Abstract

Introducing and implementing corporate sustainability poses many challenges to business organizations. In this longitudinal, inductive study, we focus on how such challenges are handled in a Dutch bank that is developing its sustainability policies. We examine why there is such a high degree of tension and conflict within the organization and identify how the development of these policies is affected by the interplay between subcultures and institutional logics. We show how different subcultures affect the enactment of logics by infusing the rational and mindful behavior coming from logics with (sub)cultural values, beliefs, and assumptions. In turn, conflicting logics amplify subcultural characteristics between groups by shaping different behavior and practices. Together, this leads to a magnification of subcultural differences while, at the same time, logics are increasingly being perceived as incompatible.

The recent financial crisis challenges the conventional thinking of companies concerning their social responsibilities in wider society (Fassin & Gosselin, 2011; Giannarakis & Theotokas, 2011; Hargie, Stapleton, & Tourish, 2010). Companies are increasingly triggered to reach beyond their mere economic responsibilities and to also take their environmental and social responsibilities into account. Whether corporations follow up on these responsibilities or merely engage in symbolic acts, such as “window dressing” or “greenwashing,” is often not clear (Delmas & Cuerel Burbano, 2011; Harris & Crane, 2002; Weaver, Treviño, & Cochran, 1999). We still have limited insight into the internal development, adoption, and maintenance of corporate sustainability policies and practices within organizations (De Lange, Busch, & Delgado-Ceballos, 2012; Linnenluecke & Griffiths, 2010).

Despite concerns about the commitment to become more sustainable, there seems to be a growing societal consensus that the maximization of profit can no longer be the only goal of corporations (Kleine & Von Hauff, 2009). Since the start of the financial crisis in 2008, banks, in particular, have been under a magnifying glass. A mix of inadequate regulation, the dominant banking industry culture that is “striving primarily or exclusively for shareholder value maximization” (Wiek & Weber, 2014, p. 9), and profit maximization are observed as key contributors to the global financial crisis (Maggetti, 2014; Moshirian, 2011; Spicer et al., 2014). Critics point to a need for change in market and firm culture (Spicer et al., 2014), as well as to institutional change such as in banking regulation and governance (Levine, 2012). Banks try to respond to this institutional pressure to manage their reputational risks (Furrer, Hamprecht, & Hoffmann, 2012; Mulder & Koellner, 2011) and to regain trust and legitimacy (de Graaf & Stoelhorst, 2013; Fassin & Gosselin, 2011; Hargie et al., 2010; Herzig & Moon, 2013). Consequently, the societal logic of sustainability has been gaining terrain in the field of banking as is also visible by the clear rise in the number of corporations reporting on their sustainability actions and goals during the last few decades (De Lange et al., 2012; Global Reporting Initiative [GRI], 2012; Kolk, 2004). Still, such an increase in sustainability reporting and policy development does not necessarily mean that companies really improve their environmental and social performance (Lyon, 2004; Weaver et al., 1999). All these developments hence pose notable challenges to banks, as well as to other organizations, not in the least because of the many barriers that can hinder institutional and organizational cultural change (Linnenluecke & Griffiths, 2010; Olsen & Boxenbaum, 2009).

To better understand how organizations internally deal with the increasing institutional pressure to become more socially responsible, and to capture the role of organization culture and institutional logics therein (Hinings, 2011; Zilber, 2011), we conducted a longitudinal, inductive study over 43 months at DUTCH Bank, a large commercial bank in the Netherlands. We identified subcultural differences based on professions between two different departments and the presence of two different logics relevant for both departments: a market logic and a sustainability logic. During moments of interaction, members from the different departments struggled to understand each other’s approach to sustainability issues, resulting in a high degree of tension and conflict between them. Ultimately, the two logics were mutually perceived as incompatible and conflicting. We suspect that an explanation for this struggle over sustainability lies in the interplay between organizational subcultures and institutional logics. To better understand this interplay during the development of sustainability policies within DUTCH Bank, our main research question asks,

There has been a recent discussion about the uncomfortable similarity between the concepts of organizational (sub)culture and institutional logics (Aten, Howard-Grenville, & Ventresca, 2012; Caprar & Neville, 2012; Harris & Crane, 2002; Hinings, 2011; Zilber, 2011). With this article, we aim to contribute to this literature by theoretically and empirically teasing these two related constructs apart. In doing this, we make three contributions.

First, the question of how individuals translate and enact logics into action during everyday organizational activities is still lacking empirical research (McPherson & Sauder, 2013). Individuals carry institutions and they are not passive (Zilber, 2002); they interpret logics and then translate them into action (McPherson & Sauder, 2013). As logics are open to multiple interpretations (Voronov, De Clercq, & Hinings 2013; Zilber, 2002), individual enactment of logics can vary across individuals. The resulting actions consequently provide traction to specific interpretations of a logic. These differences in logic interpretations, translations, and strategies for action then again can lead to (further) misunderstanding between different subcultures (Howard-Grenville, 2006) and thus may spur a high and sustained degree of tension and conflict.

Second, even though we know that organizations can experience the coexistence of multiple logics (Besharov & Smith, 2014; Glynn & Raffaelli, 2013; Greenwood, Raynard, Kodeih, Micelotta, & Lounsbury, 2011; Reay & Hinings, 2009), we still need a better understanding of how organizations internally deal with such institutional pluralism (Battilana & Dorado, 2010; Besharov & Smith, 2014) as well as with heterogeneity in organizational responses to institutional logics (Greenwood, Díaz, Li, & Céspedes Lorente, 2010). We argue that differences in interpretations and enactment of logics between subcultures can provide a possible explanation.

Third, when multiple logics are accessible in an organization, actors can be selective in how to adhere to any particular logic (Voronov et al., 2013). Actors’ responses to multiple logics are reflections of their perceptions of these logics and can be reflections of which logic they consider dominant. “The prioritization of logics will be determined by the relative power of each logic’s representative. Thus, when one logic is represented, it is that logic that will be embedded in organizational decisions and behaviours” (Greenwood et al., 2011, p. 349), and thus, it is the dominant logic that guides organizational actors’ behavior (Thornton, 2004). When there is a clear dominant logic, then there is no conflict, as Besharov and Smith (2014) have pointed out. However, in making this argument, they did not account for the presence of subcultures. As McPherson and Sauder (2013) already recognized, “actors affiliated with a professional or organizational group will closely adhere to that group’s primary logic” (p. 22). At DUTCH Bank, we found in each of the two subcultures that individuals adhered to a different primary logic, making that logic their dominant logic. The two subcultures thus each adhered to different dominant logics, providing them with contradictory prescriptions for joint action and implicating extensive conflict (Besharov & Smith, 2014).

In the next section, we discuss the main concepts that guided our research: subcultures, logics, and sustainability, and the relationship between them. As is common in inductive studies (cf. Dutton et al., 2006; Nag, Corley, & Gioia, 2007), the theoretical review serves as “a set of orienting points that anchored our research question, informed our methods and provided direction for our analysis” (Harrison & Rouse, 2014, p. 1258). We then discuss how we conducted our research and analyzed our data, followed by a description of the empirical setting. In our results, we zoom in on the development of two sustainability policies at DUTCH Bank. This offers relevant insights on the interplay between subcultures and logics and the consequences thereof.

Subcultures, Logics, and Sustainability

The aim of this article is to understand the interplay between subcultures and institutional logics during sustainability policy development within a large and complex organization, where the policy development phase is the entire phase before a policy is officially approved and implemented. Before we examine how subcultures and institutional logics appeared in our empirical study, we first briefly discuss the literature on both concepts.

Organizational Subcultures

Organizational culture has been defined in many ways (Linnenluecke, Russell, & Griffiths, 2009; Martin, 2002; Ouchi & Wilkins, 1985; Sackmann, 1992; Van Maanen, 2011), underlining that culture is a heterogeneous and encompassing term characterizing human behavior within organizations. As Sackmann and Philips (2004) noted, defining culture is context dependent and underpinned by different methodological approaches, theories, and assumptions. In the literature, the focus on “cognitive components such as assumptions, beliefs, values, or perspectives as the essence of culture” (Sackmann, 1992, p. 140) often prevails. Including broader methodological and theoretical contexts, culture can be viewed as “a broad system anchored by values or overarching toolkits, within which categories, frames, and stories serve as cultural manifestations, which congeal, express and diffuse commitments, ideas, and beliefs among actors” (Giorgi, Lockwood, & Glynn, 2015, p. 4). Given our interest in understanding how an organization is developing its sustainability policies, these definitions are appropriate starting points for our research.

Although organizations are seen as having an overall organizational culture, this culture often consists of several subcultures (Martin, 2002; Sackmann, 1992). Subcultures can be defined as “whatever cultures arise in the divisions, departments, and other fairly stable subgroups of that organization” (Schein, 1992, p. 256). Due to functional and departmental differences, each subculture develops its own values, behaviors, patterns, artifacts, and practices by which they grow apart from other subcultures within the organization, making them distinct parts of the overall organizational culture (Lok, Westwood, & Crawford, 2005). Within subcultures, basic assumptions can become so much taken for granted that their members share interpretations of essential information (Howard-Grenville, 2006; Lok et al., 2005), leading to misunderstandings and to differences in interpretations, problem definitions, and strategies for action between different subcultures (Howard-Grenville, 2006). This can result in serious problems when these subcultures meet and interact (Bloor & Dawson, 1994; Howard-Grenville, 2006) and may cause conflicts, also about the way sustainability practices and standards should be interpreted, accepted, and operationalized (Faber, Jorna, & van Engelen, 2005; Füssel & Georg, 2000).

