Abstract

Conventional earthquake risk modeling involves several notable simplifications, which neglect: (1) the effects on seismicity of interactions between adjacent faults and the long-term elastic rebound behavior of faults; (2) short-term hazard increases associated with aftershocks; and (3) the accumulation of damage in assets due to the occurrence of multiple earthquakes in a short time window, without repairs. Several recent earthquake events (e.g. 2010–2011 Canterbury earthquakes, New Zealand; 2019 Ridgecrest earthquakes, USA; and 2023 Turkey–Syria earthquakes) have emphasized the need for risk models to account for the aforementioned short- and long-term time-dependent characteristics of earthquake risk. This study specifically investigates the sensitivity of monetary loss (i.e. a possible earthquake-risk-model output) to these time dependencies, for a case-study portfolio in Central Italy. The investigation is intended to provide important insights for the catastrophe risk insurance and reinsurance industry. In addition to salient catastrophe risk insurance features, the end-to-end approach for time-dependent earthquake risk modeling used in this study incorporates recent updates in long-term time-dependent fault modeling, aftershock forecasting, and vulnerability modeling that accounts for damage accumulation. The sensitivity analysis approach presented may provide valuable guidance on the importance and appropriate treatment of time dependencies in regional (i.e. portfolio) earthquake risk models. We find that the long-term fault and aftershock occurrence models are the most crucial features of a time-dependent seismic risk model to constrain, at least for the monetary loss metrics examined in this study. Accounting for damage accumulation is also found to be important, if there is a high insurance deductible associated with portfolio assets.

Keywords

Introduction

Several recent earthquake events (e.g. 2010/2011 moment magnitude MW 7.1–6.2 Christchurch sequence, New Zealand; 2019 MW 6.4–7.1 Ridgecrest sequence, USA; and 2023 Turkey–Syria MW 7.8–7.5 sequence) have emphasized the need to explicitly account for time dependencies in seismic risk assessments. This is because short-term (i.e. months to years) space-time clustering of earthquakes after large mainshocks can cause significant amplification of damage and loss due to the relatively large ground-motion intensities that aftershocks can produce (e.g. Marzocchi and Taroni, 2014; Papadopoulos and Bazzurro, 2020), and the increased vulnerability of building stock/infrastructure systems after the main event and before any repair actions (e.g. Gentile and Galasso, 2021; Hatzigeorgiou and Beskos, 2009; Kam et al., 2011). The occurrence of mainshocks is also governed by long-term (i.e. decades to centuries) time-dependent mechanisms, such as elastic rebounding (Reid, 1910)—that is, faults cyclically accumulating elastic strain energy and releasing it when the fault rocks’ internal strength/capacity is reached—and stress-based fault-interaction triggering (Toda et al., 1998), which causes long-term clustering of large mainshocks (Mignan et al., 2018).

Yet, the current state-of-practice in seismic portfolio risk assessment involves some significant simplifications that neglect the aforementioned time-dependent features of earthquake risk. Investigations of the effects of these simplifications on portfolio risk calculations have been sparse. Porter et al. (2017) performed a sensitivity study with the long-term time-dependent version of the Uniform California Earthquake Rupture Forecast (UCERF3, Field et al., 2014), exploring the effect of elastic rebound behavior on financial risk (monetary loss) estimates for the state of California. Papadopoulos and Bazzurro (2020) accounted for both aftershocks and (a relatively simplistic representation of) damage accumulation in an investigation of monetary loss estimates for a region in Central Italy. These studies further underline the importance of considering various time dependencies in seismic risk calculations, but neither incorporate a complete suite of time-dependent features in their respective assessments. Other related sensitivity studies have limited their focus to site-specific risk implications associated with aftershocks and damage accumulation for specific building types (e.g. Han et al., 2015, 2016; Tesfamariam and Goda, 2017).

This study involves a more comprehensive investigation of the effects of time dependencies in portfolio earthquake risk models, which is specifically intended to provide important insights for the catastrophe (CAT) insurance and reinsurance industry. The event-based time-dependent earthquake risk assessment approach presented here is an end-to-end framework that integrates existing methodologies for: (1) long-term time-dependent fault modeling that includes fault-interaction triggering between major known faults; (2) aftershock occurrence modeling; and (3) state-dependent vulnerability modeling to capture the impact of damage accumulation due to multiple ground motions. This study then explores the sensitivity of a selection of portfolio-level monetary loss metrics to the integrated features of the framework. For the first time in the literature (to the best of the authors’ knowledge), the investigation also considers the hours clause, a time-dependent earthquake insurance policy feature stipulating that the insurer will cover all financial losses that accumulate in a prescribed number of hours after a catastrophic event begins. Accurately modeling the implications of this clause in CAT risk models is challenging, given the lack of a standard approach in insurance practice for assigning loss claims to specific hours or events (Mitchell-Wallace, 2017) and the absence of spatiotemporal seismicity clustering (i.e. aftershock occurrence modeling) in conventional earthquake risk models.

The study focuses on common monetary loss metrics, that is, average annual loss (AAL, also known as the pure premium or expected annual loss) and return period (RP) loss (also known as “value at risk”). These metrics cover both ground-up loss (the total amount of loss incurred before applying any insurance or reinsurance financial structures) and gross loss (the loss to the insurer after limits and deductibles are accounted for, but before any form of reinsurance is considered). The case-study portfolio examined for the investigation is located in Central Italy. It is a subset of the European Seismic Risk Model 2020 exposure dataset (ESRM20, Crowley et al., 2021a), including 136,000 buildings and a total replacement cost (structural, non-structural, and contents) of €27.4 billion.

