Abstract

Financial instruments that help provide revenue certainty are fundamental for project finance in liberalized electricity markets. Improved management of locational risk caused by network congestion is becoming increasingly important with a growing share of production from geographically remote renewable resources. Nodal markets have financial transmission rights (FTRs) to enable participants to manage locational risk, but there is no evidence that FTRs have been used to support project finance. Through a stochastic equilibrium model in which market participants invest in production assets and trade risk, we show that long-term FTRs promote surplus-maximizing generation investments and reduce the cost of capital. Investors pair them with energy price hedges and thus protect themselves against both types of risk. Our results suggest that altering the definition and allocation of FTRs to match the needs of project finance, e.g., by enabling new generators to procure a long-term right at the time of interconnection, could help ensure a complete risk market and encourage efficient investments.

Keywords

1. Introduction

The transition to liberalized electricity markets in the 1990s ushered in a paradigm that aimed to promote competition and encourage merchant investments in generation. A key condition for competition is accessible markets. Electricity markets, where sales and purchases of energy are subject to the physical conditions of power systems and congestion can prevent the transfer of energy, are vulnerable to violations of this requirement. Among methods for congestion management, the nodal pricing design proposed by Schweppe et al. (1988) is typically seen as ideal, as the resulting locational marginal prices support efficiency in both short-term dispatch and long-run investment in models with no uncertainty (Holmberg and Lazarczyk, 2015). However, nodal prices can vary substantially within a system, leading to basis risk for buyers and sellers transacting between two different locations when uncertainty is considered. One possible remedy is transmission rights allowing market participants to ensure transmission service. Because physical transmission rights are susceptible to perverse incentives in a design that focuses on a coordinated spot market (Hogan, 2013), financial transmission rights (FTRs), 1 proposed by Hogan (1992), became the contract of choice. 2 A point-to-point FTR is simply an obligation or option to the price differences for a given quantity between two locations (either nodes, zones, or hubs) in the system. Unlike physical rights, these purely financial instruments do not influence the efficient dispatch of power systems. Ideally, FTRs complete the market for risk and enable efficient long-run outcomes despite the uncertainty inherent in electricity systems.

In spite of attractive theoretical properties, academics debate the efficiency of FTR market arrangements in practice. 3 Real-world FTR markets have encountered an array of challenges. Key among these is the empirical finding across multiple markets showing that FTR payouts regularly exceed auction proceeds, at significant expense for ratepayers (Baltaduonis et al., 2017; Leslie, 2021; Opgrand et al., 2022). Several explanations have been proposed for this finding, including the inherent risk in the assets and information asymmetries between market participants. An FTR pays the price difference between a source node and a sink node, and thus protects against the congestion charges between the two locations. In practice, however, contracts between every node pair in a transmission system produce a great quantity of instruments for a small number of bidders. This limits liquidity and makes it challenging to decide bids (Siddiqui et al., 2005). One remedy is to limit the trades that can be made, e.g., by aggregating nodes to zones, but this breaks the FTR’s property as a perfect hedge (Benjamin, 2010). Additional opportunities for error arise because simultaneous feasibility tests performed in FTR auctions typically assume a known grid configuration, while the actual status of the grid is uncertain (Kristiansen, 2007; Deng et al., 2010; Alderete, 2013). Issues in FTR markets have been sufficiently pervasive to lead some observers to suggest their dissolution (Parsons, 2020).

For the purposes of this paper, the most important issue is that industry reports no evidence that FTRs have been used to support project finance (Eberhardt and Szymanski, 2017). Given that a primary motivation of FTRs was to provide a guarantee of long-term transmission service to generators, their absence from project finance is perplexing. In protecting a project’s downside and enabling stronger guarantees on debt service, hedging arrangements can enable developers to obtain low-cost debt and reduce the cost of capital. Accordingly, credit ratings favor projects with predictable floor revenues (Prabhu et al., 2017). For example, merchant investments in gas-fired power plants in the United States are often supported by heat rate call options and revenue puts that ensure stable revenue streams (Eberhardt and Szymanski, 2015). Renewable generators, meanwhile, typically rely on physical or virtual power purchase agreements (PPAs) with utilities or corporate purchasers (Bartlett, 2019; Kobus et al., 2021). The absence of FTRs is growing more important with trends in the financial arrangements supporting new capacity. Historically, utilities provided long-term offtake contracts with power producers (Eberhardt and Szymanski, 2015). Because of their familiarity with and ability to influence grid operations and investments, utilities have natural protection against locational risks and could therefore sign “busbar” contracts settling at the generator locations. The financial institutions and corporate purchasers that have recently become more important counterparties do not have the same level of comfort with grid exposure that utilities have. With different preferences and requirements for financial contracts, they prefer to settle contracts at liquid hubs instead of project locations (Bartlett, 2019). As a consequence, projects are more frequently asked to carry the basis risk associated with price differences between the project location and the settlement location. The magnitude of this basis risk represents a growing concern as the expansion of wind and solar outpaces that of transmission (Goggin et al., 2018).

