Abstract

For sustained business growth, it is imperative to be proactive rather than reactive to issues of public interest. Had the new banking regulation amendments been introduced earlier, could they have prevented the Punjab and Maharashtra Cooperative (PMC) Bank debacle?

The bank being put under the limits of the Reserve Bank of India (RBI) for six months was the dreaded headline on 23 September 2019. This was later revealed to be one of the country’s worst financial scams. PMC Bank, a top 10 cooperative bank, was interdicted by the RBI for under-reporting the loan sum sanctioned to HDIL (Housing Development and Infrastructure Limited) and misreporting non-performing assets (NPA) in their annual report. As an immediate consequence, all core activities of the bank came to a halt. Customers who had put their life savings in the bank never imagined that it would result in the deaths of up to eleven people and the devastation of hundreds of homes. It raises an important question about the governance standards upheld by a financial institution such as PMC Bank. Are the recent amendments to the Banking Regulation Act (2020) adequate to strengthen the regulations and corporate governance practices? Furthermore, will these amendments instil trust in a new depositor already perplexed by such news?

Introduction

Mr Patel, a 60-year-old retiree, wants to put all of his life savings into a bank term deposit. He has worked hard his entire life and has set aside a significant sum of money for his retirement. He has seen numerous instances of people, organizations or groups running away with other people’s money in his life. As a result, he is more inclined to safety and reasonable returns in this period of his life, despite being conservative and careful. He talked to a lot of his friends and conducted some research to spot the right avenue that would be safe and yield higher returns. Finally, he chose to place all of his savings into a term deposit with a reputable cooperative bank because of its trustworthiness and greater interest rates than other banks, particularly commercial banks.

His aspirations were dashed when he read the headline on 23 September 2019: PMC Bank has been placed under the RBI’s (Reserve Bank of India) control for six months, which eventually turned out to be one of the country’s greatest financial swindles (Sokhi, 2019). He also learned about PMC’s unholy partnership with HDIL’s promoters (Kapoor, 2019a). He is now left with a slew of unresolved questions: How did a well-known cooperative bank become involved in such a scam? What caused this crisis in the first place? Is this a result of the RBI’s negligence? How did HDIL proponents pull off such a massive con? Is this a wake-up call for the RBI? In such a case, what will happen to the depositor’s money?

In such an uncertain circumstance, he decided to pose these issues to a panel of experts who could explain the situation to him, helping him to make an informed decision regarding his investment strategy.

About PMC Bank

A single branch of the Punjab and Maharashtra Cooperative (PMC) Bank was established on 13 February 1984, in a modest office in Sion. Under the Cooperative Societies Act, 1955, the bank is currently a Scheduled Urban Cooperative Bank (UCB), operational in multiple states and controlled and overseen by the RBI and CRCS (Central Registrar of Cooperative Societies).

The bank’s operations span seven significant Indian states. It has been able to expand its network to 137 locations throughout different states over the years. In March 2019, total income of ₹12.98 billion (USD 171.63 million) was earned from deposits of ₹116.17 billion (USD 1.54 billion) and credit of ₹83.83 billion (USD 1.11 billion). The company’s net earnings were estimated to be around ₹ 0.996 billion (USD 13.17 million). 1

The Chairman of PMC Bank was S. Waryam Singh, and the Vice Chairman was S. Balbir Singh Kochhar. The bank was one of the top 10 cooperative banks in the country. The RBI gave it scheduled status in 2000, making it the country’s youngest bank. In 2004, the Central Registry Office bestowed multi-state status on the PMC Bank. The bank was thereafter included in the National Platform. The RBI additionally licensed it as a Class I authorized dealer for the forex industry in 2011 (Kapoor, 2019b; Sokhi, 2019).

Cooperative Banks in India

Established in India under the Cooperative Societies Act of 1912, cooperative banking institutions are cooperatives. These banks are governed by RBI regulations under the Act of Banking Regulation 1949 as well as laws for cooperative societies under the Banking Laws Act 1955. Both urban and rural cooperative banks exist in India. Non-scheduled and scheduled are two sorts of UCB. The two types of scheduled and non-scheduled banks are single-state and multi-state. The RBI regulates and monitors UCB, as do the State Registrar of Cooperative Societies (RCS) for single-state banks and the CRCS for multi-state banks. In India, rural cooperative credit banks offer both short-term and long-term loans.

In the majority of states, the three-tiered short-term credit framework consists of Primary Agricultural Cooperative Societies (PACCS) at the village level, District Central Cooperative Banks (DCCB) at the district level and State Cooperative Banks (SCB) at the state level. The short-term credit structure offers credit ranging from one to five years. The long-term credit framework addresses the farmers’ requirements for credit up to twenty years. It consists of two tiers: State Agriculture and Rural Development Banks (SARDBs) and Primary Agriculture and Rural Development Banks (PARDBs), which operate at the village level (Kapoor, 2019b).