While subcultural differences between different departments thus may provide one explanation for the difficult development of sustainability policies, these differences might not be the only explanation. Members of different departments can also be guided by different institutional logics, derived from their positions in fields that are broader than the organization itself, such as the professions or the market segments in which they operate. Therefore, we now turn to theory on institutional logics.

Institutional Logics

Institutional theory has become very prominent in organizational studies, aiming “to understand why and how organizations adopt processes and structures for their meaning rather than their productive value” (Suddaby, 2010, p. 15). Institutions are observable through the structure and practices associated with them (Scott, 2001; Zilber, 2002) and are enacted through institutional logics (Reay & Hinings, 2009). Reay and Hinings (2009) defined institutional logics as

the basis of taken-for-granted rules guiding behaviour of field level actors [they] are the organizing principles that shape behaviour of field participants [ . . . ]; they refer to a set of belief systems and associated practices, they define the content and meaning of institutions. (pp. 629-631)

As such, institutional logics provide organizational members and their leaders with “a means for understanding the social world and the guidelines on how to interpret and function in social situations” (Greenwood et al., 2011, p. 318) and thus have implications for roles, skills and competences, practices, protocols, and performance criteria (Greenwood et al., 2011; Reay & Hinings, 2009; Thornton, 2002, 2004).

As most organizations are heterogeneous and “composed of functionally differentiated groups pursuing goals and promoting interests” (Greenwood & Hinings, 1996, p. 1024), a plurality of logics may be relevant to any single organization. This relevance can be translated into different perspectives within an organization; these perspectives in turn can challenge the internal balance between different actors and their daily practices (Besharov & Smith, 2014; Reay & Hinings, 2009). We speak of conflicting logics when their “respective systems of meanings and normative understandings, built into rituals and practices, provide inconsistent expectations” (Greenwood et al., 2011, p. 321). Different logics are associated with different organizational principles and thus require a different set of rational, mindful behaviors from actors (Reay & Hinings, 2009; Thornton, 2004).

When multiple logics are accessible within the organization and its wider environment, actors can be selective in how to adhere to, or call upon, a particular logic (Voronov et al., 2013). Logic enactment then might occur differently in specific departments, which could lead to a strengthening of the respective logics. Two different logics were represented in our case; for purposes of clarity, we already briefly introduce them here. On the field level, the financial sector propagates a market logic. This market logic highlights competitive advantage and a shareholder value orientation, emphasizing maximizing profit, efficiency, and economically motivated behavior (Friedland & Alford, 1991; Thornton, Ocasio, & Lounsbury, 2012). The sustainability logic is a societal logic that can be seen as entering the field of finance more prominently since the start of the financial crisis. This logic guides behavior characterized by concerns for social justice and environmental preservation, and could include elements such as personal commitment to reduce ecological footprints, waste reduction, and fair employment (Bansal & Roth, 2000; De Clercq & Voronov, 2011).

Before turning to our ideas on the interplay between institutional logics and subcultures, we zoom in on the concept of corporate sustainability which is important for the context in which our research took place.

Corporate Sustainability

Sustainability is a problematic concept which has been defined in numerous ways (Caprar & Neville, 2012; Faber et al., 2005; Kleine & Von Hauff, 2009; Linnenluecke et al., 2009), resulting in confusion and impediments regarding its operationalization, interpretation, and implementation within organizational practices (Bansal, 2005; Faber et al., 2005). On the global level, sustainability became known as sustainable development, from the Brundtland World Commission in 1987 which defined sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (Brundtland Report, 1987, p. 43). In relation to organizations and based on strategy and management literature, it was soon addressed with the term corporate sustainability (Linnenluecke & Griffiths, 2010). Following Caprar and Neville (2012), we define corporate sustainability as “creating long-term value by adopting a business approach that is equally mindful of economic, social, and environmental implications” (p. 231).

A common theme in many of the contemporary sustainability definitions is the need for business organizations to not only focus on financial objectives but to also incorporate social and environmental objectives. Sustainable development is built on three principles: environmental integrity, social equity, and economic prosperity (Bansal, 2005; Brundtland Report, 1987). All three are increasingly considered equally valid and necessary within business (Bondy, Moon, & Matten, 2012) and “if any one of the principles is not supported, economic development will not be sustainable” (Bansal, 2005, p. 198). Within sustainability research, the focus primarily lies on how businesses respond to societal and environmental concerns (Füssel & Georg, 2000) and how they manage their impact on these issues (Epstein, 2008). Less is known about how businesses translate sustainability values into their operational practices (Bansal, 2005; Linnenluecke & Griffiths, 2010; Wickert & de Bakker, 2016). Developing and implementing sustainability policies is one way to make such a translation.

Sustainability issues touch upon multiple levels and often are quite complex in and of themselves (Reinecke & Ansari, 2016). A combination of theoretical perspectives can help in gaining insight into how organizations internally handle the adoption of corporate sustainability practices (Linnenluecke & Griffiths, 2010) of which the development of sustainability policies is a part. Hence, the situation at DUTCH Bank during the development of sustainability policies provides a suitable research opportunity that would benefit from applying multiple perspectives (Aguinis & Glavas, 2012; Reinecke & Ansari, 2016).

Combining Culture and Logics

An organizational culture perspective can be used to explain how sustainability is perceived within the organization at the (sub-)organizational level (Athanasopoulou & Selsky, 2015), where it may hinder or facilitate sustainability adoption (Caprar & Neville, 2012). Fostering a business culture that is supportive of sustainability thus is a key challenge for organizations (Maon, Lindgreen, & Swaen, 2010). However, subcultural differences between departments can lead to variation in understandings of sustainability between these departments (Harris & Crane, 2002; Howard-Grenville, 2006). Cultural studies on sustainability adoption have showed that compatibility between sustainability principles and cultural norms and values increases the likelihood of sustainability adoption (Caprar & Neville, 2012). Therefore, when subcultural differences lead to different understandings of sustainability issues, they might inhibit the organizational responses or create ambiguity about the purpose and scope of sustainability policies.

Furthermore, the institutional context in which an organization is embedded may help to understand the pressures that shape acceptance or disapproval of sustainability actions and policies within an organization (Aguinis & Glavas, 2012; Athanasopoulou & Selsky, 2015; Caprar & Neville, 2012; Glynn & Raffaelli, 2013). Institutional theory shows that “pressures from local, national, or global institutions that promote sustainability directly contribute to sustainability adoption via the well-known legitimacy and mimetic mechanisms” (Caprar & Neville, 2012, p. 238). Institutional logics have been explored before as a key element within sustainability practice implementation (Glynn & Raffaelli, 2013; Lounsbury, Ventresca, & Hirsch, 2003). Glynn and Raffaelli (2013), for instance, used institutional logics to explain the conflicting institutional pressures that organizations experience to become more socially responsible whereas Lounsbury and colleagues (2003) highlighted the transformation process of socioeconomic practices toward sustainability.

Yet, as pointed out earlier, within a large organization, a multiplicity of institutional logics often exists. These logics may offer competing templates for how and why to do certain things. Such opposing demands may be perceived as competing and may thus challenge the process of sustainability policy development as market logics will offer different templates than sustainability logics. Considering both organizational subcultures and institutional logics as being based on different mechanisms, can help in understanding the difficulties in developing sustainability policies within an organization. By stressing the differences in mechanism, we thus disentagle the notion that institutions and culture are “uncomfortably similar” (Caprar & Neville, 2012, p. 236) as they overlap on theoretical, methodological, and empirical grounds (Aten et al., 2012; Caprar & Neville, 2012; Hinings, 2011). Consequently, we can regard subcultures and institutional logics as particularly close because discussions of each of these concepts share much of the same wording such as symbols, meaning, or values.

Examples of overlap in language are explanations of organizational culture as carriers of institutional logics (Scott, 2001; Thornton, 2002), or institutional logics being reproduced by cultural assumptions (Friedland & Alford, 1991), in turn leading toward the cultural embeddedness of a particular logic (Thornton et al., 2012). These similarities make institutions “thoroughly cultural” (Giorgi et al., 2015, p. 27). The relationship between both concepts is further explored by Caprar and Neville (2012), who argued that culture 1 can facilitate or hinder “the development or adoption of institutional pressures for sustainability in that particular context [in which] institutional pressures for sustainability are both generated and observed” (p. 232).

While it is tempting to think along the lines of similarities between subculture and logics, we argue that there is value in exploring the differences between both concepts to better understand what drives and/or hampers the development of sustainability policies within an organization. After all, the basic processes underlying these concepts are quite different. As organizations are not culturally homogeneous and subcultures often exist (Howard-Grenville, 2006; Martin, 2002; Sackmann, 1992; Schein, 1996), such subcultural differences may increase the complexity of selecting the relevant logic(s). As each professional group brings in its own logic (Besharov & Smith, 2014), multiple logics can coexist within one organization and thus can vary across subunits (Binder, 2007). The meaning of institutional logics is not fixed (McPherson & Sauder, 2013) or, as Binder (2007) argued, “no one institutional logic is matter-of-fact for everyone in the organization; rather, several different logics are common-sensical for different organizational departments and their staffs” (p. 568).

