Abstract

Introduction

The negative association between socio-economic position and depression is firmly established (Fryers et al., 2003; Kessler et al., 2008; Levinson et al., 2010; Lorant et al., 2003) and financial hardship appears to be an aspect of socio-economic position particularly salient for depression (Butterworth et al., 2009; Lewis et al., 1998; Mirowsky and Ross, 2001; Rodgers, 1991; Skapinakis et al., 2006; Weich and Lewis, 1998a; Whelan, 1994). Measures of hardship assess whether an individual or household has gone without necessities (e.g. meals) or experienced subminimal standards of living due to inadequate financial resources (Whelan, 1993; Whelan et al., 2001). As such, financial hardship reflects the consequences of insufficient resources without having to define an ‘adequate’ income. It has been suggested that hardship may mediate the relationship between other measures of socio-economic position and depression (Kessler et al., 1987; Rodgers, 1991; Thomas et al., 2007). Jenkins and colleagues (2008) examined the related concept of debt (whether people were seriously behind in payments such as their mortgage, rent or utilities) and found that the association between mental disorders and debt was stronger than that between income and mental disorders, and that the association between income and mental disorders was reduced after adjustment for debt. There is consistent evidence of a strong contemporaneous relationship between financial hardship and depression (Butterworth et al., 2009; Lahelma et al., 2006; Lorant et al., 2007; Mirowsky and Ross, 2001; Weich and Lewis, 1998a). The experience of financial hardship may play an important role in the aetiology and development of depression or may maintain existing symptoms (e.g. by limiting activities to aid recovery) and have a reinforcing effect on depression (Butterworth et al., 2009; Lorant et al., 2003; Mirowsky and Ross, 2001; Weich and Lewis, 1998b). Alternatively, mental disorders may cause significant impairment and may impact on educational attainment, labour-force participation, unemployment and earnings, and therefore could be conceptualised as a cause of hardship (Kessler et al., 1995, 2008; Levinson et al., 2010).

Existing epidemiological research that examines financial hardship is significantly limited by a reliance on dimensional scales of depression, with few studies using clinical or diagnostic measures. This may obscure the strength of the association between financial hardship and depression if hardship is particularly prevalent or pervasive amongst people with severe symptoms. In one of the few relevant previous studies using diagnostic measures, Skapinakis and colleagues (2006) found that hardship (‘financial difficulties’ in their terminology) was associated with both increased risk of onset and maintenance of major depression measured using the revised Clinical Interview Schedule (CIS-R; based upon a structured diagnostic interview) but that hardship was not associated with a measure of non-specific psychological distress based on the General Health Questionnaire (GHQ). Jenkins et al. (2008) also used the CIS-R in their examination of the association between debt and mental disorders. In a recent US study, Heflin and Iceland (2009) assessed depression using the Composite International Diagnostic Interview (CIDI), another structured interview, and found that material hardship mediated much of the association between poverty and depression in a sample of mothers with young children. There is a lack of studies of hardship using standardised clinical assessments of depression and based on representative general population surveys from outside of the UK.

A further limitation to previous research on this topic is the lack of investigation into the role that sex and age may play in the relationship between financial hardship and depression. The prevalence of hardship differs across the life course (Mirowsky and Ross, 1999) and by sex (Butterworth et al., 2009). There is mixed evidence in the literature as to whether the association between hardship and depression varies by age. Mirowsky and Ross (1999) reported that the association was weaker for older respondents and postulated that older adults are less susceptible to distress in the face of hardship because they are better equipped to cope with negative events due to life experience. However, Weich and Lewis (1998a) and Butterworth and colleagues (2009) found no evidence that the relationship between hardship and depression varied with age. Thus, the role of age and sex requires further clarification.

The current study has two distinct aims. (1) To examine the contemporaneous association between financial hardship and depression using a well-validated diagnostic instrument and data from a large Australian national survey. We hypothesis that, compared to other measures of socio-economic circumstances, hardship will be amongst the strongest correlates of depression and that the effect of hardship will remain evident after controlling for a broad range of individual-, household- and area-level measures. (2) The study also examines whether there is demographic variation in the association between hardship and depression and explores potential reasons for inconsistencies in previous research assessing differences in the relationship between hardship and depression across age. By providing information about the relationship between socio-economic position and depression and identifying population subgroups that may be most impacted by financial hardship, the results of this study will provide valuable information for the planning and targeted delivery of services at a national level.

