Abstract

The strategic role of Information and Communication Technologies (ICT) is growing in various companies. Small and Medium Enterprises (SMEs) adopt ICT solutions to support their processes and to improve their products and services. Because of SMEs' scarce resources and inadequate ICT competencies, they need support from ICT suppliers in the ICT adoption process. Little attention has been paid to the business models and strategies of ICT suppliers in the academic and professional literature, and SMEs find it difficult to determine the characteristics of available ICT suppliers and to choose the supplier that best responds to their needs and aims.

The goal of this paper is to provide a detailed picture of the ICT sales channel and its players in the European market. A classification framework is proposed and eleven different business models are identified. The paper is based on a case study methodology that included 53 semi-standardized interviews with CEOs (Chief Executive Officers) and marketing and communications managers at leading European ICT suppliers coupled with the literature review.

1. Introduction

Today, Small and Medium Enterprises (SMEs) recognize the important role that Information and Communication Technologies (ICT) may have in supporting business processes and in the development of products and services.

ICT suppliers can play an important role for SMEs as enablers of ICT adoption and generators of business innovation, but this potentially important role for ICT suppliers is not yet fully exploited in practice.

ICT suppliers, which operate in the ICT sales and distribution channel (e.g., hardware resellers, software houses, system integrators) are facing a period of significant change in their strategies and business models. In the academic and professional literature, three main kinds of ICT suppliers can be identified, depending on their commercial offerings: hardware resellers, software houses and system integrators. However, the authors believe that this classification should be re-considered for several reasons: the growing strategic role of ICTs in supporting business in companies of different sizes and in different industries, the evolution of companies' needs and the development of ICT vendor strategies (e.g., Microsoft, HP, IBM, SAP) that create more complex and continuously evolving ICT business models and strategies among suppliers. It is important for SMEs to choose the right ICT partner with the most suitable characteristics and competencies; a partner that can offer the most appropriate technologies and support during the adoption process. Given these considerations, the goal of this paper is twofold. One aim is to propose a classification framework to analyse the strategic positioning and the competencies of ICT suppliers, and the other aim is to identify the main strategic trends in the European market.

The classification framework, based on an empirical analysis of the European market, could be useful to various players: i) ICT suppliers' top management, in order to define strategic actions more effectively; ii) ICT vendors that exploit ICT suppliers to market their products and services especially to SMEs, in order to recruit and select the most suitable sales channel partners; iii) corporate ICT decision makers (e.g., Chief Technology Officers, Chief Information Officers), in order to help them understand the competencies and the products and services offered by different ICT suppliers so that they may select the most effective external partner for the company.

In order to achieve these goals a case study methodology was used to analyse 53 ICT suppliers operating in the European market.

2. Literature overview

In the last ten years, ICT has become an important element in company processes, in products and services distributed to the market, in enabling strategic and organizational change projects and in the re-definition of business models. ICT is thus a potential source of uniqueness and competitive advantage for companies [1, 2]. Today, ICT managers (referred to as Chief Information Officers in large companies) are more involved in strategic activities aimed at innovating companies' products and services, processes and business models [3, 4].

A direct link between ICT and company performance was established by Powell and Dent-Micallef [5] who found that highly ICT-capable companies (i.e., those that invest heavily in information technology) out-perform competitors that do not invest to the same extent. These results suggest that ICT could offer companies a competitive advantage, allowing them to differentiate themselves in the marketplace.

However, because prior studies focused on large and often diversified companies, it is unclear whether or not these results could be generalized to SMEs [6]. Supposedly, the more flexible managerial capabilities of SMEs dictate the level of success of ICT adoption and the resulting positive effects on financial performance [7].

Many SMEs try to adopt ICT to support their business. On account of their limited resources, ICT adoption in SMEs is different from its adoption in larger businesses [8, 9], [10, 11], [12, 13]. The existing literature documenting some of the drivers and barriers to ICT adoption within SMEs is very extensive [14, 15], [16, 17], [18, 19], [20]. Drivers positively influence ICT adoption, while barriers negatively influence ICT adoption. Drivers and barriers may come from within SMEs or from outside SMEs. Independent, impartial consultants and ICT suppliers are an often-cited source of assistance for SMEs in the ICT adoption process [9, 19], [21]. Despite the number of studies available however, there are only a few that consider strategies to guide SMEs in the ICT adoption process.

