Abstract

This article examines fintech platforms’ strategies of development and growth through an analysis of the Philippines’ finance super app, GCash, home to over 90 million registered users and crucial in a country where poor rural infrastructure, weak institutions, and perceived barriers to financial account ownership have led to historically low financial inclusion. Drawing from a platform biography of GCash's development, alongside a walkthrough of its super app form, the study examines GCash as a platform, super app, and megacorp, tracing how GCash evolved from its SMS remittance-based foundations into a sprawling constellation of services. GCash not only extends access to financial services but also structures transactions and shapes the cultural and economic conditions of everyday exchange. We argue that GCash operates simultaneously as a catalog of digital transactions—revealing the interconnections among markets, persons, and technology—and as a financial infrastructure whose reach is structured by corporate conglomerates, state support, global capital, and digital architectures. These highlight the tensions at the heart of GCash: its promise of “finance for all” is entangled with its embedding in a megacorp and its reliance on partnerships with global capital. By foregrounding these tensions, the article situates GCash within broader dynamics of the super-appification of finance, underscoring how platform-led financial inclusion efforts are bound up with the consolidation of corporate power and the governance challenges of financialization in contexts of infrastructural weakness and economic precarity.

GCash is a Philippine financial super app home to 94 million registered users (Pascual, 2024) and 5.8 million merchants and social sellers (Globe Telecom, 2023b). Operated by G-Xchange Inc. and owned by Globe Fintech Innovations Inc., the super app began as an SMS-based SIM toolkit service introduced in 2004 by Philippine telecommunications conglomerate Globe for sending and receiving e-money using text-based menus. The mobile app was then launched in 2012 and referred to as “a mobile commerce service” in 2013 (Globe Telecom, 2013), “the country's leading e-wallet” in 2019 (Excelity Global, 2019), and finally, the “#1 Finance Super App” by 2023 (GCash, 2023). Today, GCash provides financial services like savings, bills payment, credit, investments, and insurance, as well as nonfinancial functions like shopping, gaming, wellness, delivery booking, and job search.

By March 2022, GCash's monthly gross transactions reached P500 billion (US$8.5 billion) in value (Globe Telecom, 2022a), with the app becoming a noun for electronic money (e.g., “I have GCash”) and a verb for transactions (e.g., “I’ll GCash you”) in the local vernacular. Its role as a financial super app is crucial in the Philippines, where poor rural infrastructure, weak institutions, and perceived barriers to account ownership have led to low financial inclusion (Bangko Sentral ng Pilipinas, 2022a; Hasnain et al., 2015)—a gap recognized by GCash leadership early on (Alampay & Bala, 2010). Positioned as the “National Champion for Financial Inclusion” (Globe Telecom, 2023b: 151), GCash promises unbanked and underbanked populations with digital financial solutions by directing a large client base of prepaid mobile phone users toward app-based finance (Jain and Gabor, 2020). But despite the role it has grown to play in the Philippine financial ecosystem, there are few scholarly studies on GCash, with dominant analyses focusing on usability and consumer acceptance (e.g., Gabriel et al., 2022; Gumasing et al., 2023).

Thus, this paper explores, first, how GCash has evolved from an SMS-based platform for mobile remittance and load transfer into an integrated platform that organizes a wide range of financial and nonfinancial transactions and, second, how the super app's design, as a communicative and performative tool, actualizes and configures these transactions. We build on the scholarship on the interrelationships of conglomerates, megacorps, platforms, and super apps (Athique and Kumar, 2022; Srnicek, 2024; Steinberg et al., 2025) as well as works illustrating the plural and distinct processes of “platform capitalisms” (Steinberg et al., 2025). Our analysis further aligns with work showing how platforms’ corporate ambitions are embedded in the design of super apps (Jia et al., 2022; Steinberg et al., 2025), where market dominance is pursued through an “aggressive combination of technological design and commercial strategy” (Athique and Kumar, 2022). This process not only formats access to financial services but also reconditions the very terms of exchange—allowing the platform to capture value from individual transactions and extended “transaction chains” (Athique, 2023), while simultaneously advancing financial inclusion and entrenching corporate power.

GCash's fintech-first trajectory—as opposed to other super apps that started in communication (e.g., WeChat) or mobility (e.g., Grab)—established early trust as a regulated money transfer tool and facilitated rapid adoption, especially in light of the Philippines’ large diaspora and limited banking infrastructure. As we discuss in the succeeding sections, strategic development of multi-sided markets and major investments consolidated both its capital strength and ambitions, with the digital platform extending earlier forms of industrial organization and local capital accumulation (Athique, 2019; Athique and Kumar, 2022). Further, GCash operates within the Philippines’ “Test and Learn Approach,” a regulatory sandbox model that allows fintech companies to shape innovation flexibly (Bangko Sentral ng Pilipinas, 2022b; Mendoza and Macadato, 2022). Studying GCash therefore provides a critical lens on conglomeration in the time of platforms (Athique and Kumar, 2022; Jia et al., 2022; Srnicek, 2024; Steinberg et al., 2025; van der Vlist et al., 2025), while also showing how super apps configure the conditions of digital transactions in pursuit of both financial inclusion and commercial growth.

The formatting of platforms and the performative dynamics of super apps

Described as “do-everything apps” (Steinberg et al., 2025: 1407), super apps represent a convergence of a wide variety of services within a single ecosystem that influence user interactions and broader exchange cultures (Chen et al., 2018; Goggin, 2021; Jia et al., 2022; Nieborg and Helmond, 2022; van der Vlist et al., 2025). In our analysis of GCash, we engage Athique and Kumar’s discussion on the integration of super apps, platforms, and the digital megacorp to examine the super app as the “sensory enclosure of the retail marketplace,” (Athique and Kumar, 2022: 2) in the do-everything software users install into their phones and the platform as the technical and business ecosystems that make the app's services possible. This paper thus makes a distinction and relation between the GCash super app and the wider GCash platform upon which the app is built. Further, understanding platforms as conglomerates (Jia et al., 2022; Srnicek, 2024), we looked beyond the app interface and into the interlocking technologies, infrastructures, business relationships, and capital interests that make up the GCash digital megacorp (Athique, 2019; Athique and Kumar, 2022; Gawer, 2014, 2021).

This study also engages Steinberg's “threefold process of formatting of platforms” (Steinberg, 2020: 2–3), originally studied in the context of the LINE super app, to map how GCash constructs, symbolizes, organizes, and orders transactions. Extending this analytical lens, we examine GCash's: (a) formatting of a wide array of financial and e-commerce services for exchange as “strategy to construct multi-sided markets” that are platform ready (in other words, how it defines what transactions are); (b) identification and construction of markets as sites of exchange (how it defines the conditions for transacting); and (c) identification of producers and consumers who can participate in these markets (how it defines transactional subjects).

