Abstract

This paper traces Kakao’s corporate strategies—with a focus on conglomeration and valuation—in order to trace how the company’s trajectory led to its current status as a near-monopoly. Starting as a chat app which now has 43 million active users in South Korea, Kakao became a conglomerate by expanding its operations across different business sectors such as transportation, entertainment, fintech, etc. Kakao’s diversification of businesses and conglomeration should be understood in relation to its corporate strategies and forms, not as the natural outcome of technological innovation. Aspiring to become an entertainment conglomerate, not just a platform company, Kakao has expanded the scope of its business by acquiring start-ups and competitors, spinning off in-house startups as subsidiaries, and making strategic mergers between subsidiaries. Kakao has also placed greater focus on boosting valuation rather than profitability, a crucial strategy for leveraging high valuations to consolidate its market dominance. Tracing Kakao’s affinities to chaebol, I further propose a framework for thinking about the relationship between the state, tech, and finance. Collusion between the state and tech has occurred through deregulation, which has allowed tech companies to become financial capital.

Introduction

Kakao Corp., one of the two largest platform companies in South Korea, started as the chat app KakaoTalk, a “must use” app that almost every smartphone user has on their phone in South Korea. The company introduced the chat app in 2010, immediately following the release of the iPhone in the Korean market. KakaoTalk was quickly and widely adopted by the nation, with the number of users reaching 20 million within a year, and then 42 million by March 2012 (Park and Kim, 2016: 62). Kakao later leveraged this large user base for its instant messaging app to expand into—and “platformize”—shopping, games, advertising, entertainment, payments, mobility, and intellectual property. As The Washington Post describes it, Kakao is now “Facebook messenger, WhatsApp, Uber, Google Maps and Venmo wrapped into one” (Pietsch, 2022).

Offering various apps and services—including KakaoTalk (now having 43 million active users in a country of 51.6 million people), Kakao T (a ride-hailing app connecting taxi drivers and passengers with 30 million users as of 2021), Kakao Pay, and KakaoBank among others—Kakao is the 15th largest business group in South Korea as of May 2022, with more than a 100 firms under its wing, including KakaoBank Corp. and Kakao Games Corp. (Kang, 2021; Kim, 2022a). When its data center was set on fire in October 2022, it was not just chatrooms that were disrupted; the entire nation experienced disruptions in their daily lives and businesses. A local newspaper reported that Kakao’s service failure created problems for “mom-and-pop store owners and small online shopping mall operators, who suffered errors in customer management, online booking and payments, while taxi drivers failed to receive calls from Kakao T users” (Kim, 2022a). After the incident, President Yoon said that the services provided by Kakao are considered part of the country’s “basic infrastructure.” As this incident demonstrates, the everyday life of Koreans today is organized and mediated by Kakao.

Kakao’s significance lies not only in that it was the first mobile chat app to launch in East Asia (Jin and Yoon, 2016) but also in that it is a primary example of super apps, or “do-everything apps” (Steinberg, 2020; Steinberg et al., 2022). A super app refers to “a particular model of an app that assumes most functions of the smartphone can be done within either a single app or a suite of apps” (Steinberg et al., 2022: 1409). Korean scholars also claim that Koreans’ use of most online services (e.g., search, shopping, social media, watching videos) within one platform/portal rather than using multiple platforms is a very local-specific phenomenon (Won and Park, 2021). As van der Vlist et al. (2024) point out, super-appification entails not just platformization but conglomeration as well. I examine Kakao’s corporate strategies—with a focus on conglomeration and valuation—in order to trace how the company’s trajectory led to its current status of being a near-monopoly—or, more accurately, a duopoly along with the other tech giant, Naver. As a recent special issue of Media, Culture & Society on super apps points out, “the emergence of super apps is predicated upon the ability of corporate giants to deploy their monopoly power in national and regional markets” (Steinberg et al., 2022: 1406). I therefore draw on the literature that emphasizes the need to understand platformization not just through technicality and materiality but also through industry logics and corporate forms, strategies, and rhetorics (Athique and Kumar, 2022; Jia et al., 2022; Kim, 2023; Lee, 2019; Plantin and Punathambekar, 2019; Steinberg et al., 2022), with a focus on historical and regional specificities (Jin, 2023a; Steinberg, 2019, 2020).

This article also adds to the literature that discusses the prominence of monopoly and oligarchy in platform capitalism (Athique and Kumar, 2022; Kenney and Zysman, 2016; Langley and Leyshon, 2017; Rahman and Thelen, 2019; West, 2022). Along with India’s Jio, Japan’s LINE, and Southeast Asia’s Grab, the prominence of Kakao instantiates the Asian origins of the super app. Building on previous research on South Korea’s platformization, which has been mostly studied in relation to cultural production (Cho, 2021; Jin, 2023b; Kim and Yu, 2019; Park et al., 2023), I contribute to the body of work that draws attention to tech giants outside of the US (Athique and Parthasarathi, 2020; De Kloet et al., 2019; Steinberg, 2019; Yeşilbağ, 2022; Zhang, 2020) to “decenter ‘the West’ in discussions of platformization” (Steinberg et al., 2024: 2). In order to analyze Kakao’s corporate strategies, I primarily relied on Kakao’s annual reports, financial statements, press releases, executive interviews, other public-facing documents, as well as media articles, industry reports, and scholarly literature on Kakao and other platforms.

Conglomeration of Kakao through M&As

In studying the corporate trajectory of Tencent—which operates China’s super app WeChat—Jia et al. (2022) identify conglomeration, financialization, platformization, and infrastructuralization as its four interrelated institutional strategies. Conglomeration here is defined as “corporations seeking to benefit from economies of scope and scale through integrated organizational structures and diversified, yet concentrated corporate ownership” (1441). Similarly, Kakao became a conglomerate by expanding its operations across different business sectors such as entertainment, transportation, healthcare, fintech, among others. This expansion is seen as more diversified than the trajectory of Tencent (van der Vlist et al., 2024). Many believe that the diversification of businesses and the conglomeration of platform companies are natural outcomes of technological innovation. Instead, I contend that Kakao’s conglomeration should be understood in relation to its corporate strategies and forms. Kakao expanded the scope of its business by acquiring start-ups and competitors, spinning off in-house startups as subsidiaries, and making strategic mergers between subsidiaries.

