Abstract

In this paper, we explore the potential deterrent effect of federal pretrial agreements by examining the extent of violations subsequent to an organization signing a pretrial agreement. More specifically, this research examines the subsequent criminal, civil, and regulatory violations of 161 publicly-traded firms that signed federal deferred prosecution agreements and non-prosecution agreements between 2001 and 2020. Our analysis identified 87 recidivist companies with a total of 629 subsequent violations, eight of which were criminal violations. While most companies had only one subsequent violation, one company had 63 noted violations after signing the pretrial agreement. Our exploratory analyses reveal that companies paying larger penalties as part of the pretrial agreement were less likely to have subsequent violations, and, when examining U.S.-based companies only, that larger organizations were more likely to have subsequent violations. These preliminary results are important to understanding both corporate deterrence generally, and the use of pretrial agreements as a corporate deterrent specifically.

“Deferred prosecution and non-prosecution agreements occupy an important middle ground in the resolution of corporate crime cases . . . by requiring the adoption of solid internal controls and ethics and compliance programs, the agreements encourage corporations to root out illegal conduct, prevent recidivism, and ensure that they are committed to business practices that meet or exceed applicable legal and regulatory mandates.” [Emphasis added]

(Testimony of U.S. Attorney David E. Nahmias to the Committee on the Judiciary, (U.S. House of Representatives, 2008)

When organizations are accused of federal crimes, federal prosecutors can elect to resolve these matters using settlement agreements with organizational defendants rather than criminal trials. Prosecutors use three main agreements: plea agreements (also called plea bargains), deferred prosecution agreements (DPAs), and non-prosecution agreements (NPAs). Prosecutors offer plea agreements after filing criminal charges, allowing the organization to plead guilty and pay a penalty rather than undergoing a trial. DPAs and NPAs are treated differently than plea agreements: they do not require a guilty plea. Non-prosecution agreements and DPAs are distinct from each other, in that organizations are eligible to be charged with a crime in the case of a DPA. However, that organization can have the criminal charges negated if it successfully completes the terms of the agreement. No criminal charges are ever brought against a company in the case of an NPA, but the company is still assessed a penalty for the illegal activity it allegedly conducted (Alexander & Cohen, 2015; Bohrer & Trencher, 2007; Podgor, 2018). Deferred prosecution agreements and NPAs are often collectively referred to generally as pretrial agreements, which is the term we will use throughout this paper to include both types of agreements. Although the use of pretrial agreements began in the early 1990s, very few organizations signed these pretrial agreements until the 2000s. Since then, the number of completed pretrial agreements has steadily increased (Claypool, 2019; Garrett & Ashley, 2022; Gibson, Dunn & Crutcher LLP, 2020).

Despite this increase, there has been little empirical attention given to these agreements, and relatively few examinations of sentencing and punishment of organizational defendants more generally (Alexander & Cohen, 1999, 2015; Calathes & Yeager, 2016; Cohen, 1989; Davis, 2008; Garrett, 2014; King & Lord, 2018; Markoff, 2013; Piquero & Davis, 2004). This makes sense given both the historical lack of available data and the relative rarity of corporate criminal prosecutions. In a recent review of the prosecution and punishment of corporate criminal offenders, Diamantis and Laufer (2019) conclude that “the vast majority of corporate crime is not referred for prosecution, the vast majority of corporations referred for prosecution are not convicted, and substantially all convicted corporations are sanctioned in ways that continue to raise fundamental questions” (p. 467). Statistics from the U. S. Sentencing Commission support this conclusion: In fiscal year 2020, 94 organizations were convicted of crimes (felonies and serious misdemeanors). Between fiscal years 2016 and 2020, this figure ranged from 94 to 132 organizations (United States Sentencing Commission, 2021). This is despite the fact that the costs of white-collar crime outweigh the costs of “street crime” by far, with occupational theft and frauds alone estimated to result in annual victimization costs of at least US$1.6 trillion (Cohen, 2016). Although reliable estimates are unavailable, the costs of corporate crimes, such as financial institution frauds and environmental crimes, are expected to be even higher. With this in mind, legal and academic scholars alike wonder if pretrial agreements are a good alternative to criminal prosecution.

Among the fundamental questions concerning the use of pretrial agreements is whether they achieve the goal to deter future corporate crime described previously by U.S. Attorney David E. Nahmias. Following Clinard and Yeager (1980), we define corporate crime as violations of criminal, civil and administrative law carried out within an organizational setting. The purpose of this study is to examine the subsequent behavior of organizations that previously signed pretrial agreements, identifying later instances of civil, criminal, and administrative violations. If corporate pretrial agreements do have a specific deterrent effect, there will be fewer organizations involved in subsequent violations. Below we provide a brief history of organizational sentencing (pre- and post-Booker) and the increased use of pretrial agreements, followed by a review of the criminological research on corporate crime deterrence and its potential application to pretrial agreements. We then proceed with a description of the study that is the basis for this paper, our results, and concluding thoughts.

