Abstract

This paper argues that the state’s capacity to tax corporations in order to fund itself is reaching crisis proportions. Following decades of trade liberalization, deregulation, and globalization, large multinational companies have been able to take advantage of tax competition between states in order to avoid taxation and offset their obligations. This crisis, arguably, has been facilitated by state actors and exacerbated by non-state actors: we explore the ways in which multi-national corporations (MNCs) manipulate their capital, assets, and supply chains to minimize their tax burdens; and we further consider the ways in which media narratives construct this issue and whether they challenge the practice or intensify it. Discourse surrounding taxation plays a huge part in what is considered acceptable. While the old adage that “death and taxes” cannot be avoided, it has become clear that large companies, helped by a tax avoidance industry do indeed manage to do just that. Discourse analysis reveals the ways in which ideology can be used to manage consensus around this potentially controversial subject and this paper seeks to explicate that by examining the frames, presuppositions and discursive formations present within the discourse structure. The argument is developed through a comparative case study research design demonstrating the different policy-based, economic and historical contexts of the two jurisdictions which offer some insight and explanation of the distinctive ideological discursive formations that are present within the discourses.

Introduction

The decade since the Great Financial Crash has witnessed an amplification of discourses on the role of tax avoidance in reducing the state’s capacity to fund itself and redistribute wealth (Mazzucato, 2015; Picciotto, 2013, p. 77; Piketty, 2014; Stewart, 2014; Zucman, 2021). Since the late 1970s, states’ capacity to tax corporate profits has been hampered by deregulation of national economies (Harvey, 2007; Hope, 2009; Stewart & Godley, 2011) and proliferated global finance flows. This has allowed asset-rich, multi-national corporations (MNCs) to remain mobile, taking advantage of increasingly competitive corporate tax rates around the globe. Economic deregulation, liberalization, and globalization of recent decades has led to an increased concentration of business-ownership (Bohle & Regan, 2021), typically a handful of gigantic firms that transcends national boundaries and define the economic outlook of states, especially smaller ones, dependent upon capital inflow. From the state’s perspective, this inability to levy tax on mobile corporations is reaching a crisis point, prompting the Organisation for Economic Cooperation and Development (OECD) to intervene with the Base Erosion and Profit Shifting (BEPS) initiative and refocus taxation around a global minimum rate.

How we talk publicly about tax matters: This study explores the role of media, from a constructivist perspective (Potter, 1996, p. 3; Shotter & Gergen, 1994), in the formation and manipulation of ideology surrounding the payment of taxes and examines whether media, along with other non-state actors, contribute to the deepening crisis of corporate tax avoidance globally. By focusing upon the tax practices of Google and Apple, the paper explores temporality associated with the digitization of global capitalism which has concentrated power within the Information and Communications Technology (ICT) industries as they continue to serve as the nervous system of globalizing capital (Hope, 2009).

The next section outlines relevant features of the global corporate taxation context before a section which introduces the main discourses of corporate taxation at play globally. This is followed by a section focusing on the particular approach to discourse used in the paper. This leads to a section where the empirical contexts in this study of corporate taxation discourses are situated. The particular methods and data choices are then explained, before a section showing the findings. A discussion and conclusion section completes the work.

Corporate Taxation

Since the late 1970s, coinciding with the advent and proliferation of neoliberal ideologies, states’ capacity to tax corporate profits has been hampered by competition between states, deregulation of national economies and the increasingly widespread availability of access to the mechanisms of international tax avoidance (Sikka, 2015). Fuchs (2018) notes the emergence of a “tax avoidance industry” servicing MNCs dominated by the “big four” (DeLoitte & Touche, Pricewaterhouse Coopers, KPMG, and Ernst & Young) accountancy firms which attribute one-third of their combined global income (approximately £25 billion) to the design, marketing, and implementation of artificial tax avoidance arrangements (Sikka, 2015). In the decade since the Great Financial Crash, the role of tax avoidance has shown to be partly responsible for a further drop in the taxes corporations pay (Toplensky, 2018) and in reducing many states’ capacity to raise funds (Mazzucato, 2015). The OECD’s attempts at rectification around a global minimum effective corporate tax rate had stalled prior to agreement by Ireland in October 2021.

For many, especially larger states, the fall in corporate tax revenue has provoked a number of responses. The U.S. have traditionally focused upon the neoliberal tax reform agenda (Infanti, 2012) emphasizing comparisons between different jurisdictions and what this purports to offer the predominantly U.S.-owned MNCs (Marian, 2012, p. 146). Trump administration’s plan was for the corporate tax rate to be lowered to 21%, and similar debate was taking place in Australia as its government proposed a reduction in corporate tax from 30% to 25% on the basis of “increased investment and productivity in a globally competitive environment” (Ingles & Stewart, 2018). Yet Washington and other capitals has begun focusing upon “tax reform” in the corporate tax context, a strong feature of recent presidential election campaigns, with an emphasis on falling revenue-neutral changes that seek to broaden the tax base while lowering the tax rate (Hungerford, 2013).

In neoliberalism, lowering corporate taxation rates is even more important for smaller states in attracting MNCs and promoting development. Some state’s tax revenue that has used this policy prescription have become heavily reliant on their share of the reducing global taxation of MNCs. Dependence on relatively large shares of global corporate tax revenue is very vulnerable to changes in corporate practices, in turn dependent on a range of uncertain future contingencies including the continuing tax competition between states (Picciotto, 2013). Even states that are seemingly winning the tax competition game are aware, based on the logic of race to the bottom, that their wins in corporate revenue are unstable in the long run.

Globally too, there had been evidence of the reform discourse, with developing countries coming under pressure to reform and broaden their tax base (Stewart, 2012). The OECD’s attempts to tackle global tax avoidance and evasion using the Inclusive Framework for BEPS program obtained agreement from all OECD countries (OECD, 2021). Brauner (2014) recognizes a paradigmatic shift from the extant emphasis on competitiveness and perfect competition toward a more collaborative regime of international taxation. The current period is one of change and uncertainties as to how a new corporation tax regime may affect those concerned. Beckert (2020) has shown how such uncertainties concerning the future are handled by “imagined futures” which drive modern economies or create crises in them.

Corporate Tax Discourses

The imagined futures to which Beckert (2016) refers can be explored by analyzing the discourses used to construct them. Discourse studies have shown that since at least the 1980s that economic imaginaries have largely been of the neoliberal variety, with its variety seemingly giving some of its apparent tenacity (Mirowski et al., 2020). Neoliberal economic imaginaries have been challenged not only by critics but also the realities such as the 2008 GFC (Global Financial Crisis), the COVID-19 pandemic, the ecological crises, and perhaps most centrally, the growing inequality within most advanced economies (McBride, 2022). Since taxation is central to both how market processes distribute resources and to the redistribution resources allocated by the market, taxation discourses play a central role in economic imaginaries. Discourses of taxation vary in their circulation, and there have discourse studies of taxation, often embedded in wider economic imaginaries at a number of levels. Maesse and Nicoletta (2021) have examined such discourses at the level of EU institution building. Relevant discourses of National and international policy professionals and institutions have been analyzed in works such as Borrás et al. (2015) with the discourses of politicians addressed by works such MacDonald et al. (2023).

Mass media sources are arguably one of the most important resources to examine on corporate tax discourse and so is the focus of this article. Media has an impact upon the perceptions and knowledge of economic processes, thus influencing preferences of the public of economic policy making—as Veblen suggests, the press is an “educational system”(Grisold & Theine, 2020). The media system itself forms part of the wider economic structure offering a commodity for sale within the market (Fuchs, 2009; Smythe, 1981) and so critical examination of their discourses is essential as the media are deeply embedded into structures of domination. Early work by Chen and Meindl (1991) recognizes that the media constitutes an important medium for the construction of public opinion on corporate tax practices. Empirically, Kneafsey and Regan (2019), show the strong influence on mass media is in forming views the public’s views on corporate taxation. Bell and Entman’s (2011) study addresses what they recognize as a deficit of political communications research work, examining the media’s coverage of taxation issues. Economic discussions concerning issues of economic inequality tend to focus upon quantitative evaluation (Antonelli & Rehbein, 2018; Galbraith, 2012) but how these evaluations are in turn mediated to the public have been until recently much less commonly addressed (Grisold & Theine, 2020).

Previous discourse studies show that taxation in the media has been addressed in the context of its redistributive possibilities (Thomas, 2018). An international comparison of media coverage of Piketty’s (2020) surprise economics bestseller showed mediated coverage of redistributive solutions to the financial crisis and contend that news media discourse on redistribution policies tend to discredit politics and assign a high-ambivalent role to government and the state (Grisold & Silke, 2019; Grisold & Theine, 2020; Rieder & Theine, 2019; Theine, 2019; Theine & Rieder, 2019).

More recently, in the United States, particular discursive emphasis is placed upon the implications for global companies, many of them U.S.-owned and operating in other jurisdictions. This has become a feature of the U.S. presidential campaigns of the last decade, and whether or not tax amnesties are realized or loopholes closed down, it can be argued that the discourse surrounding taxing corporations has certainly changed. In the European context countries, such as Ireland and the United Kingdom, have argued that regional or global cooperation on such taxation would infringe upon their national sovereignty (Berkhout, 2018). Radaelli’s (2013) studies recognize that sovereignty remains a key feature of discourse within the European Union on tax policy; and in particular, that some tax policies, such as corporation tax, are more susceptible to the process of “Europeanization.” Berkhout (2018) found that the discourses focus upon the consideration of competitiveness against other countries for attracting foreign investment emphasising how these debates are influenced by corporates interests seen in such practices as frequent movement of personnel from public interest roles to private employment.

Critical Discourse Analysis

This article takes a Critical Discourse Analysis (CDA) approach to investigating such corporate tax discourses. Given the dynamic natures of corporation taxation policy, such discourses are important for “imagined futures.” Whereas CDA as an approach is well-established within discourse studies, the differing uses of the term discourse within political studies demands that some further explanation be provided here. Political studies can be viewed as examining interest, institutions, and ideas, a discursive approach focusses on communicative interaction. Various discursive approaches have been used in, and are gaining increased recognition in the study of politics (Carstensen & Schmidt, 2016; Howarth & Griggs, 2012; MacDonald et al., 2023) though the analysis of discourse is often blunted where it is interpreted merely as a route to understanding ideology as traditionally viewed. The confusion arises partly because, for discourse analysis, ideology is embedded in discourse, especially for critical versions like CDA (Carvalho, 2008). As discourse analysis has advanced, its understanding of ideology has become increasingly clear (Van Dijk, 2006), making it quite distinctive from the traditional understandings of ideology. The discursive approach to ideology used here is to study ideology as a communicative interaction, necessarily mediated in some materiality (from sound waves to paper to radio waves) shaped not so much by the cognitive connections in the brain, much less by logics of a mind, but by the material nature and genre-specificities (from Twitter to news interview conventions) affordances in which the discourse takes place.

