Abstract

This article investigates the link between board members’ past professional experiences and the terms and conditions of the debt contracts of their current firms. In particular, we examine whether directors’ past bankruptcy experience affects the pricing and nonpricing terms of public debt contracts. Using a sample of 8,142 bond issues in the United States in the period 1995 to 2015, we document higher credit spreads and smaller bond sizes for firms with such directors, suggesting that bondholders are concerned about past bankruptcy experience. Our results remain robust to different model specifications. This effect is moderated for bankruptcies that are likely driven by macroeconomic shocks such as the dotcom bubble and the global financial crisis. We also show that our findings are not explained by bond issuers with an elevated risk of default and seem instead to be driven by directors serving on key monitoring committees, indicating that prior bankruptcy experience raises concerns about the company’s corporate governance. Finally, mediation analysis offers some evidence of a limited negative indirect effect of prior bankruptcy experience on the terms of debt contracts through the firm’s financial and investment policies. Overall, our findings suggest that lenders incorporate information about past professional experiences of directors into public debt contracting.

Keywords

Introduction

The consequences of corporate bankruptcy have received considerable scholarly attention. Filing for bankruptcy results in significant negative abnormal returns (e.g., Beneish & Press, 1995; Rose-Green & Dawkins, 2000) and reputation loss (Devers et al., 2009). Firms that do so are stereotyped as low-quality and low-reliability (Xia et al., 2016). Bankruptcy proceedings are also costly for the board members of bankrupt firms. For example, Gilson (1990) reports that such individuals experience reputation penalties in the form of reduced career opportunities.

Although bankruptcies are high-impact events for both the firms and the individuals involved, we know relatively little about how directors’ prior bankruptcy experience affects their firms’ decision-making and outcomes. Our study seeks to cast light on this issue by investigating the effects of directors’ prior bankruptcy experience on the terms of bond contracts of firms they join subsequently. 1 We specifically focus on corporate bond issues for two main reasons. First, corporate bonds are the main source of external financing for U.S. firms. According to the Securities Industry and Financial Markets Association, outstanding U.S. corporate bonds amounted to more than US$9,598 billion in the last quarter of 2019. 2 Second, bond contracts might give rise to severe agency problems between managers and bondholders. Unlike private debt lenders, bondholders do not have access to private borrower information and cannot directly monitor managerial decision-making (e.g., Bharath et al., 2008). Bond contracts also include fewer covenants relative to private loans (e.g., Ball et al., 2015). Hence, bondholders need to rely on additional screening mechanisms to mitigate information asymmetry and effectively control their risk exposure. We argue that obtaining information about corporate directors’ prior experience and incorporating it within the bond contracts is one such mechanism.3,4

To assess whether prior bankruptcy experience matters for bondholders, we examine the effect of such experience on key pricing (credit spread) and nonpricing (maturity and bond size) terms. We define prior bankruptcy experience (hereafter, BE) as serving on the board of a bankrupt firm within the period of financial distress, which is on average within 5 years of the bankruptcy filing. We refer to directors with such experience as BE directors and firms that subsequently appoint them as BE firms. 5 Our main prediction is that the presence of a BE director is associated with higher credit spread and lower maturity and bond size.

Ex ante, there are several reasons why a director’s prior experience at a financially troubled firm may negatively affect their current firm’s debt contract terms. First, Fama and Jensen (1983, p. 315) posit that individuals experience “devaluation of human capital” in cases of material adverse events, which negatively affects their future career prospects and reputation. Indeed, empirical evidence indicates that directors experience significant reputation penalties measured by a loss in board appointments following adverse events such as bankruptcies (e.g., Gilson, 1990) and financial fraud (e.g., Fich & Shivdasani, 2007). Drawing on signaling theory, we posit that appointing directors with a tarnished reputation to corporate boards may signal poor corporate governance quality and raise concerns regarding the abilities of board members to monitor and advise management effectively and maintain financial soundness, thus increasing corporate governance risk.

Moreover, firms currently experiencing or expecting financial difficulties in the near future may be more likely to appoint a BE director to help cope with financial distress. That is, appointing BE directors may signal imminent financial problems and increased default risk.

Finally, past professional experiences may affect a firm’s financial and investment risk tolerance. For example, in a recent paper, Gopalan et al. (in press) document increased financial and investment risk for firms interlocked with a bankrupt firm. Their findings suggest that directors exposed to less-costly bankruptcies lower their assessments of distress costs and engage in more risky behavior. Hence, past bankruptcy experience could also signal a shift in the firm’s risk tolerance. To the extent that the appointment of a BE director raises concerns about corporate governance risk, the future financial health of the company, or financial and investment risk tolerance, we expect that prior bankruptcy experience is reflected in less advantageous debt terms for the borrower.

To test whether director bankruptcy experience gives rise to negative externalities, we identify a sample of 489 firms that filed for bankruptcy between 2000 and 2014 with available financial data on Compustat and board network data on BoardEx. We then trace BE directors’ subsequent career choices and explore whether appointing them influences key pricing (credit spread) and nonpricing (maturity and bond size) bond contract terms of the BE firms. Our results provide evidence that director bankruptcy experience is associated with the firm’s bond contract terms. Specifically, we document that the presence of a BE director is associated with an increase in credit spread of 20.4 basis points (bps) and a decrease in bond size of 22.6% on average, which is both statistically and economically significant. However, contrary to our expectations, our main results indicate a positive effect of prior bankruptcy experience on bond maturity. Additional analysis shows that this positive effect is driven by speculative-grade issues, while for investment-grade bond issues, the association is negative, albeit insignificant.

Our findings support the notion that the appointment of a BE director raises concerns about the corporate governance, risk tolerance, or the future financial health of a firm. While empirically disentangling these potential explanations is challenging in our setting, we conduct several additional tests to cast some light on the channel through which past bankruptcy experience affects the terms of bond contracts. First, we examine the corporate governance channel by investigating whether the BE director’s role on the boards of the bankrupt and the BE firms moderates the effect of past bankruptcy experience on the terms of bond contracts. To the extent that a BE director’s appointment raises concerns about the quality of the BE firm’s corporate governance and increases corporate governance risk, we expect to see more pronounced effects for firms with BE directors in key monitoring positions. Indeed, we find that the role of the BE director in a key monitoring committee explains the effect of past bankruptcy experience on debt contract terms that we observe. This provides support for the corporate governance explanation.

Next, we test the impending financial difficulties channel by examining whether our results are explained by firms whose performance is expected to deteriorate in the future. To this end, we partition our sample based on the credit ratings of the issues, because credit ratings reflect the likelihood of default, and repeat our main analysis separately for the subsamples of investment-grade and speculative-grade bond issues. If the impending financial difficulties channel is supported, we expect to find statistical significance for the speculative-grade issues but none for the investment-grade bond issues. Nonetheless, these analyses show that our results remain qualitatively similar for the subsample of investment-grade bonds but less so for the speculative-grade bonds. This indicates that the observed relationship is not driven by firms with a high probability of default, failing to provide support for the impending financial difficulties channel.

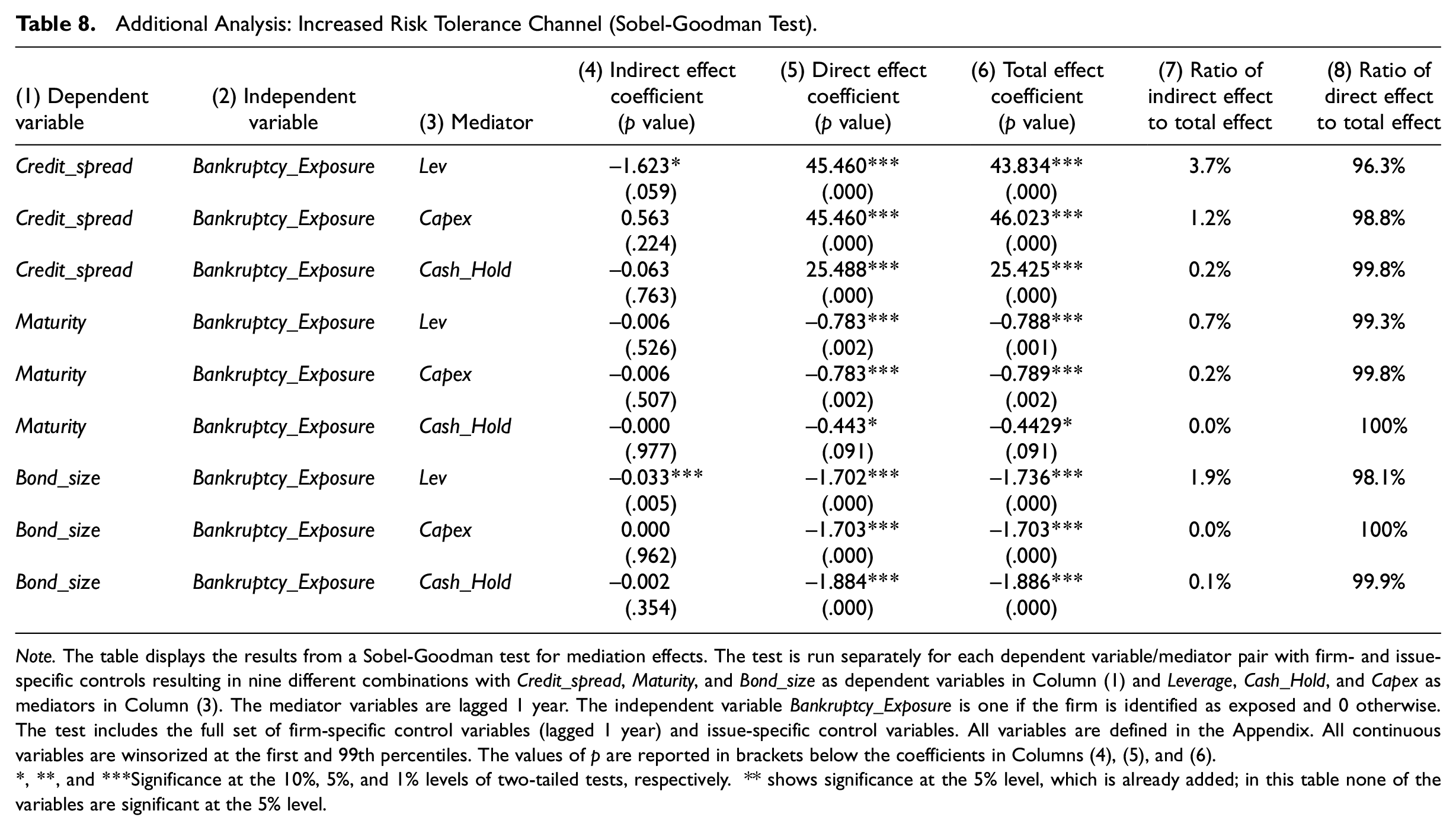

Third, it is plausible that a BE director’s appointment signals a shift in the firm’s financial and investment risk tolerance. To assess whether prior bankruptcy experience has an indirect effect on the design of bond contracts through the financial and investment policies of the firms, we apply a Sobel-Goodman test (MacKinnon et al., 1995; Sobel, 1982). The results provide limited support for the prediction that a firm’s financial and investment policies mediate the relationship between bankruptcy experience and bond contract terms. Hence, we find only limited evidence that the risk tolerance channel explains our main results. Thus, our additional analysis supports the corporate governance channel, although we cannot completely rule out alternative explanations.

Finally, as an additional analysis, we show that the effect of past bankruptcy experience on the terms of bond contracts is not homogeneous. Specifically, we do not observe any significant change in bond contract terms if the bankruptcy was filed during the dotcom bubble burst of the early 2000s and the global financial crisis (GFC) of 2007 to 2009. This suggests that bankruptcies likely driven by macroeconomic shocks do not damage BE directors’ reputation significantly and do not impose negative externalities on the BE firms.