The Debate on the Appropriateness of Pretrial Agreements

Prior to 1989, organizational sentencing at the federal level was negotiated by judges, prosecutors, and organizational defendants. Between 1989 and 1991, the U.S. Sentencing Commission developed mandatory sentencing guidelines as part of overall reform efforts. The goal of the guidelines was to: (1) remove bias from individual sentencing by specifying ranges of incarceration time based on the seriousness of the offense and defendant’s criminal history, (2) implement so-called “truth in sentencing,” whereby defendants would serve determinate periods of incarceration and/or community supervision, and (3) with regard to organizations, increase criminal fines levied against organizations found or pleading guilty to criminal offenses (Piquero & Davis, 2004). After the United States v. Booker decision in 2004, both individual and organizational sentencing guidelines became advisory rather than mandatory. While much attention has been given to the impacts on individual sentencing post-Booker, relatively little attention has been paid to organizational sentencing. Piquero (2007) notes that “[Booker’s] impact on organizational guidelines and sentences is not quite as clear [as for individual sentencing changes] and it will not be an easy research endeavor to determine it.” (p. 499)

Scholars have noted a trend since the Booker decision for federal prosecutors to pursue more criminal cases against organizations, while at the same time encouraging prosecutors to negotiate pretrial agreements–DPAs and NPAs–that allow organizations to avoid the mark of a criminal conviction. Such agreements tend to be used more commonly, although not exclusively, in cases involving financial frauds (Garrett, 2014; Uhlmann, 2013). Related to the increased use of pretrial agreements is the impetus for organizations to police themselves, including both external cooperation with prosecutors and federal regulators and developing internal policies and practices to demonstrate the company’s willingness to comply with the law. In fact, the imposition of either compliance programs or an independent monitor, or both, is a common condition of prosecution agreements (Garrett, 2014).

In exchange for either not being criminally charged now (DPAs), or never being charged (NPAs), the organization pays a penalty. The penalties associated with pretrial agreements are intended to both punish organizations for criminal behavior and deter future criminal activity. The former is primarily accomplished through fines, disgorgements, restitution, and other monetary penalties. The latter is achieved through conditions that could include the imposition of corporate compliance measures, the assignment of a third party to “monitor” compliance, organizational restructuring, and an agreement that the company will not commit subsequent crimes. The federal government argues that holding organizations responsible for misconduct through actions including signing pretrial agreements deters future illegal activity (United States Department of Justice, 2015). While they have their benefits, pretrial agreements are viewed with some skepticism in the criminal justice, legal, and review literatures.

The development of pretrial agreements has been compared to the use of diversion in the juvenile justice system (Eisinger, 2017; Garrett, 2014). Deferred prosecutions were included in the renewal of the Speedy Trial Act in the early 1970s, with first-time juvenile offenders in mind (Werle, 2019). As Garrett (2014) notes, the use of deferred prosecutions for white-collar defendants—and organizational defendants in particular—did not begin in earnest until the early 2000s. Legal scholars point to the Arthur Andersen case in particular as a watershed moment when the use of DPAs in particular began to be more common (Markoff, 2013; Martin, 2014; Werle, 2019). The prevailing opinion that criminally convicting Arthur Andersen for its role in the Enron Corporation scandal resulted in the company’s bankruptcy and eventual closing caused some to prefer sanctioning alternatives (including DPAs) that might not cause a company’s demise (Markoff, 2013). Like juvenile diversion, the DPA allows offenders to escape the threat of the formal criminal sanction in exchange for the defendant’s agreement to criteria set by the government.

Scholars have offered a variety of reasons why the use of pretrial agreements to sanction corporate crime is either inappropriate or misplaced as currently practiced in the U.S. (and in the U.K. with DPAs), and suggest either radical changes to their implementation or the outright abolition of such agreements. For example, some have argued that signing pretrial agreements with organizations where there appears to be plenty of proof of a crime undermines the effectiveness of pretrial agreements as a deterrent (Albonetti, 1987; King & Lord, 2018; Uhlmann, 2013). Akin to plea bargaining, such agreements may do a disservice to due process in that they allow some organizations (i.e. larger, more powerful corporations) to negotiate better deals than those with fewer legal and financial resources (Arlen, 2016; Garrett, 2014; King & Lord, 2018; Wilt, 2015). In addition, companies that sign pretrial agreements and avoid pleading guilty also avoid the stigma of the criminal sanction (Uhlmann, 2013).

Conversely, those scholars that support the use of agreements have argued that signing pretrial agreements offers the prosecution a better assurance of holding organizations accountable in comparison to a possible acquittal at trial, as well as saving both the government and accused organization the time and expense of the trial (Alexander & Lee, 2017; Podgor, 2018; Robinson et al., 2005). Pretrial agreements allow companies to continue to operate, whereas they might be forced to shut down during or after a criminal prosecution. Furthermore, pretrial agreements allow organizations to be penalized beyond the scope of penalties that are available in a criminal conviction, giving prosecutors more discretion to levy heavier penalties. Notably, organizations can be fined more harshly with an agreement than they could be with a conviction (Xiao, 2013). The aspects of agreements that involve corporate “monitoring” by contracted third parties, and the government’s scrutiny of corporate governance, have also been cited as examples of prosecutorial “overreach” and a possible violation of the rule of law (Arlen, 2011; 2017; Wilt, 2015).

Taking a contrasting view, former federal prosecutor Samuel Buell (2016) stated: [T]he net effect of prosecutions on business, even if the government brought many more of them than it does, will remain far less costly to business than major programs of regulation. And, for corporations, the benefit of prosecutions is that they displace regulation. Punishing companies and people in the wake of a big corporate scandal—whether it be Enron, BP, GM, Exxon, Tylenol, the Ford Pinto, or any other—is an immediate, highly visible, and direct salve to the public’s outrage at both corporations and the government . . . The effect is to direct attention away from structural changes, including effective regulatory reform, and onto the project of punishment. Focus eyes backward and people won’t look forward [emphasis in original] (p. 241).