As a company known for a chat app, its first breakthrough for conglomeration was its 2014 merger with Daum Communications—which was operating South Korea’s second-largest portal site called Daum—to form the $7.4 billion (market cap) Daum Kakao (Mac, 2015). Daum began with an email service in 1997, and it grew into a comprehensive portal site with an array of services including blogs, a search engine, news curation, e-commerce, etc. While the form of the merger was Daum’s takeover of Kakao, this was Kakao’s strategy for going public on KOSDAQ while bypassing the IPO process (a “backdoor listing”). The merger provided Daum Kakao (whose name was quickly changed to Kakao) with a larger balance sheet, enabling it to move into new business lines (Song, 2015). The merger is also seen as opening a new chapter in South Korea’s platformization, marked by the duopoly of Kakao and Naver (Jin, 2023a).

After the merger, Kakao tried to identify key business sectors by taking up O2O (Online to Offline) as a core strategy. Exemplified by transportation, food delivery, real estate agencies, and accommodations—and inspired by Uber and Airbnb—“O2O” was an important buzzword in South Korea’s tech scene in the first half of the 2010s (see Ryu, 2016). In 2015, Kakao’s new CEO declared that the corporation was “looking at every O2O service you could possibly imagine” (Lee, 2015), and Kakao was indeed trying to expand its service portfolios into hairdresser bookings, house cleaning, and flower deliveries. However, many of these were neither profitable nor attractive to investors. Such O2O strategies were also met with the criticism that they would eventually wipe out small businesses. Kakao, therefore, began to shift its strategy in 2016–2017 toward more platformization with a concentration on its strengths, including mobility, content, and fintech (see Chae, 2017). 1

Acquiring start-ups and competitors for the purpose of spinning off a new subsidiary has been a crucial strategy for Kakao’s conglomeration. Take Kakao Mobility Corp. as an example: Kakao acquired several firms in order to spin off Kakao Mobility as a child company. Soon after its merger with Daum, Kakao launched a taxi-calling app called Kakao Taxi in March 2015. Two years later, it was renamed as “Kakao T” which is no longer just a taxi-hailing app. Kakao T is now a comprehensive transportation service app including taxi-hailing, searching and paying for nearby parking, replacement driver (a designated driver service) booking, and navigation. To expand Kakao Taxi to Kakao T, Kakao acquired several start-ups and competitors. In 2016, it purchased a start-up company LOC&ALL that had developed a mobile navigation system with more than 2.4 million monthly active users (Choi, 2016). As the company was acquired by Kakao, its navigation app Kimgisa was renamed Kakao Navi. Kakao also acquired a parking platform operator Parking Square the same year in order to start a parking service. It was through this series of M&As that Kakao expanded the scope of services available on Kakao T. The number of Kakao T’s users reached more than 1.7 million by December 2017 (Kwon, 2018), and Kakao spun off Kakao Mobility Corp. as a new subsidiary in 2017.

Kakao Mobility has continued to build its value chain by acquiring competitors such as My Valet (a parking and valet management system app developer) in 2020 and GSPark24 in 2021 (Kang et al., 2020; Park, 2021). As a result, Kakao T has more than 28 million users in addition to 250,000 taxi drivers and 150,000 replacement drivers, which provides Kakao with massive consumer data regarding mobility and transactions (The Herald Economy, 2021). Crucially, Kakao does not just operate as an intermediary or mediator (Jin, 2017a) in the transportation sector; instead, Kakao Mobility itself became a taxi company by acquiring nine taxi companies (Kim, 2022b).

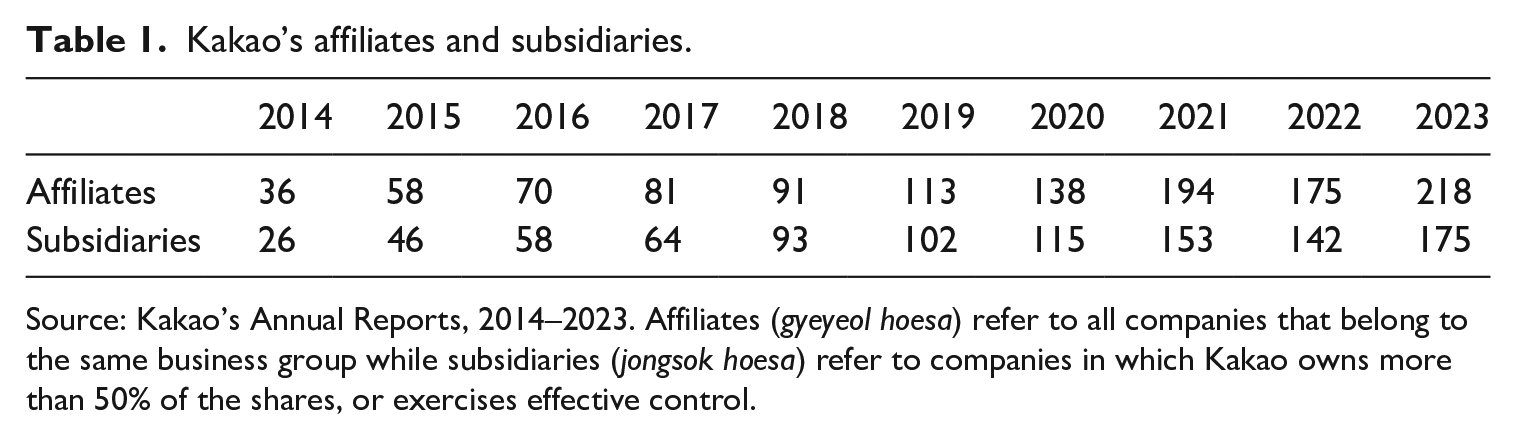

As the result of mergers and acquisitions, Kakao has 175 subsidiaries (including domestic and overseas) as of the end of 2023, hitting the second highest number among big businesses in South Korea—it is second only to the SK Group—and is the 15th largest in terms of the combined market cap of itself and its subsidiaries (Byun and Lim, 2023; See Table 1). This level of rapid diversification has been unmatched. The other tech giant, Naver, for instance, had only 54 affiliates as of May 2022 (Ban and Lee, 2022), much smaller than Kakao’s 175.

