Abstract

Never before in living memory has economic destruction been so severe as it has been caused by the COVID-19 pandemic. The pandemic has struck at a time when the economy has already been slowing due to structural problems. Therefore, hastening the recovery process and accelerating the pace of economic growth requires the government not only to provide substantial stimulus but also to implement structural reforms. The stimulus provided so far has been mainly by the RBI on the supply side in terms of reducing interest rate, augmenting augment liquidity, restructuring loans to stressed sectors, moratorium on repayment of loans to severely impacted businesses and regulatory forbearance. The fiscal stimulus on the demand side has not been significant and amounted to just about 1.5 percent to 2 percent of GDP. The sharp contraction of the economy by 15.7 percent in the first half has substantially eroded revenue collections requiring both central and state governments to sharply reduce both government consumption and investment expenditures. Faster recovery in the second half of the year will crucially depend upon heavy lifting by the governments which requires them to increase consumption expenditures, transfers as well as capital expenditure by scaling up borrowing as well as monetizing the assets. The aggregate fiscal deficit as well as outstanding debt are likely to show a sharp increase which will raise questions of sustainability. The government has initiated a number of reforms, particularly to infuse flexibility to land and labour markets, reform regulatory systems in education and healthcare, and has made additional borrowing to the states conditional on undertaking power sector reforms, property tax reforms and improving the ease of doing business. However, implementation of these reforms holds the key. There is a need to urgently address problems of the financial sector. Reforms in sectors such as police and judiciary too are overdue to protect the life and property of people and enforce contracts.

Introduction

This article analyses the impact of coronavirus pandemic on public finances of the union and state governments in India. The virus struck the economy which was to cause serious disruption in economic activity and income and employment levels. Although Indian economy has been slowing down since 2018, rather than pursuing structural reforms to rejuvenate the growth process, the focus has shifted completely to ramping up health infrastructure and saving lives and providing livelihoods to the affected persons. The pandemic disrupted the lives of a large majority in the unorganized sector, particularly to the migrant labourers who, with loss of employment and little reserves to support, started in large numbers back to their villages even on foot in the absence of transport facilities creating a serious humanitarian crisis. The state governments, being closer to the people are faced with severe fiscal challenges of fighting the pandemic and providing for livelihoods. The Constitution assigns the responsibility of healthcare to the states, but their historical neglect of the sector is coming to roost now.

Both short- and long-term impacts of the pandemic are severe on economic growth and poverty. The immediate challenge for the government is to find fiscal resources for facing the immediate crisis and provide stimulus for the revival of economic activity. This article attempts to analyze the fiscal fall put of the pandemic and explores the ways to deal with the problem. Section 2 will provide a background for the discussion. Section 3 will analyze the impact of the lockdown on the growth of the economy, prospects of revival of growth and the fiscal impact. It is often said that the crisis is the mother of reforms and it is important that the opportunity provided by this crisis should not be wasted. The fiscal impact of the pandemic will be severe, and the rule based fiscal policy will be completely thrown overboard to meet the crisis. Avoiding rating downgrade in this environment would require laying down clear and transparent fiscal adjustment path and restoring credibility to the fiscal numbers which have become non-transparent due to various obfuscations. Therefore, section 4 will discuss the various reform measures that the governments, both at centre and states should undertake not only to revive the economy but also take into a higher growth trajectory. The concluding remarks are provided in the last section.