In response to the possibility that corporate prosecutions may have collateral consequences on innocent parties, scholars have found that the probability of organizations going out of business after being prosecuted, or facing the corporate death penalty (a.k.a. the “Arthur Andersen effect”), is very low (Greife & Maume, 2020; Hamdani & Klement, 2008; Markoff, 2013). Markoff (2013) studied 51 public companies that were convicted of crimes between 2001 and 2010, and found that none of the companies failed because of their conviction. Others have found that financial penalties are often so low that organizations are not financially harmed when they are penalized because the amounts are significantly lower than the organizations’ profits (van Wingerde & Kluin, 2018). Examining the collateral consequences of agreements, Lee (2017) found that organizations entering into agreements did not suffer from decreased stock returns in the 5 days after the agreement, but organizations that entered plea agreements did show decreased stock returns. These studies demonstrate that it is not necessary to use pretrial agreements to avoid the collateral consequences of a prosecution because the consequences are not severe. To the contrary, sanctioned companies may even receive dispensations or waivers to allow them to continue conducting business as usual (Viswanatha, 2015). What may present a valid argument for or against pretrial agreements is their effectiveness as a deterrent to future violations committed by the offending organization.

Deterrence, Criminal Prosecutions, and Pretrial Agreements

Some scholars have argued that corporate deterrence can only be achieved under specific circumstances. These include when the punishment threatens the organization’s operating status (Hamdani & Klement, 2008), financial profits (Claypool, 2019), public image (Alexander & Arlen, 2018; Campbell, 2019), or ability to obtain government contracts (Hill, Jr., 2014). Corporate criminal prosecutions and pretrial agreements may not have similar results in terms of deterring future criminal behavior. White-collar crime scholars have made clear that criminal sanctioning is only a part of corporate crime sanctioning, and a relatively small one at that, as a good deal of organizational misconduct is dealt with by regulators and—in many cases—the company itself (Brown, 2001; Fisse & Braithwaite, 1993; Huisman, 2014; Schell-Busey et al., 2016).

While the bulk of the sources debating corporate recidivism are non-empirical, several articles have empirically examined how deterrence works for corporations. Some have found evidence of corporate deterrence. Block and colleagues (1981) examined if an increase in federal enforcement to combat price fixing resulted in a deterrent effect among companies in the bread industry. The study focused on federal criminal and civil antitrust sanctions. Their examination of 17 companies strongly suggested a deterrent effect when the Department of Justice increased antitrust enforcement. Another study found that small and medium sized companies were more likely to be deterred compared to large ones (Gunningham et al., 2005).

Simpson and colleagues (2014) conducted a meta-analysis of corporate crime deterrence by locating studies examining various strategies for the prevention and control of corporate crime, both at the corporate and individual levels. They utilized 40 studies that used a variety of research methods and varying formal legal and administrative interventions, including laws specific to corporate crime, punitive and non-punitive corporate sanctions and punishments, and regulatory investigations. Their results showed relatively few significant deterrent effects across different units of analysis and types of studies. Examining punitive sanctions, their results showed a tendency toward a nonsignificant deterrent effect in both cross-sectional and longitudinal studies. Legal interventions showed a modest deterrent effect at the corporate level in cross-sectional studies, but the researchers were unable to calculate an effect size for legal interventions at the individual level or in longitudinal studies. Regulatory policies had a significant crime deterrent effect at the individual-level only. The ultimate conclusion of their research is that there were not enough methodologically rigorous studies to draw many strong conclusions regarding existing corporate crime interventions.

Whether and to what extent criminal prosecutions specifically influence subsequent corporate criminal activity is an unanswered question (Almond & van Erp, 2020). Similarly, whether pretrial agreements deter subsequent criminal behavior is rarely empirically examined. The federal government’s position is that pretrial agreements achieve deterrence because companies need to make progress reports, pay fines, and meet compliance standards, and if they do not they will be in breach of that agreement (United States Department of Justice, 2015). Organizations fear bad publicity in particular because it may affect their profits; however, agreements are not stigmatizing enough to cause a hit to corporate reputations or income (Campbell, 2019; Garrett, 2007, 2014; Uhlmann, 2013). Unlike high-profile cases (e.g., Enron, Goldman Sachs, BP) where “naming and shaming” may have a direct impact on a company’s bottom line, most pretrial agreements received no more than a press release on the Department of Justice Web site (van Erp, 2011). Relatively low-profile pretrial agreements can mask the amount of damage an organization caused (Alexander & Arlen, 2018), meaning that the public cannot see the full impact of the organization’s activities and stop their patronage.

An additional factor when considering the deterrent effect of pretrial agreements is related to the likelihood of a breached agreement resulting in subsequent criminal charges. Claypool (2019) found that few organizations were punished for subsequent violations of the pretrial agreements. In some violations, organizations that violated agreements were charged criminally, but in others, the pretrial agreements were re-negotiated or the terms extended (Claypool, 2019).

Another consideration of determining the deterrent effect of agreements is related to what activities are intended to be deterred by signing agreements, since organizations can be sanctioned in multiple ways. In its report discussing the tracking of pretrial agreements, the United States Government Accountability Office noted: … According to the Senior Counsel to the Assistant Attorney General for the Criminal Division, DPAs and NPAs are tailored to address the violations of a specific law based on specific misconduct. Therefore, if the company entered into a DPA or NPA because it violated the Commodity Exchange Act, for example, it could be problematic to consider subsequent violations of the Foreign Corrupt Practices Act as recidivism (2009, p. 22).