The Day of Crisis

After discovering that the Punjab and Maharashtra Cooperative Bank Ltd. (PMC Bank), headquartered in Mumbai, had underreported and misreported non-performing assets (NPAs) and other financial data for more than six months, the RBI placed an embargo under Section 35A (sub-section 1) of the Banking Regulation Act 1949 on the bank, preventing it from conducting any major banking operations for the next six months (Sokhi, 2019). The RBI’s order did not mean that the banking license was revoked. The order stated that the bank shall be deprived of its core banking activities, such as renewing or issuing loans, making acquisitions, accepting new deposits or disbursing any payments except for employee salaries, energy bills and other office expenses, as of 24 September 2019. ATM services were withdrawn from the payment system, as were online banking facilities. Regardless of the type of account they had, depositors were not allowed to withdraw more than ₹1,000 (Sokhi, 2019).

PMC Bank customers were stunned and enraged by this news, and they rushed to the bank’s various branches to have their questions answered by bank officials. The customers were further dismayed when branch officials were absent from several branches and ATMs were either shut down or temporarily non-functional with a letter of apology taped on them. This caused further mystification outside Mumbai’s branches of the bank (Mengle, 2019; Sokhi, 2019).

Adverse Repercussions

This scam came down as a thunderclap for the bank’s customers. The festive season was approaching, while the bank was placed under the RBI administrator with withdrawal limits. It was reported that eight PMC depositors lost their lives in the aftermath of this scam (Press Trust of India, 2019e). Customers who used a PMC Bank account to make EMI payments on loans from other institutions were denied the funds. The payment of monthly utility service-linked user accounts was also denied. This crisis reportedly claimed the lives of more than 11 individuals because of the severe financial losses sustained by the customers. The first incidence was the suicide of Nivedita Bijlani, who had a bank account balance of over 10 million (USD 0.13 million) (Press Trust of India, 2019c). Another incident was reported in which Murlidhar Dharra, an 83-year-old PMC Bank customer with deposits totalling over ₹8 million (USD 0.105 million), was unable to withdraw the money owing to RBI limitations. He died as a result of his inability to come up with the funds to pay for a life-saving heart operation (Press Trust of India, 2019d). These were some of the depositors at PMC Bank who were suddenly left in the lurch. In the end, customers who had put their trust in the bank to keep their money safe ended up being the ones responsible for their financial difficulties (Press Trust of India, 2019b, 2019c, 2019d).

A strong correlation exists between financial news and stock prices. Consequently, following the exposure and revelation of this fraud, despite PMC Bank not being listed on the Sensex and Nifty indices, the bank’s stocks experienced a significant decline. On the national stock exchange (NSE), the share price of Yes Bank witnessed a decline of 25.42% from 55.50 to 41.40. In comparison, the share price of State Bank of India fell 10.24% from 301.70 to 270.80, RBL Bank fell 14.12% from 382.95 to 328.85, Induslnd Bank fell 2.53% from 1419.60 to 1383.55 and IDFC First fell 6.72% from 43.10 to 40.20. The aforementioned share price was recorded on 20th September 2019 and 30th September 2019. 2

Core Reasons of the Scam

The nucleus of the crisis was the under-reporting of the loan sum approved to HDIL (Housing Development and Infrastructure Limited), a listed real estate development company that was already bankrupt, as well as the misreporting of the NPAs in their annual report by the PMC Bank.

It all began when the HDIL promoters opened a deposit account with PMC Bank in 1986. This was the beginning of their unholy relationship. When that relationship grew, it became an illegal lender-to-borrower linkage. S Waryam Singh, chairman of PMC Bank, held a 1.91% stake in HDIL till September 2017. In 2005, he joined the HDIL board as a director and later resigned to rejoin the PMC Bank as chairman in 2015 (a post he had held previously between 1999 and 2005). Furthermore, Singh served as a non-executive director at HDIL, was identified as one of the promoters of the company and had dealings with several other organizations managed by the Wadhawans, the HDIL founders. He was the director of the bank during his stint at HDIL (Kapoor, 2019a). Despite the involvement of the PMC Bank management in this scam, it is plausible that senior bank officials also took part and complied with the management’s instructions due to personal reasons or financial gain.

