Abstract

Purpose

This study explores the features and consequences of heterogeneity among clients of the largest Islamic microfinance institution in Pakistan, identifying differences in business and household outcomes between sub-groups of borrowers.

Study Design

Our research is based on a longitudinal survey of 500 new clients of the institution conducted between 2015 and 2017, which we use to construct a unique dataset of entrepreneurs applying for interest-free microcredit loans. Evidence of significant heterogeneity was found among entrepreneurs at the time of the baseline survey.

Findings

We find differences in business and household outcomes between different types of entrepreneurs based on their level of need. In particular, ‘necessity’ entrepreneurs, who were poorer at the time of the baseline survey, tended to experience greater reductions in poverty levels over the study period, while female clients were found to have decreased their savings frequency more than male clients over the sample period.

Contributions

Our results challenge the conventional approach in microcredit programmes to treat the poor as a homogenous group to whom a rigid loan product is offered. We investigate this issue in the specific context of religious communities and institutions, which may further compound issues of client heterogeneity given a range of additional operational objectives. We also make a theoretical contribution in terms of applying agency theory and transaction cost economics in this novel context.

Implications

Our findings have several theoretical and managerial implications with respect to the application of the Shari'ah principles of Islamic Finance among a heterogenous group of entrepreneurs.

Introduction

Entrepreneurial credit, particularly microfinance, has become a widely adopted and respected development tool (Stewart et al., 2012). The growth in microfinance provision around the world has been paralleled by an increase in academic research studying how microfinance contributes to poverty reduction, and/or how to optimise the performance of microfinance institutions (MFIs) (e.g. Banerjee et al., 2015; Hermes & Lensink, 2011; Khandker, 2005). Within this line of research, heterogeneity among clients can affect the way in which they interact with the microfinance sector, and help explain variations in the business and household outcomes associated with the provision of microcredit. This is a particularly important issue given that entrepreneurial characteristics and aspirations may vary significantly between the developing and developed world (Raven & Le, 2015).

The literature addressing the impact of microfinance programmes has largely focused on comparisons between groups of borrowers and non-borrowers. However, a smaller number of studies have investigated differences between microcredit clients, notably with respect to gender and wealth levels prior to applying for loans (Haase, 2013, p. 13). Gender differences have been extensively explored from a range of perspectives, including access to microfinance (e.g. Agier & Szafarz, 2013; Guérin, 2011), the use to which microcredit loans are put (Garikipati, 2008; Goetz & Sen Gupta, 1996), as well as their impact (Hashemi et al., 1996; Kabeer, 2001). In terms of variations in client wealth, studies by Coleman (1999, 2006), Legovini (2002) and Hulme and Mosley (1996) find consistent evidence to suggest that the benefits associated with microcredit tend to be enjoyed by ‘better-off’ clients. Hulme and Mosley (1996, pp. 134–136) further argue that differences in entrepreneurial characteristics affect the likelihood of success in business ventures and suggest that these characteristics should be considered in the design of microfinance programmes. However, despite this evidence, many microcredit programmes still treat the poor as a homogenous group to whom a rigid loan product is offered. In addition, comparatively few studies investigate these issues in the context of religious communities and institutions, which may further compound issues of client heterogeneity given a range of additional operational objectives.

The study makes use of a unique longitudinal dataset of 500 clients of Akhuwat Islamic Microfinance (AIM), a partner of the UK-based crowdfunding platform Lendwithcare (LWC) since February 2013. AIM was created in 2001 with the mission to “alleviate poverty by empowering socially and economically marginalised segments of society through interest-free microfinance and in the process harnessing their entrepreneurial potential and enhancing their capacity through economic and social guidance” (Khan, Kustin, & Khan, 2017, p. 18). As an Islamic microfinance institution, AIM is based around a number of key Shari’ah principles that guide its operations. First, riba, which is commonly translated as interest or usury, is prohibited. Secondly, any transaction that involves excessive uncertainty (gharar) and risk, deceit or fraud is not allowed. Third, involvement in haram or proscribed activities, such as the production and sale of alcohol, pork, and illegal drugs, is prohibited. Finally, a financial transaction should be directly or indirectly linked to a real, tangible economic activity or asset, as opposed to financial speculation or debt (Khan, Kustin, & Khan, 2017). Following these principles, Muslims are encouraged by Islamic teachings to provide interest-free Qard Hasan loans to those with the greatest need, which is generally understood to more vulnerable sections of society. Among entrepreneurs, particularly vulnerable groups are likely to include poorer ‘necessity’ entrepreneurs, females and those lacking experience of formal credit markets (Lingappa & Rodrigues, 2023).

Given these guiding religious principles, entrepreneur heterogeneity is an important issue within Islamic microfinance. Islamic microfinance faces a number of particular challenges (Tisdell & Ahmad, 2018), including reaching the ‘poorest of the poor’, and satisfying religiously motivated entrepreneurs in Muslim countries whose financial needs are not met by conventional microfinance (Hassan, 2015; Zulkhibri, 2016). Client heterogeneity is theoretically interesting in this context because, despite Shari’ah principles pulling institutions towards the introduction of uniform standards, Islamic finance remains largely segmented and heterogenous (El-Gamal, 2002). More specifically, Islamic microfinance must design products that adhere to Shari’ah principles while simultaneously meeting diverse client needs. The issue has also been shown to have a significant impact on the preferences of Muslim borrowers (El Ebrashi et al., 2018), as well as and the performance of Islamic MFIs (Mobin et al., 2017). These preferences lead to strong arguments against ‘one size fits all’ policies typically associated with Islamic finance (Mertzanis, 2017). For example, while some clients might favour profit–loss sharing contracts (such as mudarabah or musharakah), others may prefer contracts with fixed fee structures.