The Background

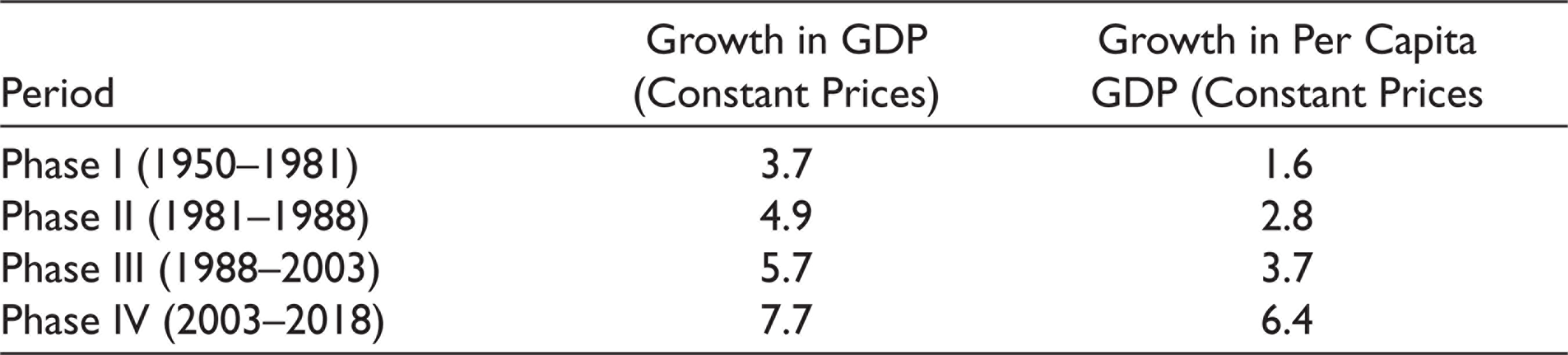

The coronavirus pandemic which struck India has come as a tragic break to the Indian growth story. The economy that was growing at over seven per cent in the current millennium came to a grinding halt after the severest lockdown wan announced when the pandemic struck. There was a steady acceleration in the growth rate after liberalizing reforms were initiated in successive phases from 3.7 percent during the period 1950–1981 to 7.7 percent during 2003–2018 (Table 1). Achieving double digit growth was found to be in the feasible realm and exploring the policy paradigm required to achieve this was not found to be unrealistic. 1 The growth, in turn, had significant impact on reducing poverty as poverty ratios according to the official poverty line declined sharply from 45.7 percent in 1993–1994 to 22 percent in 2011–2012 (Panagariya, 2020).

Phases of Economic Growth in India

Just a few months before the Coronavirus pandemic struck, that the Prime Minister of India set an aspirational goal of transforming into a five trillion dollar economy target by 2024–2025 from the present level of 2.9 trillion dollar. Of course, the target was ambitious as it required sustained growth at over 9 percent (or nominal growth at 14 percent) at the prevailing exchange rate. The NITI Aayog had estimated that to achieving the target required additional investment of ₹108 trillion and 78 percent of this was supposed to be made by the union and state governments equally and the remaining 22 percent was to be from the private sector. This also implied that the capital outlay of the centre will have to increase from the prevailing 3.5 trillion (2019 2020 RE) to ₹10 trillion by 2024–2025 which required significant additional resource mobilization and releasing larger volume of resources for investments by compressing government consumption expenditures, subsidies and transfers.

Although most observers felt that the target of USD 5 trillion was more an aspirational, no one had an inkling that even before the ink of the investment projections dried, there would be a catastrophe in the form of COVID-19 pandemic. The severest lock down that followed when the pandemic broke virtually closed the economy from all business activities and threw the economy to terrible uncertainty. The pandemic is still on the rage and there is considerable uncertainty about the possibility of a second wave. With the vaccine for the virus some distance away, there is a palpable fear and insecurity among the people and in spite of the relaxations in the lockdown, businesses are yet to fully revive. With selective relaxations, even as the businesses attempt to revive, they are now severely constrained by supply side disruptions on the one hand and lack of labour on the other.

It is not surprising that the first quarter estimate of GDP out by the Ministry of Statistics and Programme Implementation shows the most severe contraction in the economy seen in recent memory. At 23.9 percent, the contraction was the highest among the G20 countries. The gross value added shrank by an unprecedented 22.8 percent. The second quarter estimate shows a substantial recovery at −7.5 percent. Of course, with continuous contractions in two successive quarters, the economy has entered into a technical recession. Although the contraction of this order is still one of the highest among major economies and, in normal times, it should have rung alarm bells, coming in the back of 23.9 percent contraction in Q1, the better-than-expected performance brings in some cheer, though, it is too early to lift the gloom.

The contraction in the first half of the year is 14.1 percent with agriculture and allied activities registering a positive growth of 3.4 percent, and industry and services shrinking by per cent and per cent respectively. For the year as a whole Agriculture is likely to show a stellar performance due to bountiful Kharif harvest already seen and the expectation of higher production in the Rabi crop as well. While the industry and services sector will recover, as the structural problems remain unaddressed and with compressed government consumption expenditure due to lower revenue collections, their contraction is likely to continue even in the second half of the year. The Monetary Policy Committee of the RBI has estimated contraction in the economy for the whole financial year at 7.5 percent.

