Abstract

This article examines the impact of sustainability-oriented governance factors on companies reporting on due diligence requirements of conflict minerals (DDRCM). We use the rating scores that are assigned by the Responsible Sourcing Network (RSN) on a sample of multinational companies between 2015 and 2019. We consider whether the existence and type of an independent external audit, the existence of sustainability reports to communicate a firm’s message, the inclusion of sustainability-related targets in executive compensation contracts, and the existence of board-level sustainability committees are associated with DDRCM reporting. We find that the combined effect of sustainability-oriented governance factors is associated with higher DDRCM reporting suggesting that sustainability governance plays an effective role in shaping the corporate response to conflict mineral risks. We also find that effective boards moderate the association between sustainability governance and DDRCM reporting suggesting that effective boards can substitute for the resources that are required for sustainability governance.

Conflict minerals can be defined as minerals that are mined under conditions of armed conflict and violation of human rights and are sold or traded by armed groups (Islam & van Staden, 2018). In unstable regions that are affected by armed conflict, the profits from mineral mining and trade can play a role in escalating and prolonging violent conflict (Islam & van Staden, 2018). Many international companies have followed a variety of due diligence practices to ensure that they do not contribute to human rights violations (Kim & Davis, 2016). To assist companies in respecting human rights and avoid contributing to the conflict by purchasing minerals from conflict-affected areas, the Organization for Economic Co-operation and Development (OECD, 2013) published the International Guidance for Responsible Supply Chains in 2013. OCED aimed to guide commitments toward respecting human rights and higher social standards (Vadlamannati et al., 2021). Section 1502 of the U.S. Dodd–Frank Act requires U.S.-listed companies to disclose whether they use conflict minerals and whether these minerals originated in the Democratic Republic of the Congo (DRC) or an adjoining country (Banerjee, 2021). This Act sought to reduce the human rights harms that are caused by armed groups in the DRC, who use the profit from the sale of minerals to fund the conflict (Dalla Via & Perego, 2018; Islam & van Staden, 2018). Other developed countries have implemented similar legislation, such as the 2015 Modern Slavery Act in the United Kingdom and the 2017 European Union (EU) Conflict Minerals Regulations (Islam & van Staden, 2018).

This study aims to provide evidence on the role of sustainability governance in improving companies’ reporting on due diligence requirements of conflict minerals (DDRCM). Given the increased expectations regarding accountability in the realm of human rights, the adoption of sustainability governance measures could influence how companies disclose information about DDRCM. The central question guiding this research is: the impact of sustainability-oriented governance factors on companies ‘reporting on DDRCM? To answer this question, we propose the following four questions: Does the existence and type of an independent external audit affect DDRCM? Do sustainability reports communicate a firm’s message affect DDRCM? Does the inclusion of sustainability-related targets in executive compensation contracts affect DDRCM? And finally, do board-level sustainability committees affect DDRCM?

The decision to address these questions was motivated by the fact there has been increased stakeholder concern and public pressure because of the lack of transparency in conflict mineral due diligence by global corporations (Islam et al., 2018; Islam & van Staden, 2018). Furthermore, firms with human rights policies may reduce severe human rights abuses over the long term (Olsen et al., 2022). Governments should pass regulations to address human rights impacts and implement corporate responsibility to respect rights. Therefore, accountability for human rights should be integrated into the existing due diligence practices, which will have implications for reporting and assurance practices (Backer, 2012). However, despite the significant implications of the recent developments in corporate activities related to human rights, they are still under-investigated in the existing accounting literature (Dalla Via & Perego, 2018; Kim & Davis, 2016; McPhail & Ferguson, 2016). Following Vadlamannati et al. (2021), we are motivated to focus on multinationals with the largest market capitalization in their sectors who submitted their conflict minerals reports between 2015 and 2019. These companies are worthy of investigation because they are under public pressure and are expected to have more resources to address human rights abuses buried in their supply chains (Responsible Sourcing Network, 2019).

From a theoretical perspective, resource dependence theory (RDT) proposes that firms should have access to outside resources that could facilitate their survival and success (Hillman & Dalziel, 2003; Shaukat et al., 2016). Meanwhile, sustainability governance mechanisms (e.g., board-level sustainability committee and independent external assurance) represent capital resources that can help to provide the expertise, supervision, and incentives to enhance sustainability activities and communications with different stakeholders (Al-Shaer, 2020). Firms that have independent external assurance are likely to have greater abilities to access external resources (Al-Shaer & Zaman, 2018). In addition, sustainability committees can be seen as an internal resource that can help a company to supervise its sustainability activities (Al-Shaer, 2020; Peters & Romi, 2015) and also help manage its reputational risk (Shaukat et al., 2016). Therefore, we argue that firms that have an independent external assurance and a sustainability committee that operates on the board are more committed to reporting more information on DDRCM. In addition, stakeholder theory proposes that firms are committed to offering transparent information about the impact of their activities to their stakeholders (Dubbink et al., 2008). Therefore, sustainability reporting is a key mechanism for managing the relationship between a firm and its stakeholders (Al-Shaer et al., 2022). Providing separate sustainability reports can enhance a company’s image by directly communicating its social and environmental practices and building better relations with stakeholders (Helfaya & Moussa, 2017). Companies can also respond to stakeholder’s demands for enhanced sustainability performance by using sustainability targets in executive compensation, which may help to improve the transparency of social and environmental activities (e.g., DDRCM; Maas, 2018). Consistent with this view, we argue that firms that publish separate sustainability reports and link executive compensation with sustainability targets will be more committed to human rights-related issues. Corporate boards can help to attract external resources for firms and then direct these resources toward improving the firm’s sustainable strategies (Helfaya & Moussa, 2017; Shaukat et al., 2016). They can also promote a firm’s strategic decision-making and induce firms to set their CSR agenda and align management decisions with the stakeholder’s expectations (García-Sánchez, 2020; Jizi, 2017). Consequently, an effective board can play a moderating role in the relationship between sustainability governance and DDRCM.

Several studies have empirically investigated corporate behavior vis-à-vis human rights issues in the supply chain (Hofmann et al., 2018; Kim & Davis, 2016; Ng et al., 2020). However, few accounting studies have examined due diligence practices for conflict minerals and the factors associated with them (Elayan et al., 2021). The accounting studies that have been published only consider conflict mineral reporting practices by applying the content analysis method (Dalla Via & Perego, 2018), and none of them have used the rating scores assigned by the Responsible Sourcing Network (RSN) to reflect the transparency and accountability of corporate conflict mineral due diligence practices. Furthermore, despite increasing evidence to highlight the importance of firm-level and board characteristics in enhancing DDRCM (Dalla Via & Perego, 2018; Sankara et al., 2017), studies of sustainability-oriented governance factors as drivers for better DDRCM are generally rare. Therefore, this study contributes to the knowledge of corporate DDRCM. It is motivated by a research gap that is associated with corporate responsiveness to the broader stakeholder concerns and the debate over the lack of corporate transparency concerning human rights.

This study contributes to the existing literature in several ways. First, unlike prior work by Sankara and colleagues (2017)—which explored whether board-specific characteristics are linked with a firm’s filing of conflict mineral forms and meeting the minimum requirements of the conflict mineral by using an indicator variable for corporate filings—we use the rating scores that are assigned by RSN, which reflect the transparency and accountability of corporate conflict mineral due diligence practices. This unique rating system ranges between 0 and 100 and is based on 24 KPIs divided across the following three themes: (a) Risk Management indicators, (b) Human Rights Impact indicators, and (c) Effective Reporting indicators. Second, our study complements the work of Dalla Via and Perego (2018)—who measured conflict mineral disclosures with the content analysis method and investigated disclosure determinants, including monetary compensation, board characteristics, corporate governance pillar scores, and a firm’s reputation—and adds to the literature by investigating whether sustainability-oriented governance factors, which were ignored in previous research, influence corporate reporting on DDRCM. More specifically, we investigate the impact of an independent external audit—as well as the type of audit provider, the existence of a sustainability committee on the board, and the inclusion of sustainability-related targets—on executive compensation. Our research provides insights into the role that governance mechanisms tailored toward sustainability can play in promoting companies reporting on DDRCM. These mechanisms are anticipated to be responsive to the stakeholder’s concerns about human rights. Third, compared with the samples that were analyzed in these previous studies, our study uses a more recent sample of multinational companies between 2015 and 2019. Finally, unlike prior studies that do not address endogeneity concerns and suffer from selection bias (Dalla Via & Perego, 2018), we address endogeneity and respond to the call by Dalla Via and Perego (2018) by applying various testing techniques—including the Heckman Two-Stage Estimation, 2SLS estimators (with IVs) and Propensity Score Matching (PSM)—to overcome interdependencies, sample selection bias, and omitted variable issues when exploring the link between sustainability governance and DDRCM reporting.

We use a sample of multinational companies that received rating scores from RSN between 2015 and 2019. 1 Our results show that the combined effect of sustainability governance mechanisms is associated with higher DDRCM reporting. Furthermore, we find that effective corporate boards moderate the relationship between sustainability governance and DDRCM reporting. We perform robustness tests, including a full-sample analysis using OLS regression, subsample analyses, and an endogeneity test by employing the Heckman (1979) two-step, 2SLS estimation and PSM approaches. Overall, our findings hold with the baseline analysis. Our findings suggest that adherence to conflict mineral due diligence requirements occurs in firms with efficient sustainability governance systems. Sustainability-oriented governance mechanisms would facilitate corporate communications on human rights issues and improve companies’ reporting on DDRCM.

In the following sections of this article, we discuss conflict, human rights, governance, and corporate accountability reforms, outline the theoretical framework, develop our hypotheses, outline the research method, and present our findings. We conclude the article with the implications of our results and avenues for future research.

Conflict Mineral, Human Rights, Governance, and Corporate Accountability Reforms

The literature shows a growing interest in “the human rights responsibilities of business, which include (a) the respect and protection of human rights along corporate value chains, (b) the avoidance of causing or contributing to human rights violations through business activities and conduct, and (c) the provision of remedy to those whose rights have been violated by business” (Schrempf-Stirling et al., 2022, p. 1283). It appears that efforts have been made to reduce human rights violations (McCorquodale & Nolan, 2021; Wettstein et al., 2019). One of these efforts is the 2010 Dodd-Frank Act, which was the first due diligence requirement to specifically target companies’ human rights violations (Elayan et al., 2021; Sankara et al., 2017). Section 1502 of the Act requires U.S.-listed companies to submit annual conflict mineral reports to the Securities and Exchange Commission (SEC) if they are subject to the conflict minerals provision (Banerjee, 2021). According to Section 1502 of the Act, the due diligence process requires firms to identify, prevent, mitigate, and explain how they respond to any adverse human rights impact. The Act also states that companies’ obligations go beyond their operations, and they are responsible for the supplier’s actions in the supply chain (Islam & van Staden, 2018; Weller, 2020). The Organization for Economic Co-operation and Development (OECD, 2013) released Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas in 2013, and the OECD (2017) Due Diligence Guidance for Meaningful Stakeholder Engagement in the Extractive Sector. These aim to support companies in upholding human rights and preventing their involvement in conflict by purchasing minerals from conflict-affected areas. Therefore, it is believed that OECD’s guidance improves commitments toward respecting human rights and higher social standards (Vadlamannati et al., 2021).

Other developed countries have implemented similar legislation, such as the 2015 Modern Slavery Act in the United Kingdom and the 2017 EU Conflict Minerals Regulations (Islam & van Staden, 2018). The 2015 Modern Slavery Act represents a more lenient type of regulation that heightens corporate responsibilities for divulging and reporting on voluntary efforts to address and prevent forced labor within worldwide supply chains (LeBaron & Rühmkorf, 2017). The 2017 EU Conflict Minerals Regulations require companies to report on their approach to handling conflict minerals and their capability to eliminate the financing of these conflicts and the associated social and human rights abuses (Silva & Schaltegger, 2019). Consequently, companies need to show their accountability and ethical behavior in preventing human rights violations in the supply chain by complying with the conflict mineral reporting requirements (Voss et al., 2019). Furthermore, corporate sustainability reports are a key communication channel that companies can use to communicate their accountability to the market and stakeholders and to declare how they address human rights issues related to conflict minerals embedded in their products (O’Brien & Dhanarajan, 2016).

The literature shows that there has been a surge in corporate governance reform worldwide (Rossouw, 2005). Rossouw (2005, p. 101) concluded that besides these underlying values of corporate governance, mention is also made of specific moral obligations that the board of directors and the company should abide by. Prominent among these ethical obligations are ensuring that the company always act on high ethical standards so that the reputation of the company will be protected as well as respecting the rights of all shareholders, but particularly those of minority shareholders.

Therefore, the protection of human rights became one of the duties of the board of directors. Many companies will be prepared to engage with ethics as part of their corporate governance reform (Demise, 2005). In this research, we aim to examine the extent to which sustainability-oriented governance factors affect CMRs.

Theoretical Framework

Our study uses multitheoretical framework to understand the impact of sustainability-oriented governance factors on CMRs. Resource dependence theory (RDT) indicates the firm as an open system that relies on external resources in its environment to survive (Pfeffer & Salancik, 2003). According to RDT, firms engage in collaborations with external stakeholders to manage their dependency on critical resources. It proposes that organizations that lack certain resources will develop relationships with other organizations to obtain those required resources (Ulrich & Barney, 1984). Based on RDT, firms need to have essential access to outside resources that could facilitate their survival and success (Hillman & Dalziel, 2003; Shaukat et al., 2016). Because firms need to deal with the multiple interests of a wide variety of stakeholders, they may need to appoint a third party to externally audit their sustainability reports for legitimacy and credibility needs (Liao et al., 2018). Independent external assurance helps to address the interests of regulatory bodies and social groups and reduce pressures from stakeholders who want to be informed about companies’ behavior in preventing human rights violations (Voss et al., 2019).

Sustainability external assurance can be considered to be a crucial resource for firms and helps to provide confidence in the information being reported (Peters & Romi, 2015). RDT highlights that companies may rely on external parties for specific resources and expertise. This can help companies to reduce their dependency on internal resources and enhance the credibility of operations (Shaukat et al., 2016). Therefore, hiring an external assurance provider to verify sustainability reporting including companies’ conflict mineral reporting is an example of seeking external expertise and resources. Conflict mineral reporting can be complex, and sustainability external assurance adds credibility to the process. This shows to stakeholders, including investors that firms’ reporting is trustworthy. This, in turn, reduces the organization’s resource dependency on stakeholders who may be concerned about ethical sourcing and reporting quality. Thus, external assurance can enhance companies’ access to external resources. For example, this can attract investors who are more confident in the company’s commitment to ethical practices and its transparent reporting and it can also help maintain good relationships with regulators, reducing the risk of legal penalties.

