Abstract

After more than two decades of searching, the holy grail of integrating norms into management and organization research remains elusive. Researchers still lack a clear framework that explains value creation in relation to normative values, and, in turn, a means to incorporate values into research methods and generate value-based practical insights. To fill that need, this article presents an epistemological framework for understanding value creation. The practical inference framework centers on the activity of practical reasoning, a kind of reasoning that is legitimized by intrinsic values. It turns the ordinary epistemic equation on its head by seeking reasons rather than causes, and justifications rather than descriptions. In doing so, it shows how both factor analytic and newer, divergent methods of research can integrate with a robust architecture of value creation in ways that offer relevant knowledge for managers and society.

Keywords

A pressing question of our age is whether our homage to value creation is muddled. Do we pay tribute to a concept that may destroy value in the very act of creating it? Do we sacrifice some values on the altar of others? A rare theme that unites thinking about contemporary business models is the acknowledgment of the importance of value creation (Zott, Amit, & Massa, 2011, p. 1021). Yet, unless “value creation” is a clever euphemism, then underlying values must be at stake in the process whereby value is created, whether those values are merely ones of enhancing social-economic welfare and fulfilling duties to owners, or something more. The question of how values inform value creation haunts management and organization research. The values of fairness and sustainability crowd our research agenda; yet the very urgency of the topics adds to the urgency of finding a value-creation framework that may harness and sustain them.

The practical inference framework articulated here draws upon both practical and theoretical reasoning by understanding research in terms of justified choice and intrinsic values such as social-economic welfare and fairness. In so doing, it honors the premise implicit in all management and organization research, that research can inform the process of creating genuine value. The importance of “value creation” is widely acknowledged (Zott et al., 2011), but the meaning of the term remains opaque and highly varied, with only a few interpretations stepping beyond the intuition of a simple two-way, exchange-oriented flow of value between the firm and the customer. Most often, the focus is on economic value for the firm (Freudenreich, Lüdeke-Freund, & Schaltegger, 2020). The practical inference framework developed below points to a more robust, inclusive interpretation of value creation by inserting reasons and justifications into an integrated pattern of agent-centered decision-making. To date, even champions of openness have hesitated to go in this direction, but I will elaborate why this is necessary and how this can be done.

Previous work has already led the way to this framework. Sensemaking approaches advanced by Karl Weick and others (Reinecke & Ansari, 2015; Weick, 1995) showed how reason and contextual judgment can be reconciled in practice. Earlier epistemic approaches identified the importance of practical reason and “phronesis” (practical wisdom) in understanding management behavior (Flyvbjerg, 2006; Nonaka & Toyama, 2007; Sandberg & Tsoukas, 2011). The “turn to practice” (Gehman, Trevino, & Garud, 2013) encouraged the evolution of divergent research methods already under way (Argyris & Schon, 1974; Ketokivi, Mantere, & Cornelissen, 2017; Lamprou, 2017). Early in the evolution of “stakeholder theory,” scholars distinguished three ways in which stakeholder theory might be understood: descriptive, instrumental or normative (Donaldson & Preston, 1995). Many hoped that these three would converge in a “managerial” approach that reached beyond merely describing existing situations and predicting cause-effect relationships, to “recommending” attitudes, structures, and practices “that, taken together, constitute stakeholder management” (Donaldson & Preston, 1995, p. 67; Phillips, Barney, Freeman, & Harrison, 2019). Later, Jones and Wicks (1999) echoed this goal with an influential call to integrate both social science and ethics-based arguments into a “managerial” conception of stakeholder theory. However, two decades later, the holy grail of normative integration remains aspirational both in stakeholder theory and elsewhere. Management and organization researchers to date lack a means to pinpoint specific types of research that can create value for a wide group of constituents. Researchers want to deliver insights to managers that harness values that are relevant to society, but so far they lack the right tools to do so.

To satisfy this need, the present article advances an epistemic framework for practical reasoning that is framed in terms of practical inference and grounded by intrinsic values. It is a framework that offers different methods of research a natural entry point into the world of practical decision-making and shows the impracticability of “rational choice theory,” the go-to option still for much contemporary social science.

Intrinsic Values in the Value-Creation Process

It is no surprise that the researcher wants her work to matter and to help practitioners make the world better (Waddock, 2015). But questions of “better” and “worse” are notoriously difficult, presenting both a barrier and an enigma for researchers. Researchers know that better explanations do not necessarily make for a better society (good explanations can be used for good or ill), and they are often conflicted about claims of “value-neutrality.” In this regard, the historic turn away from quantitative factor analytic methods to “divergent” methods such as narratives, causal mechanisms, and “thick” explanations marked a boiling point of frustration with purely quantitative ones, and, for many researchers, a turning away from value-sanitized outcomes. Researchers balked to see values such as fairness or sustainability either left implicit or rationalized through methods or generalized functional values such as efficiency and profit, with no guidance given to actors in practical contexts (Ghoshal, 2005). But, as we shall see, the question of justified value creation frustrates both traditional and newer “divergent” methods.

The key to the practical inference approach that I offer here consists in two connected concepts: intrinsic values and practical reasoning. Intrinsic values are alone capable of transforming narrow practical reasoning into practical wisdom or “phronesis”; in other words, only intrinsic values can transform practical activity into fully-justified value creation. In explicating the classical Greek concept of phronesis, Flyvberg explains that it involves values that go “beyond analytical, scientific knowledge (episteme) and technical knowledge or know how (techne),” and involves judgments and decisions made in the manner of an exemplary social actor (Flyvbjerg, 2006, p. 2). This definition tracks well with Aristotle (1962) and his famous distinction between theoretical and practical reasoning. In order to count as “phronesis” an action has to be justified by the deepest of values (“Eudemonia”). The deepest or “intrinsic” values are part and parcel of a constellation of concepts, choice, practical reasoning and purpose that inter alia define “values.” Such values are “intrinsic” because they reflect intrinsic worth and constitute non-instrumental reasons for justifying choice (Donaldson & Walsh, 2015; O’Neill, 1992; Rønnow-Rasmussen, 2015).

For purposes of the present discussion, it is the logical form of an intrinsic value that matters. Intrinsic values are those that guide and justify choice at the deepest level. The focus here is on how such deep values can assist actors in practice with their reasoning, and how they can fill epistemic gaps in existing methods of research. Intrinsic values have been a frequent topic in discussions of philosophers, economists, and legal theorists (Dorsey, 2012; Kreps, 1997; Sunstein, 1994; Taylor, 1989; Zimmerman, 2015). They are, as with all values, reasons for acting where the object of the act is seen as worthy of pursuit (Donaldson & Walsh, 2015, p. 288). This definition taps a legacy in moral philosophy, one that defines values in terms of reasons and that relates values to human interests (Perry, 1914, 1926). T. M. Scanlon’s position, reflected in the approaches of contemporary moral theorists, is that “to call something valuable is to say that it has other properties that provide reasons for behaving in certain ways with respect to it” (Scanlon, 1998, p. 96).

Practical reasoning, emphasized in the writings of Kant and Aristotle, may be understood broadly as the process of reasoning when acting and choosing (Aristotle, 1943; Kant, 1788). Intrinsic values sit in the catbird seat of the ordinal ranking of practical reasons. Their defining feature is their status of being non-derivative, i.e., as having a worth that does not depend upon a higher-level value. They are “hypernorms” in the sense that they sit in judgment of lower-order norms (Donaldson & Dunfee, 1999). Again, they are intertwined conceptually with a constellation of concepts that includes choice, practical reasoning, and purpose. Purposes are part and parcel of practical reasoning because purposes serve as reasons for acting, whether at the individual or organizational level.

The underlying epistemic role of intrinsic values is to complete the justification of an action. Consider a thought-experiment. Someone asks a friend why she is applying for a job, and the friend answers, “Because I value a salary.” The friend persists, “So why do you value a salary?” “Because,” she says, “I want to contribute to my family.” But the friend continues, “So why do you value contributing to your family?” “Stop!” comes the reply, “I do not value contributing to my family for some other reason; I think contributing to one’s family is something worth doing for its own sake.” In doing so, she flags that at least for her the value of “contributing to family” constitutes an intrinsic value. Any epistemic chain of practical justification must end somewhere, and intrinsic values are by definition those reasons that are meant to count as full-stop explainers. However, even when serving as the highest value in a chain of practical reasoning, intrinsic values must be understood as “synoptic,” which means that in decision-making situations their value must be adjusted in the context of other intrinsic values that are relevant to the particular act (Dancy, 2004). For example, the pursuit of the intrinsic value of freedom of speech may sometimes require adjustment in light of the value of avoiding harm to others (do not yell “fire” in a crowded theater).