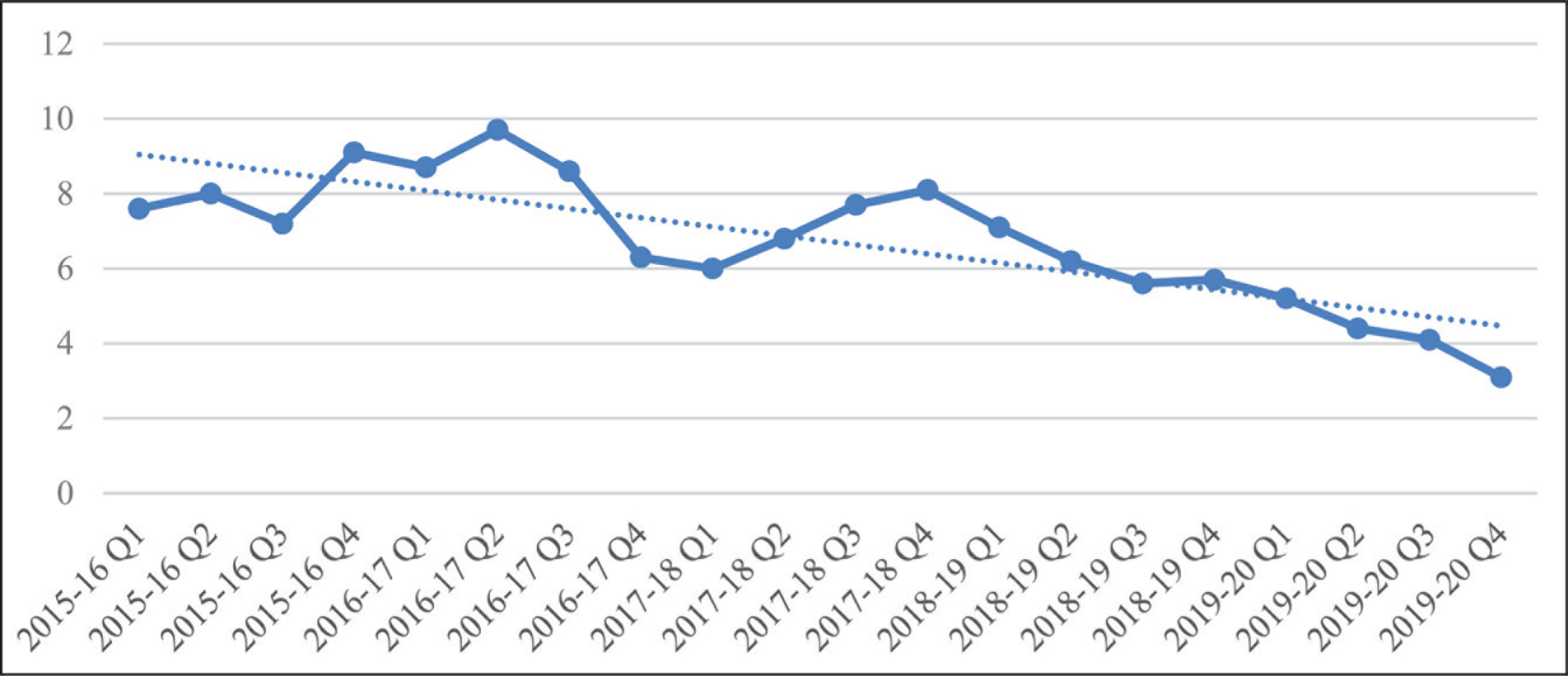

The pandemic struck at the time when the economy was already slowing down. The estimated GDP growth at 4.2 percent in 2019–2020 was the lowest in the last 11 years. The quarterly growth trend since 2015–2016 presented in Figure 1 shows a steady decline in the growth to reach 3.1 percent in the fourth quarter of 2019–2020 and this was the lowest in 44 quarters. It is seen that even as the economy gradually recovered from the shock of demonetization in the third quarter of 2016–2017, to reach 8 percent growth in the fourth quarter of 2017–2018, the subsequent quarters show a steady decline.

