Abstract

As an important choice of strategic transformation of energy enterprises, digital transformation has a profound impact on the stock price fluctuation of enterprises. From the perspective of dynamic capacity and environmental regulation, analyzes influences of digital transformation upon energy companies’ share movement volatility, constructs a theoretical model that considers digital transformation and stock price volatility as the primary effects, dynamic capabilities as the mediator, and environmental regulation as the moderator. In addition, the study employs data from China’s A-share listed energy enterprises from 2013 to 2020, utilizing a fixed-effect model to perform an empirical test. The findings demonstrate a significant positive correlation between the digital transformation of energy enterprises and the volatility of stock prices, indicating that the greater the extent of digital transformation, the higher the volatility of enterprise stock prices. Among the dimensions of dynamic capability, only adaptability and innovation ability appears to mediate the relation between digital transformation and stock price fluctuation. Moreover, environmental regulation positively moderates the relationship between digital transformation and the learning ability dimension. Finally, from the macro and micro levels, this study puts forward the policies and supportive measures to stabilize the stock price of energy enterprises, and suggestions on how to implement the digital transformation strategy reasonably according to their own development status and characteristics to provide valuable insights for encouraging the digital transformation among energy firms.

Keywords

Introduction

As the digital economy advances rapidly, digital technology has gradually emerged as the premier instrument [1] for China to attain the objective of achieving carbon neutrality. China, being the world’s leading energy producer and consumer, has a perpetual energy supply that is vital in ensuring top-notch development. The energy sector, being a decisive factor in China’s economic development, has, however, emerged as the sector with the highest carbon emissions in the country, which poses a significant threat to both the ecological environment and social development. In the context of carbon neutrality, it is necessary to reduce carbon emissions by adopting digital transformation, which is based on digital technology. Digital transformation, which is an integral phase for enterprises in adhering to the Industry 4.0 developmental law, should be reflected in the capital market activities [2] to some extent, thereby affecting the stock prices of enterprises.

At present, the research on the correlation between digital transformation and enterprise stock price mainly focuses on two aspects: stock price crash risk and stock price fluctuation. The former mainly studies the inhibition effect of enterprise digital transformation on the risk of stock price collapse [3] and the nonlinear relationship [4], while the latter examines the internal mechanism of digital transformation exacerbating stock price volatility. Research shows that digital transformation will directly improve the quality of accounting information of enterprises, improve the system and quality of internal control information disclosure, reduce the occurrence of information asymmetry between enterprises and market investors, form governance effects on enterprise information disclosure, and enhance the ability of enterprise risk control and risk prevention. Therefore, enterprises with a higher degree of digital transformation, The lower the risk of a stock price crash [5]. Other studies have found that the impact of digital transformation on stock price crash risk presents an inverted U-shaped trend of first aggravating and then restraining. Moreover, while the impact of digital transformation on stock price crash risk is influenced by increasing agency costs and cultivating management’s overconfidence, the impact of digital transformation on stock price crash risk is also different among different types of enterprises, and the impact is more obvious in small and non-high-tech enterprises. As digital transformation advances, large enterprises and high-tech enterprises can benefit from its positive empowering effects more quickly.

According to the existing research results, the influencing mechanism of the relationship between digital transformation and stock price volatility of enterprises is still unclear, the research perspective is single, and the relevant research literature is not rich enough. Based on this, this study takes Chinese energy companies listed on the main board of Shanghai and Shenzhen Stock Exchange as samples to test the impact of digital transformation on stock price volatility theoretically and empirically. Compared with the existing literature, the marginal contributions of this paper are as follows: First, in view of the environmental turbulence faced by the digital transformation of energy enterprises and the continuous strengthening of the state’s environmental control, environmental regulation is introduced as the regulatory variable and dynamic capacity is introduced as the intermediary variable, which is a beneficial supplement to the internal impact mechanism of digital transformation and stock price volatility, and enriche relevant research; Second, existing literature has not analyzed the impact on stock price volatility based on the perspective of digital transformation of energy enterprises. This study not only expands the research perspective on stock price volatility, but also helps to find new factors to stabilize stock price volatility of energy enterprises. Third, through the analysis of the impact mechanism and action path of digital transformation on stock price volatility, more accurate suggestions are provided for energy enterprises to implement digital transformation and market investors to invest in energy enterprises with digital transformation.