Methods

Sample

The analysis used data from the confidentialised unit record file of the 2007 Australian National Survey of Mental Health and Wellbeing (NSMHWB). The survey methodology identified a stratified, multistage area probability sample of private dwellings from across Australia, and selected one household member aged between 16 and 85 years from each household for interview. This resulted in a sample of 8841 respondents from 14,805 households; a response rate of 60%. Interviews were conducted by trained interviewers from the Australian Bureau of Statistics (ABS). Further details of the survey methodology are available elsewhere (ABS, 2009a; Slade et al., 2009).

Measures

The 2007 NSMHWB included Version 3.0 of the World Mental Health Composite International Diagnostic Interview (WMH-CIDI 3.0) to determine whether respondents met diagnostic criteria for an affective, anxiety, and/or substance use disorder at any point during their lifetime, and whether this disorder was present in the past 12 months and 30 days. For this analysis, we largely focus on the 12-month prevalence of depressive disorders (major, moderate and minor episodes according to International Classification of Diseases (ICD) 10 criteria). Interviews were conducted via Computer-Assisted Personal Interview procedure. The survey collected data on respondents’ demographic characteristics including: age, sex, marital/partner status and regional location (major urban, other urban or other). Age was categorised into three groups of young (16 to < 35 years), middle-aged (35 to < 65 years) and older (65+ years) adults. Indicators of socio-economic position included: educational attainment, labour-force status, occupational skill level (classifying those in clerical, sales, machinery operating or labouring jobs as ‘low skill’), financial hardship (see below), housing tenure (renting vs other), sources of personal income (relying on government pensions or payments as main source of income), equivalised household income (income adjusted for household composition), and area-level socio-economic status (SES). Area-level SES was measured using the Socio-Economic Indexes for Areas (SEIFA) Index of Relative Socio-Economic Disadvantage. This measure was created by the ABS from extensive socio-economic information collected within geographic areas during the 2006 Census (ABS, 2008). Areas in the lowest SEIFA quintile were considered disadvantaged areas. Equivalised household income (based on the modified OECD approach; ABS, 2009b) was also classified as low if in the bottom quintile. The cut-points for these measures of socio-economic position were selected to maximise the consistency of the size of the population identified by each criteria and those identified as experiencing hardship (see Table 1). Further sensitivity analyses focused on the youngest age group: contrasting results for those aged 16–24 years with those aged 25–34 years, and differentiating between those living with their parents/guardians and those with other (i.e. more independent) living arrangements.