Financial Deception Strategy

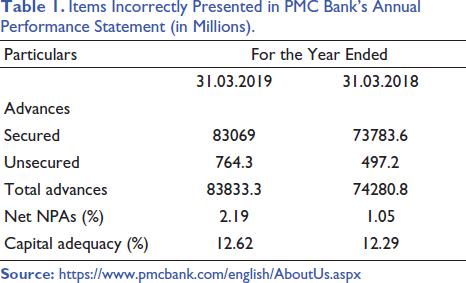

PMC Bank’s net exposure to the HDIL group was ₹62.26 billion (USD 823.2 million) (including interest accrued in related accounts). It was four times the statutory limit and accounted for roughly 73% of the bank’s total loan book of around ₹83.83 billion (USD 1.11 billion) as of 31 March 2019. Just ₹4.40 billion (USD 58.17 million) was reported to the RBI, which left the remaining ₹57.86 billion (USD 765.04 million) unaccounted for. The bank concealed this crucial data by reporting a net NPA of only 2.19% as of 31 March 2019, while the real NPA rate was 60–70% (IANS, 2019; Kapoor, 2019a). Despite HDIL’s payment defaults, the loan was not acknowledged as a NPI by PMC Bank’s auditors (IANS, 2019). The item presented incorrectly in PMC Bank’s Annual Performance Statement is indicated in Table 1. 3

Items Incorrectly Presented in PMC Bank’s Annual Performance Statement (in Millions).

Moreover, PMC Bank extended a loan at a time when the Bank of India and several other financial institutions, including Dena Bank, Syndicate Bank, Corporation Bank, etc., had filed several petitions against HDIL in the National Company Law Tribunal (Mumbai bench) for loan defaults under the Insolvency and Bankruptcy Code (Section 7). Furthermore, despite an unpaid loan against HDIL, PMC Bank granted a loan of about ₹965 million (USD 1.28 million) to HDIL, which it used to clear their dues to the Bank of India (Kapoor, 2019b).

The Mumbai Police’s Economic Offence Wing (EOW) found 21,049 phony accounts in the bank’s databases after conducting an investigation. They were used as a substitute for the HDIL group’s 44 real accounts. In these forged accounts, the HDIL group’s loan total was evenly disbursed. The PMC Bank capitalized on the dual regulation of UCBs, which prohibits the RBI from performing administrative and management functions, including supervising boards, removing directors, auditing, incorporating, registering, managing, amalgamating, reconstructing or liquidating UCBs (Rai & Choudhary, 2019). These responsibilities were supervised by the CRCS under the Cooperative Societies Act of the States. RBI could only regulate banking-related matters, including inspection, interest rates, lending policies, investments, prudential exposure rules, license issuance, cash reserve maintenance, statutory liquidity and capital adequacy ratios, and inspection.

Legal Actions Undertaken

The Economic Offenses Wing in Mumbai arrested the Chairman of PMC Bank. The office-bearers were also suspended. Moreover, in October 2019, HDIL’s promoters were arrested as well. The statutory auditors who made their job easier by concealing and misreporting financial data were also detained. The Bombay High Court formed a three-member panel to value and sell HDIL’s immovable properties in order to hasten the collection of the unpaid dues from the crisis-hit PMC Bank. The Enforcement Directorate seized properties worth ₹38.3 billion (USD 506.4 million) under the Act on Money Laundering Prevention (Press Trust of India, 2019a).

Immediate Corrective Measures taken

After media reporting and exposure of the scam, there was a widespread outcry and pressure on the RBI. The original withdrawal limit of ₹1,000 was raised over time to a total of ₹0.1 million (USD 1.32 thousand) by the RBI on 19 June 2020 (Roy, 2020). In total, 84% of the bank’s depositors were able to redeem their full account balances. The RBI has taken several significant measures to strengthen cooperative banks and to avoid a repetition of such a crisis in the future. PMC Bank has requested EOIs (Expressions of Interest) from potential investors in order to secure the bank’s recapitalization and return to business (Panda, 2020). In her budget for fiscal year 2020–2021, the Hon’ble Finance Minister, Smt. Nirmala Sitharaman, stated that the insurance cover on bank deposits would be raised from ₹0.1 million to ₹0.5 million (IANS, 2020). However, the customers will not receive the same in the first lot.

Banking Regulation Amendments 2020

In the aftermath of the PMC Bank crisis, the hon’ble finance minister, Smt. Nirmala Sitharaman, tabled the Banking Regulation (Amendment) Bill, 2020. By amending the Banking Regulation Act of 1949, the Banking Regulation (Amendment) Bill of 2020 grants the RBI greater regulatory authority over cooperative banks concerning capital, management, audit and liquidation (Press Trust of India, 2020; Reserve Bank of India, 2021). It includes the following major provisions (Reserve Bank of India, 2021):

Establishing an Umbrella Organization: It would provide liquidity transfers and capital assistance to the UCB when required. It will also unify the IT framework among all UCB members, which will assist UCB partners in upgrading to new technological breakthroughs.