Heterogeneity among Islamic microfinance clients also has theoretical implications in terms of agency theory and transaction cost economics. For example, if clients differ in their levels of social capital or moral commitment, it may be necessary to adjust screening mechanisms and levels of contract enforcement accordingly. Traditional microfinance studies, such as Armendáriz and Morduch (2010) have shown that variations in client characteristics can significantly affect repayment performance and risk profiles. In the Islamic context, where financing is based on ethical, social, and profit-sharing commitments, understanding heterogeneity is even more critical. Differences in risk aversion, financial sophistication, and commitment to Islamic ethical norms can affect not only individual loan performance but also the overall sustainability of the microfinance institution. Microfinance organisations may therefore also have to adopt more nuanced portfolio and risk management approaches than is typical in conventional frameworks. From a social impact perspective, Islamic microfinance aims not only at financial inclusion but also at poverty alleviation through ethical financing. A heterogeneous client base implies that the impact of microfinance can vary widely depending on client characteristics. Understanding these differences can help refine outreach strategies and tailor interventions to maximize both financial performance and social impact, thereby providing a rich theoretical framework to study how ethical values and economic behaviours intertwine within the setting of Islamic microfinance.

In light of the theoretical and managerial considerations outlined above, the research question addressed in this study is: To what extent do heterogenous entrepreneurs’ characteristics associate with variations in business and household outcomes between different groups of Islamic microfinance clients? Investigating this question offers important insights into the practical implications of client heterogeneity in Islamic microfinance markets, and can inform and help refine the decision-making process at the institutional level. The structure of this paper is as follows. Section 2 reviews the literature on microfinance, leading to the development of a number of hypotheses relating to variations in business and household outcomes between different entrepreneurial groupings. Section 3 provides details on the data and methodological approach. Section 4 explores the implications of the differences found between the selected groups of MFI clients and how these have translated into entrepreneurial and household outcomes. Section 4 also contains a set of alternate model specifications as a robustness check, which demonstrate that our main findings are robust to different modelling approaches and measurements of key variables. Section 5 concludes.

Microfinance, Entrepreneurship and Entrepreneurs

The concept of microfinance is not new. Originating in the informal funerary practices among stonemasons in Ancient Egypt, and the Vedic era in Indian history (Wilson, 2015), and extending through the saving and credit ‘tontines’ of Africa (Tello Rozas & Gauthier, 2012) into the relatively recent establishment of the Grameen Bank in 1983, microfinance has become synonymous with small-scale entrepreneurial development in emerging economies 1 . The barriers faced by low-income populations trying to access formal financial services, particularly credit, derive from the strong informational asymmetries that exist in conventional financial markets (Stiglitz & Weiss, 1981). In order to overcome these asymmetries, the microfinance movement has developed strategies and mechanisms to reach out to latent borrowers (e.g. relaxation of collateral requirements, group lending with joint liability, progressive lending), and tailored support services accordingly (Mersland & Strøm, 2011).

The underlying principle behind microfinance initiatives is that relaxation of credit constraints expedites the development of entrepreneurial ventures, increases productivity and profits, and delivers enhanced returns for the loan recipient. Access to microcredit is also expected to associate with growth in household consumption and/or savings. This improved economic situation, in turn, enhances the capability to invest further in the business via own funds or improved access to credit (Duvendack et al., 2011; Hermes & Lensink, 2011). From this perspective, entrepreneurship is perceived as a solution to poverty (Bruton et al., 2013). Behind this reasoning is the assumption that borrowers invest the money received in the businesses and these are successful, although this is not always the case (Duvendack et al., 2011).

The most vulnerable entrepreneurs that are often the most desirable recipients of Islamic microfinance are a heterogeneous group that are often differentiated on the basis of their wealth (poverty) and/or gender (Haase, 2013). Additionally, the prior experience of formal credit channels has been identified elsewhere in the microfinance literature as a significant factor affecting entrepreneurial performance (Bradley et al., 2012; Karlan & Morduch, 2010). These arguments are used as the basis of an investigation into whether such heterogeneity associate with variations in both business and household outcomes among a sample of Islamic microfinance clients. The rationale for this analysis is outlined below, leading to the development of formal research hypotheses.

Opportunity and Necessity Entrepreneurs

Lack of capital has been identified as a major constraint to business development among low-income populations in developing countries (McKenzie & Woodruff, 2008; Vial & Hanoteau, 2015). In this context, the promotion of microcredit programmes has been legitimised by a belief in the notion of ‘opportunity entrepreneurship’. This perspective sees the poor as natural entrepreneurs who can successfully establish and develop businesses, providing they have access to the financial means needed to exploit such entrepreneurial opportunities (Acs et al., 2012; Audretsch et al., 2008; Koellinger et al., 2007). Several authors argue, however, that many impoverished households are not entrepreneurs by choice, but are pushed into self-employment to survive - and are therefore better characterised as ‘necessity’ entrepreneurs (Brewer & Gibson, 2014; Kent & Dacin, 2013).

In the microfinance literature, opportunity and necessity entrepreneurs tend to be differentiated in terms of their poverty levels. Karnani (2009, p. 81) suggests that only a small proportion of the poor possess the abilities, vision, creativity and motivation needed to be ‘true’ entrepreneurs and be able to intentionally identify and take advantage of business opportunities. Wealthier microcredit clients are better placed to enter the business realm on their own, as opposed to on enforced terms (Acs et al., 2012) and they are less risk averse than poorer ‘necessity’ entrepreneurs (Vial & Hanoteau, 2015). They are, thus, more capable of seizing business opportunities and benefit more from access to business loans (Hulme & Mosley, 1996).