Impact mechanism analysis and hypothesis proposal

Impact mechanism analysis

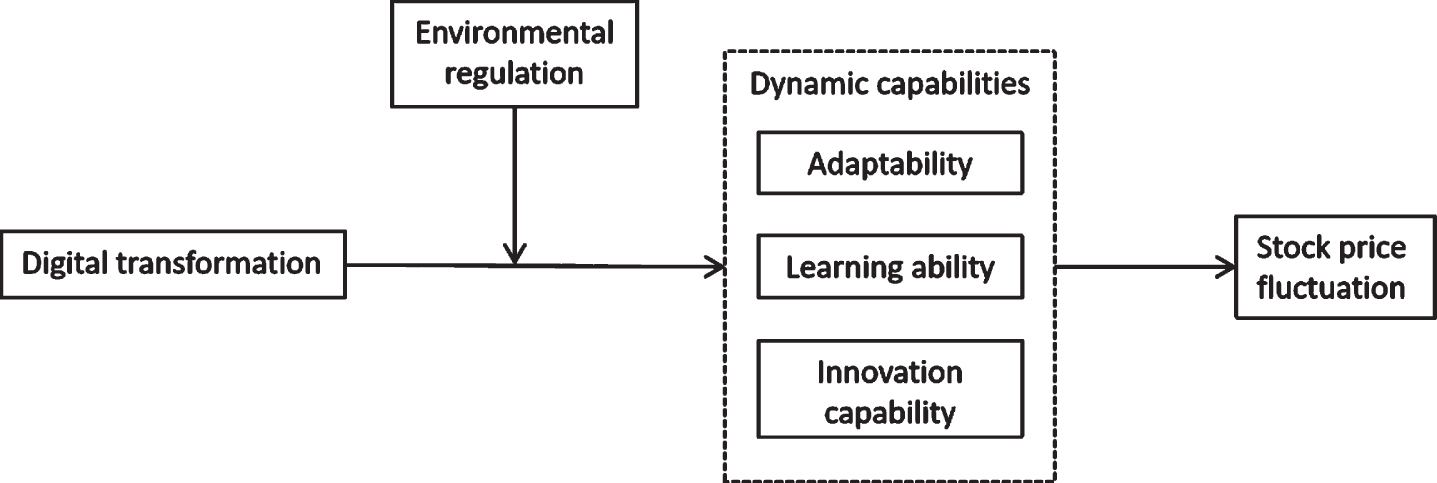

The dynamic capability theory is predicated on the resource-based theory and the enterprise capability theory, offering a framework that elucidates how enterprises can enhance their ability to adapt dynamically to their environments, effectively responding to shifts in external technologies and markets [6]. Teece (1990), a prominent American scholar, was the first to introduce the concept of “dynamic capability,” defining it as an enterprise’s capacity to tackle complex environmental changes by means of internal and external resource integration, construction, and ultimate reassignment. Early research into dynamic capabilities focused on product development, technological innovation, strategic management, and industrial development. However, recent digital transformation research indicates that digital transformation can reshape an enterprise’s dynamic capabilities [7]. The foundation of digital transformation is rooted in the dynamic capabilities of enterprises [8], and digital transformation has the same impact as the learning dimension of dynamic capabilities. Meanwhile, digital transformation is highly intricate and uncertain. Enterprise dynamic capabilities serve as a means to navigate uncertain environments and explain how enterprises respond to technological and market changes. Research indicates that the effective implementation of dynamic capabilities into an enterprise’s digital transformation strategy is the fundamental driver for building dynamic capabilities, finally promoting overall digital transformation, enhancing operational efficiency and effectiveness [9]. This, in turn, enables enterprises to attain and maintain sustainable competitive advantages. Therefore, the dynamic capability theory presents an effective dimension for analyzing the relationship between enterprise digital transformation and stock price fluctuations. Firstly, digital transformation typically stimulates the evolution of enterprises’s dynamic capabilities. Secondly, dynamic capabilities ensure that enterprises gain a competitive advantage, and the fluctuation of an enterprise’s stock price is a key external manifestation of competitive advantage [10]. Building on this, the study draws on Wang et al.’s (2007) [24] categorization of dynamic capability dimensions (i.e. adaptability, learning ability, and innovation ability) to explore issues related to digital transformation (see the theoretical framework diagram in Fig. 1).

Frame model.

In accordance with the law of development, companies are bound to undergo the phase of digital transformation, wherein their concepts of ingenuity and effectiveness will indubitably manifest themselves through the fluctuations in the capital market’s stock prices [11]. Firstly, from the vantage point of the financial infrastructure, most corporations possess a limited lifespan, making it arduous to comply with the financing requirements of the capital market. The process of digital transformation can stimulate the establishment and expansion of the enterprise credit system, thereby ameliorating the restraints that impede companies from acquiring adequate funding [12]. The aggravation of funding restraints frequently elevates the probability of a decline in stock prices [13]. As such, the digital transformation process can indirectly stabilize stock prices. Secondly, by means of digital transformation, corporations have significantly enhanced their capacity to excavate internal and external data, refine their ability to process and assimilate external data, and expedite the upgrade of their products and services in response to market development trends, with the ultimate goal of augmenting the innovative impetus of the companies [14]. This approach effectively averts the market shocks stemming from environmental uncertainty, consequently precluding substantial fluctuations in stock prices. In addition, research has demonstrated that in the event of a public crisis emergency, digital transformation strategies can alleviate the impact of systemic shocks on enterprise stock price volatility, thus curtailing the recovery time for companies [15]. According to the aforementioned investigation, the following hypothesis is proposed:

Hypothesis 1a: Digital transformation of energy enterprises can significantly reduce stock price volatility.