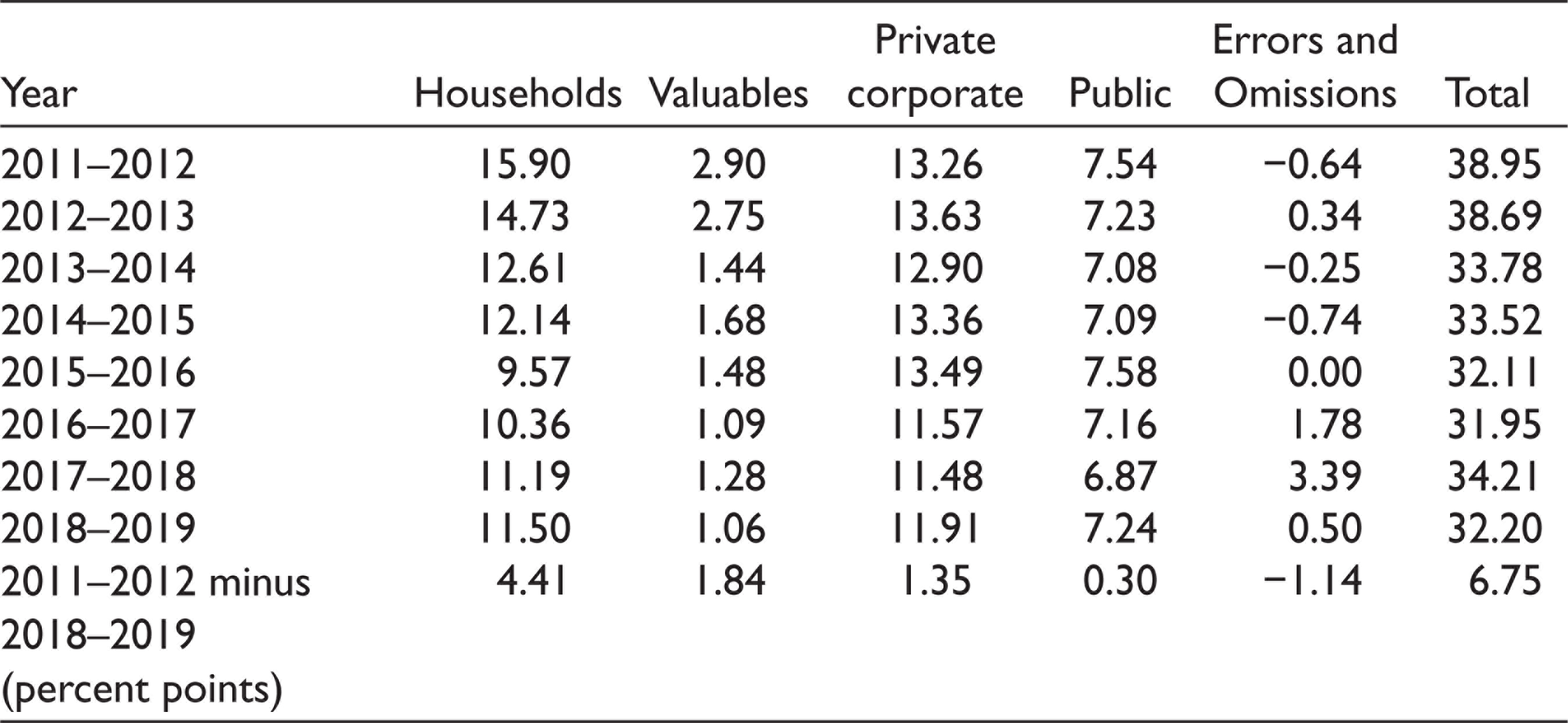

The steady decline in the growth of GDP is the reflection of declining saving and investment in the economy. The aggregate investment as measured by gross capital formation (GCF) as a ratio of GDP (current prices) showed a steady decline from 39 percent in 2011–2012 to 32.2 percent in 2018–2019. Of the 6.8 percent point fall in aggregate GCF, 6.2 points (including valuables) was from households, 1.4 points were from corporates 0.3 point was from the public sector. Thus, the decline was witnessed in all the sectors, though a predominant proportion was by the households. Similarly, over the period 2011–2012 to 2018–2019, the percentage of gross domestic saving to GDP declined by 4.5 percent points and the entire fall was due to decline in household sector’s physical savings.

In fact, GCF in 2019–2020 the ratio of Gross Fixed Capital Formation (GFCF) to GDP showed a sharp decline from 32 percent in the first quarter of 2019–2020 to 28.8 percent in the last quarter. The private final consumption expenditure was slowing down, and exports were declining. The only engine of growth that kept the growth rate ticking was the Government consumption expenditure, and with significant contraction in revenues and the reluctance of the government to expand fiscal deficit, even that is likely to be a casualty. In fact, the in the first half of the year, private financial consumption expenditures declined by 18.9 percent, government consumption expenditures by 4 percent and capital formation by 28.1 percent. The sharp decline in the capital formation would have serious repercussions on the long-term growth prospects.

The reasons for the steady slowdown in the economy have to be found in the continuing balance sheet crisis in the corporates as well as the commercial banks. Although the Insolvency and Bankruptcy Code (IBC) has been hailed as a landmark reform, there have been problems of implementation and with undue delays in resolving the stressed assets of the corporates, the balance sheets of the banks continue to be stressed. In addition, the fear of investigative agencies on lending decisions had turned the public sector bankers to be risk averse. The non-banking financial companies (NBFC) crisis beginning with the failure of Infrastructure Leasing and Financial Services (IL&FS) and followed by Dewan Housing and Finance Limited (DHFL), Reliance Capital and Altico deepened the malice. These developments have adversely impacted on corporates, infrastructure financing and liquidity availability for the small and medium enterprises (SMEs). The NBFCs crisis worsened the stressed balance sheets of the banks further.

Sectoral Investment Trends (Per cent of GDP at Market Prices)

Thus, the pandemic has struck the economy when the economy was already reeling under structural problems and therefore, relaxation of the lockdown, by itself, will not achieve the recovery at the required pace. In other words, fast recovery is unlikely unless the government comes out with substantial fiscal stimulus, but the sharply declining revenues and already high outstanding debt does not permit large additional borrowing. The pandemic has shown that, postponing structural reform any longer would only be at economic peril. Therefore, it is imperative that the government should initiate serious structural reforms to both ease supply side restrictions and to propel consumption and investment demand. However, the lack of fiscal space constrains the Government from carrying out any significant counter-cyclical fiscal policy.