In this paper, we investigate how incomplete markets for locational risk can affect long-term investment efficiency. In particular, we show how combinations of long-term FTRs with appropriate instruments to hedge price risk over a project’s lifetime have a positive impact on project finance. When these combinations are available, the total surplus gets closer to a total surplus maximizing benchmark. Moreover, investors obtain lower cost of capital because they can hedge both locational and price risks. While FTRs seem like an apparent solution to offset locational risk, the observation that they are not used suggests that auction designs currently in use are not well matched to the needs of project finance. For example, contract periods for auctioned FTRs are often one month to three years (Arce, 2013), which are far below the expected lifetime of a generator. In practice, it is also challenging to estimate the required fixed quantity of FTRs and particularly so for intermittent renewable production. 4

FTRs’ ability to hedge locational risk and the consequent impact on project finance have not received much scrutiny in the academic literature, despite the industry’s concern about locational risk. A report issued by the Wind Solar Alliance, a U.S. nonprofit that promotes renewables, states that “[f]uture PPAs will need to be structured for delivery assurance, with explicit considerations for generators to hedge congestion risk through the purchase of transmission rights” (Goggin et al., 2018). While several studies investigate how FTRs can fund merchant investments in the transmission system (e.g., Kristiansen and Rosellón, 2006, 2010; Sahraei-Ardakani, 2018; Karimi et al., 2020; Biggar and Hesamzadeh, 2020), to the best of our knowledge, Petropoulos and Willems (2020) is the only study besides ours that investigates FTRs’ impact on generation investment. Our methods are different, but complementary. Petropoulos and Willems (2020) build a stylized model where an incumbent fossil-fuel based technology competes against a low-carbon technology for transmission capacity. The incumbent is the first mover and faces a real option problem of whether to invest now or wait and learn more about the competitor before making a decision. FTRs are the only financial instrument and the producers earn revenues in a spot electricity market. Whereas Petropoulos and Willems (2020) emphasize the choice between physical or financial rights, our focus is on incompleteness in markets for locational risks and interactions with other hedging instruments. In this context, our modeling framework also resembles that of De Maere D’Aertrycke and Smeers (2013), which does not include generation investment decisions but does demonstrate the effect of FTR illiquidity on prices and quantities in futures markets.

In order to study the main features of FTRs, other hedging arrangements, risk aversion, and project finance in electricity markets, we use a stochastic equilibrium model. Specifically, we expand the model in Mays et al. (2019) to include a transmission system and FTR trading. This framework allows several risk-averse producers to compete in a spot electricity market, trade risk, and invest in generation capacity. The cost of capital is endogenous because trade in FTRs and other instruments to reduce price risk impacts investments. Stochasticity introduces different spot electricity market scenarios, where risk-averse producers want to protect themselves against unfavorable outcomes. As a result, we can investigate the impact of FTRs with a combination of different contracts through the hedge portfolio and energy mix that emerge in equilibria.

Our contribution is therefore in extending the literature on risk trading in electricity markets and developing a framework that allows investigation into the effect of FTRs on generation investment decisions. We provide a method to investigate how locational risk influences trade in energy hedges, how market participants use them, and the consequent impact on investments. This kind of study is important because the industry is arguably facing the largest fuel switch in its history, brought about by new demand growth patterns, increased investments in renewables, and looming disruptive technologies (Prabhu et al., 2017). Effective risk sharing can help ensure that the transition to a low-carbon power system is accomplished in an efficient way.

2. Numerical Experiment Set-Up

In order to assess the impact of FTRs on project financing, we formulate a stochastic equilibrium model where producers invest, trade risk, and compete in a spot electricity market representative of liberalized U.S. markets. This section presents an overview of the modeling framework, while Appendix A.1 provides a detailed account.

2.1 Electricity market model

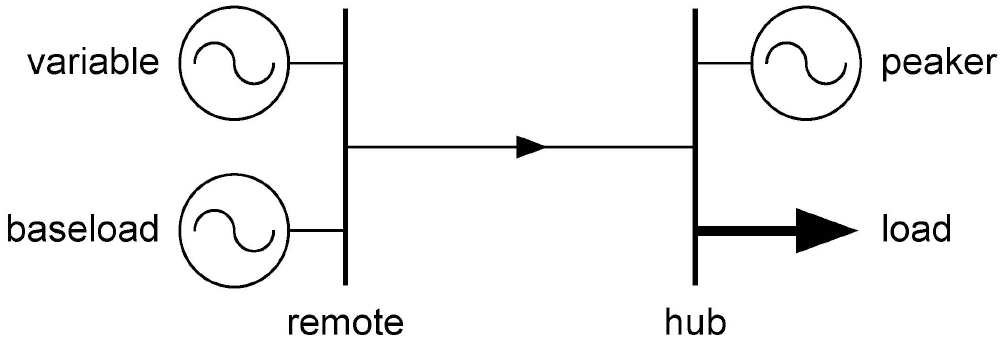

We consider a two-node power system, illustrated in Figure 1, which consists of a remote node and a central hub node. Because the nodes can have different prices, the system can exemplify locational risks while being simple enough to analyze causes and effects of risk trading. 5 The system has three technologies representative of current power systems: baseload (high capital costs but low and certain operating costs, e.g., nuclear plants), intermittent renewable (moderate capital costs and no operating cost but variable availability, e.g., wind power plants), and peaker (low capital costs but high and uncertain operating costs, e.g., natural gas-fired plants). Baseload and renewables require space and are usually at geographically remote locations. They therefore reside at the remote node. The peaker is at the hub together with a load serving entity that represents consumers. A transmission line connects the two nodes, but limited transmission capacity causes different energy prices at the remote and hub nodes. In line with U.S. markets, where the generators’ counterparties want to settle contracts at liquid hub locations, energy price hedges only trade at the hub node. This introduces locational risks for producers at the remote node because they sell electricity for remote node prices but must settle energy price hedges with payouts decided from energy prices at the hub node. Hub-settled energy price hedges alone will therefore provide incomplete risk trading for the remote generators. An FTR that matches the duration of the energy price hedge, however, can reduce locational risks and bring the system closer to complete risk trading.

Illustration of the power system used in the numerical experiments.