However, digital transformation can yield adverse effects on corporations. Initially, the costly investment in the short run of digital transformation may impair the functioning of corporations and engender negative information, exacerbating the level of asymmetry between corporations and the external world. Consequently, this can influence the fluctuations in stock prices in the capital market [16]. Secondly, at this juncture, corporations are still confronted with various impediments in executing digital transformation, including deficient managerial skills, inadequate data accessibility, limited resources, and technical competencies [17]. Additionally, there are environmental uncertainties linked to public administration in the public sector [18], which obstruct the execution of digital transformation strategy and relegate digital labor to the periphery, thereby creating a divergence between the sustained execution of the strategy and the first hypothesis [19]. The confidence of investors in investments has been shaken, leading to a loss of trust in corporate stocks. If a significant amount of selling occurs within a short time frame, it is likely to cause substantial fluctuations in stock prices [20]. Finally, corporate executives frequently display eagerness to undertake extensive investments and anticipate successful accomplishment of complete digital transformation. They execute technological changes without formulating a comprehensive digital transformation plan [21]. This may result in the failure of digital transformation and consequent operational risks such as investor divestment, thereby having a certain impact on corporate stocks [22]. In conformity with the preceding investigation, this study posits the hypothesis as follows:

Hypothesis 1b: The digital transformation of energy enterprises can significantly enhance stock price volatility.

Mediation of dynamic capabilities

The significant function of dynamic abilities [23] in the course of digital transformation has been extensively discussed in the available literature. Its importance lies in maintaining a competitive advantage for enterprises. The adaptability factor can impact the fluctuation of enterprise stock prices due to digital transformation. Enterprises must have the ability to reallocate their resources to identify and seize opportunities, which is referred to as adaptability. Digital transformation may meaningfully enhance the efficiency of information process and circulation. Additionally, digital technology has the capability to revolutionize the business model and innovation system that enterprises rely on. The utilization of more advanced tools enables enterprises to design, produce, and provide support for products and technological innovations across the entire organization, thereby facilitating the enhancement of enterprise adaptability [25]. The adaptability of enterprises in an unpredictable environment, such as the capital market, is frequently demonstrated by the fluctuation of monthly closing prices of their stocks [26]. Additionally, adaptability is the foremost factor in stabilizing the stock market. In the absence of robust adaptability, the introduction of digital technology alone cannot be integrated into enterprise organizational operations and innovation methods, nor can it be manifested in the fluctuation of enterprise stock prices. According to the foregoing investigation, this study makes the subsequent hypothesis:

Hypothesis 2a: Adaptability plays a mediating role in the relationship between digital transformation of energy enterprises and stock price fluctuations.

Through its learning ability, digital transformation has the potential to influence the fluctuation of enterprise stock prices. Learning ability refers to an enterprise’s capability to recognize, assimilate, and convert internal knowledge while effectively utilizing external knowledge. The digital transformation of enterprises promotes continuous activation, assimilation, and updating of knowledge to achieve objectives such as quickly seizing innovative opportunities, resource restructuring, and enhancing enterprise capabilities [27]. As the digital ecosystem becomes increasingly prevalent, the boundary between an enterprise’s internal and external environment becomes progressively indistinct. This leads to the achievement of interactive learning effects between internal cognition and external environment. By assimilating and integrating substantial amounts of information and knowledge from digital transformation, operational capabilities that support digital transformation can evolve into high-dimensional dynamic capabilities, resulting in the driving of enterprise innovation. In addition, digital transformation is continuously refined through ongoing exploration and experimentation. The learning ability is capable of evaluating potential business opportunities, innovative businesses, and business models, as well as diagnosing potential risks associated with digital transformation for enterprises. This helps to enhance their ability to prevent and effectively avoid any hidden crises during their transformational period, ultimately mitigating any negative impact on enterprise innovation performance [28]. Additionally, innovation activities often have a significant effect on enterprise stock prices [29]. Given the aforementioned analysis, this study postulates the following hypothesis:

Hypothesis 2b: In the relationship between digital transformation of energy enterprises and stock price fluctuations, enterprise learning ability plays a mediating role.

Through its innovation ability, digital transformation has the potential to impact the volatility of stock prices for enterprises. This ability refers to an enterprise’s capacity to create new products and models to explore new markets. According to research, digital transformation has the potential to optimize an enterprise’s organizational structure, improve the efficiency of information transmission and innovation potential, and finally boost its innovation capability [30]. The innovation ability of an enterprise comprehensively reflects its market competitiveness, profitability, and development prospects. This will inevitably influence the intrinsic value of their shares, investors’ psychological expectations, and their trading decision-making behavior. Consequently, different stocks may exhibit varying price fluctuation trends even when subjected to the same systemic risk wave [31]. A separate study demonstrated that during a financial crisis, an enterprise’s innovation capability can positively impact the excess returns of the stock market and can significantly bolster economic stability and investor confidence [32]. Based on the preceding analysis, this study postulates the following hypothesis:

Hypothesis 2c: innovation capability plays a mediating role in the relationship between digital transformation of energy enterprises and stock price fluctuations.

