Abstract

While the emergent literature has clearly documented the unfolding of housing financialisation in urban China, a counter-trend occurring simultaneously has received little attention. Focusing on the revival of affordable housing and Shanghai’s shared-ownership housing (SOH) scheme, this study examines how housing financialisation is simultaneously facilitated and managed by the state. Rather than extending housing finance to low-income groups as in many Western societies, the statecraft in China is characterised by segmented housing (de-)financialisation. On the one hand, the strategy has included as many families as possible for housing financialisation; on the other hand, it has excluded low- to middle-income families to reduce financial risk and maintain social stability. SOH merges the two rationales into one by using financial capacity as an implicit eligibility criterion. While lower-middle-class families have been drawn into shared homeownership, they have been frustrated by constraints on assetisation and have become losing subjects of financialisation.

Keywords

Introduction

In parallel with the global trend of urban financialisation, Chinese cities have experienced similar changes. Serving as a spatial fix to the capitalist accumulation crisis, urban built environments, such as land, infrastructure, housing etc., have been widely treated as financial assets (He et al., 2020; Shen and Wu, 2020; Wu et al., 2021; Wu, 2022). Existing studies have recognised the dominant role of the state as one of the most significant differences from urban financialisation in Western societies (Wu, 2021). In particular, how the state enables and executes financialisation has become the focus of much research. It is well documented that various innovative financial instruments have been introduced by the state, including local government financing platforms, municipal bonds, chengtou bonds, wealth management products etc. (Feng et al., 2022a; Pan et al., 2017). These techniques are widely used not only to finance development but also to deliver public services (Shen, 2022). The power of the state is reinforced rather than diminished through financialisation (Feng et al., 2022b).

However, what has not been fully studied is a counter-trend in which the financialisation process is regulated by the state. First, since financialisation is orchestrated by the state in China (Wu, 2021), the way the state controls the process and outcome is equally important as the way it creates and promotes financial instruments and markets. The relationship between the two is significant for understanding the state-finance symbiosis in China (Aalbers, 2022). Second, the ‘who’ question, i.e., the agency of actors, is critical to delineate the fragmented and contested process of (de-)financialisation (Fields, 2017b; Pike et al., 2019). A few studies have highlighted the different stances and practices taken by multiple governments (Li et al., 2022; Shen, 2022). However, these studies remain largely state-centred. Extending the analysis to the experiences of non-state actors offers complementary yet significant insights into a full understanding of urban (de-)financialisation in China.

In the sphere of housing, the state had deliberately leveraged housing investment to boost domestic consumption in response to the 2008 global financial crisis (Wu et al., 2021). What has been largely ignored is the revival of affordable housing schemes that took place during the same period (Shi et al., 2016; Zhou and Ronald, 2017a, 2017b). In fact, echoing the post-crisis responses to the increasing unaffordability of housing in Western cities (Wetzstein, 2019; Wijburg, 2021a), since the late 2000s, the Chinese state has launched a series of regulations to cool down the overheating housing market. In addition to various policies of home-purchase restriction and mortgage restriction, the renewed state commitment to the provision of affordable housing represents a major component of the state’s efforts to achieve housing de-financialisation. The two concurrent processes, which have seldom been linked, together reflect well the statecraft around finance in China, that is, to promote economic growth while maintaining social stability.

Focusing on the revival of affordable housing and Shanghai’s shared-ownership housing (SOH) scheme, this study aims to examine how housing financialisation is simultaneously facilitated and managed by the state in urban China. The focus here departs from the analysis of capital flows and aggregate data, and centres instead on the socially embodied processes of housing (de-)financialisation. Among other affordable housing schemes, the SOH scheme offers a good case for study because it was purposely designed to bridge the housing market and the state-based social security system; the tensions between the two are inherently internalised in the scheme. Thus, the design and management of SOH can be useful to understand the (de-)financialising of housing.

This research draws on two rounds of intensive fieldwork in 2009–2010 and 2019. Notably, during this period, the state’s priorities had increasingly shifted from financialisation to de-financialisation. This, however, exactly reflects how (de-)financialisation as statecraft is a specific spatial–temporal strategy. The first round was conducted when affordable housing schemes were first trialled and formulated. Interviewees included officials, developers and applicants. The second round was conducted when the whole system and relevant policies were well established. We conducted interviews with buyers in two SOH communities in Pudong, Shanghai, which were coded and referred to as HD and HR plus a serial number in the paper. We also interviewed several applicants who were not successful in the application. In total, 56 semi-structured interviews were conducted. Interviewees included officials and staff in multiple-level governments (24), private and state-owned developers (4), as well as SOH applicants (15) and buyers (13). In addition, we kept track of relevant policy changes by secondary data analysis of planning and policy documents as well as media reports and relevant academic research in Chinese.

Theoretical framework

Housing (de-)financialisation in political economy

Although housing has not been really granted an important role in political economy traditions, recent studies have rediscovered the centrality of housing to contemporary financialised capitalism (Aalbers and Christophers, 2014; Fernandez and Aalbers, 2016; Smart and Lee, 2003). In economic terms, housing as a commodity is special because it can act as an asset that can generate income and attract investment. By absorbing over-accumulated capital, housing became the object of financialisation (Fields, 2018). Focusing on its crucial role in the circulation of capital, the existing literature has analysed the increasing scale and rapid dispersal of mortgage debt in different regions and countries across the world (e.g., Bohle, 2018; Jordà et al., 2016; Kalman-Lamb, 2017; Kutz and Lenhardt, 2016; Pereira, 2017). Various innovative financial instruments and techniques have been created to turn housing into a liquid financial product. Mortgage securitisation is widely adopted as the key means for financialising homeownership (Gotham, 2009; Walks and Clifford, 2015). Recently, various corporate landlords – private equity firms, hedge funds, real estate investment trusts (REITs), and listed real estate firms – as well as private individuals, have entered the rental housing sector. The emerging models, such as ‘build-to-rent’ and ‘buy-to-let’, have provided new mechanisms for the financialisation of rental housing (Aalbers et al., 2019; Wijburg et al., 2018).

Meanwhile, the social-political aspect of housing financialisation and its implication for the welfare state are also critical. Since the post-war era, homeownership has been widely promoted for broader societal and political goals. Mass homeownership is presented as a model to deliver welfare benefits, which would ensure widespread access, equalise wealth distribution and provide economic security (Arundel and Ronald, 2021). In the Fordist era, homeownership was viewed as a ‘social contract’ between the state and individual households (Forrest and Hirayama, 2015; Ronald, 2008). As a key element for the expansion of the middle class, homeownership was central to social stability and political conservatism.