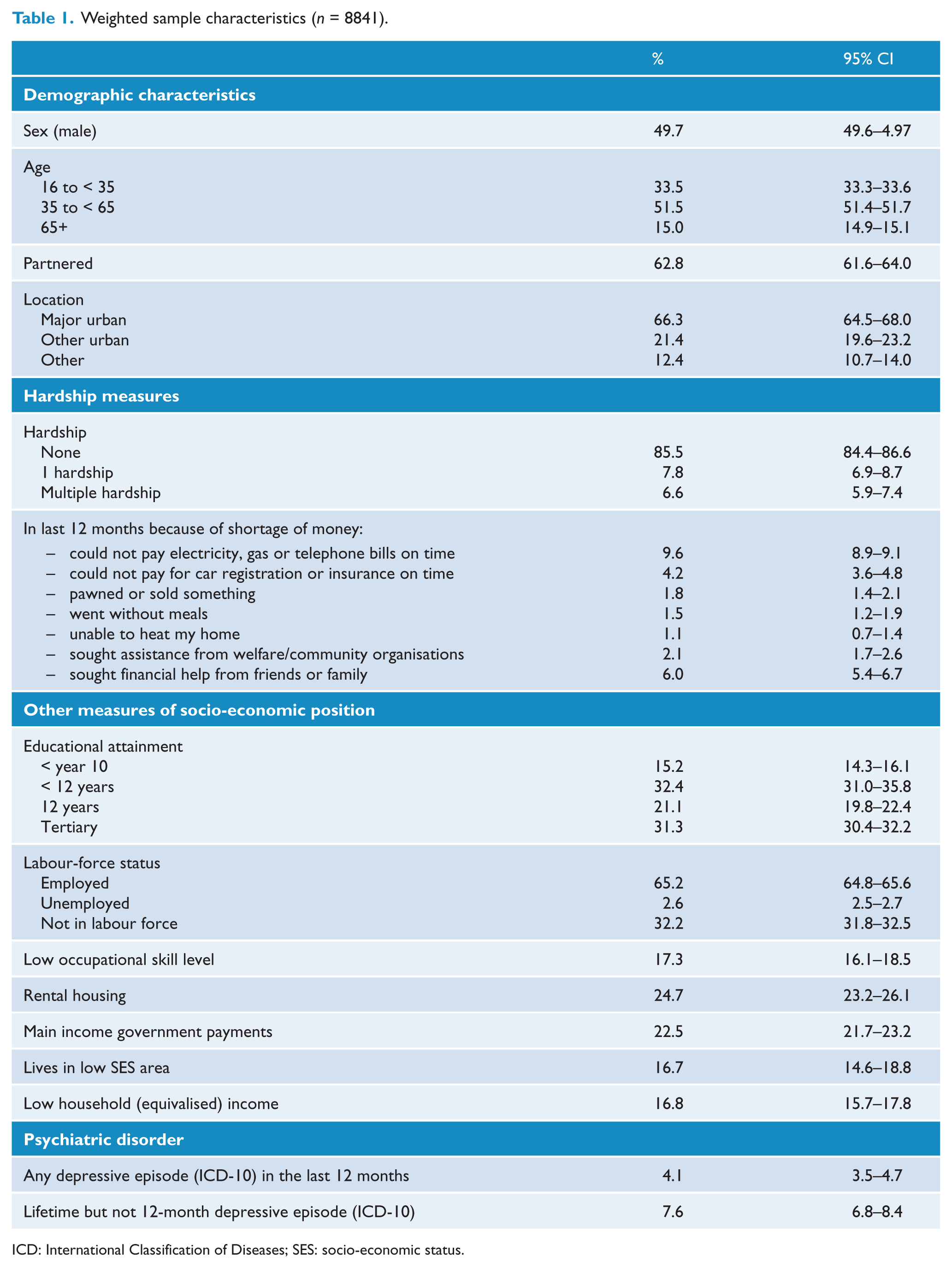

Weighted sample characteristics (n = 8841).

ICD: International Classification of Diseases; SES: socio-economic status.

Financial hardship was assessed by asking respondents whether their household had, in the past 12 months, experienced any of seven indicators of deprivation such as: being unable to pay bills, going without meals or basic services, and seeking welfare or financial assistance from others. These questions were adapted from items in the 1998–99 ABS Household Expenditure Survey (ABS, 2000; Bray, 2001). Consistent with previous analysis of the psychometric properties of these items (Butterworth and Crosier, 2005), factor analysis based on a tetrachoric correlation matrix confirmed that these seven items loaded onto a single factor (only 1 eigenvalue greater than 1; factor loadings between 0.81 and 0.91) and the seven items demonstrated moderate internal constancy (Kuder–Richardson coefficient of reliability of 0.73). A measure was constructed indicating whether respondents had experienced none, one, or two-or-more of these seven hardships. Measures of financial hardship, such as those used in the current study, are evaluated against clearly specified markers or benchmarks of deprivation (e.g. being unable to heat one’s home due to a shortage of money). The specific criteria used may be basic necessities (food, shelter, clothing, health care) or more relative factors (access to car, household appliances) (Butterworth and Crosier, 2005; Heflin and Iceland, 2009; Whelan et al., 2001).

Analysis

Logistic regression analyses were used to evaluate the correlates of depression. The univariate association between each indicator of socio-economic position (including the individual measures of financial hardship) and the odds of depressive disorder was first examined. Subsequently, all indicators were entered simultaneously in a multivariate model to examine their unique contribution. Demographic covariates were also included in this multivariate model. The potentially moderating roles of age, sex, and partner status were then tested using cross-product interaction terms. Because of the potential heterogeneity in living circumstances of those in the youngest age group, further analyses focused on these respondents, evaluating potential age differences and the role of living with parents versus living independently. For simplicity, the financial hardship measure used in these interactions was condensed to a binary variable of ‘0’ versus ‘any hardship’. Each interaction was considered in a separate multivariate model that adjusted for all other indicators of socio-economic position and demographic variables. Although only cross-sectional data are available, we also examined some temporal aspects of the association between hardship and depression by using data on timing of depression. We used multinomial logistic regression analysis to contrast the association of current (12-month) hardship with current (12-month) depression, with prior but not current depression, and with no lifetime history of depression, reporting relative risk ratios (RRR). Data were weighted to population benchmarks, and jackknife replicate weights provided with the dataset by the ABS were used to derive standard errors and confidence intervals. All statistical analyses were conducted using STATA 11.0.