Kakao’s affiliates and subsidiaries.

Source: Kakao’s Annual Reports, 2014–2023. Affiliates (gyeyeol hoesa) refer to all companies that belong to the same business group while subsidiaries (jongsok hoesa) refer to companies in which Kakao owns more than 50% of the shares, or exercises effective control.

From a tech company to a media conglomerate

Kakao recently made global news headlines by becoming a major shareholder for SM Entertainment, one of the most iconic K-pop agencies. Kakao acquired its majority stake after a dramatic battle with BTS’s agency HYBE. The acquisition battle between Kakao and HYBE was quite sensational, and lots of Koreans would joke that it was more fun to watch than K-dramas. 2 It was surprising to many ordinary people because Kakao was still perceived primarily as a platform company that had little to do with K-pop. However, Kakao has been expanding, quite aggressively, into the media and entertainment industry, furthering its diversification.

Kakao Entertainment Corp. represents Kakao’s aspiration to become the next Disney or Marvel. It also represents how Kakao has strategically merged its subsidiaries, not just spun off new subsidiaries. As an entertainment, media, and publishing company, Kakao Entertainment was established in 2021 through a merger between Kakao Page Corp. and Kakao M Corp. Having operated two content platforms (KakaoPage and Daum Webtoon), Kakao Page Corp. owned more than 8500 IPs in webtoons and web novels—considered the largest pool of original content in South Korea—along with an extensive distribution network (Noh, 2021). Popular TV series such as Itaewon Class (2020, JTBC) and The Uncanny Counter (2020–2021, OCN)—both streamed on Netflix in the US—were adapted from webtoons originally published on KakaoPage/Daum Webtoon. Kakao M operated as a music label, talent agency, and production companies in TV, film, and theater. The merger between these two subsidiaries allowed the new company, Kakao Entertainment Corp., to vertically and horizontally integrate production and distribution of media content. In other words, Kakao expected the merger to “complete a value chain in the entertainment business that includes the intellectual property of story lines, artist management, production, and platforms on which the created content can be played” (Jin, 2023b: 65).

Kakao’s English press release described the merger as “the first-ever large-scale merger between subsidiaries of Kakao Corp.,” painting the newly formed Kakao Entertainment as “one of the largest Korean entertainment companies, which will generate over KRW 1 trillion in annual revenues” (Kakao Entertainment, 2021). It goes on to say:

Through the merger, Kakao Entertainment will have an unparalleled business portfolio and value chain including 50 subsidiaries and affiliates across major verticals of the entertainment industry. (. . .) Upon this foundation, Kakao Entertainment will expand its investment and strategic partnerships with industry leaders to grow into a global entertainment player. The company will not only diversify its business but also focus on producing blockbuster media franchises that can captivate global audiences and seek various ways to create synergies among combined assets. (Kakao Entertainment, 2021)

Two pivotal moments in the earlier history of Kakao’s media conglomeration include its merger with Daum (2014) and the acquisition of Loen Entertainment (2016). In the mid 2010s, Kakao had to find new revenue streams and improve profitability, as its chat app was already reaching market saturation and its game business was struggling. Through the merger with Daum, Kakao not only expanded its mobile-centered business structure to the web, but it also made it possible for Kakao to connect its platform business to its content business. At that time, the lack of “content” was seen as Kakao’s major weakness since it couldn’t “lock in” KakaoTalk users without content (Kim, 2014). Through the merger, Kakao enhanced market competitivity by gaining the intellectual properties and content that Daum had accumulated (Kang, 2014; Lee and Park, 2018). In particular, Daum Webtoon 3 proved to be crucial to Kakao’s incursion into the entertainment industry in the following decade.

Kakao’s aspiration to become a global media conglomerate is seen as the result of a growing competition with the global platform industry. In the late 2010s Kakao began to see its advertising revenues decrease, global platforms gain market shares, and the domestic market become saturated (Park et al., 2023). Media scholars posit that the strategy to use media contents to attract users to platforms might appear unusual in the US, because “it was generally understood that platform companies did not create content but merely mediated transactions between complementors, advertisers, and end-users and monetized the user data collected” (Park et al., 2023: 2426). Such a strategy, however, is commonly found in East Asia where platform operating companies are media conglomerates as well as tech giants (Steinberg et al., 2022).