Different subcultures can stress different interpretations of each of the available logics, for they provide different meaning systems (Geertz, 1973), as “actors perceive the meaning of institutions and infuse their actions with meaning based on these perceptions” (Dacin et al., 2002, p. 47). Consequently, subcultural differences can intersect with institutional logics (Voronov et al., 2013; Zilber, 2002) and highlight certain aspects of each of them differently. This can be problematic because multiple meaning systems can provide inconsistent expectations of the overall organizational goals, referring to these logics (Greenwood et al., 2011). The interplay between logics and subcultures thus is complex and has been noticed in the literature, though not often identified as such. With this study, we recognize this interplay and dissect it by identifying mechanisms of amplification and magnification, combining insights from both organizational culture and institutional theory. This is important because our findings might contribute to an explanation of why some sustainability initiatives succeed while others do not. We argue that an answer to this question lies not only in the complexity and differences between multiple logics and subcultures, but also in them reinforcing one another.

Method

In our research, we applied an inductive approach (Gioia, Corley, & Hamilton, 2013; Nag et al., 2007) with the purpose of elaborating existing theory by combining insights from theory on organizational culture and institutional logics. With this, we aim to develop a deeper understanding of the interplay between logics and subcultures during sustainability policy development. To answer our research question, we conducted a longitudinal empirical study of 43 months with a strong ethnographic character. The strength of an ethnographic approach is to provide detailed accounts of life in organizations; this approach is useful to capture the life-worlds of organizational actors and cultures (Ybema et al., 2009) and very suitable to answer “why” and “how” questions (Van Maanen, 2011). Such research involves lengthy fieldwork as this increases the odds that researchers uncover and identify activities, interpretations, and setting-specific cues (Barley, 1990; Van Maanen, 2011). Our research follows Aguinis and Glavas’s (2012) suggestion that to understand processes that unfold over time, sustainability research would benefit from qualitative research and data collection approaches that employ a longitudinal empirical study. In the next sections, we highlight the research setting, access, approach, data collection, and analysis.

Research Setting

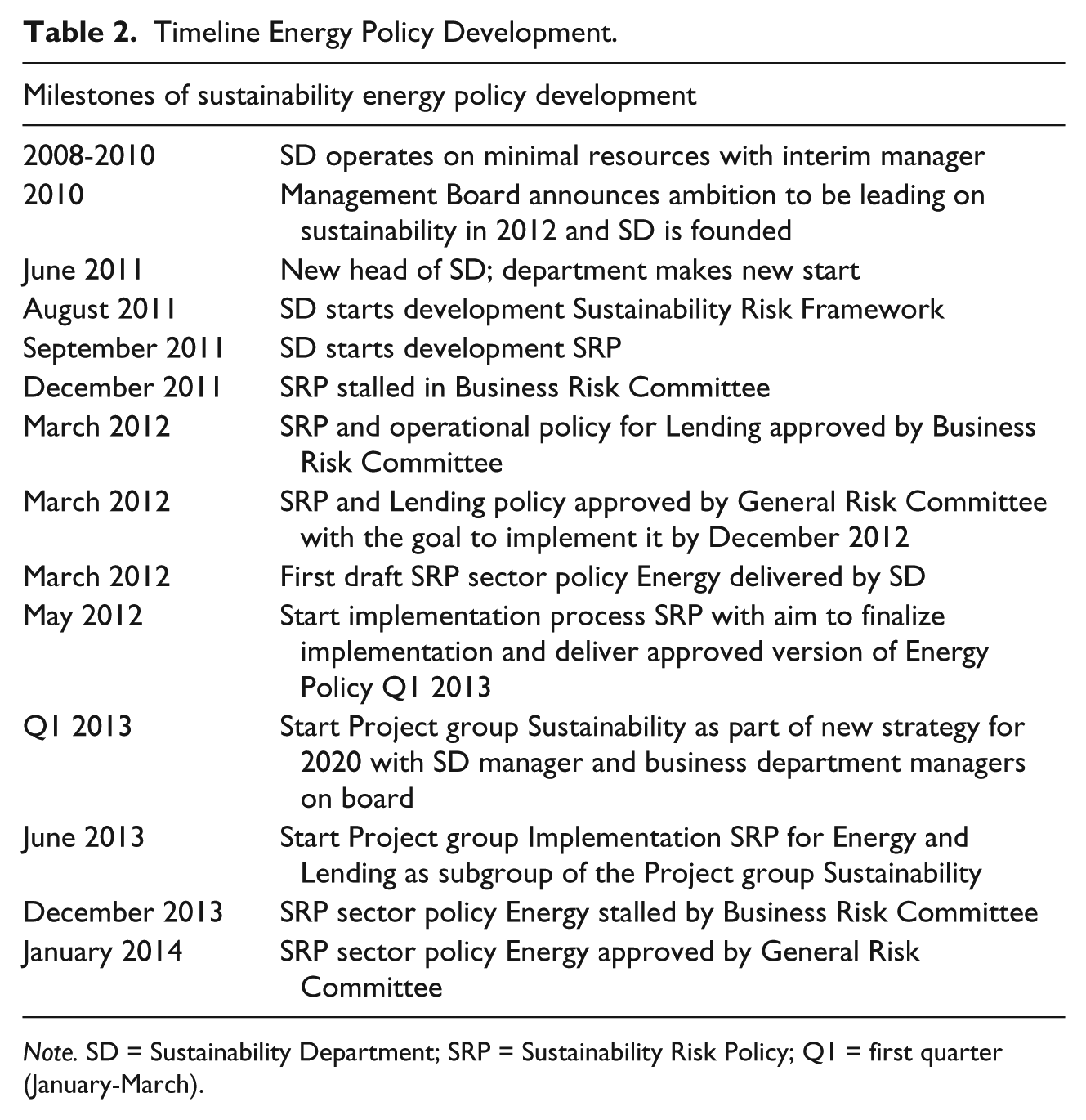

The setting for our study is DUTCH Bank, a large commercial bank in the Netherlands. Up until 2007, this bank was “a leading international bank” which received several awards for sustainable banking. In 2008, during the financial crisis, a major reorganization started and survival became the bank’s number one priority after having been bailed out by the Dutch government. Sustainability lost its prominence within the organization, until in 2010, the Board of Directors of the “new” DUTCH Bank announced that sustainability needed to be put back on the agenda. In June 2011, the sustainability department (SD) was reinstated with a new manager and mostly new employees. The Board of Directors gave the SD the task of developing a sustainability policy with the aim of having “a prominent position as a sustainable bank [ . . . ] in line with the mission to bring sustainable solutions to [DUTCH Bank’s] clients, to be achieved by fully incorporating sustainability into the bank’s daily business” as defined in DUTCH Bank’s Sustainability Risk Policy. This was particularly challenging because of earlier large-scale restructuring of the bank.

The SD started with the development of a “Sustainability Risk Framework.” Core to this framework was the development and implementation of a Sustainability Risk Policy. This Sustainability Risk Policy contained operational risk policies, and sector-specific policies (such as Energy, Defense, and Agriculture), cross-sector policies, and an exclusion list containing a range of practices the bank would not engage in with clients, transactions, or activities.

In this article, we examine how the SD and the involved business departments (BDs) collaborated in the development of the sector policy for Energy. The development of the Energy Policy evolved into a constant cycle of adjustments. Several times deadlines were postponed due to tensions between the departments involved and disagreements about the policy content and process. These delays negatively affected the collaboration between the SD and the BDs which in turn further deferred the policy development.

Access to the Field and Role of the Researcher

We conducted an in-depth study at DUTCH Bank from November 2011 until June 2015. Research access was acquired through previous ties with the organization as the first author used to work as an employee at DUTCH Bank from 2007-2008. This prior work-relationship helped to gain access, even though she was unfamiliar with the headquarters, as well as with the SD or any of the respondents. The SD functioned as the “home department” during the fieldwork period.

During the years of fieldwork, a close relationship between researcher and site was established which required frequent self-reflection and the taking into account of “personal biases, world-views, and assumptions [ . . . ] while collecting, interpreting, and analysing data” (Suddaby, 2006, p. 640). The risk of gradually adopting an informant’s view and losing the ability to take the helicopter-view necessary to theorize from the data (Gioia et al., 2013) is present in such circumstances. To encourage self-reflection, and to remain critical of the research findings, the second and third author often took on the role of the devil’s advocate (Gioia et al., 2013), constantly challenging and reflecting the first author’s interpretations and assumptions based on the data collected. Besides, the first author remained an observer rather than becoming a participant-observer, not having any active role within the organization, nor being paid by the bank to study them or to provide consultancy. These considerations together allowed for the assembly of a rich and detailed dataset.

Data Collection

As we highlight the development of the Energy Policy in this article, we selected a relevant subset of our data including observations, interviews, emails, and policy documents derived in the period of November 2011 up until January 2014, when the Energy Policy was approved. The entire dataset (November 2011-June 2015), including policy implementation, which is outside the scope of this article, offered additional contextual information.

During the period of November 2011-January 2014, the first author was present at the bank with an average of 2 to 3 days a week. She observed meetings between individuals from the SD and four different BDs. These meetings were between groups of individuals from both departmental groups and evolved around discussing feedback from the BDs on draft versions of the policy the SD provided, and discussions about the scope of the policy and of the sustainability standards to be included. In total, 32 formal meetings were attended during this period. Presentations on sustainability topics from the SD to regional BDs and also by several senior managers of different organizational units offered additional opportunities for observing, as did other events organized internally such as “Sustainability Day” and a “Human Rights Conference.” During all these events, the first author was “madly making notes on what the informants are telling [us], conscientiously trying to use their terms, [ . . . ] to help us understand their lived experience” (Gioia et al., 2013, p. 19). Such events also offered networking opportunities to find more respondents. In total, eight presentations and two events were attended.

