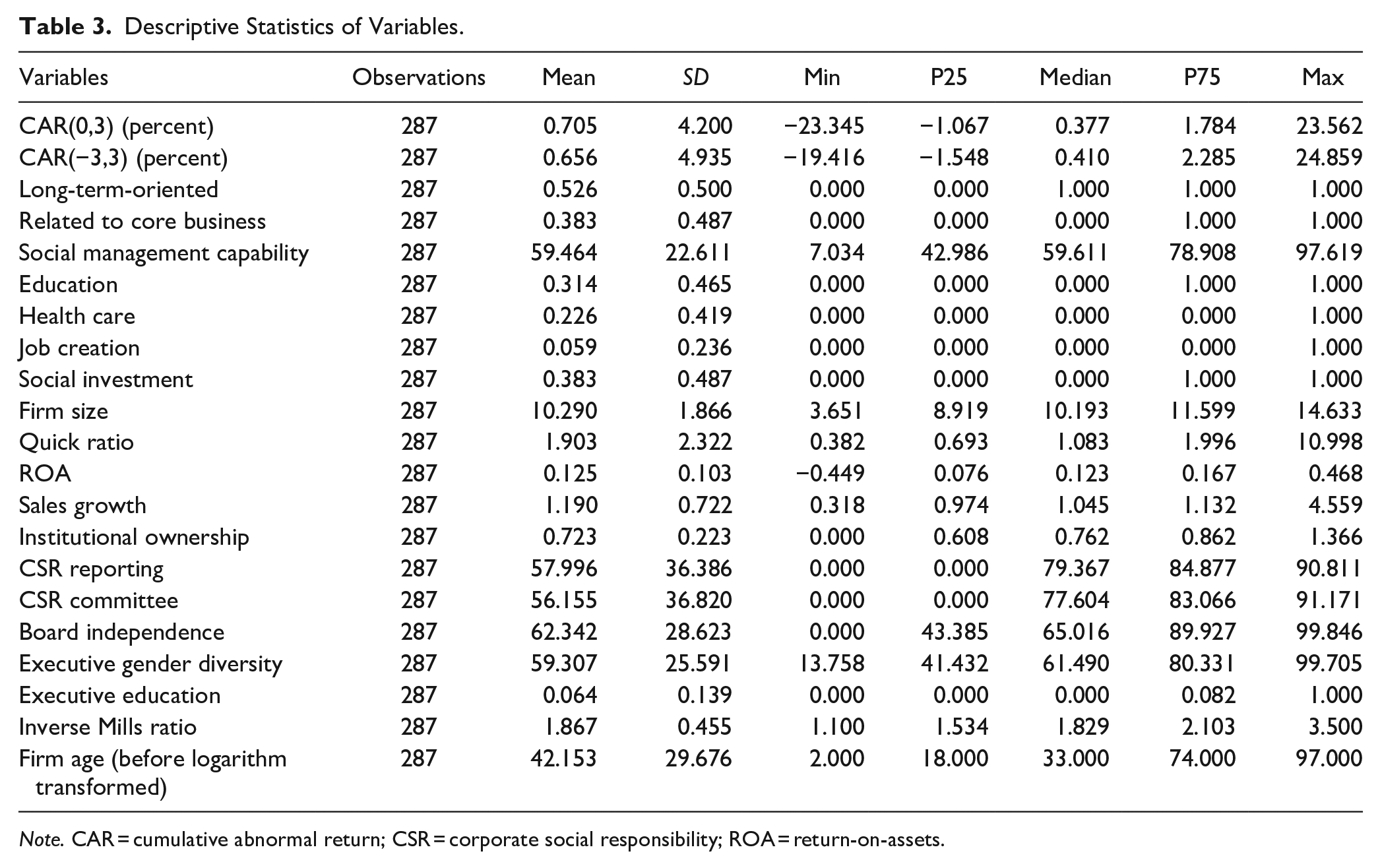

To test H2 to H4, we used the CAR from day 0 to 3 as the dependent variable. In a robustness check, we used the CAR from day −3 to 3 as an alternative dependent variable, yielding qualitatively identical conclusions (Supplemental Appendix Table F). We eliminated 147 announcements in this step because of missing financial data, CSR data, or both, in the COMPUSTAT and Thomson Reuters ESG databases, reducing the sample size for regression analysis to 287. We examined the CAR from day 0 to 3 with the reduced sample size (i.e., 287) and found it remained significantly positive (0.71%, p = .025). The magnitude showed no statistical difference compared to the CAR in the full sample of 434 observations. Therefore, the potential survival bias due to missing financial variables has been mitigated. We present the descriptive statistics in Table 3 and the correlations of the variables in Table 4. The maximum variance inflation factor among all variables is 3.7, which is well below the generally accepted threshold of 10, indicating that multicollinearity is not a serious concern.

Descriptive Statistics of Variables.

Note. CAR = cumulative abnormal return; CSR = corporate social responsibility; ROA = return-on-assets.

Correlations.

Note. N = 287; coefficients with absolute value >.12 are significant at the .05 level. CSR = corporate social responsibility; ROA = return-on-assets.