The sociotechnical shaping of transactions and transactional conditions within super apps occurs through different mechanisms. First, super apps build connections and make visible a network of disparate traditional and emergent markets of goods and services (Steinberg, 2020), facilitating transactions by providing a seamless and integrated experience across these diverse industries and activities (Helmond, 2015). Second, platforms dictate what is transactable, how transactions are conducted, and the norms surrounding these interactions (van der Vlist et al., 2025). By making transactional possibilities visible, platforms establish and reinforce transactional cultures within their ecosystems while also making possible the aggregation of this transactional data to enrich a platform's capitalization (Athique and Kumar, 2022; Langley and Leyshon, 2021). Crucially, platforms’ “financialization” and “infrastructuralization” strategies are at the base of these transactional possibilities (Jia et al., 2022) and are crucial to understand their growth as a megacorp (Athique and Kumar, 2022). Eichner (1969) defines the megacorp as a firm whose sheer scale within its industrial sector and prominence in financial markets enable it to exert structural dominance. Such critical mass allows the megacorp to consolidate market power and effectively insulate itself from meaningful competition (Athique and Kumar, 2022).

We conducted a platform biography to examine GCash's origins and developmental trajectory and an app walkthrough to understand GCash's articulation in super app form. This combined approach provides not just a map of transactional possibilities but also a window into the megacorp dynamics shaping fintech super apps that, in turn, impact the transactional conditions of millions of people. Attending to the multi-sided functionality of platforms, scholars emphasize the value of examining how platforms develop and operate historically across multiple stakeholders (Helmond and van der Vlist, 2019; Zhang and Chen, 2022), while (Steinberg 2024: 2) urges researchers to examine “paraplatforms,” which include lineage dynamics “preceding the platform historically” and “informing the platform industrially.”

In this study, we trace GCash's trajectory from its beginnings as a provider of financial services to its subsequent expansion into e-commerce and e-government, situating this growth within its ownership ties to Globe, Ant Group, and Ayala as part of a wider megacorp structure. We also examine the evolution of its financial services portfolio through a review of annual investor reports and online publications by GCash/Mynt and its parent company Globe, alongside regulatory documents such as privacy notices, acceptable use policies, terms and conditions, and issuances from the country's central bank, the Bangko Sentral ng Pilipinas (BSP). Publications by GCash's strategic partners, including the Ant Group, were analyzed to situate its operations within broader industry developments and governance frameworks. Keywords include GCash, super app, fintech (Philippines), Globe Fintech Innovations, digital financial transactions (Philippines), digital payments (Philippines), digital wallet (Philippines), digital banking (Philippines), and finance app (Philippines) to identify scholarly articles and reports on the developing Philippine fintech sector from GCash's inception in 2004 up until 2025. Constructing GCash's developmental timeline (see Figure 1) allowed us to establish a longer view of its infrastructural vision, including its ambitions and trajectory, the socioeconomic and political environment in which it operates, and the broader corporate dynamics and practices that function to generate new forms of digital power and influence.

Visualizing GCash’s origins and development (2004–2025). Multiple sources cited in-text.

Meanwhile, the walkthrough method allowed us to examine the GCash super app's “technological mechanisms and embedded cultural references” (Light et al., 2018: 882) through direct engagement with its interface from registration to app closure. 1 This approach centers the app as a key site for the production and materialization of social meaning, uncovering how apps script interactions, collect user data, or embed business models into everyday transactions (Duguay and Gold-Apel, 2023). Examining GCash's interface provides a critical visual and interactive entry point into the platform's logics and ambitions, even as it presents itself as a neutral tool or intermediary (Gillespie, 2010) in the everyday transactional cultures of exchange and sociality. Drawing from the concept of mediators in actor–network theory, this method considers interfaces as mediators, which construct or transfer meaning, configure relations among actors, and guide user interaction as part of the apps’ larger function of cultural and economic transformation (Light et al., 2018). Because design choices are material traces of the parent company's strategy and expansive ambitions of capturing everyday financial life, this analysis of mediator characteristics treats the app interface as a site of governance: who can participate, which fields and steps are mandatory, how features are represented, grouped, or sequenced, which affordances are foregrounded or hidden, and how visual and textual rhetoric establishes cultural meaning. We used version 5.67.0 of the app between the months of June 2023 and October 2023, on a new account created with a newly registered SIM card on an Android OS mobile phone as well as an established GCash account on an iOS device. The analysis is based on field notes generated during app use, taking note of available screens, functions, and representations.

Our findings are organized into four main sections. We start by outlining the origins of GCash as a vehicle for embedded finance, illustrating its distinctive origins and implications for its subsequent reimagining as a super app. We then examine who can transact, discussing how the app defines who can access GCash's functions and features. Next, we explore what transactions are as defined by the app, how they make visible the breadth of transactions and transactional possibilities, and how “transaction chains” (Athique, 2023) are facilitated on the super app. The fourth section then examines the conditions for transacting and how the app reconfigures the ways transactions are culturally understood and experienced. We conclude by reflecting on how these dynamics together shape transaction ecosystems in the Philippines and what they reveal about the broader logics and strategies of platform capitalism.

Origins and trajectory of GCash

GCash, operated by G-Xchange Inc. (GXI), is part of Mynt—considered the Philippines’ first and only $5 billion unicorn and a leader in mobile financial services. Mynt also owns Fuse, a financing arm that expands access to microloans and business loans (GCash, 2023). GCash and Fuse illustrate how a single fintech company has combined mobile payments, digital savings, insurance, investments, e-commerce, e-government services, and credit to drive financial services at scale in the Philippines. The GCash super app is owned by Globe Fintech Innovations Inc. (doing business as Mynt). Mynt itself is a joint venture between the Globe Group, through its corporate venture builder 917Ventures (35.53% stake); Ant Group, an affiliate of Alibaba Group (33.77%); and Ayala Corporation, one of the Philippines’ largest conglomerates (30.7%) (Reuters, 2024). Globe is majority-owned by Ayala Corporation and Singapore's Singtel, while Ant Group's largest shareholder is Alibaba. At the center of this ownership structure is the Ayala family, a long-standing land-owning elite (Pinches, 1992) whose business empire extends across real estate, utilities, banking, and telecommunications. Through Mermac Inc., the family holds the controlling stake in Ayala Corporation. Mynt's valuation doubled to US$5 billion in 2024, following Ayala Corporation's increased equity stake and the entry of Japan's Mitsubishi UFJ Financial Group (MUFG) as a new investor (ABS-CBN News, 2024; Reuters, 2024). This convergence of entrenched local elites and global capital underscores how GCash's rise is not simply a story of financial inclusion but also of how megacorps and transnational investors shape the infrastructures of everyday transactions.