The modeling framework consists of a two-stage structure of investments followed by operations. In the first stage, producers invest in generation assets, while both producers and consumers secure financial contracts to hedge risks over project lifetimes. Agents on both sides of the market are risk-averse and aim to maximize risk-adjusted surplus. Producers do this by selling energy in spot electricity markets, selling energy price hedges or receiving payout from acquired FTRs. They invest in generation capacity that maximizes the risk-adjusted surplus. The load, on the other hand, maximizes risk-adjusted surplus from the utility of using energy, selling FTRs, and receiving payouts from energy price hedges bought or FTRs not sold. Load and generators are exposed to price risk in different directions because the load wants to prevent high prices and generators want to protect against low prices. They are therefore natural counterparties for hedges. Our case study does not consider financial traders. Although they are active in FTR auctions, their main activity is to find undervalued and illiquid FTRs rather than trade established and liquid paths (Leslie, 2021). A system operator performs a perfectly competitive economic dispatch in the second stage and determines market-clearing spot prices at each node. We assume a perfectly competitive market in both investment and operations. 6 The economic dispatch determines revenues from production and payouts of contracts. Both revenue streams depend on uncertainty surrounding demand, renewable availability, and fuel prices. We use the ten demand, four renewable availability, and ten fuel price scenarios from Mays et al. (2019), which is based on PJM data from 2017. 7 This creates 400 scenarios, each representing a year of operations, that we assume have a uniform probability distribution. Because market participants trade contracts before uncertainty realizes and the system operator clears the market, they consider the distribution of contract payouts when trading.

2.2 Risk trading model

To model risk aversion for both generators and load, we use a combination of the expected value and the conditional value at risk (CVaR) of surplus. The latter puts all emphasis on the

Because each energy price hedge matches the risk faced by a specific production technology and FTRs protect against locational risks, trade in all contracts should approximate a complete risk market. Whenever a contract is unavailable, the market for risk is incomplete. We investigate this effect through separate experiments on all sixteen combinations of contracts, from none to all. Contracts are either not available or they can trade in unrestricted volumes. We emphasize that this is a simplification of actual market settings where risk trading may be partially complete and market participants will also consider liquidity risk. PPAs, for instance, which resemble the unit contingent contracts, are often bilateral contracts and may not be as freely traded as our model. In a practical context, the “no trading” situation can be interpreted as long-term contracts either being unavailable or illiquid. In project finance, investors must obtain long-term contracts to secure favorable funding conditions. Our framework reflects this by considering contract duration over a project’s lifetime. Even though there may be liquid markets for short-term contracts, like current FTR auctions, we assume that these do not contribute to project finance because they are not able to secure revenue streams over the projects’ lifetimes. Hence, we consider short-term contracts as “no trading” in our context.

As a benchmark for the results, we use a model that co-optimizes all investments and operations considering the society’s risk preference. A benevolent decision-maker considers the producers and load’s decision problems to select optimal investments in generation capacity. This model, described in Appendix A.1, identifies a social optimum that is equivalent to the competitive equilibrium that would arise under the assumption of complete risk trading, i.e., with an Arrow– Debreu security corresponding to each scenario (Ehrenmann and Smeers, 2011; Ralph and Smeers, 2015; Philpott et al., 2016; Ferris and Philpott, 2022). When all four of our defined contracts are available, surplus in equilibrium reaches near the level of the social optimum, indicating that this much smaller set of instruments is enough to support near-complete markets in risk.

2.3 Decomposition algorithm and convergence

The set of market participants and scenarios make it computationally demanding to find equilibria directly for all experiments. We therefore use the decomposition algorithm proposed by Mays et al. (2019) to find equilibria. Appendix A.1 includes a mathematical description of the algorithm. The main notion of the approach is that all investors must have risk-adjusted profit of zero in a perfectly competitive market. After the algorithm defines the necessary initialization parameters (like initial generation capacity, contract prices, tolerance limits for convergence, strike prices for contracts, and step sizes for updates), it enters an outer loop that incrementally updates generation capacities in the direction that move the risk measures toward zero. Within the outer loop, the system operator clears the spot electricity market that decides energy prices and hence the operating profit and payouts from financial instruments. The algorithm must then clear the financial market to get contract prices to calculate risk measures for the new capacity mix. This is done in an inner loop that iteratively updates contract prices until sales match purchases. The process continues until the algorithm finds an equilibrium where generation capacities are sufficiently close to zero or it reaches an iteration limit.

Although the solution approach is the same as Mays et al. (2019), we use it on a more complex model that includes a power system, FTRs, and settlement locations for contracts. This makes the model more intricate because it introduces more variables that influence each other and the convergence criteria. If transmission never congests, there are no locational risk and the model becomes equivalent to the one in Mays et al. (2019). Congestion is a key factor because it causes price differences that introduce decisive shifts in allocation of surplus between load and producers. Whereas the uncongested model experiences gradual changes in risk measures according to the gradual changes in capacity investments, this is not the case for a model with transmission where marginal changes in capacity can congest the line and hence produce a shift in risk measures. In practice, this makes it challenging to select step sizes and for the algorithm to converge. None of our experiments reached an equilibrium through risk measures sufficiently close to zero, but had to use a limit of 50,000 iterations. Near this limit, the algorithm oscillates between two capacity mixes that marginally congest and uncongest a time block every other iteration. The marginal changes in capacity mixes are insignificant and do not impact capacity investments within the decimal point that we report results for. Appendix A.1 has further discussion on the stopping criterion and related challenges.

We emphasize that because the equilibrium model is a non-convex problem, we cannot guarantee that the equilibrium found by the decomposition algorithm is unique. Our objective, however, is not to replicate actual market conditions, but instead to illustrate how transmission basis risk can be an important aspect of project financing. Although we cannot make conclusions about the magnitude of inefficiency the inability to hedge locational risk causes, we can demonstrate the direction. Hence, we performed experiments on a range of different risk parameters and initialization values and ensured that all of them moved toward equilibria in the same directions as the results presented and in line with intuition and behavior found in Mays et al. (2019).

