Abstract

The management was reviewing Tesco’s entry into India and its joint venture Trent Hypermarket Private Limited’s operations. After withdrawal from Thailand and Malaysia, India remained one of the most important retail destinations for Tesco. The management was pondering over the expansion of operations in India. The local leadership was entrusted with developing a Roadmap-2025 with an inclusive store expansion plan to build profitability by delivering high customer value.

Tesco

In a meeting with the board of directors in March 2020, the top management of Tesco was discussing expanding the business of Tesco in the Asian subcontinent, wherein they had several options to choose from. Tesco’s internal assessment suggested that there are plenty of untapped opportunities in Asia. YouGov reputation survey established Tesco Lotus was the 10th most valued brand in Thailand (YouGovBrandIndex, 2019), and Tesco’s reputation was getting stronger in Malaysia (Aman, 2019). Despite Tesco’s success in Thailand and Malaysia, it had to retreat in March 2020 from both markets.

Despite recent exits from Thailand and Malaysia, Tesco was fully committed to capitalizing on possible growth and expansion opportunities in Asia. The strategic fit analysis of the company suggested that Asia was reset for growth. Tesco’s management identified that to be successful in Asia the retailer must master: reducing running cost and capital expenditure (CAPEX) create new propositions based on differentiation, seizing high-value growth opportunities. For Tesco, lowering the running cost of large stores, improving return on small stores and creating convenience remained on top of its agenda in Asia.

The top management was reviewing its entry and operations in India. The review report suggested that on the financial performance front, its Indian subsidiary was improving, whereas store expansion was lower than expected. Tesco’s management was worried and highly concerned about the growth of store expansion in India. After Tesco’s exit from Thailand and Malaysia, the tension in India operations was much more prominent.

Top management of India operations was asked to develop a Roadmap-2025 for India expansion. In this context, Mr Aniket Bansal—the Head of Retail Operations (India), was asked to prepare a Roadmap-2025 and submit the same by 15 August 2020. Deciding on the right format mix and store expansion was the key to the Roadmap-2025.

On 20 April 2020, Aniket called Mr Daniel Mitra—the Head, Finance, and Mr Varun Verma—Head, Projects and Engineering and Ms Laxmi Madhavan—Associate Director of Information Technology for a meeting to chalk out the future course of action. 1 Aniket greeted his colleagues and said he was facing several dilemmas, including consolidation vs. expansion, and opening small stores vs. large stores.

Tesco’s Background

Tesco was founded in 1919 as a group of market stalls in London by Jack Cohen (Tesco, n.d. (a)). After Cohen purchased a shipment of tea in 1924 from T. E. Stockwell and combined the initials of the company with the first two letters of his surname, the Tesco name was derived. Through the 1930 and 1940s, Tesco acquired stores and expanded its operations across London, into the suburbs and neighbouring counties (Tesco, n.d. (a)), introduced a concept of self-service stores to the UK market. The company’s market capitalization was valued at £25.19 billion (Tesco, 2020a).

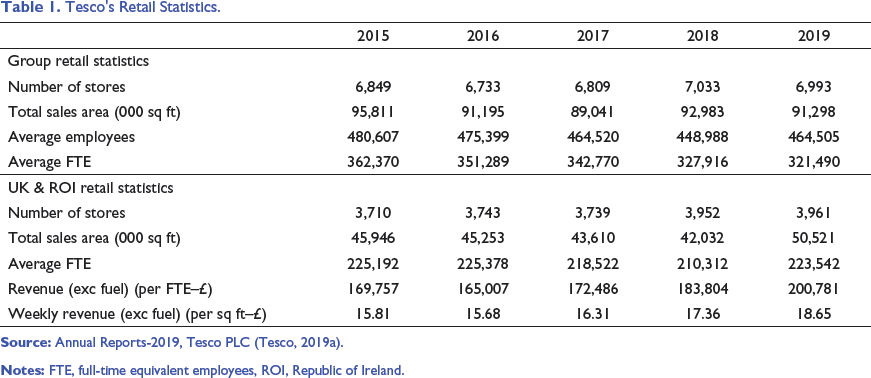

Tesco, a United Kingdom-based multinational retailer, operated in domestic and international destinations such as Ireland, Poland, Czech Republic, Slovakia, Hungary, Malaysia, China and India. The retailer had a strong workforce of 464 thousand, operating over 6,993 stores across the world, out of which 3,961, 2,038 and 895 stores in the UK and Republic of Ireland (ROI), Asia and Central Europe, respectively (Table 1). The group achieved sales of £56.9 billion in 2019 compared to £49.9 billion in 2015. The retailer operated 91,298 thousand square feet of retail space with an average full-time equivalent employee of 321,490. The retailer generated an operating profit of over £2.2 billion in 2019.