Our article contributes to the existing literature from two perspectives. First, it expands the still-nascent literature on the effects of prior experiences with distress on corporate behavior and outcomes. Existing studies focus mostly on how prior personal or professional experiences shape corporate financial and investment policies. For example, Bernile et al. (2017) find that CEOs exposed to natural disasters without extreme consequences behave more aggressively. Dittmar and Duchin (2016) document that firms led by CEOs with prior distress experience tend to take fewer risks, and Gopalan et al. (in press) show that board interlocks with a bankrupt firm are associated with subsequent higher risk taking at the focal firms. 6 To our knowledge, ours is the first study that examines the effect of director bankruptcy experience on bondholders. In particular, we show that appointing a director with prior bankruptcy experience is likely viewed as a negative signal by bondholders and results in less advantageous borrowing terms. Our findings also complement the evidence presented in Gow et al. (2018), who document negative stock market reactions to the appointment of directors with disclosed experience in adverse-event firms. 7

Second, we add to the literature on the role of corporate governance in debt contracting. Several empirical studies suggest that both external (Bhojraj & Sengupta, 2003; Chava et al., 2009; Cremers et al., 2007) and internal (Anderson et al., 2004; Fields et al., 2012; Klock et al., 2005) corporate governance mechanisms are priced in debt contracts. While these studies predominantly focus on the structural characteristics of corporate governance, we investigate the effect of an additional aspect—a director’s prior experience at a distressed firm—an observable characteristic, which has not been previously studied in this context. Our analysis suggests that appointing a director with such experience increases corporate governance risk and is reflected in more costly debt.

This article proceeds as follows. In the next section, we develop our hypotheses. Section “Research Design and Sample Selection” outlines the sample selection and the methodology employed to test the effects of BE directors on firms’ bond contracts. Section “Empirical Results” presents our main findings and robustness checks. The following section describes our additional analyses, and the final section concludes.

Hypothesis Development

Corporate boards allocate their time between monitoring and advising (Adams & Ferreira, 2007). In times of distress, board members may affect the probability of bankruptcy in at least two important ways. First, high-quality monitoring should support an effective response to financial distress and restrict the opportunities for insiders to mask poor financial performance by misrepresenting accounting data (Fich & Slezak, 2008). Second, board members may reduce bankruptcy risk by providing guidance and assistance in negotiating the restructuring of liabilities and outstanding loans with the firm’s creditors. The advisory function of the board is especially relevant for firms with a high level of complexity (Darrat et al., 2016). The ability of directors to manage the situation thus has an important effect on the outcome, that is, whether the company will recover from financial distress or file for bankruptcy.

In the case of a negative outcome, directors’ actions are closely scrutinized (Gilson, 1990). Indeed, they might be held personally liable if the courts determine that they were not acting in the company’s best interests. Moreover, following a bankruptcy filing, directors experience reputation loss and substantial labor market penalties (Gilson, 1990; Gopalan et al., in press), consistent with the view that they might be held responsible for failing to prevent financial distress. While the findings of extant research suggest that firms are less likely to appoint directors who have been previously involved with bankruptcy, little is known about whether appointing such a director could have any real consequences. This is the gap that our study aims to address. In particular, we investigate whether appointing a BE director has unintended consequences on the terms of issued bonds.

Drawing on prior literature (e.g., Certo, 2003; Certo et al., 2001), we argue that the appointment of a BE director serves as a credible signal for the appointing firm. Specifically, prior involvement with a bankrupt firm may serve as a negative signal about the director’s quality and raise concerns about the firm’s corporate oversight, thus increasing corporate governance risk. In addition, it might be perceived as an increase in the appointing firm’s default risk because director bankruptcy experience may cast doubt on this person’s ability to adequately address similar adverse events in the future. Finally, it is possible that the appointment of a BE director indicates a shift in a firm’s risk tolerance (Gopalan et al., in press).

All else being equal, more information about the borrower’s corporate governance should allow creditors to make better investment decisions and reduce investment risk by acquiring additional information or demanding more stringent contract terms and compensation for the additional risk. While private lenders like banks can demand private information to reduce information asymmetry and monitor firm performance to reduce risk exposure (Bharath et al., 2008), bondholders have access only to publicly available information. To the extent that firm riskiness increases due to the appointment of a BE director, bondholders would require higher returns as compensation for the additional risk. Hence, we hypothesize that the risk premium demanded by the bondholders is greater for firms with BE directors. This prediction is formally stated as follows:

Among the terms of debt contracts, maturity is of primary importance because it alleviates agency costs such as asset substitution problems and improves the monitoring of managerial behavior through more frequent controls (Barclay & Smith, 1995; Lou & Vasvari, 2013). Thus, we expect that riskier firms tend to issue bonds with shorter maturities compared with less risky issuers. Given that we expect firm riskiness to increase due to the appointment of a BE director on the board, we posit the following:

Finally, bond size is an indicator of the perceived ability of the issuer to repay its debt. Firms with low default risk and high ability to generate future cash flows can borrow more (Lou & Vasvari, 2013). In our setting, we argue that a BE director’s appointment casts doubt on the firm’s ability to overcome potential financial difficulties and the effectiveness of the corporate governance mechanisms. If this is the case, we expect that all else being equal, BE firms will issue bonds of smaller size. Hence, we expect the following:

Research Design and Sample Selection

Bankruptcy Experience Measure

Our independent variable, Bankruptcy_Exposure, is an indicator variable equal to one if the bond issuer appoints a director who has been involved with a bankrupt firm within a 5-year period before the bankruptcy event (i.e., the “exposure” period) and the bonds are issued within a 5-year period after the bankruptcy event (i.e., the “contamination” period) and after the appointment of the director, and zero otherwise. To define the “exposure” period, we check for signs of financial distress using the Altman z score (Altman, 1968) to ascertain that the firm was already in distress when the director left it, if the end date of the appointment is before the bankruptcy date. 8 On average, the bankrupt firms in our sample show signs of distress (Altman z < 1.81) about 5 years before the bankruptcy. 9 Therefore, we assume that the “exposure” period spans between Year t− 5 and Year t, where Year t is the year in which the firm declares bankruptcy. 10

Furthermore, we define a “contamination” period, that is, the period after the bankruptcy, during which we expect the negative reputation effect from the involvement with a bankrupt firm to be manifested. In our main analysis, we define the “contamination” period to be the 5-year period after the bankruptcy date. We choose to limit the “contamination” period because we expect that recent events are more salient to decision-makers and more likely to influence their perceptions and behavior (Hogarth & Einhorn, 1992). The BE director must have been appointed after that person’s reputation had been “contaminated,” that is, after the bankruptcy event, for a firm to be considered BE. 11 We also require that the bonds be issued after the bankruptcy event and after the BE director is appointed for Bankruptcy_Exposure to equal one. Figure A2 in the Online Appendix provides a graphical representation of the bankruptcy exposure identification strategy.

Model Specification and Variables

To test our predictions that the appointment of a director with bankruptcy experience is associated with less advantageous bond contract terms, we estimate the following regression models:

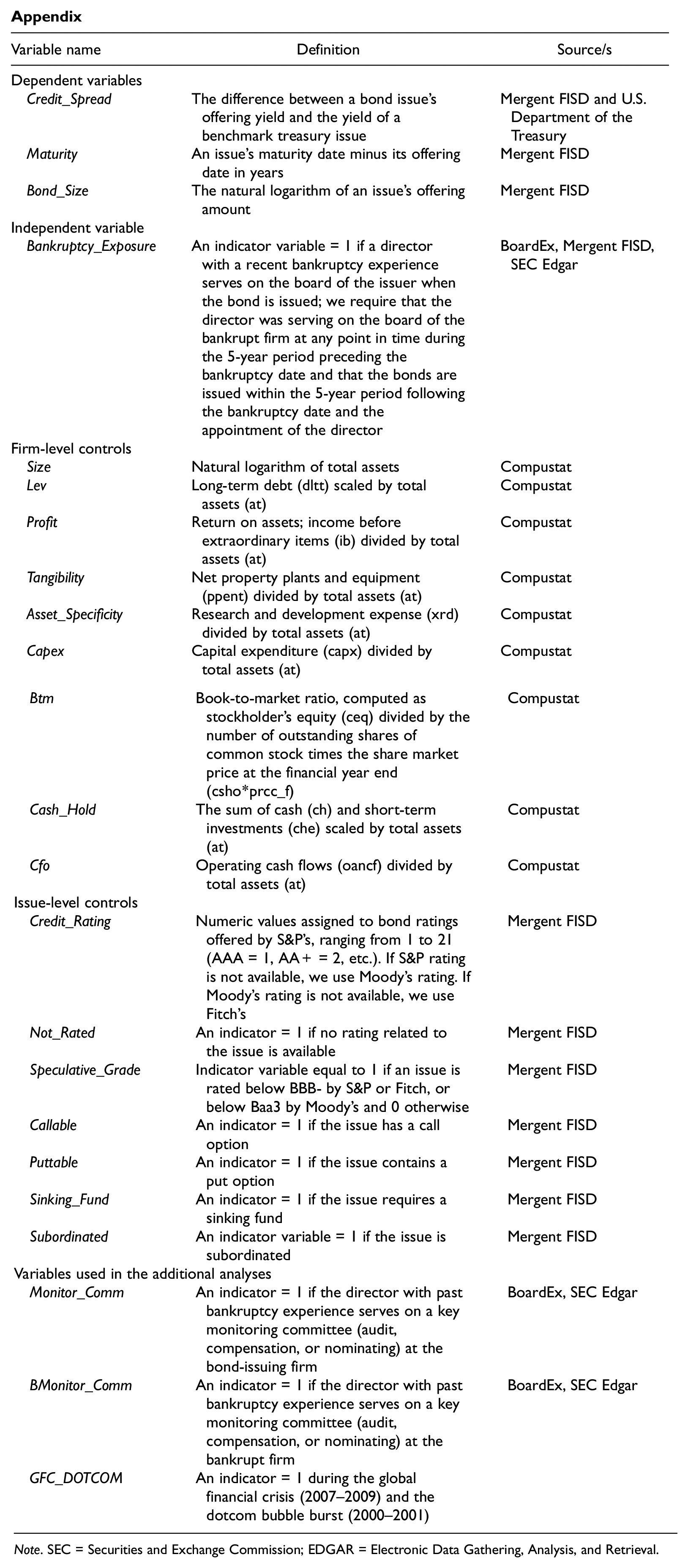

where Bankruptcy_Exposure is the main variable of interest. It represents a dichotomous variable equal to 1 if a BE director serves on the board of firm i when bond j is issued, and 0 otherwise. Credit spread (Credit_Spread) is measured as the difference between bond yield as reported in Mergent Fixed Income Securities Database (FISD) at the time of the bond issue and a benchmark treasury yield related to U.S. Treasury bonds issued on the same day with a comparable maturity. 12 Maturity (Maturity) is the difference in years between the bond maturity date and the issue date. Bond size (Bond_Size) is estimated as the natural logarithm of the face value of the bond. In all models, we include a number of control variables to account for the firm- and bond-level characteristics that are likely to affect credit spread, maturity, and bond size. Smaller, more leveraged, and less profitable firms generally have high agency costs and are likely to obtain less favorable bond terms. To proxy for the firm’s agency costs, we include firm size (Size; natural logarithm of total assets), leverage ratio (Lev; long-term debt divided by total assets), and profitability (Profit; return on assets). We also control for the firm’s default risk by including controls for operating cash flows (Cfo; cash flows from operating activities divided by total assets), asset specificity (Asset_Specificity; research and development expense divided by total assets), and asset tangibility (Tangibility; net property, plant, and equipment divided by total assets). Finally, to proxy for the firm’s investment opportunities, we include the ratio of the firm’s book value to the market value (Btm). The firm-level controls are lagged 1 year unless otherwise specified.