Focusing on the literature on ICT suppliers, it is evident that they can be a source of important ICT capabilities for companies of different sizes: ICT suppliers support companies' innovation and change processes through technological innovation; ICT suppliers offer specialized ICT competencies that increase the dynamic capabilities of companies [22]. According to continuous innovation theory [3], innovation requires the ability to combine exploitation and exploration capabilities. Exploration capabilities can be strengthened by the experience of ICT suppliers. External Information Technology (IT) capabilities represent a very effective tool in the pursuit of organizational goals, especially when a company's internal ET capabilities are lacking [13]. The lack of IT capabilities is often more visible in SMEs than in other companies. SMEs face specific problems in the formulation of their innovation strategies as a result of deficiencies arising from their limited resources and range of technological competencies [23, 24]. SMEs have smaller budgets for IT investments than larger companies, so financial limitations have traditionally prevented SMEs from making investments in large and complex IT applications. In addition, smaller companies are often managed and operated by owner-managers who are pivotal individuals that drive the organization forward [25]. Owner-managers may have significant product and domain expertise but limited IT skills [26, 27]. Together, these findings, along with prior research about the level of IT knowledge in SMEs, suggest that collaborative efforts with external IT suppliers may be a good, if somewhat risky, investment for SMEs, which are more likely to obtain benefits from strategic partnerships in the IT industry than large companies [28, 29], [30].

As a consequence, another topic often discussed in the literature concerns the creation of a “strong relationship with the ICT supplier” [31, 32]. Although the majority of technology managers want to have a strong relationship with their ICT suppliers and to share knowledge and competencies, they often act in a way that undermines this goal. Many companies, especially SMEs, lose out on the potential benefit of a close relationship by engaging in value-destroying behaviour by paying too much attention to costs.

With regard to the new, prominent role of ICT suppliers, especially in the context of SMEs, the literature has mainly focused on the “client's perspective” by analysing how suppliers are selected and the benefits of stronger relationships with ICT suppliers [31, 33]. These studies offer operative suggestions, but they do not help companies to identify the most suitable supplier, in terms of strategy, competencies and other important aspects of supplier fit. This lack of guidance in the search and selection process could be a problem, particularly for SMEs.

A few studies examine ICT vendors' perspectives, including motivations, strategies, business models and products offered [34].

The existing academic and managerial literature about ICT suppliers can be classified into two main categories: 1) qualitative contributions [35, 36], [37, 38], [39, 40] focusing on the analysis of ICT suppliers and their business models, competencies, main internal activities and organization; and 2) quantitative contributions provided by research centres (e.g., Forrester Research, Reed Research Group, National Electronic Distributors Association, Isuppli Corporation, National Electronic Distribution Association, Avnet, Inacom and Kompass) focusing on the size of the ICT market targeted by ICT suppliers.

Few studies from the first category go beyond a “traditional classification” of the ICT suppliers' business models. In fact, the majority of academic and professional contributions indicate only three kinds of players in the ICT distribution channel: (i) hardware resellers that sell hardware products (e.g., PCs, servers, storage systems) from well-known brands (e.g., HP, IBM, Acer, Fujitsu, Siemens); (ii) software houses that sell self-developed software applications (e.g., ERP - Enterprise Resource Planning - systems, CRM - Customer Relationship Management - applications, business intelligence applications, CAD – Computer Aided Design, PLM - Product Lifecycle Management - systems); and (iii) system integrators that customize and integrate software applications provided by software vendors for company users (e.g., Microsoft, SAP, Oracle).

With regard to the second category, quantitative data and figures on the size of the ICT market targeted by ICT suppliers are available mainly through research companies.