Based on this description, the interpretation of the effectiveness of pretrial agreements as a deterrent partially depends on the types of crimes that you believe pretrial agreements are intended to be deter.

The purpose of this study is to examine the subsequent violations of any type—civil, criminal, or administrative—by organizations that have signed pretrial agreements. We expect that if corporate pretrial agreements do have a specific deterrent effect, there will be fewer organizations involved in subsequent violations.

The Current Study

Our analysis explored the following research questions: 1. What percentage of companies that previously signed pretrial agreements have subsequent criminal, civil, and regulatory violations? How many of these are criminal violations specifically? 2. Is there a difference in the number of violations for companies that signed DPAs versus NPAs? What was the average time to recidivate for these companies? 3. Is the type of violation that was the basis for the agreement related to recidivism? 4. Is the total payment dictated in an agreement related to recidivism rates?

Data

For the current study, we use a sample of pretrial agreements archived in the Corporate Prosecution Registry (CPR) database (Garrett & Ashley, 2022) The CPR contains records of organizations that signed federal organizational agreements between the years 1992–2020, including plea agreements, DPAs, and NPAs. The data, which are publicly available, include the organization’s name and details of the agreement, including the date(s) the agreements were proposed and completed. The database, as of August 2021, contains records of 611 DPAs and NPAs, the two federal corporate agreements of interest that are included in the CPR. The federal government does not maintain a database of these agreements, so private efforts like the CPR are useful sources for this kind of information.

The sample used in this study consists of 167 pretrial agreements involving 161 firms that at one point in time were traded publicly. We determined a firm to be a public corporation using the WRDS Compustat database, which uses a unique ID, similar to a stock ticker, to identify companies traded on major stock exchanges (e.g., NYSE). We used two other databases – Mergent and Standard & Poor’s NetAdvantage – to confirm a company’s public status. When necessary, we used the Securities and Exchange Commission’s (SEC) Company Filings EDGAR search (Electronic Data Gathering, Analysis, and Retrieval system) to further examine a company’s ownership.

We chose to focus on publicly-traded companies for a number of reasons: publicly-traded entities require more transparency to their shareholders and the public, meaning that more data are available on public organizations than private organizations. Transparency in finances, ownership and corporate structure are required of both domestic- and foreign-owned public companies by the SEC. Additionally, public companies are required to disclose to the Securities and Exchange Commission whether their senior financial officers have adopted a code of ethics, and why they have not if that is the case. These codes of ethics require ethical conduct by the corporate financial officials, timely and accurate financial reporting by the company, and compliance with governmental regulations (Sarbanes Oxley Act of 2002, 2002). Private companies are not required to disclose this information. Public companies also arguably allow for more opportunities for crime due to larger and more complex corporate structures, which may make it easier to hide wrongdoing and concomitantly harder for authorities to detect (Benson & Simpson, 2015; Prechel & Morris, 2010). Public companies often have larger revenues than smaller companies, and may not be deterred even by substantial penalties because they can afford to pay them. Publicly traded companies also have different abilities to engage in crime prevention compared to smaller companies. With their generally higher revenues, public companies are able to afford more crime-preventative mechanisms, which could theoretically act as a deterrent.

Our source for subsequent criminal, civil, and administrative violations (i.e., recidivism) is Good Jobs First’s (GJF) Violation Tracker (https://www.goodjobsfirst.org/violation-tracker), which GJF describes as “the first wide-ranging database on corporate misconduct (Good Jobs First, 2021).” It is a publicly available database that includes records of criminal, civil and regulatory violations for which an organization paid a monetary penalty as reported by both federal and state enforcement agencies in the United States. Although the database has served as the basis for studies of corporate misconduct by journalists, business scholars, and economists, to our knowledge criminologists have not utilized these data to examine white-collar and corporate crime (Raghunandan & Rajgopal, 2021; Soltes, 2019). 1

Variables

We measure recidivism as any subsequent recorded violation by the organization with a penalty greater than US$10,000. 2 Any violation was coded as 1; non-recidivists were coded as 0. We also examine the time to recidivism, the number of new violations, and the total penalties for new violations. We selected larger-penalty sanctions because our preliminary review of violations revealed that most violations resulting in a sanction less than US$10,000 tended to consist of relatively minor infractions (e.g., OSHA regulatory violations).