Event-based time-dependent earthquake risk assessment framework

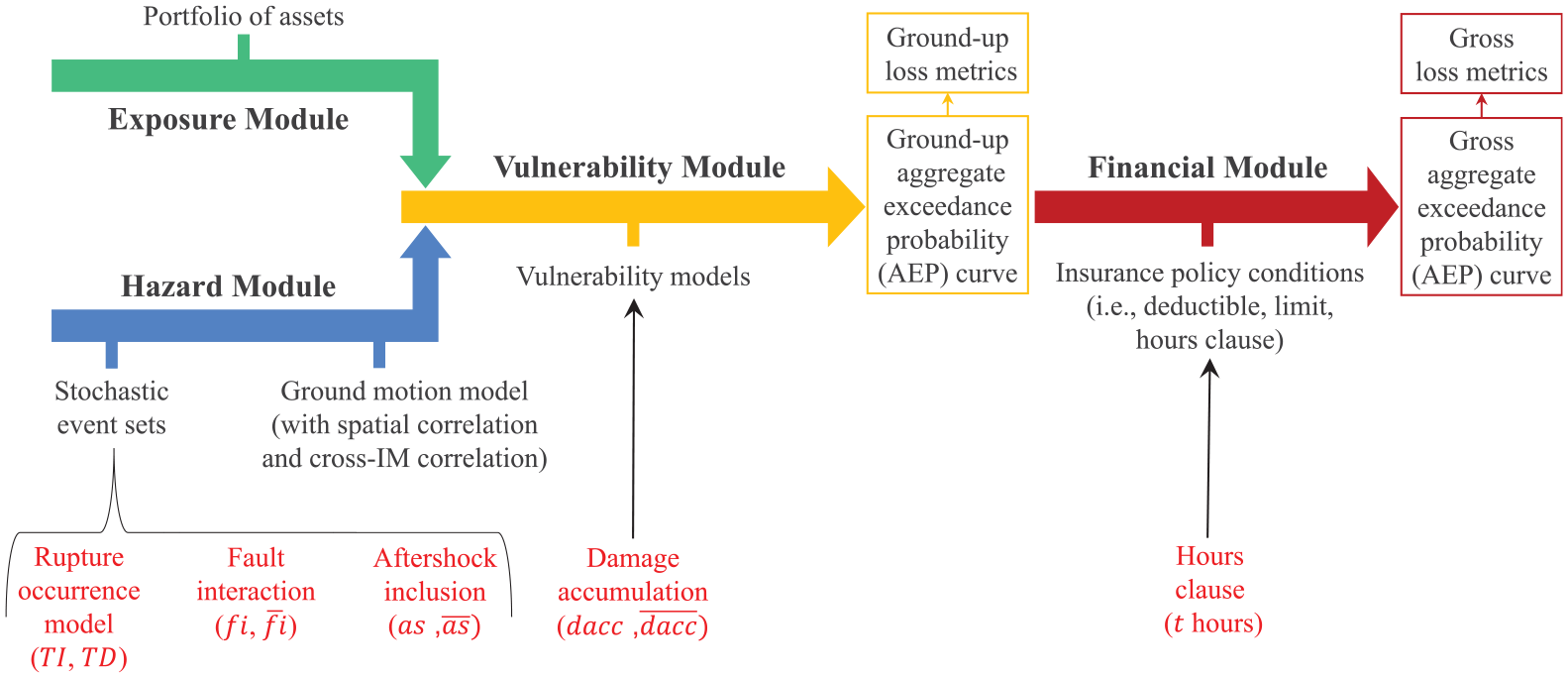

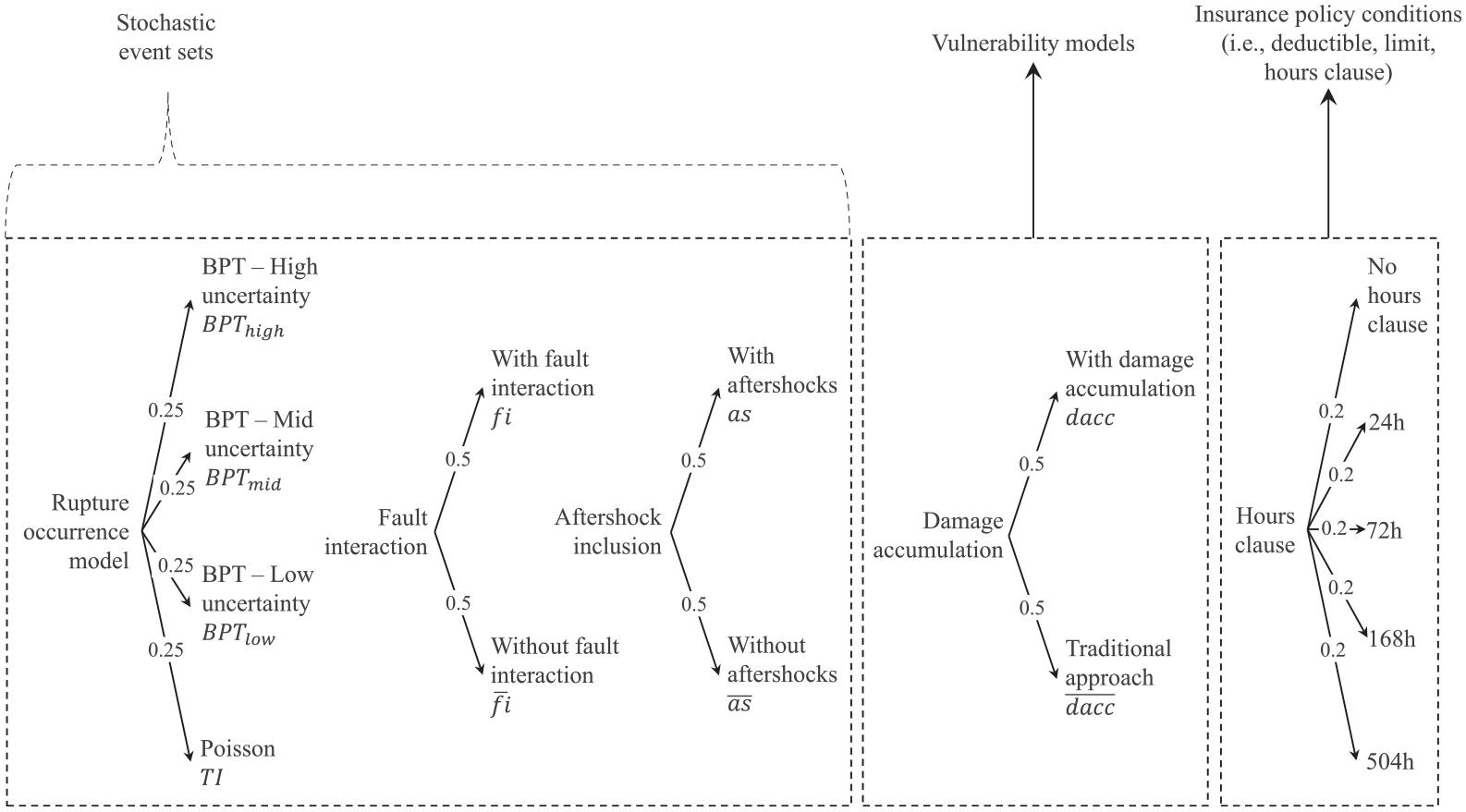

Figure 1 outlines the event-based time-dependent earthquake risk assessment framework used in this study. The framework follows the general structure of a conventional CAT risk model, integrating hazard, exposure, vulnerability, and financial modules (Mitchell-Wallace, 2017). Time-dependent components are represented as a series of input options, which are subsequently investigated through a sensitivity analysis. These input options represent epistemic uncertainty in the considered CAT risk model.

Flowchart of the event-based time-dependent earthquake risk assessment methodology used in this study. Time-dependent input options are displayed in red font.

The seismic hazard module generates stochastic event sets (i.e. synthetic catalogs of earthquake ruptures) based on simulated seismicity for the region of interest over a number of years. A number of time-dependent input modeling options that influence the stochastic event-set generation process are included and relate to: (1) fault rupture occurrence modeling (which can be either time-independent –TI– or time-dependent –TD); (2) fault-interaction modeling (included –fi– or not –

The exposure module contains a portfolio of assets, which are mapped to specific building types. The taxonomy information is then used to select appropriate vulnerability models in the vulnerability module. These vulnerability models are used in conjunction with the ground-motion fields generated at each asset’s location to compute a set of ground-up (gu) loss metrics. The first of these metrics is LRgu,a,e, which is the ground-up loss ratio (LR) for the ath asset and the eth earthquake obtained from the corresponding mean vulnerability model (where the loss ratio is the estimated repair cost divided by the asset’s replacement cost). Two alternative approaches to vulnerability modeling are considered for computing LRgu,a,e:

The approach used in conventional seismic risk assessments (indicated with

The approach of Iacoletti et al. (2023) which makes use of the state-dependent vulnerability models to capture loss accumulation due to multiple ground motions (indicated with dacc). These vulnerability models define the LRgu,a,e of an initially damaged building (i.e. which reached a certain

The asset-level ground-up loss related to each earthquake, Lgu,a,e, is calculated by multiplying the LRgu,a,e with the replacement cost of the ath asset. The portfolio ground-up loss for an earthquake, Lgu,e, is then the sum of all Lgu,a,e across the portfolio. The annual portfolio ground-up loss for each simulated year of the stochastic event set, Lgu, is calculated as the sum of the corresponding Lgu,e values. The ground-up aggregate exceedance probability (AEP) curve then provides the annual probability of Lgu exceeding a certain loss level and is determined as outlined in Crowley and Silva (2013). Ground-up AAL, AALgu, is calculated as the integral under the Lgu AEP curve. The Lgu corresponding to a prescribed RP X, in the Lgu AEP curve (denoted as the X-RP Lgu) is read directly from the curve.

