Abstract

This study aims to determine the impact of COVID-19 on air connectivity in the Association of Southeast Asian Nations (ASEAN) region, specifically focusing on infection, vaccination and fatality rates. To examine the impact of COVID-19 on the ASEAN air transport industry, a panel data series was created. The panel covered data from 57 airlines with different business models in the 10 ASEAN member states from January 2019 to July 2022 (31 months). The results of the study have shown that there is a significant inverse linear relationship between full-service and low-cost international flight movements, passenger demand and vaccination rate, infection rate and fatality rate. At the country level, Brunei experienced the lowest drop in air passenger demand, followed by the Philippines, Thailand, Malaysia and Cambodia. Other countries (Indonesia, Lao PDR, Myanmar, Singapore and Vietnam) were not significant predictors of passenger demand. The study’s results have indicated that an increase in infection rate has a greater impact on the international air travel market compared to the domestic market. The reduction rate of the domestic market is only half that of the international market, while the fatality rate demonstrated no differences. This study represents a valuable contribution to the existing knowledge of the pandemic’s impact on the air transport industry, focusing on Southeast Asian countries. It provides evidence to help stakeholders in the aviation industry prepare for future related crises. The study concludes that fostering greater cooperation and coordination among ASEAN member states in managing health crises and facilitating the aviation industry can promote economic growth, enhance resilience and strengthen regional integration in the long run.

Introduction

The COVID-19 pandemic has had a profound impact on the global economy, leading countries to implement various policies aimed at slowing down the spread of the virus. These measures have included quarantine requirements, social distancing measures, mandatory vaccinations, domestic lockdowns and border closures (Busato et al., 2021; Law & Katekaew, 2022; Shin et al., 2022). Both the economy and the population of affected countries have been significantly affected by the pandemic. Reduced business activities have resulted in increased unemployment rates as companies have downsized and implemented temporary and permanent layoffs (Parkinson, 2021). The aviation industry has been particularly hard-hit by the pandemic, with government policies causing significant disruptions to air travel. Travel restrictions have effectively halted passenger air transport, and although most airlines have continued to operate, flight frequencies have been drastically reduced due to limited travel demand (OECD, 2020b). The ASEAN (Association of Southeast Asian Nations) region, which was previously experiencing rapid growth in aviation, has been severely impacted. According to a report by the Asian Development Bank (2023), total passenger traffic in Southeast Asia increased by over 150% from 200 million passengers in 2009 to over 510 million passengers in 2019. This growth was mainly attributed to the rise of the middle class and efforts to liberalise the aviation market (The ASEAN Post, 2019). However, the pandemic has brought the ASEAN aviation market to a standstill, with extensive quarantine requirements and border closures making air travel nearly impossible. During the pandemic, 9 out of 10 ASEAN countries closed their borders, and 5 countries imposed strict lockdown policies, according to the Organisation for Economic Co-operation and Development (OECD, 2020a).

As travel demand has plummeted, airlines in the ASEAN region have downsized their operations, with some facing financial difficulties and others filing for bankruptcy or ceasing operations. Thai Airways International, Philippine Airlines and Thai Air Asia X have filed for bankruptcy protection in May 2020, September 2021 and May 2022, respectively. Additionally, Nokscoot ceased operations in June 2020, and Garuda Indonesia faced the threat of bankruptcy during the COVID-19 era (Damayanti & Shibata, 2022; Kotoky, 2022). The governments in the ASEAN region have implemented strategies to promote domestic travel and establish designated international travel corridors, with the aim of supporting their economies and employment rates. These initiatives have effectively stimulated the aviation industry, attracting more people to travel (Menon, 2020). Singapore, facing a lack of domestic tourism, has entered into special travel corridor agreements with various countries. These agreements include New Zealand and Brunei in September 2020, Germany in September 2021, South Korea and the USA in October 2021 and Malaysia, Sweden, Finland, India and Indonesia in November 2021 (Global Monitor, 2022). By March 2022, the ASEAN countries have begun reopening their borders, leading to a resurgence in air travel demand. However, the Southeast Asian economy is expected to recover at a slower pace compared to other countries in the Asia Pacific region due to its lower vaccination rate (Asian Development Bank, 2021). The recovery process for ASEAN countries is anticipated to be more protracted, given the varying levels of development and government response policies. Developed nations with greater resources and well-established infrastructure are expected to recover more effectively than developing nations (Daly et al., 2020). Governments in the ASEAN region have responded differently based on cultural differences, degrees of government authoritarianism, public solidarity and trust in the government (Khor, 2022). A study conducted by Purnomo et al. (2022) has concluded that Thailand was the most prepared in mitigating the pandemic compared to other ASEAN countries, while Brunei and Singapore have achieved the highest vaccination rates (Chu et al., 2022). These factors significantly impact the recovery time from COVID-19.

