Abstract

A financial risk early warning system (FREWS) is a disclosure and tracking mechanism that provides advance notice of potential issues, hazards, and potentials that might affect the business’s finances. Some elderly individuals living alone may experience financial difficulties, which may hinder their ability to pay for appropriate medical care, property maintenance, and other essential expenses. Financial difficulties can add tension and diminish their quality of life. Financial results, investment risk, and possible insolvencies may all be detected by implementing early warning systems. Management might use the window of opportunity provided by early warning systems to avert or lessen the impact of possible issues. Almost all FREWS rely on some financial statement analysis. Financial measures are combined with the EWS, accounting information, to determine the firm’s success in its field. Organizational success depends on effective financial oversight, which is at the heart of each business. Studying the enhancement of early warning capacities is relevant because there are no adequate risk evaluation methods to generate realistic estimates. To minimize the FREWS, this research provides a systemic model based on a second-order block chain differential equation (SBDE). China’s systemic financial liabilities have also been quantified using the expected investment returns of 64 selected financial enterprises in China between February 2006 and September 2020 as the datasets. The financial risk warning approach is compared and analyzed primarily using analytical and comparative techniques. The suggested method is 96% accurate in experiments. Consequently, the proposed algorithm compares favorably to others regarding both computing efficacy and precision and has strong predictability.

Keywords

Introduction

The introduction of the evolving global economy, networking financial system, and financial technology has modified organizations’ economic models and risk profiles. Organizations must act quickly to push beyond the limitations of conventional data, technology, and organization in financial risk management. The rise of internet technology, which is now extensively utilized in many areas of daily life, has aided in the growth of the social economy. Also, it has altered how the finance system operates. The banking industry uses big data to advance toward digitalization and based its growth on personal computing. Although undercutting the traditional financial paradigm, it accomplishes organizational transformation. As the development of integrating the global economy quickens, banks have to take on more risks, and new credit hazards have also risen. In this context, banks must now modify the management mechanism for Technology credit risk evaluation via technological and scientific developments [1]. Severe financial risks like the Asian and economic crises have recently challenged the financial system’s sustainability globally. Establishing an appropriate EWS to anticipate future severe financial risks is crucial for successful preparation against these risks. Unless the bulk of financial resources’ prices decline at once or the collapse of one institution puts other institutions at risk, a financial crisis doesn’t happen. Abnormal conduct can be determined by departures from typical behavior. Look for unusual behavior, feelings, or beliefs. Evaluate the behavior’s regularity and severity. Abnormal conduct occurs more commonly or intensely than usual for the person or environment. Abnormal conduct typically disrupts relationships, career, and social life. Improper conduct hampers everyday activities. Consider behavioral persistence. Chronic conduct could be unhealthy. psychologists, psychiatric counselors, and doctors often need to diagnose deviant conduct. Based on defined criteria, clinicians can do thorough exams and provide reliable recommendation.

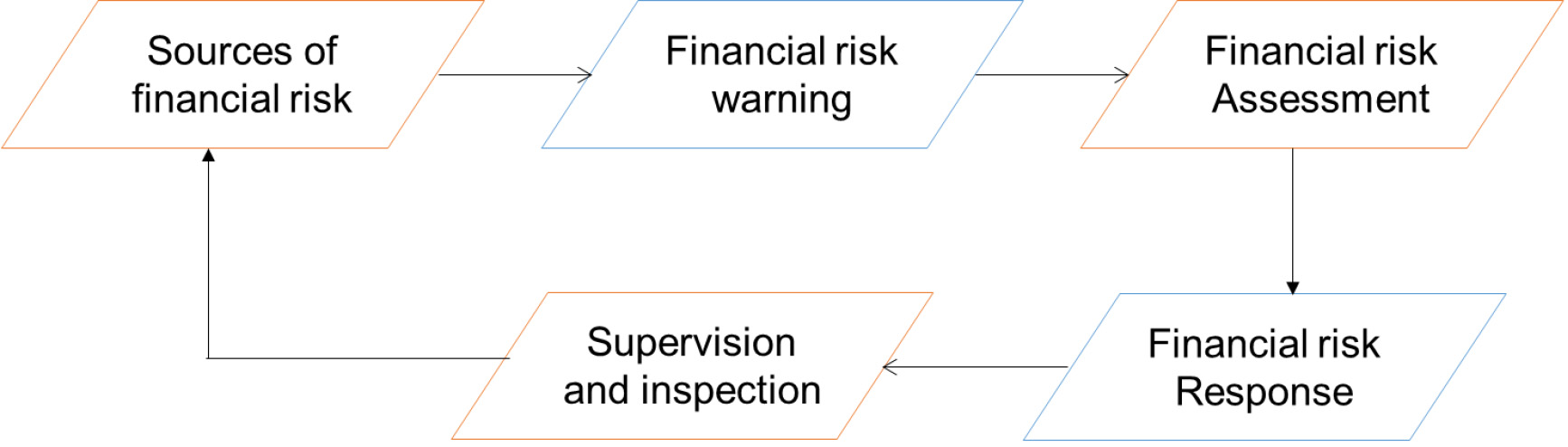

Consequently, worldwide financial system collapses during a period of crisis. The financial system is at risk even during a financial crisis as damages spread throughout financial institutions. Because of their capacity to uncover nonlinear variations in variables, computational techniques have progressively supplanted the usage of regression analysis, such as response variables in predictive modeling and EWS, in recent years. This has improved the effectiveness of early financial warnings. The Basel Agreement and existing supervision, focusing more on personal financial risks, expose the financial sector to macroeconomic shocks since systemic risks are not adequately monitored [2]. In September 2021, worldwide the average age of adults was 18 years and older. Adults have key roles in the employment, economy, family life, and society’s decisions. However, births, deaths, migration, and other demographic shifts affect the size of the population. Thus, for the latest data on the worldwide adult populace, consult trustworthy sources like the UN, the World Bank, or national statistics organizations. There has long been discussion regarding how the financial system and the economy are driven by narrative emotion. The years before the global financial crisis serve as an illustration. Like in numerous past incidents, the financial sector transfer function sense of happiness connected to the notion of a new paradigm. This time, the significant positive sentiment was justified by the conviction that markets were now more efficient and that risk was distributed more evenly throughout the system, allowing higher returns to be sustained. The crisis brought attention to the function of narrative feeling again. This approach recognizes story and emotions as economically significant but often interprets this as representing segments and sub-behavioral bias and reframing or quantitative irrational swarming [3]. Systemic risk in finance refers to a crisis that destroys a financial system, a market, a region, a nation, or even the world markets. Even now, economic growth has not yet wholly recovered from the consequences of these tragedies brought on by structural financial risk. As a result, during the last ten years, a significant amount of innovative academic research, including examining the economic system, financial supervision, observing cross-border capital flows, etc. In recent years, experts and government representatives have utilized the concept of a systems financial risk evaluation of the likelihood of harm to consumers, financial markets, and even the economy. The common assumption is that financial institutions’ strong connection builds expansive networks and enhances the chance of risk transfer. Network analysis, behavioral modeling, and complex systems theory are necessary for economic and financial policy. With increasingly linked financial networks, the significance of accountability and leadership has received much attention [4]. Figure 1 depicts the financial risk prediction system.