In addition, sustainability reports are important communication tools that companies may use to convey their economic, social, and environmental impact (Romero et al., 2019). Based on RDT, a firm’s survival and success depend on the resources in its environment (Hillman & Dalziel, 2003). Therefore, the publication of sustainability reports can be considered a strategic decision and a capital resource that can enhance a company’s image by directly communicating social and environmental practices and building better relationships with stakeholders (Helfaya & Moussa, 2017; Schnittfeld & Busch, 2016). Firms are committed to offering transparent information about the impact of their activities to their stakeholders (Dubbink et al., 2008). Providing sustainability reports is a strategic approach that can lead to better relations with stakeholders and can help not only to improve firms’ image but also to increase firm value (Romero et al., 2019; Shubham et al., 2018).

Another component of sustainability-oriented governance is the connection of sustainability-related targets to executive compensation. According to the stakeholder theory, companies should not solely focus on maximizing shareholder wealth but should also consider the needs and expectations of their various stakeholders (Hawkins, 2006; Jamali, 2008). Therefore, meeting the requirements of shareholders is fundamentally linked to fulfilling the demands of other stakeholders. Also, based on the stakeholder perspective, CSR-linked compensation aligns the interests of managers with the broader interests of stakeholders (Derchi et al., 2021; Radu & Smaili, 2022). Companies can incentivize managers to respond to stakeholder’s demands by using sustainability targets in executive compensation (Al-Shaer & Zaman, 2019; Maas, 2018). This helps to align the executive’s interests, and encourages them to enhance corporate social and environmental performance (Al-Shaer & Zaman, 2019; Berrone & Gomez-Mejia, 2009). The inclusion of sustainability-related targets in executive compensation is likely to hold executives accountable for the company’s sustainable performance and encourage them to engage in strategic activities that lead to better social and environmental performance (Al-Shaer & Zaman, 2019; Maas & Rosendaal, 2016).

A sustainability committee can play a crucial role in supervising sustainability activities, promoting sustainability issues, and enhancing the quality and reliability of sustainability reports (Al-Shaer, 2020; Peters & Romi, 2015). Sustainability committees have the required expertise to manage potential social and environmental risks, increase strategic opportunities, develop corporate goals toward sustainability, and enhance corporate social and environmental engagement (Al-Shaer et al., 2022; Helfaya & Moussa, 2017; Peters & Romi, 2015; Shaukat et al., 2016). In addition, a sustainability committee is likely to help manage reputational risk and avoid litigation costs (Helfaya & Moussa, 2017; Rodrigue et al., 2013). Elayan and colleagues (2021) argue that companies report information on conflict mineral due diligence to avoid reputation risk from prospective human rights practices. Based on RDT, firms may establish mechanisms, such as a sustainability committee to manage external dependencies and gain access to critical resources (Al-Shaer et al., 2022; Al-Shaer & Zaman, 2018). In this case, companies depend on various stakeholders including investors to provide financial support, maintain a positive reputation, and ensure legal compliance. Therefore, companies that have sustainability committees can proactively address the external pressure and resource dependence they face regarding conflict mineral reporting. This committee is tasked with overseeing and guiding firms’ sustainability efforts, including conflict mineral reporting practices. Thus, a board-level sustainability committee can help firms access external resources in the form of investments and partnerships (Shaukat et al., 2016). It can also reduce the risk of negative reputational effects and regulatory penalties by ensuring compliance with conflict mineral reporting requirements.

Board governance is one of the key factors influencing decision-making regarding corporate environmental and social practices (Al-Shaer et al., 2022; Haque & Ntim, 2018). Although Dalla Via and Perego (2018) use agency theory to explain how a firm’s internal factors are associated with greater adherence to conflict mineral regulation, we build our argument based on resource dependency theory and argue that board composition is an important internal competitive resource that helps enhance a firm’s development and promote corporate sustainable strategies (Shaukat et al., 2016). In addition, the board of directors can help facilitate access to resources to ensure business sustainability and enhance a firm’s image (Hillman & Dalziel, 2003; Jizi, 2017; Shaukat et al., 2016).

Empirical Literature Review and Hypotheses Development

In recent years, corporate behavior vis-à-vis human rights issues in the supply chain has received wide attention among academic researchers. For example, Kim and Davis (2016) discuss the challenges to global supply sustainability and showed that a company’s internal and supply chain complexities are the biggest obstacles to determining whether its products are free of conflict minerals. Hofmann and colleagues (2018) address the difficulties in performing due diligence across a firm’s supply chains to comply with the Dodd–Frank Act and concluded that there is a need for a comprehensive approach to supply chain due diligence. Hence, firms can proactively manage their supply chain and reduce reputational risk.

Although corporate reporting about their efforts to combat human trafficking has not been promising in its practical effects (Van Buren et al., 2021), Stoop and colleagues (2018) examine the post-legislation effects of the Dodd–Frank Act and concluded that these regulations reduce resource conflicts. Furthermore, Van Buren and colleagues (2021) argue that firms with substantial supplier relationships, including retailing and those with significant outsourcing of manufacturing are considered more connected to human trafficking compared with firms without supplier relations. Elayan and colleagues (2021) explore the market’s reactions to conflict mineral reporting and find that conflict mineral reporting informs investors about the extent of human rights violations that result in negative market reactions. In light of this, some companies may be reluctant to report conflict minerals information due to commercial sensitivity, potential legal liability, and the possibility of reputation damage (O’Brien & Dhanarajan, 2016; Preuss & Brown, 2012). However, Swift and colleagues (2019) argue that reporting on conflict mineral due diligence can increase the visibility of the company’s supply chain, thereby enabling managers to increase sales and thus profits. Similarly, creditors are likely to provide more trade credit to companies with more visibility in the supply chain (Ng et al., 2020). Dalla Via and Perego (2018) examine the impact of board and firm-level characteristics on conflict mineral reporting practices and conclude that strong corporate governance mechanisms are associated with better practices in terms of conflict mineral reporting. Effective boards will not only increase the transparency of information provided but also enhance the effectiveness of the board’s decisions toward sustainability (Ben-Amar & McIlkenny, 2015; Liao et al., 2018).

Despite extensive research into human rights violations in the supply chain from various social science perspectives, there are few studies of conflict mineral due diligence practices and the factors associated with them (Elayan et al., 2021; Islam & van Staden, 2018). Sankara and colleagues (2017) and Dalla Via and Perego (2018) examine the impact of board and firm-level characteristics on conflict mineral reporting practices and show that these characteristics are associated with better practices. Our study investigates the impact of sustainability-oriented governance factors, which have been ignored in previous research, on conflict mineral due diligence measured by the rating scores assigned by RSN.

Sustainability Reporting Assurance and DDRCM Reporting

Based on RDT, independent external assurance as an element of sustainability governance mechanisms represents capital resources that not only help provide the supervision to improve sustainability activities and communications with different stakeholders (Al-Shaer, 2020) but also give confidence in the sustainability practices and information reported (Peters & Romi, 2015). Thus, independent external assurance is expected to enhance a company’s behavior in preventing human rights violations (Voss et al., 2019). Independent external assurance is one component of sustainability-oriented governance. Previous research has shown that companies can strengthen the credibility of their sustainability reports by having them externally audited by a third party (Du & Wu, 2019). Therefore, the choice of assurance may help to determine the substantive sustainability issues that need to be addressed to enhance transparency and reporting quality and reduce stakeholder pressures (Al-Shaer et al., 2022). The external audit of conflict mineral reports helps to confirm that the design of the due diligence plan conforms to the recognized due diligence framework and is likely to improve compliance with due diligence requirements and the quality of conflict mineral reports (O’Brien & Dhanarajan, 2016; Sankara et al., 2016). Herda and Snyder (2013) argue that even for companies that consider that their minerals are conflict-free, there is a need for an independent private audit to assure the conflict minerals report. However, there are still concerns about the reliability of the independent assurer in improving the transparency of human rights reporting (Kaspersen & Johansen, 2016; O’Brien & Dhanarajan, 2016). Previous research finds that external audit provided by Big 4 accountancy firms improves the credibility of information due to their expertise in risk assessment and concerns about litigation risk in providing assurance (Al-Shaer et al., 2022; Du & Wu, 2019). Companies that use independent external audits of their sustainability reports demonstrate a commitment to transparency and accountability in their environmental and social practices. Such an audit is vital for stakeholders and is typically conducted to ensure the accuracy and reliability of sustainability reporting. This transparency may also extend to other aspects of corporate responsibility, such as conflict minerals reporting. Thus, when companies commit to transparency and accountability through externally assured sustainability reporting, they may be more likely to extend the same level of scrutiny to their conflict mineral reports. This can be driven by the expectation that investors and stakeholders want assurances on various aspects of a company’s ethical and sustainable practices. Therefore, firms that have their sustainability reports externally audited by a third party will be more inclined to comply with conflict mineral due diligence requirements and hence, have better conflict mineral ratings. Given the foregoing discussion, we propose the first hypothesis:

Publication of Sustainability Reports and DDRCM Reporting

Sustainability reports communicate what companies need to convey about their responsibilities (Gray & Herremans, 2012). Based on the stakeholder perspective, firms should create value, not just for shareholders but for all stakeholders. Providing social and environmental information through separate sustainability reports may be a strategic approach for better stakeholder management, and may help to enhance a company’s reputation and value (Helfaya & Moussa, 2017; Romero et al., 2019; Shubham et al., 2018). Thus, firms that publish separate sustainability reports could be more inclined to address conflict mineral activities and commit toward human rights-related issues. Mahoney (2012) concludes that companies that publish sustainability reports have higher corporate social ratings than companies that do not. Romero and colleagues (2019) find that sustainability-related information provided by companies that publish sustainability reports is of higher quality than that of companies that include it in their annual reports. Companies are likely to put more effort into addressing conflict mineral activities in the supply chain through their reporting channels to improve legitimacy and reduce reputation risk (Flynn & Walker, 2021). Based on these arguments, companies that publish a stand-alone sustainability report are expected to be more inclined to address the alignment of their goals and activities with societal values, such as human rights, and thus will have higher CMRs. Given the foregoing discussion, we propose the second hypothesis:

Sustainability-Linked Executive Compensation and DDRCM Reporting

Linking executive compensation with sustainability targets can support long-term environmental strategies and may help to promote sustainability activities (Al-Shaer et al., 2022; Baraibar-Diez et al., 2019). Based on stakeholder theory, firms need to satisfy the needs of a wide variety of stakeholders including investors, employees, and communities (Hawkins, 2006; Jamali, 2008) and, therefore, fulfilling the requirements of shareholders is indeed interconnected with addressing the demands of other stakeholders. Companies that strike a balance between generating returns for shareholders and meeting the diverse needs of stakeholders are more likely to achieve sustained success. Also, based on the stakeholder perspective, CSR-linked compensation aligns the interests of managers with the broader interests of stakeholders (Derchi et al., 2021; Radu & Smaili, 2022). The inclusion of sustainability-related targets in executive compensation is likely to hold executives accountable for the company’s sustainable performance and encourage them to engage in strategic activities that lead to better social and environmental performance (Al-Shaer & Zaman, 2019; Maas & Rosendaal, 2016). In this regard, using sustainability targets in executive compensation may motivate CEOs to act in stakeholders’ interests by enhancing their social and environmental performance (Al-Shaer et al., 2022; Al-Shaer & Zaman, 2019; Maas, 2018).

Previous studies have investigated executive compensation and incentive plans related to social and environmental disclosures (Berrone & Gomez-Mejia, 2009; Dalla Via & Perego, 2018; Maas & Rosendaal, 2016). For example, Dalla Via and Perego (2018) find that monetary compensation is associated with a greater commitment to conflict minerals regulation. Incentivized managers are motivated to improve the reporting on conflict minerals activities to gain support from various stakeholders (Dalla Via & Perego, 2018). As a result, it is expected that firms that link executive compensation to sustainability-related targets are likely to be more sensitive to human rights issues and more inclined to adhere to conflict mineral requirements. Given the foregoing discussion, we propose the third hypothesis:

Sustainability Committees and DDRCM Reporting

Based on RDT, a board-level sustainability committee can be seen as an internal resource that helps companies supervise their sustainability activities (Al-Shaer, 2020). Board-level sustainability committees can play an essential role in managing external dependencies and gaining access to critical resources (Al-Shaer & Zaman, 2018). Companies with sustainability committees proactively manage external pressures and resource dependence, addressing the social aspects of a firm. These committees oversee sustainability efforts, including conflict mineral reporting, and can attract external resources like investments and partnerships, fostering sustainability and compliance (Shaukat et al., 2016). Firms that have a board-level sustainability committee may have a better ability to manage potential social and environmental risks, increase strategic opportunities, and improve corporate social and environmental activities (Helfaya & Moussa, 2017; Shaukat et al., 2016). Therefore, based on this view, the board-level sustainability committee can enhance corporate human rights practices to avoid potential reputation risk and develop better external relations with stakeholders (Shaukat et al., 2016). Therefore, we argue that the board sustainability committee facilitates access to external resources by integrating sustainability into strategic planning, fostering stakeholder engagement, and establishing industry connections. This committee identifies external resources essential for the company’s operations and explores efficiency measures, reducing dependence on these resources. By engaging with stakeholders including suppliers, it cultivates relationships that may provide access to additional resources, expert knowledge, and sustainable practices, mitigating risks associated with resource scarcity and environmental concerns (Hillman et al., 2000). In the context of conflict mineral reporting, the committee’s efforts to engage with suppliers and ensure responsible sourcing align with ethical practices. It supports supplier due diligence processes, transparency in mineral sourcing, and regulatory compliance. By doing so, the committee helps the company a positive image, attracting ethically conscious customers and investors, ultimately strengthening the company’s position in a competitive market and ensuring compliance with regulations such as the Dodd-Frank Act, which mandates conflict mineral reporting.

The literature has highlighted the importance of a sustainability committee about sustainability governance (Peters & Romi, 2015). A firm that has a sustainability committee can demonstrate commitment and effective planning toward environmental and social responsibilities (Al-Shaer et al., 2022; Shaukat et al., 2016). Thus, addressing sustainability issues at the board level by having a sustainability committee operating on the board can be considered to be a strong indicator of a firm’s commitment toward social practices, including human rights-related issues, which will positively impact CMRs. Given the foregoing discussion, we propose the fourth hypothesis:

The Moderating Role of Effective Boards on Sustainability-oriented Governance- DDRCM Reporting Nexus

Effective boards can encourage reporting on sustainable development activities to ensure communication with different stakeholders (Ben-Amar & McIlkenny, 2015; Haque & Ntim, 2018; Ntim, 2016; Ntim & Soobaroyen, 2013). They help to monitor reporting practices, which increase the credibility of sustainability reports (Miras-Rodríguez & Di Pietra, 2018). Based on resource dependency theory, board composition can be considered to be an internal competitive resource that helps enhance a firm’s development and promote corporate sustainable strategies (Shaukat et al., 2016). Thus, board composition is a crucial factor in enhancing a firm’s sustainability practices and image (Hillman & Dalziel, 2003; Jizi, 2017; Shaukat et al., 2016). Therefore, effective boards may reduce social conflicts and enhance corporate human rights practices (Dalla Via & Perego, 2018).

