Abstract

Continuous trading is currently becoming the standard for intraday electricity markets. In this paper, we propose frequent auctions as a viable alternative. We argue that batching orders in auctions potentially leads to lower liquidity cost, more reliable, less noisy price signals, and allows for better alignment of market outcomes with the technical realities of the transmission grid. In an empirical study, we compare the German continuous intraday market with counterfactual outcomes from frequent auctions. We find that traded volumes tend to be higher for continuous trading; however, the auction market benefits from lower liquidity costs and less noisy price signals. Furthermore, we critically discuss the suitability of continuous trading in the presence of network constraints and technical restrictions of conventional units. Taken together these findings suggest that in sparsely traded intraday markets, pooling orders in frequent auctions may be beneficial.

Keywords

1. Introduction

In the last decades, electricity markets in most countries have seen fundamental changes due to the transition of the electricity sector from a vertically integrated, state controlled sector of the economy to a competitive industry. In addition, the electricity sector is the key to sustainable energy systems, facilitating a substantial increase in the use of renewable energy and consequently the phase-out of fossil fuels.

Electricity markets are typically organized as a sequence of forward markets that trade products with ever shorter maturity and temporal resolution. Most market designs feature a day-ahead market that allows to trade electricity one day ahead of delivery and a market that gives firms the possibility to adjust their positions until shortly before physical delivery.

The latter markets—organized either as real-time or intraday markets—are of increasing importance because of the growing short-term uncertainty in production from renewable energy sources. Prominent examples for real-time markets include most U.S. electricity markets (Milligan et al., 2016), while European short-term markets are organized as intraday markets.

In this paper, we focus on intraday markets, which have received a fair amount of attention in the recent academic literature (e.g., Hagemann and Weber, 2013; Kiesel and Paraschiv, 2017; Uniejewski and Weron, 2018; Janke and Steinke, 2019; Marcjasz et al., 2020; Narajewski and Ziel, 2020; Baule and Naumann, 2021; Balardy, 2022). There are currently two prevailing designs for intraday trading (Ocker and Jaenisch, 2020): continuous markets and repeated auctions. Both designs have their strengths and weaknesses: Auction based markets impose low entry barriers for participating firms and facilitate relatively high liquidity by pooling demand and supply. However, existing auction markets suffer from long lead-times making it difficult to trade the production of renewable energy sources and to quickly react to new information (Holttinen et al., 2013), mostly because there are only a handful of auctions with the last one closing several hours before delivery.

In contrast, continuous trading ensures a high level of immediacy as traders can instantaneously act on new information. Furthermore, since a trader can, in theory, accept orders for different products with known prices simultaneously, the continuous market makes it easier to trade complex profiles in asset backed trading. The main downsides of continuous trading are the higher complexity of trading, the lower liquidity (Kuppelwieser and Wozabal, 2021), which leads to low quality price signals that are often dominated by noise, and the incompatibility of order-book based trading with the physical realities of the electrical grid. Despite these downsides the recent trend is to discontinue auction based designs in favor of continuous trading (Ocker and Jaenisch, 2020).

The contribution of this paper is the investigation of a market design, which represents a compromise between the extremes of continuous trading and infrequent auctions and is well suited to deal with the idiosyncrasies of electricity markets. In particular, we propose that orders should be batched in frequent auctions which are repeatedly conducted for every traded product until shortly before physical delivery of electricity starts. Ideally, such a market has the potential to combine the advantages of both designs while avoiding most of the disadvantages.

To get an idea how frequent auctions could impact market outcomes, we conduct a case study for the German market by creating a counterfactual for auction outcomes based on detailed order-book level data submitted to the EPEX continuous intraday market for the German market zone in the years 2017 and 2018. To this end, we construct hypothetical auction outcomes for a single auction per product as well as auctions which are repeated every 60 minutes, 15 minutes, five minutes, and every minute. Our results show that the distribution of volume-weighted prices remains virtually identical when switching to any of the proposed auction formats. When examining the traded volume, we are able to show theoretically that under certain conditions auctions clear less orders and therefore lead to lower traded volumes than continuous trading. This theoretical result is largely confirmed in our numerical experiments.

Despite the results on traded quantities, liquidity costs, measured as costs of round trip trades as in Kuppelwieser and Wozabal (2021), are lower for auction based trading than for continuous trading. Based on these results, we argue that even though auctions tend to clear less volume, they are preferable in terms of liquidity cost.

Finally, we use a kernel regression based approach to investigate the signal to noise ratio of the price signals generated by the two market designs. We find that prices generated by frequent auctions are significantly less noisy than the prices resulting from continuous trading and are therefore expected to produce more reliable price signals that are more closely tied to changes in the fundamental value of the traded product.

This paper relates to several earlier works that discuss the specific advantages of auctions for electricity intraday markets: Neuhoff et al. (2016) studies the impact of the intraday auction in the German market that clears one day before delivery and find that the auction has a higher liquidity and lower volatility than continuous trading. Furthermore, the authors argue that auctions are better suited for smaller players that do not have the capacity to take part in a continuous intraday market.

Similarly to the market design proposed in this paper, Deutsche Börse Group (2018) proposes a model for frequent intraday auctions that takes into account transmission infrastructure to explicitly price scarce interconnector capacities, allows for more complex order types, and increases liquidity. The authors argue that these goals can be achieved in auctions, due to the increased time for clearing and the possibility to take into account orders at different locations in the network.

Ocker and Jaenisch (2020) discuss continuous trading and auction based intraday markets in the European context and identify liquidity, the resilience against the exercise of market power, and efficiency of the use of transmission capacity as the main advantages of auctions over continuous trading.

The rest of the paper is organized as follows: In Section 2, we review the trade-off between continuous trading and auctions as it is discussed in the finance literature and argue that frequent auctions have the potential to combine the advantages of both designs. In Section 3, we review the current European market design with a special emphasis on the German market, which we use in our case study. Section 4 details the computation of the counterfactual based on the order book data for the German market, while Section 5 discusses the numerical outcomes of the comparison between continuous trading and frequent auctions and optimal auction frequencies. Section 6 summarizes and concludes the paper.

2. Literature Review

In this section, we discuss the literature on the trade-off between continuous and auction based trading in Section 2.1 and then proceed to discuss how the specifics of the electricity market influences the choice between the two market designs in Section 2.2.

2.1 Continuous Trading versus Auctions in the Finance Literature

The finance literature discusses the choice between auction based trading and continuous markets as a trade-off between liquidity and quality of the price signal versus the possibility to react quickly to new information. Continuous trading is at one extreme of this trade-off, offering maximal immediacy. Having a single auction is the other extreme which would be, by definition, welfare optimal if there was no information flow during the time the auction market is open.

Although continuous trading is the prevailing market design in all major markets trading shares, futures, options, and other financial products, there are prominent critical voices in the finance community. Most of these authors advocate to replace or complement continuous trading by auctions in order to either improve liquidity and the quality of the price signal (e.g., Schwartz, 2012) or to avoid the excesses of high frequency trading that effectively imposes a fee on trading and thereby lead to welfare losses (e.g., Budish et al., 2015).

Kregel (2001) provides an account of the historical roots of continuous trading and points out that in early stock exchanges trading was organized in auctions. However, since, without computer technology, auctions had to be performed sequentially in order to give every trader the chance to participate in all auctions, auctioning became impractical as the number of listed companies increased. To resolve this problem, trading floors where brokers could continuously strike bilateral deals evolved. This form of trading eventually lead to continuous trading as it is practiced today. Paradoxically, nowadays the use of modern information technology, whose absence necessitated this development, is to blame for most of the adverse effects of continuous trading.

One of the advantages of continuous trading is its immediacy, i.e., the ability of market participants to instantaneously trade on information whenever it arrives. Correspondingly, in a classic paper, Brennan and Cao (1996) show that, if the timing of information is not predictable and specific assumptions on a demand for immediacy and risk aversion of market participants hold, continuous trading yields a Pareto efficient equilibrium that is preferable to auctions.

However, in a survey of equity traders Economides and Schwartz (2001) find that there is no fundamental economic reason to execute trades within seconds or minutes. Based on these findings, Steil (2001) argues that the demand for immediacy is endogenous to continuous trading and would almost entirely vanish if trading would take place in auctions. In particular, traders want to react fast to either profit from being the first to react to new information or to avoid front-running of other market participants. When trading is organized via auctions, the notion of being first looses its meaning and front-running cannot occur. Furthermore, Economides and Schwartz (2001) find that the lack of liquidity in continuous trading might actually reduce immediacy for larger positions, since traders are forced to trade patiently over longer time periods to avoid an excessive price response to their trades.

Recently, Budish et al. (2015) and Aquilina et al. (2021) take a slightly different angle in criticizing continuous trading when studying the impact of high frequency trading on market outcomes. The authors observe that treating time as continuous in trading systems, that serially process orders, opens the door for latency arbitrage where high frequency traders compete on speed to capitalize on new information that signals a change in the fundamental value of traded assets by sniping stale orders of other market participants that are slower to react. The authors argue that the resulting arms race for speed is socially wasteful and effectively introduces a fee on trading that reduces liquidity.

In particular, Aquilina et al. (2021) find that frequent batch auctions would reduce the cost of liquidity by 17% and that a remarkably large portion of overall trading volume (about 20%) can be attributed to latency-arbitrage races. Similarly, Wah and Wellman (2013) find in a simulation study that replacing continuous markets with periodic call markets eliminates latency arbitrage opportunities and achieves substantial efficiency gains.

There is a strand of literature that explores the trade offs between continuous trading and repeated auctions. An early paper in this direction is Garbade and Silber (1979) who investigate how the frequency of trading influences liquidity risk and identify two opposing effects: Firstly, longer auction periods help to collect more participants in an auction and therefore reduce the noise in the price signal and therefore liquidity risk. Secondly, they identify the drift in the equilibrium price as driving the volatility risk up as auction intervals become longer and the shocks in equilibrium prices increase between to consecutive auctions. Hauser et al. (2001) extend this argument and find that more liquid stocks tend to have less return volatility when continuously traded whereas discrete trading with longer intervals is preferable for thinly traded stocks.

Du and Zhu (2017) propose a model of sequential double auctions, which allows to capture the trade-off between the welfare increasing ability to react quickly to information changes and welfare decreasing bid shading both of which increases in the frequency of trading. In the model, frequent trading reduces liquidity (and thus welfare) in every single auction, but increases welfare by reducing externally assumed holding costs of agents.

Complementing this theoretical research, there is a large body of empirical literature that informs the discussion based on observational data from stock markets. Pagano and Schwartz (2003) show that complementing continuous trading with call auctions lowered execution costs and improved price discovery in the Paris stock exchange. Comerton-Forde et al. (2007) find similar results for the Singapore stock exchange.