Empirical support for these arguments can be found in the work of Bradley et al. (2012), who established that firm performance was inversely correlated with poverty levels across a sample of 201 microcredit clients in Nairobi. In this study, borrowers are classified as either opportunity or necessity entrepreneurs based upon their wealth status when they take up their loan. This process leads to the development of the following hypotheses:

Entrepreneur Gender

Female entrepreneurs have been shown to declare lower microenterprise returns than male entrepreneurs in randomized control trials conducted in Sri Lanka (Mel et al., 2008) and Ghana (Fafchamps et al., 2011), as well as in research conducted in Nigeria by Adekunle (2011). Differences were attributed to a tendency for female-led businesses to be smaller in size; concentrated in less capital-intensive sectors where returns and growth opportunities are lower and competition is more intense (Bardasi et al., 2011; Bruhn, 2009; Coleman, 2007). They may also reflect women’s constrained spatial mobility, and/or lower educational levels, which inhibit their ability to deal with business administration (Guérin, 2011; Thorpe et al., 2014). Borghans et al. (2009) also found that female entrepreneurs tend to be more risk averse than men; a finding supported by the meta-analysis of Byrnes et al. (1999). The perceived value of savings is also expected to be higher for women, since they face more significant constraints in access to finance (Armendáriz & Morduch, 2010). Therefore, additional income generated by businesses financed through microcredit, at least partially, is expected to be applied in savings.

Heterogeneity among female entrepreneurs may also be a result of discriminatory practices against female entrepreneurs at both a societal and institutional level. These include women being precluded from owning land and other assets,

2

as well as financial institutions being less predisposed to lend to female-led businesses due to a perception they are less creditworthy (Agier & Szafarz, 2013; Carter et al., 2007; Deere et al., 2013). These gender-related arguments have been corroborated in microfinance studies conducted in Pakistan by Asim (2009) and Zulfiqar (2017). Therefore, our second hypothesis is:

Formal Credit Experience

Cultural and social norms (Guérin et al., 2012) as well as religious factors (Harper, 2017) can be influential in the decision to apply for a business loan. Harper (2017) identifies a potential incompatibility between microfinance and Islamic principles related to credit, notably the prohibition of riba (interest). As a result, many low-income Muslim entrepreneurs are unwilling to apply for loans through conventional interest-based microcredit programmes (Hassan, 2015). Similarly, in their research into microcredit provision in the rural areas of Morocco, Morvant-Roux et al. (2014, p. 306) found a lower propensity for debt among ‘conservative households’ (measured in terms of the head of household’s views on women’s rights and freedoms), as well as a fear of indebtedness dampening entrepreneurial demand for credit.

‘On the job’ experience has been shown to have a positive impact on the managerial capability of the entrepreneurs and their business performance (Adekunle, 2011; Bradley et al., 2012; Obeng et al., 2014). It helps entrepreneurs ask the right questions and build knowledge of business networks and markets (Basu & Goswami, 1999; Franck, 2012) as well as boosting entrepreneurs’ confidence. Similarly, if households become more accustomed to employing formal credit and previous experiences are perceived as positive, these experiences can help overcome fear and reluctance to apply for microcredit (Karlan & Morduch, 2010). In addition, entrepreneurs who have previously borrowed funds are also better placed to choose the best financial provider to satisfy their specific investment needs, and to deal with the loan management process. We therefore propose our third hypothesis, namely:

Data and Methods

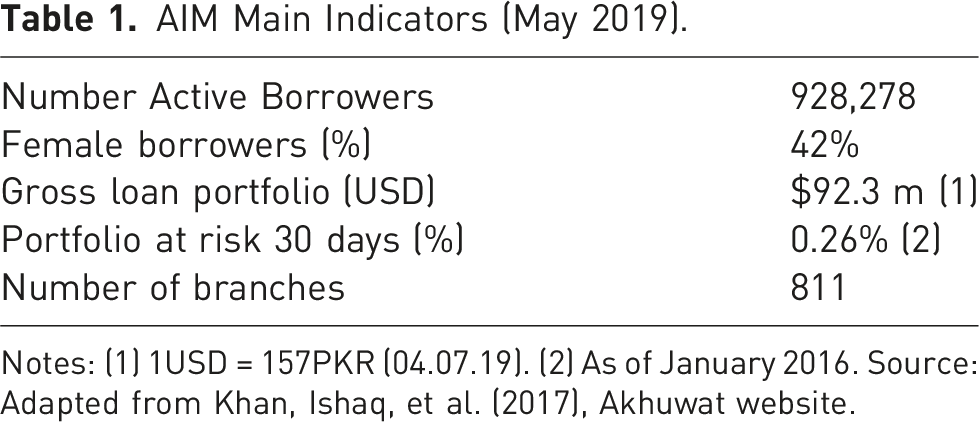

AIM Main Indicators (May 2019).

Notes: (1) 1USD = 157PKR (04.07.19). (2) As of January 2016. Source: Adapted from Khan, Ishaq, et al. (2017), Akhuwat website.

