Abstract

This case illustrates Bollywood, the Hindi film industry, operating out of Mumbai. As an industry, Bollywood is at crossroads today, trying to create a sustainable business model. The case dives deep into the structure of the industry, the conduct of its existing players and its performance. The case stands out as a means for understanding industry-level competitiveness and the unique profitability patterns. It addresses the concerns of the incumbents of Bollywood and how they can draw lessons from its peer—the Tamil film industry in Chennai—in terms of a regulated sustainable business model.

As I recall the fable of the goose that laid golden eggs, I have several questions running on my mind—Are artists, exhibitors and major service providers killing the golden goose? Will the short-sighted bottom line-focused corporate actions destroy the profitability of the Hindi entertainment industry in the long run? Will Bollywood producers be able to strike the right balance between creativity and profitability? (Pahlaj Nihalani, promoter of Chiragdeep International, a movie production house in the Mumbai film industry)

Pahlaj Nihalani was a successful movie producer in the Mumbai film industry (aka Bollywood). Chiragdeep International, the production house that he ran and owned, had a string of hits like Aankhen, Shola Aur Shabnam, Ilzaam, Haathkadi, etc., in the 1990s under its belt. Though not one of the A-listers, Nihalani was respected in the Bollywood circles for his perspicacity and judiciousness. Nihalani also used to be the Chairman of Central Board of Film Certification (CBFC) under the Ministry of Information and Broadcasting, a position he held from January 2015 to August 2017. For such a man, the above words carried a definite sense of foreboding and desperation. This desperation was creeping in because Nihalani found himself on a very sticky wicket. His latest production, Rangeela Raja, which had one of the superstars of the 1990, Govinda playing two characters, was not getting theatrical distribution. He had clear notions about why things had come to such a pass in the Mumbai film industry. He believed that such a scenario was the fallout of increasing corporatization of film-making and distribution.

The Mumbai film industry was getting split across the middle with the increasing presence and gradual dominance of the film corporations. Standalone production houses like Chiragdeep were stuck between the competitive pressures from those corporate entities and focus on creating content for their core customer base. As Nihalani opined

The entertainment industry is run by a glamorous mafia. They all sit, eat, sleep and make movies together. Solo producers like me with no corporate backing are being pushed out of the film industry in the name of corporatization. After the government added the film industry to the list of legitimate industries, the corporatization of Bollywood—and the wider entertainment industry—began.

Similar views were expressed by leading the trade analyst, Komal Nahta

The most important quality a producer should possess is the ability to assess which scripts will work and at what price. Because corporates came in ill-equipped, they started applying business principles to the film industry and went completely wrong. It took 10–15 years because they had deep pockets. An individual producer would have shut shop in 3–4 years.

Thus, Nihalani and other such producers whose primary intent was providing content to the viewers were getting a short shrift when it came to certification troubles, marketing opportunities and availability of cheaper options. Their chances were getting crowded out by the financial influence of the corporations.