Credit spread, maturity, and bond size are also likely to be influenced by the bond contract’s specifications. Call options increase the flexibility of the issuer and are expected to be positively associated with credit spread. Accordingly, we include an indicator for whether the issue includes a call option (Callable). Put options (Puttable) and sinking fund (Sinking_Fund) clauses are beneficial for bondholders and are expected to be negatively associated with credit spread, whereas for subordinated designation (Subordinated) clauses, we predict a positive association with credit spread. Finally, bondholders take into account the credit ratings provided by credit rating agencies. We control for the issue’s credit rating by including the numerical equivalent of S&P (or Moody’s or Fitch) credit ratings at the issue date (Credit_Rating). 13 High values of the Credit_Rating variable correspond to worse credit ratings and are associated with high default risk. If a rating is not available from any of the three credit agencies, we assign the issue the lowest credit rating, that is, the highest numerical value, and include a dichotomous variable Not_Rated equal to one if no rating is available and zero otherwise. 14 Issues with credit ratings below BBB- for S&P and Fitch and Baa3 for Moody’s are considered to be of speculative grade. We include an indicator variable equal to one if the issue is of speculative grade and zero otherwise.

To control for the possibility that the pricing and nonpricing terms depend on the industry membership, we include industry fixed effects (Industry FE) (e.g., Jorion et al., 2009; Lou & Vasvari, 2013) based on the two-digit Standard Industry Classification (SIC) codes. We include year fixed effects (Year FE) to account for time-variant macroeconomic factors that could influence bond terms. In addition, bond size exposes bondholders to higher potential losses in case of default. Hence, we control for Bond_Size in model specifications with Credit_Spread as the dependent variable. We also control for the bond’s maturity because longer debt maturities are associated with higher agency costs and the probability of default (Costello & Wittenberg-Moerman, 2011; Demiroglu & James, 2010). Similarly, we include Credit_Spread and Bond_Size and Credit_Spread and Maturity in model specifications with Maturity and Bond_Size as dependent variables, respectively. All variables included in the analysis are defined in the Appendix.

To account for the contemporaneous correlation between the error terms in Models (1), (2), and (3), we employ Zellner’s seemingly unrelated regression (SUR) method (Zellner, 1962), which estimates the parameters of the three equations simultaneously. If H1 is supported, we expect the coefficient of interest β1 in Model (1) to be positive and significant. If H2 and H3 are supported, we expect the coefficient β1 in Models (2) and (3), respectively, to be negative and significant.

Sample Selection

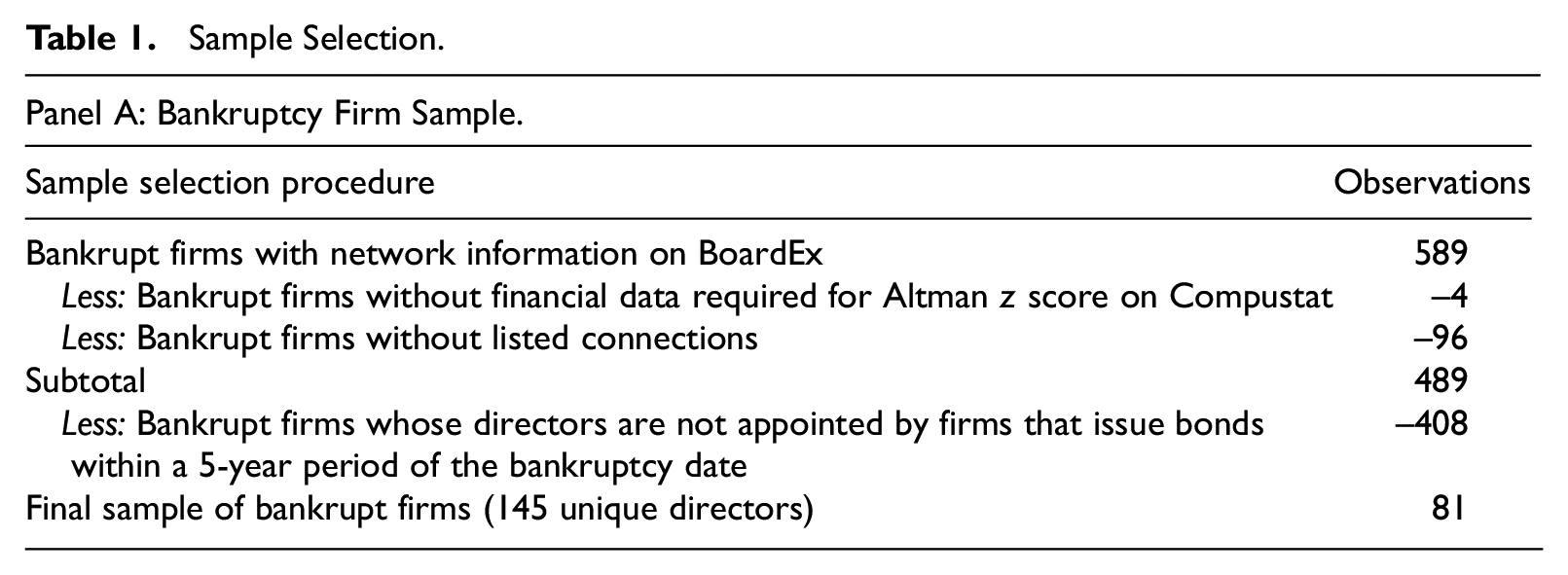

Our initial sample of bankrupt firms consists of 589 U.S. firms that filed for Chapter 7 or Chapter 11 bankruptcy in the period between 2000 and 2014 with board connections data available on BoardEx. 15 Four of these bankrupt firms do not have financial data available on Compustat, and other 96 are connected only to private firms. Our sample of bankrupt firms is then further narrowed to 81 bankrupt firms, whose former directors are appointed by the U.S. publicly traded companies that issue bonds within 5 years of the bankruptcy filing date with available information on Mergent FISD.16,17 Table 1, Panel A details the bankruptcy firm sample selection process.

Sample Selection.

Panel B: Bond Issues Sample.

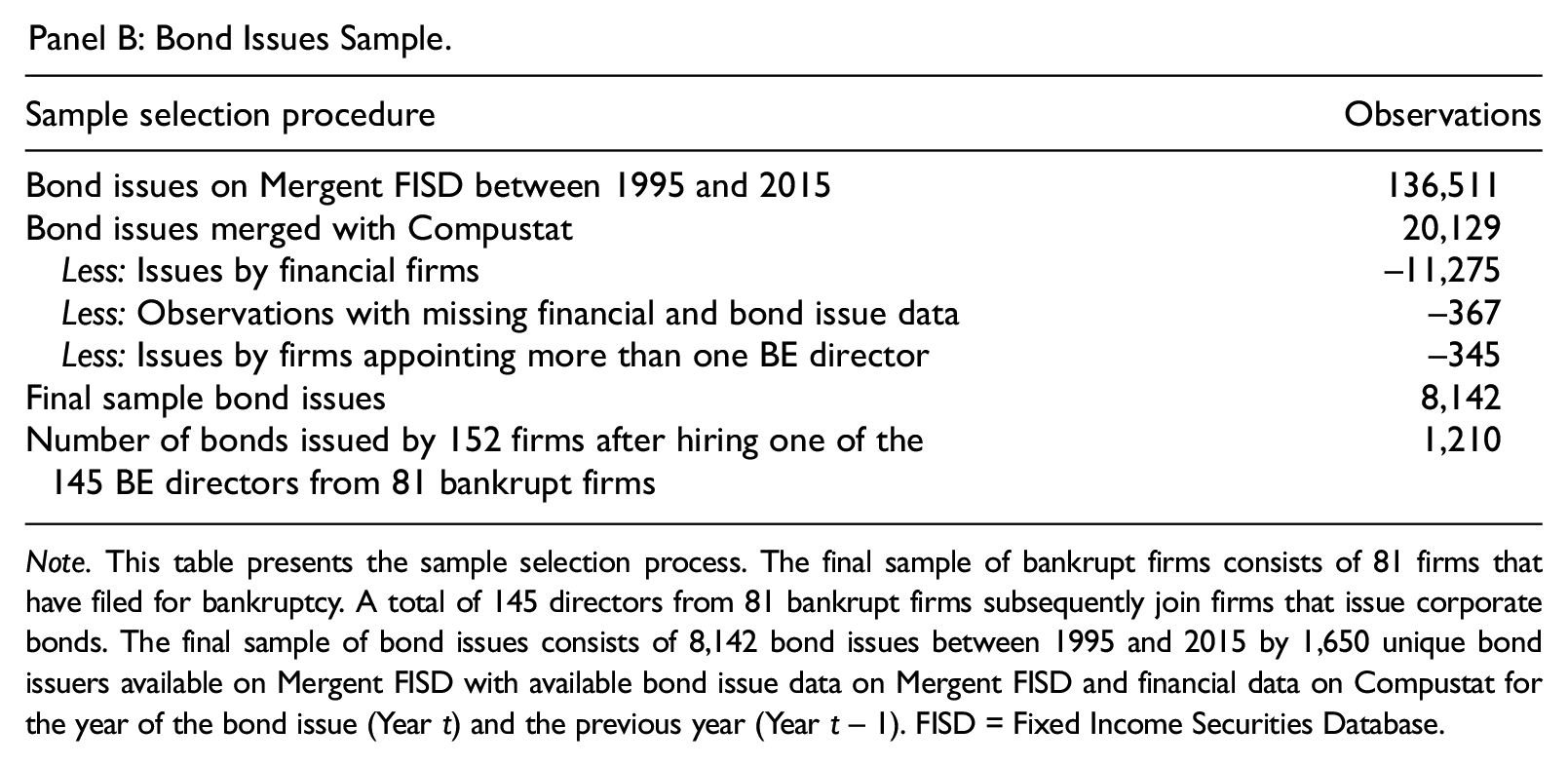

Note. This table presents the sample selection process. The final sample of bankrupt firms consists of 81 firms that have filed for bankruptcy. A total of 145 directors from 81 bankrupt firms subsequently join firms that issue corporate bonds. The final sample of bond issues consists of 8,142 bond issues between 1995 and 2015 by 1,650 unique bond issuers available on Mergent FISD with available bond issue data on Mergent FISD and financial data on Compustat for the year of the bond issue (Year t) and the previous year (Year t − 1). FISD = Fixed Income Securities Database.

Table 1, Panel B presents the sample selection of bond issues. To mitigate concerns that firms appoint directors specifically due to their bankruptcy experience, we exclude 345 issues by 28 issuers where more than one BE director is appointed during the contamination period. We expect that such firms are more likely to be experiencing financial difficulties and hence seek to appoint directors with relevant distress experience. Indeed, there seem to be fundamental differences between these firms and those that appoint only one director. Firms appointing more than one BE director are significantly smaller in size, less profitable, and much more likely to issue speculative-grade bonds than firms appointing only one BE director. Reinserting issuers with more than one BE director in the sample does not change our main inferences (see Table A5 in the Online Appendix).

The final sample of bond issues consists of 8,142 bond issues between 1995 and 2015 by 1,650 unique bond issuers with available bond issue data on Mergent FISD and financial data on Compustat for the years of the bond issue (Year t) and the previous year (Year t− 1). 18 Of those bonds, 1,210 (approximately 14.9%) are issued by 152 firms after hiring one of 145 BE directors from 81 bankrupt firms.