Akhuwat’s main product is Qard Hasan loans, accounting for around 80% of all loans provided. In order to cover its operational costs, Akhuwat generates income from a variety of sources. As well as the non-refundable application fee associated with all Qard Hasan loans, the grant funding that Akhuwat receives from various institutional donors has a proportion specifically assigned for operational costs. Furthermore, the organisation also receives sadaqah (voluntary charity) donations from well-wishers (including many from the Pakistani diaspora abroad), returns from bank deposits, and even the sale of books and other items. In recent years, Akhuwat has also diversified its products to include other Shari’ah compliant finance financing mechanisms such as Ijarah (leasing), Musharaka (profit and loss sharing), Murabaha (cost-plus contracts), and Bai Salam (advance payment for goods). These financing arrangements are generally for greater amounts than Qard Hasan loans and cover all their own operational costs. A unique feature of Akhuwat is that borrowers contribute voluntarily to ‘community donation programme’ boxes which are placed in all branch offices. However, income from this source is not used to cover operational costs, instead it is only used to fund further loans to low-income microenterprises as well as supporting Akhuwat’s non-microfinance activities related to providing education and basic health services. Borrower donations are motivated both by faith and a of sense of solidarity with other poor people (Khan et al., 2017).

The present study, undertaken in conjunction with Lendwithcare, is based on a longitudinal research design, which aimed to assess the changes in the business and household characteristics of Pakistani entrepreneurs during the period between taking and repaying their first loan from AIM. Three AIM branches in Pakistan’s second most populous city of Lahore (specifically in the areas of Badami Bagh, Kot Khawaja Saeed and Kahna Nou) and one in the smaller city of Kasur (all located in Punjab province) were selected for inclusion in the study. The sample population was made up of 500 entrepreneurs who had successfully applied for a first loan during the period of the first wave of the survey (April to June 2015). The average loan amount and duration were PKR 20,000 3 (≈ 130USD at the time) and 14 months, respectively. Sample selection was determined by logistical and security conditions in the country, and the cost of accessing a representative sample of borrowers. The same 500 microcredit clients were invited to participate in the second wave of the survey in 2017, with 447 agreeing to participate.

Badami Bagh Kot Khwaja Saeed and Kahna Nau are areas within the city of Lahore, while the city of Kasur is located some 33 miles to the south. There are no significant differences in the religiosity of the areas with the vast majority of inhabitants being Sunni Muslims with very small pockets of Shia Muslims and Roman Catholic Christians. Badami Bagh and Kot Khawaja Saeed are densely populated urban areas characterised by their proximity to large wholesale markets. As a result, these areas have a wide range of commerce and trade related enterprises, as well as workshops, craft (particularly related to embroidery and weaving), and manufacturing businesses. In contrast, Kahna Nau is a peri-urban area located on the outskirts of Lahore and as a result has a mix of commerce and agricultural activities. Kasur is also an urban area, although less densely populated than Badami Bagh and Kot Khawaja Saeed, and is surrounded by rural areas. It has similar businesses to the aforementioned two areas in Lahore, but it is also renowned as a centre for footwear manufacturing. In all areas, it is common for businesses, particularly those managed by women, to be home-based.

The interviews were conducted by independent enumerators and responses were elicited in two areas. During the interviews, the wealth status of the respondent during both waves of the study was first ascertained using the Poverty Probability Index (PPI); a country-specific poverty measurement tool based on responses to ten questions relating to household characteristics and asset ownership. The answer to each question is given a score based on the country scorecard and the sum of these scores gives the PPI score for that particular household, ranging between 0 and 100. PPI scores can then be used to identify a household’s likelihood of falling below a selected income poverty line. For example, in the case of Pakistan, a PPI score of 50 means that the likelihood of the household being below the $2.50/day international poverty line is 72.8% (Schreiner, 2010). In this study, the PPI score corresponding to more than 50% likelihood of the household income being below the poverty line was used as a threshold to classify clients as necessity (scores below or equal to 64) or opportunity (scores above 64) entrepreneurs. 4

Second, a questionnaire devised by the research team was applied in order to capture information relating to socio-demographic status (age, gender, marital status, education level, household size, etc.), business characteristics (type of activity, length of operation, revenue variation), financial practices (business funding sources, loan purpose, etc.), as well as exposure to external shocks such as chronic health conditions 5 . Finally, gender and formal credit experience were captured through binary variables, taking the value of 1 if the respondent was female, or had previously funded the business with loans from a formal source respectively.