On the other hand, Muscarella and Piwowar (2001) find that for assets traded on the Paris stock exchange, the traded volume increases when stocks are shifted from auction based trading to continuous trading and decreases when the shift goes in the other direction.

Twu and Wang (2018) show in a case study of the Taiwan stock exchange that decreasing the interval between consecutive auctions improves overall market quality. Contrary to these findings, Hu and Chan (2005) and Hu (2006) find that shorter intervals correspond to a worse signal-to-noise ratio in prices at the exchange.

Lauterbach (2001) shows that for most stocks on the Tel-Aviv stock exchange liquidity and the quality of the price signal improved after being shifted to continuous trading but also identifies some exceptions of stocks that are thinly traded and for which continuous trading does not work well. Finally, Chelley-Steeley (2008, 2009) finds that market quality on the London stock exchange improves with the introduction of a closing call auction and that this improvements are especially pronounced for the least actively traded securities.

Overall, the emerging picture is ambiguous. However, it seems fair to conclude that thinly traded stocks tend to profit from auction based formats. This suggests that intraday markets for electricity, which, except for a brief period shortly before delivery, are characterized by rather low activity could profit from an auction based design.

2.2 Continuous Trading versus Auctions in Electricity Markets

In this section, we describe key differences between electricity markets and financial markets, discuss the applicability of continuous trading in electricity markets, and highlight where auctions might have advantages or disadvantages.

A continuous market design allows to trade immediately and all current orders are visible to each trader (transparency). However, since intraday markets for electricity are, compared to most financial markets, rather thinly traded and many market participants do not have the ability to react fast to new information, the loss in immediacy is likely to be marginal when switching to a market design with frequent auctions.

In an auction the submission time of orders is irrelevant. Therefore auctions help to create a level playing field without advantages for those who are able to act quickly and therefore prevent front-running and other costly excesses of high frequency trading as they are observed in financial markets. Furthermore, the technical complications and high fixed cost of operating a trading desk that participates in continuous trading at competitive speeds might hinder market entry of some firms. Hence, an auction-based market might facilitate more participation and ultimately a more liquid market (Ocker and Jaenisch, 2020).

Another difference between the two market designs is price variance and the quality of the price signal, i.e., the information about fundamental values that is contained in the price. While an auction based market design with too few auctions disseminates information slowly and might lead to large price shifts between auctions (see Garbade and Silber, 1979), a design with frequent auctions can be used to address these issues. Furthermore, by pooling orders in auctions extreme bids and offers are likely to be infra-marginal and therefore do rarely directly influence the clearing price. Because individual orders in an auction are not observable by market participants, the decision on how to trade would likely be more influenced by observable shocks such as changes in forecast for demand or renewable production than by the actions of other market participants. Taken together this shifts the focus of traders away from an introspective view on the markets towards fundamental factors, which potentially reduces trading-induced noise in the price signal.

One of the advantages of continuous trading is that firms can more easily trade complex profiles involving more than one product. Consider the example of an electricity storage that wants to buy electricity in one period, store it, and then sell it at a later point in time. In continuous trading the storage can accept existing limit orders for two products at the same time for known prices and thus minimize the risk that only one leg of the transaction is executed. Contrast this to the same situation in an auction setting, where it could very well happen that the bids of the trader are only accepted in one of the auctions leaving the storage with an open position. This situation can be circumvented by submitting perfectly inelastic supply or demand functions with the effect that the storage owner may not receive the arbitrage value she had hoped for (see also the discussion in Löhndorf and Wozabal, 2022).

Next we discuss to what extent the market design can deal with technical properties of the underlying electricity network and how this might affect the choice of the trading system. In particular, we remark that electricity markets are special because generators, consumers, and traders interact through a rather unforgiving physical system whose failure induces significant negative external effects on societies as a whole (Kirschen, 2021). That is the reason why effectively all electricity markets have a transmission system operator as a centralized authority that has the objective to secure continuous electricity supply for as many customers as possible.

In electricity markets, network constraints that result from the aforementioned physical limitations introduce complications in market-clearing because the resulting power flows have to be computed for every trade. Flow-based market coupling reflects congestion in the network and assigns prices to transmission capacities accordingly and therefore would be the first-best solution. However, the computational performance of the ensuing calculations depends non-linearly on the size of the network and can cause latency in continuous trading, which would slow the pace of clearing the market and decrease the advantage of immediacy. Hence, if power flows would be accurately computed while clearing the market, this would effectively act as a speed limit for continuous trading.

These leaves two options to price transmission capacities in continuous trading: (i) exogenously defined locational markets, which obviously is inefficient because cross-border trading is restricted even if market conditions would allow for it, (ii) transmission capacity is allocated for free on a first-come first-served basis (Ehrenmann et al., 2019). The latter approach aggravates the potential race for speed in continuous markets. Summarizing, it is highly unlikely that a sequence of bilateral trades through continuous trading is able to solve the complementary goods problems for energy and transmission capacity (Mansur and White, 2012; Ehrenmann et al., 2019).

In contrast, flow based market-coupling can easily be accounted for in an auction that centrally maximizes welfare subject to transmission constraints. In this setting, locational prices can be easily constructed from the duals of the energy balance constraint and the duals of the transmission constraints (see, e.g., Graf and Wolak, 2020). The advantage is that the price of congestion will be defined endogenously based on orders. At this point it is important to highlight that in meshed electricity networks with loops, transferring 1 MW of electricity from one node to another affects every single flow in the network. Consequently, clearing the market jointly with many different offers and bids at different locations will increase the efficiency of the market outcome (Ehrenmann et al., 2019). Even more important in terms of computational complexity are constraints that link several time instances (Neuhoff et al., 2016). Both attributes favor auctions because computation time is less critical compared to continuous trading markets (see also Deutsche Börse Group, 2018).

We also want to emphasize that because orders are cleared sequentially in continuous trading, liquidity is critical when blocks of energy are traded. More precisely, in continuous trading a block-offer will only be sold conditional on the presence of a market participant willing to buy a given block bid. In practice this constraint can lead to severe liquidity crunches (Neuhoff et al., 2016). In contrast, in auctions block-offers can easily be traded against multiple simple demand bids, if auctions for several products are cleared simultaneously (Ehrenmann et al., 2019).

Finally, we remark that with continuous trading dispatchable units that participate in the reserve markets may use schedule changes ordered by the transmission system operators to front-run the continuous intraday market. In particular, if market operators with dispatchable units obtain the information that one of their units’ output will be changed due to a reserve market activation only a fraction of a second before the public, this information can be monetized on the continuous intraday market. If an auction would take place, e.g., every five minutes, the timing of when the information of a schedule change will be released is less critical and all market participants are in the same position to react to this information update. Hirth and Mühlenpfordt (2021) empirically study this aspects for the German intraday market where information on balancing actions is not published in real-time. The authors find a statistically robust correlation between reserve activation and intraday price changes.

3. German Wholesale Electricity Market Design

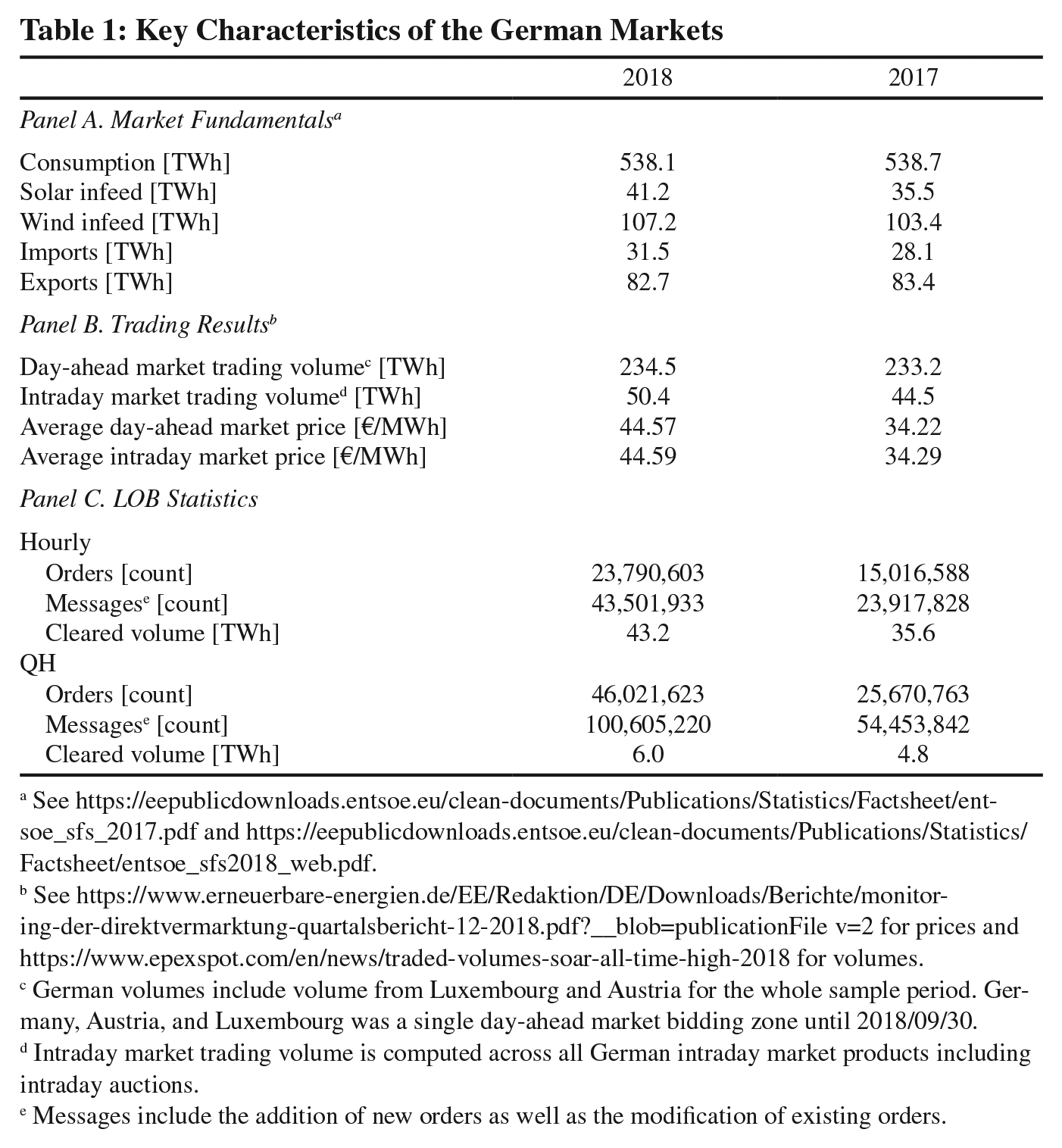

In this section, we review German short-term wholesale electricity markets consisting of a day-ahead market, an auction market for quarter-hourly products, and a continuous intraday market. Table 1 contains key characteristics of the German electricity sector in Panel A, an overview of market results in Panel B, as well as some statistics on the LOB in Panel C. As can be seen Germany has a reasonably large fraction of variable renewables in the form of wind and solar PV. This drives the growth of the intraday market, which as of 2018 traded roughly one sixth of the volume of the day-ahead market at virtually the same average prices. For a in-depth discussion on the liquidity of the intraday market, we refer to Kuppelwieser and Wozabal (2021).