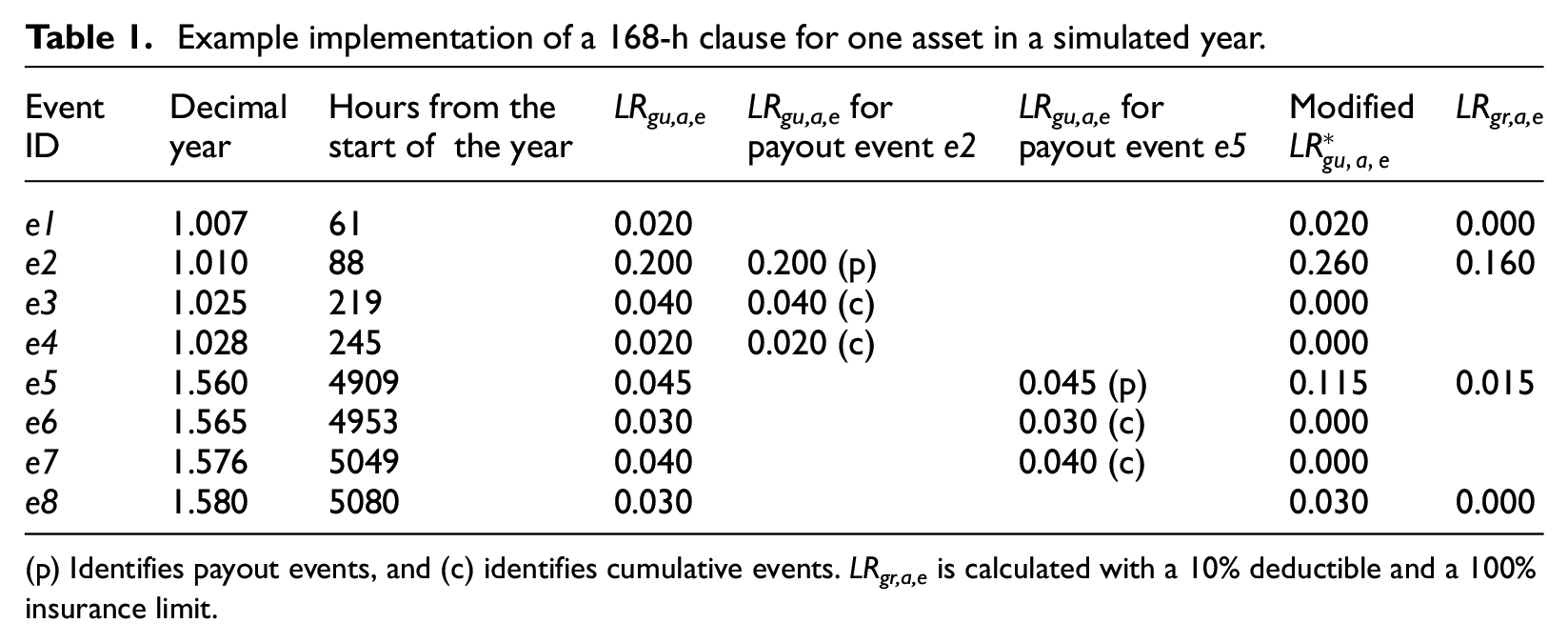

The hours clause input option to the financial module is implemented for the ath asset, the nth simulated year of the stochastic event set, and t hours in the clause, according to the following procedure:

Identify the events simulated within the nth year;

Order the identified events according to their associated LRgu,a,e value, from the highest to the lowest;

For each ordered event (referred to at this stage as a “payout event”), do the following:

(a) If the event belongs to the hours-clause window of a previous payout event, skip the next two steps and relabel the event as a “cumulative event” (see next step);

(b) Identify other events (referred to as “cumulative events”) occurring within t from the current payout event;

(c) Add the LRgu,a,e of the identified cumulative events to that of the current payout event, to produce

This procedure is based on the idea that the event most likely “triggering” a claim is the one causing the largest loss to the policyholders (which might be different for each asset). However, this assumption might not be consistent with the practices of all insurers and reinsurers. The number of hours in a typical hours clause depends on the peril and is typically 168 for earthquakes (Mitchell-Wallace, 2017). Table 1 provides an example implementation of a 168-h clause. Event e2 is the first payout event since it is associated with the largest LRgu,a,e. Events e3 and e4 are cumulative events of e2 because they occur within a 168-h time window. Event e5 is identified as the second payout event since it is associated with the second largest LRgu,a,e value and did not feature as a cumulative event for e2. Events e6 and e7 are the corresponding cumulative events because they respectively occur within 44 and 140 h of event e5. The final payout events, e8 and e1, do not have any associated cumulative events. In a year like the one shown in Table 1, the insurer would have to pay a policyholder twice for the LRgr,a,e caused by two clusters of events (regardless of whether the payout event in the cluster was a mainshock or an aftershock).

Example implementation of a 168-h clause for one asset in a simulated year.

(p) Identifies payout events, and (c) identifies cumulative events. LRgr,a,e is calculated with a 10% deductible and a 100% insurance limit.

Gross (gr) loss metrics are computed as the final output of the framework. The asset-level gross loss ratio, LRgr,a,e, is calculated by applying insurance limits and deductibles to each asset’s

Variance-based sensitivity analysis

Variance-based sensitivity analysis is used to investigate the effects of introducing earthquake risk modeling time-dependent features on AALgu, AALgr, and X-RP Lgu outputs. For a given model of the form