Given the growing strategic role of ICT suppliers in supporting SME innovation processes, our research focuses on ICT suppliers' characteristics in order to help SMEs to select the best partner from among them.

As we have shown, the existing literature is extensive but fragmented and usually does not focus on SMEs. Nor do studies focus on important issues such as strategies, core competencies and organization of ICT suppliers. The results of these studies are also relatively obsolete because they do not consider the most recent developments and trends in the ICT channel, such as M&As and partnerships. In addition, there are no models in the literature for the classification of ICT suppliers' specific competencies.

Our research aim is to gain a better understanding of ICT suppliers' nature by classifying their business models, understanding how they are evolving and studying their specific competencies. On the one hand it could help companies, especially SMEs, to choose the best ICT suppliers and, on the other hand, it could also be useful to the ICT suppliers' managers to help them understand how to organize their structures and competencies to better serve a particular area of the market.

3. The methodology of the empirical analysis

The present research is based on case studies, which are defined by Yin [41] as “empirical inquiries that investigate a contemporary phenomenon within its real-life context, especially when the boundaries between phenomenon and context are not clearly evident.” Case study methodology seems appropriate for two reasons: i) case studies provide both qualitative and quantitative results by combining several data collection methods (e.g., interviews, questionnaires, archives) [42]; ii) the case study method is well-suited to describe ICT suppliers.

When using the case study methodology, at least two different decisions must be made: first, how many studies to carry out (one or more) and, second, the type of case study (e.g., explanatory, descriptive, exploratory). Despite their complexity, multiple exploratory case studies seem to be most appropriate for the purpose of describing a phenomenon that is poorly analysed in the literature and data for statistical analysis is inappropriate, unavailable or too expensive to collect [43].

The analysis is divided into the following sections:

research design;

case study implementation;

analysis of data and interpretation of case study evidence;

assessment of research quality.

3.1 Research design

As suggested by Yin [41], the study questions are identified first. In accordance with the research objectives, these questions are as follows:

What is the strategic positioning of the ICT sales and distribution channel? In other words, what products and services do the various companies acting in the ICT sales and distribution channel offer and what is their target market?

What are the most relevant competencies related to different strategic positions?

What are the main strategic trends affecting European ICT suppliers?

Because attention must be paid to different sub-units within a company, we use embedded case studies or multiple unit of analysis, which include the following units of analysis: ICT suppliers' strategic directors (e.g., CEO, managing director), managers of sales and marketing, and managers of technical areas.

3.2 Case study implementation

The concept of population is important because the population defines the set of entities from which the research sample is drawn [42]. A total of 53 semi-standardized interviews were conducted with European ICT suppliers. A formally structured interview schedule consisting of the sections presented in Table 1 was used.

Interview Sections

In addition, questions that fit the main research aims were generated, developed and adapted because a dearth of information on ICT suppliers made it impossible to determine all the relevant questions in advance. In this way, we benefitted from the advantages of both standardized and non-standardized interviews.

We did not select the cases randomly because, as noted by Pettigrew [44], only a limited number of cases can usually be studied and it therefore makes sense to choose specific cases in which the process of interest is “transparently observable.” Cases were selected because they conformed to the main requirements of the study, while demonstrating both the similarities and differences considered to be important for the data analysis. To find the most relevant European ICT suppliers, three main sources of information were considered:

the Politecnico di Milano School of Management's database, which contains approximately 200 ICT suppliers;

the databases of ICT sales partners provided by the main ICT vendors in Europe (e.g., HP, IBM, Acer, EMC2, Microsoft, SAP, Oracle); and

commercial databases (e.g., Kompass).

ICT suppliers were selected for analysis using the following criteria: i) total turnover above €4 million; ii) number of references collected from 1,000 SMEs analysed by the Politecnico di Milano School of Management's Observatory dealing with “ICT in SMEs”; iii) broad coverage of all possible business models (in the selection phase, the ICT suppliers' business models were only analysed through secondary sources such as websites and company documents); and iv) availability to participate in the research project.

