Abstract

This article discusses the relationship between cultural production and platform companies by mapping the rapidly evolving political economy of the real-time animation platform Unity. Focusing on Unity's corporate growth and infrastructural extensions beyond its platform boundaries, we argue that Unity has become the de facto default for the development of immersive apps through the creation of workflow monopolies in the production and circulation of 3D real-time animation content. To retrace the impact of Unity's broader diffusion, we draw on an archive (2004–2023) of corporate documentation and promotional material, news coverage, and industry data. This historiography allows us to situate Unity within Unity Technologies’ corporate strategy, which keeps developers “tethered” to its proprietary platform. We found that Unity's growth developed along three overlapping periods: (1) corporate growth through business partnerships; (2) infrastructural integration via the development and acquisition of new tools; and (3) sectoral expansion beyond the media industries. Similar to other dominant platform companies, Unity Technologies’ commitment to the platformization of cultural production allowed it to standardize and control workflows in a variety of industries that utilize immersive apps in product development and marketing.

Introduction

Every day, thousands of software applications or ‘apps’ are developed to create immersive 3D experiences. Distributed via the app stores of Google, Apple, Huawei, Tencent, or Samsung, such immersive apps include games, but also architectural walkthroughs, film animations, and automotive simulations. Thus far, research on apps has predominantly focused on app store governance (Gillespie, 2018), app distribution platforms and economics (Nieborg et al., 2020; Zendle et al., 2023), and ‘culture in the age of apps’ (Morris and Murray, 2018). Less attention has been paid to a new class of digital platform companies that operate business models oriented towards cultural workers instead of end-users and that have come to function as ‘platform tools’ (Foxman, 2019; Nicoll and Keogh, 2019). To be sure, many popular apps, such as transportation or connectivity apps, do not use Unity because they do not contain 3D content, but for those that do, Unity has become a dominant platform tool. What began as a game engine to ‘democratize game development’ (Unity Technologies, 2010) has expanded into a pan-industry platform to ‘help you work better in your industry’ (Unity Technologies, 2021). Engines are best understood as ‘integrated software packages that include physics engines, graphics rendering, and tools for building, lighting, and animating game assets’ (Chia, 2022: 192–193). Like other popular software packages, such as Adobe's Creative Suite and Microsoft's Office, Unity has emerged as the go-to software environment that provides an all-in-one set of tools, art assets, business analytics, and monetization and marketing affordances for those interested in developing interactive, 3D immersive environments that people will experience through smartphones, tablets, or virtual reality (VR) headsets. Today, the 3D real-time animation platform has been adopted by hundreds of thousands of developers and designers around the globe in various segments of the cultural industries and far beyond.

This paper examines how Unity (the engine) morphed from a software tool primarily used by game developers into a production platform used for the creation of 3D apps outside of the digital games industry because of Unity Technologies’ (the corporation) ability to create a workflow monopoly in multiple adjacent industries. A workflow is the process through which ‘a piece of work passes from initiation to completion’ (OED, 2023). The notion of a workflow is closely aligned with the notion of a production ‘pipeline’, a term game industry professionals use to describe: ‘the production chain of design concepts, assets, animations, scripts, audio, and more, each of which are “fed into” [Unity] and made interoperable through the engine's underlying code framework’ (Nicoll and Keogh, 2019: 11). In the media industries, specific software or platform environments establish workflows to efficiently complete tasks in a particular order, particularly repetitive tasks. Because pipelines constitute a professional practice that structures the game development process, they ‘institute design standards, which streamline game-making ideas and techniques into common production workflows, default design methodologies, and accessible 3D toolsets’ (Chia, 2022: 193).

Building on these insights, we will hereafter use the notion of the digital workflow to illustrate how production platforms not only afford the creation and modification of software but are also infrastructurally integrated with distribution platforms; that is, they provide their users with end-to-end services that structure the entire production process. In Unity's case, this high level of integration encapsulates all stages of cultural production: content creation, distribution, marketing, and monetization. As a result, Unity Technologies has attained a dominant position in the digital economy, and therefore, its tool suite has come to follow the economic logic of monopolization, wherein one or a small handful of corporations control a market by leveraging economies of scope and scale. Unity, thus, has become the de facto default for the development of immersive 3D apps (and increasingly other areas of creative work such as architecture, industrial, and automotive design) through its ability to establish and maintain digital workflows for this app genre and combine this with an economic logic that compounds advantages for Unity Technologies as a monopolist. As such, our focus is on the institutional circumstances under which these workflows come into being by considering corporate relationships and infrastructural dependencies. We are acutely aware that the practical implementation of workflows by developers is a process of constant negotiation, the exact nature of which falls outside the scope of this paper. In other words, our goal is to map Unity's evolution, that is, to historicize its institutional path from a software tool into a digital workflow monopoly.

Our historical analysis contributes to two debates in the broader field of platform and app studies. First, we build upon scholarship on the ‘platformization of cultural production’, which discusses the ways in which cultural producers elect to become ‘platform-dependent’ during the creation, distribution, marketing, and/or monetization of cultural content (Poell et al., 2021). For example, when using Unity, creating audiovisual content simultaneously locks developers into a chosen platform's distribution infrastructures. Scholarship on this topic has expanded recently by investigating the effects of the platformization of, for example, building information modelling (BIM), as well as industries such as construction and architecture (Boeva et al., 2023). This scholarly focus on the expanded use of such tools has gained urgency because of the ongoing ‘softwareization’ of cultural production (Lesage and Terren, 2024).