Overview

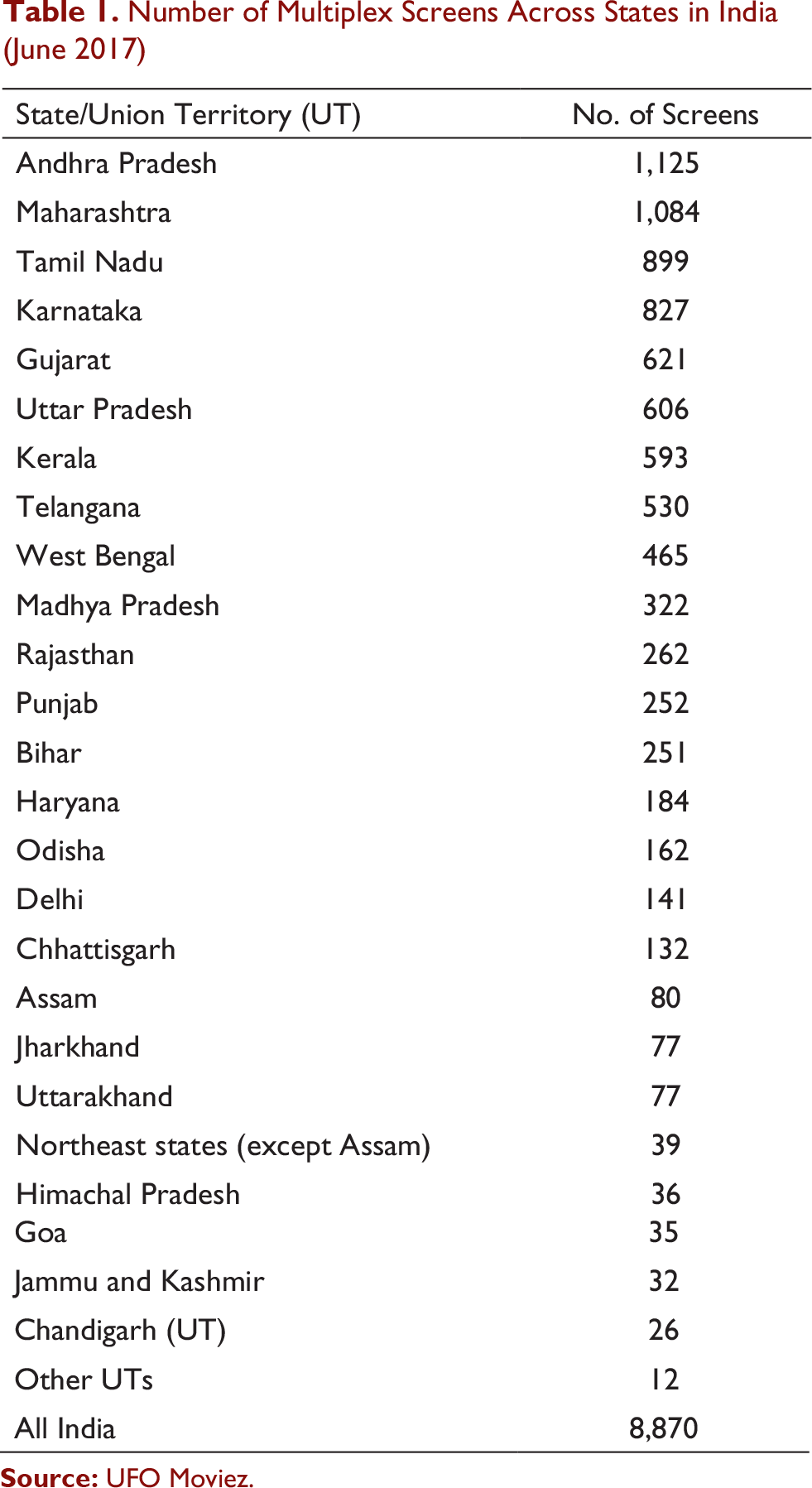

Number of Multiplex Screens Across States in India (June 2017)

In an exclusive report filed for Reuters India (Jamkhandikar, 2014), Shailesh Kapoor of Ormax Media, a firm that tracked Bollywood films, had highlighted that the box-office revenue was undergoing a dip due to high domestic ticket prices and lacklustre content.

While ticket price was a challenge that the industry needed to address, lack of quality content was a pressing issue that Bollywood was facing. This had given way to the consistent success of the Hollywood blockbusters in the country. In 2015, except for films like Baby, Dum Laga Ke Haisha, Badlapur, NH10 and Piku, no other film had performed well at the box office. On the contrary, Hollywood films like Fast & Furious 7 and Avengers: Age of Ultron had bigger openings and longer runs at the Indian box office.

Experts suggested that it was not only production budget constraint but also the lack of planning and overspend on marketing that were affecting Hindi cinema; for instance, a Hollywood film typically took 36 months to plan and 12 months to execute, whereas an Indian film took 6 months in planning and 18 months in execution (Ernst & Young, 2013). While one could suitably discount the differences due to the scale of Hollywood projects, the gap was still significant. This showed that a meticulously planned movie project could save a lot of time in execution, as was evident from the Hollywood numbers.

The Evolution of Business in Bollywood

On 3 May 2013, the Hindi Cinema celebrated 100 years of its existence. A hundred years ago on that very date (NDTV, 2013), producer Dadasaheb Phalke released his silent film, Raja Harishchandra at the Coronation Theatre in Mumbai (then Bombay). The film was subtitled in Hindi and English. Then the industry grew from strength to strength through landmark films like Mughal-e-Azam (1960) and Sholay (1975). These films not only serve interesting content but also brought about major changes in filming and projection technologies. Sholay was the first Indian film to have a stereophonic soundtrack and was presented in the 70-mm widescreen format. However, the distribution format did not see any change.

The first multiplex cinema hall was set up by PVR in Saket, Delhi in 1997. As on January 2015, PVR, Inox, Cinepolis and Carnival Cinemas were the top four multiplex chains across India (Malvania, 2015). There were 15–20 regional players and some local players in various states. The total count of multiplex screens was about 2,050, and the total count of single screens was about 14,000. The key differences between a single screen theatre and a multiplex were in the number of screens and the seating capacity. While a multiplex had a minimum of three screens, its seating capacity was almost a third of a single screen theatre. The other big change that occurred in Bollywood was the total metamorphosis of the production business model.

From Studio Model to Production House to Corporatization

Over the years, the Hindi film industry has moved from being semi-organized to fragmented to organized and dominated by big players. During the initial years, the studio model was popular. Under this model, all aspects of film-making from acting, technical matters for post-production, marketing and distribution were done in-house by the studios. Thus, the activities could be visualized in the form of a corporate value chain wherein sequential activities combine to create and deliver value for the consumer within the boundary of the firm. In this system, all the artists and technicians were employees of studios, who were either paid a salary or were under contract for longer periods. This approach helped studios standardize their film-making style, achieve economies of scale leading to cost efficiencies and develop their own brands in the film industry. The producers would get the finances from the film distributors with a guarantee of screening the film in cinemas for a certain period. Loans would be repaid in terms of box-office collections with no further liability of the producer. Distributors would keep the entire profits earned from the film without sharing with the producers. Nihalani mentioned, ‘Until the advent of what is referred to as ‘corporatization,’ which started to take shape in some seriousness about five years ago, there was no integration between production, distribution, or exhibition, although that is beginning to change now’.