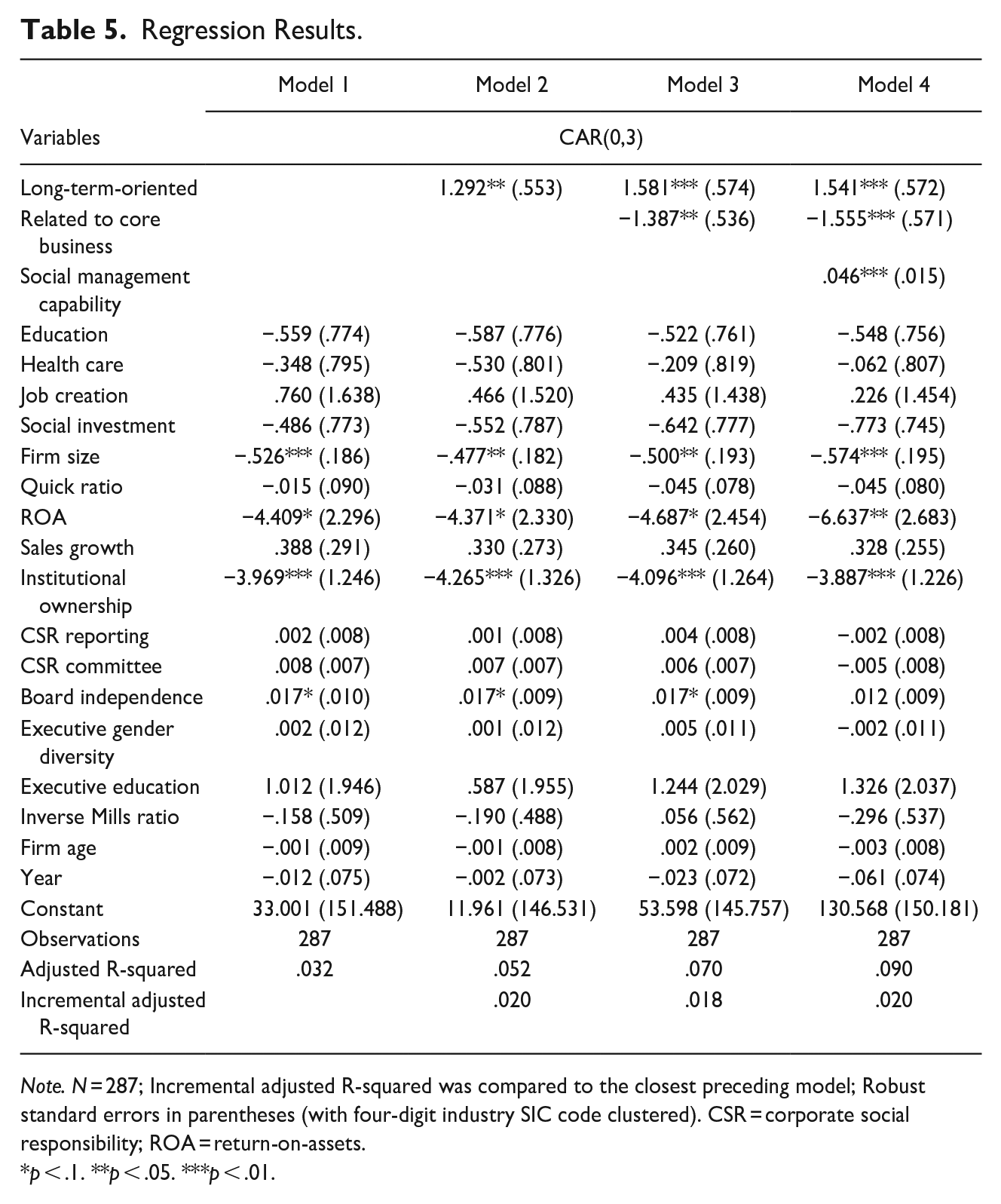

Table 5 summarizes the regression results. Model 1 includes all control variables, whereas Models 2, 3, and 4 incrementally include the variables of long-term orientation; relatedness to core business; and social management capability to test H2, H3, and H4, respectively. The incrementally adjusted R-squared values of Models 2, 3, and 4 show increases of 2%, 1.8%, and 2%, respectively, compared to their respective preceding models. This indicates an improvement in model fit due to the inclusion of these variables.

Regression Results.

Note. N = 287; Incremental adjusted R-squared was compared to the closest preceding model; Robust standard errors in parentheses (with four-digit industry SIC code clustered). CSR = corporate social responsibility; ROA = return-on-assets.

p < .1. **p < .05. ***p < .01.

The coefficient for long-term orientation is statistically significant and positive (Model 2 coefficient = 1.292, p < .05; Model 4 coefficient = 1.541, p < .01). This indicates that long-term-oriented CDIs have a more positive CAR compared to short-term-oriented CDIs. Therefore, H2 is supported.

The coefficient of relatedness to the core business is statistically significant and negative (Model 3 coefficient = −1.387, p < .05; Model 4 coefficient = −1.555, p < .01). The CDI remotely related to core businesses has a more positive CAR compared to those closely related to core businesses. Thus, H3a is rejected while H3b is supported.

Finally, the coefficient for social management capability is statistically significant and positive (Model 4 coefficient = .046, p < .01). CDI has a more positive CAR when firms show higher social management capabilities. Thus, H4 is supported.

In a separate analysis, we examined the three variables individually in three separate models to address the potential correlations among them. The results, presented in Supplemental Appendix Table G, are essentially comparable to those obtained in the main analysis.