Intrinsic values defy epistemological gravity. They are both economically and otherwise “incommensurable” (Sunstein, 1994), and in a hard sense (Chang, 2002). For understandable reasons social scientific researchers are eager to reduce intrinsic values to mere psychological processes, including desires and preferences, and to interpret intrinsic values as properties of subjective experience. But intrinsic values cannot become grist to any kind of reductionist mill, even a subjective one. The philosopher, Charles Taylor, expresses the difficulty brilliantly: “This model is false,” he notes, “to the most salient features of our moral phenomenology. We sense in the very experience of being moved by some higher good that we are moved by what is good in it rather than it is valuable because of our reaction” (Taylor, 1989, p. 74). Whitehead makes a similar point in denying the possibility of reducing intrinsic values to desires (Whitehead, 1929, pp. 344–345) and cites Aristotle’s words from the Metaphysics (Aristotle, 1978, pp. 1072a 1023–1032): the primary objects of desire and of thought are the same. For the apparent good is the object of appetite, and the real good is the primary object of rational wish. The desire is consequent on opinion rather than opinion on desire; for the thinking is the starting point.

A non-intrinsic value in turn is a derivative (instrumental) value whose worth ultimately depends on its ability to contribute to the satisfaction of one or more intrinsic values (Donaldson & Walsh, 2015). Examples include return on investment, reduced transaction costs, increased market share, reduced product cycle time, and reduced employee turnover. In business we speak of these as supporting higher-order instrumental values such as firm efficiency, productivity, and profitability. But even efficiency and profitability stand on a lower rung of the normative ladder of justification than the higher-level intrinsic values that must eventually secure them, such as social-economic welfare, health, happiness, or fairness. Non-intrinsic values are, in effect, orphans awaiting parentage. The parents, in contrast, are final reasons for acting.

The task of determining precisely which values belong on a single authoritative list of intrinsic values is left aside in this discussion. Even a cursory glance shows a remarkable overlapping consensus among existing lists. Lists from philosophers, sociologists, and social psychologists are supplemented by lists from organizational sources, such as the United Nations’ Universal Declaration of Human Rights (1948) and Sustainable Development Goals. But individual lists vary, and precisely which items to include on a final ideal list, and precisely which words to use to describe them, is a much-discussed topic (Dahlsgaard, Peterson, & Seligman, 2005; Donaldson, 1989; Paine, Deshpandi, & Margolis, 2011; Rokeach, 1973; Ross, 1930). The ongoing conversation about which items to include on an ultimate list is fated to be a forever conversation, as it should be. The conversation itself is an integral part of the broader process of practical reasoning. Practical deliberation even continues when the the items on such a list are applied to actions, because, as we shall see, particular actors must deliberate about which specific intrinsic values are relevant to their particular actions.

It is curious that so little qualitative research in management and organization theory has utilized the tool of practical reasoning directly. But while the bar is high, this much is clear: addressing issues of practical reasoning and choice means moving beyond the epistemology of description, be it thick, thin or patterned, and moving beyond the causal world of prediction and analysis. It means making an epistemic leap of faith into the realm of justified choice. Management and organization research is not alone in its hesitation and mirrors a bashfulness shared by the social sciences in general (Nonaka & Toyama, 2007; Sandberg & Tsoukas, 2011). Perhaps the very word “science” is part of the problem (Petriglieri, 2020, p. 2). Resistance may be linked to Weber’s caustic warning to social scientists about becoming directly involved in policy debates, and, in turn, the appropriateness of evaluating ends in science. 1 Perhaps researchers believe that on-boarding values risks “objectivity” in science. But while it is true that practical reasoning lacks the objective precision associated with physics or chemistry, it is nonetheless capable of either failing utterly, or succeeding brilliantly. With practical reasoning, a clear difference separates “better” from “worse” both in terms of the depth and cogency of the reasoning and the quality of the outcome.

The Hidden Architecture of Value Creation: Practical Inference

The topic of practical reasoning has received limited exposure in management and organization research to date (Feldman & Orlikowski, 2011; Flyvbjerg, 2006; Nonaka & Toyama, 2007; Reinecke & Ansari, 2015; Sandberg & Tsoukas, 2011; Warren, 1991; Young, 2001), but is a common topic for philosophical scholars (Neiman, 1999; O’Neill, 1998; Raz, 1999; Wallace, 1990). Consider the “practical inference” framework for interpreting practical reasoning that is discussed by philosophers (Kenny, 1966). This framework can, as I argue in this paper, be helpfully adapted to management and organization contexts.

Practical inference at bottom is a simple concept. Ideas make for actions. Ideas serve both as motivators and justifications for action. Other ways to explain and justify actions exist, but subjectively speaking, practical inference is primordial. Practical reasoning and its representation in practical inference is counterintuitive at one level but blindingly intuitive at another. It is counterintuitive at the level of theory, because it turns the epistemic equation upside-down by making the outcome of a reasoning process an action rather than a concept. Ideas combine to beget an act, not an idea. My idea, “close the door,” prompts me to close the door, not to draw a conclusion about doors. From the vantage point of personal experience, practical reasoning is perfectly intuitive. We are thirsty; we reach for water. We want to comfort our friend; we speak kindly to our friend. In such everyday settings, we understand that our idea of thirst or water motivates our action – and also explains it. The act follows from its idea; it constitutes an “inference” that flows from our idea. “Why did you reach for the water?” “Because I was thirsty.” “Why did you speak kindly to your friend?” “Because I wanted to comfort her.” The same intuitive understanding pervades modern theory. The microeconomist presumes that the consumer’s preference for a bottle of water both motivates and explains her purchase of a bottle of water. Indeed, indifference curves are framed using this intuition, one so primitive it scarcely receives mention.

Practical inference offers a powerful diagnostic tool for management and organization research. Unlike purely theoretical research in, say, astronomy (Bennis & O’Toole, 2005), management and organization research should connect sooner or later, directly or indirectly, to the actions of managers and organizations. Researchers of the “phronetic organization,” explains Flyvbjerg, “should focus on values and, especially evaluative judgments; for example, by taking the point of departure in the classic value-rational questions: ‘Where are we going?’ ‘Is it desirable?’ ‘What should be done?’” (Flyvbjerg, 2006, p. 7). Used as a diagnostic tool, practical reasoning has the advantage of forcing two critical questions into view: first, is the research connected to practical actions and policies? And second, are those actions and policies justified?

One version of practical inference is the so-called “practical syllogism.” In a practical syllogism, a value premise works in tandem with a factual one (Aristotle & Apostle, 1981; Broadie, 1968; Kant, 1788; Neiman, 1999; Schreck, van Aaken, & Donaldson, 2013) in order to generate an action. Here is a simple version:

This grossly oversimplifies the full process of practical inference, but allows us to identify key implications of the practical inference framework for management and organization research. In order to avoid controversies over varying versions of practical inference, a simple, generic version will do here, namely: Focal value + Facts → Justified action.

With this framing, consider how practical inference might describe a proposed initiative in corporate governance that relies upon the well-known theory of “transaction cost economics” (Williamson, 1985) and supports the proposition that including more experts on a firm’s board of directors lowers firm costs.

( ( (therefore) (

The “fact” premise in most management decisions will probably include at least a data analysis and theory segment. It might, for example, analyse data that exhibit correlations consistent with the proposition that more experts mean lower cost (the data analysis segment), while appealing to insights from transaction cost economics that signal higher costs for certain forms of governance (the theory segment). The theory segment is factual; transaction cost economics offers a positive epistemological view of the firm based on the idea that firms evolve through market forces in which market actors attempt to avoid transaction costs (Donaldson, 2012, p. 261; Williamson, 2005). Of course, the combination of fact-based theory with analysed data is a standard recipe in management and organization research.