Second, we are conversant with scholarship in app studies, which is concerned with the infrastructural politics of software applications in platform ecosystems (Gerlitz et al., 2019; Goggin, 2021) and with developing methods to study the evolution of platform markets and infrastructures (Nieborg and Helmond, 2019). In a similar methodological vein, this article draws on an archive of corporate documentation and promotional material, news coverage, and industry data to develop a ‘platform historiography’ of Unity's growth and its construction of a workflow monopoly (Helmond and van der Vlist, 2019). We hope that our study of Unity may serve as a roadmap to analyse how similar tools transform into production platforms and invite future scholarship, similar to the work of Nicoll and Keogh (2019), which we discuss below, on how tool dominance impacts creative practices at the level of the individual software developer. It is notable that our study ends in 2023, just as sophisticated large language models and machine learning tools are beginning to be rolled out on a commercial basis into cultural production platforms. We believe that similar workflow monopolies are likely to be built around these emerging technologies.

The stakes of softwareization and platform lock-in building towards end-to-end workflow monopolies across industrial sectors are quite high: cultural producers are incorporated into a value chain built around finding creative ways to extract value at every step of production, distribution, and consumption. As our study shows, Unity's growth and corporate dominance centres on the geographic Global North, but because of global inequalities, this has deeply impacted cultural and creative practices in the Global South. As (Joseph et al., 2023) have shown, Unity follows a pattern that mirrors those of global app stores, which favour a select group of global producers, leaving out the considerations of the workflows of workers in the Global South.

Before we unpack our methodology, we establish two things: first, how software tools became ‘production platforms’ via a careful combination of products and services. Second, how the broader process of platformization enables the creation of workflow monopolies by production platforms such as Unity.

From software tools to a production platform

Unity's rise mirrors, in many ways, the changing nature of ‘the platformization of the Web’ (Helmond, 2015) and the ‘platformization of cultural production’ (Poell et al., 2021). It is distinct in the sense that the company started out in much more of a straightforward way by selling tools, rather than becoming a marketplace for third-party content and providing advertising services (Nicoll and Keogh, 2019). Founded in 2004, Unity began as a game development engine for Over the Edge Entertainment, later named Unity Technologies, to develop and release the company's first game, GooBall, in August 2005. Later that month, the company released Unity, which could deploy games to four distribution environments: Windows, Mac, Mac Web, and the Mac Dashboard Widget. At the time, the integrated editor had the capability of rendering graphics and texture effects with C# and JavaScript support. The software could be acquired by purchasing a standalone license at US$1499 or with limited capabilities at US$249 for independents and small game studios. In 2009, after additional integration of developer tools and the capability to port to multiple mobile and game console environments, Unity became the first professional game engine to provide free licenses to developers (Helgason, 2009). This strategic decision allowed Unity Technologies to diffuse much more widely, particularly among emergent indie – independent third-party – developers, students, and hobbyists (Keogh, 2023). This adoption among a new generation of developers who were different from either incumbent game publishers or the more established indie game studios turned out to be crucial. With the rise of mobile media, Unity also became popular with developers building apps for Apple's App Store and Google Play (Foxman, 2019); an entirely new distribution and monetization ecosystem that turned the business of game production upside down (Nieborg et al., 2020).

Over the next decade, Unity Technologies experimented with subscription revenue models to capture a percentage of developer income based on their profits (especially those free-to-play games with ultra-high revenues in the new mobile app stores). It also provided additional features to their userbase, such as analytics and reports, a customizable splash screen, and source code access, which are desirable capabilities for companies looking to customize Unity to their industry needs. Importantly, Unity's Asset Store was introduced to offer thousands of pre-built third-party 3D models, plug-ins, and other products to simplify the development process, while Unity Technologies retained 30% of every sale (Nicoll and Keogh, 2019).

What to make of this institutional integration of products and services? There has been recognition among scholars that technology such as Unity is better understood as a ‘platform tool’ or ‘production platform’ rather than a mere software tool (e.g. Foxman, 2019). The latter can be seen as the means to perform a specific set of technical tasks in a digital production workflow. For example, Lesage and Terren (2024) stress that the ‘tool metaphor’ is context dependent: that no ‘tool’ is inherently useful, but instead relies on who is using what, and for what purpose. They argue that tools are ‘application software designed by people with a specific idea of the situation in which it is expected to be used creatively by a specific idea of a creative user’ (Lesage and Terren, 2024: 8–9). Following this understanding, Unity was initially developed with a specific user in mind – game developers – yet went on to match the market conditions of digital cultural production on a variety of distribution platforms, each subject to diverse business models. Thus, Lessage and Terren's intervention helps us understand that the imagined user is not merely using a straightforward instrument but is hailed both as a tool user and a producer of cultural commodities in a comprehensive digital workflow.

The increased level of economic and infrastructural integration into the Unity platform has had profound political, economic, and infrastructural ramifications (Poell et al., 2021). Simply put, as tools have morphed into production platforms, they ensure that workflows are uniform and integrated with a range of other proprietary production and distribution platforms (Foxman, 2019). As such, most open-source software tools, such as Twine, Blender, and GIMP, are not production platforms (Harvey, 2014) as they allow for a variety of platform-independent modes of content creation and distribution. Admittedly, the distinction between tools and platforms is not always clear-cut. While software such as Adobe Photoshop and Autodesk's Maya can be considered as software tools, these are part of the wider production platforms, Adobe Creative Suite and Autodesk industry packages. Another way to look at the difference between software and platform tools is Zittrain’s (2008) concept of ‘tethered appliances’, where users have limited capability in modifying a platform to manage the process of creating and distributing their cultural products. Production platforms would be an example of tethered technology.