Empirical Results

Descriptive Statistics

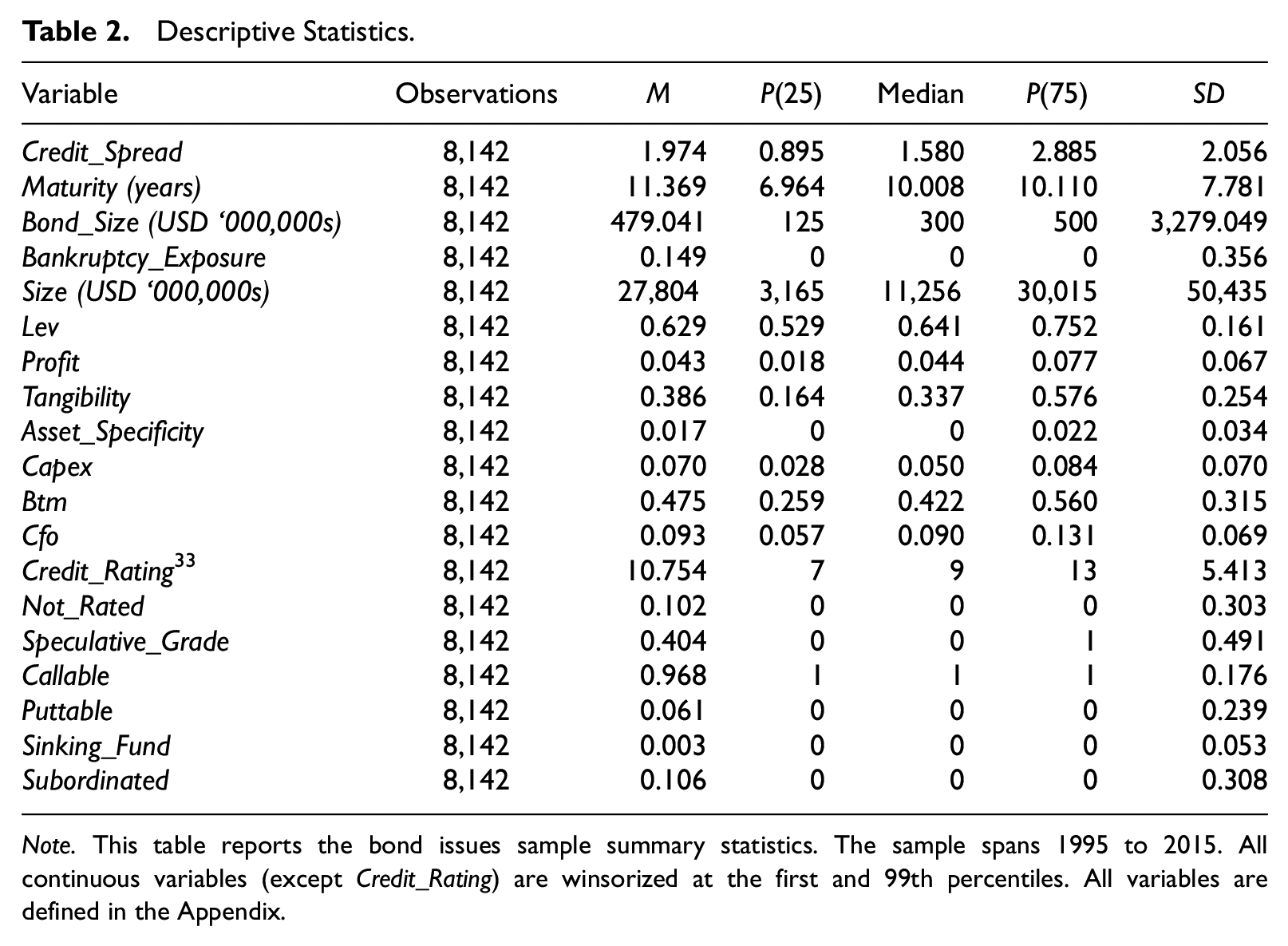

Table 2 presents the descriptive statistics for the firm- and bond-level variables employed in the empirical analysis. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentile to mitigate the effect of outliers.

Descriptive Statistics.

Note. This table reports the bond issues sample summary statistics. The sample spans 1995 to 2015. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentiles. All variables are defined in the Appendix.

On average, the bond issues included in the sample are long term with a mean maturity (Maturity) of about 11.4 years and an average credit spread (Credit_Spread) of about 197 bps. The average size of the bond (Bond_Size) is US$479 million. In the regression analyses, we use the natural logarithm of the bond offering amount, which has a mean value of 11.967 and a standard deviation of two. The average credit rating of the rated issues (Credit_Rating) included in our sample is 9.361, which corresponds approximately to a BBB rating according to S&P and Fitch and Baa2, according to Moody’s. Unrated issues (Not_Rated) are about 10.2% of the issues included in the sample. Following prior literature (e.g., Costello & Wittenberg-Moerman, 2011), we assign the lowest credit rating to unrated issues. The mean Credit_Rating thus becomes 10.754, corresponding approximately to a BB+ rating according to S&P and Fitch and Ba1, according to Moody’s. About 40.4% of the bond issues in our sample are assigned a speculative grade (Speculative_Grade).

The average bond issuer is relatively large, with total assets of US$27.8 billion and highly leveraged with a lagged long-term debt-to-total assets ratio (Lev) of around 62.9%. The mean return on assets (Profit) is 0.04, capitalized expenditure (Capex) has a mean of 0.07, and book-to-market ratio (Btm) has a mean of 0.475. 19

Univariate Analysis

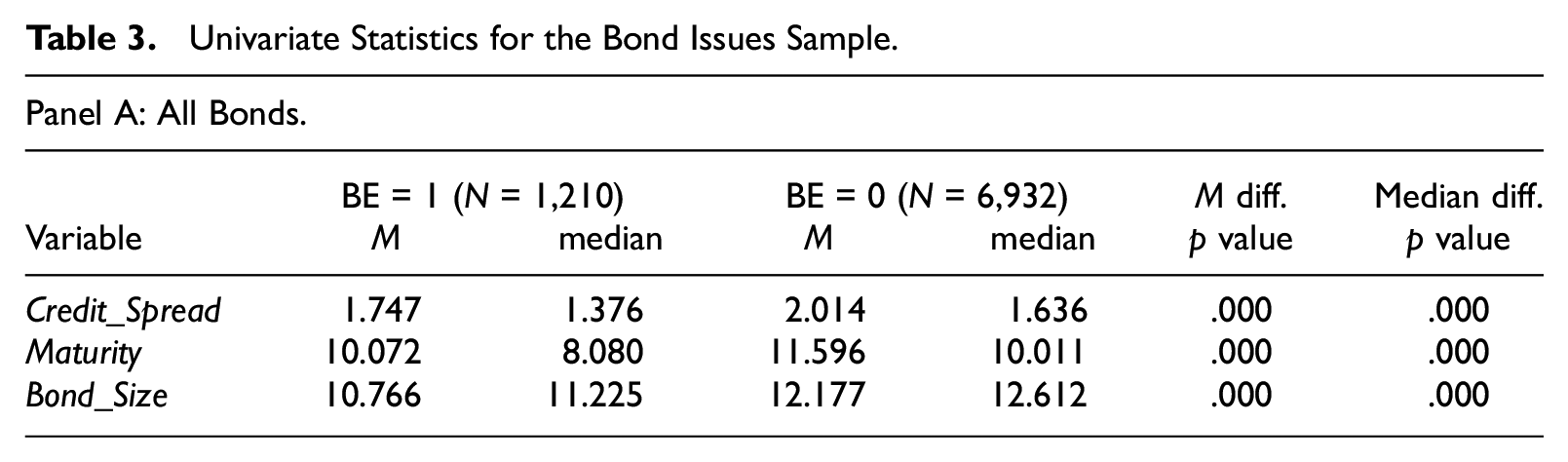

Table 3 presents the univariate analyses. Panel A provides the mean and median values of our main dependent variables—Credit_Spread, Maturity, and Bond_Size—for the subsamples of bankruptcy exposure (BE = 1) and nonbankruptcy exposure (BE = 0) bond issues. Bond issues by BE firms as a whole have significantly lower credit spreads, maturities, and bond sizes with respect to nonbankruptcy exposure issues. Yet, this observation should be interpreted with caution because, in this analysis, we do not differentiate between investment- and speculative-grade bond issues. 20

Univariate Statistics for the Bond Issues Sample.

Panel B: Investment-Grade Bonds.

Panel C: Speculative-Grade Bonds.

Note. This table reports the summary statistics for the dependent variables and tests the difference in means (t test) and the difference in medians (Wilcoxon Mann–Whitney rank-sum test). Panel A presents the summary statistics for the dependent variables for the main sample of bond issues. Panel B presents the summary statistics for the dependent variables for investment-grade bonds. Panel C presents the summary statistics for speculative-grade bonds. N is the total number of observations in each subsample. The dependent variables are defined in the Appendix. BE stands for Bankruptcy_Exposure as defined in the Appendix.

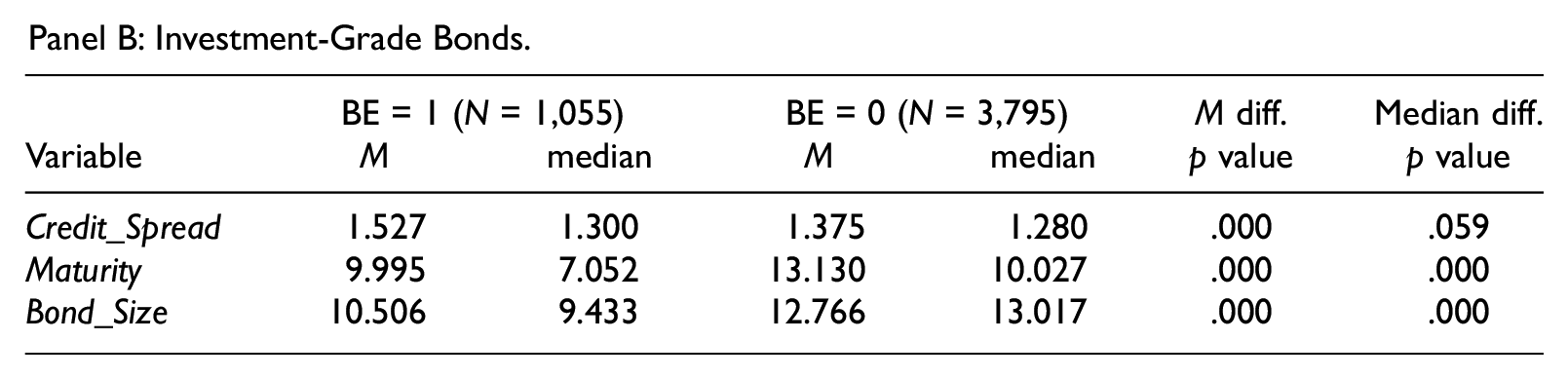

Next, given the inherent differences between investment- and speculative-grade bonds, we partition the sample by whether the bonds receive investment or speculative grade at issue. Panel B of Table 3 presents the univariate analysis of the investment-grade subsample. The t test of the means and the Wilcoxon Mann–Whitney nonparametric test provide initial support for the predictions that the presence of a BE director is associated with less advantageous bond contract terms for the investment-grade subsample. The mean (median) credit spread for the BE subsample is 1.527 (1.300), which is significantly higher than the mean (median) credit spread of 1.375 (1.280) for the nonexposed subsample. The average maturity for the issues in the BE subsample is around 10 years, which is significantly lower than the average maturity for the nonexposed firms of approximately 13 years. Finally, the average bond size of BE issues of 10.506 is significantly lower than the average size of non-BE issues of 12.766.