Key Characteristics of the German Markets

See https://eepublicdownloads.entsoe.eu/clean-documents/Publications/Statistics/Factsheet/entsoe_sfs_2017.pdf and https://eepublicdownloads.entsoe.eu/clean-documents/Publications/Statistics/Factsheet/entsoe_sfs2018_web.pdf.

See https://www.erneuerbare-energien.de/EE/Redaktion/DE/Downloads/Berichte/monitoring-der-direktvermarktung-quartalsbericht-12-2018.pdf?__blob=publicationFilev=2 for prices and https://www.epexspot.com/en/news/traded-volumes-soar-all-time-high-2018 for volumes.

German volumes include volume from Luxembourg and Austria for the whole sample period. Germany, Austria, and Luxembourg was a single day-ahead market bidding zone until 2018/09/30.

Intraday market trading volume is computed across all German intraday market products including intraday auctions.

Messages include the addition of new orders as well as the modification of existing orders.

In the following two sections, we review the current German design for short-term wholesale electricity markets. We first give a broad overview of all the markets and their integration in the larger European context in Section 3.1 and then discuss the specific market rules for intraday trading in Section 3.2.

3.1 Overview of German Short-Term Wholesale Electricity Market

The German short-term wholesale market for electricity is embedded in the wider zonal European market design, which is organized as a cascade of forward markets with the day-ahead market being especially important. Specifically, the day-ahead market determines schedules for European cross-border flows via the European single day-ahead coupling and consists of several bidding zones in which Germany represents a single zone. 1 Trading with other zones is defined through flow-based market coupling. The market is organized as a double auction that yields locational marginal prices and trades products for delivery in every hour of the following day.

The main philosophy of the German market design is that market participants should deliver on their day-ahead promises in real-time at the firm level (Cramton, 2017). However, because demand and non-dispatchable supply are uncertain, market participants have the opportunity to minimize their real-time imbalances at the intraday market that opens shortly after the day-ahead market has cleared.

In Europe, there are currently two competing types of intraday trading systems: auction markets and continuous intraday trading. In 2015, the EU committed to the long-term goal to couple all European intraday markets in a large continuous market in order to facilitate a secure energy supply, competitiveness, and fair prices (European Commission, 2015). In Germany the intraday market is hosted by the EPEX, the largest electricity exchange in Europe (see Viehmann, 2017, for a detailed description) and is organized as a continuous trading market.

Similar to day-ahead markets, German intraday markets are also coupled with other intraday markets across Europe via the single intraday coupling (SIDC). Orders of each bidding zone are collected in local limit order books, and cross-border capacities are used to build shared limit order books that are used to match orders from different zones. 2 As of today, cross-border flows in SIDC are agnostic towards Kirchhoff’s and Ohm’s laws and are computed according to shortest paths between nodes of the network. 3 Consequently, the power flows computed in SIDC might not match actual physical flows leading to potentially costly re-dispatch actions to be taken by transmission system operators (TSOs).

Unlike the electricity markets in the United States, the German market design can be described as trader-centric, because day-ahead and intraday market offerings are not tied to physical units but to traders. In a separate process market participants with dispatchable units communicate with the TSO about which units at which locations are scheduled. More generally, the European take on electricity market design aims to decouple the trading reality from the physical reality. Because the latter has to be taken care of in order to avoid system failure, complex, spatially heterogeneous, and partially intransparent processes are operated to ensure that electricity supply can be maintained even under circumstances where the trading decisions produce physically infeasible market results.

Germany requires market participants to firmly report schedules at 2:30 pm one day ahead of delivery. 4 These schedules must be within the range of the maximum physical withdrawal or injection capacity which limits arbitrage trading between the day-ahead and intraday markets. Furthermore, this framework effectively bans speculative traders that do not have a natural short or long position from participating in the day-ahead market. Nevertheless, the price differences between the day-ahead market and the intraday-market are typically small on average. If for a market participant the combined orders from spot and future markets deviate from the actual physical production or consumption at gate closure of the intraday market, the residual quantities are settled on the balancing market. The price-spread between the day-ahead market and the balancing market is often significant. Balancing prices are determined by distributing costs of reserve activation to those market participants that caused the imbalance. The German regulatory framework forbids to arbitrage between the day-ahead or the intraday market and the balancing market by creating imbalances on purpose. 5 In practice, this is less strictly enforced for producers of renewable electricity and the demand side because of the difficulties in precisely predicting production and load (see, e.g., Eicke et al., 2021).

Reserve requirements are procured in separate auctions which are held every day for the respective next day before the day-ahead market is cleared. TSOs then activate positive or negative reserve energy in real time to ensure that planned power flows are physically feasible. The revenue stream of a supplier eligible to participate in the balancing market thus consists of selling energy in the day-ahead and intraday markets and providing the flexibility to adjust prior schedule commitments in real-time that are needed to balance the system. Therefore all short-term markets are implicitly coupled.

Although in the day-ahead market transmission constraints are not explicitly accounted for within Germany, these can still be relevant and the TSOs might have to intervene by redisaptching some power plants to ensure feasible flows within the German zone. This invites what is called the INC/DEC game (Graf et al., 2020), where market participants with dispatchable capacity may be able to profit from the discrepancy between the clearing result from, for example, the day-ahead market and the actual real-time demand for their supply units. 6 Using this strategy market participants can endogenously create a demand for re-dispatch by submitting—from a system perspective—unfavourable schedules. To limit the profitability and therefore the attractiveness of this strategy, Germany uses a cost-based re-dispatch (Hirth and Schlecht, 2019).

3.2 German Continuous Intraday Market for Electricity

The German continuous intraday market opens shortly after the clearing of the day-ahead market and is organized as an order book based continuous trading market that features hourly, half-hourly, quarter-hourly, as well as block products. The intraday market remains open until 5 minutes before the delivery of the respective product starts. However, the German market zone is split up into four zones, one per TSO, 25 minutes before gate closure, even if no actual congestion is present.

Each buy and sell order on the intraday market for a given product contains basic information about quantity, limit price, and validity time. A market order is cleared immediately against the best available order in the limit order book (LOB), while a limit order is only executed with matching orders on the other side of the market up to a certain price (the limit). If this is not possible, the order is kept in the LOB until its end validity date to be cleared with future orders. If the quantities of two matched orders do not agree, the order with the higher order quantity is only partially cleared and remains in the order book with the remaining quantity.

Market participants can add the usual order qualifiers such as immediate-or-cancel (IOC) or fill-or-kill (FOK), see EPEX (2020). 7 Additionally, iceberg orders are allowed for which only a fraction of the order quantity is visible to other market participants. As soon as the visible quantity is cleared, the next part of the order is automatically placed in the limit order book.

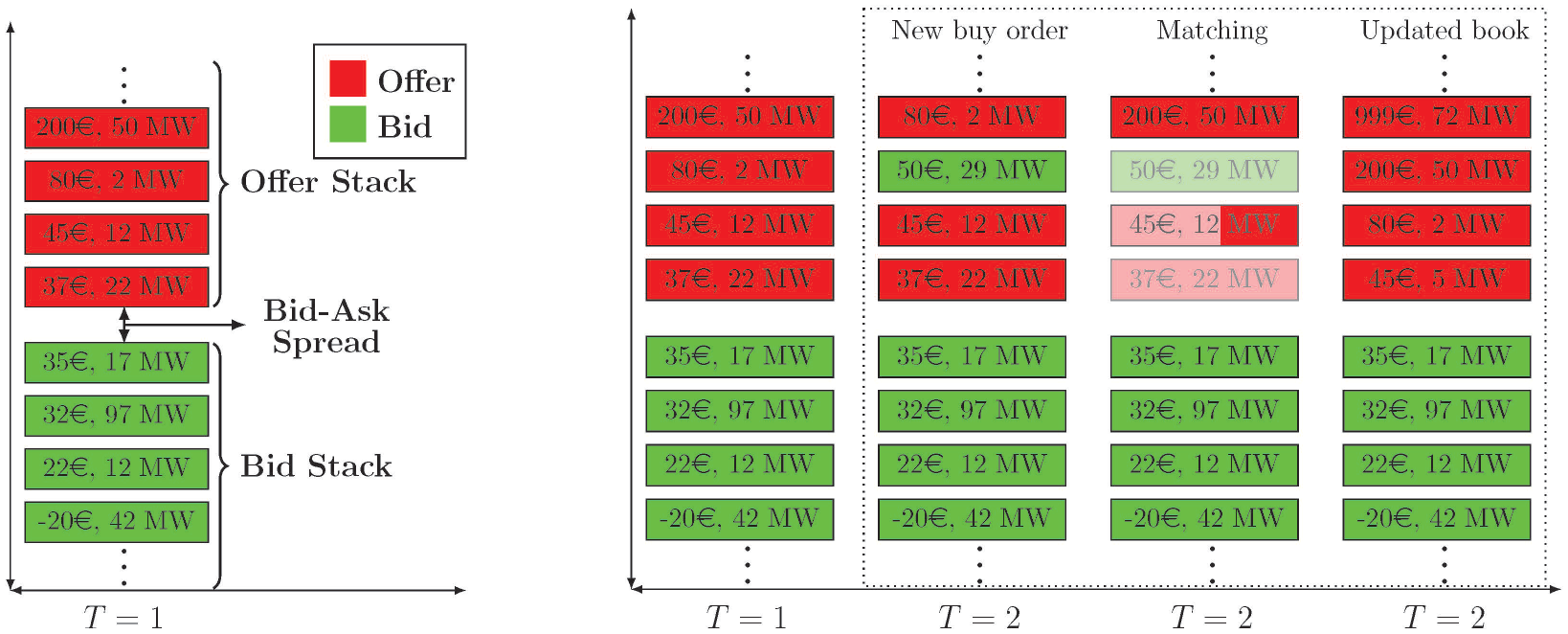

The basic mechanism of continuous trading is illustrated in Figure 1 by a concrete example: In the left panel, the state of the order book at T = 1 is displayed with the orders sorted according to their limit price. The state of the LOB changes with the placement of a new order, with the modification of an order, and at the end-validity-time of an active order. The limit price of the order with the lowest sell price is called best-ask, while the order with the highest buy price defines the best-bid, and the difference between the two prices is the bid-ask-spread.