After the advent of neoliberal globalisation, these ideologies of homeownership have largely been sustained or even reinforced (Kohl, 2020). Since housing has been transformed into a financialised commodity, homeownership has become a means of asset-based welfare provision (Doling and Ronald, 2010). The state has cut funds for the provision of public housing and dismantled housing welfare systems. Low-income families’ access to homeownership was being supported through various financial instruments. This led to extraordinarily large and widespread mortgage debt and securitisation, a rapid rise in housing prices and, later, a global financial crisis (Schwartz, 2012). Under such circumstances, financialisation has been regarded as the market solution to the housing affordability problem (Forrest and Hirayama, 2015).

So far, there has been a vast literature on housing financialisation and its crucial role in capital accumulation. However, both the economic and social-political roles of housing matter. The tensions between economic growth and social welfare lie at the very heart of the contradictions inherent in financialised capitalism (Aalbers and Christophers, 2014; Fields, 2017b). De-financialisation would become an imperative for accumulation as long as the ‘affordable crisis’ was undermining the efficacy of financialisation as an urban strategy (Wetzstein, 2017). The emergence of a worldwide revival of affordable housing programmes the in post-crisis era challenges the understanding of financialisation as a monolithic and unstoppable process (Wetzstein, 2019; Wijburg, 2021b).

Variegated housing (de-)financialisation as city statecraft

While the structural tendencies of (de-)financialisation have been widely recognised in the existing literature, more recent studies have rediscovered the crucial role of state agency in shaping the process (Karwowski, 2019). Peck and Whiteside (2016: 239) recognised a new modality of financialised urban governance, where public policies are increasingly delivered through ‘financially mediated means and in conjunction with credit market actors, agencies, and intermediaries’. Pike et al. (2019) developed the concept of city statecraft as the art of city government and management of state affairs and relations with multiple actors to understand the state-finance nexus. Based on actor-oriented and process-based perspectives, it is argued that urban governance has evolved into mixed and mutated forms of financialism, entrepreneurialism, and managerialism (O’Brien and Pike, 2019).

City statecraft is particularly apparent in the governance of housing delivery. While finance has been brought within the state, the effectiveness of public policy could be undermined. For example, former public housing providers, which are asset-rich organisations, have become increasingly entangled in capital markets (Aalbers et al., 2017), but their social objectives, i.e., to provide affordable housing for low-income households, can be jeopardised by profit-seeking financial practices and risks (Wainwright and Manville, 2017). In response, the state has developed new managerial techniques to capture private profits for public policy objectives (Raco et al., 2022).

Comparative studies demonstrate a remarkable variation in state strategies to achieve (de-)financialisation across diverse contexts (Aalbers, 2017). Understanding housing (de-)financialisation as an element of city statecraft offers the basis for a conjunctural analysis, which situates different actors, relations, and mechanisms in specific geographical and temporal contexts (Pike et al., 2019). Statecraft is inherently path-dependent and uneven, featuring different attributes and taking different forms. The existing literature reveals variegated forms of housing (de-)financialisation under heterogeneous modes of urban governance.

On the one hand, pathways to housing financialisation differ. For example, many studies on Western societies focus on the neoliberal turn in urban governance and examine the enabling role of the state in mortgaged securitisation, the financialisation of social housing providers, and the penetration of capital into rental housing (Aalbers et al., 2017; Fields, 2018; Gotham, 2009). The degree of liberalisation is recognised as a key intuitional factor for different forms of residential capitalism (Fernandez and Aalbers, 2016; Schwartz and Seabrooke, 2008).

On the other hand, cities featuring different welfare, capitalist and planning regimes respond differently to the challenges of housing affordability in the post-crisis era. In Western societies, while social-democratic city governments tend to use their regulatory and financial capacities to directly intervene in housing delivery, liberal-market city governments are more like to depend on the private sector to solve the problems (Wijburg, 2021a). However, the underlying dynamics and outcomes are nevertheless very similar in neoliberal housing contexts.

Segmented housing (de-)financialisation in China

China’s recent transition from urban governance goes beyond varieties of neoliberalism. Although the market mechanism has been introduced and deployed across nearly every aspect of urban life, the state maintains its power and manages to effectively plan and control urban transformation. Wu (2018) used ‘state entrepreneurialism’ to distinguish the Chinese case from cases of neoliberal governance. The entrepreneurial activities of city governments can be driven by a wide range of purposes rather than merely for profit. Market instruments are strategically used as a means of governance to mobilise and coordinate multiple actors (Shen et al., 2020).

(De-)financialisation as a form of city statecraft in China, therefore, has its own logic beyond the financial market. As important as development (fazhan) is stability (wending). The slogan is known as ‘development is the ultimate truth (ying daoli); stability is the ultimate task (ying renwu)’. As the leading actor initiating financialisation, the state has to strike a balance between the imperatives of economic growth and social stability (Chen, 2013). On the one hand, state power is maintained within and through the financialisation processes. The state participates in financial markets and uses financial innovation to leverage assets and fund public investments (Wang, 2015). On the other hand, the state also actively manages the markets to achieve multiple goals (Petry, 2020). Therefore, financialisation and de-financialisation are not mutually exclusive. Instead, they are intertwined with each other, and both are pragmatic instruments of statecraft.

In the housing sector, similar to many countries in the West and in East Asia, housing financialisation in China is also associated with the shift to the asset-based welfare regime. The mass privatisation of public housing and the abolishment of welfare housing allocation in the 1990s made housing a commodity rather than a welfare good (Wang et al., 2012). However, tight control over both monetary policy and land supply, and the lack of any investment vehicle for ordinary households propelled the assetisation of housing and led to soaring prices (Wu et al., 2021). In response to the affordability crisis, which, in turn, has led to increasing social discontent, the state has relaunched public housing schemes (Zhou and Ronald, 2017a, 2017b). Driven by political incentives, local officials are committed to providing more affordable housing (Sun, 2020).

Notably, however, this does not simply indicate a counter-trend of financialisation. Instead, the statecraft can be characterised as segmented housing (de-)financialisation. In the name of affordable housing, multiple schemes targeting different segments of the population were trialled and implemented (Shi et al., 2016; Zhou and Ronald, 2017a, 2017b). The home security system encompasses a spectrum of (de-)financialisation, and segments of the population are entitled to differentiated access to financial resources and tools. The strategy is to leverage as many households’ financial capacity into the housing market as possible, meanwhile ensuring the fulfilment of the basic housing needs of low-income families. Therefore, different from Western societies where housing financialisation is driven by the extension of finance to low-income groups, given the potential economic and social risks, the Chinese state has taken a conservative approach to this issue.