Motivation of study

Preventing the financial meltdowns, which caused serious effects on the world economy, is one of the main drivers. An EWS can assist in spotting early warning signs and enable decision-makers to act swiftly to avert calamities. Organizations and markets for financial products are essential to the growth of the economy. An EWS assists in safeguarding the interests of investors, consumers, and people in general by identifying systemic flaws that may result in damage. The larger economy may be negatively impacted by financial instability, which could result in loss of employment, slower economic growth, and social unrest. An EWS seeks to preserve liquidity in the economy by detecting risks and weaknesses that could jeopardize it. The major goals of a Financial Risk Early Warning Systems are to keep up stability, enhance the overall condition of the financial system, and safeguard businesses, financiers, and the general public from economic meltdowns. For authorities, politicians, and lenders, it is a vital instrument for preemptive risk management and risk mitigation in the ever-evolving field of money.

Related works

A concept designed as an EWS forecasts success rates and likely abnormalities and lowers crisis risk in cases, events, transactions, institutions, organizations, and individuals. Additionally, quantitative analysis may be used to determine their present circumstances and potential hazards. Financial EWS is a tracking and communication system that warns of potential issues, threats, and possibilities before they impact a company’s financial statements. EWSs identify financial risk, performance, and prospective business failure. EWSs allow management to seize chances to avert or lessen future issues. Financial statements serve as the foundation for almost all financial EWSs. The data sources used by EWS to represent the economic reality are financial statements and income tables. In general, the EWS is a financial statement analysis approach that uses financial ratios to identify the accomplishment analysis of a business based on its industry [5]. Severe financial risks like the Asian and economic crises have recently challenged the integrity of the financial system throughout the globe. Establishing an appropriate early EWS to detect future extreme financial risks is crucial for successful preparation against unnecessary financial risks. In reality, EWS must perform flawlessly in its categorization methodologies to identify high financial threats precisely. EWS system gives an early warning of financial and non-financial stress, and regulatory agencies or central banks utilize it to decide on policies [6].

Financial risk prediction system.

The various financial crises in the last years have demonstrated cross-border contagion. The international transmission of financial problems has shown a tendency toward normalcy with the rise of globalization of the economy and financial deregulation. The transmission process also demonstrated a trend of complexity and variety. According to empirical studies on several financial crises, the economic downturn was planned, unforeseen outbreak. The scope and depth of the financial crisis’s effects are also growing. It affects the economy, politics, and people’s means of subsistence. The likelihood of an economic slump has increased even though Conservatism and protectionism in economics have revived the global financial system. The development of an EWS for systemic financial risk is crucial. Researchers from several nations focused on developing a EWS for systemic financial risks [7]. A financial crisis will likely occur if most financial resources depreciate simultaneously or when one organization’s failure impacts other institutions. As a result, a systemic financial crisis results in the demise of the whole financial system. The financial sector is in danger if losses extend throughout financial firms during a financial crisis. The overall danger is severe, corresponding study, undifferentiated danger that threatens the economy rather than a few banks. However, the year’s global financial crisis brought systemic risk to the attention of regulatory agencies and the academic community. Consequently, the idea of contagious increased danger holds that the collapse of one banking institution will result in the loss of other financial institutions and has come to be used to describe systemic risk. The Central Bank said the systemic risk is a pervasive threat to financial stability that will seriously harm society’s well-being as it undermines the fundamental operations of the financial system and slows economic development [8].

Financial risk refers to the potential for direct investment losses brought on by business loans, governmental financing, other economic variables, and the ensuing effects of economic events. Due to the contagious nature of financial risk, the onset of financial crises sometimes results in currency devaluation, exchange rate changes, economic downturns, economic depression, and occasionally even the fall of nearby firms, nations, and the global economy. Because of the financial system’s vulnerability and the devastation caused by the financial crisis, developing an effective EWS for financial risks is crucial. Increased competition, market growth, and business innovation benefit from increased transaction size. EWS of financial risk involves identifying and analyzing current financial risk variables, assessing the likelihood and the level of potential problems, and providing technical support for risk management and mitigation [9]. A financial crisis is an economic occurrence if a business cannot pay for costs or obligations that are about to develop. The presence of a financial crisis is not random; instead, it develops gradually, often with an imposing presence. As a result, recognizing and anticipating a financial crisis is crucial and protects the interests of creditors, investors, and the government’s oversight of publicly traded businesses [10].

The research [11] used 29 third-level indicators and four first-level indicators. The study develops a mechanism for early detection of financial risk in the supply chain. The paper [12] established a fuzzy theory-based model system for intelligent real-time monitoring and early warning of economic business risks that applies intelligent computing to financial market forecasting utilizing related fuzzy theory principles. The study [13] developed a deep learning-based financial early warning model and built a financial risk EWS for e-commerce enterprises. The paper [14] proposed an early warning system for SMEs (SEWS) as a data-driven financial risk detector. The research [15] employed for corporate financial risk analysis, EWS, and a resource will be offered for decision-making on risk management. The study [16] suggests the Fuzzy association rules that satisfy the bare minimum of uncertain credibility were produced using the fuzzy cluster method (FCM), parallel rules, and parallel mining algorithm. The paper [17] investigated potential contagion risks using structured financial networks to study EWS. The study [18]. Internet finance risk reduction for commercial banking institutions. IoT and massive data technologies classify and assess banking industry risk factors. The research [19] examined EWS design, implementation, and application across various contexts, particularly in the economic and financial sectors. The paper [20] used deep learning financial crisis forecasting model will benefit significantly from this work as a reference.