Consequently, conducting a study to evaluate the impact of COVID-19 on the air transport industry in an integrated region facing challenges in planning and policymaking is crucial. This study aims to determine the effects of COVID-19 on air connectivity in the ASEAN region, focusing on infection, vaccination and fatality rates. The findings of this study will provide valuable evidence for stakeholders in the aviation industry to prepare for future crises. Notably, there has been no previous study focusing on the resilience of the air transport industry in the ASEAN region. Therefore, this study represents a valuable contribution to the existing knowledge of the pandemic’s impact on the air transport industry, particularly in Southeast Asian countries, emphasising the importance of greater cooperation and coordination among ASEAN members.

Literature Review

Over the past few decades, the air transport industry has been significantly affected by various global incidents. These incidents include the terrorist attacks in New York and Washington in 2001, the SARS outbreak in 2003 and the global financial crises between 2007 and 2008, all of which caused major disruptions and downturns in the global economy (Button, 2008). However, the COVID-19 pandemic in 2020 has had the most severe impact on the air transport industry, particularly on airlines, compared to other aviation subsectors (Bouwer et al., 2022). The implementation of entry restrictions by many countries to control the spread of the virus has brought the airline industry to a complete halt. In response to these incidents and crises, studies on aviation recovery have been conducted to help stakeholders review their response policies and provide recommendations for future events. For example, Kim and Gu (2004) studied the return and risk of airline stocks after the 9/11 attacks, while Clark et al. (2009) examined the recovery level of U.S. airlines after the same incident. Previous studies have also focused on the recovery from the SARS outbreak in 2003, such as Min’s (2005) examination of the tourism industry in Taiwan, which found that the recovery period was prolonged even after the World Health Organization removed travel advisories. Additionally, Rittichainuwat and Chakraborty (2009) defined changes in travellers’ behaviour in Thailand after the impact of terrorism and diseases, highlighting the increased perceived risk and the long-lasting effects of these changes. Opera (2010) conducted a study on the impact of the global economic crisis on the air transport industry in Europe. The results indicated that air transport confidence recovered much faster during the 2009 pandemic influenza compared to the recession in 2007. Martin and Wang (2021) examined the determinants of profitability in the U.S. domestic airline industry during the COVID-19 era. The COVID-19 pandemic differs from previous incidents and events in terms of duration and severity. According to an IATA report, it typically takes around five years for the air transport industry to recover from short-term disruptions, and longer-term disturbances will require even more time (Oxley & Jian, 2015). After the 9/11 attacks in 2001, it took nearly six years for airlines to fully recover, and the short-lived SARS outbreak between 2002 and 2003 took over a year for the industry to bounce back in most countries (Sehl, 2020). In the early stages of the COVID-19 pandemic in 2020, countries in the Asia Pacific region performed relatively well in containing the virus due to their previous experience with SARS. However, as the virus spread globally, it had a significant international impact.

Changes in Travel Behaviour

The COVID-19 pandemic has had a significant impact on air travellers’ behaviour, with travel demand directly influenced by the number of confirmed cases. U.S. airlines have observed a decrease in travel demand as COVID-19 cases increase (Josephs, 2021). Engle et al. (2020) conducted a study that found a direct relationship between the infection rate in the U.S. market and mobility demand, with a 2.31% reduction in mobility for every 0.0003% increase in the infection rate. Similar findings were observed in the South Korean and Chinese markets, where Korean air travellers only considered resuming overseas travel when the number of confirmed cases decreased (Song & Choi, 2020), and Chinese domestic tourists avoided destinations with more confirmed cases than their origins (Li et al., 2021). Yilmazkuday’s (2020) study concluded that people staying in the same country have the potential to reduce COVID-19 cases and deaths. Additionally, travellers tended to avoid countries with high death rates due to COVID-19, resulting in a decreased demand for tourism services (Okafor & Yan, 2022). During the pandemic, most people reduced their travel and avoided using public transport due to concerns about prolonged exposure and increased transmission risk (De Vos, 2020). The mortality rate of the pandemic was found to be directly associated with international travel demand (Pana et al., 2021). Public transport was identified as a significant factor in the domestic spread of COVID-19 (Zheng et al., 2020), while air transport played a role in spreading the virus internationally (Wang, 2022; Warnock-Smith et al., 2021). According to a study by Ciuffini et al. (2021), the recovery rate of public transport has been slower in Italy, Germany, Canada and the United States compared to private transport modes. The use of online platforms for conferencing and virtual meetings has become more prevalent during the pandemic, leading to speculation that business travel may not fully recover to pre-pandemic levels (Lofthouse, 2022).