Larger boards are composed of directors with different knowledge and expertise, which helps to provide better supervision and oversight (Liao et al., 2018). Furthermore, firms with more independent directors have better social and environmental performance because independent directors can put pressure on managers to enhance sustainability practices and increase reporting transparency (Fisher et al., 2019). Independent directors can attract available resources and help manage these resources toward enhancing firm’s sustainable practices (Helfaya & Moussa, 2017; Jizi, 2017). In addition, the existence of female directors on the board can enhance board discussion by bringing different views, which enables a better decision-making process (Husted & de Sousa-Filho, 2019). Firms with more female directors on the board are more socially oriented because female directors pay higher attention to ethical and social behaviors (Elmagrhi et al., 2019; Isidro & Sobral, 2015). In addition, frequent board meetings can enhance effective discussions and engagement, which promote transparency and improve the effectiveness of decision-making toward sustainability practices (Al-Shaer et al., 2022; Liao et al., 2018). The influence of CEO duality on sustainability practices remains a subject of debate within the academic literature. On the one hand, research on CEO duality, where the CEO also serves as the board chair, can have a positive impact on sustainability performance (Jizi et al., 2014). However, on the contrary, CEO duality may have a negative influence on corporate social performance (Mallin & Michelon, 2011), as the concentration of power in one individual might lead to a lack of accountability and transparency, potentially hindering sustainability efforts. Therefore, the effect of CEO duality on board effectiveness and sustainability practices, including conflict mineral reporting largely depends on the specific corporate context.

In line with agency theory, an effective board of directors can significantly impact sustainability practices by diligently monitoring and overseeing management decisions, ensuring alignment with the company’s long-term objectives and stakeholder interests (Naciti, 2019; Vitolla et al., 2020). The effect of sustainability governance on CMRs could be impacted by the existence of effective boards that monitor sustainability practices and may have higher incentives to address conflict mineral issues in the supply chain. Thus, firms with effective boards are likely to be transparent toward DDRCM and hence will have higher CMRs. Given the foregoing discussion, we propose the fifth hypothesis:

Data and Research Methodology

Data and Sample Selection

We use a sample of companies that submitted their conflict minerals reports between 2015 and 2019. These companies were assessed by RSN based on the 2015 to 2019 filling and assigned rating scores based on the companies’ due diligence. The companies that are included in this study sample are multinationals with the largest market capitalization in their sectors. 2 Large companies are under public pressure and are expected to have more resources to address human rights abuses buried in their supply chain (Responsible Sourcing Network, 2019). We collected corporate governance data from Thomson Reuters Asset4, and financial data were collected from DataStream.

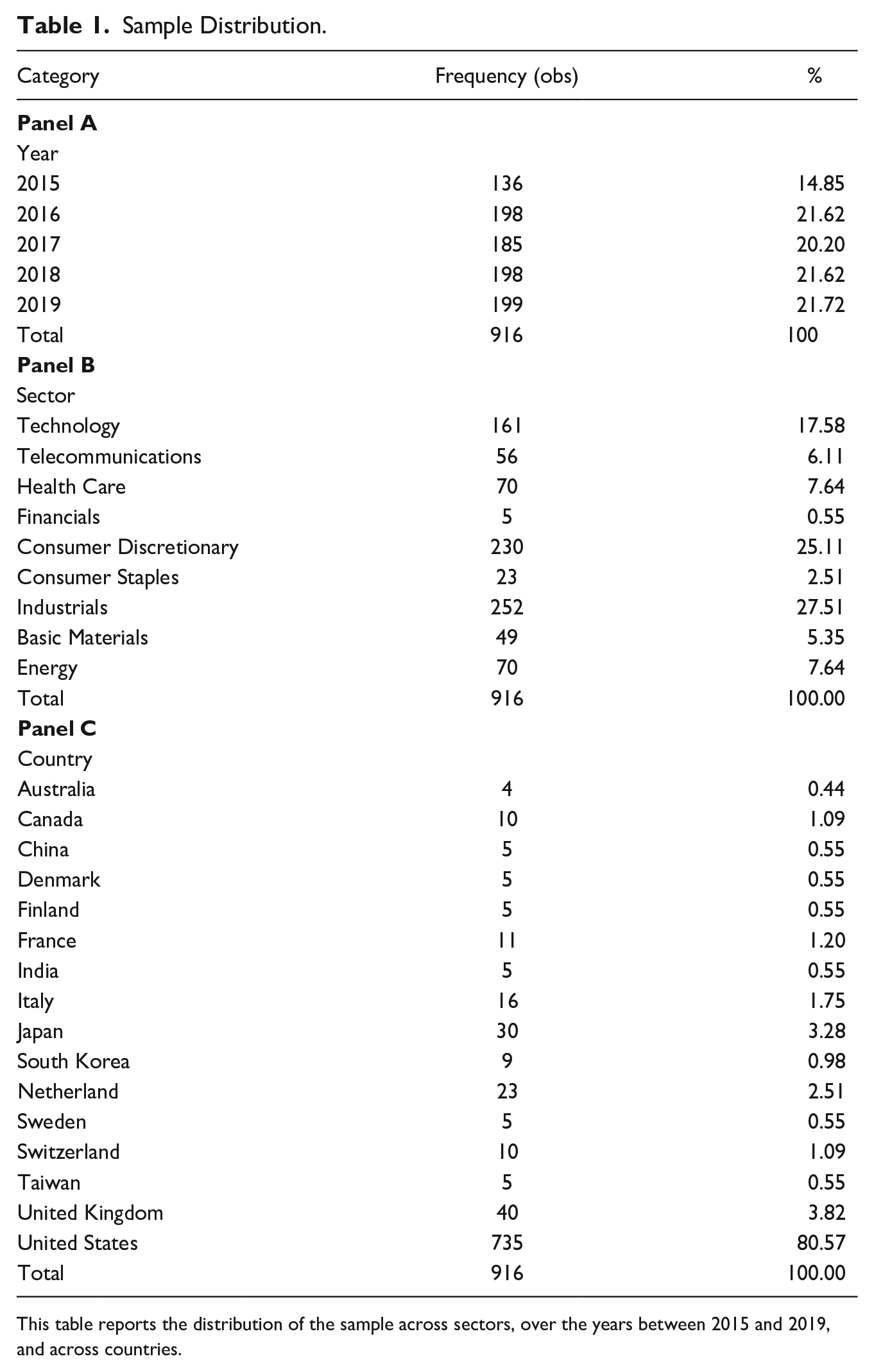

We have an unbalanced sample of 916 firm-year observations between 2015 and 2019. The sample distribution shows 136 firm-year observations in 2015; 198 observations in 2016, 185 observations in 2017; 198 observations in 2018; and 199 observations in 2019 (Table 1, Panel A). We examined the distribution of the sample based on sector. The companies are classified into nine industries, as shown in Table 1 Panel B. The largest group of observations in our sample belongs to Industrials (27.51%), including companies in Capital goods, Materials, and Technology hardware and equipment. The second and third largest industries are Consumer Discretionary (25.11%) and Technology (17.58%). We also examined the country-level sample distribution in Table 1, Panel C, which yielded 16 countries and 916 observations. 3

Sample Distribution.

This table reports the distribution of the sample across sectors, over the years between 2015 and 2019, and across countries.

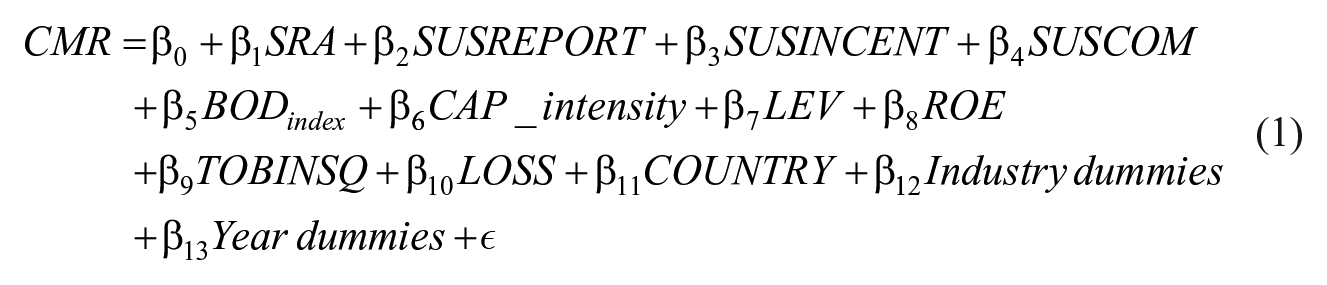

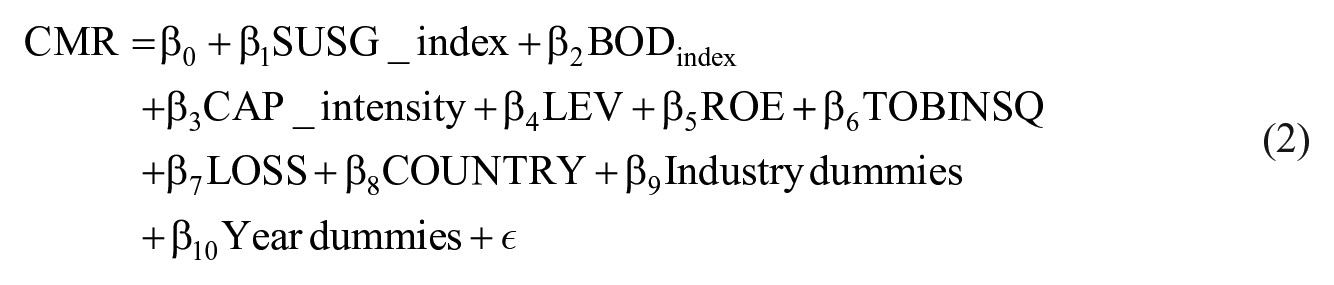

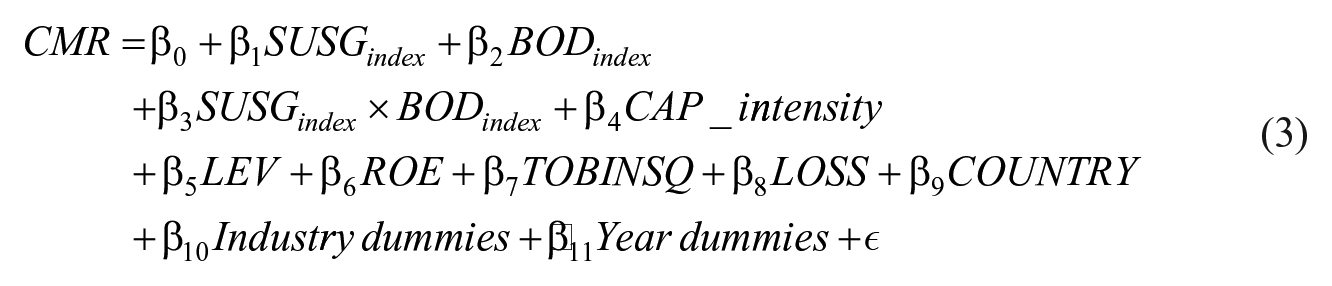

Regression Model

We conduct an OLS regression analysis with the following models:

Model 1 includes sustainability-oriented individual governance variables, Model 2 uses the composite index of sustainability-oriented governance (as discussed in Section 3.3.2), and Model 3 includes the interaction term SUSG_index × BOD_index to capture the moderation role of board governance index in the association between sustainability governance and conflict mineral ratings (CMRs). We provide the definitions of the variables in the Appendix.

Measurement of the Variables

CMRs

CMRs are measured using the rating scores assigned by RSN to companies included in our sample. RSN analyses companies’ efforts to identify, address and disclose their use of conflict minerals in the DRC region and their associated risks. It assesses companies’ attempts to publicly report their practices following a due diligence framework. 4 According to OECD (2013), “Due diligence is an ongoing, proactive and reactive process through which companies can ensure that they respect human rights and do not contribute to conflict.” As previously mentioned, RSN assesses the content of conflict mineral reports and assigns scores ranging between 0 and 100 based on the quality of the company’s due diligence activities regarding conflict mineral activities. 5

Sustainability-Oriented Governance

Our composite measure of sustainability-oriented governance is based on the following components: First, we examine whether the existence of independent external assurance will affect the CMRs scores. The objective of the independent audit is to confirm that the design of the due diligence program, as described in its conflict mineral reports, coincides with the due diligence framework that is used by the issuer (Herda & Snyder, 2013; Sankara et al., 2016). The external assurance will need to assure that the companies’ activities during the covered year are properly described in their conflict mineral reports and are reflected in their sustainability communications. According to previous research, sustainability reports that are externally assured by a third-party audit are more credible and of high quality, especially when assurance is provided by a top-tier accountancy firm (Al-Shaer, 2020; Al-Shaer & Zaman, 2018). Companies that progress toward achieving conflict-free status for their minerals are likely to request an independent external audit of their reports. The engagement of accounting firms in human rights issues could be expected to enhance the credibility and transparency of conflict mineral reporting (Sankara et al., 2016). We include assurance as a scale variable based on the existence and type of assurance. It takes the value of 3 if the assurance provider belongs to Big Four accounting firms, 2 if the assurance provider belongs to a non-Big Four accounting firm, 1 if the assurance provider belongs to a non-accounting firm, and 0 if there is no assurance (Al-Shaer, 2020; Al-Shaer & Zaman, 2018).

Sustainability reporting is considered to be a crucial communication tool that helps management demonstrate its accountability and convey information about sustainable development to stakeholders (Al-Shaer, 2020; Romero et al., 2019). Therefore, we check whether a company publishes a sustainability report (SUSREPORT) using an indicator variable that equals 1 if a firm publishes sustainability reports and 0 otherwise. Furthermore, we check whether there is some incentive related to sustainability issues for executives (SUSINCENT). To enhance the focus on sustainability-related matters, and for executives to be held responsible and accountable for any irresponsible behavior, companies will be more inclined to link executive compensation to sustainability targets (Al-Shaer & Zaman, 2019; Dalla Via & Perego, 2018; Maas & Rosendaal, 2016). The existence of a sustainability committee operating on the board helps to promote sustainability issues and increase reporting quality (Al-Shaer, 2020). SUSCOM is a binary variable that takes 1 if a board-level sustainability committee exists and is 0 otherwise. Our composite measure of sustainability-oriented governance of a firm (SUSG_index) is computed by totaling the four sustainability-oriented governance components that were discussed earlier. The composite score ranges from 0 (the minimum score) to 6 (the maximum score).