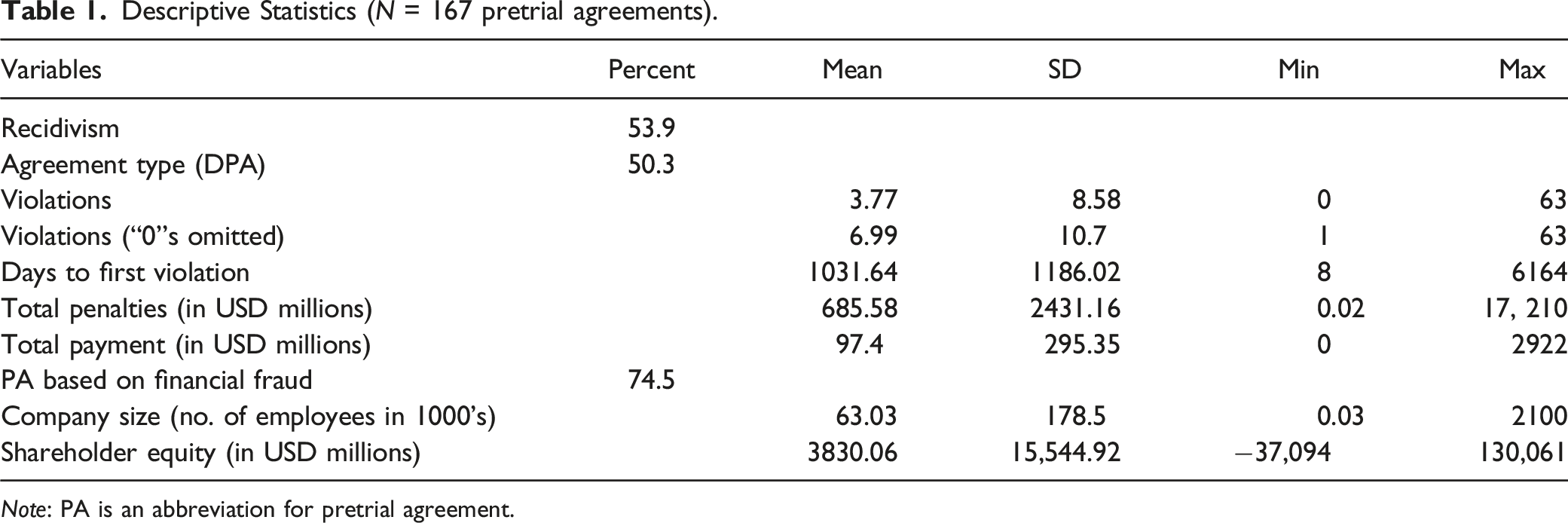

Descriptive Statistics (N = 167 pretrial agreements).

Note: PA is an abbreviation for pretrial agreement.

Using the WRDS and NetAdvantage databases, we appended several company characteristics to our existing database compiled from the CPR and Violation Tracker. We included both the total number of employees and stockholder equity as measures of company size (Wang & Holtfreter, 2012). Previous research has found both variables to have an impact on corporate violations, with size measured as number of employees having a positive relationship and equity having a negative impact (Prechel & Morris, 2010; Wang, 2008). A company’s shareholder equity is its net worth, or total liabilities subtracted from total assets. Because these measures vary by time, we chose 2007 as a midpoint. Where historical financial data for 2007 were not available from WRDS, we used 2019 data from NetAdvantage and converted the measure of equity to 2007 dollars using an adjustment for inflation. Again, because both of these measures were highly skewed, we logarithmically transformed them for use in our regression models.

Results

Table 1 provides descriptive statistics for the full dataset. This table addresses the first and second research questions relating to the number of subsequent violations for companies in the sample. The overall recidivism rate for all pretrial agreements was 53.9%. Amongst these 90 cases of recidivism, the number of subsequent violations ranged from 1 to 63 violations attributable to United Parcel Service, Inc., or UPS, with one violation being both the modal and median value. The average time to a subsequent violation was 1031 days (SD = 1186), with the shortest time span being 8 days. 3 Total penalties for subsequent violations ranged from US$21,000 to US$17B (M = US$685.8 M, Md = US$20M), and the average penalty per violation was US$5.5 million. We found that company size, in terms of both number of employees and net worth, was positively correlated with total penalties for subsequent violations (r = 0.42 and 0.56, respectively).

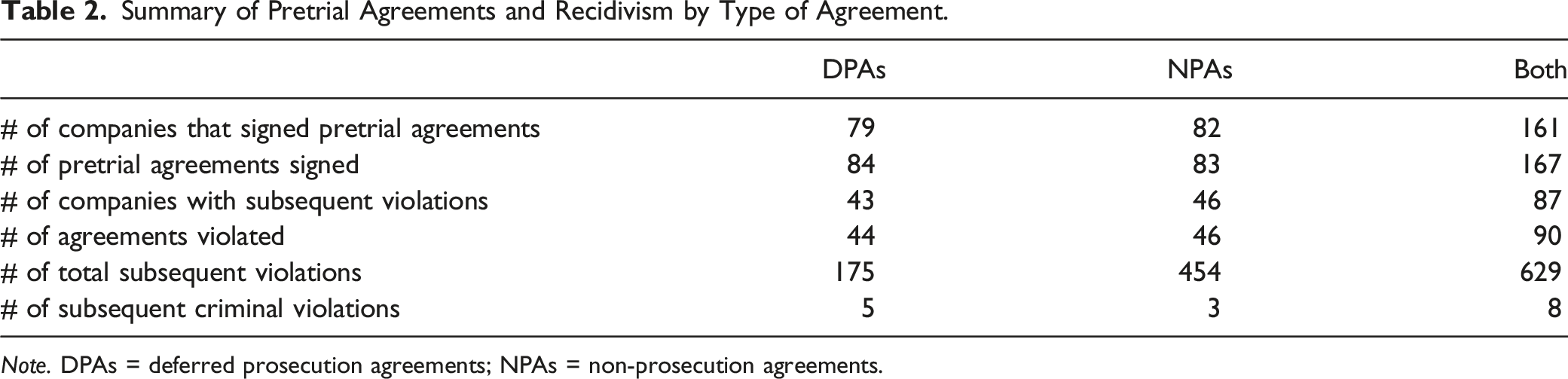

Summary of Pretrial Agreements and Recidivism by Type of Agreement.