where N is the number of generated samples,

Case study

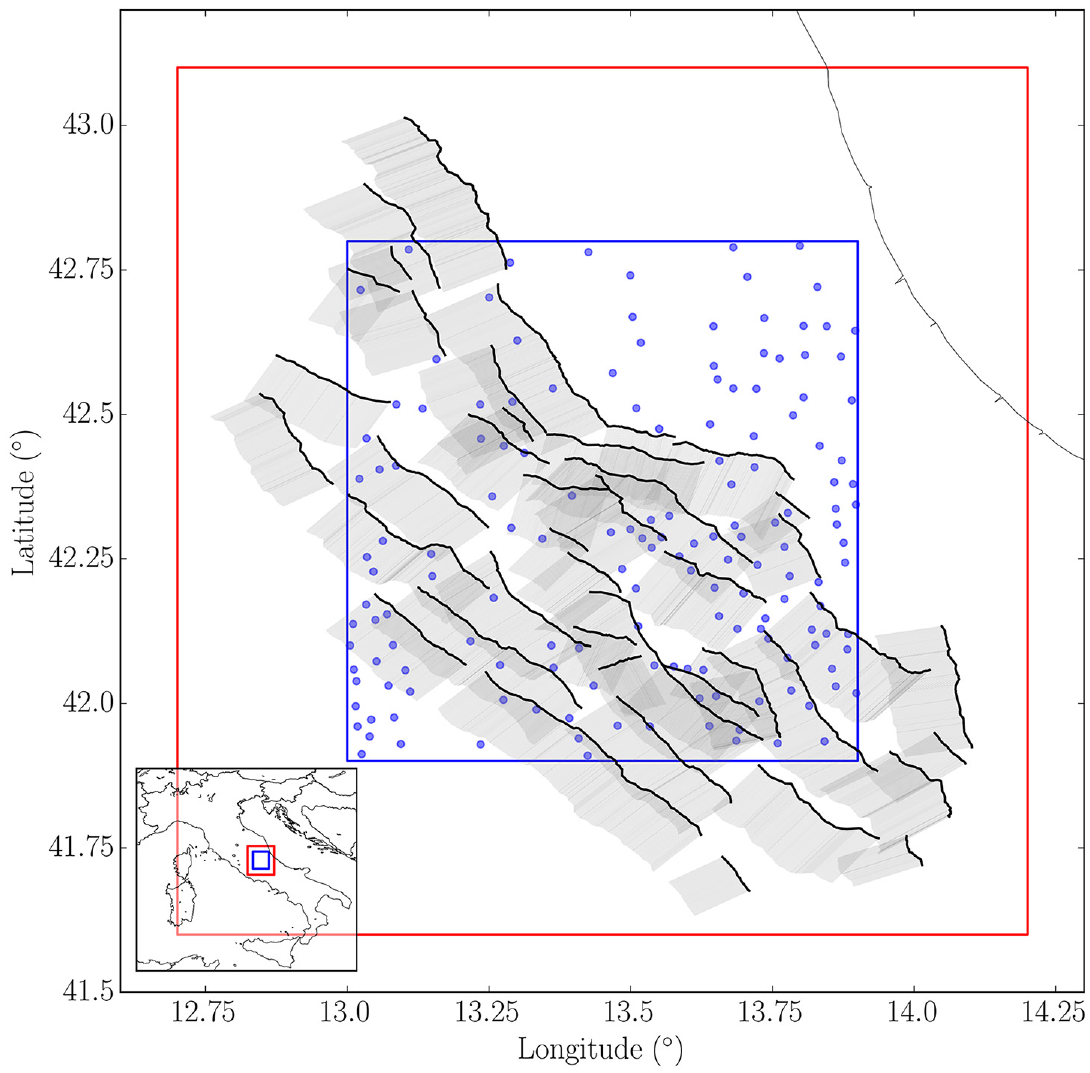

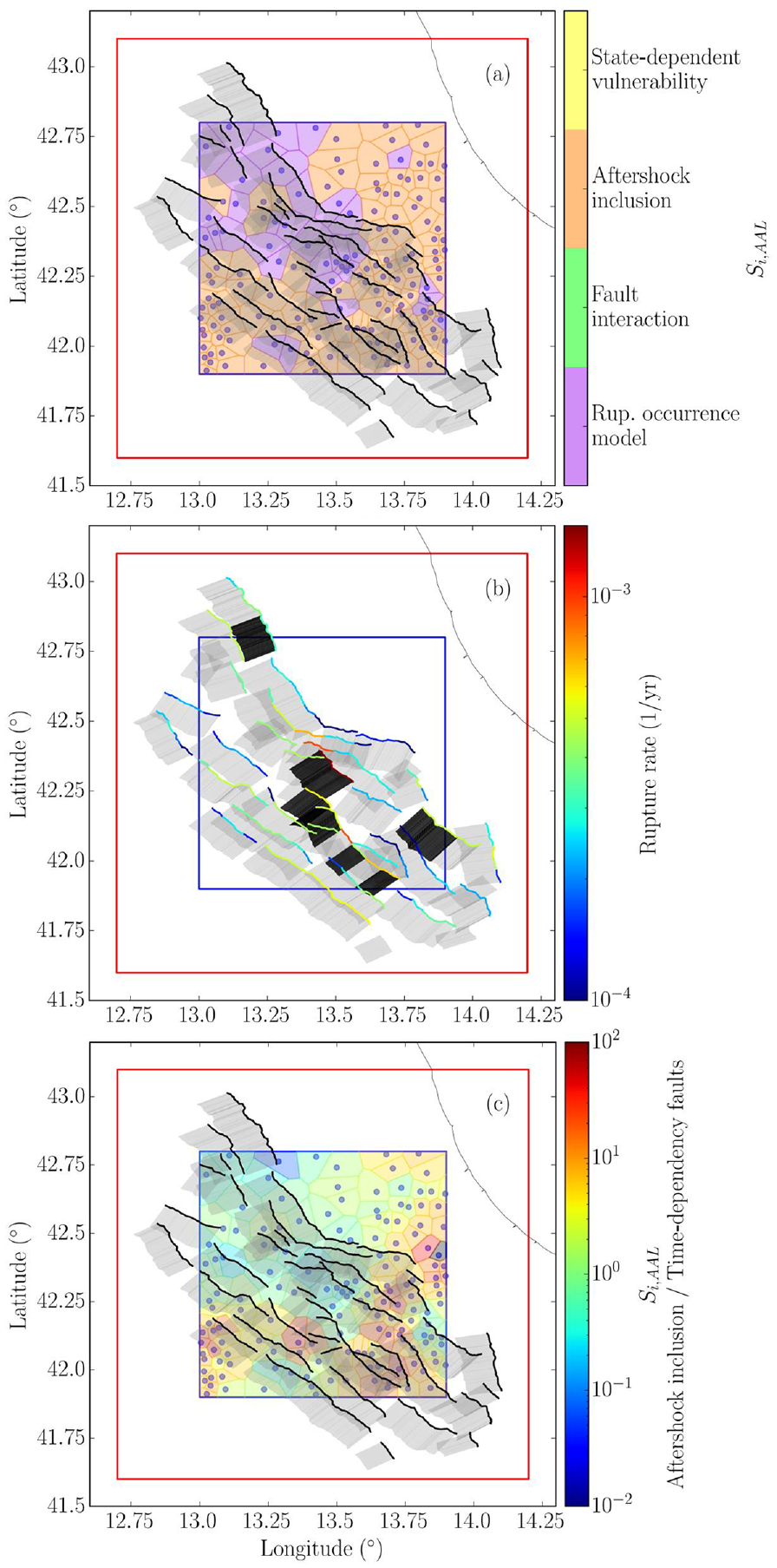

The case study is contained within the bounding box of longitudes [13°, 13.9°] and latitudes [41.9°, 42.8°] in Central Italy (Figure 2). The sensitivity results are presented for the entire portfolio described in the “Exposure module” section, and for the cities of L’Aquila, Teramo, and Avezzano specifically (i.e. only considering assets in these cities), which collectively represent around 40% of the portfolio’s total replacement value.

Case-study portfolio (subset of that presented in Crowley et al. (2021a), blue dots within the blue polygon, representing density-weighted centroids). The red polygon is the study area used in Iacoletti et al. (2022a) to generate the stochastic event sets. The 43 considered fault segments (Scotti et al., 2021) are shown in black (fault trace) and gray (geometry at depth).