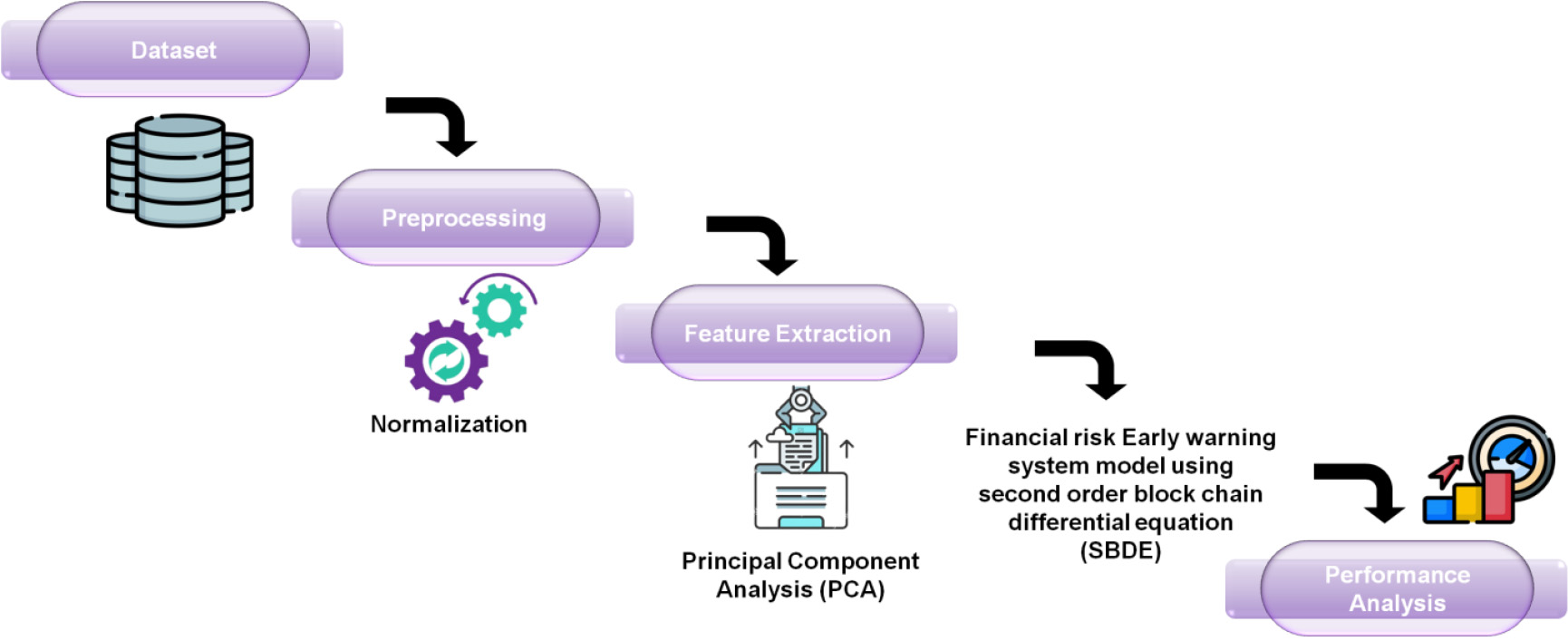

The most pervasive and debilitating business threats are financial risk, which may lead to insolvency if owners aren’t forewarned and taken precautions. Incorrect financial data misled buyers and taught others to use financial data to draw wrong conclusions about the country’s economy. Thus, minimizing the financial burden in business operations is a critical foundation for ensuring the firm’s long-term success. Yet, managing the financial risks of an organization is an iterative, ever-changing operation that permeates all analysis, decision, and administration. Here, we provide a comprehensive evaluation of the technique that has been suggested. Figure 2 depicts the suggested method.

Flow of proposed method.

The methodologies used to measure quantitative financial risks are diverse and unique due to the widespread disagreement among academics on the origins and prevalence of these dangers. The quantitative economic chances estimated using financial market data are reasonably objective. They are frequently utilized as standards in national and global research due to their accessibility, frequency range, and great forward-looking feature.

Thus, they employed the long-run marginal expected shortfall (LRMES) technique to evaluate China’s systemic financial threats. Considering the robust monetary character of China’s real estate business, 64 A-share listed financial organizations were chosen between February 6, 2006, and September 30, 2020, using the Chinese Securities Regulatory Board field categorization criteria. The selected firms may be representative of the status of China’s financial sector as a whole, considering that their combined valuation is equivalent to around 82.5% of the combined valuation of the banking and estate development sectors [25].

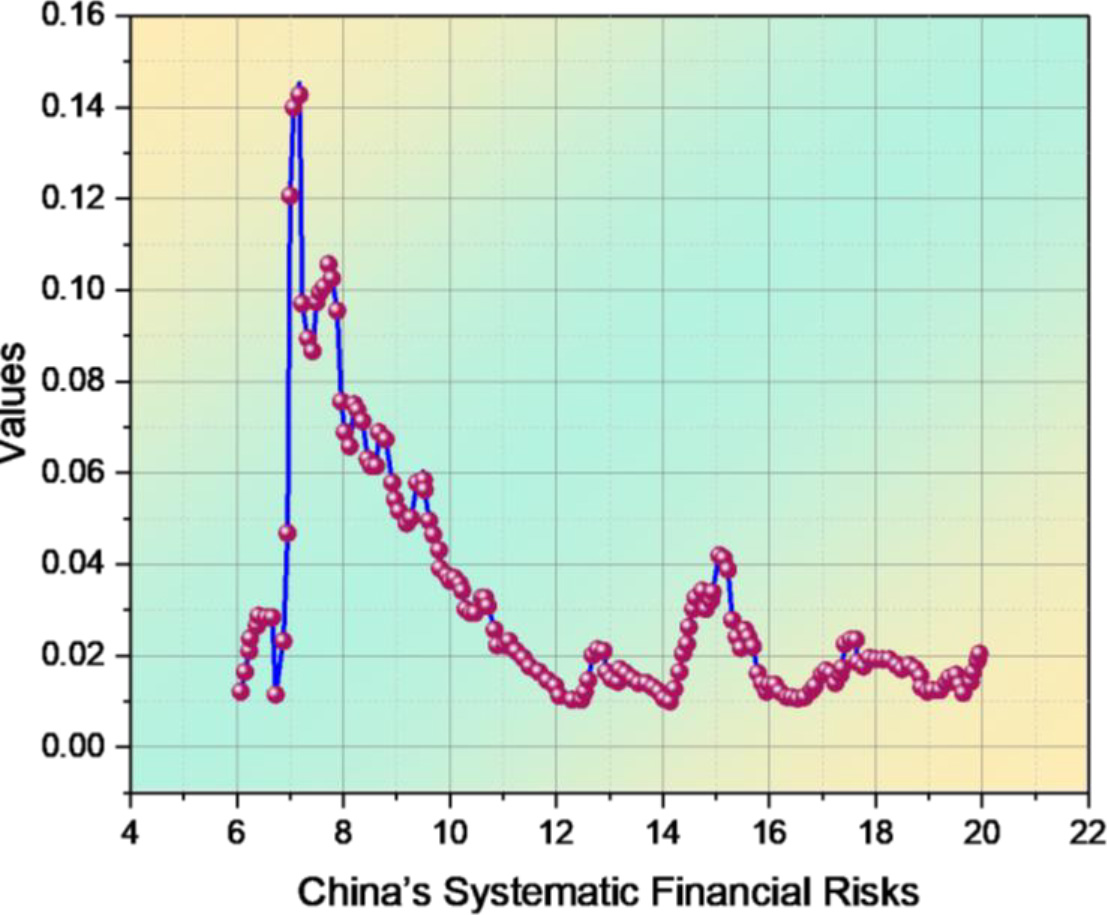

China’s systematic financial hazards were positioned at high stages during the global economic crisis of 2007–2008, the European debt crisis of 2009, and the share marketplace meltdown of 2015, as Fig. 3 illustrates. The worldwide economic meltdown made these dangers particularly evident, which is what caused this series of financial meltdowns to last so long and do so much damage.