The Moderator Variable

We investigate the moderating role of the quality of corporate boards. To construct the quality index, we include several board characteristics that the previous literature shows their association with sustainability reporting (Bui et al., 2020; Liao et al., 2015). We include board size, board independence, board meeting, board diversity, and duality role. We compute a composite index (Board_index) by totaling the proxies of the five board characteristics measured using binary variables based on the median value of these proxies (Al-Shaer, 2020; Al-Shaer et al., 2022). As a result, the corporate board quality index includes, BODSIZE: Dummy variable if the number of board members is higher than the industry median, 1; otherwise 0; BODIND: Dummy variable if the percentage of independent directors on the board is higher than the industry median, 1; otherwise 0; BODMEET: Dummy variable if the number of board meetings is higher than the industry median, 1; otherwise, 0; BODDIV: Dummy variable if the percentage of female board members is higher than the industry median, 1, otherwise 0, and DUALITY: Dummy variable takes a value of 1 if the CEO has the presidency of the company and chair of the board, 0 otherwise.

Control Variables

Consistent with the CSR literature (Al-Shaer et al., 2022; Bui et al., 2020), we control for several firm-specific financial variables. We include a firm’s financial positions (LEV, CAP_intensity), financial performance (ROE, LOSS), and firm efficiency (TOBINSQ). Firms in good financial positions own the cash and resources and are more likely to engage in sustainable development projects, whereas firms in critical financial positions may refrain from engaging in these projects (Al-Shaer et al., 2022). We also control for country-specific variables. We control for national culture and use the national culture dimensions proposed by Hofstede et al. (2010). We computed a holistic culture score that represents the level of cultural system development following the previous approach by García-Sánchez and colleagues (2016) and Martínez-Ferrero & García-Sánchez (2017). Thus, we measure Culture as the mean value of Long-term Orientation (LTO) and Indulgence (IND) and the inverse of Individualism (IDV), Masculinity (MAS), Uncertainty Avoidance (UA), and Power Distance (PD). We also control for the natural log of the GDP of each country (in dollars) collected from the World Bank. Finally, we control for year, country, and industry fixed effects, which capture the time-invariant impact of year, country, and industry affiliation on our dependent variables (Al-Shaer et al., 2022; Gerwanski et al., 2019; Giuliani et al., 2023).

Empirical Results and Discussion

Descriptive Statistics

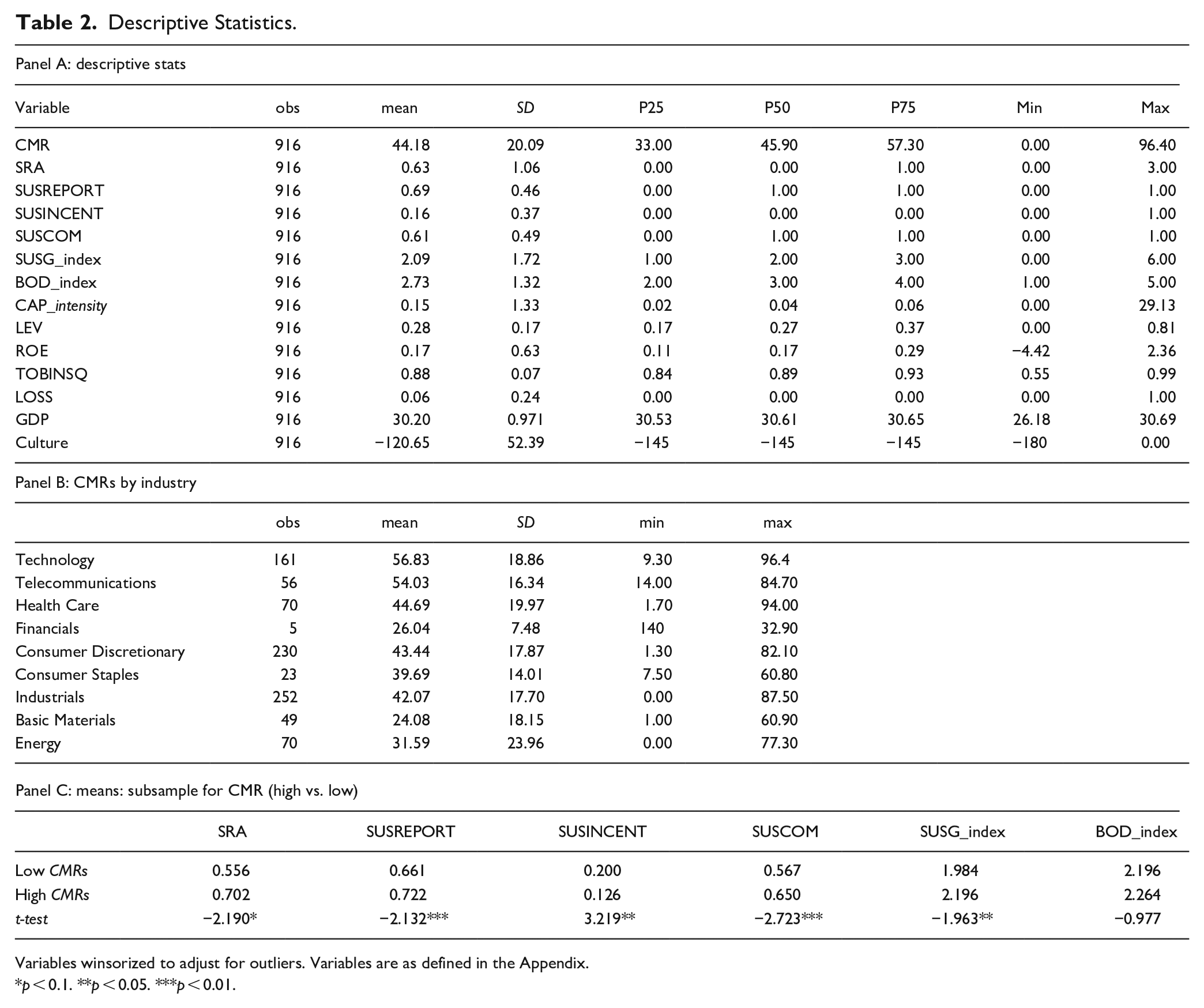

Table 2, Panel A provides the descriptive statistics of the variables that are included in our model. The mean value of CMRs is 44.18 and the median is 45.9. The highest rating achieved is 96.40 and the lowest rating is 0. The mean value of SRA is 0.63, which indicates that a larger proportion of our sample firms do not have an independent external audit. On average, 69% of companies publish stand-alone sustainability reports, 16 % of companies link executive compensation to sustainability-related targets, and 61% of our sample firms have a sustainability committee operating on the board. 6 Finally, the mean value of the BOD_index is 2.73, ranging between 1 and 5. Regarding firm-specific variables, we find that the mean value of capital intensity ratio is 0.15, the mean value of leverage is 0.28, the mean value of ROE is 0.17, the mean value of TOBINSQ is 0. 88, and on average 6% of our sample firms reported a loss. We also find that the mean value of holistic culture score is -120.65 and the mean value of GDP is 30.20 measured by the natural log of each country’s GDP (in dollars).

Descriptive Statistics.

Variables winsorized to adjust for outliers. Variables are as defined in the Appendix.

p < 0.1. **p < 0.05. ***p < 0.01.

Table 2, Panel B shows the descriptive statistics of CMRs by industry. Companies belonging to the Technology industry appear to have the highest CMRs (M = 56.83, SD = 18.86), and companies belonging to the Telecommunication industry have the second highest CMRs (M = 54.03, SD = 16.34). Companies in the Financials industry have the lowest CMRs (M = 26.04, SD = 7.48). In Table 2, Panel C, we report the means and t-tests for companies with high CMRs and those with low CMRs based on the upper quartile and lower quartile. We find in the subsample of firms with high CMRs, companies have an independent external assurance, a sustainability committee operating on the board, and they publish sustainability reports. Moreover, firms with high CMR scores have stronger sustainability governance (SUSG_index) than firms with low CMRs.

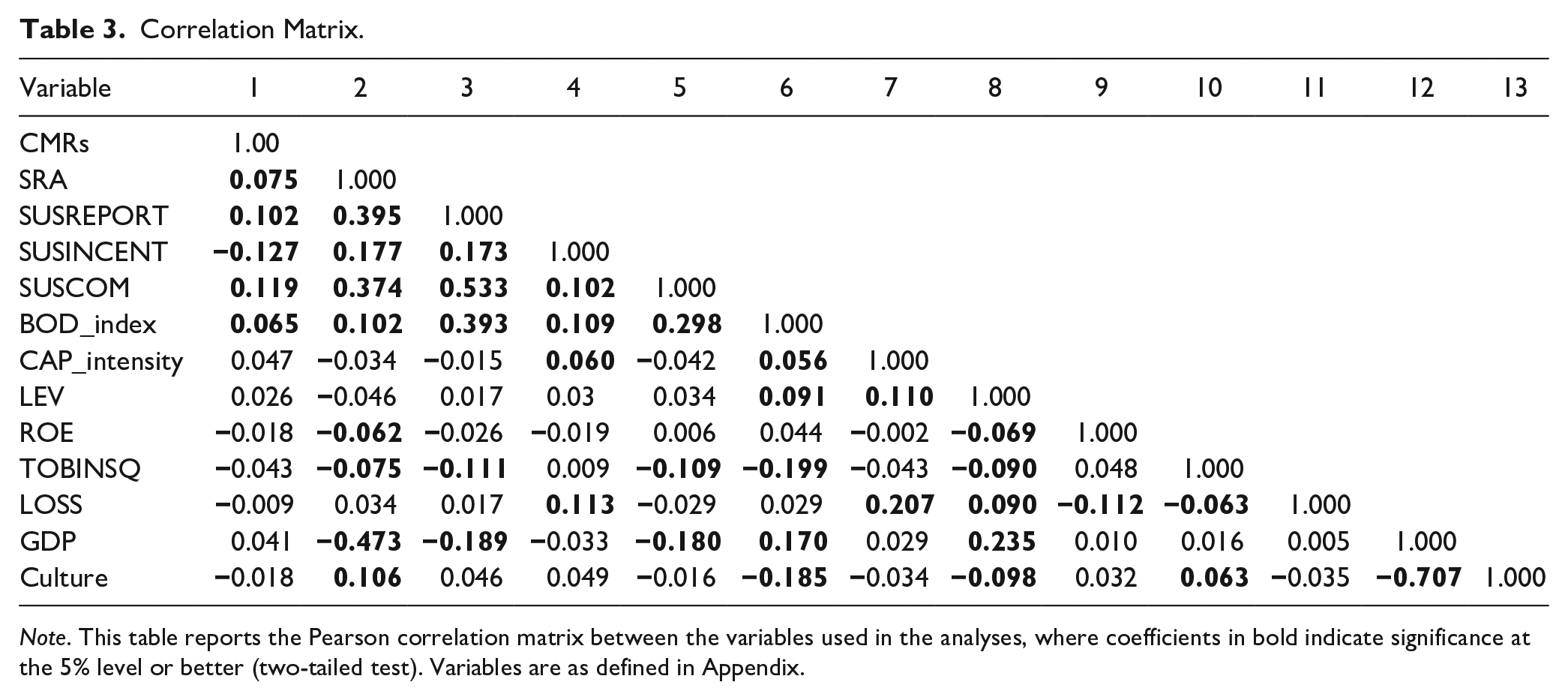

Table 3 presents the correlation matrix for variables included in our research model. CMRs are positively and significantly correlated with SRA, SUSREPORT, and SUSCOM (0.075, 0.102, and 0.119, respectively), and SUSINCENT is negatively correlated with CMRs (−0.127). Moreover, CMRs are positively and significantly correlated with BOD_index (0.065). Based on the correlation coefficients and the variance inflation factor (VIF), which ranges between 1.13 (lowest value) and 7.37 (highest value) with an average value of 2.14, we suggest that multicollinearity does not seem to be a problem in our analysis.

Correlation Matrix.

Note. This table reports the Pearson correlation matrix between the variables used in the analyses, where coefficients in bold indicate significance at the 5% level or better (two-tailed test). Variables are as defined in Appendix.

Multivariate Analysis

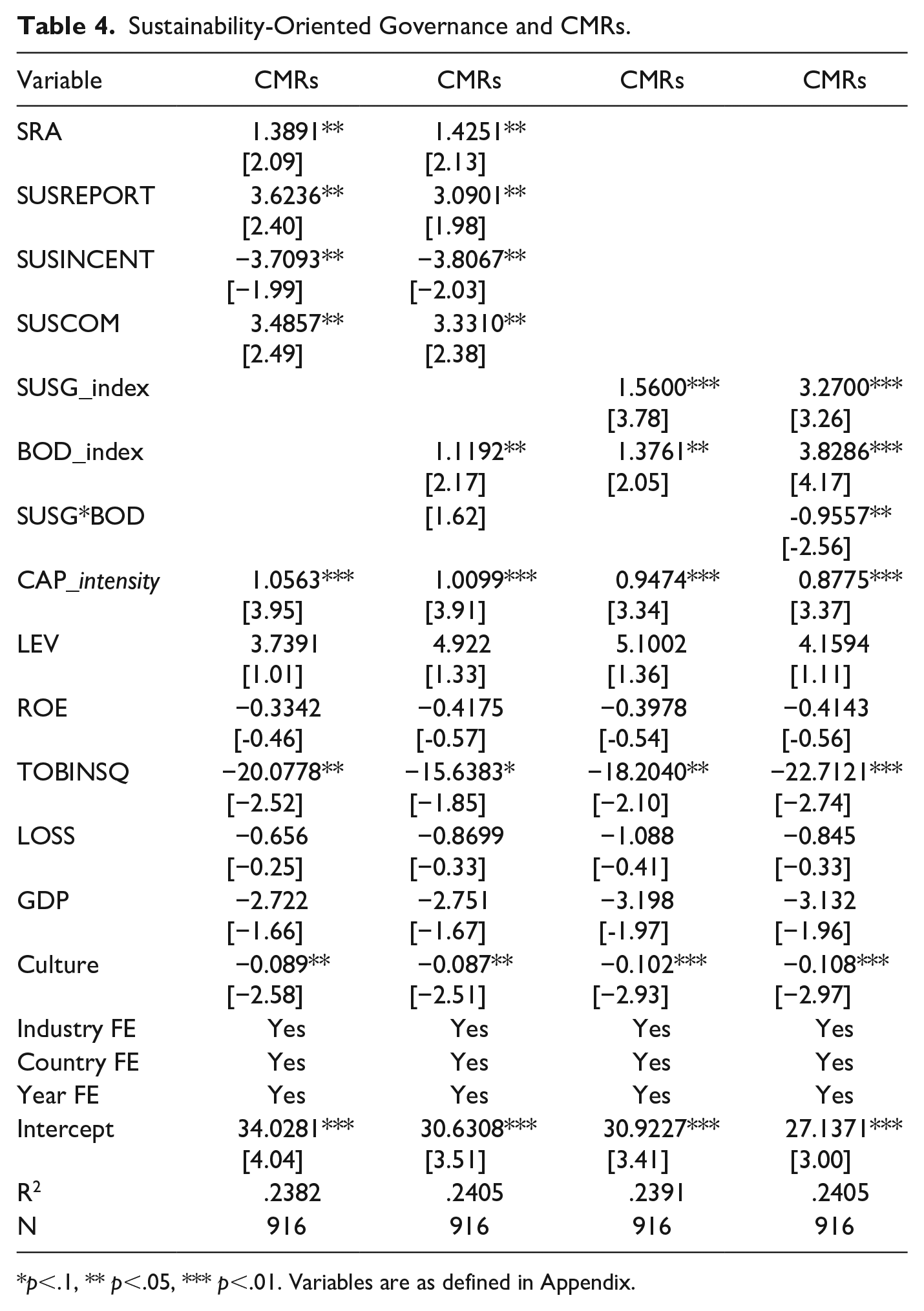

Table 4 presents the regression model results that test the impact of sustainability-oriented governance factors on CMRs and the moderation effect of board governance. Column 1 includes the individual components of sustainability-oriented governance; that is, SRA, SUSREPORT, SUSINCENT, SUSCOM, and control variables. Column 2 adds the impact of BOD_index. In Column 3, we replace individual sustainability-oriented governance variables with the composite index, SUSG_index, and Column 4 tests for the moderation effect of board governance by including the interaction term SUSG_index x BOD_index. All of the regression tests in Table 4 are applied to the full sample and have an adjusted R2 of .24.