Much of the extant scholarship on Unity is concerned with the implications of Unity having all the hallmarks of a platform (Chia et al., 2020; Jungherr and Schlarb, 2022; Whitson, 2018). For example, Foxman (2019) argues that Unity ‘locks-in’ users through the intraoperability of its software editor, its integrated asset store, and data analytics affordances. He argues that, as a result, developers become locked-in to the platform's ideologies in the process of creation and therefore have limited manoeuvrability outside of the integrated platform environment to create non-Unity conforming content. In the work of Nicoll and Keogh (2019), we find evidence of how Unity impacts labour practices as they point to the engine's constrained software infrastructure. Crucially, they find that Unity enrols its users in ‘circuits of cultural software’, which influence, mediate, and articulate cultural production workflows in a variety of contexts and industries. These circuits encourage users to adopt specific ‘grains’, such as protocols, standards, and affordances that shape their creative process. Examining the evolving business strategies of Unity Technologies, we have argued elsewhere that the company captures game developer markets – for example, game publishers, studios, and hobbyists – in local venues of game production (Young, 2021).

What all these scholars agree on is that Unity does have an outsized influence on how and what kinds of games – and by extension, real-time animated apps – are made, where, and by whom (Chia, 2022). They also dispel the myth of Unity as a uniform toolset. On the contrary, Unity Technology's hallmark has been following the logic of platformization: that is, Unity's ability to adapt and integrate itself into a wide range of possible workflows, but with Unity at the infrastructural core. As such, critically engaging with Unity's future growth becomes more relevant because of emerging technologies such as ‘the metaverse’, non-fungible tokens, and large language models, which have been or are expected to be integrated into the engine's feature set (Foxman, 2022; Jungherr and Schlarb, 2022). How to account for this outsized influence? Next, we will further discuss what it means for Unity to become a workflow monopolist.

Platforms and workflow monopolies

Unity's ability to capture game design workflows has been a long-term goal pursued by its corporate leadership. In 2014, David Helgason, Unity Technologies’ CEO at the time, gave the plenary address at the company's annual Unite Conference to outline the company's future (Unity Technologies, 2014). There, he explained that Unity got its name as software that could bring together different kinds of media, such as audio, video, and animations; professional teams, such as artists, programmers, and engineers; and distribution platforms, such as consoles and mobile app stores, to make and release digital games. Helgason went on to say: ‘we have to be an end-to-end development platform’. These comments speak to Unity Technologies’ wider business model, which ‘tethers’ (Zittrain, 2008) the production and distribution workflows of cultural workers to Unity.

Nicoll and Keogh (2019: 47) define a ‘workflow’ as ‘the ways that developers streamline, coordinate, and also individualize their labour processes with and through software’. A workflow, thus, takes different shapes and forms based on the person doing the work, be it a programmer, designer, or writer. On Microsoft Word, a workflow can be the process of creating a manuscript document styled and formatted for an electronic and print periodical to sell via subscription. On Adobe Photoshop, a workflow can be the process of creating art or editing a photograph for distribution on social media for app-advertising. And on Unity, a workflow can be the process of creating an immersive app targeted to a specific industry audience and encoded with networking, analytics, and monetization for distribution to several digital storefronts. These examples show how platforms that enable workflows also allow for customizability. Nicoll and Keogh (2019: 48) argue that ‘the question, then, is not whether Unity imposes a particular workflow on developers, but rather how it enables different relationships between multiple possible workflows’. To wit, the ‘so what’ of a workflow monopoly, then, becomes visible in how it distributes power dynamics among a videogame development team, how it sets a template for the requisite skills and roles necessary for videogame development, and how it leverages its status as a metaplatform to enroll a diversity of workflows into its software ecology (Nicoll and Keogh, 2019).

The political economy of platformization

To historicize the ascendance of Unity's workflow monopoly, we retrace the evolution of (1) the engine and (2) the scale and scope of Unity Technologies as a corporate entity. In other words, we must engage with the political economy and infrastructural politics of platform evolution as Unity morphed from a tool into a production platform. A conceptual roadmap to account for the growth of platform corporations is Jia et al.’s (2022) study of the China-based tech conglomerate Tencent, which describes four overlapping processes to account for the evolving nature of platform power: platformization, infrastructuralization, conglomeration, and financialization. While the former two are particular to platform and social media companies, the latter two have a longer history as corporate strategies deployed by transnationally operating conglomerates. This acknowledgement of historical continuity is important as it shows that platform companies tend to follow well-worn institutional grooves in their growth. It also demonstrates how infrastructural shifts and economic decisions mutually reinforce each other.

First, the process of platformization points to the question of how platforms leverage the network effects of being corporate actors constituting multisided markets; digital platform companies have situated themselves as corporate intermediaries that bring together end-users, advertisers, service providers, producers, suppliers, and physical objects. As Poell et al. (2021) note, research has shown that such markets have strong ‘winner-take-all’ dynamics leading towards monopolization and stark inequities between producers and consumers. While uniquely focused on content production rather than user connectivity or content distribution, we agree with Foxman (2019) that Unity operates a multi-sided market because it provides its users (i.e. developers) access to advertising technology (adding a side in its market) and to its asset store (providing a marketplace for buying and selling third-party content). Later in our analysis, we refer to the economic process of platformization as a form of corporate growth through expanding business partnerships, which allowed it to begin its construction of an end-to-end workflow monopoly.

The second process, infrastructuralization, builds on the first. Platformization relies on platform companies not only creating and operating markets accessible to end-users but also opening their infrastructural boundaries internally and externally. Platforms allow externally developed (‘third-party’) software development kits and software plugins to interface with their internal infrastructural systems. They expand outwardly by integrating with distribution platforms such as hardware consoles and app stores. These are notably similar in shape to what Plantin and de Seta (2019: 258) define as ‘infrastructuralization’, the process of platforms acquiring ‘properties that are typically associated with infrastructure, such as scale, ubiquity, and the criticality of use’. Simply put, platform companies tend to invest heavily in adding large-scale infrastructures to monopolize the markets for cultural production. Operating platform markets and controlling access to its infrastructure to outsiders allows platforms to strictly police their boundaries while accumulating revenue by charging a variety of users through a range of revenue models, including direct payments (e.g. for assets), subscriptions (engine licensing fees), and incurring revenue via integrated advertising in content developed with licensed technology. In our subsequent analysis, we refer to the process of creating software linkages as infrastructural integration, which typically takes the form of developing new tools, acquisition of existing technologies of tools, and providing interfaces to integrate with third-party infrastructures and tools.