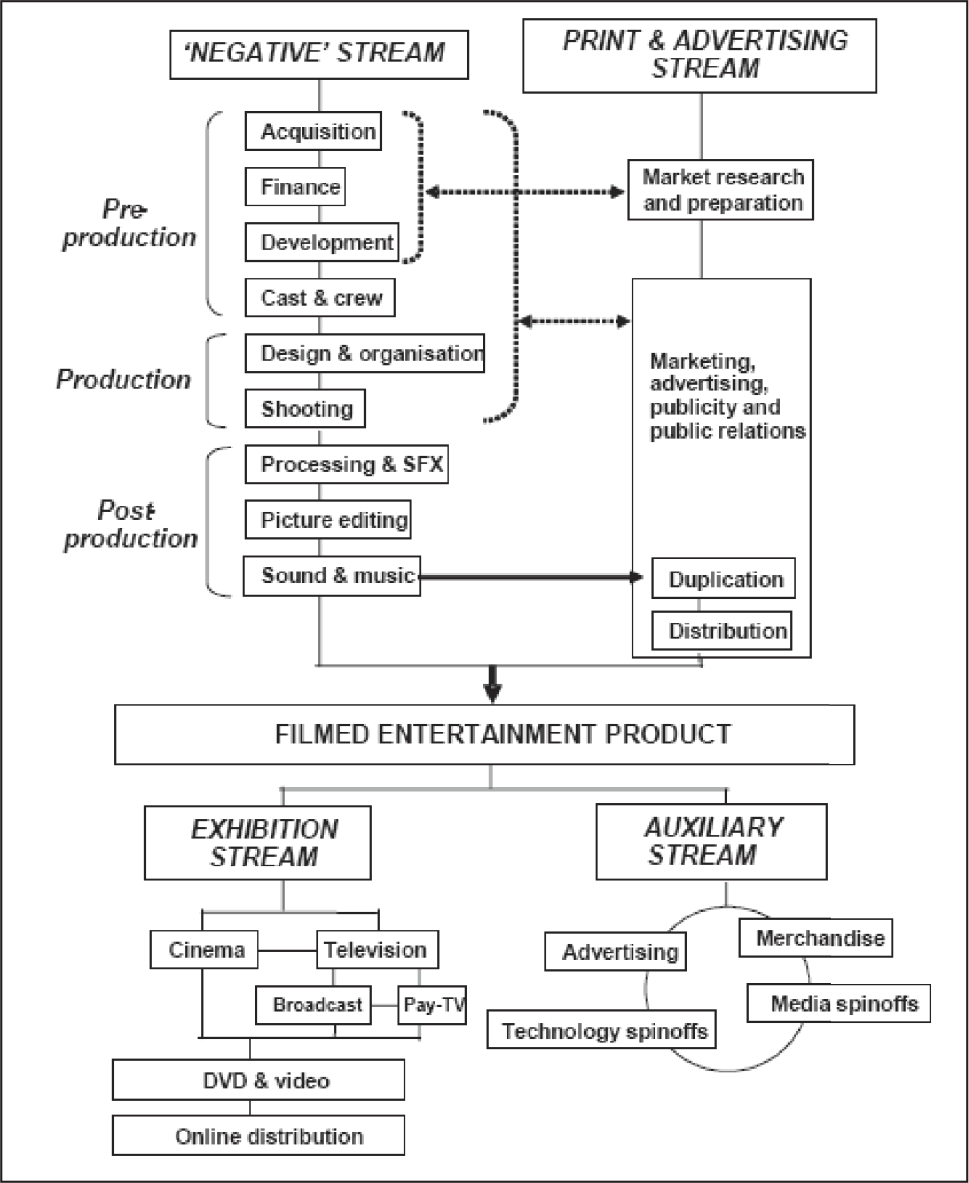

However, as the industry grew and fan clubs for film stars started emerging as well, actors started demanding higher remunerations. It was impossible for studios to retain them exclusively, and hence, actors turned professionals. From being employees, they started accepting freelance assignments. The whole value chain model metamorphosed into a value system model. In the value system, all the movie-making activities are carried out by a chain of individual businesses and freelancers who come together for the completion of the film project. The detailed value system model for the motion picture industry is given in Figure 1. Nihalani opined that

The type and extent of changes that have taken place in Bollywood since the granting of industry status, viz. corporatization, the advent of multiplexes, and the celebration of mainstream Hindi cinema in the world’s most prestigious film festivals – none of that could have been predicted by members of the industry.