The introduction of COVID-19 vaccines in March 2021 has had a significant impact on travellers’ behaviours (OECD, 2021). As governments have made significant progress in immunising their populations, leading to higher vaccination rates, they have begun to relax border closure restrictions, and international mobility has gradually returned. A study by Guo et al. (2022) has found that the effectiveness of COVID-19 vaccines is closely related to human behaviours. The authors concluded that there is a positive correlation between vaccination and mobility. High vaccination rates and increased safety measures have been key factors in rebuilding travellers’ confidence in air transport (ACI, 2022). According to a report by CAPA (2021), air passenger confidence has been improving with the rollout of vaccines, and rebuilding confidence levels is crucial for the industry’s recovery. Similar result was observed in Korea, where vaccination rates were identified as a major factor demonstrating significantly positive influence on Korean air travel confidence (Kim et al., 2022). However, a study by Rowland (2021a) observed that there was no direct relationship between increasing vaccination rates and the growth of international air travel. The recovery of international air travel has been driven by a country’s ability to manage infections effectively.

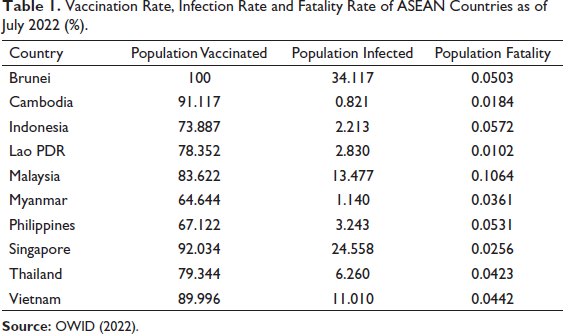

According to Our World in Data (2022), as of July 2022, the average vaccination rate in ASEAN is 82.01%, with an average infection rate of 9.97% and an average fatality rate of 0.04%. Table 1 provides the specific vaccination, infection and fatality rates for each member state of ASEAN as of July 2022.

Vaccination Rate, Infection Rate and Fatality Rate of ASEAN Countries as of July 2022 (%).

Industry Resilience

Resilience refers to the ability to recover after disruptive events. Several previous studies have examined various aspects of resilience in the air transport industry in the post-COVID-19 era. Gudmundsson et al. (2021) used the Auto-Regressive Integrated Moving Average (ARIMA) model and forecasted that it would take approximately 2.4 years for the industry to recover. However, Weston et al. (2022) presented a different perspective, concluding that the industry would not return to pre-pandemic levels until late 2025 due to the relationship between infection rates and flight availability. The speed of recovery also depends on airline decisions and external factors such as the business environment and political impacts. Liao et al. (2022) compared the recovery patterns of the Chinese low-cost carrier market after the COVID-19 pandemic and found that while these carriers were recovering quickly, they were unable to fully restore operations to pre-pandemic levels. The rapid recovery was attributed to a low number of confirmed infections, the resumption of interprovincial tours and increased government support in a deregulated business environment. Similar observations were made in a study on the impact of COVID-19 on global air traffic by Suau-Sanchez et al. (2020), which concluded that the pandemic would have long-term consequences for the industry, including downsizing in terms of the number of airlines, flight frequencies and served routes. Regarding tourism demand, Zhang et al. (2021) used autoregressive distributed lag (ARDL) models and predicted that countries in the Asia Pacific region would recover faster compared to North American and European markets. However, Rowland’s report (2021b) presented a different view, suggesting that due to low vaccination rates and a lack of regional cooperation, the recovery speed in the Southeast Asian region would be the slowest among all continents. The lack of government trust in developing countries is creating hurdles in policy implementation, leading to delayed government actions (Soto-Mota et al., 2020).

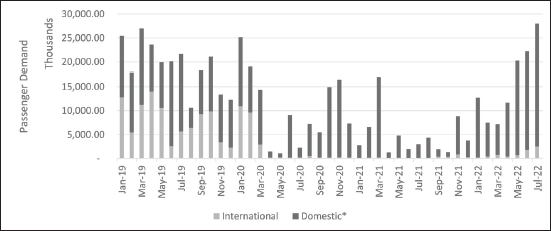

Figure 1 illustrates the passenger demand of ASEAN member states. Following the declaration of COVID-19 as a pandemic by the World Health Organisation on 11 March 2020, international passenger demand experienced a significant decline. This was accompanied by a surge in country-enforced border shutdowns and travel restrictions, leading to a sharp decrease in demand and subsequent flight cancellations by airlines. In response, airlines operating in countries with robust domestic connectivity redirected their focus towards the domestic market. However, as countries gradually eased their restrictions in the first quarter of 2022, there was a partial recovery in international travel demand.