Despite its current wide portfolio as a megacorp, GCash had more modest beginnings, initially focused on remittance and payment transfers. As an SMS-based toolkit, GCash as a financial service platform in 2004 turned ordinary text messages into a secure, low-cost mobile wallet for money transfer, designed to reach the unbanked and large population of overseas migrant workers (Alampay and Bala, 2010; Maurer, 2015). The recipient receives a domestic or international remittance via their mobile phone, with Globe Telecom issuing a GCash account via SMS to hold the transferred funds. The recipient can then withdraw (or “cash out”) the money at partner outlets. Even in this earlier SMS-based iteration, the purchasing of goods and services via GCash was possible, albeit with limited uptake, covering a few initial merchants such as fast-food restaurants and bookstores (Mendes et al., 2007). This version of GCash also allowed person-to-person (P2P) transfers, airtime purchases, bills and tuition payments, and, a year after its launch, a growing set of services (loans, insurance, charitable donations, payment of train tickets) that aimed to tie it into everyday economic life (Mendes et al., 2007; Soriano and Barbin, 2020). GCash's registration process lowered barriers to access as it could be completed over SMS, and any basic Globe handset could participate—contrasting with card-based, ATM-linked competitors such as Smart Money (Alampay and Bala, 2010; Mendes et al., 2007). In 2007, Globe Telecom reported that GCash's user base had grown to 1.4 million from 1.2 million the previous year (2008)—still representing only about 1.5% of the Philippines’ roughly 90 million population at the time. Yet by the end of that same year, GCash was already processing an average monthly transaction value of approximately PHP 6.23 billion (US$138 million) (Globe, 2008b: 65). With this approach, Globe emulated a banking network even without a banking partner (Wishart, 2006).

GCash's early rise was contingent on how effectively it tapped into local cultures of exchange as a process of embedding (Athique and Lorenzana, 2025), addressing the need for remittance mechanisms among the unbanked in a country deeply shaped by migration. Further, Filipino users were already accustomed to SMS—introduced in 1994, after which the Philippines was dubbed the “SMS capital of the world” (Mendes et al., 2007)—and to phone-based value exchange practices such as pasaload (peer-to-peer transfers of prepaid airtime) and other grassroots m-commerce innovations enabled by SMS toolkits, which normalized the idea that mobile phones could hold monetary value (Maurer, 2015; Wishart, 2006). GCash formalized and extended these practices by creating regulated e-money accounts, establishing a dense cash-in/cash-out merchant network through sari-sari (variety) stores, and building rails for remittances and microtransactions. These capabilities supported later pilots such as “Text-a-Payment” for microfinance repayments actualized via partnerships with rural banks to expand access in underbanked regions (Alampay, 2008; Mendes et al., 2007; Soriano and Barbin, 2007). Yet despite its technical architecture, which also supported m-commerce and early e-government services, GCash struggled to achieve scale. Service providers hesitated to invest given its still-limited consumer base, while potential users remained unconvinced by the relatively narrow range of available services—a chicken-and-egg dilemma that tempered its initial adoption.

The development of smartphones and mobile broadband transformed the landscape of financial exchange, prompting GCash to launch its web-based platform in 2012. Still, GCash initially struggled to keep pace with user growth, relying on a costly and inflexible legacy platform. As the platform reached greater use, its users experienced downtime, failed transactions, and service disruptions, and scaling through traditional means required cycles of hardware acquisition, licensing, and human resources. In 2017, Globe entered into a strategic partnership with Ant Financial (later Ant Group) to enhance both GCash and its lending arm Fuse (Alibaba Cloud, n.d.). This collaboration marked a turning point in GCash's trajectory, as it not only infused capital but also provided access to Alibaba's technological expertise and infrastructure. The timing of these developments proved pivotal. The partnership with Alibaba Cloud resolved critical technical bottlenecks by providing scalable infrastructure to accommodate surges in demand, while simultaneously enhancing GCash's data security and analytics capacity. This expanded the platform's ability to process and leverage vast volumes of transactional data while also repositioning it from a financial tool to a data-driven platform capable of refining and diversifying its services. The onset of the COVID-19 pandemic created the perfect conjuncture for these capacities to be amplified: Amid strict lockdowns, GCash became a financial lifeline, enabling millions to adopt and normalize digital payments almost overnight (Acopiado et al., 2022). With cloud infrastructure in place and COVID-19 spurring its wide use, the platform supported a 3.7-fold growth in monthly active users and a 1000% surge in transactions (Alibaba Cloud, n.d.). In this sense, the alliance with Alibaba was both technical and strategic as it embedded GCash within global platform capitalism while laying the infrastructural foundations for its super app ambitions and its eventual position as a central conduit for financial inclusion and consumer data in the Philippines.

Another way the GCash app has expanded its functions and features is through partnerships with a broader range of firms and suppliers in its business ecosystem (Wishart, 2006)—a strategy it continues to deploy today (Asian Banking and Finance, 2022). It started with retailers and utility companies to support the Bills function, as well as banks and remittance companies for the Send function. GCash first built the visible “distribution layer” (Athique and Kumar, 2022) of its platform through community-based sari-sari stores that served as effective cash-in/cash-out points (Balinbin, 2021). By 2020, partner outlets numbered 33,000, including pawnshops, sari-sari stores, convenience stores, and supermarkets (Cordero, 2020). To expand its capture of the overseas remittances market, GCash partnered with Western Union, allowing Overseas Filipino Workers (OFWs) to directly send money into GCash wallets from over 200 countries (Mynt, 2025a). The platform has also long partnered with established pawnshops and remittance companies like Tambunting and Cebuana for domestic remittances that support its Padala function. More recently, its partnership with Palawan Pawnshop, which has 3500 branches in remote areas nationwide, has made local remittances, digital-to-cash conversion, and related services more accessible. This partnership extends into insurance, with Palawan's products being integrated into GInsure (Mynt, 2025b). These layered infrastructures—local cash-in/cash-out networks and global remittance integrations—positioned GCash as a central hub for the inflow and outflow of money in the Philippines and within it, a crucial role in an economy where personal remittances reached an all-time high of USD 38.34 billion in 2024, accounting for over 8% of the GDP (Bangko Sentral ng Pilipinas, 2025a).

GCash “internalizes the functions of the web” by expanding its portfolio of financial and nonfinancial services with the aim of becoming a hub of everyday life. The surge of GCash users attracted more merchants in the growing social commerce sector, boosting its vendor partnerships, ending 2021 with 4.5 million merchant partners and social sellers—up from just 1 million in 2020 (Cayabyab, 2022). To support e-commerce, it partnered with platforms like Foodpanda, Grab, Lazada, Shopee, and Entrego. In 2024, its lending arm Fuse partnered with Lazada to provide cash loans to eligible sellers, facilitating the growth of online ventures (Fintech News Philippines, 2024a). Beyond consumer e-commerce, GCash's partnership with ride-hailing, logistics, and delivery platforms included cash-in/cash-out services for workers and customers that sustain everyday transactions while generating revenues from fees (Soriano, 2024). Crucially, through its partnerships with Alipay and Visa, users can make payments abroad, signaling ambitions to extend beyond domestic use into global transactions and even B2B services (ABS-CBN News, 2024).

To support the expansion of its super app, GCash also entered into partnerships with banks, which it did not have in its early days as an SMS-based SIM toolkit (Mendes et al., 2007). GSave was launched alongside digital banking company CIMB in 2019, the same year the platform also launched GInvest in partnership with ATR Asset Management Group (ATRAM). Both GCash functions would later expand with additional partnerships with Maybank, UNO, and BPI (an Ayala-owned bank) for GSave and PDAX, Easy Equities, and AB Capital Securities for GInvest. GInsure—in partnership with companies like Singlife, Standard Insurance, Pru Life UK, Generali, and Malayan Insurance—was launched in 2020. Beyond banks, GCash partnered with businesses like 7-Eleven for barcode payments (Mercurio, 2022) and worked with the government to develop a QR code system for micro-sellers, including those in public wet markets (Globe Telecom, 2023b). When the BSP rolled out automated clearing house systems in November 2017—enabling instant and next-day electronic interbank transfers (Villanueva, 2018)—GCash quickly joined the list of participating banks.