Along the spectrum, first, commodity housing, as a financialised asset, is key to sustaining rapid economic growth in the post-crisis era (Wu et al., 2021). Second, Relocation and Resettlement Housing (RRH) accommodates the displaced residents of the shantytown renewal (penggai) projects, which is an integral part of the state’s strategies to refinance earlier debts through leveraging households’ monetary compensation into the housing market (He et al., 2020; Wu, 2021). Third, owner-occupied schemes such as Capped-Price Housing and SOH, aim to support lower- and middle-income groups’ home buying. Because those buying into these schemes mostly have to depend on subsidised loans, these schemes are essentially a means for encouraging the use of financial instruments for housing investment and consumption. Lastly, rental schemes represent the state’s efforts to de-financialise housing to secure the reproduction of labour and maintain social stability. Public rental housing (PRH) targets specific pools of labour, thus meeting the needs of local economic development (Wang and Li, 2019). In order to support economic upgrading, this scheme has been widely used by governments in coastal cities to attract young, educated talents. Cheap rental housing (CRH) fulfils the basic housing needs of the lowest-income groups. It reflects the state’s efforts to provide social protection for those at the bottom of society against the consequences of housing financialisation.

The revival of affordable housing in the post-crisis era

Central state: a crisis prevention strategy for housing financialisation

In order to deal with the potential threats to social and political stability posed by rapidly increasing housing prices, the central state started working on the housing affordability crisis as early as the mid-2000s. Since 2004, a series of policies aimed at cooling housing prices were launched. In 2007, the central state issued an important policy document: ‘Suggestions from the State Council on solving the housing difficulties of urban low-income households’ (State Council, 2007). However, the outbreak of the global financial crisis in 2008 changed the policy direction, as economic development became the top priority. Because housing had been recognised as an important booster of domestic consumption, the central state implemented various policies of tax and financial deregulation to revitalise housing markets (Wu et al., 2021).

Interestingly, however, at the same time, the state also decided to increase the provision of affordable housing, which represented the other side of the coin. It was believed that the provision of affordable housing was a prerequisite for social stability, and would be particularly important if the housing market were to be further revitalised (Xie, 2009). Because housing affordability varies among individual households, the home security system should encompass a wide range of support options to suit the needs of different social groups. While the shantytown renewal (penggai) and owner-occupied affordable housing would stimulate housing consumption, public and cheap rental housing schemes were essential to support low-income families with housing difficulties. Meanwhile, thoughtful consideration was also given to the potential impacts of these schemes on the housing market as well. As long as the target groups were those who could not afford to enter the property market on their own, they would not hit the market.

In practice, this national project was promoted by applying the campaign-style policy, which usually involves the extensive use of political tools to rapidly achieve a specific policy target (Sun, 2020). Since 2008, a set of supporting policies were launched to promote different types of affordable housing. In 2011, the central state formally formulated an ambitious plan to build 36 million units of affordable housing in five years and to cover 20 percent of urban households (State Council, 2011). A nationwide campaign was then initiated to ensure the fulfilment of the plan. The Ministry of Housing and Urban Rural Development assigned annual targets to provincial-level governments, which further assigned the targets to prefectural-level cities. Lower-level officials then signed contracts with their upper-level governments, and their performance evaluations would be based on the completion of the targets (Sun, 2020).

Shanghai municipality: muddling through the campaign

Shanghai, among other Chinese cities, had been leading in the market-oriented housing reform. In 1998, when the central state decided to abandon the welfare allocation of housing, the municipality immediately launched various reforms to build the housing market. In addition to removing in-kind housing allocation, it also established a series of new institutions for the monetisation of housing subsidies, including a one-off housing allowance, a housing-provident-fund loan, etc (Shanghai Municipal Government, 1999). In particular, this strategy was also applied to the provision of housing for low- and middle-income families. The ‘Economic and Comfortable Housing’ (ECH) programme, through which the municipality organised the construction of affordable housing for low- and middle-income families, was completely halted in 1999. Meanwhile, the ‘Cheap Rental Housing’ (CRH) programme was launched to relieve the housing difficulties of only the lowest-income families. However, the recipient families needed to rent houses through the housing market themselves, and then the government paid the rent subsidies directly to the landlords. This approach was criticised as ‘a Cheap Rental Housing programme without Cheap Rental Housing’ (Cui and Li, 2019). As a result of such radical housing marketisation, the city witnessed an unprecedented housing boom in a short period. The crisis of housing affordability generated increasing social discontent. However, given land and housing development had become an important source of local revenue, the municipal government had little incentive to spend on the provision of affordable housing.

Under such circumstances, the relaunch of affordable housing schemes was largely a political imperative at the request of the central government. Shanghai municipality responded quickly to the sudden assignment. An implementation plan was launched as early as the beginning of 2008, which clearly specified the types of housing, the annual quantitative targets, the modes of supply etc (Shanghai Municipal Government, 2008). The construction of new affordable housing started immediately, while detailed operational rules were developed and refined at the same time. By 2015, the end of the 12th five-year-plan period, a comprehensive affordable housing system, known as ‘four in one’, had been well established. It included two types of ownership housing and two types of rental housing: Relocation and Resettlement Housing (RRH) for households whose original houses were requisitioned for major urban (re)development projects; shared-ownership housing (SOH) for low- to middle-income households; public rental housing (PRH) for migrants with stable employment in Shanghai; and Cheap Rental Housing (CRH) for the poorest local households in housing difficulties.

The implementation turned out to be a strategy of ‘muddling through’, which is commonly used by local officials in China to reactively cope with demands and tasks sent from higher-level governments (Zhou et al., 2013). The planned quantity targets were not fully achieved. In total, 616,300 units of affordable housing were delivered but still comprised only 66.7% of the original plan (Shanghai Municipal Government, 2017). But the objectives set by the central state had been achieved. 69.4% of the delivered units were RRH, which was actually a tool supporting urban redevelopment. The proportions of SOH, PRH and CRH were merely 14.2%, 10.7% and 5.7% respectively. These schemes could hardly generate economic profits but instead were fiscal burdens on the municipality. However, they were not insignificant, as they demonstrated the municipality’s efforts to meet the requirements of the central state. The key was to boost the housing market and provide affordable housing at the same time; both strategies were political mandates at that time.