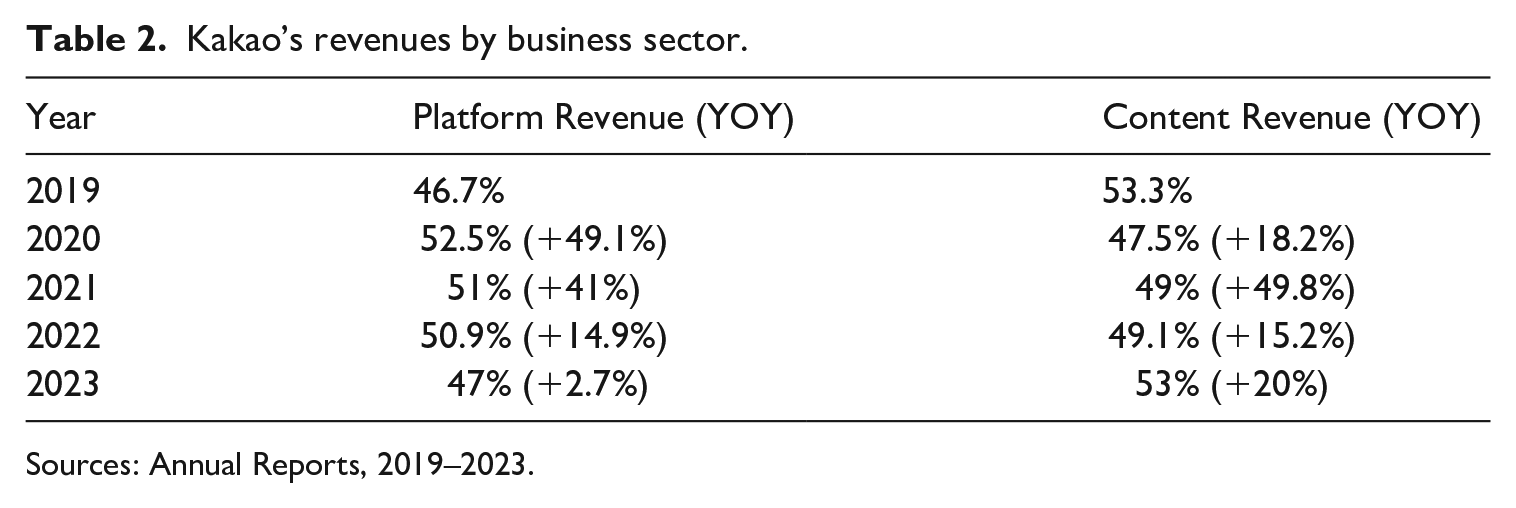

Two years after merging with Daum, Kakao acquired Loen Entertainment, which had been operating South Korea’s largest music streaming service, Melon. Following this acquisition, the sales of content skyrocketed by 157% in 2016, improving cash flow and operating profits (Hong, 2021: 79). Kakao’s ongoing concentration on entertainment is reflected in its revenues and the makeup of its affiliates and subsidiaries. According to Kakao (2022), 56.4% of Kakao Corp’s 134 domestic affiliates are content companies as of August 2022. 4 In addition, Kakao’s revenues from its content businesses (e.g. music, games, “stories” such as webtoons and web novels, “media” such as talent agencies and media production companies) surpassed revenues from its platform businesses (e.g. commerce, advertising from apps, and other revenues from Kakao Mobility, Kakao Pay, etc.) in 2023—for the first time since 2019. As Table 2 shows, the yearly increases in revenues from content businesses have been greater than the yearly increases in revenues from platform businesses since 2021. Park et al. (2023) assert that “unlike U.S.-based Alphabet and Meta, whose advertising revenues in 2021 accounted for about 81% and 97% of their total revenues, respectively, Kakao and NAVER are no longer classified as advertising platforms because the ratio of advertising revenues to their total sales has stagnated or decreased” (2429; Figure 1).

Kakao’s revenues by business sector.

Sources: Annual Reports, 2019–2023.

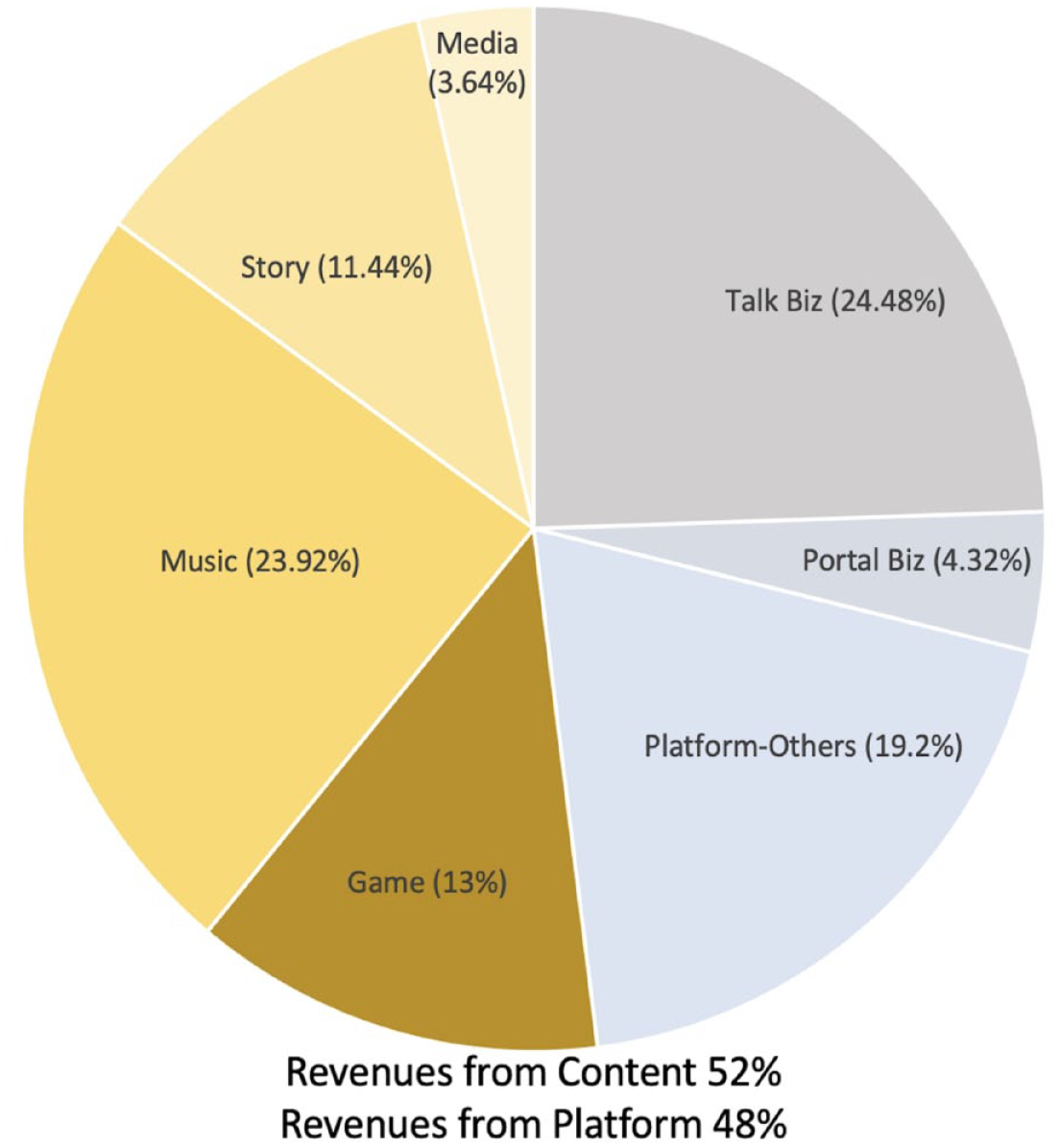

Kakao’s revenues by specific business sector, 2023 Q2.