Results

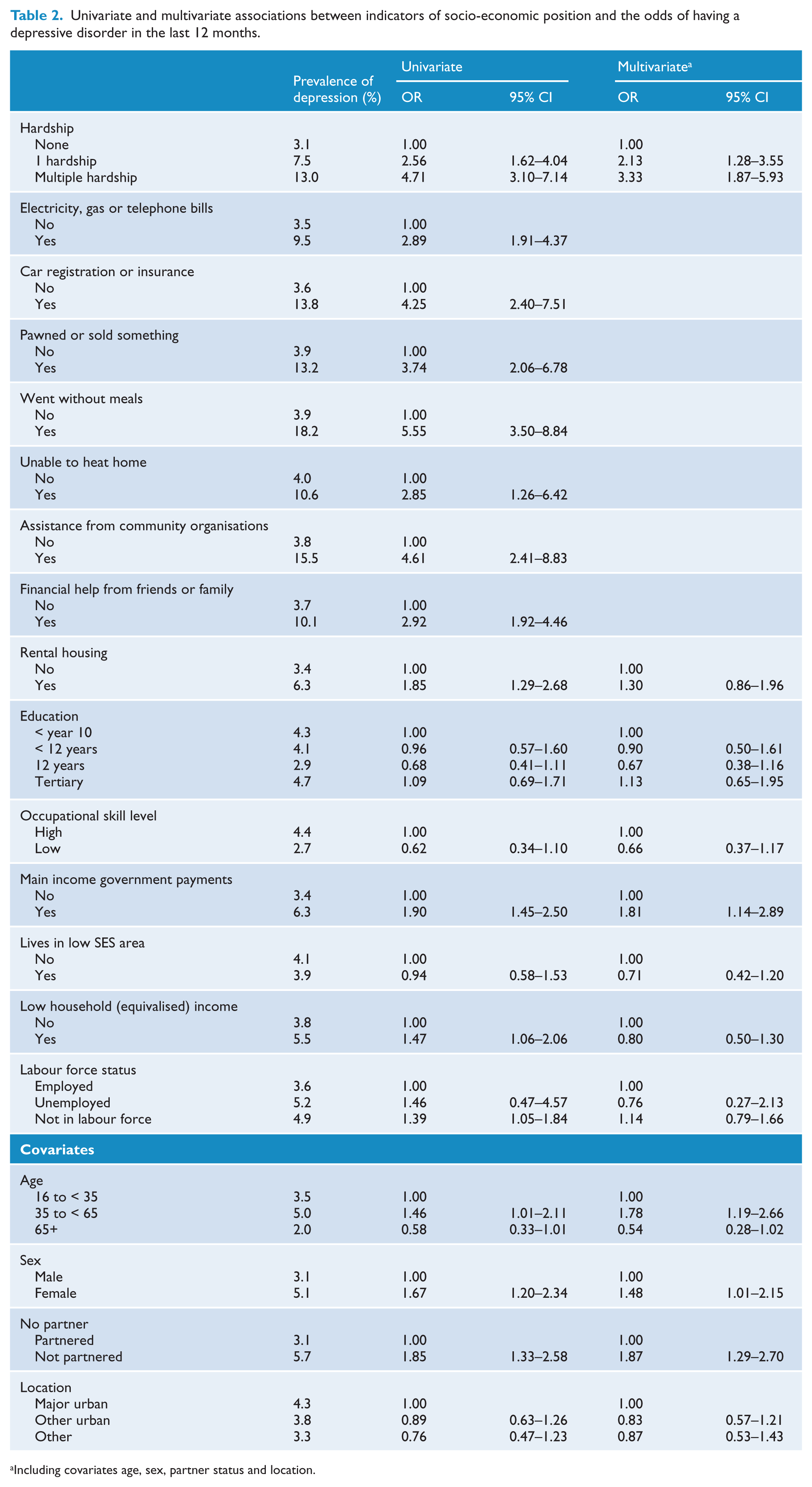

The (weighted) characteristics of the sample are presented in Table 1. While the overall prevalence of 12-month depression in the population was estimated as 4.1%, Table 2 shows that the prevalence of depression was much greater when indicators of poor socio-economic position were experienced. The most critical findings were that, overall, 3.1% of people who reported no hardship had a diagnosable depressive episode compared to 7.5% experiencing one hardship and 13.0% with two or more hardships. The results of univariate logistic regression models demonstrating greater odds were associated with experiencing one or two-or-more financial hardships, living in rental housing, being reliant on government welfare, having a low household income, and being unemployed. All of the individual measures of hardship were also associated with greater risk of depression, but particularly going without meals, seeking assistance from community organisation, difficulty paying car registration and insurance, and having to pawn or sell goods.

Univariate and multivariate associations between indicators of socio-economic position and the odds of having a depressive disorder in the last 12 months.

Including covariates age, sex, partner status and location.

The multivariate model of Table 2 shows that the two categories of financial hardship remained significantly associated with the experience of depression. The only other significant association was between reliance on government welfare payments and depression. Low income, unemployment, and housing tenure were no longer associated with a greater risk of depressive episode. The magnitude of the odds of depressive disorder amongst people with one