To facilitate the development of the ASEAN single aviation market, the ASEAN members have collaborated and developed recovery guidelines to enhance cross-border connectivity within the region during the endemic era (Irzanto, 2022). These guidelines serve as a reference for member states to support regional recovery in transport connectivity, although they do not impose any execution requirements. While most ASEAN members have relaxed travel restrictions and reopened their borders in the first quarter of 2022, the lack of coordination remains a challenge for the region. Individual member states that hastily reopened their borders implemented their own policies, resulting in a lack of regional coordination that hindered overall recovery (Lin, 2022). Given the variations in aviation development among ASEAN member states, the recovery of the aviation industry is expected to differ significantly. According to CIRIUM (2022), the domestic market in ASEAN has shown a quicker recovery compared to the international market. Consequently, countries with a large domestic market, such as Indonesia and Vietnam, have experienced better recovery. In contrast, Malaysia’s air transport industry is recovering at a slower rate due to a lack of staffing, leading to operational bottlenecks (Zhu, 2022). Singapore, where Singapore Airlines has no domestic market, has been at the forefront of reopening borders to allow the airline to resume its international network (CAPA, 2022b).

From the literature review, the objective of this study is to investigate the correlation between infection, vaccination and fatality rates on air transport demand in the ASEAN region during the pandemic. No previous research has specifically examined the resilience of the air transport industry in the ASEAN region. Therefore, this study makes a valuable contribution to the existing knowledge of the pandemic’s impact on the air transport industry, with a specific focus on Southeast Asian countries.

Data and Methodology

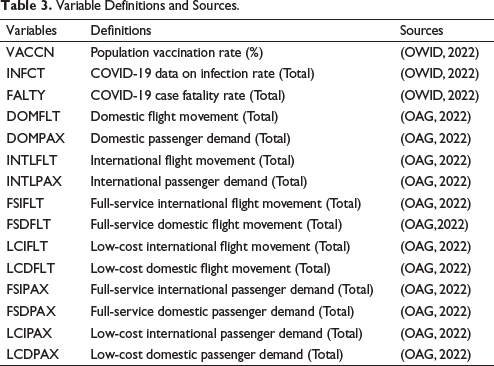

To examine the impact of COVID-19 on the ASEAN air transport industry, a panel data series was created. The panel data series included variables such as the infection rate (INFCT), population vaccination rate (VACCN), COVID-19 case fatality rate (FALTY), flight frequency (FLT) and air passenger demand (PAX). Additionally, to analyse the differences between the international and domestic markets across different airline business models, the flight movement was divided into four categories: full-service carrier international flight frequency (FSIFLT), full-service carrier domestic flight frequency (FSDFLT), low-cost carrier international flight frequency (LCIFLT) and low-cost carrier domestic flight frequency (LCDFLT). Similarly, passenger demand was divided into the following four categories as well: full-service carrier international passenger demand (FSIPAX), full-service carrier domestic passenger demand (FSDPAX), low-cost carrier international passenger demand (LCIPAX) and low-cost carrier domestic passenger demand (LCDPAX).

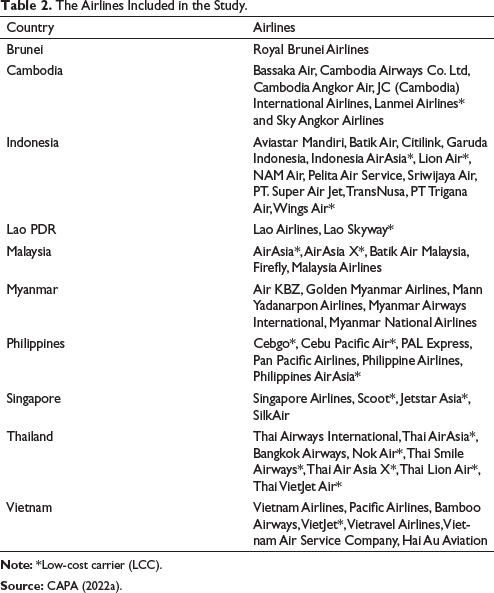

The panel data covered 57 airlines with different business models across the 10 ASEAN member states, spanning from January 2019 to July 2022 (31 months). The study encompassed the period before and after the pandemic, including several months after the countries reopened their borders to international arrivals. The airlines included in the study are listed in Table 2.

The Airlines Included in the Study.