Local affordable housing policy, therefore, was largely an ad hoc, improvised strategy. Because national priorities could change over time, the municipal government constantly readjusted the goals under new circumstances. After this round of the campaign, the targeted number of affordable housing provisions decreased in the following years. During the 13th five-year-plan period (2016~2020), 448,300 units of newly built affordable housing were provided. For the 14th five-year-plan period (2021~2025), since the key task shifted from owner-occupied to rental markets, the government proposed to provide 200,000 dormitory beds and 220,000 affordable rental units, plus 230,000 units of SOH (Shanghai Municipal Government, 2021).

(De-)Financialising housing affordability: the shared-ownership housing scheme in Shanghai

The rationale for SOH

Among Shanghai’s multiple affordable housing schemes tailored to different types of families, SOH was designed as an owner-occupied type for low- to middle-income families. Under the scheme, buyers and the government can jointly purchase the ownership of an affordable housing property. It allows families to start by buying a stake with less money, therefore making it a more affordable route into home ownership. Although the policy idea was actually imported from the UK, the operational model was quite different. The government merely provided the properties. The buyers’ share is fixed at the initial proportion and cannot be increased afterwards. While share-ownership properties in the UK are always leasehold, families buying into SOH in Shanghai do not need to pay rent on the remaining portion belonging to the government. After a restriction period of 5 years, if the buyers want to realise their investment, the government has the pre-emptive right to buy back the property. Once the government waives this right, the buyers can sell the property on the market and then share the profits with the government. Or, they can purchase 100% of the property from the government and withdraw from the scheme, after which the property can be traded as commodity housing.

Essentially, the scheme is an integral part of the broader asset-based welfare regime. In one article in Jiefang Daily (the official newspaper of Shanghai municipality), the explanations for this policy made it clear that the goal of the scheme is to ease the recipients’ entry into the housing market and to reduce their dependency on the state. Since the increase in housing prices could easily exceed income growth in big cities like Shanghai, owner-occupied affordable housing would effectively help low- to middle-income families accumulate wealth through value preservation and appreciation. Meanwhile, it could also generate incentives for these families to engage in employment. It was expected that, alongside the increase in family income, they would eventually be able to withdraw from the scheme.

The scheme also embodied the financialised logic of the ‘shareholding state’, that is, the preservation and increase of the value of state-owned assets is an important consideration. According to the regulations of the central state, land for public housing should be guaranteed through administrative allocation, i.e., local governments have to contribute land for this purpose without charging land use fees. However, the scheme has partly become the municipality’s strategy for asset appreciation. As the then Municipal Party Secretary clearly pointed out, allocating land for the SOH scheme would not reduce land and other revenues; instead, it would turn immediate incomes into long-term returns later (Cui and Li, 2019: 59). Land assetisation was an important consideration in policy design and implementation.

Specifically, first, the trading prices of SOH are always closely linked to the market value of the properties rather than the revenue of the applicants. At the time of buying, the purchase price is calculated based on three components. The settlement price consists of land and construction costs, taxes, and small profits (no more than 3% of the cost). The benchmark price is a discounted price with reference to the average market transaction price of newly-built commodity housing constructed nearby in a certain period. The selling price for each unit then fluctuates up or down with regard to the benchmark price. The fluctuation range, which shall not exceed 10%, is determined according to the floor, location and orientation of the unit. After the restriction period ends, whether the buyers buy the government’s shares or sell their shares, the price will also be calculated based on the market value of nearby commodity housing at that time.

Second, the shares of a property between the government and the household are derived from their respective inputs, and the calculation is also based on the property’s market value. The inputs the government takes into account include the reduced land leasing fees, infrastructure investments, tax relief etc. Accordingly, the share one household can buy is calculated as the ratio of the benchmark price to the 10% discounted price of commodity housing in nearby neighbourhoods. Therefore, the greater the potential for price growth, the fewer shares households can buy.

Last but not least, the delivery of affordable housing is realised through building large-scale residential communities (Daju) in the peripheral areas, with an average population of around 100,000. On the one hand, with this strategy, the municipality aimed to minimise the loss of land revenue, because land in the central city can be sold for a better price. But on the other hand, by clustering affordable housing projects into large-scale residential settlements, it also hoped that rapid population growth and infrastructure construction would boost the price of land and housing in the suburbs. In particular, in contrast to other housing types, SOH estates are usually at better locations, such as close to metro stations or commercial facilities, to drive up the rates of appreciation.

The logic underlying the scheme, however, is more than financialisation. Holding shares is also an important instrument for the government to manage speculation. This is materialised in the form of a legal agreement between the government and home buyers. As a shared owner, the government set various restrictions on the usage and resale of the properties. The ultimate purpose was to prevent any appreciation of their value. In terms of usage, buyers were not allowed either to lend or rent the property out or to use it for non-residential or commercial purposes. However, non-compliant use, such as subletting, was not uncommon. Since 2016, in order to strengthen monitoring and regulate the shared owners’ use of their properties, the government assigned the tasks of daily management to ground-level communities. Grassroots organisations, such as residents’ committees, property management and resident volunteer teams, were mobilised to monitor the usage and occupancy of shared-ownership properties.

Regarding restrictions on resale, the government had been extremely meticulous in devising the regulations on speculation as well. In order to prevent high-frequency trading, selling is prohibited for the first five years after purchase. Moreover, no mortgages can be created over SOH except for the purpose of purchasing the property itself. Finally, after the restricted period, if the buyers choose to buy the property from the government, they must pay a lump sum. If the buyers decide to sell the property, the government has the right of first refusal. When the properties are sold on the open market, the total income is split strictly in proportion to the ownership shares. This is different from the previous economic and comfortable housing scheme, where buyers needed to pay only a fixed percentage of the difference between the market selling price and the original purchase price. As before, because of shared ownership, buyers cannot obtain additional value-added income from the government’s share of property rights.

Ultimately, the rationale of the municipality is a political one, that is, the SOH scheme as part of a social project is also a project to show a political achievement. This is most evident in the way SOH is priced. When a SOH project is completed, both the developer and a valuation company as a third party propose a selling price respectively, based on building cost, the housing market and policy requirements. However, the final decision rests with the government, which tends to prioritise the social and political dimensions of the scheme. As one official commented on the principles of pricing of SOH, For sure, we need to set the price based on the costs of land and construction. Nevertheless, there is still another very important factor, i.e., the absolute value of the price. (Given that the average house price in China was less than RMB 10,000), the price per square meter of SOH, which is a social housing scheme, in Shanghai must not exceed RMB 10,000. Otherwise, it would become a national joke. (Official, Shanghai Municipal Bureau of Housing Security and Management, 2009)

As a result, the financialisation of SOH can be limited and attenuated by such non-economic considerations by the municipality. The next section examines further the design and implementation of the scheme.