However, a critical piece of the practical reasoning puzzle lies hidden behind the “focal value” segment. In order for a justified action to be truly justified, the specific focal value must itself be compatible with intrinsic values. For example, the “minimization of transaction costs” would need to be linked to an intrinsic value such as social-economic welfare and, in turn, compatible with other intrinsic values such as fairness. Otherwise, as explained above, the practical inference will be incomplete from the standpoint of fully-fledged practical reasoning, or phronesis. Implications abound for the theories in organization and management. Transaction cost economics can “warrant” a claim about efficiency but not about fairness (Ketokivi & Mantere, 2021). Transaction cost economics could not warrant, for example, the fairness or unfairness of increasing the number of industry experts on a board of directors in an instance where this meant decreasing the number of female directors.

The “actor” in Figure 1 may be either an individual, an organization or a collection of individuals and/or organizations. The “action” may be either a single act or a policy. The “focal value” may be either an intrinsic value, such as “fairness” or “promise keeping,” or it may be a non-intrinsic, derivative one, such as “shareholder value” or “cost reduction.” The right-side arrow in the diagram represents the direction of value creation; the left-side arrow, the direction of justification. Moral philosophers disagree over whether an agent’s reasons can literally be “causes” of action (Davidson, 1963; Löhrer & Sehon, 2016) and for this reason the value creation arrow shown in the diagram permits either interpretation. It may be interpreted as a traditional causal relationship or something weaker.

Displays a complete practical inference architecture and its unique two-way direction of value creation and justification.

The “facts” in Figure 1 may include data and empirical theory. For example, a particular firm’s practical reasoning might use a positive theory of corporate governance in combination with data about past corporate attempts to achieve cycle-time reduction, all in an effort to create and justify a specific cycle-time reduction policy. Or, a strategic theory of competitive advantage might be used in combination with data about industry features to justify a specific product-pricing policy. At the level of facts, it is obvious that false facts lead to unjustified action. At the level of values, as explained above, any valid justification for an action must derive not only from facts, but eventually from intrinsic, i.e., nonderivative values. Moreover, as explained earlier, intrinsic values are “synoptic,” which means that any focal value that lies behind an action must be compatible with the relevant intrinsic values at stake in the context. This requirement is depicted through the intersecting circles showing intrinsic values 1, 2, . . . etc. This means that a firm whose fairness-in-hiring policy is motivated by the intrinsic value of, say, fairness, must ensure that its policy is compatible with other connected intrinsic values, such as the intrinsic value of safety. The overall justification for a particular fair hiring policy would break down if it meant hiring unqualified safety monitors at a nuclear power plant.

One caveat is important. Practical reasoning is inherently imprecise and fails to mirror the chiseled precision found in theoretical reasoning. Again, no conclusion of practical reasoning can match one in physics or mathematics for clarity and rigor. As Aristotle notes, we should expect no more precision from a subject matter than it allows. Contemporary theorists make a similar point. Sensemaking, as noted earlier, amounts to an exercise in approximation (Reinecke & Ansari, 2015; Weick, 1995). It is a way to explain how actors create sensible justifications in the midst of ambiguous contexts, often laden with institutional complexities. As Schön notes, executives often engage in an effective, but unstudied “reflection in action” (Schön, 1983). Consensual aspects of communicative action can often succeed even in the face of imprecision, and reaching an ethical “truce” in some instances can mark an important advance (Reinecke & Ansari, 2015).

No functional area in business schools is exempt from such practical imprecision. It is one thing to articulate the capital asset pricing model in a finance class, or to delineate Porter’s “five forces” theory in a strategy class. But it is quite another to fully justify an anticipated particular purchase of firm Z by firm X in the real world or, for that matter, to justify a particular strategic act by firm Z in a competitive environment. These are instances of practical, not theoretical, reasoning. Even the best-laid theories often fail to achieve their goals in specific application, and the process of application is the sum and substance of practical reasoning. But we cannot manage without practical reasoning. Managers must eventually act, and they hope to act reasonably. Important from the standpoint of the practical inference architecture is that a clear difference exists between better or worse decisions. Some decisions flourish; others flop. The challenge, then, is to examine practical reasoning in order to see whether it reveals a path to better decision-making. As will be shown, discovering how practical inference can sometimes fail in management and organization contexts is an important first step in discovering how to make it better.

The next step is to unpack the idea of practical reasoning in specific managerial actions. This requires extrapolating the model above. For present purposes, let us consider only organizations that adopt benefit for owners as their principal value, that is, firms that are “profit-making,” and elaborate a sample action undertaken by a sample firm. Doing so will expose common conceptual gaps that can, when analysed, inspire and guide future research.