Tesco's Retail Statistics.

Overseas Expansion

Tesco's entry into Ireland in the 1980s (The Guardian, 2011) and France (The Guardian, 2014) in 1993 was not fruitful, therefore resulted in the exit. Under global expansion, in 1994 the group bought Hungary’s S-Market, kicking off a phase of international expansion that took the retailer as far as China, Korea and Turkey.

Tesco Outside Europe

Tesco’s ambitious expansion beyond familiar territory in the UK and Europe fetched a mixed bag of responses. This section presents highlights of Tesco’s operations outside Europe.

Tesco Japan

Japan, the toughest retail market offered no surprises to Tesco. The group’s entry to Japan through the low-key acquisition of the Tsurukame group of small supermarkets could not sustain in Japan. Just after eight years of operations, Tesco had no option but to retreat from Japan in 2012. The retailer failed to sense cultural differences, which troubled Tesco and many other foreign retailers such as Carrefour and Sephora (Financial Times, 2011). In Japan, Tesco failed to control cost, offer the personal touch, bridge cultural differences and more importantly, meet high customer expectations.

Tesco USA

In 2006, Tesco announced entry into the most advanced and competitive retail market-United States of America (USA). The group entered the USA in 2007 under the banner name ‘Fresh & Easy’, but the brand and its value proposition failed to impress American consumers. Therefore, Tesco exited from the US market in 2013 by liquidating unsustainable business operations. Possible reasons for Tesco’s failure in the US could be lack of adaptability to the taste of local consumers, demystifying the diversity in the US compared to the UK, and lack of patience (Opentoexport, n.d.). The Guardian called Tesco’s exit a ‘big failure’ (Butler, 2012) and probably one of the biggest strategic blunders of ignoring market research.

Tesco Thailand and Malaysia

In 1998, Tesco entered Thailand to expand its footprint in Asia. Tesco was operating under Tesco Lotus in Thailand with 1,967 stores across format generating £4.1 billion in revenue (excl. VAT, incl. fuel) in the financial year 2019. Tesco Thailand served over 13 million customers each week (Tesco, 2019b). Tesco appreciated changing consumer behaviour; in 2001, Tesco Lotus introduced ‘Tesco Lotus Express’ its first small-format store. The smaller format intended to addresses consumer concerns about convenience and affordable prices (Tesco Lotus, n.d.). In 2013, Tesco Lotus introduced an online platform for shopping. In 2017, Tesco decided to liquidate the ‘bulk selling’ operation in Thailand due to unprofitable operations (Financial Times, 2017).

Tesco Malaysia—a joint venture (JV) between Tesco and Sime Darby Berhad operated over 68 stores with revenue of £0.8 billion (excl. VAT, incl. fuel) in Malaysia.

The Tesco board conducted a due strategic review, the conclusion emerged that disposal of Thailand and Malaysia retail business was in the best interest of the shareholders. In 2020, Tesco agreed to sell its retail business in Thailand and Malaysia at a value of £8.76 billion to Thailand’s CP Group entities. The Tesco Board ‘intends to return £5.0 billion to shareholders via a special dividend with associated share consolidation’ (Tesco, 2020b). The disposal was expected to reduce indebtedness through a £2.5 billion pension contribution, and the deal was expected to cut down the funding deficit.

Tesco: Strategic Drivers and Risks

Tesco group identified six strategic drivers to become a stronger brand and relevant to the shoppers. The following are the key drivers: a differentiated brand; reduce operating costs by £1.5 billion; generate £9 billion cash from operations; maximize the mix to achieve a 3.5–4.0% margin; maximize value from the property; and innovation (Tesco, 2018). One of the conventional risks, political, regulatory and compliance, remained a strong challenge. Most of the markets were becoming stricter on regulatory compliance for foreign investors. Therefore, global operations needed to guard against anticipated political and regulatory changes.

