Abstract

The case study on Gujarat NRE Coke Limited is about a company that has been a pioneer in the metcoke industry. The company is the largest manufacturer of metcoke in India. This case study sets out the details of the company providing insight on its journey starting from its humble beginning to its glorious past to its present struggles. The case provides a picture of the economics of a company and how policy decisions of the government, changing global economic conditions and myopic legal and financial system prevailing in a country can change the fortunes of a high-flying viable company.

The views and opinions expressed in this book are the author’s own and the facts are as reported by him which have been verified to the extent possible, and the publishers are not in any way liable for the same.

All rights reserved.

No part of this publication may be reproduced, transmitted, or stored in a retrieval system, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher.

Introduction

It was a Monday Morning that Mr Arun Kumar Jagatramka, Managing Director, and Mr Mohan (name changed), representative of 109 shareholders, of Gujarat NRE Coke limited (GNCL) were brainstorming on how to prevent liquidation and revive the company. Nothing has happened since they last proposed a revival scheme in 2019.

The history of the company goes back to the year 1986 when the company was incorporated and was later listed on the Bombay Stock Exchange and Calcutta Stock Exchange in 1994. During the year 1997, the company was in financial stress and at such a critical period of the company, Mr Arun Kumar Jagatramka was appointed as its Managing Director on 28 March 1997. Overcoming various litigations, he took full control of the company with effect from 4 December 1997. Starting from 1998 onwards, GNCL has made its presence felt in the coal and coke industry and became India’s largest independent manufacture of metcoke and had also acquired coal mines in Australia. The company was the quickest off the block with a pioneering dispatch of coke to Brazil in 2004—the first ever time this was done by any Indian coke producer. The company leveraged its port-based location to report ₹334.7 million of exports to Brazil in 2003–2004, which was followed by dispatches to South Africa. In addition to repeated orders from these countries, the company enjoyed attractive long-term export enquiries for coke from the USA, Japan and Europe.

However, after 2009, the company has suffered on many counts. The global demand for coke reduced after the global financial crises of 2008. Dumping of Coke by China resulted in further dampening of Coke prices. The company faced many tax raids and unresolved tax issues. The operations of the Australian subsidiary had to be financed by the Indian parent company. The company resorted to loans from banks and other creditors to make all statutory payments. However, loans could not be paid in time due to which Corporate Debt Restructuring (CDR) was undertaken. When CDR failed, the company was referred to corporate insolvency resolution process (CIRP) under the new Insolvency and Bankruptcy Code, 2016. GNCL has been operated by Liquidator Mr Binani since January 2018 for liquidation.

It was in this context that top management and shareholders of GNCL were brainstorming on the dilemma of the revival path for the company.

Gujarat NRE Coke Limited

Transition and Growth Phase

GNCL is the major company in the Bhuj district of Gujarat in the metcoke sector which is operational and has the largest industrial set-up both in terms of manpower and scale of operations.

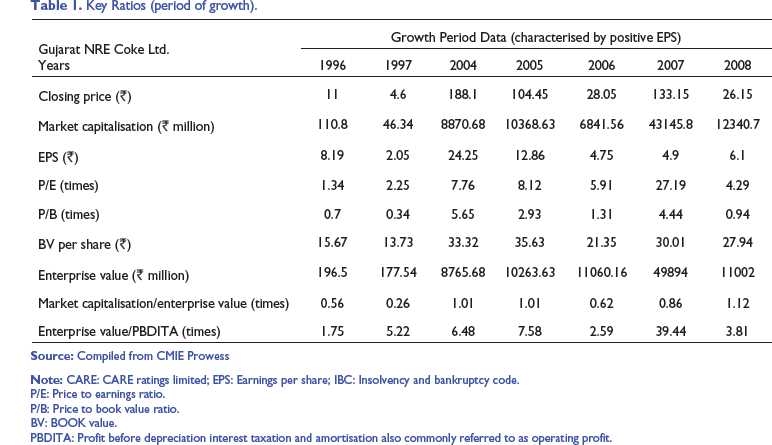

The following are the highlights of the financial and debt profile of the company during transition period of the company, that is, from 1998–1999 to 2003–2004: Improvement in credit rating by CARE from D to AA—for non-convertible debentures signifying a high asset quality by all standards and a high investment grade. The company’s interest liability reduced from ₹16.5 million to ₹15.99 million and the average debt cost declined from 17.10% in 2002–2003 to 5.37% in 2003–2004 and the debt–equity ratio reduced from 1.32 in 1998–1999 to 0.41 in 2003–2004. The company financed its aggressive expansion through a mix of retained profits and low-cost debt. Loans reduced from 131% of the total capital employed in 1998–1999 to only 27% as on 30 September 2004 as a result of many measures such as cutting costs, reducing debt, improving product quality, reduced receivables and improving overall profit. Improved cash flow management, which reduced the utilisation of cash credit facilities from ₹11.2 million in 2002–2003 to ₹4.6 million at the end of 2003–2004.