Successful actors got paid much higher remunerations as compared to the salaries in the studio system. On the other side, this increase in professional fees led the film production costs to skyrocket as the technicians also moved out of the studio payrolls and started charging more. As the production cost shot up, the distributors now only bore 50 per cent of the total cost, which forced film producers to look for other sources of finances. Promissory note system became the most prevalent source of financing. In this semi-formal system, the producers would write an unconditional order to financers to pay. This gave way to several independent financiers to make their debut as co-producers. These producers did not necessarily have the know-how on film-making but had huge sources of finance. This was the time when black money was pumped into the system, and high rates of interest (up to 40 per cent per annum) prevailed. The high cost of film production and these financing structures made film production a risky profession until the advent of corporate players in the industry. As Nihalani mentioned, ‘I belong to this industry as much as those who are currently monopolising the A-list stars.’ While the law was amended in 2000 to allow the film industry to qualify for bank credit, the underworld’s influence within Indian cinema had already become deeply entrenched and pervasive. In many instances, film-makers and celebrities were forced to accept underworld financing whether they wanted to or not. Mahesh Bhatt once observed that ‘there’s hardly anybody in the film industry who has…not been contacted by the mafia’. In 2001, the Indian film industry was accorded ‘Industry’ status by the government and the institutional financing came into the system (India Brand Equity Foundation, 2013). Applying for a loan and insurance (though Subhash Ghai had done it first a few years back for Taal) (Sharma, 2016) were options that producers could now avail. Many corporate houses stepped forward to invest in movies. In 2002, the government allowed 100 per cent foreign direct investment (FDI) (Knowledge@Wharton, 2011) in film production, exhibition and distribution. International studios such as Fox, Warner and Disney made an entry into the Indian market. Production houses such as UTV Software Communications, Eros International Media, Reliance Entertainment, Viacom 18 Motion Pictures and Balaji Telefilms adopted a professional approach and started focusing on ‘breaking even’ even before the release of a film. Nihalani strongly believed that film-makers should not be content with earning all their profits from a small segment of the audience, which is what the advent of multiplexes with their exorbitant ticket rates have done to the film business. The industry should be trying to grow its audience, not shrink it.

These production houses employed two strategies targeted at (a) production and (b) cash flow.

On the production level, these houses negotiated deals with various equipment suppliers and brand tie-ups to took care of the other costs involved in film-making. Also, some opted for part-production and revenue sharing post production. Such strategies helped production companies to de-risk and offset the disproportionate dependence on theatre revenues. Another regular practice that production houses were following was to link the remuneration of an actor to the performance of the film. On the cash flow level, the corporate bodies were focused on milking the various rights such as music, television, satellite, home video, Internet, digital, in-flight, overseas, and merchandizing. This helped in generating substantial revenue. Hence, even when a film failed at the box-office, these production houses would lose just 10–15 per cent. However, if a film turned out to be a hit, these houses earned a big profit.

From Physical Prints to Digital Prints

In the era of pre-digitization, movies were released in the tier-I cities in the first phase and tier-II and tier-III cities in the subsequent phases. On average, Indian producers made 200–300 celluloid prints of their film and managed to cover not more than 700 cities during the first phase. Pirates made use of this phased release schedule and introduced pirated versions of the film in the market. The scenario had improved over time; a movie would be released pan-India and in 1,500–1,800 screens on an average. For big banner films, the number was around 4,000–4,500 screens.

In 2010, depending on the length of the film, the cost of a 35-mm film print would vary between ₹35,000 and ₹50,000 (Dubey, 2012). A few had expected that with digitization this cost would come down to ₹200 (creating a digital disk and sending the same to a movie theatre by courier), but then, the cost was about ₹15,000 per digital print per screen for 2 weeks.

Earlier, film reels had silver iodide and hence had a resale value of approximately ₹40 per kg. But, they did not bring returns to the distributor or a producer. Distributors advised exhibitors to destroy physical prints to prevent piracy. The era of digitization was marked with speed in terms of go-to-market, had taken better control on piracy and had helped in reducing the cost.

Health of Bollywood

The rule of the jungle had always been the survival of the fittest. Corporatization helped in regulating the industry. However, independent producers had been wiped off the slate. In the name of de-risking the business, portfolio management and innovation, corporates had played a major role in pushing the cost of film production and promotion to such an extent that independent producers were not able to match. This made independent producers non-efficient and non-productive despite having created good content. Nihalani was saddened that the decentralization in the industry created serious hurdles in terms of collecting reliable data about revenues—no one can really mention accurately how much money a film had made. ‘Unlike any other business’, Nihalani said, ‘Success and failure are all relative to which position you occupy in the chain. The last three years have been very demanding’. But not just independent producers, even corporates were witnessing a decline in the return on investment. There were several factors that had affected the health of Bollywood.