Having clarified the distinctive understanding of ideology in discourse analysis as more mediated and material communicative interaction than purely cognitive or conceptual, it is possible to understand more specifically the way ideology is used in the approach taken here. Fairclough’s CDA interpretation of ideology (Fairclough, 1995) is rooted in the Gramscian theory of ideological hegemony. Gramsci’s theory recognizes the deep relationship between the state and civil society: a hegemonic system involving rule by consensus as well as coercion. Developing Gramsci’s concept, Riley observes that as hegemonies emerge, the interests of a single social class, the dominant class, become fused with the interests of society as a whole (Riley, 2011: 16) and he notes that the capacity of the dominant group to dominate is based upon its ability to develop intra-class hegemony. For Gramsci, the nature of common sense is that is not rigid or immobile, but continually transforming itself, and importantly “enriching itself with scientific ideas and with philosophical opinions that have entered ordinary life,” becoming the folklore bridging philosophy, science, and economics of the specialists, reflecting a popular knowledge at a given place and time: It is not “critical and coherent, but disjointed and episodic” but it does possess a “logic” and history and draws upon past ideas, traditions, and in the CDA adopted here, the affordances of materiality of the media in which the discourses take palace, to construct solutions to new problems (Gramsci, 1971). This gives us an understanding of how ideology draws from prominent theories and concepts and distils them, making them accessible to wider audiences. Hall and O’Shea offer further clarity into the use of common-sense ideology, particularly in a neoliberal context; determining common sense to be a form of “everyday thinking” and easily accessible knowledge which offers a framework of meaning to make sense of the world; relying upon easily accessible knowledge (Hall & O’Shea, 2013). Eschewing complicated ideas or sophisticated argument, “common sense” tends to work intuitively rather than requiring deep thought, wide reading, or critical reflection, parsing knowledge into chunks for easy digestion. Within the CDA approach adopted here, governance is operated through such hegemonic discourses, which shape but never determine outcomes. In times of crisis, when the discourses of an imagined future break down (Beckert, 2016) it often results in the creation of new discourses that imagine different futures constructed from an assemblage of elements of discourses available and the affordances of the media in which communicative interaction takes place.

CDA holds that ideology is embedded in discourse; however, what ideology means can be somewhat more contested (Carvalho, 2008) and while ideological stances can often be the most fundamental influence to shape a text, some analyses of discourse do not always fully reveal themselves. Ideological mechanisms exist at the level of the implicit often making them difficult to identify (Fairclough, 1995). These assumptions and presuppositions can be deeply embedded, sometimes subconscious, and so do not easily reveal themselves. Carvalho concurs that ideological standpoints are not always explicit in texts, drawing attention to Allan’s (2010) suggestion that “appearing natural” is central to the ideologically shaped work of representing reality in the news media. In “Understanding News” Hartley recognizes the difficulty in identifying what he terms “ideological closure” and acknowledges that this often requires substantial interpretive work on behalf of the analyst (Hartley, 1982). Carvalho (2008) points out that while in some texts, normative political and value claims are relatively apparent, analysts must learn to identify “relatively subtle mechanisms and devices”. Building upon the work of Chilton, Carvalho identifies “critical discourse moments” as moments worthy of investigation: these moments offer an opportunity to become immersed in a discourse, while it is live and abundant and numerous perspectives are present in the discussion. Chilton observes that these are “periods that involve special happenings which may lead to a challenge to the established discursive positions” (Chilton, 1987).

Historical and Political Background

Much discussion on the merits and demerits of market liberal approaches or neoliberalism has taken place since its advent in the late 1970s (Harvey, 2007; Jessop, 2002). In particular, a key debate took place between prominent globalization advocate Geoffrey Garrett (2001) and one of its key critics, Dani Rodrik (2011); the intervening years have seen both the continued expansion of the globalization phenomenon as well as aspects of its implosion in the wake of the financial crash. However, while criticism of globalization mounts from quarters where previously the phenomenon had received support (Rodrik, 2011) one of its facets has remained steadfast, arguably it has gathered pace: that is the avoidance of corporation tax by global corporations (Stewart, 2020). While much emphasis has been placed on the continued development of tax policy, the key focus of this paper is on how the discourse on tax policy emerges and how that discourse evolves in the mediated public sphere.

While geographically close, the economic and social histories of the United Kingdom and Ireland are very different, although those histories are fundamentally intertwined. The passage of time has seen Ireland’s position change from a state almost entirely dependent upon Britain and its economic sphere to a more diverse position: on the one hand, Ireland can be considered to compete with Britain for global investment while on the other it serves as the “back office” of London in financial flows and in particular to Ireland’s role in global finance flows, primarily via London as facilitated by, among other things, ICT (Breathnach, 2000). A distinction can therefore be drawn between financial services, where the United Kingdom and Ireland complement each other and non-financial industries where there is more competition between these jurisdictions. While Britain and Ireland have come to their respective low tax strategies in different ways and at different times, this study seeks to examine the similarities and divergences underpinning media discourses concerning this economic policy.

Both Irish and British jurisdictions examined in this study can be considered low Corporation Income Tax (CIT) environments. Figures obtained from the Tax Foundation show that in 2019, CIT rates across Europe ranged from a minimum of 9% in Hungary to a maximum of 34% in France, with a mean and median of 22% respectively: This places both countries at the low end of the spectrum using just the headline rates (Ireland at second lowest at 12.5% and Great Britain fourth at 19% (Asen, 2019)).

While Ireland had been using tax incentives (mainly tax exemption from profits on exports and substantial relief on asset depreciation) to attract Foreign Direct Investment to an otherwise sparse industrial landscape since the 1950s, the U.K.’s turn toward lowering corporate tax rates began during the Thatcher administration, from a high of 52% in 1980 (Trading Economics, 2021). The rise of financial innovation, such as securitization and derivatives trading in the 1990s (Stewart & Godley, 2011), led to Britain’s reliance upon global finance flows, including foreign-owned corporate tax income, via the City of London, for its economic prosperity. For its part, Ireland’s corporation tax policy has evolved to include contentious avoidance mechanisms, such as the Double Irish (Fuchs, 2018), the facilitation of stateless income (Stewart, 2020), and various special arrangements like the one with Apple, the media coverage of which is examined in this study.

Such was the controversy surrounding corporation tax and its avoidance in the United Kingdom over the past decade that the parliament convened the UK House of Commons Committee of Public Accounts in 2012 and 2013 (Fuchs, 2018) (known as the Public Accounts Committee or PAC). Chaired by Labour MP Margaret Hodge, it published numerous reports on taxation and specifically on the concern of the organized tax avoidance industry and the extent to which it facilitates corporate tax avoidance (UK House of Commons Committee of Public Accounts, 2012a, 2012b, 2013a, 2013b, 2013c, 2015).

Previous research has captured the scope of the neoliberal orientation of mediated discourse in Ireland over the past several decades (Kirby, 2004; Phelan, 2014; Preston & Silke, 2011; Silke & Graham, 2017). Neoliberalism in Ireland has borrowed from both U.S. and European forms: the former characterized by low corporate and individual taxes, light regulation of the financial system, public–private partnerships, and low levels of public spending on social programs indicative of the U.S. approach (O’Hearn, 2001). In Britain, recent studies examine the media’s role in constructing these various aspects of neoliberalism: throughout, and in the wake of the Great Financial Crash and its ensuing crises (Berry, 2019; Denti & Fodde, 2013); austerity discourses the deficit debate and reconstructed narratives surrounding the economic crisis (Basu, 2018; Berry, 2019).

Sovereignty is certainly a key issue in the discourses of taxing corporates in Ireland: Graham and O’Rourke (2019) identify the discourse of “bureaucratic overreach” into member states’ sovereignty by the European Commission in the wake of its 2016 ruling on Apple’s tax. Kneafsey and Regan (2019) identify sovereignty as an issue in the context of the Apple Ruling which depicts the EC’s ruling as “an infringement on national sovereignty and a direct threat to the Irish FDI growth regime” (2019; p. 4).

In the United Kingdom context, corporate tax avoidance has become prominent in mediated discourse. This is arguably a reciprocal function of the extent to which the issue has obtained and maintained political salience (Dallyn, 2017). Review of the literature on the subject (Ashour, 2021; Birks & Downey, 2015; Dallyn, 2017) attributes increased media coverage of corporate tax avoidance to the emergence of U.K. Uncut. Lee (2015) examined media coverage of tax avoidance in the United Kingdom, during two periods (2010–2011 and 2012–2013) and found that increased media attention does not necessarily stimulate companies to improve the quality and quantity of their tax disclosures in their corporate reporting (Lee, 2015), suggesting that companies view regulatory bodies as their most powerful stakeholder, over any negative media treatment they many receive, and that ultimately places responsibility upon regulatory enforcement to foster tax transparency (Ashour, 2021).

Data and Methods

This study examines discourses on two critical events or “critical discourse moments” (Carvalho, 2008) from two radio news shows concerning the corporation tax arrangements of Apple and Google in 2016, in two jurisdictions, Ireland and the United Kingdom, using a comparative approach. This type of analytical approach, using a two-country case study offers the opportunity to evaluate and contrast the often subtle similarities and distinctions present in both discourses. The first of the critical discourse moment examined here is the European Competition Commission’s ruling on Apple’s tax arrangements with Ireland in August 2016 (EC, 2020). The second critical event is the somewhat lesser-known arrangement between Google and the then British Chancellor of the Exchequer, George Osbourne, in January of that year, known as Diverted Profits Tax (DPT).

Carmel (1999) identifies some difficulties associated with cross-national research, such as language and cultural transferability and linguistic translatability; however, given the literal and figurative closeness of Ireland and the United Kingdom, sharing language, and sociocultural characteristics, such as a similar media environment, and an equivalent economic and political culture, these problems are minimized and the two present as useful case comparators. While Ireland and the United Kingdom are similar in terms of their democratic models, although the U.K. is a constitutional monarchy and Ireland a republic, both use the parliamentary model whose Executive is headed by a prime minister, or Taoiseach in Ireland’s case (Lijphart, 2012). They do differ somewhat in their electoral systems: the U.K. adheres, in the main, to the Westminster or “majoritarian” model of democracy, which favors a majority party system, dominated by a two-party approach; whereas Ireland has moved toward a “consensus” approach, tending to feature coalition governments that produce a more equal power relations between the executive and legislative functions (Lijphart, 1991). The U.K. and many of its former colonies adhere to the plurality approach, in which parties contest elections as single-member districts (Lijphart, 1991). Ireland, however, favored the introduction of a proportional representation system in order, primarily, to reflect the interests of the unionist and nationalist traditions on the island (Carstairs, 2013): notwithstanding developments in Northern Ireland, the Republic largely oscillated between two main parties in multi-party government, which has in recent years tended to produce coalition governments geared toward a more consensus-based type of rule (Lijphart, 1991).

Within mass media this study focusses on broadcast media as it has the capacity to speak directly into the audience’s listening space, often forming the direct basis for social and familial discussion. The choice of news radio, rather than television, for this study was driven by the analytical rigor afforded by being able to focus on sound only and by the useful time-pressure the radio news genre puts on communication that necessitates, less ambivalent statements, than longer former written articles affords in discussing economic issues (FitzGerald & O’Rourke, 2016).