Financialisation and de-financialisation of SOH

Debt finance as a must-have

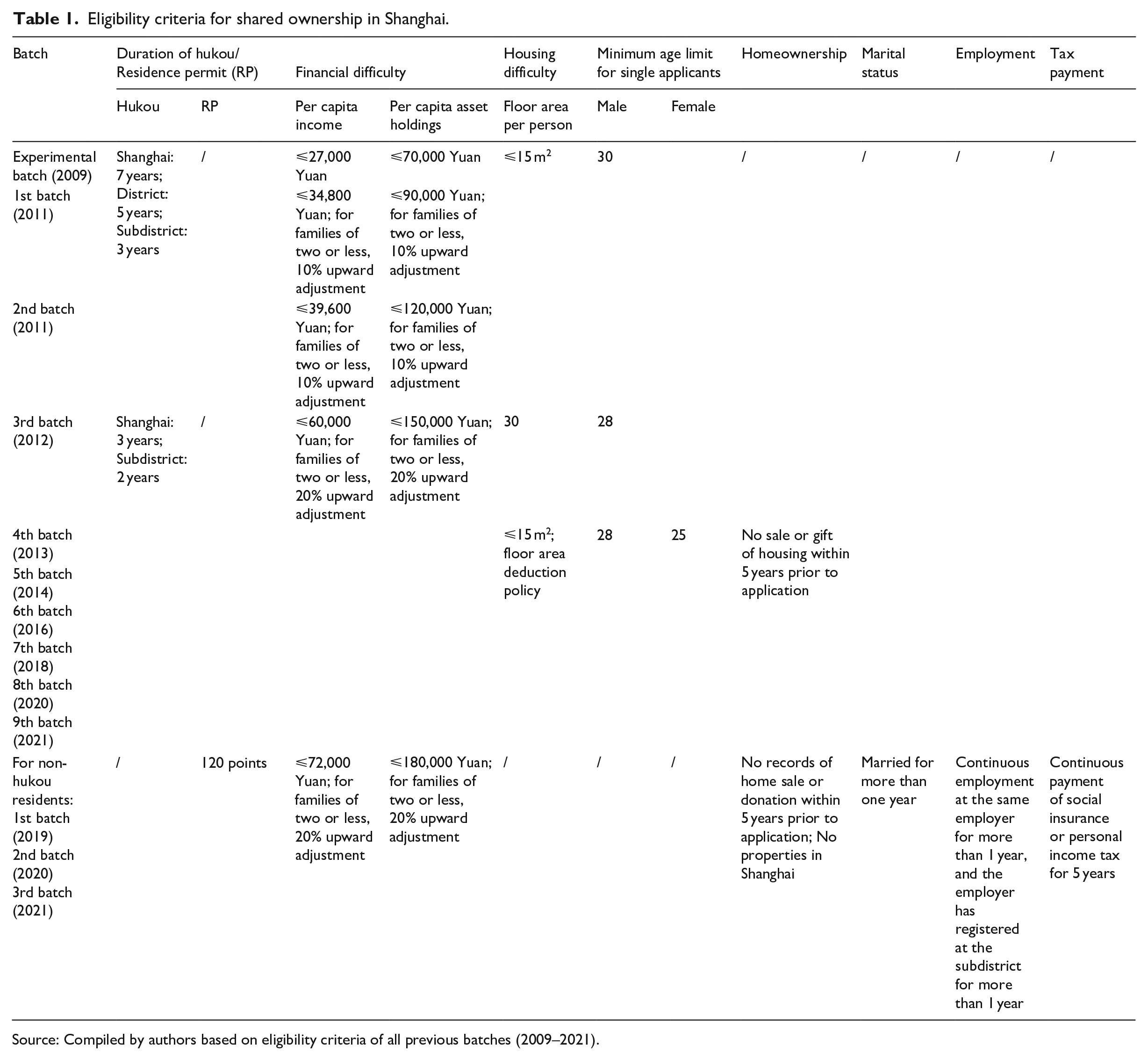

The SOH scheme aims to tackle the housing difficulties of low- and middle-income families by lowering the entry costs to homeownership. Accordingly, the eligibility criteria are set around two key aspects, i.e., housing condition, and income and assets. In addition, the buyers used to be required to have obtained local hukou for a certain number of years, although the coverage of the scheme was extended to non-hukou migrants in 2018. In order to destock the units built at the request of the central state, the thresholds have been gradually raised and relaxed to include more families (see Table 1). Initially, in 2009, the income threshold was RMB 27,600 per capita per annum, and the asset threshold was RMB 70,000 per capita. In 2014, the thresholds were raised to RMB 72,000 per capita per annum and RMB 180,000 per capita respectively. Although the standard for housing difficulty has been kept under 15 km2 per person, for large families, a certain amount of floor area can be deducted since 2013.

Eligibility criteria for shared ownership in Shanghai.

Source: Compiled by authors based on eligibility criteria of all previous batches (2009–2021).