Tesco: Competition and Branding

Tesco operated in a highly competitive market in the UK, which was facing stronger competition from Asda, Sainsbury and Morrison. Tesco-UK’s largest retailer could have been hit hard by the proposed merger of Sainsbury’s and Asda. Fortunately, the merger deal was blocked by the Competition and Market Authority—the watchdog (Wood, 2019).

Core to Tesco’s success story was the customer. Tesco’s chief customer officer Alessandra Bellini rightly pointed out that ‘The times when Tesco thrives as a business are when it puts its customers at the centre of it and when we haven’t done that, things haven’t gone so well for us’ (The Grocer, 2019). The stated core purpose of Tesco was ‘serving shoppers a little better every day’, therefore, they try harder to understand the customer and meet their needs. Further, the retailers ensured sourcing excellent quality, affordable and sustainable products (Tesco, n.d. (b)) to serve their customers.

Tesco’s Need for Expansion

By the end of March 2020, based on the financial and strategic fit analysis for expansion in the Asian subcontinent, Tesco realized that the retail sector in India was in the growth phase and contributed about 10% of the gross domestic product (GDP) in 2018. The retail industry continued its growth path to reach £673 billion in 2018 at a compound annual growth rate (CAGR) of 13%. The first time this industry was expected to exceed the £779 billion mark by 2020 (IBEF, 2020b).

India was the fifth-largest global destination in the retail space. Therefore, Tesco committed to expanding its business in India. The management team in India was rigorously thinking about an apt expansion plan with minimal chances of failure. Aniket was asked to offer more insights on the same and decide about the location as well as store formats as per the feasibility of expansion in those areas.

Tesco in India

Tesco in Bengaluru, established in 2004, was a multi-disciplinary team with the goal ‘to create a sustainable competitive advantage for Tesco by standardizing processes, delivering cost savings, enabling agility and empowering colleagues to do even more for customers’.

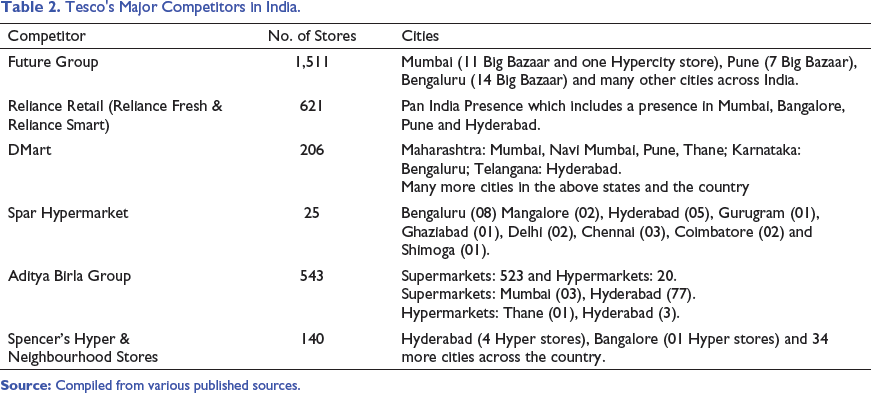

Tesco's Major Competitors in India.

Generally, subject to regulatory permissions, an international retailer could enter the international market through any mode of entry, namely non-controlling interest, setting up international stores, merger or takeover, franchise model, a JV and cash and carry.