The regulatory role of environmental regulation

The ultimate objective of environmental regulation is to safeguard the environment, and it primarily takes the form of a tangible system and intangible consciousness that serves as a restraining force [33]. Studies reveal that environmental regulation not only has a direct impact on the production and consumption of energy but also changes the conduct of energy companies and advances the adjustment of the industrial structure by controlling the supply side [34]. However, when environmental regulation becomes excessively stringent, it can impose a considerable burden on energy enterprises, and hinder the enhancement of ecological efficiency by reducing productive investments [35]. Therefore, environmental regulation can regulate the relationship between digital transformation and dynamic capabilities to a certain extent.

First and foremost, the factor price of polluting production may increase due to environmental regulation, compelling enterprises to make strategic adjustments. When environmental regulation benchmarks reach a particular threshold, the industry actively upgrades its overall operating structure, compelling it to shift towards a low-carbon direction [36]. For technology and knowledge-intensive industries, it is necessary to conduct digital transformation proactively. By utilizing advanced digital technology, the status of highly polluting industries can be enhanced while promoting the implementation of corporate social responsibility [37]. Secondly, environmental regulation policies have been introduced by the government to regulate the conduct of enterprises. To evade penalties, enterprises frequently endeavor to improve their production and disposal processes in a scientifically efficient manner, alter their technical routes, consumer demands, and competitive environment, whilst the business ecosystem and value chain system continue to evolve dynamically [38]. The change of environmental regulation frequently results in the disparity between the external environment and the capabilities of enterprises. This necessitates the adjustment and restructuring of internal and external capabilities to adapt to the rapidly changing regulatory environment. The “Porter Hypothesis” postulates that environmental regulation serves as a catalyst for promoting enterprises’ innovative behavior. This is mainly because enterprises can effectively surmount their own resistance in the face of external pressure triggered by environmental regulation and convert external environmental protection policy pressure into a driving force for innovation [39]. Furthermore, environmental regulation mandates enterprises to enhance their dynamic capabilities continuously through organizational learning [40]. Several studies have demonstrated that organizational learning plays a critical role in stimulating the evolution of dynamic capabilities in response to environmental regulation [41]. Based on the above analysis, this study posits the following three hypotheses:

Hypothesis 3a: environmental regulation can positively regulate the relationship between digital transformation and adaptability of energy enterprises.

Hypothesis 3b: environmental regulation can positively regulate the relationship between digital transformation of energy enterprises and learning ability.

Hypothesis 3c: environmental regulation can positively regulate the relationship between digital transformation and innovation capability of energy enterprises.