3. Results and Discussion

We conduct numerical experiments on the two-node system in Figure 1 to assess how FTRs impact investments and social surplus. Appendix A.1 outlines the modeling framework, which we implement in Julia (Bezanson et al., 2017), using the

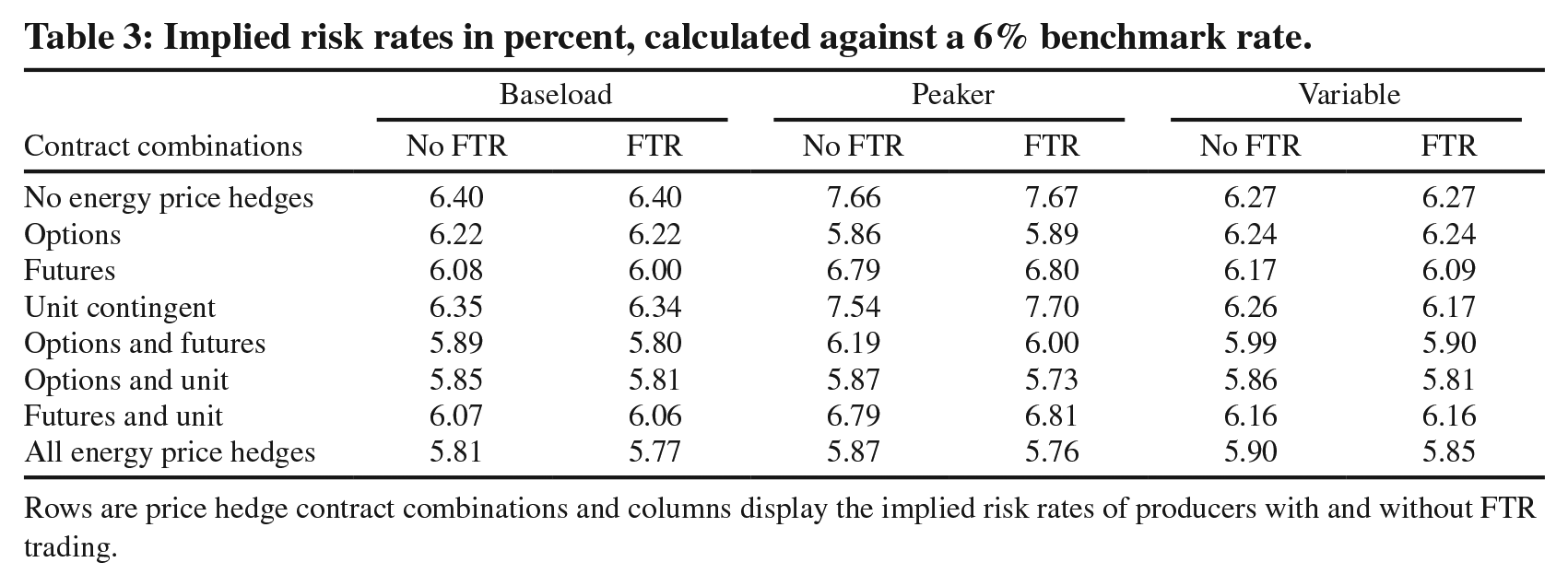

Equilibria feature zero risk-adjusted profit for all technologies, meaning that risk-adjusted profits earned in operation equal the annualized upfront investment cost. Implicitly, this annualized investment cost is calculated using the cost of capital that would prevail with no price or quantity risk. Zero risk-adjusted profit would imply non-zero profit in expectation when measured against the same discount rate; the zero-profit condition therefore implies a different, endogenously calculated cost of capital when evaluated against risk-neutral probabilities. With details of the calculation described in Appendix A.1, we use this risk-neutral profit to calculate a weighted average cost of capital (WACC). For the calculation we assume a 20-year project lifetime and a 6% benchmark rate.

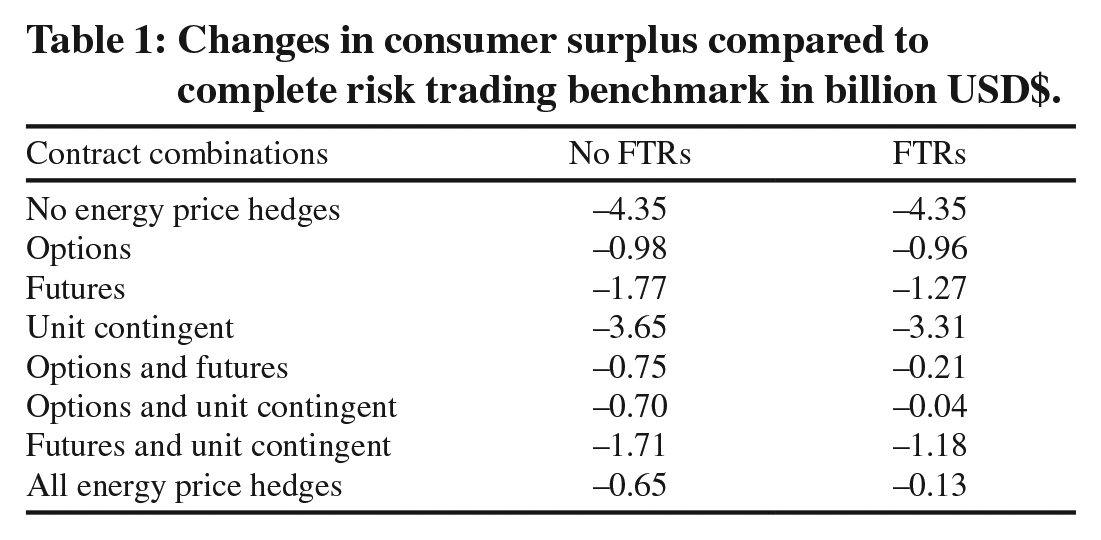

FTRs improve social surplus whenever futures or unit contingent contracts are available (Table 1). The increase in consumer surplus ranges from USD$340M to USD$660M per year. Futures and unit contingent contracts are the preferred instruments for baseload and variable producers. Because these generators reside at the remote node and sell at remote node prices, they experience incomplete hedging from the hub-settled energy price hedges. With FTRs, however, they expose themselves to hub prices instead, which improves the hedging capability of the hub-settled future and unit contingent contracts. In effect, they acquire FTRs to hedge their locational risk. The consumer surplus increases when they are able to do so. A situation where only FTRs are available does not improve surplus because the risk market does not become more complete. It just allows the remote producers to be exposed to hub prices instead of remote prices so they still carry energy price risk.