The Chinese government devised a fiscal incentive plan worth RMB 4,000 billion and a fairly loose monetary policy to mitigate the adverse effects of the global financial crisis on the country’s actual industry. The aim was to regulate and reduce the overall threat. After then, the influence of unfavorable events including the COVID-19 pandemic, the Sino-US trade war (2018M03), and the historic “money shortage” of China’s banking sector caused the total risk to somewhat increase. All things considered, the LRMES measurement results fit with the changing trajectory in China’s structural risk taking quite well.

China’s systematic financial risks (2006M02–2020M09).

Predictor variables must be normalized until entered inside any application to standardize the variable ranges for estimation and evaluation because of the signals’ varying forms. This is the equation for that procedure precisely:

The business and financial risk assessment indications are comprehensive, with the variables connected to create an evolutionary system. This is necessary because finances and economic risks are complex and derived from all elements’ threats. The effectiveness of businesses and technological advancement are positively related to the degree of financial development because greater degrees of economic progress allows for more significant economies of scale in exchanges, less expensive transactions, and more opportunities for specialization and work division.

In order to minimize the size of the novel index in the event of a minor quantity of information beating, filter duplicate data, and acquire comprehensive indexes linked to the hazard of sporting events, numerous important elements may be converted using PCA into no relevant indexes. The following are the PCA steps:

Consider that the research field is a, choice B indexes in this region and set the index’s sample matrix as

Where

Consider that

Where

The detailed risk rating

Where

The steps involved in FREWS risk detection, risk evaluation, advance detection, and treatment are analogous to those taken by the immune response when dealing with foreign antigens. The first stage of financial burden early warning is detection and evaluation, which entails learning about potential economic hazards and where they could come from before employing quantitative and qualitative techniques to determine the severity of such hazards. Appropriate methods are implemented for early warning of threats beyond the purview of law enforcement. Financial risk early-warning outcomes would be sluggish to respond with any mechanism, which might result in expenses. Still, as individuals gain experience, they may be better able to react fast in the face of identical hazards and enhance risk avoidance and management effectiveness.

K-fold cross-validation

Describe the Model weights were selected using the K-fold cross-validation criteria for the average prediction in this section. The sample is split into K groups, each of which is handled to verify the model, called a validation sample. The overall squared prediction errors for all groups were decreased, and the model weights are then chosen. In contrast to the Mallows test or additional requirements, which the calculation considering the penalty term in nonlinear models on an individual basis, Implementing K-fold cross-validation is simple and adaptable, seldom depending on the model’s structure.It begins with the data being divided into K groups at random, after which the following actions are carried out for each group:

As the testing dataset, pick one of the training folds. The training set consists of the remaining K groupings. Utilize the chosen training dataset to educate the model, and then use the testing dataset to assess it.

The derivatives of a value of order 2 are the only variant of the function seen in this special kind of fractional derivative that utilizes the block chain. An equation involving a variable and its derivation is called a differential equation. Second-order differential equations are those that include a variable and its second derivative. SBDE is usually more challenging than first-order problems. Learners usually learn about linear differential equations of the second derivative. The universal solution to a linear algebraic differential equation of the second order is

Utilizing function notation, this expression may be rewritten. Differential function

The differential equation in which

Determining the optimal solutions to the homogeneous issue is the usual method for solving (2).

Considering one specific approach to the non-homogeneous case,

Hence, the universal solution to (2) is

A nonlinear second derivative might have a specific solution with multiple ways to locate it. Some examples of these techniques are guesswork, the method of Unspecified Coefficients, the Variance of Factors Technique, and Green’s equations.

The

The Wronskian towards a block chain-based on 2nd differential equation has been provided by

If it is nonzero, then the results are linear functions.

Derivatives of the second order having variable coefficients are the basic kind. A second-order system of linear equations with a steady variable has a generic form where

Here, the three constants are

It is possible to solve (10) by guessing that

As the two results

Algorithm 1 shows the Second-order block chain differential equation.

As a result, it reduces financial risk based on the SBDE method. To demonstrate the effectiveness of a proposed approach, its efficiency and accuracy are compared to those of modern techniques like Support Vector Machine (SVM) [22] Long Short Term Memory (LSTM) [23] and Deep Neural Network (DNN) [24]. Logistic Regression, Mean Square Error (MSE), Root Mean Square Error (RMSE), Accuracy, Risk Prediction Rate, Prediction Time, and Time Efficiency are some of the estimated metrics for the suggested technique.

Logistic regression

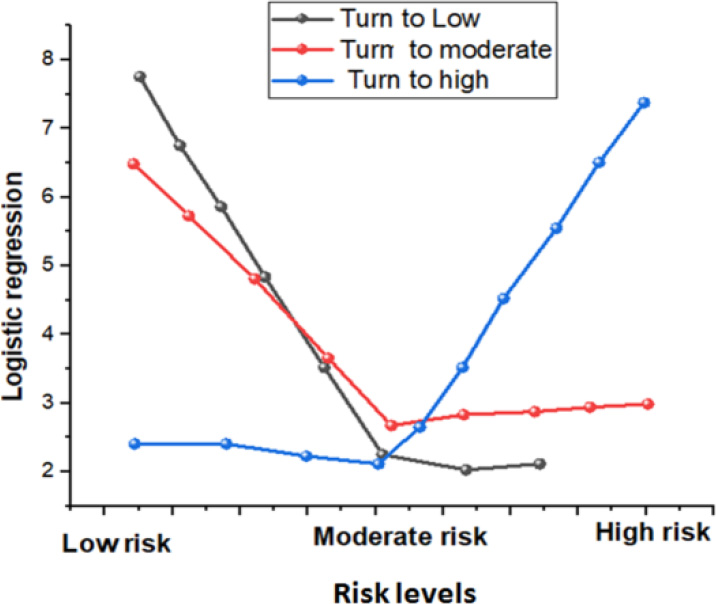

A statistical modeling approach called logistic deterioration is use to forecast the possibility that a particular financial event or risk will occur within a specified time period. Based on a collection of input factors or traits, it is used to estimate the likelihood of a poor financial event, such as loan default, bankruptcy, or market instability. The output of the logistic regression model may be thought of as a probability score, with higher scores denoting a larger possibility that the risk event will occur. The model may categorize occurrences into several risk categories are shown in Fig. 4 by defining an appropriate threshold, which helps financial organizations prioritize their risk management strategies and allocate resources efficiently.