All 12 employees of the SD were interviewed in-depth, at least once. Four of the 12 persons belonged to the Risk & Policy team and were directly involved in policy development: They were key respondents for this research and were interviewed many times throughout the process. In the period between November 2011 and January 2014, we conducted 35 interviews with SD employees. Other respondents came from the senior management level of the bank and the four different BDs directly involved with the Energy Policy. In total, 12 in-depth interviews were conducted with respondents outside the SD. We complemented these interviews with two interviews with other relevant actors such as the interim manager of the SD, who had managed this department before and during the merger. Interviews lasted from 30 min to 2 hr while observations amounted to about 452 hr, all the time taking extensive notes, during or shortly after an encounter.

Interviews in more formal settings were recorded. Examples of formal settings were planned interviews taking place in private rooms in which an atmosphere of privacy could be built, scheduled interviews during lunch, and also formal planned meetings between employees from the different departments. Interview themes were determined beforehand to provide some structure to the conversation and to keep the interviews on topic. Themes were based on the expertise, role, and function of the respondent and policy development issues relevant at the time of the interview.

In addition to the more formal interviews, we also conducted many informal, spontaneous interviews that usually had a conversational character and therefore were not recorded. Yet, keywords were written down and the conversation was transcribed afterward. Such interviews happened on multiple occasions throughout our fieldwork and took place across desks, during lunch, while having coffee or going for a walk outside the office.

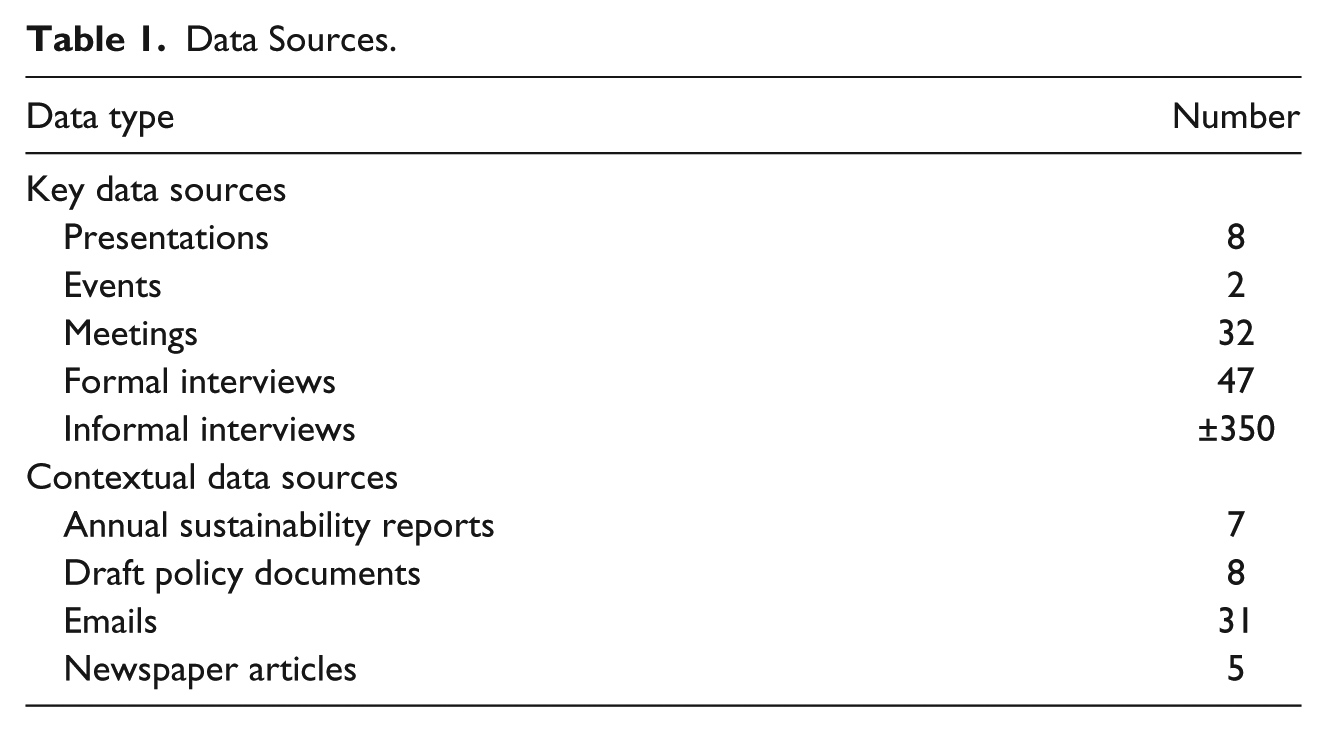

Our data further consisted of a wide variety of resources such as multiple versions of the policies, DUTCH Bank’s annual sustainability reports (2007, 2008, 2010, 2011, 2012, and 2013), emails between (groups of) individuals from the SD to the BDs and vice versa, internal newsletters such as the employee magazine, news articles from Dutch and international newspapers and the Internet, the bank’s intranet, chief executive officer (CEO) blog, and the bank’s “insider” group on Facebook in which only sustainability-related topics were being posted, shared, and discussed. Finally, the first author had access to all of the bank’s main buildings in Amsterdam and full access to the SD’s digital library and office documents as well as her own DUTCH Bank email address. An overview of data sources is provided in Table 1.

Data Sources.

Data Analysis

Months of ethnographic material, images, idioms, and stories are only a representation of realities in which a researcher tries to capture the experience and meaning making of those studied (Van Maanen, 2011). Interviews and field notes were transcribed for analysis. Emails were converted to Word documents and added to the interview and observation data. Newspaper articles, published interviews with spokespersons from within the bank (e.g., members of the Board of Directors), publications on the CEO’s blog, and financial as well as sustainability reports were used as contextual data.

All interviews, observations, emails, minutes from attended meetings, draft documents from the policy, and other policy-related documents were printed and mapped chronologically. As such, our data provided a readable document which gave us the whole “story” of the process we studied.

Data collection and analysis were done simultaneously (Corbin & Strauss, 1990). In analyzing data, we moved between induction and deduction, also known as “abduction,” “the process by which a researcher moves between induction and deduction while practicing the constant comparative method” (Suddaby, 2006, p. 639). Following a round of close reading, we started to code our data. First, the dataset was entered into MaxQDA, a software package for qualitative data analysis, suitable for (open) coding and analyzing large amounts of text.

The first-order coding relied on open coding (Corbin & Strauss, 1990). Here we found data excerpts with many references to how employees approached the policy development process, referred to the financial crisis, or interpreted sustainability. We identified expressions of tension and conflict. When analyzing and ordering these data excerpts, we signaled characteristics of organization culture and institutional logics. We coded excerpts as “organizational culture” when respondents referred to what values motivated them, and to ideas, beliefs, and ideals: the “soft” side of organizational life. We coded an excerpt as “institutional logics” when they talked about their key performance indicators (KPIs), rules and structures, performance criteria, roles, protocols, and department goals as motivating their actions: the “hard” side of organizational life. We then went back to the literature to try and understand these emerging codes and ensure that we attributed them correctly to our data (Huy, Corley, & Kraatz, 2014).