Seismic hazard module

The stochastic event sets used in the case study have been developed by Iacoletti et al. (2022a) for Central Italy, within the bounding box of longitudes [12.6°, 14.2°] and latitudes [41.6°, 43.2°]. Iacoletti et al.’s (2022a) approach for stochastic event-set generation combines fault-based seismicity, distributed seismicity, and aftershocks simulated with a simulator based on the Epidemic-Type Aftershock Sequence (ETAS) model. Fault-based seismicity is simulated based on 43 fault segments (shown in Figure 2) from the Fault2SHA Central Appennines laboratory (Faure Walker et al., 2021; Scotti et al., 2021). Fault data required to calibrate the fault-based seismicity modeling component (i.e. slip rates, paleoseismic records, and date of the last event) are taken from the works by Scotti et al. (2021) and Valentini et al. (2019), and other available data sources (see Iacoletti et al., 2022a, for more details). One time-independent and three time-dependent fault rupture occurrence models are used. The time-dependent fault rupture occurrence models are based on the Brownian Passage Time (BPT; Matthews et al., 2002) model with different levels of recurrence uncertainty (Field et al., 2015): high

Exposure module

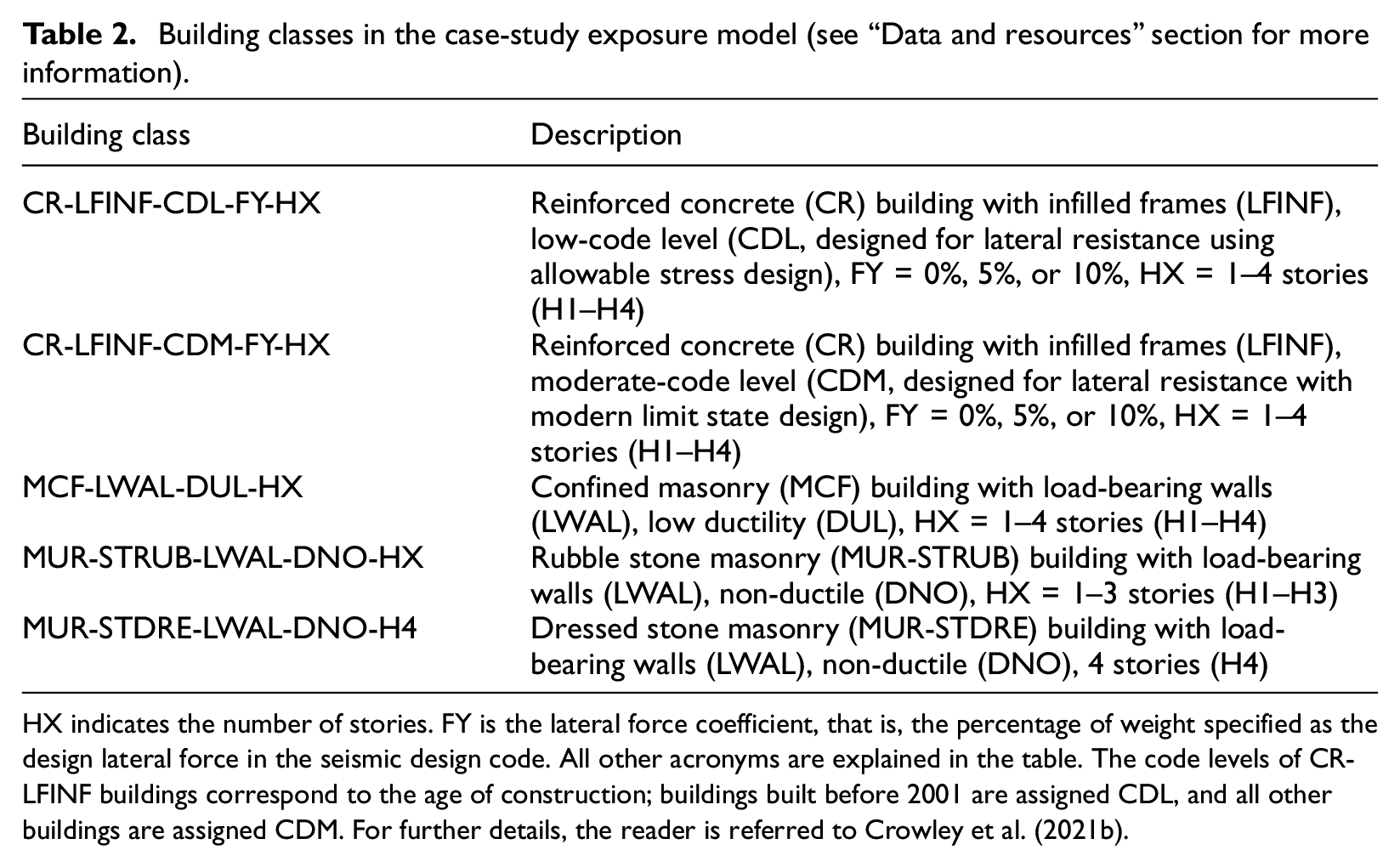

The case-study portfolio (shown in Figure 2) is a subset of the ESRM20 residential building portfolio for Italy, which was developed using 2011 public census data provided by the Department of Civil Protection (Crowley et al., 2020, 2021a). The number of buildings and associated total replacement costs (structural, non-structural, and contents) of this portfolio are aggregated at Administrative Level 3 (i.e. roughly equivalent to a township or a municipality) and represented by a density-weighted centroid, which is calculated from the built-up area density map (Crowley et al., 2021a; Dabbeek et al., 2021). Each centroid is associated with assets of different building types (classes), which describe the material and type of the lateral load-resisting system, the seismic code or ductility level, and the building height (in terms of number of stories). This case-study portfolio contains around 136,000 buildings, representing 8188 asset entries, 157 unique locations, 32 different building types, and a total replacement cost of €27.4 billion. A summary of the ESRM20 residential building classes that feature in the case-study portfolio is provided in Table 2.

Building classes in the case-study exposure model (see “Data and resources” section for more information).

HX indicates the number of stories. FY is the lateral force coefficient, that is, the percentage of weight specified as the design lateral force in the seismic design code. All other acronyms are explained in the table. The code levels of CR-LFINF buildings correspond to the age of construction; buildings built before 2001 are assigned CDL, and all other buildings are assigned CDM. For further details, the reader is referred to Crowley et al. (2021b).

Vulnerability module

We use the suite of single-ground-motion (i.e. mainshock-only) and state-dependent vulnerability models developed by Iacoletti et al. (2023) for the building types used in this study (available at https://github.com/SalvIac/sequence_frag_vuln). These models have been developed based on the energy-based probabilistic seismic demand model by Gentile and Galasso (2021), which is a physically consistent model that accounts for the accumulation of damage (even though it is solely based on numerical analyses and requires further experimental/field validation). The IM associated with each state-dependent and single-ground-motion vulnerability model is the average spectral acceleration at a range of periods of interest (which vary for each building type), calculated from the capacity curve associated with each taxonomy (Iacoletti et al., 2023; Martins and Silva, 2021). Each state-dependent vulnerability model is conditional on the previous

Ground-up losses

Figure 3 provides the uniformly weighted logic tree of time-dependent input options investigated. The number of samples N and the number of years K of generated seismicity are case-study-dependent and affect the computational time needed to run the sensitivity analysis. For this study,

Logic tree used in the sensitivity analysis.