Analysis of logistic regression.

Accuracy is referred to the risk of the financial data instances being classified correctly to the total instances number, which is given by

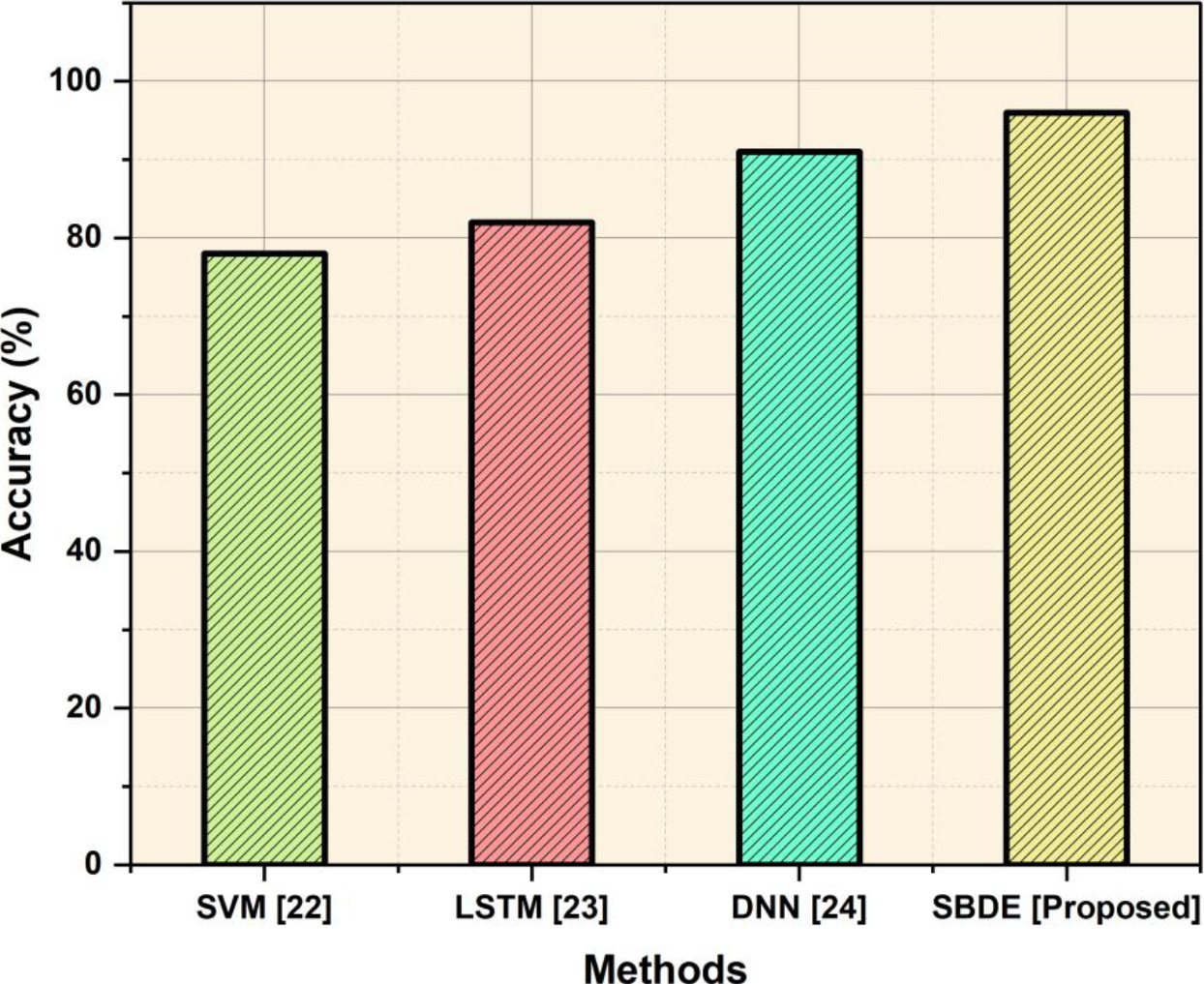

The proposed and existing systemof accuracy is shown in Fig. 5. The accuracy of the suggested SBDE approach is offered to reduce financial risk. SVM has attained 78%, LSTM has attained and DNN has achieved 82%, whereas the proposed system reaches 91% of accuracy. It shows that the proposed approach has more precision than the existing one. Table 1 depicts the values of accuracy.

RMSE amplifies and aggressively corrects substantial financial risk errors using the square form.

Computation of accuracy

Analysis of accuracy.

Analysis of RMSE.