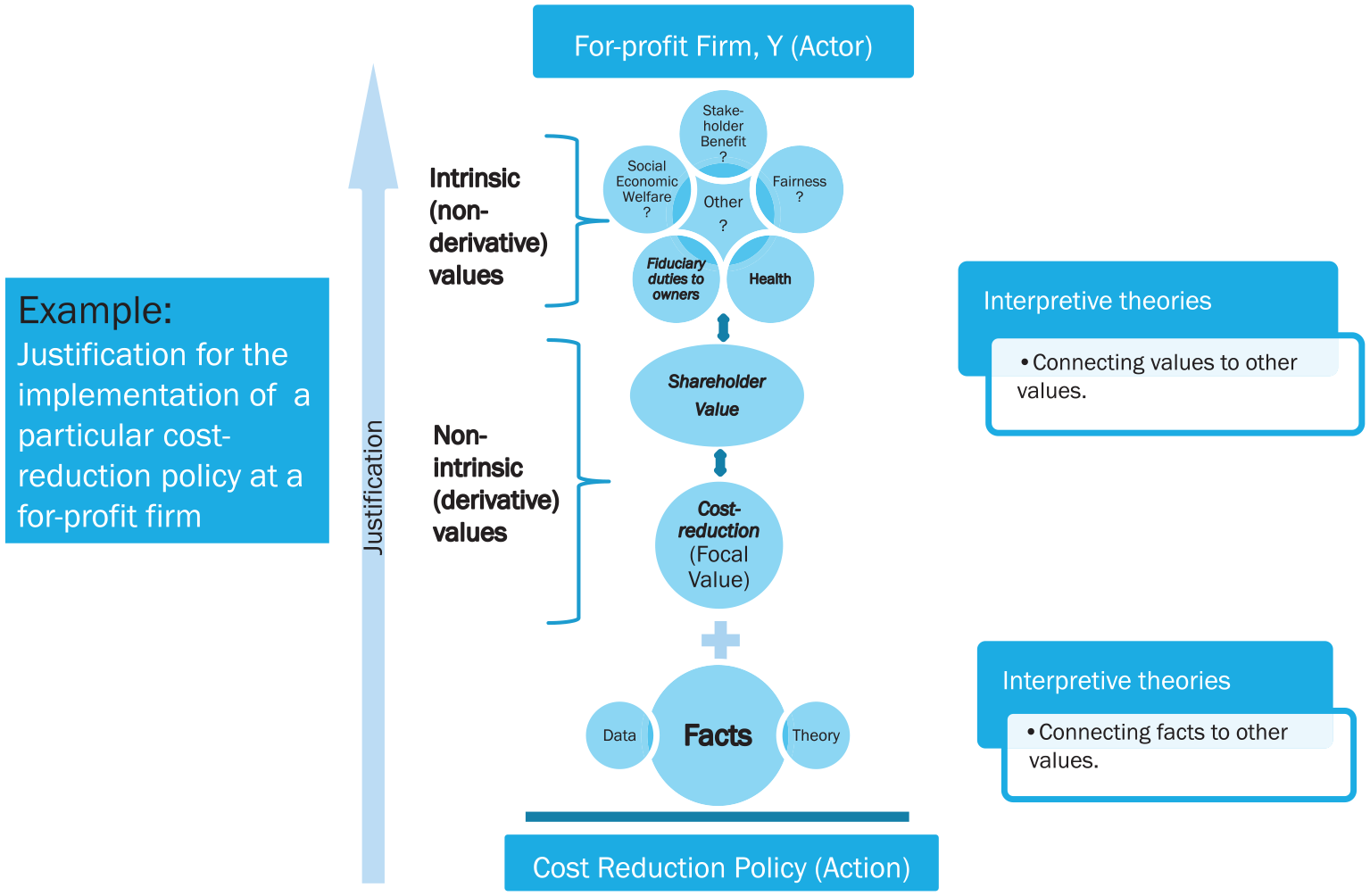

An example of practical inference in management and organization

In Figure 2, as in Figure 1, the actor may be either an individual, an organization or a collection of individuals and/or organizations. In the example shown, the actor is a business organization, firm Y, that enacts a cost reduction policy. Firm Y’s action, as noted earlier, stands in need of practical justification. The path from action to final justification can be long and complex but must connect at some point to nonderivative or intrinsic values in order for the action to be fully justified, that is, in order for it to qualify as an instance of phronesis or practical wisdom. For profit-making firms, the focal value of cost reduction is commonly justified by the immediate senior non-intrinsic value of owners’ benefit, or “shareholder value.” Consider an instance where firm Y, a local hospital, plans merging into a multihospital system in order to eliminate redundancies and reduce administrative costs for the purpose of enhancing shareholder value. Contextual facts for the merger include data about costs and staffing and theories about informational asymmetries in the development of scope economies (Dranove & Shanley, 1995, pp. 57, 62). Two obvious questions arise: (1) Are such non-intrinsic values as shareholder value capable of making an eventual connection to intrinsic values such as fiduciary duties to owners and health? (2) Are the facts such as costs and informational asymmetries capable of making an eventual connection to the same set of intrinsic values?

Displays an example of practical reasoning in a for-profit firm where the focal value is cost reduction.

Figure 2 illustrates the role of intrinsic (non-derivative) and non-intrinsic (derivative) values in practical inference. The focal value in the example is subordinated to another, more senior, non-intrinsic value, namely, “shareholder value.” The value of cost reduction, thus, is justified by its service to enhancing shareholder value. But even the non-intrinsic value of shareholder value remains orphaned unless tied to a higher intrinsic value. The example shows a potential direct line of justification that firm Y might take from shareholder value to two specific intrinsic values, namely, “fiduciary duties to owners” and “health.” However, because of the synoptic character of intrinsic values, more than these two intrinsic values may be at stake and, if so, other intrinsic values must be compatible when considered in the context of the firm’s action. For example, if the planned cost reduction policy necessitates a layoff that unfairly discriminates against minorities, the justification fails.

Shown at the top right side are value-oriented interpretive theories that help the actor understand the connections in context among different values at the value stage of practical inference. Such theories are meant to handle problems, such as the one above, where specific intrinsic values must be made compatible with other values, intrinsic or not. Again, the non-intrinsic value of “shareholder value” must be compatible with an adequate set of intrinsic values. Moreover, even at the higher level of intrinsic values, those values must be internally consistent. For example, the intrinsic value of “meeting one’s fiduciary duties” in a given context must not flagrantly violate the intrinsic value of “health.”

Shareholder value is common in formally articulated interpretive theories of management and commonly referenced by practitioners. Proponents of “mid-level” interpretive theories such as normative stakeholder theory argue that if a firm’s action satisfies the normative criteria specified by the theory, criteria that usually include not only shareholder value but other values, then the action under consideration automatically achieves intrinsic value justification. In contrast, “high-level” interpretive theories, such as utilitarianism or theories of communicative action, aim at ensuring a mutually satisfactory and compatible set of intrinsic values. They reach beyond particular goals such as shareholder value in order to establish weights and relationships among intrinsic values and arbitrate conflicts between intrinsic values, for example, between economic welfare on the one hand and fairness on the other. Shown at the lower right side of the diagram are fact-oriented interpretive theories, such as theories of strategic management, for linking facts and other values, whether intrinsic or non-intrinsic. For example, in the example mentioned above where firm Y, a local hospital, plans to enhance shareholder value through a merger with other firms, a resource-based theory of strategy (Barney, 1991) might identify costly-to-copy staffing capabilities within the broader hospital industry. Fact-oriented interpretive theories constitute methods for assembling facts for inclusion in the practical reasoning process.

Actors in practice do not always reach to a non-derivative or intrinsic level, but often settle for conventions or rough ideas of, say, “shareholder value.” Hence, helping actors make the connection between facts/non-intrinsic values to intrinsic values in order to complete the chain of justification is a promising target for management research. Some research methods may prove superior to others, as will be discussed below.

How Interpretive Theories Fill Gaps in the Practical Inference Architecture

Factor analytic or variance-based methods remain important for value analysis, but are, in effect, promissory notes awaiting redemption. In the context of practical inference, data and numbers must eventually be reconciled with intrinsic values, or otherwise remain orphaned. Even newer “divergent” methodological approaches whose conclusions are still framed in a traditional “this affects that” format must be reconciled with intrinsic values.

Interpretive theories help solve this orphan problem and address predictable gaps in the architecture of how actions are justified. Gaps exist where weak or missing connections harm the rational integrity of the overall value-creation process, and occur not only between facts and values, but also between values and other values. Interpretive theories, then, help with three kinds of gap.

A gap of the first kind raises questions such as “will this set of facts achieve firm A’s value of cost reduction?” A gap of the second kind raises questions such as “will firm A’s sensitive payment to its supplier’s agent, undertaken for the purpose of enhancing shareholder value, satisfy the intrinsic value of integrity?”; or “will firm A’s creation of an incentive structure, undertaken for the purpose of achieving cycle-time reduction, result in unnecessary physical risks to employees and thus violate the intrinsic value of safety?” A gap of the third kind raises questions such as “will firm A’s enthusiastic commitment to the intrinsic value of freedom of expression permit hateful speech to flourish and thus collide with the intrinsic value of human dignity?” This third type of gap invokes high-altitude moral concepts and for this reason is often neglected in management and organization research. But the challenges it provokes for practicing managers can be ferocious. Google’s CEO, Sundar Pachai, faced such a daunting challenge when deciding whether to fire James Damore, the author of the infamous “Damore Memo” (Hsieh, Crawford, & Mehta, 2018). In the memo, Damore argued that fewer women held key positions at Google because of gender-linked differences in their intellectual strengths and abilities. Pachai’s decision forced him to reconcile two of Google’s intrinsic values in a single decision: freedom of expression and an inclusive work environment.

Gap #1-level interpretive theories

Interpretive theories such as theories of strategy/competitive advantage assemble facts for inclusion in the practical reasoning process and make the connection between facts and non-intrinsic/intrinsic values. The most inclusive of such theories are able not only to establish connections between data and, say, the non-intrinsic value of “competitive advantage,” but also between data and intrinsic values such as “sustainability.” New interpretive theoretical approaches are reconfiguring traditional strategic theory. For example, Nonaka and Toyama interpret strategic management as a form of “distributed phronesis” that aims at “common goodness” in each particular situation. Here “common goodness” stands as the intrinsic value to be integrated with strategic data (Nonaka & Toyama, 2007, p. 371). Using a different approach but with a similar aim, Kramer and Porter’s “creating shared value” interpretation of strategy attempts to connect competitive advantage to the intrinsic value of the “advancement of economic and social conditions” in communities (Porter & Kramer, 2006, 2011). The success of Porter and Kramer’s interpretation may be questioned (Crane, Palazzo, Spence, & Matten, 2014), but its direction towards intrinsic value cannot.

Gap #2-level interpretive theories

Both “mid-level” and “high-level” interpretive theories address gap #2 between non-intrinsic and intrinsic values. Mid-level interpretive theories include normative stakeholder theory (Jones & Felps, 2013; Phillips, 2011), CSR/deliberative democracy (Scherer, 2015; Scherer & Palazzo, 2007), team production theory (Blair & Stout, 1999), social contract theory (Donaldson & Dunfee, 1999), and Pareto optimality (Jones et al., 2016; Sen, 1985). Proponents of mid-level interpretive theories argue that if an action satisfies the normative criteria specified by the theory, for example if it achieves “Pareto optimality,” or satisfies “legitimate stakeholders’ interests,” then the act automatically achieves intrinsic value justification.