Limit Order Book Clearing Mechanism

The dynamics of the order book are exemplified in the right panel of Figure 1: A bid with a price higher than the lowest ask is added to the book at T = 2 and then cleared against the cheapest possible offers until either the whole order is fulfilled (as is the case in the figure) or there are no offers with lower prices left. Note that the clearing is instantaneous, i.e., columns 3–5 of the figure are purely illustrative and do not correspond to market states that can be observed by traders.

4. Counterfactual Frequent Auction Design

To assess how a transition to frequent auctions affects intraday electricity prices, we construct counterfactual market results based on observed order book data from the German continuous market. We conduct a ceteris paribus analysis where the market design changes, but the orders of the market participants stay the same, i.e., we use the historical orders submitted to the continuous market as auction bids. For the purpose of this paper, we consider hourly and quarter-hourly products traded at the EPEX and disregard the half-hourly products in order to keep our numerical study manageable.

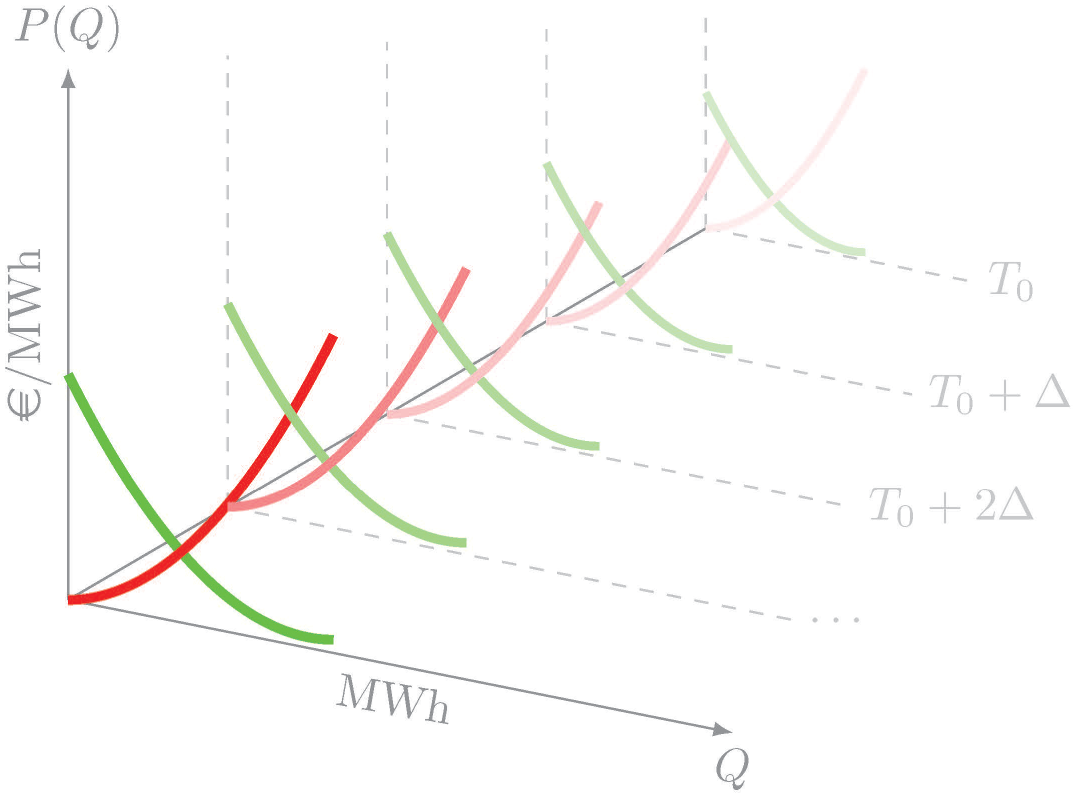

In Figure 2, we visualize a stylized sequential auction design for one product in a single-zone market. The main idea is that a uniform price auction is run repeatedly with the last auction shortly before delivery and the first auction several hours before that. Auctions should be frequent enough to allow for a timely reaction to new information but leave enough time between auction clearings in order to ensure sufficient participation—and thereby liquidity—in every single auction. We therefore envision auctions that are run simultaneously somewhere between every hour and every few minutes for all traded products. We believe that the flow of fundamental information pertaining to electricity supply and demand is such that this design does not represent a relevant limitation of immediacy in trading. For the sake of simplicity, we propose the auctions to be evenly spaced in time. After an auction clears, the next one immediately opens and bids and offers are collected by the market operator until gate closure.

Stylized Sequential Batch Auctions for One Product

To construct auctions, we fix a product, i.e., a specific hour or quarter-hour in which electricity is delivered and an auction interval

For every auction k, the cleared quantity is defined as the maximizer

where

In the single zone case and with no product dependencies the market-clearing thus simply involves constructing

When dealing with these piecewise constant functions, there is some ambiguity about the clearing price as defined in (1) and, in some cases, also the cleared quantity that maximizes welfare. We resolve this ambiguity in the same way, as it is done in the current design of the Italian intraday auctions (Caramanis and Inc., 2002; Graf and Wolak, 2020).

In particular, if the piece-wise constant functions (2) and (3) intersect either at one point

In case that the functions intersect at a horizontal part of the functions –1 and

In case an offer or bid is not cleared or only partially cleared but has an end validity date that extends into the next auction period, we place the remaining quantity as an order in the next auction. In particular, for the k-th auction, we include orders with an end-validity date after

Clearly, while the obtained prices mimic the results of a hypothetical frequent auction market, the analysis has several limitations, which are discussed in the following:

The experiment suffers from the issue that we use orders that were submitted to a continuous market to construct counterfactual auction results. This is of course suboptimal, since it can be expected that market participants would change their bidding behavior if the market design would change to frequent auctions.

However, under the assumption that the willingness to buy/sell certain quantities is exogenously given, one can expect roughly the same bidding behavior in a continuous market and frequent auctions. In particular, participants will trade on the same side of the market in both designs and bid prices should not change too much.

There are several data imperfections in the limit order book data as supplied by EPEX: (a) A subset of orders in the order book for 2017 and 2018 is cleared via XBID with orders from other countries. Although we do not have access to the order books for other European countries, we can identify the orders in question. To be able to reproduce the historical clearings, we add virtual orders of the size of the cleared German orders on the respective other market side. We set the limit price to the price of the observed clearing, the quantity to the cleared quantity, and the end-validity date to the date of the clearing with the foreign order. We also use these orders when constructing the counterfactual auction outcomes. However, since this process of order book completion is clearly not perfect and we might be additionally missing orders from abroad which are not cleared in continuous trading, cross border trading has the potential to distort our results. Having said that, we remark that cross border trading often is limited in practice due to scarce interconnector capacities between countries. (b) In the data provided by EPEX, the end-validity time of cleared orders is overwritten with the clearing time in case an order is cleared. As a result, information is lost and some of the orders we consider would have been valid for longer than is visible in the available data. (c) Market orders are not explicitly identified and limit prices for these orders are not set to the maximum/minimum possible price of EUR ±9,999/MWh, but to the last bid/ask price the order is executed against.

Furthermore, we ignore block-orders. Considering these orders would introduce a dependence between auctions for different products and complicate our experiment. While this is very much possible in an auction based framework, which is much less sensitive to increased computation times resulting from the ensuing complications than continuous trading, we avoid coupling auctions to keep the discussion simple.

5. Numerical Results

In this section, we discuss the comparison of the outcomes for the continuous market with the counterfactual auctions. We consider quarter-hourly and hourly products with auctions being cleared every

In our experiments, we consider the full German order book of 2017 and 2018 containing roughly 39 mln orders and 67 mln messages to the exchange for the hourly products and 72 mln orders and 155 mln messages for the quarter-hourly products (see Table 1). All computations, except visualizations, including the clearing algorithms for both market regimes and the computation of liquidity costs are implemented in JAVA.

5.1 Prices

In this section, we compare the distribution of prices generated by the two clearing methods. To that end, we define the volume-weighted price of a product in continuous trading as