Overvaluation

If conglomeration is a crucial strategy for centralizing control over consumer data and cultural production, financialization has allowed conglomerates to increase market share. The combination of conglomeration and financialization is a key institutional strategy that allows platform companies to create and control markets and exert infrastructural power (Jia et al., 2022; van der Vlist et al., 2024). While Jia et al. (2022) perceive financialization primarily as a means of debt-financed mergers and acquisitions, I see financialization more broadly to emphasize how the raison d'être of corporations has drastically changed under financialization and the consequent rise of shareholder-oriented governance. As Michel Feher (2009: 27) aptly puts it, the major preoccupation of financialized corporations became “capital growth or appreciation rather than income, stock value rather than commercial profit.” Likewise, Kakao has invested more in boosting valuation and market capitalization—rather than increasing operating profits—through M&As, spinoff IPOs, and buying back its own shares.

First of all, Kakao’s merger with Daum was partly due to its concern over valuation, in addition to the purpose of rapid capital mobilization. Industry watchers found the merger between Daum and Kakao unexpected, because Kakao initially planned to go public in 2015 (Kang, 2014). However, Kakao’s profit streams were still seen as weak, which put its management on edge about obtaining their desired valuation if they applied for a new IPO (Lee and Park, 2018). It therefore overturned its original plan and chose to merge with Daum so that it could get a backdoor listing on KOSDAQ—South Korea’s tech-laden secondary bourse. Moreover, for Kakao, mobilizing capital in order to develop new business models and expand into the global market was a time-sensitive issue. Given that the process for a new IPO takes approximately one year, the backdoor listing helped Kakao boost its market cap and mobilize capital immediately (Lee and Park, 2018). In May 2017—less than two years after the backdoor listing—Kakao applied for a listing on KOSPI, South Korea’s benchmark bourse, anticipating that its KOSPI listing would boost its share price and bring more overseas institutional investors to Kakao. At this point, Kakao was the second-largest listed firm on KOSDAQ (Park, 2017).

In addition, Kakao began to rush out spinoff IPOs as a means of raising capital, dismantling its own promise to “seek growth through innovation” (Choi, 2022). It is not uncommon for platform companies to list subsidiaries in order to boost market capitalization (Jia et al., 2022), but Kakao’s approach was so extreme that it angered its own shareholders. As of October 2023, Kakao has five subsidiaries (including itself) listed on KOSPI or KOSDAQ; Kakao Games (September 2020), KakaoBank (August 2021), and Kakao Pay (November 2021) all went public in the span of 1 year. Since this series of spinoff listings, Kakao has continued to try listing a number of other subsidiaries, including Kakao Mobility and Kakao Entertainment. Crucially, Kakao used the funds it raised through its IPOs to acquire more competitors and IPs. For instance, the Kakao Games IPO brought in about 384 billion Korean won (approx. $323.7 million) for the company (Huang, 2020), and Kakao Games said they would use 85% of these funds for M&As and the acquisition of new IPs (Park, 2021a). Kakao Pay, which raised approximately $1.3 billion through its IPO, announced that a majority of the IPO proceeds would be used for mergers and acquisitions (Lee and Lee, 2021). The series of IPOs boosted Kakao Group’s market cap; at one point it ascended to being the fifth highest business group in South Korea, following behind the market caps of listed companies in the Samsung, SK, LG, and Hyundai groups (Yoon, 2021a).

Spinoff listings have been one of Kakao’s most contested corporate strategies. The spinoff IPO is contested for several reasons. Most crucially, it is problematic because a spun-off company is not required to compensate the parent company’s shareholders when it holds an initial public offering (Choi, 2022). The value of the parent company’s stock is likely to be weakened when its child company goes public; although from the parent company’s perspective, this allows it to raise capital without sacrificing its ownership stake. Therefore, when Kakao floated three subsidiaries in 2020–2021, it was able to maintain its control over them at the expense of individual shareholders (Choi, 2022). Spinoff IPOs seem to happen rarely in the United States. For example, Alphabet (the owner of Google) is currently listed on NASDAQ, and for legal reasons it is unlikely that Alphabet would list Google separately (Choi, 2022). 5 In 2022, Kakao even tried to list its “grandchild” company Lionheart (Kakao Game’s subsidiary). Kakao Games acquired a majority stake in the online game developer Lionheart with funds raised by IPO. With Lionheart’s hit online game Odin—which was published by Kakao Games in 2021 and topped the country’s app store rankings—Lionheart became Kakao Games’ core cash cow with Odin being the company’s only IP (Kang, 2022; Ko, 2022). Kakao Games tried to list Lionheart only a year and 8 months after its own IPO, although the plan was heavily contested by small investors and was quickly canceled (Kim, 2022c).