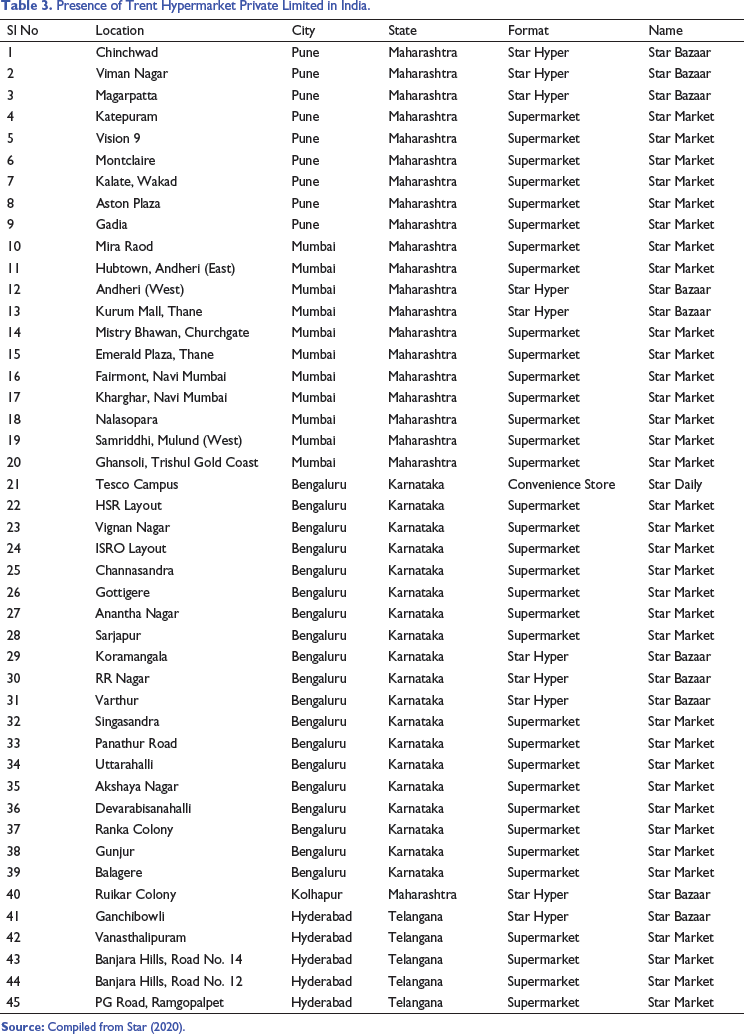

Due to prevailing regulatory restrictions, in 2008, Tesco entered India through a cash and carry format, essentially a wholesale business. Relaxations in foreign direct investment (FDI) norms for the retail sector enabled Tesco to seal a deal with the Trent Limited—A Tata group company to operate a JV (50:50) under Trent Hypermarket Pvt Ltd (THPL). In 2014–2015, Tesco invested about £82 million (Verma, 2014) to acquire 50% stake in THPL. Tesco management felt that JV was the safest route for Tesco to increase its presence in India. The deal was expected to offer a durable first-mover advantage to Tesco in India. THPL operated multiple formats such as the Star Bazaar, Star Market and Star Daily, which meant Tesco got immediate market access to retail business in India.

Presence of Trent Hypermarket Private Limited in India.

Star Market was a supermarket predominantly positioned ‘as a one-stop-shop’ providing solutions to the shopper's monthly and top-up needs for ‘groceries, fresh produce, FMCG products, personal grooming, and general merchandise’ (Star, 2020). Star Market was the anchor concept targeted at the monthly and top-up needs of consumers. THPL operated 34 stores under the name of Star Market in Maharashtra, Karnataka and Telangana. The size of the store was in the range of 5,000–10,000 sq ft (Trent, 2019).

THPL also operated Star Daily—a neighbourhood format store ranging between 2,000 and 5,000 sq ft stocking vegetables, groceries, fish and poultry (Mazumdar, 2018). As reported by Financial Express, due to financial un-viability THPL had shut down 20 Star Daily stores. Only Star Daily was operational in Tesco Campus, Bengaluru, to serve its employees.

The media reported that THPL intended to expand store count to 200 stores by 2020 (Mazumdar, 2018). However, by March 2020, the retailer could manage operations of only 45 stores, which included 10 Star Hyper, 34 Star Market and one Star Daily.

THPL generated a total income of £98 million in FY19 vis-à-vis £93 million in FY18. The losses declined from £8.75 million in FY18 to £8.2 million in FY19 (Trent, 2019).

Retail Sector in India

Indian retail industry had become one of the most dynamic and fast-paced industries with the addition of several new players in recent years. Total consumer spending was expected to increase from £129 billion in 2017 to nearly £2.55 trillion by 2020. It accounted for more than 10% of the country's GDP and about 8% of the employed population. As per AT Kearney Retail Development Index-2019, India was placed in the second position (Kearney, 2019).

The rapid expansion of retail could be driven by urbanization, income growth, nuclearization and attitudinal shift (BCG-RAI, 2015). As per the Boston Consulting Group (BCG) study, the average household income was expected to increase from £4,528 in 2010 to £13,067 in 2020. During the period under consideration, urbanization improved to 40%, and over 200 million households to be nuclear. Further, 75% of the population would fall under Generation-I, individuals who had grown up in the liberalized economy.