where

where

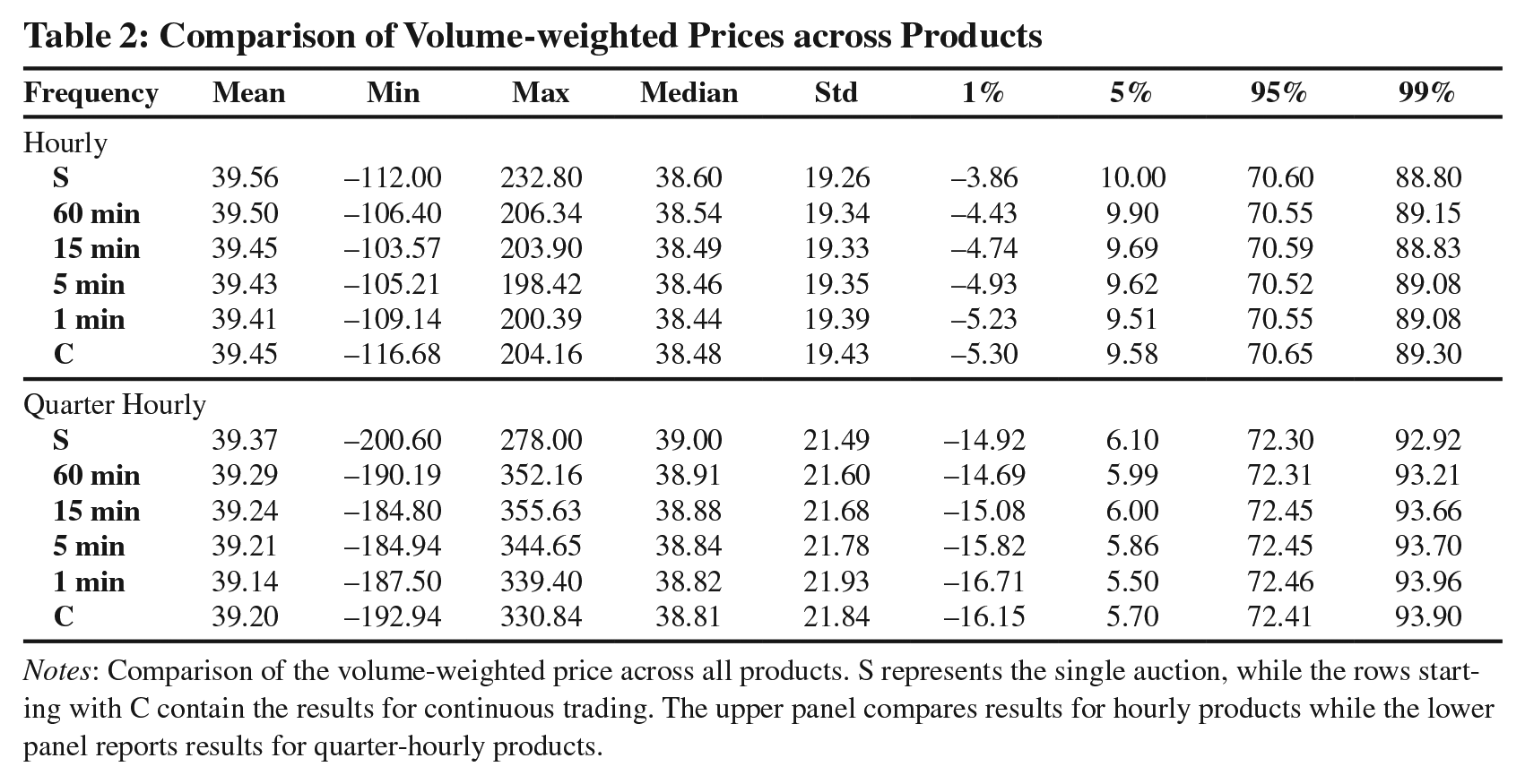

Statistics for the volume-weighted prices across all hourly and quarter hourly products for continuous trading and the five auction formats are reported in Table 2. As can be seen, the distributions of the volume-weighted prices are quite similar, which implies that no fundamental disruptions in price levels are to be expected when transitioning from continuous trading to frequent intraday auctions. The fact that not only the average volume-weighted prices but also the 1%, 5%, 95%, and 99% quantiles are practically identical is quite surprising and indicates that, averaged over products, not even the most extreme prices change substantially with the introduction of frequent auctions.

Comparison of Volume-weighted Prices across Products

Notes: Comparison of the volume-weighted price across all products. S represents the single auction, while the rows starting with C contain the results for continuous trading. The upper panel compares results for hourly products while the lower panel reports results for quarter-hourly products.

We conclude that the effect of a transition to frequent auction on average price levels and distributions are negligible for both product types and across all proposed methods of clearing.

5.2 Traded Volume

Next we analyze the cleared volumes for both market designs. Since auctions have the reputation to produce more reliable price signals and lower liquidity cost for participants, on a first glance, it seems intuitive that the quantity cleared in an auction would exceed the quantity cleared in continuous trading (see also Deutsche Börse Group, 2018).

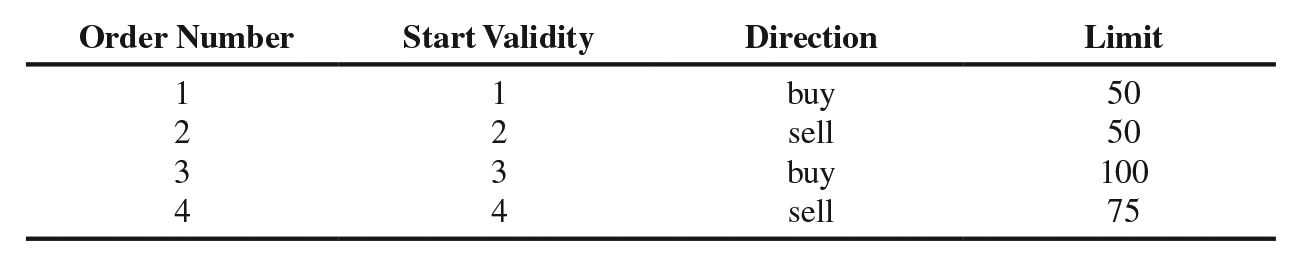

However, ceteris paribus, this intuition turns out to be wrong as we show below. To give an idea why this is the case, consider the following small example. Suppose for a certain product, the following orders are recorded in the limit order book:

where all orders have an end-validity date of 4 and a size of 1 MWh.

Clearly, in continuous trading, order 1 would be cleared with order 2 and order 3 with order 4, leading to an overall traded quantity of 2 MWh. If instead the orders would be cleared in a single auction at time t = 4, the clearing price could be anywhere between 50 and 100 and only orders 2 and 3 would be cleared, which leads to a cleared quantity of only 1 MWh. However, note that the auction, by design, achieves the maximum welfare gain of 50, while the welfare gain from continuous trading is only 25. This example shows that even if all orders are collected in a single auction the volume that is cleared in continuous trading may be larger.

Note that the situation in the above example is not at all pathological or exceptional but rather the rule in a situation where continuous trading is replaced with a single auction at the end of the trading window. In fact, we can prove the following proposition.

Proof. Assume without loss of generality that the size of all orders equals the minimum order quantity. Note that any sequence in which orders arrive will always lead to a state of the order book where either all bids or all offers that are cleared in the auction are also cleared in continuous trading. If this was not the case, at least one bid and one offer which would have been cleared in the auction would remain in the book. By definition the price of the offer is smaller than or equal the auction price and the price of the bid is larger. Hence, the orders should have been cleared in continuous trading, which leads to a contradiction, establishing the claim. □

Observe that continuous trading yields the same outcome as the auction if the orders arrive in pairs sorted according to the marginal welfare gain of matching them, i.e., at

Note that the above argument does not consider block bids or complications in power flow calculations which might lead to computational challenges that cannot be resolved in the short time frames available to clear orders on the continuous intraday market. The incorporation of these aspects might actually reverse the above result in favor of auction markets as for example observed in Neuhoff et al. (2016) for block bids.

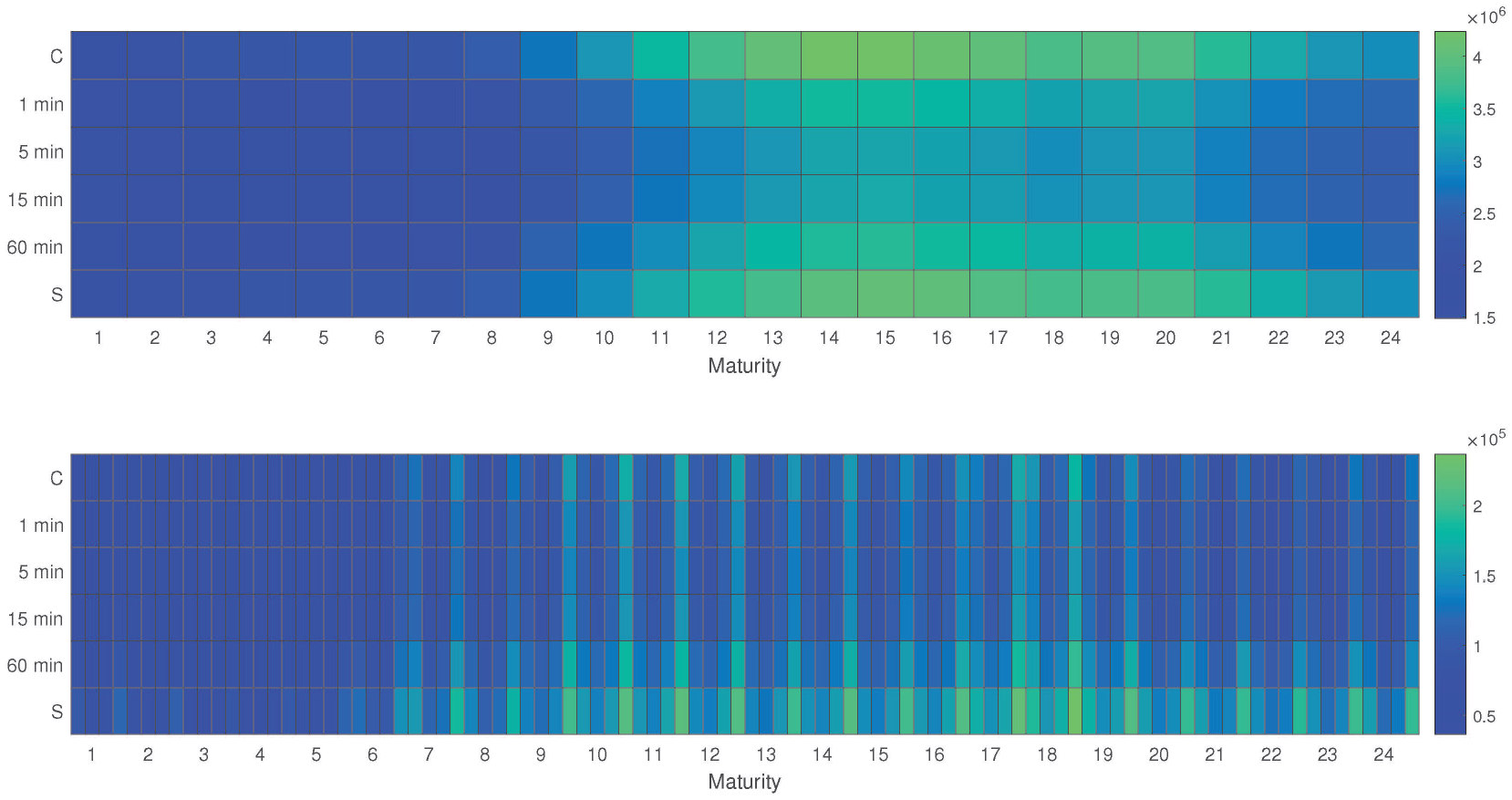

Figure 3 displays heatmaps showing the aggregate traded volumes for all hourly and quarter-hourly products throughout the investigated period and for all market designs. As expected, the figure shows a clear pattern with less trading in the night and morning hours and a volume peak in the afternoon. While Proposition 1 does not do justice to the complexity of repeated auctions, the described effect remains valid and dominates in the numerical examples for hourly products: continuous trading clears slightly more volume than even the single auction, especially in the early afternoon, and significantly more volume than the more frequent auctions. This is all the more the case, since the orders we use to compute counterfactual auction outcomes are generated for continuous trading and consequently the limit prices for many orders are chosen such that they are adapted to the price level at the time of submission and therefore are more or less immediately executed in continuous trading. An analysis for the number of cleared orders instead of the cleared volumes yields similar results.

Comparison of Total Clearing Volumes

For quarter-hourly products the situation is less clear and the effect discussed in Proposition 1 is offset by the fact that we extend the end-validity date of the orders to the end of the auction period and thereby artificially increase the number of active orders relative to continuous trading. Also note that for quarter-hourly products the liquidity is generally lower, which leads to a rather wide bid-ask spread and volatile best-bid and best-ask prices, which in turn results in many orders that are cleared in auctions but not in continuous trading.