The state has a crucial role in GCash's surge. Building on its history as a platform for conditional cash transfer programs for poor communities in the mid-2000s (Alampay and Cabotaje, 2014), GCash later became a government delivery channel for COVID-19 social amelioration programs. Between 2020 and 2022, digital transfers enabled the rapid rollout of emergency relief measures, sustaining households when mobility was severely restricted (Athique and Lorenzana, 2025). GCash, through affiliation with Ayala Corporation, is well placed to secure such government partnerships as it evokes institutional legitimacy compared to newer, less established fintech players. GCash's role as a government fintech partner was reinforced by broader policy to promote a “cash-lite” economy: The Digital Payments Transformation Roadmap and the Philippine Development Plan 2020–2023 set a target of converting 50% of all retail payments into digital form (Bangko Sentral ng Pilipinas, 2020)—a goal surpassed in 2023 when digital transactions reached 57.4% of total retail payment volume and 59.0% of value (Fintech News, 2024b). Executive Order No. 170 (s. 2022) further mandated government agencies to adopt secure digital disbursement systems for salaries, allowances, financial aid, and public transactions, laying the groundwork for broader adoption ahead of the proposed Digital Payments Act in Congress (Parrocha, 2022). Most recently, GCash partnered with the Department of Trade and Industry (DTI) and the state-owned Development Bank of the Philippines (DBP) to launch a loan financing product for sari-sari store owners and wet market vendors. While framed as expanding financial access for small-scale entrepreneurs, the initiative also incorporates informal and micro-enterprises more deeply into GCash's credit infrastructure—an integration actively promoted by the government. By integrating access to loans directly through mobile wallet, GCash extends its reach beyond digital payments into the governance of everyday livelihood economies, further embedding itself in the financial routines of Filipinos (Soriano, 2026).

GCash's growth has been driven not only by its cultural embedding in everyday financial practices—from remittances to household payments—but also by its deliberate cultivation of strategic partnerships with major global investors and partners to boost its technical infrastructure, as well as with local businesses and government to legitimate it as a partner not just for financial inclusion, but also for national development (Figure 1). Its alliances with community-based stores, retailers, pawnshops, and remittance companies expanded its distribution infrastructure; investments by global companies boosted its technological infrastructure and financial portfolio; collaborations with global and local financial businesses deepened its role in both remittance flows and e-commerce; and partnerships with government agencies positioned it as a conduit for social welfare distribution, public payments, and microfinance. Taken together, these linkages demonstrate how GCash has consolidated its position as both a cultural and institutional fixture in the Philippine economy, integrating daily practices with wider structures of state and market. Scholars have emphasized that platform growth relies on network effects: The more users adopt a platform, the more valuable it becomes to others (Srnicek, 2024). As illustrated in Figure 1, the combination of these strategies allowed GCash's user population to soar, justifying and also reinforcing super app development and growth. This dynamic feeds into data-driven returns to scale, as an expanding user base generates ever more information that can be leveraged to refine or launch app services, in turn drawing in additional users, and can also be used for capitalization (Langley and Leyshon, 2021). With this context established, we now turn to the functions and dynamics of GCash as a super app and how these strategic partnerships are reflected in the app's design.

Who transacts

In a country with historically low financial inclusion and a super app aiming to remove barriers to financial access, the question of “who transacts?” becomes imperative. This identification of distinct groups of users and service providers who have access to the GCash super app is part of the platform's configuration of its boundaries (Gawer, 2021).

On the consumer side, we began with scrutinizing download, registration, and entry protocols (Light et al., 2018). To download the app, a person must have a cellphone with at least an iOS14 or Android 5x operating system, and their own mobile number, which serves as their main account identifier. These initial requirements form barriers to entry for those with older phone models or those unable to afford the app's material requirements. Upon download, the registration process requires a user's full name, birthdate, e-mail address, home address, and sources of funds, which must match one's valid government ID. This step verifies a user's legitimacy in compliance with the guidelines of the Philippines’ central bank and regulations by the Anti-Money Laundering Council. It also filters out individuals not belonging to the app's target market: those under 18, who are relegated to a closed-off section of the app called GCash Jr., and those without a valid ID, which is needed to verify one's account.

After registration, users must undergo a verification process that determines whether GCash can function as a usable financial infrastructure. Unlike the relatively frictionless act of signing up, verification is lengthier and more demanding, requiring users to upload a photo and government-issued identification—documents that remain unevenly accessible in the Philippines, where an estimated 16 million individuals lack any proof of identity (Marskell et al., 2018). Verification thus operates both as a technical safeguard from risk and as a gatekeeping mechanism that stratifies users according to their capacity to meet documentary and biometric requirements. This stratification has concrete financial consequences. Unverified users are restricted to a significantly lower e-wallet limit (P10,000 compared to P100,000 for verified users) and are denied access to core transactional functions such as sending money, making online or QR-based in-store purchases, withdrawing funds, or accessing credit and investment services. Funds that are “cashed in” by unverified users are effectively locked into a narrow circuit of consumption such as bill payments or mobile load purchases, thereby restricting financial autonomy while still enabling platform-mediated value capture.

Embedding the regulatory logics of the Bangko Sentral ng Pilipinas directly into design (GCash, 2025), the super app further reinforces a hierarchy through interface cues and temporal penalties. Other users are warned when transferring money to unverified accounts, marking these users as risky or incomplete participants in the platform economy. Accounts that remain unverified for extended periods are suspended or deleted, and balances left in the system are gradually depleted through maintenance fees until they reach zero. Access to credit is also contingent on verification as only verified users are assigned a GScore, GCash's internal credit metric, which we discuss further in the next section. Thus, financial inclusion here is conditional: Users must first render themselves legible to the app through identity documents, biometric data, and transaction histories before being deemed creditworthy.

These layered barriers reveal a tension between GCash's public framing of “finance for all” (Globe, 2022b) and the operational realities of building a super app that satisfies regulatory, technical, and commercial imperatives. While Globe reports that 92% of GCash users come from low- and lower-middle-income groups and 78% of users reside outside Metro Manila (Maligro, 2025), the verification regime demonstrates how app-based inclusion parameters are graduated and uneven, offering partial access while disciplining users into compliance with both the state and platform's technical demands.

What transactions are

As a financial super app, GCash defines the possibilities for transactions to its 94 million users. As illustrated in our platform biography, GCash's collaborations with banks, trading firms, insurance providers, government agencies, and service companies make possible a robust bills payment platform (Balinbin, 2022). Partnerships with other organizations enable additional functionalities, such as job search, shipping, shopping, and games. Together, these linkages create an ecosystem dependent on the GCash platform and are visualized on the app's Home Page and Log In screens by the image of an open backpack, from which images of items like a piggy bank, a calculator, a book, bills, and vouchers come out. The visual representation reflects how GCash as a platform has internalized the functions of the web, both financial and nonfinancial, to become a portal of everyday digital life.