The company has enjoyed unparalleled interest among its shareholders in the past as the company has shared its wealth with the shareholders of the company by rewarding them with multiple dividends and bonuses. Snapshots of the rewards reaped by the shareholders of the company are as follows:

The company has paid multiple dividends between 2000–2001 and 2010–2011. The company has paid dividend as high as 45% and 50% in a year in the past during 2003–2004 and 2004–2006. The company has rewarded its shareholders with multiple bonuses. Total shareholder return (TSR) increased from ₹150.3 million in the year 2001–2002 to ₹3310.6 million in the year 2003–2004. The year-on-year market capitalisation of the company had increased by 571.16% in the year 2003–2004. An investor who had invested ₹0.1 million in the equity shares of the company as on 3 April 2000 had a value of ₹19.0 million as on 31 March 2010, which is an increase of more than 190 times in the value of his investments.

Key Ratios (period of growth).

P/E: Price to earnings ratio.

P/B: Price to book value ratio.

BV: BOOK value.

PBDITA: Profit before depreciation interest taxation and amortisation also commonly referred to as operating profit.

The Downturn

While the metcoke industry was in boom in the year 2008, the global financial crisis in the very beginning of 2009 caused it to crash down. As a result, even though the company had made huge investments in coking coal mines in Australia through its subsidiaries, the company was unable to raise independent capital for the continuous investments required in coal mines in Australia because of commodity downturn at the end of 2008. As the Australian subsidiaries could not raise capital on their own, the burden of supporting them fell on the parent company, GNCL. The company, being a holding company, had to support its subsidiaries, and while extending required support, the debt of the company became overstretched. The global financial crises of 2008 and the foreign acquisitions proved very costly to the company, and it drove the company to a state of financial distress and liquidation. The volatility in coal prices added to cash flow mismanagement. Apart from this, there were tax raids, unresolved tax issues and discussions for one time settlement (OTS) which derailed the focus of the management from growth to resolving the regulatory compliances. Land prices in India also doubled affecting the financial viability of new projects in India. From 2010, onwards, the financial health of the company detracted. Between 2011 and 2013, while the coal production increased three times from 60,000 tonnes a month in 2011 to more than 0.2 million tonnes per month in 2013, the company cash flows suffered tremendously. Sensing good business acquisition, one of the big Indian steel producers, Jindal Steel and Power Limited (JSPL) undertook large stock acquisition in the open market and this reduced the public holding to mere 4%. Cash position became so bad that it became extremely difficult to pay weekly wages. The steel producer JSPL further invested in acquiring fresh equity at low valuation. Finally, the control of the company was in hands of JSPL. The fall of coal prices, a strong Australian dollar, poor global financial environment, stock market crashes and poor liquidity forced GNCL to accept the open offer from JSPL. Jindal’s group holding increased to 53.62% and Gujrat NRE’s holding reduced to 43.30%. The stock prices reached a rock bottom in June 2013. Inability in meeting daily cash needs and poor equities market forced the management to undertake debt which further added to downward financial spiral. In 2013, the company was in a bad shape and was referred by bankers for CDR.

During this period, an externality of import of Chinese Coke further reduced the cash inflows. Anti-dumping duty was finally imposed by the Government of India in November 2016, but by then, GNCL was already in comma. CDR failed. With CDR failing, the company had submitted a debt realignment scheme to the lenders in February 2016, which was under consideration of the bankers. The bankers had got independent valuation done of all the fixed assets of the company and a Techno Economic Viability (TEV) study was also conducted by independent consultants, namely Mott McDonalds at the insistence of the lenders, and the said TEV report was also accepted by the lenders. However, no conclusion was arrived at by the lenders.

GNCL accounts were classified as non-performing assets (NPAs). Demonetisation of high currency notes took away whatever little cash the company had. A situation of total paralysis arose. It was then in March 2017, Mr Arun Kumar Jagatramka proposed to the board that GNCL should be referred for CIRP under the new Insolvency and Bankruptcy Code. Mr Jagatramka approached the Kolkata Bench of National Company Law Tribunal (NCLT) for getting GNCL admitted to the IB Code under Section 10. On expiry of the 270 days for revival of the company, the company was put under compulsory liquidation. This decision had put in jeopardy the employment of 1,178 employees and 0.2 million public shareholders who had full faith in the revival of the company. The NCLT Kolkata Bench took cognisance of these facts and passed a landmark order of putting GNCL into liquidation as a ‘Going Concern’ on 11 January 2018. The liquidator was asked to try and sell the company as a going concern.