The two programs selected for study, BBC’s “Today” and RTÉ’s “Morning Ireland,” are exemplary cases of the radio genre of extended news interviews. Both RTÉ and BBC are public service broadcasters whose coverage of key social and political issues, often form the basis of mediated discourse throughout the day. BBC’s “Today” has been in existence since 1957 and commands an influential role within broadcast radio, which, based upon key political interviews, has become and remains an important institute in British politics (Williams, 2010). Morning Ireland, commenced in 1984, remains Ireland’s most listened to radio program (Joint National Listenership Research [JNLR], 2012) and arguably its most influential, comprised of, like its BBC counterpart, significant political interviews (Whelan, 2009). Morning Ireland typically contains approximately 12 feature items of 6 to 8 min apiece (plus others in news and roundups); BBC’s “Today” is similarly structured. By focusing upon a relatively narrow selection of news items, radio broadcasts like “Morning Ireland” and “Today” whittle down the news agenda which, effectively given their early-morning time slots, can determine much of the rest of the day’s news agenda, across news media genres. These analyses further facilitate the analyst’s overall conception of a topic’s context, and it is to providing such an analysis that we now turn.

Findings

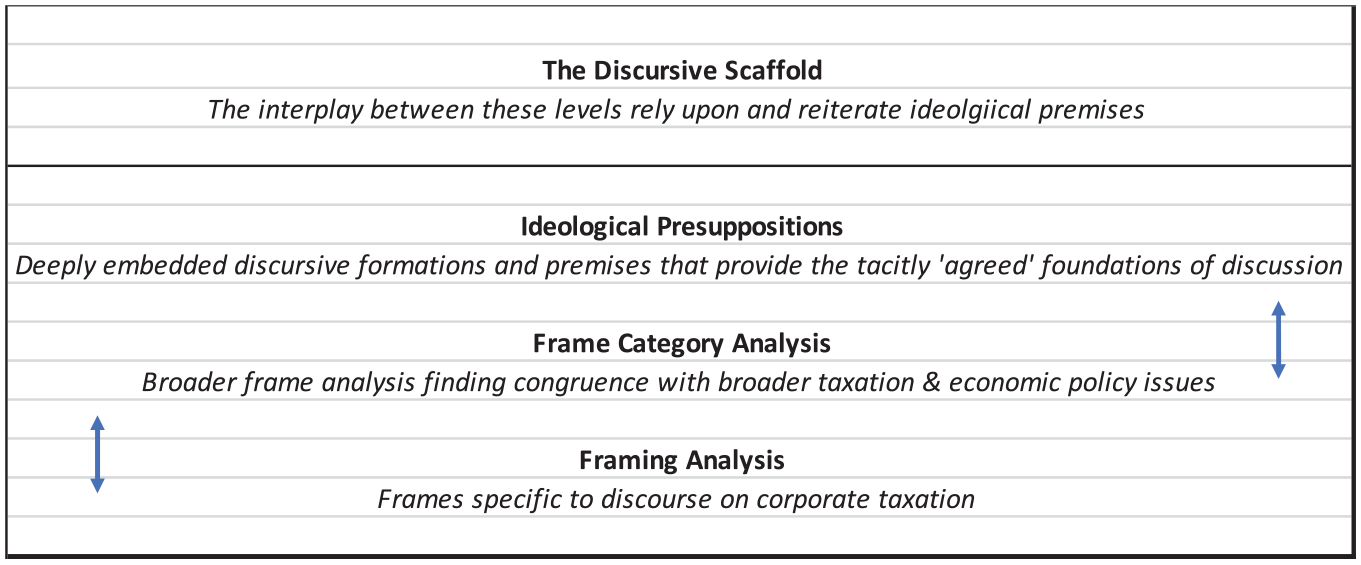

One of the key contributions of this paper is to attempt to explicate some of more latent aspects of discourse analysis. Ideological stances within media analysis can often be the most fundamental influences upon that coverage, but they do not necessarily reveal themselves fully and can be difficult to identify (Fairclough, 1995). Discourse is multifaceted and both assumptions and presuppositions can be deeply embedded, sometimes subconscious; they do not always disclose themselves clearly. Carvalho (2008) draws particular attention to this, noting that ideological standpoints are not always explicit in texts, instead requiring the analyst to engage in considerable interpretive work to make sense of the discourse, and must learn to identify the “relatively subtle mechanisms and devices” that are present in mediated news texts. This is the crux of this paper from a methodological perspective: Developing a “Discursive Scaffold,” this paper seeks to examine the dialectical relationship between these frames, frame categories, and the ideological presumptions that they rest upon and reinforce. Comprehensive discourse analysis rests upon a variety of techniques, from framing analysis, source analysis, to meticulous fine-grained textual analysis.

We present a comprehensive fine-grained analysis with a particular emphasis upon framing, details of which are compiled and presented in Figure 4. This table gives an insight into framing, demonstrating its comprehensive and intricate nature. Entman’s (1993) seminal work on framing states that it “promotes a particular problem definition, causal interpretation, moral evaluation, and/or treatment recommendation” which serves to determine how audiences likely think about and categorize news information they’re processing: our analysis seeks to build upon that premise.

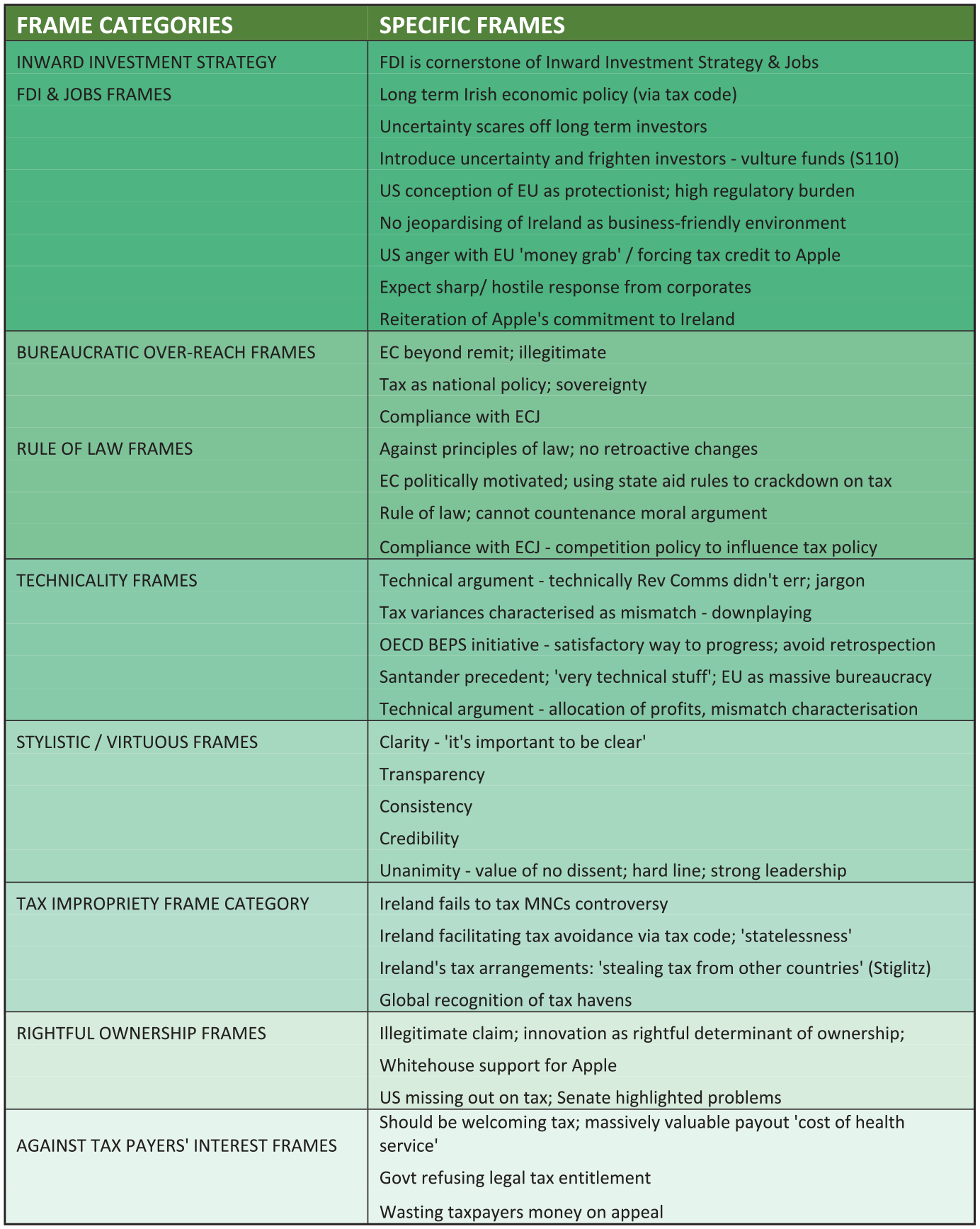

When media coverage is comprehensive, as in this study, frames can be very extensive and complex within the text and so can themselves be further classified into frame categories. Examination of these frame categories show that their content is less nuanced and tends to find parallels within news media coverage more generally. For example, our analysis identifies some broad frame categories such as “bureaucratic overreach,” “diminishing public trust,” and the “importance of foreign direct investment,” which, although characteristic of this discourse on corporate taxation, are typical features of mainstream mediated news discourse more generally. This helps us to step up from the particulars of this specific discourse analysis and recognize the parallels that are present in media coverage that is evident. Building further upon this examination allows us to identify and classify broader ideological presuppositions or discursive formations that are present within discourse, thus demonstrating the scaffolding nature of our analysis. These often serve as an ideological shortcut for broadcasters and journalists when assembling a discussion and are based upon relatively uncontested constructs, such as “a public intolerance of corporate tax avoidance” in the United Kingdom context versus a “general acceptance of low corporate tax rates” in Ireland, that help to reveal the ideological underpinnings of economic policy within the respective jurisdictions. Figure 1, entitled “The Discursive Scaffold” illustrates our argument.

The discursive scaffold.