Changes in consumer surplus compared to complete risk trading benchmark in billion USD$.

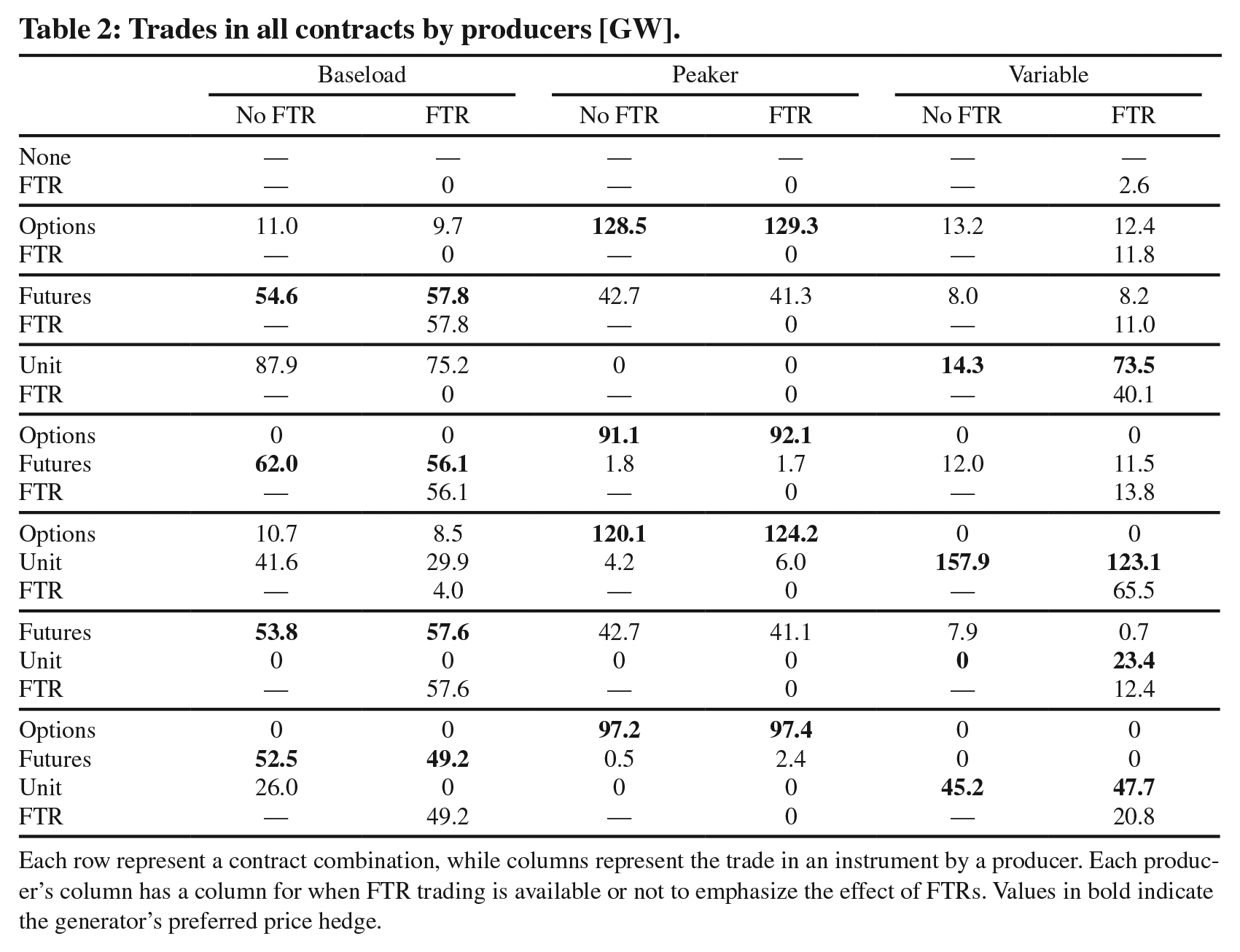

Table 2 outlines the contract trades that occur under the different contract combinations. The producers are mainly inclined toward instruments that match their price risk whenever available: baseload secures revenue streams through futures, the peaker reduces its dependence on scarcity prices by selling options, and the variable producer protects its revenue streams against its intermittent production by unit contingent contracts. The load purchases a portfolio of contracts from the three producers to manage its exposure to scarcity and fuel prices. The generators also use the other price risk instruments to a smaller extent. In particular, baseload and variable producers both trade futures and unit contingent contracts when their contract of choice is not available. This is because these contracts behave similarly. Only generators on the remote node are interested in FTRs. The peaker sells at the hub where it settles contracts and does not experience location risks. 11 The baseload resource acquires the exact same amount of futures and FTRs whenever both are available. This is to remove all locational risks from the hub-settled futures. The variable producer is the most frequent FTR buyer. It acquires FTRs in all instances, albeit slim volumes in cases without unit contingent contracts. FTRs help to secure revenues in high production hours when congestion, and thus lower prices at the remote node, is more likely. Furthermore, FTRs’ ability to hedge locational risk encourages trade in hub-settled unit contingent contracts.

Trades in all contracts by producers [GW].

Each row represent a contract combination, while columns represent the trade in an instrument by a producer. Each producer’s column has a column for when FTR trading is available or not to emphasize the effect of FTRs. Values in bold indicate the generator’s preferred price hedge.