Clearly, the effect of the extended end-validity date plays a larger role for the single and the 60-minute auctions than for the auctions with higher frequencies as is also visible from the results in Figure 3, which demonstrate that the two former auctions clear more volume than continuous trading while the latter clear less. However, since the described effect is an artefact of how we compute counterfactual auction results, we conclude that, by and large, volumes in continuous trading tend to be higher than in auctions.

Hence, if the goal of a market design is to generate trading volume, then continuous trading can be considered superior to auctions. However, traded volume is usually not viewed as an end in itself but rather a means to decrease liquidity costs and produce more reliable price discovery.

We will show in the following sections that a transition from continuous trading to frequent auctions would likely positively impact these aspects, even if less volume is cleared. For this reason and since auction trading is easier to handle, especially for smaller market participants who might be overburdened by the complications of a continuous market, we expect that participation and therefore traded volumes would increase relative to our benchmark if an auction based trading regime would be established.

5.3 Liquidity Costs

Liquidity is typically a vague term as, e.g., argued in Schwartz et al. (2020). In order to compare liquidity costs between auctions and continuous trading, we use an approach proposed in Kuppelwieser and Wozabal (2021) who employ a cost of a round-trip (CRT) measure as a surrogate for liquidity cost. The CRT is calculated as the hypothetical cost of buying and immediately selling a certain quantity of electricity and can be calculated for auctions as well as for continuous trading.

In particular, for the continuous market, the buy and sell sides of the LOB are sorted at each point in time t by price to obtain . . .

This allows us to define the CRT measure at time t for a volume V as

In order to deal with spikes in the continuous CRT, we transform CRT t into a discrete measure as proposed in Kuppelwieser and Wozabal (2021). In particular, we define CRT τ at a time point τ by averaging over 15 minutes of CRT t before τ, i.e.,

where

Trading in the German continuous intraday market mostly occurs a few hours before physical delivery. Therefore CRTs of early time periods with little trading are rather high. In order to avoid an upwards distortion of computed CRTs for continuous trading we therefore consider the trading volume-weighted CRT as defined in Kuppelwieser and Wozabal (2021)

where

In order to calculate the CRT for auctions, we add a bid of size V as a market order to the orders of a specific auction k trading a product h and then clear the market obtaining a price

Similar to the CRT for continuous trading, we use cleared volumes as weights in order to calculate the cost of roundtrip

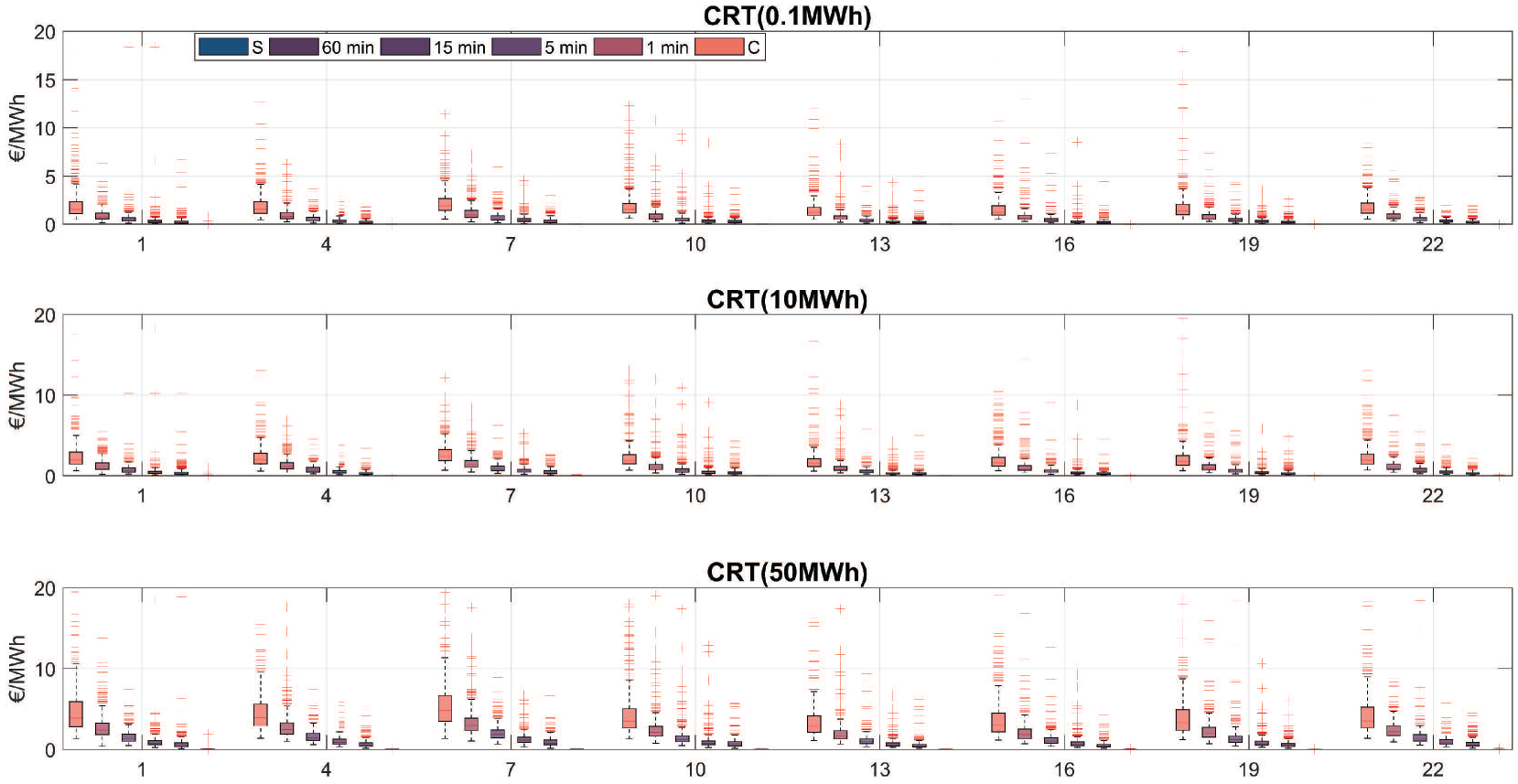

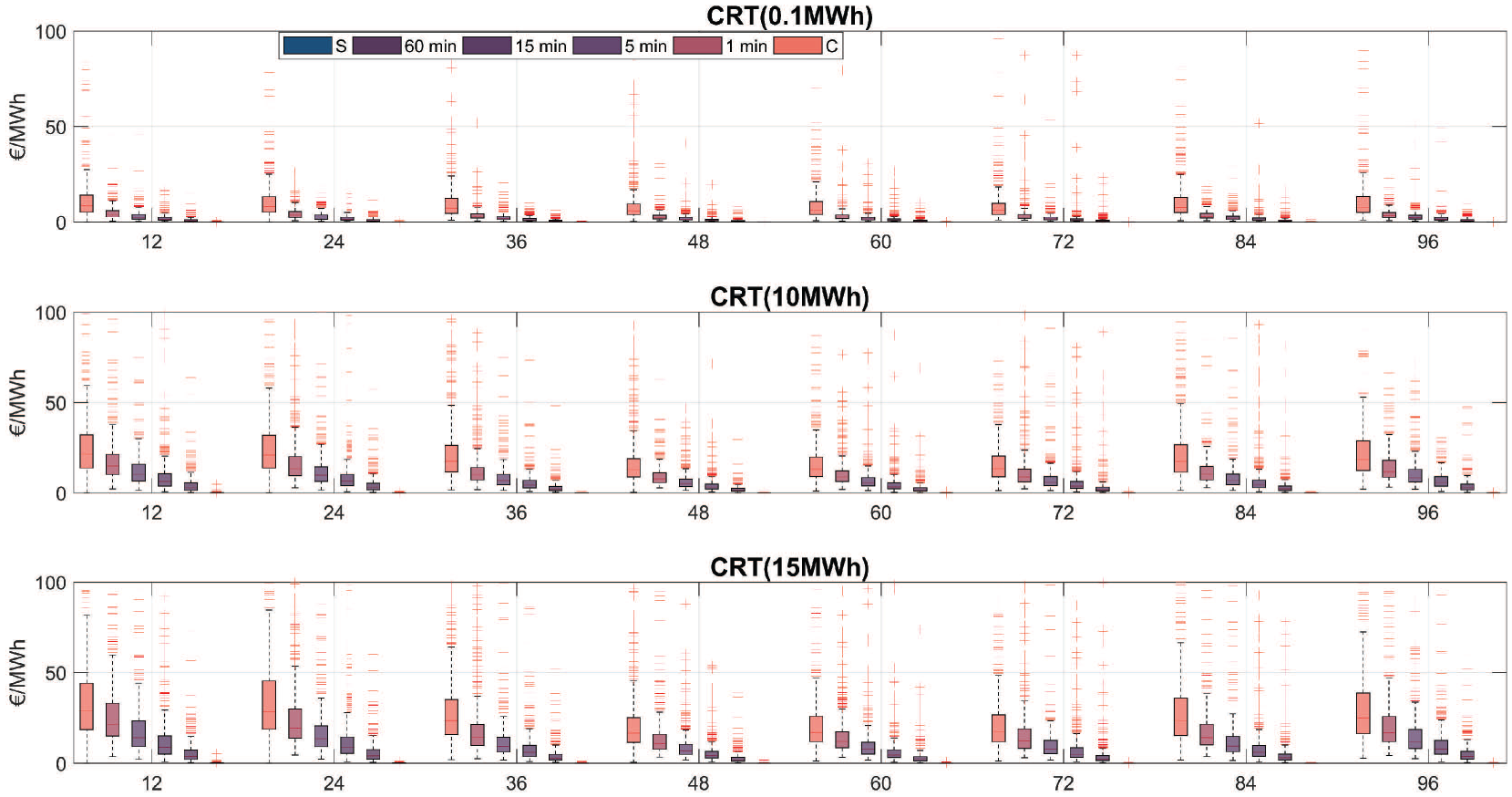

The comparison between auctions and continuous clearing are shown in Figure 4 for hourly products and in Figure 5 for quarter hourly products for selected products (the results for the rest of the products are structurally identical and are therefore not displayed to keep the presentation tractable). The figure demonstrates that CRT costs of continuous trading are significantly higher than that of auctions for hourly products. The analysis shows that especially for

CRT-Costs for Selected Hourly Products for all Market Designs

CRT-Costs for Selected Quarter-Hourly Products for all Market Designs

The lower liquidity cost for auctions based trading would likely increase market participation and traded volumes and therefore further decrease liquidity costs. Hence, lower liquidity cost can be considered one of the main advantages of auction based trading. Especially for products which are less traded such as quarter hourly products.