Results and Discussion

Baseline Entrepreneur Heterogeneity

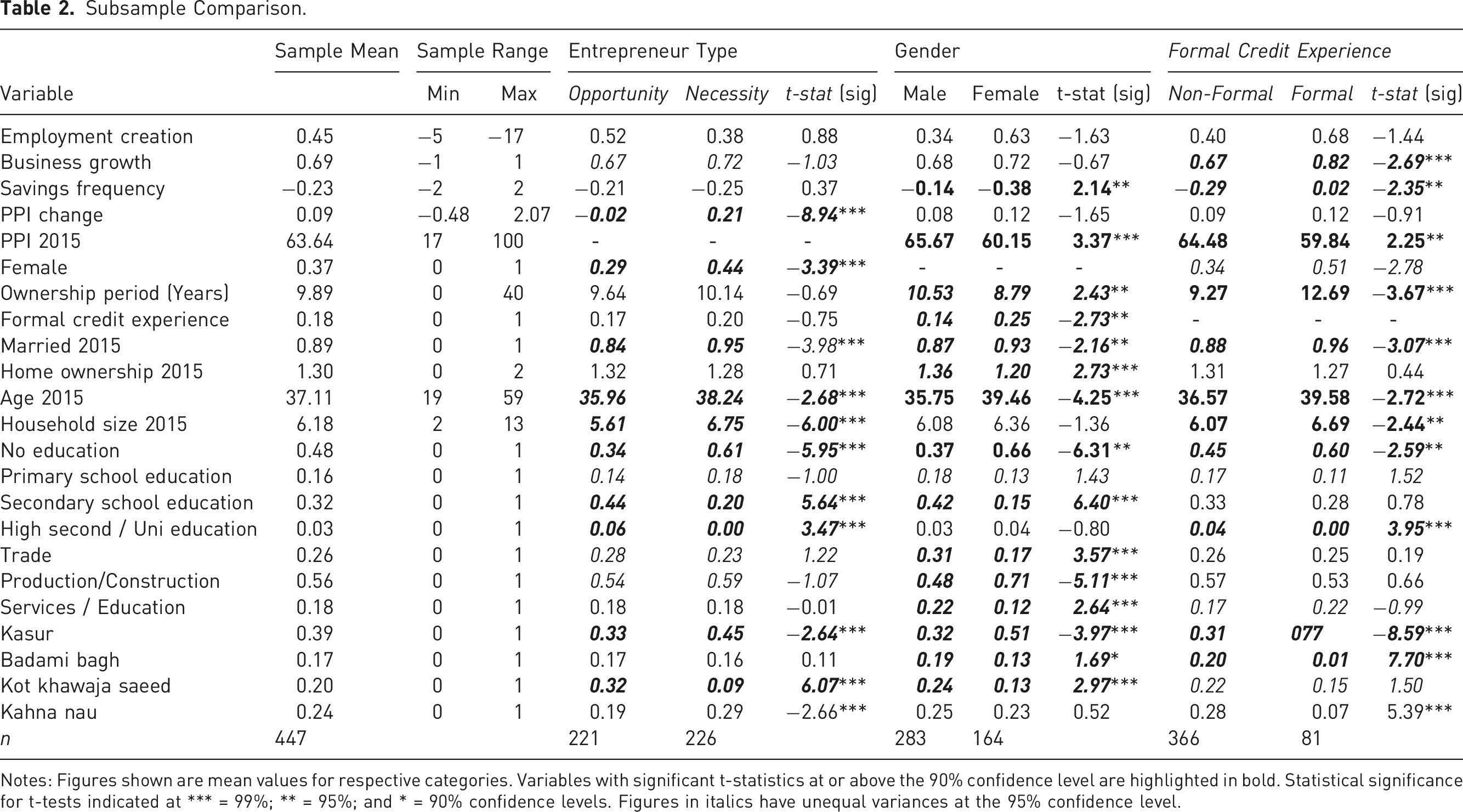

Subsample Comparison.

Notes: Figures shown are mean values for respective categories. Variables with significant t-statistics at or above the 90% confidence level are highlighted in bold. Statistical significance for t-tests indicated at *** = 99%; ** = 95%; and * = 90% confidence levels. Figures in italics have unequal variances at the 95% confidence level.

In particular, the results show a number of significant differences between male and female entrepreneurs, which corroborates results from previous studies conducted in Pakistan (Asim, 2009; Zulfiqar, 2017). On average, female clients tended to be poorer (average PPI score in 2015 was 5 points lower), older, less educated (66% were illiterate compared to 37% of males) and less likely to own their house. They also typically had less business ownership experience (8.8 compared with 10.5 years). Although only a quarter of female clients reported previous formal credit experience, this was still significantly higher than for males (14%). This higher propensity of women to use formal credit can be explained by greater difficulties in accessing other sources of finance, such as savings or borrowing from family and friends.

The results also indicate the existence of gender differences regarding personal income derived from the business. Female entrepreneurs earned, on average, significantly less than males, similar to the findings of other studies (e.g. Mel et al., 2008; Zulfiqar, 2017). These variations in business performance for female entrepreneurs are likely to be the result of lower levels of literacy and management experience (Coleman, 2007; Guérin, 2011) as well as differences associated with the type of activity. More specifically, female entrepreneurs in these regions typically have responsibility for performing household duties and may face associated restrictions on their mobility as a result, meaning that many such businesses will typically be home based. However, as female entrepreneurs become older, they tend to relegate household duties to daughters and particularly daughters-in-law as they live in extended households, leaving more time to engage in business activities.

Regarding the differences between ‘opportunity’ and ‘necessity’ entrepreneurs at baseline, Table 2 shows that these differences were observed mainly in respect to sociodemographic characteristics (gender, age, marital status, educational level and household size). Statistical differences between the sub-groups suggest that necessity entrepreneurs are more likely to be female, married and older than the clients identified as opportunity entrepreneurs. They also tend to live in larger households (6.8 members vs. 5.6) and have lower levels of education (61% were illiterate). However, no significant differences were observed for business indicators between the two groups, specifically ownership period and type of activity. The analysis of the differences between microcredit clients with and without formal credit experience is comparatively more nuanced. Entrepreneurs with formal credit experience were more likely to be older, less educated, poorer (lower average PPI score), and living in larger households. They were also more likely to be more experienced as business owners, and to have reported growing business revenues over the period.

Finally, the data presented in Table 2 highlights two variables for which statistically significant differences between the defined sub-groups were found for all three analyses. The first of these variables is age, with the results conforming to expectations – necessity entrepreneurs, females, and those clients with formal credit experience were typically older than their equivalent counterparts. The second common difference related to entrepreneurs based in the city of Kasur. Despite all branches being located in an urban context and the city not being far from Lahore, clients based in Kasur were more likely to be female and classified as necessity entrepreneurs than those from the other branches. While we can only speculate on the reason for this trend, one possibility is the (relatively uncommon) presence of two female loan officers in the branch office in Kasur city. Clients may feel more comfortable approaching them and they may feel more comfortable dealing with female clients. Kasur-based clients were also more likely to have had access to formal credit prior to applying for the microcredit loan. These results imply that location should not be looked upon uniquely from the common rural/urban perspective, but should also take into account differences in socio-economic characteristics and MFI targeting strategies between urban areas.