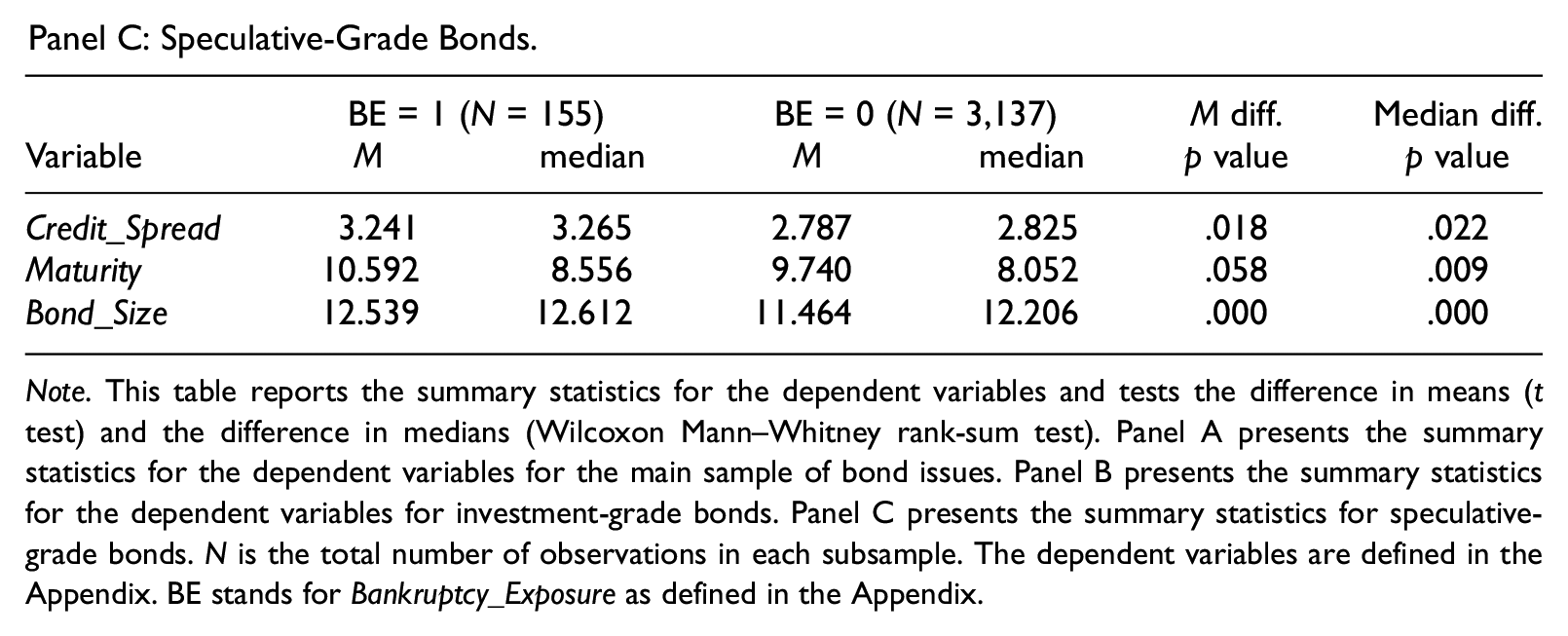

Panel C details the mean and median and the results of the t test and the Wilcoxon Mann–Whitney nonparametric test for the speculative-grade subsample. We observe a higher average credit spread for the BE bond issues consistent with the findings for the investment-grade subsample. However, the average maturity and bond size are higher for the BE subsample, indicating that the presence of a BE director has different implications for the terms of the bond contracts depending on the rating. Specifically, while appointing BE directors might be perceived negatively for investment-grade issuers, speculative-grade issuers in (or close to) financial distress likely appoint BE directors specifically because of their experience at distressed firms, which might be viewed favorably by lenders. 21

Multivariate Analysis

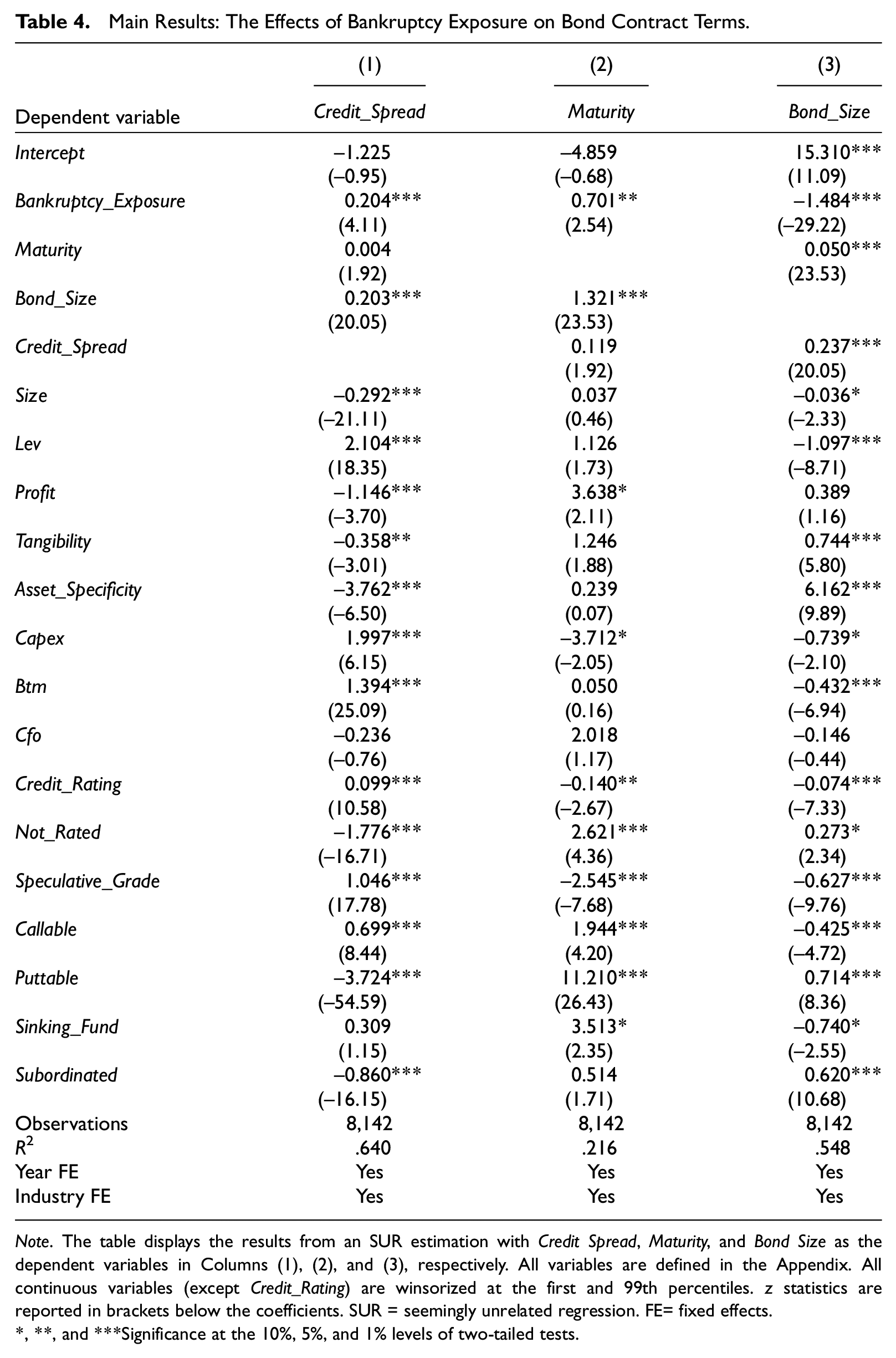

We study the association between the presence of a BE director and the terms of bond contracts within an SUR equations framework to estimate the parameters simultaneously and account for the correlation between the error terms of the three equations. Table 4 presents the results from the SUR estimation of Models (1), (2), and (3). The coefficient of interest β1 is positive and significant (z = 4.11) in Model (1) as expected, supporting the prediction that BE firms bear a higher bond spread after controlling for a series of firm- and issue-specific characteristics, industry, and year fixed effects. More specifically, the presence of a BE director (Bankruptcy_Exposure = 1) is associated with an average increase in credit spread of 20.4 bps, which is both economically and statistically significant. 22 The coefficient of Bankruptcy_Exposure in the estimation of Model (2) is positive and significant (z = 2.54), suggesting that BE issues have higher maturity than non-BE issues, which is contrary to our prediction in H2. 23 Finally, focusing on bond size (Table 4, Column [3]), the coefficient β1(Bankruptcy_Exposure) is negative and significant (z = −29.22), providing support for the prediction that bankruptcy exposure is negatively associated with bond size. On average, appointing a BE director is associated with a 22.6% reduction in bond size.

Main Results: The Effects of Bankruptcy Exposure on Bond Contract Terms.

Note. The table displays the results from an SUR estimation with Credit Spread, Maturity, and Bond Size as the dependent variables in Columns (1), (2), and (3), respectively. All variables are defined in the Appendix. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentiles. z statistics are reported in brackets below the coefficients. SUR = seemingly unrelated regression. FE= fixed effects.

**, and ***Significance at the 10%, 5%, and 1% levels of two-tailed tests.

The coefficients of the control variables are generally consistent with predictions based on prior studies. Larger, more profitable firms with more tangible assets can borrow at a lower cost. Unsurprisingly, the bond-level characteristics appear to be important determinants of bond contract terms. Specifically, higher quality bonds, measured by a lower credit rating score, are associated with a lower credit spread, longer maturity, and larger bond size. However, investors in speculative-grade bonds demand higher credit spread, lower maturity, and smaller bond size. Callable bonds provide flexibility to the issuer and, as expected, are associated with higher credit spread and smaller bond size. 24 The results remain consistent if the contamination period is restricted to 3 years. 25

Robustness Checks

The analyses presented thus far provide evidence that bankruptcy exposure is associated with the terms of the firm’s bond contracts. However, a major concern is that directors with experience at a bankrupt firm are not randomly assigned to firms. 26 While we include a set of control variables aimed to capture different firm- and bond-level characteristics, to mitigate endogeneity concerns further, we perform a series of robustness tests.