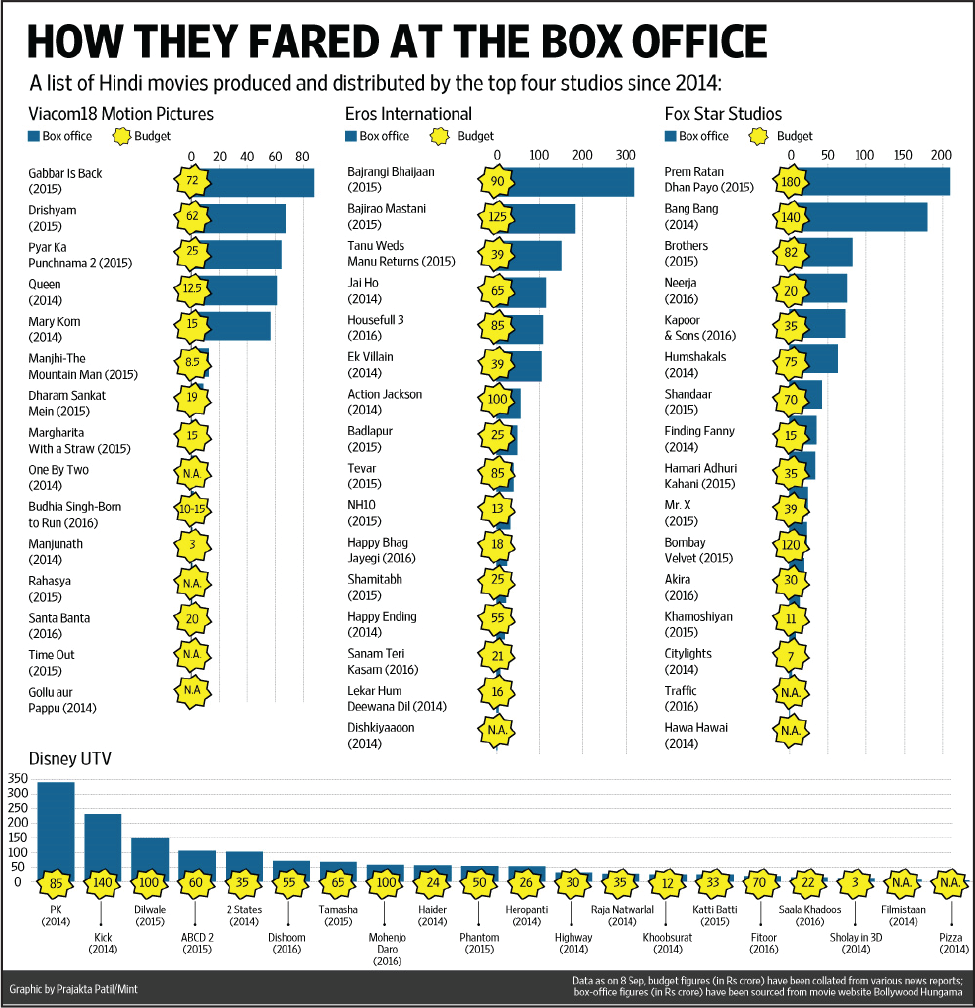

The corporatized production houses, especially the multinationals even with their deep pockets, had not fared very well either. Sony Pictures, PVR Pictures and Warner Bros. had all closed down operations in Mumbai (Figure 2). Among the domestic firms, Reliance Big Pictures and the movie division of SaReGaMa had also shut up shop (Krishna, 2016). The biggest casualty of this turbulence had been Disney. After the successive failures of Fitoor and Mohenjo Daro in the box office, Disney decided to end its operations in Hindi movie production business. Industry analysts like Komal Nahta were very forthright in criticizing the new investment model that Bollywood seemed to be using in the movie production process without much attention towards the creative aspects (Jha, 2016). Several industry experts and insiders like Nihalani seemed to be focusing on the neglect of the content and scripts leading to the generic decline of the industry health.

Cost of Film Production and Promotion

The cost of film production and promotion had increased significantly. While it was arguable that inflation was to be blamed for rising expenditure and, hence, the cost of production, it had to be borne in mind that there were unwarranted expenses that had led to extremely high costs; for instance, the cost of the lead star’s personal staff such as physical trainer and manager had nothing to do with the film; yet, producers had been bearing this burden. Wherever the lead star was shooting in the world, the presence of his/her personal staff was almost a requisite. This was paid by the producer over and above the star’s professional fees. Nihalani had had to go through ‘this ordeal right through his career, but the severity had increased in the past 5-6 years’. It had to be borne in mind that the fee of Bollywood stars comprised up to 40 per cent of the total production budget, whereas in all regional language films and other countries, it ranged from 15 per cent to 20 per cent of the total budget. The astronomically high remuneration for top actors was the reason why production budgets had spiralled, a move Nihalani called ‘studios digging their own graves’. Individual producers such as Sajid Nadiadwala or Karan Johar often shared a personal rapport with movie stars, built over several years; in contrast, it was tougher for studios to develop a relationship with stars, and that was where gigantic remuneration figures came in. Atul Mohan, the editor of trade magazine Complete Cinema, said only corporate entities could afford the kind of money top stars have begun to demand today.

The cost of film promotion had increased to an unimaginable extent. There was no fixed percentage set aside for promotions. In some cases, the marketing budget of the film could exceed the cost of film production. Vicky Donor could be cited an as an example. For a film like English Vinglish, the promotion spend was nearly the same as that of production. The marketing budgets of films such as Yeh Jawaani Hai Deewani, Yamla Pagla Deewana 2 and Raanjhanaa were as high as 30 per cent of the total cost (Kohli-Khandekar, 2015).