In Jia et al.'s (2022) study of the popular chat app WeChat, it becomes clear that the corporate entity Tencent that owns WeChat became a particularly dominant industry actor by not only adding sides to its market (e.g. advertising) and by integrating its infrastructure, but also by engaging in a different kind of corporate expansion referred to as ‘conglomeration’. The traditional definition of conglomeration is a ‘firm with non-interdependent operations managed through financial control’ (Jia and Kenney, 2022: 61). In the context of platform companies, it refers to sectoral expansion into adjacent industries that are not necessarily part of the core strategy during the platform's launch. For example, Tencent launched as a ‘mobile first’ company, focused on the intersection of telecommunications and mobile technology, such as pager services (Jia et al., 2022). Especially important to its strategy of conglomeration were online gaming apps that demonstrated an interest in business synergy across its many divisions (Jia et al., 2022; cf. Negro et al., 2020). In our study of Unity Technologies, we take note of acquisitions and the entry into markets that have gone beyond the original platform's business scope of developing tools for game designers, such as automotive and architectural drawing, that mark the deliberate corporate strategy of conglomeration.

The fourth corporate mechanism, ‘financialization’, refers to the general political economic environment of global neoliberal capitalism and cannot be separated from the above strategy of conglomeration (deWaard, 2024). Financialization refers to the ascendant power of finance capital in the late twentieth century as a response to a steady decline in business profits (Dumenil and Levy, 2004). Banks and other financial interests grew to take a more prominent role in the structural conditions of firms to ensure steady returns, resulting in two strategies: (1) growing the global value chain to reduce costs, which then (2) increased surplus extraction to pay dividends to shareholders, share buy-backs, and, most importantly for our study, mergers and acquisitions. As Jia and Winseck (2018: 37) note, ‘in this sense, heightened merger and acquisition activities reflect the processes of financialization and contribute to them as well’. Unity Technology's growth has come largely through a debt-fuelled merger spree in the now past era of cheap credit. The concept of financialization thus helps us understand how this happened and why it was an essential ingredient to create a workflow monopoly.

Methodology: Platform historiography and critical political economy

To examine the platformization, infrastructuralization, conglomeration, and financialization of Unity, we adapt the methodological framework of platform historiography to trace the economic growth and infrastructural extensions that enabled Unity's sectoral expansion into multiple industries and establish its end-to-end workflow monopoly. Platform historiography ‘foregrounds the methodological considerations and reflections associated with the use of multiple sources to interpret platforms’ pasts’ (Helmond and van der Vlist, 2019). These multiple sources include the use of live websites (at the time of research) and web-archived content to trace how a platform emerged and operated in the past, and how it may have changed over time. Helmond and van der Vlist (2019) frame the implementation of platform historiography along two entry points: the study of developer-side histories (i.e. resources made for and created by developers) and business-side histories (i.e. company advertising, news, and documentation). We focus on the business-side history of Unity Technologies that includes live (2021 to early 2023 during the data gathering phase of the project) and web-archived versions of Unity Technologies’ website via the Internet Archive's Wayback Machine (2004 to 2021). We ended our data gathering in early 2023, as this was when Unity's spending binge ended. While examining resources created by developers can illuminate labour perspectives into how workflow monopolies are perceived and experienced by workers, such analyses are outside the scope of our research, in focusing on how Unity Technologies developed its platform.

Several case studies have used platform historiography to study the platforms of Meta, Tencent, and Twitter. For example, in Nieborg and Helmond's (2019) account of Facebook Messenger as a platform instance of Facebook (now Meta), they retrieved developer documentation, product documentation, and financial disclosures via Facebook's website on the Internet Archive's Wayback Machine to demonstrate Facebook's ‘platform evolution’. These archived boundary resources demonstrated Facebook's infrastructural ambitions via technical documents that provided ‘detailed information about (1) the introduction of new platform resources, such as new APIs and SDKs; (2) the data, functionality, and development options they make available; and (3) the instructions for their technical implementation’. Likewise, they traced Facebook's platform boundaries using, again, developer documentation from the Wayback Machine, but also Facebook's blog archives and trade publications alongside interviews with some of Facebook's marketing partners to reveal the company's relationships with third-party developers over time. The accrual of business and program partnerships revealed how Facebook, through the acquisition and integration of infrastructural properties over time, ‘speaks to Facebook's growing ubiquity by embedding itself in other markets and industries to render technical and business operations more widely and immediately available’.

Furthermore, these levels of sectoral expansion via infrastructuralization are also evident in Jia et al.'s (2022) analyses of Tencent's WeChat. In their study, they use platform historiography to collect tech news, reports by commercial market data providers, WeChat blogposts, and Tencent corporate documentation to trace Tencent's mobile development from 2011 to 2021. Their analyses demonstrate how, through conglomeration and financialization, Tencent was able to rapidly shift from controlling its own portal to distributing apps through the MyApp store, to developing WeChat into a ‘super app’ (i.e. an app offering instant messaging, social networking, payments, and video services all in one discreet mobile application). And, finally, in Burgess and Baym's (2020: 113–114) biography of Twitter, they analyse the intersections of technology, design, business models, and cultures of use to discuss how Twitter has shifted over time, reconstructing the histories of key, platform-specific features, and interviewing end-users to discuss their experiences with the platform. Using the dual entry points of a business- and developer-sided history, they study the frictions that can occur between platforms and end-users as platforms programmatically optimize their infrastructure into a specific workflow. In each study, we find that the economic growth and infrastructural extensions of platforms lead to monopolistic, winner-take-all market conditions. Because Unity Technology's growth and expansion follow a similar corporate path, we follow a similar approach as forwarded in these three platform historiographies.