Sustainability-Oriented Governance and CMRs.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

The results show that SRA is significant at the 0.05 level, and is positively associated with CMRs in Column 1 and Column 2. SUSREPORT is significant at the 0.01 level in Column 1 and the 0.05 level in Column 2 and is positively associated with CMRs. SUSCOM is significant at the 0.05 level and positively associated with CMRs in Column 1 and Column 2, while SUSINCENT is significant at the 0.05 level and negatively associated with CMRs in Column 1 and Column 2. When we include our composite measure, SUSG_index, in Column 3, the result shows that it is significant at the 0.01 level and positively associated with CMRs.

Regarding board governance, we find that BOD_index is statistically significant at the 0.05 level in Column 2 and Column 3, and is positively associated with CMRs. This finding suggests that implementing internal governance mechanisms positively impacts conflict mineral reporting (Dalla Via & Perego, 2018). More importantly, Colum 4 shows that the interaction term SUSG_index x BOD_index is significant at the 0.01 level and negatively associated with CMRs, while its individual components, SUSG_index and BOD_index are significant at the 0.01 level, and are positively associated with CMRs.

We will next examine the economic significance of the results. In Column 3, we multiply the standard deviations of SUSG_index and BOD_index values by the coefficients of SUSG_index and BOD_index, respectively. Accordingly, an increase of SUSG_index by one standard deviation yields an increase in CMRs by 6.073% (i.e., 1.560 x 1.72= 2.6832; and 2.6832/44.18= 6.073% of the mean CMRs). Similarly, an increase in BOD_index by one standard deviation results in a 4.111% increase in CMRs (i.e., 1.3761 x 1.32= 1.8165; and 1.8165/44.18=4.111% of the mean CMRs).

The findings suggest that companies that publish sustainability reports and get their reports assured by independent external audits demonstrate their ethical behavior and commitment to transparency and accountability in their environmental and social practices. The independent external audit of sustainability reports is vital for stakeholders to ensure the accuracy and credibility of sustainability reporting. This credibility and transparency may also extend to other aspects of corporate responsibility, such as conflict minerals reporting. Thus, those companies are more likely to get an independent audit that helps in improving the credibility of conflict mineral reporting, and consequently their CMRs. Although the audit of CMRs by external audits is not mandatory, the voluntary adoption of external assurance services that are provided by the Big 4 accounting firms is likely to improve the CMR levels. Companies that publish separate sustainability reports could be more inclined to address conflict mineral activities and commit to human rights-related issues. Moreover, sustainability committees drive CMRs because they oversee and review social issues. However, our results show a negative effect of the explicit linkage of sustainability-related targets in executive compensation on CMRs when included individually in the regression model. This may happen because executives are mainly held accountable and compensated for financial performance (Bui et al., 2020), which affects their incentives to engage in sustainable projects. When we measure the strength of sustainability-oriented governance of a firm using a composite index, the results show that the combination of these factors is likely to improve CMRs. Overall, our findings show support for the first, second, and fourth hypotheses, and do not support the third hypothesis on the association between sustainability-related incentives in executive compensation and DDRCM reporting. The result of the moderation effect reported in Column 4 supports the fifth hypothesis about the moderating role that corporate boards play in the association between sustainability governance and DDRCM reporting. This suggests that companies that spend more resources on strengthening their sustainability governance can substitute for board efforts (e.g., having the expertise in conflict mineral due diligence or the interest in addressing them in response to stakeholders’ concerns).

The findings support the views of the RDT and stakeholder theory that sustainability governance mechanisms and the composition of the board can be seen as unique resources that help firms improve their reporting practices (Helfaya & Moussa, 2017; Jizi, 2017; Peters & Romi, 2015). Consequently, companies should be able to acquire resources to provide assurance services within a firm’s corporate governance framework (Peters & Romi, 2015). Sustainability committees have a resource connection with sustainability experts, which helps to provide perceptive guidance to the management about the stakeholders’ prospects (Amran et al., 2014; Shaukat et al., 2016). Moreover, sustainability reporting can be considered to be a key mechanism for managing the relationships between firms and stakeholders (Al-Shaer, 2020). Meanwhile, the board plays a service role, which refers to their responsibility to facilitate access to resources (Jizi, 2017), and encourage reporting on sustainable development practices to ensure communication with various stakeholders (Ben-Amar & McIlkenny, 2015; Helfaya & Moussa, 2017).

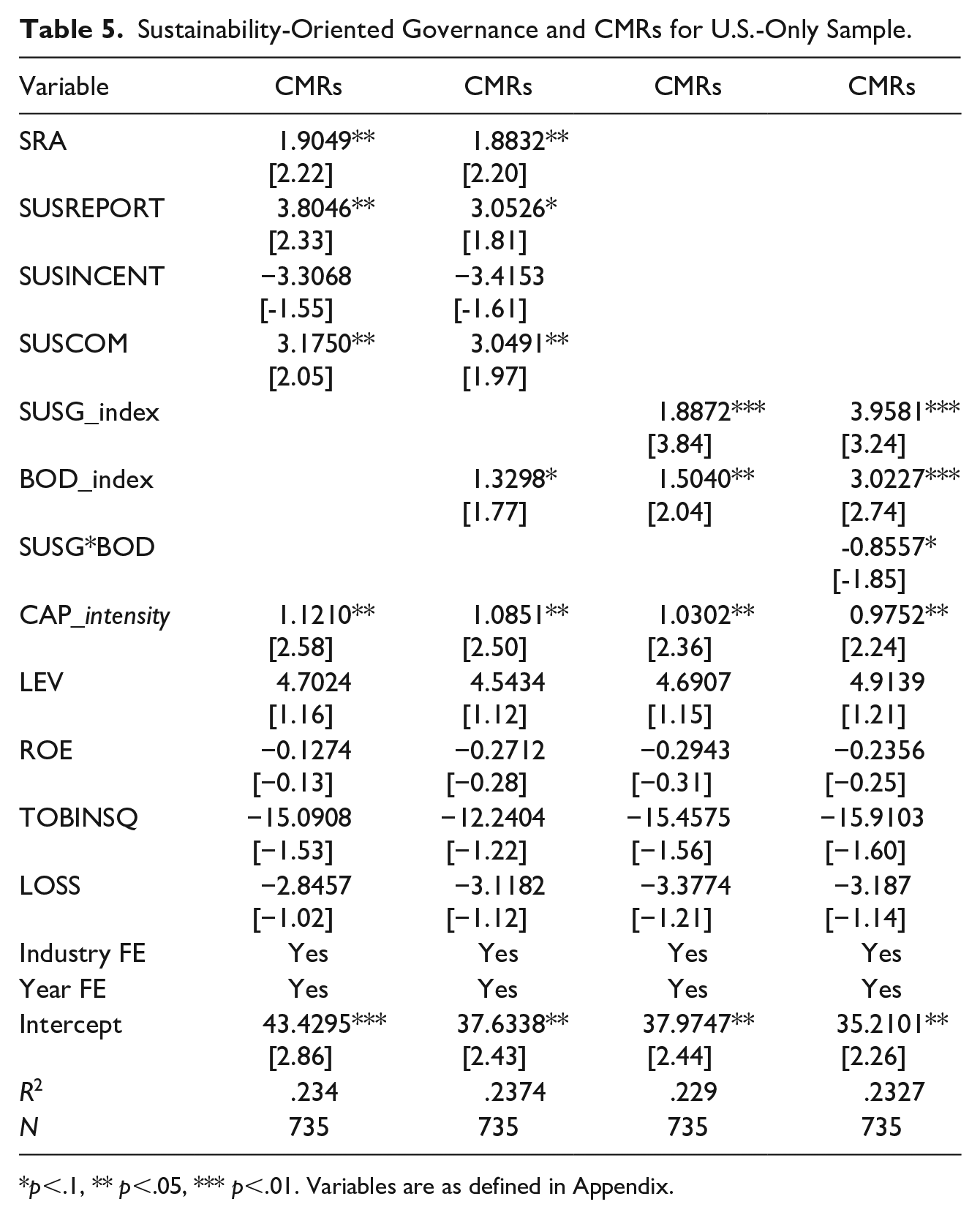

In the supplementary analysis that is presented in Table 5, we run the same regression tests for U.S. firms only. Sankara and colleagues (2017) claim that the requirements of conflict mineral due diligence are considered to be among the first non-environmental social mandatory practices in the United States. Therefore, it is important to examine the impact of sustainability governance on CMRs for a sample of U.S. firms, especially given that they dictate a large proportion of our study sample. The results reported in Table 5 are consistent with our main findings reported in Table 4. They also confirm the positive association between sustainability-oriented governance and CMRs, and the moderation role of the board governance in this association. 7

Sustainability-Oriented Governance and CMRs for U.S.-Only Sample.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

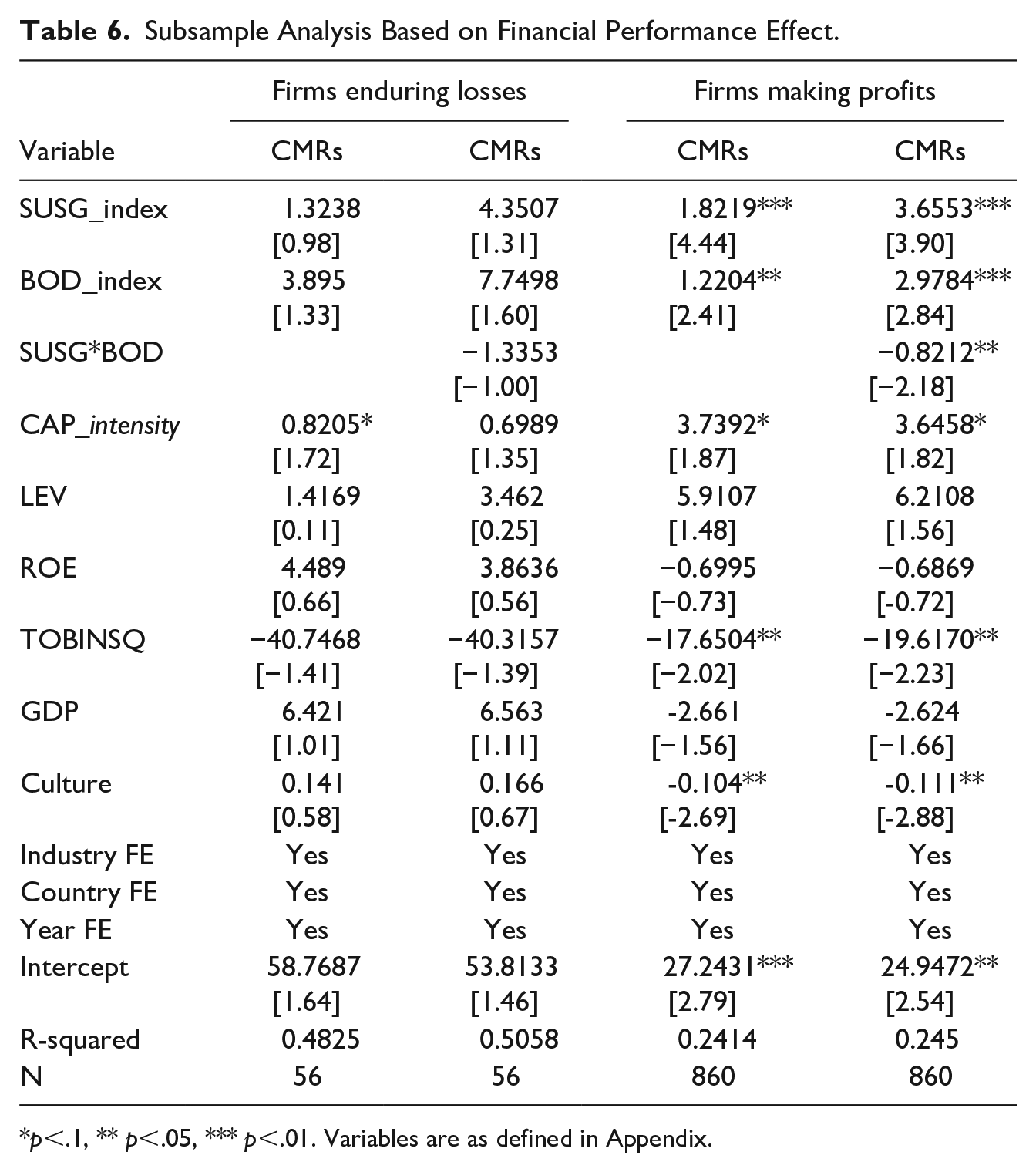

Giuliani and colleagues (2023) conclude that firms with better financial performance are highly likely to engage in abusive behaviors when compared with firms of the same industry peers. Consequently, companies with strong financial performance could be subject to intense scrutiny from investors, and therefore the conflict mineral practice would be expected to adequately keep investors informed. Meanwhile, the pressure to comply with certain social requirements may conflict with the most operationally efficient actions. Companies may continue to use conflict minerals if the cost of changing suppliers exceeds the benefits of gaining a reputation as a responsible sourcing company (Baik et al., 2021). Therefore, in Table 6, we test the impact of a firm’s financial position on CMRs by dividing the sample into profitable firms (i.e., firms that are reporting profits at the end of the financial year) and firms that are making losses at the end of the financial year. We find that sustainability-oriented governance factors are more likely to play a role in CMRs for profitable firms. This suggests that corporate financial health decreases the lenience for the lack of conflict mineral practices because companies have the required resources and organizational capabilities to adopt the best practice of responsible sourcing. However, companies that suffer from financial constraints might be more prone to strategically avoid engaging in conflict mineral practices.