To determine the research objectives, the data of population vaccination rate (VACCN), infection rate data (INFCT) and fatality rate (FALTY) from Our World in Data (2022) were utilised as the dependent variables. Flight movement and passenger demand from OAG (2022) were used as the independent variables. Flight movement was divided into domestic flights (DOMFLT) and international flights (INTLFLT), while passenger demand was further divided into domestic passenger demand (DOMPAX) and international passenger demand (INTLPAX). Based on these selected variables, the following time series data regression models were created. These theoretical models were used to estimate the general flight movement and passenger demand based on (1) vaccination rate, (2) infection rate and (3) fatality rate:

where αi, βi are regression coefficients, i is the cross-section unit and t represents the period (January 2019 to July 2022).

To analyse the variations in flight movement and passenger demand among airlines with different business models, the flight movement was further categorised into the following four types: full-service carrier international flight frequency (FSIFLT), full-service carrier domestic flight frequency (FSDFLT), low-cost carrier international flight frequency (LCIFLT) and low-cost carrier domestic flight frequency (LCDFLT). Additionally, the passenger demand was divided into the following four categories: full-service airline international passenger demand (FSIPAX), full-service airline domestic passenger demand (FSDPAX), low-cost carrier international passenger demand (LCIPAX) and low-cost carrier domestic passenger demand (LCDPAX). These variables were used as independent factors to estimate air passenger demand and flight movement based on the airlines’ business models, taking into consideration the vaccination rate, infection rate and fatality rate:

where α i , β i are regression coefficients, i is the cross-section unit and t represents the period (January 2019 to July 2022).

Analysis

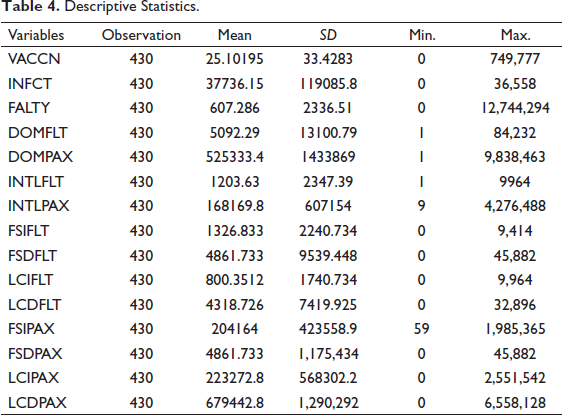

This study utilises the panel data regression method to examine the relationship between the population vaccination rate (VACCN), infection rate (INFCT), fatality rate (FALTY) and air transport demand data in the ASEAN region. Panel data regression, also known as fixed-effects regression or longitudinal regression, is a statistical technique used to analyse data that consists of observations over multiple time periods and for multiple entities or individuals. It is particularly useful when studying the relationships between variables while accounting for the potential impact of unobserved factors that may affect the dependent variable (AitBihiOuali et al., 2020; Suryan, 2017; Tesfay, 2016). Regression models for panel data analysis can be categorised into fixed effect models and random effect models, considering the presence of group effects, time effects, or both (Hwang & Shiao, 2011; Zdaniuk, 2014). The fixed effect model assumes that the independent variable is fixed, while the dependent variables change in response to the level of independent variables. On the other hand, random effect models determine the individual effects of the independent variables as random variables over time. The appropriateness of the models, whether fixed effect or random effect, was determined using the Hausman test. The Hausman test measures the equality between fixed effects and random effects. If the Hausman test yields a significant p-value, the fixed effects model is chosen as it corrects for unique errors in the regression (Green, 2008). Table 3 provides information about the variables used in the estimation procedure, and Table 4 presents the descriptive statistics.

Variable Definitions and Sources.

Descriptive Statistics.

Results

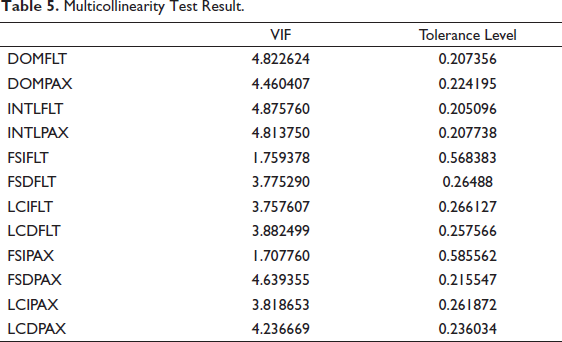

Multicollinearity can pose challenges in panel studies when there is a correlation among independent variables in a regression model, potentially affecting the accuracy of the results. As noted by Siegel (2017), the presence of multicollinearity makes it difficult to discern the specific effects of one variable on another through multiple regression analysis. Hence, it is crucial to assess for multicollinearity in the model. The results of the variance inflation factor (VIF) test and tolerance value, as shown in Table 5, indicate that the VIF values of the variables are below 5 and the tolerance value exceeds 0.20. This suggests that there are no issues of multicollinearity among the variables (Hair et al., 2010).

Multicollinearity Test Result.