Theories of corporate purpose and governance are salient mid-level theories for addressing value gaps in the practical reasoning of corporate organizations. Classic versions of these theories such as “shareholder primacy” are showing their age and are poorly-equipped to bridge gaps with intrinsic values. Newer versions of shareholder primacy are now under development (as will be explained below), but the older, classical versions yield feeble, counterintuitive outcomes when applied to intrinsic values such as sustainability or gender equity. The connection between, say, transaction cost reduction and gender equity is opaque at best and counterintuitive at worst. Newer theories of corporate governance and corporate purpose interpret focal values in terms of intrinsic values. Even before Matten and Moon (2008) contrasted North American and European approaches to CSR, and Walsh and Margolis famously criticized corporations’ socially inhospitable economic logic (Margolis & Walsh, 2003; Walsh, Weber, & Margolis, 2003), debates flourished about intrinsic values versus economic values, and which aims, which purposes, which objectives, and which ends should motivate the corporate organization. Multiple CSR interpretations that challenge the shareholder primacy model invoke intrinsic values such as deliberative democracy (O’Riordan & Fairbrass, 2008). Moreover, “stakeholder” conceptions frequently integrate conceptions of fairness and other values with stakeholder satisfaction and preferences (Blair & Stout, 1999; Freeman, 1984; Freeman, Harrison, Wicks, Parmar, & deColle, 2010; Freeman, Phillips, & Sisodia, 2020; Harrison, Barney, Freeman, & Phillips, 2019; Phillips, 1997; Phillips, Freeman, & Wicks, 2003). Social contract approaches view corporate purpose through the lens of intrinsic values such as legitimacy and fairness (Donaldson & Dunfee, 1999; Dunfee, 1998; Sacconi, Antoni, & Frey, 2011), and other efforts in the corporate purpose domain link corporate activities to long-standing concepts of intrinsic value such as “citizenship” (Moon, Crane, & Matten, 2005). Donaldson and Walsh define the very concept of “business” in terms of intrinsic values and then work backwards to understanding the purpose of individual firms. Their definition of the concept of business interprets “business success” as the optimization of “collective value,” where collective value is denominated in terms of “intrinsic values” (Donaldson & Walsh, 2015).

Even traditional shareholder primacy conceptions of governance, those that derive from neoclassical economic theory, are now being interpreted in ways that reveal a surprising connection to intrinsic values. It has always been easy to show that neoclassical conceptions of corporate governance such as agency theory and transaction cost economics (Jensen & Meckling, 1976; Williamson, 1985, 2002) rely quietly upon intrinsic values such as fiduciary duties, rights of property, and the sanctity of contracts (Donaldson, 2012). But gaps have been illustrated between these theories’ focal value of efficiency and other intrinsic values (Donaldson, 2012; Kim & Mahoney, 2005; Moran & Ghoshal, 1996). With this in mind, recent work by economists Hart and Zingales attempts to close these gaps while preserving the shareholder primacy framework. Their approach optimizes around both the financial and intrinsic moral values of shareholders (Hart & Zingales, 2017; Mejia, 2019). Other neoclassical economic theories have expanded their interpretive reach with the evolution of concepts that attempt to measure the value of “fairness,” using, for example, the Lorenz curve and the Gini coefficient (Fleurbaey, 2012).

Gap #3-level interpretive theories

In contrast, “high-level” interpretive theories such as utilitarianism, virtue ethics, distributive justice (Rawls, 1971), and communicative action (Habermas, 1984) are broad philosophical attempts that stretch beyond particular goals, such as shareholder value, in order to fix weights and relationships among intrinsic values. They attempt to arbitrate conflicts between intrinsic values such as economic welfare on the one hand and fairness on the other. For example, the weightings of intrinsic values by financial actors can vary in different cultural contexts. Firms in different cultures may exhibit different patterns of practical inference while undertaking the same action. A decision by Alibaba in China to protect customer data may be linked to China’s cultural value of social harmony, while in the US the same decision by Amazon is linked to the value of individual freedom. A particular organization at one stage of evolution may consider a set of intrinsic values to be satisfactory, and later conclude that the set is incomplete. In 2004, the founders of Google, Sergey Brin and Larry Page, consented to an interview with Playboy magazine (Page & Brin, 2004, p. 55). In the interview, the dominant intrinsic values reflected by Brin and Page were “open and free conversation” and the famous Google aphorism, “Don’t be evil.” By 2020 it was clear that no senior executive at Google would ever consent to an interview with Playboy, and Google’s corporate value “commitments” had been expanded to “including all voices” and “advancing sustainability.”

Determining whether a decision reflects an unbalanced or incomplete set of intrinsic values requires analysis at the highest level of normative reflection. In some instances, a given imbalance may be spotted by managers on the scene, as when the leaders at Google realized that Google’s values needed to include gender diversity and environmental integrity. In other cases, for example, where an imbalance exists between one culture’s values and another’s, an appeal to broad normative theories may be required. Philosophical normative theories are now being used by management and organization researchers to aid leaders who must sometimes wrestle at the highest level of practical reflection. Sandberg and Pinnington (2009, p. 1138) explain how central aspects of practical reasoning such as knowledge and understanding are integrated into a specific professional competence, using interview data viewed through an existential philosophical lens. Feldman and Orlikowski contrast empirical, theoretical, and philosophical approaches in understanding practical decision-making (Feldman & Orlikowski, 2011, p. 1240). And Tomkins and Simpson (2015) expand the Heideggerian approach to the intrinsic value of “care” into the domain of leadership, articulating a concept of “caring leadership.” In a similar vein, Spence draws on contemporary philosopher, Virginia Held (2006), to examine the implications of feminist ethics (Spence, 2016) through the concept of care. Not only Western but Eastern philosophy is now used to evaluate intrinsic values in management, for example, in Kim’s analysis of Confucian values in the workplace (Kim, 2012).

Why the Default Option for Understanding Decision-Making Fails

The challenge for any agent from the standpoint of practical inference is obvious: to use facts, theories, and individual goals (focal values) in ways that connect to values. The problem of values is so critical and so obvious that behavioral researchers are forced to address it, but have so far not succeeded. Over the past 80 years, they have addressed the problem by using the simple concept of the “preference”; it is the golden link, they assume, that is designed to complete the chain of behavioral justification. And while many interpretive theories in management and organization follow this same preference logic, 2 the pedigreed home of the preference, the place where it finds its most sophisticated articulation, is “rational choice theory.” Aligned closely to economic theory, rational choice theory (Bernoulli, 1954 [1738]); von Neumann & Morgenstern, 1944) stands proudly as the sophisticated, default model for decision-making. This is true even when, as often happens, the rational choice model is adjusted in line with the cognitive biases shown by behavioral economics. 3 Forests of academic literature have debated the strengths and weaknesses of rational choice theory, and while we cannot tramp through those forests here, the reasons why rational choice theory is an unpalatable option for reaching fully-justified choices in practical inference are clear, and also noteworthy. The key idea in sophisticated rational choice models, again, is the preference: if an individual prefers A to B, then she values A more than B (Hausman, 2013). The problem is that even though the menu served up by rational choice theory can be lengthy, the dishes are all dominated by a single ingredient: the preference. This means that all rational choice dishes taste the same.

Rational choice theory is too thin for practical reasoning because preferences, whether considered singly or in combination, miss the target of intrinsic value. Preferences fail to provide sufficient justification, i.e., reasons, for all-things-considered choices. The problem goes beyond enlightened self-interest. Even if one agrees with moral philosophers Baier (1995) and Gauthier (1986) that a form of enlightened self-interest can generate patterns of behavior consistent with morality, rational choice theory fails to offer adequate reasons for choices justified by inherent values such as fairness, privacy, and human dignity (Mitnick & Lewison, 2019). Merely acting in ways that are consistent with values is not the same as taking values seriously.

Moral philosophers debate the question of preferences, but concur that they do not add up to intrinsic values (Chang, 2000; Chang, 2002; Rabinowicz, 2012, 2017; Rønnow-Rasmussen, 2017). They extend their complaint to all other members of the family of personal properties: namely, goals, desires, attitudes, objectives, aims, interests, purposes, hopes, dislikes, likes, ambitions, intentions, and aversions. Here we recall Charles Taylor’s insight (mentioned above) that in instances where we are moved by a higher good, we sense that we are moved to value it because of what is good in it, rather than its being valuable because of our reaction. Of course, preferences can be ranked, collated, linked, and optimized. But even in the grandest of enlarged schemes, such as in the welfare equations of modern economics, simple, sun-clear intuitions about demands for human dignity and social fairness refuse deduction from their theoretical premises. Even Pareto optimal states can be morally awful. Make one person the complete owner of an entire island upon which ninety-nine other people live, and the island economy may be Pareto optimal but little better than a slave state. From a practical inference perspective, the intrinsic value of fairness is abandoned. In an important sense, we should expect nothing more, or less. To be sure, techniques of rational choice theory have dazzled in many areas of first-order organizational life and have contributed immensely to the storehouse of organizational knowledge. But brilliant results by rational choice theory elsewhere are matched by drab and dingy uses at the level of intrinsic human value, for example with topics such as warfare and environmental policy.