Subsample Analysis Based on Financial Performance Effect.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

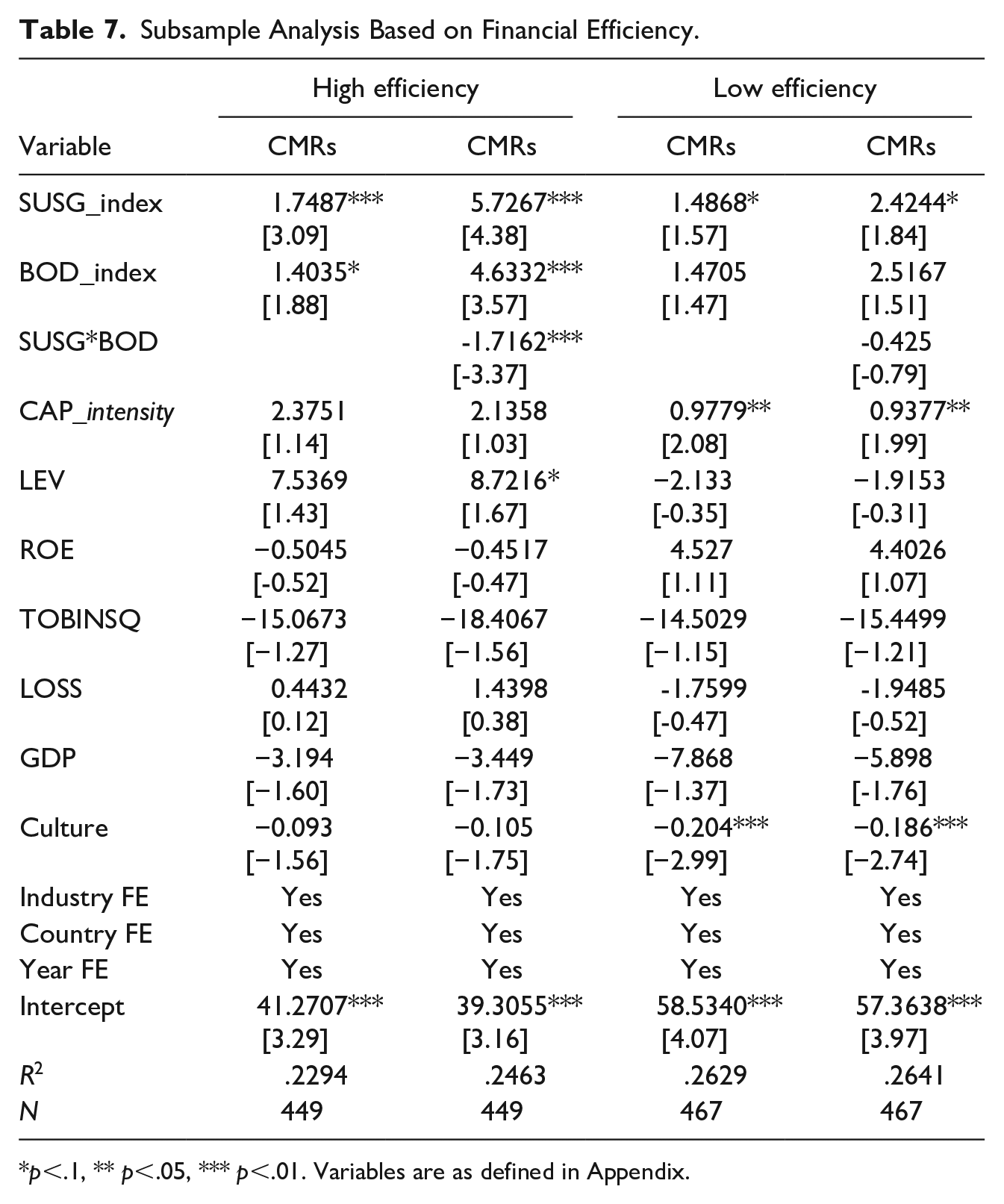

We provide more insight into the role that the financial efficiency of a firm may play in CMRs in Table 7. A business is efficient with its resources when it succeeds in transferring materials, labor, and capital into services and products that produce revenues. Efficient companies are characterized by a higher degree of social responsibility (Binh et al., 2022; Khediri, 2021). This may affect the tendency of firms to adhere to conflict mineral due diligence requirements. In Table 7, we divide the sample into subsamples of firms with high or low efficiency. We use the capital intensity ratio measured by assets over sales, where firms are more efficient when they use fewer assets to earn revenue. Our results are more pronounced and consistent with the baseline findings for companies with better financial efficiency. This indicates that sustainability-oriented governance factors seem to impact CMRs for companies with high financial efficiency more than companies with poor financial efficiency.

Subsample Analysis Based on Financial Efficiency.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

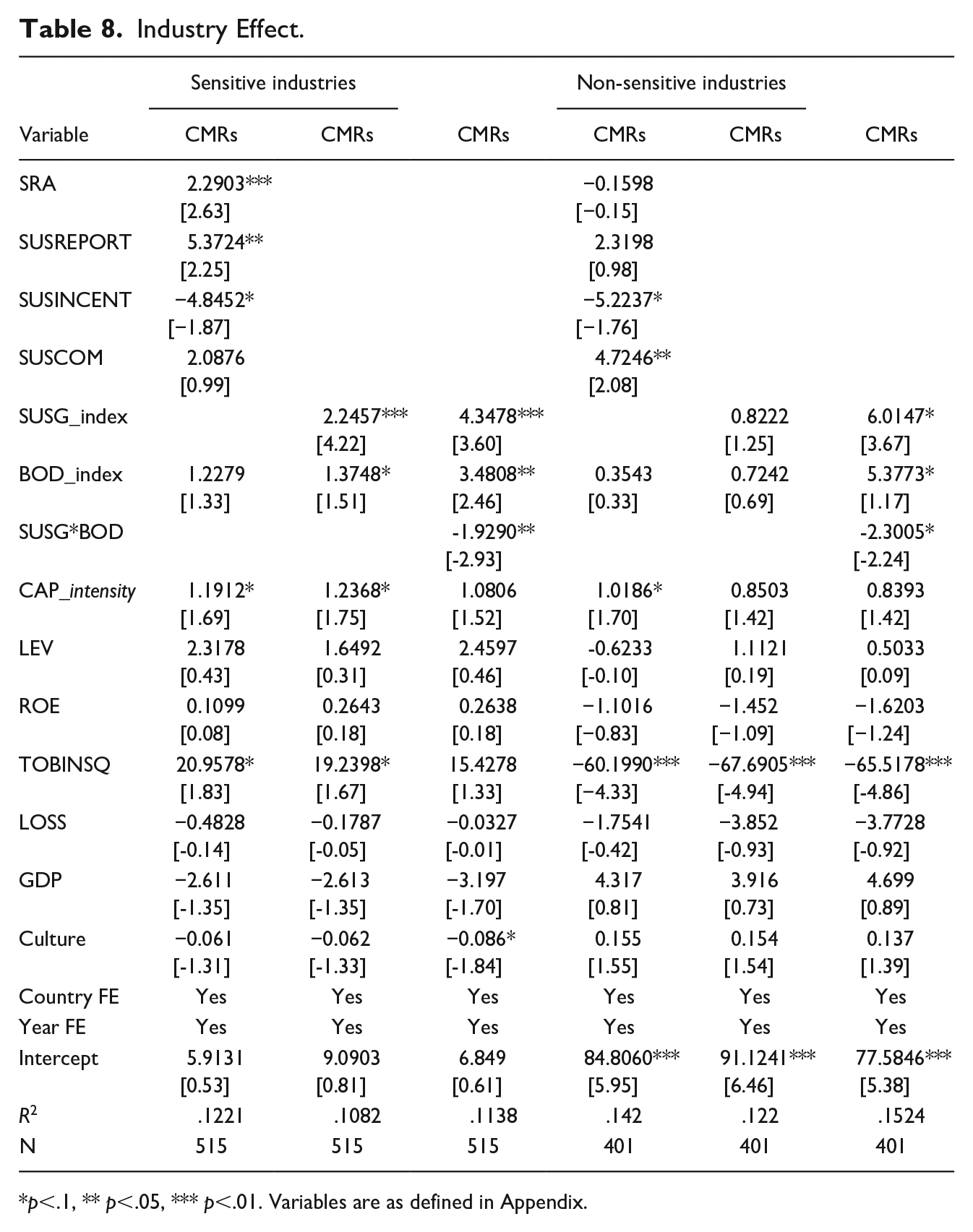

Table 8 shows the industry effect. Companies belonging to different industries may vary in their interest in sustainability and their association with conflict minerals. Therefore, we divide the sample into sustainability-sensitive firms and non-sensitive firms. We classify firms as sustainability-sensitive and are particularly linked to conflict minerals when they operate in the technology, telecommunications, industrial (including metals, technological hardware, and aerospace and defense industries), basic materials (including chemicals and mining), and energy industries. Meanwhile, companies belonging to financial, consumer discretionary, consumer staples, and health care industries are classified as non-sensitive firms. Our results are more pronounced and consistent with the baseline findings for companies operating in the sustainability-sensitive sectors. This indicates that companies from these sectors are more likely to engage in conflict mineral practices.

Industry Effect.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

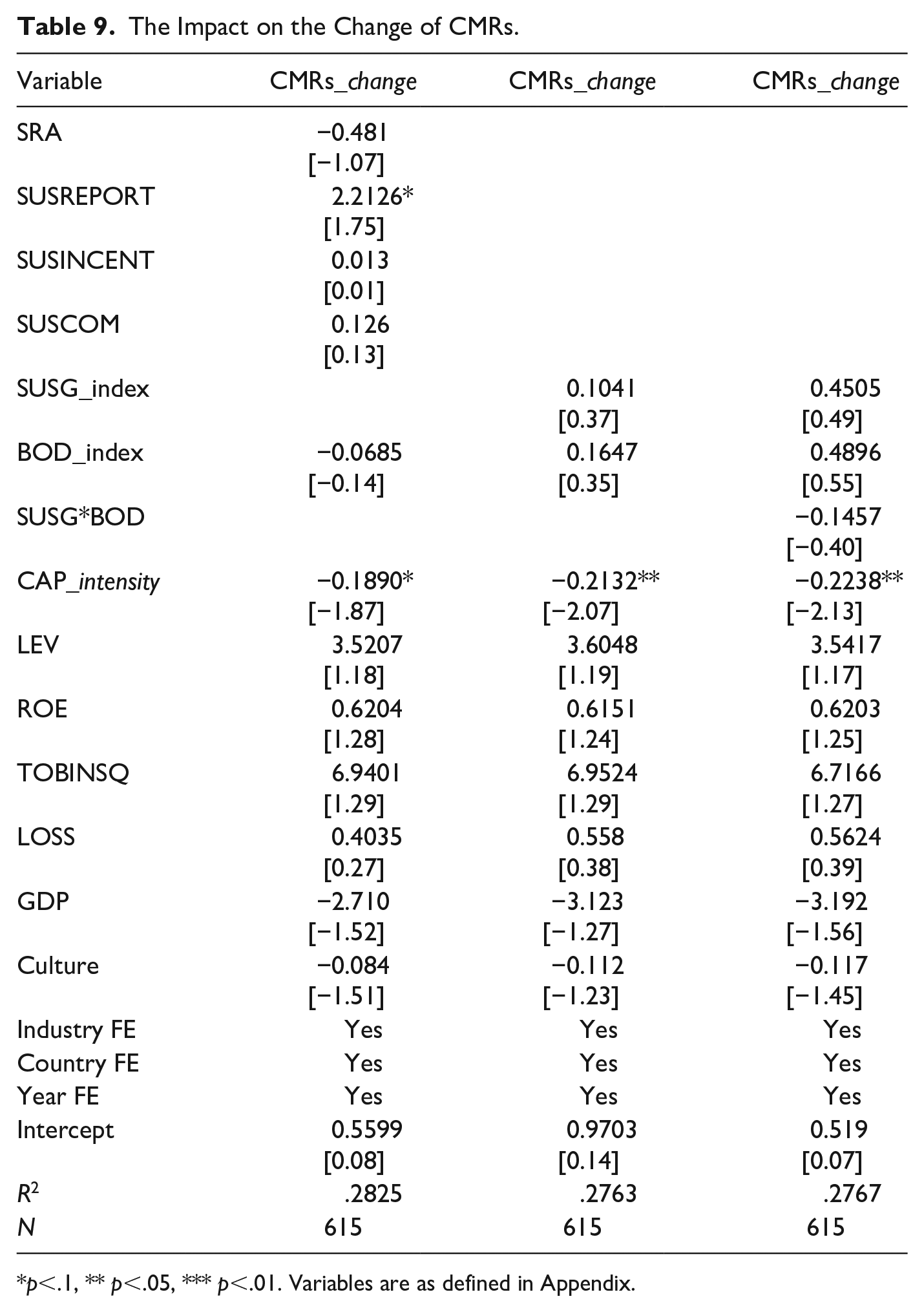

We investigate the effect of sustainability-oriented governance on the change of CMRs (CMR_change) in Table 9. The role that sustainability-oriented governance mechanisms may play in shaping the corporate response to conflict mineral risks may change over time. As a result, we investigate the effect of sustainability-oriented governance on the change that occurs in CMRs from year to year. To test this, we create a balanced sample of 123 observations per year and a total of 615 firm-year observations. Table 9 shows that sustainability governance factors are not significantly associated with CMR_change, which indicates that the continuation of conflict mineral ratings over the years of the conducted study is associated with persisting sustainability governance, which directs firm’s resources toward improving its sustainable strategies (including those associated with conflict minerals).