Furthermore, it is crucial to assess the stationarity of panel data as non-stationary data can result in less accurate findings due to the issue of spurious regression. The stationarity of the data was examined using the Dickey–Fuller test, a widely used statistical test for analysing stationary time series by investigating the presence of a unit root (Shrestha & Bhatta, 2018). One advantage of this test is its applicability regardless of whether the null hypothesis is one of integration or stationarity. The results of the unit root test (Table 6) confirm that the selected variables in the study are non-stationary at the first difference. This implies that the null hypothesis of the unit root test was rejected at the 5% significance level for both the individual intercept and the individual intercept plus trend. Therefore, the evidence strongly supports the integration of all variables, making them suitable for this study.

The Panel Unit Root Test.

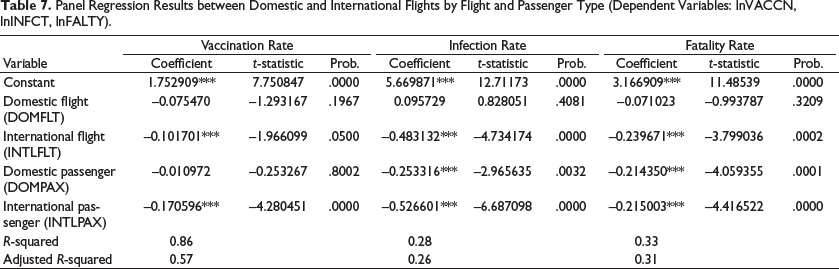

Based on the results of the Hausman test, which yielded a p-value of less than .05, it was determined that the fixed effect model was appropriate. The regression results presented in Table 7 demonstrate significant inverse relationships between the vaccination rate, infection rate, fatality rate and international flight movement, as well as international passenger demand. Additionally, there is a significant inverse relationship between domestic passenger demand and the infection rate and fatality rate. Specifically, a 1% increase in the vaccination rate corresponds to a decrease of 0.10% in international flight movements and 0.17% in international passenger demand. Similarly, a 1% increase in the infection rate leads to a decrease of 0.48% in international flight movement, 0.52% in international passenger demand and 0.25% in domestic passenger demand. Furthermore, a 1% increase in the fatality rate results in a decrease of 0.23% in international flight movement, 0.21% in international passenger demand and 0.21% in domestic passenger demand within the ASEAN region.

Panel Regression Results between Domestic and International Flights by Flight and Passenger Type (Dependent Variables: lnVACCN, lnINFCT, lnFALTY).

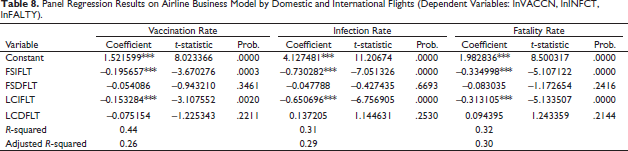

The regression results presented in Table 8 indicate a significant negative relationship between full service and low-cost international flight movements and the vaccination rate, infection rate and fatality rate. Specifically, a 1% increase in the vaccination rate results in a decrease of 0.19% in full service airlines’ international flight movement and 0.15% in low-cost airlines’ international flight movement. Similarly, a 1% increase in the infection rate leads to a decrease of 0.73% in full service airlines’ international flight movement and 0.65% in low-cost airlines’ international flight movement. Furthermore, a 1% increase in the fatality rate results in a decrease of 0.33% and 0.31% in full service airline international flight movement and low-cost airline international flight movement, respectively.

Panel Regression Results on Airline Business Model by Domestic and International Flights (Dependent Variables: lnVACCN, lnINFCT, lnFALTY).

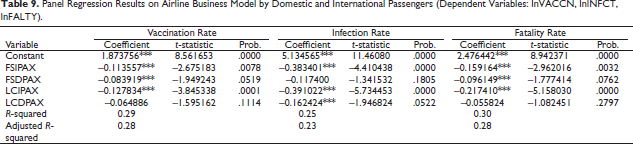

The regression results shown in Table 9 indicate that there is a significant inverse relationship between the vaccination rate, infection rate, fatality rate, and both full service and low-cost international passenger demand. Specifically, a 1% increase in the vaccination rate leads to a decrease of 2.67% in full service airline international passenger demand, 3.8% in low-cost airlines’ international passenger demand and 1.94% in full service airline domestic passenger demand. Similarly, a 1% increase in the infection rate results in a decrease of 0.38% in full service airlines’ international passenger demand, 0.39% in low-cost airlines’ international passenger demand and 0.16% in low-cost airline domestic passenger demand. Furthermore, a 1% increase in the fatality rate leads to a decrease of 0.15% in full service airlines’ international passenger demand, 0.09% in full service domestic passenger demand and 0.21% in low-cost airlines’ international passenger demand.