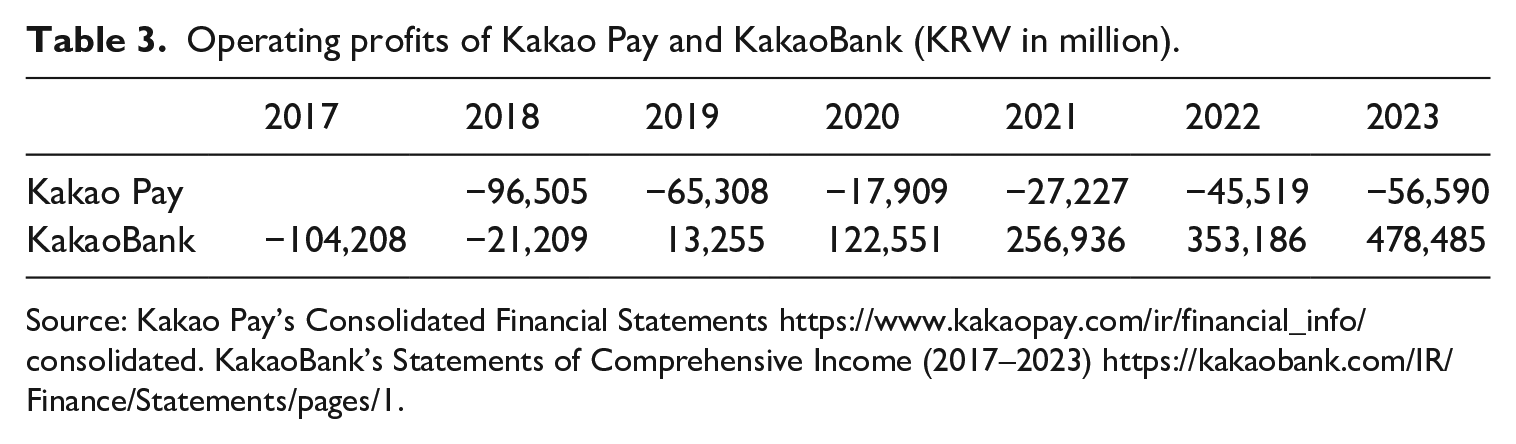

In a sense, tech giants such as Kakao represent the zeitgeist of finance and asset capitalism where “the corporation itself is ultimately a financing device” (Davis, 2009: 5). The primary reason for the existence of corporations seems to be valuation rather than profitability. As Birch and Bronson (2022) point out, the valuation of tech companies is based on the expectation of future earnings, not on current profitability. Kakao’s CEO once explicitly stated that increasing operating profits was not a top priority for Kakao, as he put more emphasis on aggressive M&As (Kakao, 2018; Kim, 2018). Several analysts rated Kakao more favorably the next day (Cho, 2018; Lee, 2018). Kakao’s operating profits show that its major subsidiaries such as KakaoBank and Kakao Pay have had negative profits in recent years, demonstrating that Kakao has been more focused on boosting share prices and valuation than on increasing profits. While KakaoBank’s operating profit turned positive in 2019 and has remained so, Kakao Pay exemplifies the drastic inconsistency between profits and market cap.

As Kakao Pay prepared for an IPO, it was leaked that Kakao Pay set its enterprise value at 16 trillion won ($14.4 bn), 60% higher than the market consensus of 10 trillion won ($9 bn) (Jun, 2021a). When the firm submitted its securities registration statement to the Financial Supervisory Service (FSS) in July 2021, it submitted a price band of 63,0000 won to 96,000 won, expecting its market cap to reach between 9.8 and 12.8 trillion won (Jun, 2021b; Yoon, 2021b). The FSS asked Kakao Pay to cut its share price and valuation, and Kakao Pay had to delay its IPO twice. Although it lowered about 6% of its targeted IPO from $1.63 billion to $1.3 billion (Park, 2021b), the method and the comparable companies that Kakao Pay deployed to calculate its valuation remained controversial because the firm used a less common method for valuation called “growth-adjusted EV/Sales” and compared itself to PayPal Holdings, Square, and PagSeguro Digital. The inclusion of PayPal Holdings played an important role in the overvaluation of Kakao Pay, which ended up raising $1.3 billion (1.53 trillion won) at the $9.9 billion valuation in its IPO (Kim, 2021a; Park, 2021b). On the first day that Kakao Pay went public, its stock price more than doubled its IPO price, giving the company a valuation of more than $21 billion (Yoon, 2021a). Despite its high valuation, Kakao Pay has continually failed to turn a profit since its listing (see Table 3). Its CEO and seven other executives exercised $75 million (90 billion won) worth of stock options only a month after the IPO, triggering fierce criticism from the public (Lee and Yang, 2022).

Operating profits of Kakao Pay and KakaoBank (KRW in million).

Source: Kakao Pay’s Consolidated Financial Statements https://www.kakaopay.com/ir/financial_info/consolidated. KakaoBank’s Statements of Comprehensive Income (2017–2023) https://kakaobank.com/IR/Finance/Statements/pages/1.

Higher valuations are crucial to market monopoly because firms can leverage their high valuations to borrow more cheaply, while lower borrowing costs enable them to acquire more competitors. This “cycle of higher capitalization, lower borrowing, and acquisitions” (Birch and Cochrane, 2022: 50) has resulted in Kakao’s current status as a megacorp and super app. It is noteworthy, however, that Kakao’s IPO sprees are very peculiar. Naver, for instance, has dozens of subsidiaries, but other than Naver Corp. itself, none of them has been listed on KOSDAQ/KOSPI.

In October 2023, three executives of the Kakao group were prosecuted for stock price manipulation in its bidding war over SM Entertainment, which resulted in the arrest of Kakao’s chief investment officer. They were accused of buying $178 million in shares of SM in an attempt to disrupt HYBE’s offer (Lee and Kang, 2023). This ongoing story exposes ethical concerns about the business practices of tech giants, but it also points to a loophole in the megacorp’s valuation practice. In January 2023, Kakao Entertainment secured an investment of $964 million from leading sovereign wealth funds—Singapore’s GIC and Saudi Arabia’s PIF—based on a valuation of about $9.1 billion (Park, 2023). As “the biggest overseas financing in a South Korean content company,” Kakao Entertainment’s ruthless battle for the acquisition of SM Entertainment is seen as tied to the pressure that the oversized valuation put on the company (Song, 2023). While the institutional investors behind today’s tech firms are “not in the business of demanding positive quarterly profit reports” but are committed to “the longer-term project of consolidating market domination” (Rahman and Thelen, 2019: 183), the valuation-focused practice of tech megacorps competing in capital markets has proved to be detrimental not just to small investors but to the entire tech industry as well.