In addition to the variables tested for hypotheses, some control variables emerged as significant factors influencing CAR. For example, we found that larger and more profitable firms conducting a CDI might trigger a more negative investor reaction, possibly because investors often have higher expectations of larger and profitable firms. When these firms engage in CDIs, investors may scrutinize their actions more critically, expecting substantial impacts and returns. In addition, CDI can lead to a more positive CAR for firms with higher levels of board independence. Firms with higher board independence tend to have greater credibility and trust in investors. When such firms announce a CDI, investors may be more confident in the initiative’s authenticity.

Other Robustness Checks

To improve the validity of the conclusions obtained from the primary analysis, we conducted several robustness checks.

Propensity Score Matching

The primary analysis used Heckman’s two-stage analysis to mitigate selection bias concerns in testing the moderating hypotheses (H2–H4). However, selection bias in testing the direct impact (H1) was not fully addressed. It is possible that firms under greater mimetic pressure to improve CSR performance are more likely to implement CDIs and that investors may react more positively to these firms. To address this, we adopted propensity score matching (PSM), following Ding et al. (2018) and Paulraj and De Jong (2011). First, we used the results from our selection model (as detailed in Supplemental Appendix Table E) to estimate the propensity scores (i.e., probability) of engaging in CDIs for all firms in both the sample and control groups. We then matched each firm in our sample with a control firm from the same industry (classified by the same 4-digit SIC code) that had the closest propensity score. To estimate the abnormal CAR, we calculated the difference between the CAR of each sample firm and its matched control firm. The analysis results, presented in Supplemental Appendix Table H, show that the abnormal CARs remain significantly positive in both periods of day 0 to 3 and day −3 to 3 (p < .01) as well as in other windows including day 0 to 2 and 0 to 1 (p < .01), −2 to 2 and −1 to 1 (p < .05). These results indicate that selection bias is not a serious concern for H1.