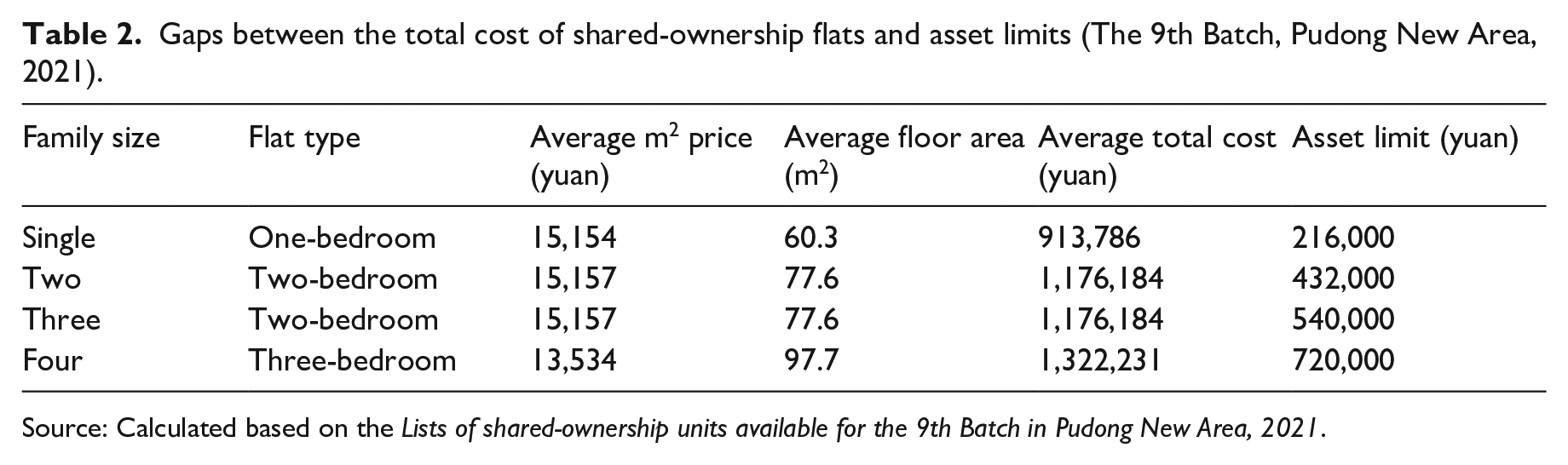

Nonetheless, however, because the price of SOH is closely linked to the market value of the properties rather than the affordability of low-income families, a paradox has emerged: those who can afford it don’t qualify, whereas those who do qualify can’t afford it. Although the threshold of income and assets has been greatly increased since the pilot batch in 2009, it remains impossible for applicant families to pay in full. Taking the latest batch released in Pudong New Area in 2021 as an example, there was a total of 1,095 units available for eligible applicants, including 317 one-bedroom flats for single-person households, 631 two-bedroom flats for two- and three-person households and 147 three-bedroom flats for households with more than four members. As Table 2 clearly indicates, there were huge differences between the total cost of the flat and the asset limit of the applicant families. For instance, the average square metre price for three-bedroom flats was around RMB 13,534, and the average total cost would be RMB1,322,231. In a scenario where the gap was smallest, if a four-person family wanted to apply for a two-bedroom flat, they would still be short of around RMB 602,231. Under such circumstances, for applicant families, debts have become inevitable.

Gaps between the total cost of shared-ownership flats and asset limits (The 9th Batch, Pudong New Area, 2021).

Source: Calculated based on the Lists of shared-ownership units available for the 9th Batch in Pudong New Area, 2021.

Financing the purchase of SOH

For many applicant families, difficulties in raising extra funds have become a major obstacle to obtaining SOH. One strategy is to buy a smaller flat than the one they are eligible for. Among our interviewees, two three-person families had purchased a one-bedroom type. Both had chosen to make a full lump sum payment with their savings because they did not want to struggle under debt stress or take financial risks (Interview, June 2019). For example, one interviewee bought a one-bedroom property using her parents’ savings. She explained as follows: My parents could just afford to buy a one-bedroom apartment here. The price was just right, a bit more than their savings. . . They did not want me to take out loans because they were quite prudent. . . But the living conditions have not changed significantly. I still have to live on the balcony in the living room, while my parents live in the bedroom. (Interview, Buyer HD2, June 2019)

However, many families, who did not want to compromise on size and living standards, gave up at the last minute due to the lack of money, even though they had gone through the entire application process. This was most prominent with regard to the pilot batch, in which the dealing rate was lower than 30% (Qiu, 2010).

In response to the dilemma, rather than lowering the price of SOH, the government soon launched preferential loan policies to provide financial support for these families. Households in China have two ways of obtaining a mortgage for house buying. One is commercial mortgages, which are loans borrowed from banks. However, for low- and middle-income families, it is not easy to obtain and afford commercial mortgages. As early as 2004, commercial banks were required to strictly scrutinise the borrower’s ability to repay the loan. Specifically, the borrower’s monthly repayments of home loans and all debts must not be more than 50% and 55% of his or her monthly income respectively.

1

Moreover, interest rates of commercial mortgages are usually a few basis points higher than the benchmark interest rate set by the central bank. Because commercial banks operate based on a commercial logic that privileges profitability and minimises risks, the municipality can hardly require them to lend to applicant families on favourable terms. There are no differences between mortgages for commodity housing and for SOH. As the then director of Housing Security Division of Shanghai Housing Security and Housing Administration explained, The government’s role is gatekeeping and distribution while making loans is a business of commercial banks, which are market players with their own calculation of risks. What the government could do is merely coordinate. (Qiu, 2010)

The other way to finance the purchase of SOH is through Housing Provident Fund (HPF) loans. HPF is a national compulsory saving and loan scheme. It mandates that both employees and employers contribute 5 to 12% of the employees’ salary on a monthly basis to the employees’ personal HPF accounts. 2 Funds in the accounts can be used for housing-related expenditures, including the purchase, construction or repair of self-occupied housing or the payment of rent. More importantly, HPF participants can apply for HPF loans granted by local Housing Provident Fund Management Centres, for which the down-payment requirements and interest rates are lower than for commercial mortgages. Because the management of HPF is under the municipality’s own responsibility, HPF loans became the key instrument for supporting the SOH scheme. By September 2021, a total of 77,800 (57.84%) households had used HPF loans for the purchase of SOH. The loan amount reached RMB 28.205 billion, accounting for 32.8% of the total amount of SOH transactions (Shanghai Municipal Housing and Urban-Rural Development Management Committee, 2021).

Interestingly, in terms of maximum loan amounts, down-payment requirements and interest loans, there is little difference between HPF loans for SOH and commodity housing, except that the buyers of SOH can get mortgages on the same terms as can first-time homebuyers, whether they already have a home or not. Instead, the most important particularity lies in the fact that joint mortgages with family members are offered to the buyers of SOH. Specifically, the borrowers’ spouses, parents and children can act as Gongtong Jiekuan Ren (literally, co-borrowers) of HPF loans to make mortgage repayments, even if their names are not added to the property deeds. In addition, the borrowers’ siblings can act as Buchong Huankuan Ren (literally, supplementary repayers), whose funds in their HPF accounts can be used to repay the debts.

On the one hand, the family mortgage fits very well in the Chinese family-based welfare regime, where family intra- and intergenerational mutual support is the pivot of welfare provision. On the other hand, mortgage eligibility essentially functions as a measure that assesses applicants’ earning capacity and prevents speculation. Intergenerational cooperation based on welfare eligibility and financial capability is quite common. Among our interviewees, except for one migrant family, all the local families with mortgages had managed to purchase SOH through intergenerational cooperation. While the ‘poor elderly’ were eligible for the SOH scheme, they needed to rely on their children, i.e., the ‘promising young’, to take out loans. Two families had to wait until their children had graduated from university and started working before being able to buy their new homes: We were very interested in this scheme since it was first launched. I viewed some houses at that time, and they were not very far. . . There were no SOH available in central locations afterwards. I was going to sell our original house and exchange it for a new home, even if we needed to borrow some extra money. However, I was not eligible for a mortgage. So, I had to wait until my daughter started working and could get a loan. (Interview, Buyer HR3, July 2019)

Nevertheless, many families that were beneficiaries did not use mortgages to purchase SOH. By the end of 2018, of the total number of families, only 63% had bought SOH using loans (Cui and Li, 2019). This was because many families took a conservative stance on borrowing. Importantly, the high risk of becoming unemployed after moving to SOH in the suburbs was a significant consideration. One interviewee explained the reasons for not borrowing from the banks: I certainly had considered taking out a loan at the time. It means that you need to have a stable job, and you cannot make any changes. If you quit or want to change jobs, it can be very stressful if you don’t get another one immediately. However, buying a shared ownership property meant that I could hardly stay in the same job and work in the central areas. In that case, I would have had to spend five hours commuting every day, which would be very exhausting. In addition, there were actually no concessionary mortgages granted by the government. (Interview, Buyer HD1, June 2019)

Another major cause, however, is that many families were not eligible for loans. This was either because their income could not meet the requirements of the mortgage, or because they were not covered by the HPF programme, as they were self-employed or worked in the informal sector.