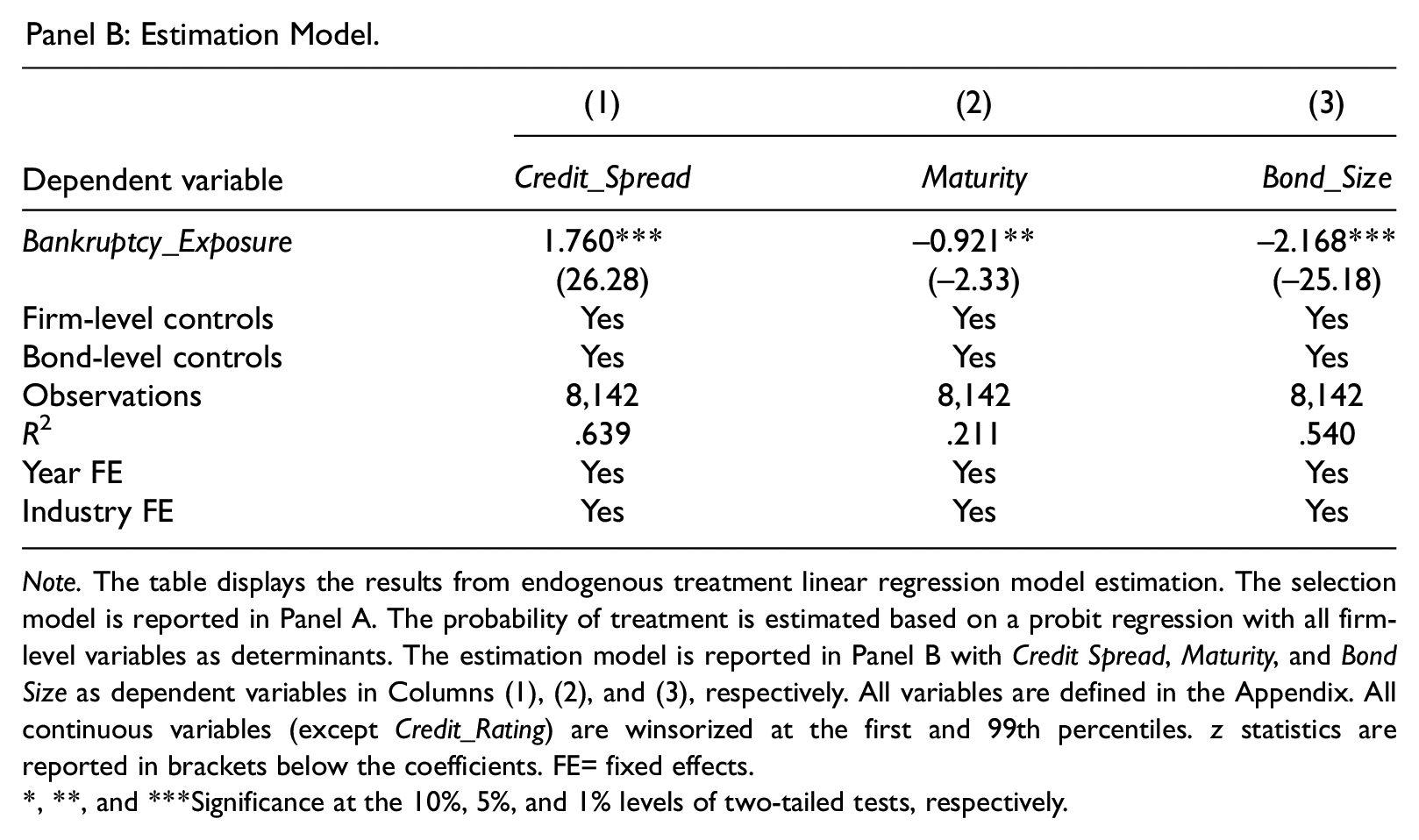

First, to address concerns that the sample of bond issues by BE firms is nonrandom, we employ two treatment effects models: (a) an endogenous treatment effects linear regression model and (b) a treatment effects model with inverse probability regression adjustment. These two models incorporate the endogeneity of the appointment of a BE director in the estimation of the bond contract terms.

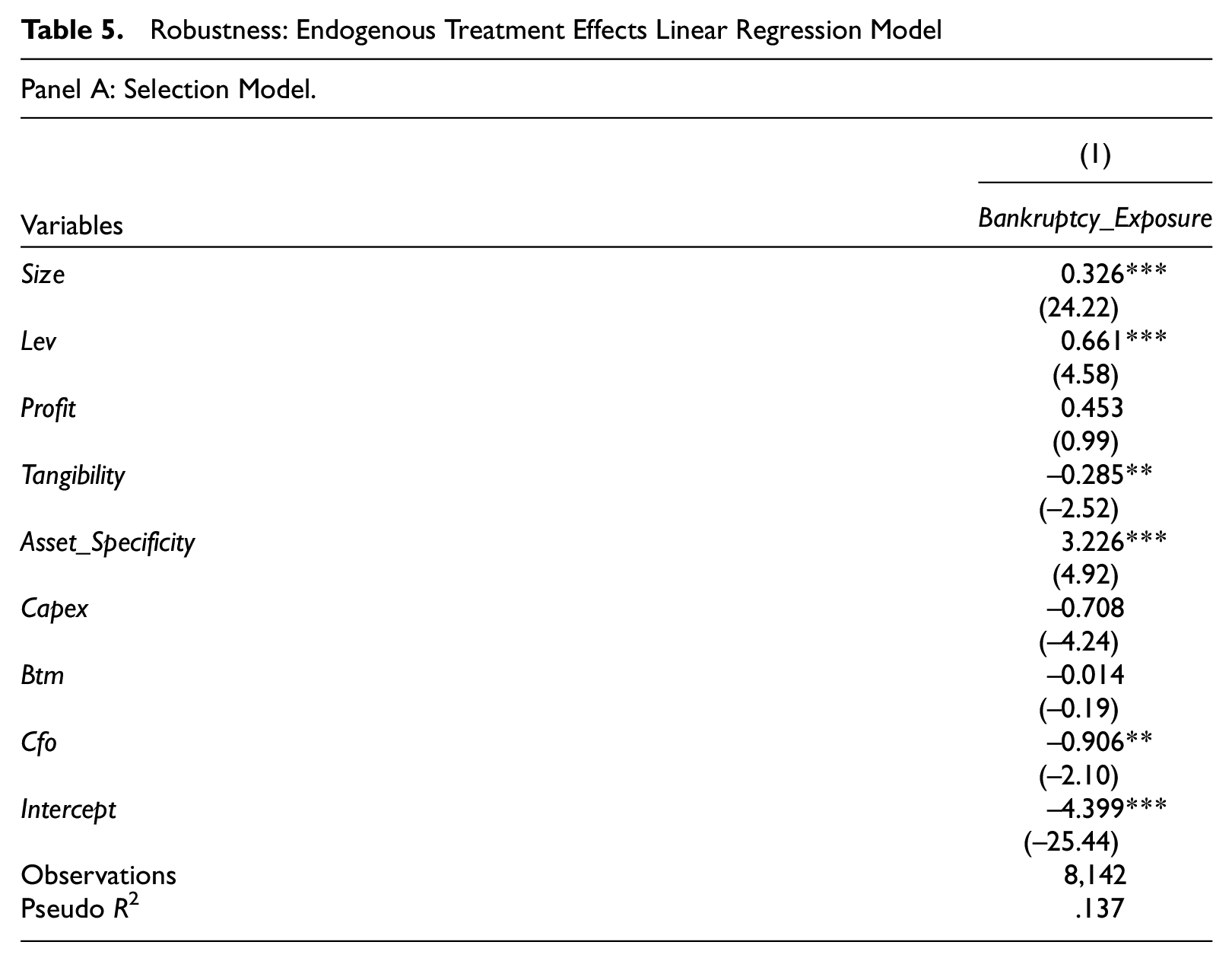

The endogenous treatment effects linear regression model requires a two-step estimation. 27 In the first stage, presented in Table 5, Panel A, we model the probability of appointing a BE director as a function of observable firm-level covariates (i.e., size, leverage, profitability, tangibility, asset specificity, capital expenditure, book-to-market ratio, and operating cash flows). 28 In Table 5, Panel B displays the results from the estimation model with credit spread, maturity, and bond size as the dependent variable in Columns (1), (2), and (3), respectively. Bankruptcy_Exposure coefficient in Model (1) is positive and significant (z = 26.28), consistent with the prediction that the appointment of a BE director is considered a risk factor and priced consequently by bondholders. Moreover, in the test of Model (2), β1 is negative and significant (z = −2.33), providing some support also for the hypothesis that past bankruptcy experience is related to lower maturity (H2). 29 Finally, in Model (3), β1 is negative and significant (z = −25.18), confirming the previously reported results and supporting the prediction that bankruptcy exposure results in a smaller bond size. The signs and the magnitude of the control variables’ coefficients, not reported here for brevity’s sake, are consistent with those reported in Table 4 and generally in line with prior research.

Robustness: Endogenous Treatment Effects Linear Regression Model

Panel B: Estimation Model.

Note. The table displays the results from endogenous treatment linear regression model estimation. The selection model is reported in Panel A. The probability of treatment is estimated based on a probit regression with all firm-level variables as determinants. The estimation model is reported in Panel B with Credit Spread, Maturity, and Bond Size as dependent variables in Columns (1), (2), and (3), respectively. All variables are defined in the Appendix. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentiles. z statistics are reported in brackets below the coefficients. FE= fixed effects.

**, and ***Significance at the 10%, 5%, and 1% levels of two-tailed tests, respectively.

Next, we employ an endogenous treatment model with inverse-probability-weighted regression adjustments. The treatment group consists of firms with a BE director, and the probability of treatment is estimated based on the observable firm-level covariates also used in the previous model. The results of the estimation model, presented in Table A11 in the Online Appendix, are qualitatively similar to the results reported in Table 5. 30

Finally, to address the possibility that some unobservable time-invariant firm-specific characteristics bias our results, we examine the effects of director bankruptcy experience on the terms of bond contracts by focusing only on the subsample of bond issues by firms that appoint a BE director during the sample period. This approach allows us to contrast the terms of the bond contracts before and after the change in the Bankruptcy_Exposure status, effectively using firms as their own controls (e.g., Ettredge et al., 2012; Hail & Leuz, 2009). The results, presented in Table A13 in the Online Appendix, are qualitatively similar to our main results. The effect on maturity is negative, albeit not significant at the conventional levels.

Additional Analyses

Channels Through Which Bankruptcy Exposure Affects the Terms of Bond Contracts

Our main findings support the prediction that past bankruptcy experience is associated with the terms of bond contracts. This is consistent with the notion that the appointment of a BE director increases the riskiness of the firm by raising concerns about the firm’s board oversight (i.e., corporate governance risk), risk tolerance (i.e., financial and investment risk), or future financial health (i.e., distress risk). Next, we turn to some additional analyses to provide insights into the channels through which past bankruptcy experience affects bond contract terms.