or multiple hardships changed little following adjustment for other indicators of socio-economic position. Financial hardship demonstrated the strongest association with depression relative to the other variables. Considering the other demographic measures, the odds of depression were lower amongst people with a partner and higher for women. Compared to those in the youngest age group, those in the middle age group reported a significantly greater risk of depression and those in the oldest age group were marginally less likely to report a 12-month depressive episode. Geographic location was unrelated to prevalence of depression in the multivariate model.

Data on history of depression (current 12-month disorder, previous but not 12-month disorder, no history of depression) were examined using multinomial logistic regression analysis. Amongst those not reporting current hardship, 7.3% reported prior but not 12-month depression (95% CI = 6.4–8.2%) and 3.1% reported 12-month depression (95% CI = 2.6–3.5%). In contrast, for those currently experiencing hardship, 9.3% reported prior but not 12-month depression (95% CI = 7.0–11.6%) and 10.0% reported 12-month depression (95% CI = 7.4–12.6%). Multinomial logistic regression models included all covariates and used no history of depression as the reference category for the dependent variable. While the results showed that there was an association between current hardship and prior but not 12-month depression (RRR = 1.43, 95% CI = 1.04–1.98), the association between current hardship and current (12-month) depression was much stronger (RRR = 2.76, 95% CI = 1.82–4.20). Direct comparison of these two categories confirmed the significance of this difference (RRR = 1.93, 95% CI = 1.17–3.18).