For the families who did not use loans, there were usually two ways to raise funds, i.e., selling their original house and borrowing money from relatives. It was not uncommon that the applicant families had already been homeowners. Many had bought public housing from work units or from the government at low prices during housing privatisation. Despite their small size, the houses were in central locations and could be sold for a good price. For instance, one interviewee used to own a 41 m2, one-bedroom flat in the city centre and had run a tea house nearby. Due to not being eligible for a loan, he sold the flat for about RMB 1 million in 2013, which was sufficient for an 85 m2, three-bedroom shared-ownership property in the suburbs (Interview, Buyer HD5, June 2019).

Notably, for families that were either unable or unwilling to take out loans, their living conditions had not been improved substantially. For those that bought properties of a smaller size, than they were qualified to apply for, the total floor area of their new home was much the same as that of their original one (Interview, Buyer HD2 and Buyer HD4, June 2019). Some people who had sold their houses recognised that they had missed an opportunity to accumulate wealth. As one interviewee commented with regret, This is by no means a profitable business. Let me give an example. My original house in the city centre was 500,000 yuan. If I hadn’t sold it, the price must have increased, and all gains from the increase would have gone to me. The price of housing in that location would be even better than here, and the rate of increase would be much higher. Although the price of this property has gone up, only 70% of the growth is mine. The state will share 30% of the profits (Interview, Buyer HD1, June 2019).

In comparison, families who had kept their original houses benefited most, even if they needed to pay off their debts every month. For instance, one family we interviewed borrowed a total of RMB 400,000 as a mortgage for their HPF and purchased a two-bedroom property measuring 72 m2. Afterwards, they rented out their original 27 m2 flat for a monthly rental income of RMB 2,500. Given the monthly repayment was around RMB 4,000, it was not a burden for them at all. In addition, the house price of the original home had also increased significantly (Interview, Buyer HD8, June 2019).

Constraints on assetisation and the losing subjects of financialisation

While access to formal housing finance is the admission ticket to homeownership, the ability to cash in the appreciated value of the properties is key to achieving the SOH scheme’s goal of providing asset-based welfare. Ironically, however, because the government established various regulations to prevent speculation, the beneficiary families could hardly assetise their properties. Nominally, they could get the profits in two ways. One way would be to sell their shares to the government. However, the government actually does not have any incentive to buy the shares back. Although it would not be expensive, since most reclaimed properties would be used for public rental housing, the government would not want to buy them if there was not so much of a demand (Interview, officer of Pudong Housing Security and Management Bureau, July 2019).

The other way would be to sell the properties on the market. But there are numerous constraints as well. First, in order to become the outright owner of the property, one would first have to buy the remaining shares from the government at the market price. However, given that the rise in household incomes has been far less than the growth rate of housing prices, most families still would not be able to afford it. Taking the SOH community we studied as an example, in 2013, the unit price at the time of purchase was around RMB 8,000~10,000. By 2019, it had reached as high as more than RMB 33,000. Buyer HR2 bought a 78 m2 two-bedroom flat, which cost around RMB 440,000 for a 70% share. If the family were to buy the remaining shares from the government, it would cost more than RMB 770,000. Apparently, it would be almost impossible for them to earn that much money in five years, not to mention the fact that they would still have to pay the mortgage during this period. In the words of another interviewee who would have needed RMB 720,000 to buy the remaining shares, ‘Even if we don’t eat or drink, how many years will it take to save RMB 720,000?’ (Interview, Buyer HR3, June 2019). One interviewee also raised doubts about the reasonableness of referring to the price of commodity housing, Even if in the same location, you can hardly compare SOH with commodity housing. Housing quality, community environment, density, and who your neighbours are – none of these factors of the two is comparable. But they are all significant determinants of housing prices. (Interview, SOH Applicant, January 2022)

Second, the prohibition on the use of mortgages for buying the remaining shares is another critical issue. It is strictly stipulated that the money needs to be paid in cash in one lump sum. Different from the ‘staircasing’ process of the shared-ownership scheme in the UK, there is no way to apply for further advances or to remortgage. Moreover, the shared owners are not allowed to sell it first and then share the money with the government. They must pay off the debt before that. This is particularly a problem for the young who can afford loan repayments. As one interviewee complained, It might be understandable that the remaining shares are to be sold at the market price of nearby commodity housing. You get 70% of the appreciation in value and the other 30% should belong to the government. But without mortgages, families like us can hardly afford to buy the extra portion in cash in one lump sum, as long as housing prices keep rising. This is unreasonable. (Interview, Buyer HR2, June 2019)

However, from the perspective of the government, this was justified to ensure that the SOH scheme would not become a short-term investment channel.

Last but not least, a recently issued policy restricting the share owners’ purchase of other houses was a serious blow to many households. According to Shared Ownership Housing (SOH) Management Regulations (Municipal Government Decree [2016] No. 26), even after the restricted period, the share owners are not permitted to buy commodity housing unless they withdraw from the SOH scheme through either selling their shares or buying out the shares of the government. On the one hand, when applying for SOH, most families tended to list all the members, either to qualify, to obtain a bigger house, or to obtain a mortgage. With this new policy, it became difficult for the younger generation to buy properties of their own. Because purchasing a home is a prerequisite for marriage in Shanghai, this had given rise to much dissatisfaction: Without this clause, there would actually be no problem living here forever. . . Now, even if your child has found a good job, let’s say, with a monthly salary of RMB 50,000 or RMB 10,000, he/she has become richer, he/she will still not be eligible to buy another home. Do you think this is reasonable? (Interview, Buyer HD1, June 2019)