In an interview with Daily News and Analysis (Naval Shetye, 2013), a film-maker said, on the grounds of anonymity,

We feel cornered into partnering or tying up with a studio because that’s the only way we are ensured that our film can match up to the high levels of marketing that’s the norm these days. There’s just no limit to how much these studios are willing to spend, and it’s impossible for an independent filmmaker to match up to that hype that they create, and so naturally our films suffer even if the content may be just as good, if not better.

The high cost of film acquisition remained yet another reason for the undoing of a studio. There are two levels of producers in the industry today—boutique production houses including the likes of Dharma Productions (of Karan Johar), Nadiadwala Grandson Entertainment (of Sajid Nadiadwala) and studios such as Viacom18 Motion Pictures, Eros International, Fox Star Studios and Walt Disney Studios. Boutique production houses were those that had upscaled from being a conventional entrepreneurship and family business to a corporate set-up managed by professionals. Studios entered the entertainment industry as professional ventures. Single producers were known to charge anything between ₹40 million and ₹150 million per film when they sold movies to studios for distribution. Studios referred to such movies as ‘acquired films’ and the model as ‘acquisition-based’ model.

Nihalani expressed serious concerns about the flawed approach of the acquisition-based mode,

When you run with a purely acquisition-led approach, you’re paying a significant premium, have little control over the product, and you’d end up in very one-sided deal structures, which is hardly collaborative. As a result, it is important to know what producers should be chasing—is it volume, top line or big film-focused or is it based on content and business fundamentals such as story material, bottom-line, risk mitigation and cost-efficacy? If you focus on fundamentals, the results have been far better.

Creativity could rarely flourish under such insecurity.

In an interview with Bollywood Hungama (2014), film-maker Sanjay Gupta said

The high Print & Advertisement (P&A) works very well for most studios to show fake and escalated costs to producers. Otherwise whoever said that touring the country with your entire cast will ensure footfalls in theatres? There is hardly a debate though that the need of the hour is to control the ridiculously escalating costs of marketing.

One interesting case in point was the split in promotion costs across geographies. Historically, Mumbai had been contributing a larger share to the lifetime domestic box-office collection of any film. However, over the years, the business in Mumbai city and Delhi had almost become the same. Given the scenarios, it was interesting to study the marketing budget allocation—Delhi had no outdoor promotions, no hoardings, no posters, fewer advertorials and fewer newspaper jacket ads. In the era of social media and peer-to-peer communication, marketing largely helped the first-day numbers. After that, word of mouth in the digital media took over and helped consumers make the viewing decision. When it came to a content-oriented film that lacked conventional star power, it was not essential to run a 10–12 weeks’ pre-release campaign and to typically spend about ₹80–100 million. Usually, viewers decided about watching a movie just a few days before the release. Though most producers agreed that spending that high a cost towards the promotion of a small-to-medium budget film was not viable, they eventually did succumb to the pressure.

Earning from the Sale of Satellite Broadcasting Right

The earning from the sale of satellite broadcasting rights increased significantly in 2012 and 2013. In most cases, the revenue earned from broadcasting rights became the largest for the producer. Satellite channels started maximizing their return on investment by telecasting the film’s television premiere as early as in the fifth week of its theatrical release. This drastic shortening of the theatrical window had, in turn, pressurized the producers and distributors to maximize their revenue from the box office during the first week of theatrical release. Hence, producers had been forced to boost marketing activities and spend. The exhibitors also were not fond of the short theatrical window because their audiences now did not care if they missed a film in the cinemas; they were confident that very soon they would get to watch it in their homes—for free! This domino effect was adding to the marketing spends.

The year 2014 had brought a wave of change—the earnings from the sale of satellite broadcasting rights dropped by more than half as compared to that of 2012. But, ironically, the marketing spend did not come down.

Experts believed that this correction in price was bound to happen, a few reasons were cited as follows:

Change in consumer viewership: There was a decline in the time spent on watching films from 20 per cent to 18 per cent. Star India, one of the biggest bidders for film rights, was now more focused on sports and general entertainment. A 12-min cap on advertisements per clock hour that had been introduced by the Telecom Regulatory body, TRAI, in the last quarter of 2013 had made monetization tougher for broadcasters.

Many broadcasters were opting for developing special weekend content in smaller budgets and acquiring rights of cheaper regional films which they dubbed into Hindi and then telecast them.

Cost to Consumers Versus Earning of Producers

On an average, when two people visited a multiplex, they would spend about ₹1,500. After taking out the money spent towards purchase of snacks and beverages, parking, entertainment tax, exhibitor rent and distributor commission, not more than ₹200 went to the producer. This shows that less than 15 per cent of what the audience spent at the multiplex went to the maker of the film. On top of that, the introduction of a uniform goods and services tax (GST) regime from 1 July 2017 had pushed up the ticket prices considerably as the entertainment industry had been placed in the 18 per cent slab.