As more contracts become available, risk trading moves toward a complete market. Table 2 shows that producers can then trade their preferred contracts and Table 1 demonstrates that this provides more consumer surplus. This is because the ability to hedge risks results in lower cost of capital, as shown by the implied risk rates in Table 3. Lower cost of capital encourages investment in certain technologies. Consider for instance when only options are available: the peaker then has a 5.86% risk rate for investment compared to 7.66% in the no contract situation. Incomplete risk markets can thus cause suboptimal investment incentives. When more contracts become available, Table 1 displays that consumer surplus gets closer to the complete trading ideal.

Implied risk rates in percent, calculated against a 6% benchmark rate.

Rows are price hedge contract combinations and columns display the implied risk rates of producers with and without FTR trading.

FTRs have a positive impact on project financing only when they are paired with one of the hub-settled energy price hedges (Table 3). The remote generators receive spot market revenues from sales at their node, but their financial contracts settle against hub prices. When FTRs are the only available contract, there is virtually no interest in the instrument. It simply changes what energy price the producers are exposed to, and thus does not contribute to protect against risk. However, whenever the preferred contract for the remote producers, futures or unit contingent contracts, are available, the cost of capital decreases when they can also obtain FTRs. This is because FTRs reduce the locational risks between the prices the remote producers are exposed to at their own node and the prices that energy price hedges clear against at the hub. In effect, they can better protect against unfavorable outcomes and ensure better floor revenues that reduce the cost of capital. The peaker, unaffected by locational risk because it is located at the hub node where energy price hedges settle, does not receive cost of capital benefits by FTRs themselves. It does, however, experience spillover effects from the investment incentives experienced by the other generation technologies when FTRs are present. For example, FTRs and unit contingent contracts can create incentives to invest in the variable resource rather than baseload on the remote node. This large share of intermittent production introduces more scarcity prices that encourage investments in peaker capacity.

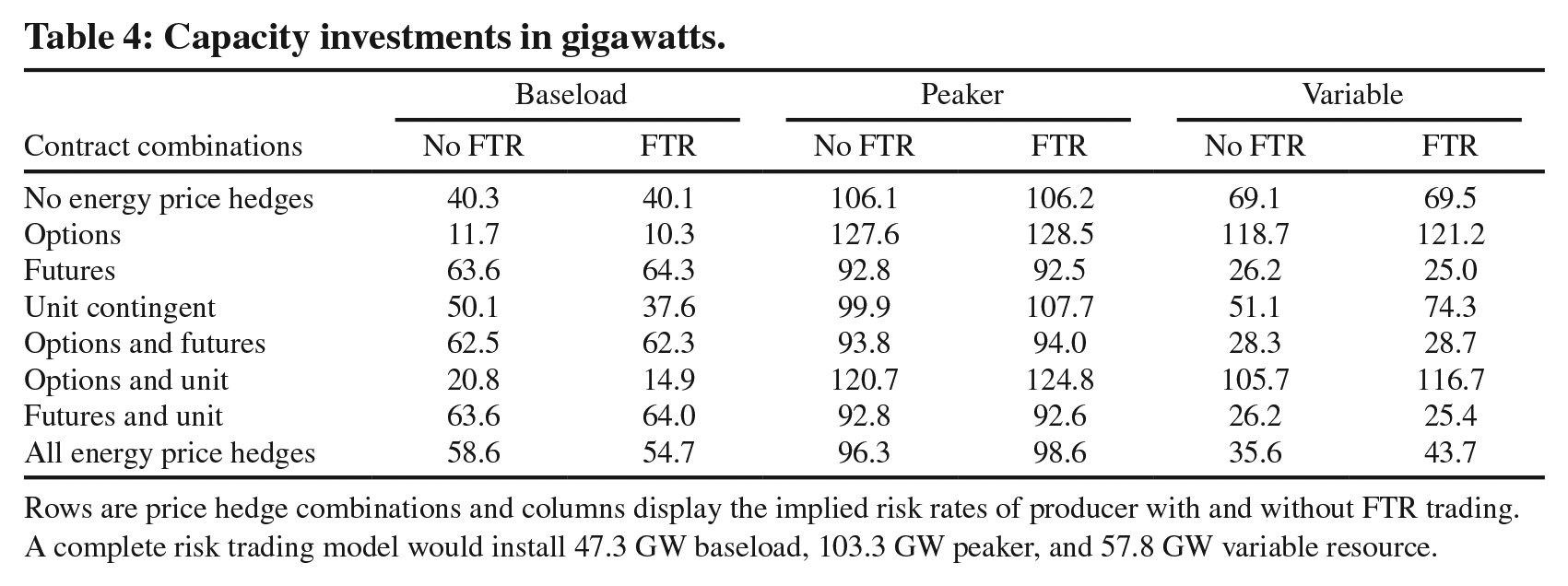

A low cost of capital provides investment incentives because it makes investments cheaper. Table 4, which outlines the capacity investment for the different contract combinations, reinforces this observation. Energy price hedges are potent drivers for investment, as illustrated by how available futures and options expand baseload and peaker capacity, respectively. Except for cases with unit contingent contracts, barring the “futures and unit contingent” combination, FTRs’ impact on investments are within a couple of gigawatts. FTRs make the variable producer increase or baseload decrease their sales of unit contingent contracts (Table 2). Both situations benefit the variable producer, which increases its capacity. The baseload resource can keep its ground by pairing FTRs and futures in the “futures and unit contingent” combination. Consistent with congestion being a small percentage of total cost, we observe that FTRs have less impact on investments than the energy price hedges. The capacity investments suggest that FTRs’ favorable influence on consumer surplus, shown in Table 1, is mainly from changes in risk-adjusted revenue streams rather than the mix of investments.

Capacity investments in gigawatts.

Rows are price hedge combinations and columns display the implied risk rates of producer with and without FTR trading. A complete risk trading model would install 47.3 GW baseload, 103.3 GW peaker, and 57.8 GW variable resource.