The state-tech-finance Nexus and Kakao’s affinities to Chaebol

To reach market dominance and combat its rival Naver, Kakao has carried out business practices akin to those of chaebol. Referring to family-owned conglomerates such as Samsung and Hyundai, chaebol is known for concentrated ownership, generational succession, collusion with military dictatorship, owner-controlled management, and labor exploitation, to name a few.

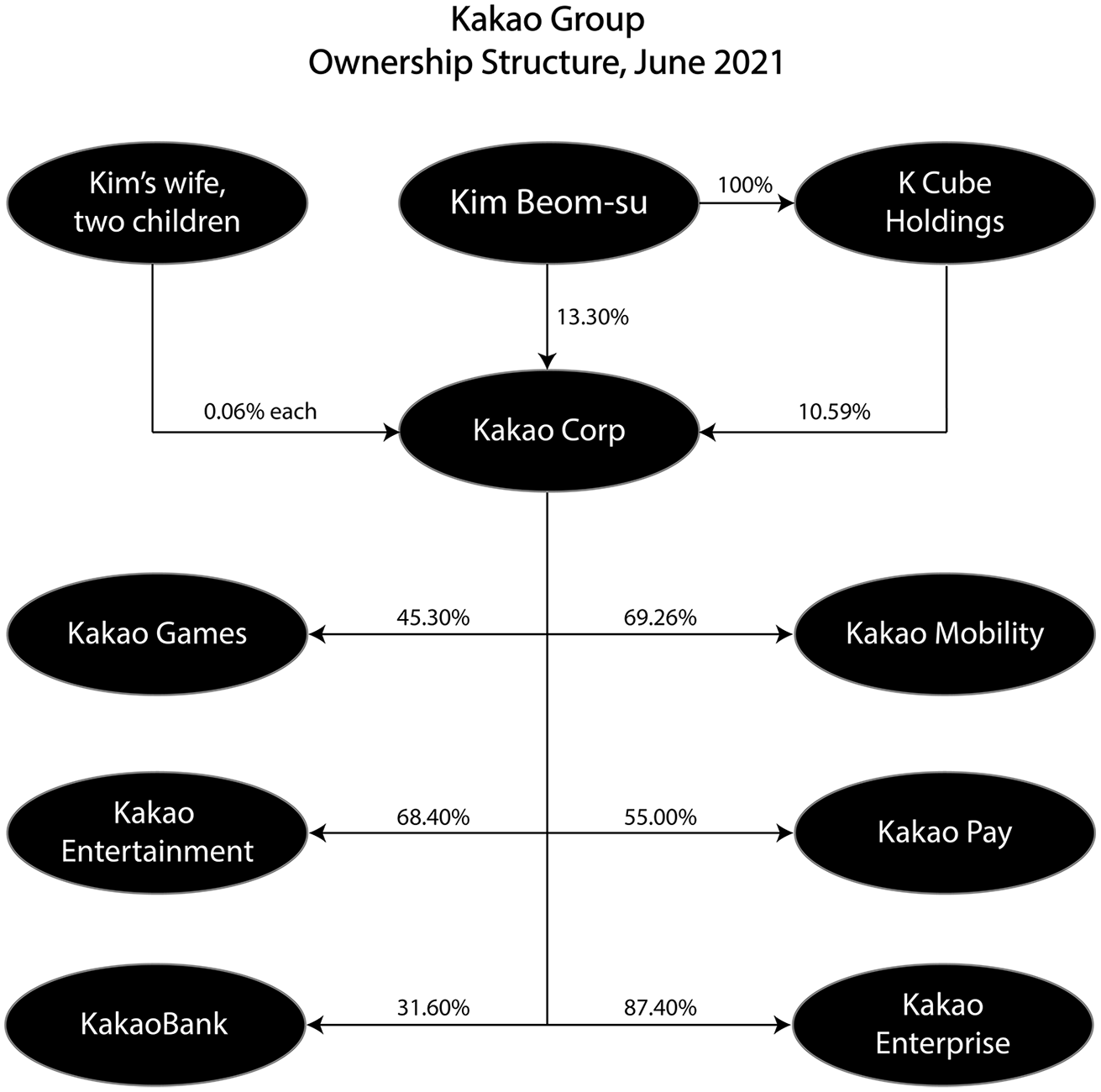

When it comes to ownership, Kakao’s structure has been centralized around its founder and chairman Kim Beom-su, whose position within Kakao is similar to the position of other chaebol founders/chairmen. In addition to his stake of 13.30% in Kakao Corp., K Cube Holdings—Kakao Corp.’s holding company which owns more than 10% of Kakao Corp.’s shares—is 100% owned by Kim Beom-su and managed by his family members (Baek et al., 2021) (see Figure 2). After Kakao merged with Daum, the newly formed company said Kim Beom-su “will stay out of management affairs but will continue to ‘suggest business visions and directions’” (Kang, 2014). While Kim Beom-su has tried to cultivate a reputation that is different from the notorious reputation of chaebol owners (Kim, 2020), data and testimonies about his management style demonstrate otherwise. In particular, Kim has exercised control over decision-making processes such as CEO appointments and M&As (Yang and Cha, 2018). As Athique and Kumar (2022) observe of the Indian megacorp Reliance Jio, “the separation of ownership and management as per the North American corporate form is not fundamental to the status, function or strategy of a conglomerate oligopoly” in Asia (1420).

Kakao group’s ownership structure in June 2021.