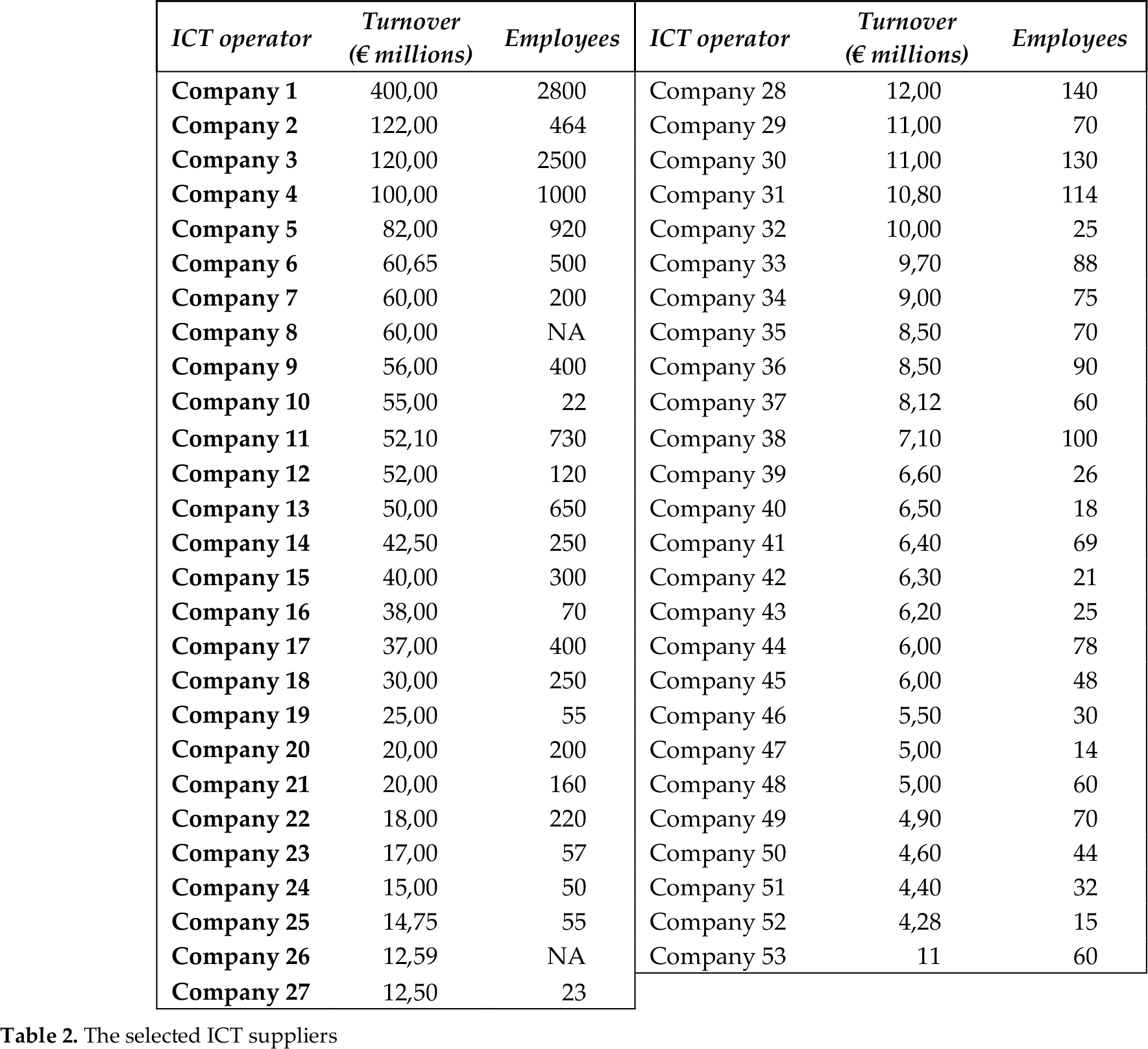

Fifty-three European ICT suppliers were selected using these criteria (see Table 2).