Panel Regression Results on Airline Business Model by Domestic and International Passengers (Dependent Variables: lnVACCN, lnINFCT, lnFALTY).

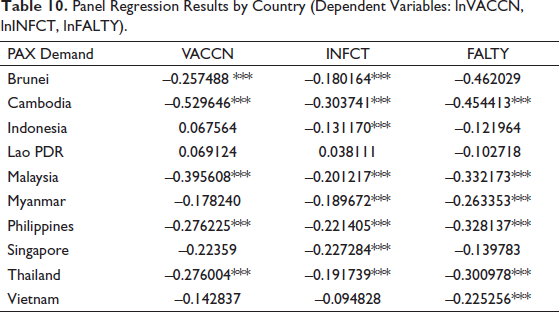

To gain a better understanding of the impact of vaccination rate, infection rate and fatality rate on air passenger demand at the country level, the results of the regression analysis for each member state in the ASEAN region are presented in Table 10. The regression model examining the relationship between vaccination rate and air transport demand reveals that Brunei experiences the smallest decrease in air passenger demand (–0.25%), followed by the Philippines and Thailand (–0.27%), Malaysia (–0.39%) and Cambodia (–0.52%). However, the other countries in the region (Indonesia, Lao PDR, Myanmar, Singapore and Vietnam) do not show significant predictive power for passenger demand. In terms of the regression model analysing the relationship between infection rate and air transport, Indonesia demonstrates the smallest reduction in passenger demand (–0.13%), followed by Brunei (–0.18%), Thailand (–0.19%), Malaysia (–0.20%) and an equal decrease between the Philippines and Singapore (–0.22%), with Cambodia experiencing a slightly larger decline (–0.30). Lao PDR and Vietnam, on the other hand, do not show significant results in this regard. Lastly, the regression model examining the relationship between infection rate and air passenger demand indicates that Vietnam experiences the least decline in demand (–0.22%), followed by Myanmar (–0.26%), Thailand (–0.30%), the Philippines (–0.32%), Malaysia (–0.33%) and Cambodia (–0.45%). The results for Brunei, Indonesia, Lao PDR and Singapore, however, do not demonstrate significance.

Panel Regression Results by Country (Dependent Variables: lnVACCN, lnINFCT, lnFALTY).

Discussion

The COVID-19 pandemic has brought about significant changes in the air transportation market, causing the aviation industry to come to a halt due to border closures and travel restrictions imposed by governments. Prior to the pandemic, ASEAN was recognised as one of the world’s fastest-growing aviation markets, accounting for 10% of global traffic (Sobie, 2020). The findings of this study clearly indicate that the increase in infection rate has a greater impact on the international air travel market compared to the domestic market. The reduction rate in the domestic market is only half of that in the international market, while the fatality rate shows no significant difference. This aligns with the report by the Federal Aviation Administration, Eurocontrol and the European Commission (2021), which states that domestic traffic was less affected than international traffic in both the United States and European air transport markets. This is because airlines are able to respond more quickly in the domestic market, as it is not subject to the closure of international borders. When comparing the impact on airline operations based on their business models, it is evident that full service airlines in ASEAN experience a greater reduction in international flights compared to low-cost carriers. A higher infection and fatality rate leads to a higher reduction rate in international flights for full service airlines, as opposed to low-cost carriers. This could be attributed to the flexibility of low-cost airlines in adapting to market changes. Fontanet-Pérez et al. (2022) define that airlines operating with low-cost and low-fare business models in the North American market were more successful in managing the effects of unexpected crises and were more adaptable to sudden market changes. However, this observation differs in the European market, where smaller and low-cost airlines performed significantly worse compared to full-service carriers, as the latter received more government support during crises. Additionally, the different responses of countries in the region at the time of the pandemic led to varying performances of airlines operating with different business models (Kökény et al., 2021).

When comparing passenger demand, this study has observed that full-service airlines were less affected in their international market compared to low-cost airlines as the infection and fatality rates increased. Despite the significant decrease in passenger demand during the pandemic, more passengers chose to travel on full-service airlines rather than low-cost carriers in the ASEAN region. This could be attributed to larger airlines continuing to operate flights on selected international routes for connectivity and humanitarian purposes, as well as differences in confidence levels among travellers in their choice of airline. The changes in air travellers’ behaviour during the COVID-19 era have made nonstop flights more appealing, as most travellers prefer to minimise their exposure at connecting airports. Additionally, air travellers have expressed concerns about onboard safety to reduce the risk of COVID-19 transmission during their trips (Kungwola et al., 2022). They worry that smaller aircraft sizes and shorter turnaround times used by low-cost airlines increase the chances of infection. Many low-cost airlines maximise their cabin configuration by installing the maximum number of seats, which raises concerns about seat pitch for air travellers (Manish, 2020). Another area of concern is the short turnaround time. Low-cost airlines have significantly shorter aircraft turnaround times compared to full-service carriers, and air travellers are worried about the cleanliness of the aircraft (Schultz et al., 2020).