The government could have pulled the economy out of the recession through substantial fiscal stimulus by significant expansion in public spending. During the global financial crisis, the Government had provided substantial fiscal stimulus both by way of increase in expenditures and tax cuts. Unfortunately, in the prevailing situation of slowing economy and raging fiscal imbalance does not permit any significant fiscal action. The revised estimate of fiscal deficit of the central government for 2019–2020 was placed at 3.8 percent of GDP. However, actual figures finalized by the Controller General of Accounts showed the deficit at 4.6 percent. In addition, off budget borrowings through issuing short term bonds, unsecured loans and borrowing from the NSSF by the Food Corporation of India towards meeting food subsidy and its arrears, special banking arrangements to cover arrears of fertilizer subsidy, financing irrigation projects from the Long Term Irrigation Fund created by the NABARD, and financing of railway projects through borrowings from the Indian Railway Finance Corporation have been substantial, estimated at over 1.8 percent of GDP. In addition, as pointed out by the Comptroller and Auditor General (C&AG), the government under transfers the amount of cesses collected to various funds to be placed in the Public Accounts to show lower revenue and fiscal deficits. 2 Even if other public sector borrowings are ignored, the total borrowings by the government itself directly and through the aforementioned institutions worked out to about 6.5 percent of GDP. When the fiscal deficits of the states are included the total deficit from the government account works out to 9 percent of GDP and for other borrowings from other public enterprises another 2 percent. Thus, the public sector borrowing alone is substantially higher than household sector’s net financial saving which is estimated at 7.6 percent of GDP.

The fiscal deficit estimate of 3.5 percent projected for 2020–2021 in the budget, was an underestimate, but the severe lockdown following the COVID-19 pandemic from March 35 made it completely irrelevant. To begin with the revised estimate of revenue for 2019–2020 itself was far too optimistic. As it turned out, the actual gross tax revenue collection of the union government in the year turned out to be lower than the revised estimated by almost 12 percent. As the budget estimate of tax revenue for 2020–2021 was estimated by taking the revised estimate of the previous year as the base, it was an overestimate to begin with. In other words, to realize budgeted tax revenue estimate for 2020–2021, the growth required from the previous year’s actual collection is 20.4 percent and that would have been unlikely even in a normal year.

The Lockdown, Economic Contraction and Fiscal Impact

The lockdown brought the economy to a grinding halt and the contraction in the economy drained the tax revenues. Even after the relaxations in many restrictions, with continued spread of the pandemic, full-fledged recovery has not been possible because of continued restrictions on many sectors and business hubs which are the hotspots. Besides, supply chain disruptions (partly due to restrictions on the imports from China) and unavailability of skilled migrant labour have continued to constrain full scale recovery. The RBI and the government have announced a series of measures, but most of them are in terms of reducing interest rate, ensuring liquidity, restructuring loans to stressed sectors, regulatory forbearance, and moratorium. These by themselves are not likely to revive the economy and substantial additional measures needed. The distribution of free food grains to the vulnerable sections has avoided starvation deaths, but demand side measures have not been significant. The fiscal measures announced include additional allocation to Mahatma Gandhi National Rural Employment Guarantee ₹400 billion, providing cash vouchers in lieu of Leave Travel Concession (LTC), extension of production linked incentive for 10 more key sectors in addition to the three sectors which were given earlier, front loading the Kisan Samman Nidhi which was already in the budget and providing 2 percent of GDP additional borrowing space to the state governments.

While the situation demands that the Government should provide a substantial demand stimulus by increasing expenditures, it has been careful to avoid unsustainable deficits and debt and the fear of rating downgrade. As mentioned earlier, the estimates contraction of the economy in the full year according to RBI would be 7.5 percent. At current prices, the contraction could be about 3.5 percent (assuming implicit deflator of 4 percent) for the year, the tax revenue is likely to be lower than the budgeted by ₹4.5 trillion, and after devolution (₹1.7 trillion), the net tax revenue is likely to be lower by ₹3.8 trillion. The non-tax revenue is likely to be lower by about ₹1 trillion mainly due to lower collections from railways and dividends from enterprises including the RBI. The disinvestment proceeds are also likely to fall short by ₹1 trillion from the budgeted ₹2.1 trillion. Thus, the shortfall in the net revenue from the budgeted is likely to be ₹5.8 trillion and this may be compensated by the additional excise duties levied on petroleum products by about ₹0.5 trillion. The total fiscal effect of the stimulus measures announced at the central level is likely to be ₹2 trillion. Thus, the fiscal deficit of the central government in the year is likely to go up from the budget ₹7.96 trillion to about ₹15.3 trillion which works out to about 7.7 percent of GDP.