Allow UCBs to Raise Funds: As the UCBs are not listed, the new amendment will help the UCB, with prior sanction of the RBI, issue equity, preference or special shares to its members, as well as anybody else that lives in their region of operations, at face value or at a premium. Furthermore, UCBs can also issue unsecured debentures, bonds or other similar securities to individuals with a 10-year or longer maturity. However, there is no mention of redemption.

Criteria for Management Qualifications: Individuals who have been convicted of a depraved character offense or who are insolvent are not permitted to serve as chairman of cooperative banks, per the amendment. If the chairman does not satisfy the requisite qualifications, the RBI possesses the jurisdiction to dismiss him and, if the bank is unable to do so, designate a successor. Additionally, the bill stipulates that a minimum of 51% of the members of the Board of Directors must possess specialized knowledge or practical experience in fields including but not limited to accounting, finance, economics or law. It grants the RBI the authority to order a bank to reestablish the board in the event that it fails to meet the stipulations. The RBI may remove individual directors and appoint appropriate replacements if the bank fails to comply.

Supersedure of Board of Directors: The RBI has the authority, under the Banking Regulation Act of 1949, to appoint an administrator and issue an order to supersede the Board of Directors of multi-state cooperative banks for a maximum of five years. In the case of other cooperative banks, the RBI would petition the RCS to take precedence over the board. However, the amendment now grants the RBI authority to take precedence over the Board of Directors in all cooperative banks. If the bank has a state RCS registration, the RBI may issue the order after consulting with the appropriate state government and requesting its input within the RBI-specified timeframe.

Audit: The amendment would ensure that audits of cooperative banks are carried out in the same manner as those of scheduled commercial banks. A qualified individual would conduct an audit of the accounts, and prior sanction from the RBI would be necessary for the appointment, reappointment or removal of an auditor. The RBI may mandate a special audit for the transactions and time periods that are specifically outlined in the order. In the past, the RBI’s authority was limited to supervising cooperative institutions through an additional audit.

Authorize Task Force on Urban Cooperative Banks (TAFCUB): Although TAFCUB has received authorization to address the difficulties faced by financially troubled banks in their early stages of distress, it has not yet started the supervisory action framework (SAF).

Alternative Mandatory Mergers: Small banks that do not satisfy the basic requirements but continue to operate will be encouraged to merge voluntarily. This, however, will necessitate timely supervisory interventions.

PMC Bank’s Resolution

Although the new provisions in the Banking Regulation (Amendment) Bill, 2020, won’t immediately ameliorate the situation at PMC Bank, they will be beneficial and affective for cooperative banks—in this case, UCBs—if PMC Bank-related scams arise in the future. The RBI has given Centrum Financial Services Limited and BharatPe ‘in-principle approval’ to establish a small finance bank (SFB), clearing the path for the organization to acquire the financially troubled PMC Bank. BharatPe, in collaboration with Centrum Group, has established a consortium and received a SFB license, making it the pioneer fintech company in India to hold its own SFB license. After the creation of the SFB, all of the liabilities and assets will be merged into the newly formed SFB (Sahay, 2021).

Mr Patel’s Mystification and Way Forward

Mr Patel looked at the current predicament of UCBs and found that UCBs are still minimally regulated by the government (state or central), notwithstanding the amendments, owing to the perception that they are democratic organizations. Furthermore, to stay afloat in the banking sector, UCBs continue to adopt a flexible regulatory capital requirement for maintaining a minimum level of capital and reserves (net worth), a capital-to-risk weighted asset ratio (CRAR) or a capital adequacy ratio. On the other hand, amendments under the Banking Regulation Amendment Act, 2020, such as forming an umbrella organization and allowing UCBs to raise funds, reinforcing governance, authorizing a task force on UCBs (TAFCUB), abolishing the market share aim and implementing alternative mandatory mergers would all have a substantial impact on how UCBs function. As a result of these amendments, RBI may now be able to effectively manage UCBs. Mr Patel’s research was completed. The meeting with the expert group has likewise come to an end. Now that he has all of the facts, he can make an informed decision. His understanding of the facts has confused him, though. He is trying to comprehend: why did they pull off an unholy relationship without apprehension? Should not our system be proactive rather than reactive? Both the benefits and drawbacks of current UCBs have put him in deep thought.

Footnotes

Declaration of Conflicting Interest

The authors declared no potential conflicts of interest concerning the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.