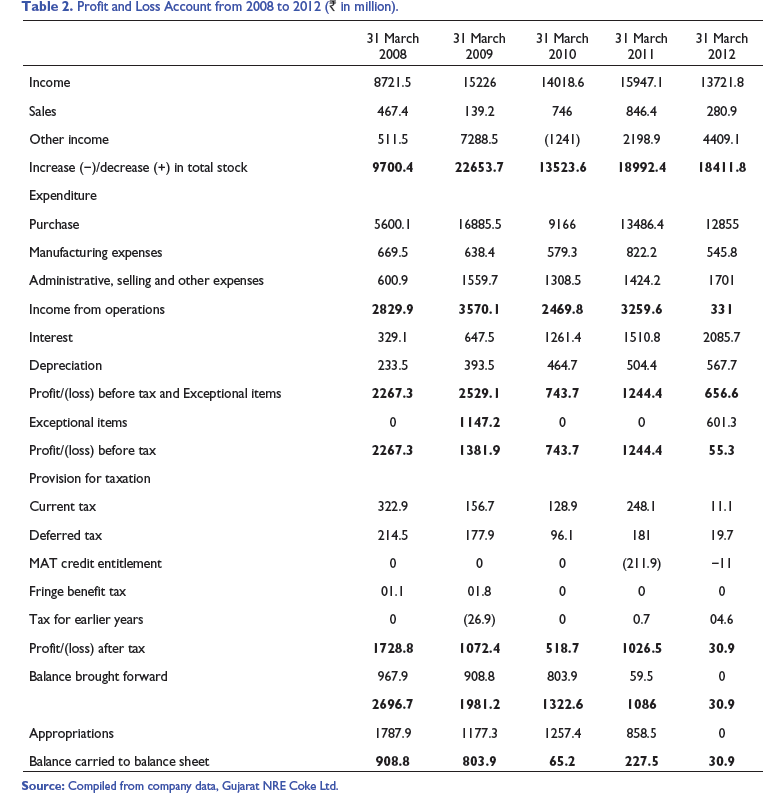

Profit and Loss Account from 2008 to 2012 (₹ in million).

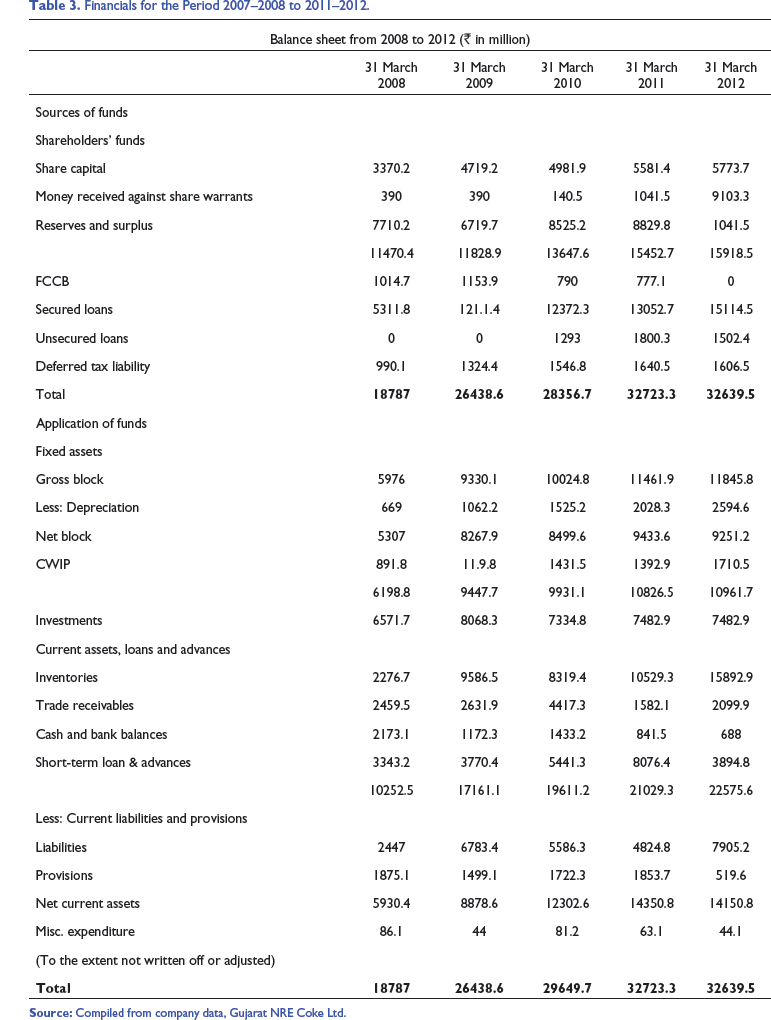

Financials for the Period 2007–2008 to 2011–2012.