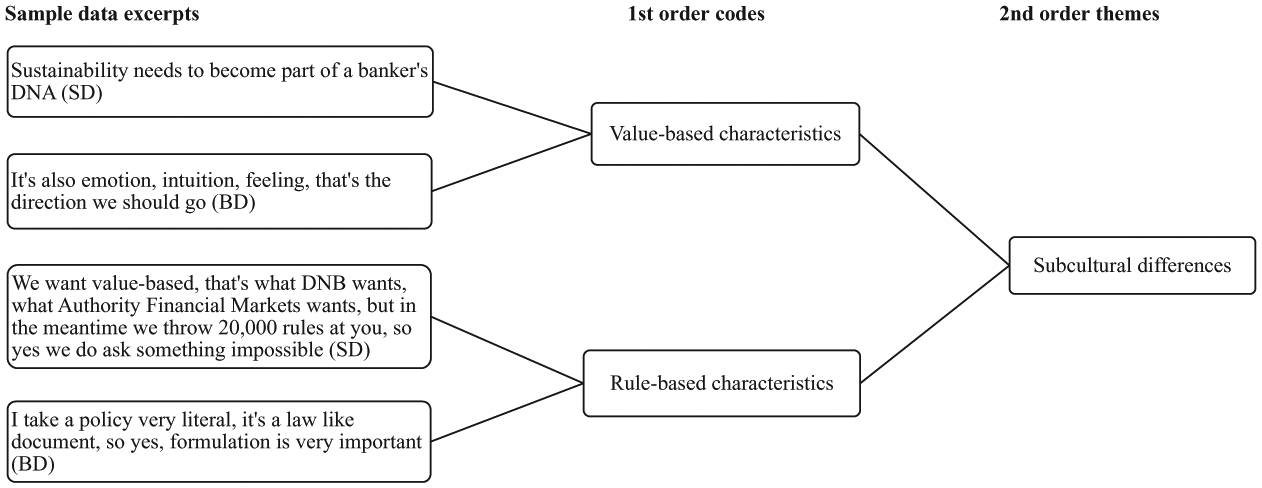

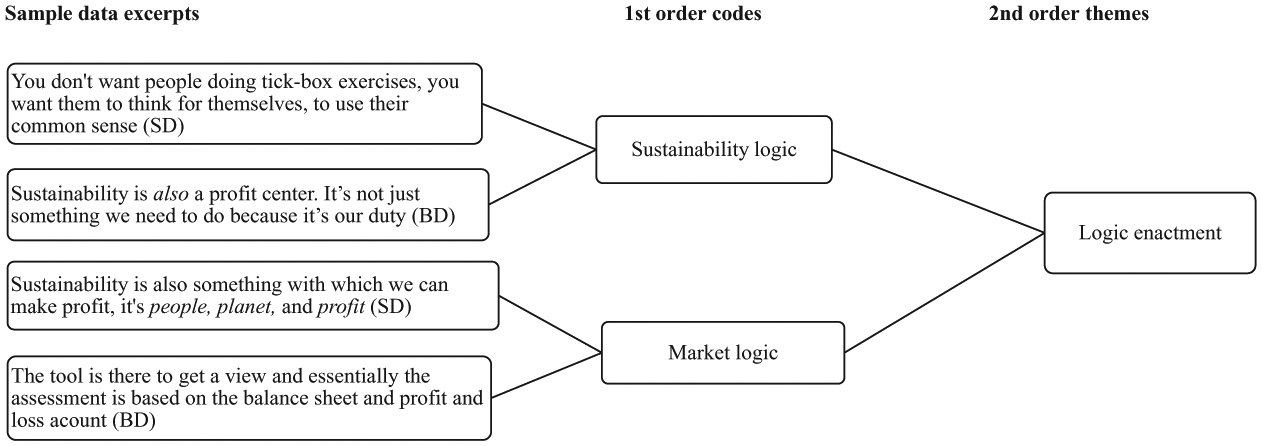

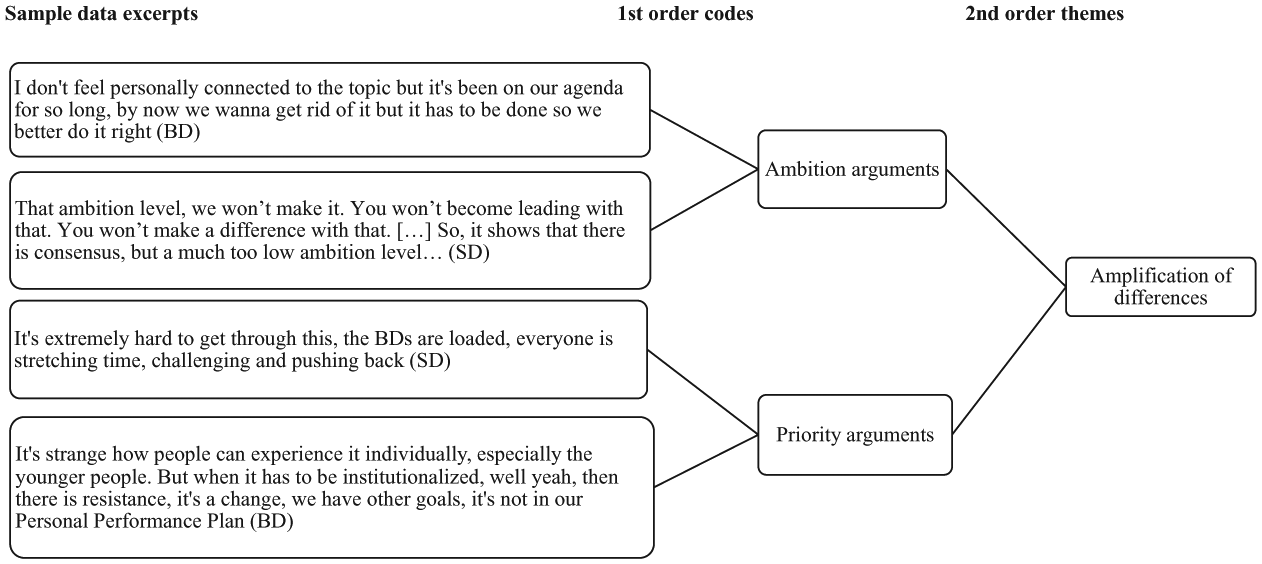

As a next step, we grouped our codes into second-order concepts, following the “Gioia method” (Gioia et al., 2013) to connect our data to theory. Here, we identified the possible role of subcultures and the presence of multiple logics. When looking at our first-order concepts, we saw a division between our different “culture” codes, which we could ascribe to different subcultures. Our “logics” codes could be grouped into two different categories: either market or sustainability logics. In doing so, we relied on prior research, both for culture (Giorgi et al., 2015) and for market and sustainability logics (Bansal & Roth, 2000; De Clercq & Voronov, 2011; Friedland & Alford, 1991; Glynn & Raffaelli, 2013; Thornton et al., 2012). The resulting data structures are presented in Figures 1 to 3.

Subcultural differences.

Logic enactment.

Amplification of differences.

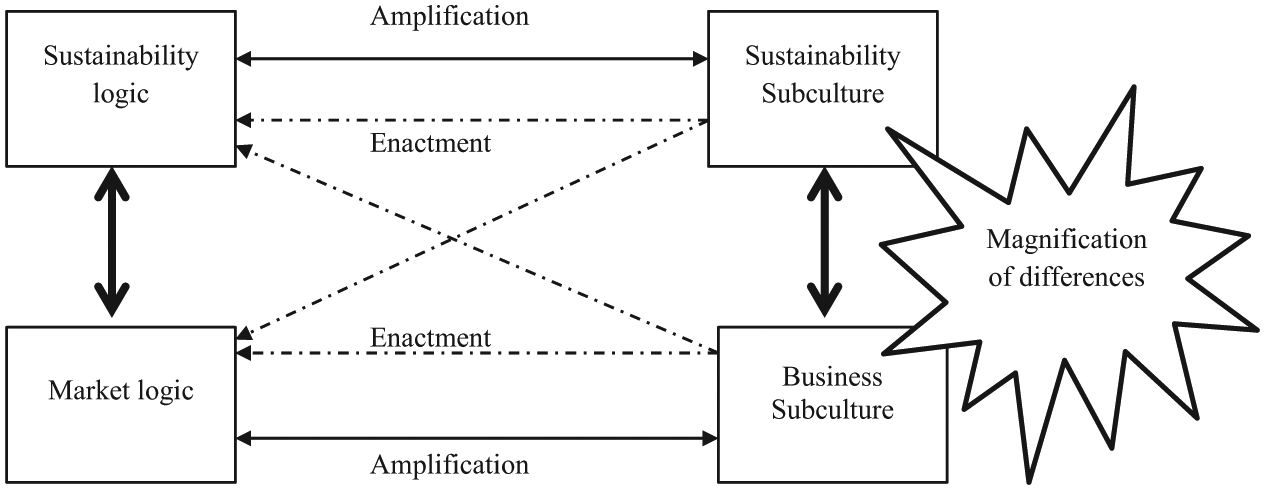

The constructs presented in Figures 1 to 3 do not sufficiently explain the complexity of the process we studied and the tension and conflict we observed therein, nor how this complexity and tension could be caused only by either the identified subcultural differences or different logics. We closely reexamined our data and discussed among the authors why what we saw and heard in practice went beyond what the literature told us about the problems that exist when either subcultures or logics differ and collide. This led us to wonder whether there was an interplay between subcultures and logics that reinforced one another. Hours of observing the many meetings had shown how employees from the SD and the BDs seemed to live in different worlds and did not seem to have a shared understanding of what they were talking about. This situation seemed to get worse over time. When reflecting upon this to our respondents during one of our several reflection sessions, it appeared that the mutual differences reinforced one another and that these became amplified as we will present in our results section (see Figure 4).

Interplay between logics and subcultures.

To strengthen reliability and to ensure the trustworthiness of our analyses, we took several measures. Key interviews and observations were read several times by at least two of the three authors. Research findings and the first author’s interpretations of “what was going on” were often reflected upon with respondents to test the accuracy of our understanding. This was either in the form of presentations or informal coffee or lunch get-togethers. As such, respondents could confirm the impressions or add some nuances. We also triangulated the multiple data sources; comparing and contrasting data across different sources to validate that a particular practice could be ascertained either through multiple forms of evidence (e.g., interviews and observations), or through multiple instances of the same form of evidence (e.g., multiple interviews; Voronov et al., 2013).

In the next section, for reasons of confidentiality, all respondents are portrayed anonymously and labeled and numbered as business department employee (BDx) or sustainability department employee (SDx).

Sustainability Struggles: The Interplay Between Logics and Subcultures

This is impossible, this is crazy! I mean, it is not, you know, like I am going to make war on that, that is absolutely not the case, but there is a misunderstanding between where we want to be and what is now the case. So taking the best practice that is in our own tools, this is not invented, to say well this is our standards and if you want to be a client of [DUTCH Bank] you need to meet these standards, then uhm . . . that obviously contravenes the whole growth strategy of [our BD], for the bank it has been decided on the higher level, that [our BD] needs to grow, well . . . we wouldn’t grow with these standards . . . I mean, we feel responsibility to implement the policy and we are very serious about it. [ . . . ] So in fact the policy should look at what we have, what is the business, otherwise you are talking about ideas, and we can all have ideas but it still needs to fit the portfolio. And of course everybody wants to improve things [ . . . ] in the process, but I don’t think it needs to complicate the process of the policy, it should ease the process of the policy, depending on the approach of the policy. (BD1)

This quote illustrates a major conflict between the SD and the BDs about sustainability performance standards that the SD had included in a draft version of the Energy Policy. During this conflict, differences between the SD and the BDs in both their subcultures and enactment of logics became magnified. In this section, we elaborate on how the interplay between subcultures and logics during the policy development process resulted in a magnification of differences, causing this particular BD respondent to make such a statement.