Variations in Business Outcomes

In order to test hypotheses relating to business outcomes (H1a, H2a, H3a), we measure two variables representing expected outcomes of microcredit programmes: business growth and employment creation (as per Armendáriz & Morduch, 2010). The ‘business growth’ variable was constructed on the basis of self-reported changes in sales revenue experienced by the respondent’s business over the period. This could be described as either ‘growing’ to which a value of ‘+1’ was assigned, ‘stable’ (0) or ‘decreasing’ (−1). The ‘employment creation’ variable corresponded to the net creation of jobs, paid or unpaid, during the period (a part-time job was accounted as 0.5 of a full-time position). The results presented in Table 2 (above) suggest that business growth associated with both business ownership period and prior access to formal credit, with the differences between the respective subgroups being found to be statistically significant at the 99% confidence level.

Correlation Coefficients.

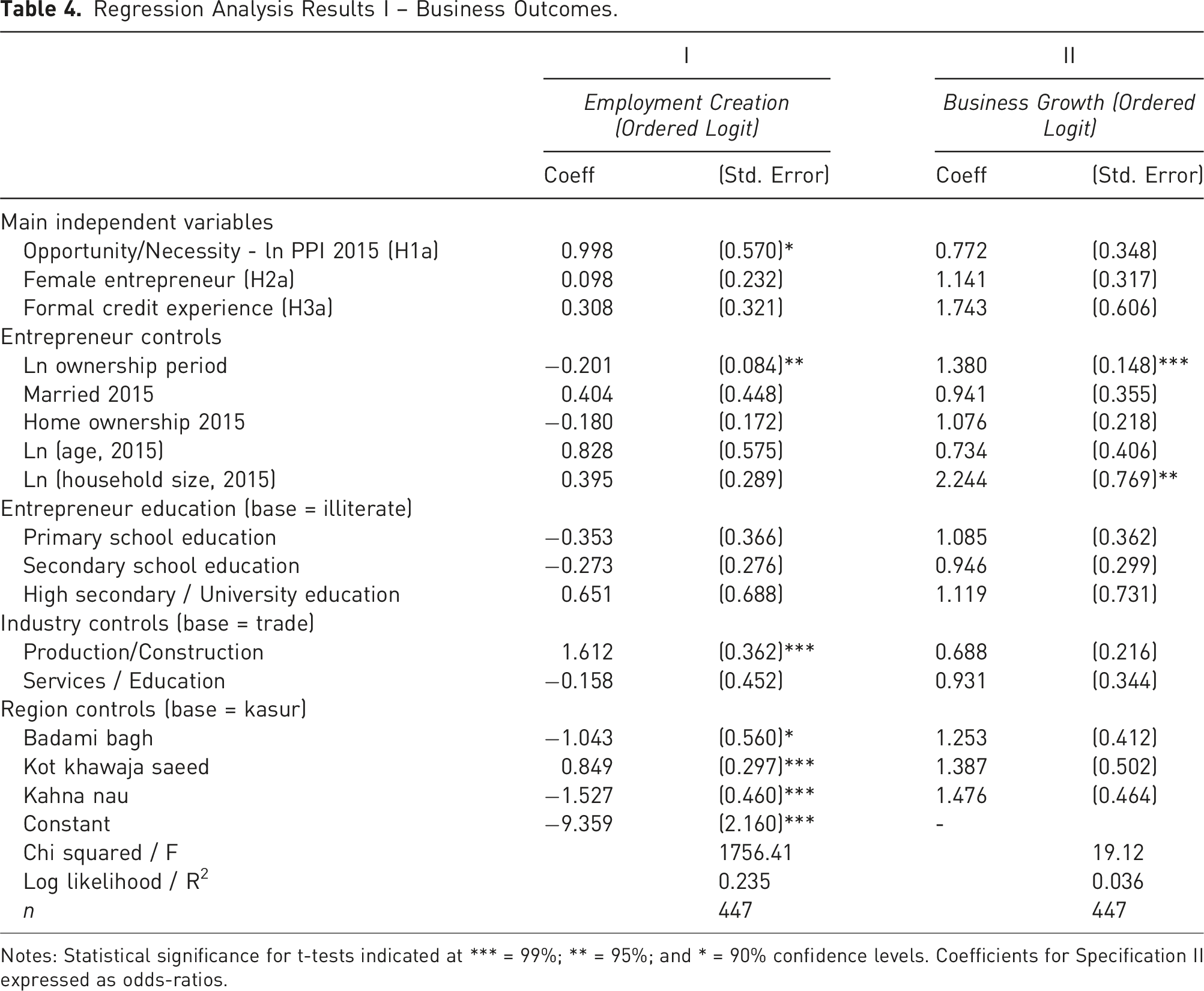

Regression Analysis Results I – Business Outcomes.

Notes: Statistical significance for t-tests indicated at *** = 99%; ** = 95%; and * = 90% confidence levels. Coefficients for Specification II expressed as odds-ratios.

Specification II is an ordered logit regression capturing whether business growth has declined, remained the same or increased over the period. Coefficients are reported as odds-ratios. These results do not lend support to hypotheses H1a, H2a or H3a. Overall, the data available and the model specifications did find that entrepreneur characteristics and heterogeneity to be significantly associated with variations in business growth, which may instead be related to wider economic, social and cultural environmental factors. It is particularly noteworthy that the results do not show any evidence of variation in business growth according to the gender of the entrepreneur, implying that female-led businesses do not necessarily grow less than male-led businesses. It is possible that this finding is the result of lower average/mean business growth and greater variance we observe for female entrepreneurs compared with males in our sample, which may end up ‘cancelling out’ the gender effect in terms of our regression coefficient estimates. Whatever the reason, the result challenges findings from the aforementioned studies in Sri Lanka, Ghana, and Nigeria and implies a potential influence of religion on business performance. In this context, it would be useful for future studies to explore the role of the family approach followed by AIM in compliance with Islamic principles, particularly how other family members are involved in the loan process and the management of the business.