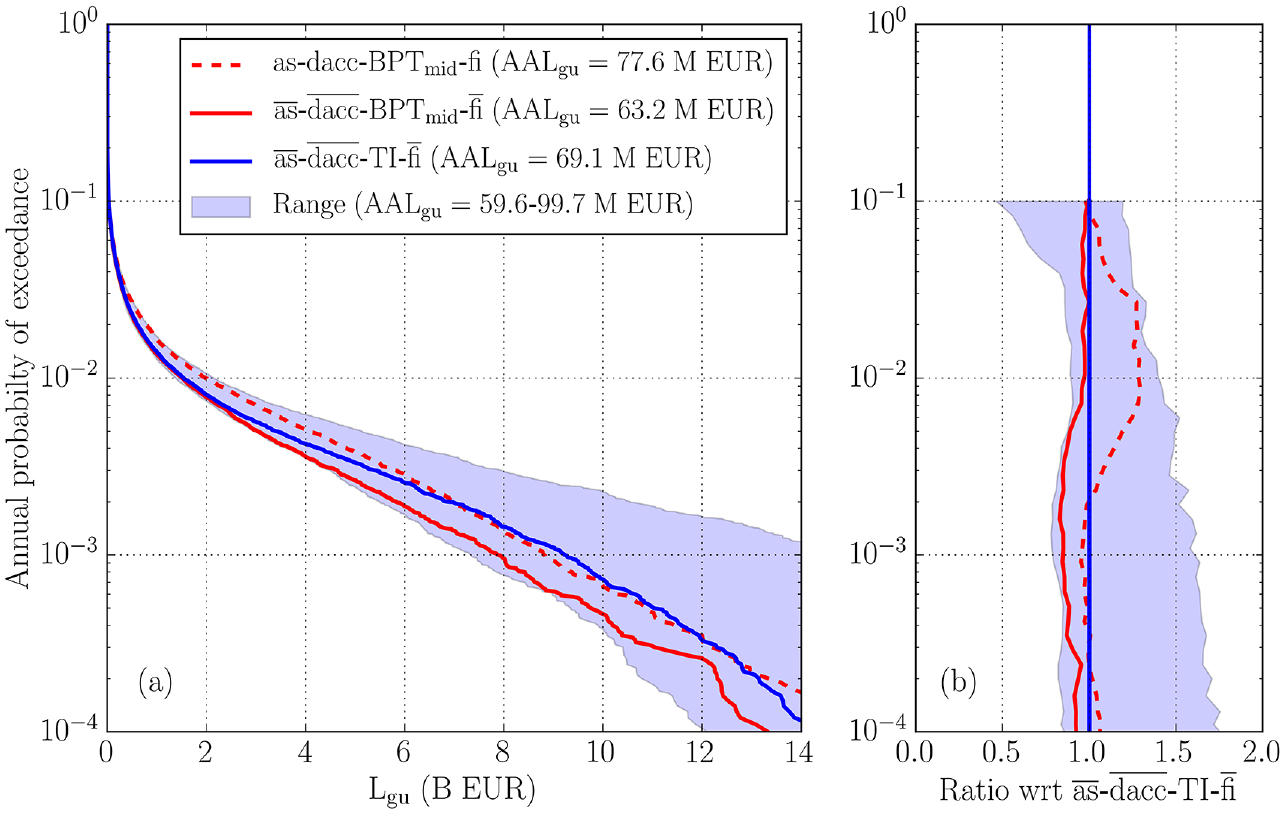

(a) Lgu AEP curves for

Figure 5 provides

At L’Aquila, the highest

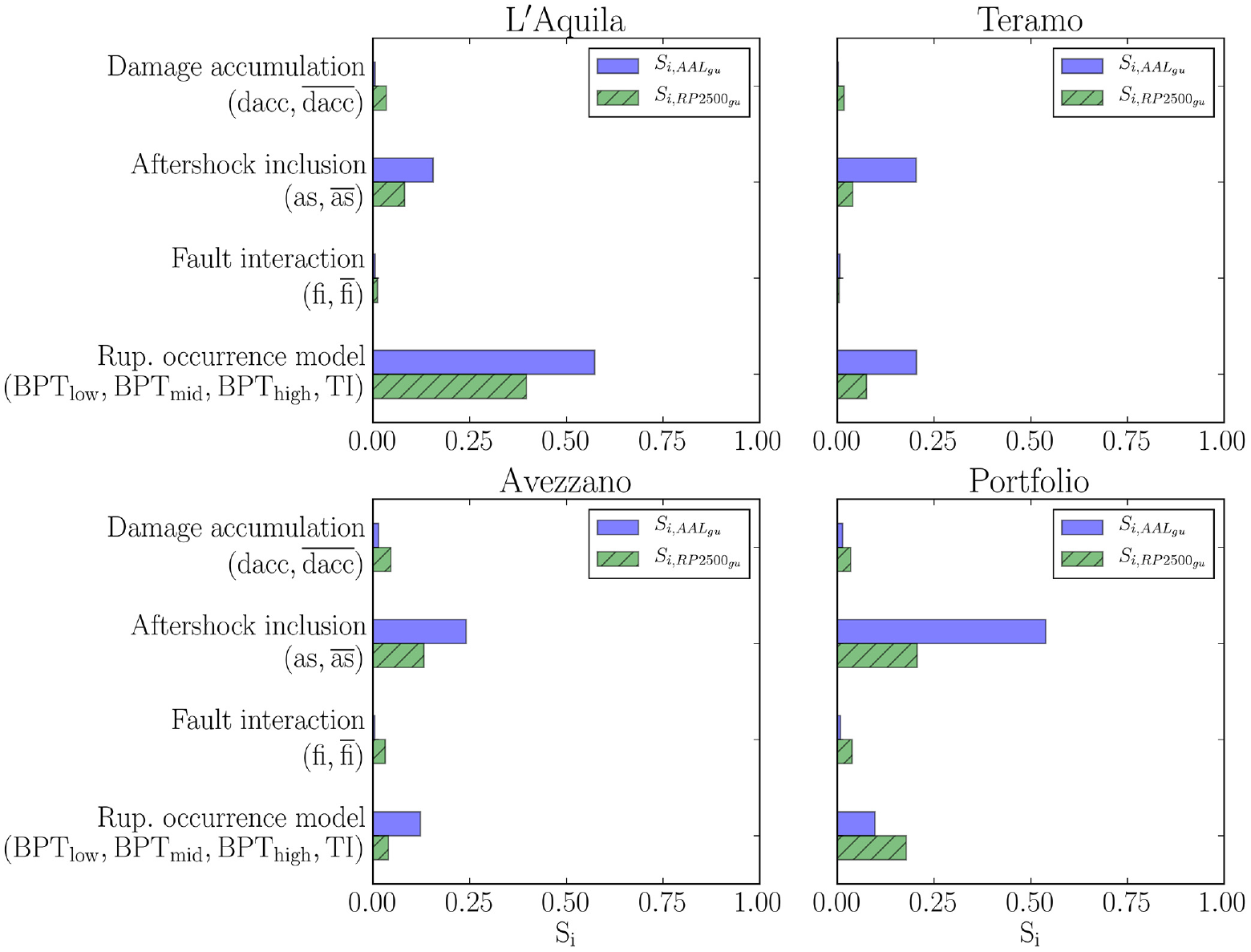

The sensitivity analysis for AALgu is repeated at each centroid of the portfolio (see Figure 2) separately to explore the spatial variability of corresponding

Maps of (a) the time-dependent input option associated with the highest

Gross losses

The sensitivity of gross losses is investigated for 5-h-clause windows (see Figure 3): 0 (equivalent to no hours clause), 24, 72, 168, and 504 h, using three levels of deductible (set respectively as 0.1%, 1%, and 10% of the replacement cost of each asset). The insurance limit is set to 100% of the replacement cost of each asset. Reinsurance considerations are neglected in this study for simplicity.