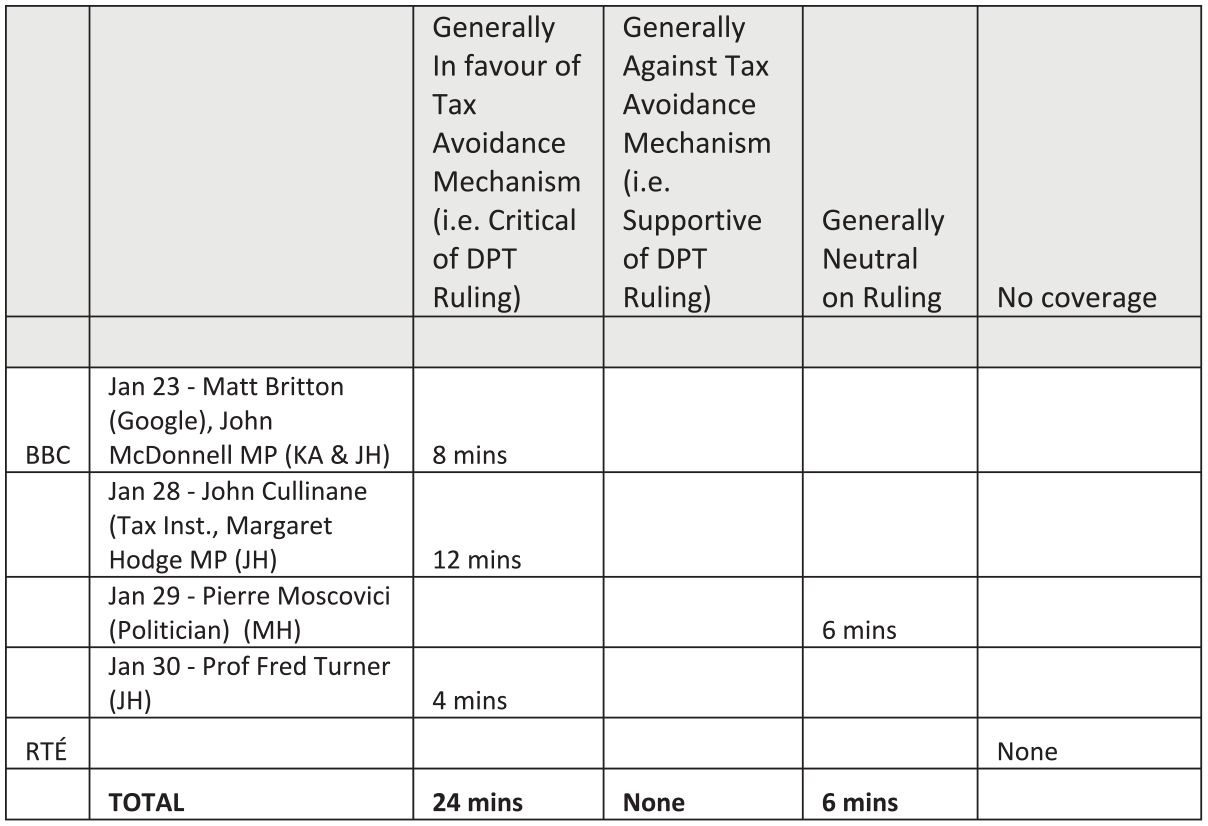

Both tax rulings offer interesting perspectives on the interaction between business and the state in their surrounding discourses. DPT, sometimes referred to as “Google Tax” was introduced as an anti-tax avoidance provision to prevent the diversion of profits to other regions with lower tax rates. It was introduced in advance of the OECD’s BEPS initiative which sought to implement a similar cooperative mechanism across states to prevent profit shifting for the purposes of tax avoidance. In spite of the stated attempts of the DPT initiative, the ruling in Britain received criticism from many quarters: those who opposed any state intervention in global trade, and those who felt that this particular intervention on behalf of the state was inadequate to ensure appropriate levels of corporate taxation. In the European case, the Commission’s ruling regarding Apple and Ireland deemed that the Irish state had granted illegal tax benefits to Apple, which the Commission considered breached EU competition rules against state aid: in effect, these two cases are instances of state intervention, but with different targets. Much of the criticism of the EC ruling came from those who felt that member states like Ireland should retain tax sovereignty to facilitate free international competition and trade, even if that meant corporates using tax avoidance mechanisms; whereas support for the ruling tended to come from those who oppose corporate tax avoidance and the means to expedite it. The following two charts represent an overview of all of the coverage of the two rulings in both media, beginning with DPT. Figure 2 is based upon a general content analysis and shows that the vast majority of the BBC coverage was critical of the DPT ruling and special corporate tax arrangements with individual companies generally. Although RTÉ covered the issue of corporate tax avoidance obliquely, it did not cover this ruling specifically during its news cycle.

Coverage of DPT ruling.

Following the announcement by the Office of the Chancellor of the Exchequer in relation to the Google deal, on January 22nd, 2016, we looked at the coverage on the Today program on the subsequent days. This research is exhaustive in that we examined all of the broadcast data that existed from the shows during the 2-week timeframe surrounding the announcements. On BBC, there was a total of five features that covered the topic, four of which were feature interviews and the last formed part of a news roundup. RTÉ’s archive was examined for the same period and intriguingly affords the Google DPT deal almost no coverage. Interestingly, the broadcaster manages to cover the issue of tax avoidance in general terms without mentioning the Google arrangement with the U.K. Chancellor and HMRC. During the period between January 22nd and February 10th there are four pieces of coverage which feature the issue of tax avoidance, but they specifically avoid reference to the U.K. case. This lack of coverage by RTÉ of the Google tax deal is interesting because while the broadcaster is clearly interested in reporting issues relating to tax avoidance, it has entirely overlooked the real live case of its nearest neighbor, suggesting a degree of textual absence (Huckin, 2002) on the subject, by its failure to pay any attention to the specifics and implications of the Google DPT case in the neighboring jurisdiction. While we recognize the difficulty in determining the exact nature of discursive silence, we must wonder at the missed opportunity by RTÉ to widen the parameters of its debate.

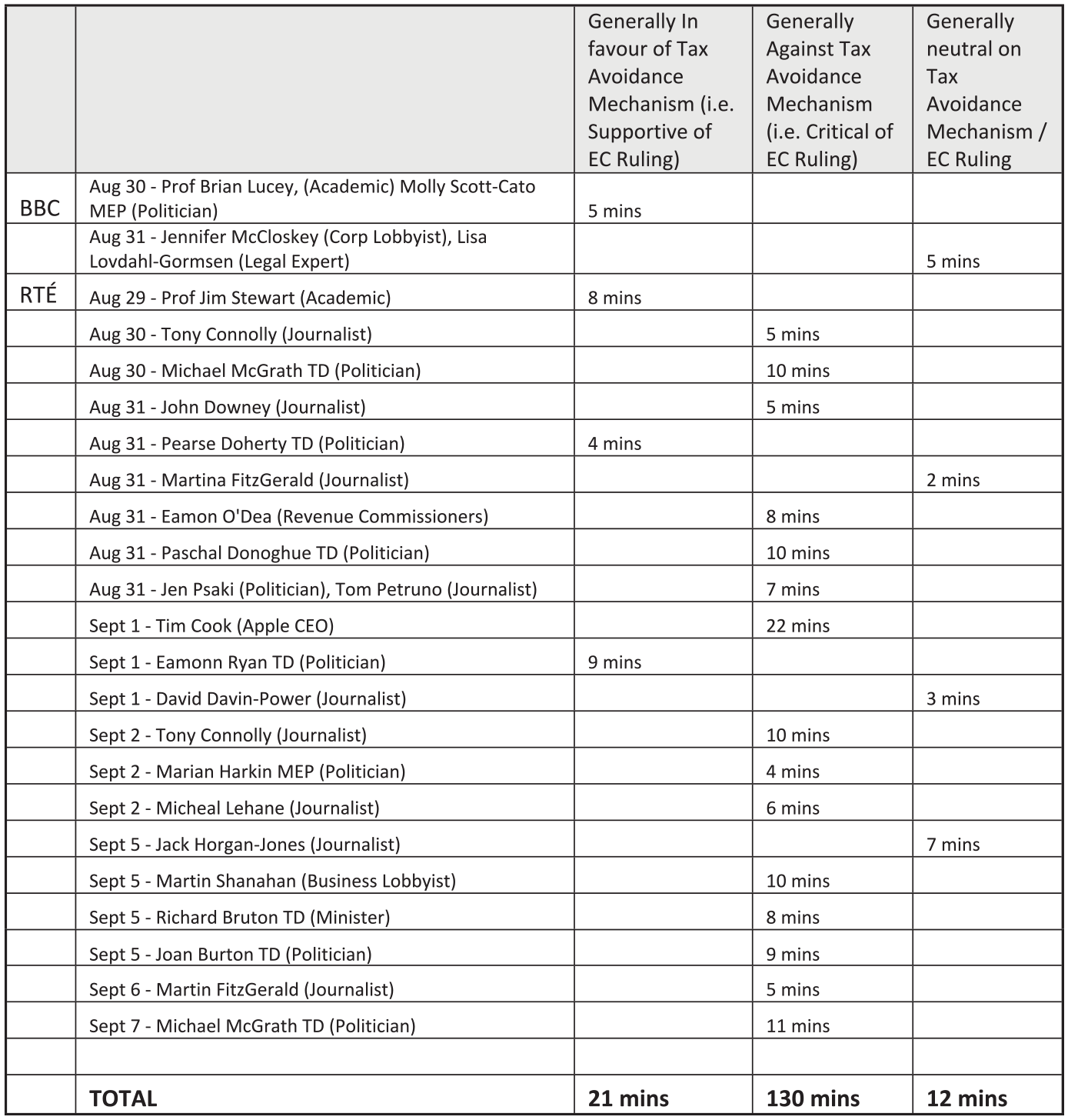

In the same way, we examined the period of coverage surrounding the Apple Ruling by the European Commission. While the issue was featured by the BBC Today program, that coverage pales by comparison with RTÉ’s exposure of the same topic (see Figure 3, above). BBC carried two features on the ruling: on August 30th and August 31st, whereas RTÉ’s coverage ran to 21 separate features, in addition to substantial straight new pieces. By comparison, RTÉ’s coverage on the ruling ran from August 29th to September 7th, involving primarily politicians, both government and opposition and journalists and political correspondents (see figure above).

Coverage of European Commission’s ruling on Apple.

Examination of the two corpuses revealed some interesting patterns in the data. As a fundamental analytical foundation, all of the features were categorized into three elementary classifications regarding their position on tax avoidance mechanisms given their impact upon the mobility of global trade. These classifications were: “Generally critical of Corporate Tax Avoidance and special tax arrangements” which captured those critical of corporate tax avoidance; “Generally supportive of Corporate Tax Avoidance and special tax arrangements,” which broadly encapsulated those arguments in favor of unrestricted trade and the use of tax to inhibit it; and “Generally Neutral on Corporate Tax Avoidance and special tax arrangements.” These classifications were also chosen as a means of categorization because they are broadly comparable and thus could span the nuances of both rulings and their respective coverage. Broadly, none of the BBC’s features is classified as “Generally Supportive of the DPT Ruling”—criticism of the ruling was widespread—views expressed and aired were generally in favor of mechanisms designed to inhibit profit shifting and necessitate the payment of corporate tax. One of the four BBC broadcasts was classified as having neutral or balanced coverage of the ruling. As indicated, RTÉ did not provide any specific coverage of the British DPT Ruling.