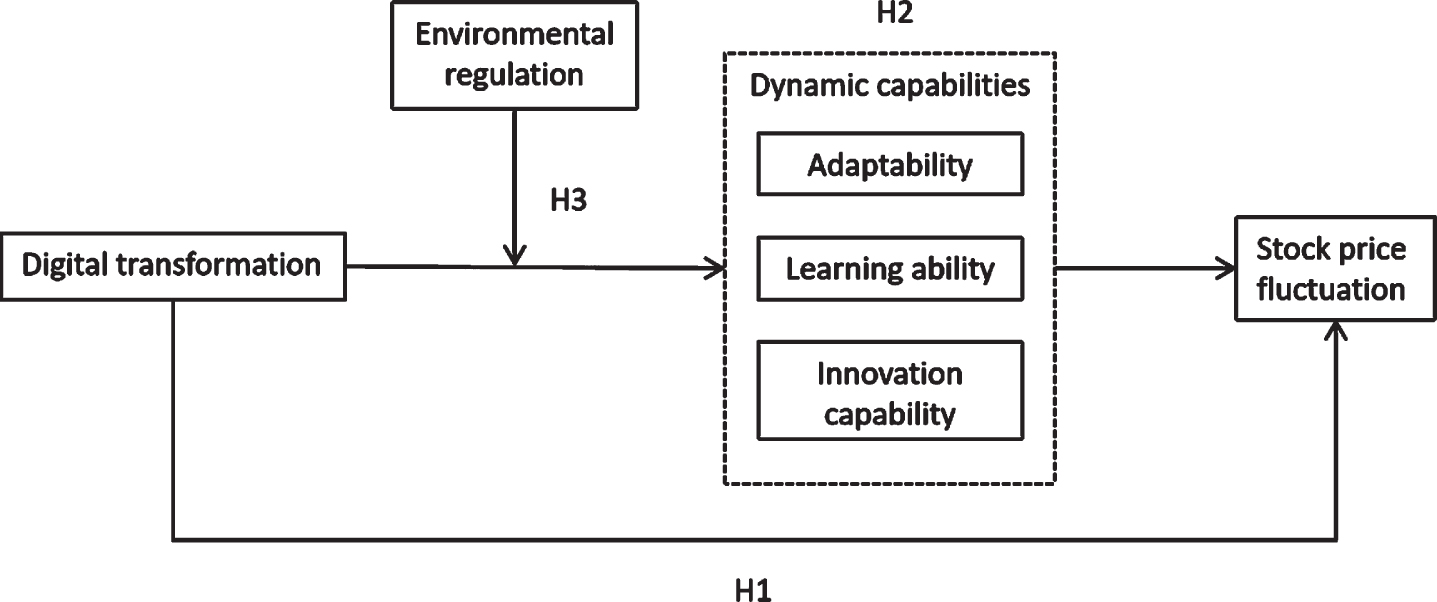

To elucidate, the research framework model of digital transformation and stock price fluctuation of energy enterprises built by the Institute is shown in Fig. 2.

Research framework.

Sample selection and data source

The impact of digital transformation on the volatility of stock prices in Shanghai and Shenzhen A-shares of energy enterprises is explored in this study, by measuring the pertinent indicators. In 2013, the notion of Industry 4.0 was proposed, and subsequently, digital transformation gradually assumed the central position in the strategic choices of companies. With the introduction of dual carbon objectives and the concomitant policies, energy enterprises commenced the exploration of the digital transformation path in various sub-industries. The digital transformation process involved the creation of comprehensive data streams, the deep integration of big data, the Internet of Things, and other digital technologies. This led to the growing enthusiasm for intelligent operation and digital transformation. Therefore, this study collects data according to the latest list of listed energy enterprises provided by CSMAR Database, and comprehensively considers the availability of data and other factors, and finally chooses 2013-2020 as the sample interval.To ensure the reliability of the statistical data, samples that do not satisfy the following conditions are excluded: (1) companies lacking the relevant indicator data; (2) those affected by outliers, including ST and *ST, firms that were delisted or IPOed during the study period; (3) companies listed on the Beijing Stock Exchange, as well as B shares and H shares, are excluded, and only energy enterprises listed in A shares are considered; (4) to eliminate the interference of abnormal values, a 1% and 99% tail shrinking treatment is applied to continuous variables. Enterprises that have attained a certain industrial scale and are highly representative in the industry are selected, resulting in 1395 panel data samples from 211 enterprises.

Variable selection

Interpreted variable

Direct observation of the fluctuation in stock prices is not feasible. Instead, the annualized volatility is a widely-used measure that objectively reflects enterprise risk and represents the most effective way to evaluate the volatility risk of investment targets. To ensure data availability and indicator representativeness, this research has adopted the techniques employed by Cheng Fei and Zhang Qingjun [42], Liu Jinyin and Song Dan [43]. Specifically, the annual volatility (Vola) has been selected to gauge the stock price oscillations of publicly-traded firms. The standard deviation (Mstdev) of monthly stock return rate, excluding cash dividend reinvestment, has been chosen as the benchmark. Consequently,

Explanatory variable

At present, the measurement of digital transformation is categorized into two types. The first method is based on word frequency, where annual reports crawl keywords to analyze digital transformation. Wu Fei [2] represents this approach. The second approach was proposed by Zhang Yongshen [44] that measures the digital transformation of enterprises based on the percentage of digital technology intangible assets in intangible assets. Considering the current situation of investment in digital transformation by energy enterprises, and to quantify the degree of digital transformation more accurately, this study refers to the measurement method of Zhang Yongshen et al. For instance, when the details of intangible assets contain keywords related to digital technology such as “software,” “network,” and “smart platform,” those detailed items are defined as intangible assets of enterprise digital technology. Subsequently, these items are summarized, and the proportion of total intangible assets for the year is calculated.

Intermediary variable

The utilization of cross-sectional data collected through questionnaires in previous studies failed to capture the progression of dynamic capabilities of enterprises over time. Hence, this study has adopted Yang Lin et al.’s measurement technique [45] to assess the three dimensions of dynamic capability using time series data. To quantify the adaptability of enterprises, Ad represents the negative value of the coefficient of variation of annual R&D and capital expenditure of the sample enterprises, which reflects the ease of resource allocation. The learning ability of enterprises is evaluated by the method of Zhang Jichang and Long Jing [25], using the ratio of annual R&D investment and operating income of the enterprise and represented by DC Ab. To determine innovation capability, the study uses the two indicators of annual R&D investment intensity (total R&D investment/total assets) and the proportion of technical personnel of the sample enterprises, which are standardized separately, and then aggregated to obtain the comprehensive value of innovation capability. The innovation capability is represented by DC In.