Variations in Household Outcomes

The analysis now turns to exploring associations between entrepreneur characteristics and variations in household outcomes. First, the variation of household savings frequency is calculated on the basis of the self-reported savings frequencies captured in both surveys, which were described as ‘never’ (0), ‘occasionally’ (1) or ‘regularly’ (2). The variation between these categories resulted in five potential scenarios, which capture both the amplitude and the direction of the change (e.g. an entrepreneur who saved regularly in 2015 and reported never saving in 2017 was assigned a value of ‘-2’, whereas an entrepreneur who saved occasionally at baseline and declared saving regularly in 2017 is assigned a value of ‘+1’.

Returning back to Table 2, the results of the T-tests demonstrate that savings frequency tended to decrease after being granted the microcredit loan. Although empirical evidence on savings variation has been mixed, the findings of this study contradict theoretical expectations outlined in the model of Duvendack et al. (2011), whereby savings are suggested to typically increase following the provision of loans. In addition, it should be noted that the largest decrease in savings frequency was observed among female entrepreneurs. Despite the percentage of women saving regularly in 2017 remaining higher than men (52% and 48%, respectively), the gap between them substantially declined compared with 2015, where the percentages were 62% and 52% respectively. The analysis also explores associations between entrepreneur characteristics and poverty status on the basis of variations in PPI scores observed over the course of the sample period.

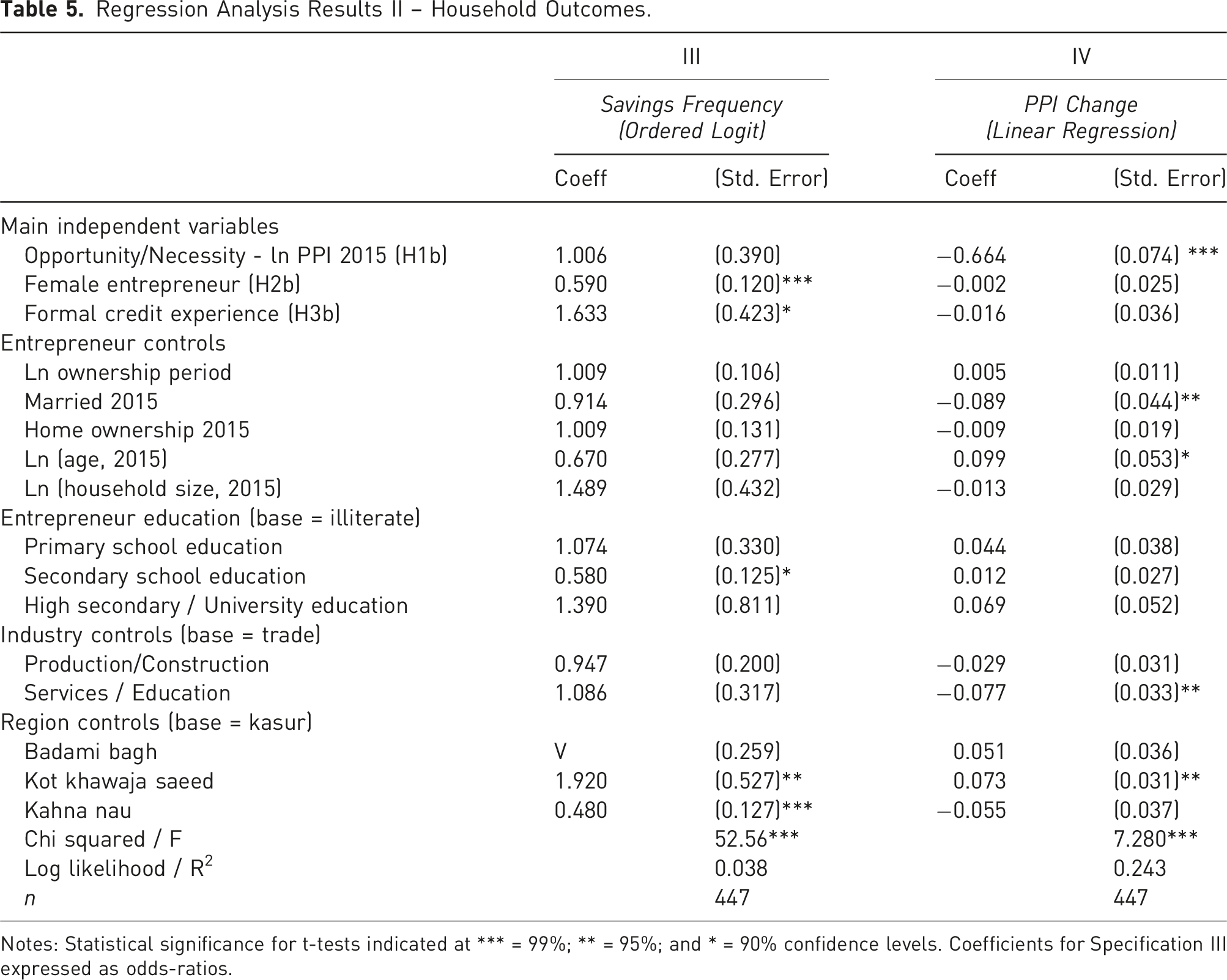

Regression Analysis Results II – Household Outcomes.