The app's main functions take up half of the screen on the app's Home Page, with a View All button that takes the user to a full list of functions categorized into seven clusters (see Figure 2).

Discursive construction and symbolic visualization of transactions

Presenting itself as a one-stop shop for both financial transactions and lifestyle services, GCash's labeling and categorization of its different functions discursively construct the nature of those transactions. One way the app does this is by naming certain digital transactions so that they are more recognizable. For example, the function GCash Padala references long-established means of sending remittance to distant relatives, with an icon that resembles Pera Padala (Western Union-like) kiosks.

The app also discursively constructs certain transactions to be more palatable, allowing them to elide negative cultural connotations. GCash offers three borrowing options—GGives (installment purchases), GLoan (cash loans deposited directly into the GCash wallet), and GCredit (a revolving credit line accepted by partner merchants)—yet all are subsumed under a single interface category: Borrow, locally translated as “pahiram” a term used for benign, everyday social transactions like borrowing a pencil or a piece of clothing. By foregrounding “Borrow” discursively as a unifying function, GCash reframes a range of distinct financial instruments with serious obligations as a single, commonsense act of short-term help rather than as differentiated forms of indebtedness. We discuss further consequences of the Borrow function in conditioning transactional logics in the later section.

The app also discursively made casino gaming more palatable by grouping it with other services under the umbrella category called “Enjoy.” Notably, due to public clamor, GCash was pressured to de-link all casino gaming from its e-wallet effective 16 August 2025 in compliance with the BSP Memorandum M-2025-029 (Bangko Sentral ng Pilipinas, 2025b). Nonetheless, when this was still active during our walkthrough, casino gaming appeared just as normal and enjoyable as other functions within the category, such as casual gaming, shopping, and buying food. It also calls its casino gaming function simply “Games,” which can be easily confused with the function “Play” for non-gambling games.

Organization, emphasis, and ordering of transactions

The app not only defines what transactions are, but it also highlights certain transactions for greater visibility. The first method for this has to do with how the app's different transaction functions are stacked on the Home Page. Of the 42 functions available on the app during our walkthrough (see Figure 2), 11 are shown on the Home Page—namely, Send, Load, Transfer, Bills, Borrow, GSave, GInsure, GInvest, GLife, A+ Rewards, and GForest. GCash shows users its expected and desired transactions in the way the Home Page lays out these 11 functions. The first two rows feature GCash's financial services in Send and Transfer, reflecting the historical importance of international and domestic remittances both to GCash's historical roots (as discussed in the earlier section) and to Philippine migration culture (Hasnain et al., 2015), as well as the rise of digital merchant and utility payments (Mesina-Romero et al., 2022) in Load and Bills.

The GCash “View All” page lists its different functions under seven categories. Note: screenshots were taken in August 2023.

The second and more conspicuous way the GCash app directs user attention is through function highlights. Each time users log in, the app presents a banner—“Something new for you!  ”—with a button to “Discover” (see Figure 3). In our walkthrough, this often centers on a recurring promotion of Borrow. In four of the first five logins we observed, including immediately after creating an account, the highlighted function was Borrow (i.e., the middle image in Figure 3 is translated as: “Tap Borrow to access loan options that fit your budget!”). This persistent prioritization reflects Mynt's dual ownership of both GCash and Fuse, its lending arm. What appears as a neutral interface design choice can be interpreted as a commercial strategy, embedding borrowing into the everyday app experience and steering users toward credit products that directly benefit the wider corporate structure.

”—with a button to “Discover” (see Figure 3). In our walkthrough, this often centers on a recurring promotion of Borrow. In four of the first five logins we observed, including immediately after creating an account, the highlighted function was Borrow (i.e., the middle image in Figure 3 is translated as: “Tap Borrow to access loan options that fit your budget!”). This persistent prioritization reflects Mynt's dual ownership of both GCash and Fuse, its lending arm. What appears as a neutral interface design choice can be interpreted as a commercial strategy, embedding borrowing into the everyday app experience and steering users toward credit products that directly benefit the wider corporate structure.

Upon log in, the “Discover” banner precedes a function highlight. Note: screenshots were taken in August 2023. In our walkthrough, we were presented with the Borrow highlight almost exclusively.