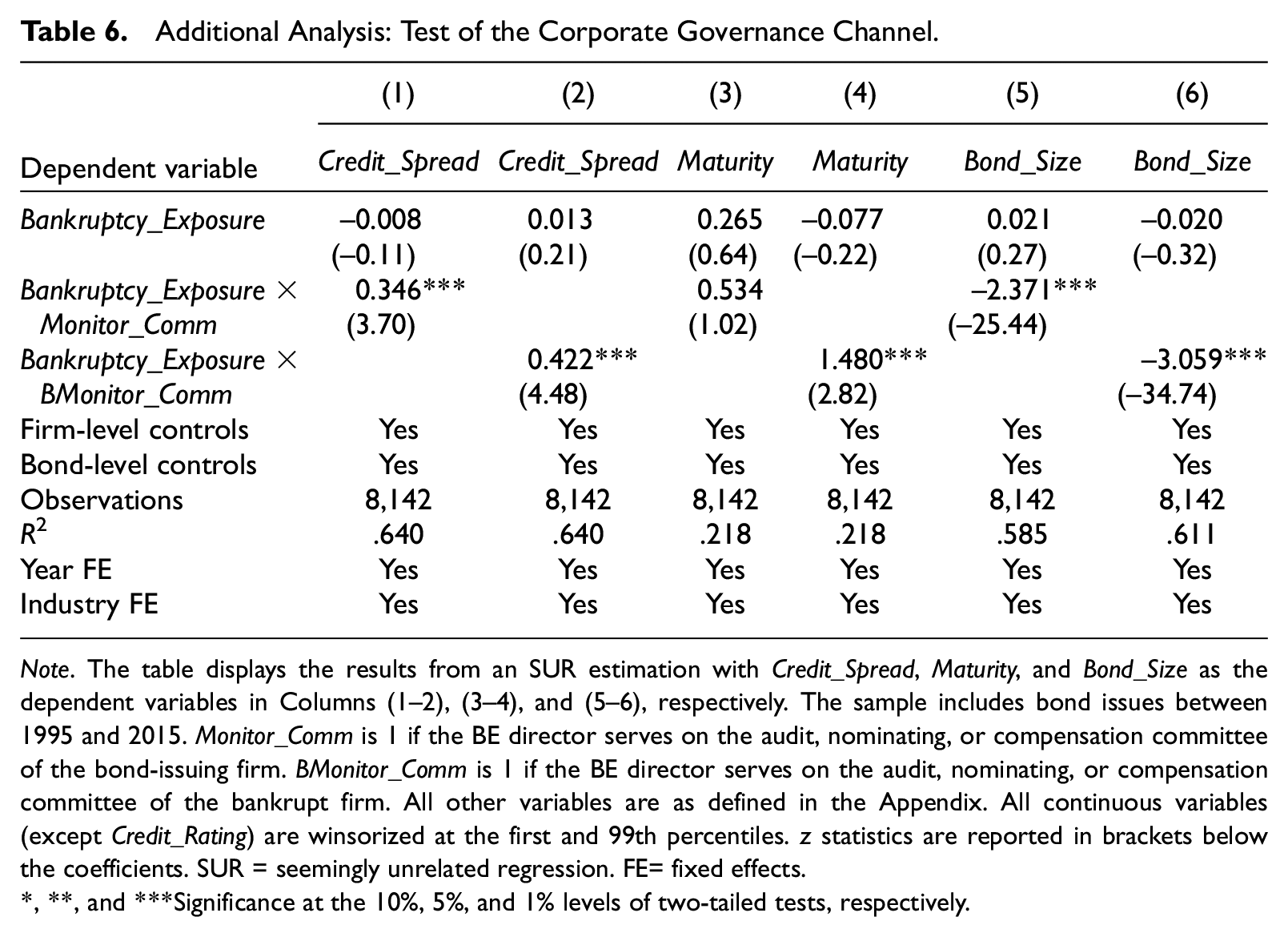

Corporate governance channel

According to the corporate governance channel, the appointment of a director with a tarnished reputation raises concerns about the firm’s corporate governance, which is reflected in stricter contract terms. We examine this channel by exploiting the role of the BE director on the board of the bankrupt and the BE firm. Faleye et al. (2011) identify the audit, nominating, and compensation committees as the key monitoring committees because their main responsibilities include closely monitoring management and maintaining high corporate governance quality. To the extent that the bondholders are concerned about the quality of the corporate governance of the BE firms after the appointment of a BE director, we expect that the effects of past bankruptcy experience on bond contracts are more pronounced if the BE director serves on a key monitoring committee.

To test whether the effect of Bankruptcy_Exposure on credit spread, maturity, and bond size is driven by firms with BE directors serving on key roles, we define two new dichotomous variables. Monitor_Comm equals one if the BE director serves on a monitoring committee in the bond-issuing firm, and BMonitor_Comm equals one if the BE director serves on a key monitoring committee in the bankrupt firm. Monitor_Comm is one for 72% of our Bankruptcy_Exposure issues (872 observations) and BMonitor_Comm is one for 62% of the Bankruptcy_Exposure issues (750 observations). We interact Monitor_Comm and BMonitor_Comm with Bankruptcy_Exposure and expect these interaction variables to be positively associated with credit spread and negatively associated with maturity and bond size.

The results are presented in Table 6. We document a positive and significant effect of the interaction variables on credit spread (Columns [1] and [2]) and a negative and significant effect on bond size (Columns [5] and [6]), in line with the expectation that past bankruptcy experience is particularly relevant for firms with BE directors serving on key monitoring committees. Notably, the effect of Bankruptcy_Exposure becomes insignificant after including the interaction variable in the analysis, suggesting that observations with Monitor_Comm or BMonitor_Comm equal to one explain our results fully. 31 It is important to note that all directors who serve on a key monitoring committee at the bankrupt firm also serve on a key monitoring committee at the bond-issuing firm. Hence, it is impossible to empirically disentangle the effects of being on a key committee at either the bankrupt firm or the bond-issuing firm. Overall, these findings suggest that bondholders are likely concerned about the corporate governance quality of firms appointing BE directors, providing support for the corporate governance channel. 32

Additional Analysis: Test of the Corporate Governance Channel.

Note. The table displays the results from an SUR estimation with Credit_Spread, Maturity, and Bond_Size as the dependent variables in Columns (1–2), (3–4), and (5–6), respectively. The sample includes bond issues between 1995 and 2015. Monitor_Comm is 1 if the BE director serves on the audit, nominating, or compensation committee of the bond-issuing firm. BMonitor_Comm is 1 if the BE director serves on the audit, nominating, or compensation committee of the bankrupt firm. All other variables are as defined in the Appendix. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentiles. z statistics are reported in brackets below the coefficients. SUR = seemingly unrelated regression. FE= fixed effects.

**, and ***Significance at the 10%, 5%, and 1% levels of two-tailed tests, respectively.

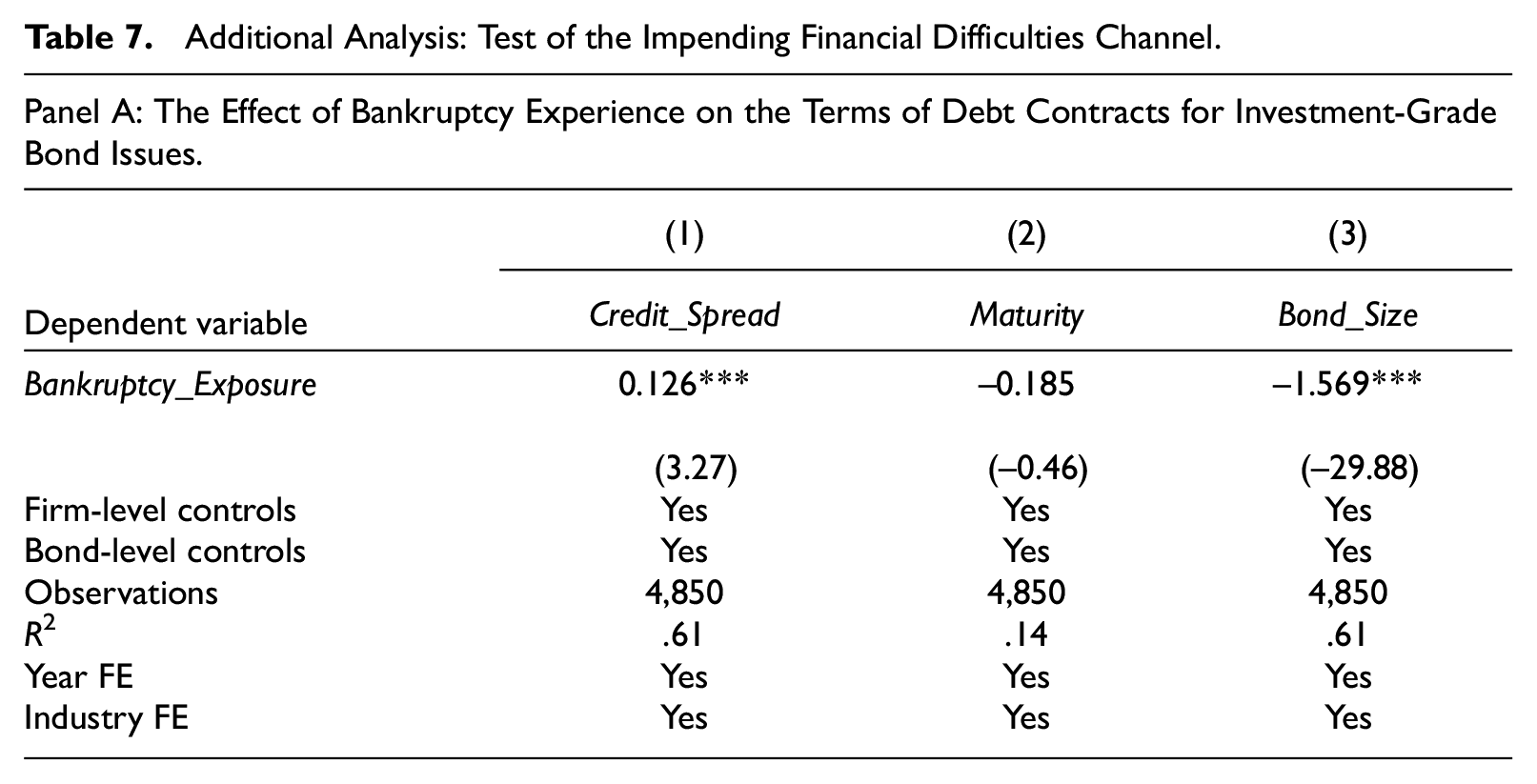

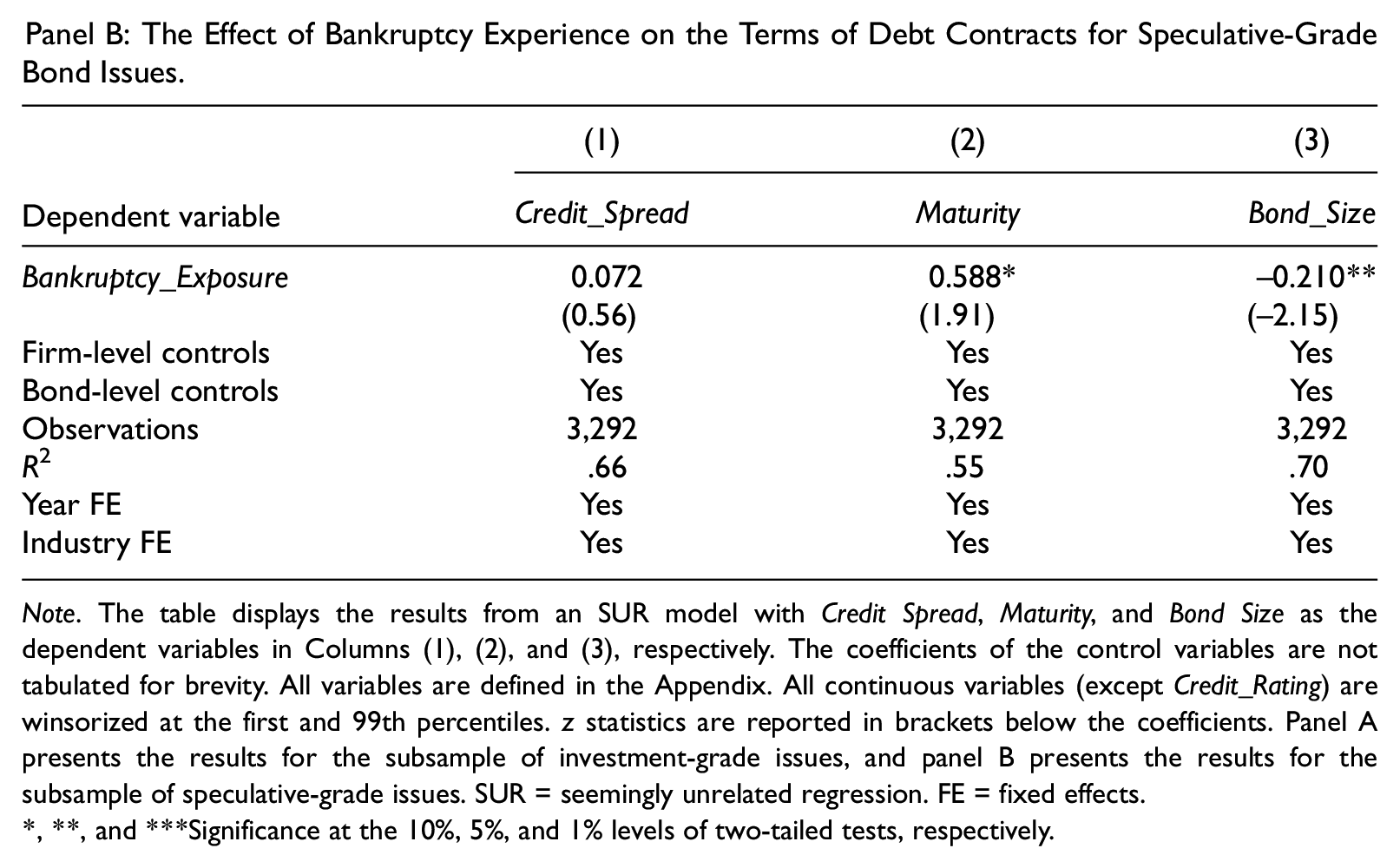

Impending financial difficulties channel

If the appointment of a BE director signals imminent financial problems, we expect that our results are driven by BE firms with a high probability of default or firms that expect adverse shocks to their performance in the future. To test this assertion, we run two additional tests.