Moreover, to the extent that microeconomics in its most sophisticated versions relies on the notion of preferences, such as revealed preference theory (Samuelson, 1938), the analogy with rational choice theory is exact, and the problems similar. Amartya Sen, in his well-known article, “Rational Fools” (1977), shows why intrinsic values such as “commitment” cannot be understood as an ordinary preference. Amartya Sen, A. O. Hirschmann, and others note that the powerful parsimony of standard economic theory is purchased at the cost of making non-instrumental activities “undertaken for their own sake” theoretically indigestible (Hirshmann, 1985, p. 11). One can acknowledge that economic theory includes the intrinsic values of property, promise-keeping, and fiduciary responsibility in its very assumptions, but cannot deny that this meager collection lacks the breadth to justify actions that must be measured by fairness, health, dignity, and other intrinsic values. Indeed, the analysis of consumer preferences and budget limitations that takes center-stage in much of microeconomics is heavy with “indifference curves,” in which all preferences of economic agents are simply “given.” Kenneth Boulding referred to this cherished notion as the “Immaculate Conception of the indifference curve” (Boulding, 1969). 4

In all these ways, then, the predicament that intrinsic value discovers within modern business schools is akin to the “opt-in,” “opt-out” problem for internet consent. The “default” selection is that of rational choice leavened by the conceptual quirks of behavioral economics (see Notes 2 and 3), and not “reasoned choice.” The result is that business students must “opt out” of the rational choice model. A better standard would involve an “opt-in” standard where business school students were allowed more than one set of models to opt into for different contexts, and where at least one of those choices included a wider palette of intrinsic values. The failure of the model points to the need for a replacement. The practical inference approach not only avoids the flaws of the rational choice model, but has the added advantage of framing management decision-making in day-to-day terms such as “shareholder value,” “fiduciary duty,” “integrity,” and “sustainability,” with important implications for what those values mean for the behavior of actors.

The failure of rational choice illuminates also a systemic flaw in the way we undertake management and organization research. Nearly every published academic journal article, whether factor analytic at its core or otherwise, makes implicit reference to at least one intrinsic value, namely, economic welfare. Economic welfare, transcribed through intermediary values such as profit, shareholder value, fiduciary duty, and efficiency, is the unspoken intrinsic value supporting most business research from the standpoint of practical reasoning. And this picture rates respectably well: it deserves four out of five stars. Business makes its distinctive contribution to intrinsic value by leveraging the three distinctive channels of economics, i.e., production, exchange, and distribution, in the service of economic welfare (Donaldson & Walsh, 2015). In turn, management and organization research’s principal contribution to practical reasoning is deemed to be economic prosperity, not fairness, dignity, or rights. But it is not a five-star picture. The problem is that placing economic welfare in the foreground of the intrinsic value picture of management and organization blocks our view of the background, one colored by other intrinsic values such as fairness, voice, privacy, and dignity. The background of Van Gogh’s Starry Night is as important as its foreground. Backgrounds bear scrutiny.

What a Practical Inference Approach Means for Research in Business Ethics

The practical inference view illuminates two prominent areas of current research: business ethics and the broader field of management and organization research. Consider first business ethics. One well-known factor analytic approach in business ethics is “behavioral ethics,” with a heavy emphasis on quantitative data, factor-analysis, variance studies, and thin descriptions. Do its findings align with the practical inference architecture described above? The answer is that, yes, behavioral ethics contributes to the practical inference process, but only to a point owing to the narrowness of its methods and limitations of its quest. It is helpful to see why.

Behavioral ethics stands at the fact-oriented level of the practical inference pyramid, and offers information for firms and individuals to use in the value-creation process. Most of its factual contributions point out human biases. The fruits of behavioral ethics in this sense are largely negative, as in its parent field of behavioral economics (Tversky & Kahneman, 1973). They identify biases, not reasons; failures, not successes; mistakes, not achievements (Ariely, 2008, 2012; Bazerman & Tenbrunsel, 2011). The take-aways are typically about “blind spots” such as general self-serving biases (Tenbrunsel, Diekmann, Wade-Benzoni, & Bazerman, 2010), distance biases (Wade-Benzoni & Tost, 2009), look-back biases (Shu & Gino, 2012), beneficence biases (Gino, Ayal, & Arielyet al., 2013), and conflict of interest biases (Moore, Tetlock, Tanlu, & Bazerman, 2006). Both behavioral economics and behavioral ethics can be seen as articulating in behavioral terms what the Greeks called “akrasia,” that is, the allowing of a mere preference or emotion to go against reason (Aristotle, 1962, pp. VII.1–10), in which system 1 thinking, the faster, emotional kind, can be corrected by the slower and more logical system 2 thinking. Hence, behavioral ethics, despite the narrowness of its methods, contributes to value creation, but only to a point. “Blind spots” can inform choices in the service of fairness or honesty, and “nudges” can be used for “good.” But only with special assistance.

Like Google Maps; biases in behavioral ethics can help the traveler, but also like Google Maps, cannot choose the destination. The problem of choosing the destination relates to the “gaps” discussed above in the value-creation chain. In research design, the destination, or “focal value,” is chosen at the outset by the designer of the study. Consider a behavioral ethics study whose focal value is honesty. “Honesty” must be defined for the sake of measurement. Behavioral ethics studies usually do so in terms of certain patterns of behavior such as not inflating one’s success on a paid task, say, by counting the number of dots on one side of a line (Gino & Ariely, 2012). Two obvious gaps in the inference chain of value creation arise: first, how does the focal value of “honesty” fit with higher-order focal values such as shareholder value? and second, how does honesty as measured by the study relate to both the intrinsic value of honesty and the synoptic requirement of compatibility with other intrinsic values? Suppose that a higher level of honesty in firm A damages rather than increases shareholder value, which happens to be firm A’s top-level focal value. Should more dishonesty be allowed? Or suppose that honesty as defined in the study clashes in practice with other intrinsic values. Perhaps firm A’s new policy to enhance honesty involves harsh punishment for offenders in a division of the firm overwhelmingly staffed by women and people of color. Here the achievement of honesty might clash with the value of fairness. On both questions, a behavioral ethics approach remains mute. To give voice to such issues, a behavioral study would need to confront intrinsic values head-on, as rational justifications for action. But a behavioral study, like all factor analytic studies, cannot confront full-bodied justifications head-on because its methods lack the proper tools. It is no surprise that behavioral ethics has virtually nothing to say about contemporary moral dilemmas such as autonomous cars in which choices about intrinsic values must be made between saving the life of a single driver and the lives of multiple pedestrians.

An advantage of a practical inference view is that it can connect factor analytic research in areas such as behavioral ethics to values through specialized interpretive theories having a normative focus. Consider the problem above of whether an autonomous vehicle should be programmed to save the life of a single driver or multiple pedestrians. Behavioral ethics can identify biases relevant to this problem such as “bounded ethicality” (Bazerman & Tenbrunsel, 2011); biases prompted by implicit associations about gender, race, and other demographic groups. Such biases are confirmed in MIT’s “moral machine” factor analytic study that gathered 40 million decisions from people in 233 countries and found that on average people preferentially spare women over men, athletes over overweight persons, and executives over homeless people (Awad et al., 2018). Such preferences are “biased” insofar as they clash with the simple intrinsic value of “equal human worth.” However, jettisoning preferences entirely in the design of autonomous vehicles seems hasty insofar as preferences can aid the cultural adoption of technology (citizens must agree with a solution to adopt the technology), and because preferential differences may identify a need to sometimes relax the “equal human worth” principle. For example, respondents in the MIT survey happen to preferentially favor children over very old adults, and law-abiding pedestrians over law-breaking pedestrians, and their doing so may not be wrong. This challenge, now discussed in technology journals under the heading of VA (value alignment), implies the need for a hybrid, or “factor analytic +Plus,” approach that aligns values in machines and people in a way that combines bottom-up factor analytic preferences with top-down interpretive theories. This is the approach taken by Kim, Hooker, and Donaldson (2021) who make use of the behavioral ethics literature while proposing that designers of VA systems incorporate ethics by utilizing a hybrid approach in which both ethical reasoning and empirical observation play a role. Factor analytic findings are coupled with normative interpretive theory. Machine learning systems trained by lay people’s perceptions are coupled with formalized normative principles, e.g., double-effect theory and categorical imperatives, through the use of quantified modal logic. In this way, the authors are able to generate test propositions for any given action plan in an AI rule base (Kim et al., 2021).