Placebo Tests

To establish that the effects observed from our CDI were not due to random chance, we conducted placebo tests. First, following Paulraj and De Jong (2011), we analyzed the CARs of the matched control firms generated through PSM. The results from this test (shown in Supplemental Appendix Table I) indicated that the CARs for these control firms were statistically insignificant (p > .1) across all event windows, thereby supporting the specificity of the observed effects for the CDI activities in both Table 2 and Supplemental Appendix Table I.

In addition, we implemented a more extensive placebo test by creating a set of “fake sample firms.” For each firm in the actual sample, we randomly selected a counterpart firm from the same industry using the 4-digit SIC code to construct this pseudo-sample. We then examined the abnormal returns of these fake sample firms over the same event window of day 0 to 3 and −3 to 3, repeating this process 1,000 times to ensure statistical robustness. Our findings from this extensive testing (shown in Supplemental Appendix Figures J1 and J2) revealed that a significant majority of these fake sample firms demonstrated nonsignificant mean CARs (p > .1, or above the dash line) within the specified periods. This outcome further corroborates our initial findings, suggesting that significant CARs associated with real CDI activities are not a product of random fluctuations in the market but are instead a result of CDI events.

Longer-Term Analysis

Our primary analysis captures a short-horizon stock price change caused by CDI. However, one may wonder if increased stock market performance is consistent over a longer time frame (e.g., annually). Thus, we conducted a regression analysis with a firm-year panel dataset of the matched samples yielded from the PSM. In this extended analysis, we used annual Tobin’s Q to measure long-term firm stock market performance. We specifically examined the impact of CDI over a 7-year window (from 3 years before to 3 years after the CDI event) through a two-way fixed-effect regression analysis, using a binary independent variable to indicate CDI presence (“1” for CDI implementation, “0” otherwise). We also included relevant firm-level control variables as well as time and firm dummy variables to robustly control for potential confounders. Our regression results (shown in Supplemental Appendix Table K) demonstrated a positive and significant impact of CDI on Tobin’s Q (coefficient = 4.964, p < .05), thereby providing empirical support for H1 on a yearly basis.

Subsample Analyses

The primary analysis employed a regression model to test the moderating effect of three variables on the variation in CAR due to CDI. In a separate analysis, we categorized our samples into subgroups based on moderators to provide a description of CARs in different groups, illustrating the boundary conditions of H1. However, we noted that these results were unconditional, without control variables. The results presented in Supplemental Appendix L show that the long-term-oriented samples had a significantly positive CAR in both periods of day 0 to 3 (1.03%, p < .01) and day −3 to 3 (0.71%, p < .1), whereas no significant results were found in the short-term-oriented samples (p > .1).

In addition, the CDI samples not related to the firm’s core business yielded a positive CAR in both periods of day 0 to 3 (0.85%, p < .01) and day −3 to 3 (0.79%, p < .05), whereas there were no significant results in those samples related to the firm’s core business (p > .1).

Finally, the sample firms with stronger social management capabilities (those scoring higher than the sample 55th percentile, Su et al., 2015) demonstrated a significantly positive CAR during the day 0 to 3 period (0.95%, p < .01). Conversely, there were no significant results in those samples with social management capability scores lower than the 45th percentile (Su et al., 2015; p > .1). These results further reinforce the robustness of our analysis.

Regression With CAR Winsorized

Table 3 shows that CAR values range from −23.345% to 23.562%. Some may argue that these huge changes could distort the distribution of CAR in the regression analysis. To address this, we winsorized the CAR at the 1% level to reduce the influence of extreme observations. The additional regression results, presented in Supplemental Appendix M, show that our findings remain robust and unchanged compared to those in Table 5.