Regulation Mechanism in the Tamil Film Industry

The Tamil film industry that operated out of Chennai, and popularly known as the Kollywood, was self-regulated. Unlike its Mumbai peer, Kollywood did not indulge in lavish marketing spend. While the cost of production of films varied from ₹20 million to ₹600 million, the upper limit on marketing spend for big films was ₹50 million. Every movie spent just enough to create awareness. There was no cut-throat competition to lure the audience via mega advertising campaigns; rather, they allowed the content to speak for itself. This policy adopted by producers had not only helped in controlling the cost but has also improved their bargaining power with the exhibitors.

Unlike in Bollywood, the Tamil film industry did not pay exhibitors to run trailers of an upcoming film or for placing standees and other film branding and publicity material in the theatre. Producers believed that exhibitors were business associates, and they should shoulder equal responsibility in film promotion. All multiplex chains and single-screen theatres ran trailers of upcoming Tamil films and placed their branding material in prominent locations 1 week before the release (at no cost). Interestingly, the same exhibitors charged Hindi film producers an exorbitant price for playing trailers of upcoming films and placing the promotional material within the theatres. The exhibitors offered a basic pre-release package of 2 weeks to Bollywood producers but but only a few films would opt for in-cinema advertising for 4 weeks and more.

The remuneration of lead stars in the Kollywood was decided based on the box-office performance of their last three films. This ensured that the cost did not escalate to an unrealistic level, and producers were not the only ones penalized for a film’s failure. In Bollywood, there was no method to determine a star’s remuneration, and this had led to sky-high fees of the sought-after celebrities despite some of their films having not worked at the box office in the past years.

Every Bollywood film team visited several cities in India for promotion before the release of the film. On the other hand, in Kollywood, the lead cast of select films visited Coimbatore, Madurai and Trichy only after the film released and was enjoying a positive word of mouth. The decision was made based on the film’s present performance at the box office and the sentiments of the audience. Producers made an informed decision to spend extra to improve their return on investment.