At the country level, there is a clear indication that Brunei has the highest vaccination rate and the slowest drop in passenger demand in ASEAN. Even though this result aligns with a study by Guo et al. (2022), which found a positive correlation between vaccination and mobility. However, it cannot be concluded that there is a clear inverse linear relationship between the vaccination rate and air travel demand in ASEAN. Cambodia, despite having the second-highest vaccination rate, has also experienced the largest decline in air passenger demand in the region. This finding is consistent with a study by the Official Airline Guide (OAG), which found no clear relationship between rising vaccination rates and increasing international air transport demand in 22 countries worldwide (Rowland, 2021b). Despite the vaccination rate being a crucial factor in travel decisions, many travellers still harbour concerns regarding the effectiveness of vaccines produced by specific companies due to a lack of transparent data on clinical trial results (Zaini & Hoang, 2021). Brunei and Singapore have the highest infection rates among all ASEAN member states due to their high population density and small country size. The results of this study indicate that countries with large domestic air connectivity markets have experienced lower declines in air passenger demand compared to those with smaller domestic markets. This is especially true for archipelagic countries like Indonesia and the Philippines, as well as large landscape countries like Thailand and Myanmar, where air transport plays a crucial role in supporting economic development. There is also a reverse linear relationship observed between the fatality rate and air travel demand in six countries within the ASEAN region. As the fatality rate increases, air travel demand decreases in Cambodia, Malaysia, Myanmar, the Philippines, Thailand and Vietnam. The number of deaths has influenced air travellers’ decisions regarding travel. This finding aligns with a study by Pana et al. (2021) on the impact of the first wave of COVID-19 on international travel, which found that international travel was the strongest predictor of increased mortality during the pandemic. A similar result was also observed in a study by Rastegar et al. (2021), where higher travel intentions were identified in countries with lower fatality rates, indicating that the public has developed trust in the government’s ability to handle the pandemic crisis.

Conclusion

The research emphasises the profound influence of the pandemic on the demand for travel. It is evident that the current situation calls for enhanced coordination and collaboration among the member states of the ASEAN to effectively handle health crises and ensure the seamless operation of the aviation industry. The study underscores the significant repercussions that the pandemic has had on the travel sector. With travel restrictions, lockdowns and concerns about health and safety, there has been a notable decline in travel demand. This decline has affected various aspects of the aviation industry, including airlines, airports and related businesses.

In light of these challenges, it has become increasingly evident that a comprehensive and coordinated approach is necessary to address the issues arising from health crises. Despite ASEAN’s concerted efforts to foster a unified regional health response to COVID-19 through the establishment of various working groups such as the Emergency Response Assessment team and the ASEAN Coordinating Centre for Humanitarian Assistance on Disaster Management (AHA Centre, 2018), it is evident that each member state has displayed diverse responses throughout both the pandemic and the subsequent endemic era (Rollet, 2022). ASEAN member states must work closely together, sharing information, best practices and resources to effectively manage and mitigate the impact of such crises on the travel industry. ASEAN can take inspiration from the European Union (EU)’s approach in building trust between governments and the public, which is a crucial factor for the successful implementation of policies. The EU has established effective mechanisms such as Health Policy Coordination, Cross-Border Healthcare cooperation, and Information Sharing and Early Warning Systems, which enable timely and transparent communication and a coordinated response to health emergencies (Leloup, 2021). By adopting similar mechanisms, ASEAN can enhance trust and improve its response to health crises.

Furthermore, closer coordination in the aviation sector within ASEAN can minimise the impact of future crises by creating a larger domestic market for the aviation industry (Law & Katekaew, 2022). The establishment of the ASEAN Single Aviation Market, which removes borders between ASEAN countries, leads to increased competition, lower airfares for travellers and improved connectivity between ASEAN countries. This not only benefits the aviation industry but also promotes economic growth, resilience and regional integration in the long run.

In conclusion, fostering greater cooperation and coordination among ASEAN member states in managing health crises and facilitating the aviation industry is crucial for promoting economic growth, enhancing resilience and strengthening regional integration. By establishing a regional organisation and implementing effective mechanisms, ASEAN can build trust, ensure collective decision-making and improve the overall response to health crises while benefiting the aviation industry and the region as a whole.

Footnotes

Acknowledgements

The author is grateful to the anonymous referee of the journal for useful comments. Views are author’s own. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.