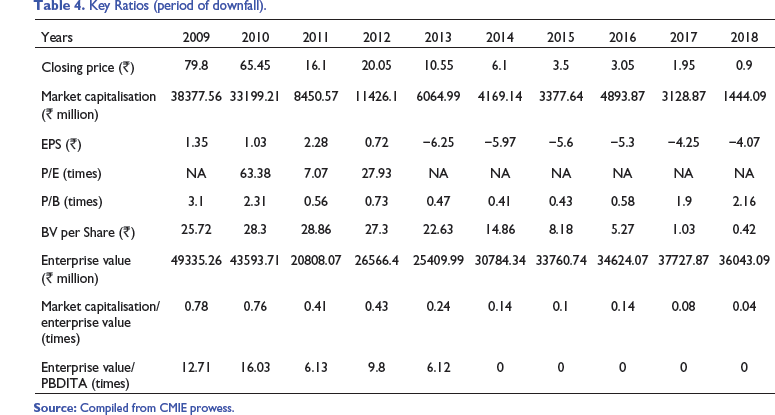

Key Ratios (period of downfall).

Current State of Affairs of the Company

The Sudden Impact of 29A

Gujarat NRE had applied u/s 10 of the IB Code with the management confident of reviving and servicing the sustainable debt besides generating large employment strength of the company.

However, with sudden introduction of Section 29A in the IB Code, the promoters became ineligible to propose a resolution plan and the company was forced into liquidation in January 2018.

Since 11 January 2018, the company has been in liquidation and is run by the liquidator on a going concern basis. Even during the period of liquidation, the company has continued to employ about 900 personnel directly and more than 10,000 families indirectly across the country. The company has posted revenue of around ₹10,000 million during the period of liquidation. On 2 March 2020, the Hon’ble Tribunal had heard the liquidator and the Chairman of the Tribunal convened a meeting of the shareholders and creditors of the company and other stakeholders and extended the period of liquidation by further 6 months.

The liquidator has taken the following steps for revival of the company:

On receiving an order from the Hon’ble National Company Law Appellate Tribunal, New Delhi, the liquidator promptly issued an Expression of Interest (EoI) inviting a scheme of Compromise and an Arrangement under Section 230 of the Companies Act, 2013, from the shareholders and/or creditors of the Company on 31 October 2019. On receiving a scheme of Compromise and an Arrangement from the shareholders of the Company on 30 November 2019, the liquidator moved to the Hon’ble National Company Tribunal, Kolkata bench and presented the scheme before the Tribunal for their direction. The Hon’ble Tribunal directed to hold a meeting of the creditors and shareholders of the company on 21 February 2020. A meeting of the creditors and the shareholders of the company was held on 21 February 2020 to consider the scheme of Compromise and an Arrangement under Section 230 of the Companies Act, 2013, proposed by the shareholders of the company for the revival of the company. The liquidator had independently convened a meeting of the financial creditors of the company to understand the financial matrix and their comments and views on the scheme on 19 February 2020. The liquidator and the Chairman of the meeting of the creditors and shareholders had submitted their respective reports with the Hon’ble NCLT, Kolkata Bench on 2 March 2020, and the Hon’ble NCLT asked the company to initiate a dialogue with the financial creditors to find out their requirements for favouring the scheme.

Metcoke Industry Analysis

The metcoke industry is dependent on steel industry. Hence, the changes in the steel industry directly affect the metcoke industry. Unfortunately, the steel industry has not been doing very well due to intense competition from China. Many companies engaged in steel production have been referred to NCLT due to non-payment of their dues. Other changes in the industry included the following: (a) in 2012, iron ore mining in Karnataka was banned by Supreme Court which led to large-scale inventory pile up with zero sales. (b) Massive dumping of coke from China during 2013–2016 further killed the domestic metcoke industry. Indian metcoke import had increased significantly from 2012 till November 2016 due to major dumping/import of metcoke from China and prices tumbled to new lows. The price of metcoke crashed to such low levels that there was little difference between prices of metcoke and that of coking coal, which is the principal raw material used in production of metcoke. This resulted in lack of demand as well as squeezing of margins on metcoke produced by the company thereby causing huge losses. (c) Domestic metcoke industry employs a large number of unskilled labour from Schedule Caste (SC)/Scheduled Tribe (ST) as well as Other Backward Classes (OBCs). With unskilled labour, the industry was not able to achieve efficiency levels similar to that of China.