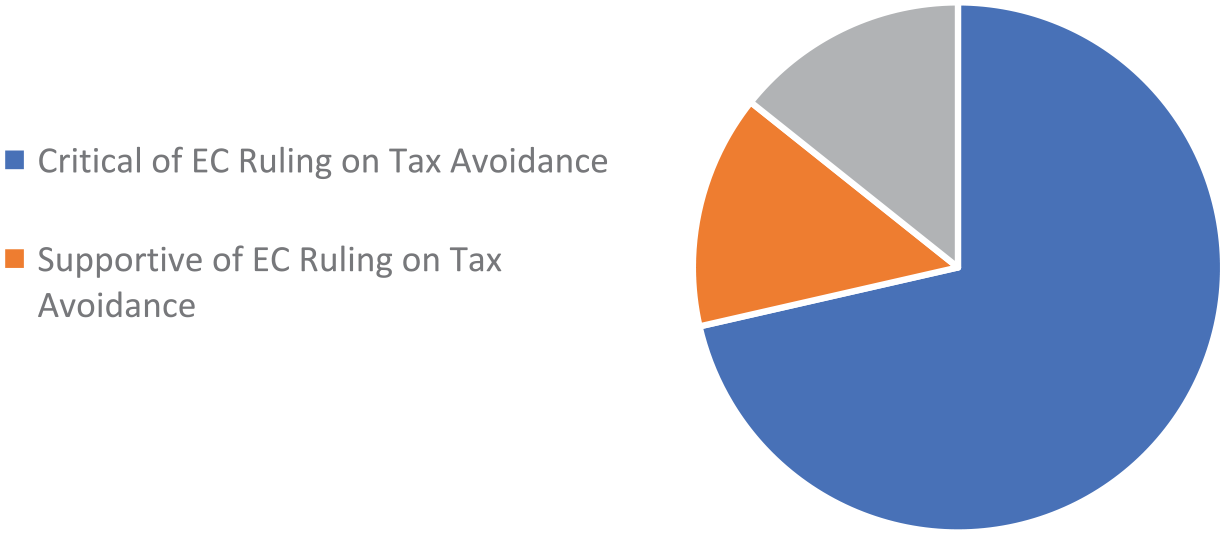

Coverage of the Apple Ruling was extensive from RTÉ. BBC broadcast two relatively short features on the subject, one broadly critical of tax avoidance and the other fairly balanced. RTÉ’s coverage ran to 21 features over 10 days, predominantly with politicians and journalists, including their own political correspondents. The vast majority of the broadcaster’s coverage was classified as “Generally Critical of EC Ruling on Apple,” and the mechanisms directed toward global corporates who seek to avoid taxation, depicted in Figure 4 below. In total, 15 of the 21 features were critical of the EC ruling, whereas only three were supportive of it and three more categorized as neutral on the subject. Of the 163 min of RTÉ coverage on the ruling, a considerable 130 min were critical of the EC’s position while only 21 min were broadly classified as supportive of the EC’s attempts to curtail global corporate tax avoidance. Further analysis revealed the nature of the criticism of the European Commission’s decision and this can be viewed in greater detail below and in the following tables classifying frames and frame categories that imbued the discourse.

RTÉ coverage of Commission’s Ruling on Apple.

A key finding is that these discourses are deeply imbued with ideological presuppositions surrounding the controversial subject, which are often latent rather than clearly manifest in the discourse, consistent with the controversial nature of taxation generally. The analysis reveals a critique within BBC coverage of complex corporate tax arrangements of MNEs that includes “lack of tolerance” and “collective mistrust” of such activities. Contrasting with RTÉ’s reportage which suggests a greater degree of acceptance of the complex accounting arrangements that facilitate low taxes by international corporations and a resignation to the political and economic implications of such practices. These ideological presuppositions, it is argued, are characteristic of the respective jurisdictions and are reproduced and reiterated in the discourse.

This finding is indicative of the nature of economic development in Ireland, which has for decades relied upon foreign direct investment and a degree of dependency upon global finance flows within the world economy (O’Hearn, 2001). The historical context of the nature of the political economy between Britain and Ireland cannot be overlooked. British economic development has, by contrast, been very different: dependent upon its empire, and the legacy of that empire and its role in the establishment of British-led Atlantic economy has meant that Britain has played much more dominant economic role historically (Beatty et al., 2016). Unlike in Ireland, which seems to recognize its dependency upon foreign capital, British reportage reflects a more complex and comprehensive economic discourse recognizing the role of the domestic economy and the implications thereupon of offering low taxation rates to global corporations. The jeopardy that this places upon small, locally-owned businesses through their inability to compete, is recognized and discussed, and in so doing, makes manifest a more integral and deep-seated economic ideology.

The table above (Figure 5) charts the frames and broader frame categories that dominate RTÉ’s coverage of the EC Ruling, in descending order. Our analysis groups the specific frames (those particular to this discourse on corporate taxation) into broader frame categories. This assists us in identifying parallels in coverage between this discourse and other discourses concerning economic issues. By far, the most dominant frames were those pertaining to the maintenance of inward investment strategy, supporting foreign direct investment and jobs. The other key concern that features throughout the discourse manifests as a concern for the importance of the rule of law and that the EC’s intervention amounts to bureaucratic overreach, consistent with previous findings (Graham & O’Rourke, 2019). While the overarching analysis demonstrates clear bias in RTÉ’s coverage, it is by examining how these frames manifest that one can determine their ideological tendencies. Repeatedly, speakers refer to jobs as a well-worn tool to highlight to audiences that their own economic wellbeing depends upon their support for inward-investment based strategies. Similarly, references to bureaucracy and bureaucratic overreach are connoted negatively rather than depicted as a necessary state intervention in protection of its citizens. These types of ideological premises, imbued throughout the discourse, serve as shortcuts for broadcasters and journalists to communicate subtly with audiences without making that ideology clearly manifest.

Frame categories and frames of RTÉ discourses.

Another prominent theme to emerge from the analysis of the discourse is that of technicality. In numerous interviews various forms of this frame emerged, oftentimes characterizing the “tax variances” as a “mismatch.” This very much underplays the vast sums of unpaid tax that the EC’s ruling stipulates. This was offered by way of justification of the Revenue Commissioners’ role in executing the alleged “sweetheart deal” that Apple was found to have received. RTÉ’s Tony Connolly, reporting upon this and similar EU tax cases describes it as “very technical stuff”: This type of frame often dissuade audiences, discouraging them from becoming too interested in an intricate topic or expecting to understand its complexities.

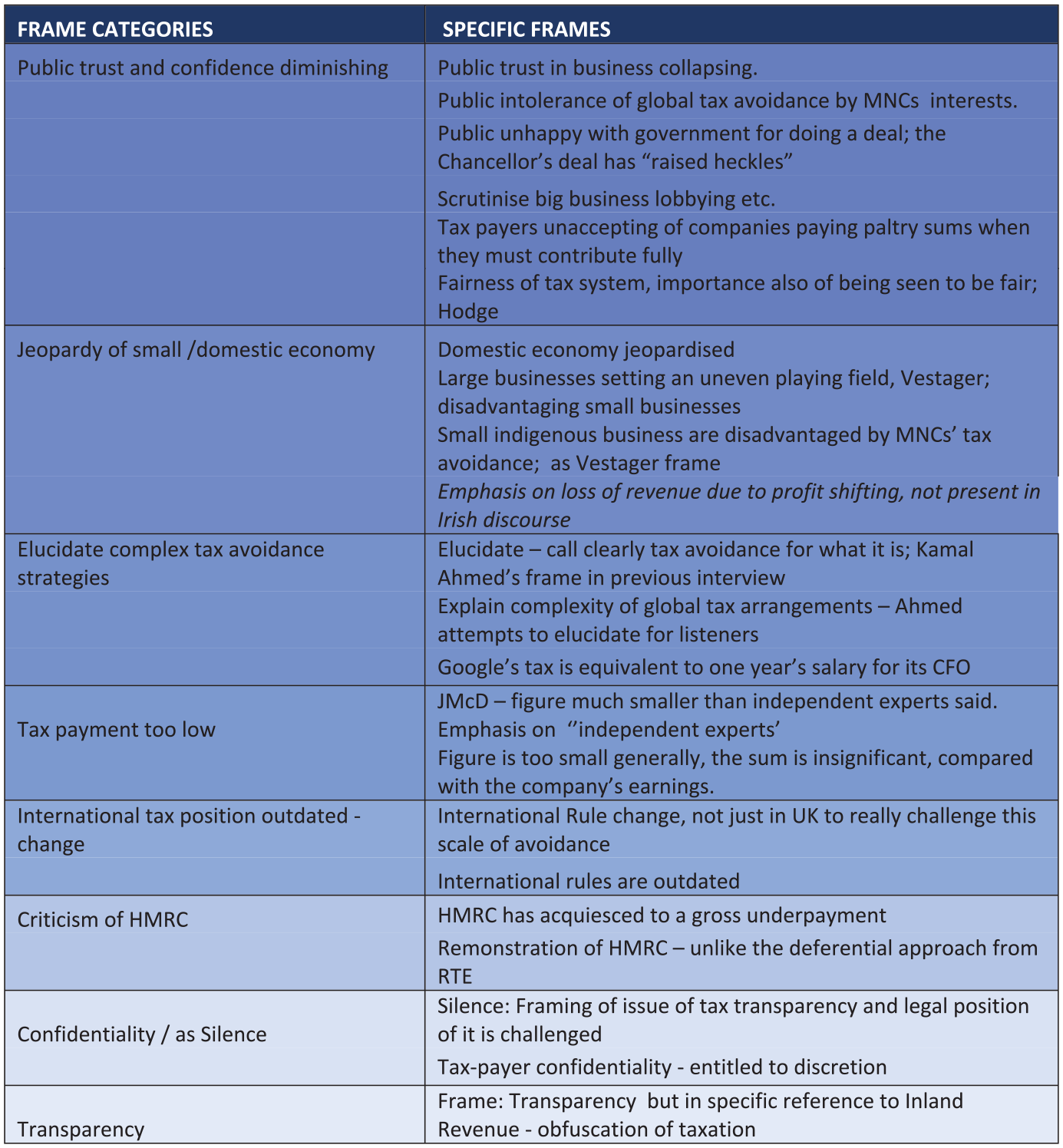

The table above (Figure 6) outlines the BBC’s coverage depicting the specific frames and broader frame categories in that reportage. Undoubtedly, the most dominant theme to emerge from the analysis is that of “diminishing public trust and confidence.” Various detailed frames were contained within concerning: the collapse in public trust of business; distrust of the government; intolerance of tax avoidance by large multinationals; and general discontent within the fairness of a tax system that favors global corporations over smaller businesses and citizens.

Frame categories and frames of BBC discourses.

When we compare both corpuses, we see that this dominant theme of distrust from the U.K. discourse really does not feature strongly in the Irish discourse: where tax impropriety does feature, it does so mainly within the context of “Ireland as a tax haven,” “stealing tax from other countries.” This notion of stealing tax certainly does not feature within the BBC’s discourse.

The other key theme to arise from the BBC analysis is that of jeopardy of the domestic economy. Recognition of the disadvantages faced by smaller, indigenous businesses in the “uneven playing field” created by multinational tax avoidance was mentioned by numerous key speakers, including Commissioner Vestager herself and was emphasized in the United Kingdom discourse. There was no equivalent within the RTÉ discourse: a domestic Irish economy simply did not feature in the extensive debate. This is indicative of Ireland’s reliance upon inward investment for economic development and the corresponding disregard in policy terms for the so-called indigenous economy.