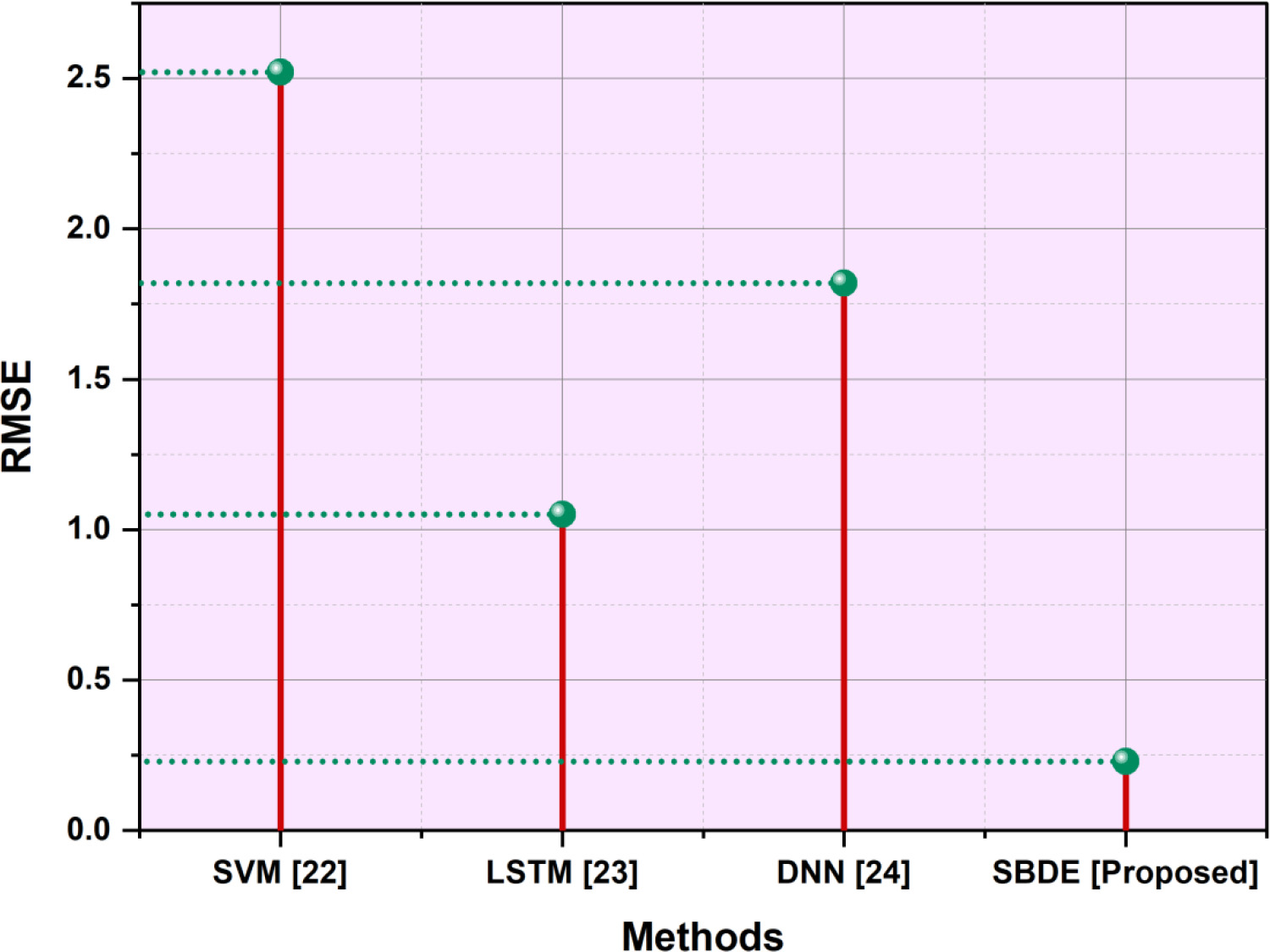

Figure 6 show the RMSE of the planned and existing organization. The RMSE of the suggested SBDE approach that is being offered for reducing financial risk. SVM has attained 2.52%, LSTM has achieved 1.05% and DNN has achieved 95%whereas the proposed system reaches 1.82% of RMSE. It shows that the proposed approach has less RMSE value than the existing one. Table 2 depicts the importance of RMSE.

To measure error, use mean squared error (MAE). The MAE shows that reducing financial risk matches the data. The MAE represents the mistake in weather forecasting.

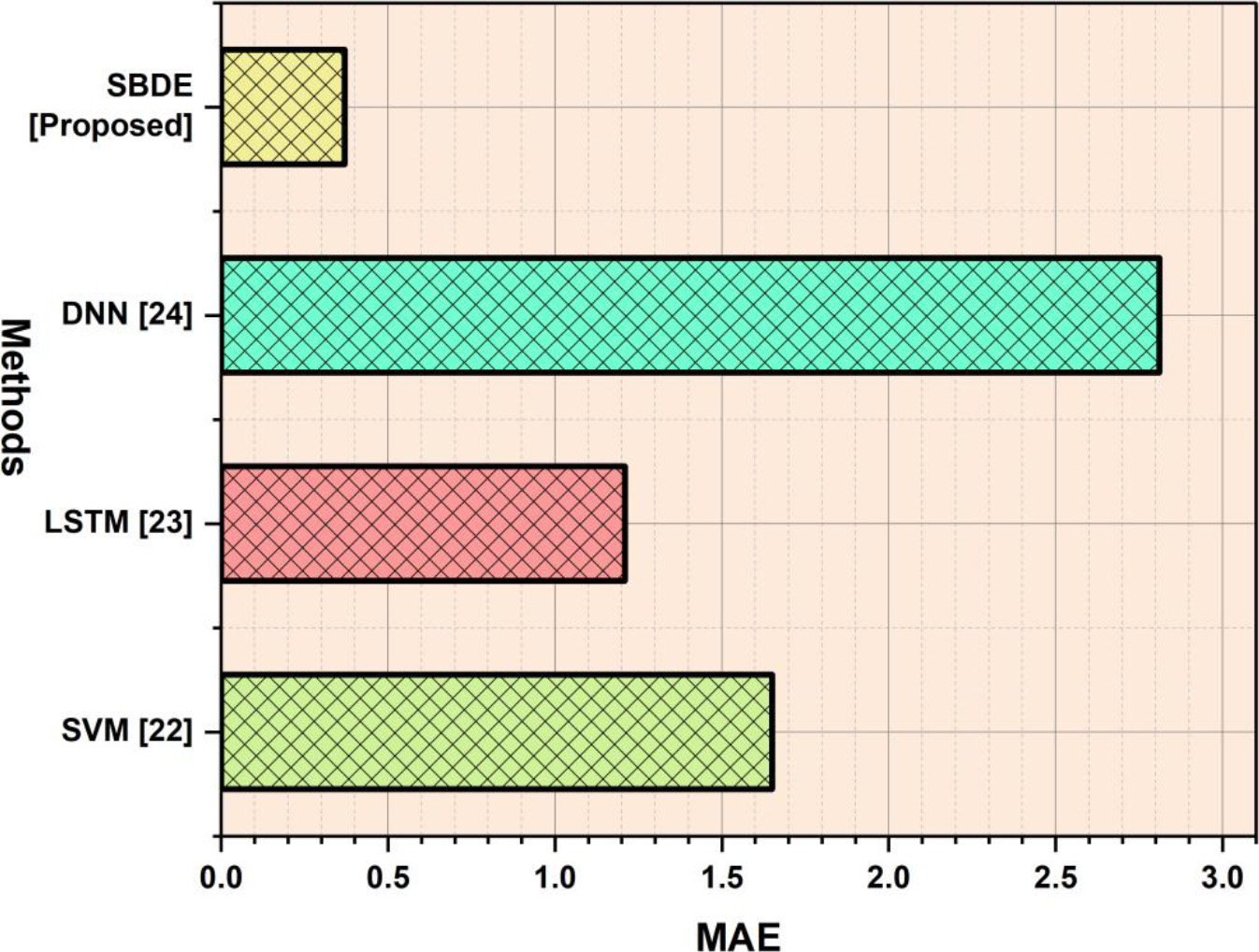

Figure 7 shows the MAE of the proposed and existing system. The MAE of the suggested SBDE approach is being offered to reduce financial risk. SVM has attained 1.65%, LSTM has achieved 1.21% and DNN has achieved 2.81% whereas the proposed system reaches 71% of MAE. It shows that the proposed approach has less MAE than the existing one. Table 3 depicts the values of MAE.