Liquidation Under IBC, 2016

GNCL is being operated by a liquidator since January 2018 and has remained operational even 3 years in liquidation. Almost 1,000 employees continue to receive their monthly wages through the operational cash flow of the company. GNCL has one of the lowest attrition rates in the country. Ninety per cent of employees including key managerial persons have been with the company for more than 10 years. Large bank dues of ₹38,000 million and very low liquidation value of around ₹3,500 million is the main hindrance in the liquidation process. However, large potential upside in equity value exists due to inherent volatility in Coke business and changes in share prices which can improve the valuation; for example, share price of GNCL moved up from ₹8 in March 2014 to ₹19 in May 2014 (CDR scheme was approved during that period and all plants were closed then).

The Legal Battle in Courts

The promoters proposed a scheme for revival u/s 230 of the Companies Act, but the same has been stuck in litigation by unsecured creditor thereby preventing timely revival of the company. After almost 2 years of litigation before NCLT and National Company Law Appellate Tribunal (NCLAT), the promoters appeal is now being heard by the Supreme Court. The Insolvency and Bankruptcy proceeding started in 2017.

As a corporate debtor, the company filed an application under Section 10 of the Insolvency and Bankruptcy Code, 2016, for initiating CIRP on 23 March 2017 before the National Company Law Tribunal, Kolkata Bench (hereinafter referred to as ‘the NCLT’) and the same was admitted on 7 April 2017. Mr Sumit Binani was appointed as the Interim Resolution Professional (‘IRP’) and he was later confirmed and appointed as Resolution Professional (‘RP’) by the Committee of Creditors (COC).

COC had also confirmed the appointment of PricewaterhouseCoopers (PWC) to assist in preparation of the resolution plan. On 23 June 2017, in terms of Section 25(2)(h) of IBC, a notice was published in the leading national daily inviting EoI from third parties for submission of the resolution plan for the corporate debtor with a cut-of date of 10 July 2017 for obtaining necessary details and Information Memorandum from the Resolution Professional. However, Mr Binani, the Resolution Professional, did not receive any bid or enquiry from anyone.

Meanwhile, RP convened several meetings of COC and viable options for revival of the company were discussed among the COC members. Based on such discussions and confirmation of COC, a resolution plan was submitted by the promoter, that is, Mr Arun Kumar Jagatramka, in August 2017 on behalf of the company and the same was under consideration and final stage of approval.

While various revival options were being discussed, being a time-bound process, CoC thought it prudent to extend the period of CIRP by 90 days as permitted under the Code. The said application was finally approved by CoC and granted by NCLT vide its order dated 19 September 2017. As such, the CIRP period was extended till 1 January 2018.

However, on 23 November 2017, the President of India promulgated the Insolvency and Bankruptcy Code (Amendment) ordinance 2017 which debarred the promoters of the company from submitting a resolution plan. Hence, the plan submitted by Mr Arun Kumar Jagatramka, promoter of the company became void and infructuous.

Unfortunately, since more than 8 months had already elapsed with no final resolution owing to the ordinance, being confident on the future viability of the company and its performance the COC members invited EoI from third parties to arrive at a viable resolution. However, owing to paucity of time with less than a month left for the expiry of the CIRP process, no resolution could be arrived at.

However, a resolution plan was submitted by Rare Asset Reconstruction Private Limited on 25 December 2017 which was deliberated upon by COC on 26 December 2017 and 28 December 2017 but finally was not accepted.

Subsequently, the employees and workmen of the company submitted a comprehensive resolution plan to the Resolution Professional on 30 December 2017 which again could not be deliberated upon and considered due to paucity of time under CIRP which ultimately expired on 1 January 2018.

It is pertinent to mention that during the CIRP process, the company has been operating as a going concern and has also made operational profits in the month of October and November 2017.

However, since no resolution plan could be approved by COC within the permitted CIRP timeline, the Hon’ble NCLT ordered for liquidation of the otherwise profitable and operational company with effect from 11 January 2018 vide its order dated 11 January 2018. In the present case, liquidation order was an outcome of legal compulsion under IBC being a time bound process and a result of the ordinance leading to no resolution for the revival of the company.