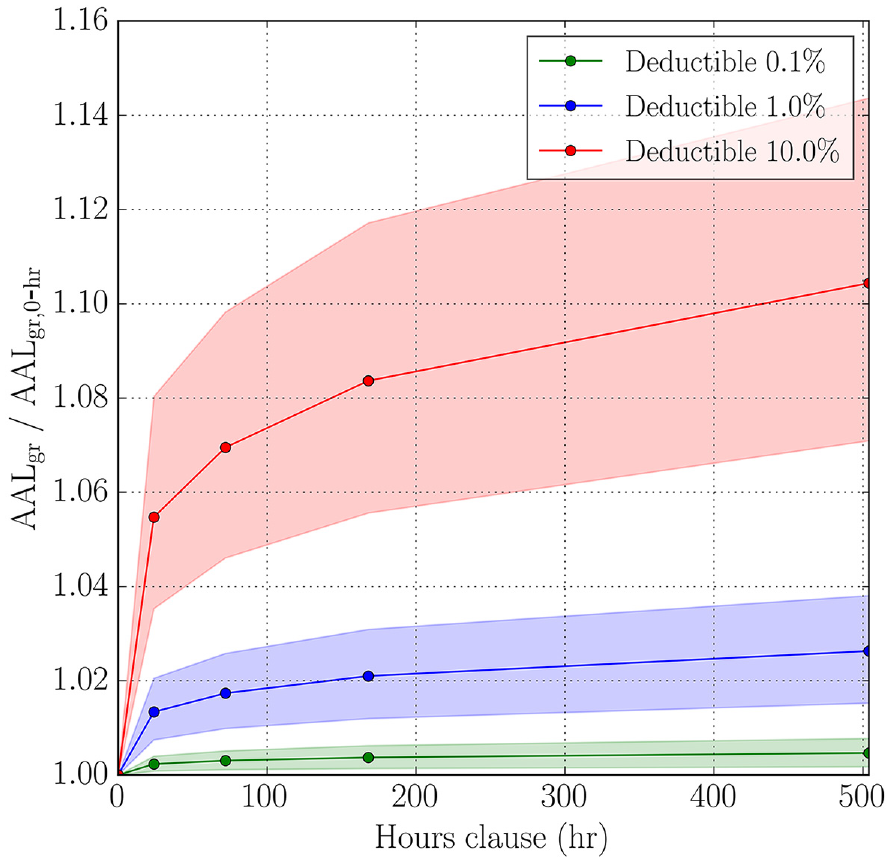

Figure 7 demonstrates the effect of different hours-clause windows and deductibles on AALgr, for sets of logic-tree branches that include aftershocks (as). The AALgr increases (with a decreasing gradient) as the hours-clause window increases and more (cumulative) event losses are accounted for. The decreasing gradient reflects the decreasing rate of aftershocks over time (Utsu et al., 1995).

Ratio between AALgr and

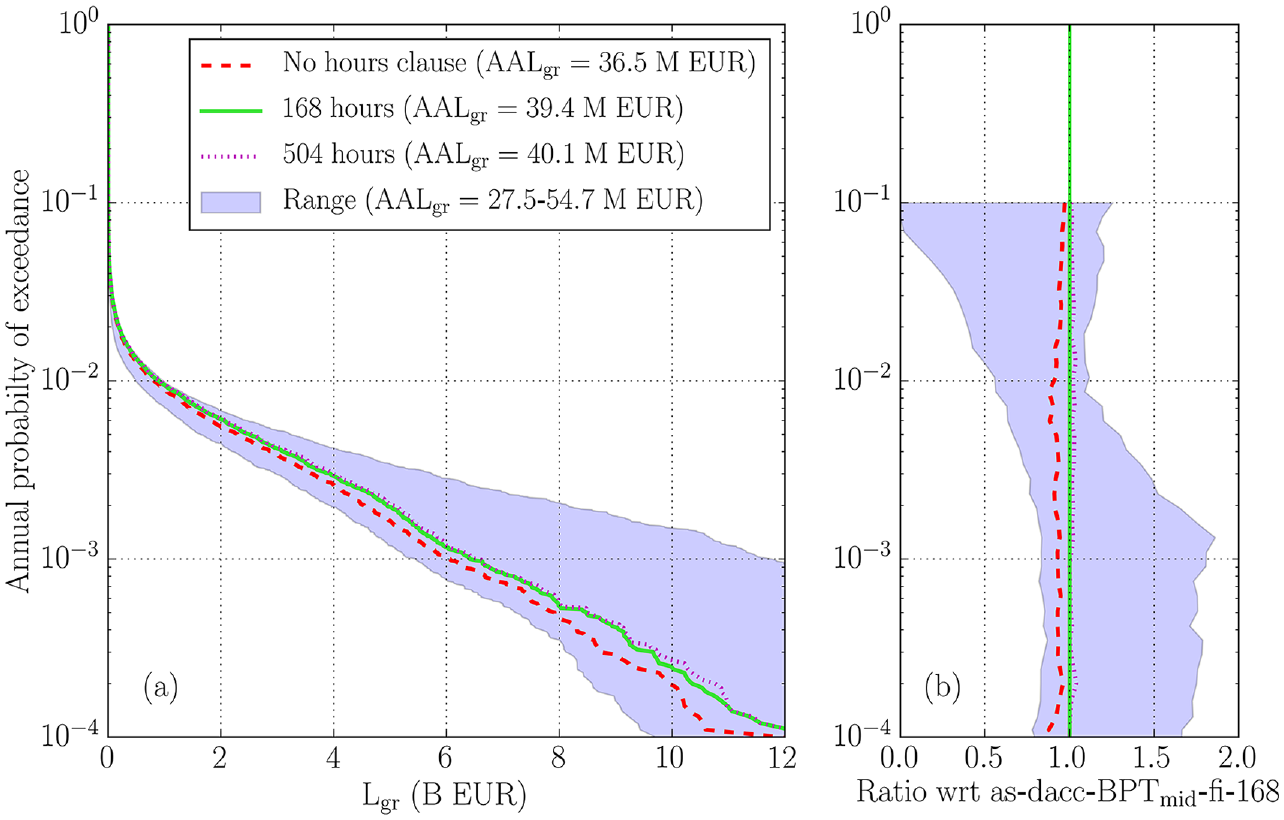

Figure 8 displays the effect of different hours-clause windows on the Lgr AEP curve, for the most complex set of logic-tree branches (i.e.