5.4 Noise versus Signal

The intra-product price path, that is, the price process for a single product between gate-opening and gate-closure during each trading session, can be volatile. Price changes during this period either occur due to arrival of new information, changing the fundamental value of the traded product, or due to noise induced by the trading process itself. While the former is a desirable feature of information processing by the market, the latter distorts this information. Hence, any good market design has to navigate the trade-off between these effects with the aim to maximize the information contained in prices while keeping noise as low as possible.

In order to study this issue for intraday markets prices, we propose to disentangle the price curve into signal and noise. While the constructed signal aims to capture the real underlying values of the product, the noise is defined as the transient deviation of the prices from these values.

To this end, we employ a locally linear regression framework (see, e.g., Hollander et al., 2014) with a normal kernel to decompose intra-product price paths into signal and noise. The principal idea of this framework is to perform linear regression locally at x weighting observations less, the further they are away from x. We focus on the price processes between gate closure and five hours before gate-closure because trading activity in more distant hours from gate closure is typically very low. We round the transaction times of the continuous market as well as the counterfactual market-clearing prices onto a second by second grid with N = 18,000 ticks for the considered five hour period. If there is more than one transaction in a given second before gate-closure, we compute the quantity-weighted average price and if there is no transaction, we fill the missing values with data from the previous second.

The derived price path serves as input to the local linear regressions that we perform for each product. More precisely, for a vector of prices

where

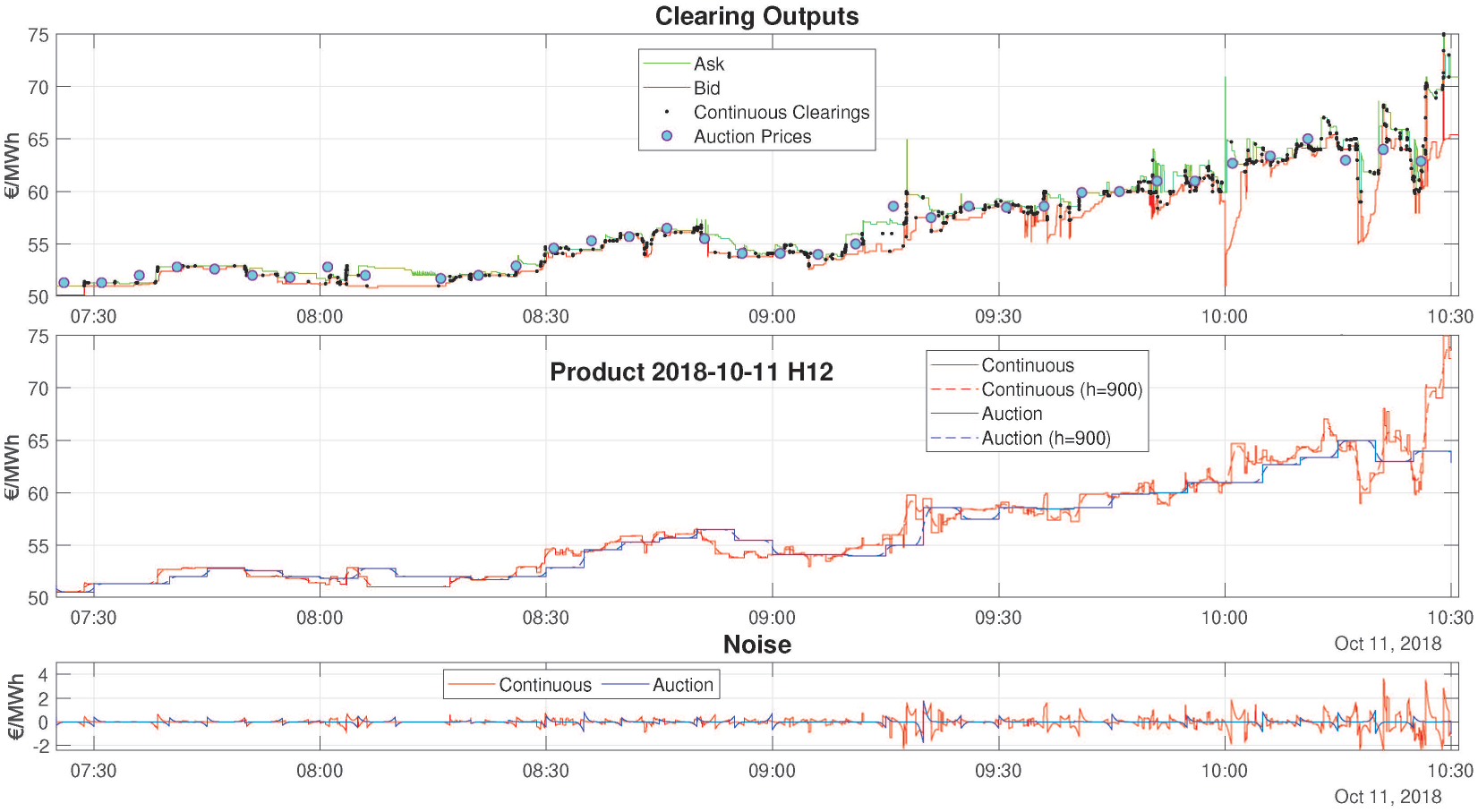

The approach is visualized in Figure 6. At the top panel, we display bid and ask values, executed transactions, as well as counterfactual auction market-clearing prices for the product with delivery between 11:00 and 12:00 on the 2018–10–11 for continuous trading and the 5-minute auction. The solid red line and solid blue line at the panel in the center show the prices for continuous trading and frequent auctions. At the panel in the middle in Figure 6, the dashed red line and dashed blue line represent the extracted signal. At the bottom panel, the noise defined as the difference between the solid and the dashed line is depicted.

Decomposing Price Paths into Signal and Noise for the Hourly Product with Delivery between 11:00 and 12:00 on 2018–10–11

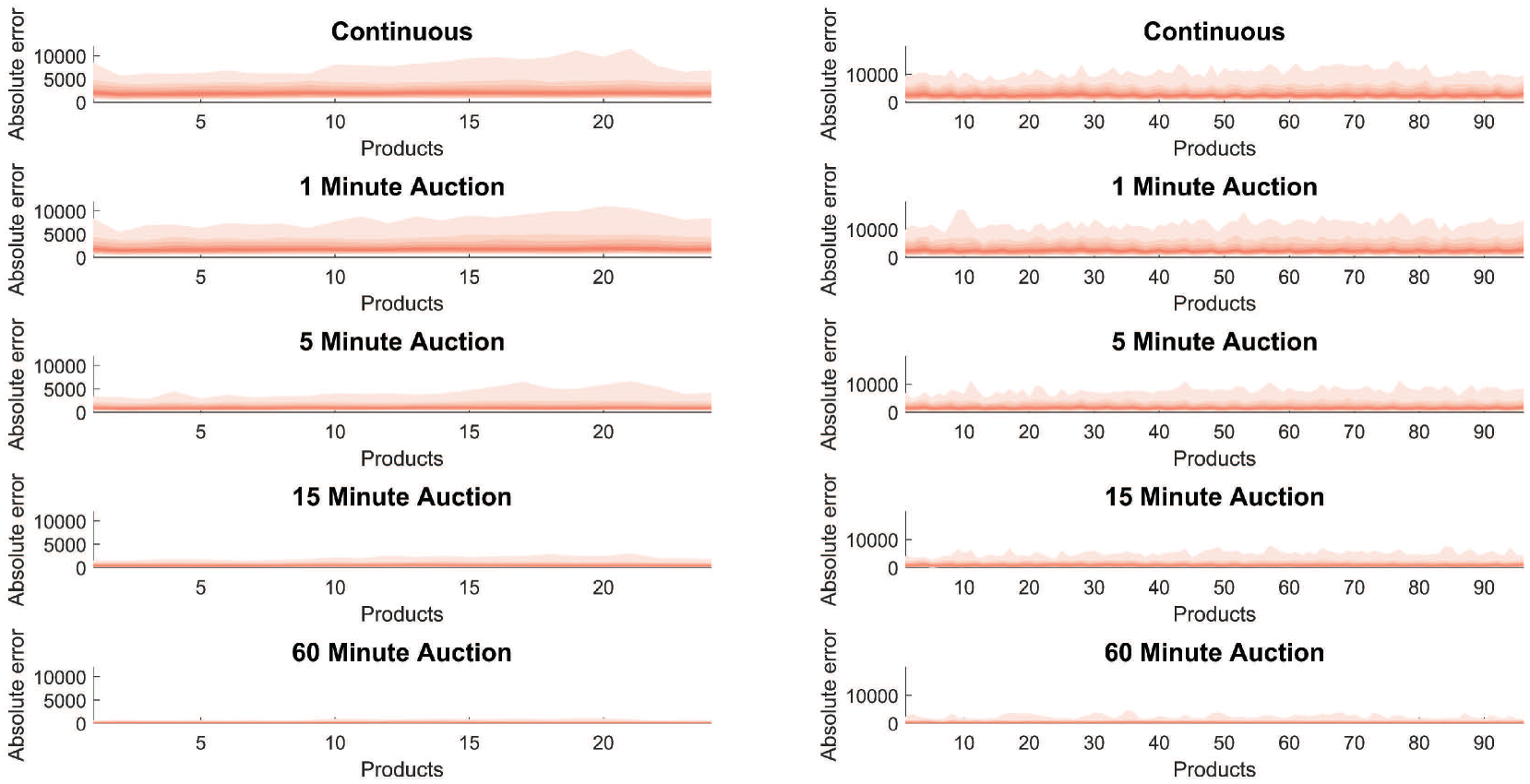

In order to compare the signal-noise trade-off of frequent auctions with continuous trading, we compute the sum of the absolute deviations between price and signal on the grid for all products. Average noise of the price signal decreases in clearing frequency, i.e., continuous auctions have the highest average noise level followed by auctions cleared every minute through auctions cleared every hour. The fan charts in Figure 7 summarize these results comparing different market designs for the hourly market (left column) and the quarter-hourly market (right column). In aggregate, we find that for both product categories, the noise is the largest for continuous trading (hourly products: 2,226.05, quarter hourly products: 2,817.06), followed by auction-clearing (i) every minute, (hourly: 2,041.39, quarter hourly: 2,735.07 10 ), (ii) every five minutes (hourly: 1,034.01, quarter-hourly: 1,695.48), (iii) every 15 minutes (hourly: 518.45, quarter-hourly: 983.19), and (iv) every 60 minutes (hourly: 180.36, quarter-hourly: 383.40). The qualitative interpretation of the results, i.e., that the signal quality is lower for continuous trading and that continuous trading thus leads to noisier price paths compared to auctions, remains unchanged for bandwidths of h = 300 and h = 600.