Linking capacity investments to the contract trades from Table 2, we observe that the baseload resource manages to completely de-risk its revenue when futures and FTRs are both included. With an assumed availability of 90 percent in all time periods, the baseload resource trades 90 percent of its total capacity in futures and FTRs. It thus manages to remove all locational risks of being exposed to remote prices while settling futures at the hub node. The baseload resource cannot follow this consistent strategy when FTRs are not available. The variable producer, by contrast, cannot de-risk completely because its production is variable; the unit contingent contract tracks this variability, but FTRs are a fixed-volume instrument. Moreover, it is more affected by the market environment for its risk trading strategy. The “option and unit contingent contract” and “future and unit contingent contract” combinations illustrate this phenomenon. These are contrasting cases where the variable producer sells 157.9 GW unit contingent contracts and installs 105.7 GW production capacity in the former, 12 while the latter has no trade in unit contingent contracts and only a 26.2 GW capacity investment. Options and unit contingent contracts complement each other because they encourage investments in both the peaker and variable producer. Variable production provides cheap electricity when it produces, but its intermittent nature increases the risk of scarcity events. These events are the main profit drivers for the peakers. At the same time, options encourage peaker investments, which remove baseload from the market (Table 4). A peaker-dominated production portfolio increases non-scarcity prices because of higher operating costs. The load will therefore be more willing to buy unit contingent contracts to stimulate variable production to decrease prices, particularly when the system has sufficient peakers to protect against scarcity events. Futures and unit contingent contracts, however, behave similarly. Investors are reluctant to build peaking resources without option contracts, which increases the risk of scarcity events if the energy mix contains large shares of variable production. As a result, the load is hesitant to acquire unit contingent contracts and prefers futures from the baseload resource, which provides a more dependable output than the variable producer.

Investment and risk trading follow the same behaviors observed by Mays et al. (2019) for the same system without transmission and FTRs, and hence no locational risks. This is because the producers still face the same price risks and and are thus drawn to the same instruments in both cases. Transmission constraints limit the supply that the load can receive from the remote generators, which reduce investments in remote capacity. This particularly curbs investment in the variable resource because transfer capacity rather than load will limit sales on high-production time periods. Congestion also introduces more periods where the variable resource sets the price at the remote node rather than the peaker. Investments are therefore not as exaggerated as in Mays et al. (2019), where some contract combinations lead to no baseload capacity due to large investments in peaker and the variable resource. FTRs amplify the incentives of energy price hedges for the remote producers because they reduce locational risks and improve the energy price protection.

Despite quite different equilibrium capacity mixes, Table 1 shows that the “option and future,” “option and unit,” and “all” combinations all achieve near-optimal social surplus when FTRs are available. This indicates that there is a range of energy mixes that can provide a similar level of service. In particular, we observe that baseload and the variable producer are somewhat interchangeable as the provider of low-cost electricity. Risk markets influence which technology becomes the preferred option. The producer with the best hedging possibilities is in a better position to invest. This is an important policy insight: complete risk markets for a particular technology encourages investments in it. Markets for risk can therefore be a tool to, for instance, facilitate carbon-free investments. But similarly, incomplete risk markets can discourage them.

From our experiments, the “option and unit” case is of particular interest due to its similarity to the present situation in most U.S. electricity markets. The option contract mimics a capacity construct, which are present in all U.S. markets except the Electric Reliability Council of Texas, while unit contingent contracts resemble the PPAs widely available for renewable producers. In this configuration, moving from no trade to complete trade in FTRs improves annual surplus in the example system by roughly USD$660M. As discussed in the previous paragraph, this configuration results in near-optimal social surplus when FTRs are available. Indeed, with FTRs included, this case somewhat anomalously achieves slightly higher surplus than even the “all” contract case (Table 1). Since we expect the social surplus to increase in general when more derivatives are available (Willems and Morbee, 2010), this result is likely an artifact of the algorithm, which does not necessarily completely converge to an equilibrium (see Appendix A.1 for details).

4. Conclusion

Predictable revenue streams, obtained through financial instruments, are key to secure financing for generation investments in liberalized electricity markets. Financial institutions and corporations are increasingly the counterparties for these contracts. In contrast to utilities, the traditional hedge providers, these actors want to settle contracts at liquid hubs instead of project locations. Projects are therefore exposed to basis risk from the price difference between the node where they sell electricity and the hub where they settle financial contracts. Despite their ability to hedge basis risk in theory, there is no evidence that FTRs have been used to support project financing. At present, FTRs typically cover much shorter time frames than required for project finance, and furthermore may not be available until after financing must be secured.

Through a stochastic equilibrium model where market participants invest in generation and trade financial instruments to hedge risks, we show the potential for long-term FTRs to have a positive impact on project financing. They decrease the cost of capital and encourage investments that increase social surplus when they are available. Market participants are not interested in the FTRs themselves, but combine them with other financial contracts to hedge both locational and energy price risks. Complete markets for risk, including long-term FTRs, are required to achieve surplus-maximizing outcomes.

The transition to a low-carbon power system, brought about by ambitious environmental targets for 2050, depends on generation investments on an unprecedented scale. With a greater share of energy coming from geographically remote renewable resources, many actors in the industry have raised concerns over locational risks and methods to hedge it over project lifetimes. Our results suggest that reforms to the definition and allocation of transmission rights may help push systems to more complete risk trading. At least three avenues for moderate reform are possible. First, changes in the timing of auctions could help ensure that generators have the ability to secure rights farther in advance. Second, new generators could be given the option to purchase a long-term transmission right as part of the interconnection process. Third, new and existing generators (or some subset of generators) could be assigned a portion of transmission system costs currently paid by load, receiving transmission rights in exchange. In this third approach, the goal would be to match the default allocation of hedges to the party with the greatest exposure to basis risk. Any of these three approaches could be pursued without major changes to the definition of FTRs themselves. More fundamental changes, such as introducing FTRs with time-varying volumes or relaxing the revenue adequacy requirement, might also enable more complete risk management but introduce more significant complications. A comparison between these and other approaches represents an important direction for future work to support an efficient transition to a decarbonized energy mix.