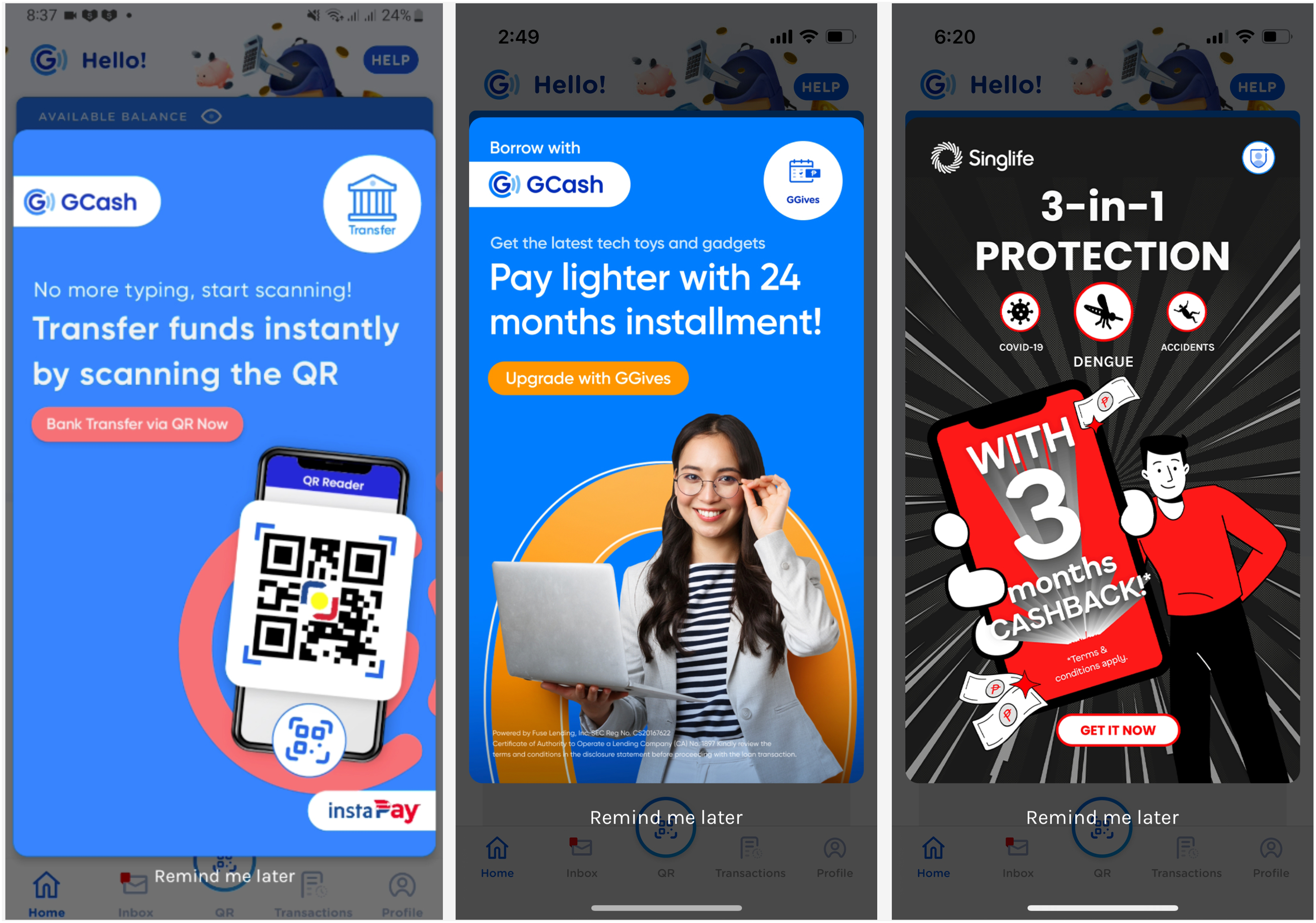

Third, the app directs the flow of activity through pop-ups, which appear when users log into the app (see Figure 4). This illustrates how GCash leverages its interface as a promotional surface to foreground specific services that align with corporate priorities. The login banners highlight not only core payment functions such as fund transfer via QR (left) but also cross-promoted financial products such as installment shopping payment via GGives (center), a lending service tied to Mynt's ownership of Fuse, and Singlife insurance (right), a partner provider. The app actively curates visibility in ways that normalize borrowing and insurance within everyday financial practices. This design underscores the platform's dual role: an infrastructure for user transactions and a strategic marketplace that directs attention toward profit-generating services within GCash's broader corporate ecosystem.

Pop-ups upon logging in. Note: Screenshots were taken in August 2023. Singapore-based Singtel owns 22.27% of Globe shares (Globe Telecom, 2023b).

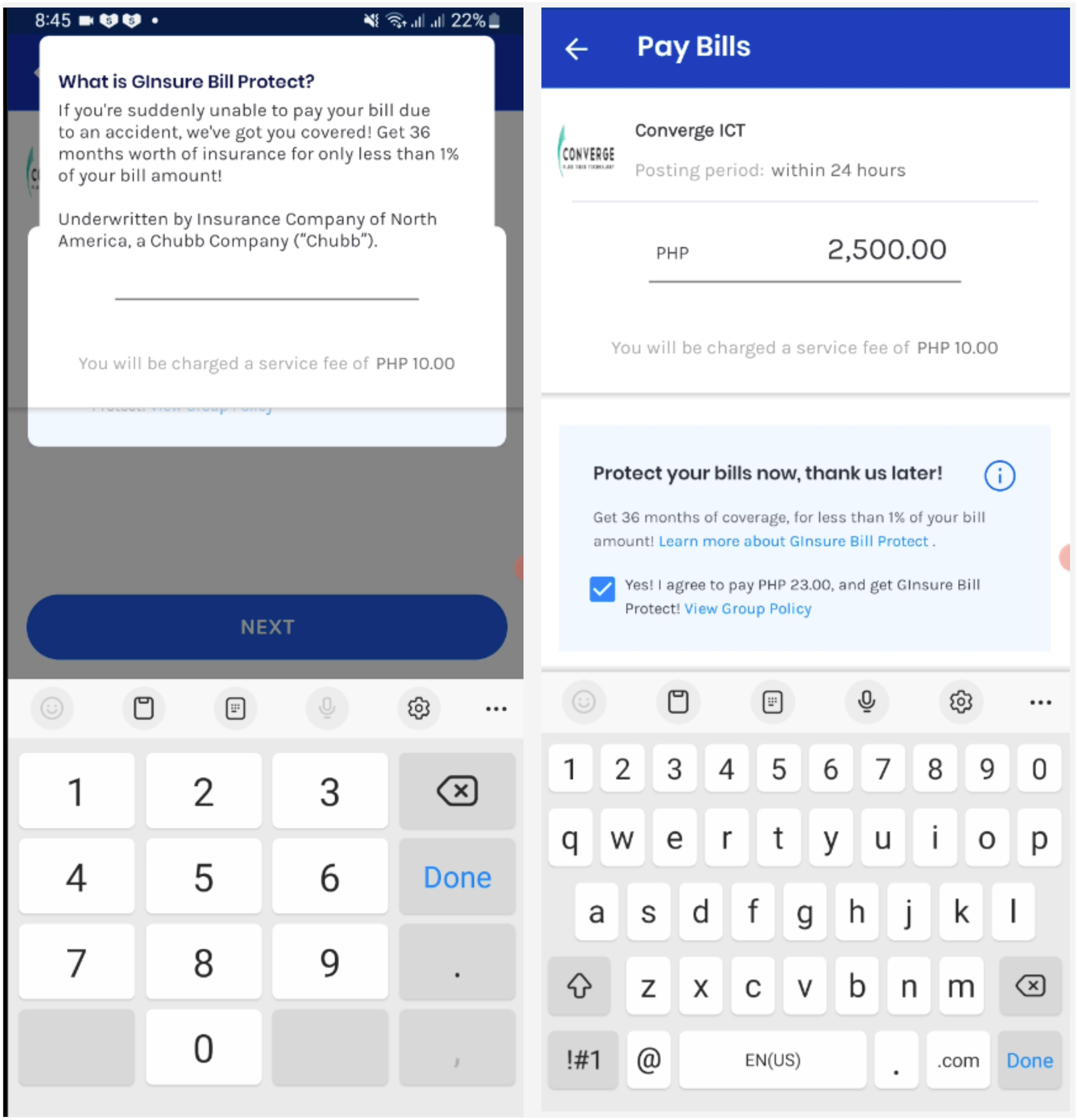

Finally, the app guides the flow of activity by triggering transaction chains, conducted by embedding a subsequent transaction after another or actively suggesting functions and features during and after certain transactions (see Figure 5). For instance, GCash encourages users to avail of its bill protection insurance product when transacting under the Bills function. When using GCash to pay for an internet bill, for example, we were served a pop-up screen about GInsure Bill Protect. For our P2500 (US$43) bill payment transaction, the checkbox next to “Yes! I agree to pay P23.00 (US$0.40) and get GInsureBill Protect!” was automatically ticked, which means that users have to consciously opt out of the service if they do not want to avail of it.

The Bill screen with a pop-up about GInsure Bill Protect, which is auto-ticked. Note: screenshots were taken in August 2023.