Subcultural Differences

In September 2011, the SD started with several rounds of consultation in which the SD consulted all BDs involved with the Energy Policy and requested their comments on a draft version of the policy (for a timeline, see Table 2).

Timeline Energy Policy Development.

Note. SD = Sustainability Department; SRP = Sustainability Risk Policy; Q1 = first quarter (January-March).

During the meetings in which the draft versions were discussed, we noticed how employees from the SD and the BDs seemed to approach the policy differently. These differences showed characteristics of organizational subcultures because they referred to how employees valued sustainability and the perceptions they had of how to read the policy.

One of the main subcultural differences we found was between a value-based and a rule-based culture. The bank’s Board of Directors had assigned the SD to develop sustainability risk policies with the goal of fully incorporating sustainability into the bank’s daily business. The SD interpreted this assignment, as repeatedly indicated by various SD employees, as

Bankers need to develop a sustainability gene in their bankers DNA.

Such a statement reflects how the SD wanted to infuse the entire business organization and its members with sustainability values. During meetings with BDs, the SD employees often expressed their concerns that working according to the new Energy Policy should not be viewed as a “tick-box exercise.”

The second subcultural characteristic we identified referred to how to read the policy and reflected the rule-based culture of the BDs. The BDs were used to taking policies very literally: For them, a policy was a law-like document. One BD employee gave feedback on a draft version, stating that

the policy is written very theoretically and stands far from current practice. (BD2)

For the BDs, this distance between policy and practice was problematic because it felt like the Energy Policy was not applicable as they were guided by a rule-based culture: “For me policy is like law, it should not allow room for interpretation” (BD1). The policy should prescribe how practice should be. The SD members, however, had a “softer” interpretation of the Energy Policy:

This is also soft-law, unwritten rules, and expectations of society. You should be able to be held accountable in the court of public opinion. [. . .] You want a level playing field, that also your competition has these standards. (SD1)

The purpose of the Energy Policy was, according to the SD, to provide the BDs with guidance on how to deal with sustainability risks when taking on new clients. With the sustainability performance standards included in the Energy Policy, the SD intended to leave room for interpretations to enable a tailor-made application:

A policy does not contain working instructions, there are tools for that which the business may come up with themselves. (SD2)

Yet, the application of the policy as such was not understood by the BDs. They kept expressing their concerns about how the policy would restrict them in taking on new clients and thus in their opportunities for doing business.

Figure 1 illustrates how we derived components of subcultural differences from our primary data and shows more examples thereof. How these subcultural values and beliefs of the SD and the BDs informed the interpretation and enactment of the sustainability and market logics is addressed in the next section.

Enactment of Logics

From our observations in meetings and interviews, but also through informal small talks, for example, while waiting for the elevator on the way to a meeting, we found that two logics were relevant for the SD and the BDs in the process of developing sustainability policies.

Sustainability logic

Within the SD, the sustainability logic was primarily represented, demonstrating a wider societal focus. When talking about the sustainability risk policies, an SD employee, for example, translated sustainability as follows:

We will be nailed in the public domain if we don’t have policies. (SD3)

To them, this logic reflected what society expected from the bank, for instance illustrated by what nongovernmental organizations (NGOs) wanted. The sustainability logic involved a wider look at the bank’s environment; it encompassed a different set of stakeholders compared with the market logic. When the BDs were talking about sustainability, it referred to what their respective industries, their markets asked of them:

Ideals of NGOs are unrealistic, sustainability has to be from the business, bottom up. (BD1) Our sustainability agenda is not driven by the agenda of the NGO. It is driven by the business, by the industries, by the fact that companies that are not sustainable, we are running risks we are not willing to define, it’s for that matter, so this is also a different angle, a different driver . . . (BD3)

BD employees thus interpreted sustainability more limited, in terms of a business case and risk management:

Everybody knows, out there, if you have enough contacts with a lot of companies, then you will see that all of them are considering sustainability, and they need to. Because otherwise they are getting big problems. It’s a business case. (BD3)

These quotes illustrate how values from their subcultures informed the SD and the BDs to develop different interpretations of the sustainability logic; this made it more complicated for them to develop a shared approach of the policy process.

Market logic

Even though all respondents claimed to believe sustainability was very important for their organization, they did not forget that the core logic of being a bank is about making money. However, the SD did not define those as financial goals based on deals or transactions but promoted sustainability efforts by DUTCH Bank whenever they could by trying to frame the market logic differently. When talking about making profit, they included people and planet as well:

With that we also show that sustainability is not only for “goat-woollen socks” [a Dutch expression similar to “tree huggers”] but also something with which we can make money. And there is nothing wrong with that, because it is people, planet and profit. (SD3)

BD employees, in contrast, saw the policy as being required to address sustainability aspects while talking to clients about business but were not reinterpreting the market logic in response to the inclusive definitions used by the SD. For the BDs, conversations with clients should concentrate on the client’s business:

I’m there to talk about his financials, not where he manufactures the soles of the shoes he’s selling. (BD5)

BD employees nevertheless were able to reinterpret sustainability within in a market logic, invoking growth as the major driver:

. . . frustrating or restrictive, yeah then there might be some truth in it. So yes. And sometimes the difference between some ideology and what is commercially achievable. Because eventually we have to make money and so far the bank’s policy has not been as if we want to be a [sustainable bank]. (BD4)

Typical in the quotes is that they reflect a difference in logic interpretation between the SD and the BDs, at least through the eyes of this BD employee when pointing at an apparent difference between ideology and commerce. It was very clear from the situational context in which this conversation took place, that “ideology” was attributed to the SD. Therefore, this quote is illustrative for how differences between subcultures become amplified due to differences in logic interpretation, a mechanism we elaborate upon below.

As the quotes in this section illustrated, the Energy Policy development process laid bare some clear differences between the SD and the BDs, not only between their subcultures but also between how they enacted the two respective logics. The complexity at DUTCH bank seemed to be that both logics were relevant to them but that in order for the organization to function well, they needed to find a common interpretation of the market (and, vice versa, the sustainability) logic. Which logic was dominant differed for each of the type of departments involved.

For the SD, the kind of behavior prescribed by the sustainability logic was closer to their specific subcultural values; likewise, for the BDs, the market logic was closer to their specific subcultural values. This affected how they enacted their favorable logic: the values, belief, and meaning systems of each subculture accordingly infused logics, leading to different interpretations of those logics and differences in logic enactment. During the policy development process, the SD and the BDs clashed to have their interpretations of both logics represented within the policy. In moments of interaction, these differences caused misunderstandings, leading to further tension and conflict amplifying the differences. Figure 2 illustrates how we derived characteristics of logic enactment from our data excerpts.

Amplification of Differences

The growing differences in how the SD and the BDs approached sustainability resulted in a division between “idealists” versus “pragmatists.” These labels were often applied during interviews and we argue that they reflect how differences between subcultures reinforced the already existing differences in logic interpretation and frustrated the possibilities for joint enactment of logics. The SD representatives, for instance, were seen as “tree huggers” by BD employees while the BD employees were characterized by SD people as “money making soldiers.” Employees of both the SD and the BDs used different arguments when trying to convince each other of their points of view. These arguments were based on ambition and priority. When analyzing these arguments, we noted that the SD and the BDs created a constant emphasizing of differences in logic interpretation, amplifying the differences between them. Labeling one another here was one visible characteristic of amplification.

Ambition

The ambition level of sustainability standards incorporated within the Energy Policy was often a topic of discussion and reflected the subcultural differences between the SD and the BDs. BD employees saw the Energy Policy, and in particular its sustainability performance standards, as too ambitious and too restrictive on their business opportunities. Meanwhile, SD employees continued talking about their BD colleagues as being only business-focused and not thinking about the outside world, relating to their logic interpretation:

In reality this is quite complicated because it is not the interest of the business; it is not their cup of tea. The business is not proactive; they have to choose between making money and implementing the policy . . . They see the [sustainability] policy and sustainability as “saying no” [to business opportunities], but that’s not the case, it is about the position we, as a bank, have to take. (SD4)

This SD quote illustrates how the SD perceived the BDs. In the eyes of this SD respondent, and based on similar expressions from SD colleagues, we often heard claims that sustainability “is not the interest of the business.” In the SD employees’ view, BD employees had no knowledge on the topic (“it is not their cup of tea”) and making money is what their day-to-day practices are all about. “Saying no to business opportunities” is how the BDs interpreted the sustainability logic, according to the SD.

Priority

The second topic we identified as being a regular point of contestation was priority. The Board of Directors had given the SD the assignment of fully incorporating sustainability in the bank’s daily business. The SD adhered to the sustainability logic as their dominant logic and saw the development of the Energy Policy as their number one priority. Or, as this SD respondent said,

Finishing this policy, it is included in my personal achievement appointments for this year. (SD2)

For BD, this clearly was not the case:

But at the top they don’t prioritize so we at the shopfloor are fighting over it. [ . . . ] “We need to make money” remains dominant so they [SD] enter meeting with a certain attitude and resistance because of this filter. In the new strategy there are 10 sub-strategies. Sustainability is number 10. But the others also affect the business. Everything coming at us from headquarters’ towards business managers is on top of their business as usual. The bank’s Board of Directors says “sustainability is important” but the other 9 are there as well. Sustainability is number 10, what does that say about hierarchy? (BD5)

As shown in the quote we started this results section with, a “growth strategy” that “has been decided on the higher level” was the message the BDs received from the Board of Directors. For the BDs, the sustainability logic was relevant but the market logic was more dominant. For the SD, it was the other way around, the market logic was relevant but the sustainability logic was more dominant. Figure 3 illustrates how we identified the mechanisms of amplification from our data excerpts.