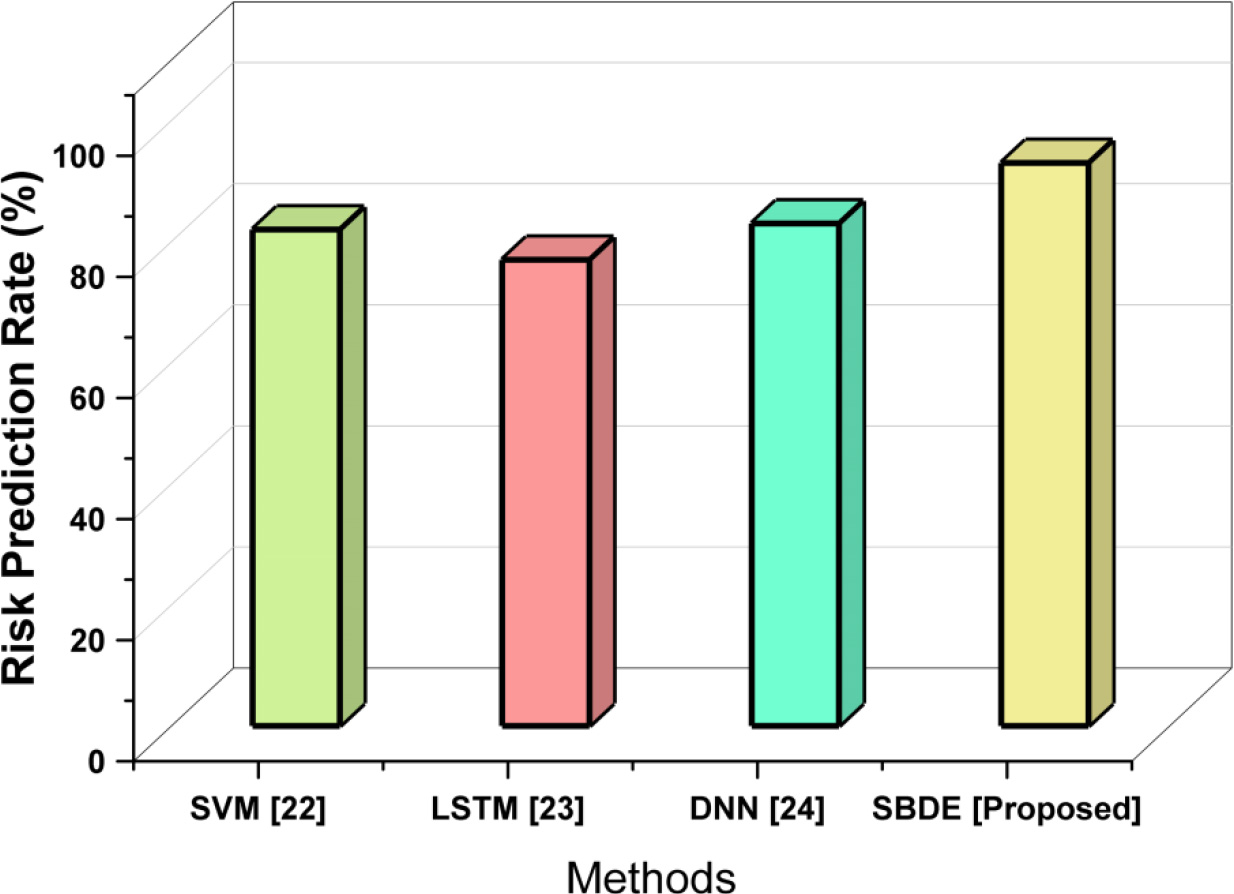

A statistical model that integrates data from financial indicators is a risk prediction rate model. Any metric that forecasts an occurrence’s financial risk is a risk prediction indicator. Figure 8 shows the risk prediction rate of the proposed and existing system. The risk prediction rate of the suggested SBDE approach is being offered for reducing financial risk. SVM has attained 82%, LSTM has achieved and DNN has attained 77%, whereas the proposed system reaches 83% of the risk prediction rate. It shows that the proposed approach has more risk prediction rate than the existing one. Table 4 depicts the values of the risk prediction rate.

Computation of RMSE

Computation of RMSE

Computation of mean absolute error

Computation of risk prediction rate

Analysis of mean absolute error.

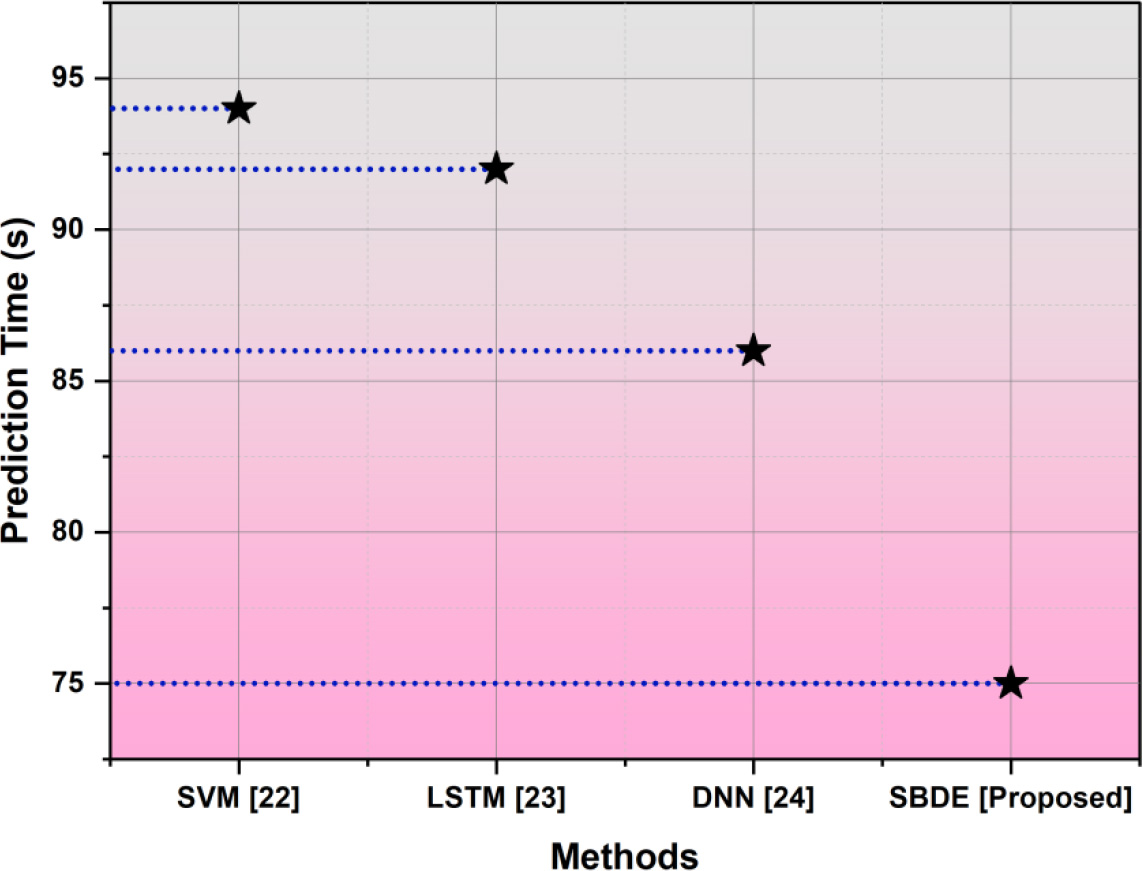

The period over which a model is supposed to forecast a given financial risk is known as the model’s prediction time. For systems that are changing dynamically through time, it is crucial to comprehend the prediction time, when events have happened, and when financial risk forecasts are being generated. The prediction time of the proposed and existing system is shown in Fig. 9. The prediction time of the suggested SBDE approach that is being offered for reducing financial risk. SVM has attained 94%, LSTM has attained 92% and DNN has achieved 89%whereas the proposed system reaches 86% of the prediction time. It shows that the proposed approach has more risk prediction rate than the existing one. Table 5 depicts the values of prediction time.