Ordinance Affecting Survival of Companies

The promoter of the company became ineligible to revive a viable company after the ordinance issued in 2017. Mr Arun Kumar Jagatramka feels that the turnaround of GNCL from 1997 to 2004 could have been repeated in 2021 had he been in-charge of the company. The resolution plan for revival of the company which was under consideration of COC could not be approved. The valuable work and the time invested by the COC members for 8 months in a restrictive period of 9 months to draw a viable and acceptable resolution plan for revival of the company vis-à-vis recovery of their debts became futile and invalid. CoC was left with no alternate option for revival of the company, since no EoI was received from third parties during CIRP period prior to implementation of the ordinance. Hence, the company was compulsorily put to liquidation under the process of law. Mr Mohan expresses his feeling to Mr Arun Kumar Jagatramka that IBC in an attempt to protect the interest of creditors and lenders is putting the survival of companies at risk. The survival of companies is very important for employment generation and growth in gross domestic product (GDP) for any nation.

It is also pertinent to note that during the CIRP stage, a transaction audit was conducted by an independent auditor in terms of Section 43, 45, 50 and 66 of IBC with respect to preferential, undervalued, extortionate credit and fraudulent transactions, respectively, and no adverse observations were reported by the auditor. Subsequently, during the liquidation stage, a forensic audit was also conducted by an independent audit firm duly appointed by the liquidator, the report of which also did not contain any adverse observations.

It is noteworthy that almost 2 years have elapsed since the commencement of liquidation and the company still continues to run its operations without disturbing the employment of any of its personnel. However, the cloud of uncertainties continues to hover around the company which has a direct, adverse impact on its performance.

Liquidation Process

Regulation 2B of the Insolvency and Bankruptcy Board of India (Liquidation Process) Regulations, 2016, provides for proposing a Compromise and an Arrangement under Section 230 of the Companies Act, 2013, for restructuring of the corporate debtor and also provides that such a process shall be completed within a period of 90 days of the order of liquidation under Subsection (1) and (4) of Section 33 of Insolvency and Bankruptcy Code, 2016. In its judgment dated 24 October 2019, NCLAT has allowed a Compromise and an Arrangement to be proposed by the members of the corporate debtor through the liquidator.

Furthermore, the Hon’ble NCLAT and Hon’ble Supreme Court of India have clarified through their judgments that the primary focus of the legislation is to ensure revival and continuation of the debtors. The Hon’ble NCLAT has clearly directed that the last stage for a corporate resolution process shall be death by liquidation, which should be avoided, and went on to provide steps for revival of the corporate debtor as follows:

By Compromise and an Arrangement with the creditors, class of creditors or members or class of members in terms of Section 230 of the Companies Act, 2013. On failure, the liquidator is required to take steps to sell the business of the ‘Corporate Debtor’ as going concern in its totality along with the employees.

The Hon’ble NCALT have further highlighted that the liquidator is required to act and take steps under Section 230 of the Companies Act. If the members or the ‘corporate debtor’ or the ‘creditors’ or a class of creditors like ‘financial creditor’ or ‘operational creditor’ approach the company through the liquidator for Compromise and an Arrangement by making proposal of payment to all the creditor(s), the liquidator on behalf of the company will move an application under Section 230 of the Companies Act, 2013, before the Adjudicating Authority.

Subsequently, the liquidator has invited a scheme of Compromise or Arrangement under Section 230 of the Companies Act, 2013, from interested members/creditors of the corporate debtor, who are eligible under the applicable provisions of the Companies Act, 2013, and the Insolvency and Bankruptcy Code, 2016, vide a notice circulated in leading newspapers having nationwide circulation dated 30 October 2019.

Hence, to save a viable company which has been a pioneer in the Coke Industry, from being liquidated and to bring forth the benefits which may arise out of the revival of the corporate debtor, the shareholders of the company, proposed a Compromise and an Arrangement Scheme under Section 230 of the Companies Act, 2013, though the liquidator of the company.

Promoter Scheme Rejected

After the liquidation order for the company as a going concern was passed on 11 January 2018, which was a first in the country, Mr Arun Kumar Jagatramka, promoter and shareholder of GNCL (hereinafter referred to as “

However, Jindal Steel and Power Limited, an operational creditor of the company obtained a stay on the said meetings of the stakeholders of the company from Hon’ble National Company Law Appellate Tribunal, New Delhi and reserved their order on following question of law:

In a liquidation proceeding under Insolvency and Bankruptcy Code, 2016, (hereinafter referred to as the ‘I&B Code’) can the scheme for Compromise and an Arrangement can be made in terms of Sections 230–232 of the Companies Act?

If so, is the promoter eligible to file application for Compromise and an Arrangement, while he is ineligible under Section 29A of the I&B Code to submit a ‘resolution plan’?