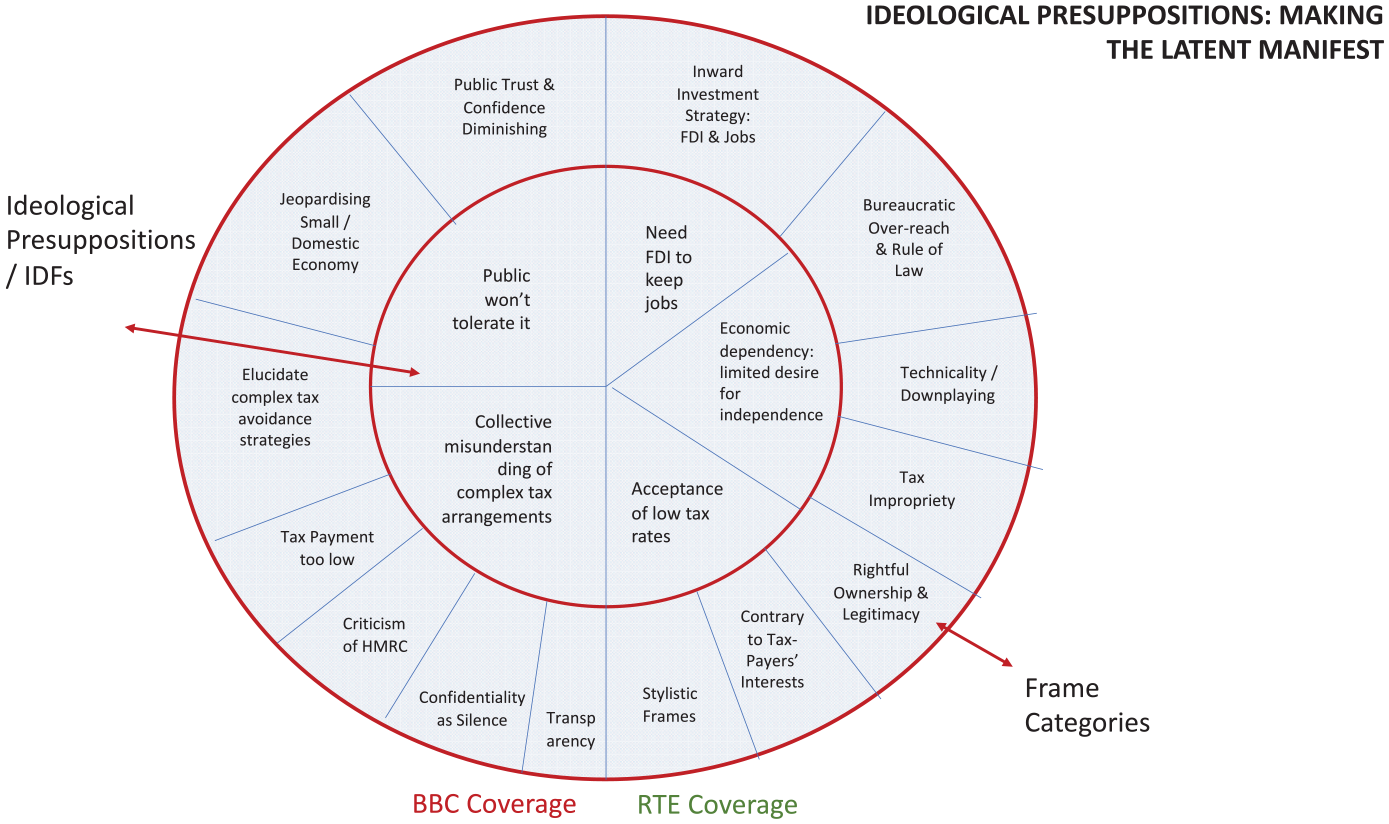

Further analysis sought to illuminate the more deeply embedded aspects of ideology within the discourse that are indicative of the nature of that discourse generally. Our discursive scaffold builds upon the frames and frame categories to endeavour to recognize the key ideological presuppositions imbuing the discourse. The BBC discussion had two key premises: (a) public intolerance and (b) collective misunderstanding of tax avoidance mechanisms; in the RTÉ discourse they were three key ideological presuppositions, the most dominant presupposition is that (a) Ireland is dependent upon Inward Investment (FDI) for employment; (b) Ireland is economically dependent on global trade flows; and (c) acceptance of low tax rates generally. These foundational premises can be said to provide the “tacitly agreed” basis of the discussion, providing a relatively uncontested base upon which the discourse builds. In the Irish context, we find that the discourse is comprised of characteristic neoliberal constructs: the need for free trade and FDI to keep jobs; and a general acceptance of low corporate tax rates. A more nuanced third presupposition, that of dependency on the world economic system is indicative of Ireland’s complex economic history and recognizes Ireland’s place in a world system dependent upon global trade.

By contrast, BBC discourse builds upon the generally accepted assumption of “public intolerance” for tax avoidance and its various manifestations. This foundational premise underpinning BBC discourse correlates with the other key premise of “collective misunderstanding of complex tax arrangements.” Taking both premises together, we can infer that the tax avoidance strategies pursued by global corporates are perceived within British discourse to be contrived and mendacious and this reinforces the public’s misgivings about them. From an ideological perspective, this suggests a general suspicion of both politics and politicians. Figure 7 illustrates this:

Ideological presuppositions.

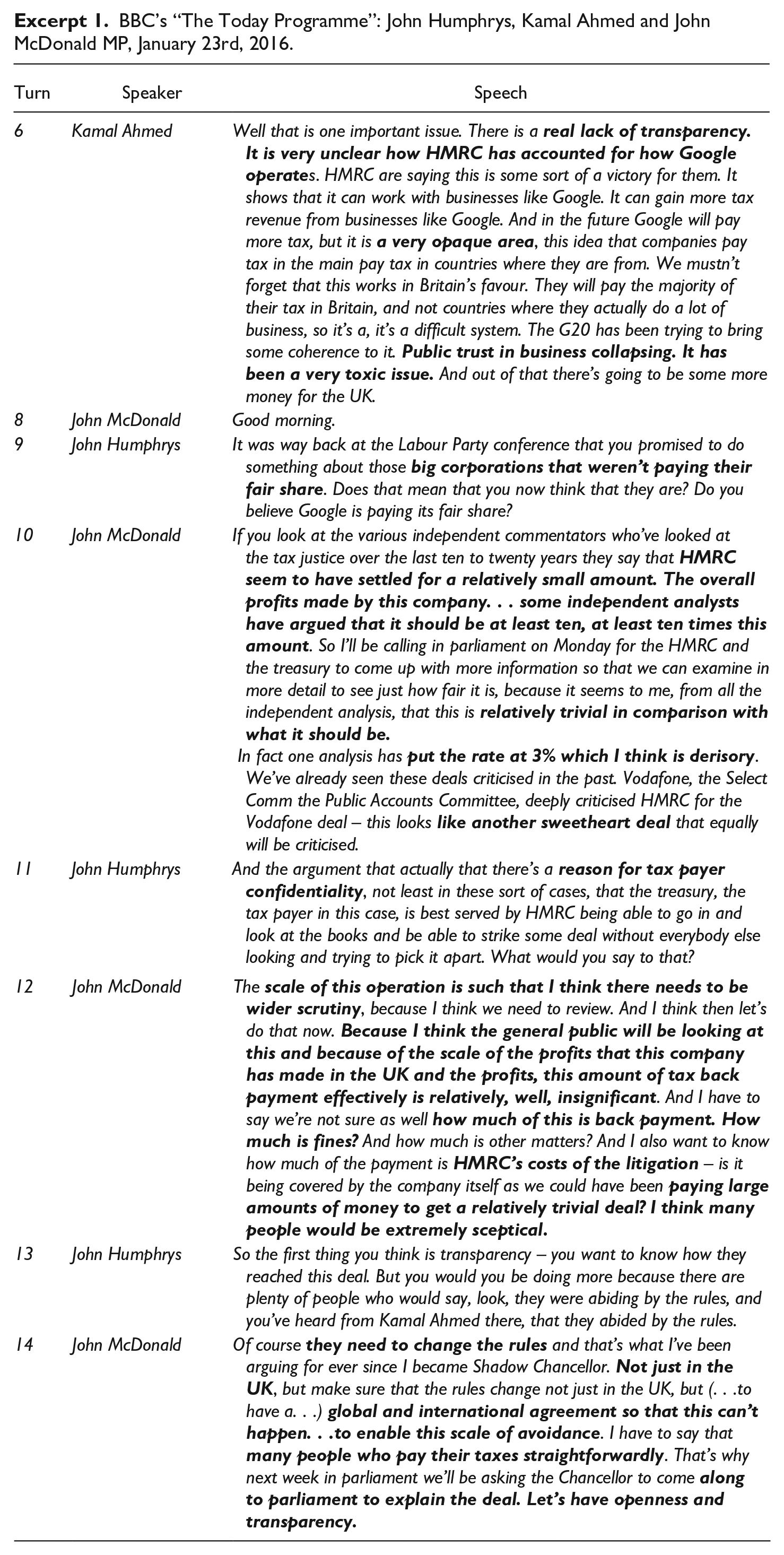

These two ideological presuppositions within the BBC coverage imbue the various debates and are consistent threads underpinning the discourse. The first premise is perhaps the most clear and revealing and resides in the idea that the public are fundamentally unhappy with the tax arrangements of global MNCs and are not willing to support it as a political position. This is articulated in statements such as “big businesses are not paying their fair share” and Economics Editor Kamal Ahmed’s observation that this is a “very toxic issue” with a “real lack of transparency.” Moreover, speakers recognize that the public won’t tolerate such “sweetheart deals” made by politicians undermining of public trust in business who do “not paying their fair share” of taxation, which is especially intolerable to a public who pay their own taxes fully (Excerpt 1).

BBC’s “The Today Programme”: John Humphrys, Kamal Ahmed and John McDonald MP, January 23rd, 2016.

The second premise of the BBC coverage is (b) that there is a recognition of a collective misunderstanding of such complex tax arrangements by the general public. Humphrys’ references continually throughout the interview that companies have been using “smoke and mirrors to pay less tax.” Ahmed dwells at the beginning of the interview to explain and contextualize the Google payment which he highlights is “less than they pay per year to their Chief Financial Officer.”