Regulating variable

Strengthening the stringency of environmental regulations will inevitably result in increased investment costs for energy firms. In light of this, the research adopts the measurement method proposed by Cui Guanghui and Jiang Yingbing [46], which uses the level of environmental protection investment made by enterprises as a proxy for their compliance with environmental regulations. This measurement encompasses both capital and expenses. The former comprises expenses related to the purchase and renewal of emission reduction equipment and environmental protection production lines, which are primarily categorized under the construction in progress section of the financial statements. The latter consists of expenses related to pollution discharge, greening fees, and environmental management system certification fees, primarily categorized under the “management fees” item in the balance sheet.

Control variable

To avoid potential measurement inaccuracies arising from the omission of crucial variables, and given that digital transformation entails a resource-intensive and high-cost endeavor [47], solely organizations possessing the requisite resources and capabilities can undertake such transformations [48]. Consequently, this study incorporates additional potential variables that might exert influence on the “digital transformation - stock price fluctuation” trajectory, employing these as control variables. For instance, the size of an organization is denoted by the natural logarithm of the total assets held by the sample company at the conclusion of the period; nature, a categorical variable, assumes a value of 1 for state-owned enterprises, 2 for private enterprises, 3 for foreign-funded enterprises, and 4 for other entities; the geographical location of the organization is categorized into three distinct economic zones; the age of the organization is ascertained by the number of years since its establishment; the top side, gauged by the ownership proportion of the largest shareholder; the stock turnover rate, calculated as the aggregate of daily turnover rates within a given year divided by the trading days of stocks within that same year; and the return on equity (ROE), expressed as the ratio of net profit to net assets (Refer to Table 1 for a comprehensive overview).

Variable definition and measurement

Variable definition and measurement

To verify the direct impact of digital transformation on stock price volatility, the mediating effect of firm dynamic capabilities, and the moderating effect of environmental regulation, based on mediating and modulating effect models [53] the research established the subsequent reference model for empirical testing:

In the benchmark regression model, i represents the firm and t represents the time period; Vola (stock price fluctuation) is the dependent variable; Digital serves as the primary explanatory variable; Mediator stands for the intermediary variables’ three dimensions of dynamic capabilities; Ers functions as the regulatory variable. Model (1) represents an empirical formula that test hypothesis 1; the combination of Model (1), Model (2), and Model (3) can test hypothesis 2, while Model 4 can assess hypothesis 3.

Descriptive statistics and correlation analysis

The descriptive statistics of the main research variables are presented in Table 2. Among these, the minimum and maximum values of energy enterprise’s share price fluctuation (Vola) are 0.650 and 1.950, respectively, with a standard deviation of 0.262, signifying the fluctuating nature of the sample enterprise’s share prices. Digital transformation displays a minimum value of 0.000 and a maximum value of 1.030, with a standard deviation of 0.399, implying differences in the degree of digital transformation among sample enterprises. The minimum value of adaptability is -1.690, with a mean value of -0.667 and a standard deviation of 0.460, indicating an appropriate adaptability level among sample enterprises, with certain differences in resource allocation. The average value of learning ability is 2.048, with a maximum value of 9.230 and a standard deviation of 2.217, signifying an average R&D investment intensity of 2.048% among sample enterprises, with significant disparities. The average value of innovation capability is 0.198, with a maximum value of 1.4 and a standard deviation of 0.255, indicating a relatively high level of innovation capability among sample enterprises.

Descriptive statistics of variables

Descriptive statistics of variables

Table 3 displays the correlation coefficients of the main variables in this paper. The correlation coefficient between enterprise digital transformation and stock price fluctuation is 0.793, surpassing the 1% significance level test, affirming a positive correlation between digital transformation and enterprise stock price fluctuations. Hypothesis 1b is preliminarily verified. The correlation coefficients between enterprise digital transformation and adaptability, learning ability, and innovation ability are 0.250, 0.142, and 0.174, respectively, passing the 1% significance level test. This implies a positive correlation between enterprise digital transformation and innovation ability, learning ability, and adaptability. The correlation coefficients with enterprise stock price fluctuation are 0.273, 0.163, and 0.182, also surpassing the 1% significance level test, indicating a significant positive correlation between the three dimensions and the volatility of enterprise stock prices. The correlation coefficient between digital transformation and environmental regulation is 0.033. In addition, the correlation coefficients between environmental regulation and adaptability, learning ability, and innovation ability are -0.047, 0.210, and 0.089, respectively. Among all the variables, only learning ability passes the significance level test of 1%. As environmental regulation increases the cost of pollution control for enterprises, it drives energy enterprises to continually enhance their learning ability. Simultaneously, the innovation effect stimulated by environmental regulation can undoubtedly aid enterprises in boosting their learning ability.

Correlation coefficient matrix of main variables

Note: * means p < 0.1, ** means p < 0.05, ** means p < 0.01. The same below.