Note. DPAs = deferred prosecution agreements; NPAs = non-prosecution agreements.

Only eight cases of recidivism were criminal violations, which involved these corporations: Bristol-Myers Squib, JPMorgan Chase & Co., Johnson & Johnson, MoneyGram International, Monsanto, Pfizer, Pilgrim’s Pride Corporation, and the Royal Bank of Scotland. Five of these criminal violations were for companies that signed DPAs and three were for companies that signed NPAs. We note that this is a different pattern than the total number of combined violations, in which companies that signed NPAs had far more subsequent violations than companies that signed DPAs (454 for NPAs vs. 175 for DPAs). Given that DPAs are often considered to be the harsher pretrial agreement because of the threat of criminal charges that is absent with NPAs, we might expect that companies that signed DPAs would be more deterred from committing criminal activity; however, our results do not support this. With such a small sample size, it is difficult to draw conclusions about the role of pretrial agreements in deterring criminal violations. It may be that because companies signing DPAs were more likely than those receiving NPAs to be monitored subsequently that such monitoring and increased compliance enforcement resulted in more serious violations coming to light, but that remains for future research to discern.

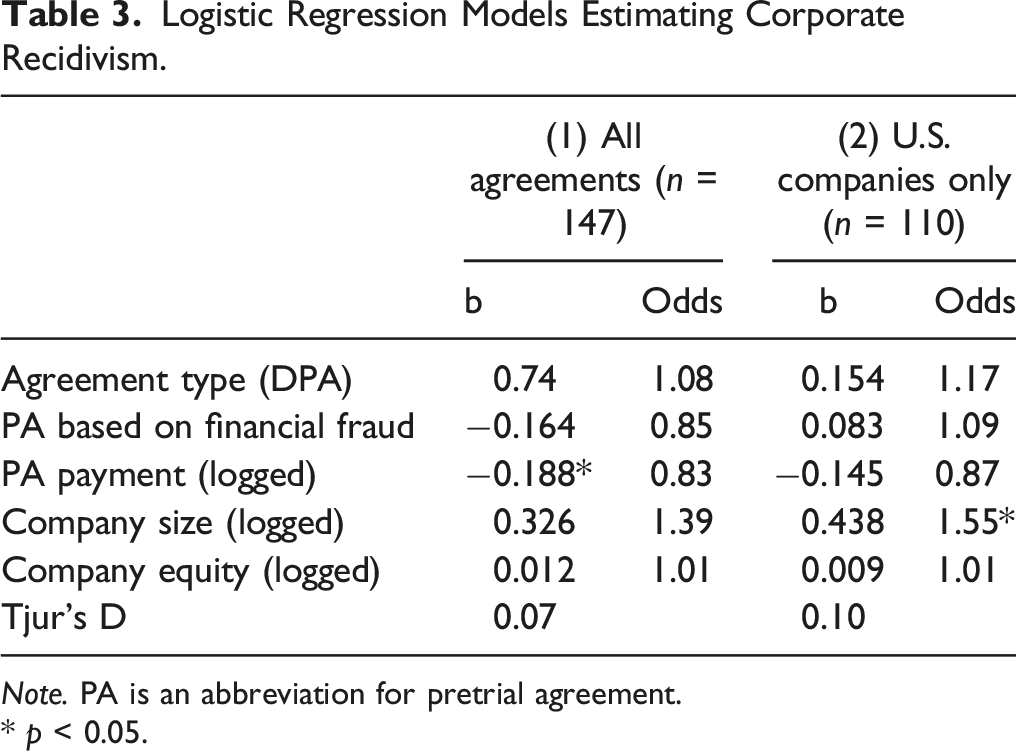

Logistic Regression Models Estimating Corporate Recidivism.

Note. PA is an abbreviation for pretrial agreement.

* p < 0.05.

When we reduced the sample to agreements involving companies based in the U.S. (Model 2), we see that larger companies are significantly more likely to reoffend than smaller ones. All other things being equal, the predicted probability that a large company will engage in recidivism is 81%. This particular finding is consistent with previous studies of corporate crime (Clinard & Yeager, 1980; Garrett, 2014; Gunningham et al., 2005). Larger companies may have more violations because they have more opportunities to commit crime than smaller companies. Because larger companies have more employees than smaller companies, they have more employees who are in positions to commit crime. Additionally, larger companies potentially have more business relationships, partnerships, subsidiaries, products, operations, etc., both internationally and domestically, that create additional opportunities for crime. Unfortunately, we cannot explain why company size may not be as pertinent in the full sample including all companies.

Discussion

Although scholars have examined and learned a great deal about sentencing trends and patterns, and there are a multitude of studies on recidivism, the vast majority of this research has focused on individuals involved in the criminal justice system. Akin to the lack of research on white-collar crime in general, studies of corporate crime sanctioning are few and far between. Studies of organizational recidivism are rarer still. This is not altogether surprising, as data on white-collar and corporate crime are difficult to come by and not collected in a systematic way by the federal government (Simpson, 2019). It is helpful to note critical criminologists’ reminder that the state either often or always moves in lockstep with the interests of the powerful in society, including corporations (Barak, 2017; Stretesky et al., 2014). Perhaps a more prosaic reason for the paucity of research on corporate crime and sentencing is disagreement concerning the status of corporations as criminal actors, and the criminal liability of organizations in general (Piquero, 2007). The U.S. is one of the few countries in the world that permits the criminal prosecution of companies as well as individuals. This raises difficult questions for those seeking to empirically examine phenomena such as recidivism, something presumed to be an individual behavior or outcome, albeit often a sociologically-determined one.