From the 1960s through the 1980s, the authoritarian and military regimes of South Korea strategically collaborated with chaebol for export-oriented growth by channeling capital to chaebol companies through the state-owned banks (Chang, 2019; Song, 2009). To be more specific, when the government allocated capital, consumer credit was highly restricted, while domestic capital was channeled to chaebol. In this regard, economists Shin and Chang (2003) call this model “the state-banks-chaebol nexus” in which South Korea’s development model operated in close cooperation and consultation between the government, commercial banks, and big businesses. Chaebol companies were able to borrow money at favorable terms while ordinary citizens had no access to bank loans. Chaebol took advantage of this system for financial and real estate speculation in order to increase assets and expand their market share across different business sectors (Yang, 2018). Not just manufacturing and heavy industries, chaebol conglomerates took over retail sectors, sweeping away small and medium-sized businesses. As workers and consumers, Koreans have lived inside the chaebol’s walled garden—from the washers and dryers they use at home to the vehicles they drive, the cell phones they use, the television and films they watch, and the grocery stores and bakeries where they shop.

In drawing attention to the new forms of market dominance that Kakao exercises, which replicate the legacy of the chaebol, I suggest “the state-tech-finance nexus” as a developing framework for further investigating monopolizing strategies of megacorps in Asia. While this framework could include the subsidies that Kakao (and Daum Communications) have received from the government, 6 collusion between the state and tech has occurred most crucially through deregulation. For instance, while Kakao acquired at least 93 companies between 2016 and 2021, only 5 out of the 93 M&As were closely reviewed by the Fair Trade Commission and no sanctions followed (Lee, 2021).

More importantly, the state-tech-finance nexus means that the state, through various deregulatory measures, paved the way for tech giants to become financial capital. When Kakao launched an Internet bank in 2017, it could not own more than 4% of the shares of KakaoBank because of existing legal restrictions that enforced the separation of financial and industrial capital. Established in 1982, the so-called eunsanbulli (the separation of banks and industrial capital) was mainly intended to prevent chaebol from owning banks. This restriction was relaxed in 2019 to allow industrial capital to own up to 34% of the shares of an Internet bank (Kim, 2021b). Importantly, this new measure applied only to a specific kind of industrial capital “focused on ICT,” not to traditional chaebol corporations. As a result, Kakao immediately increased its shareholding of KakaoBank to 34%, becoming its largest shareholder. In that same year, KakaoBank began to outperform its competitor and turned a profit for the first time (Cho, 2022; Park, 2019).

Kakao has been charged for ruthlessly sweeping out mom-and-pop stores in various sectors. The Kakao group might call such expansion as the formation of the ecosystem (Lee, 2016), but it is noteworthy that “the term ‘ecosystem’ is primarily deployed to rationalize multi-product, multi-market, multi-division business empires using market power to create a walled garden around their customers” (Jia et al., 2022: 1430). In the era of super platforms, Jia and her colleagues write, “the ‘ecosystem’ metaphor is deployed to normalize proprietary cross-sector businesses and customer lock-ins” (Jia et al., 2022: 1430). In the same way that Koreans were locked inside the walled garden of chaebol for decades, Kakao locks users in its walled garden, which in turn gives Kakao higher valuation. Recall that valuation of Kakao and its subsidiaries is based on the expectation of future earnings, not on the current profitability. Such expectation is derived from the users in and of a platform business’s so-called ecosystem (Birch and Bronson, 2022). Taken together, Kakao’s takeover of diverse business sectors has more to do with customer lock-ins and monopolistic control over personal data, which will further reinforce Kakao’s market power.

Conclusion

I have examined Kakao’s corporate strategies with a focus on conglomeration—including its turn to a media conglomerate—and valuation-oriented strategy. While the government’s support for the tech industry intended (even if partially) to decentralize market power of chaebol, this article demonstrates how Kakao has become a new type of chaebol whose growth was not always based on technological innovations. Kakao has built a platforms empire of multi-market and cross-sector businesses, by issuing stocks, listing subsidiaries, and acquiring startups and competitors by leveraging high valuations. Its duopoly status is leading to further customer lock-ins, predatory pricing, and market disruptions. The rhetoric that Kakao apps and services are national infrastructures, therefore, should be carefully approached. The treatment of Kakao as infrastructure would reinforce, as Lee (2023) points out, the idea of Too-Big-To-Fail—which was deployed to rescue chaebol during the 1997 Asian financial crisis—and will make it even more difficult to implement regulatory measures.

Kakao’s trajectory demonstrates that platformization should be understood through corporate forms and strategies—such as conglomeration and over-valuation—as well as through the technicality or materiality of apps. Tech giants such as Kakao comprise a primary example of the shifting corporate strategies under financialization. My analysis shows not only how Kakao mobilizes capital and leverages high valuations, but also how it has become a financial powerhouse itself, much like China’s Tencent (Jia et al., 2022). Furthermore, the state-tech-finance nexus that I suggest as a developing framework for understanding Kakao’s paths to market dominance calls attention to the pivotal role that the state has played, parallel to the process of financialization.

Echoing the argument that the notion of platform capitalism should be pluralized as platform capitalisms (Steinberg et al., 2024), my analysis furthers our understanding of platform power in East Asia, emphasizing the continued importance of historical and regional approaches to super apps and megacorps. Much like what other scholars observe of Japan and China (Jia et al., 2022; Steinberg, 2019), Kakao’s stride toward becoming a media conglomerate shows how the tech giant deploys content to attract users to its platform, an unusual strategy in North America but a pervasive method in East Asia. Likewise, the imprints of chaebol found in Kakao’s business strategy, including concentrated ownership and spin-off IPOs, compels us to reconsider the Silicon Valley-centric model of platform capitalism. My analysis, therefore, extends Steinberg’s (2019) argument that where platform is theorized is as crucial as how it is defined. Further research will be needed to probe how the state-led framework of technology-for-development (see Chakravartty, 2004) ended up consolidating private media power in East Asia and how it undermines the democratic public sphere (Nam, 2024).

Footnotes

Acknowledgements

I am grateful to Dal Yong Jin, Chankyung Pak, and anonymous reviewers from the Media Industry Studies Interest Group at ICA for providing insightful feedback on an earlier draft of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.