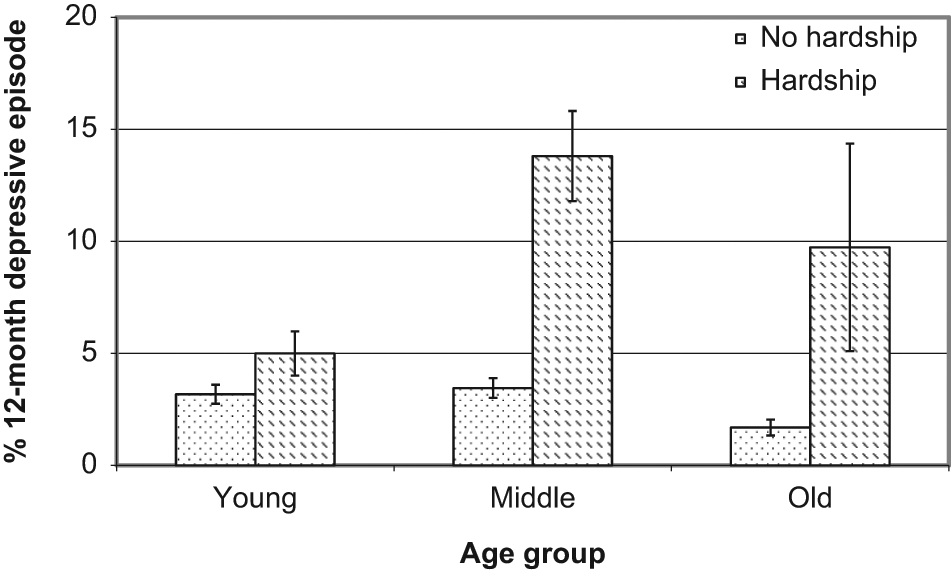

A series of logistic regression models examined potential moderating effects of socio-demographic characteristics. Non-significant interaction terms indicated that the association between hardship and depressive episode was not moderated by sex (OR = 0.81, 95% CI = 0.41–1.61) or partner status (OR = 1.37, 95% CI = 0.69–2.71). However, the association between hardship and depression differed across age groups (interaction terms: ORyoung vs middle = 2.48, 95% CI = 1.35–4.53; ORyoung vs old = 3.58, 95% CI = 1.05–12.15). To interpret this interaction, the multivariate model presented in Table 2 was conducted separately for each of the three age groups. These models showed that the relative odds of depression associated with the experience of hardship increased with increasing age: youngest age group OR = 1.23, 95% CI = 0.70–2.16; middle age group OR = 3.53, 95% CI: 2.05–6.09; and oldest age group OR = 4.10, 95% CI = 1.16–14.51. A somewhat different pattern is evident if absolute differences in the prevalence of depression are considered. Figure 1 shows that the greatest absolute difference in the prevalence of depression for people with and without financial hardship is evident for the middle age group (difference of 10.3%), with the absolute difference in the prevalence of depression due to hardship less amongst older (8.0%) and younger (1.8%) people. To place these findings in context, further analysis showed that the experience of any hardship was much more common amongst those in the youngest (17.7%, 95% CI = 15.9–19.6) and middle (15.3%, 95% CI = 13.6–17.0) age groups than amongst older respondents (4.4%, 95% CI = 3.3–5.6).

Prevalence of 12-month depressive episode (and standard errors) by financial hardship across age groups.

A number of sensitivity analyses focused on respondents in the youngest age group. A non-significant interaction term showed that the effect of hardship did not differ for those aged 16–24 years and those aged 25–34 years (OR = 2.15, 95% CI = 0.64–7.29). Further, the association between hardship and depression in the (original) youngest age group (16–34 years) was not influenced by living arrangements (interaction term OR = 0.87, 95% CI = 0.15–5.06), with the effect of living arrangements (living with parents vs other) also non-significant (OR = 0.99, 95% CI = 0.48–2.04).

Discussion

This study examined the relationship between financial hardship and 12-month depressive episode in a national sample of Australian adults. Financial hardship was found to be strongly associated with the experience of depression, and more so than other commonly examined indicators of low socio-economic position such as low income, unemployment, and living in a disadvantaged area. These latter indicators did not demonstrate an independent association with depression after adjustment for hardship. Only reported reliance on welfare payments (those reporting government pensions as their main source of income) remained significantly associated with increased risk of depression independent of hardship. While current hardship was associated with a modest increased risk of prior (but not current) depression, hardship was much more strongly associated with current (12-month) depression. Finally, we found that the association between hardship and depression was greatest, in a relative sense, amongst the oldest in our sampled population but noted that the greatest absolute difference was evident amongst middle-aged respondents.

Although Australia is an affluent western society, the personal experience of financial hardship was not uncommon (around 15% of the sample reported some experience of hardship). While hardship was associated with depressive episodes, there was also evidence of a dose–response with multiple hardship almost doubling the odds of depression over experience of a single type of hardship. In the current study, hardship was defined as difficulty meeting the basic requirements of daily life due to a lack of financial resources, including being unable to heat one’s home, having to sell possessions, going without meals, not paying utility bills on time, and asking for help from community organisations (Bray, 2001; Butterworth and Crosier, 2005). We note the conceptual similarity between these items and measures used by others in the research literature (e.g. household overcrowding, ownership of household appliances, access to a car, difficulty purchasing food or clothing, debt; or having services/utilities disconnected) and which have been found to be associated with poor mental health (Heflin and Iceland, 2009; Jenkins et al., 2008; Lewis et al., 1998; Lorant et al., 2007; Mirowsky and Ross, 2001; Skapinakis et al., 2006; Weich and Lewis, 1998a, 1998b; Whelan, 1993). As with much of this previous research, we found that financial hardship was not only the most powerful socio- economic correlate of depression, but that it also mediated or accounted for the association between other measures of social position and depression (Heflin and Iceland, 2009; Kessler et al., 1987; Rodgers, 1991). In fact, in analysis not reported here, the modest univariate association between low income and depressive episode was entirely explained by the inclusion of the hardship measure, similar to the findings related to debt by Jenkins and colleagues (2008).