Fan Chart of Noise with Extreme Percentiles of 1% and 99%

Interpreting the results in the classical framework by Garbade and Silber (1979), we conclude that the chosen auction design decreases the noise from continuous trading while at the same time avoiding high price shocks induced by overly long auction intervals.

5.5 Optimal Auction Frequency

In this section, we condense the findings of the previous sections in order to come up with a recommendation for an optimal auction design. In particular, we are interested in an optimal auction frequency and use welfare as a guiding principle. We note that by the nature of our model it is not possible to fully quantify the welfare implications of different frequencies. However, the literature review in Section 3 as well as our numerical results can nevertheless be the basis of an informed discussion.

The most striking trade off between different auction frequencies is the choice between immediacy and liquidity. Immediacy has positive welfare effects if players have a preference to have their orders cleared quickly, while the lack of liquidity induces a cost of trading, which ultimately results in less transactions and therefore also in less overall welfare.

Especially, the former effect is hard to quantify, since it is nearly impossible to elicit preferences for immediacy from market participants. However, in line with Schwartz (2012), we think that all proposed auction formats are frequent enough and the loss of immediacy is nearly non-existent. On the other hand, our analysis shows that liquidity costs are substantially higher for continuous trading and are sharply decreasing in auction frequency for auction based market designs. More specifically, looking at Figures 4 and 5 it seems that any frequency longer than 5 minutes substantially decreases liquidity cost relative to continuous trading.

Another welfare relevant implication of the choice of a specific auction frequency is the quality of the resulting price signals. If correct, prices provide information about the fundamental value of goods and are the basis for welfare optimal decisions by the participants of the intraday market. On the other hand, if prices do not correctly reflect fundamental values, decisions based on these prices might be sub-optimal from a welfare perspective. Furthermore, in a setting were prices are noisy, market participants may be unsure about their informational content and consequently may be hesitant to trade at all. This could, for example, lead to situations where asset-backed market participants prefer to invest in physical storage capacity to internally hedge their real-time imbalances rather than sharing storage assets in a common market (e.g., Terça and Wozabal, 2021). These effects jointly decrease welfare in case price signals are not reliable. The results of Section 5.4 show that the noise component is substantial in continuous trading and decreases with the auction interval

Another aspect is the quality of market clearing. As argued in Section 2.2 welfare optimal clearing of electricity markets is computationally challenging. Firstly, clearing requires power flow computations in order to arrive at a physically feasible solution that can be supported by the electric grid. Secondly, the nature of some generation plants makes the production of fluctuating outputs rather expensive which necessitates the existence of block bids, i.e., bids for longer, uninterrupted time intervals. This implies that in electricity markets, clearing is more complicated than merely intersecting demand with supply and welfare optimal results cannot be found instantaneously. Instead, the ensuing computations take anywhere between a couple of seconds to several minutes. Since this time cannot be spent in continuous trading, market results may be sub-optimal from a welfare perspective. In contrast, in frequent auctions there is more time for market clearing, which enables better quality market results. In the estimation of the authors, a frequency of 15 minutes or longer would give the market operator enough time to find reasonably good auctions results.

Lastly, as shown in Budish et al. (2015), continuous trading can lead to a prisoner’s dilemma among trading firms that ends up in an socially wasteful arms race for speed in reacting to signals. The benefits of frequent auctions in this context is that this effect vanishes, resulting in increased welfare which is allocated to benefit those market participants that have an actual physical position rather than arbitrage traders. 11 While any auction frequency studied in this paper would avoid the aforementioned prisoner’s dilemma, the 1-minute auction might still be a challenge for some firms in terms of speed. We therefore think that any auction with a frequency of at least 5 minutes would give market participants ample time to react to new information and avoid sniping of stale orders.

Summing up, based on our analysis, we think that, while an auction frequency of 1-minute might still share many of the problems associated with continuous trading, the 5-minute and the 15-minute formats strike a good balance between immediacy and the advantages of auctions in terms of reduced liquidity cost and the quality of the price signal and the market results.

6. Conclusion and Policy Implications

In this paper, we investigate the use of frequent auctions for intraday electricity markets. The proposed design can be seen as a compromise between continuous trading, the de-facto standard in European intraday markets, and infrequent auctions as they have been used for some time in countries such as Spain, Italy, or Greece. Ideally, frequent auctions decrease liquidity costs and improve the quality of the price signal relative to continuous trading, without severely limiting electricity traders to react quickly to new information over infrequent auctions.

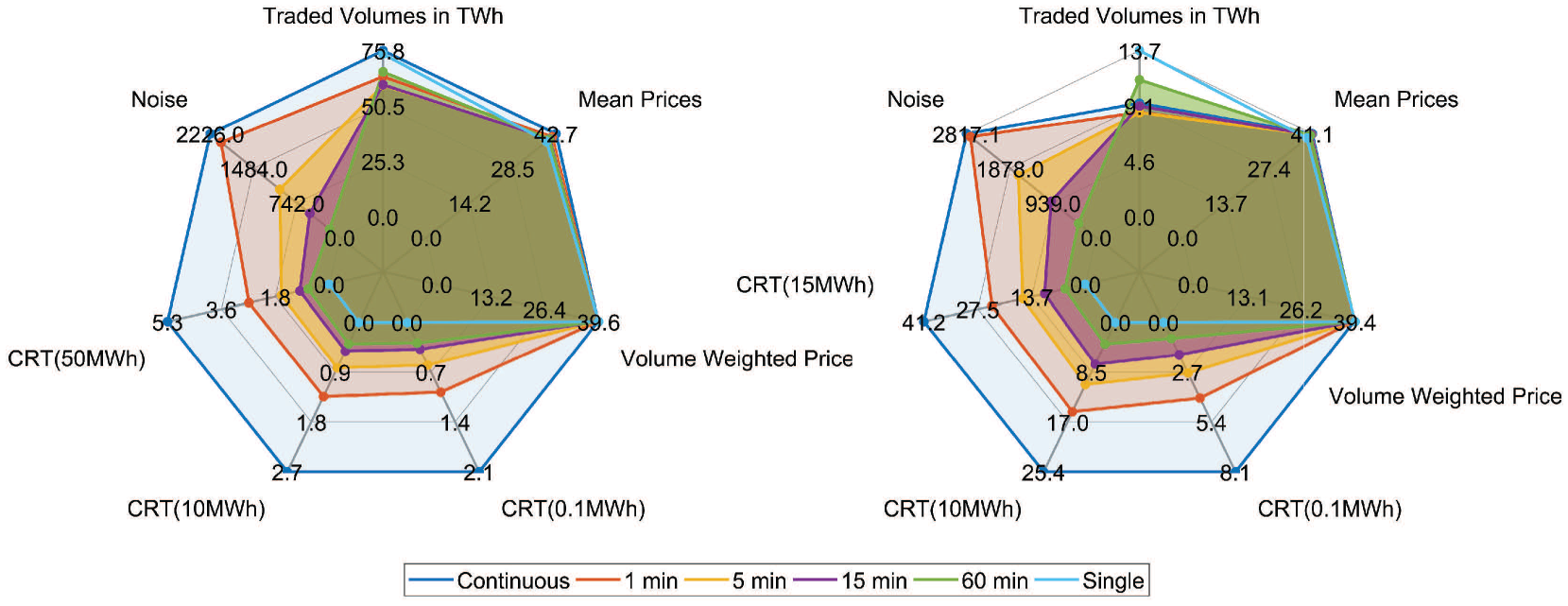

We construct counterfactual auction outcomes from historical limit orders submitted to the German continuous market to investigate how prices, traded quantities, liquidity costs, and the signal to noise ratio of the price process would change if the market design was to transition to frequent auctions. We summarize the results of the resulting numerical comparison Figure 8.

Overview of Results for Prices, Traded Quantities, Noise, and Liquidity Costs for Hourly and Quarter-Hourly Products

We find that average and volume-weighted prices do not significantly differ between the two market designs. Our findings are ambiguous for traded volumes: uniformly lower volumes in auctions for hourly products and higher volumes for most auctions of quarter-hourly products. However, the latter effect is an artefact of how we construct the counterfactual auction outcomes so that we conclude that overall auctions lead to less traded volume, which is also supported by theoretical considerations in Proposition 1.

Despite the decreased volumes, the cost-of-roundtrip markedly decreases for all considered auctions, i.e., liquidity costs are higher for continuous trading. Finally, looking at the measurement of noise in the price signal, we observe that auction based trading produces more robust and reliable price signals that are less affected by transient short-term shocks that are not connected to fundamental changes of the value of the traded product.

Overall and in accordance with Deutsche Börse Group (2018), Ehrenmann et al. (2019), and Ocker and Jaenisch (2020), we conclude that the proposed auction design to a large extent captures the advantages of both continuous trading and auctions. In particular, the fact that auctions are frequent and the last auction takes place close to delivery mitigates the disadvantages of previously existing auction systems which had only few auctions with the last one closing several hours before physical delivery.

Furthermore, auctions give the clearing authority the possibility to account for the realities of the restrictions imposed by the physical properties of electricity grids: An auction based intraday market design would allow for more time to clear the market, making it possible to price cross-border capacities implicitly and making it easier to integrate block orders. Overall, if the market design is chosen carefully, we thus believe that prices would more accurately reflect true scarcity rents and would thus be more closely connected to prices on the balancing market.

Lastly, on an administrative level, auctions are simpler allowing more participants to take part in trading. This is especially true, since day-ahead markets, which most market participants are familiar with, are also organized as auctions. Furthermore, since orders are batched over longer time periods, there are no speed advantages for advanced traders and therefore no possibility for latency arbitrage in an auction based market.

An interesting topic for further research, would be whether a combination between auctions and continuous trading outperforms both extremes. In such a design, auctions could improve liquidity at times when there is little trading, typically long before delivery, and ensure a high immediacy when the market is sufficiently liquid. These ideas are implemented in stock markets that combine continuous trading during the day with opening/closing auctions (Schwartz, 2012) as well as, for example, in the current Spanish and Italian intraday market designs which feature both auctions and continuous trading.

Footnotes

Acknowledgements

Christoph Graf gratefully acknowledges financial support from the Austrian Science Fund (FWF), J-3917, and the Anniversary Fund of the Oesterreichische Nationalbank (OeNB), 18306.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.