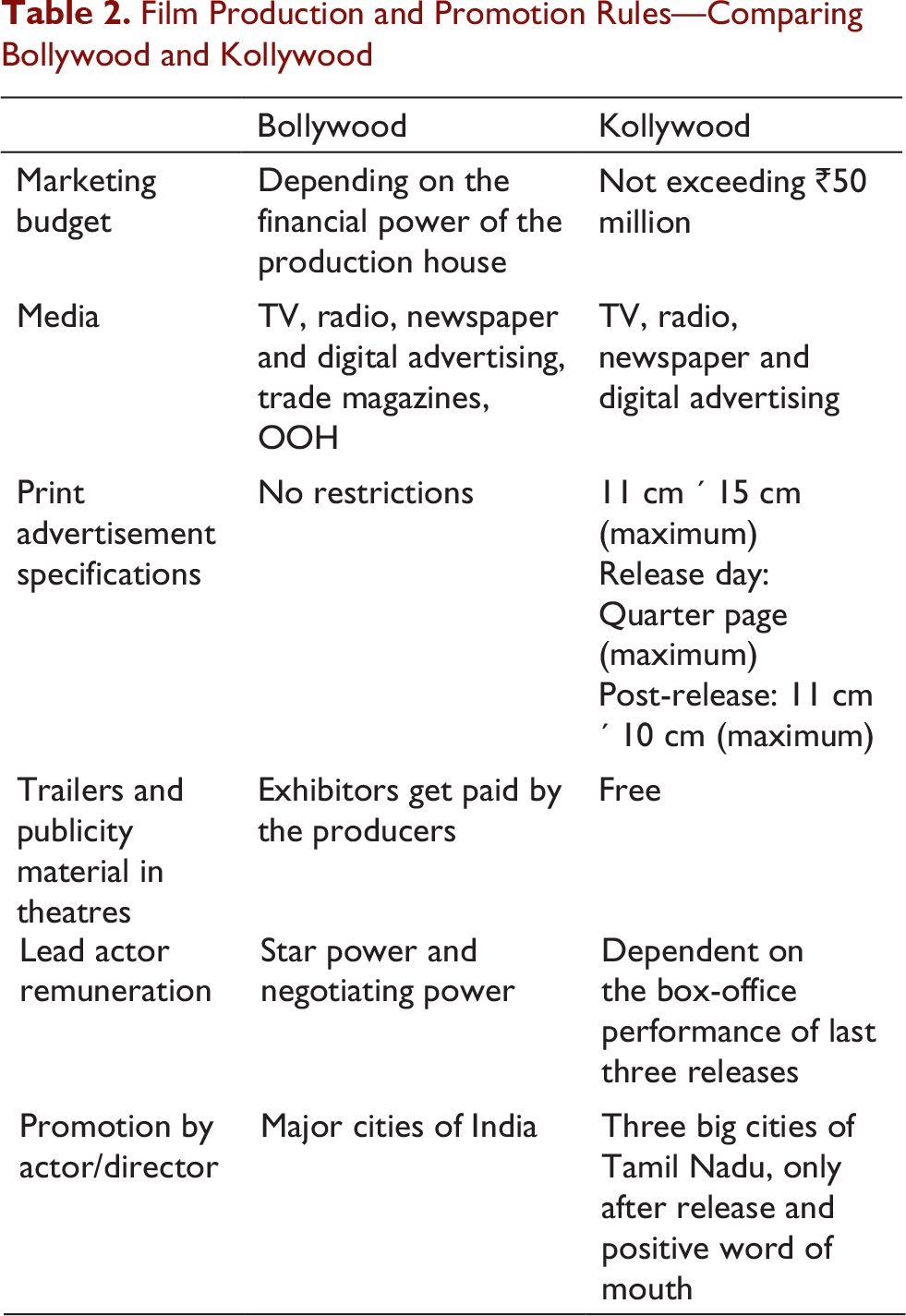

Film Production and Promotion Rules—Comparing Bollywood and Kollywood

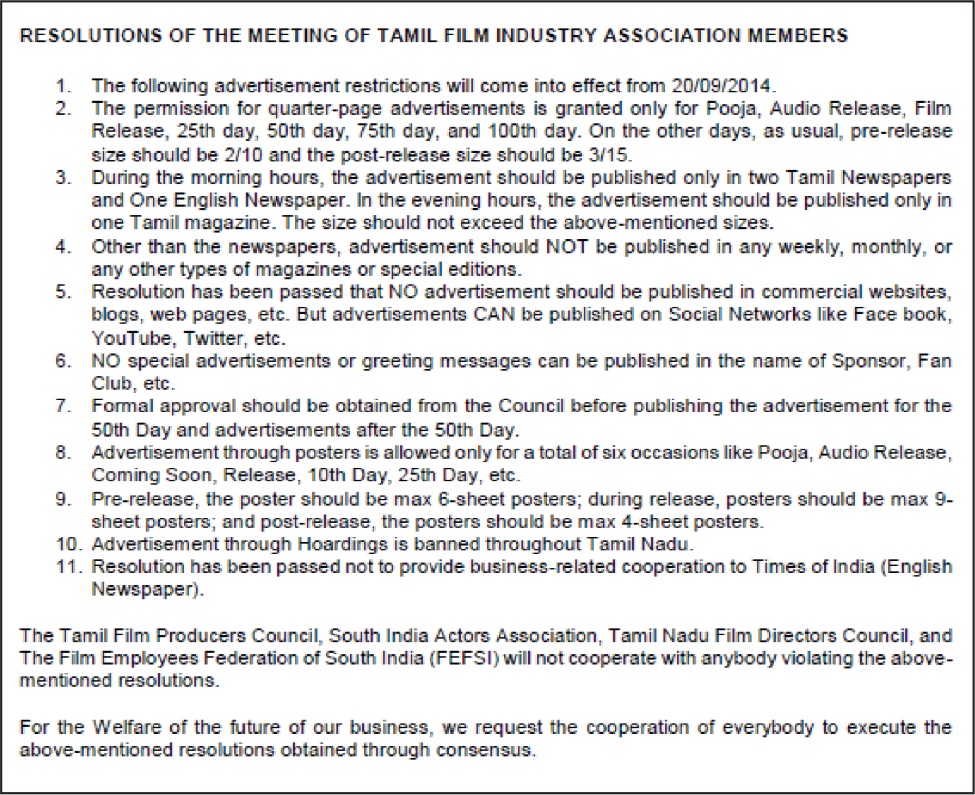

There were four major industry associations in Chennai—the Tamil Film Producers Council, South Indian Artistes’ Association, Tamil Nadu Film Directors Council and The Film Employees Federation of South India (FEFSI). Members met from time to time and discussed issues and potential threats. They had been taking major steps to ensure that the profitability of the industry was maintained. Recently, all four associations came together to regulate the differences in newspaper advertisements and other advertisement restrictions. After a thought-provoking discussion and with the consensus of all members, few resolutions were finalized (Figure 3).

The Dilemma

Nihalani believed that it was a remarkable feat achieved by the Bollywood film industry that had managed to survive, continued to make successful films, touched people’s hearts and its films are seen by millions of people all over the world. Despite hostile or indifferent government policies, high rates of taxation, complete disinterest by much of the organized sector, scarcity of capital, and a very decentralized structure, the Hindi film industry had managed to survive and grow. But moving forward, could there be a sustainable business model benefitting all types of film producers in the industry. Could he, as a veteran and respected producer, take the initiative in shaping the opinions of his peers into creating a structure for ensuring industry sustainability? Or should he stick to his core passion of producing films and pray that others do their bit earnestly?

What actions could he take so that his short-term problem of finding a distributor for Rangeela Raja was sorted out? And what could he do for the overall industry so that the producers and production houses were ensured a decent return to continue being important players? In a creative industry, Nihalani wondered, the competition was not about putting your competition out of business, but to make sure that the pie kept increasing so that various competitors of different sizes and styles could flourish together.

Footnotes

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship and/or publication of this article.