In addition to the scholarship of platform historiography, we also draw on Corrigan’s (2018) critical political economic approach to trade press analysis to ‘burrow down’ into our data set and ‘listen in’ to the discourses therein. This allows us to verify a document's authenticity, credibility, representativeness, and meaning (Scott, 1990). Like Jia et al. (2022), we aim to increase the credibility and representativeness of our findings by gathering data from two key sources: (1) documentation produced by Unity Technologies; and (2) journalistic accounts via news sources. While publicly disseminated information from Unity Technologies can provide important context to understand the development of Unity over time, corroborating this information via external journalist accounts can verify the credibility of Unity's documentation and improve the representativeness of the conclusions we draw in our analysis. In short, we do not take Unity's documentation at face value. In many instances, drawing on journalist accounts revealed acquisitions and transformations within Unity Technologies which were not covered by press releases from the company itself (e.g. mass layoffs). More recently, Corrigan (2024: 23) has argued that using corporate documents and the trade press allows political economists to ‘not just document business practices, but to learn to see it as practitioners do’. This puts us in the shoes, so to speak, of those making choices in these companies and helps us conceptualize the stated and unstated social processes at play. For example, when we conceptualize the concept of an end-to-end workflow monopoly, this is informed by the stated goals of the company, the journalistic record of it, but also our own theoretical framework, leading us to label it as a ‘monopoly’, which no corporate supervisor would willingly say on the record.

To capture these journalistic accounts, we searched the news and financial databases of Bloomberg, Factiva, and Factset. A variety of search terms were used to capture Unity, Unity Technologies, and Over the Edge Entertainment to ensure most documents were gathered. Once obtained, these documents were analysed to verify their relevance to Unity Technologies and not to irrelevant subjects using common terms such as ‘unity’ and ‘technologies’. In addition, taking our cues from Jia et al. (2022) we used the Internet Archive's Wayback Machine to examine periodic iterations of Unity's website for company press releases, patch notes, and updates to Unity software and services, acquisition and integration of third-party software, blogs and announcements from Unity's executive officers, and feature pieces on Unity use cases in a variety of industry contexts. From these collective documents, we identified additional and relevant sources of corporate documents, such as Helgason's plenary keynote at Unite 2014 on Unity Technologies' YouTube channel, which provide insights into the company's internal deliberations and corporate strategies.

Altogether, this corpus enabled us to build timelines of notable events in Unity Technologies' evolution and break it down into three major areas of analysis: Unity Technology's corporate growth through business partnerships; Unity's infrastructural growth through acquisitions; and Unity's sectoral expansion into adjacent industries as it launched new product tools and forged new ecosystems. All of these expanded the workflow possibilities of Unity into non-gaming related industries, solidifying its new role as a workflow monopolist.

Unity's economic growth through business partnerships

In the following analysis, we argue that software creation tools transform into production platforms through corporate partnerships with software and platform companies, infrastructural integration of tools through acquisitions, and workflow optimization into industry sectors to solidify an end-to-end workflow monopoly. This trifecta of growth, integration, and optimization of markets and tools comes to situate Unity as an end-to-end production platform that establishes workflow monopolies in targeted industries. Furthermore, we demonstrate how Unity Technologies has been able ‘scale’ over the past two decades, which can provide a further window into how ‘Big Tech’ companies become dominant in their respective industries (Birch and Bronson, 2023).