In the case of the states, the aggregate deficit will depend on the permission given to them to borrow. Although their Fiscal Responsibility and Budget Management (FRBM) allows them to borrow up to 3 percent of their respective Gross State Domestic Product (GSDP), the aggregate fiscal deficit of the states has been around 2.3 percent to 2.5 percent of GDP in recent years. This year, however, with severe contraction in both their own revenues and tax devolution from the centre, they are likely to use their entire fiscal space. In addition, as a part of the stimulus, the centre has allowed them to borrow an additional 2 percent of their GSDP. Their borrowing from 3 percent of GSDP to 3.5 percent is without any conditions. However, additional one per cent of GSDP borrowing will be permitted only on fulfilling four reform conditions, each giving additional quarter per cent. The reforms to be undertaken are: (a) One nation, one ration card which requires linking Aadhar number into ration cards and installing point of sale machines in all fair price shops; (b) improvement in ease of doing business which requires (i) district level assessment of ease of doing business as Department of Promotion for Industry and Internal Trade norms, (ii) automatic renewal of state industrial, commercial licenses to business and (iii) making randomized inspections with prior notice and full transparency; (c) Power sector reforms which entail reducing aggregate technical and commercial losses, direct benefit transfers to farmers instead of lower tariffs and reducing the gap between average cost and average revenues; and (d) Urban local body reforms requiring the states to notify property tax floor rates according to circle property values and notify water and sewer charges. If at least three of the four reform conditions are satisfied, the states can borrow the remaining half a per cent of GSDP.

There are questions on whether the centre should have imposed conditions for borrowing at a time the states are faced with severe fiscal distress. Of course, Article 293 (4) states that “A consent under clause (3) may be granted subject to such conditions, if any, as the Government of India may think fit to impose”. It must also be admitted that the four reform conditions are important. However, this is for the time in the history of the country that conditions have been stipulated for the market borrowing by the states. In fact, the 15th Finance Commission has been asked in its Terms of Reference (TOR) to make recommendation on the conditions that the Government if India may impose on the states while providing consent under Article 293 (3) of the Constitution and the Commission is yet to make the recommendation on the issue. Perhaps, instead of imposing conditions when the states are facing a fiscal distress situation, the Government of India could have had discussions with them and found appropriate ways to implement the reforms. In any case, the states do not have much choice, and even if some states avoid undertaking power sector reforms for political reasons, the aggregate borrowing of the states is likely to be about 4.5 percent of GDP.

The former discussion leads us to make important inferences on the fiscal consequences caused by the COVID-19 crisis. First, the combined fiscal deficit of the centre and states is likely to be about 12 percent–13 percent of GDP and the corresponding debt is likely to be over 85 percent–90 percent of GDP. Second, financing such large volume of deficit in a situation where the net financial savings of the households is just about 7.6 percent of GDP and this year, the country is likely to show marginal current account surplus. Therefore, besides indirect monetization of deficits through large and frequent open market operations to keep the yields low to enable the Government to borrow at lower cost, it may be necessary to finance a part of the deficits through direct monetization. Third, much of the additional fiscal deficit is to mainly to meet the shortfall in revenues and this does not have any additional stimulus content. In other words, the prevailing situation warrants that the Government should undertake active counter-cyclical policy, but the lack of fiscal space will constrain its ability and to that extent, the revival of the economy will not be swifter or other ways like monetization of assets to increase investments will have to found. Fourth, much of the capital expenditure by the Government has been at the state level. While the capital expenditure of the central government has been hovering around, the, the states have been spending about 3 percent of GDP. In the past, the states have been having a marginal revenue surplus and the entire borrowings have been used for spending on the capital account. This is likely to change and most states are likely to postpone their plans for capital expenditures, as the shortfall in revenues is likely to be larger than the permitted additional borrowing. The slower growth of capital expenditure is likely to adversely impact on the medium-term growth prospects.

Even as there have been progressive relaxations, the normal resumption of economic activities looks still distant due to continued restrictions on economic activities in some sectors and urban hotspots. In addition, supply disruptions and migrant labour problems continue to constrain economic activities. The sectors such as transport, tourism and hospitality will continue to contract due to social distancing requirements and lack of confidence of consumers. Therefore, the recovery will continue to be staggered.

Even when it recovers to the pre-pandemic level of incomes, it is doubtful whether the economy will return to a high growth trajectory of 7 percent growth seen during the last two decades prior to the crisis. The twin balance sheet problem continues to rage. The corporates are under severe strain and have postponed their investment plans and the SMEs are struggling to survive. The non-performing assets (NPAs) in the commercial banks are set to rise sharply after the moratorium and restructuring period gets over and not surprisingly, they have turned risk averse and unwilling to lend. The implications of extended moratorium on loan repayments, restructuring of the debt of corporates and SMEs, regulatory forbearance undertaken in the wake of the coronavirus crisis will all become clearer when these are lifted and that would show the extent of real damage to the balance sheets of the corporates as well as the banks from the pandemic. Besides, many public sector banks (PSBs) are preoccupied with adapting to the mergers and are simply not thinking about lending. Thus, the borrowers are unwilling to borrow, and lenders are unwilling to lend. The government could have spent its way out to trigger economic revival, it simply does not have the fiscal space. According to the stress test done by the RBI, the NPA of scheduled commercial banks could rise from 8.5 percent in March 2020 to 12.5 percent in September 2020 under the baseline scenario and 14.7 percent under “very severe stress scenario”. The NPA of the PSBs is stated to rise from 11.3 percent in March 2020 to 15.2 percent under a baseline scenario and 16.3 percent under very severe stress in September 2020.