Analysis of risk prediction rate.

Analysis of prediction time.

Computation prediction time

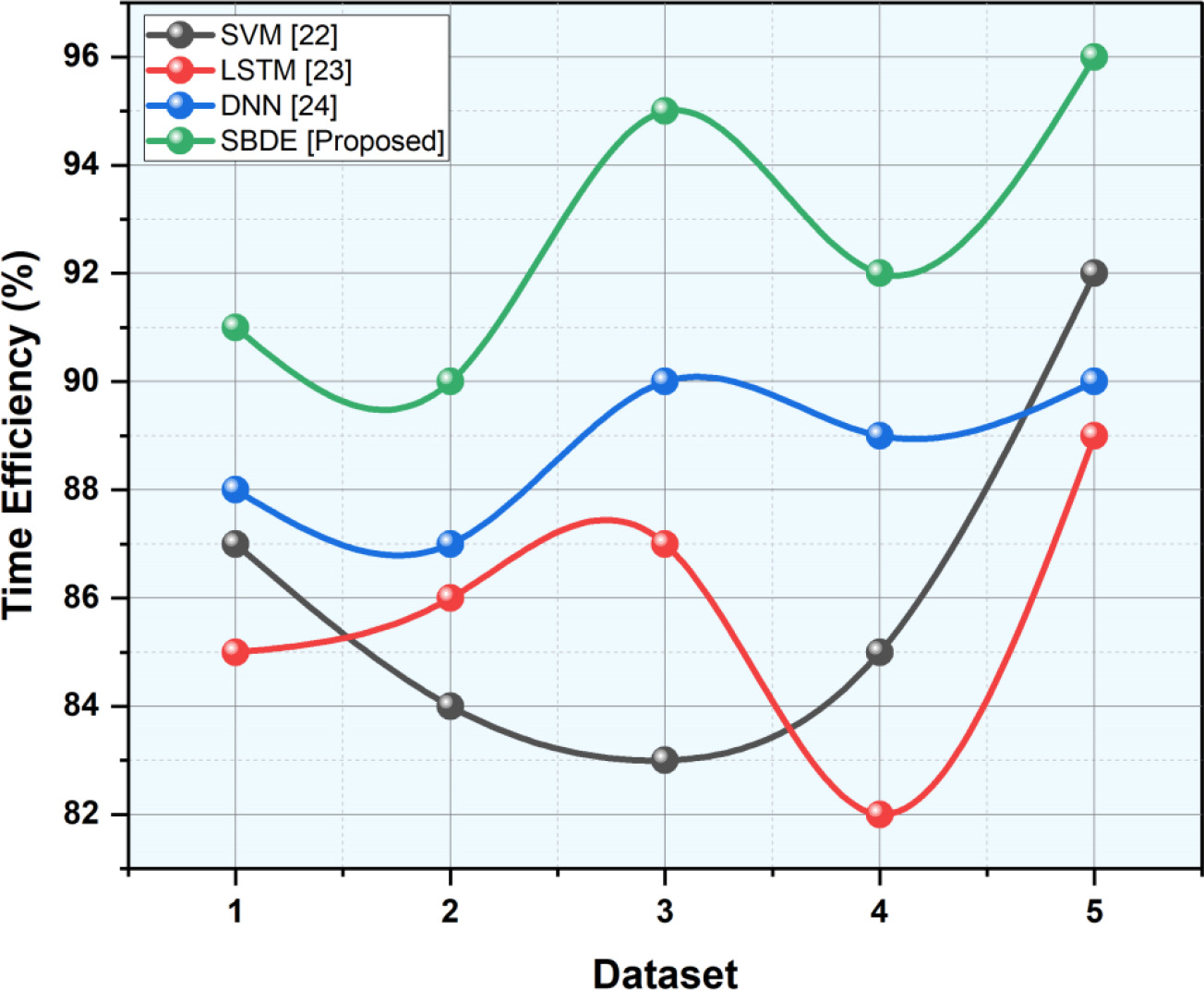

Time efficiency, commonly referred to as time complexity, is a measurement of how an algorithm’s or computation’s execution time develops as the amount of input data increases. It measures how long an algorithm needs to do a job as a function of the size of the input. In computational analysis, time efficiency gives information on how effectively an algorithm uses computer resources, especially the time of the central processing unit (CPU). The Time Efficiency of the suggested SBDE approach is being offered for reducing financial risk. SVM has attained 87%, LSTM has achieved 85% and DNN has attained 88%, whereas the proposed system reaches 93% of the time efficiency. It shows that the proposed approach has more time efficiency than the existing one. Figure 10 and Table 6 depicts the values of the risk prediction rate.

Computation of time efficiency

Computation of time efficiency

Analysis of time efficiency.

Financial risk administration involves identifying, assessing, and accepting or mitigating financial hazards. This study suggested a financial risk prediction the system centered on the SBDE, performed measure choosing and data manufacturing, built a money risk EWS model, classified cash risk types, optimized money risk control, and done a real-world test and result assessment. The study contributed Data analysis, knowing usual user behavior, and considering security and privacy issues are needed to assess aberrant smart home user activity. Before spotting anomalous activity, you must define typical smart home user behavior. This entails evaluating user data trends over time. Consider smart home system user engagement, device usage trends, and energy use. Continuous tracking to track user activities, this helps spot abnormalities and responds to dangers to safety faster. Using a variety of qualitative and quantitative methodologies, the first step in financial risk warning is determining the point of risk. Appropriate procedures are implemented to carry out risk warnings for hazards more significant than those that the security services can handle. The goal function exceeds the minimal value in some period regions while using SBDE. Only the worldwide minimum is displayed. The standard procedure needs the squared amount of the research throughout the search operations errors are continuous and model grouping requires a great deal of previous information to provide a good clustering model. The grades show that the optional methodology is extra accurate than existing methods. The study’s findings demonstrate that the SBDE technique can successfully avoid the perceived adverse effects of arbitrary division thresholds and continually improve the financial risk prediction process.