Supplemental Material

sj-pdf-1-enj-10.5547_01956574.45.1.sris – Supplemental material for Congestion Risk, Transmission Rights, and Investment Equilibria in Electricity Markets

Supplemental material, sj-pdf-1-enj-10.5547_01956574.45.1.sris for Congestion Risk, Transmission Rights, and Investment Equilibria in Electricity Markets by Simon Risanger and Jacob Mays in The Energy Journal

Footnotes

Appendix

Acknowledgements

The authors would like to thank David Morton and Stein-Erik Fleten for feedback and discussions. This research was supported, in part, by the Power Systems Engineering Research Center.

1.

FTRs have different names in different markets, like Transmission Congestion Contracts (TCCs), Congestion Revenue Rights (CRRs), and Transmission Congestion Rights (TCRs). We will stay consistent and use FTRs throughout this paper.

2.

Flowgate contracts (FGRs) introduced by Chao and Peck (1996) are alternative or complementary contracts (see, e.g., O’Neill et al., 2002). But these are rarely used because traders prefer the hedging properties of point-to-point FTRs (![]() ).

).

3.

Several works (e.g., Bartholomew et al., 2003; Deng et al., 2004; Siddiqui et al., 2005; Zhang, 2009; Hadsell and Shawky, 2009; Adamson et al., 2010; Deng et al., 2010; Baltaduonis et al., 2017; Olmstead, 2018; Leslie, 2021; Opgrand et al., 2022) investigate and discuss the efficiency of FTR markets, with no consensus on whether the markets are inherently inefficient.

4.

To solve the challenge of bidding fixed-volume FTRs, Biggar and Hesamzadeh (2013) and ![]() propose an alternative FTR design that follows production and consumption volumes and then provide better hedges.

propose an alternative FTR design that follows production and consumption volumes and then provide better hedges.

5.

A point-to-point FTR just considers the price difference between two locations. The two-node system is sufficient to create such a difference. A more complex system would introduce an FTR for each possible pair of nodes. To ensure clarity in interpreting numerical results we avoid a network and limit to the two-node example with a single FTR. From the perspective of generation investment, the key issue is modeling price differences between a project location and a hub node where contracts settle, regardless of whether those differences arise due to congestion of a single line or more complex network flows.

6.

FTRs can in theory be used to exploit market power (see, e.g., Pritchard and Philpott, 2005; Joung et al., 2013). An example is cross-product market manipulation, where market participants make unprofitable bids in the spot market, for instance to provoke price differences, to benefit their FTR positions. Ledgerwood and Pfeifenberger (2013), Birge et al. (2018), Lo Prete et al. (2019), and ![]() study this particular violation.

study this particular violation.

7.

We made some slight adjustments to the renewable availability profiles. ![]() have several time periods with the same availability, which resulted in longer congestion periods and hence larger shifts in surplus. Because this caused some convergence difficulties we made small alterations to make sure that each timeblock had a separate availability, but the average availability remains the same. We discuss this numerical phenomenon further in Appendix A.1.

have several time periods with the same availability, which resulted in longer congestion periods and hence larger shifts in surplus. Because this caused some convergence difficulties we made small alterations to make sure that each timeblock had a separate availability, but the average availability remains the same. We discuss this numerical phenomenon further in Appendix A.1.

8.

An ideal energy-only market with a call option with strike price equal to an electricity price cap approximates a capacity market design (Mays et al., 2019).

9.

Ensuring revenue adequacy is more complicated in practice because the status of the grid may be unknown when performing a simultaneous feasibility tests that decides FTR volumes that ensure revenue adequacy (see, e.g., Kristiansen, 2007; Deng et al., 2010; Alderete, 2013).

10.

We also did experiments with a relaxed revenue adequacy condition that allowed FTR trades above the limit set by transmission capacity. ![]() shows that only the “option and unit,” “future and unit,” and “all” contract combinations hit the FTR limit. Removing the trade volume restriction resulted in a couple of gigawatts of additional trades in these cases, with an insignificant impact on investment outcomes. These results are limited to our two node set-up and parameters, and cannot be interpreted as general remarks on the impact of FTR volume limits or the revenue adequacy condition.

shows that only the “option and unit,” “future and unit,” and “all” contract combinations hit the FTR limit. Removing the trade volume restriction resulted in a couple of gigawatts of additional trades in these cases, with an insignificant impact on investment outcomes. These results are limited to our two node set-up and parameters, and cannot be interpreted as general remarks on the impact of FTR volume limits or the revenue adequacy condition.

11.

In separate experiments where transmission investments were uncertain, the peaker bought a small amount of FTRs when options were not available and it acquired futures or unit contingent contracts instead. This is a hedge against the price risk of different transmission capacities rather than locational risk. Still, it illustrates the multifaceted nature of FTRs. In other respects, the uncertain transmission experiments gave similar results as the ones we report for fixed transmission.

12.

This result is a clear discrepancy between installed capacity and traded volume. In real markets, producers must manage to satisfy their contractual obligations. Our model clears the market without considering physical backing, so a producer sells contracts as long as its financially profitable to do so regardless of capacity. The “option and unit contingent contract” combination is a special instance where extensive investments in peaker capacity, supported by sales of call options, trigger substantial demand for unit contingent contracts. In effect, the unit contingent prices increase and the variable producer sells beyond its capacity.

13.

The simplified economic dispatch problem (1) assumes that the system operator can control energy transfer zijt. This neglects loop flows, which can be included in the model by for instance calculating zijt using power transfer distribution factors (PTDFs) and net power injections at the nodes.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.