The current results not only show that hardship is more strongly associated with depression than other socio- economic measures, but also suggest that people in similar socio-economic circumstances with respect to income and other characteristics have different experiences of hardship. This is, we contend, another strength of hardship measures. Unlike income or derived poverty measures, hardship directly assesses the impact of a lack of resources on exclusion while taking account of potential moderating factors such as wealth, assets, use of credit or debt, and the availability of non-cash benefits such as the sharing of resources and support from family and friends (Bray, 2001; Butterworth et al., 2009; Nolan and Whelan, 1996). It should also be recognised that the experience of hardship may, in part, reflect differences in financial management and budgeting skills and the different costs incurred by different individuals/households (e.g. additional expenditure associated with disability, tobacco or other dependencies, housing circumstances) (Bray, 2001; Butterworth and Crosier, 2005; Siahpush et al., 2007).

There is differentiation and debate between neo-material and psychosocial explanations of health inequalities (Lynch et al., 2000; Marmot and Wilkinson, 2001; Muntaner et al., 2004). Our consideration of hardship and the findings of this study are consistent with a neo-material approach in attributing the increased risk of affective disorders directly to the inadequacy of material circumstances. From this point of view, the current experience of hardship is considered within the context of an accumulation of adversity across the life course and associated limited access to protective resources including health and social services (Heflin and Iceland, 2009; Lynch et al., 1997, 2000, 2004; Pudrovska et al., 2005). While we found that all of the individual hardship items were strongly associated with the experience of depression, the strongest relationship was evident for being unable to afford meals. This was consistent with our previous research from Canberra (Butterworth et al., 2009) and suggests, consistent with a neo-material explanation, that the most profound mental health effects of hardship are associated with food insecurity. However, it is equally plausible to hypothesise that difficulty meeting the basic necessities of life results in feelings of despair, demoralisation, lack of control and helplessness (i.e. a psychosocial perspective) (Brown, 2002; Kahn and Pearlin, 2006; Marmot and Wilkinson, 2001; Pudrovska et al., 2005; Reading and Reynolds, 2001). Irrespective of the theoretical perspective, the current findings suggest that financial hardship is a potent stressor and associated with the experience of depression. Accordingly, recognising and addressing the material disadvantage experienced by the most vulnerable people in society may be one aspect of appropriate interventions to improve population mental health (Heflin and Iceland, 2009; Marmot and Wilkinson, 2001). Over and above the effects of hardship, welfare reliance remained significantly associated with 12-month depressive episode. Again, we cannot discern whether this is a reflection of Australia’s highly targeted, universal welfare system, which means that welfare receipt may be a proxy identifying those in the most adverse social circumstances or whether it reflects the psychological stigma associated with welfare receipt (Butterworth, 2003).

While the results of the current study are consistent with a role of financial hardship in the aetiology of depression, there is no unambiguous epidemiological evidence to confirm this hypothesis. Evidence of the social costs of mental disorders demonstrate that mental disorders may disrupt educational attainment, limit career prospects, and lead to reduced income (Kessler et al., 1995, 2008). Therefore, depression could be conceptualised as a factor leading to financial hardship and deprivation. Cross-sectional analyses report a strong contemporaneous relationship between financial hardship and depression, and several longitudinal studies have also shown that change in hardship is associated with change in depression (Heflin and Iceland, 2009; Lorant et al., 2007; Mirowsky and Ross, 2001; Rodgers, 1991; Weich and Lewis, 1998a). The conclusion from several studies using a prospective cohort design is that prior hardship is more strongly (or exclusively) associated with the maintenance of depression/mental illness, rather than onset (Lorant et al., 2003; Skapinakis et al., 2006). Further, Lorant and colleagues (Lorant et al., 2003; Skapinakis et al., 2006) reported that lagged change in hardship (deprivation in their terminology) was not associated with subsequent change in depression. In the current study, the cross-sectional association between the reported experience of financial hardship in last 12 months and the 12-month prevalence of depression demonstrates the salience of hardship but cannot disentangle these alternative causal pathways. However, in considering lifetime prevalence of depression, we found that the association between hardship and depression was largely restricted to a contemporaneous relationship, and that for those experiencing hardship the risk of prior depression was half the risk of current depression. While recognising the limits of the retrospective data on which this analysis was based, this finding does not provide compelling evidence that history of depression increases vulnerability to hardship or support a temporal sequence of depression leading to hardship. However, further research using longitudinal data is needed.