Hastening Reforms

Crisis is good opportunity to initiate reforms and the Government should not waste this crisis by not undertaking them. Structural reforms are needed not only to revive the economy but also to take it to a higher growth trajectory. In the short term, the government will have to substantially increase public spending even in the resource constrained situation prevailing at present. Faced with hard budget constraints, some of the state governments have embarked on an ambitious programme of monetizing residential and commercial land in urban centres and selling of leased land to the lessees, regularizing building and land use violations at a high fee and increasing the floor space index to shore up their finances. Hopefully, they will start correcting the historical mistake of not spending adequately on public health, particularly on preventative healthcare by strengthening the wellness centres. Creating a strong web of wellness centres will minimize curative healthcare through hospitalization. The pandemic has clearly brought home the importance of public spending on healthcare. The pandemic has clearly brought home the importance of public spending on healthcare.

As mentioned earlier, sharp decline in revenue collection following the GDP contraction is likely to increase the aggregate fiscal deficit to 12 percent–12.5 percent of GDP. Nevertheless, with the economy contracting by 15.7 percent in the first half of the year, inaction on this front will only be the economy’s peril. The fear of downgrade by credit rating agencies should not deter the government from loosening the purse for, the probability of down grade will be even more if the economy continues to contract and measures to revive it are not undertaken. The principle of war finance is not to follow any principle, and this is the time to inject substantial fiscal stimulus to revive aggregate demand. Of course, the government will have to bring out transparent numbers and a credible fiscal adjustment plan from the time when the pandemic subsides and amend the FRBM Act to provide for the appointment of an independent Fiscal Council to monitor the fiscal targets in the future (Rao, 2020b).

The central government has initiated reforms in a number of areas and that should help to improve the economic environment in the medium and long term. Merging of 24 central labour laws into four codes is an important reform to impart greater flexibility to the labour market and ending the inspector raj. This has been talked about for long without much progress. The Industrial Relations Code allows the manufacturing units up to 300 workers to hire and fire without the Government’s approval and for those with more than 300 workers, approval is needed but if the labour department does not respond within the time frame, the approval is deemed to have been received. The three new legislations enacted in the farm sector provides flexibility to the farmers to sell their products anywhere. The amended Essential Commodities Act deregulates production, storage, supply and distribution cereals, pulses, potato, onion and oilseeds and enables the private sector to play important role in these activities. The Farmers’ (empowerment and protection) Agreement of Price Assurance and Farm Services Act, allows the small farmers to enter into agreement with corporates for contract farming. Hopefully, the raging controversy on the three legislations and the farmers; agitations currently under way will not result in the government from compromising on the basic tenets of the three Acts.

In the social sector, the National Medical Commission Act, 2020, abolishes the 64 year old tainted Medical Commission of India, ends the inspector raj and enables the appointment of mid-level community health providers to bridge shortages of medical professionals in rural areas. By liberalizing private medical education with 50 percent seats earmarked in private medical colleges and deemed universities, it augments the number of seats. Similarly, the New Education Policy gets rid of multiple regulators such as University Grants Commission (UGC) and All India Council of Technical Education (AICTE) and replaces it with a single regulator – Higher Education Council of India. UGC was both a regulator and a funding institution.

A number of areas where the government will have to initiate reforms to improve the economic environment, to ease of doing business and to end the inspector raj. These are necessary to reverse the declining investment climate in the country and secure better mechanisms for price discovery for the farmers in the medium and long term. However, the immediate task the Government has to address is the removal of supply and demand constraints to lift the economy out of the morass. This requires the Government to initiate measures to (a) increase public consumption and investment, (ii) undertake banking reforms to accelerate lending, (b) police and judicial reforms to protect life and property and enforce contracts and (c) reverse the protectionist trend in the last three years in the interest of making the domestic production sector competitive and export oriented.

The stimulus package announced so far was mainly to improve liquidity, provide moratorium and restructure loan repayments. The Government did not have the luxury of providing a large fiscal stimulus with little fiscal space aggravated by sharp contraction in revenues. Nevertheless, in these exceptional times, the Government will have to loosen the purse and should not be fixated on fiscal targets for this and the next year. More importantly, it should front load disinvestment and monetize assets to increase public investment spending. In the given geopolitical situation, defence expenditures will have to be increased and the pandemic demands higher allocation to the health sector. The states have embarked on a number of measures to raise revenues including monetizing land. The union government should fast track disinvestment as well as monetize its assets like land to augment spending. The ministries such as defence and railways have large tracts of land which can be monetized. Hopefully, companies like Air India will be privatized soon.