Aside from these methods for directing a user's flow of activity, GCash engages mechanisms to encourage continuous use, an effect that app scholars have called “platform enclosure” (Athique and Kumar, 2022; Pitre, 2022). The first is the app's GScore system, a proprietary credit rating system based on in-app transaction behavior. Cashing in regularly, paying for bills or transactions, and using GInvest, GSave, and GInsure functions can increase one's GScore. Failing to pay on time on Borrow transactions (GLoan, GCredit, and GGives) will decrease one's GScore. Having a high GScore can increase a user's credit limit and lower their interest rates, should they choose to use the Borrow function. The GScore also affects credit outside of the app. In the absence of a universal credit scoring system in the Philippines, the GScore system provides users with no previous banking history or formal credit record the opportunity to build credit, as GCash's lending arm Fuse reports to the Credit Information Corporation of the Philippines. Aligning with GCash's “finance for all” vision, the GScore system provides access to credit through both its internal score and an external credit record, which can be powerful motivators for regular GCash app use. The second mechanism is the in-app green initiative called GForest, a function that allows users to collect virtual trees equivalent to real-life trees planted by GCash. Buying load, paying bills, cashing in online, and sending money on GCash allow users to earn Green Energy Points, which are used to plant and grow virtual trees.

Configuring the conditions of transacting

Aside from defining who can transact and what transactions are, the GCash super app configures the conditions of transacting by making its services available to a wide range of users, including the “sachet economy” (Asian Banking and Finance, 2022; Soriano, 2026), which is consistent with its origins of catering to the “unbanked” and low-income market. Referring to the marketing and sale of consumer products such as soaps and detergents in small, single-use quantities to appeal to low-income consumers, GCash has lowered or removed minimum requirements for financial transactions like savings, investing, and insurance, attending to its historical trajectory of reaching lower-income classes. Thus, to transact as part of the GCash platform, service providers are compelled to create formats of financial goods and services that cater to the app's target user base (Steinberg, 2020) and at the same time make them “platform-ready” (Helmond, 2015). For instance, the Bank of the Philippine Islands (BPI)—a bank also owned by Ayala—appears as an option in GCash's GSave function and offers an app-exclusive #MySaveUp account. This type of account has a minimum deposit of P1 and a maintaining balance of P0—features that are markedly different from its more traditional savings account types. Its GLoad function offers a wide range of promotions that allow topping up mobile phone credit in small increments. Under the app's Grow category, the savings function GSave does not require a minimum deposit, unlike most traditional bank accounts, while its investing function GInvest allows users to begin investing in local stocks for as low as P50 (US$0.86). The function GInsure provides insurance products for as low as P10 (US$0.18). Depending on one's GScore, a user can borrow anywhere from P1,000 to P125,000 (US$17-2161) under the function GLoan, payable in 5–24 months, at an interest rate of 1.59%–6.99% per month. In this way, the super app provides a more accessible alternative to traditional banking institutions and promotes digital payments for businesses within its ecosystem (Mesina-Romero et al., 2022). As we discussed in the earlier section, however, all these are impeded by verification mechanisms that condition the entry and usage by the lowest-income users who, due to their financial positions, encounter difficulty in securing the identification requirements needed for verified GCash accounts. To date, around 10% of GCash users have a GSave savings account while less than 5% (3.9 million) have secured loans from GLoan (Globe Telecom, 2024a).

GCash also configures users’ understanding and experience of transactions through its strategic use of language. For example, where one would traditionally “deposit” money into a bank account, GCash users instead “Cash In.” Similarly, what is typically a “bank transfer” becomes “Send,” framing peer-to-peer exchange less as a formal financial transaction and more as an everyday act, akin to sending a message or remittance. This linguistic shift not only distances users from the institutional weight of banking but also aligns with existing micro-exchange cultures in the Philippines, such as sending mobile phone load or small amounts of cash (Athique and Lorenzana, 2025).

Further, GCash mobilizes language to foreground its Borrow function which encompasses GCredit, GLoan, and GGives. More accessible and less institutionally loaded than “credit” or “loan” often associated with banking, “Borrow” carries a notably softer moral valence than the Filipino term utang (debt), the latter being associated with obligation, shame, or social indebtedness. GCash's borrow functions are therefore strategically cast as “abot-kamay”—a “helping hand” that is within reach of one's phone (Athique and Lorenzana, 2025) embedding credit within everyday practices of financial coping. This framing aligns borrowing with immediacy and necessity rather than long-term financial risk, positioning platform-mediated debt as a pragmatic solution for making ends meet. In doing so, GCash's interface language configures transactional conditions by normalizing credit use while obscuring the varying terms, costs, and obligations attached to different borrowing products, folding them into a seemingly benign and accessible feature of the super app. Notably, the app's promotion of the Borrow function, which encourages users to take credit from partner companies, is in line with GCash's outlook for 2023, which explicitly includes increased market penetration of its lending products (Globe Telecom, 2023b). The function is also promoted outside the super app and through SMS. In our walkthrough, we found that GCash sends SMS messages to the GCash user promoting the GLoan, GGives, and GCredit options under Borrow several times a week. Figure 6 above shows some sample messaging sent to our GCash-registered phone number in the span of 1 week:

SMS messages sent by GCash to the linked mobile number to promote its Borrow function.

In a country where most borrowers get loans from informal sources like friends, family, and informal lenders (Bangko Sentral ng Pilipinas, 2022a), fintech companies like GCash are moving to provide accessible formal credit solutions to more people (FinTech News, 2023). According to Globe's third quarterly report for 2023, GCash disbursed a total of P103 billion to 3.4 million unique borrowers, the majority of whom belong to lower-income classes and the 21–35 year age bracket (Globe Telecom, 2023b) and two-thirds of whom are women (Globe Telecom, 2024b). Further, the unique borrowers of GCash's loan products doubled year-on-year (Maligro, 2025). While the Globe report described these numbers as “leading the way into financial inclusion” (Globe Telecom, 2023b: 14), the aggressive promotion of easy, accessible loans both within and outside the GCash super app normalizes loans and debt while also making it easier and more private, giving users the ability to borrow money without reaching out to friends, family, and informal lenders. This change in the conditions of transacting is crucial because Filipinos tend to have a negative perception of loans, with over half hesitant about credit products and not wanting to be indebted (TransUnion, 2023). Filipinos have also been described as the most stressed about debt in the Asia Pacific region (Bankbase, 2021), with 67% overwhelmed by debt and 60% struggling to pay bills because of debt servicing, which leads to even more debt. But by presenting loans as a convenient “abot-kamay” (helping hand) for expenses like utility bills, travel, and shopping in punchy advertisements, GCash is normalizing debt and placing itself as a go-to provider of safe credit. This dynamic is amplified by Mynt's ownership of both GCash and Fuse, its micro- and business-lending arm.

It is worth noting here that financial literacy is low in the Philippines (Klapper et al., 2015), and Globe's efforts for financial literacy—particularly in terms of debt—could receive equal, if not more aggressive treatment as its Borrow promotions. The loan application process is also remarkably smooth, lacking the “friction” that slows down GCash app users in the interest of improving security (Distler et al., 2020) when sending money through the Send and Transfer functions. 2 Although this ease of borrowing allows Filipino GCash users to access credit quickly and efficiently, it does pose a risk of app users not fully understanding the terms of the loan or credit they are getting.