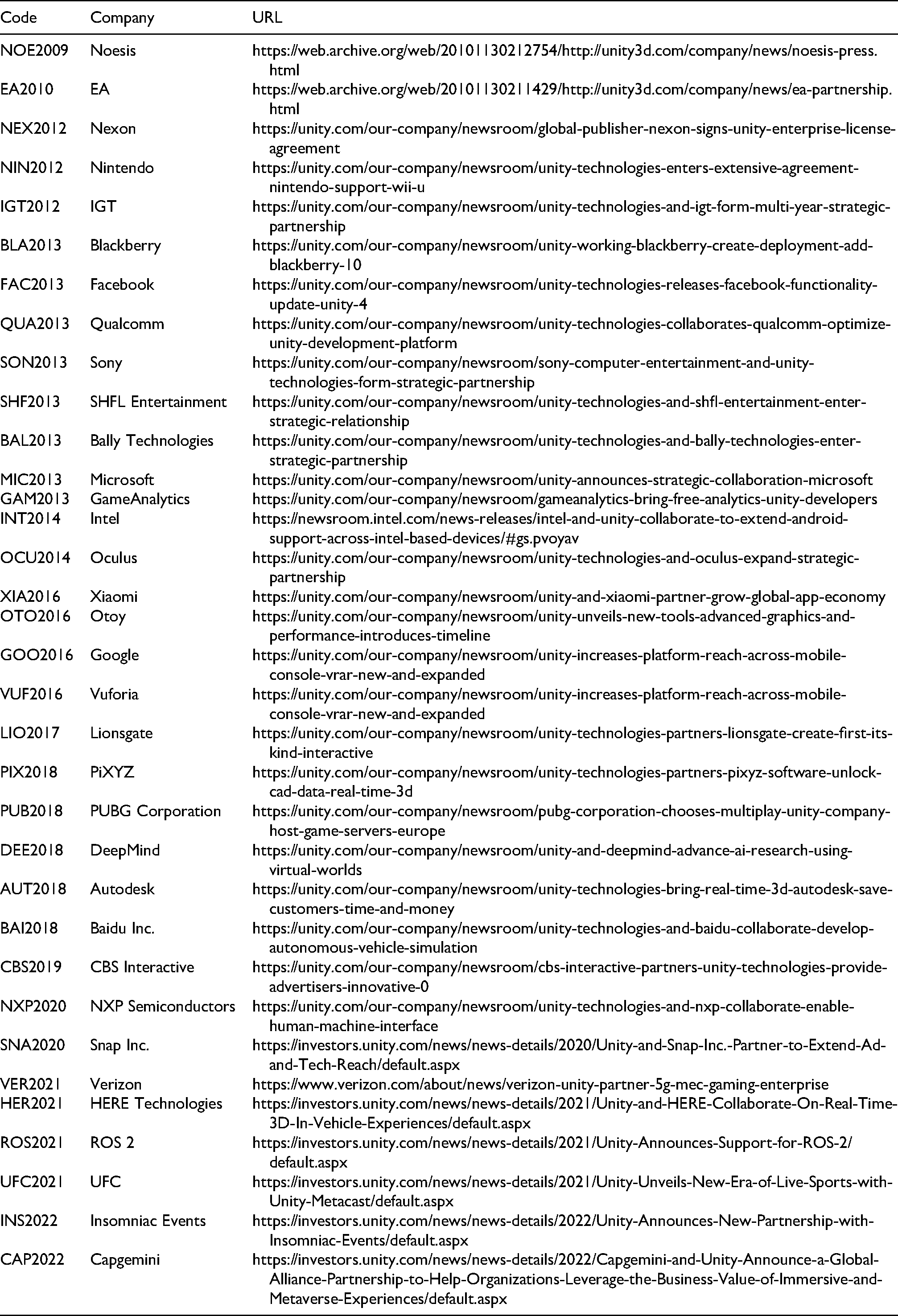

In our dataset, we identified at least 34 business partnerships between Unity and other companies across multiple industry sectors from 2004 to early 2023, see Appendix 1. We say at least 34, because not all partnerships were announced by Unity and were only discovered through other company announcements found on Bloomberg, Factiva, and Factset. Prior to the release of Unity version 5 in 2015, almost all these partnerships were with major game companies such as EA (EA2010), Nintendo (NIN2012), and Sony (SON2013). Following the standardized annual release of Unity (e.g. 2017.1 in 2017, 2018.1 in 2018, and so forth), there was a significant increase in building partnerships with companies that either provided technical software for integration within the product suite itself or established a new platform instance tailored to a specific industry workflow. These partnerships demonstrate elements of financialization (Jia and Winseck, 2018) and the initial growth in what Lesage and Terren (2024) identify as the ‘specific idea of a creative user’ of Unity as a set of tools and as a workflow.

The first significant partnerships outside of the game industry took place in 2018 with Pixyz (PIX2018), Autodesk (AUT2018), and Baidu (BAI2018). The partnership with Pixyz resulted in the Unity Industry Bundle with the release of Unity 2018.3, which provided a suite of tools optimized for Pixyz computer-aided design or ‘CAD’ workflows into the Unity environment. Pixyz’ own tool instances, such as Pixyz Studio and Studio Editor for CAD optimization, Pixyz Pipeline for batch-processing large file sets, and Pixyz Review for file viewing, were all pipelined through the Pixyz plugin installed in Unity. This ensured that CAD files and models were streamlined into Unity's environment. Unity was so pleased with the partnership that in their post-SEC filing financialized spending spree, Pixyz became one of Unity's first acquisitions (PIX2021). The partnership and subsequent acquisition of Pixyz built an ecosystem of workflows for designers and developers in the game, film, architecture and construction, and automotive industries to manage their CAD files from creation to dissemination in a secure, tethered pipeline via Unity plugins and instances.

Later that year, Unity built a partnership with Autodesk, a large US-based provider of CAD software, to ensure full data interoperability between their products, specifically Autodesk Revit, VRED, and Shotgun, which are used for BIM, cross-reality (XR), and animators. This, in turn, provided additional workflows in the architecture and construction, automotive, and film industries (AUT2018). The Unity–Autodesk partnership did not come out of nowhere but was built on a previous collaboration to develop the FBX Exporter plugin for the release of Unity 2017.2 to ensure the pipeline of 3D models and data in Autodesk's licensed proprietary FBX file format between its popular Maya and 3DMax products, which are go-to software in game development (Lian, 2017). To accommodate these specific functionalities, the Unity Reflect instance was provided, which integrated Autodesk's Revit for BIM workflows in the architecture and construction industry. This ensured that as architects design BIMs for potential construction products, their designs are optimized within Unity's production platform ecosystem before dissemination via the Unity Reflect Viewer, which integrates into augmented reality (AR), VR, mobile, and desktop devices. In sum, this collaboration is prototypical for how end-to-end workflows are created and become a tethered environment for the development of BIM models, from ideation all the way down to the client construction firm and potential customers.

Lastly, also in 2018, Unity formed a partnership with the Chinese search giant Baidu to develop the Apollo autonomous vehicle simulator, allowing developers to test autonomous vehicles in 3D simulated real-world situations (BAI2018). The partnership tapped into Unity's growing relationships with other automakers such as BMW, General Motors, Toyota, Volvo, and the Volkswagen Group. Its goal: to provide automotive engineers with a simulator to quickly test and validate product safety features within a 3D virtual environment before using a test driver, test facility, and costly product resources. The development of the Apollo instance complemented the release of the Unity Simulation instance in 2019, meant for broader product safety and testing in virtual environments, and the Unity Forma instance in 2020, for digital marketing production drawing from 3D engineering data. Alongside the instances developed in partnership with Pixyz and Autodesk, workers in the automotive industry now have access to an end-to-end production platform to build, test, and market their products before any chassis is manufactured. In all these partnerships we listed, we see a variety of processes at play: increasing levels of creative lock-in in a variety of non-gaming industries, partnerships that can lead to future conglomeration, and ultimately, the increasingly financialized growth motives of Unity Technologies. All of this leads down a road towards redistributed power dynamics around workflows (Nicoll and Keogh, 2019) and lock-in (Foxman, 2019).