The selected ICT suppliers

Before undertaking the interviews, a pilot test was conducted with practitioners. As a result, the wording of some of the questions was changed to make them easier to understand. All the interviews were conducted in the same way in order to obtain comparable results (i.e., we offered each subject the same stimulus). The respondents successfully answered all the questions. The telephone interviews, which lasted one hour on average, were recorded and transcribed. The transcriptions were subsequently reviewed and approved by the interviewees.

3.3 Data analysis and interpretation of the case study evidence

The responses from interviewees were summarized, interpreted and tabulated, using the transcripts, according to the themes of the research questions. More detailed data were encoded in two files: the central database (a simple Excel spreadsheet) and a Word document containing a full summary of each of the interviews. If any information remained unclear and/or more data were needed, interviewees were later contacted with additional questions. The data analysis was conducted using two complementary approaches; a within-case and a cross-case analysis. The first approach seeks to generate insight [44, 45], while the second enables between-case comparisons to highlight similarities and differences between responses.

3.4 Assessment of research quality

The validity and reliability of case studies rests heavily on the accuracy of the information provided by the interviewees and can be validated by using multiple sources or by looking at data in multiple ways [41, 42]. We exploited multiple sources of evidence (e.g., interviews, questionnaires, archives), the reports were reviewed by the interviewees and a protocol was written.

4. The ICT suppliers' classification framework

The aim of this section is to present a classification framework to characterize ICT suppliers' strategic positioning based on the results of the empirical analysis.

The classification framework uses the following traditional strategic variables: market scope and portfolio scope. Market scope refers to the size of the companies in the target market (e.g., number of employees). According to the European Union classification, there are four main market scope categories: micro-companies (1–9 employees) or consumers, small companies (10–49 employees), medium companies (50–249 employees) and large companies (more than 250 employees). Portfolio scope refers to products and services offered by the ICT suppliers. Five main portfolio scope categories were identified: i) hardware and software infrastructure (e.g., network systems, desktop computers, laptops, servers, storage systems, printers, operating systems, office automation software); ii) advanced IT services (e.g., planning, design and implementation of complex ICT infrastructure, such as voice over IP systems, high-end servers, storage systems); iii) management software (e.g., company resource management systems, customer relationship management applications, business intelligence applications); iv) system integration services (e.g., customization and integration of software applications developed by third parties); and v) business consulting (e.g., consultancy services focused on business process re-engineering/re-organization before the launch and adoption of critical ICT applications).

Given the two strategic variables, nine different strategic positions were identified (see Figure 1), which are described in the following sections.

The strategic positioning of the ICT suppliers

4.1 Basic resellers

Basic resellers offer simple ICT products (e.g., LANs, desktop computers, laptops, notebooks, printers, mono-processor servers) to micro/small companies, or even to consumers in some cases. In addition, basic resellers often supply basic software applications (e.g., office automation applications, operating systems, simple security systems) and basic ICT services (e.g., set-up and maintenance of small local networks, PCs, mono-processor servers).

Basic resellers can be grouped into two main categories based on their target market.

Basic resellers focused on micro-companies: these are small resellers that mainly target micro- or small companies in the same geographical area (e.g., an industrial district). Sometimes, these resellers target consumers through their stores.

Basic resellers focused on medium to large companies, also called “corporate resellers”: these are larger resellers that target their products and services to medium/large companies or public sector authorities.

4.2 Value-added hardware resellers

Value-added hardware resellers offer complex hardware products (e.g., high-level servers, storage systems, complex communication technologies) and advanced ICT services (e.g., design, planning and maintenance of complex ICT infrastructures), as well as basic hardware and software products. These resellers mainly target their products and services to medium and large companies that require such advanced products and services, and exploit smaller companies to supply them with basic hardware and software products.

The empirical analysis shows that value-added hardware resellers can be grouped into two categories according to the function of the products and services in their portfolio:

Value-added hardware resellers focused on the IT infrastructure: these players supply hardware and high-level implementation, installation and maintenance of complex IT infrastructure (e.g., multi-processor servers, storage systems, complex security systems).