Another advantage of the practical inference approach is that it directs the researcher to discover how divergent research can help satisfy practical inference requirements by connecting behaviors to intrinsic values directly. For example, Gehman and colleagues (2013) investigate the development of an honor code in a large business school over a ten-year period by focusing upon the emergence and performance of “values practices.” The values are framed by the researchers explicitly in terms of intrinsic values: “By values practices we mean the sayings and doings in organizations that articulate and accomplish what is normatively right or wrong, good or bad for its own sake – a position that resonates with Aristotle’s Nicomachean Ethics” (Gehman et al., 2013, p. 84). By collecting data from archival records, ethnographic observations, and stakeholder interviews, and by zeroing in on moments of controversy among stakeholders, the study is able to focus on values practices in processual terms unfolding over time (Gehman et al., 2013, p. 87).

Finally, a practical inference approach shows that the problem of “all facts and no values” has a corollary problem: “all values and no facts.” Just as over-attention to simple facts can decouple values, over-attention to intrinsic values can decouple facts. A preoccupation with intrinsic values produces theoretically robust, but practically sterile, conclusions. When forgotten by researchers, this has been called the “normativistic fallacy” (Schreck et al., 2013), and is the flip-side of the “naturalistic fallacy” or attempting to derive an “ought” from an “is.” Consider the value-heavy issue of the “moral agency” of corporations. Business ethics journals regularly feature articles that investigate whether the corporation is a full-fledged “moral agent” (Sepinwall, 2015). Such articles investigate whether a corporation can enjoy the moral right of free political expression or religious freedom. But even though the analysis of moral agency and legal personhood are important in framing value-creating decisions, such analysis cannot by itself yield reasoned decisions in the absence of facts and context. Whether Chic-fil-A should close all its locations on Sundays to support a Christian outlook is not a question answered adequately by whether or not Chic-fil-A is a moral agent. What are the contextual facts? Might the policy bankrupt the firm? Might the policy in some contexts clash with Chic-fil-A’s focal value of “being a part of our customers’ lives and the communities in which we serve”? What do the data say about customer reactions to firms that espouse religious views? From a practical inference perspective, values without facts are blind.

This all highlights the need for increased attention to how business ethics research fits with genuine value creation. It also implies the importance of a division of labor among topics and methods of research both in the field of business ethics and in the broader field of management and organization research. It is to this broader arena that we now turn.

What a Practical Inference Approach Means for Management and Organization Research

Two broad epistemic doors now open to management and organization research, both of which expose the value-creation quandary. The first may be understood loosely as a factor analytic approach, one that emphasizes quantitative methods and variance-oriented analysis. It was inspired by the emphasis on scientific methods in the mid-twentieth century that placed management and organization research on a path of unity with broader science (Khurana, 2007). The second was pushed open by researchers who felt cramped by the methodological narrowness of the traditional approach (Bennis & O’Toole, 2005; Ghoshal, 2005; Mintzberg, 2004), and opens to a promising mix of methodological strategies including narratives, causal mechanism, philosophical analysis, “thick” explanations, typology, semantics, syntactics, synthetic control groups, and qualitative comparison analysis. Yet neither approach fully explains the significance of values in value creation.

A practical inference perspective on management and organization research means more than adding intrinsic values to old recipes. It means new recipes that can relate facts to values in the context of practical reasoning, recipes inspired by the vision of agents creating value in the fullest sense. Hence, a practical inference approach realigns research towards two distinct lines of explanation: justification and causation. In organizational theory this approach elevates the idea of “process” to the most salient feature of value creation. As Tsoukas reminds us, the shared acknowledgment by researchers that organizations can be seen ontologically both as an entity and a process should be laid against the truth that organizations must be known epistemologically through patterns of relations and organizations enacting patterns of relations (Tsoukas, 2017, pp. 136–137). Unfortunately, the price tag for more process is sometimes more complexity.

Complexity can be taken to extremes, as Tsoukas may be prone. In his article, “Don’t simplify, complexify,” he recommends a complex “system of picturing” that “consists of an open-world ontology, a performative epistemology, and a poetic praxeology” (Tsoukas, 2017, p. 132). The researcher should see “every drop of experience” as a novel reconstruction of experiences from which the drop emerged (Tsoukas, 2017, p. 147). The researcher should treat organizational activity as “non-trivial action,” in contrast to the dominant view in which behavior obeys decision rules that generate predictable behavior. “Insofar as organizations consist of interacting nontrivial agents,” Tsoukas writes, “they have emergent properties too, which cannot be mapped out in advance. The future is open,” and “unknowable in principle” (Tsoukas, 2017, p. 145).

Unfortunately, this enthusiasm for complexity places it on a collision course with simplicity, the regulative ideal which, along with explanatory power, coherence, and predictive power, is a hallmark not only of theoretical but practical reason (Kuhn, 1962; Urry, 1973). The future is not in principle unknowable. A CEO’s discovery of a simple, decision-making value such as “always scan for environmental sustainability” may make her actions more predictable even as it helps her actions better fulfill the demands of practical reasoning. Practical and theoretical reasoning alike seek an economy of interpretation: parsimony. The entire universe of data picturing an agent’s context at a given time is theoretically speaking, unfathomable, just as an infinitely nuanced list of values is, practically speaking, unusable. The high-resolution photograph of a territory is not a map.

An advantage of a practical inference view is that it separates good complexity from bad, where good complexity is seen to foster wise decision-making and bad retard it. Good complexity enhances the integration of the reasons (values) of the agent and the facts (correlations, regularities, and context for the act). Overcomplexity can short-circuit value creation by denying finite agents the requisite simplicity for knowledge and action. However, oversimplification of the agent’s particular context, as Tsoukas correctly notes, can disassociate that context from the aims (values) of the agent resulting in the failure of the value-creation process. The department chair of a prominent finance department once confided to me misgivings about the financial theories used by Wall Street bankers in the run-up to the 2008 financial crisis. “I’ll tell you how the bankers got those theories,” he exclaimed in exasperation, “we taught them those theories!” Whether financial theories should, like bottles of aspirin, carry warning labels about simplifying assumptions is an intriguing question. Regardless, simplifying assumptions discarded from the process of value creation are perilous.

Reframing studies

To avoid orphaned conclusions and to bridge other practical inference gaps, researchers should reconsider well-worn habits of manuscript preparation. The dominant form of published management and organization research currently, whether factor analytic or not, is of the form, “X affects Y.” It is almost never “Action X is justified by reason Y.” In terms of the value-creation model displayed in Figure 1, this means that most published management and organization research emphasizes the causal, top-down arrow of value creation instead of the justificatory, bottom-up arrow, and focuses on the lower, derivative value segment of practical inference instead of the upper, non-derivative value portion. To some extent this is understandable. However, a need exists for studies to better connect “X affects Y” findings to the entire two-directional value architecture. Notably, researchers can offer conclusions to practitioners as either mere tools, or something more. Published studies vary along a spectrum with fully segregated studies at one end and fully integrated studies on the other. Studies with partially integrated findings lie in between. A practical inference perspective encourages researchers to move their findings along this integration spectrum toward the “integration” end.