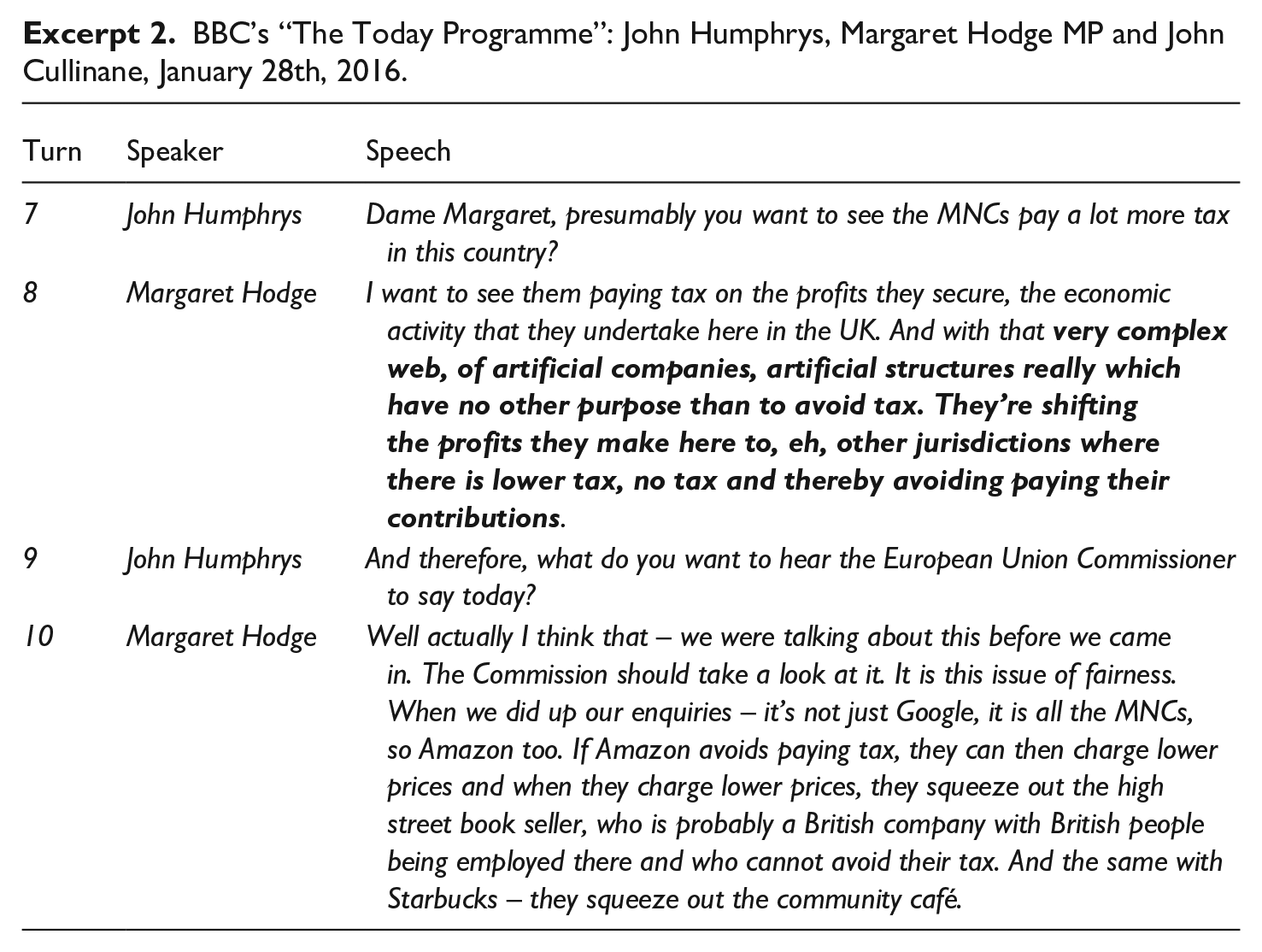

This is further illustrated by the interview with former PAC Chairperson Hodge in which she refers to the “very complex web, of artificial companies, artificial structures really which have no other purpose than to avoid tax.” She’s elucidating the convoluted nature of contemporary tax practices, designed to facilitate global corporate tax avoidance while at the same time remaining impenetrable to the public generally, and thus above public scrutiny: Hodge, however, is intent on explicating them and illuminating them within the discourse, noting that the British public won’t tolerate the unfairness of such practices, which allow different tax rules for different companies. She highlights the injustice of profit shifting which allows international companies to “avoid paying their contributions” while pointing out the potential harmful consequences for the domestic economy when smaller British companies, such as the “high street book seller, who is probably a British company with British people being employed there and who cannot avoid their tax. . . squeezed out by Amazon” who can undermine competition by cutting prices while avoiding paying their taxes in the United Kingdom (Excerpt 2).

BBC’s “The Today Programme”: John Humphrys, Margaret Hodge MP and John Cullinane, January 28th, 2016.

From the RTÉ corpus, three key ideological presuppositions form the foundation of the discourse: the most dominant presupposition is that (a) Ireland is dependent upon Inward Investment (FDI) for employment; (b) Ireland is economically dependent with limited desire for independence; and (c) acceptance of low tax rates.

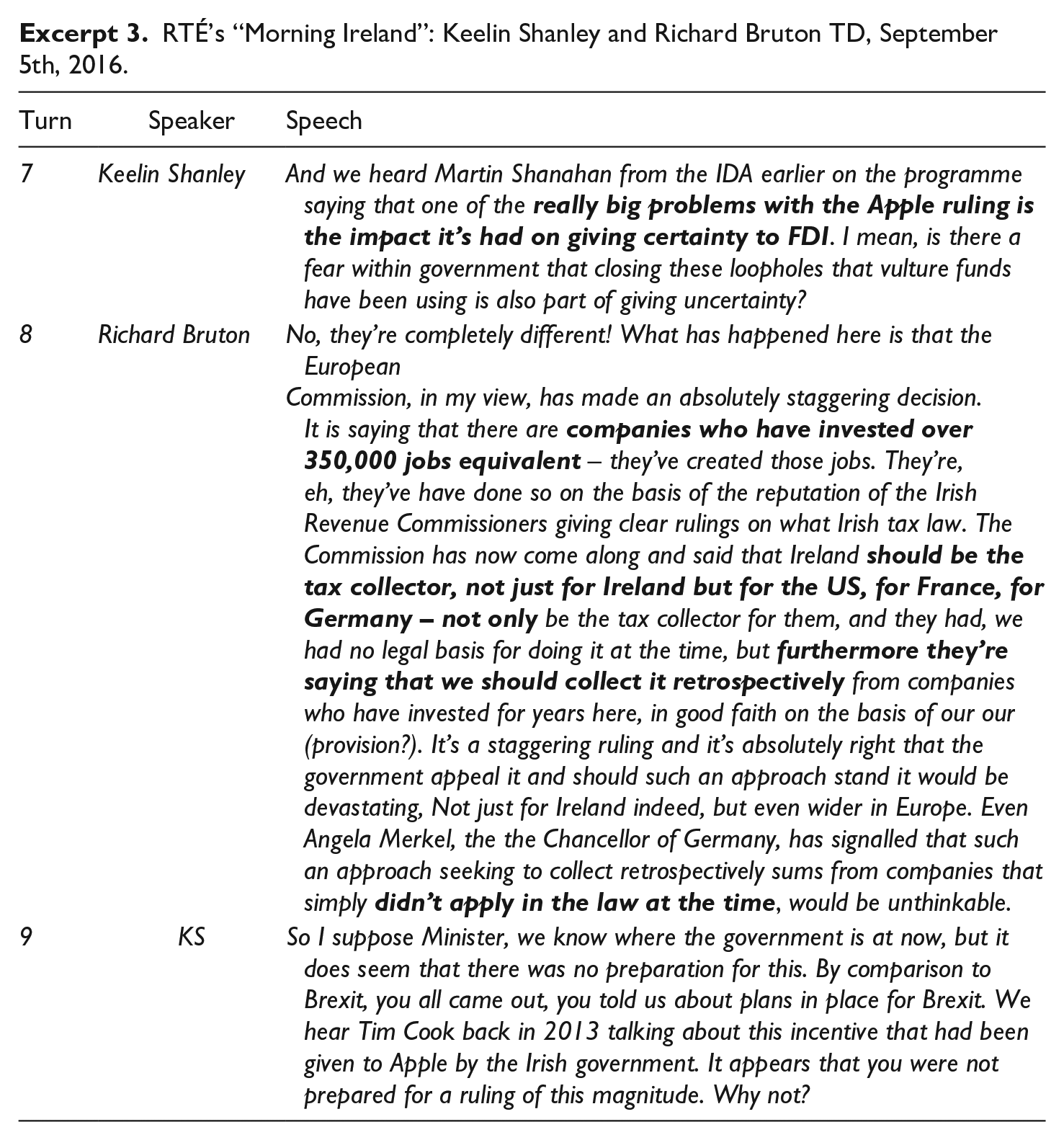

The first presupposition reinforcing the widely held premise is that Ireland needs to maintain FDI in order to keep jobs. Little discussion permeates beyond the mantra of what “jobs” mean—such as their quantity, their nature, and how much value they contribute economically. Inherent to this premise is the omniscient presumption that Ireland depends on foreign investment: any criticism of foreign investment may jeopardize it and in turn jeopardize jobs—this is an oft-used trope in Irish media that immediately resonates with listening audiences by communicating potentially abstract economic policy decisions at a level they can certainly relate to. RTÉ’s Keelin Shanley’s interview with Minister Richard Bruton reinforces the government’s position on FDI indicating that the EC’s decision impacts upon the “companies who have invested over 350,000 jobs equivalent” did so based upon the reputation of the Irish Revenue Commissioners “clear rulings on Irish tax law” which prohibits retrospective collection “from companies who have invested here for years in good faith.” (Excerpt 3)

RTÉ’s “Morning Ireland”: Keelin Shanley and Richard Bruton TD, September 5th, 2016.

The second presupposition that emerges from the RTÉ discourse is that (b) Ireland is economically dependent with limited desire for independence. This concerns Ireland’s acknowledgement of its place in the global economic system, that it is aware and defensive of its dependent role with little desire for autonomy (with the notable exception of its tax sovereignty). There is a general recognition pervading the discourse that Ireland recognizes its role as providing low rates of corporation tax to foreign-owned businesses to encourage them to locate in the country: conversely, what is absent is any real sense of a domestic economy, which features distinctly in the United Kingdom discourse.