Value-added hardware resellers focused on communication and networking infrastructure, such as complex networking systems and voice over IP systems.

4.3 Resellers of third-party software solutions

Resellers of third-party software solutions offer simple software applications (e.g., software to manage accounting, production and warehousing) developed by software vendors that are easy to install at the customer's site. The target market is micro/small companies and professionals (e.g., lawyers and accountants).

4.4 Software houses

Software houses develop and customize management software applications for companies in various industries. Several types of software applications are developed, including web applications (e.g., corporate websites, eCommerce websites, intranet applications and extranet applications), ERP systems, CRM applications, business intelligence applications and mobile and wireless applications. The target market is medium or large companies. Software houses also supply complex industry-specific software applications to larger companies (e.g., applications for the financial, banking or telecommunication industries).

Software houses and integrators of third-party solutions supply integration and customization of management software applications developed by well-known software vendors (e.g., Microsoft, SAP and IBM) in addition to offering self-developed software applications.

4.5 Vertical system integrators

The core business of vertical system integrators is the integration of specific and unique software applications developed by a software vendor. This specialization results in a close partnership with the software vendor that develops the software application. Sometimes, vertical system integrators develop industry-specific “vertical” software applications based on the standard release of the software, which are subsequently promoted by the software vendor. The target market is mainly medium-sized companies that are often in industries for which the system integrator has developed the “vertical” software applications.

4.6 Horizontal system integrators

Horizontal system integrators are focused on the integration and customization of various software applications developed by third-party software vendors. Horizontal system integrators are called horizontal because they remain independent of third-party software vendors. The horizontal system integrators' target market is large companies.

The empirical analysis shows that several ICT suppliers combine competitive positions. For instance, some software houses or system integrators that supply large volumes of hardware products also assume the role of value-added hardware resellers.