Table 4 displays the results of the regression analysis concerning the impact of digital transformation on stock price volatility. The regression coefficient of the digital transformation index (Vola) is 0.509, which passes the 1% statistical significance test. When the control variable (M (2)) is added to model M (1), the relevant regression coefficient of digital transformation decreases, implying that the added control variable could have absorbed some factors that influence stock price volatility. Despite this, the significance of the correlation between digital transformation and stock price volatility remains unchanged. Thus, it can be concluded that there exists a positive and significant correlation between the degree of digital transformation of enterprises and the fluctuation of their stock prices. As the process of digital transformation in energy enterprises is time-consuming and requires a substantial investment, it encompasses considerable risks and may not demonstrate its effect in the short term. Nonetheless, it has a substantial impact on the stock market [49]. Based on the empirical evidence, hypothesis 1b is supported.

Digital transformation of enterprises and stock price fluctuation

Digital transformation of enterprises and stock price fluctuation

Table 5 displays the findings from the experiment conducted to determine the intermediary effect of dynamic capabilities upon the correlation between enterprise digital transformation and share price fluctuations. Models 3 to 5 represent the mediating effect of the three dimensions of dynamic capability, respectively. The regression coefficient of adaptability in model 3 (β=0.034, p < 0.01) and the regression coefficient of digital transformation (β=0.390, p < 0.01) are significant at the 1% level, suggesting that adaptability played a mediating role. Previous research has demonstrated that, under the macroeconomic backdrop, adaptability to internal and external shocks is crucial in ensuring the smooth development of the stock market [50]. On the other hand, the learning ability in model 4 (β=0.000, p > 0.01) did not reach a significant level, despite the significant correlation between digital transformation and learning ability (β=0.395, p < 0.01), indicating no mediating effect on learning ability. This may be due to the fact that the learning ability of enterprises is not entirely synchronized with the information available in the stock market [51]. In model 5, the regression coefficient of innovation capability (β=0.063, p < 0.01) and digital transformation (β=0.388, p < 0.01) reached a significant level, demonstrating a significant correlation between digital transformation and innovation capability, and that innovation capability played a mediating role. This is because innovation ability can enhance investor confidence through the “signal display” mechanism, resulting in investors being less negatively affected by the impact of systematic risk, and the company’s stock price rising [52]. Therefore, we can conclude that part 2 of the hypothesis is supported by empirical evidence, which suggests that dynamic capabilities partly mediates the correlation between digital transformation and enterprise stock price volatility.

Mediation effect test of dynamic capability

Mediation effect test of dynamic capability

Table 6 presents the regulatory influence of environmental regulations on the dynamic capabilities of enterprises in relation to digital transformation. Model 2 illustrates the analysis results of the moderating impact of environmental regulations on the adaptability of enterprises. Upon examination of the table, it is evident that the interaction term coefficient between environmental regulations and enterprise digital transformation (β= 0.002, p > 0.01) is insignificant, thus refuting the regulatory effect of environmental regulations on the adaptability of enterprises in relation to digital transformation. Model 6 demonstrates the regulatory impact of environmental regulations on the innovation capability concerning digital transformation. It is apparent from the table that the interaction term coefficient between environmental regulations and digital transformation (β=0.003, p > 0.01) is also insignificant, indicating the absence of moderating effects of environmental regulations on the relationship between digital transformation and innovation capability. In essence, the implementation of environmental regulations by enterprises does not have an impact on the influence of digital transformation on adaptability and innovation capability. This may be due to the fact that digital transformation is a pervasive trend in contemporary times, where adaptability and innovation capability are inevitable outcomes for enterprises entering the digital era, regardless of external environmental pressure. Notably, the interaction coefficient of environmental regulation and digital transformation is significant (M (4)), and there is a notable correlation between digital transformation and learning ability. However, due to the crowding-out effect of environmental regulation on enterprises’ R&D investments, the improvement of absorptive learning ability in enterprises is negatively affected. In light of the above analysis, hypothesis 3 has been successfully validated by empirical testing.

Regulatory role of environmental regulation

Regulatory role of environmental regulation

The correlation between public emergencies and the digital transformation process of enterprises, as well as volatility of stock prices, is closely intertwined. The impact of public emergencies is severe, resulting in a halt to production across all sectors of society, intensifying the downward pressure on the economy. Consequently, the real economy and capital market are inevitably influenced, hindering the digital transformation process of enterprises. Failure to consider this factor may lead to endogenous interference. Therefore, this study eliminated the global epidemic crisis variables by excluding enterprise samples from 2020 and selecting samples from 2013 to 2019 for regression testing once again. The empirical regression analysis (Table 7) indicate that the primary conclusion “digital transformation of enterprises significantly enhances stock price volatility” (M (1)), the intermediary effect (M (2) - M (4)), and the moderating effect (M (5) - M (7)) remain unaltered. In conclusion, the research findings are robust. The digital transformation of enterprises can effectively stimulate stock price fluctuation, lending additional support to the core research hypotheses of this paper.