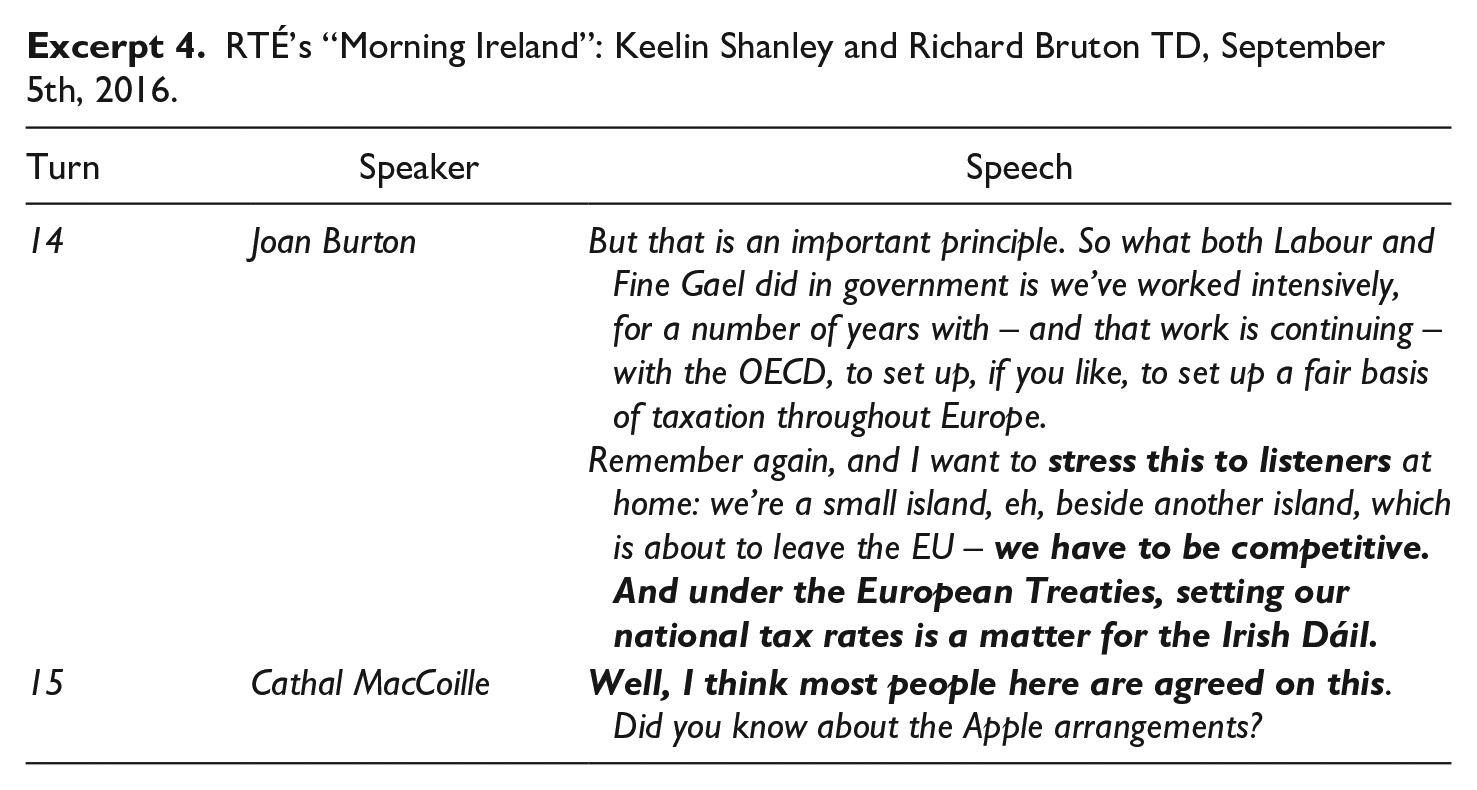

The third key premise surrounds (c) acceptance of low tax rates, in relation to Corporate Income Tax (CIT). The extent to which the public is aware of and arguably has internalized the corporation tax rate and its significance is telling in this regard: It is omnipresent in the discourse and continuously reinforced. Contrary to other rates of taxation such as personal PAYE income tax, CIT in Ireland is particularly low, and Jim Stewart points out the discrepancy between the headline rate of 12.5% and the lower still “effective rate.” In the discourse, this is largely unquestioned. Even on the left of the political spectrum, both Sinn Féin and the Trotskyite People Before Profit Alliance have conceded that they would settle for a “minimum effective rate of 12.5%” (People Before Profit Alliance, 2018); improbable in other European member states. The interview between journalist Cathal MacCoille and then Labour Leader Joan Burton illustrates the extent to which acceptance of low tax rates imbues the discourse. MacCoille’s response to Burton’s call for the need to remain competitive—a euphemism for maintaining low CIT rates—is “I think most people are in agreement here.” What might be dismissed as a seemingly innocuous statement actually reveals a lot: namely, the extent to which media actors have accepted Ireland’s corporate tax position: not only does MacCoille not question Burton as to what she understands “competitive” to be, he decides that their listening audience, referred to as “most people here,” agree, implying that dissent from this view is a marginalized position. This deep ideological premise is assumed, and reinforced with ease, using what Schegloff terms “establishing common ground”—a key observable feature of talk-in interaction which confirms agreement between speakers and suggests an amenable audience (Schegloff, 2006) (Excerpt 4).

RTÉ’s “Morning Ireland”: Keelin Shanley and Richard Bruton TD, September 5th, 2016.

By examining two corpuses from two different but comparable media organizations we develop a broader understanding of which ideological premises features within a particular discourse and which do not: this juxtaposition of two data sets is an important value of using comparative analysis. The key presuppositions that were present in the respective discourses were not a feature of the other discourse, therefore we can posit that they are ideologically characteristic of the respective jurisdictions. That is to say that public intolerance of tax avoidance was not a premise of the RTÉ discourse; neither was there reference to the Irish public’s incomprehension of the complex tax arrangements of global corporates: these were key premises of the BBC coverage. Likewise, BBC coverage did not build upon the premise of dependence upon foreign direct investment: arguably Britain constructs itself as an economic powerhouse and thus does not discursively dwell on its dependence upon receipt of international finance flows for economic prosperity, thus demonstrating the impact of economic history within different temporal contexts. A key distinction in ideological premises between the two corpuses is the discursive recognition in RTÉ’s coverage that low tax rates are accepted for MNEs; whereas, in the BBC’s discourse, this is undoubtedly not the case. These ideological presuppositions identified here form the basis of the discursive interplay on the issue of corporate tax in Ireland and the United Kingdom.

Discussion and Conclusions

A strong feature throughout the BBC discourse was that of collective misunderstanding and mistrust of the tax avoidance mechanisms that global corporates are using, which wasn’t evident in the RTÉ discourse. Based upon the Public Accounts Committee’s findings (UK House of Commons Committee of Public Accounts, 2013, 2015a, 2015b, 2015c) regarding the “tax avoidance industry” (Sikka, 2015) perhaps there is a clearer recognition, politically, of what global corporations are attempting to achieve with these artificial mechanisms, as well as a collective distrust and intolerance among the public for such artificial measures that contravene the principles of tax fairness by allowing global companies to reduce their tax burden when ordinary citizens and small local businesses cannot. The corporation tax crisis is thus constructed in the United Kingdom media as one of public intolerance of tax injustice and the illegitimacy of corporate and government behavior. This stands in contrast to the key discursive premise underpinning discourse on corporate taxation in Ireland surrounding the construction within the media of the economy’s dependence on Foreign Direct Investment (Graham & O’Rourke, 2019). This dominant discursive formation gives rise to the sub-formation surrounding the dependence on FDI for jobs; and while a broader discourse surrounding the best way for a small country like Ireland to be globally economically involved, this emphasis upon employment tends to serve as a handy shortcut for the media to remind audiences that their very jobs may depend on keeping corporate taxes low. In essence, rather than have a deeper, more involved discussion about what Ireland’s role in the global business environment should be and whether the country wishes to facilitate extreme market-liberal practices by offering tax concessions to big business, the Irish radio discourse confines itself to the dependence of jobs on FDI and in turn on a low corporate tax rate.

The seeming importance of the U.K.’s parliamentary committee in influencing the discourse is perhaps worthy of further investigation. Ireland with its similar parliamentary structure has its own Public Accounts Committee, which at times has played important roles in public discourse (e.g., on deposit interest taxation evasion scandal (O’Regan, 2010)). Whereas Ireland’s constitution constrains the work of such parliamentary committees (O’Leary, 2014), the constraint largely concerns the issue of personal culpability and has allowed such committees to influence media discussion of issues as the banking crisis of 2009. Yet there was no evidence in our data of parliamentary influence on the construction of the corporate taxation in Irish public discourse.

Our analysis shows a difference too in the construction of national independence in the media of the United Kingdom and Ireland. The Irish discourse constructs the EU as a threat to its tax sovereignty with the discourse accepting Ireland’s dependence on the world system, and arguably attempting to determine the terms on which it accepts the dominion of world tax competition. Somewhat paradoxically however, given the advent of Brexit, discourse within the U.K. had recognized and called for European intervention in these very instances of tax avoidance and the U.K.’s discourse, by contrast, seems to expect its state to make stronger demands of multinational companies. This may be attributable to a legacy of Britain’s historic influence upon global trade; or it may be a function of the majority-party system of politics in which the left of the Labour Party has, in recent years, become influential, and may explain the push for additional state involvement which is evident from the BBC discourse. Ireland in contrast, seems caught too in its traditional economic policy path of lower taxes. Both the discourses in the United Kingdom and Ireland then seem captured in the face of the present crisis of corporation taxation by reflections on past crisis and the way it is imagined that those were solved (O’Rourke & Hogan, 2013). Moreover, this contemporary time period characterized by the digitization of global capitalism has effectively consolidated power within these asset-rich, highly mobile ICT industries as they continue to serve as the nervous system of global finance flows (Hope, 2009).

Regarding the genre of political radio interviewing, it is worth noting that the two broadcasting institutions use different interactional practices (Schegloff, 2006)—RTÉ used the head-to-head format while BBC favored mediated, triangulated discussion. Possibly due to the complex and technical nature of this subject, it may be wise to have two experts of opposing positions discuss, with moderation, rather than force generalist journalists to challenge experts on issues in which they are not schooled. This arguably places the journalist at a disadvantage in a head-to-head scenario, researchers notwithstanding, and they might be better suited to moderating conversations between experts from opposing points of view than poke holes in the arguments of experts themselves.

While there are differences in the ideological presuppositions of the discourses between Ireland and the United Kingdom, it is interesting to note that, regardless of those differences, low corporation tax policies persist. Therefore, an inference that may be suggesting itself pertains to the malleability and pragmatism of neoliberalism, or market-orthodoxy, as an ideology, in that such policies of low taxation can be enacted in historically and contemporaneously different economic environments. In essence, while Ireland and Britain have come to their low tax strategies in very different ways, and at different times, the premise holds that such neoliberal tenets operate with pragmatism and seem able to readily attach themselves to many different economic and ideological scenarios. In the current context of crisis, the sustainability of such policies may be questionable.

Throughout this study, we have developed our understanding of ideological presuppositions as the codified tropes that imbue discussions of higher-level subjects making them relatable to wider audiences. When subjects such as corporate taxation enters into the public sphere, it is typically through mediated discussion, which of necessity must consider its audience and their capacity to engage with and decipher its coverage, and methodologies like CDA with a critical capacity are vital. Therefore, the content must be relevant, and will of course be different to the nature of corporate tax discussion that may exist between, for example, corporate tax lawyers or academic economists, whose understanding of the intricacies of the subject would make such dialogue obscure to non-specialist audiences. Mediated discussion considers its audience; and broadcasts become distillations of more profound treatments—in effect, the journalists and presenters decipher and digest higher level discussions and regurgitate them for more accessible content, but CDA provides us with the tools to deconstruct that. Questions of corporation tax become parsed as foreign investment, jobs, and bureaucracy, for ease of absorption by the audience.

This study finds that crisis is not a natural phenomenon but one which has been created by state actors and exacerbated by non-state actors: both multinational companies assisted by a tax avoidance industry (Sikka, 2015) and media in their respective ways. Drawing from a constructivist perspective, we can infer that the media plays a significant role in the existence and development of crisis: the narratives it constructs can either permit and encourage practices of corporate tax avoidance or they can admonish and rebuke them. This study sees evidence of both, in different jurisdictions. Having examined both U.K. and Irish media coverage of corporate tax, this study finds that U.K. media is much more critical of the crisis situation of surrounding corporate tax avoidance and the ensuing problems it presents for states, whereas Irish media narratives are less inclined to challenge tax corporate tax avoidance and instead frame in a positive economic light.

Moreover, the Covid crisis has demonstrated the vulnerabilities of industries large and small and has prompted the intervention of governments to alleviate many of the difficulties, both economically and socially, that it has created. Interestingly, while some powerful corporate interests, from airlines to retail giants, have suffered significant losses, tech giants like Apple, Amazon, Google, and Microsoft have flourished in the increased demand for digitization as the forced closure of tangible economic activity obliged people to turn to online activity instead and accelerated the pace at which the virtual achieves domination. This of course has the potential to exacerbate the taxation crisis even further as increased digitization further mobilizes assets. Recent efforts by the OECD to introduce a minimum tax rate on corporate profits has failed to be ratified by Ireland (Reuters, 2021) emphasizing the country’s outlier status.

Finally, should the tax amnesty proposed by the Biden administration bear fruit, it may pose the questions: Has the Covid crisis brought about a shift toward an interventionist Neo-Keynesianism approach to economic policy making necessary to revitalize economies? If so, does that pose a challenge to the dominance of neoliberalism over the last four decades? Has the pandemic done what the financial crash did not? Or will neoliberalism bounce back from this crisis, like every other it’s faced in the last 40 years?

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.