First, we partition the sample based on the bond rating assigned at issuance, as it captures the probability of default, and we replicate our main tests separately for the subsamples of investment- and speculative-grade issues. Of all observations, 4,850 are assigned to the investment-grade subsample and 3,292 to the speculative-grade subsample. Table 7, Panel A, presents the SUR estimation results on the subsample of investment-grade bond issues. The coefficient of Bankruptcy_Exposure is positive and significant (β1 = 0.126, z = 3.27) in Column (1), indicating a positive effect on Credit_Spread, negative but not significant in Column (2), and negative and significant (β1 = −1.569, z = −29.88) in Column (3) indicating a negative effect on Bond_Size. The coefficients of the control variables (untabulated for brevity) are qualitatively and quantitatively similar to the previously reported results. Table 7, Panel B, reports the results for the speculative-grade subsample. The effect of Bankruptcy_Exposure on Credit_Spread is not significantly different from zero, while the effect on Bond_Size is negative, consistent with the results for the investment-grade subsample, but smaller in magnitude. The effect on Maturity is positive and weakly significant. This analysis fails to provide support for the impending financial difficulties channel.

Additional Analysis: Test of the Impending Financial Difficulties Channel.

Panel B: The Effect of Bankruptcy Experience on the Terms of Debt Contracts for Speculative-Grade Bond Issues.

Note. The table displays the results from an SUR model with Credit Spread, Maturity, and Bond Size as the dependent variables in Columns (1), (2), and (3), respectively. The coefficients of the control variables are not tabulated for brevity. All variables are defined in the Appendix. All continuous variables (except Credit_Rating) are winsorized at the first and 99th percentiles. z statistics are reported in brackets below the coefficients. Panel A presents the results for the subsample of investment-grade issues, and panel B presents the results for the subsample of speculative-grade issues. SUR = seemingly unrelated regression. FE = fixed effects.

**, and ***Significance at the 10%, 5%, and 1% levels of two-tailed tests, respectively.

Second, we classify firms into life cycles following the approach outlined by Dickinson (2011). Issues by firms classified as being in a shakeout or a decline life cycle in any year during our sample period are removed from the sample. The findings of this analysis, presented in Table A14 in the Online Appendix, are consistent with those reported previously.

Increased risk tolerance channel

Prior professional experience at a bankrupt firm may affect the risk tolerance of the individuals involved and their current firms (e.g., Gopalan et al., in press). Hence, it is possible that the BE firms in our setting may increase their financial and investment risk, which in turn results in less advantageous bond contract terms.

In all model specifications presented thus far, we control for the firm’s financial leverage, operating cash flows, capital expenditures, and R&D investments to ensure that we are not capturing any effects on the terms of bond contracts that could be due to the firm’s financial and investment policies. However, to directly assess whether and to what extent the firm’s financial and investment policies mediate the effect of prior bankruptcy experience on the terms of bond contracts, we conduct a Sobel-Goodman test for mediation (MacKinnon et al., 1995; Sobel, 1982) separately for each outcome variable (i.e., Credit_ Spread, Maturity, and Bond_Size) and for each potential mediator (Lev, Cash_Hold, and Capex). The results, presented in Table 8, indicate that the indirect effect of bankruptcy experience on credit spread through leverage accounts for only 3.7% of the total effect, whereas the direct effect accounts for the remaining 96.3%. Furthermore, leverage partially mediates the effect of prior bankruptcy experience on bond size. The indirect effect explains 1.9% of the total effect of prior bankruptcy experience on bond size, whereas the direct effect explains the remaining 98.1%. Hence, we document only limited evidence in support of the increased risk tolerance channel.

Additional Analysis: Increased Risk Tolerance Channel (Sobel-Goodman Test).

Note. The table displays the results from a Sobel-Goodman test for mediation effects. The test is run separately for each dependent variable/mediator pair with firm- and issue-specific controls resulting in nine different combinations with Credit_spread, Maturity, and Bond_size as dependent variables in Column (1) and Leverage, Cash_Hold, and Capex as mediators in Column (3). The mediator variables are lagged 1 year. The independent variable Bankruptcy_Exposure is one if the firm is identified as exposed and 0 otherwise. The test includes the full set of firm-specific control variables (lagged 1 year) and issue-specific control variables. All variables are defined in the Appendix. All continuous variables are winsorized at the first and 99th percentiles. The values of p are reported in brackets below the coefficients in Columns (4), (5), and (6).

**, and ***Significance at the 10%, 5%, and 1% levels of two-tailed tests, respectively. ** shows significance at the 5% level, which is already added; in this table none of the variables are significant at the 5% level.

Taken together, our additional analyses provide support for a corporate governance channel. Yet, we acknowledge that we cannot completely rule out all alternative explanations.

Do the Main Findings Depend on the Causes of Bankruptcy?

Our results are consistent with the notion that appointing directors with a damaged reputation can be costly for the firm in question. To the extent that this effect is due to the capital providers attributing responsibility to board members for corporate distress, we expect lower reputational penalties and hence lower (or no) effects for bankruptcies taking place in exceptionally challenging market conditions or adverse macroeconomic shocks such as the dotcom bubble of the early 2000s or the GFC of 2007 to 2009. To test this assertion, we generate an indicator variable, GFC_DOTCOM, for bankruptcies during the years 2000 and 2001 (the dotcom bubble) and 2007, 2008, and 2009 (the GFC) and interact it with our main variable of interest, Bankruptcy_Exposure. The findings, presented in Table A15 in the Online Appendix, show that the interaction variable is significantly negatively associated with credit spread and positively associated with bond size, completely mitigating the effects of Bankruptcy_Exposure. That is, the net effect of bankruptcy exposure on the terms of bond contracts is indistinguishable from zero for firms appointing directors whose prior firms filed for bankruptcy, likely due to exogenous shocks to firm performance.

Conclusion

In this article, we investigate how a director’s past bankruptcy experience affects the pricing and nonpricing terms of public debt contracts. We document higher credit spread and smaller bond size for firms with such directors. This is in line with the argument that directors’ career records and prior experiences are relevant for investor decision-making. Our findings are robust to implementing treatment effects models and other specifications. This mitigates, albeit without eliminating, endogeneity concerns. In addition, our findings with respect to maturity are mixed and should be interpreted with caution. Specifically, while we document a positive effect on maturity, which appears to be driven by speculative-grade issuers, the effect for investment-grade issues is negative but insignificant.

Our main findings are consistent with a number of potential explanations. The additional tests support a corporate governance channel. Our interviews with global fixed-income asset managers also indicated that they view the appointment of bankruptcy-experienced directors on the board as a red flag signaling poor corporate governance. Instead, we do not find evidence for the impending financial difficulties and the increased risk tolerance channels. Future research could provide additional evidence on the channels through which past professional experiences affect debt contracting.

Taken together, our evidence suggests that board members’ professional experience matters for debt contracting purposes and appointing directors with prior bankruptcy experience has real economic consequences for bond-issuing firms. What remains an open question is whether the cost of equity capital is also higher for firms that appoint such directors and whether prior bankruptcy experience matters for private lenders. We believe that these are interesting avenues for future research.

Supplemental Material

sj-pdf-1-jaf-10.1177_0148558X211015533 – Supplemental material for Corporate Bankruptcy and Directors’ Reputation: An Empirical Analysis of the Effects on Public Debt Contracts

Supplemental material, sj-pdf-1-jaf-10.1177_0148558X211015533 for Corporate Bankruptcy and Directors’ Reputation: An Empirical Analysis of the Effects on Public Debt Contracts by Stefano Gatti, Mariya N. Ivanova and Gabriel Pündrich in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

| Variable name | Definition | Source/s |

|---|---|---|

| Dependent variables | ||

| Credit_Spread | The difference between a bond issue’s offering yield and the yield of a benchmark treasury issue | Mergent FISD and U.S. Department of the Treasury |

| Maturity | An issue’s maturity date minus its offering date in years | Mergent FISD |

| Bond_Size | The natural logarithm of an issue’s offering amount | Mergent FISD |

| Independent variable | ||

|

|

An indicator variable = 1 if a director with a recent bankruptcy experience serves on the board of the issuer when the bond is issued; we require that the director was serving on the board of the bankrupt firm at any point in time during the 5-year period preceding the bankruptcy date and that the bonds are issued within the 5-year period following the bankruptcy date and the appointment of the director | BoardEx, Mergent FISD, SEC Edgar |

| Firm-level controls | ||

| Size | Natural logarithm of total assets | Compustat |

| Lev | Long-term debt (dltt) scaled by total assets (at) | Compustat |

| Profit | Return on assets; income before extraordinary items (ib) divided by total assets (at) | Compustat |

| Tangibility | Net property plants and equipment (ppent) divided by total assets (at) | Compustat |

| Asset_Specificity | Research and development expense (xrd) divided by total assets (at) | Compustat |

| Capex | Capital expenditure (capx) divided by total assets (at) | Compustat |

| Btm | Book-to-market ratio, computed as stockholder’s equity (ceq) divided by the number of outstanding shares of common stock times the share market price at the financial year end (csho*prcc_f) | Compustat |

| Cash_Hold | The sum of cash (ch) and short-term investments (che) scaled by total assets (at) | Compustat |

| Cfo | Operating cash flows (oancf) divided by total assets (at) | Compustat |

| Issue-level controls | ||

| Credit_Rating | Numeric values assigned to bond ratings offered by S&P’s, ranging from 1 to 21 (AAA = 1, AA+ = 2, etc.). If S&P rating is not available, we use Moody’s rating. If Moody’s rating is not available, we use Fitch’s | Mergent FISD |

| Not_Rated | An indicator = 1 if no rating related to the issue is available | Mergent FISD |

| Speculative_Grade | Indicator variable equal to 1 if an issue is rated below BBB- by S&P or Fitch, or below Baa3 by Moody’s and 0 otherwise | Mergent FISD |

| Callable | An indicator = 1 if the issue has a call option | Mergent FISD |

| Puttable | An indicator = 1 if the issue contains a put option | Mergent FISD |

| Sinking_Fund | An indicator = 1 if the issue requires a sinking fund | Mergent FISD |

| Subordinated | An indicator variable = 1 if the issue is subordinated | Mergent FISD |

| Variables used in the additional analyses | ||

| Monitor_Comm | An indicator = 1 if the director with past bankruptcy experience serves on a key monitoring committee (audit, compensation, or nominating) at the bond-issuing firm | BoardEx, SEC Edgar |

| BMonitor_Comm | An indicator = 1 if the director with past bankruptcy experience serves on a key monitoring committee (audit, compensation, or nominating) at the bankrupt firm | BoardEx, SEC Edgar |

| GFC_DOTCOM | An indicator = 1 during the global financial crisis (2007–2009) and the dotcom bubble burst (2000–2001) | |

Note. SEC = Securities and Exchange Commission; EDGAR = Electronic Data Gathering, Analysis, and Retrieval.

Acknowledgements

The authors thank Sasson Bar-Yosef, Anne Beatty, Claudia Imperatore, Craig Lewis, Erik Lie, Annalisa Prencipe, the participants at the 2018 Annual Accounting Conference in Berlin, Germany, and the 2018 European Accounting Association (EAA) Congress in Milan, Italy, and especially Bharat Sarath (editor) and two anonymous referees for helpful comments and suggestions. Mariya N. Ivanova gratefully acknowledges financial support from the Tore Browaldhs foundation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Mariya N. Ivanova received financial support from the Tore Browaldhs foundation.

Data Availability

The data used in this study are available from the indicated sources.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.