5. The ICT suppliers' competencies

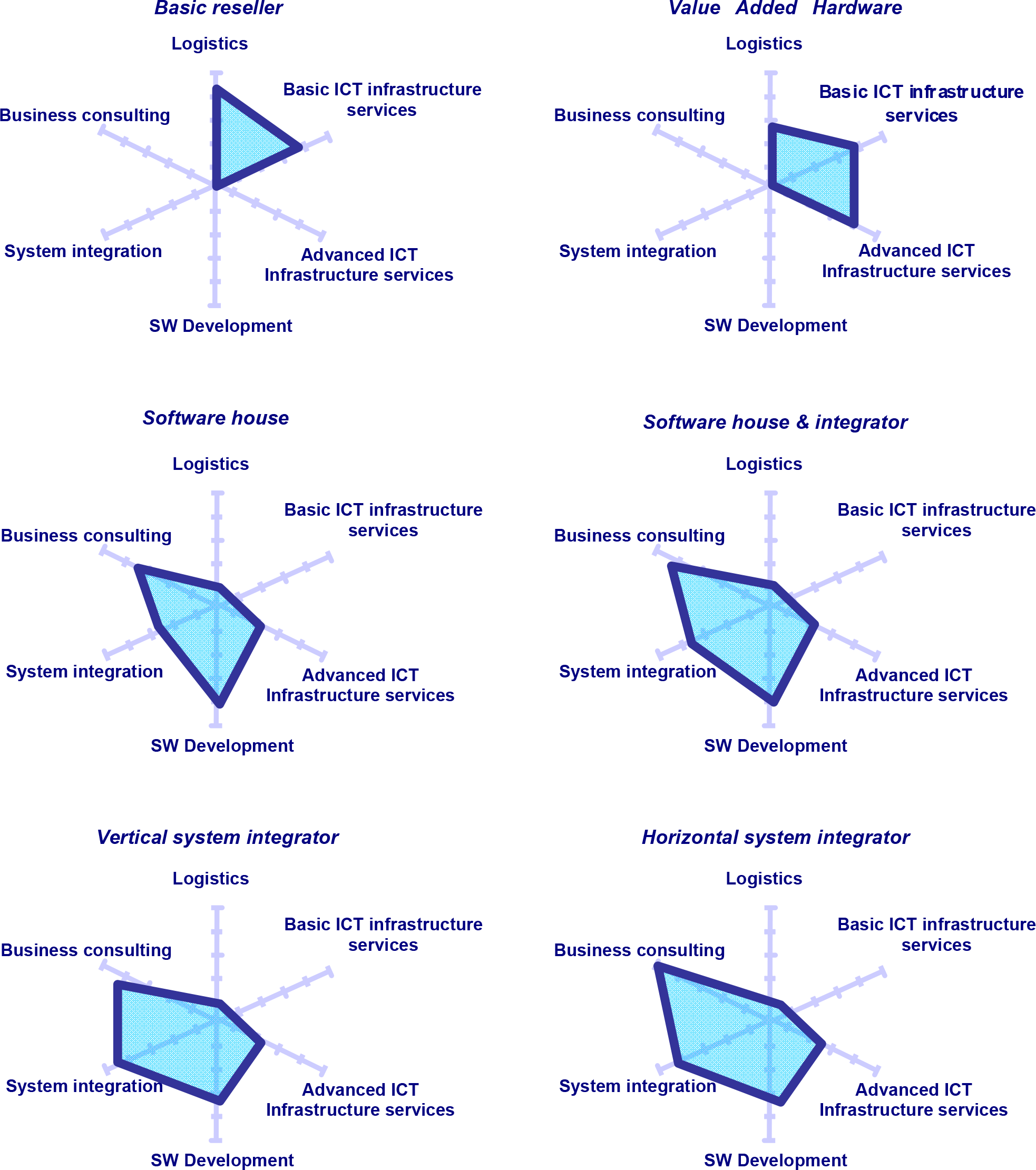

The most important internal competencies were analysed for each competitive position. Six main competencies were identified through the empirical analysis and the literature review (Figures 2):

logistics competencies concerning supply and management/integration with suppliers, warehousing, dispatching and shipping of merchandise, as well as pre-sales and customer care services;

basic ICT infrastructure services supplying basic IT services dealing with the configuration, installation and maintenance of simple ICT infrastructure;

advanced ICT infrastructure services including the design, planning and implementation of complex ICT infrastructure;

software development competencies focused on requirement analyses, design, implementation, integration and testing of applications developed in programming languages (e.g., Java, Cobol, C++, Visual Basic);

system integration competencies in the customization and implementation of software applications (e.g., ERP systems, CRM applications, business intelligence applications) developed by software vendors (e.g., SAP, Microsoft, IBM); and business consulting competencies focused on organizational analysis and business process reengineering.

The competences mapping scheme

Based on the results of the empirical analysis, the most common competence-profile for each competitive position was defined and is presented in Figure 3.

The competence profiles

In addition to these competencies, all the ICT suppliers need commercial and marketing skills, the nature of which depends on their target market (i.e., small, medium or large companies). More precisely, a supplier that targets a substantial number of micro- or small companies needs marketing skills in analysis and segmentation, direct marketing and telemarketing activities, and telesales. The need to reach many, geographically disparate, small companies has encouraged some software houses to develop their own sales channel made up of small software resellers. These software houses have developed skills in sales-channel management, including the recruitment and selection of resellers and training capabilities. However, a supplier focused on medium or large companies will need sales skills and technical and relationship-based skills in addition to the competencies related to market analysis and segmentation.

6. Conclusions

The empirical analysis shows that several business models other than traditional classifications can be described in the ICT sales and distribution channel. For each business model different competencies are required in order to create competitive advantages.

Moreover, there are several strategic trends affecting the evolution of these companies in Europe, highlighting the struggle of many companies to develop sustainable business models in a competitive landscape. The results of the analysis can help ICT suppliers to define strategic actions more effectively, they can help ICT vendors that use ICT suppliers to market their products and services to SMEs to recruit and select the most suitable sales channel partners, and they can help corporate ICT decision makers (e.g., Chief Technology Officers, Chief Information Officers) to select the most effective external partner for their company by clarifying the competencies, products and services offered by different ICT suppliers.