Magnification of Differences

The long quote we started this result section with comes from a meeting about the sustainability performance standards the SD formulated within the Energy Policy. This meeting was held after BD employees commented on a draft version of the Energy policy, prepared by the SD based on input the BDs had delivered during previous meetings. Apparently, the SD had translated the BDs’ input not in the way the BDs had intended. This BD respondent wrote the following comment in the draft policy:

These documents lack consistency, lack quality, are disconnected from reality and show abundance of ignorance regarding the topics they address. [. . . ] Overall, it seems like the author(s) of the draft already had a clear opinion on the industry, and wrote the policy from that perspective instead of first testing their own assumptions. [. . . ] The author(s) seem(s) to lack a basic understanding of the industry. (BD6)

More similar feedback was given by BD employees. Remarkable in these comments was that according to the business employees, SD employees had a predetermined opinion about BD business practices. Because the Energy Policy concerns sensitive industry practices such as mining, oil, and gas, the BDs felt like the SD perceived them as “dirty” anyway. This expression clearly shows how far the distance between the SD and the BDs had grown. They only seemed capable of seeing how different they were from one another, and what different interpretations they had of what the Energy Policy should become. Another BD respondent expressed concern for business opportunities and demonstrated strong adherence to the market logic:

These standards, they are just not realistic. If the SD claims that they are derived from the “best practices” in the industry . . . None of our top 5% clients can abide by those standards, they are just not realistic. If we apply this policy, we can stop doing business. (BD1)

Applying this policy, according to them as a law-like document, would be a huge restriction on their business growth and they claimed the policy to be not realistic, disconnected from reality, the market. With this, they emphasized the SD’s attitude as being idealists, far from reality and having their own assumptions. These comments show magnification of the subcultural differences between the SD and the BDs, indicating how the SD had their own reality and ideals, and no knowledge of business practices whatsoever. Also, as BD employees were concerned about reaching their financial goals, they kept emphasizing how they were obliged to apply the standards from the policy as rules. Both the SD and the BDs relied on their respective logics more firmly while falling back onto their own subcultural values and beliefs. They had become so polarized that interaction became unpleasant for all involved and logics seemed incompatible. Consequently, they were unable to find common ground, leading to an impasse.

In January 2014, a year later than initially planned, the Energy Policy was finally approved by a Risk Committee consisting of senior business managers. Two issues contributed to the eventual approving of the Energy Policy. First, the annual Employee Engagement Survey showed a significant lack of knowledge among employees about the bank’s sustainability activities and second, the Fair Bank Guide (an NGO initiative) scored DUTCH Bank lowest among its peers. Senior management determined that the Energy Policy needed to be approved so employees internally would become more knowledgeable and DUTCH Bank would receive a higher score in the Fair Bank Guide ranking. However, the feeling among SD employees was that the overall policy development had unnecessarily taken up considerably more time than needed. Also, the SD representatives called the approved Energy Policy a “consensus document.” Meanwhile, a member of the Board of Directors afterward encouraged the head of the SD “to [from now on] choose their own path and not kill the policy by over-negotiation.” As an SD respondent noted,

Group interests prevail above the overall interests [of the bank]. So yes, when [the BD] thinks “yes, hold on, this constrains my commercial opportunities” then they’re against it. And then you will have a watered down story that is eventually approved at a higher level. (SD3)

Discussion

You know, we were idealists back in 2009, but if you look at it now, what we were able to realize . . . Well, that’s how difficult it is. (BD6)

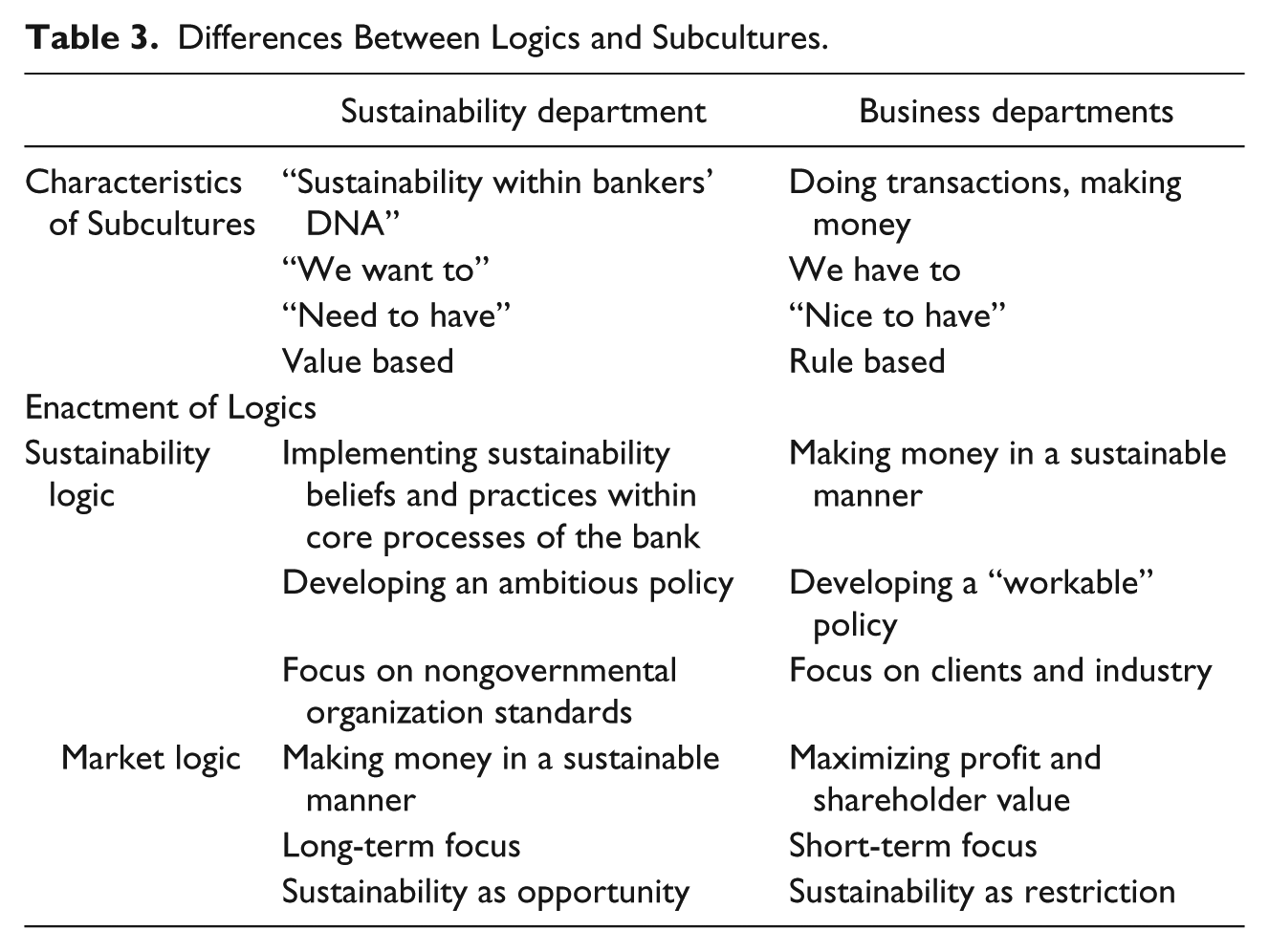

In this article, we sought to answer the question how the interplay between subcultures and institutional logics affects the development of sustainability policies within an organization. Some scholars argue that, in an ideal situation, business cultures should be supportive of sustainability (Maon et al., 2010) and that institutional logics should promote sustainability practices (Haberberg et al., 2010). Yet, organizations are rarely (if ever) culturally homogeneous (Martin, 2002; Sackmann, 1992; Schein, 1992), consisting of different subcultures while a variety of logics may guide organizational actions (Besharov & Smith, 2014; Reay & Hinings, 2009). Not surprisingly, in studying sustainability policy development within DUTCH Bank, we encountered both the presence of different subcultures and different logics, see Table 3 for an illustration of subculture and logic differences.

Differences Between Logics and Subcultures.

Earlier research suggested that differences in subcultures can have a significant impact on employee awareness of sustainability practices and on “how employees understand corporate sustainability differently” (Linnenluecke et al., 2009, p. 447). Yet, subcultures only explain in part why different employees develop different understandings of sustainability (Linnenluecke et al., 2009) while the role of institutional logics in this process has mostly been neglected.

In our case, two logics were relevant: a market logic and a sustainability logic. As we have observed, employees interpret logics they encounter within their own subcultures and in doing so, they emphasize different aspects of those logics (Voronov et al., 2013; Zilber, 2002). How they respond to multiple logics depends on how they interpret these different logics. These interpretations can be reflections of which logic they deem dominant (Greenwood et al., 2011).