According to the BCG’s report modern trade to expand faster primarily due to rapid consumer evolution, supply-side evolution and positive regulatory environment (BCG-RAI, 2015). The steady growth of modern trade, attracted Indians to do 10% of their shopping in modern stores (Agarwal, 2018).

By the end of December 2019, India’s wireless and broadband subscribers stood over 1,151 million and 662 million (TRAI, 2020). Rising Internet and mobile penetration enabled retailers to widen their customer, product and service base. As a result, the Indian e-commerce market was expected to grow to £142 billion by 2026 from £27 billion as of 2017 (IBEF, 2020a).

Retail Landscape in India

The retail landscape was being shaped by the latest trends as well as emerging market forces. Technological and economic trends had the most profound impact on the transition of the Indian retail sector. Competitive pressures were compounding due to an increase in the number of Indian and international retail players.

In India, policy reforms, decision-making and implementation of the same improved substantially during 2014–2019 (Mishra, 2019; Panagariya, 2020). However, Transparency International reported, ‘even in democracies, such as India, unfair and opaque political financing and undue influence in decision making and lobbying by powerful corporate interest groups result in stagnation or decline in control of corruption’. In Corruption Perception Index-2019 (Transparency International, 2019), India was placed at 80th position along with Benin, Ghana, China and Morocco with a score of 41.

On the contrary, the World Bank acknowledged India’s reform measures, which were visible in its improvement in the ranking of ease of doing business. Amongst the 190 economies, India ranked 63 with a score of 710 (World Bank, 2020). In terms of ease of doing business ranking, India was well on course to figure among the top 50 economies in the world. The World Bank appreciated efforts made by India to start a business, dealing with construction permits, trading across borders and resolving insolvency.

Goods and services tax (GST) had also improved the taxation on the product by keeping different products in separate tax slabs according to their need and importance. According to Lalit Malik, chief finance officer, Dabur India Ltd ‘post GST scenario, general trade took time to adjust to the new norms and modern trade came up to speed very fast, improving its overall saliency from 13% a year ago to 15% of overall revenues now’ (Agarwal, 2018).

Food Safety and Standard Act, 2006 empowered the Food Safety and Standards Authority of India to ‘regulate their manufacture, storage, distribution, sale, and import, to ensure availability of safe and wholesome food for human consumption and matters connected therewith or incidental thereto’ (Ministry of Law and Justice, 2006).

FDI in Retail in India: Scope for Tesco

Indian retail trade received £1.42 billion (DIPP, 2019) in FDI equity inflows between April 2000 and December 2019. In 2012, the Government allowed up to 51% FDI in multi-brand retail subject to reasonable conditions (Ministry of Commerce & Industry, 2012). Further, in January 2018, the Government permitted 100% FDI in single-brand retail subject to certain conditions (DIPP, 2018), which opened a window for foreign players in the Indian retail market.

As per consolidated FDI Policy (DIPP, 2017) and amendments thereafter, FDI in multi-brand retail had reasonable restrictions as given below:

The minimum amount to be brought in, as FDI, by the foreign investor, would be £70.83 million. Around 50% of the first trench invests (£70.83 million) to be invested in back-end infrastructure, which included ‘investment made towards processing, manufacturing, distribution, design improvement, quality control, packaging, logistics, storage, ware-house, and agriculture market produce infrastructure’ (PIB, 2019). Around 30% sourcing from Indian micro, small and medium enterprises. Minimum population (one million as per Census 2011) of the cities for setting up retail outlets. Setting up retail outlets needed clearance from the concerned state governments.

Sates/Union Territories such as Andhra Pradesh, Assam, Delhi, Haryana, Himachal Pradesh, Jammu & Kashmir (now UT), Karnataka, Maharashtra, Manipur, Rajasthan, Uttarakhand, Daman & Diu and Dadra and Nagar Haveli (Union Territories) had agreed to allow setting up retail outlets under revised FDI norms (DIPP, 2017).

In the case of single-brand retail, up to 49% of FDI through the automatic route was followed, and beyond 49%, the applicant had to go through the government route. In single brand retail, FDI beyond 51% needed to fulfil 30% sourcing from Indian micro, small and medium enterprises, including those operating in special economic zones (DIPP, 2020).