Notes: Statistical significance for t-tests indicated at *** = 99%; ** = 95%; and * = 90% confidence levels. Coefficients for Specification III expressed as odds-ratios.

The estimates for Specification III show no statistically significant relationship between variation in the frequency of saving and opportunity/necessity entrepreneurs and therefore do not support hypothesis H1b. The results do show that the odds ratio of being in a higher savings category decreased by around 0.41 for female entrepreneurs compared with males; in other words, female entrepreneurs were less likely to have increased savings activity over time compared with male entrepreneurs, similarly to the results of the t-tests. One potential reason for these findings could be that business returns were not as high as expected, implying a reduced capacity to save regularly. However, as average business and household incomes increased over the period, a more plausible explanation is that the additional income was preferentially used for other purposes, including consumption and voluntary donations to AIM.

As part of its religious culture, the MFI encourages its clients to become donors reciprocating the support they have received through the access to the interest-free loan. Donations, similarly to savings (Morduch & Hailey, 2002), can be seen as social insurance, giving the clients the sense of being part of a community that helps each other in case of need (Khan, Kustin, & Khan, 2017). This seems to be widely accepted within the sample of entrepreneurs in this study, with 93% of all participants reporting donating during the previous 12 months. Female clients donated more frequently as 74% declared regularly donating, compared with 61% of male clients. However, although made regularly, these donations tend to be rather small (20 PKR ≈ 0.13USD according to information from an AIM representative) and most likely not related to the decisions on savings. It would be, thus, interesting to collect data on the amounts of savings and donations to confirm that there is no substitution effect at this level and explore other factors affecting savings.

Finally, the results for Specification IV indicate that one of the most powerful predictors of a change in PPI score over the sample period is the variation between opportunity and necessity entrepreneurs. More specifically, a 1% increase in baseline PPI score was shown to associate with a 0.66-unit reduction in PPI over the sample period. The negative coefficient implies that the entrepreneurs who were poorer at baseline were the ones more likely to show an improvement in the poverty level over time. In the same way as the result of the t-tests for the ‘opportunity’ versus ‘necessity’ entrepreneurs, it suggests that the poorest clients have benefited relatively more than better-off clients over the sample period, which supports hypothesis H1b. Conversely, gender is not shown to associate with a statistically significant variation in PPI score over the sample period, which does not support hypothesis H2b. In common with earlier results regarding variations in business growth by gender, this finding calls for further analysis of the family loan approach and its implications in terms of business and household outcomes. Specification III also shows (somewhat weaker) appositive association between savings frequency and formal credit experience, therefore offering some support for hypothesis H3b.

Conclusion

This study examines differences in characteristics as well as business and household outcomes among a sample of Islamic microfinance clients. The results empirically support the presence of significant differences among clients with respect to three key characteristics; namely opportunity/necessity entrepreneurship, gender and previous formal credit experience. Differences were found to be stronger between male and female entrepreneurs, a finding not exclusive to Islamic contexts. Differences were also observed between necessity and opportunity entrepreneurs with respect to their socio-demographic characteristics, as the former are more likely to be women. The findings of the study demonstrate that among entrepreneur characteristics, only opportunity entrepreneurship associates positively with business growth. Conversely, neither gender nor credit experience were associated with significant variations in business growth. The former result is particularly important, as it challenges the argument that female-led businesses have lower growth potential and calls for further analysis of the role of AIM’s family approach in the provision of loans.

By contrast, this study does find evidence of statistically significant variations in household outcomes among specific groups of entrepreneurs. In particular, the results show a reduction in household savings frequency over the course of the sample period. Changes in poverty levels over the course of the sample period have also differ according to entrepreneur characteristics. Most notably, the results demonstrate a greater increase in PPI (i.e., a larger reduction in poverty level) among those with lower PPI scores at the time of the baseline survey. This result suggests that microfinance loans in this context benefit the households of the poorest entrepreneurs to a greater extent than the wealthiest. Alternate results estimated using logit models are consistent with all of the relationships outlined above, indicating that our main findings are robust to different modelling approaches. However, it should be noted that a small number of other findings not outlined above appear to be sensitive to the ways in which the dependent variables are measured.

The results of this research share some commonalities with previous studies on conventional microfinance (e.g. related to business experience). However, they also draw attention to specificities of the Islamic microfinance model that calls for further research; namely the family loans approach and the donations programme. In particular, our study finds mixed evidence in relation to the effectiveness of microfinance loans based on entrepreneur characteristics. In particular, opportunity entrepreneurs (lower levels of poverty at baseline) are more likely to experience improved business outcomes as a result of their loans, while necessity entrepreneurs (higher levels of poverty at baseline) were more likely to experience improved household outcomes. In relation to gender, our results show that female entrepreneurs experienced similar business outcomes to males, but actually ended up saving less.

These results highlight the complexity inherent in meeting Islamic microfinance objectives among a diverse and heterogenous client groups, particularly in terms of meeting the imperative to help those in the greatest need. Acknowledging client heterogeneity and understanding its association with variations in business and household outcomes can therefore be crucial to identify differences between Islamic and conventional microcredit programmes and maximising the outcomes of microfinance programmes implemented at a micro level.

Footnotes

Acknowledgements

This research was conducted in collaboration with Lendwithcare, a crowdfunding platform initiative of CARE International UK, along with their partner microfinance institution Akhuwat Islamic Microfinance (AIM) based in Pakistan. The authors are grateful to Dr. Amjad Saqib, Executive Director of AIM for enabling this research the research, as well as to Shahzad Akram and Shakeel Ishaq for their valuable comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.