Two recent books and painted the grim picture of the Indian banking system and chinks in its regulation (Acharya, 2020; Patel, 2020). The problems confronting the financial system in general and banks in particular are systemic. Acharya (2020) has persuasively argued that fiscal dominance has adversely impacted financial stability in a variety of ways and Patel (2020) has alluded to the constraints in regulation due to government’s ownership of banks. The Financial Stability Report (FSR) released by the RBI recently has underlined the vulnerability of the Indian banking system and in particular PSBs. The balance sheets of the PSBs are likely to worsen substantially after the moratorium period is over and restructuring process is gone through. According to the FSR, under a baseline scenario, the gross NPAs of the PSBs would go up from 11.3 percent in March 2020 to 15.2 percent in March 2021 under a baseline scenario, and to 16.3 percent under very severe stress scenario. The Capital to Risk Weighted Assets Ratio (CRAR) is estimated to deteriorate from 14.6 percent in March 2020 to 13.3 percent in baseline scenario and to 11.8 percent under very severe stress scenario. The volume of recapitalization required is humongous.

Postponement of reforms in this sector by the government will be at its own peril. The time is opportune to implement the P. J. Nayak Committee recommendations to substantially reduce the government ownership of the banks. The proceeds from disinvesting in bank shares can be used for their recapitalization. Simultaneously, the Government should distance itself from the management by abolishing the Department of Financial Services and creating a separate holding company to oversee the functioning of these banks. The Government should also take measures to distance itself and empower the Boards to take management decisions. Reducing the government shareholding to the minority status will also enable the RBI to subject these banks to closer regulatory scrutiny as in the case of private sector banks. 3

There are other reforms needed to make land available for entrepreneurs wanting to relocate from China. The most important reform needed in the country today is judicial reforms to ensure that the basic duty of the state, of ensuring property rights and enforcing contracts in a timely manner is accomplished and that is the most important factor in the ease of doing business. The last three years have seen a steady creeping of protectionist stance in the government and the pandemic and the stand-off with China has raised the pitch for more protection. This is self-defeating as the history in this country has shown. Denying the benefit of goods at international prices to the consumers to protect the producers has only helped them not to be competitive and ask for more protection. Hope the government will reverse the trend quickly and make the economy export oriented.

The time is opportune to initiate structural reforms in a number of areas which would help the economy to move towards higher growth potential. Many of the reforms needed at present have been highlighted in Panagariya (2020). The recent attempts at reforming labour laws and in the agricultural sector would help in creating more flexible land and labour laws. The IBC enacted is a great reform, but the implementation is stuck for several reasons and they need to be removed to hasten the resolution process. It is also important to reverse the protectionist tendency that has crept into the policy regime in the last three years to impart greater competitiveness. There are still large infrastructure gaps that need to be bridged and substantial investments are required to be made. One of the most important and urgent call should be on judicial reforms. Protecting life and property of the people and enforcement of contracts is the basic public good that the government must provide. Long judicial delays result in most people being denied justice and the powerful sections resorting informal and illegal means to secure justice. Incentive to invest and grow depends on ensuring speedy and efficient resolution of the disputes.

Concluding Remarks

The COVID-19 pandemic has created an unprecedented economic devastation of the economy. In hastening the recovery process, the RBI has taken a number of initiatives to ensure adequate liquidity, declare moratorium on repayment of loans, restructured loans to selected sectors based on the recommendations of the committee chaired by Mr K. V. Kamath. However, the fiscal stimulus to augment aggregate demand has not been significant. The already high fiscal deficit caused by the sharp decline in revenues does not provide much additional space. The government too has been extremely cautious to avoid downgrading by the credit rating agencies.

The principle of war finance is not to follow any principle, and this is the time for throwing caution to the winds and undertake substantial expenditures to stage fast recovery. Even the credit rating agencies have indicated that their analysis in the prevailing situation is based on how fast the economy recovers rather than what the volume of fiscal deficit is. The contraction in GDP in the first half of the year at 15.7 percent, the worst among all major emerging economies and therefore, the government will have to come up with substantial additional stimulus to accelerate growth. Furthermore, it is also important to substantially disinvest and undertake expenditures on infrastructure. The government should also get its inventory on land and monetize it in parts particularly for spending on sectors such as defence and railways.

The government has initiated a number of reforms in earnest, particularly to infuse flexibility to land and labour markets, regulatory systems in education and healthcare, and has made additional borrowing to the states conditional on undertaking power sector reforms, property tax reforms and improving the ease of doing business. However, implementation of these reforms holds the key for their effectiveness. There is considerable urgency in the reform of the banking sector to ensure smoother credit flow to productive sectors. The moratorium and restructuring done during the pandemic is likely to subject them banks to severe stress as revealed by the stress test conducted by the RBI in its financial stability report. Also, reforms in sectors such as police and judiciary are overdue for the basic incentive for investment decisions is to protect the life and property of people and enforce contracts to improve the ease of doing business in the country.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.