Discussion and conclusion

Using the case of GCash, this article examined how fintech platforms embed themselves into everyday transactional cultures of exchange and sociality where poor rural infrastructure, weak institutions, and barriers to financial account ownership have historically limited financial inclusion. Drawing from a platform biography of GCash's development alongside a walkthrough of its super app form, we traced the platform's evolution from its remittance-based foundations to its current constellation of services as a megacorp. We conceptualized this trajectory as one of transactional restructuring—where the app defines who can transact, what transactions mean, and how transaction chains are organized, backed up by a wide ecosystem of strategic partnerships wielded to support the platform's growth and functioning. This restructuring not only shapes access to financial services but also reconfigures the very conditions of Filipino transactional life.

GCash exemplifies the dynamics of megacorps (Athique & Kumar, 2022). Like its global counterparts, it has expanded far beyond a single-purpose fintech through partnerships, acquisitions, and internal ventures that generate new streams of data. We see some common tendencies in terms of how GCash collaborates with the government, in parallel with the experience of Reliance in India (Athique and Kumar, 2022) and Alibaba and Tencent in China (Zhang and Chen, 2022). Aside from the government, collaborations with retail chains, pawnshops, insurance providers, and remittance companies extend its reach across multiple domains, while its integration with Fuse (lending), GLife (e-commerce and gaming), and other branded services illustrates how it develops users’ subjectivities as multifaceted consumers continually nudged by its super app design. While this expansion is often celebrated as advancing financial inclusion—particularly through government partnerships and sachetized services that reach lower-income users—it simultaneously creates new forms of differential access and reconfigures Filipino users as a broad field of borrowers, shoppers, gamers, jobseekers, and even “environmental advocates” within its super app ecosystem. In this way, GCash consolidates itself as both cultural infrastructure and economic sphere, embedding deeply in Filipino everyday life while reorganizing financial and commercial practices around an extensible, conglomerate model of platform capitalism.

The rise of GCash as a super app consolidates this logic. Spanning payments, credit, insurance, e-commerce, and even state-welfare distribution, it extends discussions around the cultural economic influence of Asian super apps (Chen et al., 2018; Goggin, 2021; Steinberg, 2020; Zhang and Chen, 2022) where platforms position themselves as indispensable infrastructures of daily life. In the Philippines, such expansions are framed as a public good: GCash is lauded as a champion of financial inclusion and welfare distribution, and government partnerships are further encouraged by the app's having reached a critical mass of users. Yet what is distinctive is not simply its range of services but its integration of user attention, behavior, and data into a centralized, privately owned system. Here, asset management refers not only to the ownership of diverse businesses but to the orchestration of entire markets around flows of data and the capture of consumer habits.

As scholars caution (Athique and Kumar, 2022; Srnicek, 2024; Steinberg et al., 2025), such platforms demand critical reflection on their power and macroeconomic implications, noting that super apps are often rewarded with escalating valuations and even state endorsement. This produces a tension: GCash is positioned as a tool for social inclusion and national development while simultaneously consolidating private power over critical financial and social infrastructures. Why such entities remain insulated from the financial discipline that challenged earlier conglomerates (Soriano, 2026; Srnicek, 2024) raises critical questions about new dependencies at both the national and even the household level. In the Philippine case, GCash even mediates public functions, blurring distinctions between public utility and private enterprise. Its cultural ubiquity and institutional entrenchment produce new forms of financial inclusion but also deepen dependencies on a single corporate platform.

Through partnerships with small and large businesses, collaborations with government, and the strategic upgrading of its technological infrastructure, GCash has positioned itself to scale and dominate a wide range of everyday transactions that underpin the Philippine economy. This includes not only routine payments but also practices of borrowing and short-term credit that formalize and platformize long-standing monetary practices of reciprocity and redistribution. The expansion of these services underscores the consequences of megacorps taking over the provision of everyday financial needs, including borrowing to make ends meet, which have historically relied on social relations of trust, obligation, and mutual aid (Athique and Lorenzana, 2025). From informal lenders or loan sharks, the platformization of multiple pathways to credit reconfigures these traditional relations into digital transactions governed by data extraction, algorithmic assessment, and fee-based access, reshaping how financial precarity is managed and monetized.

The role of global capital—most notably the technological and financial backing of Chinese giant Alibaba—has been central to GCash's trajectory, embedding GCash within wider circuits of investment and platform finance while boosting its technical architecture. These dynamics not only sustain its current dominance but also point to future transformations, as signaled by its announced plans for public listing. Crucially, GCash's ownership by the Filipino-owned Ayala Corporation underscores how the Philippine digital economy remains intertwined with long-standing elite capital. Emerging from a landed family conglomerate that has historically dominated real estate, banking, telecommunications, and utilities (Pinches, 1992), Ayala's control of GCash extends this dominance into the infrastructures of everyday finance. GCash also illustrates how colonial-era elites retool their power by embedding themselves in both physical and digital infrastructures of daily life, of course, in partnership with global capital (Maurer, 2015).

Distinguishing between GCash the super app and GCash the platform allows us to examine two separate sites of formatting. The GCash super app formats transactions, conditions for transacting, and transactional objects on the side of the user through the deliberate design choices that comprise screens, functions, and representations, as uncovered by our walkthrough. The super app is thus a site of bilateral communication between GCash and the user, who may resist these messages to a certain degree. On the other hand, the GCash platform—with its interlocking technologies, infrastructures, business relationships, and capital interests—functions behind the scenes, governed by both technical and business logics and participated in by internal and external stakeholders. Within this multilateral site of formatting, the very definition of a transaction—what it entails, who is allowed to participate, and under what conditions—is already shaped by a wide array of actors long before a user opens the app. Together, these two sites of formatting can provide a lens for understanding how power is organized and exerted in the context of indispensable super apps.

While our focus here is on GCash, we hope the analysis extends and contributes to wider debates on how fintech platforms embed themselves within local transactional cultures and how they are also shaped by global and local infrastructures (Athique and Kumar, 2022; Chopra et al., 2013; Jain and Gabor, 2020). In doing so, we see how platform capitalism advances corporate ambitions for growth and enclosure under the language of financial inclusion, echoing findings elsewhere, such as from Africa (Langley and Rodima-Taylor, 2022) and India (Athique and Kumar, 2022; Jain and Gabor, 2020). With super apps like GCash expanding in scope and influence, our study underscores the need to interrogate the assumptions and logics embedded in financial platforms, the actors who shape them, and the power relations they generate. In the Philippines, where the government pursues a “test and learn” approach that leaves technological innovation largely in the hands of the market (Bangko Sentral ng Pilipinas, 2022b; Mendoza and Macadato, 2022), these findings force us to confront urgent questions about who governs financial super apps, how megacorps consolidate their dominance, and what this concentration of power means for the country's digital economy.

Footnotes

Ethical approval

This manuscript received the Ethics Board approval of the authors’ university (Project Number 2024-002C).

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project is funded by the Australian Research Council (Digital Transactions in Asia).

Declaration of conflicting interests

One of the authors is a member of the editorial collective of the journal. To ensure integrity of the review process, this author was not involved in all stages of editorial decision-making and peer-review process.