Nevertheless, it is our hope that this exploratory study of recidivism amongst organizations contributes to the existing literature and provokes more research in this area. The relative lack of corporate crime research stands in disproportionate contrast to the staggering financial and environmental costs of corporate crimes. Based on publicly available, non-governmental data on companies that were referred for criminal prosecution to federal authorities—but avoided criminal conviction—we found that the extent of recidivism was significant. Over half of the companies in our dataset were cited for either a civil or criminal violation subsequent to signing an agreement putatively undertaken to ensure their compliance with law. And although our initial foray into modeling the prevalence of recidivism produced little in the way of statistically significant findings, we believe there is much more work to be done in this line of research.

One of the most important tasks for future research will be to compare recidivism data for companies that pled guilty with those that entered into sentencing agreements that allowed them to avoid conviction. Arguments that some companies are not only “too big to fail,” but also “too big to jail,” have received some empirical support. Larger companies—particularly financial institutions—were not only bailed out economically during the 2008 recession but also bailed out of having to face the stigma of a criminal conviction for their illegal actions at the time (Garrett, 2014; Markoff, 2013). When we limited our data to domestic companies, we found this to be a salient factor as well. Larger companies like Deutsche Bank and Monsanto were more likely to have engaged in at least one violation subsequent to their prosecution agreement. But we still know relatively little about which companies are granted such agreements, and whether the agreements have a marked impact on the likelihood of re-offending relative to those that plead guilty.

Alexander and Arlen (2018) state that prosecutors have three considerations when deciding between a criminal charge or prosecution agreement (in this case, a DPA): “the potential threat to the firm and its customers of exclusion or delicensing [a possibility only where there is a criminal conviction], whether a firm that detected misconduct reported it or not, and the degree to which the firm conducted a full investigation and cooperated with authorities, or, alternatively resisted the government’s efforts to obtain information” (pp. 117–118). A potential problem with this line of reasoning is the privilege that companies have over individuals when it comes to criminal investigations. If the firm thinks the government is pursuing conviction, it may prompt them to cooperate, which in turn may prompt the government to enter into a prosecution agreement with the company. Despite the machinations involved in the choice of a prosecution agreement or guilty plea, the question remains: Are plea agreements or prosecution agreements more likely to result in recidivism? Although the possibilities of reputational damage and negative media attention may both be operant for companies pleading guilty versus those offered prosecution agreements (Alexander & Arlen, 2018), we do not know whether or how these collateral consequences translate to the possibility of future violations. Based on recidivism research with individuals, we might expect that, like juveniles and first-time offenders, companies diverted from the criminal sanction will be less likely to re-offend (Knoth & Ruback, 2021).

There is also the consideration of what changes the organization may have made post-sentencing. Did they replace some or all of their executive officers or board of directors? If there was a compliance program or independent monitor ordered as part of the prosecution agreement, did this lead to structural changes in the company that may influence their likelihood to engage in further violations? 6 Because the companies are publicly traded, there is more information on their structure and finances that could and probably should be incorporated in further research.

Limitations of the Current Study

Like all studies, ours is not without its limitations and complications. A clear concern when conceptualizing this study was the difficulty in agreeing on how to measure corporate recidivism. Obviously, using a different measure of recidivism would result in different results.

It is clearly not possible to use the same criteria to measure corporate deterrence as individual deterrence because many traits applicable to people are not applicable to organizations. Since organizations can be charged with violations of civil, criminal, and regulatory law, each on the state and federal levels, we had to determine which of these kinds of violations should be considered recidivism. As previously mentioned, the United States Government Accountability Office (2009) reported that pretrial agreements are only intended to prevent the same type of activity that initiated the agreement. However, scholars historically have considered any type of violation to be recidivism, since companies are rarely criminally prosecuted (for more information on the types of interventions used with companies, see Simpson et al., 2014). Our decision was to include all violations reported in the Violation Tracker because there was no clear guidance on what violations should be considered as a case of recidivism.

The nature of conducting research on organizations lends itself to several complications based on the relative fluidity of organizational operations. Organizations can change their ownership structures, leadership structures, or merge and acquire companies relatively easily. Some of these changes can be completed without much publicity. Many changes in ownership, company mergers, or acquisitions involve changing an organization’s name to reflect its new identity. Organizations can also change their names in an attempt to avoid bad publicity, potentially after a violation, scandal, or being on the wrong side of legal action. While we attempted to track the companies in our sample as completely as possible, it is possible that we did not find cases that were listed in the Violation Tracker under a company’s alternate name. We noted all company name changes that we learned during the course of our research and attempted to conduct searches on all name variations, but there are likely records under other names that we did not find. We found previous or subsequent names, nicknames, or common abbreviations for 57 of the 161 companies in our sample. Records in the Violation Tracker could be under any of these names, complicating the calculation of subsequent cases. For example, our sample included the Bank of New York, which is currently known as Bank of New York Mellon Corp. The records for this bank were included in the Violation Tracker under the names Bank of New York, Bank of New York Mellon, Bank of New York Mellon Corp., Bank of New York Mellon Corporation, The Bank of New York, The Bank of New York Mellon, and BNY Mellon.