(a) Lgr AEP curves for

Figure 9 provides the

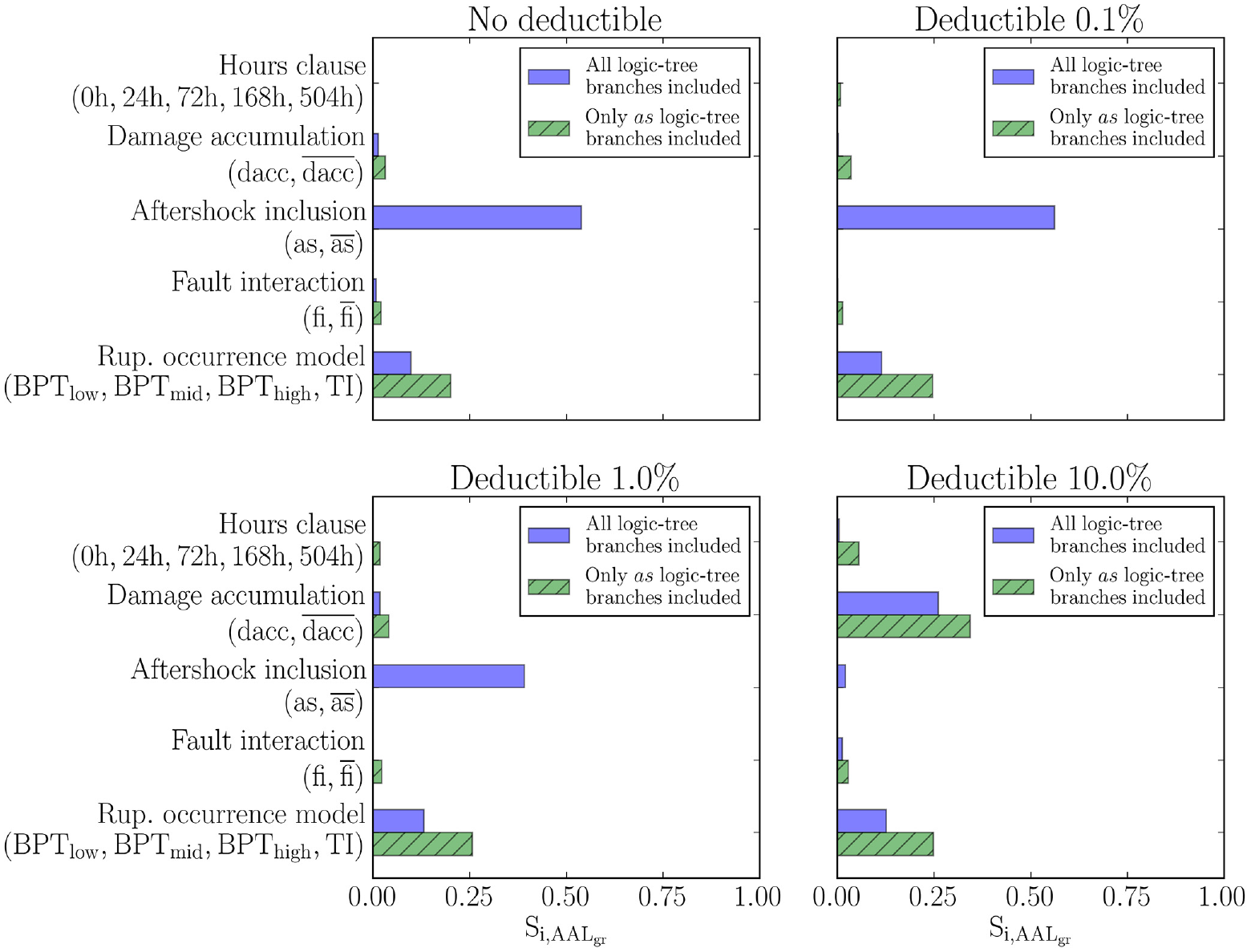

The sensitivity analysis is repeated to further explore

Conclusions

This study explored the sensitivity of a selection of monetary loss metrics to various time dependencies often neglected in conventional earthquake risk models. An event-based time-dependent earthquake risk assessment methodology was used for the sensitivity analysis, accounting for long-term time-dependent rupture occurrences that include the effects of fault interaction, short-term hazard increases caused by aftershocks, and damage accumulation in assets due to multiple ground motions occurring in a short time period. The investigation was designed to provide important insights for the catastrophe insurance and reinsurance industry, so specific insurance features (e.g. hours clauses) were also considered in the calculations. A sample portfolio in Central Italy, including the cities of L’Aquila, Teramo, and Avezzano, was used as a case study for the investigation.

The sensitivity analysis revealed that the AALgu and 2500-year-RP Lgu loss metrics are most sensitive to the choice of long-term fault rupture occurrence model and whether or not aftershocks are accounted for. Thus, these two modeling features are the most important to constrain when developing a time-dependent seismic risk model (at least for the case study investigated). AALgu is generally more sensitive to the modeling of aftershocks than 2500-year-RP Lgu. This is because aftershocks increase the short-term hazard estimates and corresponding losses at low RP. Time-dependent fault rupture occurrence models can also significantly affect AALgu close to a fault that recently ruptured (e.g. at L’Aquila). The sensitivity of specific-RP Lgu to aftershock modeling and fault rupture occurrence modeling respectively decreases and increases with increasing RP. This means that the choice of fault rupture occurrence model is more important than the consideration of aftershocks for large-RP Lgu (including the 2500-year-RP Lgu metric specifically examined). The sensitivity of the loss metrics to the modeling of vulnerability is relatively low but increases with increasing RP and larger losses produced by subsequent aftershocks. However, the fragility/vulnerability models used in this study are based on a probabilistic seismic demand model that has not been validated using experimental or field data, which could have affected the sensitivity results. Therefore, the effects of damage accumulation on risk obtained in this study should be treated as illustrative only. The sensitivity of the ground-up loss metrics to fault interaction is low, such that this modeling feature is the least important to constrain in a time-dependent seismic risk model.

The sensitivity results are generally similar in the case of gross losses; the long-term rupture occurrence and aftershock modeling components are also the most crucial to constrain for AALgr. However, if there is a high deductible level associated with portfolio assets (around 10%, as considered for the case study), then accounting for damage accumulation also becomes important. The sensitivity of AALgr to the length of the hours clause is generally relatively low.

The findings of this study focus on the sensitivity of relative loss metrics rather than absolute loss estimates and are limited in applicability to the case study, the logic-tree structure, and the underlying methodologies and assumptions. For instance, the calculation of Lgr depends on the implementation details of the hours clause. The process insurers use for assigning loss claims to specific hours or events is not standardized across the industry; the implementation procedure could be refined to better match the practices of specific insurers. The methodology used in this study could be extended by additionally considering reinsurance (and associated reinstatement clauses). Adopting alternative hazard modeling or damage accumulation methods, and/or focusing on another case-study region (where, for instance, fault interaction has higher impacts, e.g. California, King et al., 1994), could lead to different sensitivity results. Nevertheless, the sensitivity results obtained provide some valuable guidance on the treatment and importance of time dependencies in advanced large-scale (i.e. portfolio) earthquake risk models.

Footnotes

Acknowledgements

The authors thank Dr Crescenzo Petrone, Dr Umberto Tomassetti, and Dr Myrto Papaspiliou from Gallagher Re for the input and feedback on the study. The authors thank Dr Athanasios Papadopoulos, Prof. Paolo Bazzurro, and one anonymous reviewer for insightful comments that helped improve the quality of this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: S.I. was supported by the UK Engineering and Physical Sciences Research Council (EPSRC), Industrial Cooperative Awards in Science & Technology (CASE) grant (Project reference: 2261161) for University College London and Willis Towers Watson (WTW), through the Willis Research Network (WRN).

Data and resources

The ESRM20 residential exposure model for Italy used in this study is available at https://gitlab.seismo.ethz.ch/efehr/esrm20_exposure/-/blob/master/_exposure_models/Exposure_Model_Italy_Res.csv, last accessed 28 September 2022. The ESRM20 vulnerability mapping file is available at https://gitlab.seismo.ethz.ch/efehr/esrm20/-/blob/main/Vulnerability/esrm20_exposure_vulnerability_mapping.csv, last accessed 28 September 2022. The ESRM20 capacity curves used to calibrate the vulnerability models (Iacoletti et al., 2023) are available at ![]() , last accessed 28 September 2022.

, last accessed 28 September 2022.