The government allowed 100% FDI through an automatic route for setting up Cash & Carry Wholesale Trading/Wholesale Trading (including sourcing from medium scale enterprises) in India. Further, Government allowed 100% FDI under the Government approval route for ‘retail trading, including through e-commerce, in respect of food products manufactured and/or produced in India’ (DIPP, 2017). In India, 100% FDI was permitted under the automatic route in the marketplace model of e-commerce, but FDI was not permitted in the inventory-based model of e-commerce.

Consumer Preferences and Behaviour

Preferences of consumers started to shift from conventional to modern and technology-driven products. BCG observed that: ‘increasingly, people were spending more on experiences, customized products, and time-saving services’ (BCG, 2019). Millennials had different preferences than the previous generation. Technology products were more needed than ever, such as smartphones and other white goods in the retail market. The importance of customer service was growing rapidly in India. So, for a new player in the Indian retail market, it was important to emphasize on customer experience and customer engagement.

Need and demand for electronics and gadgets were fastly increasing. Besides the megacities, ‘consumption in cities with less than five lakh population was picking up’ (Mukherjee, 2019), which could be considered a very good sign for retailers. Younger and middle-class consumers with modern tastes certainly excited retailers.

A market survey by ProdegeMR reported that 46% of Indian consumers bought groceries from supermarkets, followed by corner shops (41%) and Online (13%). A study by Capgemini indicated that a majority of customers would shift towards online shopping in India. Indian shoppers invariably wanted value for money. A survey by AC Nielson found that 54% of the shoppers were ‘deal seekers’, which retailers required to keep in mind while designing retail strategies.

Rise of Internet and Mobile Users

As per the Telecom Regulatory Authority of India, by the end of December 2019, India’s wireless subscribers stood over 1,151 million (TRAI, 2020). Just over 662 million subscribers were using broadband connections. Internet Statsworld reported by the end of June 2019 over 560 million Internet users in India (Internetworldstat, n.d.). The retail industry benefited a lot from the increasing number of Internet users in India. Internet accessibility helped retailers to reach beyond conventional turf. Rising Internet and mobile penetration enabled retailers to widen customer, product and services base.

Food and Grocery Retailing

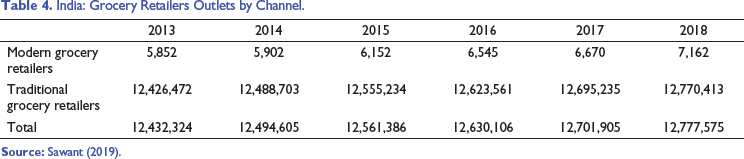

India: Grocery Retailers Outlets by Channel.

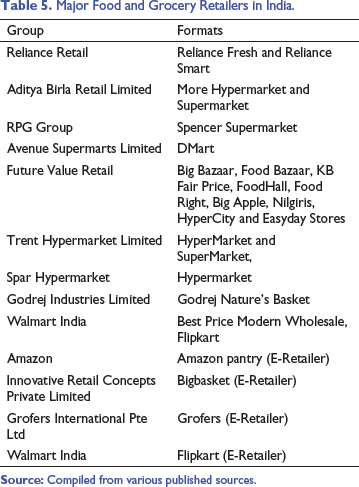

Major Food and Grocery Retailers in India.

The retail market was noticing significant changes in the past few years. Almost the entire modern grocery retail market was concentrated in the hands of leading retailers such as Future Group Ltd, DMart, Future Group Ltd, Aditya Birla Ltd, Reliance Retail Ltd, Spencer’s Retail Ltd and Spar India.

Online F&G retailers started to create their footprint in metropolitan areas. Of late, they are expanding to smaller cities and towns. By the end of 2019, online penetration of grocery retailing still accounted for a very small share in the total grocery retail sector, but analysts predicted that online grocery retailing had a huge potential soon. The grocery and food retail offered lower margin, volume and frequency of purchase could add to financial viability.

Online retailers such as Bigbasket, Grofers, Amazon pantry and Flipkart were aggressively expanding their reach. The online grocers were driving sales through variety, convenience delivery and affordable price. Groceries being an essential purchase for every household, were bought frequently, which offered great opportunities for online retailers to retain their customers.

Tesco’s Expansion in India

Tesco’s recent most departure from Thailand and Malaysia raised multiple concerns over its international strategy. Tesco’s US expansion was extremely stressful and unrewarding. Tesco’s retraction from Thailand and Malaysia did not leave any leg space. Tesco already identified risks associated with business growth. Under the emerging circumstances, business expansion in India must be strategized to de-risk failure.