The Hon’ble Appellate Tribunal thereon passed an order on 24 October 2019 which upholded the first question by saying

11. During the liquidation stage, ‘Liquidator’ required to take steps to ensure that the company remains a going concern and instead of liquidation and for revival of the ‘Corporate Debtor’ by taking certain measures. They also quoted …In view of the provision of Section 230 and the decision of the Hon’ble Supreme Court in ‘Meghal Homes Pvt. Ltd.’ and ‘Swiss Ribbons Pvt. Ltd.’, we direct the ‘Liquidator’ to proceed in accordance with law. He will verify claims of all the creditors; take into custody and control all the assets, property, effects and actionable claims of the ‘corporate debtor’,

However, the Hon’ble NCLT barred any such scheme of Compromise and Arrangement to be proposed by any promoter who is ineligible under Section 29A of the Insolvency and Bankruptcy Code.

Complying with the order of the Hon’ble NCLAT, the liquidator floated an EoI inviting a scheme from shareholders and/or creditors of the Company. Responding to this, 109 shareholders of the company proposed a scheme of Compromise and Arrangement between the company and its creditors and shareholders through the liquidator which was placed before the Hon’ble NCLT, Kolkata Bench for passing necessary orders. The Hon’ble NCLT, Kolkata Bench passed directions to hold meeting of the creditors and shareholders of the company and appointed a Chairman for the said meeting on 6 January 2020. The meeting of the creditors and shareholders was convened and held on 21 February 2020.

New Proposed Scheme for Revival u/s 230 of the Companies Act

In the meantime, after surviving in liquidation for over 2 years, 109 shareholders (including a large no. of employees) proposed a scheme for revival u/s 230 of the Companies Act in November 2019. The highlights of the scheme as far as it concerns the secured lenders are as follows:

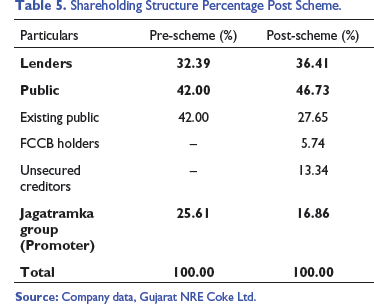

No haircut, that is, they will receive all their payments. No moratorium, that is, payments will start immediately. No additional funding, that is, no more loans will be undertaken to pay existing loans. Gross debt repayment in three parts Sustainable debt of ₹4000 million repayable in 10 years on quarterly basis with 8.1% interest. Issuance of ₹380 million equity shares aggregating to ₹3,800 million (Table 5). 0.01% cumulative redeemable preference shares (CRPS) of ₹30,210 million (up to 20 years). All existing securities and guarantees to continue.

Shareholding Structure Percentage Post Scheme.

Twenty-five per cent conversion to equity shares.

Seventy-five per cent haircut.

More than 0.2 million shareholders to benefit from revival of business and appreciation of company valuation.

Resumption of trading on the stock exchanges.

Both equity and ‘B’ equity shares of ₹10 each to be consolidated as new equity shares of ₹10 each.

Salary and wages—₹5,000 million;

custom duty (at current rate)—₹7,500 million; and

Goods and Services Tax (GST)—₹7,000 million.

Continued employment to around 1,000 employees and workmen plus future employment to 1,500 employees/workmen; indirect employment to 10,000 families currently going up to 25,000 families in future.

Protection of investor’s wealth of more than 0.2 million shareholders.

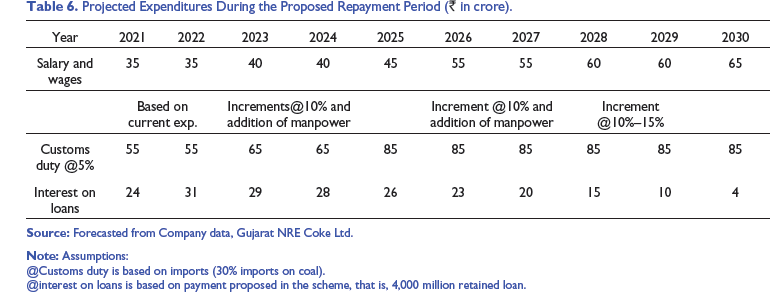

Projected Expenditures During the Proposed Repayment Period (₹ in crore).

Assumptions:

@Customs duty is based on imports (30% imports on coal).

@interest on loans is based on payment proposed in the scheme, that is, 4,000 million retained loan.

As such, banks need to focus on getting maximum value for their exposure and also work towards maximisation of benefits which may accrue to all the stakeholders from the scheme by playing a proactive role in the passage of the scheme with or without reasonable minor amendments, if any required.