The most common form of published study today is a factor analytic, fully segregated kind, such as Odziemkowska and Henisz (2021). These studies omit all reference to an agent’s potential value-creating opportunities. However, many studies attempt partial integration by reviewing opportunities for value connections in their “discussion” or “implications” sections. In a special section entitled “practical implications,” authors Mitra, Post, and Sauerwald in “Evaluating Board Candidates” (2020) connect their work directly to intrinsic values. Our study, they write, “holds practical relevance for female directors, firms seeking to address gender disparities on their boards, advocates for female leadership, and board advisory organizations” (Mitra et al., 2020, p. 104). Least common but rising in number are fully integrated studies that integrate findings fully with a practical inference architecture, sometimes through the use of normative interpretive theories and moral psychology (Gu & Neesham, 2014). For example, Gossy uses a normative conception of stakeholder welfare extending beyond shareholders and debtholders to construct a risk management rationale for corporate finance decisions that is further informed by his analysis of data from Austrian and German industrial companies (Gossy, 2008). For fully integrated studies, the intrinsic value concepts need not derive from traditional interpretive theories such as “CSR,” “stakeholder,” or “social contract.” They may, instead, derive from the intrinsic values embedded in aspirational global goals, such as the United Nations Sustainable Development Goals. For example, Hughes et al.’s study of the migrant population and poorly paid farmers in India shows how blockchain technology could offer significant benefits for farmers and BPL Indian citizens while at the same time supporting UN sustainable development goals (Hughes et al., 2019, p. 128).

In sum, it is not a mark of honor that a study lacks prescriptive significance. Focusing on integration allows a combination of positive and normative social science. Even factor analytic studies are capable of finding ways to connect to the practical inference requirements of value creation. As management and organization scholars, our habit of waiting until the closing “discussion” section merits rethinking. The farther along the spectrum of value-creating integration that an article’s entire reasoning moves, the better.

A division of labor

A practical inference approach encourages attention to value-laden topics, and entails a division of labor in studying them. It thrusts obvious topics to the center of the research table: those that either risk intrinsic value imbalances or are already denominated in terms of intrinsic values. Researching them often requires special skills from mainline disciplines including psychology, law, sociology, philosophy, history, and economics, as well as from functional areas such as marketing, finance, accounting, and organizational behavior. Consider the topic of algorithmic transparency in AI and machine learning algorithms, an issue which exposes a potential imbalance among the intrinsic values of fairness, trust, privacy, and accountability. Fairness demands that algorithmic bias against marginalized groups be avoided; trust, that consumers be handed more than a black box; privacy, that sensitive information be protected; and accountability, that algorithms be auditable. Even the intrinsic value of human health becomes an algorithmic issue, in the form of algorithmic “addiction.” Advancing our understanding of such an issue requires a mix of disciplinary talents, including psychology, philosophy, and economics, as Bhargava and Velasquez (2020) demonstrate in their work on algorithmic addictiveness.

This division of labor includes the use of divergent research methods to close gaps in the practical inference process. We have seen that interpretive theories close gaps for both factor analytic and alternative qualitative research approaches. But whereas “factor analytic” variance-focused methods have clear advantages in achieving sophisticated measurement of management and organization phenomena, and while factor analytic theories can be connected eventually to intrinsic values through the use of interpretive theories, other “divergent” approaches have advantages in the areas of linguistic robustness and contextual complexity. The language of such divergent studies frequently fuses moral and descriptive qualities in a way that permits facts to become intertwined with values – even at the data collection stage. This is the so-called language of “thick value concepts” that practicing managers often use in value-laden situations (Van der Linden & Freeman, 2017, p. 353). In contrast, a factor analytic approach is less linguistically agile because its limited conceptual range omits two valuable modes of knowledge, thick description and pattern description (Cornelissen, 2017, pp. 378–379). In this way, the richer language of divergent, qualitative methods can sometimes highlight the “synoptic” requirement of practical inference discussed above, even as it better displays complex value motivation from an agent’s experiential perspective.

Divergent methods can help explain how firms actually engage in the various stages of practical reasoning, and how firms make new discoveries about value creation. The process by which a manager or organization comes to a deeper understanding of inclusive value creation, or comes to engage a new set of practices that satisfies genuine value creation, remains largely mysterious today. Yet the topic of value discovery has already been championed by divergent researchers, showing how new methods can reach into the evolutionary patterns of experiential discovery. Methods of process, moral theory, communicative analysis, semantics, narrative, interview, thick description, history, syntactics and others, can sometimes capture value-creation issues that leave narrower, quantitative methods tongue-tied. Communicative and deliberative analysis, for one, has emerged as a powerful method of analysis and helped illuminate the discovery process at the level of actors (Scherer, 2015; Scherer & Palazzo, 2007). So too can experiential analysis. For example, Kolb’s work on experiential learning advances a “cycle” concept of experiential learning moving from concrete experience through reflective observation and abstraction to active experimentation (Kayes, Kayes, & Kolb, 2005; Kolb, 1984), and this approach is in line with ongoing calls to give managers the opportunity to learn from their own experience (Mintzberg, 2004). In a similar experiential vein, postmodern scholars have used “high-involvement” research designs (Cunliffe, 2003; Shotter & Katz, 1996). Other scholars routinely elicit descriptions from the manager’s first-person perspective (Argyris & Schon, 1974); and still others articulate the logic of practice in studies of organizational events (Feldman, 2000, pp. 620–626). These studies speak to the totality of practitioners’ experience in the context of action, and, from a practical inference perspective, allow asking questions about the discovery of “better and worse” value creation.

Value imbalances appear in many other contexts of management and organization research, such as in global value chains where intrinsic values such as human rights and religious or ideological norms clash beyond borders. Skills in organizational theory, marketing, and strategy must be honed for such topics. Even within countries, populism and polarization pose special challenges for reasoned value creation, as the US firm, Dick’s Sporting Goods, discovered when it was criticized for being on the wrong side of “gun rights,” or Nike learned when its 2018 advertisement featuring Colin Kaepernick was accused of being “unpatriotic.” Attempts to help corporate actors navigate the shoals of such value challenges, such as Mayer and Baird’s (2021), show the benefits of specialized knowledge in legal theory, corporate governance, social contract theory, and marketing. We can anticipate that a turn towards practical inference research will fuel not only studies about traditional interpretive theories such as corporate purpose or strategy, but about global efforts that formalize intrinsic values through policies and agreements, such as the UN sustainable development goals, United Nations Global Compact, the International Organization for Standardization (with its ISO 14000 series on environmental management), and AccountAbility (with its AA1100 sustainability, assurance and, stakeholder engagement standards).

New areas of research opportunity

New opportunities for research are visible on the horizon of the practical inference framework. Many pressing societal areas for research are already denominated in terms of intrinsic values, such as LGBTQ+, gender, work-life balance, free speech, employee privacy, obesity, and sustainability. These issues are obvious. Less obvious, however, are issues about industries denominated in terms of intrinsic values, such as healthcare, legal services, and education. From the vantage point of practical inference, the existence of such industries implies a need to investigate whether interpretive theories, including those of strategy and corporate purpose, should move to automatically include the industry’s relevant intrinsic value alongside shareholder value as firm goals. Can a healthcare, legal services or education firm satisfy the value requirements of the practical inference perspective without embodying the goal of advancing health, justice or knowledge (Donaldson, 2019)?

The agent-centered practical inference framework also highlights a fact obscured by non-agent centered research: how agents are sometimes motivated by intrinsic values in a collective context. Stakeholders of firms, collections of firms, and entire industries can be galvanized through the shared purpose of health or environmental integrity. During the pandemic that began in 2020, biotech firms, old-line pharmaceutical companies, hospitals, and medical supply manufacturers (producing ventilators, masks, and other breathing devices) cooperated to develop and distribute new vaccines for Covid-19 (Crick & Crick, 2020, p. 210). Not all of the collective behavior of these firms could be explained using simple calculations of optimized self-interest. Notably, the practical inference framework’s definition of an “agent” includes not only individuals, or firms, but collections of individuals and firms. Future research may shed light on what happens when entire collections of stakeholders, or collections of firms, engage in practical reasoning inspired by intrinsic values.

Conclusion

A practical inference framework sees value creation as a creative process of practical reasoning guided by values. The goal of value creation is to achieve wise, all-things-considered behavior justified in terms of intrinsic values. Management and organization epistemology is at its best when it moves closest to actors and agency in context, the lynchpin of professional knowledge. A practical inference perspective avoids untethered orbits of research with no gravitational pull from the center of practical reasoning, which, at least for business school contexts, is value creation in its fullest sense. A proper model of value creation, as we have seen, displays two directional arrows: an “up-arrow” of justification and a “down-arrow” of causation. A practical inference view recenters research around this bi-directional concept.