On the other hand, this restriction significantly increases the cost of buying a second home, meaning many families do not even consider it. Among our interviewees, one retired lady did not have any hope of buying out the government, although her daughter works in the financial industry and is paid quite well. We now think we will stay here until death. My daughter is thinking of buying a new home. We are getting old, and the hospital is not convenient here. But there’s no way to get the money. It would be too expensive if the state were to sell it based on market prices. . . And you must first buy out the 30% share before you can buy commodity housing. The government also charges extra tax for a second home. For ordinary people like us, this is not possible. . . There is a great difficulty, and we don’t have any confidence. (Interview, Buyer HR1, June 2019)

Another interviewee planned to buy a home in a good school district because his daughter would soon be starting school. He felt quite frustrated although he had already paid off the mortgage for this property. If you have no plans to buy a second home, you don’t have to buy out; you live in a 100% home with 70% of the money anyway. But from the beginning, we planned to buy another one; the educational resources here are poor. For this, we borrowed short-term loans. The monthly repayment was RMB 8,000, which was quite stressful. But this has become really difficult. (Interview, Buyer HR2, June 2019)

Because of these constraints on assetising SOH, some families regretted not buying full-ownership commodity housing. Essentially, they had missed an opportunity to cash in on their investments because they could not afford to. Some interviewees explained their regrets as follows: Housing prices have been rising all along, and so have the government’s shares. It means that later, you will need more and more money to buy out. If you have complete ownership, you feel very relieved when the prices rise. But now you have very mixed feelings. (Interview, Buyer HD1, June 2019) When I think back on it, I should have gritted my teeth and bought a home on the market. It would also have been a house (whose price would be rising), but I would own 100% of the product. I would be thankful for this. But speaking from the heart, it seems like I still got duped. At that time (five years ago), only an extra sum of RMB 30,000 was needed to buy a house with complete ownership like this. Now you would have to pay RMB 70,000. (Interview, Buyer HR1, June 2019)

Against the backdrop of the rapid increase in the price of housing, the interviewees also realised that the more shares they bought, the less stress they had now. Those who purchased SOH in central locations but owned fewer shares were thought to have lost more. But from a business point of view, there is no loss for the government. The shares one could buy were well-fixed. For properties in remote locations, a 30/70 split is applied. But for those in good locations, one could purchase only a 50% share, because the government wanted to hold more. You see, the government has its own calculations. (Interview, Buyer HD1, June 2019)

The negative effects of being trapped in a particular place might be passed on to younger generations. Many older people relied on the support of their children to buy the SOH, but the young could hardly afford to buy a home of their own. Most said that they would stay there until they died anyway, and their children would need to sort it out themselves (Interview, June 2019).

Conclusion

While there is an emergent literature on urban financialisation in China, the countervailing tendencies inherent in it have not been fully studied. Focusing on the resurgence of affordable housing policy and based on a case study of SOH in Shanghai, this paper examines the statecraft in housing (de-)financialisation in the post-crisis era in urban China. Rather than only or simply enabling housing financialisation (Miao, 2022; Wu et al., 2021), the state has carefully designed and managed a housing system for segmented housing (de-)financialisation. It aims to guarantee that those with financial resources and capacity are leveraged into the housing and financial markets, whereas those without are kept out but are supported by social security. Bridging the market and security, SOH in Shanghai as an affordable housing scheme has come to epitomise this statecraft. It draws low- to middle-income households into homeownership by providing subsidised loans, but at the same time, constraints are imposed on assetisation for risk management and speculation prevention.

This study also offers new insights into housing (de-)financialisation under state entrepreneurialism in the Chinese context. First, it is demonstrated that the financial logic is mixed with social and political ones. Certainly, massive projects of affordable housing, which would stimulate infrastructure investment and domestic consumption, have been initiated as an integral part of China’s post-crisis development. But in social terms, they are essential for social reproduction and stability, which is particularly important against the background of housing financialisation. In political terms, they are counted as an important political achievement by local officials. Housing financialisation and de-financialisation as a statecraft articulates and attends to multiple goals. The state prioritises one over the other for different population segments and at different times.

Second, the study also advances the literature by taking a closer look at the relations both within and beyond the state actors involved in housing (de-)financialisation. In contrast to earlier studies that highlighted different objects of multi-scalar states in urban financialisation, the central and local governments do share common interests. Both are struggling with balancing economic growth and social stability for political legitimacy. While the central state has designed and orchestrated housing (de-)financialisation, local governments seek to align themselves with national priorities by offering new housing schemes and innovative financial instruments, such as SOH and intergenerational family mortgages. Meanwhile, households have been selectively drawn into financialisation based on their financial capacity. However, given that homeownership has become essential for asset-based welfare, those low- and middle-income families excluded from financial services or constrained by financial regulations have missed the opportunity for assetisation. For buyers of SOH, they are not merely uncertain or unwilling subjects of financialisation (Fields, 2017a; Langley, 2007) but are also losing ones. Even though their living conditions have improved, as their home has increasingly become treated as a financial asset, partial ownership, as well as difficulties of assetisation, have trapped them in the scheme, making them regretful and frustrated.

More generally, the case of affordable housing schemes in China draws attention to the counter-trend to financialisation. Instead of an all-consuming and overwhelming process, financialisation is inherently intertwined with de-financialisation. As Wijburg (2021b) noted, following the logic of capital accumulation, de-financialising initiatives and practices are imperative in response to the inevitable problems of financialisation that undermine the regime itself. In the sphere of housing, the internal contradiction that the maximisation of profit margins might threaten the base of social reproduction is key to understanding the worldwide revival of housing affordability interventions in the post-crisis era (Wetzstein, 2019). In China, more recently, housing de-financialisation has gone even further beyond the provision of affordable housing. The state has enacted strict regulation and restriction policies on house buying and mortgages. Further work on de-financialisation and its consequences is needed to unpack the ongoing changes both in China and beyond.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of thisarticle: The work is supported by the National Natural Science Foundation of China [42171222]; the China National Social Science Fund [20BSH148]; as well as by Fudan University’s ‘Double First Class’ initiative key project ‘Sociological Theory and Method Innovation Platform for Social Transformation and Governance’.

Notes

Author biographies

Jie Shen is Professor at the School of Social Development and Public Policy, Fudan University. Her research focuses on urban and regional development in China, including suburbanization, segregation and urban governance.

Xiang Luo is a PhD Candidate at the School of Social Development and Public Policy, Fudan University and a senior engineer at Shanghai Pudong Planning and Design Institute. His research interests include planning, development and governance in urban China.

Zhe Sun is Assistant Professor at the Economic Sociology Department, Shanghai University of Finance and Economics. His research interests include housing market, gated-community and urban governance.