It is noteworthy that the new scheme is proposed to repay the entire outstanding debts to the banks without any haircut or moratorium. The revival of the company will not only benefit them in terms of realisation of their outstanding debts but also enhance the value of their equity investments in the company of about 33% which is substantial. As such, prospects of benefits accruing to the banks are extremely lucrative, and there is no reason for them to ignore the same and push the company to liquidation. Mr Mohan fully agrees with Mr Arun Kumar Jagatramka that it is important to revive the companies rather than close and liquidate the same. This will bring maximum benefit to the lenders, the employees and the public shareholders.

Impact of the Liquidation on the Company

Currently, the company is being operated as a ‘Going Concern’ under liquidation, due to which there is shortage of working capital. The company is unable to operate any of its coke plants. Also, its steel plant is running at partial capacity. Furthermore, only 45 out of its 62 windmills are operational. As of November 2019, there were about 640 workmen and employees on the rolls of the company. Additionally, about 300 security personnel/contractual manpower was employed by the company. There has been no default in payment of their wages and salary but there have been delays. There are no instances of any retrenchment of workers or employees. Only a handful of its suppliers and customers have dealt with the company during liquidation period owing to uncertainty prevailing on the survival of the company. Taxes and duties to the government exchequers have been duly submitted within the stipulated period. During the overall liquidation period, there have been operating profits in the steel unit. However, due to lean wind season, in the past few months, there have been losses in the steel unit. The company has been able to generate total revenue of around ₹9000 million since liquidation commencement date.

Impact of Liquidation on Uncertainty in Running Business as a ‘Going Concern’

Uncertainties of employment of about 1,000 people employed by the company.

Uncertainties of livelihood of around 10,000 families indirectly associated with the company through its transporters, security agencies, dealers, vendors, etc.;

Subversion of the eco system around an operational company—uncertainties of livelihood that has developed around the plants through various shops, job works etc., providing a deadly blow to the rural populace of the villages in which the plants operate.

Uncertainties of future employment options.

Loss of value of around 0.2 million public shareholders including the applicants.

Secured lenders hold 33% take in the company. Liquidation will lead to loss of value of the shares held by the secured lenders.

Loss of creative value potential of the assets.

Loss of economic value of productive plant and machinery.

Due to the uncertainties attached to liquidation, the value of the plants is diminishing significantly.

Negligible value to be received when plants get sold as scrap brick by brick—financial loss to lenders and investors.

India would lose self-reliance on a critical raw material and would depend on countries like China to dictate supply and price. GNCL is one of the largest manufacturers of metcoke in India. Liquidation of the company would mean that India’s metcoke production would suffer a hit and the secondary steel plants, chemicals and zinc plants which do not have their own coke unit but buy from open market would now be dependent primarily on imports for the critical raw material requirement. This would also result in loss of foreign exchange.

Loss to exchequer in terms of GST, Customs Duty, income tax, etc.

Liquidation of the company will be against the spirit of ‘Make in India’.

Conclusion

This is a case of a company named GNCL which had huge NPA in 1997. With change of leadership, a turnaround occurred during the period of 1997–2003. The company was able to pay most of its debt, improve its credit worthiness and improve its profitability. The directors of the company became over ambitious and undertook international acquisitions in Australia. The international acquisition heavily affected the cash flows of the parent company in India. The global financial crises of 2008–2009 and henceforth the external conditions of massive dumping by China and poor demand of domestic Coke in India lead to total cash flow mismanagement. The management also faulted by giving a high dividend pay-out in place of conserving cash for growth. This led to build up of massive corporate debt and later losing the control to another company. The CDR scheme also failed, and hence, GNCL was referred for revival under IBC, 2016. As the process of revival was time barred under IBC, the company was forced to undergo liquidation as a “Going Concern”. The promoter Jagatramka Group proposed a scheme of revival; however, the same could not be approved due to a new ordinance which barred promoters from buying back their companies at discount. Hence, the shareholders have proposed a new scheme which has also been reproduced above. The main idea of this case is to promote a philosophy of limiting liquidation and promoting revival of companies which have been built on strong fundamentals. GNCL has suffered primarily due adverse business environment and legal conditions. With the improvement in the ease of doing business, the shareholders and the employees are extremely hopeful that the company will regain its past glory and emerge to a global leader provided the proposed scheme is accepted by the banks and other lenders. The dilemma that still clouds the minds of shareholders, bankers, other creditors, the promoter and the liquidator is that how to move this company out of liquidation as a “Going Concern” and revive the company.