Unity's infrastructural integration through acquisitions

To leverage its position as the default tool in these industry workflows, Unity Technologies also had to gain control over key assets in its end-to-end pipeline. To that end, in 2010, Unity released its in-house Asset Store. In an interview with gameindustry.biz, Helgason states that it took about 2 years of development to create this marketplace for third-party content (Elliott, 2010). While the Asset Store is still a critical piece of Unity, 2 years of development is slow for a company such as Unity Technologies to rapidly expand and grow its production platform. The company would either need to develop business partnerships to gain access to key infrastructures or acquire those infrastructures for optimization within Unity. Therefore, Unity Technologies acquired 25 companies from 2014 to 2023, which infrastructuralized the Unity instances and allowed for further integration with existing technologies, external tools, and platforms.

Following Unity Technologies’ SEC filing in 2021, the company went on a spending spree of acquiring 12 companies in 2 years, primarily around tools for workers in the aforementioned industry sectors – architecture and construction, film, and automotive industries, see Appendix 2. Whereas in previous years Unity Technologies had to build partnerships, going public meant that access to finance capital allowed them to acquire infrastructural objects and technologies in their end-to-end industry workflows. For example, the acquisition of VisualLive's construction AR tools was funnelled into the Unity Reflect instance in support of transforming BIM data in the architecture and construction industry (VIS2021). Likewise, the acquisition of the deep learning company RestAR integrated their tools to scan and render physical consumer products in high-quality 3D with the Unity Forma instance for marketers (RES2020).

Unity also took the opportunity to acquire companies that can be described as pan-industry tools, which optimized Unity's production platform for any industry work environment. The acquisition of Codice Software's PlasticSCM provided additional version control functionality to Unity Cloud with the ability to handle the large asset repositories, massive binary files, and thousands of concurrent users, all while supporting distributed and centralized repositories with merging options (COD2020). The acquisition of the high-performance remote desktop company Parsec rolled their high-end streaming technology into the Unity Cloud (PAR2021). Likewise, the acquisition of SyncSketch incorporated the company's collaboration tools into Unity Cloud, which allowed teams to communicate, provide feedback, and contribute to projects in real-time (SYN2021). The integration of these additional infrastructural elements into Unity instances catered to globally operating customers who communicated across continents and time zones. It is notable that once these kinds of productivity tools are adopted by users, they have a lock-in effect because of data portability issues.

Perhaps one of the most interesting acquisitions during this 2-year window was in visual effects (VFX) for animators primarily in the film and game industries, but also applicable to the architecture and construction, and automotive sectors. The first of these VFX acquisitions was Interactive Data Visualization, the creator of SpeedTree, which provides a 3D suite of vegetation modelling and environment creation products for architecture, games, VFX, and real-time simulations (INT2021). The press release mentions how this nature environment builder has been used for notable video game series such as Assassin's Creed, Call of Duty, and The Witcher, while highlighting its role in the architecture and film industries, noting it's Scientific and Technical Academy Award from the Academy of Motion Picture Arts Sciences for contributions to ‘hundreds of major films, from indie projects to the highest-grossing films of 2020’ (INT2021). Later in 2021, Unity acquired Weta Digital, known famously for its VFX in film and television series such as Lord of the Rings, Avatar, and Game of Thrones (WET2021). This monumental acquisition included all the tools, engineering pipelines, and VFX assets from a company known for innovation in the film industry. The last of these VFX acquisitions included Ziva Dynamics with its understanding of complex 3D anatomical simulation and real-time artistry tools (ZIV2022). The press release included a video demonstration from a digital human, Emma, who spoke of the technology's ability to create lifelike, real-time characters with rapidly processing faces and expressions (ZIV2022).

Taken together, these last three focused VFX acquisitions show how Unity Technologies solidified its pan-industry VFX pipelines to include 3D environments, tools and assets, and characters. It was not surprising to see Unity Technologies release its Unity Artistry Tools later in 2022, which provides a ‘complete toolchain for 3D creation, simulation, and rendering, for any size of production’ (Unity Technologies, 2022). Alongside the additional acquisitions to expand and optimize its Cloud, Forma, and Reflect services and instances, Unity Artistry Tools demonstrates how Unity Technologies specifically targeted tools and assets to control each stage of its end-to-end workflow pipeline, so workers stay tethered to the Unity infrastructure for the creation of immersive experiences.

Sectoral expansion into adjacent industries

It is worth reiterating our argument: Unity is a production platform that is increasingly used by other, seemingly non-adjacent industries. It has done this by demonstrating to non-game design users its utility as well as its dominance in their sectors. This growth and expansion of Unity Technologies and its Unity production platform are inextricably tied to its ability to wield finance capital to increase its market share. This, in turn, leads to dominance of those people, infrastructures, and assets tied to its end-to-end workflow monopoly. As discussed in the previous sections, Unity used business partnerships to integrate third-party technologies and strategically acquired companies to own and optimize technologies and assets along its multiple sectoral industry workflows. As this last section will illustrate, to effectively control and optimize industry workflows, requires the continued use of corporate power (i.e. the ability to partner with ‘big tech’ companies, such as Meta) and finance power (i.e. the ability to purchase smaller tech companies and become a competitive ‘big tech’ company, again, like Meta) to release new features, assets, and instances within Unity. Both platform and finance power are needed for companies such as Unity Technologies to scale as they expand vertically within an industry and laterally into multiple industry sectors.

In 2015, Unity released Unity 5, which supported development for 21 game platforms with an end-to-end production platform for game development, ensuring developers created, analyzed, and monetized their games within Unity's all-in-one package (Unity Technologies, 2015a). With the release of Unity 5.1 later in 2015, Unity Technologies started a trend of integrating additional features for other sectoral industries, such as XR integration for VR and AR 3D immersive experiences to optimize rendering workflows for VR and AR devices such as Microsoft's HoloLens, Samsung's Gear VR, and Oculus's Rift – the leading VR devices at the time (Unity Technologies, 2015b). This not only provided game developers with additional platforms to build games for, but also workers in the architecture and construction industries, as emphasized on their website at the time (Unity Technologies, 2015c).