Because the companies in our sample are publicly traded, they can be “parent companies” to other companies with similar names and work in tandem with those companies (called subsidiaries). Measuring recidivism can be difficult when a subsidiary and its respective parent company are penalized (Yannett et al., 2017). Similarly, records of violations can include partial company names that might be the company in our sample, a subsidiary or related company, or a company by the same or a similar name that is not related. For example, “Helmerich & Payne” is listed as a company that signed a pretrial agreement in the CPR. We conducted additional research and identified the full company name as Helmerich & Payne, Inc. We also identified that Helmerich & Payne International Drilling Company is a subsidiary of Helmerich & Payne, Inc. Therefore, records listed specifically under “Helmerich & Payne International Drilling Company” were not considered cases of recidivism for Helmerich & Payne, Inc. However, we could not determine if records listed only under “Helmerich & Payne” were for the parent company or subsidiary. When this situation occurred, we conducted additional research to determine if these similar names were factually the company in our sample, but additional information was not available for some cases. When we could not determine if the record in the Violation Tracker was for our company, we did not count it as a violation.

Additionally, to effectively count the subsequent violations, we had to be able to identify duplicate violations. It is not unusual for one company to be sanctioned by multiple entities for the same action, so we attempted to identify violations that appeared duplicative to determine if they should be considered a recidivist case or not. The Violation Tracker assisted with this by using an asterisk to indicate duplicate penalties, such as when a company was sanctioned by the federal government as well as a specific state. When we found multiple violations for the same activity in the VT data, we removed duplicates from the dataset, retaining the single federal case. There were some records where we could not accurately make a determination regarding duplication, in which case we again did not count the violation as a subsequent violation. We used the agreement date when determining whether a violation should be considered a recidivist violation, but this was not straightforward. It is possible that a company could be undergoing other legal or regulatory action with another agency at the same time as the pretrial agreement. We cannot know exactly when illegal behavior took place or when the agency learned of the activity, only when an agency took legal action. To address this complication, we decided to rely on a comparison of the agreement date in the CPR to the recorded dates for subsequent violations.

As with prior research, we did not find much evidence that subsequent violations reinstated the presumed sanctions that were deferred by the pretrial agreement. The major conclusion from this research is that pretrial agreements do not appear to deter violations generally, but they may deter criminal violations specifically. Therefore, the major policy implication is that if the government would like to deter violations generally, adjustments could be made to the pretrial agreement process. Perhaps more stringent criteria could be required to initiate an agreement, the penalties could be raised, or the subsequent violations could be punished more harshly.

Implications of the Current Study

This research has multiple policy implications, many of which were highlighted by the U.S. government in fall 2021. In her speech on October 28, 2021, U.S. Deputy Attorney General Lisa O. Monaco highlighted the need to “strengthen the way we [the federal government] respond to corporate crime” (Monaco, 2021). She noted that: “going forward, prosecutors will be directed to consider the full criminal, civil and regulatory record of any company when deciding what resolution is appropriate for a company that is the subject or target of a criminal investigation” (Monaco, 2021). Rather than focusing only on relevant previous charges, Monaco stressed taking a broader look at previous violations to ensure the punishment is appropriate given the entity’s history. This was because investigators in her office noted that “somewhere between 10% and 20% of all significant corporate criminal resolutions involve companies who have previously entered into a resolution with the department” (Monaco, 2021). Monaco stressed that recidivist behavior should be taken seriously.

Deputy Attorney General Monaco also expressed some concerns with the use of pretrial agreements, several of which came to light during this research as well. Monaco said that organizations should not be able to sign multiple pretrial agreements because that sends the message that pretrial punishments are not taken seriously (Monaco, 2021). Additionally, organizations that breach the terms of their pretrial agreements should be seriously punished for their violations. Monaco reported that she would be forming a Corporate Crime Advisory Group composed of varied governmental representatives who are involved in corporate criminal enforcement to ensure her goals of strengthened punishment are achieved (Monaco, 2021).

These suggestions from Deputy Attorney General Monaco encourage purposeful tracking of corporate violations, increased penalties for corporate violators (especially repeat violators), and dedicated efforts to enforce prosecution to ultimately deter corporate crime. This research has identified that these are valid concerns the government is right to emphasize. Our results suggest that increased transparency and enforcement might decrease corporate crime, but we cannot definitively say what factors are tied to corporate recidivism after this preliminary examination. Our results cannot determine causality between the signing of pretrial agreements, or the penalties associated with those agreements, and subsequent offenses. It does appear that companies that are assessed higher payments have decreased rates of recidivism. Based on our results, the severity of the penalty may be more important in reducing corporate crime than greater enforcement.

Criminological research on the ineffectiveness and draconian nature of “three strikes and you’re out” and other get-tough policies suggest this isn’t the answer, but the realistic perception that it's “three strikes and no one cares” when it comes to corporate crime is also clearly problematic.

Footnotes

Acknowledgments

The authors would like to thank Brandon Garrett, Jon Ashley, and Philip Mattera for providing public access to the data used in this study. The authors would also like to acknowledge the University of North Carolina Wilmington’s Research Community in International Trade and Exchange (RCITE) and U.S. District Courts Multi-Court Exemptions Court Programs Division for their support of this research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by University of North Carolina Wilmington’s Research Community in International Trade and Exchange (RCITE).