We examined whether the association between financial hardship and depression varied according to age in an attempt to resolve inconsistencies evident in the literature. While Mirowsky and Ross (2001) found that this association was weaker amongst older people, Weich and Lewis (1998a) found no evidence of a moderating effect of age and Butterworth and colleagues (1998a) reported no statistical significance but a tendency for the effect of hardship to lessen with increasing age. The current study produced a pattern of results different from these again, with the association between hardship and depression greatest for the oldest group. However, this in part reflected the low overall prevalence of affective disorders amongst older adults; the greatest absolute difference attributable to hardship was evident in middle age. Interestingly, we found that the association between hardship and depression was not significant in the youngest age group (aged 16–34 years), which was the age group with the highest prevalence of hardship. Again, the discrepant findings across studies may be due to methodological differences. Mirowsky and Ross used a continuous measure of age (centred at 45 years), whereas the other studies categorised age. Reference points also differ between studies. The age of the older groups also differed between studies: 64–68 years in Butterworth’s study, 56–75 years in Weich and Lewis’s study and 65–85 years in the current study. Finally, the current study evaluated data from a diagnostic clinical interview, whereas the other studies used dimensional scales of depression or general mental health. Obviously, further research on this topic is necessary, but it does seem that the adverse effects of hardship on depression may be greatest for those groups for whom hardship is rare. Further research could consider if this reflects a stigmatising influence of financial hardship such that the impact is less in subgroups where hardship is more of a shared experience.

Study strengths and limitations

The present study of financial hardship and depression is one of very few to: (1) include a diagnostic measure of depressive episode; (2) use representative population data; and (3) include a measure of personal financial hardship along with a wide range of other indicators of socio-economic position (see also Skapinakis et al., 2006). This represents a significant advance in the literature. Moreover, our current analysis extended previous studies that have used similar methodological and measurement approaches by including a more thorough range of socio-economic indicators (i.e. in addition to the measures used by Skapinakis and colleagues (2006), we included welfare receipt and area-level disadvantage) alongside a comprehensive and psychometrically tested measure of financial hardship (Butterworth and Crosier, 2005). However, the current study was largely based on cross-sectional data, with retrospective data on the timing of depression available but hardship only assessed in the previous 12 months. Thus, the extent to which we could examine how changes in hardship were associated with changes in depression over time, or attempt to determine the causal nature of their association was limited. It is also important to recognise that the response rate for the NSMHWB was lower than expected (Slade et al., 2009) and may, therefore, compromise the validity of the findings. This, however, is a factor influencing epidemiological research worldwide (Galea and Tracy, 2007). We also acknowledge that the statistical power of financial hardship may not simply reflect current circumstances, but that hardship may be a marker of severe and entrenched adversity that accumulates across the life course. Finally, with data collected in 2007, the survey preceded the onset of the Global Financial Crisis and, thus, a potential increase in hardship at the population level.

In conclusion, the current study showed that financial hardship is the strongest socio-economic correlate of depressive episode and emphasised the contemporaneous relationship between hardship and depression. This supports the view that the experience of deprivation is more relevant to mental health than other markers of social position or area-level indicators, and is consistent with social and clinical models regarding the development and maintenance of depression. The results identify a potentially important mechanism to explain the association between adverse socio-economic circumstances and mental health. Our findings are consistent with efforts to reduce the prevalence and burden of depression via social and economic policies that address inequalities in living standards.

Footnotes

Funding

PB is supported by NHMRC Population Health Career Development Award Fellowship No. 525410.

Declaration of interest

The authors report no conflicts of interest. The authors alone are responsible for the content and writing of the paper.