When Unity 5 came to the end of its lifecycle, Unity Technologies’ announced Unity 2017, which would incorporate these adjacent industries: ‘Unity 2017 will bring the start of a series of features designed specifically for artists and designers across disciplines, from technical artists, to lighting artists, animators and more’ [emphasis added] (Unity Technologies, 2017). Following the addition of the architecture and construction industry, the film industry was next with the release of Unity 2017.1, which included Timeline and Cinemachine to create cinematic content and procedural cinematography to control sequences and compose shots. Unity released a short film – Adam – which teased Unity's capabilities in film animation and production the previous year, in 2016. This was followed by a collaboration with Disney's Pixar on Coco VR to coincide with the release of the film Coco in 2017. When Unity 2018 was released the following year, Unity's Solutions page listed ‘architecture, engineering & construction’, ‘automotive and transportation’ and ‘film’ as some of the industries using Unity to develop their 3D immersive products (Unity Technologies, 2018).

In the following five years, Unity released Pixyz integration with 2018.3 for CAD and drafting, a Unity Reflect Instance for BIM, Unity Simulation instance for product safety, Unity Mars instance for XR experiences, and Unity Forma instance for automotive product configuration in marketing, to name but only a few. Each of these integrations and standalone instances provides specific workflow pipelines for the development of immersive products in these industries. While Unity Technologies has its own team of engineers working to build and integrate these platform instances and optimize workflows for these industries, it was through wielding finance power for strategic acquisitions that enabled Unity to rapidly expand into these adjacent sectors and establish itself as a default pipeline for any company's workflow solutions.

Discussion and conclusion

The rapid growth of Unity Technologies the past decade has been nothing but meteoric. The company's approach to corporate growth, infrastructuralization, and sectoral expansion resulted in Unity becoming the go-to tool to create 3D games, as well as other cross-reality immersive experiences. While there are competing real-time animation platforms, such as Epic Games’ Unreal Engine or Amazon's Lumberyard (Amazon, 2021), Unity Technologies’ focus on economic and infrastructural integration with industry-specific technologies and companies has made it indispensable for many immersive 3D app workflows. As a result, global businesses such as Disney, Toyota, and Nintendo use Unity in their design process when they want to develop such apps. What once could be chalked off as one of the many software tools within the game industry has grown into a dominant end-to-end production platform for products in numerous industries.

Unity Technologies’ corporate trajectory is not unique. Amazon, Alphabet, and Meta have also grown rapidly to become dominant platforms for internet searches, e-commerce, and connectivity, respectively. Indeed, it can be argued that Unity has become part of the small group of US-based production platforms developing most content on the internet. What our analysis demonstrates is how technology companies and software applications become digital platforms, and that production platforms are no exception in their effort to monopolize industry workflows within end-to-end pipeline infrastructures. In the case of Unity Technologies, we found that the company formed strategic partnerships and acquired companies to control its end-to-end workflow of 3D data within its suite of tools and services. We also found that to stay relevant as a production platform, Unity must continually expand, integrate, and optimize its platform or risk losing out to other platforms, such as Epic Games, Adobe, Amazon, and Microsoft.

Similar to other longitudinal studies of how platform companies institutionally evolve over time (e.g. Nieborg and Helmond, 2019), our findings reveal how a platform company emerges from economic growth from business partnerships, infrastructural extensions via development and acquisition of new tools, and sectoral expansions into adjacent industries. In each of these overlapping periods, we see how Unity Technologies identified workflows in the process of cultural production that it needed to become part of its end-to-end pipeline. If Unity could not build a piece of pipeline in-house, it used its corporate power to establish a partnership with a company that had what it needed and built a plugin for optimization. When Unity had the capital, it wielded its finance power to acquire that piece of the pipeline directly and optimized its infrastructure within its platform. In each case, we see an inclination to expand and control virtually all workflows from beginning to end in the process of cultural production.

We also note that our research demonstrates other important characteristics that define the intersection of cultural production and workflows: that a monopoly in this space is not entirely the product of a top-down process. Many of the acquisitions and integrations made by Unity were the result of partnerships which were generated out of existing synergies in production and distribution. These synergies are often those developed or requested by the workers themselves through trial and error and a long-standing process of creative workflow development over many years. Unlike the work of Nicoll and Keogh (2019), our research does not account for how specific workflows changed by way of worker preferences because we did not conduct interviews or engage in an ethnography; see Whitson (2013) and O’Donnell (2014) for more in-depth discussions on the difficulties in researching software developers. Yet, we would be remiss to note that many of the integrations that Unity achieved over these years would have been welcomed by its users. In this way, we can see how workflow monopolies are developed out of a unique confluence of capital flows and user interests. It should come as no surprise that platform monopolies are only too happy to take advantage of such inclinations among workers.

In the same way that Unity Technology's corporate trajectory is not unique, nor is its strategy of control to monopolize the workflows of cultural production. We see similar efforts by ByteDance, Microsoft, and Adobe in the realm of short-form video, office productivity suites, and media production environments, respectively. While not arguably as well known, the rapid growth of immersive 3D digital content suggests it is only a matter of time before a competitor joins these household names for control over the workflows of cultural production. Unity Technologies has already placed itself in a dominant position to control the market share of 3D app development next to other immersive content platforms, such as Epic Games’ Unreal Engine. One thing is clear, though: as fewer companies control the tools of cultural production, the more tethered workers become to its workflows. As companies such as Unity Technologies continue to control and monopolize the workflows of cultural production, the more the material world around us will continue to be built in its image.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Appendix 1. Identified business partnerships with Unity Technologies (2009–2022)

Appendix 2. Identified mergers and acquisitions by Unity Technologies (2014–2022)