The Impact on the Change of CMRs.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

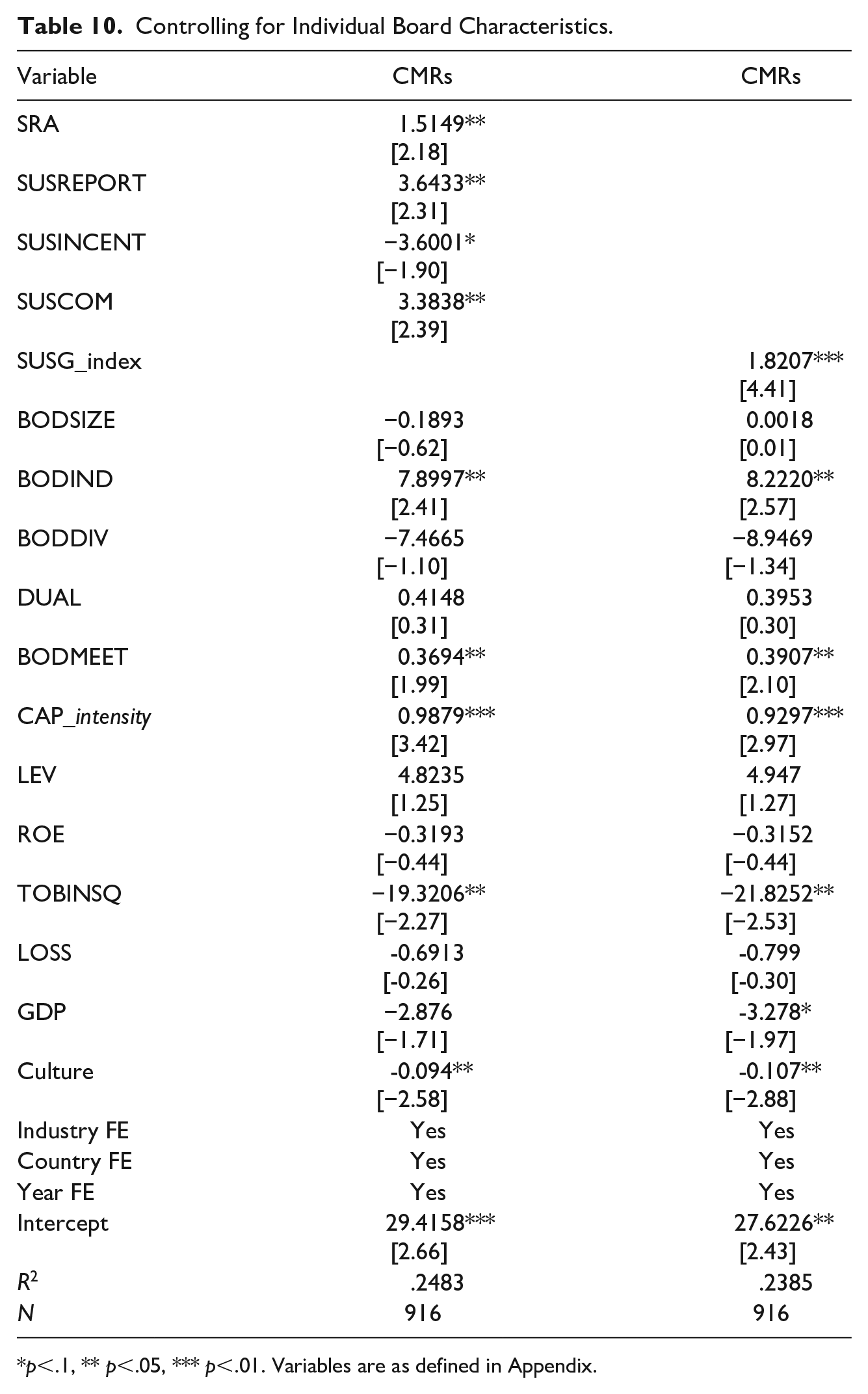

In Table 10, we replace the corporate board quality index (BOD_index) with board individual characteristics (i.e., BODSIZE, BODIND, BODMEET, BODDIV, and DUALITY) to capture their individual effects. Our findings for the independent variables (i.e., sustainability-oriented governance factors) remain consistent with the initial baseline analysis. Regarding the individual board characteristics, we find both BODIND and BODMEET are significant at the 0.05 level and are positively associated with CMRs. This result is in line with agency theory and suggests that a larger proportion of independent directors on the board helps to enhance monitoring and control, while frequent board meetings improve discussion and address effective CSR strategies (Al-Shaer et al., 2022; Jizi, 2017).

Controlling for Individual Board Characteristics.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

Additional Analysis: Addressing Endogeneity

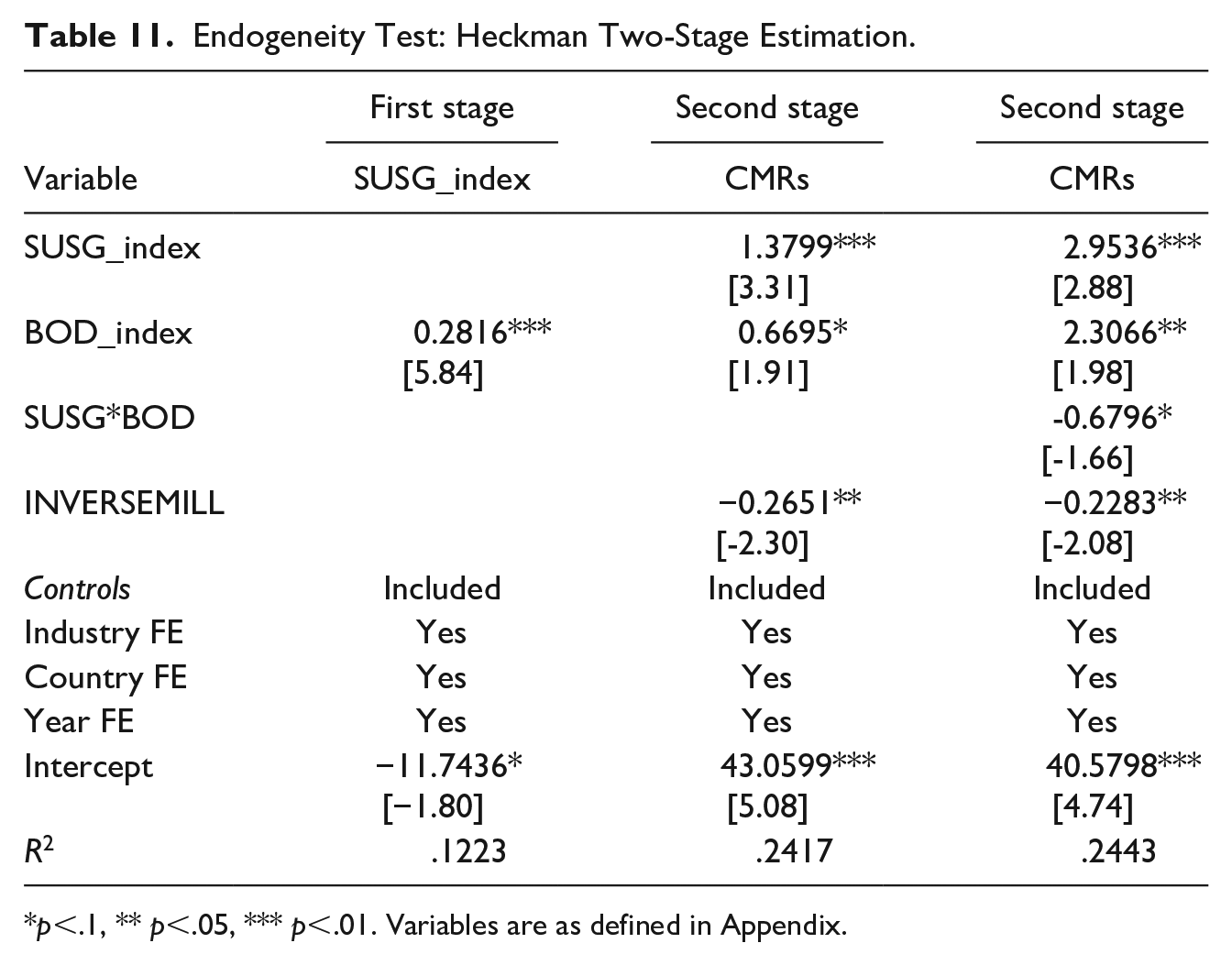

Given that the audit of conflict mineral reporting by external parties is not mandatory (Dalla Via & Perego, 2018), the voluntary adoption of an independent audit could be a managerial choice and is therefore subject to selection bias. Moreover, the reporting of sustainability information is voluntary and is subject to a high degree of discretion (Muslu et al., 2019). In addition, the linkage of sustainability targets to executive compensation is a growing corporate practice for better governance and accountability (Al-Shaer & Zaman, 2019). Table 11 addresses the endogenous self-selection bias of sustainability governance variables by using the Heckman-type correction. Heckman (1979) proposes a two-stage estimation procedure to take endogeneity bias into account. In the first stage, we model the decision to have a sustainability governance system in a firm, in which we regress SUSG_index on the board and company-specific variables. We then calculate the inverse Mills ratio (IMR) and include it in the regression of our main findings from the multivariate analysis. The interpretations remain the same when applying the Heckman (1979) two-step approach. The results for the first and second stages are reported in Table 11.

Endogeneity Test: Heckman Two-Stage Estimation.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

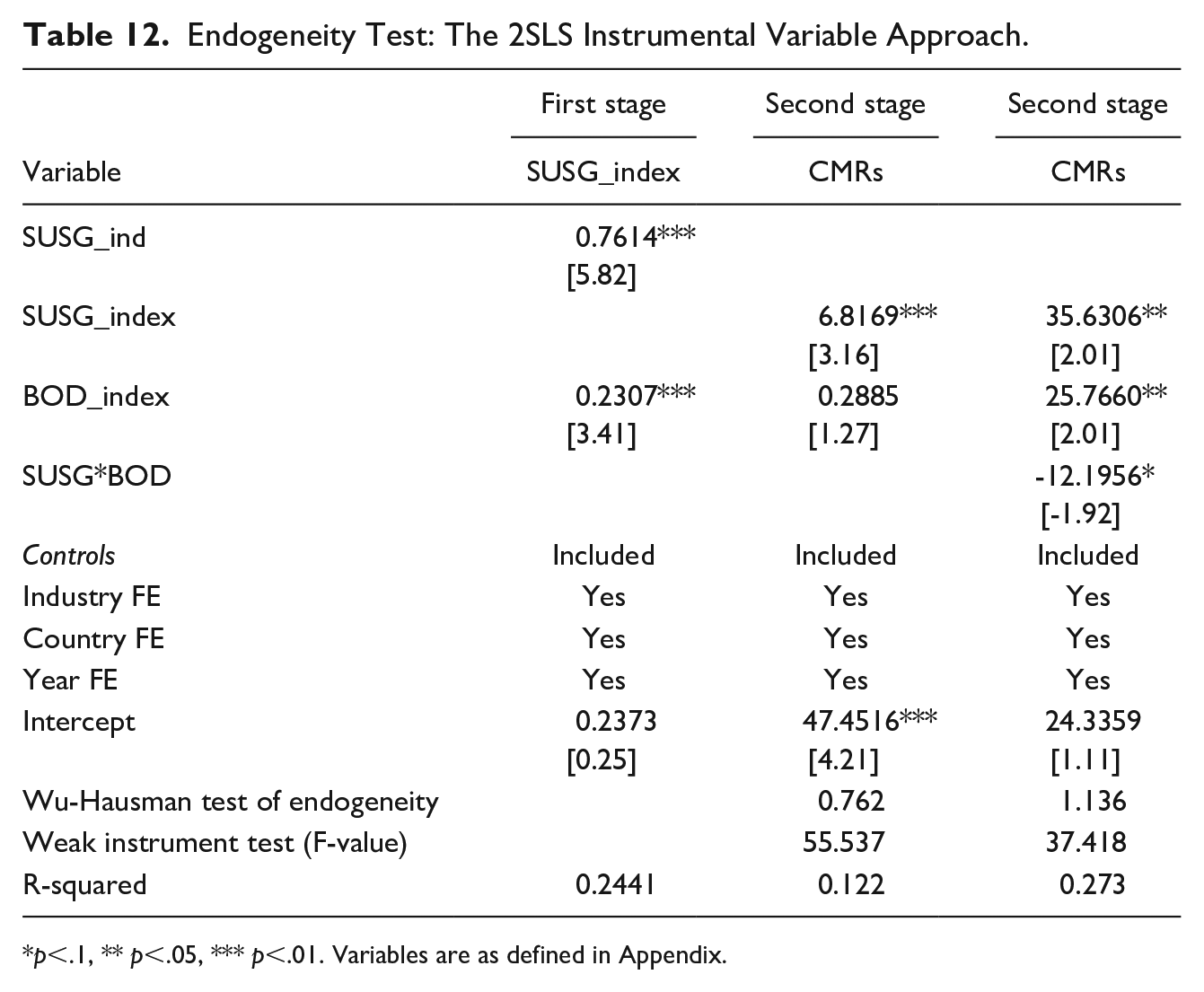

To control for any potential endogeneity arising from unobservable omitted variables (i.e., firm incentives), we apply 2SLS instrumental variable regressions. The 2SLS approach requires a variable to be found that is correlated with the first-stage dependent variable (SUSG_index) but is not correlated with the second-stage dependent variable (i.e., CMRs). To accommodate this issue, we use the industry average of the independent testing variable (SUSG_index), excluding the focal firms, as the instrumental variable (Murcia et al., 2021; Wang & Li, 2008). We expect that SUSG_index will be correlated with its industry norms, while it is unlikely that industry-mean sustainability governance is linked to CMRs. In the first stage, we regress the endogenous variable SUSG_index on the instrumental variable (SUSG_ind) and other control variables. The second stage uses the fitted values from the first stage to instrument the endogenous variable. Overall, the results of the 2SLS regression analysis that are reported in Table 12 are compatible with the baseline analysis results.