Discussion

In this study we explored the shareholder value implications of CDIs, CSR initiatives focusing on secondary stakeholders (Meade, 2021). Our results deviate from extant limited empirical studies on the performance implications of secondary CSR (Hillman & Keim, 2001; Van der Laan et al., 2008), showing that CDIs can trigger positive responses from shareholders. Informed by path dependence theory and signaling theory, we found three factors that can influence the shareholder value of CDIs. Consistent with both path dependence theory and signaling theory, CDIs exhibiting long-term orientation can lead to more positive shareholder responses than short-term-oriented CDIs, and firms possessing higher levels of social management capability can generate more positive shareholder responses from CDIs than firms with lower levels of such capability. However, contrary to path dependence theory’s predictions, but in alignment with signaling theory, we found that CDIs less related to the firm’s core business are more effective in enhancing shareholder value than those closely aligned with the firm’s core business.

Contrary to path dependence theory’s prediction, our results show that CDIs closely related to a firm’s core business trigger fewer positive shareholder responses than those unrelated to the firm’s core business. In other words, venturing outside a firm’s comfort zone (core business) in CDIs appears to increase a firm’s shareholder value. This finding is consistent with signaling theory (Connelly et al., 2011) in the context of CSR. Specifically, this theory suggests that firms undertaking CDIs unrelated to their core business could be perceived by the main stakeholders as making a more sincere, genuine commitment to CSR compared with those focused on their core business. For example, how surprising would it be if Microsoft donated its Office suite to a local elementary school? Similarly, stakeholders, including shareholders, would likely not be impressed if IKEA simply donated a few toys packages to a nearby kindergarten. From the perspective of path dependence, pursuing CDIs closely related to a firm’s core business may be resource-efficient. However, stakeholders might view these efforts as self-serving or profit-driven rather than genuinely addressing the more challenging or urgent issues the community faces. In contrast, when a firm steps outside its core business to address salient community issues, it sends a strong signal that it genuinely cares about improving the community by engaging with a broader range of CSR concerns. In these cases, it may be more financially beneficial for the company to focus on doing the right things—genuinely addressing significant community needs—rather than just doing things well such as efficiently leveraging core business strengths in CSR activities. Our results, therefore, provide stronger support for signaling theory, suggesting that authenticity in addressing CDIs has a greater positive impact on shareholder value than purely resource-efficient strategies. We will now discuss the theoretical implications of these findings for the CSR literature, with a particular focus on secondary CSR.

Theoretical Contributions

To date, there has been limited empirical research on the performance implications of secondary CSR, including CDIs (Chang et al., 2014; Godfrey et al., 2009; Hillman & Keim, 2001; C. Kim et al., 2024; Lu et al., 2023). Considering that firms purposefully extend their CSR activities beyond primary stakeholders, our study makes a timely contribution to the empirical CSR literature by focusing on CDIs as an important form of secondary CSR. Our results show that CDIs can indeed trigger positive shareholder responses, which is largely in line with instrumental stakeholder theory. As such, our findings suggest that secondary CSR, such as CDIs, can foster firm–stakeholder relationships, although possibly less effectively than primary CSR (Flammer, 2015; McWilliams & Siegel, 2000; Servaes & Tamayo, 2013).

Second, recent empirical studies (Lu et al., 2023) have suggested that secondary CSR can be seen as a “value stabilizer” that does not significantly increase firm value but reduces the variability of a firm’s market value. By integrating instrumental stakeholder theory with path dependence theory, we have outlined a CSR engagement strategy that transforms a value stabilizer into a value enhancer for firms. Importantly, this strategy for secondary CSR differs from the one used for primary CSR although some similarities remain. For example, Tang et al. (2012) found that relatedness is a key element for effective primary CSR engagement. However, our findings show that secondary CSR initiatives unrelated to a firm’s core business tend to be more financially rewarding.

Third, our findings also show that primary and secondary CSR, often viewed as separate and mutually exclusive, are actually interconnected. We show that the experiences and insights gained from engaging in primary CSR, as reflected in a firm’s social management capability (Huq et al., 2016), can be leveraged to enhance secondary CSR efforts. Our findings challenge the traditional compartmentalization of CSR activities and suggest the need for a more holistic view of CSR for firms.