When multiple logics exist, it is the dominant logic that ultimately guides behavior (Thornton, 2004). Yet, in our case, we identified a difference in logic dominance between the different subcultures. This makes sense because individuals are likely to prioritize logics “favourable to their material interests or normative beliefs” (Greenwood, et al., 2011, p. 318). Within the business subculture, the market logic was closer to their interests and beliefs and thus dominant, while within the sustainability subculture, the sustainability logic was favorable and thus dominant, leading to two dominant logics. Both logics can provide guidance to how sustainability is to be implemented within an organization but with considerable differences in terms of practice emphasis (Glynn & Raffaelli, 2013). This could be observed in differences in enactment of these logics between the SD and the BDs. During moments of interaction, differences in subcultures and logic enactment were constantly emphasized which amplified how they differed from one another even more as shown in Figure 4.

This amplification became visible through labeling and arguments based on differences in ambition and priority and showed how the SD and the BDs struggled with developing a sustainability policy. As shown in Figure 4, this struggle led to a magnification of the differences between both subcultures and logics, making the two logics seem incompatible, thereby resulting in an impasse. This was problematic because a market logic and a sustainability logic are not necessarily incompatible as such. Success stories about organizations that succeed in implementing sustainability initiatives can be found in the literature (cf. Jamali, 2010; Lee, 2011) while the wider literature on hybrid organizations also discusses how organizations try to make multiple logics compatible (Battilana & Dorado, 2010; Pache & Santos, 2013). Rather than focusing on different logics as such, our study underlines the need for more emphasis on the interplay between subcultures and logics that both contain elements that drive them further apart rather than reconciling them. In our case, this was illustrated by the repeated discussions that slowed down the process of policy development and ultimately resulted in the version of the Energy Policy being approved only as a watered down “consensus” document.

Although set in a specific context, our study thus confirms earlier findings in the literature that multiple logics can coexist within organizations (Besharov & Smith, 2014; Binder, 2007; Reay & Hinings, 2009), but it extends these findings by suggesting that such a multiplicity of dominant logics may well coexist due to the presence of subcultures. Besharov and Smith (2014) approached logic multiplicity at the organizational level, assuming organizational homogeneity and stating that when there is a dominant logic there will be no conflict. Yet, we argue that when different logics are dominant within different subcultures, there is a multiplicity of dominant logics that provide contradictory prescriptions for organizational actions, implicating extensive conflict. This points out that the effect subcultures can have on the multiplicity of logics deserves more attention from institutional scholars and could serve to extend the work of Besharov and Smith and other recent developments in institutional theory.

Conclusion

To answer our research question, we conducted a long-term inductive study, examining the interplay between subcultures and institutional logics within sustainability policy development. To analyze our findings, we used insights from both institutional theory and organizational culture.

With this research, we have made three contributions. First, we already knew that the meaning of institutional logics is not fixed; individual actors interpret logics differently and translate them into action (Voronov et al., 2013; Zilber, 2002). Yet, we lacked empirical research on how they do so (McPherson & Sauder, 2013). In this study, we found that individuals interpret logics informed by their subcultural values, beliefs, and assumptions. These subcultural differences caused for differences in logic interpretations, translations, and enactment leading to different understandings of the policy development process we studied.

Second, we argue that acknowledging that individuals interpret and enact logics from their subculture can provide insight into how organizations internally deal with institutional pluralism (Battilana & Dorado, 2010; Besharov & Smith, 2014) and also offer a possible explanation for heterogeneity in organizational responses to institutional logics (Greenwood et al., 2010).

Third, we found that subcultures can also determine how actors can be selective in adhering to a particular logic (Voronov et al., 2013). Actors prioritize logics based on the interest they have in that logic as a group (Greenwood et al., 2011). Subcultures can be examples of such groups, making employees of a certain subculture be representatives of their primary logic. As in each of the two subcultures we studied individuals adhered to a different primary logic and had different interpretations of the two logics, this interplay led to extensive conflict.

With our findings, we respond to recent calls by scholars in organizational culture and institutional theory to combine both streams of organizational research to deepen our insight in the processes involved (Aten et al., 2012; Hatch & Zilber, 2011; Hinings, 2011; Zilber, 2011) and offer new insights to both organizational culture and institutional theory (Caprar & Neville, 2012; Giorgi et al., 2015; Howard-Grenville, 2006). In addition, according to Athanasopoulou and Selsky (2015), research about sustainability could benefit from the use of multiple perspectives. Combining institutional theory and organizational culture is an example of how multiple perspectives lead to new insights for the development of sustainability policies inside organizations.

Furthermore, we note that our detailed analysis of policy development as a separate stage of implementation provides an answer to recent calls for more attention to the adoption of sustainability practices (Linnenluecke & Griffiths, 2010; Wickert & de Bakker, 2016). Policy development is a stage within the overall implementation process of sustainability policies that has largely been neglected (Maon et al., 2010) while it offers an opportunity to look beyond the facade of window dressing. Focusing on policy development laid bare subcultural differences between departmental groups and how these groups enacted the logics guiding them. It provided us with insights into an interplay we had not expected and might also play an important role during the next stage of policy implementation.

Managerial implications of this study would be that managers should be more aware of the differences between subcultures and the effects these may have on for their organization’s relevant logics and vice versa (Wickert & de Bakker, 2016). Sustainability policy development in large organizations might benefit from a project structure, managed by someone who is able to translate or bridge between the different approaches and interpretations employees from different subcultures bring to the table. Also, when high tension and conflict occur, it would be necessary to identify what lies at the origin of it. A watered down consensus document may not be a desirable outcome.

It would also be relevant for managers to prevent amplification and magnification to occur. Further research could investigate what the consequences of these mechanisms are for policy implementation, and whether they might lead to practice variation. Even though practices have not been the focus of this study, for managers and policy makers, it would be useful to know how new practices should be interpreted as “organizations seek to integrate these practices into existing technologies, cultural contexts, and political arenas” (Ansari, Fiss, & Zajac, 2010, p. 85). Practices may vary and diffuse when translated to local contexts (Ansari et al., 2010), such as subcultures, but are also interpreted within these subcultures, as we show, contributing to a possible diffusion of practices. Amplification and magnification could also trigger practices to be varied when diffused. Watered down consensus practices, following a watered down consensus policy, could be the outcome.

This study also has a few limitations. First, we conducted our research at a time when many different pressures were exerted on the bank because of the financial crisis in general and a recent merger and restructuring in particular. This was a very turbulent period, potentially highlighting mechanisms and choices that raised tensions that might be unique to this specific case, even though some other studies suggest similar processes in other settings (Olsen & Boxenbaum, 2009).

Second, we highlighted the role of subcultural differences and institutional logics in sustainability policy development but we acknowledge that these processes do not occur in isolation. Our observations and interviews showed other processes that require attention if the focus is extended beyond subcultures and logics. Project meetings were regularly overflowing with frustration and emotion. Emotions play a role in disrupting, creating, and maintaining institutions (Voronov & Vince, 2012). What role do emotions play in the relation between sustainability initiatives and outcomes? And could we speak of specific sustainability-related emotions (Aguinis & Glavas, 2012)? These questions suggest that personal motivation, in addition to a professional involvement, also plays a role during processes of developing sustainability policies. More attention to the role of individual emotions during such processes therefore is relevant.

Several other angles for further research can also be distinguished. First, the alteration of organizational responses to logic complexity and how they vary across time “is a neglected but important theme that deserves serious attention” (Greenwood et al., 2011, p. 351). Even though our findings provide an explanation for how organizations internally deal with the multiplicity of logics, future research “should delve deeper into the dynamic patterns of complexity that confront organizations, arising from the multiplicity of logics to which organizations must respond, and the degree of incompatibility between those logics” (Greenwood et al., 2011, p. 334). This is important because when we can predict logic complexity, organizations can learn how to recognize and manage this complexity, and how to mitigate challenges (Greenwood et al., 2011).

Second, in our case study, it became evident that in motivating why DUTCH Bank should become more socially responsible and sustainable, external pressures based on societal expectations and NGO pressure played a significant role. External pressure to become more socially responsible could lead to external legitimacy (Drori & Honig, 2013; Scherer, Palazzo, & Seidl, 2013). However, the variety of internal responses to external legitimacy processes has received only limited attention in research, even though they are critical for the adoption of new ideas (Drori & Honig, 2013). The translation of external pressures into internal legitimacy processes is a relevant research topic, including the role of subcultural differences and conflicting logics. This would extend the research presented in this article by including the notion of legitimacy as a motivational factor for sustainability implementation.

Overall, we have tried to take a first step in teasing two uncomfortably similar and related constructs apart by theoretically and empirically identifying an interplay between subcultures and logics. We have shown that this interplay amplified mutual differences, and that continued interaction caused individuals from different subcultures to struggle for and over sustainability. This struggle further magnified differences between subcultures and in logic enactment, making the two relevant logics seem incompatible. This in turn affected sustainability policy development in such a way that it slowed down the process, and led to a watered down, consensus document. We hope that with this article, we triggered institutional and organization culture scholars to further combine both streams of theory and examine the interplay between logics and culture within and beyond the area of sustainability research.

Footnotes

Acknowledgements

The authors thank Dennis Schoeneborn, Janni Thusgaard-Pedersen, and three anonymous reviewers for reviewing earlier versions of this article. We also benefited from discussions and feedback by participants of European Group for Organizational Studies (EGOS) 2012, the “Amsterdam Seminar on Sustainability, Society & Business” (ASSSB), and a Paper Development Workshop in 2012 at the Organization and Management Theory Division of the Academy of Management annual conference. The authors give a special word of thanks to the handling editor, Andy Crane, for his stimulating guidance throughout this lengthy process.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.