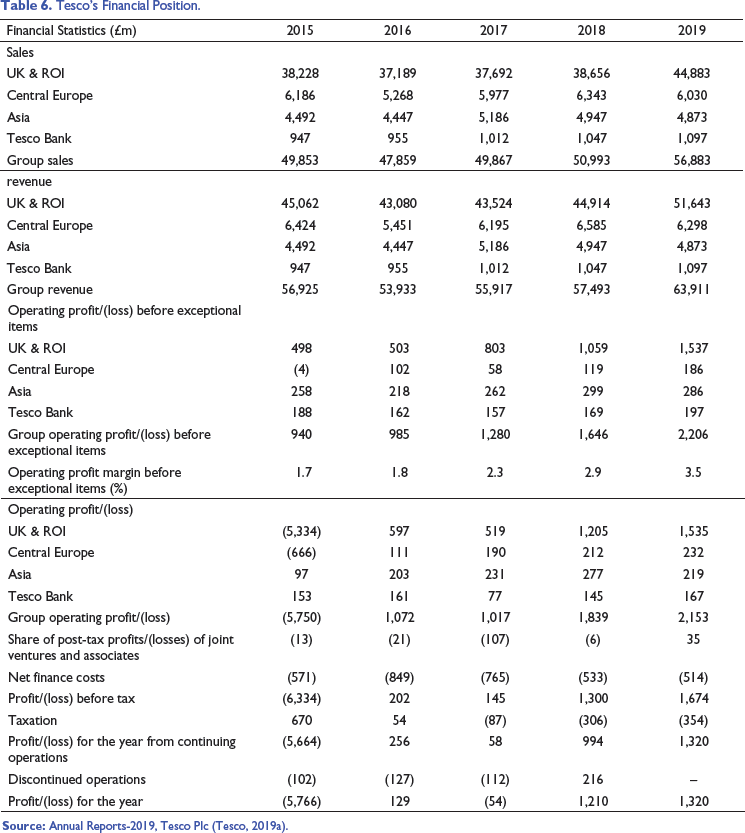

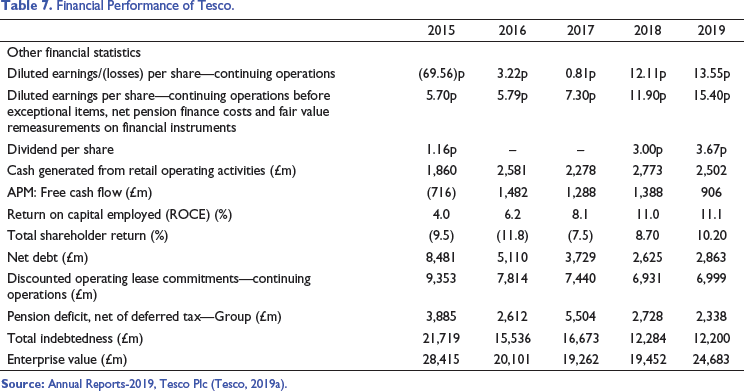

Tesco Group’s Financial Performance

Tesco’s Financial Position.

Financial Performance of Tesco.

Store Strategy

Investment in the retail business was dependent on various components such as location, cost of leasing or renting a shop in a proper location, setup cost of the supermarket, inventory cost, business setup cost and cost of technology. Developing a store strategy was one of the most critical decisions in retail operations. Tesco India’s expansion strategy was primarily dependent on the type of format choice, its location, and geographic spread of the stores in India.

According to Jamshed Daboo, managing director, THPL, opening a ‘Star Market’ store (8,000–10,000 sq ft) needed an investment of £290,783–387,710. A new ‘Star market’ store could generate annual revenue in the range of £67849–96,928 and a gross margin of 10%–14%. A ‘star hyper’ required an investment of £775,421, roughly the cost of opening two ‘Star Market’ stores.

A distribution centre of 70,00 sq ft required investment of £2.42 million (The Economic Times, 2017). The retailer was planning to open more Star Market (Figure 1) than any other store format.

Daniel and Varun offered their insights, but Aniket struggled to figure out the year-wise opening of stores and distribution centres by 2025.