Robustness test of rejected samples

Robustness test of rejected samples

Recent studies have shown that fluctuations in stock prices may be influenced not only by digital transformation but also by enterprise size. To enhance the accuracy and comprehensiveness of this investigation, Hansen’s threshold regression model was utilized to empirically test the threshold effect of enterprise size on the relationship between digital transformation and fluctuations in enterprise stock prices. Firstly, a step-by-step approach was employed to determine the appropriateness of the method, followed by the determination of the number of thresholds and the specific form of the model. The results of the test indicate that only a single threshold is significant. As a result, this study opted to use a single threshold model. The single threshold panel regression model can be presented as follows:

Where, i and t signify the enterprise and year, respectively. Volmit represents the fluctuation in stock prices of enterprise i in year t, Natureit represents to the enterprise’s nature, Regionit signifies the location of the enterprise, Ageit refers to the enterprise’s age, Topsideit denotes the concentration of equity, Turnoverit represents the stock turnover rate, Roeit signifies the return on net assets, I (.) indicates the indicator function, and Sizeit represents the enterprise’s size, which is a threshold variable with a threshold value of γ. Furthermore, μ i denotes an individual-specific effect, φ t denotes a time-specific effect, and ɛ it is the random disturbance term.

Table 8 displays the results of the threshold data analysis. The sole threshold successfully underwent the 0.05 significance level test. The regression coefficient for the “digital transformation— stock price volatility” pathway remains statistically significant both before and after the threshold value, with no change in sign. However, only the slope varies; implying that the impact of digital transformation on stock price volatility differs before and after the threshold value. Once the threshold is exceeded, digital transformation plays a more evident role in promoting stock price volatility. One possible explanation for this observation is that the magnitude of a firm positively correlates with digital transformation. This correlation allows firms to respond more efficiently to significant uncertainties, thus stabilizing their stock prices.

Panel threshold model parameter estimation results

Panel threshold model parameter estimation results

From a theoretical perspective, this study examines the internal mechanism of the impact of digital transformation on enterprises and their stock price volatility. And tested from the empirical point of view, leading to the conclusion that (1) digital transformation can notably boost stock price volatility in enterprises. Additionally, after scrutinizing the results and removing the sample data from specific years, the aforementioned conclusion remains unchanged. This study contributes to the literature by building upon Wu et al.’s (2021) perspective that digital transformation can considerably enhance the liquidity of enterprise’s stocks. (2) The findings indicate that only the adaptability and innovation ability dimensions of digital transformation play a mediating role in the relationship with stock price fluctuation, while learning ability does not pass the mediating effect test. These results serve to enrich the relevant research on dynamic ability. (3) Environmental regulation was found to only moderate the learning ability dimension of the relationship between digital transformation and dynamic capabilities, but not the adaptability and innovation ability dimensions. (4) The results of the threshold effect test demonstrate a difference in the promotion effect of digital transformation on stock price volatility before and after the threshold value of enterprise size. Specifically, the promotion effect of digital transformation on stock price volatility is more evident for energy enterprises whose enterprise size exceeds the threshold value.

This study presents the subsequent policy recommendations. Firstly, it is recommended that the government introduce relevant policies to stimulate energy firms to actively implement digital transformation. Particularly, for small-scale energy firms, there should be an increase in the support for digital transformation, the provision of an enabling environment for small-scale energy firms to implement digital transformation, and the promotion of digital transformation to attain a positive economic impact. Secondly, in the course of choosing the practical approach to digital transformation, energy firms should adequately plan the digital path based on their own developmental status and features. Instead of hasty efforts towards success, they should enhance the proportion of R&D investment and technical personnel, consequently boosting their innovative ability, striving to align digital technology with the requirements of digital transformation, and realizing stable investor confidence in the firms [7]. Thirdly, the government should develop and enhance environmental laws and regulations, leveraging the guiding function of environmental regulations to actively promote green production and facilitate digital transformation of firms. The appropriate environmental regulation can effectively enhance the learning capability of firms and reduce the cost and complexity for stakeholders to access comprehensive and high-quality information. This, in turn, can enable accurate assessment of enterprise risks and decrease stock price fluctuations resulting from irrational expectations.

In addition, this research suffers from certain limitations that warrant acknowledgment. Firstly, the domain of quantitative research into digital transformation remains relatively nascent. Drawing on the dynamic capability theory and a regulatory environmental perspective, this study investigate the impact mechanism of enterprise digital transformation on fluctuations in stock prices. Nevertheless, there are still other intricate mechanisms that demand urgent understanding. Subsequent research may explore the impact mechanism of these two factors from diverse dimensions, ultimately illuminating the influence of digital transformation on stock price volatility. Secondly, the samples utilized in this study primarily concentrate on energy enterprises. Thus, the impact of digital transformation on stock price volatility in other industries remains obscure, necessitating further confirmation to generalize this conclusion. In the future, scholars may further test the relationship between digital transformation in enterprises across various industries and fluctuations in stock prices, broaden the range of sample research, and enhance the robustness of research conclusions.

Footnotes

Acknowledgment

Supported by the Project of Cultivation for Young Top-notch Talents of Beijing Municipal Institutions (BPHR202203211).