Managerial Implications

Community development has become an important dimension of CSR (Smulowitz et al., 2020), with firms increasingly pursuing various programs and initiatives designed to address salient issues plaguing the local community. Although researchers in disciplines such as sociology (Meade, 2021) and urban development (McLennan & Banks, 2019) have provided valuable insights into how such corporate CDIs can effectively benefit the local community, our results provide a different perspective on how corporate CDIs can also provide financial benefits to firms. To create a virtuous circle where taking on more social responsibilities leads to increased shareholder value, CSR researchers have long explored and justified various CSR programs and initiatives (Barnett et al., 2020). Our results thus provide clear guidance for firms seeking to “kill two birds with one stone” by addressing critical community issues while enhancing shareholder value. For firms aiming to achieve these goals, it is important for managers to select CDIs that reflect the firms’ long-term commitment to solving specific community issues. Short-term-oriented CDIs may be perceived by shareholders as less genuine. By engaging in long-term-oriented corporate CDIs, firms can convey their dedication to improving local communities, which in turn generates positive shareholder responses. Additionally, managers should step outside their comfort zone (core business) to find solutions that benefit local communities. Focusing too narrowly on core business-related CDIs may lead stakeholders to question a firm’s commitment, limiting goodwill and trust in its stakeholder relationships (Jones et al., 2018). Finally, our results highlight the importance of leveraging firms’ social management capabilities in promoting shareholder value from CDIs. Firms with stronger social management skills can generate greater shareholder value from CDIs than those lacking such capabilities. Drawing upon these findings, we suggest that stakeholders could consider the firm’s social management capabilities and potential shareholder responses when planning a specific type of CDI. Overall, our findings can help managers formulate a more firm-specific and effective CSR strategies (Jones et al., 2018) to guide their engagement in corporate CDIs.

Limitations and Future Research

Our study has several limitations that warrant further research on this promising topic. First, firms should not view the increase in shareholder value from CDIs as an end goal; they must also work toward sustainable solutions that improve the long-term well-being of the local community. Although our results show that conducting CDI is positively linked with increased Tobin’s Q, future research could explore additional longer-term performance metrics and moderators to determine the extent to which the focal firm and the local community can benefit from corporate CDIs. Second, this research primarily relied on data collected from public firms, which limits the generalizability of the results to private firms. We encourage future researchers to examine the different motivations and performance consequences associated with private firms’ CDIs. Finally, it would be valuable to understand the distinct effects of corporate CSR practices aimed at primary versus secondary stakeholders. In this regard, future researchers could compare the circumstances under which firms choose to implement CSR practices that target primary or secondary stakeholders. Moreover, it is important to understand how firms can leverage resources to create complementarity in achieving CSR goals for both primary and secondary stakeholders.

Conclusion

We argue that CDIs, as an important type of CSR practice targeting secondary stakeholders, can enhance shareholder value when paired with effective engagement strategies. We posit that firms can strengthen positive shareholder value by engaging in CDIs with a long-term orientation or those closely aligned with their core businesses. We also argue that firms with high social management capabilities can generate higher shareholder value through CDIs. The results of an event study show that CDI announcements are associated with a significant increase in shareholder value during the 3 days following the announcements. Importantly, the financial impact of CDIs on shareholder value is amplified by a long-term orientation and strong social management capabilities. Our findings suggest that a stabilizer can be developed into an enhancer through strategic stakeholder engagement that acknowledges CSR’s path-dependent nature. Therefore, our findings can help firms develop an effective stakeholder engagement strategy for conducting secondary CSR.

Supplemental Material

sj-docx-1-bas-10.1177_00076503251329762 – Supplemental material for From Stabilizer to Enhancer: Effective Engagement Strategies for Secondary Stakeholders in Corporate Social Responsibility

Supplemental material, sj-docx-1-bas-10.1177_00076503251329762 for From Stabilizer to Enhancer: Effective Engagement Strategies for Secondary Stakeholders in Corporate Social Responsibility by Di Fan, Chengyong Xiao, Xun Tong, Yan Shao and T. C. E. Cheng in Business & Society

Footnotes

Acknowledgements

The authors are grateful for the research assistance of Deyan Shterev, Man Fong (Amy) Li, and Wei Chen.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Fan acknowledges the financial support of the National Natural Science Foundation of China (Grant No. 72202197).

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.