Endogeneity Test: The 2SLS Instrumental Variable Approach.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

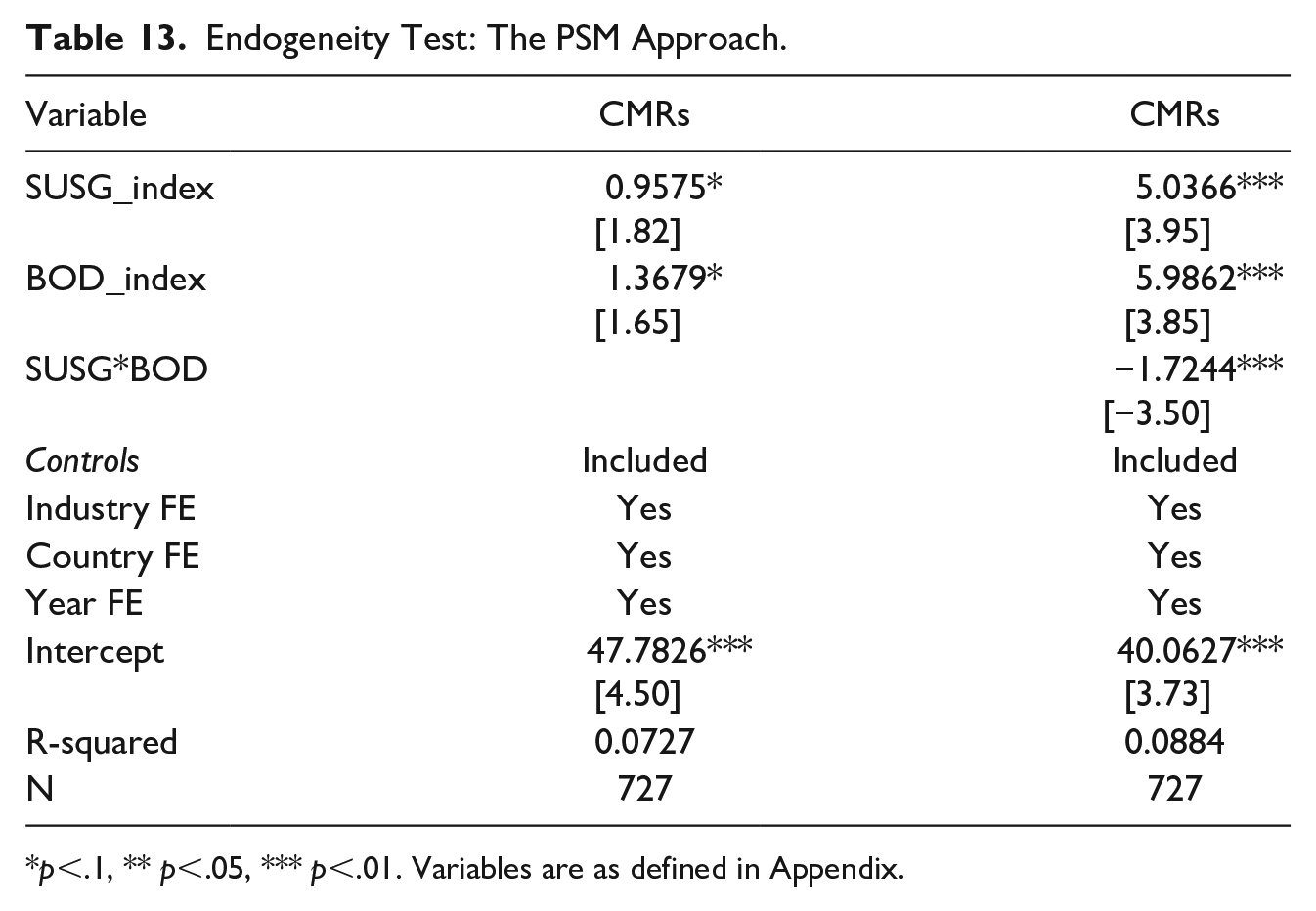

We further address the endogeneity that may result from model misspecification using the PSM technique. We follow a model developed by Leuven and Sianesi (2003) and created treatment and control groups by dividing the sample into quartiles based on SUSG_index. Toward this end, we use top quartile values for SUSG_index and assign a value of 1 for the treatment group (this includes observations that fall inside the distribution’s top quartile with the highest SUSG_index scores) but 0 for the rest of the values representing the control group (this includes the remainder of the sample). We run the first stage of the PSM approach by employing a probit model that uses SUSG_index as the dependent variable. The variables that determine sustainability governance are used as regressors (board and firm-specific variables). We then estimate the propensity score and match based on it for each year-industry group, utilizing the nearest neighbor matching technique with a 1% radius matching approach (Albitar et al., 2023). We then re-examine our model for the matched sample and report the results in Table 13. 8 The results for the matched sample remain the same after using the PSM technique and are consistent with baseline findings that sustainability governance is positively associated with CMRs, and that board governance plays a moderation role in this association.

Endogeneity Test: The PSM Approach.

p<.1, ** p<.05, *** p<.01. Variables are as defined in Appendix.

Summary and Conclusion

Previous studies have investigated the impact of board characteristics and firm-specific characteristics on corporate actions to address and report on conflict minerals (Dalla Via & Perego, 2018). We extend these studies by considering sustainability-oriented governance factors and their impact on CMRs. In particular, we consider whether the existence of independent external audits, the existence of sustainability reports to communicate a firm’s message, the inclusion of sustainability-related targets in executive compensation contracts, and the existence of board-level sustainability committees with special oversight roles for sustainability processes are associated with CMRs. The results confirm our hypotheses about the impact of sustainability-oriented governance in shaping the corporate response to conflict mineral risks. Furthermore, we investigate the moderating role that effective boards can play in the relationship between sustainability governance and CMRs. We find that companies with strong board governance can substitute for sustainability governance mechanisms in improving CMRs.

The choice of assurance may help to determine the substantive sustainability reporting process, which needs to be undertaken to enhance transparency and reporting quality and reduce stakeholder pressures (Al-Shaer et al., 2022). Researchers have questioned the degree of independence of assurance practice and have shown that it works more like an internal management tool to tackle specific risks and issues rather than a practice to enhance transparency, credibility, and accountability (Kolk & Perego, 2014). Despite previous concerns, the majority of existing studies have found that assurance provided by Big 4 accounting firms enhances the credibility of information due to their expertise in risk assessment and consideration of litigation risk in providing assurance (Al-Shaer et al., 2022). Consequently, companies should consider increasing the transparency of their global supply chain by purchasing an independent audit of conflict mineral reports. The objective of this audit is not to confirm that the company’s products are free of conflict minerals. Instead, the objective is to confirm that its due diligence conforms to the framework used by the company and is described well in the conflict mineral reports (Sankara et al., 2016). For example, Intel Corporation supports the development and implementation of due diligence practices and a responsible mineral sourcing program, and has had its conflict mineral reports audited by Ernst & Young for its fiscal years 2017, 2018 and 2019. 9 As companies progress toward achieving conflict-free status for their minerals, a significant increase in independent external audits and the engagement of accounting firms in human rights issues could be expected to enhance the credibility and transparency of conflict mineral reporting and mitigate reputational risk (Sankara et al., 2016).

The results of this study have several implications for theory and practice. First, we offer a multitheoretical approach combining the RDT with stakeholder theory and agency theory to examine the association between sustainability governance and conflict mineral ratings and the moderating role of board quality. Thus, our study lies at the intersection of these theories. In line with this paradigm, our evidence documents that it is necessary to consider the influence of sustainability-oriented governance mechanisms, which demonstrate corporate ethical behavior and represent essential capital resources, on corporate communications on human rights issues. From the perspective of stakeholder theory, our results demonstrate that sustainability governance mechanisms can induce firms to set their CSR agenda and align management decisions with the stakeholder’s expectations (García-Sánchez, 2020; Jizi, 2017). Our results also support that effective boards can moderate the role that sustainability governance plays in enhancing CMRs.

This study has important practical implications for companies to improve corporate practices in the areas of risk management, human rights impact, and effective reporting. Companies are encouraged to show their ability to innovate beyond developing a compliance strategy—they should also implement a process of planning the supply chain to achieve a unified and robust response to conflict mineral risks. Corporate governance needs to address a firm’s unethical behaviors and hold them accountable for their business’s wider impact on society. Therefore, there is a need for further investigation of independent audit practices to oversee the assurance of a company’s human rights reporting. As our results suggest, sustainability-oriented governance mechanisms would facilitate communication and engagement with stakeholders on human rights issues. Consequently, investors, customers, and regulators should place more pressure on companies, encouraging them to put more effort into addressing the harm of violence linked to the conflict minerals that are embedded in their products. It is imperative to understand the role of global organizations in influencing corporate transparency about human rights, in line with the expectations of the broader community. Our study aims to recommend some ways to construct more informed debates in the press and society on what companies do to ensure that they do not contribute to conflict and human rights abuses.

Our study provides opportunities for future research on conflict minerals. First, our sample includes well-known multinational companies with large market capitalization. Therefore, future research could include a sample of small firms and investigate their conflict mineral practices. Second, our study provides evidence of the relationship between sustainability-oriented governance mechanisms and CMRs. Therefore, further research into casual relationships and the assessment of different rationales that may affect the relationship between sustainability-oriented governance and CMRs is needed. Third, this study examines the moderating role of board governance in the relationship between sustainability governance and CMRs. Consequently, future research could examine the moderating role of ownership structure in this association. Future research could also examine the impact of country-level variables, such as Hofstede’s national culture and the World Bank Governance Index, on CMRs. Finally, this study uses rating scores prepared by RSN, which provide a comprehensive and thorough assessment of a company’s due diligence for conflict mineral practices (Dalla Via & Perego, 2018). Further research could apply an alternative measure of conflict mineral adherence, including developing measures obtained from textual analysis and a qualitative approach that includes conducting interviews with various stakeholder groups, such as customers, employees, and supply chain partners, to obtain their opinions about responsible mineral sourcing programs. It would also be interesting to explore substantive versus symbolic compliance with adherence to conflict minerals under the Dodd–Frank Act. It is imperative to understand the role of global organizations in influencing corporate transparency about human rights in line with the expectations of the broader community. Our study aims to recommend some ways forward for constructing more informed debates in the press and society on what companies do to ensure they do not contribute to conflicts and human rights abuses.

Footnotes

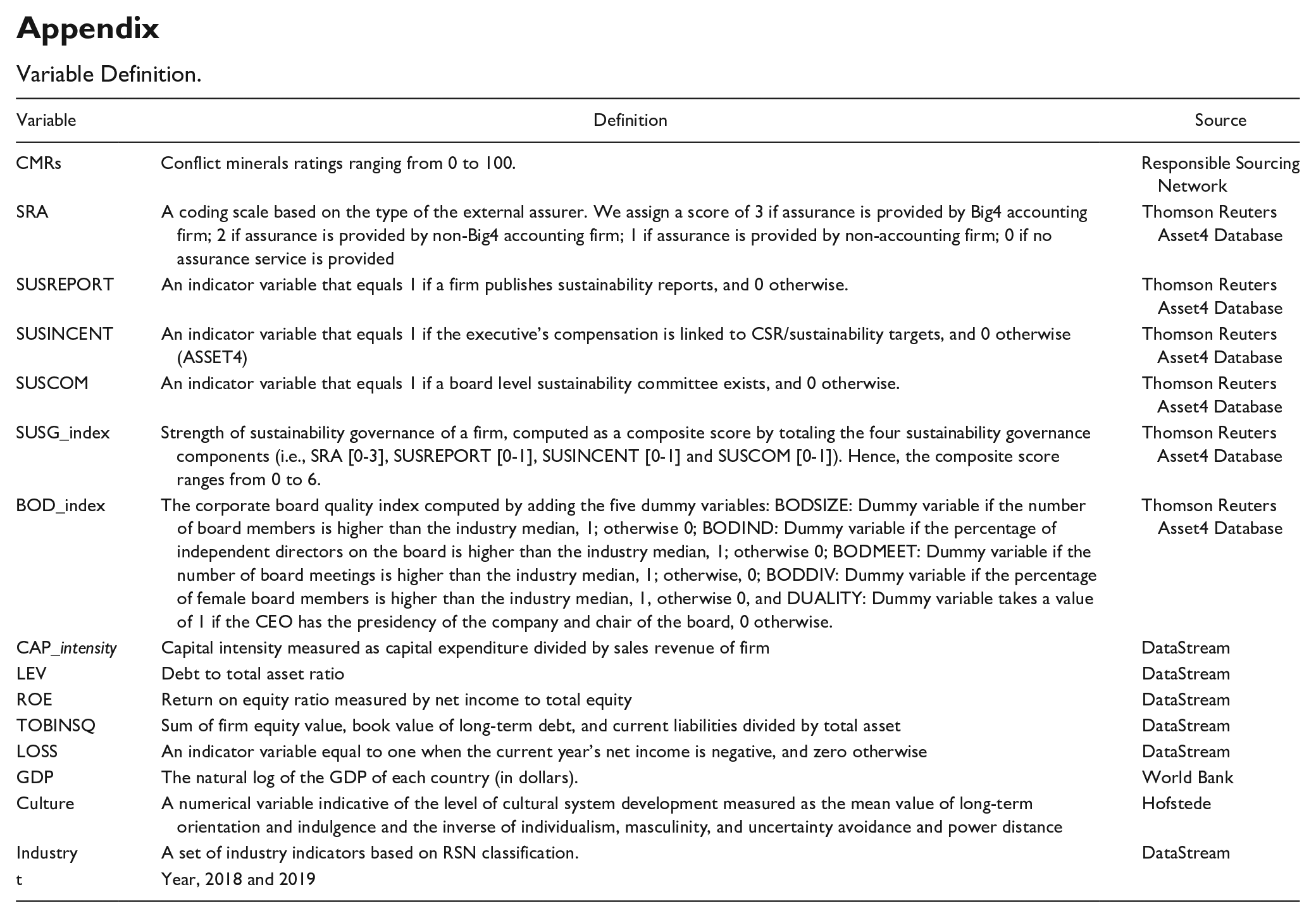

Appendix

Variable Definition.

| Variable | Definition | Source |

|---|---|---|

| CMRs | Conflict minerals ratings ranging from 0 to 100. | Responsible Sourcing Network |

| SRA | A coding scale based on the type of the external assurer. We assign a score of 3 if assurance is provided by Big4 accounting firm; 2 if assurance is provided by non-Big4 accounting firm; 1 if assurance is provided by non-accounting firm; 0 if no assurance service is provided | Thomson Reuters Asset4 Database |

| SUSREPORT | An indicator variable that equals 1 if a firm publishes sustainability reports, and 0 otherwise. | Thomson Reuters Asset4 Database |

| SUSINCENT | An indicator variable that equals 1 if the executive’s compensation is linked to CSR/sustainability targets, and 0 otherwise (ASSET4) | Thomson Reuters Asset4 Database |

| SUSCOM | An indicator variable that equals 1 if a board level sustainability committee exists, and 0 otherwise. | Thomson Reuters Asset4 Database |

| SUSG_index | Strength of sustainability governance of a firm, computed as a composite score by totaling the four sustainability governance components (i.e., SRA [0-3], SUSREPORT [0-1], SUSINCENT [0-1] and SUSCOM [0-1]). Hence, the composite score ranges from 0 to 6. | Thomson Reuters Asset4 Database |