Value Proposition

Star emphasized delivering value to the customer. The key differentiation was offering quality and reasonably priced fresh produce at convenient locations. Over the years, the retailer was able to build a strong reputation of best in class ‘Fresh Food’, which was fastly becoming a destination for consumers. The ‘Fresh Food’ was a strong puller of footfall in the store. In line with Tesco’s strategy in the UK, the retailer directly engaged with 250 farmers for bringing farm fresh to the stores through a robust network of collection and distribution centres.

Location Selection

The selection of appropriate locations was one of the critical factors to be considered for entering into a market and expanding business or opening new stores. This directly affected sales. Tesco had a deeper understanding of the fact that location was held central to success in the UK. In terms of variation and dissimilarity of consumer taste, preferences and disposable income, India offered more challenges than the UK. A slight change in the preferences of consumers could critically impact the top-line and bottom-line of the retailer.

So far, THPL was extremely cautious and careful about store expansion. The core fundamental behind the calibrated expansion was the evolution of a sustainable business model. THPL followed a clustered expansion strategy with stores in the states of Maharashtra, Karnataka, Telangana and Gujarat, intending to create a local scale and be closer to customers.

The clustered approach allowed the retailer to achieve (a) a better understanding of local needs and preferences; (b) cost efficiency due to economies of scale; (c) brand visibility; and (d) better coordination of distribution and logistics.

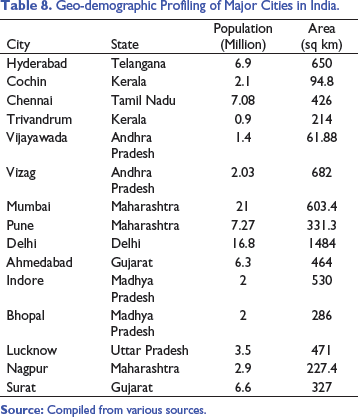

Geo-demographic Profiling of Major Cities in India.

Store Format

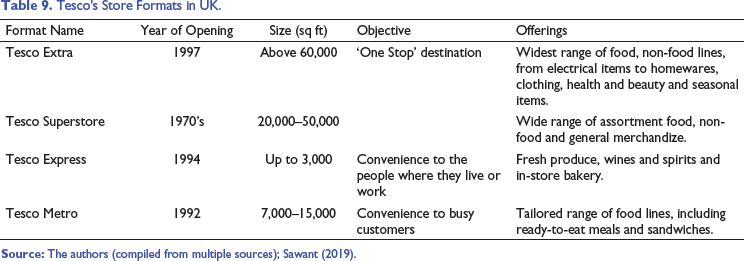

Tesco's Store Formats in UK.

Aniket was not quite sure of which format could help Tesco to succeed in India. Daniel believed that small formats could be the way forward. Laxmi felt online could support physical stores to grow. Aniket had to work out an optimal store mix, delivering profitability and driving a fast-mover advantage.

Own Brand

Tesco’s own brands contributed sales of about £17.7 billion (Tesco, 2019b). Generally, Tesco had three ranges of private labels, namely: basic, standard and finest, to meet customer requirements and compete with Aldi, Asda and other retailers in the UK.

Following the footstep of Tesco Group, THPL was trying to strengthen the offering of its own brands, a viable business model. The retailer continued focusing on the expansion of ‘exclusive range in defined categories at affordable prices and great quality benchmarked with leading brands’ (Trent, 2019). Star’s own brands offered 300 stock keeping units (SKUs), with continued upbeat offtake by consumers. The retailer was selling its own brands under the following banners:

Klia: Launched in 2017 (Cleaning-aids, home care & hygiene products). Fabsta: Launched in 2018 (Packaged food and beverages). Skye: Launched in 2018 (Personal care products).

In terms of revenue, several own brands ranked one or two (in terms of sales) in multiple sub-categories. The own brands were able to effectively compete with the third-party national or international brands.

The Decision

Aniket organized several meetings with key members of his team. The team carried out multiple meetings and deliberations to explore all possibilities of retail augmentation. Based on the background work, market intelligence and strategic vision of the company, the management had to decide upon the expansion plan. Critical decisions were to be taken on expansion front, which included the number of stores to be opened by 2025, the number of new retail destinations to be added, and the year-wise addition of stores across destinations. Despite serious attempts, Aniket was struggling to decide the right kind of store or format mix, which would bring maximum revenue and profitability.